venture financing and start-up performance in israel · venture capital funds in israel ... public...

TRANSCRIPT

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv

Commercial Wing

Venture Financing and Start-Up

Performance in Israel

Table of Content:

Part 1: Overview of the Israeli Innovation Ecosystem

1. Israel's Innovative Capacity and Technological Robustness

1.1 Spending on R&D

1.2 High Quality University System – S&T

1.3 Hi-Tech "Iron Triangle": Academia, Industry & Gov.

1.4 Technology Transfer Organizations (TTO) in Israel

2. Government Support: Office of the Chief Scientist

3. Venture Capital Funds in Israel

3.1 Israeli VC Fund-Raising Trends

3.2 Foreign VC Fund-Raising Trends

3.3 First Investments Made by VCs in 2013

4. Notable Israeli Exits, Mergers & Acquisitions, 2004-2013

4.1 Major Exits and M&As, 2004-2013

Part 2: Venture Financing in Israel

1. Stages of Venture Financing – Taxonomy

2. Return on Equity (ROE): Total Exits vs. Capital Raised by

Israeli Start-Ups

3. Case Studies: Financing Models for Asian Investments in

Israel

3.1 Japan

3.2 South Korea

3.3 China

4. Indo-Israeli Innovation Partnerships

Part 3: India and Israel – Future Outlook

Annexure: Performance Analytics

Report Prepared by:

Daniel Shkedi

Marketing Officer

June 2015

0 0

Part 1:

Overview of the Israeli

Innovation Ecosystem

Israel: Economic Indicators

Population:

8.345 Million (June 2015)

GDP (PPP), 2014:

$286 Billion

GDP per Capita (Prices), 2015:

$34,600

GDP per Capita (PPP), 2014:

$33,400

GDP Real Growth (2015, Est.):

3.2%

GDP–Sector Breakdown, 2014:

Services: 71.9%

Industry: 25.7%

Agriculture: 2.4%

Export of Goods, 2014:

$66.58 Billion

Import of Goods, 2014:

$71.89 Billion

FDI Stock, 2014:

$97.05 Billion (home)

$83.62 Billion (abroad)

FOREX Reserves (Dec. 2014):

$89.77 Billion

Inflation Rate (04/2015):

-0.5%

Unemployment Rate, Q1/2015:

5.4%

Annual Budget (2014):

NIS 434 Billion

(Approx. $113.5 Billion)

Public Debt-GDP Ratio (2014):

67.4%

Credit Rating (2014):

Moody’s: A1

Standard & Poors: A+

Fitch: A

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 1

Part 1: Overview of the Israeli Innovation Ecosystem

With over 3000 newly founded technology companies, Israel has the highest density of start-ups

in the world. Currently, there are more than 80 Israeli companies listed on the NASDAQ index

in the New York Stock Exchange (NYSE), more than Japan, S. Korea, Singapore, India,

Germany, France and Hong Kong combined. Some of the leading companies include: Taro

Pharmaceuticals, Check Point, Elbit Systems, Teva Pharmaceuticals and NICE systems. More

than 50% are technology companies and the rest are healthcare-oriented, consumer services,

public utilities and consumer durables. The total market capitalization on NASDAQ of all Israeli

companies is more than $85 Billion.

The Israeli innovation ecosystem has been a source of many groundbreaking advances. For

instance, Firewall (Check Point), voicemail (Comverse), USB flash drive (M-Systems), VoIP

(Vocaltec), digital printing (Indigo), are just a few examples of forefront solutions, which Israeli

companies have pioneered or were among the first to commercialize. Israeli start-ups have

continuously driven innovation across all major technology sectors. For example, Amdocs and

Comverse in telecommunication applications, Mercury in IT management, Check Point in

security, DSPG in semiconductors, Mellanox in Infiniband, and Verint and NICE in contact

center applications.

In addition to Israel’s international presence in leading stock exchanges and markets, many

major global tech companies have some subsidiary/research center in Israel, including Intel,

Microsoft, Google, Cisco, Facebook, Applied Materials, Apple, IBM, Oracle, Motorola and

Hewlett-Packard. Consequently, 39% of Israeli high-tech employees work in the R&D

departments of multinational companies. Many innovations from these R&D centers make their

way to households across the globe. For instance, Pentium PC/laptop processors (Intel), Google

Suggest (Google) and most of Hewlett-Packard’s Software infrastructure.

