valuation of ip assets

TRANSCRIPT

© November 2006 Global Business Solutions. All rights reserved. [email protected] © November 2006 Global Business Solutions. All rights reserved. [email protected]

Valuation of IP AssetsValuation of IP Assets

November 24, 2006November 24, 2006byby

S.A. Chenthil KumaranS.A. Chenthil KumaranGlobal Business SolutionsGlobal Business Solutions

ChennaiChennai

BackgroundBackground

IPR Assets are recognized as the most IPR Assets are recognized as the most important asset of many of the world’s important asset of many of the world’s largest and most powerful companies;largest and most powerful companies;

It is the foundation for the market It is the foundation for the market dominance and continuing profitability of dominance and continuing profitability of leading corporations. leading corporations.

It is often the key objective in mergers and It is often the key objective in mergers and acquisitions.acquisitions.

Broad Range of Intangibles With ValueBroad Range of Intangibles With Value

The obvious intangiblesThe obvious intangibles PatentsPatents CopyrightsCopyrights TrademarksTrademarks

Bundles of intellectual capital and intangible Bundles of intellectual capital and intangible assetsassets The Technical BundleThe Technical Bundle The Marketing BundleThe Marketing Bundle The IT BundleThe IT Bundle

Technical Bundle of IntangiblesTechnical Bundle of Intangibles

Key patentsKey patents Trade secretsTrade secrets FormulaeFormulae Packaging technology and sourcesPackaging technology and sources Process technologyProcess technology Design technologyDesign technology New product technologyNew product technology Technical data sheetsTechnical data sheets Evaluation dataEvaluation data Proprietary test resultsProprietary test results Plant and production designPlant and production design Product specificationsProduct specifications

Marketing Bundle of IntangiblesMarketing Bundle of Intangibles

Corporate name and logoCorporate name and logo Primary trademarkPrimary trademark brand namesbrand names Sub-brand names and trade dressSub-brand names and trade dress Worldwide trademark registrationsWorldwide trademark registrations Secondary trademarksSecondary trademarks Packaging design and copyrightsPackaging design and copyrights Consumer advertisingConsumer advertising Marketing strategyMarketing strategy Product warrantiesProduct warranties GraphicsGraphics Promotional conceptsPromotional concepts Worldwide public relations effortsWorldwide public relations efforts

IT Bundle of IntangiblesIT Bundle of Intangibles

Enterprise solutionsEnterprise solutions Custom applicationsCustom applications Data warehousesData warehouses Master licensesMaster licenses Source codeSource code DatabasesDatabases Data miningData mining Domain names / URLsDomain names / URLs E-commerce sitesE-commerce sites Third party software toolsThird party software tools Credit / payment systemsCredit / payment systems

IP ValuationIP Valuation

Valuation Is Context Specific & Time Valuation Is Context Specific & Time CriticalCritical

