venture capital in india-ppt

TRANSCRIPT

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 1/84

Private Placement

Private Equity

Venture

C

apital

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 2/84

Atul 2

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 3/84

Atul 3

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 4/84

Atul 4

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 5/84

Atul 5

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 6/84

Atul 6

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 7/84

Atul 7

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 8/84

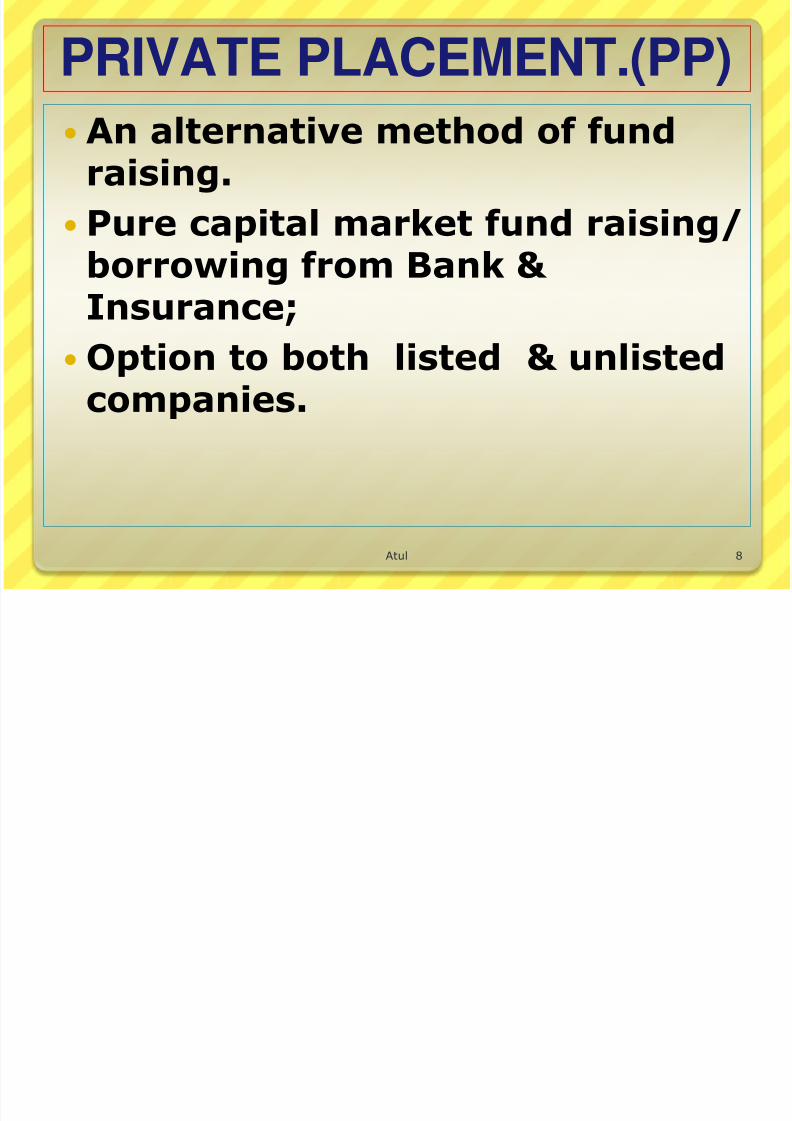

PRIVATE PLACEMENT.(PP)

An alternative method of fundraising.

Pure capital market fund raising/

borrowing from Bank & Insurance;

Option to both listed & unlisted

companies.

Atul 8

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 9/84

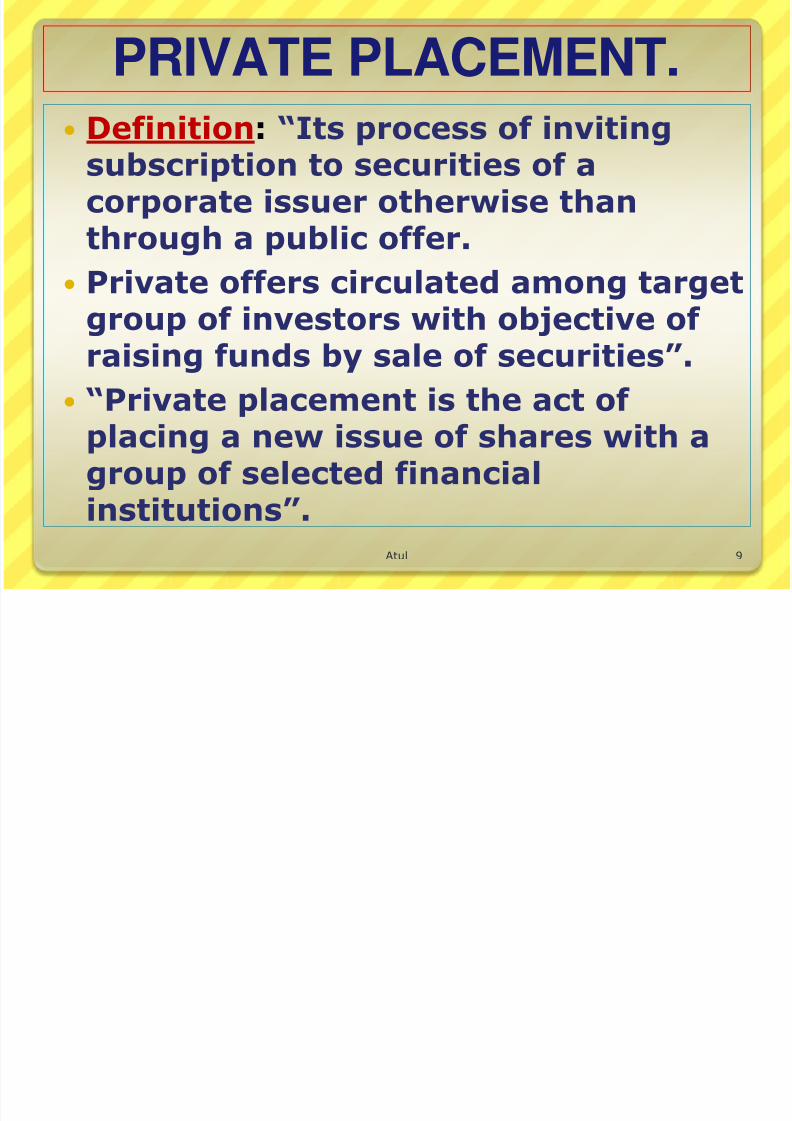

PRIVATE PLACEMENT.

Definition: “Its process of invitingsubscription to securities of acorporate issuer otherwise thanthrough a public offer.

Private offers circulated among targetgroup of investors with objective of raising funds by sale of securities”.

“Private placement is the act of placing a new issue of shares with agroup of selected financialinstitutions”.

Atul 9

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 10/84

PRIVATE PLACEMENT.

Bloomberg defines P P as “The transferringof securities to a small group of investors.The sale of bond or other securities directlyto a limited Nos. of investors, aninstitutional investor like insurance

Co..antithesis of public offering”.

PP Does not require issue of prospectus andregulatory clearance.

when securities proposed to be listed need

to comply listing regulations.

Atul 10

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 11/84

PRIVATE PLACEMENT.

Other than fund raising , the objectiveis to accommodate strategicinvestors.

Objectives:

(a) Consolidate Promoters‟ stake;

(b) induct a strategic investor/s;

©Provide stake to Working Directors, keymanagement executives;

(d) ESOP plan;

(e) Reward shareholders with bonus issue.

Atul 11

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 12/84

PRIVATE PLACEMENTS1. Can be used for either private (not publicly

traded) stock offerings or other ownershipshares of a business

2. For a formal private placement, the investormust be an accredited investor

3. Private placement memorandum – similar toa prospectus, details the risks of an offering,business officers, actual and pro formafinancial standards, and related material

4. Subscription agreement – a contractbetween the business and the investorsrequiring the investor to provide the agreedupon capital

Atul 12

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 13/84

PRIVATE PLACEMENTS

5. Private Placement Defineda. A private placement is an agreement for equity

investment in a business made directlybetween the business and the investor

b. Offered to a limited number of investorsc. Illiquid – ownership interests can not be

publicly sold or purchased – generally, theprivate placement agreement specifies who theinvestor will be, and the ownership interest is

not transferabled. No regulation – because private placements are

a direct contract between a business and aninvestor, they are not regulated

Atul 13

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 14/84

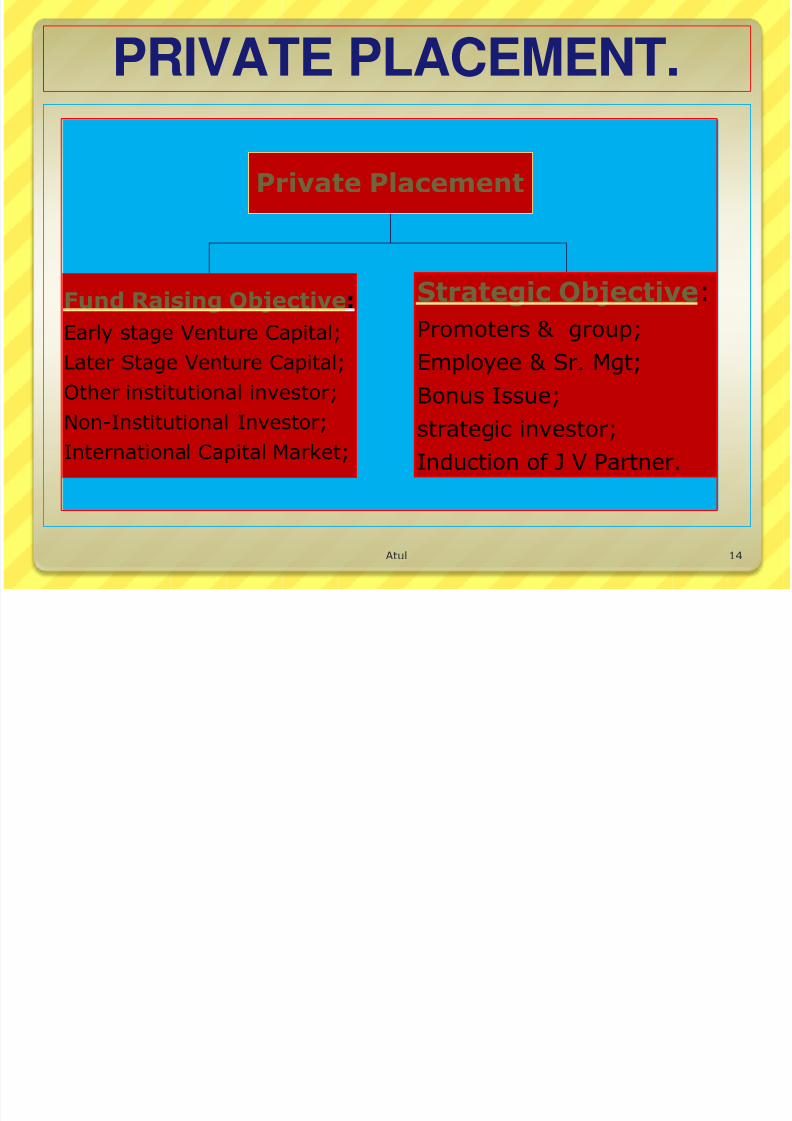

PRIVATE PLACEMENT.

