value added tax (vat) - - get a free blog here

TRANSCRIPT

Taxation Summary for AY 2013-14

Page 1 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

VALUE ADDED TAX (VAT) INTRODUCTION:-

Every Sovereign state is in need of a large amount of revenue to meet its cost of administration.

Such Revenues are usually raised by the States in the form of various taxes.

Such taxes are of two types Direct Taxes, Indirect Taxes

Direct Taxes : Tax incidence directly falls on the payers and which cannot be passed on to any body else. Ex : Income tax, Wealth tax.

Indirect Taxes : Tax burden is passed on to ultimate

consumers.

Ex : VAT,Custom duties, Excise duties etc.

Meaning of VAT VAT is a Tax levied on the value added at each stage. Thus, it is a multistage tax with a provision for granting set off(credit) of

the tax paid at the earlier stage. It is also termed as “Consumption type” tax and works on the principle of ‘tax credit system’.

Variants of VAT (a). Gross product variant

*Allows deductions for taxes on all

purchases of raw materials and

components,

*No deduction is allowed for taxes on

capital inputs.

So, capital goods carry a heavier tax

burden as they are taxed twice.

Modernization and upgrading of P & M is

delayed due to this double tax treatment.

(b) Income Variant

*Allows for deductions on purchase of

raw materials and components as well

as depreciation on capital goods.

However, selecting the method of

measuring depreciation is difficult as

depreciation basically depends on the

life of an asset as well as on the rate of

inflation.

(c)Consumption variant

*Allows for deduction on all purchases

including capital assets.

*No distinction is made between capital

and, current expenditure as gross

investment is deductible in calculating

value added.

*Among the three varieties of VAT, the

consumption variant is widely used by

several countries because of the following

merits.

(1)It does not affect decisions regarding

investment because the tax on capital

goods is also set off against the VAT

liability.

(2)From the administrative point of view

the consumption variant is convenient as

there is no need to distinguish between

purchases of capital goods and

consumption goods.

Methods for Computation of VAT Addition Method :

*This method aggregates all the factor

payments including profits to arrive at the

total value addition.

*On that total, rate is applied to calculate

the tax. This type of calculation is mainly

used with income variant of VAT.

*A drawback of this method is that it does

not facilitate matching of invoices for

detecting.

Invoice Method :-

*This is the most common and Popular

method for computing tax liability.

*Tax is imposed at each stage of sale

on the entire sales value and the tax

paid at the earlier stage is allowed as

set-off.

*In India, this method is followed

under Central Excise Law.This method

is also called the “Tax Credit Method”

or “Voucher Method”.

*Under this method, possibility of tax

evasion will be reduced to a minimum

Subtraction Method

*Here tax is charged only on the value

added at each stage of the sale of goods.

*Value adopted is simply taken as the

difference between sales and purchases.

*Since, the total value of goods sold is not

taken into account, the question of grant of

claim for set-off or tax credit does not

arise.

*The tax liability arrived under this

method will remain the same as in the

invoice method as long as the same rate of

tax is attracted on all inputs.

