vat and international regulatory impact on global ariba ... invoicing and regulatory requirements...

TRANSCRIPT

VAT and international regulatory impact on global Ariba deployments2018

2

Presenters

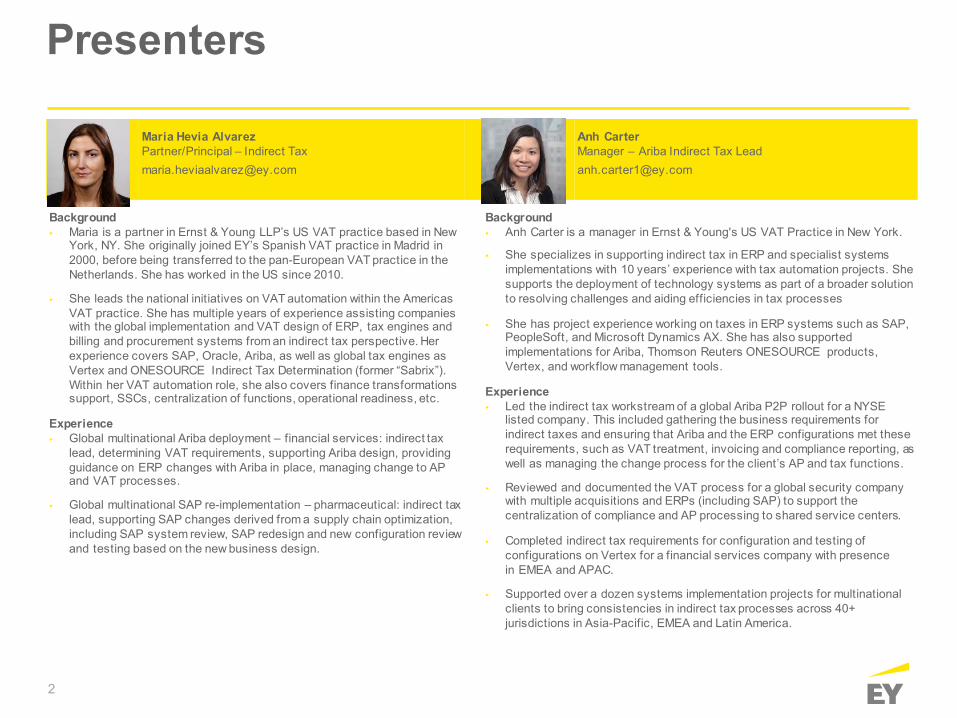

Maria Hevia AlvarezPartner/Principal – Indirect [email protected]

Anh CarterManager – Ariba Indirect Tax [email protected]

Background► Maria is a partner in Ernst & Young LLP’s US VAT practice based in New

York, NY. She originally joined EY’s Spanish VAT practice in Madrid in 2000, before being transferred to the pan-European VAT practice in the Netherlands. She has worked in the US since 2010.

► She leads the national initiatives on VAT automation within the Americas VAT practice. She has multiple years of experience assisting companies with the global implementation and VAT design of ERP, tax engines and billing and procurement systems from an indirect tax perspective. Her experience covers SAP, Oracle, Ariba, as well as global tax engines as Vertex and ONESOURCE Indirect Tax Determination (former “Sabrix”). Within her VAT automation role, she also covers finance transformations support, SSCs, centralization of functions, operational readiness, etc.

Experience► Global multinational Ariba deployment – financial services: indirect tax

lead, determining VAT requirements, supporting Ariba design, providing guidance on ERP changes with Ariba in place, managing change to AP and VAT processes.

► Global multinational SAP re-implementation – pharmaceutical: indirect tax lead, supporting SAP changes derived from a supply chain optimization, including SAP system review, SAP redesign and new configuration review and testing based on the new business design.

Background► Anh Carter is a manager in Ernst & Young's US VAT Practice in New York.

► She specializes in supporting indirect tax in ERP and specialist systems implementations with 10 years’ experience with tax automation projects. She supports the deployment of technology systems as part of a broader solution to resolving challenges and aiding efficiencies in tax processes

► She has project experience working on taxes in ERP systems such as SAP, PeopleSoft, and Microsoft Dynamics AX. She has also supported implementations for Ariba, Thomson Reuters ONESOURCE products, Vertex, and workflow management tools.