1. Israel’s Innovative Capacity and Technological Robustness

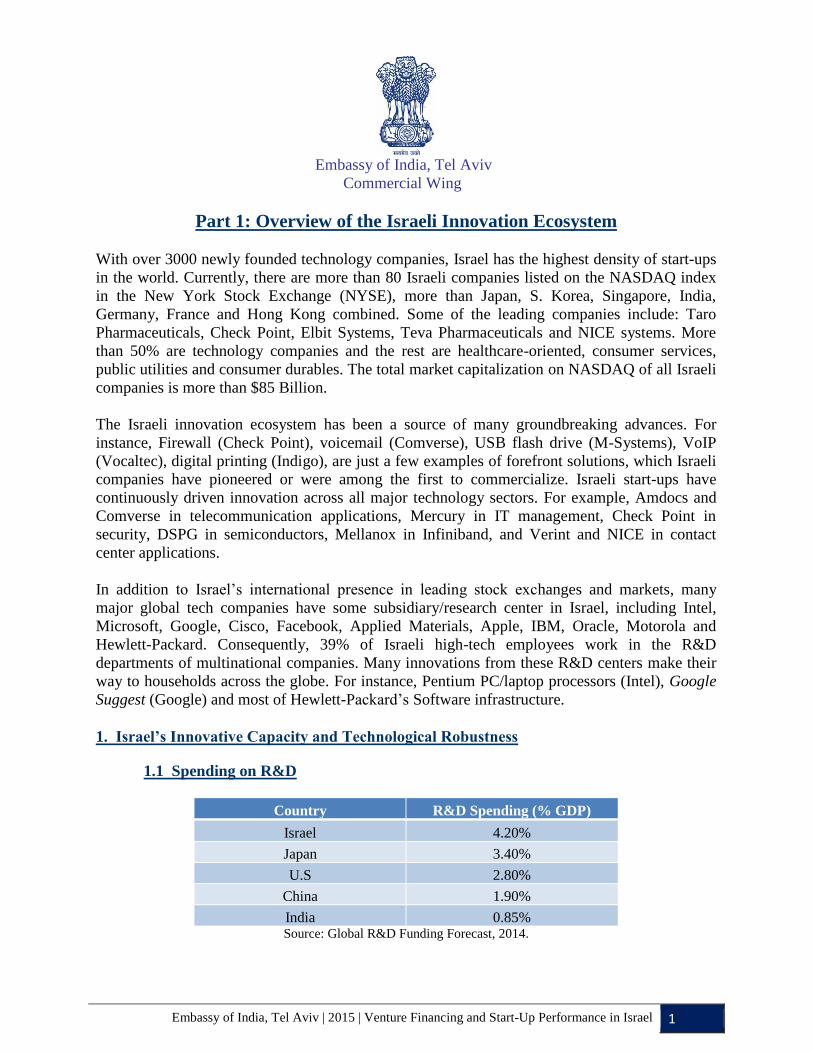

1.1 Spending on R&D

Country R&D Spending (% GDP)

Israel 4.20%

Japan 3.40%

U.S 2.80%

China 1.90%

India 0.85% Source: Global R&D Funding Forecast, 2014.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 2

In relative terms, Israel is an R&D powerhouse. In 2013, it spent 4.2% of its GDP on

science and technology R&D. For comparison, Japan invested 3.4%, the U.S-2.4%,

China-1.9% and India invested 0.85%. These figures may also indicate the strength of

Israel’s scientific institutions and R&D hubs, which are ranked 1st in the world for their

high-tech accomplishments (WEF Global Competitiveness Yearbook, 2013-2014). Israel

is also ranked high in terms of scientific support (3rd) and for its technological

infrastructure (4th). Israel’s relative abundance of scientists and engineers is ranked 8th in

the world.

1.2 High Quality University System – S&T Excellence

Recent surveys of the most prominent universities in the world have placed three Israeli

universities among the top 100. These institutions were included in the 2013 Academic

Ranking of World Universities (ARWU), an annual survey published by the Center for

World-Class Universities at Shanghai Jiao Tong University. The three universities are:

The Hebrew University of Jerusalem (59th place), Technion – Israel Institute of

Technology (77th place) and Weizmann Institute of Science (92nd place) — were all

included in the prestigious list. To date, 12 Israeli scientists, scholars and statesmen have

won the Nobel Prize (Chemistry – 6; Economics – 2; Peace – 3; Literature – 1), an

important indicator contributing to Israeli universities’ high ranking. Nobel Laureates

such as Dan Shechtman, Avram Hershko, Ada Yonath, Israel (Robert) Aumann and

Aaron Ciechanover continue to be associated with the above three institutions, either as

faculty or emeritus professors.

1.3 Hi-Tech "Iron Triangle": Academia, Industry and Government Ranked first in the world for know-how transfer and in the top ten for university-industry

collaboration (WEF Global Competitiveness Yearbook, 2013-2014) Israel has developed

an efficient innovation-stimulating structure. The close ties between academia, industry

and government create a "High-Tech Iron Triangle" that enables scientific innovation to

be quickly converted into marketable products and profitable business initiatives. These

dynamics have brought Israel to $25 billion in technological exports annually.

1.4 Technology Transfer Organizations (TTO) in Israel A prominent factor that is driving Israel’s innovative capacity is an efficient technology

transfer and commercialization mechanism. The vast majority of Israeli universities and

R&D institutes have sub-units dedicated to identifying scientific concepts which can be

commercialized and efficiently transferred as products to the private sector.

The leading TTOs in Israel include: Yeda R&D Company Ltd. (Weizmann Institute of

Science), Yissum Ltd. (Hebrew University of Jerusalem), Ramot (Tel Aviv University),

T3 – Technion Technology Transfer (Technion) and BGN Technologies (Ben-Gurion

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 3

University). The TTOs have also formed an umbrella organization, Israel Tech Transfer

Organization (ITTN). Currently, there are 12 partnering TTOs which comprise the

shareholders. ITTN is in the process of adding new members from Government-owned

medical centers and R&D institutions.

Tel Aviv University's Ramot Ltd. demonstrates the effectiveness of the Israeli technology

transfer mechanism. Founded in 1956, Ramot is a private, limited company, which is

partially owned by the Tel Aviv University. The company has a board of eleven

directors, comprised of serial entrepreneurs, TAU professors and CEOs of R&D-driven

companies. Ramot enjoys a reputation as a leading "go-to-source" innovation center

which has produced 65 start-up companies and registered over 70 patents a year. An

additional 300 patents are currently commercially available while awaiting the

finalization of the patenting process.

The company's technology transfer mechanism is based on the following model: First,

business development officers scout through the university's various departments for

new, cutting-edge research projects, preferably at an advanced stage. Second, initial

negotiations with the scientist begin, and Ramot presents the partnership structure and

revenue sharing model. Once an agreement is reached, Ramot follows-up on the project

and conducts financial feasibility checks. Third, Ramot's in-house legal and intellectual

property departments create a legal framework for the invention, including: licensing,

ownership and royalty payments. Finally, Ramot aids the scientist (and/or the spin-off

company) to commercialize the product and enter new markets. During this phase, Ramot

actively reaches out to industry leaders along with angel investors and VCs (in projects

that require additional funding).

Ramot's revenue stream is comprised of Licensing Fees, Royalties and Spin-Off Company

Exit Fees. The organization is headed by Mr. Shlomo Nimrodi (CEO) with five business

development officers in charge of different sectors (hi-tech, telecom, engineering,

computing & life sciences). The company also has in-house legal, intellectual property,

finance and project management departments.

2. Government Support: Office of the Chief Scientist The Encouragement of Industrial Research and Development Act of 1984 constitutes the general

mandate of the Office of the Chief Scientist (OCS). The OCS, which is part of the Israeli

Ministry of Economy, is the bureau responsible for government support of industrial R&D. The

bureau has various support channels for start-ups such as: the R&D Fund, Tnufa Program,

Magnet Program and Global Enterprise Collaboration Program. The application process is

similar in all channels, as companies approach the fund, then technological evaluators screen

proposals through a committee of experts. Finally, grants are given as a percentage of total

approved R&D expenditures with “strings attached” in case of commercial success.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 4

The OCS operates through MATIMOP (Israeli Industry Center for R&D), the executive agency

in charge of promoting industrial R&D cooperation between Israeli and foreign companies.