Private Placement

Fund Raising Objective:

Early stage Venture Capital;

Later Stage Venture Capital;

Other institutional investor;

Non-Institutional Investor;

International Capital Market;

Strategic Objective:

Promoters & group;

Employee & Sr. Mgt;

Bonus Issue;

strategic investor;

Induction of J V Partner.

Atul 14

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 15/84

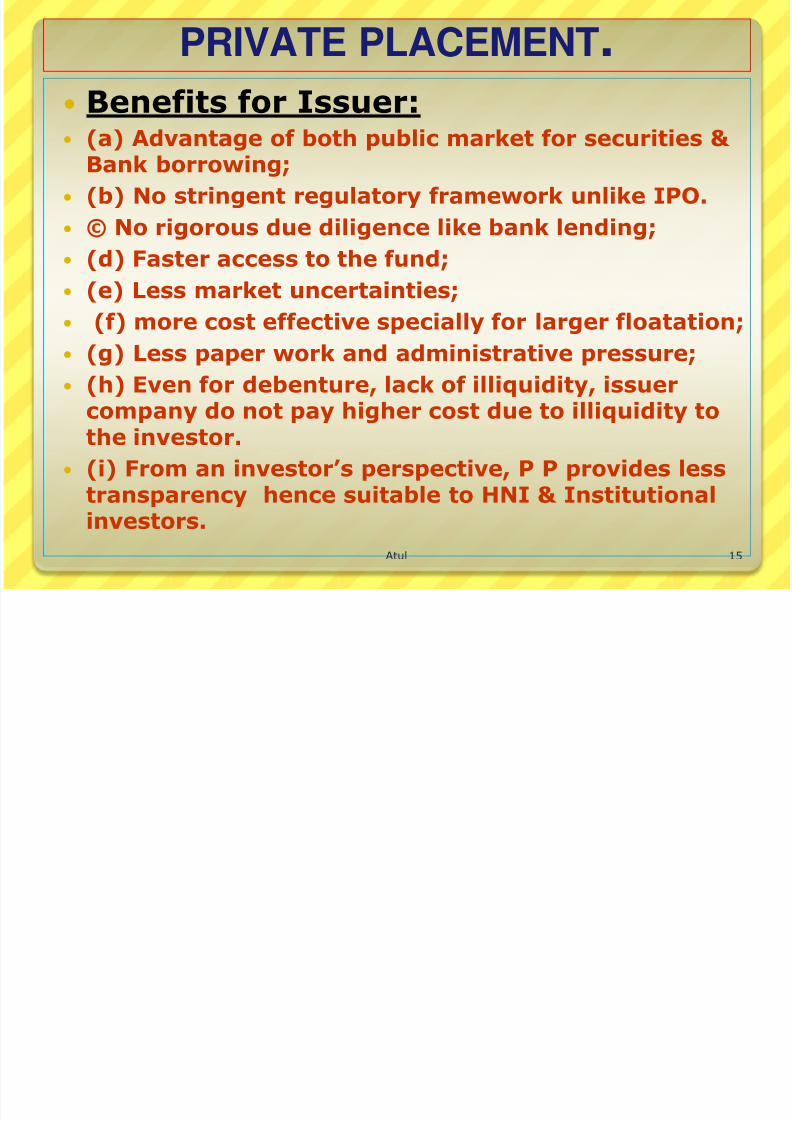

PRIVATE PLACEMENT. Benefits for Issuer: (a) Advantage of both public market for securities &

Bank borrowing;

(b) No stringent regulatory framework unlike IPO.

© No rigorous due diligence like bank lending;

(d) Faster access to the fund;

(e) Less market uncertainties;

(f) more cost effective specially for larger floatation;

(g) Less paper work and administrative pressure;

(h) Even for debenture, lack of illiquidity, issuer

company do not pay higher cost due to illiquidity tothe investor.

(i) From an investor‟s perspective, P P provides lesstransparency hence suitable to HNI & Institutionalinvestors.

Atul 15

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 16/84

PRIVATE PLACEMENT.

PrivatePlacement of

Debt Securities.

PSU

Bonds

Bonds fromBanks &

Institutions

Corporatedebt

Securities

Atul 16

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 17/84

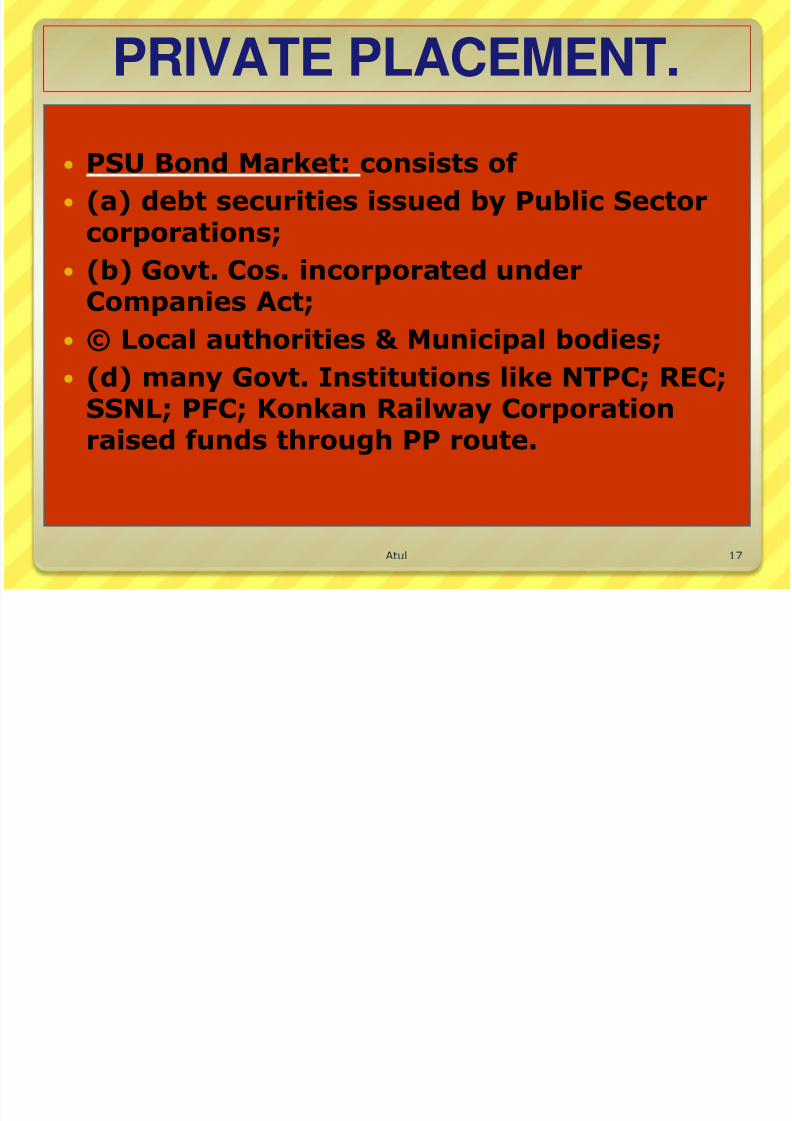

PRIVATE PLACEMENT.

PSU Bond Market: consists of

(a) debt securities issued by Public Sectorcorporations;

(b) Govt. Cos. incorporated underCompanies Act;

© Local authorities & Municipal bodies;

(d) many Govt. Institutions like NTPC; REC;

SSNL; PFC; Konkan Railway Corporationraised funds through PP route.