CONTEXT + TIME = VALUE OF IPCONTEXT + TIME = VALUE OF IP

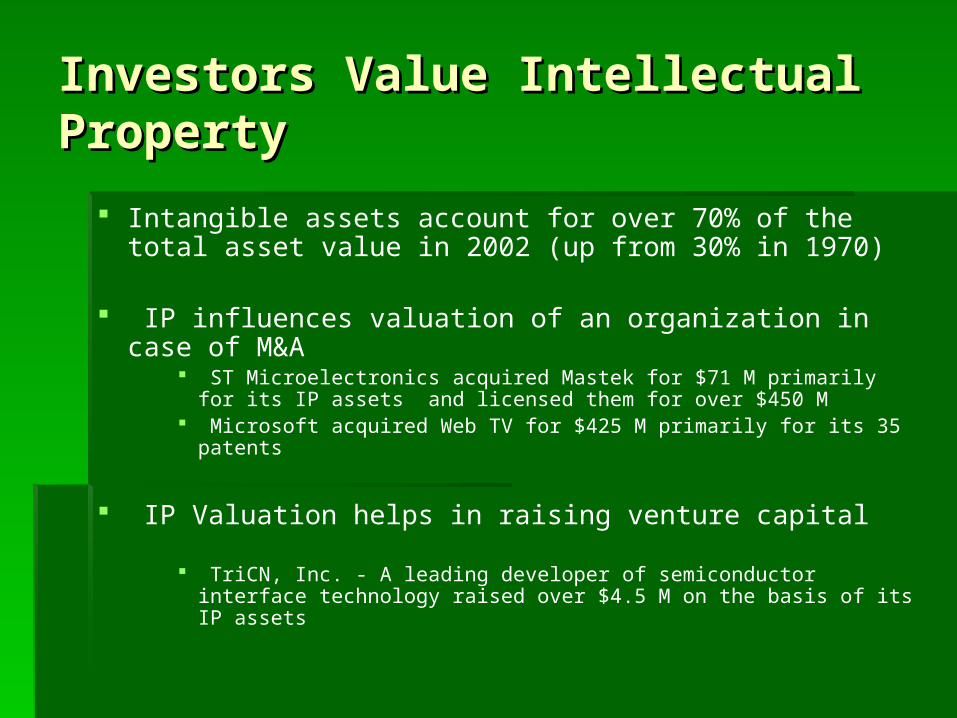

Investors Value Intellectual PropertyInvestors Value Intellectual Property

Intangible assets account for over 70% of the total asset value in 2002 (up from 30% in 1970)

IP influences valuation of an organization in case of M&A

ST Microelectronics acquired Mastek for $71 M primarily for its IP assets and licensed them for over $450 M

Microsoft acquired Web TV for $425 M primarily for its 35 patents

IP Valuation helps in raising venture capital TriCN, Inc. - A leading developer of semiconductor interface

technology raised over $4.5 M on the basis of its IP assets

The IBM StoryThe IBM Story

Annual licensing revenue increased from $30 M in 1992 to over $1.3 B in 1999

•Innovation encouraged through Performance Management System

•Approximately $5 B per year in R&D since 1996

•Over 3,000 patents filed every year

•Current active portfolio has 21,000 patents in the United States and 38,000 patents worldwide

•Leading the USPTO list of top patent filing companies for the past eight years

R&D Process Financial GainsIntellectual Property

Reasons for Valuing IP AssetsReasons for Valuing IP Assets Corporate Mergers & AcquisitionCorporate Mergers & Acquisition LitigationLitigation Fund RaisingFund Raising IPOIPO Joint VenturesJoint Ventures Intra Company TransfersIntra Company Transfers Financial ReportingFinancial Reporting Assignment or Acquisition of IP Assets Assignment or Acquisition of IP Assets Licensing in or out the IP AssetLicensing in or out the IP Asset Investment in the IP Asset (E.g. For further Investment in the IP Asset (E.g. For further

development)development)

Factors Driving IP ValueFactors Driving IP Value

IndustryIndustry Market ShareMarket Share ProfitsProfits New TechnologiesNew Technologies Barriers to EntryBarriers to Entry Growth ProspectsGrowth Prospects Legal ProtectionLegal Protection

PURPOSES AND USES OF IP PURPOSES AND USES OF IP VALUATIONSVALUATIONS

♦ ♦ Financial ReportingFinancial Reporting

♦ ♦ Sale Transaction SupportSale Transaction Support

♦ ♦ LicensingLicensing

♦ ♦ Strategic AlliancesStrategic Alliances

♦ ♦ Infringement DamagesInfringement Damages

♦ ♦ Transfer PricingTransfer Pricing

♦ ♦ Equity RaisingEquity Raising

♦ ♦ Collateral-based FinancingCollateral-based Financing

Valuation Effort RequiredValuation Effort Required

CircumstanceCircumstance

Expected Expected Degree of Degree of ScrutinyScrutiny

Level of Level of Effort Effort

RequiredRequired

LitigationLitigation Very HighVery High LargeLarge

Tax-Related VenturesTax-Related Ventures HighHigh LargeLarge

Joint VenturesJoint Ventures HighHigh LargeLarge

Intra-Company TransfersIntra-Company Transfers HighHigh LargeLarge

Valuation Effort Required Valuation Effort Required (cont.)(cont.)

CircumstanceCircumstance

Expected Expected Degree of Degree of ScrutinyScrutiny

Level of Level of Effort Effort

RequiredRequired

Business Decision MakingBusiness Decision Making MediumMedium MediumMedium

Licensing Licensing (Sale & Purchase)(Sale & Purchase)

MediumMedium MediumMedium

In-Kind ContributionIn-Kind Contribution MediumMedium MediumMedium

R&D InvestmentR&D Investment MediumMedium MediumMedium

VALUATION OF IP - THREE VALUATION OF IP - THREE APPROACHESAPPROACHES

♦ ♦ Market ApproachMarket Approach

♦ ♦ Cost ApproachCost Approach

♦ ♦ Income ApproachIncome Approach

MARKET APPROACHMARKET APPROACH

♦ ♦ Provides indications of value by studying Provides indications of value by studying transactions of property similar to the transactions of property similar to the property for which a value conclusion is property for which a value conclusion is sought.sought.