Experience► Led the indirect tax workstream of a global Ariba P2P rollout for a NYSE

listed company. This included gathering the business requirements for indirect taxes and ensuring that Ariba and the ERP configurations met these requirements, such as VAT treatment, invoicing and compliance reporting, as well as managing the change process for the client’s AP and tax functions.

► Reviewed and documented the VAT process for a global security company with multiple acquisitions and ERPs (including SAP) to support the centralization of compliance and AP processing to shared service centers.

► Completed indirect tax requirements for configuration and testing of configurations on Vertex for a financial services company with presence in EMEA and APAC.

► Supported over a dozen systems implementation projects for multinational clients to bring consistencies in indirect tax processes across 40+ jurisdictions in Asia-Pacific, EMEA and Latin America.

3

What is VAT?

4

What is VAT?

► Value-added Tax

► At bottom, VAT systems are similar to sales tax systems, in that both are aimed at taxing private consumption, rather than transactions between businesses

► The key difference between sales tax and VAT is that ► Sales tax is generally charged only on consumption itself (single-stage cumulative tax); whereas ► VAT is also charged on transactions between businesses ⏤ but may then be recovered (multiple-

stage noncumulative tax)

► There are additional differences between VAT systems and sales tax

► VAT was first suggested in Germany in the wake of WWI, and first introduced in France in 1954

► The largest of all the global indirect taxes

► The average VAT rate is 19%-21% (and increasing)

► No VAT in the US and US territories, e.g., Puerto Rico. The possibility of introducing VAT in the US has been floated from time to time

5

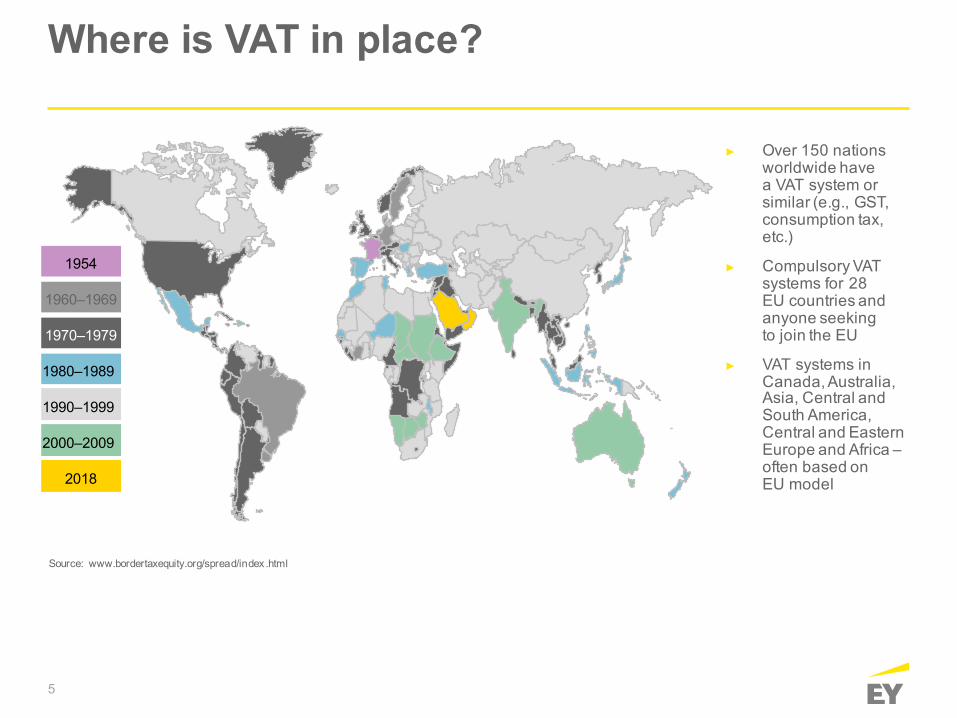

Where is VAT in place?

► Over 150 nations worldwide have a VAT system or similar (e.g., GST, consumption tax, etc.)

