valueguide july12 cover final - rakesh...

TRANSCRIPT

July 2012 Sharekhan ValueGuide2

Sharekhan ValueGuide July 20123

CONTENTS

Many a times, the equitymarkets tend to moveagainst the prevailingconsensus wisdom andconsequently catchmost market participantsby surprise. Just whenthe expectations had hita nadir and equities were threatening to tumble down to new yearly lowstowards the end of 2011, the Indian equity market had surged with anunexpected sharp rally at the beginning of the new year. This time aroundalso, the equity markets climbed the wall of worries to register smartgains in the month of June.

REGULAR FEATURES

Report Card 4

Earnings Guide I

TECHNICALS

Sensex 29

Stock Updates 18Sharekhan Special 25Sector Updates 27Viewpoint 28

From Sharekhan’s Desk EQUITY

06

Markets never fail to surprise FUNDAMENTALS

DERIVATIVES

View 30

TECHNICALS

Crude Oil 31Gold 32Silver 32

FUNDAMENTALSCopper 32Lead 32Zinc 33

Gold 34Silver 34Crude Oil 34

Copper 35Natural Gas 35Nickel 35

TECHNICALS

FUNDAMENTALS

USD-INR 37EUR-INR 37

GBP-INR 37JPY-INR 37

disclaimerDISCLAIMER: “This document has been prepared by Sharekhan Ltd.(SHAREKHAN) This Document is subject to changes without prior notice and is intended only for the person or entity to which it is addressed to and maycontain confidential and/or privileged material and is not for any type of circulation. Any review, retransmission, or any other use is prohibited. Kindly note that this document does not constitute an offer or solicitation for thepurchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. SHAREKHANwill not treat recipients as customers by virtue of their receiving this report. The information contained herein is from publicly available data or other sources believed to be reliable. While we would endeavour to update theinformation herein on reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current.Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. We do not represent that information contained herein is accurate or complete and it should not be reliedupon as such. This document is prepared for assistance only and is not intended to be and must not alone betaken as the basis for an investment decision. The user assumes the entire risk of any use made of this information.Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the meritsand risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake toadvise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. This report is not directedor intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contraryto law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions orto certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. SHAREKHAN & affiliates may have used the information set forthherein before publication and may have positions in, may from time to time purchase or sell or may be materially interested in any of the securities mentioned or related securities. SHAREKHAN may from time to time solicit from,or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to,computing or compiling the information have any liability for any damages of any kind. Any comments or statements made herein are those of the analyst and do not necessarily reflect those of SHAREKHAN.”

Sharekhan Ltd, Regd Add: 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway

Station, Kanjurmarg (East), Mumbai – 400 042, Maharashtra. Tel: 022 - 61150000. BSE Cash-INB011073351; F&O-

INF011073351; NSE – INB/INF231073330; CD - INE231073330; MCX Stock Exchange: CD - INE261073330 DP: NSDL-IN-DP-NSDL-

233-2003; CDSL-IN-DP-CDSL-271-2004; PMS INP000000662; Mutual Fund: ARN 20669. Sharekhan Commodities Pvt. Ltd.: MCX-

10080; (MCX/TCM/CORP/0425); NCDEX -00132; (NCDEX/TCM/CORP/0142)

COMMODITY

CURRENCY

PMS DESKProPrime - Top Equity 38ProPrime - Diversified Equity 39ProTech - Diversified 40ProTech - Nifty Thrifty 41ProTech - Trailing Stops 42

MUTUAL FUNDS DESK

Top MF Picks (equity) 44

Top SIP Fund Picks 45

RESEARCH BASED EQUITY PRODUCTS

Market Outlook 07Top Picks Basket 10Switch Ideas 14

INR-GBP 36INR-JPY 36

ADVISORY DESKMID Trades 43

INR-USD 36INR-EUR 36

Derivative Trades 43

July 2012 Sharekhan ValueGuide4

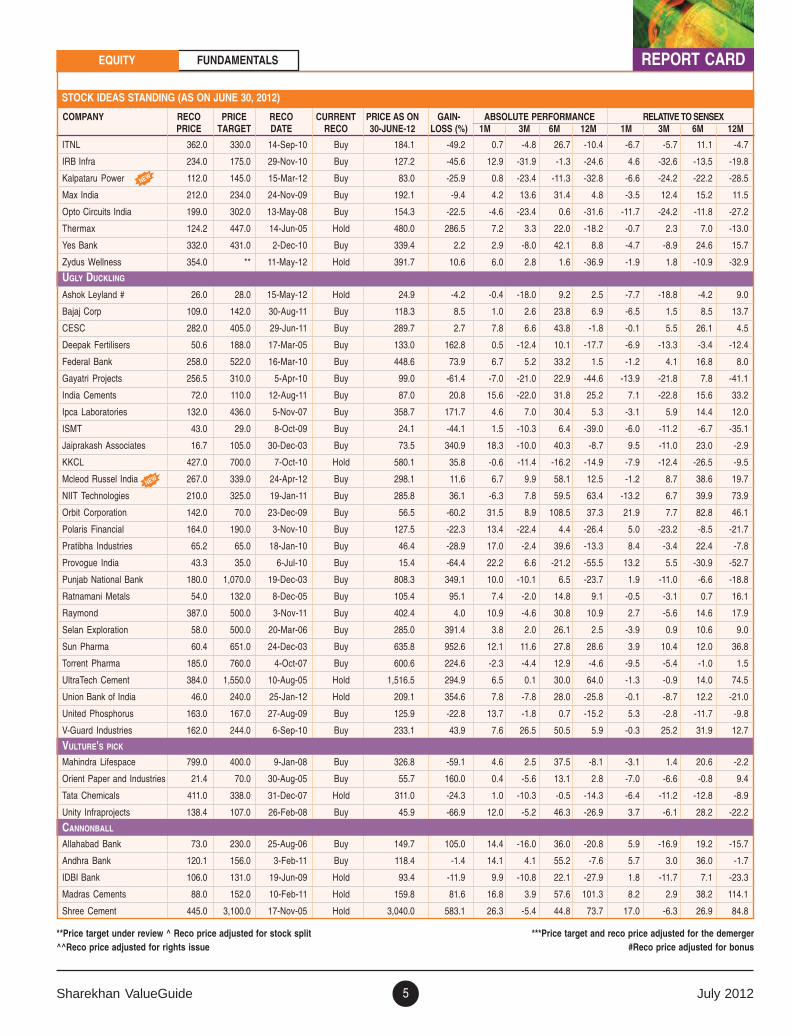

STOCK IDEAS STANDING (AS ON JUNE 30, 2012)

REPORT CARD

COMPANY RECO PRICE RECO CURRENT PRICE AS ON GAIN- ABSOLUTE PERFORMANCE RELATIVE TO SENSEXPRICE TARGET DATE RECO 30-JUNE-12 LOSS (%) 1M 3M 6M 12M 1M 3M 6M 12M

EVERGREEN

GSK Consumers 2,544.0 3,000.0 14-Dec-11 Buy 2,748.6 8.0 -2.5 -0.8 9.7 15.9 -9.7 -1.8 -3.9 23.3

HDFC 540.0 785.0 19-Nov-07 Buy 653.2 21.0 1.5 -1.3 1.9 -5.9 -6.0 -2.3 -10.7 0.1

HDFC Bank 71.6 570.0 23-Dec-03 Hold 563.6 687.1 12.2 9.3 33.1 12.9 3.9 8.1 16.7 20.1

Infosys 689.1 ** 30-Dec-03 Hold 2,509.2 264.1 3.3 -11.3 -8.1 -12.2 -4.3 -12.2 -19.4 -6.5

Larsen & Toubro 1,768.0 1,529.0 18-Feb-08 Buy 1,397.8 -20.9 19.2 6.8 40.5 -22.7 10.4 5.7 23.2 -17.7

Reliance Ind 283.5 800.0 5-Feb-04 Buy 737.9 160.3 4.6 -0.5 7.8 -16.9 -3.1 -1.5 -5.5 -11.6

Tata Consultancy Services 426.3 1,364.0 6-Mar-06 Buy 1,277.5 199.7 3.9 10.7 11.8 10.2 -3.8 9.6 -2.0 17.2

APPLE GREEN

Aditya Birla Nuvo 714.0 943.0 6-Dec-05 Buy 807.0 13.0 7.5 -14.6 9.0 -10.1 -0.5 -15.5 -4.4 -4.4

Apollo Tyres 37.0 91.0 27-Jul-09 Buy 79.0 113.5 -8.8 -0.8 33.7 1.6 -15.5 -1.8 17.2 8.1

Bajaj Auto 1,533.0 1,690.0 18-May-12 Hold 1,572.9 2.6 4.1 -6.3 -1.2 11.8 -3.6 -7.3 -13.3 18.9

Bajaj Finserv 545.0 703.0 26-Apr-08 Hold 684.4 25.6 4.4 11.9 59.4 33.1 -3.3 10.8 39.8 41.6

Bajaj Holdings 741.9 1,134.0 26-May-08 Buy 780.9 5.3 -0.8 -4.2 14.6 7.7 -8.1 -5.2 0.4 14.5

Bank of Baroda 239.0 865.0 22-Feb-12 Buy 732.9 206.7 9.0 -5.7 12.9 -14.0 1.0 -6.7 -1.1 -8.5

Bank of India 309.0 384.0 22-Feb-12 Hold 347.1 12.3 3.9 -2.3 33.0 -13.0 -3.7 -3.3 16.6 -7.4

Bharat Electronics 1,108.0 1,805.0 25-Sep-06 Buy 1,340.5 21.0 7.7 -12.1 0.0 -15.2 -0.2 -13.0 -12.3 -9.8

Bharat Heavy Electricals 120.4 250.0 11-Nov-05 Hold 232.5 93.1 9.6 -9.6 -1.7 -42.2 1.5 -10.5 -13.8 -38.5

Bharti Airtel 313.0 362.0 8-Jan-07 Buy 305.1 -2.5 0.8 -9.7 -11.2 -22.6 -6.6 -10.7 -22.1 -17.6

Corp Bank 218.0 564.0 19-Dec-03 Buy 417.3 91.4 5.4 3.0 25.0 -16.8 -2.3 2.0 9.6 -11.5

Crompton Greaves 50.4 123.0 19-Aug-05 Hold 121.2 140.5 8.2 -12.2 -3.5 -52.7 0.2 -13.1 -15.4 -49.7

Divi's Labs 767.0 1,122.0 31-May-11 Buy 1,025.2 33.7 9.8 33.8 32.0 30.2 1.7 32.4 15.7 38.5