♦♦RequirementsRequirements Active market involving comparable propertyActive market involving comparable property Past transactions of comparable propertyPast transactions of comparable property Access to transaction price informationAccess to transaction price information

DisadvantagesDisadvantages

Search for a comparable market Search for a comparable market transaction is futiletransaction is futile

Lack of compatibilityLack of compatibility IP transactions are part of a larger IP transactions are part of a larger

transaction and details are kept transaction and details are kept extremely confidentialextremely confidential

It is never possible to find a transactionIt is never possible to find a transaction

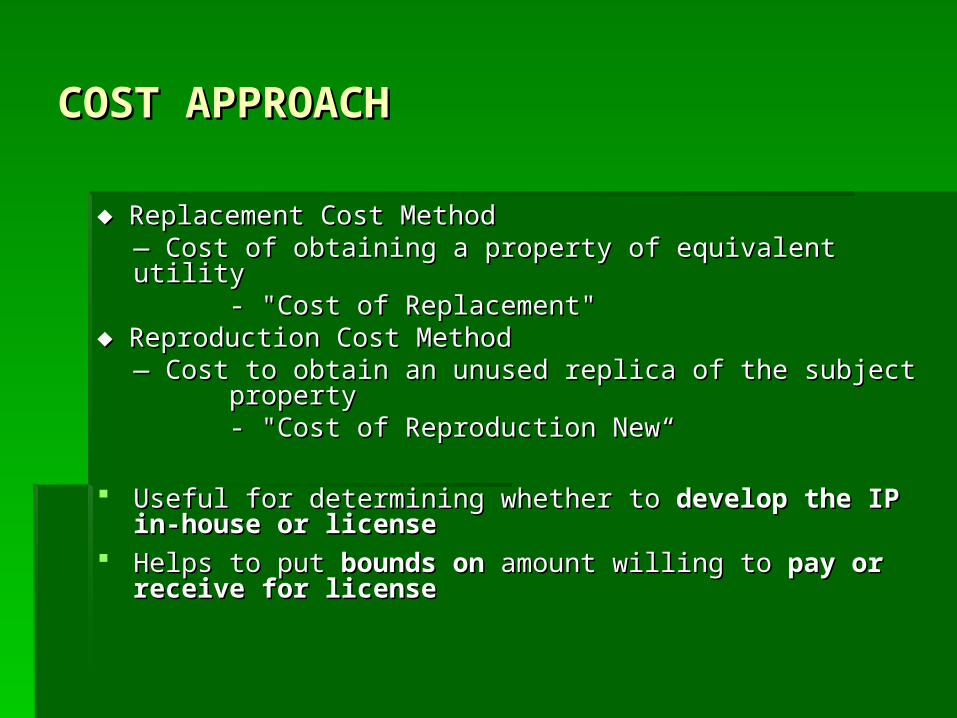

COST APPROACHCOST APPROACH

♦ ♦ Replacement Cost MethodReplacement Cost Method— — Cost of obtaining a property of equivalent utilityCost of obtaining a property of equivalent utility

- "Cost of Replacement"- "Cost of Replacement"♦ ♦ Reproduction Cost MethodReproduction Cost Method

— — Cost to obtain an unused replica of the subject Cost to obtain an unused replica of the subject propertyproperty- "Cost of Reproduction New“- "Cost of Reproduction New“

Useful for determining whether to Useful for determining whether to develop the IP in-house or develop the IP in-house or licenselicense

Helps to put Helps to put bounds onbounds on amount willing to amount willing to pay or receive for pay or receive for licenselicense

DisadvantagesDisadvantages

This approach ignores changes in the This approach ignores changes in the time value of money and ignores time value of money and ignores maintenance Cost. maintenance Cost. Does not account for Does not account for market demand.market demand.

INCOME APPROACHINCOME APPROACH

♦ ♦ Assess the ability of IP to produce cash flowAssess the ability of IP to produce cash flow Based on discounted cash-flow theory Based on discounted cash-flow theory

= Present value of cash flow generated from future = Present value of cash flow generated from future sales over useful lifetime of IPsales over useful lifetime of IP

Key pointsKey points Identify revenue portion generated by IPIdentify revenue portion generated by IP Anticipate growth in projectionsAnticipate growth in projections Anticipate duration of revenuesAnticipate duration of revenues Evaluate risks affecting projections (market, IP, Evaluate risks affecting projections (market, IP,

technology)technology)

Economic Benefits ValuationEconomic Benefits Valuation

This method is based upon the principle This method is based upon the principle that an IP asset must produce a net that an IP asset must produce a net economic benefit during its life in order to economic benefit during its life in order to have any value i.e. the benefit of the have any value i.e. the benefit of the asset over its lifetime must exceed cost.asset over its lifetime must exceed cost.

