valuation report - centuria · 2018-01-11 · valuation as deemed appropriate. the subject property...

TRANSCRIPT

Valuation Report

Address

60 Brougham Street Geelong

Under Instructions From:

Centuria Property Funds Limited

Date of Valuation:

07 December 2017

Cushman & Wakefield

Level 3, 111 Coventry Street

South Melbourne VIC 3205

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2

Liability limited by a scheme approved under Professional Standards Legislation

TABLE OF CONTENTS

1 Executive Summary .................................................................................................................. 4

1.1 Valuation Assumptions ............................................................................................................. 8

1.1.1 Critical Assumptions ................................................................................................................. 8

1.1.2 Verifiable Assumptions ............................................................................................................. 8

2 SWOT Analysis ...................................................................................................................... 10

3 Risk Assessment .................................................................................................................... 11

4 Introduction ............................................................................................................................ 12

4.1 Instructions ............................................................................................................................. 12

4.2 Definitions .............................................................................................................................. 12

4.3 Date of Valuation .................................................................................................................... 12

4.4 Independence of Valuer .......................................................................................................... 13

4.5 Information Sources ............................................................................................................... 13

5 Property Details ...................................................................................................................... 14

5.1 Legal Description .................................................................................................................... 14

5.2 Town Planning........................................................................................................................ 14

5.3 Location ................................................................................................................................. 15

5.4 Site Details ............................................................................................................................. 15

5.5 Utilities ................................................................................................................................... 16

5.6 Environmental, Heritage and Cultural ...................................................................................... 17

6 Improvements......................................................................................................................... 18

6.1 Description of Improvements .................................................................................................. 18

6.2 Services ................................................................................................................................. 18

6.3 Accommodation & Internal Finishes ........................................................................................ 20

6.4 Onsite Parking ........................................................................................................................ 21

6.5 Building Areas ........................................................................................................................ 21

6.6 Building Condition and Utility .................................................................................................. 21

6.7 Occupational Health and Safety .............................................................................................. 21

7 Tenancy Details ...................................................................................................................... 22

8 Financial Analysis ................................................................................................................... 26

8.1 Income Summary ................................................................................................................... 26

8.2 Outgoing Expenses ................................................................................................................ 26

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3

Liability limited by a scheme approved under Professional Standards Legislation

8.3 Capital Expenditure ................................................................................................................ 27

9 Market Commentary ............................................................................................................... 29

9.1 Economic Overview ................................................................................................................ 29

9.2 Regional Office Market Overview ............................................................................................ 30

10 Market Evidence ..................................................................................................................... 34

10.1 Rental Evidence ..................................................................................................................... 34

10.1.1 Rental Summary ..................................................................................................................... 36

10.2 Sales Evidence ....................................................................................................................... 36

10.2.1 Sales Summary ...................................................................................................................... 41

11 Valuation Methodology ........................................................................................................... 42

11.1 Highest and Best Use ............................................................................................................. 43

11.2 Capitalisation Approach .......................................................................................................... 43

11.3 Discounted Cash Flow Approach ............................................................................................ 46

11.4 Direct Comparison .................................................................................................................. 49

11.5 Summary of Valuation Approaches ......................................................................................... 50

11.6 Sales History .......................................................................................................................... 50

11.7 Selling Period & Marketability ................................................................................................. 50

11.8 Suitability for Mortgage Purposes ........................................................................................... 50

11.9 Insurance Estimate ................................................................................................................. 51

11.10 Valuation Qualifications .......................................................................................................... 51

12 Valuation ................................................................................................................................ 53

Appendix 1: Letter of Instruction

Appendix 2: Certificate of Title

Appendix 3: Plan of Consolidation

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 4

Liability limited by a scheme approved under Professional Standards Legislation

1 Executive Summary

Valuation Details

Instructing Party: Centuria Property Funds Limited

Reliant Party(s) & Purpose: - Centuria Property Funds No. 2 Limited (CPF2L) for Acquisition

Purposes

- Centuria Property Funds No. 2 Limited (CPF2L) as Responsible

Entity to advise investors in the proposed unlisted trust for Current

Market Value purposes

- Commonwealth Bank of Australia (CBA) for First Mortgage Security

Purposes

Basis of Valuation: Market Value

Type of Report: Full

Interest Valued: Freehold subject to existing tenancies

Date of Valuation: 07 December 2017

Date of Inspection: 07 December 2017

Registered Proprietor(s): 11029/247: Impact Funds Management Pty Limited

Property Overview

Planning Scheme: Greater Geelong Planning Scheme

Zoning: Activity Centre Zone 1

Site Area: 5,475 square metres

Ecologically

Sustainable

Development (ESD):

Energy 5.5 star

Water 5.0 star

Greenstar rating 5.0

Brief Description:

The subject property comprises a modern quality commercial office facility of concrete frame, glazed

curtain wall and lightweight panelling construction known as the 'TAC Building' incorporating lower and

upper ground retail floors and six upper levels of office accommodation in association with basement and

ground level car parking.

The property is located on the south eastern corner of Brougham and Clare Streets in the core of the

Geelong commercial precinct. Immediate surrounding development comprises established lower rise

commercial and retail facilities in association with two new high rise office developments, one nearing

completion and one to be developed.

Geelong is an established and historic regional city being Victoria's largest provincial centre and is located

approximately 12.5 kilometres south west of Avalon Airport and 75 kilometres southwest of the Melbourne

CBD.

Selling Period & Marketability:

In the event the property was offered for sale we consider it would meet with good demand, with an

anticipated selling period of approximately 3-5 months under current market conditions and subject to a

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 5

Liability limited by a scheme approved under Professional Standards Legislation

professional marketing campaign. Having regard to characteristics of the asset we expect the most likely

purchaser to be an Institutional investor.

Lettable Area

Office 14,816 sqm

Retail 1,281 sqm

Total 16,098 sqm

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 6

Liability limited by a scheme approved under Professional Standards Legislation

Tenancy Details

WALE (by Income): 10.62 years

WALE (by Area): 10.57 years

Current Vacancy: 0%

Number of Tenants: 30

Financial Details

Area (sqm) / Passing Income Market Income Variance to Market

Car Spaces $ pa$psm

$pcm$ pa

$psm

$pcm$ pa %

Office 14,816 $6,340,784 $428 $8,222,991 $555 ($1,882,207) -29.7%

Car Parking 338 cars $887,931 $219 $900,211 $222 ($12,280) -1.4%

Retail 1,281 $543,224 $424 $624,795 $488 ($81,570) -15.0%

Miscellaneous 2 $59,266 $29,633 $59,266 $29,633 $0 0.0%

Outgoing Recoveries $1,712,243 $106 $0 $0 $1,712,243 100.0%

Total Gross Income $9,543,448 $593 $9,807,263 $609 ($263,814) -2.8%

Less Total Outgoings $1,871,101 $116 $1,871,101 $116

Net Income $7,672,348 $477 $7,936,162 $493 ($263,814) -3.4%

Gross Income on Vacant Areas $0

Gross Income on New Leases $0

Total Gross Income (Fully Leased) $9,543,448 $593

Net Income (Fully Leased) $7,672,348 $477

Outgoing Recoveries

Fernwood Investements Pty Ltd 482 sqm

Rush Hour Café Pty Ltd 236 sqm

Major Tenants Transport Accident Commission 14,861 sqm

Impact Investment Group 520 sqm

Office14,816 sqm

92.03%

Retail1,281 sqm

7.96%

Miscellaneous2 sqm

0.01%

Categories By Area

Office$7,979,439

83.61%

Car Parking$887,931

9.30%

Retail$616,812

6.46%

Miscellaneous$59,266

0.62%

Categories by Gross Passing Rent

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

LEASE EXPIRY PROFILE

GROSS PASSING RENT (FULLY LET)

AREA

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 7

Liability limited by a scheme approved under Professional Standards Legislation

Valuation Approach(s)

Capitalisation Rate: 6.75%

Adopted Capital Value Rate: $7,250 psm

Discounted Cash Flow Inputs Discounted Cash Flow Outputs

Discount Rate: 8.00% Discounted Terminal Value: $62,607,872

Avg Growth Rate Office Net 2.96% NPV of Cash Flows: $60,788,104

Avg Growth Rate Net Present Value (net of costs): $116,735,651

Avg Growth Rate Retail Net 3.27% Terminal value growth: 1.32% pa

Terminal Yield: 7.25% Capital Expenditure (escalated): $5,555,513

Valuation Conclusions

Valuation Date 7 December 2017

Capitalisation Approach $115,250,000

Discounted Cash Flow Approach $116,750,000

Direct Comparison $116,700,000

Market Value $116,000,000

10.62 years

6.61%

Reversionary Yield 6.84%

6.71%

Internal Rate of Return (inc. Capex) 8.09%

Improved Value psm $7,206

Valuation

Subject to the leases described herein

$116,000,000 - Exclusive of GST

(One Hundred and Sixteen Million Dollars)

Weighted Average Lease Expiry (by Income)

Passing Initial Yield

Equivalent Yield

Cushman & Wakefield (Valuations) Pty Ltd

John Waugh FAPI

Certified Practising Valuer

Head of Valuation and Advisory, ANZ

Mars Njoo AAPI

Certified Practising Valuer

Director - Valuation and Advisory, Victoria

IMPORTANT NOTE: All data provided in this summary is wholly reliant on and must be read in conjunction with the

information provided in the attached report. It is a synopsis only designed to provide a brief overview and must not be

acted on in isolation.