Taxation Summary for AY 2013-14

Page 2 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

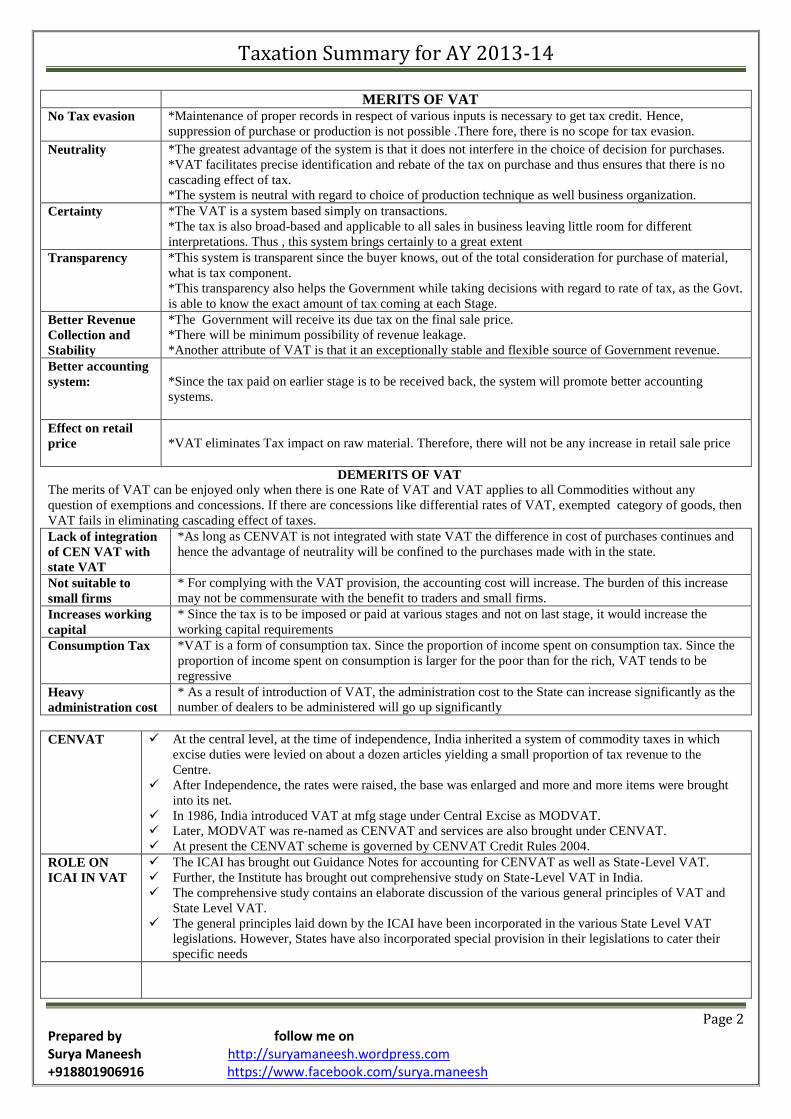

MERITS OF VAT

No Tax evasion *Maintenance of proper records in respect of various inputs is necessary to get tax credit. Hence,

suppression of purchase or production is not possible .There fore, there is no scope for tax evasion.

Neutrality *The greatest advantage of the system is that it does not interfere in the choice of decision for purchases.

*VAT facilitates precise identification and rebate of the tax on purchase and thus ensures that there is no

cascading effect of tax.

*The system is neutral with regard to choice of production technique as well business organization.

Certainty

*The VAT is a system based simply on transactions.

*The tax is also broad-based and applicable to all sales in business leaving little room for different

interpretations. Thus , this system brings certainly to a great extent

Transparency

*This system is transparent since the buyer knows, out of the total consideration for purchase of material,

what is tax component.

*This transparency also helps the Government while taking decisions with regard to rate of tax, as the Govt.

is able to know the exact amount of tax coming at each Stage.

Better Revenue

Collection and

Stability

*The Government will receive its due tax on the final sale price.

*There will be minimum possibility of revenue leakage.

*Another attribute of VAT is that it an exceptionally stable and flexible source of Government revenue.

Better accounting

system:

*Since the tax paid on earlier stage is to be received back, the system will promote better accounting

systems.

Effect on retail

price

*VAT eliminates Tax impact on raw material. Therefore, there will not be any increase in retail sale price

DEMERITS OF VAT

The merits of VAT can be enjoyed only when there is one Rate of VAT and VAT applies to all Commodities without any

question of exemptions and concessions. If there are concessions like differential rates of VAT, exempted category of goods, then

VAT fails in eliminating cascading effect of taxes.

Lack of integration

of CEN VAT with

state VAT

*As long as CENVAT is not integrated with state VAT the difference in cost of purchases continues and

hence the advantage of neutrality will be confined to the purchases made with in the state.

Not suitable to

small firms

* For complying with the VAT provision, the accounting cost will increase. The burden of this increase

may not be commensurate with the benefit to traders and small firms.