Atul 17

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 18/84

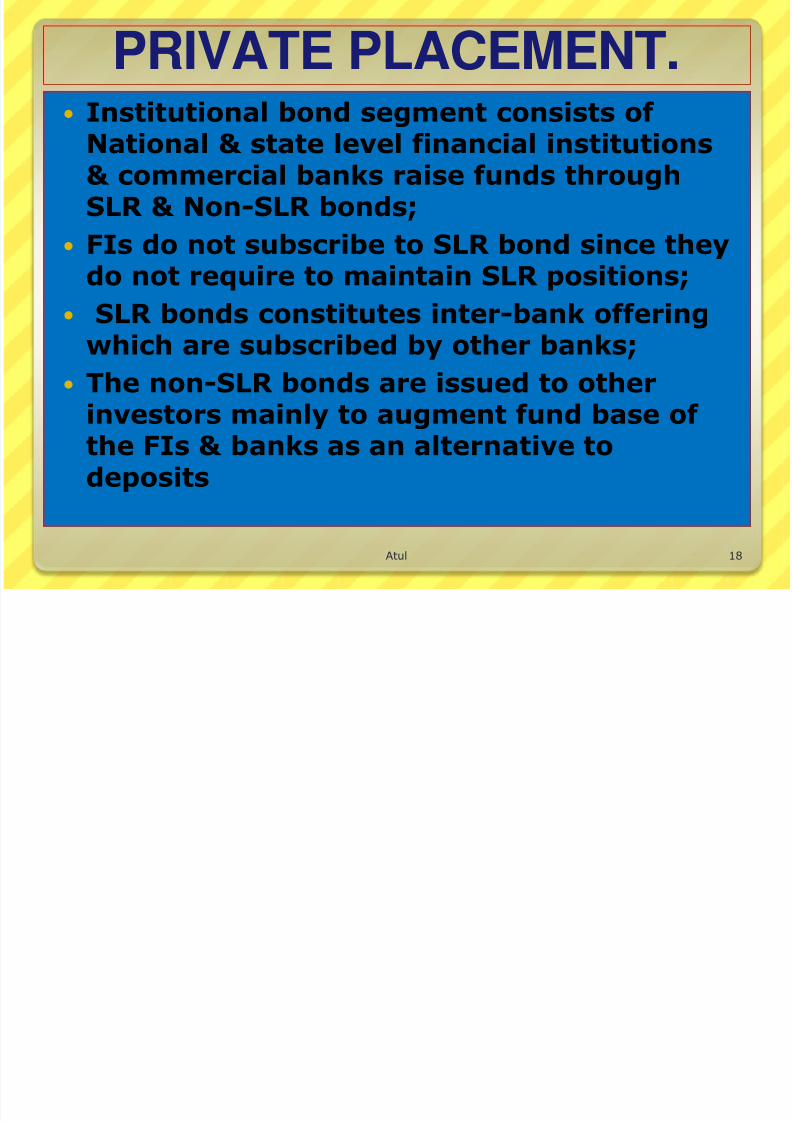

PRIVATE PLACEMENT. Institutional bond segment consists of

National & state level financial institutions& commercial banks raise funds throughSLR & Non-SLR bonds;

FIs do not subscribe to SLR bond since they

do not require to maintain SLR positions; SLR bonds constitutes inter-bank offering

which are subscribed by other banks;

The non-SLR bonds are issued to other

investors mainly to augment fund base of the FIs & banks as an alternative todeposits

Atul 18

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 19/84

PRIVATE PLACEMENT. Corporate Debt market consists of private

sector companies that issue debenture to

F I; banks & other investors to raise fundsas substitute to long-term borrowingthrough Term Loans;

. Its easier to issue Debenture as they arerated instruments. Where as long term loanpass through long drawn appraisal by allsyndicate lenders. Higher the grading of

debentures, the securities paper can lowerthe cost of borrowing.

Atul 19

M k S f P i l Pl d

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 20/84

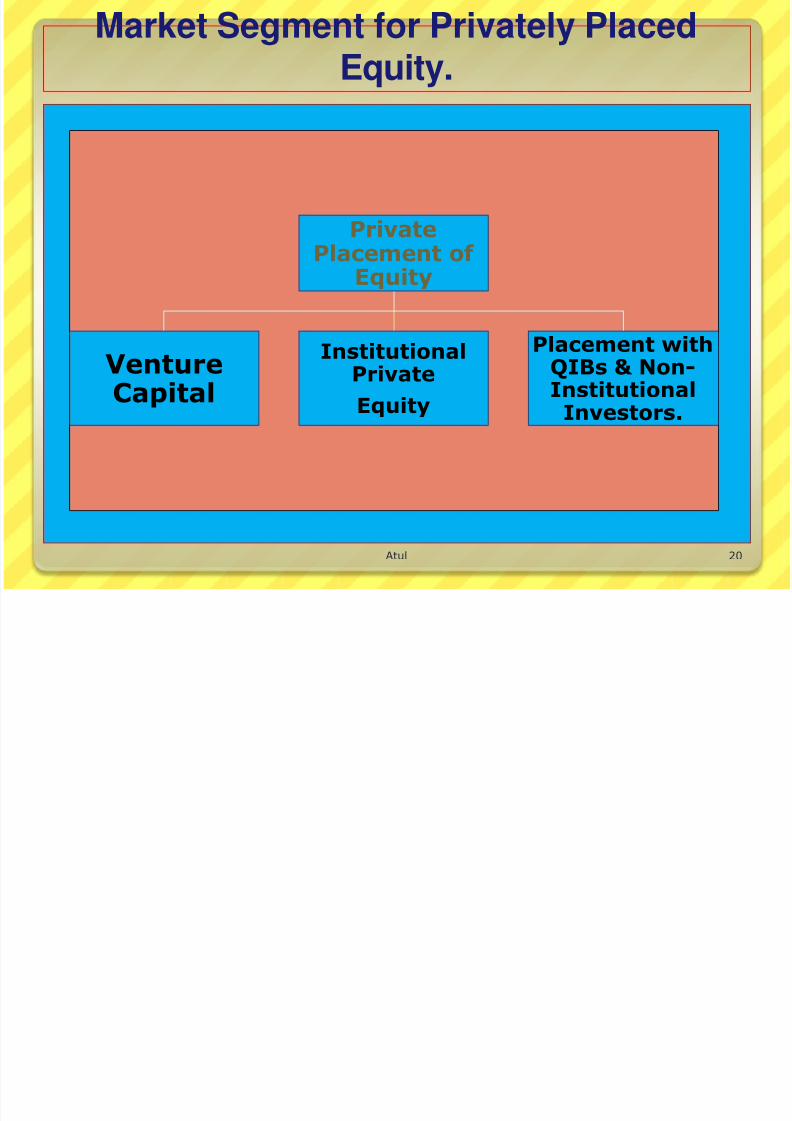

Market Segment for Privately PlacedEquity.

PrivatePlacement of

Equity

VentureCapital

InstitutionalPrivate

Equity

Placement withQIBs & Non-Institutional

Investors.

Atul 20

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 21/84

PRIVATE PLACEMENT. Main investors in pvt. market are QIBs such

as banks; insurance companies; MutualFunds; registered venture capital funds;FIIs & others.

Unregistered foreign pvt. equity investors

unregistered Venture Capital fund/PE fundalso form significant part but they do notqualify in QIB category.

In Debt market, investors are mutual funds;

banks & insurance companies; PF & Pensionfunds;

Though HNI investors also invest still its onvery low percentile.

Atul 21

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 22/84

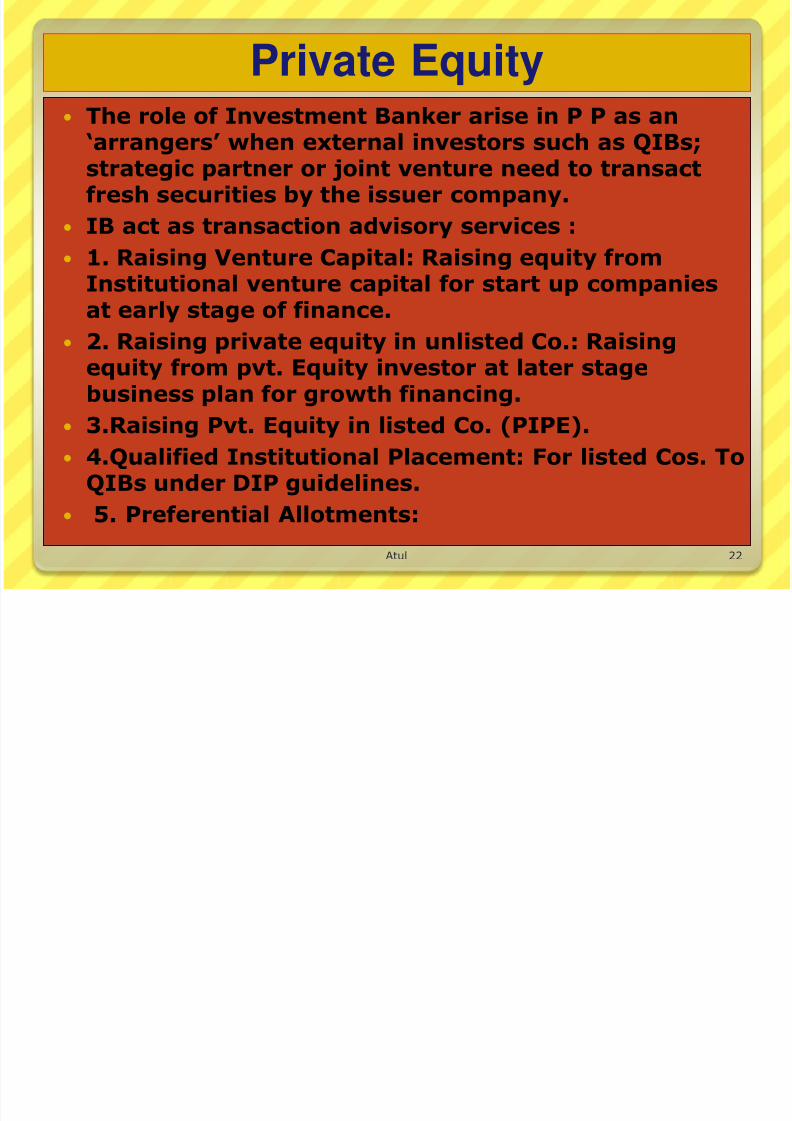

Private Equity The role of Investment Banker arise in P P as an

„arrangers‟ when external investors such as QIBs;strategic partner or joint venture need to transactfresh securities by the issuer company.

IB act as transaction advisory services :

1. Raising Venture Capital: Raising equity from

Institutional venture capital for start up companiesat early stage of finance.

2. Raising private equity in unlisted Co.: Raisingequity from pvt. Equity investor at later stagebusiness plan for growth financing.

3.Raising Pvt. Equity in listed Co. (PIPE).

4.Qualified Institutional Placement: For listed Cos. ToQIBs under DIP guidelines.