Liability limited by a scheme approved under Professional Standards Legislation.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 8

Liability limited by a scheme approved under Professional Standards Legislation

1.1 Valuation Assumptions

1.1.1 Critical Assumptions

The NLA of the Transport Accident Commission varies from the definition within the PCA code of

measurement. The Lease states the NLA includes various back of house areas including loading dock and

accessways for the exclusive use of the tenant. The Lease states these areas are included in NLA. This

does increase the NLA from that under the normal method of measurement by approximately 460 sqm. We

have had regard for this point in our assessment.

The voids and stairwells on levels 2-5 are also included in NLA.

We have assumed that all information supplied in conducting our valuation consists of a full and frank

disclosure of all information that is relevant.

All other professional/consultancy advice provided and relied upon is true and correct.

While all reasonable endeavours have been made to clarify the accuracy of the information provided, it is

assumed that the information provided consists of a full and frank disclosure of all information that is relevant.

The subject property is a leased investment and is classified as a “Going Concern” in accordance with “A New

Tax System (Goods and Services Tax) Act 1999” and Goods and Services Tax Ruling 2002/5.

We have relied upon the lettable areas indicated on the tenancy schedule provided. Should any subsequent

surveys indicate a variation to the areas adopted within, the matter should be referred to us for review of the

valuation as deemed appropriate.

The subject property is currently subject to Lease Agreement(s). We have examined all of the lease(s).

In undertaking our valuation we have relied upon various financial and other information provided. Where

possible, within the scope of our retainer and limited to our expertise as Valuers, we have reviewed this

information including by analysis against industry standards. Based upon that review, Cushman & Wakefield

(Valuations) Pty Ltd has no reason to believe that the information is not fair and reasonable or that material

facts have been withheld. However, Cushman & Wakefield (Valuations) Pty Ltd is necessarily limited by the

nature of its role and Cushman & Wakefield (Valuations) Pty Ltd does not warrant that they have identified or

verified all of the matters which a full audit, extensive examination or "due diligence" investigation might

disclose. For the purpose of our valuation assessment, we have assumed that this information is correct.

It should be noted that in the case of advice provided in this report which is of a projected nature, we must

emphasise that specific assumptions have been made which appear reasonable based on current market

sentiment and forecasts. It follows that any one of the associated assumptions may change over time and no

responsibility can be accepted in this event. The value performance indicated above is an assessment of the

potential value trend and the indicated figures should not be reviewed as absolute certainty.

1.1.2 Verifiable Assumptions

Verifiable assumptions relate to environmental issues, structural integrity of the improvements, condition of

building services, zoning and encroachments, and can be confirmed by obtaining appropriate documentation

relating to each.

While in the course of inspection due care is taken to note building defects, no structural survey has been

made and no undertaking is given about the absence of rot, termite or pest infestation, deleterious substances

such as asbestos or calcium chloride or other hidden defects. We can give no guarantee as to outstanding

requisitions in respect to the subject building.

We have made no survey of the property and assume no responsibility in connection with such matters.

Unless otherwise stated it is assumed that all improvements lie within the title boundaries.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 9

Liability limited by a scheme approved under Professional Standards Legislation

We have requested, but not been provided with an Environmental Audit Report. Verification that the subject

property is free from any contamination should be obtained from a suitably qualified environmental expert.

Should environmental concerns be encountered, our valuation may require amendment.

Based on our site inspection we can only assume there are no obvious signs of contamination, chemical

residues or other pollution brought about by the existing or previous use of the land. There did not appear to

be any evidence of site contamination, however, a subsoils survey has not been undertaken and we are

therefore unable to report or confirm the property is free of contamination.

We have requested, but not been provided with an Asbestos Register. The non-existence of an Asbestos

Register is a non-compliance with Occupational Health and Safety Regulations. Verification the property is

free from asbestos contamination should be obtained from a suitably qualified consultant. Should any

subsequent advice indicate the property to be contaminated, we reserve the right to reassess our valuation.

The property was developed after 2003 and is not required to have an asbestos register on site.

We have not sighted a structural report on the property nor have we inspected unexposed or inaccessible

portions of the premises. We therefore cannot comment on the structural integrity, defect, rot or infestation of

the improvements nor can we comment on any knowledge of the use in construction of material such as

asbestos or other materials now considered hazardous.

We emphasise that we are not qualified building surveyors and as such our comments are subject to any

detailed survey, which would confirm the structural integrity of the improvements and services. Our valuation

assumes that there are no inherent defects with the structure or service installations and reflects the age and

apparent condition.

Reference should be made to each section of our report for specific assumptions and commentary.

The right is reserved to review and if necessary vary the valuation figure if any environmental hazard, pest

affectation, heritage or cultural restrictions are found to exist.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 0

Liability limited by a scheme approved under Professional Standards Legislation

2 SWOT Analysis

Strengths:

Quality modern commercial asset

100% occupied

Well located in Geelong commercial centre

Large site with four street frontages

Good parking provisions

5 Greenstar rating

Long WALE of 10.62 years

Quality tenant profile with 92.30% of the total development and 100% of the office leased to

Transport Accident Commission (TAC) a state government body

Geelong is a prominent and well positioned regional city with a diverse economy and work base

Weaknesses:

Three retail tenancies or 1.70% of income expire in the next 12 months however this is minor in

terms of the total asset

A large asset in a regional location. However Geelong is a large regional city and two similar

sized assets are close by the subject - one recently complete and one commencing construction

Opportunities:

Obtain new leases on the retail areas to secure short term income

The property is a modern quality asset which is securely leased with a long WALE to a sound

tenancy profile. As such we see no material opportunities in the short to medium term

Threats:

The international economic environment appears slightly more stable but still variable which can

have a potential impact upon investment sentiment, however presently the domestic economy

continues to perform steadily

The property is a modern quality asset which is securely leased with a long WALE to a sound

tenancy profile. As such we see no material threats in the short to medium term

Note: Our observations within the S.W.O.T Analysis of this report provide our opinion of the property

as at the date of valuation.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 1

Liability limited by a scheme approved under Professional Standards Legislation

3 Risk Assessment

Investment Profile:

100% occupied

Well located in Geelong commercial centre

Quality tenant profile with 92.30% of the total development and 100% of the office leased to

Transport Accident Commission (TAC) a state government body

Geelong is a prominent and well positioned regional city with a diverse economy and work base

A large asset in a regional CBD location however two similar large modern assets are close by the

subject - one recently complete and one commencing construction

The asset contains what is cosnidered to be above average plant and services in compariosn to

other similar regional office assets

Physical Asset:

Quality modern commercial asset

Large site with four street frontages

Good parking provisions

5 Greenstar rating

Cash Flow Profile:

Long WALE of 10.62 years

Three retail tenancies or 1.70% of income expire in the next 12 months however this is minor in

terms of the total asset. No further expiries until April 2022

Management:

The asset is a large property with sophisticated plant and services but incorporating a low amount

of tenancies. As such we consider the asset would involve a medium level of management

The proposed management entity, Centuria Property Funds Limited is an experienced and

professional asset manager

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 2

Liability limited by a scheme approved under Professional Standards Legislation

4 Introduction

4.1 Instructions

Instructing Party: Centuria Property Funds Limited

Reliant Party & Purpose: - Centuria Property Funds No. 2 Limited (CPF2L) for Acquisition

Purposes

- Centuria Property Funds No. 2 Limited (CPF2L) as Responsible

Entity to advise investors in the proposed unlisted trust for Current

Market Value purposes

- Commonwealth Bank of Australia (CBA) for First Mortgage

Security Purposes

Interest Valued: Freehold subject to existing tenancies

Basis of Valuation: Market Value

Type of Report: Full

Report Compliance Standards

- Australian Property Institute: Australia and New Zealand Valuation and Property Standards

(formerly Professional Practice)

- Client Standing Instructions: - Centuria Property Funds Limited

- Commonwealth Bank of Australia (CBA)

We refer to the appendix for a full copy of the instructions.

4.2 Definitions

Market Value

The estimated amount for which an asset or liability should exchange on the valuation date between a willing

buyer and a willing seller in an arm’s length transaction, after proper marketing and where the parties had

each acted knowledgeably, prudently and without compulsion.

4.3 Date of Valuation

Date of Valuation: 07 December 2017

Date of Inspection: 07 December 2017

This valuation is current as at the date of valuation only. The value assessed herein may change significantly

and unexpectedly over a relatively short period of time (including as a result of general market movements or

factors specific to the particular property). Liability for losses arising from such subsequent changes in value is

excluded as is liability where the valuation is relied upon after the date of valuation.

Reliance on a Report by a lender-client must be reasonable in all the circumstances. The Valuer will not

assume any responsibility for reliance by the lender-client on the Report after the expiration of 90 days from

the date of valuation, or the expiration of what is considered to be a reasonable time, whichever is the lesser.

The Valuer does not warrant, guarantee and/or represent that the content of the Report will remain unchanged

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 3

Liability limited by a scheme approved under Professional Standards Legislation

for any period of time beyond the date of the Report and depending upon known and/or foreseeable facts that

might impact upon such value, such further time as maybe reasonable in all of the circumstances. The lender-

client should therefore review and consider the Report, regularly and frequently, before reliance.