GAIL 476.0 410.0 1-0ct-10 Buy 352.1 -26.0 9.6 -6.4 -7.5 -18.5 1.5 -7.4 -18.9 -13.3

Glenmark Pharmaceuticals 599.0 412.0 17-Jul-08 Buy 363.1 -39.4 1.8 17.4 23.7 14.6 -5.7 16.1 8.5 21.9

Godrej Consumer Products 145.0 590.0 7-May-09 Buy 574.4 296.1 -1.1 20.0 49.8 34.4 -8.4 18.8 31.3 43.0

Grasim 1,119.0 2,775.0 30-Aug-04 Buy 2,640.9 136.0 14.5 0.5 6.1 27.2 6.1 -0.5 -7.0 35.3

HCL Technologies 103.0 550.0 30-Dec-03 Buy 476.5 362.6 -5.5 -1.0 23.9 -1.4 -12.4 -2.0 8.6 4.9

Hindustan Unilever 324.0 ** 29-Jul-11 Hold 454.5 40.3 6.2 10.8 11.6 34.9 -1.6 9.7 -2.2 43.5

ICICI Bank 284.0 1,070.0 23-Dec-03 Buy 899.5 216.7 14.8 3.2 34.1 -16.1 6.4 2.1 17.6 -10.7

Indian Hotel Company 76.6 82.0 17-Nov-05 Buy 61.8 (19.4) 9.9 -3.1 13.6 -19.3 1.8 -4.1 -0.4 -14.1

ITC# 34.8 259.0 12-Aug-04 Hold 258.9 645.0 15.0 16.2 31.0 30.0 6.5 15.0 14.9 38.3

Lupin 80.7 597.0 6-Jan-06 Buy 537.2 565.6 -0.8 1.4 19.9 20.3 -8.1 0.4 5.2 28.0

M&M 116.0 733.0 1-Apr-04 Hold 707.3 509.7 8.4 1.0 3.7 2.4 0.4 0.0 -9.0 8.9

Marico 7.7 ** 22-Aug-02 Hold 183.7 2,285.7 4.9 5.0 26.7 18.6 -2.9 3.9 11.1 26.2

Maruti Suzuki 1,163.0 1,399.0 23-Jan-12 Hold 1,169.8 0.6 6.3 -13.4 27.4 1.5 -1.5 -14.3 11.7 8.0

Oil India 460.0 600.0 11-May-12 Buy 499.4 8.6 14.7 -2.0 8.2 0.5 6.2 -3.0 -5.2 7.0

Piramal Healthcare 445.0 ** 17-Apr-12 Buy 527.9 18.6 20.4 12.0 39.6 37.0 11.5 10.8 22.4 45.8

PTC India 79.0 74.0 22-Mar-11 Buy 64.9 -17.8 16.8 5.7 67.1 -16.6 8.2 4.6 46.5 -11.2

Punj Lloyd 52.2 63.0 2-May-12 Hold 48.9 -6.4 9.2 -11.5 23.5 -35.5 1.1 -12.4 8.3 -31.4

SBI 476.0 2,725.0 13-Feb-12 Buy 2,159.0 353.6 5.0 4.8 35.7 -8.6 -2.7 3.7 19.0 -2.8

Sintex Industries^ 143.0 100.0 26-Sep-08 Buy 61.5 -57.0 14.1 -28.7 -2.4 -65.9 5.7 -29.4 -14.4 -63.8

TGBL (Tata Tea)^ 78.9 123.0 12-Aug-05 Hold 116.0 47.0 7.8 3.2 28.7 22.3 -0.2 2.1 12.8 30.2

Wipro 356.0 450.0 31-Oct-11 Buy 399.9 12.3 -1.5 -8.2 1.8 -2.8 -8.7 -9.2 -10.7 3.4

EMERGING STAR

Axis (UTI) Bank 229.4 1,620.0 24-Feb-05 Buy 1,015.8 342.9 6.3 -10.0 27.7 -20.0 -1.6 -10.9 12.0 -14.9

Cadila Healthcare# 198.3 864.0 21-Mar-06 Hold 770.3 288.4 5.4 1.5 9.4 -15.6 -2.4 0.5 -4.1 -10.2

Eros International Media 186.0 267.0 15-Nov-10 Buy 168.5 -9.4 2.0 -6.6 -17.1 -6.2 -5.5 -7.6 -27.3 -0.2

Gateway Distriparks 131.0 173.0 2-Feb-12 Buy 137.1 4.6 -3.1 -9.2 5.6 13.6 -10.3 -10.1 -7.4 20.8

Greaves Cotton^ 83.0 83.0 25-Jan-12 Hold 70.1 -15.6 2.2 -19.3 -12.3 -17.5 -5.3 -20.1 -23.1 -12.2

EQUITY FUNDAMENTALS

NEW

NEW

NEW

Sharekhan ValueGuide July 20125

COMPANY RECO PRICE RECO CURRENT PRICE AS ON GAIN- ABSOLUTE PERFORMANCE RELATIVE TO SENSEXPRICE TARGET DATE RECO 30-JUNE-12 LOSS (%) 1M 3M 6M 12M 1M 3M 6M 12M

REPORT CARD

STOCK IDEAS STANDING (AS ON JUNE 30, 2012)

EQUITY FUNDAMENTALS

**Price target under review ^ Reco price adjusted for stock split ***Price target and reco price adjusted for the demerger^^Reco price adjusted for rights issue #Reco price adjusted for bonus

NEW

NEW

ITNL 362.0 330.0 14-Sep-10 Buy 184.1 -49.2 0.7 -4.8 26.7 -10.4 -6.7 -5.7 11.1 -4.7

IRB Infra 234.0 175.0 29-Nov-10 Buy 127.2 -45.6 12.9 -31.9 -1.3 -24.6 4.6 -32.6 -13.5 -19.8

Kalpataru Power 112.0 145.0 15-Mar-12 Buy 83.0 -25.9 0.8 -23.4 -11.3 -32.8 -6.6 -24.2 -22.2 -28.5

Max India 212.0 234.0 24-Nov-09 Buy 192.1 -9.4 4.2 13.6 31.4 4.8 -3.5 12.4 15.2 11.5

Opto Circuits India 199.0 302.0 13-May-08 Buy 154.3 -22.5 -4.6 -23.4 0.6 -31.6 -11.7 -24.2 -11.8 -27.2

Thermax 124.2 447.0 14-Jun-05 Hold 480.0 286.5 7.2 3.3 22.0 -18.2 -0.7 2.3 7.0 -13.0

Yes Bank 332.0 431.0 2-Dec-10 Buy 339.4 2.2 2.9 -8.0 42.1 8.8 -4.7 -8.9 24.6 15.7

Zydus Wellness 354.0 ** 11-May-12 Hold 391.7 10.6 6.0 2.8 1.6 -36.9 -1.9 1.8 -10.9 -32.9

UGLY DUCKLING

Ashok Leyland # 26.0 28.0 15-May-12 Hold 24.9 -4.2 -0.4 -18.0 9.2 2.5 -7.7 -18.8 -4.2 9.0

Bajaj Corp 109.0 142.0 30-Aug-11 Buy 118.3 8.5 1.0 2.6 23.8 6.9 -6.5 1.5 8.5 13.7

CESC 282.0 405.0 29-Jun-11 Buy 289.7 2.7 7.8 6.6 43.8 -1.8 -0.1 5.5 26.1 4.5

Deepak Fertilisers 50.6 188.0 17-Mar-05 Buy 133.0 162.8 0.5 -12.4 10.1 -17.7 -6.9 -13.3 -3.4 -12.4

Federal Bank 258.0 522.0 16-Mar-10 Buy 448.6 73.9 6.7 5.2 33.2 1.5 -1.2 4.1 16.8 8.0

Gayatri Projects 256.5 310.0 5-Apr-10 Buy 99.0 -61.4 -7.0 -21.0 22.9 -44.6 -13.9 -21.8 7.8 -41.1

India Cements 72.0 110.0 12-Aug-11 Buy 87.0 20.8 15.6 -22.0 31.8 25.2 7.1 -22.8 15.6 33.2

Ipca Laboratories 132.0 436.0 5-Nov-07 Buy 358.7 171.7 4.6 7.0 30.4 5.3 -3.1 5.9 14.4 12.0

ISMT 43.0 29.0 8-Oct-09 Buy 24.1 -44.1 1.5 -10.3 6.4 -39.0 -6.0 -11.2 -6.7 -35.1

Jaiprakash Associates 16.7 105.0 30-Dec-03 Buy 73.5 340.9 18.3 -10.0 40.3 -8.7 9.5 -11.0 23.0 -2.9

KKCL 427.0 700.0 7-Oct-10 Hold 580.1 35.8 -0.6 -11.4 -16.2 -14.9 -7.9 -12.4 -26.5 -9.5

Mcleod Russel India 267.0 339.0 24-Apr-12 Buy 298.1 11.6 6.7 9.9 58.1 12.5 -1.2 8.7 38.6 19.7

NIIT Technologies 210.0 325.0 19-Jan-11 Buy 285.8 36.1 -6.3 7.8 59.5 63.4 -13.2 6.7 39.9 73.9

Orbit Corporation 142.0 70.0 23-Dec-09 Buy 56.5 -60.2 31.5 8.9 108.5 37.3 21.9 7.7 82.8 46.1

Polaris Financial 164.0 190.0 3-Nov-10 Buy 127.5 -22.3 13.4 -22.4 4.4 -26.4 5.0 -23.2 -8.5 -21.7

Pratibha Industries 65.2 65.0 18-Jan-10 Buy 46.4 -28.9 17.0 -2.4 39.6 -13.3 8.4 -3.4 22.4 -7.8

Provogue India 43.3 35.0 6-Jul-10 Buy 15.4 -64.4 22.2 6.6 -21.2 -55.5 13.2 5.5 -30.9 -52.7

Punjab National Bank 180.0 1,070.0 19-Dec-03 Buy 808.3 349.1 10.0 -10.1 6.5 -23.7 1.9 -11.0 -6.6 -18.8

Ratnamani Metals 54.0 132.0 8-Dec-05 Buy 105.4 95.1 7.4 -2.0 14.8 9.1 -0.5 -3.1 0.7 16.1

Raymond 387.0 500.0 3-Nov-11 Buy 402.4 4.0 10.9 -4.6 30.8 10.9 2.7 -5.6 14.6 17.9

Selan Exploration 58.0 500.0 20-Mar-06 Buy 285.0 391.4 3.8 2.0 26.1 2.5 -3.9 0.9 10.6 9.0

Sun Pharma 60.4 651.0 24-Dec-03 Buy 635.8 952.6 12.1 11.6 27.8 28.6 3.9 10.4 12.0 36.8