5. Preferential Allotments:

Atul 22

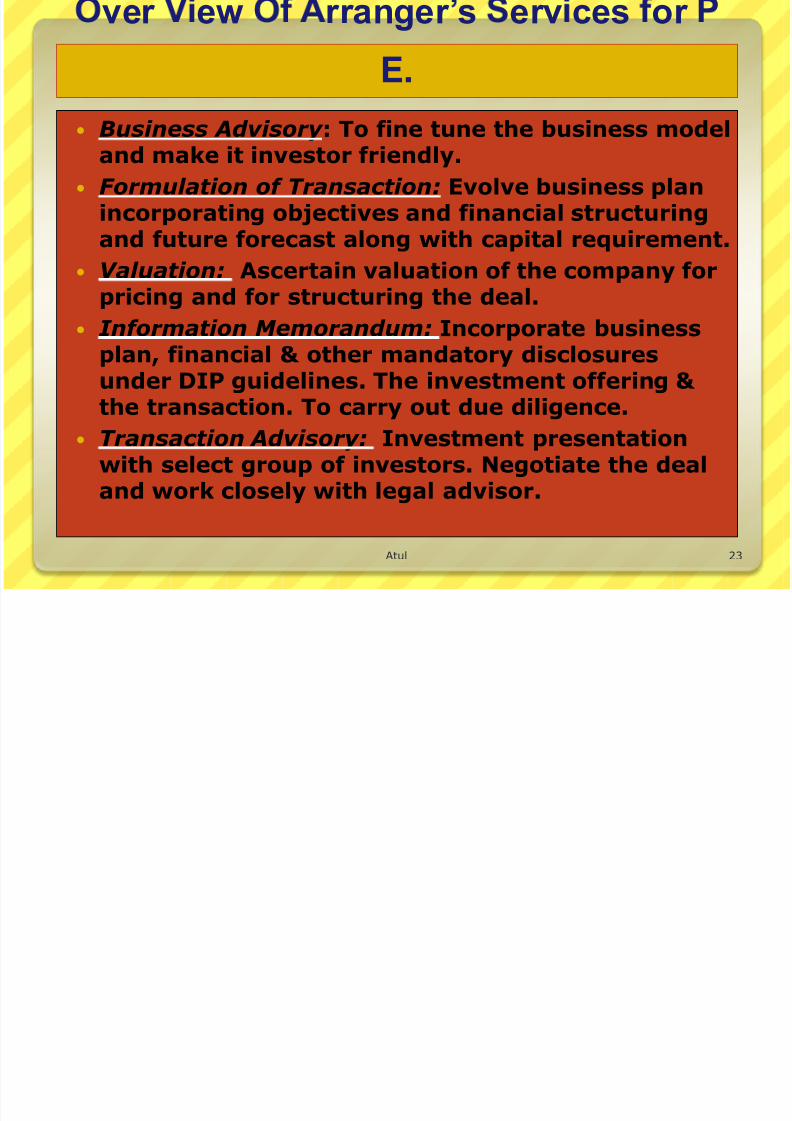

ver ew rranger s erv ces or

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 23/84

ver ew rranger s erv ces or

E. Business Advisory : To fine tune the business model

and make it investor friendly.

Formulation of Transaction: Evolve business planincorporating objectives and financial structuringand future forecast along with capital requirement.

Valuation: Ascertain valuation of the company forpricing and for structuring the deal.

Information Memorandum: Incorporate businessplan, financial & other mandatory disclosuresunder DIP guidelines. The investment offering &

the transaction. To carry out due diligence. Transaction Advisory: Investment presentation

with select group of investors. Negotiate the dealand work closely with legal advisor.

23Atul

8/2/2019 Venture Capital in India-Ppt

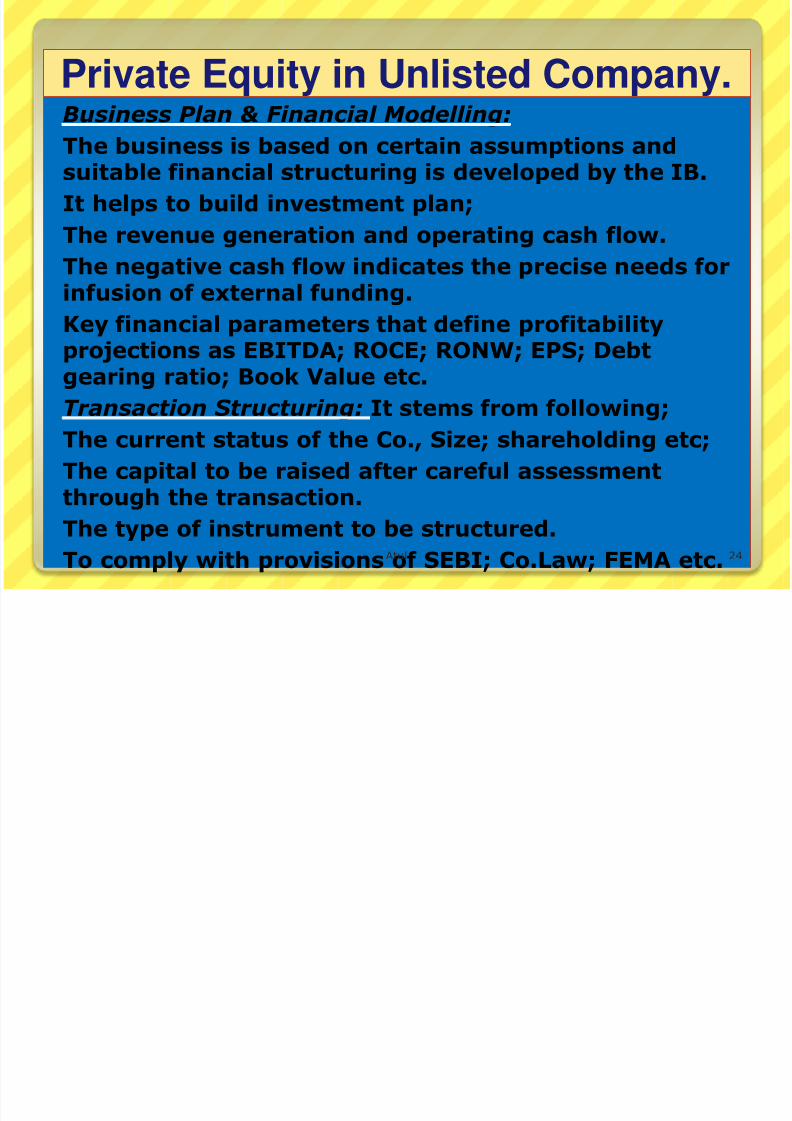

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 24/84

Private Equity in Unlisted Company.Business Plan & Financial Modelling:

The business is based on certain assumptions andsuitable financial structuring is developed by the IB.

It helps to build investment plan;

The revenue generation and operating cash flow.

The negative cash flow indicates the precise needs forinfusion of external funding.

Key financial parameters that define profitabilityprojections as EBITDA; ROCE; RONW; EPS; Debtgearing ratio; Book Value etc.

Transaction Structuring: It stems from following;The current status of the Co., Size; shareholding etc;

The capital to be raised after careful assessmentthrough the transaction.

The type of instrument to be structured.

To comply with provisions of SEBI; Co.Law; FEMA etc.Atul 24

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 25/84

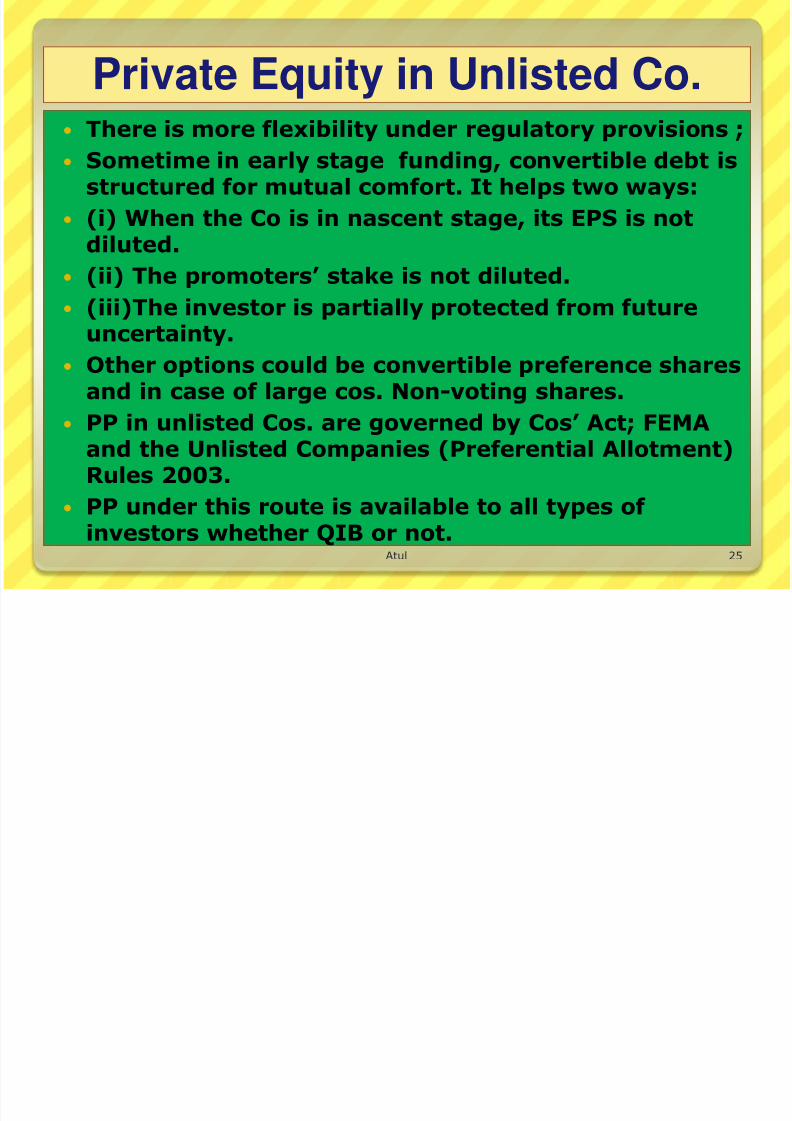

Private Equity in Unlisted Co. There is more flexibility under regulatory provisions ;

Sometime in early stage funding, convertible debt isstructured for mutual comfort. It helps two ways:

(i) When the Co is in nascent stage, its EPS is notdiluted.