► Compulsory VAT systems for 28 EU countries and anyone seeking to join the EU

► VAT systems in Canada, Australia, Asia, Central and South America, Central and Eastern Europe and Africa –often based on EU model

1954

1960–1969

1980–1989

2000–2009

2018

1970–1979

1990–1999

Source: www.bordertaxequity.org/spread/index .html

6

How VAT works(Sales tax rate: 10%)

Buys 450+45

Total tax collected45

Stage 4consumer

Buys (100)Sells 250

Stage 2makes trees intofurniture

Sells 450+45

Sales tax remitted to gov’t

45

Stage 3furniture shop

Buys NilSells 100

Stage 1sells trees

Buys (250)

7

How VAT works(VAT rate: 10%)

Buys 450 + 45

Total tax collected45

Stage 4consumer

Buys (100 + 10)Sells 250 + 25

To Gov’t 15

Stage 2makes trees intofurniture

Buys (250 + 25)Sells 450 + 45

To Gov’t 20

Stage 3furniture shop

Buys NilSells 100 + 10

To Gov’t 10 Cash flow

Stage 1sells trees

8

Tax rates and exemptions

► General treatment: standard VAT rate applies (17%–27%)► Reduced VAT rate may apply to specific supplies (5%–18%)

► Will differ on a country-by-country basis► Exemptions with the right to deduct the input VAT

► Taxable supplies “zero rated”► Export of goods, services connected with export of goods► Intra-community supplies of goods to another EU member state ► Financial services supplied to non-EU customers

► Exemptions without the right to deduct the input VAT► Medical, health care and social services ► Financial and insurance services► Immovable property transactions ► Option to tax available for financial and immovable property

in some countries

9

Recovery of input VAT

► VAT is generally recoverable on any inputs (purchases and expenses) incurred in relation to taxable business activity

► VAT is generally not recoverable on inputs incurred for the purposes of:► Private use ► Noneconomic activity, e.g., holding companies► Exempt transactions, e.g.:

► Certain financial transactions (share transactions, loans, forex, insurance)► Real estate transactions (e.g., sale and lease)► Health care► NGOs► University tuition

► Formalities: input tax is only recoverable by the taxable person who receives the supply and under the condition that it has a valid invoice and accounting documents, import resolutions, etc.