Increases working

capital

* Since the tax is to be imposed or paid at various stages and not on last stage, it would increase the

working capital requirements

Consumption Tax *VAT is a form of consumption tax. Since the proportion of income spent on consumption tax. Since the

proportion of income spent on consumption is larger for the poor than for the rich, VAT tends to be

regressive

Heavy

administration cost

* As a result of introduction of VAT, the administration cost to the State can increase significantly as the

number of dealers to be administered will go up significantly

CENVAT At the central level, at the time of independence, India inherited a system of commodity taxes in which

excise duties were levied on about a dozen articles yielding a small proportion of tax revenue to the

Centre.

After Independence, the rates were raised, the base was enlarged and more and more items were brought

into its net.

In 1986, India introduced VAT at mfg stage under Central Excise as MODVAT.

Later, MODVAT was re-named as CENVAT and services are also brought under CENVAT.

At present the CENVAT scheme is governed by CENVAT Credit Rules 2004.

ROLE ON

ICAI IN VAT

The ICAI has brought out Guidance Notes for accounting for CENVAT as well as State-Level VAT.

Further, the Institute has brought out comprehensive study on State-Level VAT in India.

The comprehensive study contains an elaborate discussion of the various general principles of VAT and

State Level VAT.

The general principles laid down by the ICAI have been incorporated in the various State Level VAT

legislations. However, States have also incorporated special provision in their legislations to cater their

specific needs

Taxation Summary for AY 2013-14

Page 3 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

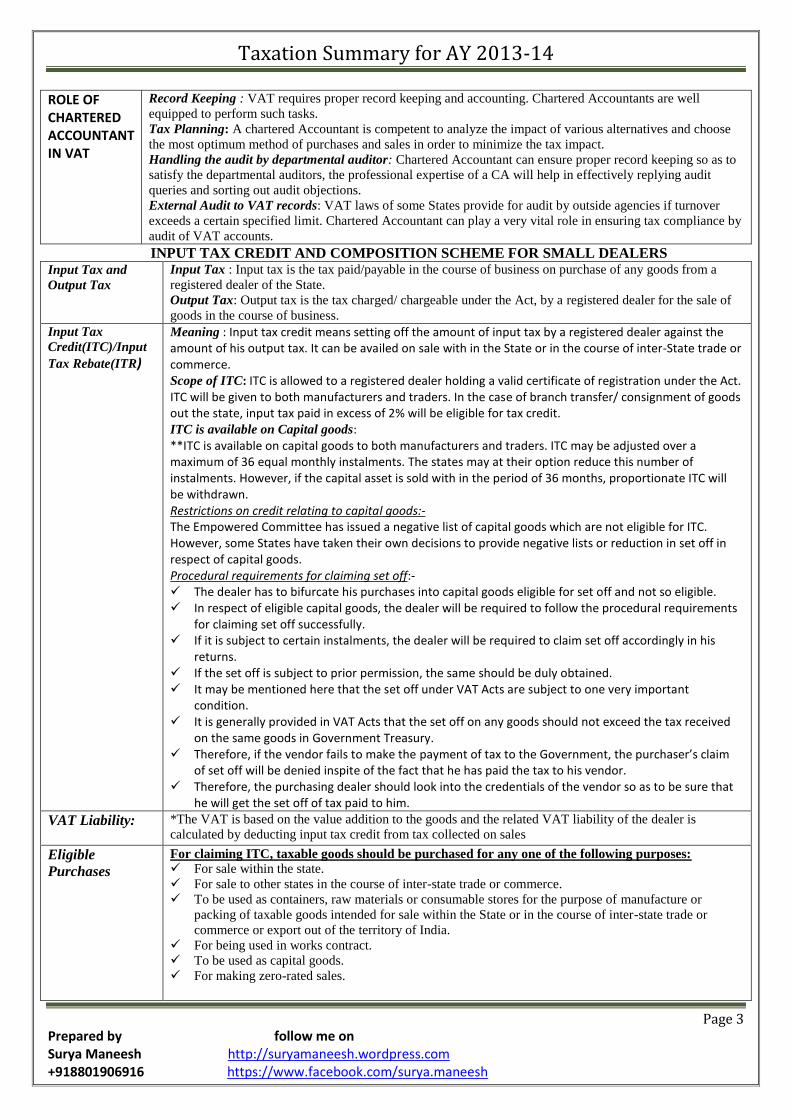

ROLE OF CHARTERED ACCOUNTANT IN VAT

Record Keeping : VAT requires proper record keeping and accounting. Chartered Accountants are well