(ii) The promoters‟ stake is not diluted. (iii)The investor is partially protected from future

uncertainty.

Other options could be convertible preference sharesand in case of large cos. Non-voting shares.

PP in unlisted Cos. are governed by Cos‟ Act; FEMAand the Unlisted Companies (Preferential Allotment)Rules 2003.

PP under this route is available to all types of investors whether QIB or not.

Atul 25

r vate nvestment n u c

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 26/84

r vate nvestment n u cEquity(PIPE).

According to Bloomberg: „It occurs when privateinvestors take sizeable stake in listed Co. Usuallywhen the equity valuation have fallen & the Co. islooking for new sources of capital‟.

Private Investment in Public Equity: Characteristics:

Private: PIPE is P P transaction between limited

group of investors & listed company subject to SEBI guidelines. Unlike FPO / Right issue, PIPE is allotted to limited distribution of securities through privately negotiated transaction.

Investment: PIPE is direct investment in Co.

Securities are issued by the Co. like in the primary market & investment proceeds go the Co.

Public: PIPE is used by a listed Co to raise capital.There are several restrictions in PIPE financing. It’s adistinct financing alternative unlike PP & IPO/FPO.

Atul 26

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 27/84

Private Equity (PIPE) EQUITY : PIPE is an equity or convertible

securities/debenture later exchanged into equity.

Why PIPE preferred against FPO/Right issue ?

Cost effective; Time saving; Less regulations;

Pricing advantage;(In bleak market price may belower than intrinsic value or BV of Co.FPO mayundersell in bleak market);

PP is mostly to Institutional investors who areinformed and long term investors and willing to payhigher valuations from future perspective.

For investors too in weak market, when shares areundervalued, investors can negotiate deal atattractive price for well performing Co.

Since it‟s a listed Co, ready exit route is available toPIPE investor besides Of market transaction.

Private Equity funds are found biggest market

players in PIPE market. Atul 27

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 28/84

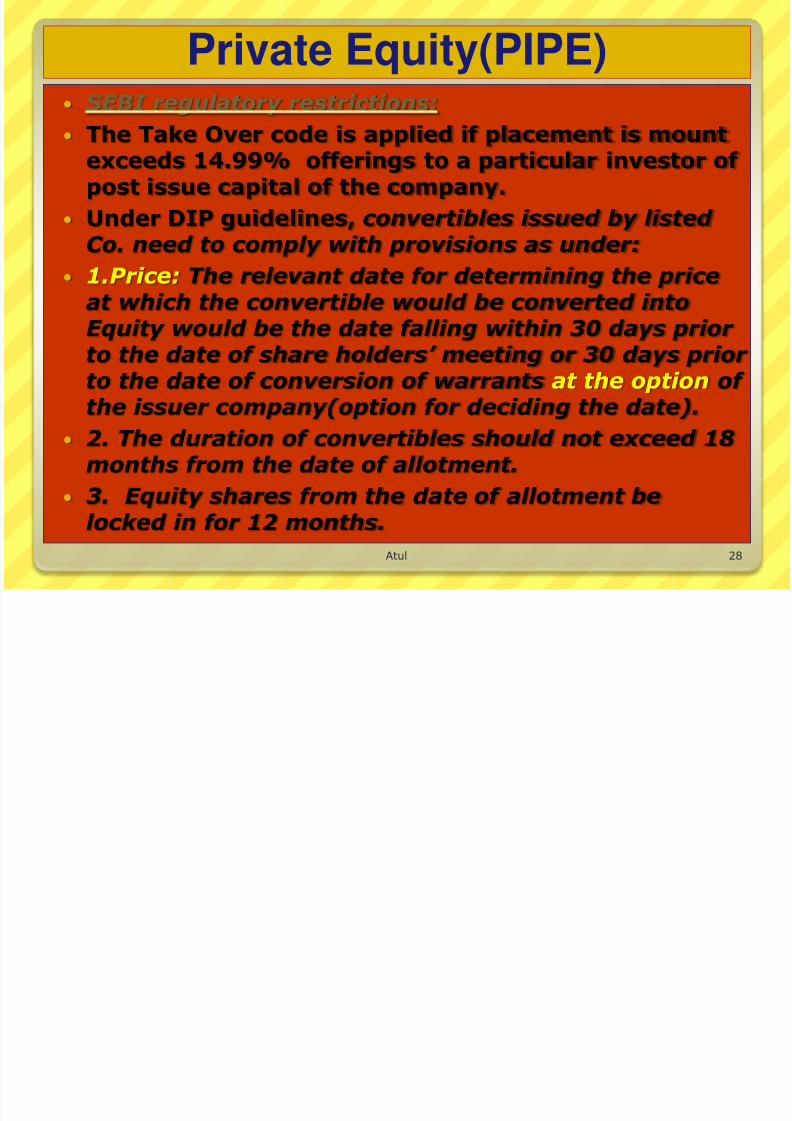

Private Equity(PIPE) SEBI regulatory restrictions:

The Take Over code is applied if placement is mountexceeds 14.99% offerings to a particular investor of post issue capital of the company.

Under DIP guidelines, convertibles issued by listed Co. need to comply with provisions as under:

1.Price: The relevant date for determining the priceat which the convertible would be converted intoEquity would be the date falling within 30 days prior to the date of share holders’ meeting or 30 days prior to the date of conversion of warrants at the option of

the issuer company(option for deciding the date). 2. The duration of convertibles should not exceed 18

months from the date of allotment.

3. Equity shares from the date of allotment belocked in for 12 months.

Atul 28

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 29/84

Private Equity (PIPE) Shareholders Approval:

The currency of the shareholders‟ approval passedunder sec.81(1A) shall be for period of 15 days fromthe date of EGM. The Co has short time for makingallotment to investors. Therefore PIPE transactionsis approved by the shareholders only after investorshave signed term sheets or entered into definitiveagreement with the company for the proposedtransaction.

Proposed amendments under new guidelines by MCArule dated 24-05/2011/

Pricing: Where warrants are issued on preferential basis where option to apply and get the sharesallotted, the issuing co. shall determine before hand the price of the resultant shares. (Cntd )……….

Atul 29

P E –PIPE- Proposed ammendments MCA

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 30/84

P E –PIPE- Proposed ammendments MCA(2011)

Other Conditions:

(i) There should not be gap of more than 30 daysbetween opening and closing of issue of P P.

(ii) For an issue of debentures or convertibledebentures or any other instruments convetible inequity shares at a later date under P P which may

result into cumulative amount of Rs.5crores or more,a company has to seek prior approval of Cent. Govt.in prescribed e-form. However no approval isrequired from the Govt. for issue of Equity Sharesunder P P.

(iii) after every issue of security under PP the coCo.Shall file with ROC return withim 30 days foallotment in the prescribed e-form duly varified by

practising professional.

All the securities issued under preferential / PP shall be keptin dematerialized form.

Atul 30

-

ua e nst tut ona

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 31/84

- ua e nst tut onaPlacement.(QIP)

QIP is similar to P P transaction except that it ismade only to QIBs. Since QIP is only to theinstitutional investors, it has more relaxation thanPIPE transaction.

Important Provisions:

(i)The issue should be only for pure equity or

convertibles except issue of warrants. (ii) The placement should strictly be to QIBs . None

of the allottees should have any direct or indirect association with the promoter group.

(iii) The Co. must be listed on national S E -BSE/NSE;

(iv)The Co. should be compliant of minimum non promoter shareholding norm under the listingagreement.

(v) There should be reservation of 10% of offer toMF. The unsubscribed portion can be allotted to QIB.

Atul 31

-

ua e nst tut ona

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 32/84

- ua e nst tut onaPlacement.(QIP)

(vi) The reference date of pricing of convertible inQIP is same as PIPE.

(vii) Convertible issued under QIP should havemaximum currency of 60 months from the date of allotment.

(viii) The currency of specia resolution passed under

sec 81(1A) shall be for a period of12 months fromthe date of EGM.

(ix) The total amount raised under QIP shall not exceed five times of the NW of the Co. prior to

palcement.

(x) The shares allotte4d under QIP can be sold in secondary market without any lock-in period but not I off market deals up to a period of one year.

(Xi) The appointment of Merchant Banker for the QIP is mandatory who shall conduct due diligence &

follow QIP guidelines, listing of shares with SE etc.Atul 32

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 33/84

P E-Qualified Institutional Placement.(QIP)

Comparative Analysis of QIP v/s PIPE.

Q I P. P I P E.

Currency of 12 months. 15 days.

Shareholders‟ 60months for convertibles. 18 months.

Resolution:

Lock in Period: No lock in for 12 months.

from date of market sale. 12 monthsallotment for off market deal.

Restriction on min. Min.2 up to Rs.250cr. & No restriction.

nos. of allottee. Min.5 above Rs.250 cr.

No single allottee >50%

Need for Merchant Appointment is must. Not necessary.

Banker.

Dislocure: Level is higher. 30days Disclosure is

after allotment to submit relatively lower.

document to SEBI & get the

approval of SE for listing. Atul

33

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 34/84

Meaning Venture capital means funds made available

for startup firms and small businesses withexceptional growth potential.

Venture capital is money provided byprofessionals who alongside managementinvest in young, rapidly growing companiesthat have the potential to develop into

significant economic contributors.

Atul 34

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 35/84

C. VENTURE CAPITAL1. Generally regarded as “seed money,” used to

help start or expand a new business

2. A business can receive venture capital as astart up, when expanding before profitability,or after the business becomes profitable (but

before a buy-out or an initial public offering)

3. The required rate of return or portion of equity required to receive venture capitalfunding is relatively high, the venture

capitalist often provides advice and may takecontrol of a corporation to protect itsinvestment

Atul 35

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 36/84

VENTURE CAPITAL

4. Forms of Venture Capital investmentsa. Debt – loan contract between the business and

the venture capital firm, generally with abovemarket interest rates

b. Equity – where the venture capital firmpurchases an ownership share of the business,generally in the form of private placementstock

c. Preferred Stock – the favored type of venture

capital investment, provides interest yieldsand seniority to capital in the event that thefirm fails, but with an equity interest if the firmsucceeds

Atul 36

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 37/84

Venture Capitalists generally:

Finance new and rapidly growingcompanies

Purchase equity securities

Assist in the development of newproducts or services

Add value to the company through activeparticipation.