Torrent Pharma 185.0 760.0 4-Oct-07 Buy 600.6 224.6 -2.3 -4.4 12.9 -4.6 -9.5 -5.4 -1.0 1.5

UltraTech Cement 384.0 1,550.0 10-Aug-05 Hold 1,516.5 294.9 6.5 0.1 30.0 64.0 -1.3 -0.9 14.0 74.5

Union Bank of India 46.0 240.0 25-Jan-12 Hold 209.1 354.6 7.8 -7.8 28.0 -25.8 -0.1 -8.7 12.2 -21.0

United Phosphorus 163.0 167.0 27-Aug-09 Buy 125.9 -22.8 13.7 -1.8 0.7 -15.2 5.3 -2.8 -11.7 -9.8

V-Guard Industries 162.0 244.0 6-Sep-10 Buy 233.1 43.9 7.6 26.5 50.5 5.9 -0.3 25.2 31.9 12.7

VULTURE'S PICK

Mahindra Lifespace 799.0 400.0 9-Jan-08 Buy 326.8 -59.1 4.6 2.5 37.5 -8.1 -3.1 1.4 20.6 -2.2

Orient Paper and Industries 21.4 70.0 30-Aug-05 Buy 55.7 160.0 0.4 -5.6 13.1 2.8 -7.0 -6.6 -0.8 9.4

Tata Chemicals 411.0 338.0 31-Dec-07 Hold 311.0 -24.3 1.0 -10.3 -0.5 -14.3 -6.4 -11.2 -12.8 -8.9

Unity Infraprojects 138.4 107.0 26-Feb-08 Buy 45.9 -66.9 12.0 -5.2 46.3 -26.9 3.7 -6.1 28.2 -22.2

CANNONBALL

Allahabad Bank 73.0 230.0 25-Aug-06 Buy 149.7 105.0 14.4 -16.0 36.0 -20.8 5.9 -16.9 19.2 -15.7

Andhra Bank 120.1 156.0 3-Feb-11 Buy 118.4 -1.4 14.1 4.1 55.2 -7.6 5.7 3.0 36.0 -1.7

IDBI Bank 106.0 131.0 19-Jun-09 Hold 93.4 -11.9 9.9 -10.8 22.1 -27.9 1.8 -11.7 7.1 -23.3

Madras Cements 88.0 152.0 10-Feb-11 Hold 159.8 81.6 16.8 3.9 57.6 101.3 8.2 2.9 38.2 114.1

Shree Cement 445.0 3,100.0 17-Nov-05 Hold 3,040.0 583.1 26.3 -5.4 44.8 73.7 17.0 -6.3 26.9 84.8

July 2012 Sharekhan ValueGuide6

Markets never fail to surprise

FROM SHAREKHAN’S DESK

from

sha

rekh

an’s

des

k Many a times, the equity markets tend to move against the prevailing consensus wisdomand consequently catch most market participants by surprise. Just when the expectationshad hit a nadir and equities were threatening to tumble down to new yearly lows towardsthe end of 2011, the Indian equity market had surged with an unexpected sharp rally at thebeginning of the new year. This time around also, the equity markets climbed the wall ofworries to register smart gains in the month of June.

After the rather pessimistic mood just a few weeks back, the sudden reversal in marketsentiments is rather surprising, given the recent slew of disappointments and negative news,such as the Reserve Bank of India’s inaction in the policy review meet, the rating down-grade of India’s outlook by another global agency and the weak onset of the monsoon. Theglobal cues also have not been encouraging except for the patchwork of a solution thatwould provide temporary relief to the troubled economies and banks in the euro zone.

Perhaps it is about expectations that were extremely low and consequently triggered atechnical upsurge in the market even at the hint of some positives emerging on the domesticas well as global front. The emerging positives, which are extensively covered in the MarketOutlook report titled “Silver lining in the midst of dark clouds” on page 7, could result ina relatively better performance by the Indian equity market in the near term.

However, this is all about the near-term outlook, which is more unpredictable and volatile.The big picture (or the long-term performance of equities), which ought to be the soleconcern of investors, is essentially driven by only two factors: corporate earnings and li-quidity.

Corporate earnings tend to move in cycles that comprise strong growth periods and alsoperiods when earnings remain sluggish for a few years. Notwithstanding the cycles theaverage growth in corporate earnings has been quite healthy even over a long period ofthree decades. That’s because the average growth in corporate earnings tends to be in line(or marginally higher) with the nominal growth in India’s gross domestic product (GDP;real GDP growth + inflation) that has averaged at annual rate of 14% since 1979. Thus,the growth in corporate India’s financial performance is quite predictable over a longerperiod of time.

On the other hand, the liquidity flows are much more unpredictable. Liquidity flows de-pend on a host of domestic and global factors that are not measurable (intangible) but alsobehavioural in nature. However, the only thing predictable about liquidity flows is thatsooner or later money does chase value. Thus, an undervalued market would eventuallyattract capital flows (though it is difficult to time this).

Having said this, we are not implying that the investors need not track important macroand company-specific information, and take appropriate necessary actions. But investorsmust not miss the wood for the trees, and get disillusioned by the all the noise (issues thatonly affect the near-term performance of the equity market). We also advocate active in-vesting and believe that there are a number of tools available to help trade with part of aninvestor’s portfolio to hedge or improve the near-term returns. Sharekhan offers a wholehost of trading products across various asset classes to cater to every market participant’sneeds and has also partnered with Online Trading Academy to provide quality tradingeducation. By adopting a combination of trading and investing strategies one will be able tonot only hedge one’s portfolio against unexpected market movements but also make thebest of the existing opportunities in all kinds of markets.�

Sharekhan ValueGuide July 20127

Silver lining in the midst of dark clouds

MARKET OUTLOOK JUNE 30, 2012

Market negotiates through a tough global environment and aseasonally weak summer: In our last Market Outlook report releasedin early May (titled “The heat is on”), we had turned cautiousagainst the backdrop of the rising crude prices and the nervousnessprior to some important global and domestic events in the alreadyseasonally weak summer period. The market did lose some groundand the overall pessimism only heightened on the back of the ReserveBank of India (RBI)’s status quo on policy rates, the downgrade ofIndia’s rating outlook and the fragile euro situation during the lasttwo months. However, we believe that the Indian equity markethas negotiated the tough period without much damage and ispotentially poised for relatively better times over the next fewmonths.

Emerging positives amid despondency: Given the slew of negatives,some of the positive developments and pointers have been largelyignored. These are as follows.

� Commodities cool off (including crude): A decent correction incommodities especially crude oil is inherently positive for theIndian economy, the corporates and the equity market. It doesthree things: eases the pressure on fiscal health; positively affectscorporate margins and makes India better placed for foreigninvestors as compared with its commodity exporting peers likeBrazil, Russia and Indonesia.

� Political changes could end policy inertia: The domestic politicalsituation has turned more conducive with the prime ministertaking charge of the finance ministry as well and the SamajwadiParty (SP) formally putting its weight behind the UnitedProgressive Alliance (UPA) II, thereby marginalising thetroublesome coalition partner Trinamool Congress’ importancein forging a political consensus to push forward the pendingand much awaited policy decisions. Mind you, we do not expectany major fireworks or path-breaking reforms but the verybreaking out of the policy inertia is enough to boost the market’sconfidence as expectations are pretty low.

� Valuations and high cash levels supportive: The rupee’sdepreciation has turned the valuations of Indian equities all themore cheaper for foreign investors who are sitting on a recordlevel of free cash (especially the Asian and emerging marketfunds), according to one of the recent surveys done for a globalbank and research house.

Euro zone: kicks the can down the road again: The euro zonemembers have come out with a patchwork of a solution to soothethe unnerved financial markets. The plan to directly supportEuropean banks and intervene in the bond markets to supportmember states has led to a burst of optimism which could fade offafter the initial reaction.

Pressure points: resumption in earnings downgrades and weakbeginning of monsoon season: It could have been better for theIndian equities but for the disappointing Q4FY2012 results of someindex heavyweights and the overall resumption of the downgradein the consensus earnings estimates by research houses after a pause

MARKET OUTLOOKEQUITY FUNDAMENTALS

SENSEX’ P/E (BASED ON ROLLING ONE-YEAR FORWARD EPS)

Source: Bloomberg

of a few months. The higher than expected asset quality concernsin the banking sector was the key negative takeaway from the Q4report card. The monsoon could also play a spoilsport. Thebeginning is weak and the increasing probability of El Nino in thelater part of the monsoon season would put further pressure on theeconomy, which is already suffering from slowing industrial activitywith signs of a slowdown in the services sector also. Moreover, aweaker monsoon would boost inflationary pressures and couldfurther delay the easing of the monetary cycle.

No runaway rally but sentiments could change for better: Havingsaid this, we are not in any way implying that the benchmark indiceswould witness a runaway rally from here but are merely suggestingthat the bias should turn positive from negative in the near term.The important thing to note is that in such an environment thebeaten-down stocks from certain sectors where some policy decisionsare initiated could surprise positively and outperform the currentlyfancied consumer and other defensive stocks in the next couple ofmonths. Beaten-down and high-beta stocks from light engineeringand construction/infrastructure sectors could turn out to berewarding contrarian bets in such a scenario. The delay in the interestrate cuts would act as a drag on the rate sensitive sectors (especiallyautomobiles) and the highly leveraged companies. In terms ofvaluation, the Sensex trades at 13.3x its FY2013 estimated earningsand 12x its FY2014 estimated earnings (in rupee terms). That isclose to 15% discount to its long-term average multiple of 15x itsone-year forward estimated earnings.

6

9

12

15

18

21

24

27

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

+1σ

15x

-1σ

Market sails through global and local turbulencesDue to the fragile European financial system, the weak macro dataof the US economy and the sharper than expected deceleration inthe Asian economies (especially China and India) the sentimentweakened for equities. On the domestic front, the policy paralysiscontinued amid threats of a ratings downgrade and even the RBIpreferred to play safe by overruling the strong market expectationof a rate cut. The investment outlook deteriorated as global funds—which were positive on equities in early 2012—became underweighton equities. However, the Indian market weathered the turbulenceswithout any major damage.

July 2012 Sharekhan ValueGuide8

MARKET OUTLOOK EQUITY FUNDAMENTALS

Green shoots wilting but paving way for more easing in the US,euro economiesA weak housing statistics, drop in the manufacturing sector’smomentum, decline in spending and consequent reduction in thegrowth forecast by the US Federal Reserve (Fed) negated the hopesof a recovery, if any, in the near term. In order to support growth,

the Fed extended the Operation Twist ($267 million). The eurozone segment showed a sharp contraction in industrial productionand retail spending with a drop in the business confidence levels.The crisis in the banking sector aggravated leading to the de-ratingof several banks in the euro area. Despite resistances, the EuropeanUnion (EU) members have agreed to take adequate measures tostrengthen the banking system. Going ahead, more measures areexpected by the USA and the euro zone nations to revive the ailingeconomies.