equipped to perform such tasks.

Tax Planning: A chartered Accountant is competent to analyze the impact of various alternatives and choose

the most optimum method of purchases and sales in order to minimize the tax impact.

Handling the audit by departmental auditor: Chartered Accountant can ensure proper record keeping so as to

satisfy the departmental auditors, the professional expertise of a CA will help in effectively replying audit

queries and sorting out audit objections.

External Audit to VAT records: VAT laws of some States provide for audit by outside agencies if turnover

exceeds a certain specified limit. Chartered Accountant can play a very vital role in ensuring tax compliance by

audit of VAT accounts.

INPUT TAX CREDIT AND COMPOSITION SCHEME FOR SMALL DEALERS Input Tax and

Output Tax

Input Tax : Input tax is the tax paid/payable in the course of business on purchase of any goods from a

registered dealer of the State.

Output Tax: Output tax is the tax charged/ chargeable under the Act, by a registered dealer for the sale of

goods in the course of business.

Input Tax

Credit(ITC)/Input

Tax Rebate(ITR)

Meaning : Input tax credit means setting off the amount of input tax by a registered dealer against the amount of his output tax. It can be availed on sale with in the State or in the course of inter-State trade or commerce. Scope of ITC: ITC is allowed to a registered dealer holding a valid certificate of registration under the Act. ITC will be given to both manufacturers and traders. In the case of branch transfer/ consignment of goods out the state, input tax paid in excess of 2% will be eligible for tax credit. ITC is available on Capital goods: **ITC is available on capital goods to both manufacturers and traders. ITC may be adjusted over a maximum of 36 equal monthly instalments. The states may at their option reduce this number of instalments. However, if the capital asset is sold with in the period of 36 months, proportionate ITC will be withdrawn. Restrictions on credit relating to capital goods:- The Empowered Committee has issued a negative list of capital goods which are not eligible for ITC. However, some States have taken their own decisions to provide negative lists or reduction in set off in respect of capital goods. Procedural requirements for claiming set off:- The dealer has to bifurcate his purchases into capital goods eligible for set off and not so eligible. In respect of eligible capital goods, the dealer will be required to follow the procedural requirements

for claiming set off successfully. If it is subject to certain instalments, the dealer will be required to claim set off accordingly in his

returns. If the set off is subject to prior permission, the same should be duly obtained. It may be mentioned here that the set off under VAT Acts are subject to one very important

condition. It is generally provided in VAT Acts that the set off on any goods should not exceed the tax received

on the same goods in Government Treasury. Therefore, if the vendor fails to make the payment of tax to the Government, the purchaser’s claim

of set off will be denied inspite of the fact that he has paid the tax to his vendor. Therefore, the purchasing dealer should look into the credentials of the vendor so as to be sure that

he will get the set off of tax paid to him.

VAT Liability:

*The VAT is based on the value addition to the goods and the related VAT liability of the dealer is

calculated by deducting input tax credit from tax collected on sales

Eligible

Purchases

For claiming ITC, taxable goods should be purchased for any one of the following purposes:

For sale within the state.

For sale to other states in the course of inter-state trade or commerce.

To be used as containers, raw materials or consumable stores for the purpose of manufacture or

packing of taxable goods intended for sale within the State or in the course of inter-state trade or

commerce or export out of the territory of India.

For being used in works contract.

To be used as capital goods.

For making zero-rated sales.