MATIMOP has numerous bilateral funds based on conditional grants. Thus, the relevant fund

provides reimbursements to companies for specific, acknowledged expenses (usually between

50%-66%, depending on the fund). In case of commercial success, the funds are considered

loans, and companies are required to repay OCS/MATIMOP through royalty payments (3%-5%

of sales). In case of non-commercialization or termination of the project, no repayment is

required.

The OCS has an important role in boosting the Israeli innovation ecosystem by providing

financial and professional support to early-stage start-ups. Pre-seed and seed stages are usually

in too early of a stage for VC financing due to the high-risk involved (no finalized products, lack

of capital and strategic partners, etc.). However, the OCS bridges this gap by providing funding

and professional guidance for entrepreneurs in these crucial early stages. The OCS' active role in

this model has been a driving force in shaping the Israeli innovation ecosystem.

MATIMOP/Foreign Trade Administration also have joint bilateral funds with India: i4RD

(India-Israel Initiative for Industrial Research and Development), KIRD (Karnataka-Israel

Research and Development) and Special Program for Opening Offices in India and China.

These programs provide active support for collaborative R&D ventures between Indian and

Israeli companies and support the opening of branch offices in India.

Another important support channel is the Technological Incubator Program. Incubators enable

novice entrepreneurs with innovative, technology-driven ideas to transform them into finalized

products/services. The program provides entrepreneurs with an R&D grant, R&D infrastructure

(office space, mentorship network, informal event programs, investor exposure and public

funding links) and various consulting services. Currently, there are 20 incubators in Israel (19

technological and one biotech). The incubators are located in Jerusalem, Tel Aviv, Haifa,

Netanya, Nazareth, Be’er Sheva, Kiryat Gat and Kiryat Shmona. The incubators specialize in IT

& telecom, biomed and medical devices, water engineering and agritech. At the moment, there

are some 160 Israeli companies (in various stages of R&D) operating in these incubators.

In 2013, the OCS' annual budget amounted to approx. $395 million. The vast majority of funds

were appropriated to the R&D Fund ($261 million) and the remainder divided between the

Magnet Program ($47 million), Technological Incubator Program ($36 million), and other early

stage projects & infrastructure ($51 million). However, the annual budget has declined by 7.9%

since 2009.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 5

3. Venture Capital Funds in Israel

The VC market in Israel is extremely vibrant and active. Currently, the market is comprised of

60-70 active funds which combine both foreign and Israeli funds. Among the most prominent

Israeli funds are Jerusalem Venture Partners (JVP), Genesis Partners, Infinity Fund, Carmel

Ventures, Evergreen Venture Partners and Pitango Ventue Partners. In recent years, more and

more leading U.S and European VC funds have opened offices in Israel: Battery Ventures,

Lightspeed Venture Partners, Susquehanna Growth Equity, Bessemer Venture Partners,

BlueRun, Blumberg Capital, Bridge Capital Fund, Partech International Inc., Defta Partners,

LLC and Ziegler Meditech Equity Partners. Furthermore, there are nearly 220 international

funds, including Polaris Venture Partners, Accel Partners and Greylock Partners, which do not

have offices in Israel, but actively invest in Israel through local representatives.

3.1. Israeli VC Fund-Raising Trends

Between 2004 and 2013, Israeli VC funds were very active and managed to raise an

accumulated $7.34 billion. It is important to note that only a handful of Israeli VCs raise

funds every year (between 2 to 17). This trend peaked in 2005, as 10 Israeli VCs raised

$1.4 billion. On the other hand, in 2010 only 2 active VCs raised a sum of $0.03 billion.

2013 was less productive than the past two years in terms of Israeli venture capital fund

raising, with 13 funds raising $526 million, almost 28% below the $725 million raised by

14 Israeli VC funds in 2012 and 28% under the 10-year average of $732 million.

In 2013, micro-VC funds accounted for almost $124 million or 24% of total capital, the

largest share in three years, while the number of micro-VCs decreased to eight, compared

to nine and eleven in 2012 and 2011, respectively

3.2 Foreign VC Fund-Raising Trends

In recent years, there has been a re-awakening of investments and activities by foreign

VCs in the Israeli market, indicating that fund-raising and the deal flow may rise in 2014-

15. In 2012, Sequoia Capital raised $200 million and established another Israeli-focused

fund, Sequoia V, focusing on technology, healthcare and energy. In addition, New York-

based Blumberg Capital completed a $150 million fund-raising round to establish a local

office in Israel and to search for new Israeli technology companies. This positive trend

continued in 2013, as Battery Ventures announced that it has raised capital for two new

funds - $650 million for its 10th fund, and a $250 million side fund to support later stage,

growth and buyout deals. Foreign venture capitalists have raised funds to increase

activity in enterprise software, network security, data storage and wireless technologies.

They have also reported some activity in life sciences, especially in the formation of new

medical device companies. In terms of VC investments, in early 2013 the capital

available for investment by funds was approximately $2.1 billion. $484 million (23%)

out of $2.1 billion financed first investments and the rest went to follow-on investments.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 6

3.3 First Investments Made by VCs in 2013

VC Fund Total First

Investments Company Portfolio

Pontifax

(Israeli) 8

TheraCoat, OCON, HeadSense, V-Wave, BioCep,

Bioblast, Eloxx, Metabomed

Pitango

(Israeli) 7

Keepy, JethroData, Taboola, SalesPredict, Ubimo,

Revizer, Carambola

Vintage

(Israeli/Foreign) 6

Innovid, Superfish, SundaySky, Wilocity, Outbrain,

TabTale

Magma

(Israeli) 6

AppWiz, WireX, CloudEndure, Foresight Info, Inplerus,

Adience

Battery

(Foreign) 6

Elastifile, SiSense, Scodix, Cyvera, Stratoscale,

PrimaryData

Horizons

(Foreign) 6

Nipendo, Kaiima, Meteo-Logic, MeMed, Aniways,

Crosswise

Lightspeed

(Foreign) 6

Scodix, Personetics, Insightera, Bluevine, PrimaryData,

Elastifile

Marker

(Foreign) 6

Interlude, iDoMoo, MobileSpaces, Eyeview, OverWolf,

Panoramic Power

Sequoia Israel

(Foreign) 5

Pyramid Analytics, Seculert, Forter, Moovit, Endospan

OrbiMed Israel

(Foreign) 5

Medigus, BioLineRX, InspireMD, Treato, Redhill

Genesis Angels

(Israeli) 5

Infinity AR, Beyond Verbal, StoreDot, Sirin, Stox

Kreos

(Foreign) 5

GetTaxi, MultiPhy, Pontis, QualiSystems, RealMatch Source: IVC Research Center.