Softening of crude prices to provide some relief on deficit frontThe current account deficit (CAD) spiralled to an all-time high of4.3% of the gross domestic product (GDP; FY2012) led by a rise inthe import bill and slower exports. However, crude oil, whichconstitutes 30% of the India’s imports and whose prices have fallenby 20% in the past three months (though the benefit has been mostlyoffset by the local currency’s depreciation), is likely to stem the risein the CAD. Further, the gold imports (10% of total imports),which have been the key driver of the rise in the CAD, aremoderating after the levies announced in the FY2013 budget.Therefore, the softening of the commodity prices will ease theinflation fears, improve the corporate performance and widen thescope for monetary easing. Traditionally, in a scenario of lowercommodity prices India outperformed the other emerging marketsdue to increased allocation from the foreign investors.

Euro summit: Will the burst of optimism last long enough?There are both good and negative takeaways from the deal announced post-Euro Summit at Brussels. First, the good news that led toa burst of optimism in the financial markets globally. The euro zone members have decided to allow the rescue fund (EuropeanStability Mechanism [$634 billion] and European Financial Stability Facility) to directly support banks and also intervene in the bondmarket to support the troubled countries of Europe. A single banking supervisor will be formed for all the euro zone banks. The aimis to break the vicious cycle between banks and their respective governments who are unable to provide the required financial supportto the banks that are too big to fail. This is seen as the first step of Europe moving towards a “Banking Union”.

The bad news is that the move would only forestall the crisis rather than find a more durable cure. In the past such decisions to kickthe can down the road only led to a burst of optimism that normally would fade away when the euro zone politics would kick in andmake it difficult to enact the announced plan in the right spirit. We keep our fingers crossed.

RISING CASH LEVELS OF GLOBAL FUNDS

Source: Media reports

EURO ZONE MACRO DATA: SLOWDOWN CONTINUES

Source: Bloomberg

- 2 5 .0

- 2 0 .0- 1 5 .0

- 1 0 .0- 5 .0

0 .0

5 .01 0 .0

1 5 .0

Mar

-06

Aug

-06

Jan-

07

Jun-

07

Nov

-07

Apr

-08

Sep

-08

Feb

-09

Jul-0

9

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan-

12

G DP IP

US MACRO DATA: GROWTH REMAINS FRAGILE

Source: Bloomberg

- 2 0 .0

- 1 5 .0

- 1 0 .0

- 5 .0

0 .0

5 .0

1 0 .0

Mar

-06

Jul-0

6

Nov

-06

Mar

-07

Jul-0

7

Nov

-07

Mar

-08

Jul-0

8

Nov

-08

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

G DP IP

IMPACT OF CRUDE PRICES ON SENSEX’ PREMIUM TO EMS

Source: Bloomberg

30

50

70

90

110

130

150

Feb

-07

Jun-

07

Oct

-07

Feb

-08

Jun-

08

Oct

-08

Feb

-09

Jun-

09

Oct

-09

Feb

-10

Jun-

10

Oct

-10

Feb

-11

Jun-

11

Oct

-11

Feb

-12

Jun-

12

-

5 .0

10 .0

15 .0

20 .0

25 .0

30 .0

Crude S ens ex p remium v s EMS

Chorus on policy inaction get shriller, some fiscal actions likelyThe criticism on policy inaction has grown shriller since the GDPgrowth tanked to 6.5% (the lowest in nine years), the rupee slidand the rating agencies threatened with downgrades. The primeminister—who has taken charge of the finance ministry as well—has indicated some measures to stimulate growth. Further, thealigning of the Samajwadi Party with the UPA cushions thegovernment on a number of fronts and may contribute to the passageof a few legislations though path-breaking reforms still look

Sharekhan ValueGuide July 20129

MARKET OUTLOOKEQUITY FUNDAMENTALS

doubtful. The government has already softened the stance on theproposed tax laws (General Anti-Avoidance Rules) to improveinvestor sentiment and is engaging with the aggrieved parties toresolve the issues afflicting the infrastructure sector. Given the lowlevel of expectation, any fiscal measure, no matter how small, willbe taken as a positive by the market.

Earnings expectation gets more conservativeAfter the FY2012 results the consensus earnings estimate for theSensex has fallen by 15% for FY2013 over the past 15 months.This largely factors the weakness in the broader economy and itsimpact on the corporate earnings. The telecommunications sectorhas seen the highest downward revisions whereas consumer goodsand energy sectors have seen a higher number of upgrades.Currently, the earnings of the Sensex are estimated to grow at ~13%in FY2013. This seems quite conservative considering the 14.1%growth delivered by the benchmark index since the 1970s. Therefore,though the incremental risks remain on account of a sluggishmonsoon and global events but the back-ended policy actions andmonetary easing could also lead to upgrades.

SENSEX’ FY2013 EARNINGS ESTIMATES

Source: Bloomberg

1200

1250

1300

1350

1400

1450

1500

1550

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Apr

-12

May

-12

Jun-

12

Pressure on rupee unabated; weak monsoon and inflation riskspersistThe rupee has depreciated due to a combination of global anddomestic factors. The reversal of the softening of crude oil pricesled by global liquidity or the deepening of the euro zone crisis could

No runaway rally but sentiments could change for betterHaving said this, we are not in any way implying that the benchmarkindices would witness a runaway rally from here but are merelysuggesting that the bias should turn positive from negative in thenear term. The important thing to note is that in such anenvironment the beaten-down stocks from certain sectors wheresome policy decisions are initiated could surprise positively andoutperform the currently fancied consumer and other defensivestocks in the next couple of months. Beaten-down and high-betastocks from light engineering and construction/infrastructure sectorscould turn out to be rewarding contrarian bets in such a scenario.The delay in the interest rate cuts would act as a drag on the ratesensitive sectors (especially automobiles) and the highly leveragedcompanies. In terms of valuation, the Sensex trades at 13.3x itsFY2013 estimated earnings and 12x its FY2014 estimated earnings(in rupee terms). That is close to a 15% discount to its long-termaverage multiple of 15x its one-year forward estimated earnings.

WPI INFLATION TREND

Source: Bloomberg

- 2 %

0 %

2 %

4 %

6 %

8 %

1 0 %

1 2 %

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

MOVEMENT OF RUPEE VIS-À-VIS USD, EURO

Source: Bloomberg

3 54 0

4 55 05 5

6 06 5

7 07 5

Jan-

00

Aug

-00

Mar

-01

Oct

-01

May

-02

Dec

-02

Jul-0

3

Feb

-04

Sep

-04

Apr

-05

Nov

-05

Jun-

06

Jan-

07

Aug

-07

Mar

-08

Oct

-08

May

-09

Dec

-09

Jul-1

0

Feb

-11

Sep

-11

Apr

-12

US D- INR Eu r o - INR

aggravate the currency risks. According to India MeteorologicalDepartment, the El Nino phenomenon is threatening this year’srainfall, which has had a weak start already. The government hashiked the minimum support price for the kharif crops which couldkeep food inflation at higher levels. A potential shortfall in the rainscould further intensify the consumption slowdown concerns andraise the agriculture related non-performing assets of banks.

SENSEX’ P/E (BASED ON ROLLING ONE-YEAR FORWARD EPS)

Source: Bloomberg

6

9

12

15

18

21

24

27

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12+1σ

15x

-1σ

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding orhaving a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

July 2012 Sharekhan ValueGuide10

Sharekhan Top Picks

SHAREKHAN TOP PICKS

Despite the disappointment from the Reserve Bank of India (RBI)’sinaction in the policy review meet and the downgrade of India’srating outlook by another leading global rating agency in June, theSensex and the Nifty have registered handsome gains of 8.8% and8.5% respectively since our last update on June 5, 2012. The TopPicks basket has performed in line with the benchmark indices andappreciated by 8.7% in the same period. However, the blendedreturn stands at 8% after accounting for the cash created (by addingone stock less to the basket) in May this year.

In this month, we are increasing the basket’s exposure to engineering,construction and infrastructure sectors by adding Larsen & Toubro

* CMP as on June 30, 2012

NAME CMP* PER ROE (%) PRICE UPSIDE(RS) FY12 FY13E FY14E FY12 FY13E FY14E TARGET (%)

Divi’s Laboratories 1,027 25.5 20.5 16.7 25.0 27.2 27.5 1,122 9

ICICI Bank 900 1.7 1.6 1.5 11.2 11.5 12.0 1,070 19

IRB 127 8.5 9.8 10.0 18.7 14.2 12.5 175 38

ITC 259 32.8 27.5 22.9 35.5 36.4 37.2 ** **

Kalpataru Power Trans 83 6.8 5.9 4.9 10.8 11.2 12.1 145 74

Larsen & Toubro 1,397 19.3 18.6 17.0 18.8 17.1 16.4 1,529 10

Mcleod Russel 298 11.0 10.0 7.8 18.6 17.7 19.5 339 14

NIIT Technologies 286 8.6 7.1 6.1 23.6 23.8 23.0 325 14

Oil India 499 8.8 8.1 7.6 19.0 19.7 18.5 600 20

Orient Paper 56 5.3 4.9 4.3 21.0 19.1 18.6 70 26

Selan Exploration 285 11.0 7.9 5.1 23.3 26.4 31.5 500 75

ABSOLUTE OUTPERFORMANCE (RETURNS IN %) CONSTANTLY BEATING NIFTY AND SENSEX (RETURNS IN %)

(L&T), IRB Infrastructure Developers (IRB) and Kalpataru PowerTransmission Ltd (KPTL) in the Top Picks basket. IRB replacesIL&FS Transportation Networks to take advantage of the widenedgap in the valuations of the two stocks. L&T, the bellwetherengineering, procurement and construction player, comes in placeof Sun Pharmaceuticals, which has appreciated by close to 28% inthe last five months and sharply outperformed the benchmarkindices since it was introduced in the Top Picks basket in February2012. Lastly, we deploy the cash to bring in KPTL, which has astrong order backlog and a healthy balance sheet.�

0.0%

20.0%40.0%

60.0%

80.0%100.0%

120.0%

140.0%160.0%

180.0%

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb

-10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb

-11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Apr

-12

Jun-

12

Sharekhan Sensex Nif ty

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

YTDCY2012

CY2011 CY2010 CY2009 Since Jan2009

Sharekhan (Top Picks) Sensex Nif ty CNX MIDCAP

SHAREKHAN TOP PICKS EQUITY FUNDAMENTALS

Sharekhan ValueGuide July 201211

SHAREKHAN TOP PICKSEQUITY FUNDAMENTALS

ITC 259 32.8 27.5 22.9 35.5 36.4 37.2 ** **

Remarks: � ITC’s cigarette business, which contributes around 60%, continues to be a cash cow for the company. The company endeavours to make a mark in theIndian FMCG market and with successful brands such as Bingo, Sunfeast and Aashirwaad, ITC is already in the reckoning among the best in the industry.With the new portfolio of personal care products gaining market share, its FMCG business promises to compete with the likes of Hindustan Unilever andProcter & Gamble.