If the property condition or circumstances vary between the date of inspection and date of valuation, we

reserve the right to reconsider our findings herein. We will not be held liable or negligent for variation in the

property for any reason whatsoever between the date of valuation and date of inspection.

4.4 Independence of Valuer

Cushman & Wakefield confirm that

The Valuer is qualified to carry out the valuation of properties in the State of Victoria.

Has experience in valuation of the type of property to be valued.

The Valuer has no pecuniary or other interests that could conflict with the proper valuation of the

property or could reasonably be regarded as being capable of affecting his ability to give an unbiased

opinion.

All investigations have been conducted independently and without influence from a third party in any

way.

The Valuer is a member of the Australian Property Institute, holds the designation of Certified

Practising Valuer and has completed the Institute’s required hours of Continuing Professional

Development and its compulsory Risk Management Module.

4.5 Information Sources

Areas provided by the vendor's Due Diligence room

Outgoings budgets provided by the vendor's Due Diligence material

Lease(s) provided by the vendor's Due Diligence material

Tenancy schedule provided by the vendor's Due Diligence material

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 4

Liability limited by a scheme approved under Professional Standards Legislation

5 Property Details

5.1 Legal Description

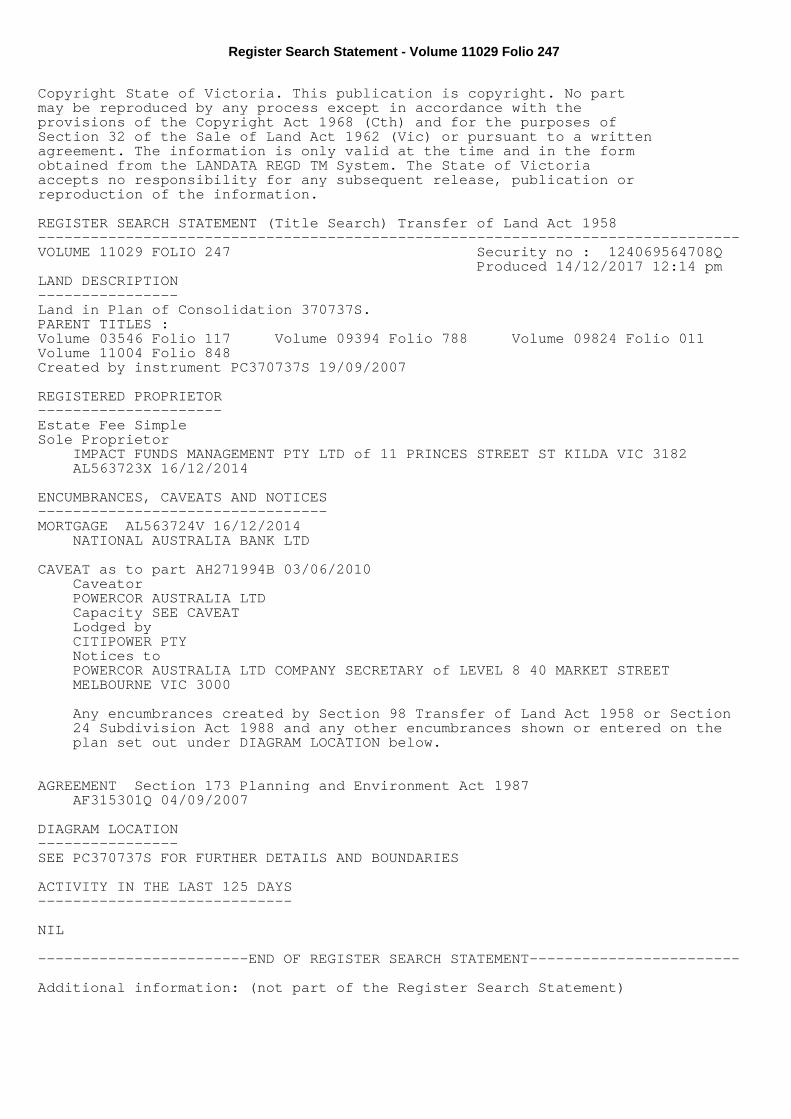

Reference Owner Notifications

11029/247 Impact Funds Management Pty Limited 3 Notifications - a

Caveat, mortgage and

Section 173 Agreement

The above notations are detailed as follows:

Notation Description

Caveat AH271994B Lease for indoor type substation and easement for powerline purposes

Section 173

Agreement

Agreement for Access Management Plan

We have had regard for the above notations in our assessment.

Overall, there are considered to be no other encumbrances or interests reported on the Certificate(s) of Title

which are considered to adversely affect the value, marketability and continued utility of the property. Should

any encumbrances, encroachments, restrictions, leases, covenants or other Instruments which are not noted

in this report be discovered, the valuation should be returned to the Valuer for comment.

The above details were obtained from SAI Global, SAI Global certifies that the information contained within

the Certificate(s) of Title has been provided electronically by Landata Systems.

We refer to the appendix for a copy of the Certificate(s) of Title.

5.2 Town Planning

Local Authority: City of Greater Geelong

Planning Scheme: Greater Geelong Planning Scheme

Zoning: Activity Centre Zone 1

Heritage: No

Purposes: To implement the State Planning Policy Framework and the Local Planning

Policy Framework, including the Municipal Strategic Statement and local

planning policies.

To encourage a mix of uses and the intensive development of the activity

centre:

o as a focus for business, shopping, working, housing, leisure, transport

and community facilities

o to support sustainable urban outcomes that maximise the use of

infrastructure and public transport.

To deliver a diversity of housing at higher densities to make optimum use of

the facilities and services.

To create through good urban design an attractive, pleasant, walkable, safe

and stimulating environment.

To facilitate use and development of land in accordance with the

Development Framework for the activity centre.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 5

Liability limited by a scheme approved under Professional Standards Legislation

The current use of the land as commercial and retail is considered permissible under the zoning.

The planning information noted has been obtained from the Department of Transport, Planning and

Infrastructure online website. We recommend that this zoning or planning area should be verified by

application to Council for the issue of a Planning Certificate pursuant to the Planning and Environment Act.

Should this information prove to be incorrect, we reserve the right to review our assessment.

5.3 Location

The property is located on the south eastern corner of Brougham and Clare Streets in the core of the Geelong

commercial precinct. Immediate surrounding development comprises established lower rise commercial and

retail facilities in association with two new high rise office developments, one nearing completion and one to

be developed and leased to the NDIS and Worksafe. The broader commercial precinct includes Deakin

University and Westfield shopping centre in conjunction with a diverse retail strip precinct. Geelong Rail

station is located approximately 500 metres to the west.

Geelong is an established and historic regional city being Victoria's largest provincial centre and is located

approximately 12.5 kilometres south west of Avalon Airport and 75 kilometres southwest of the Melbourne

CBD.A pictorial indication as to the location of the subject property is shown by the locality maps below.

Source: Nearmap.com Source: Nearmap.com

5.4 Site Details

Land Area: 5,475 square metres (approximately)

Frontage: Approximately 50.27 metres frontage to Brougham Street

Approximately 97.39 metres frontage to Clare Street

Approximately 50.92 metres frontage to Corio Street

Boundaries: Eastern: Approximately 102.23 metres

Topography/Aspect: The subject site forms an irregularly shaped lot situated street level on the Brougham Street frontage and rising along the Clare Street frontage to the rear frontage with Corio Street.

The land has been excavated and levelled to accommodate the current development.

Access: Brougham Street is a local access route receiving low to moderate traffic flow.

Clare and Corio Streets are local streets receiving low traffic flow.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 6

Liability limited by a scheme approved under Professional Standards Legislation

Vehicle access is via Clare Street whilst the loading dock is accessed from Gore

Street.

Flooding: As the subject site is not affected by a Land Subject to Inundation Overlay (LSIO) or

a Special Building Overlay (SBO), we have assumed that it is not at risk from

flooding.

Site Identification: Check measurements undertaken onsite appear to indicate that the improvements

are contained within Title Boundaries. We are not surveyors and no warranty can be

given without an identification survey. If any encroachments are noted by the survey

report, the member should be consulted to reassess any effect on the value stated

in this report.

Plan of Consolidation(s)

Plan of Consolidation 370737S

We refer to the appendix for a copy of the Plan of Consolidation(s).

5.5 Utilities

Electricity: Available and connected

Water: Available and connected

Sewer: Available and connected

Telephone: Available and connected

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 7

Liability limited by a scheme approved under Professional Standards Legislation

5.6 Environmental, Heritage and Cultural

Site Contamination

The land is currently used for office and retail purposes.

We are unaware of the previous use of the site.

We have requested, but not been provided with an Environmental Audit Report. Verification that the subject

property is free from any contamination should be obtained from a suitably qualified environmental expert.

Should environmental concerns be encountered, our valuation may require amendment.

We have carried out a search of the EPA’s Priority Sites Register at the time of completing this valuation and

confirm that the subject property is not listed.

Based on our site inspection we can only assume there are no obvious signs of contamination, chemical

residues or other pollution brought about by the existing or previous use of the land. There did not appear to

be any evidence of site contamination, however, a subsoils survey has not been undertaken and we are

therefore unable to report or confirm the property is free of contamination.