Taxation Summary for AY 2013-14

Page 4 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

Common goods used for taxable goods and tax free:-

**Taxable goods means goods other than the goods which are specified in the Schedule for

tax-free goods. Where the purchased goods are used partially for the purposes specified then ITC

shall be allowed proportionally to the extent the purchases are used. Purchase not

eligible for ITC:

Purchases from unregistered dealers

Purchases from registered dealers who opt for composition scheme.

Goods used for personal use or provided as free of charge as gifts.

Purchase of goods as may be notified by the Government.

Where the purchase invoice is not available.

Goods purchased from other countries or other states.

Where there is evidence that the purchase invoice is a fake one.

Where the invoice does not show the amount of tax separately

Goods which are used in the manufacture of exempted goods.

Goods on which tax was paid under an earlier Act but under VAT they are covered under exempted

items.

Carrying over of

ITC

ITC is first to be utilized for payment of VAT. The excess credit can be then adjusted against the CST.

After the adjustment of VAT and CST, excess credit, if any, will be carried over to the end of the next

year. If there is any excess unadjusted input tax credit at the second year, then the same will be eligible

for refund. However, some states have decided to grant refund after the end of the first financial year

itself.

Refund to

exporters

Under the basic design of the White Paper, refund of ITC to exporters is granted within 3 months from

the end of the period in which the transaction for export took place.

Exemption/Refund

to SEZ/EOU

Units located in SEZ and EOU are granted either exemption from payment of input tax or refund of input tax within 3 months. However, State Governments may reduce the period of 3 months.

COMPOSITION SCHEME FOR SMALL DEALERS Principle Small dealers with annual gross turnover not exceeding Rs.50 lakhs shall have the option for a

composition scheme with payment of tax at a small percentage of gross turnover. Threshold

exemption Limit

Registration for VAT will not be compulsory for small dealers below threshold (Rs.5 lakhs) turnover,

and there will be a provision of an optional and simple composite scheme of taxation of small

percentage of gross turnover.

However, the States are allowed to increase the threshold limit to Rs.10 lakhs with the condition that

the concerned State should bear the revenue loss on account of increase in the limit beyond Rs.5 lakhs.

State Laws to

provide for

composition

Scheme

The States have to provide composition scheme for small dealers whose total turnover exceeds Rs.10

lakhs but does not exceed Rs.50 lakhs. Such a dealer shall have the option for a composition scheme

with payment of tax at a small percentage of gross turnover.

However, in such cases, a dealer shall not be authorized to issue vatable invoices. The rate of

composition tax may be as low as 0.25%. Further, the tax can be levied on taxable turnover instead of

gross turnover. Besides this, the State Government may frame different types of schemes for different

classes of customers

Features of

Composition

Scheme

Features:

The decision to join the Scheme is an individual decision of the dealer.

Payment of very small amount of tax.

Filling of simple return.

Advantages:

It saves a lot of labour and effort in keeping records.

It simplifies calculation of tax liabilities of dealer.

Disadvantages:

The dealer cannot avail input tax credit on inputs.

The dealer cannot issue vatable invoices.

Eligibility for the

Composition

Scheme

Every registered dealer whose turnover does not exceed Rs.50 lakhs in the last financial year is generally

entitled to avail the scheme.

However, the following are not eligible for the composition scheme:

A manufacturer or a dealer who sells goods in the course of inter-State trade or commerce; or

A dealer who sells goods in the course of import into or export out of the territory of India.

Taxation Summary for AY 2013-14

Page 5 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

A dealer transferring goods outside the State otherwise than by way of sale or for execution of

works contract.

Exercising of

Option

A dealer who intends to avail composition scheme shall exercise the option in writing in the year in

which he gets himself registered.

For this, the dealer has to intimate to the Commissioner. If the dealer avails this scheme, he need not

maintain any statutory records as prescribed under the Act. Only the records for purchase, sales,

inventory should be maintained.

The dealer should not have any stock of goods which were brought from outside the State on the day he

exercises his option to pay tax by way of composition and shall not use any goods brought from outside

the State after such date.