10

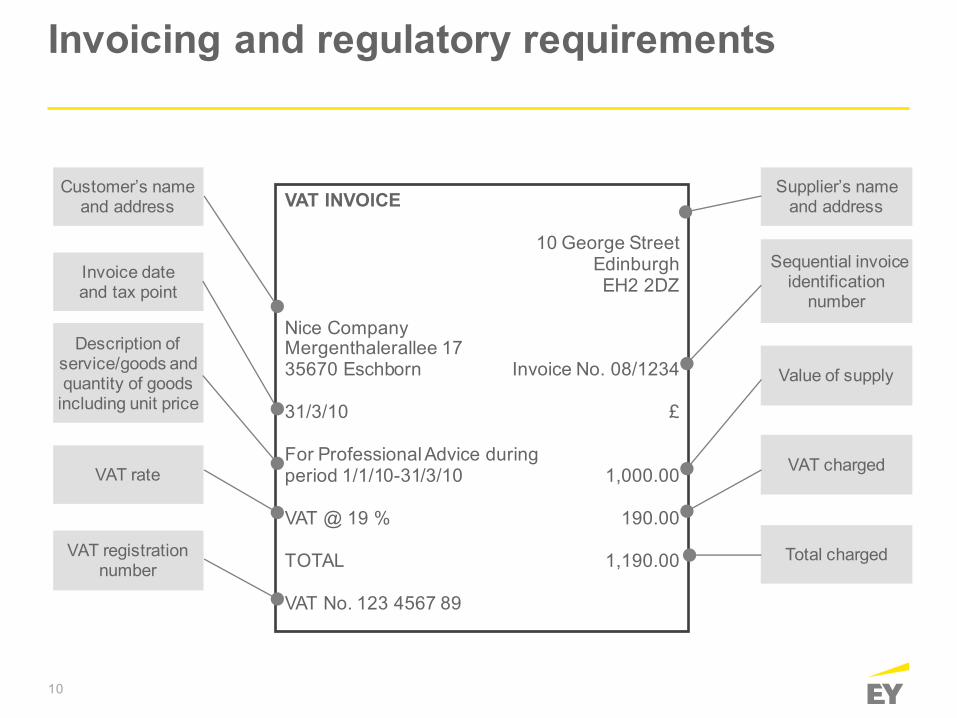

Invoicing and regulatory requirements

VAT INVOICE

10 George StreetEdinburghEH2 2DZ

Nice CompanyMergenthalerallee 1735670 Eschborn Invoice No. 08/1234

31/3/10 £

For Professional Advice duringperiod 1/1/10-31/3/10 1,000.00

VAT @ 19 % 190.00

TOTAL 1,190.00

VAT No. 123 4567 89

Customer’s name and address

Invoice date and tax point

Description of service/goods and quantity of goods

including unit price

VAT rate

VAT registration number

Supplier’s name and address

Sequential invoice identification

number

Value of supply

VAT charged

Total charged

Page 11

What is the impact of VAT?

12

Why VAT matters?v

► Failure to reclaim input VAT or recoverable VAT ⏤ then VAT becomes a cost for the business

► Risk of overdeducting input VAT incorrectly charged by the vendor ► Cash flow impact

► Pay and reclaim later► Some countries do not repay excess input VAT over output VAT ► Have to carry forward (notably South American and Eastern European countries)► Some countries make it very difficult to reclaim credit VAT (notably Italy/Greece)

► Compliance burden to file returns► Penalties and Interest (5%–200%)

13

Why VAT matters? Driving change into VAT management

Increased focus of tax authorities

Cash pressures within the business

Increased supply chain complexity

Further business push into emerging markets

Increased tax automation

Impact on indirect tax functions

Expansion of shared service centers

14

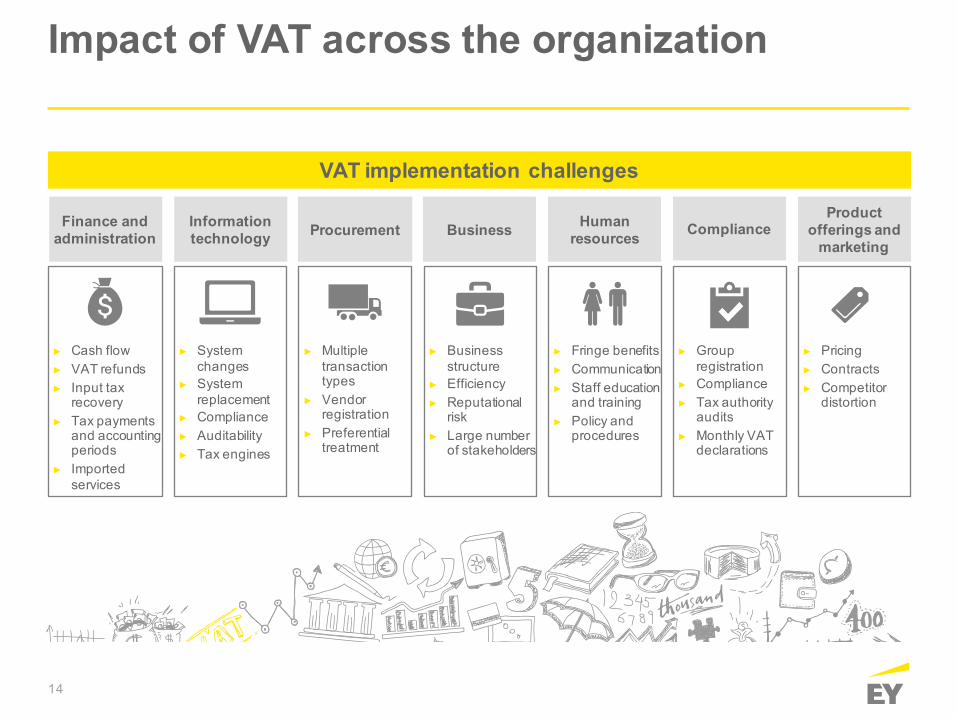

Impact of VAT across the organization

VAT implementation challenges

► Cash flow► VAT refunds► Input tax

recovery► Tax payments

and accounting periods

► Imported services

► System changes

► System replacement

► Compliance► Auditability► Tax engines

► Multiple transaction types

► Vendor registration

► Preferential treatment

► Business structure

► Efficiency► Reputational

risk► Large number

of stakeholders

► Fringe benefits► Communication► Staff education

and training► Policy and

procedures

► Group registration

► Compliance► Tax authority

audits► Monthly VAT

declarations

► Pricing ► Contracts► Competitor

distortion

Finance and administration ComplianceInformation

technology Procurement Business Human resources

Product offerings and

marketing

Page 15

What is the impact of VAT on Aribadeployments?