4. Notable Israeli Exits, Mergers & Acquisitions, 2004-2013

In recent years, there have been some high-profile, high value buy-outs of Israeli startups. 2006

marked the most-prosperous year during this period, with all accumulated exits that year

amounting to $10.75 billion from 116 deals. Another interesting trend concerns the size of

acquisitions: most of the deals during this period were less than $5 million (405 deals). The

runner-up was the $20-$50 million range with a total of 118 deals amounting to $3.67 billion.

Finally, there were 4 "unicorns" ($1 billion or more) amounting to more than $10 billion.

IT, telecommunications and life sciences were the most dominant sectors in terms of companies

acquired by major global companies between 2004 and 2013. In 2006, IT & software accounted

for 62.35% of all acquisitions that year, surpassing all other sectors including life sciences,

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 7

semiconductors, cleantech and communications. In 2013, life sciences picked-up, as 34.44% of

all exits that year were from that sector. IT & software came in second with a total of 20.62% of

all acquisitions that year.

4.1 Major Exits and M&As, 2004-2013

Company: Acquired by: Year: Transaction:

Cisco 2012 $5 Billion

Lucent

Technologies 2000 $4.5 Billion

Marvell

Technology 2000 $2.7 Billion

SanDisk 2006 $1.55 Billion

Google 2013 $966 Million

IBM 2013 $800 Million

NCR 2013 $800 Million

Stratasys 2012 $634 Million

DG 2013 $517 Million

VerticalNet 2000 $507 Million

CSR 2011 $484 Million

EMC 2012 $450 Million

Johnson &

Johnson 2008 $438 Million

***

Part 2:

Venture Financing

in Israel

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 8

Part 2: Venture Financing in Israel

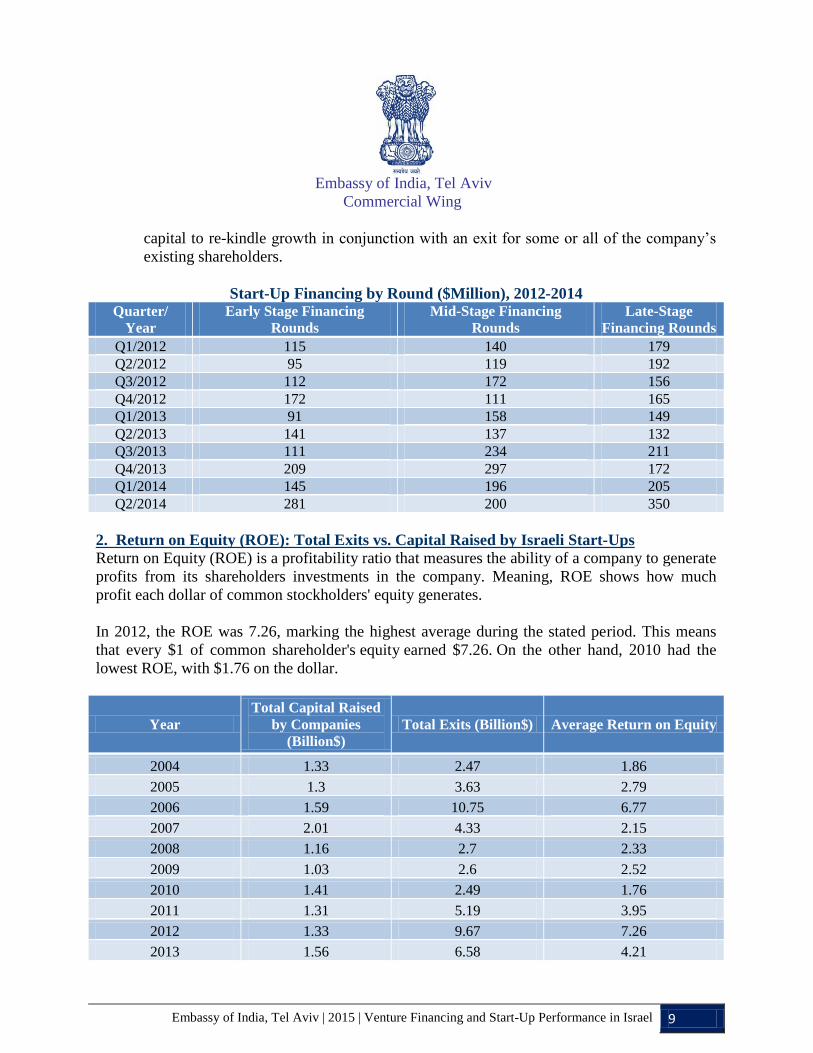

1. Stages of Venture Financing - Taxonomy

There are five distinct stages of venture financing in the Israeli ecosystem: start-up stage, seed,

growth/mid- stage, late stage, and buyouts/recapitalizations.

Start-Up Stage

Recently established companies without significant operating track-records are regarded

as in the start-up stage. Most entrepreneurs fund this stage of a company’s development

through FFF ("Friends, Family & Fools"), Bootstrapping as well as angel investments.

Seed

Seed financing rounds involve investments of less than $5 million for start-ups showing

the possibility of achievement or excellence, affirmed by key customers yet still have not

reached a cash flow break-even point. Early stage venture capital funds and angel

networks often provide these kinds of investments. Typically, seed and early venture

capital funds tend to invest in companies within their region as their principals actively

work with management on a variety of operational issues.

Growth/Mid-Stage

Growth/mid-stage investments focus on companies that have a proven concepts and

business models, and either profitable or on route to sustainable profitability. These

investments tend to range between $5 and 20 million and are directed towards assisting

the company to increase the market share of products and services. The pool of potential

venture capital investors is very robust for growth stage investments, with local Israeli

VCs and international firms willing to participate in investment rounds at this stage.

Late Stage

Late stage investments tend to be for relatively developed and stable companies seeking

to raise more than $10 million for significant strategic initiatives (international

expansion, marketing and sales, acquisitions, etc.) that will create substantial growth

advantage over their competitors. Robust and well-established venture capital firms

usually finance these rounds.