Asbestos

The subject asset was developed after the cut-off date requiring an Asbestos Register

An asbestos register is not required for a workplace if:

• the workplace was a building that was constructed after 31 December 2003

• no asbestos has been identified in the workplace

• no asbestos is likely to be present at the workplace from time to time.

(Work Health and Safety Regulation 2011 – Regulation 425 (6))

Verification the property is free from asbestos contamination should be obtained from a suitably qualified

consultant. Should any subsequent advice indicate the property to be contaminated, we reserve the right to

reassess our valuation.

Heritage and Cultural

The site incorporates a heritage overlay however the asset is a redeveloped modern building.

We have undertaken a search on the Victorian Heritage Register and the search revealed the property is not

listed or considered to have historical significance by the Heritage Council.

Right to Review

The right is reserved to review and if necessary vary the valuation figure if any environmental hazard, pest

affectation, heritage or cultural restrictions are found to exist.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 8

Liability limited by a scheme approved under Professional Standards Legislation

6 Improvements

6.1 Description of Improvements

The subject property comprises a modern quality commercial office facility of concrete frame, glazed curtain

wall and lightweight panelling construction known as the 'TAC Building' incorporating lower and upper ground

retail floors and six upper levels of office accommodation in association with basement and ground level car

parking.

Structure

Concrete frame

Floors

Concrete and raised flooring in office areas

Walls

concrete, masonry and lightweight panelling

Roof

Concrete and metal

6.2 Services

Air Conditioning

Central plant located at roof level comprising two York chillers, eight Air Handling Units (AHUs) and two

cooling towers. The air is ducted down the risers and dispersed via under floor plenums. Return air is

completed via ceiling vented recirculation.

Supplementary package units service the retail and back of house areas.

Fire Services

Sprinklers, smoke detectors, emergency lighting, exit signs hydrants and extinguishers, alarm and EWIS

Amenities

Modern contemporary style facilities with male, female and disabled facilities on each level. Showers

and end of trip facilities are located at B1.

Security Systems

Proximity card and CCTV.

Lifts

Three Otis passenger lifts servicing the office tower each with a capacity of 17 persons or 1,275 kg

Two Otis lifts servicing the carpark to level 2 each with a capacity of 17 persons or 1,300 kg

Two Otis variable speed passenger activated escalators servicing ground to upper ground

One Otis goods lift servicing B2 to level 7 (roof plant) with a capacity of 1,000kg

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 1 9

Liability limited by a scheme approved under Professional Standards Legislation

Generator

Two 500KVA diesel generators located at basement level in association with two above ground diesel

tanks. We have been advised by the Facility Manager that the generator services all base building and

essential services

Building Management System (BMS)

The Schneider BMS controls and monitors air conditioning and ventilation and includes central

temperature adjustment and fault detection. The system also monitors various fire, electrical and

hydraulic systems

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 0

Liability limited by a scheme approved under Professional Standards Legislation

6.3 Accommodation & Internal Finishes

Basement

Basement levels incorporate parking over three split levels

including part ground, bike racks and end of trip facilities

Ground Floor

Main entry from Brougham Street leading to large foyer with

double height ceiling. The ground level incorporates TAC

reception and security and offices on the western portion and

Rush Café occupying the eastern front portion. Escalators are

located in the foyer leading to the upper ground.

Carpark lifts are situated towards the rear on the western

perimeter whilst the office lifts are midway along the eastern

perimeter of the foyer.

Behind the public areas are various back of house areas

primarily storage, goods access, loading dock, amenities and

end of trip facilities.

The Upper ground level incorporates a second foyer for the

office lifts and access to the rear courtyard retail areas.

The retail area comprises a central courtyard with retail shops

to either side leading to the rear Corio Street frontage which

incorporates two shop frontages.

Three shops occupy the south western portion of the Clare

Street frontage

Fitout comprises stone tiled and timber floors, stone tiled walls

and decorative set ceilings incorporating down lighting

Upper Levels

Upper levels are occupied by office accommodation which is

generally of similar design and layout on all levels

A central atrium style stairwell is located between levels 2-6

Fitout includes carpeted floors, a combination of suspended

acoustic tile ceilings incorporating T5 fluorescent lighting, fire

services and air return.

The air is ducted directly into a raised under floor plenum

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 1

Liability limited by a scheme approved under Professional Standards Legislation

6.4 Onsite Parking

There are 338 car parking bays situated over three split levels

including ground and basement. Access to the car park is gained

via Clare Street.

6.5 Building Areas

We have been provided with a tenancy schedule by the vendor's Due Diligence room which have been

adopted for the valuation and are outlined as follows:

Lettable Area

Office 14,816 sqm

Retail 1,281 sqm

Total 16,098 sqm

We have confirmed these areas by reviewing the survey plans provided.

6.6 Building Condition and Utility

The property comprises a modern well appointed asset incorporating large functional floorplates with

excellent natural light. The building was designed to the latest standards at the time of construction and

includes many energy efficient and sustainability features not normally incorporated into other regional style

head office facilities. As such we consider the asset still maintains high quality and efficiency levels in

comparison to newer assets.

We have not sighted a structural report on the property nor have we inspected unexposed or inaccessible

portions of the premises. We therefore cannot comment on the structural integrity, defect, rot or infestation of

the improvements nor can we comment on any knowledge of the use in construction of material such as

asbestos or other materials now considered hazardous.

We emphasise that we are not qualified building surveyors and as such our comments are subject to any

detailed survey, which would confirm the structural integrity of the improvements and services. Our valuation

assumes that there are no inherent defects with the structure or service installations and reflects the age and

apparent condition.

6.7 Occupational Health and Safety

We have not sighted an Occupational Health and Safety or Essential Services report, and have assumed the

property complies with all necessary Occupational Health and Safety and Essential Services requirements.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 2

Liability limited by a scheme approved under Professional Standards Legislation

7 Tenancy Details

Lease Synopsis

The subject property is currently subject to Lease Agreement(s). We have examined all of the lease(s) and

provided a précis of the main terms and conditions are summarised as follows:

Lessee: Transport Accident Commission

Status: Signed

Premises: GF Shop 2 & Lvls G-6

Lettable Area: 14,860.9 sqm

Permitted Use: Office and any other uses permitted by law

Term: 20 years

Commencement Date: 5 Jan 2009

Termination Date: 4 Jan 2029

Options to renew: 5+15

Review Structure: Fixed 3.50%

Passing Rent: $6,362,634 pa Part Net

Passing Rate $ psm/pcm: $428

Outgoings: $1,638,655 pa

Car Parking: 327 spaces

Lessee: Impact Investment Group

Status: Signed

Premises: GF Shop 1, GF Shop 3 and GF Shop 7

Lettable Area: 519.5 sqm

Permitted Use: Retail

Term: 5 years

Commencement Date: 18 Apr 2017

Termination Date: 17 Apr 2022

Options to renew: -

Review Structure: Fixed 3.50%

Passing Rent: $241,568 pa Part Net

Passing Rate $ psm/pcm: $465

Outgoings: $51,702

Car Parking: 4 spaces

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 3

Liability limited by a scheme approved under Professional Standards Legislation

Lessee: Fernwood Investments Pty Ltd

Status: Signed

Premises: GF Shop 4 & 5

Lettable Area: 482.3 sqm

Permitted Use: Retail

Term: 7 years

Commencement Date: 1 Mar 2016

Termination Date: 28 Feb 2023

Options to renew: 5+5 years

Review Structure: Fixed 3.50%

Passing Rent: $156,000 pa Gross

Passing Rate $ psm/pcm: $323 psm

GST

All existing lease documentation contains Goods and Services Tax (GST) clauses which stipulate the Lessees

are responsible for the payment of GST in respect of the lease rental and all other goods and services

provided.

Occupancy Profile

% of gross passing

(fully let)