16

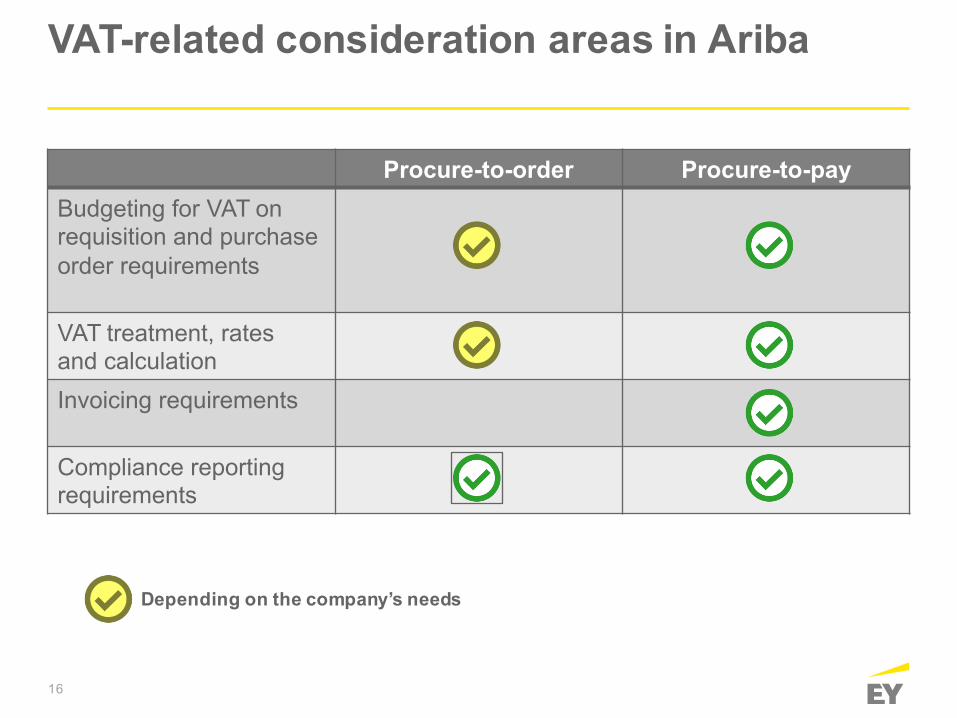

VAT-related consideration areas in Ariba

Procure-to-order Procure-to-payBudgeting for VAT on requisition and purchase order requirements

VAT treatment, rates and calculationInvoicing requirements

Compliance reporting requirements

Depending on the company’s needs

17

Requisition and purchase order requirements for VAT

► Indirect taxes could be overlooked early in the procurement process, as there are usually no regulatory requirements for their inclusion in requisitions and purchase orders. However, there could be business requirements impacted by these taxes downstream.

► Companies making VAT exempt supplies, such as financial services, may not be able to fully recover all input VAT on associated purchases.

► Input VAT could add up to 27% to the net amount (standard VAT rate in Hungary) and higher if considering multiple VAT rates in Brazil. This input VAT could be a significant additional cost to net price of purchase and should be taken into account when budgeting.

► The budget holder may not be aware of the full cost (amount to be paid to supplier and tax authorities) associated with approving the purchase.

► Cannot rely on the amounts quoted from the supplier where reverse charge applies (the VAT needs to be self-accounted by the buyer on intra-EU, imports and some domestic purchases). Supplier issued sales orders or invoices would not show the VAT amount to self-account for reverse charge.

► Purchases could be underbudgeted and could carry cash flow/working capital implications to overall business.

► Capture business requirements and process for budgeting, requisition and purchase orders► Provide VAT requirements for the determination of the full cost for budget/requisition► Provide input on design and configuration of ERP and Ariba to meet these requirements

Background

Risk

How EY can help

18

▶ There are differences in VAT treatment depending on goods and services, among other factors.▶ These are regulatory requirements that determine the correct accounting and reporting of VAT.▶ IT and other business functions may not recognize the necessity of these distinctions for VAT and the implications

of incorrectly configuring for VAT in the ERP or Ariba.