Buyouts and Recapitalizations

Buyouts and recapitalizations are more common for highly-developed and productive

technology companies. In these exchanges, shareholders sell some or all of their shares to

a VC firm in return for readily available funds. These VCs may also provide additional

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 9

capital to re-kindle growth in conjunction with an exit for some or all of the company’s

existing shareholders.

Start-Up Financing by Round ($Million), 2012-2014 Quarter/

Year

Early Stage Financing

Rounds

Mid-Stage Financing

Rounds

Late-Stage

Financing Rounds

Q1/2012 115 140 179

Q2/2012 95 119 192

Q3/2012 112 172 156

Q4/2012 172 111 165

Q1/2013 91 158 149

Q2/2013 141 137 132

Q3/2013 111 234 211

Q4/2013 209 297 172

Q1/2014 145 196 205

Q2/2014 281 200 350

2. Return on Equity (ROE): Total Exits vs. Capital Raised by Israeli Start-Ups

Return on Equity (ROE) is a profitability ratio that measures the ability of a company to generate

profits from its shareholders investments in the company. Meaning, ROE shows how much

profit each dollar of common stockholders' equity generates.

In 2012, the ROE was 7.26, marking the highest average during the stated period. This means

that every $1 of common shareholder's equity earned $7.26. On the other hand, 2010 had the

lowest ROE, with $1.76 on the dollar.

Year

Total Capital Raised

by Companies

(Billion$)

Total Exits (Billion$) Average Return on Equity

2004 1.33 2.47 1.86

2005 1.3 3.63 2.79

2006 1.59 10.75 6.77

2007 2.01 4.33 2.15

2008 1.16 2.7 2.33

2009 1.03 2.6 2.52

2010 1.41 2.49 1.76

2011 1.31 5.19 3.95

2012 1.33 9.67 7.26

2013 1.56 6.58 4.21

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 10

3. Case Studies: Financing Models for Asian Investments in Israel

In recent years, an increasing number of Asian companies, particularly from Japan, S. Korea and

China have invested in the Israeli innovation ecosystem. Examining these cases can provide new

perspectives on financing models in the Israeli ecosystem and serve as living proof to the great

business potential in the Israeli technology market.

3.1 Japan

TEL VC and Liola Technologies

During Q1 of 2014, Tokyo Electron Venture arm TEL VC completed its second

investment in Israel, by signing an investment agreement with Liola Technologies. Liola

Technologies was founded in 2010 by Daniel Porat and a team of experts in

mathematics, algorithms writing and software development. The team designed and

developed a technology, product and go to market breakthrough that enables complex

manufacturing plants to optimize their production plans and achieve increased plant

throughput.

This case study demonstrates a classic venture capital investment by a foreign VC firm in

the Israeli innovation ecosystem.

Rakuten and Viber Media

During Q1 of 2014, Japanese internet giant Rakuten acquired the Israel-based Viber

Media for over $900 million. A bulk of the purchase price, however, was contingent on

Viber meeting long-term business objectives, so the final price could be considerably

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 11

lower. Viber has about 280 million registered users around the world and grew 120%

during 2013. Around 100 million people actively use the product each month.

This case study is unique, because prior to the acquisition, Viber never received any

funding from venture capital firms for its technology, but it launched new services to

diversify its income sources. Among them was Viber Out, which allows users to make

international calls to non-Viber users at low rates.

Toshiba and Zadara Storage

Irvine, CA and Nesher, Israel-based cloud storage software developer Zadara Storage

closed an Original Equipment Manufacturing (OEM) deal (Q1 2014) with Toshiba to

offer a private label version of its Virtual Private Storage Array (VPSA) service in Japan

for Toshiba. Moreover, Toshiba invested in Zadara through Toshiba America Electronics

Components. $3 million in July 2013 and increased its investment to $10 million in

February 2014. The funding was mostly directed towards sales, support, and engineering.

This case demonstrates a financing model whereby a foreign corporation channels

relatively small, incremental investments rather than pursuing an acquisition. This model

puts weight on the R&D and growth stages.

Panasonic Corporation and TowerJazz

During Q2 of 2014, TowerJazz announced the successful completion and kick-off of a

joint venture (JV) with Panasonic Corporation. Within the scope of the JV, Panasonic

transferred its semiconductor manufacturing process and capacity tools of 8/12 inch

wafers at its Hokuriku factories (Uozu, Tonami and Arai) to the JV, committing to

acquire its products from the JV for a long-term period of at least five years of volume

production.

TowerJazz holds 51% of the shares of the JV, and its revenues are increased by

approximately $400 million per year. Panasonic Corporation is a 49% shareholder of the

JV. In consideration for its 51% equity holding in the JV, TowerJazz issued to Panasonic

870,454 ordinary shares in the value of approximately $7.5 million, which were

calculated based on TowerJazz’s average share price during the 15 trading days period

ended on March 27, 2014. As a result of holding its ordinary shares, Panasonic became a

minority stakeholder in TowerJazz, holding approximately 1.8% of TowerJazz ordinary

shares.

This case study exemplifies a financing model based on a joint venture and joint

shareholding in a manufacturing partnership. This can also serve as a viable financing

model in future investments in the Israeli innovation ecosystem.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 12

JA Mitsui and TowerJazz

During Q3 of 2014, Israel-based TowerJazz and Japanese finance body JA Mitsui

announced the signature of a five year term loan agreement to provide TowerJazz of

which Tower Semiconductor Ltd. has the majority holding, with a term loan of

approximately $85 million. The loan will be repaid in seven equal semi-annual

installments which will commence two years after signing.

This case study demonstrates another financing model based on institutional investments.

In specific cases, this sort of funding can be applicable to the Israeli innovation

ecosystem.

SUN Corp. and BacSoft Ltd.

During Q3 of 2014, Japanese SUN Corp. acquired 363.75 shares in Israel-based

Company Bacsoft Ltd., through private placement as well as from three shareholders of

Bacsoft, for $1.8 million in total.

BacSoft Ltd. engages in the field of integrated remote control and monitoring of utility

installations and industrial automation. The company offers a monitoring and control

platform for utility supply, distribution, and storage. It provides a range of solutions from

underground pipelines to aerial climate control and from isolated and inaccessible

environments to bustling urban centers. It serves customers through distributors in

Argentina, Brazil, Chile, Mexico, and Peru. The company was founded in 2002.