Atul 37

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 38/84

C. VENTURE CAPITAL

5.Sources of Venture Capital Fundinga. Partnerships – business owned by individuals

specifically to provide venture capital for otherbusinesses

b. Limited Liability Corporations – a cross

between a partnership and a corporation, doesnot have the restrictions on makinginvestments that publicly traded corporationsmust adhere to

c. Investment Management Firms – pools of money from accredited investors, with aninvestment manager making decisionsconcerning which venture capital projects tofund

Atul 38

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 39/84

The SEBI has defined Venture CapitalFund in its Regulation 1996 as ‘a fund

established in the form of a companyor trust which raises money throughloans, donations, issue of securities orunits as the case may be and makes orproposes to make investments inaccordance with the regulations’.

Atul 39

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 40/84

Characteristics Long time horizon

Lack of liquidity

High risk

Equity participation

Participation in management

Atul 40

Structure of Venture Capital backed by Start-up

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 41/84

Structure of Venture Capital backed by Start upBusiness.

Business Structure:

1. Generally associated with technology venture orknowledge intensive or innovation driven business.

2. Venture is backed by technology or to be created.

3.Requires product development & market validation.

4. Product should be successful at lab scale beforelaunched commercially.

5.Tst marketing or phased marketing is requiredsince concept selling is involved.

6.Business should be scaled up in phases.

7. Business risk is divided in phases. Investment ismonitored by the V C as mentor. V C appointsnominee on the board of the company.

Atul 41

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 42/84

Venture Capital- Financial Structure.

1. Financing starts from Seed stage to pre-IPO stage.

2.Financial risk is divided in phases. The risk rewardrelationship go down progressively.

3. Promoters may not have adequate capital. Thetechnology is allowed to be capitalised as stock.Promoters equity is more in the form of intellectual

capital and stock option than in hard cash. 4.More suitable financing trough equity. Or some

part could be by convertible instrument.

5.Tnagible asset creation is less. There is highcomponent of intellectual property creation. VC do

finance soft cost without creation of tangible asset. 6.Involves significant cash burns in product

development, research & product validation.

7.The business model should have potential for veryhigh return to investors.

Atul 42

What aVenture Capitalist look for investment

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 43/84

What aVenture Capitalist look for investmentopportunity.

1. An industry that is currently sunrise sector.

2. A concept that significantly improves the existingprocesses or has vast replacement market.

3. A business or idea that has potential for spin off business with good revenue projection.

4.A start up business with potential to become an

attractive proposition for strategic acqusition infuture.

5. A business that is in cutting edge technology andmanagement bandwidth to reach and sustainleadership position in future.

6. A business or technology that has a first moveradvantage before competitor catches up.

7. A business that has significant entry barriers.

8. A firm that offers possibilities multiple of exitoptions.

Atul 43

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 44/84

Advantages It injects long term equity finance which provides

a solid capital base for future growth.

The venture capitalist is a business partner,

sharing both the risks and rewards. Venturecapitalists are rewarded by business success andthe capital gain.

The venture capitalist is able to provide practicaladvice and assistance to the company based onpast experience with other companies which werein similar situations.

Atul 44

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 45/84

Advantages (Cont.) The venture capitalist also has a network of contacts

in many areas that can add value to the company.

The venture capitalist may be capable of providing

additional rounds of funding should it be required tofinance growth.

Venture capitalists are experienced in the process of preparing a company for an initial public offering

(IPO) of its shares onto the stock exchanges oroverseas stock exchange such as NASDAQ.They can also facilitate a trade sale.

Atul 45

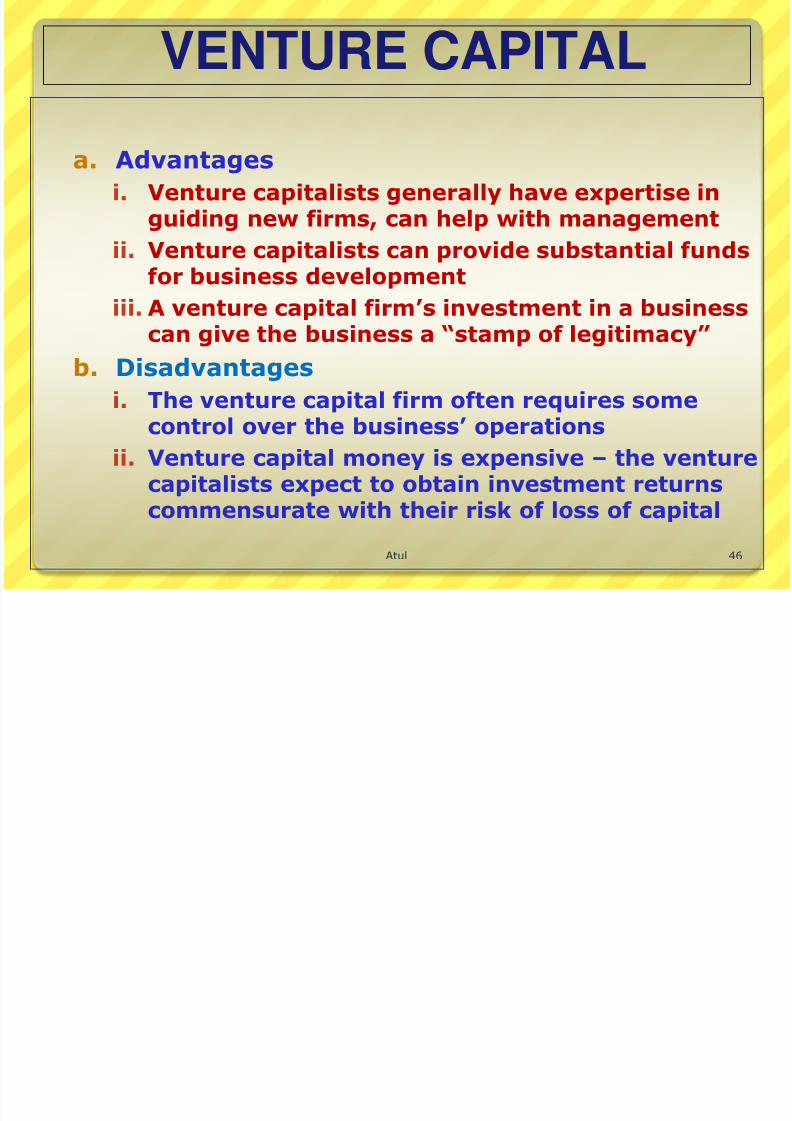

VENTURE CAPITAL

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 46/84

VENTURE CAPITAL

a. Advantages

i. Venture capitalists generally have expertise inguiding new firms, can help with management

ii. Venture capitalists can provide substantial funds

for business developmentiii. A venture capital firm‟s investment in a business

can give the business a “stamp of legitimacy”

b. Disadvantages

i. The venture capital firm often requires some

control over the business‟ operations

ii. Venture capital money is expensive – the venturecapitalists expect to obtain investment returnscommensurate with their risk of loss of capital

Atul 46

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 47/84

Stages of financing1. Seed Money:

Low level financing needed to prove a newidea.

2. Start-up:

Early stage firms that need funding for

expenses associated with marketing andproduct development.

3. First-Round:

Early sales and manufacturing funds.

4. Second-Round:

Working capital for early stage companiesthat are selling product, but not yet turninga profit .

Atul 47

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 48/84

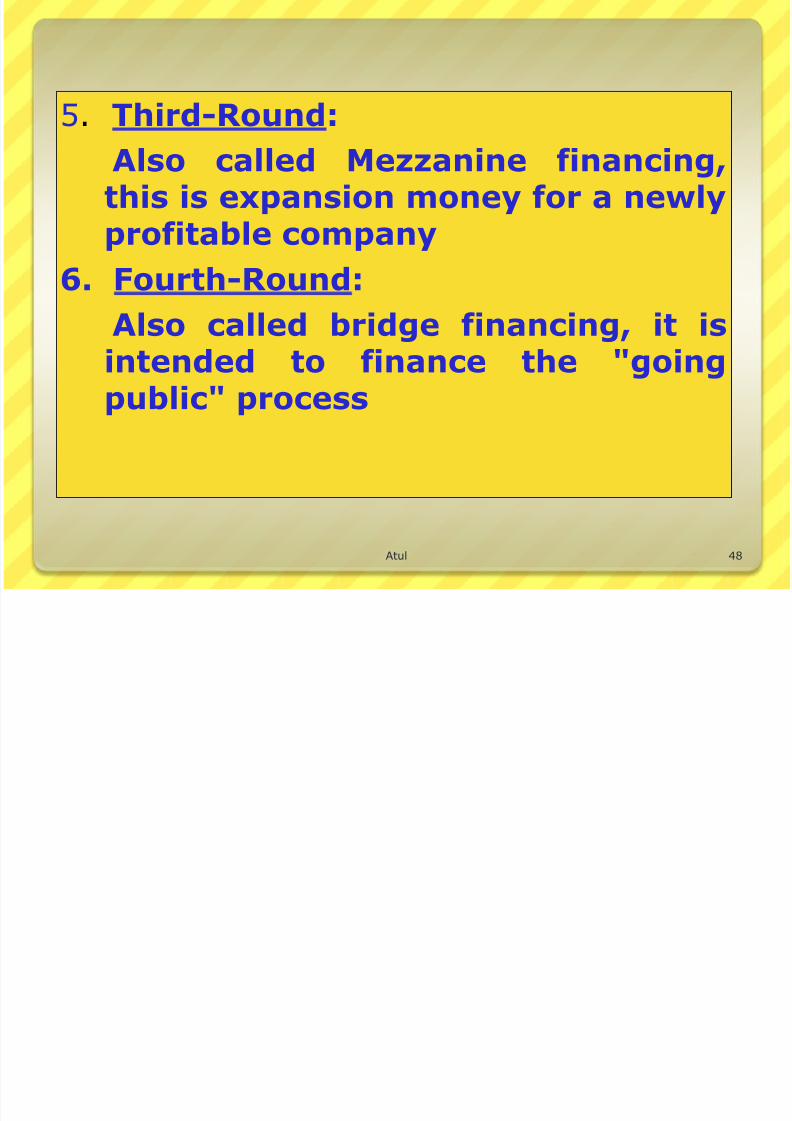

5. Third-Round:

Also called Mezzanine financing,this is expansion money for a newlyprofitable company

6. Fourth-Round:Also called bridge financing, it isintended to finance the "goingpublic" process

Atul 48

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 49/84

Risk in each stageFinancial

StagePeriod (Funds

locked inyears)

RiskPerception

Activity to befinanced

Seed Money 7-10 ExtremeFor supportinga concept or

idea or R&D forproduct

development.