� The Government of India has increased the excise duty on cigarettes by ~22% in the finance budget 2012-13. The company has already taken a priceincrease of around 12% which would help in maintaining the cigarette business’ margins at around 30%.

� ITC’s other businesses, such as hotel, agri, non-cigarette FMCG business and paper, paperboard and packaging, are showing a strong upmove and willprovide a cushion to the overall profit in FY2012.

� An increase in the taxation and the government’s intention to curb the consumption of tobacco products remain the key risks to ITC’s cigarette businessover the longer term.

� We expect ITC’s bottom line to grow at a CAGR of about 20% over FY2011-14. At the current market price, the stock trades at 22.9x its FY2014Eearnings. We like the stock from a longer-term perspective.

ICICI BANK 900 1.7 1.6 1.5 11.2 11.5 12.0 1,070 19

Remarks: � ICICI Bank is back on growth path as its advances are growing at a healthy rate (up 17.3% YoY and 3.1% QoQ in Q4FY2012). We expect the advancesof the bank to grow by 20% CAGR over FY2012-14. This should lead to a 15% CAGR growth in the net interest income in the same period.

� ICICI Bank’s asset quality has shown a turnaround as its NPAs have continued to decline over the last six quarters led by contraction in slippages. Thishas led to a sharp reduction in the provisions and an increase in the profitability. Going forward, we expect the NPAs to decline further which will lead tolower NPA provisions and hence aid the profit growth.

� With a pick-up in the business growth and an improvement in the margins the RoEs are likely to expand to about 12% over the next two years while theRoA would improve to 1.4%. This would be driven by a 12% CAGR in profits over FY2012-14.

� The stock trades at 1.4x FY2014E book value. We expect the stock to re-rate, given the improvement in the profitability led by lower NPA provisions, ahealthy growth in the core income and improved operating metrics. We recommend Buy with a price target of Rs1,070.

DIVI’S LABORATORIES 1,027 25.5 20.5 16.7 25.0 27.2 27.5 1,122 9

Remarks: � Strong FY2012 performance (PAT growth 27%) has re-affirmed our confidence in the growth potential of Divi’s Labs.

� The new DSN SEZ facility at Vishakhapatnam that started production from one of its blocks in June 2011 (the remaining blocks of this facility are likely toget operational over FY2012-13) is likely to bring better economies of scale and tax benefits.

� A near debt-free balance sheet and strong cash flow are likely to help build a war chest for pursuing strategic investments (biosimilars) and exploit growthopportunities in niche segments like high potency drugs for oncology and steroids for contraceptives.

� With the order inflow picking up and its new plant getting operational, Divi’s has a strong revenue growth visibility and the operating leverage in thebusiness will boost its margins. At the current market price the stock trades at a PE multiple of 16.7x, discounting its FY2014E earnings. We maintain ourBuy recommendation.

IRB 127 8.5 9.8 10.0 18.7 14.2 12.5 175 38

Remarks: � IRB is the largest toll road BOT player in India and the second largest BOT operator in the country. It has a portfolio of 16 projects which are all toll based,together worth Rs16,468 crore and cover 1,180km of length. Its portfolio is mostly located along the corridors with high traffic density and high growtharound Mumbai and Pune.

� Of these 16 projects, 11 are operational and five are under construction. It has an integrated business model with an in-house construction arm. Thisprovides a competitive advantage in bidding for the larger projects and captures the entire value from the BOT assets.

� Further, seven of its 11 operational projects are already debt-free and generating steady cash for the company. Continuing cash flows from these arelikely to fuel growth.

� Though the charges levied against the promoter of IRB are serious, the correction of over 30% in the stock factors in a lot of the negatives and has madethe stock available at a 40% discount to its mean average valuation multiple. The improving outlook for the road infrastructure developers should limit thedownside risk in the stock though. Moreover, any positive development on the legal issue could result in a sharp re-rating of the stock.

� At the current market price, the stock is trading at 9.8x and 10x its FY2013 and FY2014 estimated earnings respectively and the valuations are veryattractive. We maintain our Buy recommendation on the stock with a price target of Rs175.

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY12 FY13E FY14E FY12 FY13E FY14E TARGET (%)

July 2012 Sharekhan ValueGuide12

SHAREKHAN TOP PICKS EQUITY FUNDAMENTALS

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY12 FY13E FY14E FY12 FY13E FY14E TARGET (%)

KALPATARU POWER 83 6.8 5.9 4.9 10.8 11.2 12.1 145 74

Remarks: � Kalpataru Power Transmission Ltd (KPTL) is a leading EPC player in the transmission & distribution (T&D) space in India. The T&D space is poised fora significant growth in India as well as globally.

� Backed by a healthy order book position (ie 2x its FY2012E revenues) the company’s consolidated revenues are expected to grow at 17% CAGR duringFY2012-14.

� On account of a competitive bidding environment, the EBITDA margin of KPTL (stand-alone) is likely to remain subdued in the near term which is alreadypriced in the stock. Further, on account of the tightened payment norms adopted by PGCIL, KPTL could witness strain on its working capital requirementsand cash flows. Nevertheless, KPTL’s balance sheet position is better than that of its peers with relatively less leverage (a consolidated debt-equity ratioof 0.6x). Further, the peaking of the interest rate in the near future could be beneficial, as for KPTL the interest cost is the highest cost component belowthe EBITDA line.

� Given the current economic condition, we believe we are close to the peak of the interest rate hike cycle. However, if the interest rates remain at thecurrent levels, it will adversely affect the company’s performance.

� At the current market price, KPTL is trading at 5.9x and 4.9x FY2013 and FY2014 estimated EPS respectively, which is significantly lower than thehistorical average. We maintain our Buy recommendation on the stock with a price target of Rs145 (we have valued KPTL at 7.5x FY2014E and JMCProjects at 5.5x FY2014E).

LARSEN & TOUBRO 1,397 19.3 18.6 17.0 18.8 17.1 16.4 1,529 10

Remarks: � Larsen & Toubro (L&T), the largest engineering and construction (E&C) company in India, is a direct beneficiary of the strong domestic infrastructuredevelopment and industrial capital expenditure (capex) boom.

� L&T continues to impress us with its good execution skills, reporting decent numbers throughout this year despite the slowdown in the industrial capexcycle. While there has been a growth of 12% YoY in its order backlog to Rs1,45,723 crore; the order inflow remained rather muted in FY2012.

� Despite challenges like deferral of award decisions and stiff competition, the company has given robust guidance of 15-20% in revenue and order inflowfor FY2013- while this seems an uphill task, it instills confidence amongst the investors.

� Although the company reported overall decent results for the quarter, the order inflow guidance would be highly subjective to an uptick in infrastructuredevelopment activities in the country and in the Middle East region. We also feel that its diversity continues to cushion the overall financials in a toughbusiness environment.

� Sound execution track record, bulging order book and strong performance of its subsidiaries reinforce our faith in L&T. With the company entering newverticals, namely solar and nuclear power, railways, and defense, there appears a huge scope for growth. Given its excellent track record, we are quiteconfident about L&T’s success in these initiatives.

� At the current market price, the stock is trading at 17x its FY2014E standalone earnings and at an EV/EBIDTA of 9.6x. We maintain our Buy recommendationon the stock.

MCLEOD RUSSEL 298 11.0 10.0 7.8 18.6 17.7 19.5 339 14

Remarks: � Mcleod Russel India (MCR) is the world’s largest tea producer with a total area of 38,758 hectares under tea cultivation (1.1% of the world’s total areaunder tea cultivation). With a production capacity of close to 100 million kg MCR is well poised to capitalise on the growing demand for Indian black teain the global markets.

� The rising demand-supply gap of tea due to a production shortfall in the key tea exporting countries has created a favourable scenario for the domestictea producers. We expect a growth of Rs10-15 per kg in MCR’s average realisation in the next two years. This will help the margins to improve by 120-130 basis points YoY in the coming years.

� With expectations of strong cumulative operating cash inflow of around Rs680 crore over the next two years, MCR is expected to improve the dividendpay-out and/or build a cash war chest for potential inorganic initiatives in future.

� Since the tea industry is labour intensive, any labour unrest in India is the key risk for the company in the near future. Also any substantial increase in theproduction of the key tea exporting countries will improve the demand-supply gap resulting in an adverse impact on the sales realisation of the Indian teaproducers.

� The stock is currently trading at 7.8x its FY2014E EPS of Rs38.2. We maintain our Buy recommendation on the stock with a price target of Rs339.

Sharekhan ValueGuide July 201213

SHAREKHAN TOP PICKSEQUITY FUNDAMENTALS

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY12 FY13E FY14E FY12 FY13E FY14E TARGET (%)

NIIT TECHNOLOGIES 286 8.6 7.1 6.1 23.6 23.8 23.0 325 14

Remarks: � NIIT Technologies Ltd (NTL), a mid-sized IT services company, has built strong domain expertise in niche industry verticals like insurance, travel,manufacturing and retail. The company has a balanced mix of revenues coming from across verticals and geographies which would safeguard it from aslowdown in any specific industry or geography.

� The company has a strong order book of $243 million executable over the next 12 months giving it strong revenue visibility going ahead. The companyis gaining traction with a robust order intake of $453 million in FY2012, up 70% over FY2011. The robust order intake comes on the back of the multi-year,multi-million dollar deals won by the company in the past year including the Morris deal worth $85 million, the Rs300-crore worth deals won under theCrime and Criminal Tracking Network System (CCTNS) programme from three states and the euro-40-million Eurostar deal. Currently, the company ischasing at least four large deals of more than $25 million each.

� With a strong executable order book and increasing success in deal conversion NTL has got predictable business visibility for the coming quarters.Further, the strategy of offshore shift of recent large deals has played out as per expectations and the same would result in a margin improvement in thecoming quarters. At the current market price, NTL trades at attractive valuations of 7.1x and 6.1x on FY2013E and FY2014E earnings respectively. Wemaintain our Buy rating on the stock.