This case exemplifies a model of financing through a public placement. This model can

also be applicable for Israeli technology companies which have undergone an IPO.

3.2 South Korea

L&S Venture Capital and Fulcrum SP

During Q2 of 2012, South Korean VC fund L&S Venture Capital invested approximately

$700,000 in Israeli nano-technology company Fulcrum SP. The company focuses on

commercializing the use of nano-particles in products made from composite materials.

This deal marked the first time a Korean venture capital fund invested in an Israeli

technology company.

Albeit being a relatively small investment, the case study exemplifies the possibility of a

foreign venture capital fund investing in the Israeli innovation ecosystem, a model that

can be emulated by other Asian investors.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 13

Samsung and EarlySense

During Q1 2015, Korean technology giant Samsung announced that it would invest $10

million in Israeli co. EarlySense. The company has developed a system that monitors

patients who are sick enough to require continuous tracking, but are unwilling or do not

need to be physically connected to sensors. The system uses sensors embedded into a

mattress or chair cushion to monitor pulse, respiration and other vitals. The data is

transferred to a monitoring station with the system signaling in the event that something

appears amiss.

Samsung and Rounds

During Q4 of 2014, Samsung Ventures together with other international funds invested

$12 million in Israeli start-up 'Rounds'. The company produced a cross-platform

messaging app focused on real-time video chat with more than 25 million users which is

somewhat a combination of WhatsApp and Skype.

This case study demonstrates the possibility of a foreign venture capital fund investing in

the Israeli innovation ecosystem, together with other international funds in a relatively-

large B series investment.

3.3 China

Yifang Digital Technologies and Pegasus Technologies

During Q1 of 2010, digital pen developer Pegasus Technologies Ltd. became the first

Israeli company to be acquired by Chinese technological powerhouse, Yifang Digital

Technology Co. Ltd. The deal amounted to $60 million in cash and shares. Pegasus's first

product was a 3D mouse, and it was only in 2000 that it switched to developing its

current product line of digital pens, which translate handwriting into digital formats that

work with various computer standards.

This case exemplifies a typical M&A model where an Asian corporation acquires an

Israeli technology company to advance a new line of products.

Zhejiang Sanhua Co. and HelioFocus

During Q1 of 2010, HelioFocus Ltd., an Israel-based solar thermal systems start-up,

raised more than $11 million from China's Zhejiang Sanhua Co. and existing investor IC

Green Energy. HelioFocus developed a thermal system that converts sun rays into hot air

to produce electricity and is expected to boost electricity production of existing power

plants.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 14

Shanghai Fosun Pharma (Group) Ltd. and Alma Lasers

During Q2 of 2013, Shanghai Fosun Pharma (Group) Ltd. acquired approximately 96.6%

of Alma Lasers Ltd., a manufacturer of lasers used in cosmetic surgery, for $240 million.

The company, which is based is in Israel, is an internationally well-known manufacturer

of laser, light-based, radiofrequency and ultrasound products with integrated product

portfolios for aesthetic and medical applications, and businesses located around the

world.

Everbright China and Real Imaging

Breast cancer diagnostics company Real Imaging Ltd. has raised several million dollars

(undisclosed) from China Everbright Investment Management Ltd. This was the

company’s first financing round and the first investment in an Israeli company made by

Everbright and is a good example of a foreign seed investment in Israel.

Alibaba and Visualead

During Q1 of 2015, Chinese e-commerce giant Alibaba invested $5 million (two rounds)

in an Israeli startup 'Visualead'. The company that specializes in QR code technology,

and will enable Alibaba to use their technology in its various operations, which include

hopping sites and apps, a cloud computing platform, and a movie production studio.

Visualead was established in 2013, has more than half a million business users

worldwide.

4. Indo-Israeli Innovation Partnerships

Sun Pharma and the Technion

During Q2 of 2015, Indian drug powerhouse Sun Pharmaceuticals Ltd. and the Technion

– Israel institute of technology, announced that their respective organizations have

entered into an exclusive worldwide research and license agreement. This agreement

aims at the development of a joint project, based on new findings by Nobel Prize laureate

Prof. Aaron Ciechanover, Dr. Gila Maor and Prof. Ofer Binah, that can potentially lead

to the development of novel anti-cancer drugs.

This case study exemplifies a financing model where an Indian company places a direct

investment in an Israeli research institute, in order to develop new products that can in

turn be commercialized and marketed.

Tech Mahindra and Leadcom Integrated Systems

During Q4 of 2014, Tech Mahindra Ltd., an Indian telecom powerhouse which

specializes in digital transformation, consulting and business re-structuring, signed an

agreement to acquire global networks services leader Lightbridge Communication

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 15

Corporation (LCC) for an enterprise value of approximately $240 million. With more

than 5000 employees worldwide in over 50 countries, LCC generated annual revenues of

more than $400 million. Moreover, LCC has built 350 networks and engineered more

than 350,000 cell sites for over 400 leading clients in the global market.

With the LCC acquisition, Tech Mahindra became the sole owner of Leadcom Integrated

Systems, an Israeli network service-provider. Leadcom provides, management, and

implementation of telecommunications network deployment services and solutions for

pan-regional operators, vendors, and major enterprises and has some 25-30 employees at

company headquarters in Petah Tikva, Israel. Ostensibly, Tech Mahindra will convert

Leadcom into its techno-scouting unit in the Israeli innovation ecosystem and is planning

to invest $20 million in Israeli startups.

This case study exemplifies a financing model where an Indian financier acquires an

Israeli company and transforms it into an overseas branch office in order to scout for new

startups and promote new technology ventures.

Tech Mahindra and Comverse Israel Inc.

During Q1 of 2015, Tech Mahindra Ltd. and U.S-owned Comverse Israel Inc. reached a

$250 million agreement in principle on a strategic relationship, whereby Comverse will

accelerate its transformation as a global innovator in digital services by leveraging Tech

Mahindra’s expertise and scale in development and delivery of digital offerings. As part

of this initiative, some 400 Israeli employees from certain functions within Comverse’s

Digital Services business unit are anticipated to join Tech Mahindra. Tech Mahindra is a

specialist in digital transformation, consulting and business re-engineering, particularly

in the global technology industry.

Tech Mahindra will complement Comverse’s R&D and engineering operations through

innovation in product development techniques and just-in-time capability reinforcement.