The dealer should also not claim ITC on the inventory available on the date on which he opts for

composition scheme. VAT Chain under

Composition

Scheme

Loss to the Seller

If the composition scheme is availed by a dealer then such dealer cannot avail input tax credit on purchases

made by him. He cannot pass on the benefit of ITC.

Loss to the Purchaser

The purchaser shall not get any tax credit for the purchases made by him from the dealer operating under

the composition scheme.

VAT PROCEDURES

REGISTRATION

Meaning :

Registration is the process of obtaining certificate of registration (RC) from the authorities under the

VAT Acts. A dealer registered under the VAT Act is called a registered dealer. No dealer should carry

on the business of purchase and sale of goods unless he is registered and holds a valid RC.

Eligibility for

Registration:

Registration is compulsory for those dealers (a dealer means any person, who in connection with or in

the course of his business, buys or sells goods for a consideration or otherwise) whose gross annual

turnover is above Rs.5 lakhs. All existing dealers will be automatically registered under the VAT Act. A

new dealer will be allowed 30 days time from the date of liability to get registered. An application for

registration should be made to the VAT Commissioner.

Compulsory

registration:

If a dealer fails to obtain registration under the VAT Act, he may be registered compulsorily by the

Commissioner. In this event the dealer has to pay such amount of tax as assessed by the Commissioner

with the available evidence. Further, failure to get registered shall result in attracting penalty and

forfeiture of eligibility to set off all ITC related to the period prior to the compulsory registration.

Voluntary

registration

A dealer otherwise not eligible for registration may also obtain registration if the Commissioner is

satisfied that the business of the applicant requires registration. The Commissioner may also impose any

terms or conditions that he thinks fit.

Cancellation of

registration

The registration can be cancelled on:

Discontinuance of business

Disposal of business

Transfer of business to a new location or

Annual turnover of the dealer falls below the specified amount.

TIN (TIN) Tax Payer’s Identification Number is a code to identify a tax payer.

It is the registration number of the dealer.

It consists of 11 digit numerals throughout the country.

First two characters will represent the State code as used by the Union Ministry of Home Affairs.

The set-up of the next nine characters will be however different in different States.

TIN will help to cross check the information of sales and purchases among VAT tax payers.

VAT Invoice:

VAT Invoice is a document showing particulars of goods sold, tax charged and other details as may

be prescribed and issued by an authorized dealer.

The White Paper provides the following provisions in respect of VAT Invoice which are mandatory

and failure to comply will attract penalty:

Every registered dealer shall issue to the buyer a serially numbered tax invoice, cash memo or bill

with the prescribed particulars.

The tax invoice shall be dated and signed by the dealer or his regular employee.

The dealer shall keep a counterfoil or duplicate of such tax invoice.