Current Vacancies Dec-17 $0 0.0%

Year 1 Dec-18 $21,850 0.2%

Year 2 Dec-19 $11,799 0.1%

Year 3 Dec-20 $0 0.0%

Year 4 Dec-21 $0 0.0%

Year 5 Dec-22 $301,430 3.2%

Year 6 Dec-23 $301,692 3.2%

Year 7 Dec-24 $0 0.0%

Year 8 Dec-25 $0 0.0%

Year 9 Dec-26 $0 0.0%

Year 10 Dec-27 $0 0.0%

$636,772 6.7%

Current Vacancy Summary

Office 0.0%

Car Parking 0.0%

Retail 0.0%

Miscellaneous 0.0%

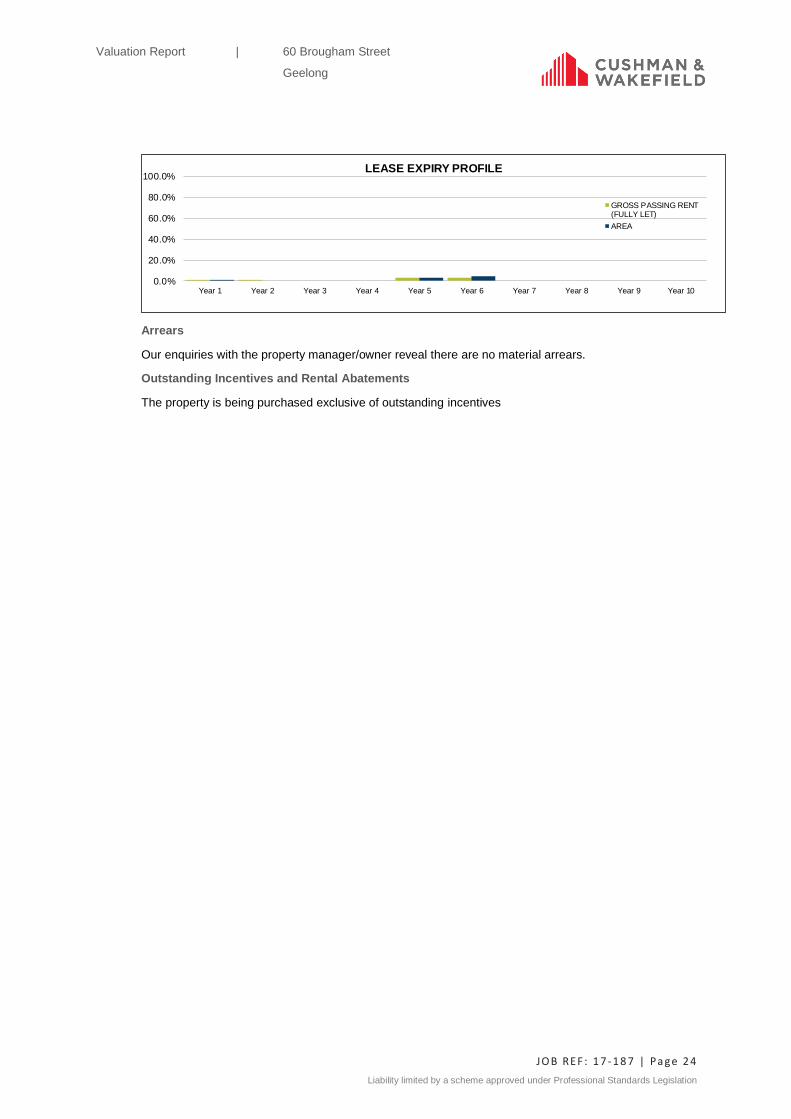

LEASE EXPIRY BY GROSS PASSING RENT (FULLY LET)

Lease Maturity Profile

Based on our analysis of the tenancy schedule and lease documentation we summarise the lease maturity

profile of the subject property as follows:

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 4

Liability limited by a scheme approved under Professional Standards Legislation

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

LEASE EXPIRY PROFILE

GROSS PASSING RENT(FULLY LET)

AREA

Arrears

Our enquiries with the property manager/owner reveal there are no material arrears.

Outstanding Incentives and Rental Abatements

The property is being purchased exclusive of outstanding incentives

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 5

Liability limited by a scheme approved under Professional Standards Legislation

Tenancy Schedule

We have been provided with a tenancy schedule by the vendor's Due Diligence material which has been adopted for the valuation and are outlined as follows. We reserve

the right to review our report should this information prove to be incorrect.

60 Brougham Street,

Geelong

Tenancy Schedule

TENANT LEVEL CATEGORY NLA CAR LEASE LEASE TERM OPTION LEASE PASSING RENT OUTGOINGS Recovery rate MARKET RENT RENT REVIEW CAP & COLLAR

(sqm) SPACES COMM EXPIRY YRS PERIOD(S) TYPE ($PA) ($psm) % RECOVERY ($PA) ($psm) ($psm) ($PA) LEASE NEXT BASIS %

(YEARS) ($pcm) $ ($pcm) ($pcm) TYPE

Impact Investment Group GF Shop 1 Retail 40.20 - 18-Apr-17 17-Apr-22 5.00 - Semi-Gross - - - $4,001 $4,001 $100 $99.5 $575 $23,115 Gross Face 18-Apr-18 Fixed % -

Transport Accident Commission GF Shop 2 Retail 43.70 - 17-Oct-16 31-Mar-18 1.45 - Gross $21,850 $500 - - $21,850 $500 $99.5 $525 $22,943 Gross Face - Fixed % -

Impact Investment Group GF Shop 3 Retail 25.90 - 18-Apr-17 17-Apr-22 5.00 - Semi-Gross - - - $2,578 $2,578 $100 $99.5 $575 $14,893 Gross Face 18-Apr-18 Fixed % -

Commonwealth Bank of Aust. ATM Miscellaneous 1.00 - 26-Nov-09 25-Nov-19 10.00 - Semi-Gross $11,799 $11,799 - - $11,799 $11,799 - $11,799 $11,799 Gross Face 26-Nov-18 Fixed % 4.00%

Fernwood Investments Pty Ltd GF Shop 4 & 5 Retail 482.30 - 1-Mar-16 28-Feb-23 7.00 5+5 Gross $156,000 $323 - - $156,000 $323 $92.8 $323 $156,000 Gross Face 1-Mar-18 Fixed % 3.50%

Rush Hour Café Pty Ltd GF Shop 6 Retail 13.80 - 4-Feb-13 3-Feb-23 10.00 5+5 Semi-Gross $22,510 $1,631 - $1,280 $23,791 $1,724 $92.8 $1,730 $23,874 Gross Face 4-Feb-18 Fixed % -

Impact Investment Group GF Shop 7 Retail 453.40 - 18-Apr-17 17-Apr-22 5.00 - Semi-Gross $241,568 $533 - $45,123 $286,691 $632 $99.5 $575 $260,705 Gross Face 18-Apr-18 Fixed % 3.50%

Rush Hour Café Pty Ltd GF Shop 12 Retail 222.10 - 4-Feb-13 3-Feb-23 10.00 5+5 Semi-Gross $101,296 $456 - $20,606 $121,902 $549 $92.8 $555 $123,266 Gross Face 4-Feb-18 Fixed % -

Transport Accident Commission G Office 870.60 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $372,585 $428 - $96,287 $468,872 $539 $110.6 $555 $483,183 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 1 Office 478.30 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $204,695 $428 - $52,899 $257,594 $539 $110.6 $555 $265,457 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 2 Office 2,001.90 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $856,739 $428 - $221,408 $1,078,147 $539 $110.6 $555 $1,111,055 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 3 Office 2,910.80 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $1,245,714 $428 - $321,931 $1,567,646 $539 $110.6 $555 $1,615,494 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 4 Office 2,881.70 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $1,233,261 $428 - $318,713 $1,551,973 $539 $110.6 $555 $1,599,344 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 5 Office 2,920.20 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $1,249,737 $428 - $322,971 $1,572,708 $539 $110.6 $555 $1,620,711 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission 6 Office 2,752.70 - 5-Jan-09 4-Jan-29 20 5+15 Semi-Gross $1,178,054 $428 - $304,445 $1,482,499 $539 $110.6 $555 $1,527,749 Gross Face 5-Jan-18 Fixed % 3.50%

. Office - - - - - - Net - - - - - - - $0 Net Face - Fixed % -

Transport Accident Commission Storeroom Miscellaneous 1.00 - 5-Jan-09 4-Jan-29 20 5+15 Gross $47,467 $47,467 - - $47,467 $47,467 $47,467 $47,467 Gross Face 5-Jan-18 Fixed % 3.50%

Fernwood Investements Pty Ltd (Perm.) Car Parking Car Parking - 3 1-Mar-16 28-Feb-23 7 5+5 Gross - - - - - - $170 $6,120 Gross Face 1-Mar-18 Fixed % 3.50%

Rush Hour Café Pty Ltd (Perm.) Car Parking Car Parking - 3 4-Feb-13 3-Feb-23 10 5+5 Gross - - - - - - $170 $6,120 Gross Face 4-Feb-18 Fixed % -

Impact Investment Group (Perm.) Covered Car Parking Car Parking - 4 18-Apr-17 17-Apr-22 5 - Gross $8,160 $170 - - $8,160 $170 $170 $8,160 Gross Face 18-Apr-18 Fixed % 3.50%

Rush Hour Café Pty Ltd (Casual) Covered Car Parking Car Parking - 1 - - - - Gross $2,000 $167 - - $2,000 $167 $170 $2,040 Gross Face - Fixed % -

Transport Accident Commission (Perm.) Covered Car Parking Car Parking - 320 5-Jan-09 4-Jan-29 20 5+15 Gross $858,981 $224 - - $858,981 $224 $224 $858,981 Gross Face 5-Jan-18 Fixed % 3.50%

Transport Accident Commission (Casual)Covered Car Parking Car Parking - 7 - - - - Gross $18,790 $224 - - $18,790 $224 $224 $18,790 Gross Face - Fixed % -

TOTAL 16,098 338 $7,831,206 $486 0.00% $1,712,243 $9,543,448 $593 $609 $9,807,263

The above information is purely for the purposes of a broad guide and whilst we understand the facts to be generally reliable, we are unable to guarantee their accuracy. Liability limited by a scheme approved under Professional Standards Legislation