Tech Mahindra will bring its experience in developing and creating a start-up ecosystem

that has helped launch path-breaking solutions for the connected world. The company

will also enable global exposure and long-term career opportunities for the employees

coming onboard from Comverse.

This case study demonstrates a joint M&A financing model, where an Indian financier

creates a joint strategic alliance with another foreign company in order to invest in

indigenously-made Israeli intellectual property and technology.

Tata Group and Ramot Ltd.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 16

During Q2 of 2013, Indian conglomerate Tata Group invested $5 million in the

Momentum Fund, which was established by Tel-Aviv University's technology transfer

office, Ramot Ltd. This investment was the first installment of $20 million promised to

Ramot by Tata and other financiers. The Momentum Fund invests in promising

breakthrough technologies in a wide range of fields, including: pharmaceuticals,

healthcare, cleantech and hi-tech.

This case demonstrates a quite unique financing model, where a conglomerate invests in

an innovation fund established by a University's technology transfer office. Afterwards,

the fund invests in early-stage innovation projects at the university.

Tata Consultancy Services (TCS) Branch Office, Israel

In 2006, Tata Consultancy Services Ltd., the third largest corporation within the Indian

conglomerate Tata Group opened a branch office in Israel. TCS Israel provides IT

services, consulting and business solutions. Unlike other centers in the network, the

Israeli center does not specialize in any particular area of technology, but has a more

holistic approach. Over the course of time, TCS has provided IT/business solutions to

Israeli powerhouses such as ZIM and Bank Yahav. In a deal with the Latter, TCS

supplied an integrated banking system called ‘BaNCS’ for approximately $700 million.

Furthermore, TCS Israel established ‘COIN’ (Co-Innovation Network) – a network of IP

management and partnering strategies to drive innovation in an environment of open

communities and solution brokers. Solutions also involve technologies wrapped in

process bundles and new software investments based on subscription rather than

ownership.

This case study demonstrates how an Indian corporation can set-up a branch office in

Israel for techno-scouting, networking and to serve as a long-arm for investments.

***

Embassy of India, Tel Aviv

Commercial Wing

Part 3:

India and Israel – Future

Outlook

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 17

Part 3: India and Israel - Future Outlook

Governments of India and Israel have strong mutual interests in each other. On one hand, the

Israeli ecosystem provides technological solutions that can solve developmental challenges in

India. On the other hand, Israel could benefit tremendously from an influx of Indian investments.

Furthermore, India and Israel endured the 2008 global crisis and did not fall into recession.

Strong macro-economic fundamentals creates a strategic fit between the two countries. Experts

(Indian and Israeli venture capital executives, Israeli entrepreneurs, government officials,

diplomats and Israeli/Indian businessmen) who were interviewed during the preparation of the

report had a positive outlook about technological capabilities of Israel and opined that the Israeli

innovation ecosystem offered lots of opportunities for foreign investors (including Indian

investors). Sectors in which this potential was profound were:

Biotechnology, pharmaceuticals and medical devices.

Renewable energy.

Agriculture technology and water engineering.

Cyber-security and software development.

IT and telecommunications.

Excellent opportunities exist for Indian investors at Technology Transfer Offices (TTOs) of

leading Israeli Universities. These investors could acquire licenses (early stage investments) for

innovative technologies which are developed in Israeli universities. Investments in growth stage

Israeli start-ups offer mature, cutting-edge technologies to Indian investors and help them in

using these start-ups as vehicles to increase presence in Western markets (Israeli start-ups are

generally present in European and US markets). Investments in Israel would also help the Indian

investors spread their risk of investment without compromising on returns.

Apart from this convergence of interests, there are also incompatibilities between the Indian and

Israeli ecosystems that should be identified:

Israeli entrepreneurs are concerned that Indian companies interested in acquiring Israeli

start-ups would close the (acquired) company’s operations in Israel. Most Israeli

entrepreneurs are interested in keeping R&D centers in Israel after the acquisition.

Indian investors are more interested in mature technologies and hence, are reluctant in

investing in early stage Israeli start-ups.

Information gaps are a problem for Indian investors. Potential Indian investors are

disinclined to invest in Israeli start-ups because they have limited access to information.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 18

Indian investors assess that investing in Israeli start-ups are costlier than investing in

European start-ups. Israeli start-ups had higher valuations because they are usually

considered value-adding technologies, which the Indian investors find difficult to

quantify.

Physical distance is a perceived obstacle. Investors from both countries prefer to stay

physically close to their investments and get actively involved in their investments.

Lack of product compatibility is another hurdle. Indian investors perceive Israeli

solutions as more suitable for the U.S and European markets rather than the

heterogeneous Indian market.

Trust deficit make due diligence processes in India longer. Hence, negotiation processes

take longer than usual. This made the situation difficult for Israelis as they prefer faster

decision making and less ambiguity regarding decisions.

***

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 18

Annexure:

Performance Analytics

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 19

Annexure: Performance Analytics

1. Total Exits ($Billion), 2004-2013

Year Total Exits ($Billion) Average Exit Deal ($Million) Total Number of Deals

2004 2.47 32.6 76

2005 3.63 37.8 96

2006 10.75 92.7 116

2007 4.33 38 114

2008 2.7 31.4 86

2009 2.6 32.5 80

2010 2.49 30.3 82

2011 5.19 51.9 100

2012 9.67 113.8 85

2013 6.58 76.6 86 Source: IVC Research Center.

Analysis:

2006 marked the most-prosperous year during this period with exits amounting to $10.75

billion from 116 deals.

2004 was the slowest year during this period, as exits amounted to $2.47 billion from

only 76 deals.

Between 2004 and 2013, the annual average per exit was $53.76 million; the annual

average of deals was 92.1.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 20

2. Deals by Size, 2004-2013

Size of Deal Total Number of Deals Total Exits ($Billion)

1. Less than $5 Million 405 $0.52 Billion

2. $5 Miilion-$10 Million 103 $0.72 Billion

3. $10 Million - $20 Million 109 $1.43 Billion

4. $20 Million - $50 Million 118 $3.67 Billion

5. $50 Million - $100 Million 68 $4.71 Billion

6. $100 Million - $500 Million 106 $21.29 Billion

7. $500 Million - $1 Billion 8 $5.82 Billion

8. $1 Billion or More 4 $12.25 Billion Source: IVC Research Center.