Taxation Summary for AY 2013-14

Page 6 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

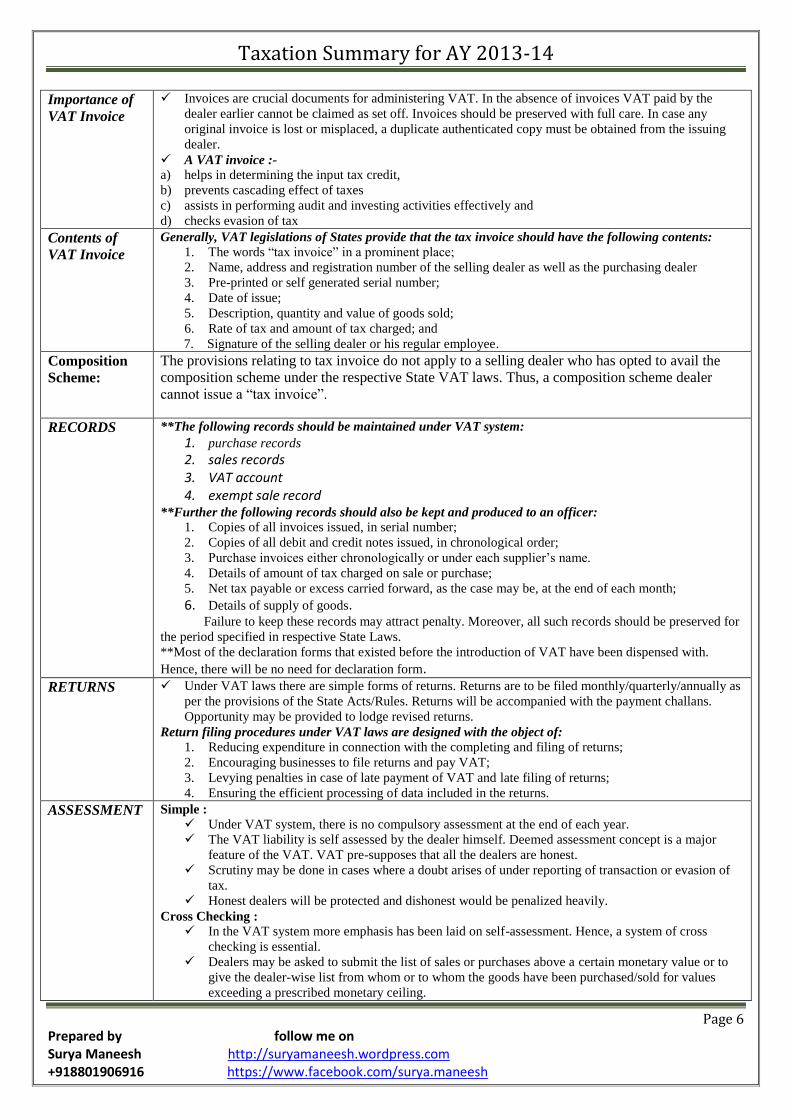

Importance of

VAT Invoice

Invoices are crucial documents for administering VAT. In the absence of invoices VAT paid by the

dealer earlier cannot be claimed as set off. Invoices should be preserved with full care. In case any

original invoice is lost or misplaced, a duplicate authenticated copy must be obtained from the issuing

dealer.

A VAT invoice :-

a) helps in determining the input tax credit,

b) prevents cascading effect of taxes

c) assists in performing audit and investing activities effectively and

d) checks evasion of tax

Contents of

VAT Invoice

Generally, VAT legislations of States provide that the tax invoice should have the following contents:

1. The words “tax invoice” in a prominent place;

2. Name, address and registration number of the selling dealer as well as the purchasing dealer

3. Pre-printed or self generated serial number;

4. Date of issue;

5. Description, quantity and value of goods sold;

6. Rate of tax and amount of tax charged; and

7. Signature of the selling dealer or his regular employee.

Composition

Scheme:

The provisions relating to tax invoice do not apply to a selling dealer who has opted to avail the

composition scheme under the respective State VAT laws. Thus, a composition scheme dealer

cannot issue a “tax invoice”.

RECORDS

**The following records should be maintained under VAT system:

1. purchase records 2. sales records 3. VAT account 4. exempt sale record

**Further the following records should also be kept and produced to an officer:

1. Copies of all invoices issued, in serial number;

2. Copies of all debit and credit notes issued, in chronological order;

3. Purchase invoices either chronologically or under each supplier’s name.

4. Details of amount of tax charged on sale or purchase;

5. Net tax payable or excess carried forward, as the case may be, at the end of each month;

6. Details of supply of goods. Failure to keep these records may attract penalty. Moreover, all such records should be preserved for

the period specified in respective State Laws.

**Most of the declaration forms that existed before the introduction of VAT have been dispensed with.

Hence, there will be no need for declaration form. RETURNS Under VAT laws there are simple forms of returns. Returns are to be filed monthly/quarterly/annually as

per the provisions of the State Acts/Rules. Returns will be accompanied with the payment challans.

Opportunity may be provided to lodge revised returns.