Start Up 5-9 Very HighInitializing

operations ordeveloping

prototypes.

First Stage 3-7 HighStart

commercialsproduction and

marketing.

Atul 49

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 50/84

FinancialStage

Period (Fundslocked in

years)

RiskPerception

Activity to befinanced

Second Stage 3-5 Sufficiently highExpand marketand growing

working capitalneed

Third Stage 1-3 Medium

Marketexpansion,

acquisition & product

developmentfor profit

makingcompany

Fourth Stage 1-3 Low Facilitatingpublic issue

Atul 50

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 51/84

Atul 51

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 52/84

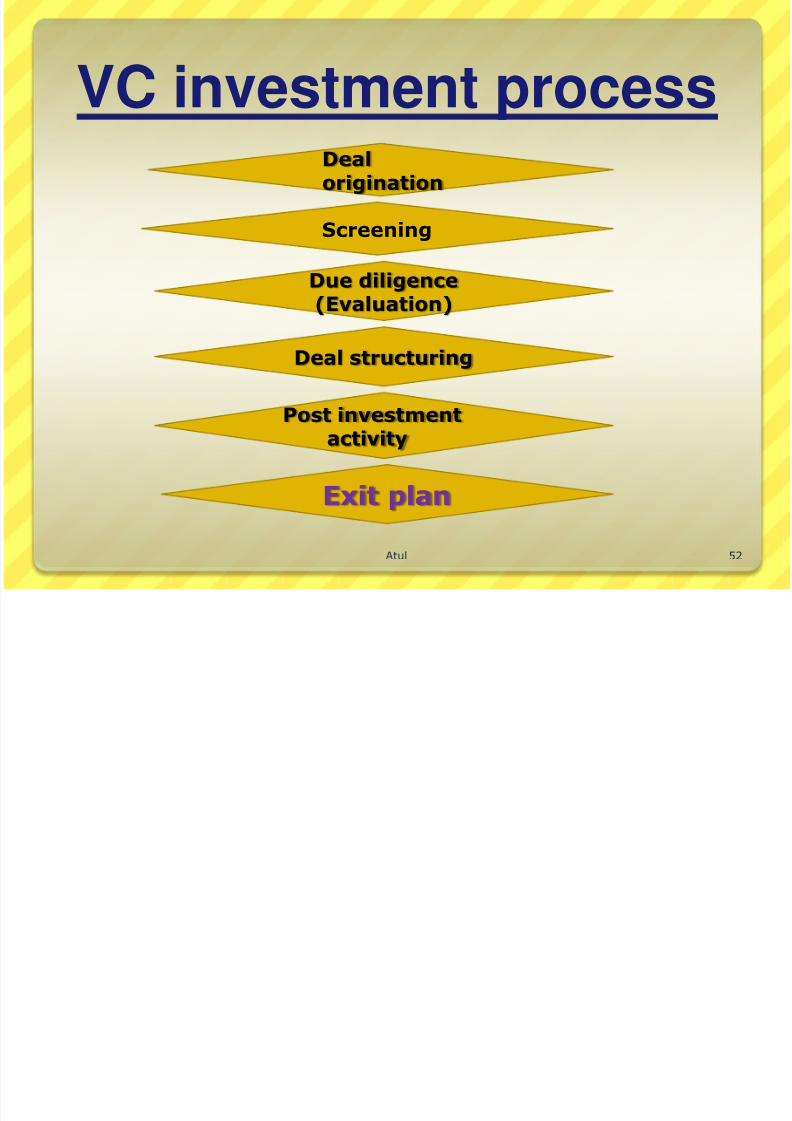

VC investment processDealorigination

Screening

Due diligence(Evaluation)

Deal structuring

Post investmentactivity

Exit plan

Atul 52

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 53/84

Atul 53

Methods of Venture

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 54/84

Methods of VentureFinancing

The financing pattern of the deal is themost important element. Following are thevarious methods of venture financing:

Equity Conditional loan Income note Participating debentures

Quasi equity

Atul 54

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 55/84

Exit route

Initial public offer(IPOs) Trade sale Promoter buy back Acquisition by another company

Atul 55

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 56/84

DEVELPOMENT OF

VENTURE CAPITALIN INDIA

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 57/84

The concept of venture capital was formallyintroduced in India in 1987 by IDBI.

The government levied a 5 per cent cess on all

know-how import payments to create the venturefund.

ICICI started VC activity in the same year

Later on ICICI floated a separate VCcompany - TDICI

Atul 57

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 58/84

India

VCFs in India can be categorized intofollowing five groups:

1) Those promoted by the Central

Government controlled developmentfinance institutions. For example:- ICICI Venture Funds Ltd.- IFCI Venture Capital Funds Ltd (IVCF)

- SIDBI Venture Capital Ltd (SVCL)

Atul 58

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 59/84

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 60/84

4)Those promoted by private sectorcompanies.For example:

- IL&FS Trust Company Ltd- Infinity Venture India Fund

5)Those established as an overseas venture capitalfund.For example:

- Walden International Investment Group- HSBC Private Equity

management Mauritius Ltd

Atul 60

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 61/84

Rules & regulations of VCin India

AS PER SEBI

AS PER INCOME TAX ACT,1961

Atul 61

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 62/84

Rules by SEBI: VCF are regulated by the SEBI (Venture

Capital Fund) Regulations, 1996. The following are the various provisions:

A venture capital fund may be set up by acompany or a trust, after a certificate of registration is granted by SEBI on anapplication made to it. On receipt of the

certificate of registration, it shall be bindingon the venture capital fund to abide by theprovisions of the SEBI Act, 1992.

Atul 62

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 63/84

Contd… A VCF may raise money from any

investor, Indian, Non-resident Indian orforeign, provided the money accepted

from any investor is not less than Rs 5lakhs. The VCF shall not issue anydocument or advertisement inviting offersfrom the public for subscription of its

security or units

Atul 63

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 64/84

Contd… SEBI regulations permit investment by

venture capital funds in equity or equityrelated instruments of unlisted companies

and also in financially weak and sickindustries whose shares are listed orunlisted

Atul 64

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 65/84

Contd… At least 80% of the funds should be

invested in venture capital companies andno other limits are prescribed.

SEBI Regulations do not provide for anysectoral restrictions for investment exceptinvestment in companies engaged in

financial services.

Atul 65

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 66/84

Contd… A VCF is not permitted to invest in the

equity shares of any company orinstitutions providing financial services.

The securities or units issued by a venturecapital fund shall not be listed on anyrecognized stock exchange till the expiry

of 4 years from the date of issuance .

Atul 66

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 67/84

Contd… A Scheme of VCF set up as a trust shall be

wound up(a) when the period of the scheme if any, is

over

(b) If the trustee are of the opinion that thewinding up shall be in the interest of theinvestors

(c) 75% of the investors in the scheme pass

a resolution for winding up or,(d) If SEBI so directs in the interest of the

investors.

Atul 67

A i i f

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 68/84

As per provision of

income-tax rules: The Income Tax Act provides tax

exemptions to the VCFs under Section10(23FA) subject to compliance with

Income Tax Rules.

Restrict the investment by VCFs only inthe equity of unlisted companies.

VCFs are required to hold investment fora minimum period of 3 years.

Atul 68

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 69/84

Contd… The Income Tax Rule until now provided

that VCF shall invest only upto 40% of thepaid-up capital of VCU and also notbeyond 20% of the corpus of the VCF.

After amendment VCF shall invest onlyupto 25% of the corpus of the venturecapital fund in a single company.

There are sectoral restrictions under theIncome Tax Guidelines which provide thata VCF can make investment only inspecified companies.

Atul 69

n an en ure ap a anP i E i A i i

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 70/84

pPrivate Equity Association

(IVCA) It was established in 1993 and is based in

Delhi, the capital of India It is a member based national organization that

- represents venture capital and privateequity firms

- promotes the industry within India andthroughout the world

- encourages investment in high growthcompanies and

- supports entrepreneurial activity andinnovation.

Atul 70

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 71/84

IVCA members comprise venture capitalfirms, institutional investors, banks,

incubators, angel groups, corporateadvisors, accountants, lawyers,government bodies, academic institutionsand other service providers to the venturecapital and private equity industry.

Members represent most of the activeventure capital and private equity firms inIndia. These firms provide capital for seedventures, early stage companies and laterstage expansion.

Atul 71

How does the Venture Capital

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 72/84

How does the Venture Capitalwork?

Venture capital firms typically source the majorityof their funding from large investmentinstitutions.

Investment institutions expect very high ROI

VC’s invest in companies with high potentialwhere they are able to exit through either an IPOor a merger/acquisition.

Their primary ROI comes from capital gainsalthough they also receive some return throughdividend.

Atul 72

Venture capital industry wise

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 73/84

Venture capital industry wisesegmentation

6.94

7.73

11.5

4.32

27.95

4.82

11.43

12.92

3.36

9.03

Percentage

IT & ITES

Energy

Manufacturing

Media & Ent.