Analysis:

Between 2004 and 2013, most of the deals were less than $5 million (405). However,

these deals generated only $0.52 billion.

Between 2004 and 2013, deals ranging from $100-$500 million (106) accounted for most

of the revenue from exits ($21.29 billion).

Between 2004 and 2013, there were 4 deals over $1 billion (“unicorns”).

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 21

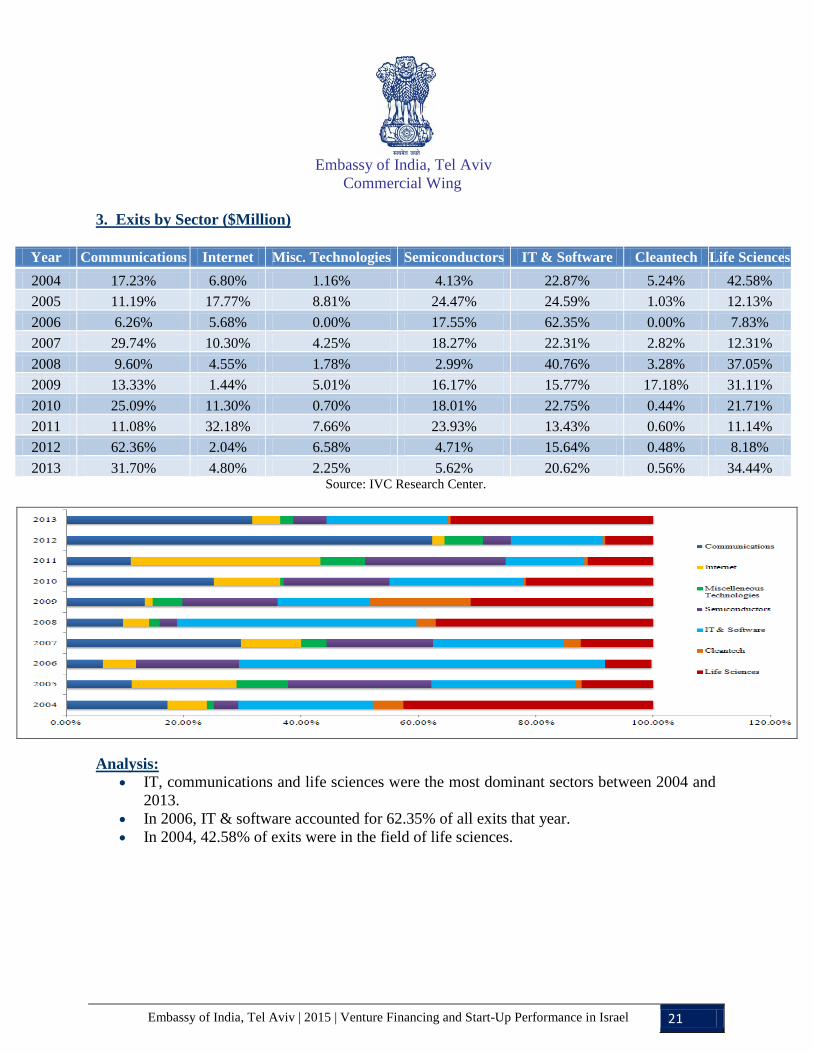

3. Exits by Sector ($Million)

Year Communications Internet Misc. Technologies Semiconductors IT & Software Cleantech Life Sciences

2004 17.23% 6.80% 1.16% 4.13% 22.87% 5.24% 42.58%

2005 11.19% 17.77% 8.81% 24.47% 24.59% 1.03% 12.13%

2006 6.26% 5.68% 0.00% 17.55% 62.35% 0.00% 7.83%

2007 29.74% 10.30% 4.25% 18.27% 22.31% 2.82% 12.31%

2008 9.60% 4.55% 1.78% 2.99% 40.76% 3.28% 37.05%

2009 13.33% 1.44% 5.01% 16.17% 15.77% 17.18% 31.11%

2010 25.09% 11.30% 0.70% 18.01% 22.75% 0.44% 21.71%

2011 11.08% 32.18% 7.66% 23.93% 13.43% 0.60% 11.14%

2012 62.36% 2.04% 6.58% 4.71% 15.64% 0.48% 8.18%

2013 31.70% 4.80% 2.25% 5.62% 20.62% 0.56% 34.44% Source: IVC Research Center.

Analysis:

IT, communications and life sciences were the most dominant sectors between 2004 and

2013. In 2006, IT & software accounted for 62.35% of all exits that year. In 2004, 42.58% of exits were in the field of life sciences.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 22

4. Total Capital Raised by Israeli Venture Capital Funds by Year, 2004-2013

Year Amount Raised by VCs ($Billion) Number of Funds

2004 0.55 6

2005 1.4 10

2006 0.96 12

2007 0.97 10

2008 1.1 10

2009 0.23 2

2010 0.03 2

2011 0.84 17

2012 0.73 14

2013 0.53 13 Source: IVC Research Center.

Analysis:

In 2005, VC fund-raising peaked at $1.4 billion.

In 2010, 2 active VC funds raised a sum of $0.03 billion.

Between 2004 and 2013, the total amount of capital raised by VCs was $7.34 billion.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 23

5. Venture Capital Funds Making First Investments: Number of Deals vs. Number of VCs

Year Number of VCs Number of Deals

2009 63 125

2010 86 151

2011 120 249

2012 122 260

2013 122 255 Source: IVC Research Center.

Analysis:

In 2011, the total number of deals increased by 64.9%.

In 2012, venture capital funds made 2.13 first investments in average.

Between 2009 and 2013, the total number of first investments made by venture capital

funds increased by 104%.

Between 2009 and 2013, the total number of venture capital funds making first

investments increased by 93%.

Embassy of India, Tel Aviv

Commercial Wing

Embassy of India, Tel Aviv | 2015 | Venture Financing and Start-Up Performance in Israel 24

6. IPO’s during 2013

Company Name Sector Stock Exchange

Alcobra Ltd. Life Sciences NASDAQ

Enzymotec Ltd. Life Sciences NASDAQ

Glatronics Ltd. Communications TMX

Kadimastem Ltd. Life Sciences TASE

Somoto Ltd. IT & Software TASE

Wix.com Internet NASDAQ Source: PwC Israel Hi-Tech Exit Report, 2013.

***