PASSING GROSS RENT

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 6

Liability limited by a scheme approved under Professional Standards Legislation

8 Financial Analysis

8.1 Income Summary

Area (sqm) / Passing Income Market Income Variance to Market

Car Spaces $ pa$psm

$pcm$ pa

$psm

$pcm$ pa %

Office 14,816 $6,340,784 $428 $8,222,991 $555 ($1,882,207) -29.7%

Car Parking 338 cars $887,931 $219 $900,211 $222 ($12,280) -1.4%

Retail 1,281 $543,224 $424 $624,795 $488 ($81,570) -15.0%

Miscellaneous 2 $59,266 $29,633 $59,266 $29,633 $0 0.0%

Outgoing Recoveries $1,712,243 $106.37 $0 $0 $1,712,243 100.0%

Total Gross Income $9,543,448 $593 $9,807,263 $609 ($263,814) -2.8%

Less Total Outgoings $1,871,101 $116 $1,871,101 $116

Net Income $7,672,348 $477 $7,936,162 $493 ($263,814) -3.4%

Gross Income on Vacant Areas $0

Gross Income on New Leases $0

Total Gross Income (Fully Leased) $9,543,448 $593

Net Income (Fully Leased) $7,672,348 $477

Income Category

8.2 Outgoing Expenses

We have been provided with budgeted outgoings by the vendor's Due Diligence material which have been

adopted for the valuation and are outlined as follows:

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 7

Liability limited by a scheme approved under Professional Standards Legislation

60 Brougham Street,

Geelong

OUTGOINGS

Year Ending: 30-Jun-18

Net Lettable Area: 16,098 sqm

Budget Budget ADOPTED ADOPTED PCA

ITEM 30-Jun-18 30-Jun-18

Benchmarks

St Kilda Rd

AMOUNT AMOUNT AMOUNT AMOUNT

( $ / PA ) $psm ( $ / PA ) $psm $psm

STATUTORY OUTGOINGS

Municipal / Council Rates $524,844 $32.60 $524,844 $32.60 $11.31

Water & Sewerage Rates $31,200 $1.94 $31,200 $1.94 $5.28

Land Tax $108,558 $6.74 $108,558 $6.74 $21.27

Fire Levy $91,632 $5.69 $91,632 $5.69 $2.12

- $0.00

Sub-Total $756,234 $46.98 $756,234 $46.98 $39.98

BUILDING OUTGOINGS

Insurance Premiums $40,680 $2.53 $40,680 $2.53 $4.48

Air Conditioning/Ventilation $173,430 $10.77 $173,430 $10.77 $7.44

Common Area Cleaning $197,340 $12.26 $197,340 $12.26 $15.35

Building Supervision $153,377 $9.53 $153,377 $9.53 $3.79

Window Cleaning - $0.00 - $0.00 -

Electricity $151,380 $9.40 $151,380 $9.40 $15.06

Fire Protection $35,051 $2.18 $35,051 $2.18 $4.31

Gas & Fuel $38,000 $2.36 $38,000 $2.36 $2.70

Lift & Escalators $42,348 $2.63 $42,348 $2.63 $4.41

4 Lifts - $0.00 - $0.00 $0.28

Repairs & Maintenance $136,360 $8.47 $136,360 $8.47 $7.95

Security $51,613 $3.21 $51,613 $3.21 $3.14

Telephone & Communication $7,380 $0.46 $7,380 $0.46 -

NABERS - $0.00 - $0.00 $0.68

Building Management Expenses $59,694 $3.71 $59,694 $3.71 $11.17

Public Liability $900

Miscellaneous $28,214 $1.75 $28,214 $1.75 $1.38

Sub-Total $1,115,767 $69.26 $1,114,867 $69.26 $82.14

NON-RECOVERABLE OUTGOINGS

Car park and truck area outgoings recovered - $0.00 - $0.00 -

Non-Recoverable Management Fees - $0.00 - $0.00 -

Non-Recoverable Other - $0.00 - $0.00 -

Total Non-Recoverable Outgoings $0 $0.00 $0 $0.00 $0.00

TOTAL OUTGOINGS $1,872,001 $116.23 $1,871,101 $116.23 $122.12

The adopted outgoings equate to $116 which is considered to fall within market parameters for a property of this age, nature and location.

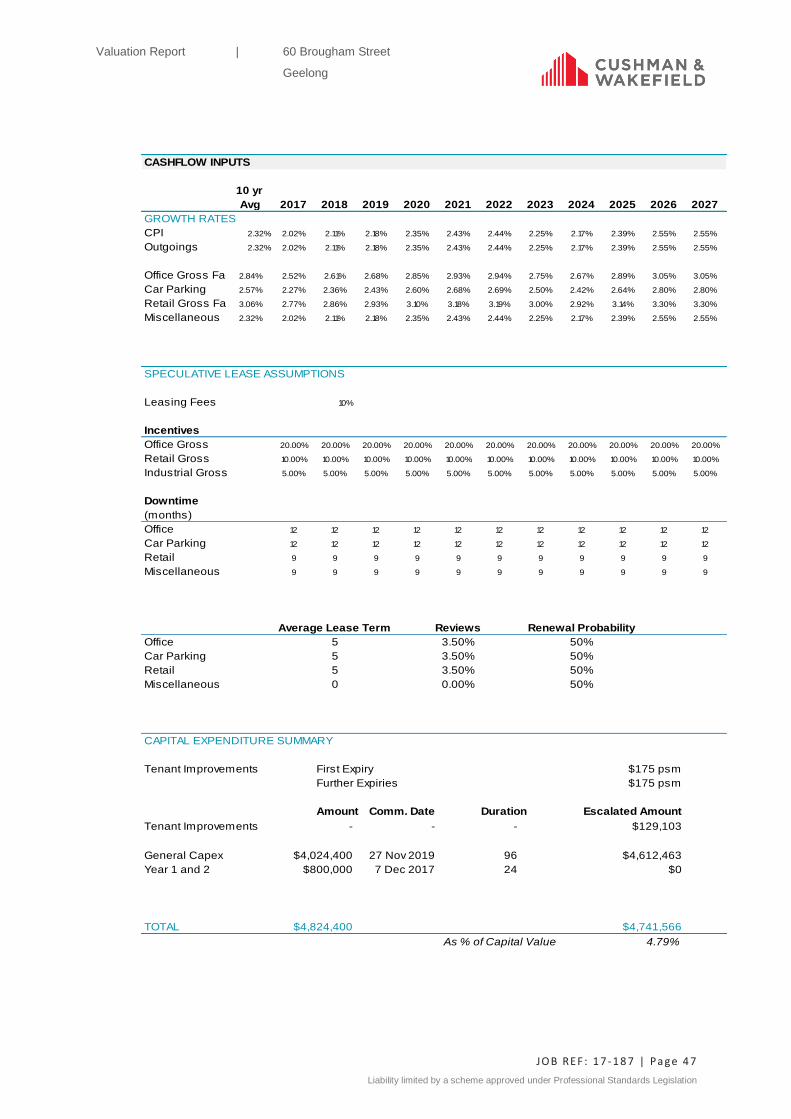

8.3 Capital Expenditure

We have not been provided with capital expenditure budgets, however have assessed and adopted the

following capital expenditure schedule for the valuation:

MAKE GOOD CAPITAL EXPENDITURE

Refurb costs for current vacancies $175 psm

1st Expiry $175 psm

2nd & Subsequent Expiries $175 psm

SCHEDULED CAPITAL EXPENDITURE $250 psm

CAPITAL EXPENDITURE INPUTS

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 8

Liability limited by a scheme approved under Professional Standards Legislation

CAPITAL EXPENDITURE SUMMARY

Description Comm Date Months End Date Current Cost Escalated Cost*

MAKE GOOD CAPITAL EXPENDITURE

Current Vacancies Dec-17 1 Dec-17 -

Year 1 Dec-17 12 Nov-18 $3,824

Year 2 Dec-18 12 Nov-19 -

Year 3 Dec-19 12 Nov-20 -

Year 4 Dec-20 12 Nov-21 -

Year 5 Dec-21 12 Nov-22 $50,122

Year 6 Dec-22 12 Nov-23 $70,768

Year 7 Dec-23 12 Nov-24 $4,389

Year 8 Dec-24 12 Nov-25 -

Year 9 Dec-25 12 Nov-26 -

Year 10 Dec-26 12 Nov-27 -

SCHEDULED CAPITAL EXPENDITURE

. - - - - -

General Capex Nov-19 96 Nov-27 $4,024,400 $4,612,463

Year 1 and 2 Dec-17 24 Dec-19 $800,000 $813,947

Total $4,824,400 $5,555,513

Capex (% value) 4.79%

* Costs are escalated from month 13 onwards.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 2 9