The net economic benefit must be The net economic benefit must be sufficiently large to provide a rate of sufficiently large to provide a rate of return with the investment risk.return with the investment risk.

Net Present ValueNet Present Value

Present Value or a Value at a future date is Present Value or a Value at a future date is calculated based on:calculated based on: The cost of design, research, development, marketing The cost of design, research, development, marketing

and distribution.and distribution. Life of the Product or ProcessLife of the Product or Process Life of the associated IPLife of the associated IP The timing and quantum of the income streamThe timing and quantum of the income stream Risk and inflation factors.Risk and inflation factors.

The above will bring the IP assets to a Net Present The above will bring the IP assets to a Net Present Value.Value.

Discounted cash flow (“DCF”) analysisDiscounted cash flow (“DCF”) analysis

Discounted cash flow (“DCF”) analysis Discounted cash flow (“DCF”) analysis sits is probably the most comprehensive sits is probably the most comprehensive of appraisal techniques. Potential profits of appraisal techniques. Potential profits and cash flows needs are assessed to and cash flows needs are assessed to arrive at the present value through use of arrive at the present value through use of a discount rate, or rates.a discount rate, or rates.

Contd…Contd…

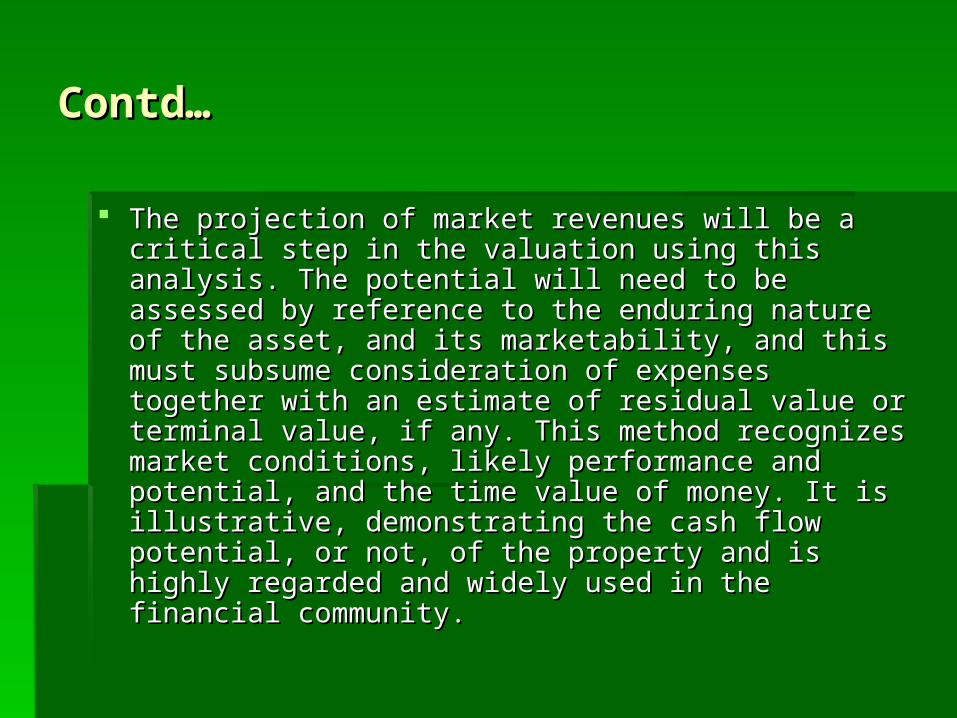

The projection of market revenues will be a critical step The projection of market revenues will be a critical step in the valuation using this analysis. The potential will in the valuation using this analysis. The potential will need to be assessed by reference to the enduring need to be assessed by reference to the enduring nature of the asset, and its marketability, and this must nature of the asset, and its marketability, and this must subsume consideration of expenses together with an subsume consideration of expenses together with an estimate of residual value or terminal value, if any. This estimate of residual value or terminal value, if any. This method recognizes market conditions, likely method recognizes market conditions, likely performance and potential, and the time value of performance and potential, and the time value of money. It is illustrative, demonstrating the cash flow money. It is illustrative, demonstrating the cash flow potential, or not, of the property and is highly regarded potential, or not, of the property and is highly regarded and widely used in the financial community.and widely used in the financial community.

ConclusionConclusion

IP Valuations are based on the IP to be IP Valuations are based on the IP to be valued (trademark, patents, Copyright valued (trademark, patents, Copyright etc), for whom its valued and purpose of etc), for whom its valued and purpose of valuation.valuation.

Normally many assumptions need to be Normally many assumptions need to be made and valuing IP assets has the made and valuing IP assets has the character of being more of an art than a character of being more of an art than a science.science.

THANK YOUTHANK YOU