▶ When the design and configuration of the ERP or Ariba are not aligned with VAT requirements, significant manual effort may be required downstream to adjust postings to ensure regulatory requirements are met. These include:

▶ Products defaulted as either goods/services on postings when the VAT treatment/place of supply rules may be different for each and should be considered separately

▶ Products defaulted to one rate of VAT at the invoice header when line items carry different VAT rates▶ Defaulted tax codes for the above that may lead to incorrect VAT compliance reporting

▶ Capture VAT requirements for AP and AR transaction flows and correct VAT treatment▶ Provide input on design and configuration to meet these VAT requirements and correct assignment of tax codes for

accurate VAT compliance reporting from ERP and Ariba▶ Support documentation for change and maintenance

VAT treatment, rates and calculation

Background

Risk

How EY can help

19

▶ A valid VAT invoice is required in order to reclaim input VAT.▶ These invoicing requirements can vary country by country.▶ AP processing review and validate invoices on postings.

► Validation is carried out on a manual basis from AP staff who may not have sufficient VAT knowledge.► Spot checks may only be carried out on a low number of invoices, creating a risk of invalid invoices going

unnoticed where high volumes of invoices are processed overall.► Potential over-recovery of input VAT without sufficient VAT invoices to support recovery.

▶ Capture VAT requirements for invoicing for each country▶ Design and support the validation of invoices by requesting mandatory electronic invoice information from suppliers

in Ariba▶ Provide training and guides to support AP processing in Ariba and ERP

Invoicing requirements and validation

Background

Risk

How EY can help

20

Key VAT activities in Ariba and ERP deployment methodology

► Business requirements document capturing:

► Local e-invoicing requirements to support VAT recovery

► VAT rate types and product mapping

► AP high-level transaction flow mapping with VAT treatment

► Provide VAT reporting requirements, including data requirements

► Determine impact to AP process with upstream changes in Source-to-Pay process

► Functional design specification and localization of global design template detailing:

► E-invoicing validations► VAT logic to reflect flow

mapping captured► ERP tax code sufficient to

meet VAT reporting requirements

► Any gaps in meeting requirements; how they could be addressed with system customization or process workarounds

► Document new AP process flow for global and local AP

► Document any changes to VAT reporting process

► Workshops to walk through changes to AP process with global and local AP teams

► Workshops to walk through any changes to VAT reporting with global and local tax teams

► Document maintenance protocol for changes in VAT requirements in Ariba and ERP systems and change request process

► Hypercare: VAT support for post go-live with Ariba and VAT reporting in ERP

► Determine deployment strategy – project plan, timeline, jurisdictions, phases► Central coordination and process integrations across stakeholders – procurement, AP, tax, systems, etc.► Global design template with key AP flows, invoicing and VAT reporting requirements in consideration of jurisdictions and systems in scope

Go-live and ongoingRequirements Design Configuration and testing

► Support during Aribaconfiguration with VAT queries

► Define relevant VAT scenarios for testing in Aribaand flow to ERP

► Assist unit testing and UAT, validate outcome against VAT invoicing, transaction flow mapping and reporting requirements

► Review Ariba and ERP integration/middleware / connectors to ensure ERP records transactions correctly

► Review compliance reports generated by ERP from VAT bookings passed from Aribato confirm accuracy

Global/core PMO

21

Thank you

22

Would you like to find out more about VAT?

Maria Hevia AlvarezVAT Principal+1 (646) [email protected]

Anh CarterVAT Manager+1 (973) [email protected]

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Indirect Tax Services

Indirect taxes affect the supply chain and the financial system. Our network of dedicated indirect tax professionals combines technical knowledge with industry understanding and access to technologically advanced tools and methodologies. We identify risk areas and sustainable planning opportunities for indirect taxes throughout the tax life cycle, helping you meet your compliance obligations and your business goals around the world. Our globally integrated teams will give you the perspective and support you need to manage indirect taxes effectively.

© 2017 EYGM Limited.2017 All Rights Reserved.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com