Liability limited by a scheme approved under Professional Standards Legislation

9 Market Commentary

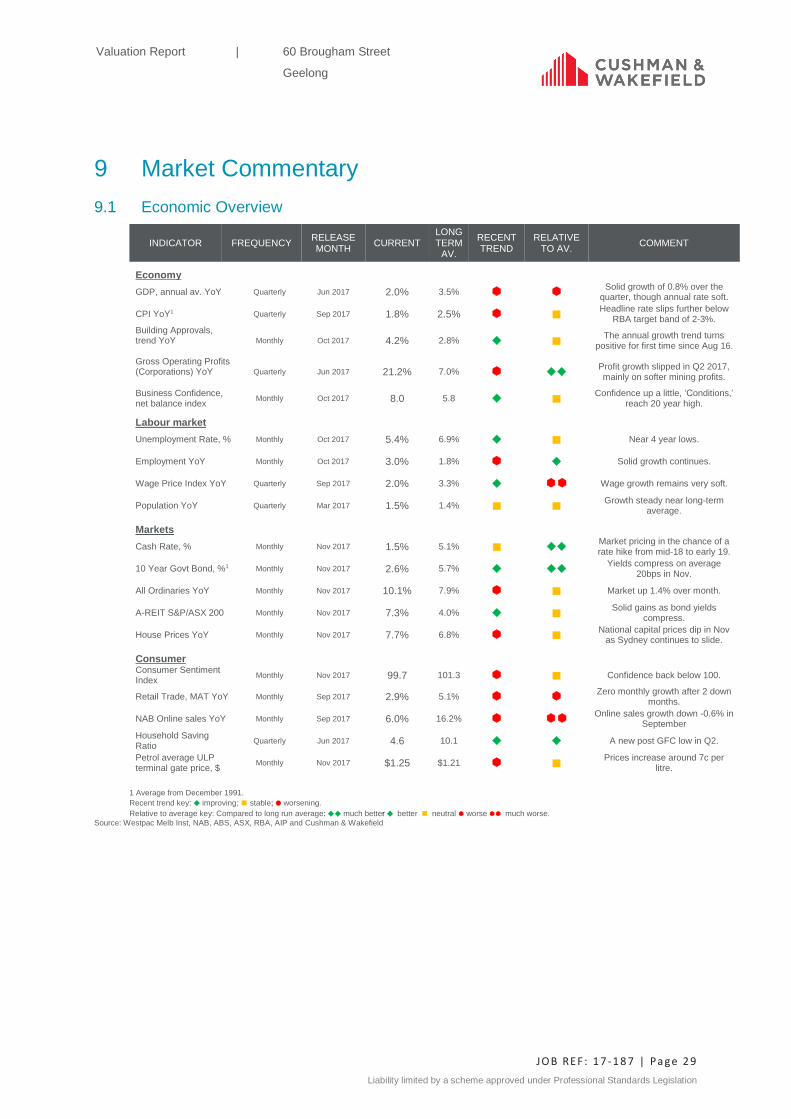

9.1 Economic Overview

INDICATOR FREQUENCY RELEASE MONTH

CURRENT LONG TERM

AV.

RECENT TREND

RELATIVE TO AV.

COMMENT

Economy

GDP, annual av. YoY Quarterly Jun 2017 2.0% 3.5% Solid growth of 0.8% over the

quarter, though annual rate soft.

CPI YoY1 Quarterly Sep 2017 1.8% 2.5% ◼ Headline rate slips further below

RBA target band of 2-3%.

Building Approvals, trend YoY

Monthly Oct 2017 4.2% 2.8% ◆ ◼ The annual growth trend turns

positive for first time since Aug 16.

Gross Operating Profits (Corporations) YoY

Quarterly Jun 2017 21.2% 7.0% ◆◆Profit growth slipped in Q2 2017, mainly on softer mining profits.

Business Confidence, net balance index

Monthly Oct 2017 8.0 5.8 ◆ ◼ Confidence up a little, ‘Conditions,’

reach 20 year high.

Labour market

Unemployment Rate, % Monthly Oct 2017 5.4% 6.9% ◆ ◼ Near 4 year lows.

Employment YoY Monthly Oct 2017 3.0% 1.8% ◆ Solid growth continues.

Wage Price Index YoY Quarterly Sep 2017 2.0% 3.3% ◆ Wage growth remains very soft.

Population YoY Quarterly Mar 2017 1.5% 1.4% ◼ ◼ Growth steady near long-term

average.

Markets

Cash Rate, % Monthly Nov 2017 1.5% 5.1% ◼ ◆◆ Market pricing in the chance of a rate hike from mid-18 to early 19.

10 Year Govt Bond, %1 Monthly Nov 2017 2.6% 5.7% ◆ ◆◆ Yields compress on average

20bps in Nov.

All Ordinaries YoY Monthly Nov 2017 10.1% 7.9% ◼ Market up 1.4% over month.

A-REIT S&P/ASX 200 Monthly Nov 2017 7.3% 4.0% ◆ ◼Solid gains as bond yields

compress.

House Prices YoY Monthly Nov 2017 7.7% 6.8% ◼ National capital prices dip in Nov

as Sydney continues to slide.

Consumer Consumer Sentiment Index

Monthly Nov 2017 99.7 101.3 ◼ Confidence back below 100.

Retail Trade, MAT YoY Monthly Sep 2017 2.9% 5.1% Zero monthly growth after 2 down

months.

NAB Online sales YoY Monthly Sep 2017 6.0% 16.2% Online sales growth down -0.6% in

September

Household Saving Ratio

Quarterly Jun 2017 4.6 10.1 ◆ ◆ A new post GFC low in Q2.

Petrol average ULP terminal gate price, $

Monthly Nov 2017 $1.25 $1.21 ◼ Prices increase around 7c per

litre.

1 Average from December 1991. Recent trend key: ◆ improving; ◼ stable; worsening.

Relative to average key: Compared to long run average: ◆◆ much better ◆ better ◼ neutral worse much worse.

Source: Westpac Melb Inst, NAB, ABS, ASX, RBA, AIP and Cushman & Wakefield

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 0

Liability limited by a scheme approved under Professional Standards Legislation

9.2 Regional Office Market Overview

The office market sector has continued to perform well in 2017 and has now reached new benchmark levels

for investment returns. This trend has been led by the CBD markets of primarily Sydney and Melbourne and to

a lesser degree Brisbane.

Driven by tenant demand Sydney and Melbourne have led the way in terms of lowering of investment

benchmarks. This in turn has also assisted the metropolitan markets in these cities which have also

demonstrated strong demand for both leasing and investment returns.

The regional office markets generally operate on different parameters to the metropolitan and CBD demand

drivers. Regional performance is based primarily upon specific local characteristics, primarily the drivers of the

local economy. This in turn drives population growth and employment demand.

Drivers of local regional economies can vary from industry and agricultural based activities to Defence

education, tourism and health.

Unlike their larger CBD and metro counterparts, regional economies tend to be more reliant upon one or two

drivers as opposed to a more diverse economic base. This in turn tends to have a more significant impact

upon a regional centre when the main driver changes. As a result regional markets often tend to swing more

than their urban counterparts. The broader the depth of a regional economy the more likely it is to withstand

change.

Prime regional office markets in Victoria are considered to be limited and are primarily

Geelong Bendigo

Wodonga Ballarat

Warrnambool

By far the most diverse and largest is Geelong being Victoria’s second largest city. It also contains the most

diverse economy with manufacturing, health (Waurn Ponds Private Hospital) and education (Deakin

University) prominent employment drivers.

Geelong has continued to grow generally in line with other major centres at an average of approximately

1.60% per annum. As at October 2017 the unemployment rate was 5.90% compared to the Victorian average

of 5.50%.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 1

Liability limited by a scheme approved under Professional Standards Legislation

Source ABS, Greater City of Geelong

According to Geelong council economic statistics the main drivers of the local economy are as follow

Health 16.00%

Education 10.80%

Manufacturing 13.00%

Retail Trade 14.50%

Source ABS, Greater City of Geelong

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 2

Liability limited by a scheme approved under Professional Standards Legislation

The above denotes that Geelong is a genuinely diverse economy unlike many other regional locations which

are focused on one major driver such as tourism or defence.

The ancillary businesses associated with Geelong’s main business drivers also tend to be more white collar or

office oriented offering potential for a broader office demand than the main occupiers themselves.

RENTS

Geelong’s economy and associated investment demand has suffered due to the closure of the main

employment driver namely the Ford factory in 2016. However, in saying this the economy is diverse with

significant sectors including healthcare, education, and government.

These have tended to support the continued structural change. Geelong is well located to the more urban

areas and also within close proximity to Avalon airport, all factors assisting its qualities as a drawcard.

The office market within Geelong is mixed. The traditional local market comprises established B grade assets

generally up to 3-5 levels. In conjunction with this property type, Geelong has an increasing number of

modern A grade office park/tower developments.

These include

Centrelink NDIA

Australian Taxation Office Worksafe

Transport Accident Commission

As a result, there is a split market for rentals in the city as follow

Modern local style office full and multiple floor $250-$350 psm

Institutional grade full floor and 1-3 levels $425-$475 psm

Institutional grade whole building $400-$450 psm

Geelong CBD average net office rental rates -Source Cushman & Wakefield Research

Incentive levels are variable and generally in the range of 15%-22.5%

INVESTMENT

The general market fundamentals for the CBD and suburban office markets have typically been positive with

limited new supply additions, improving demand and declining vacancies. The competition and lack of stock

in the CBD appears to have assisted the demand in the metropolitan markets and major regional markets.

The subject property sits as an investment grade asset. These can be very limited in many regional market

however Geelong has approximately 14 investment grade assets namely office properties above 10,000 sqm

of which 8 have transacted over the past five years, demonstrating a demand for larger quality assets in the

city.

The two assets currently under construction and the subject asset are considered above average non CBD

assets incorporating the latest building and sustainability technology and 5 Green Star rating.

However, demand for regional markets is not directly related to the urban markets. The best results for sales

of office properties in regional markets have tended to be secure long term investments.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 3

Liability limited by a scheme approved under Professional Standards Legislation

Whist yields in regional locations can vary materially due to specific local conditions there does appear to be a

more consistent trend between metropolitan and core regional assets subject to a longer term secure income

streams. Although local factors are still relevant there appears to be a general range of 50-100 basis points

above their urban counterparts.