OIL INDIA 499 8.8 8.1 7.6 19.0 19.7 18.5 600 20

Remarks: � Oil India Ltd (OIL) has several hydrocarbon discoveries across reserves in Rajasthan and the north-eastern region of India. The total 1P (proven) and 2P(proven and probable) reserves of the company stood at 505 million barrels (mmbbls) and 944mmbbls as on March 2011. In addition to the huge oilreserves, the company’s reserve-replacement ratio (RRR) is quite healthy at 1.42x which implies a comfortable level of accretion of oil reserves throughnew discoveries.

� The recent correction in the crude oil price to $93 per barrel as compared with the peak level of $124 per barrel touched a couple of months back augurswell for the company as it will reduce its subsidy burden.

� Further, OIL has cash of around Rs10,935 crore (Rs182 per share) as on March 2012 and offers a healthy dividend pay-out (dividend yield of 4.3%),which provides comfort to the investor.

� The key risks remain any adverse movement in the price of crude oil and failure in proper utilisation of the huge cash.

� We remain bullish on OIL because its huge reserves and healthy RRR would provide a reasonably stable revenue growth outlook and its stock isavailable at an attractive valuation. The fair value works out to Rs600 per share (based on the average fair value arrived at using the DCF, PE and EV/EBIDTA valuation methods).

ORIENT PAPER 56 5.3 4.9 4.3 21.0 19.1 18.6 70 26

Remarks: � OPIL, a part of CK Birla group, is a diversified conglomerate operating in three segments; cement, paper and fans. The cement division contributes over53% of the total revenue. The company benefits due to its diversified business model.

� Due to the recent increase in cement prices, the present realisation of the company is higher by over 28% over FY2011. The surge in the realisation willbe able to offset the cost inflation and the profitability of the division is likely to improve (marginally).

� In the electrical division, due to the new product launches and gaining market shares, the company has delivered over 13% revenue growth in FY2012.Going forward, the division can witness growth on the back of lighting products (CFL) and household appliances.

� The restructuring plan to demerge the cement division augurs well for the company as the uncertainty in the profitability of the paper division was one ofthe major overhangs on the stock. Hence, the valuation could get re-rated going ahead. The demerger is expected by the end of June 2012.

� However, the key concern remains the poor volume offtake in its key market, ie Andhra Pradesh (which accounts for 37% of the total dispatches).

� At the current market price of Rs56, the stock trades at PE of 4.9x and 4.3x, discounting its FY2013 and FY2014 earnings estimates respectively.

SELAN EXPLORATION 285 11.0 7.9 5.1 23.3 26.4 31.5 500 75

Remarks: � Selan Exploration (Selan) has rights to develop five small discovered (minimal exploration risk) oil fields (Bakrol, Lohar, Indrora, Karjisan and Ognaj) inCambay Basin (Gujarat) with proven oil & gas reserves.

� Between FY2006 and FY2009, Selan ramped up its production by 4x. In the next phase (FY2009-11), with stagnating oil production it did preparatorywork to ramp up drilling in the existing fields and the new field, Indrora (the most prolific one with significant reserves). Currently, the company is waitingfor the final approval for drilling which could ramp up its production significantly in the near future.

� Based on this, we expect the company to ramp up its production more than two times by FY2014 over that of FY2011. It would lead to an earnings growth(CAGR) of 47% during FY2012-14.

� At the current market price, the stock trades at a PE of 5.1x and EV/EBITDA of 2.0x based on our FY2014 estimates. We remain bullish on its productionramp-up plan and recommend Buy with a price target of Rs500.

July 2012 Sharekhan ValueGuide14

SHAREKHAN SPECIAL OCTOBER 06, 2008

Switch from BoI to PNBAnomaly in valuations among PSU banks: The entire basket ofpublic sector banks (PSBs) has corrected significantly and rightlyso, given the asset quality concerns and deterioration in the eco-nomic environment that would affect the growth of their core busi-ness. Yet some of the stocks have been beaten down excessively.Consequently, the situation has created an anomaly in the valua-tions leading to an opportunity for investors. The case in point isBank of India (BoI) vs Punjab National Bank (PNB). For the pastthree years, BoI has traded at an average discount of 16% to PNB.However, after the Q4FY2012 results the situation has reversedand BoI is now trading at a 10% premium to PNB. In our view,this is an aberration driven by a sudden jump in the slippages andrestructured accounts of PNB and a decline in the slippages of BoIin Q4FY2012. But the divergence in the performances is not sus-tainable and the anomaly in the valuations would get correctedgoing ahead.

BOI—valuations run ahead of performanceBoI reported better than expected numbers in Q4FY2012, with asequential decline in the slippages. The sequential decline in thenon-performing assets (NPAs) was contributed by higher recover-ies from the smaller accounts (technical NPAs), though restruc-tured asset rose sharply. Though the management expects to limitthe slippages in the coming quarters, we believe the same would bea tough task as it has still not accounted for the debt recast of AirIndia. Moreover, the core income growth remained volatile withpressure on the margins. Thus, the Q4FY2012 performance seemsunsustainable due to a weaker core income growth, pressure onthe NPAs and a possible decline in the recoveries. With the expec-tations running high, any disappointment in the quarterly perfor-mance would have a sharp impact on the stock price.

PNB—better positioned to manage NPAsGiven the tough macro environment where the stress on asset qualityhas aggravated for the banking sector, PNB is in a better positionto tide over the same due to a relatively better earnings growth,higher capitalisation (tier-I capital of 9.3%) and management con-tinuity. In addition, the bank has already taken a significant hit inthe previous quarters from big-ticket loans to the infrastructuresector (including the state electricity boards), Air India etc and wedo not expect any major negative surprises going ahead. More-over, PNB also has a relatively better liability mix with a currentaccount and savings account (CASA) ratio in the 36-38% range.

Relatively strong liability base to support PNB’s marginsPNB has the second largest network of 5,680 branches and a strongpresence in north India. This contributes to the strong mobilisationof deposits including the current account and savings account(CASA) deposits. The CASA ratio of PNB is quite stable at 36-38% levels compared with 34.2% of BoI. Therefore, due to adiversified advances and liabilities mix, PNB maintains a signifi-cantly higher net interest margin (NIM) compared with BoI whichstrengthens its core income growth. We expect PNB to report a

BANKING JUNE 8, 2012

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding orhaving a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

healthy growth in its NII, driven by its superior margins and loangrowth.

BoI’s return ratios to lag PNB’s ratiosPNB has consistently maintained its return on equity (RoE) in therange of 18-22% (FY2008-12). Compared with that BoI’s RoE hasdeclined from 24% in FY2008 to 14% in FY2012. Further, thereturn on assets (RoA) of PNB has been steady at around 1.2-1.3%levels while the same has come down to 0.8% for BoI. Going ahead,we expect PNB to maintain its RoE and RoA at 18-19% and 1.1%respectively driven by a 14.5% CAGR in its earnings (FY2012-14).However, BoI’s return ratios are likely to lag (RoE and RoA of15% and 0.8% respectively in FY2014) those of the peer banks.

Management continuity a key positive for PNBManagement sustainability has been one of the key issues with thePSBs as generally shorter tenures have affected the managementinitiatives. BoI’s chairman is expected to superannuate byQ2FY2013 whereas in case of PNB the sustainability of the exist-ing management augurs well for the bank.

P/BV COMPARISON BOI VS PNB

Source: Sharekhan Research

Switch from BOI (Rs353) to PNB (Rs783)Traditionally (in the past three years) BoI traded at an average dis-count of 16% to PNB and at a 5-10% discount to Bank of Baroda(BoB) mainly on account of a slower growth, a rise in its NPAs andthe weakening of its operating performance. However, of late (sinceMay 2012, post-Q4FY2012 results), BoI has been trading at a ~10%premium to PNB while the discount vis-à-vis BoB has narrowed.While volatility in BoI’s earnings is a concern, PNB is structurally astronger bank having superior operating metrics (refer to table).Thus, we believe PNB is better positioned to manage its NPAs com-pared with BoI due to a better earnings growth, higher capitalisationand management continuity. We, therefore, recommend investorsto switch from BoI to PNB. We have a price target of Rs1,070 onPNB (1x FY2014 book value).

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb

-10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb

-11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Apr

-12

Jun-

12

BoI PNB

EQUITY FUNDAMENTALSSWITCH IDEAS

Sharekhan ValueGuide July 201215

SHAREKHAN SPECIAL OCTOBER 06, 2008

Switch from ITNL to IRB

KEY POINTS� Trading premium gap at all-time high; buying opportunity in

IRB: The recent sharp correction in IRB Infrastructure Devel-opers (IRB) has created a huge divergence in the valuations ofIRB and IL&FS Transportation Ltd (ITNL). ITNL trades at a40% premium to IRB as against a mean average of an 11%premium and the usual band of a 5% to 20% premium. Not-withstanding the legal tangles of the IRB promoter, we believethat the divergence of more than 2x standard deviation (2SD)offers a compelling buying opportunity.

CONSTRUCTION JUNE 22, 2012

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

SWITCH IDEASEQUITY FUNDAMENTALS

inflation still at levels beyond the comfort zone of the centralbank), we think the interest rate reversal cycle might be delayedby one or two quarters. For the companies with a high debtburden this would mean continued pain in terms of high inter-est charges for at least the next couple of quarters. Here, wethink IRB is better placed in comparison with ITNL since thedebt/equity ratio of IRB stands at 2.5 vs 3.7 for ITNL. On acloser analysis of the interest payments we find that while IRBpays almost 40% of its operating profit as interest charge, ITNLpays 50% of the same as interest charge (due to the interestpayment on the annuity projects under construction). Further,in the last two years, IRB has been efficient in generating higherreturns on invested capital (RoIC) as compared with ITNL withthe FY2012 RoIC at 11.5% as compared with ITNL’s 9.3%.

� Switch from ITNL (Rs180) to IRB (Rs126): Fundamentally,we like both the companies and believe both would be likelybeneficiaries of the tall target set by the National HighwaysAuthority of India for project awarding this fiscal. In fact, ITNLshall score better than IRB on many financial parameters overthe long term. However, the recent event-driven sharp correc-tion in IRB has thrown open a tactical opportunity to shift fromITNL to IRB for superior returns in the near term.

ITNL’S PREMIUM OVER IRB—AT AN ALL-TIME HIGH

� IRB—sharp correction and clearance from a legal case to limitthe downside: Though the charges levied against the promoterof IRB are serious, the correction of over 30% in the stockfactors in a lot of the negatives and has made the stock avail-able at a 40% discount to its mean average valuation multiple.The improving outlook for the road infrastructure developersshould limit the downside risk in the stock though. Moreover,any positive development on the legal issue could result in asharp re-rating of the stock.