Return filing procedures under VAT laws are designed with the object of:

1. Reducing expenditure in connection with the completing and filing of returns;

2. Encouraging businesses to file returns and pay VAT;

3. Levying penalties in case of late payment of VAT and late filing of returns;

4. Ensuring the efficient processing of data included in the returns.

ASSESSMENT Simple :

Under VAT system, there is no compulsory assessment at the end of each year.

The VAT liability is self assessed by the dealer himself. Deemed assessment concept is a major

feature of the VAT. VAT pre-supposes that all the dealers are honest.

Scrutiny may be done in cases where a doubt arises of under reporting of transaction or evasion of

tax.

Honest dealers will be protected and dishonest would be penalized heavily.

Cross Checking : In the VAT system more emphasis has been laid on self-assessment. Hence, a system of cross

checking is essential.

Dealers may be asked to submit the list of sales or purchases above a certain monetary value or to

give the dealer-wise list from whom or to whom the goods have been purchased/sold for values

exceeding a prescribed monetary ceiling.

Taxation Summary for AY 2013-14

Page 7 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh

A cross checking computerized system is being worked out on the basis of coordination between the

tax authorities of Central Excise and income-tax. This cross checking system will help reduce tax

evasion and also lead to significant growth of tax revenue.

AUDIT Under VAT system considerable weightage is placed on audit work. Correctness of self-assessment will

be checked through a system of departmental audit.

A certain percentage of the dealers will be taken up for audit every year on a scientific basis.

The auditors will examine the correctness of the returns vis-à-vis the books of accounts of the dealer or

any other information available with them.

Officers of the higher rank will supervise to ensure that the audit work is done in a free, fearless and

impartial manner.

Apart from the departmental audit, many States have also incorporated the concept of audit of accounts

by chartered accounts.

However, auditing for all types of dealers may not be necessary. The selection of cases for auditing has

to be made in accordance with the criteria of the size of dealers.

In Maharashtra and Rajasthan, the dealer whose turnover exceeds Rs.40 lakhs in any year is required to

get his accounts audited in respect of such year.

PENAL

PROVISIONS

Since VAT is purely a State subject, States will have incorporated penal provisions as per their

requirements. However, these are in general more stringent than those in the earlier sales tax laws.

TAX RATES

UNDER VAT

Exempted Category

Under exempted category, there are about 50 commodities comprising of natural and unprocessed

products in unorganized sector, items which are legally barred from taxation and items which have social

implications.

4% Category

This category consists of items of basic necessities such as medicines and drugs, all agricultural and

industrial inputs, capital goods and declared goods. The schedule of commodities are attached to the

VAT Acts of the States.

12.5% Category

The remaining commodities fall under the general VAT rate of 12.5%.

1% Category

The special rate of 1% is meant for precious stones, bullion, gold and silver ornaments etc.

Non-VAT goods

Petrol, diesel, ATF, other motor spirit, liquor and lottery tickets are outside the VAT. The States

may or may not bring these commodities under VAT laws. However, it is agreed that all these

commodities will be subjected to 20% floor rate of tax.

OTHER

POINTS

Stock Transfer

Inter-State transfers do not involve sale and therefore they are not subjected to sales-tax. The

same position continues under VAT.

However, the tax paid on

(i) inputs used in the manufacture of finished goods which are stock transferred; or

(ii) purchases of goods which are stock transferred will be available as input tax credit after

retention of 2% of such tax by the State Governments.

Compensation for losses

Although the introduction of VAT may lead to revenue growth, there may be a loss of revenue in

some states in the initial years of transition.

Some of the State Governments were resistant to introduce VAT on account of this reason.

Therefore, the Government of India agreed to compensate for 100% of the loss in the 1st year, 75% of

the loss in the 2nd

year and 50% of the loss in the 3rd

year of introduction of VAT.

For latest updates and notes please follow me on by blog

http://suryamaneesh.wordpress.com/

Regards Surya Maneesh

Taxation Summary for AY 2013-14

Page 8 Prepared by follow me on Surya Maneesh http://suryamaneesh.wordpress.com +918801906916 https://www.facebook.com/surya.maneesh