BFSI

Shipping & logistics

Eng. & Const.

Telecom

Health care

Others

Percentage calculated on the total VC investment- 14,234 USB (fig. of 2007)Atul 73

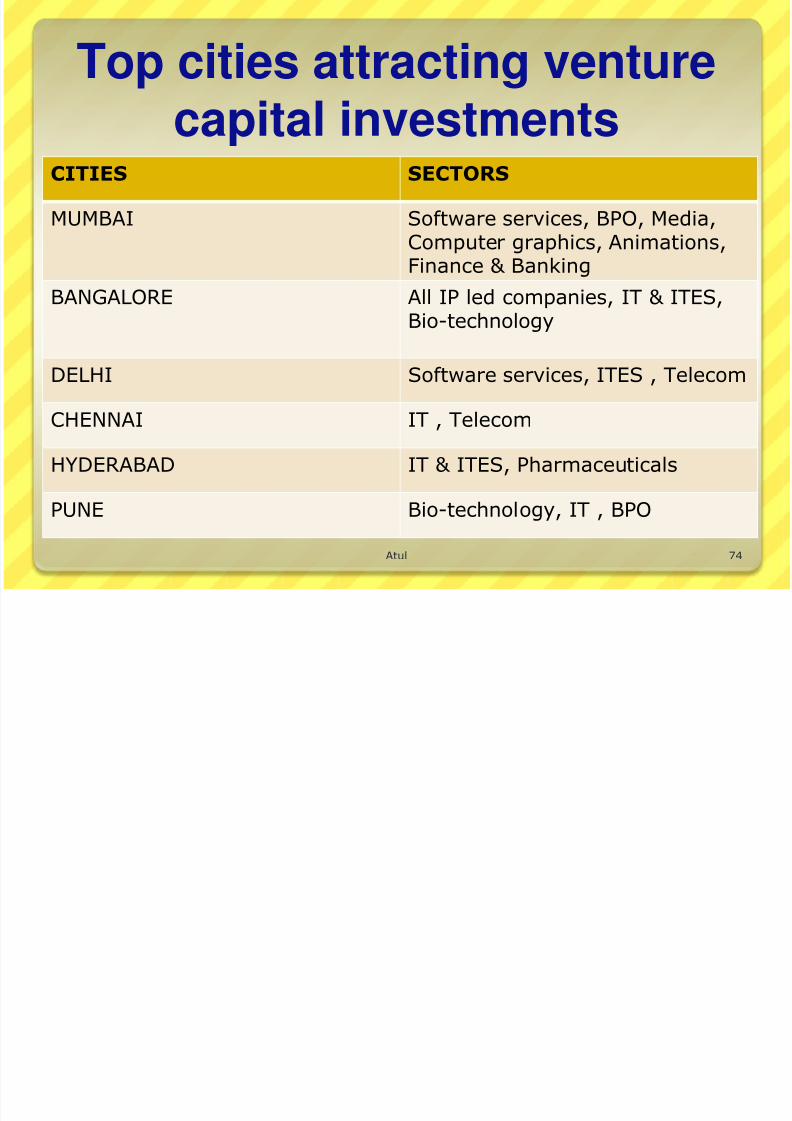

Top cities attracting venture

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 74/84

Top cities attracting venturecapital investments

CITIES SECTORS

MUMBAI Software services, BPO, Media,Computer graphics, Animations,Finance & Banking

BANGALORE All IP led companies, IT & ITES,Bio-technology

DELHI Software services, ITES , Telecom

CHENNAI IT , Telecom

HYDERABAD IT & ITES, Pharmaceuticals

PUNE Bio-technology, IT , BPO

Atul 74

Critical factors for the

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 75/84

Critical factors for thesuccess of venture capital

The regulatory, tax and legal environment should play anenabling role as internationally venture funds have evolvedin an atmosphere of structural flexibility, fiscal neutralityand operational adaptability.

Resource raising, investment, management and exit should

be as simple and flexible as needed and driven by globaltrends.

Venture capital should become an institutionalized industrythat protects investors and investee firms, operating in anenvironment suitable for raising the large amounts of risk

capital needed and for spurring innovation through start-upfirms in a wide range of high growth areas.

Atul 75

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 76/84

In view of increasing global integration and mobility of capital it is important that Indian venture capitalfunds as well as venture finance enterprises are ableto have global exposure and investment opportunities

Infrastructure in the form of incubators and R&D needto be promoted using government support and privatemanagement as has successfully been done bycountries such as the US, Israel and Taiwan. This is

necessary for faster conversion of R&D andtechnological innovation into commercial products.

Atul 76

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 77/84

Growth of VC/PE in India

1160 937591 470

16502200

7500

14234

6390

280

110

78

56

71

146

299

387

170

0

50

100

150

200

250

300

350

400

450

0

2000

4000

6000

8000

10000

12000

14000

16000

2000 2001 2002 2003 2004 2005 2006 2007 1st half of2008

Value of deals No of dealsAtul 77

Impact of recession on the VC

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 78/84

Impact of recession on the VCindustry in India

The down market virtually closed the IPO marketfor emerging companies.

With less opportunities for getting ROI investors

tend to scale back, adjust their investment focusand/or get more picky in funding companies.

The investors that put money into their fundsbecame less aggressive during recession so itwas harder for the VCs to raise money.

Atul 78

VC/PE funds to take 2 years to regaini

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 79/84

vigour

Venture capital (VC) and private equity (PE)

funds are likely to take up to two years to regaintheir 2005-07 level.

With India’s economy bouncing back and thecountry on track to achieve an 9 % GDP growth,

interest in the Indian market is re-emerging. The VC/PE fund inflow into the country in the last

five and half years has been to the tune of over$44.8 billion with investments flowing into around13,000 domestic companies.

The market regulator, SEBI, has to start lookingat a different regulatory framework for this kindof capital, which is essentially risk capital

Atul 79

IMPACT OF UNION Budget

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 80/84

g2010

The increase in weighted deduction of inhouse R&D will boost up investment inhealth care.

46% of the total investment is going toinfrastructure development which is apositive sign for investors.

Atul 80

Future prospects of VC in

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 81/84

p pIndia

VC can help in the rehabilitation of sick units. VC can assist small ancillary units to upgrade

their technologies VCFs can play a significant role in developing

countries in the service sector includingtourism, publishing, health care etc.

They can provide financial assistance topeople coming out of universities, technical

institutes, etc thus promoting entrepreneurialspirits

Atul 81

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 82/84

ICICI VENTURE CAPITALDeal sourcing

Deal evaluation

Investmentdecision

Post-investmentprocess

Exit strategyAtul 82

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 83/84

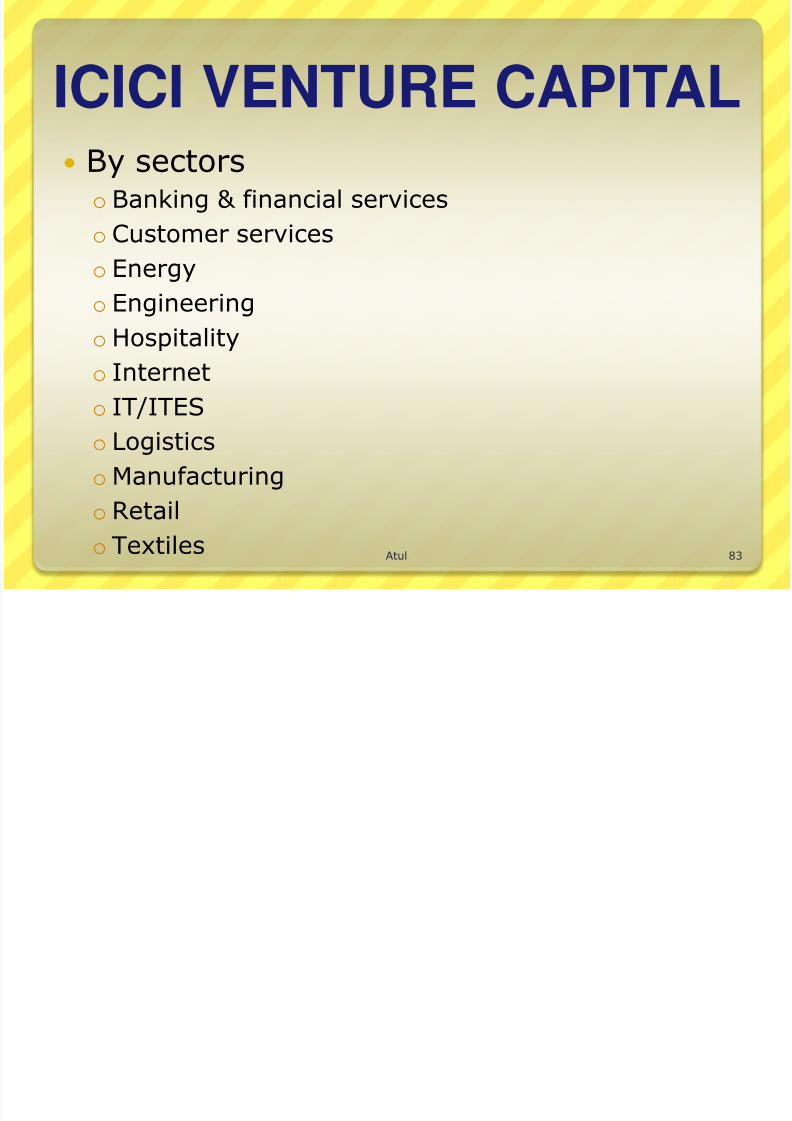

ICICI VENTURE CAPITAL By sectors

o Banking & financial services

o Customer services

o Energy

o Engineering

oHospitality

o Internet

o IT/ITES

o Logistics

oManufacturing

o Retail

o TextilesAtul 83

8/2/2019 Venture Capital in India-Ppt

http://slidepdf.com/reader/full/venture-capital-in-india-ppt 84/84