� IRB’s profitability less vulnerable to interest rates: Consideringthe economic turbulence that our country is going through (with

IRB’S ONE-YEAR FORWARD PE BAND

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb

-11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Apr

-12

Jun-

12

+2σ

+1σ

Mean

-1σ

-2σ

-

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Feb

-08

May

-08

Aug

-08

Nov

-08

Feb

-09

May

-09

Aug

-09

Nov

-09

Feb

-10

May

-10

Aug

-10

Nov

-10

Feb

-11

May

-11

Aug

-11

Nov

-11

Feb

-12

May

-12

20x

16x

12x

8x

VALUATIONS (IRB)Particulars FY2010 FY2011 FY2012 FY2013E FY2014ESales (Rs cr) 1,704.9 2,438.1 3,130.5 3,899.9 4,842.8YoY growth % 71.9 43.0 28.4 24.6 24.2EBITDA (Rs cr) 799.1 1,093.9 1,373.3 1,592.2 1,963.3Margins % 46.9 44.9 43.9 40.8 40.5Adjusted net profit (Rs cr) 385.5 452.4 495.8 431.6 422.8YoY growth % 119.2 17.4 9.6 (13.0) (2.0)Shares in issue (cr) 33.2 33.2 33.2 33.2 33.2EPS (Rs) 11.6 13.6 14.9 13.0 12.7YoY growth % 119.2 17.4 9.6 (13.0) (2.0)PER (x) 10.9 9.3 8.4 9.7 9.9Book value (Rs) 61.4 73.2 86.0 96.8 107.5P/BV (Rs) 2.1 1.7 1.5 1.3 1.2RoCE (%) 14.2 15.3 13.9 11.4 11.5RoNW (%) 20.4 20.2 18.7 14.2 12.5

July 2012 Sharekhan ValueGuide16

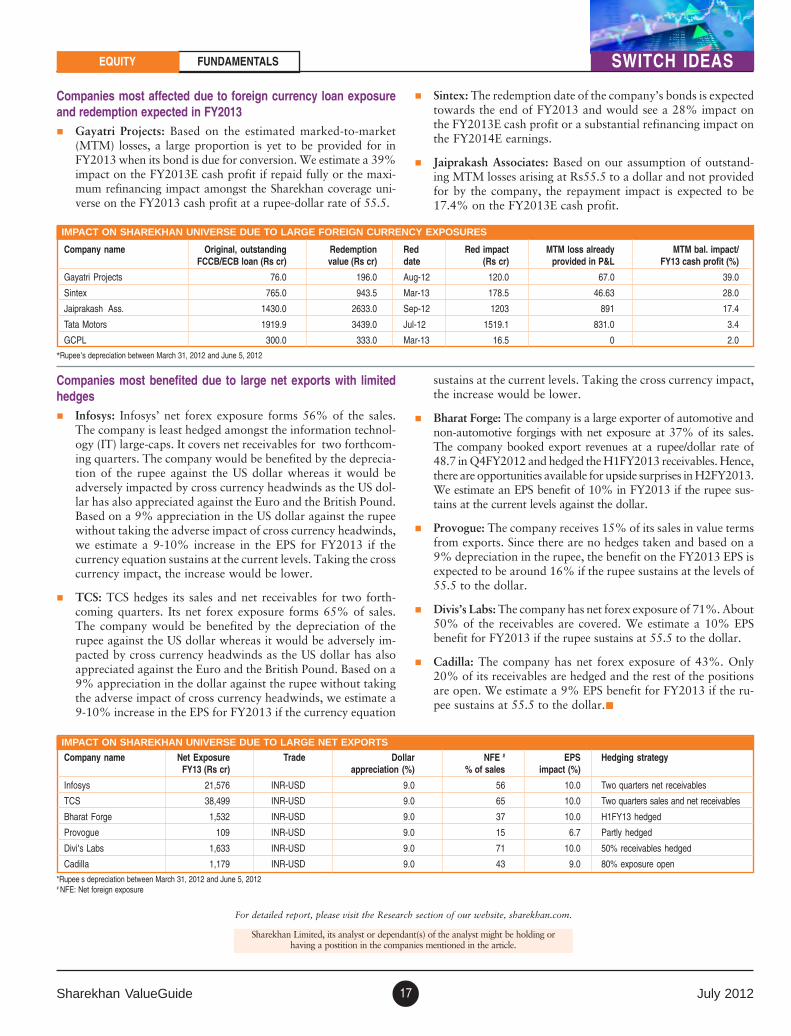

SHAREKHAN SPECIAL OCTOBER 06, 2008Impact analysis of sharp fall in rupee on

Sharekhan universeCurrency impact on Sharekhan coverage universeWe applied four conditions on our coverage universe to ascertainthe impact of the rupee’s depreciation on various companies. Ourfindings reflect that Maruti Suzuki (Maruti) and Hero MotoCorp(Hero) have been affected the most due to expensive raw materialimports and royalty pay-outs. Gayetri Projects and Sintex Indus-tries (Sintex) would be affected the most on account of their for-eign currency loan exposures. The companies that will benefit themost are Infosys, Tata Consultancy Services (TCS), Provogue,Bharat Forge, Divi’s Laboratories (Divi’s Labs) and CadillaHealthcare (Cadilla). We have assumed a rupee/dollar rate of 55.5and a rupee/yen rate of 1.40.

Companies affected due to large net forex outflows with limitedhedges� Maruti: Maruti’s direct and indirect (vendor) imports form

approximately 21% of its sales. The exports form roughly 10%of its revenues; the euro-based exports form 4% of its sales andare naturally hedged while the dollar-denominated exports getadjusted against the yen-denominated imports. We estimate thecompany’s net exposure to yen at around 16-17% of its sales.We estimate an impact of 15% on the earnings per share (EPS)if the rupee sustains at 1.40 to the yen, taking into account theimpact for H2FY2013.

FOREX PLAYS JUNE 11, 2012

� Hero: The company’s direct and indirect imports form 16%(direct 2% and indirect 14%) of its net sales while its exportsform roughly 2.0-2.5% of its sales. Hence, net of exports , theraw material cost forms around 14% of its net sales and theraw materials are largely imported by vendors in yen denomi-nation. We estimate an EPS impact of 13% if the rupee sustainsat 1.40 to the yen.

� Apollo Tyres: The imports form roughly 21% of the consoli-dated sales while the exports are pegged at 5.5% of the consoli-dated sales. Usually, the impact is felt with the lag of a quarter.Based on the net import exposure and the fact that there are nohedges, the company would see an EPS impact of 17.7% if therupee sustains at 55.5 to the dollar for the next three quartersof FY2013.

� Tata Chemicals: The company’s fertiliser imports form 22% ofits sales and are largely dollar denominated. Most of the hedgesare taken for one quarter, hence the impact of the local currency’sdepreciation would be felt from Q2YF2013 onwards. The com-pany had been able to offset the cost escalations in the past butif it is unable to pass on the price hikes to the end-customer, theimpact of the rupee’s depreciation on the EPS is expected to be15.5% over the three quarters of FY2013.

Company name Net exposure Traded Rupee’s Imported RM / EPS Hedging strategyFY13 (Rs cr) currency depreciation (%) Fuel % of sales impact (%)

Maruti Suzuki 7675 INR-YEN -13.0 17.0 -15.1 Hedged—H1FY2013Hero MotoCorp 3765 INR-YEN -13.0 14.0 -13.0 No hedgesApollo Tyres 2201 INR-USD -9.0 15.5 -17.7 No hedgesTata Chemicals 3146 INR-USD -9.0 22.0 -15.5 Qtrly. hedgingShree Cement 556.9 INR-USD -9.0 10.2 -5.3 Impact in H2FY13India Cements 544.0 INR-USD -9.0 12.0 -5.2 Impact in H2FY13

CESC 276.0 INR-USD -9.0 5.1 -3.8 No hedging

*Rupee’s depreciation between March 31, 2012 and June 5, 2012

IMPACT ON SHAREKHAN UNIVERSE DUE TO LARGE NET FOREX OUTFLOWS

Companies affected due to royalty exposure to parent with limitedhedges� Maruti: Royalty forms 5.5% of the company’s sales. The com-

pany pays royalty bi-annually. It has hedged its rupee-yen ex-posure for H1FY2013; hence, the impact would be felt inH2FY2013. We estimate an EPS impact of 4.1% if the rupeesustains at 1.40 against the yen.

� Hero: The company pays Rs180 crore as fixed royalty to HondaMotor Co. and charges the same under “depreciation” everyquarter. On new models the royalty payable is around 1% ofsales. We estimate the annual royalty bill to Honda Motor Co.at Rs989 crore for FY2013 and an EPS impact of 3.5% if therupee sustains at the current levels against the yen.

Company name Exposure Trade Rupee’s Royalty EPS Hedging strategyFY13E (Rs cr) currency depreciation (%) % of sales impact (%)

Maruti 2,483 INR-YEN -13.0 5.5 -4.1 Hedged for H1FY13

Hero MotoCorp 989 INR-YEN -13.0 3.7 -3.5 No hedges, full impact

*Rupee’s depreciation between March 31, 2012 and June 5, 2012

IMPACT ON SHAREKHAN UNIVERSE DUE TO LARGE ROYALTY PAYOUTS

EQUITY FUNDAMENTALSSWITCH IDEAS

Sharekhan ValueGuide July 201217

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding orhaving a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Companies most affected due to foreign currency loan exposureand redemption expected in FY2013� Gayatri Projects: Based on the estimated marked-to-market

(MTM) losses, a large proportion is yet to be provided for inFY2013 when its bond is due for conversion. We estimate a 39%impact on the FY2013E cash profit if repaid fully or the maxi-mum refinancing impact amongst the Sharekhan coverage uni-verse on the FY2013 cash profit at a rupee-dollar rate of 55.5.

� Sintex: The redemption date of the company’s bonds is expectedtowards the end of FY2013 and would see a 28% impact onthe FY2013E cash profit or a substantial refinancing impact onthe FY2014E earnings.

� Jaiprakash Associates: Based on our assumption of outstand-ing MTM losses arising at Rs55.5 to a dollar and not providedfor by the company, the repayment impact is expected to be17.4% on the FY2013E cash profit.

Companies most benefited due to large net exports with limitedhedges� Infosys: Infosys’ net forex exposure forms 56% of the sales.

The company is least hedged amongst the information technol-ogy (IT) large-caps. It covers net receivables for two forthcom-ing quarters. The company would be benefited by the deprecia-tion of the rupee against the US dollar whereas it would beadversely impacted by cross currency headwinds as the US dol-lar has also appreciated against the Euro and the British Pound.Based on a 9% appreciation in the US dollar against the rupeewithout taking the adverse impact of cross currency headwinds,we estimate a 9-10% increase in the EPS for FY2013 if thecurrency equation sustains at the current levels. Taking the crosscurrency impact, the increase would be lower.