Average investment parameters for investment grade assets with long term secure income profiles are

outlined below

LOCATION METROPOLITAN MAJOR REGIONAL

NSW 5.25%- 5.75% 6.25%-6.75%

VIC 5.25%-5.75% 6.25%- 7.00%

QLD 5.75%-6.25% 6.50%-7.25%

Average returns for investment grade office asset subject to long term leases- Source Cushman and Wakefield

OUTLOOK

The domestic Australian economy continues to perform well, in comparison to some major foreign economies.

Consumer and business confidence and unemployment are demonstrating some uncertainty but remain

generally steady whilst the housing market appears to have peaked.

Investor demand is extremely strong and recent sales evidence demonstrates a compressing of return

parameters between prime and secondary property. Investment returns are at benchmark levels.

As mentioned regional office markets are impacted upon by more local factors. We consider those

which offer a diverse economy and central location will be able to leverage off demand being seen in

metropolitan markets and offer an alternative to these locations.

We do not see the same pressure for investment returns as in the CBD and metro markets as a general

concept, however there has been strong evidence that quality assets subject to long term income

streams attract good interest.

In summary, although the office market is generally considered to be at a high point the depth of funds

and purchasers remains strong. We consider these factors will continue to influence the market in 2018

unless a change to economic fundamentals occurs.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 4

Liability limited by a scheme approved under Professional Standards Legislation

10 Market Evidence

In deriving a market value for the subject property we have analysed recent comparable properties. A

selection of the evidence used for the valuation is outlined as follows:

10.1 Rental Evidence

Office

There is limited evidence of large modern office accommodation similar to the subject in the immediate area.

There are however two new commercial assets similar to the subject upon which we have based our primary

evidence.

Address Comm Date

NLA (sq m)

Term (yrs)

Rental Rate ($/ sq m)

Type Reviews Incentive

1 Malop Street, Geelong

Worksafe Jan-18 14,400.0 15 $448 Net 3.75% Nil

Description: New office development incorporating an existing heritage building and ground level retail to be completed January 2018.

Comments: Located approximately 150 metres west of the subject. Considered a similar asset but overall slightly superior.

237 Ryrie Street, Geelong

Dept. of Treasury & Finance

Mar-17 603.4 3 $408 Net 4.00% Nil

Description: A modern style five level building incorporating ground level retail and upper level offices located in a core high street location.

Comments: Inferior improvements and materially smaller letting than subject.

Part Level 3, 1 Malop Street, Geelong

Dept. of Treasury & Finance

Jan-18 877.0 6+5 $460 Net 3.75% 15%

Description: New office development incorporating an existing heritage building and ground level retail to be completed January 2018.

Comments: Located approximately 150 metres west of the subject. Considered a similar asset but overall slightly superior.

43-45 Brougham Street, Geelong

NDIS Mar-17 1,943.0 2 $302 Net Undisc. Undisc.

Description: Situated within a three storey commercial office building with NAB occupying the ground floor. Refurbished established building. The rental includes 14 car bays.

Comments: Smaller inferior office building in comparison to the subject. Located directly opposite the subject property.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 5

Liability limited by a scheme approved under Professional Standards Legislation

Retail

There are several recent leases within the subject property which demonstrate a trend for the retail rents.

We also provide some further local examples in the following.

Address Comm Date

GLAR (sq m)

Term (yrs)

Rental Rate ($/ sq m)

Type Reviews Incentive

Lot 2, 6-8 Eastern Beach Road, Geelong

Dec-15 120.0 5+5 $608 Net 3% 1.60%

Description: Modern ground floor retail shop forming part of a multi level complex and occupied as a restaurant. Some kitchen fit out included in lease.

Comments: Prominent but non core location. Considered inferior to subject.

95 Malop St Geelong

Westpac Oct-15 237.0 7 $1,050 net CPI undiscl

Description: Bank branch within Westfield Geelong

Comments: Materially superior retail leasing within a regional retail centre.

95 Malop Street Geelong

Nov-15 115.0 5 $600 net CPI undiscl

Description: Bank branch within Westfield Geelong.

Comments: Materially superior retail leasing within a regional retail centre.

In addition to the above evidence there is also prelease to NDIA in a new development under construction at

13 Malop Street directly behind the subject property.

Details of this prelease are confidential however we have obtained general parameters as follow

Address NLA Proposed

Start date

Term Average Rental Rate on whole building

13-19 Malop Street 14,881 sqm 2019 20 yrs $455 psm net

Office estimate $490psm

We are also aware of a passing rental for the ATO in Ryrie Street outlined as follows

Address NLA Start Date Term Passing office rental rate

12-14 Little Ryrie Street 3,070 sqm 20 yrs $455 psm net

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 6

Liability limited by a scheme approved under Professional Standards Legislation

10.1.1 Rental Summary

Based upon evidence, including the above, we have adopted the following rentals for our valuation of the

subject property.

Office $555 psm Gross

Retail $323 psm to $575 psm Gross

Parking $2,040 pspa to $2,688 pspa Gross

Due to the specific recovery patterns on the part net leases we have adopted the above gross market

rates.

10.2 Sales Evidence

There are no sales within the immediate locality of similar sized and quality assets. We have obtained sales of

large modern commercial assets from other regional or metropolitan locations along the eastern seaboard.

Our evidence is outlined as follows

2 Kendall Street, Williams Landing

Sale Date: June 2017

Purchase Price: $58,230,000

Vendor: Cedar Woods

Purchaser: Centuria Metropolitan REIT

Lettable Area: 12,919 sqm

Site Area: 4,374 sqm

Parking: 384

Zoning: Priority Development zone

Occupancy: 100%

Major Tenant(s): Target WALE: 9.21 yrs

Analysis

Initial Yield: 6.49% Equivalent Yield: 6.49%

Sale Price psm (Lettable Area):

$4,507

IRR: 7.59% Terminal Yield: 6.75%

Compound Market Growth:

2.83%

Comments

Description

Presale of an eight level commercial office development which is now under construction within one of Melbourne's new residential growth suburbs. The property is conveniently located directly opposite the Williams Landing Rail Station and provides easy access to the Princes Freeway. The locality will form part of the shopping centre precinct for Point Cook, Truganina and Laverton suburbs.

Comparison

Located closer to Melbourne city than subject but located in a less mature location. Similar long term lease as subject but a smaller asset.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 7

Liability limited by a scheme approved under Professional Standards Legislation

800 Toorak Road, Hawthorn East

Sale Date: January 2017

Purchase Price: $281,000,000

Vendor: Investa

Purchaser: Charter Hall

Lettable Area: 41,898 sqm

Parking: 2449

Zoning: Comprehensive Development Zone

Occupancy: 100%

Major Tenant(s): Coles WALE: 13.20 yrs

Analysis

Initial Yield: 5.63% Equivalent Yield: 5.63%

Sale Price psm (Lettable Area):

$6,707

IRR: 7.07% Terminal Yield: 6.38%

Compound Market Growth:

3.29%

Comments

Description

A grade office complex built circa 1996. The accommodation comprises six (6) levels of office accommodation in association with 2,449 undercover and on grade car bays. Comparison

Superior location in metropolitan Melbourne and comprising a materially larger asset. With a slightly longer WALE. The sale was for the purchase of 50% stake in the interest.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 8

Liability limited by a scheme approved under Professional Standards Legislation

1231-1241 Sandgate Road, Nundah

Sale Date: April 2017

Purchase Price: $106,250,000

Vendor: Growthpoint Properties Australia

Purchaser: Centuria Property Funds Limited

Lettable Area: 12,980 sqm

Site Area: 5,597 sqm

Parking: 144

Zoning: MC Major centre

Occupancy: 100%

Major Tenant(s): Energex WALE: 9.58 yrs

Analysis

Initial Yield: 6.83% Equivalent Yield: 6.58%

Sale Price psm (Lettable Area):

$8,186

IRR: 7.90% Terminal Yield: 7.00%

Compound Market Growth:

2.94%

Comments

Description

A-grade office facility erected circa 2011. The accommodation comprises ground and part level 1 retail in association with six (6) levels of office accommodation and basement parking for 144 vehicles. The property is 67% leased to Energex Ltd, a Queensland government corporate entity, and is centrally located in an established inner metropolitan Brisbane commercial precinct.

Comparison

Similar style of asset in metropolitan Brisbane location. Similar WALE.

Valuation Report | 60 Brougham Street

Geelong

JO B REF : 1 7 - 1 8 7 | Pa ge 3 9

Liability limited by a scheme approved under Professional Standards Legislation

41 O'Connell Terrace, Bowen Hills

Sale Date: September 2016

Purchase Price: $52,000,000

Vendor: City of Brisbane Investment Corporation Pty Ltd

Purchaser: MHPHA Bowen Hills Pty Ltd

Lettable Area: 7,564 sqm

Parking: 129

Zoning: EC Emerging Community

Occupancy: 100% WALE: 17.9 yrs

Major Tenant(s): State Government (Qld Health) & Brisbane City Council

Analysis

Initial Yield: 6.39% Equivalent Yield: 6.72%

Sale Price psm (Lettable Area):

$6,875