� TCS: TCS hedges its sales and net receivables for two forth-coming quarters. Its net forex exposure forms 65% of sales.The company would be benefited by the depreciation of therupee against the US dollar whereas it would be adversely im-pacted by cross currency headwinds as the US dollar has alsoappreciated against the Euro and the British Pound. Based on a9% appreciation in the dollar against the rupee without takingthe adverse impact of cross currency headwinds, we estimate a9-10% increase in the EPS for FY2013 if the currency equation

sustains at the current levels. Taking the cross currency impact,the increase would be lower.

� Bharat Forge: The company is a large exporter of automotive andnon-automotive forgings with net exposure at 37% of its sales.The company booked export revenues at a rupee/dollar rate of48.7 in Q4FY2012 and hedged the H1FY2013 receivables. Hence,there are opportunities available for upside surprises in H2FY2013.We estimate an EPS benefit of 10% in FY2013 if the rupee sus-tains at the current levels against the dollar.

� Provogue: The company receives 15% of its sales in value termsfrom exports. Since there are no hedges taken and based on a9% depreciation in the rupee, the benefit on the FY2013 EPS isexpected to be around 16% if the rupee sustains at the levels of55.5 to the dollar.

� Divis’s Labs: The company has net forex exposure of 71%. About50% of the receivables are covered. We estimate a 10% EPSbenefit for FY2013 if the rupee sustains at 55.5 to the dollar.

� Cadilla: The company has net forex exposure of 43%. Only20% of its receivables are hedged and the rest of the positionsare open. We estimate a 9% EPS benefit for FY2013 if the ru-pee sustains at 55.5 to the dollar.�

IMPACT ON SHAREKHAN UNIVERSE DUE TO LARGE FOREIGN CURRENCY EXPOSURES

Company name Original, outstanding Redemption Red Red impact MTM loss already MTM bal. impact/ FCCB/ECB loan (Rs cr) value (Rs cr) date (Rs cr) provided in P&L FY13 cash profit (%)

Gayatri Projects 76.0 196.0 Aug-12 120.0 67.0 39.0

Sintex 765.0 943.5 Mar-13 178.5 46.63 28.0

Jaiprakash Ass. 1430.0 2633.0 Sep-12 1203 891 17.4

Tata Motors 1919.9 3439.0 Jul-12 1519.1 831.0 3.4

GCPL 300.0 333.0 Mar-13 16.5 0 2.0

*Rupee’s depreciation between March 31, 2012 and June 5, 2012

IMPACT ON SHAREKHAN UNIVERSE DUE TO LARGE NET EXPORTS

Company name Net Exposure Trade Dollar NFE # EPS Hedging strategyFY13 (Rs cr) appreciation (%) % of sales impact (%)

Infosys 21,576 INR-USD 9.0 56 10.0 Two quarters net receivables

TCS 38,499 INR-USD 9.0 65 10.0 Two quarters sales and net receivables

Bharat Forge 1,532 INR-USD 9.0 37 10.0 H1FY13 hedged

Provogue 109 INR-USD 9.0 15 6.7 Partly hedged

Divi's Labs 1,633 INR-USD 9.0 71 10.0 50% receivables hedged

Cadilla 1,179 INR-USD 9.0 43 9.0 80% exposure open

*Rupee’s depreciation between March 31, 2012 and June 5, 2012# NFE: Net foreign exposure

SWITCH IDEASEQUITY FUNDAMENTALS

July 2012 Sharekhan ValueGuide18

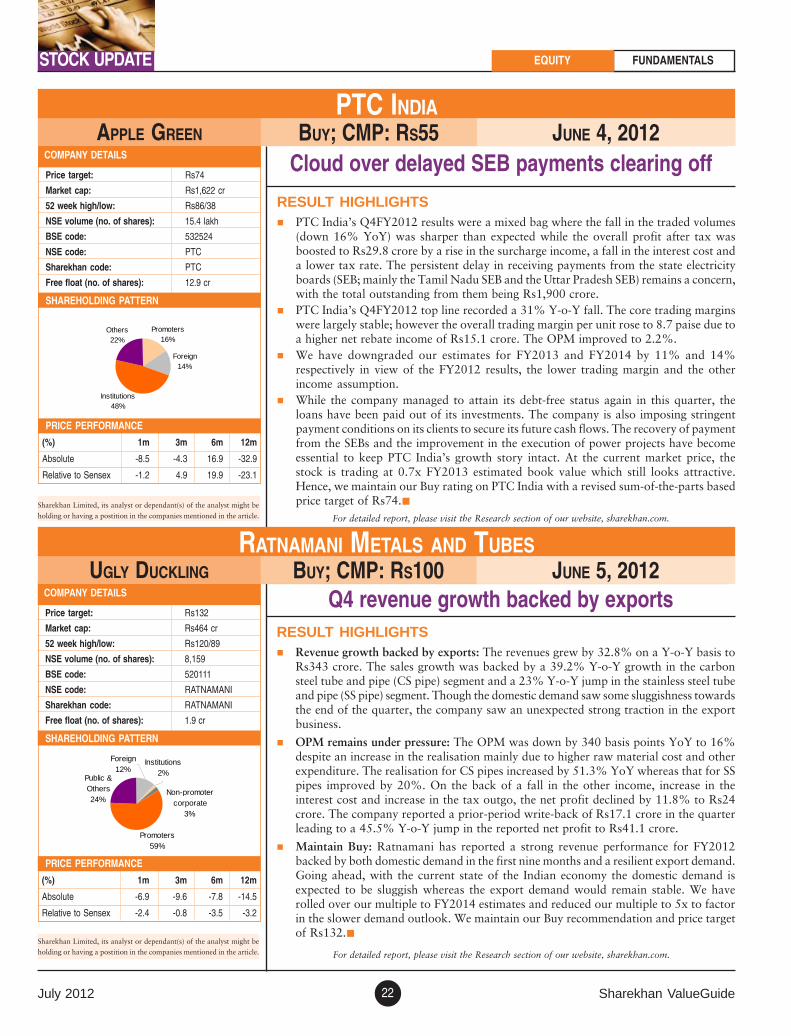

FY2012 audited PAT up 9.7% against unaudited numbersCOMPANY DETAILS

Price target: Rs1,805

Market cap: Rs10,360 cr

52 week high/low: Rs1,765/1,199

NSE volume (no. of shares): 44,272

BSE code: 500049

NSE code: BEL

Sharekhan code: BEL

Free float (no, of shares): 1.9 cr

(%) 1m 3m 6m 12m

Absolute 2.3 -17.5 -7.0 -16.7

Relative to Sensex -4.2 -17.0 -14.2 -15.2

PRICE PERFORMANCE

APPLE GREEN BUY; CMP: RS1,295 JUNE 25, 2012BHARAT ELECTRONICS

KEY POINTSFY2012 audited PAT up 9.7%: The audited financial numbers for FY2012 show animproved financial performance for Bharat Electronics Ltd (BEL) against the unauditedfinancials that were declared by the company in April this year. The FY2012 audited netprofit is higher by 9.7% at Rs829.9 crore against the unaudited net profit of Rs756.3crore.

The main reasons for the 9.7% increase in the net profit are� The operating cost decreased by Rs45.8 crore (0.8% of revenues) mainly on the back

of lower consumption of raw materials and a lower employee cost. The raw materialconsumed was lower due to a higher stock adjustment. This led the EBITDA margin torise to 8.7% in the audited financials against 7.8% in the unaudited financials.

� The effective tax rate in the audited financials reduced to 22.8% against 25.9% in theaudited financials.

Valuation and view: With the increase in the defence budget and the focus on modernisationof the defence technology, BEL is best placed to take a sizeable pie of the defence spend.The order book at 4.5x FY2012 sales gives BEL strong revenue visibility for at least thenext three years. The huge cash reserve of Rs847 per share gives the stock further support.The key risks, however, remain the timely delivery of orders and the margin performance,which has deteriorated through FY2012. We maintain our Buy rating on the stock with aprice target of Rs1,805.�

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might be

holding or having a postition in the companies mentioned in the article. For detailed report, please visit the Research section of our website, sharekhan.com.

Seizing loss in retailCOMPANY DETAILS

Price target: Rs405

Market cap: Rs3,353 cr

52 week high/low: Rs364/186

NSE volume (no. of shares): 2.4 lakh

BSE code: 500084

NSE code: CESC

Sharekhan code: CESC

Free float (no. of shares): 7.0 cr

(%) 1m 3m 6m 12m

Absolute 4.3 -12.9 25.5 -4.3

Relative to Sensex 0.8 -7.1 18.4 3.4

PRICE PERFORMANCE

UGLY DUCKLING BUY; CMP: RS267 JUNE 15, 2012CESC

KEY POINTSConsolidated results show decline in PAT: CESC reported its consolidated results withsatisfactory growth at the operational level. The decline at the net profit level was driven bydiscontinuation of deferred tax benefits this year. The power segment’s performance remainshealthy whereas the retail business continues to be loss making at the operating level.

Slow but steady improvement in reducing losses; but Spencer’s continues to burn cash: Thenet revenue from the retail business (Spencer’s) grew by 23% year on year (YoY) in FY2012.The revenues per sq ft grew by 11% to Rs11,550 in FY2012 but reported an operating lossat~13% which was 30% in FY2009. There was equity infusion of Rs108 crore in Spencer’sduring FY2012. There’s been an improvement in working capital management as inventorydays dropped from 42 days to 32 days.

ABPC yet to see profitability; gets equity injection: The net sales of ABPC jumped by 119%YoY to Rs9 crore in FY2012, driven by new store growth. However, the operating loss grewby 40%, and posted a net loss of Rs7 crore. The business however got an equity infusion ofRs10 crore in FY2012 as the management holds a positive outlook for the business.

Interest free loan from holding company to Music World to pinch investors: The sales ofthe Music World business are falling gradually; they declined by 28% in FY2012, followingan 11% YoY decline in FY2011. The losses were however restricted at Rs11 crore versusa loss of Rs13 crore in FY2011. Rs18.5 crore of interest free loan extended to MusicWorld by the holding company would pinch investors as the very outlook and the businessmodel is bleak.

Valuation and view: As expected the retail business is slowly progressing in reducing losses.However, we continue to have a Buy recommendation on CESC and retain our price targetof Rs405.�

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might be

holding or having a postition in the companies mentioned in the article. For detailed report, please visit the Research section of our website, sharekhan.com.