vermont income tax course (2016) instructor’s guide · vermont income tax course (2016) ... • a...

TRANSCRIPT

Vermont Income Tax Course (2016)

Instructor’s Guide

Item # D2H108722

Vermont Income Tax Course (2016)

A Publication of H&R Block Services, Inc., Kansas City, Missouri

The State Tax Training Team

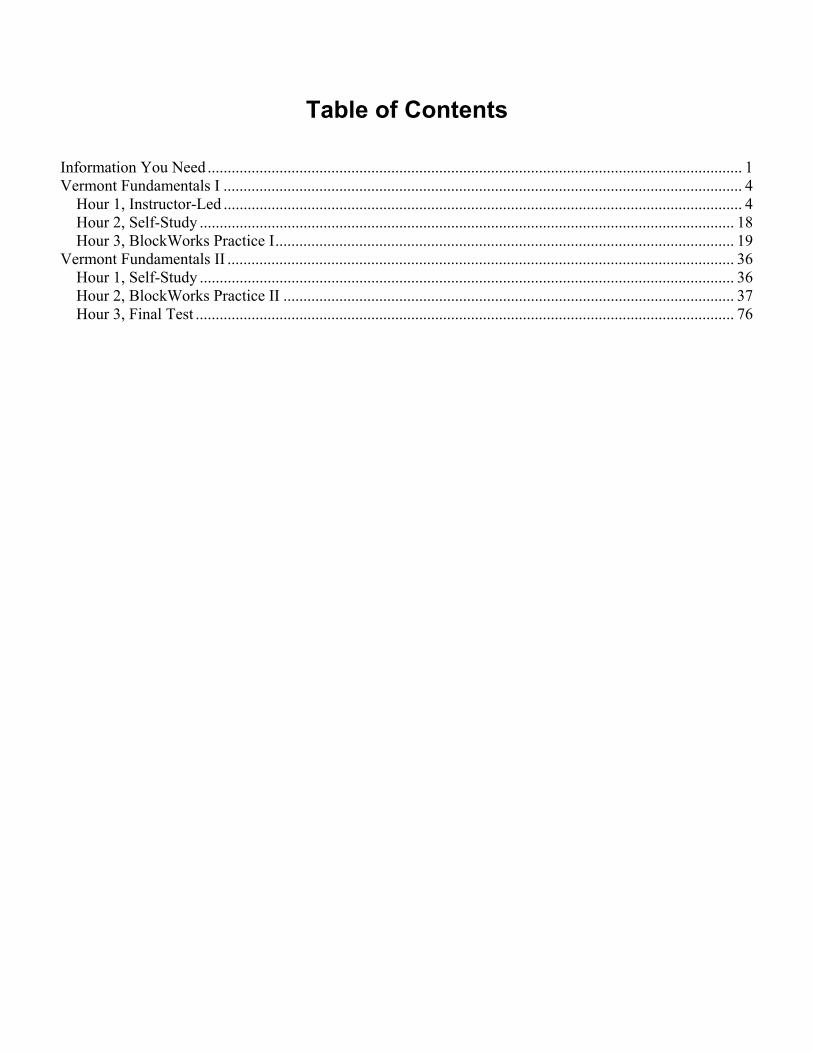

Table of Contents Information You Need ...................................................................................................................................... 1 Vermont Fundamentals I .................................................................................................................................. 4

Hour 1, Instructor-Led .................................................................................................................................. 4 Hour 2, Self-Study ...................................................................................................................................... 18 Hour 3, BlockWorks Practice I ................................................................................................................... 19

Vermont Fundamentals II ............................................................................................................................... 36 Hour 1, Self-Study ...................................................................................................................................... 36 Hour 2, BlockWorks Practice II ................................................................................................................. 37 Hour 3, Final Test ....................................................................................................................................... 76

Intentionally left blank.

Preface PURPOSE The purpose of this state course is to provide learners with an understanding of the state law as it relates to the federal law. This course does not cover all areas of state taxation, but highlights topics that are covered in H&R Block’s Income Tax Course. PREREQUISITES This course was written with the assumption that students either have good working knowledge of basic federal income tax law or are currently completing H&R Block’s Income Tax Course. CONTENT This course is designed to provide the information tax preparers will need when assisting a typical taxpayer. Because the same course content is used throughout your state, some topics may be more or less pertinent in your area. Please visit your state Department of Revenue's website for the latest forms. The information in this course is based on tax law as it applies to the 2015 tax year. Tax laws are in a constant state of change, and this course information reflects laws at the time of printing. It is your responsibility to remain current on tax law. COURSE CREDIT Credit for this course is given by completing H&R Block’s Income Tax Course. Two 3-hour sessions have been allotted for state material. COURSE COMPLETION Participants are required to take H&R Block’s Income Tax Course test in order to receive full credit hours for this course.

Intentionally left blank.

Vermont Income Tax Course Instructor’s Guide (2016)

1

Chapter 0

Information You Need Welcome to the redesigned state training for the H&R Block Income Tax Course (2016). What’s changed? We’re glad you asked!

What’s New • Two dedicated sessions will be delivered near the end of the federal course (after ethics, but before

the review for the final test). • Updated training based on the fact that students already have an established tax foundation. • Access to a digital participant’s guide that contains embedded BlockWorks video demonstrations. • Case studies written specifically for each state. • A final test that includes a case study and multiple-choice questions.

We’re excited about the new material and format, and hope you will be, too.

Overview This course, like its federal companion, is based on 2015 tax law. H&R Block wants beginning tax preparers to understand the basic principles of preparing a Vermont return; however, this material does not cover all aspects of preparing said tax return. Just like the federal text, in places the text states, “this is beyond the scope of this course” and/or something like “this is presented for awareness purposes.” While some of the material is beyond the scope of new preparers, they need to understand basic concepts so they can recognize issues and realize assistance may be needed.

Classroom Supplies • One instructor’s guide. • Instructor slide presentation, “Overview of a Vermont Tax Return.” • Participant’s guide (one for each student). • Ear buds (for recorded demonstrations). • Access to the state-specific participant’s guides (printed and digital). • Access to BlockWorks. • Access to Block Academy. Optional: • Fillable PDFs. • Projectable case study solutions.

Instructor Materials As the instructor, you will receive the instructor’s guide and the participant’s guide, and will have access to the instructor slide presentation, “Overview of a Vermont Tax Return,” and the digital participant’s guide containing embedded BlockWorks demonstrations. You will need these to effectively deliver the next six hours of training.

Vermont Income Tax Course Instructor’s Guide (2016)

2

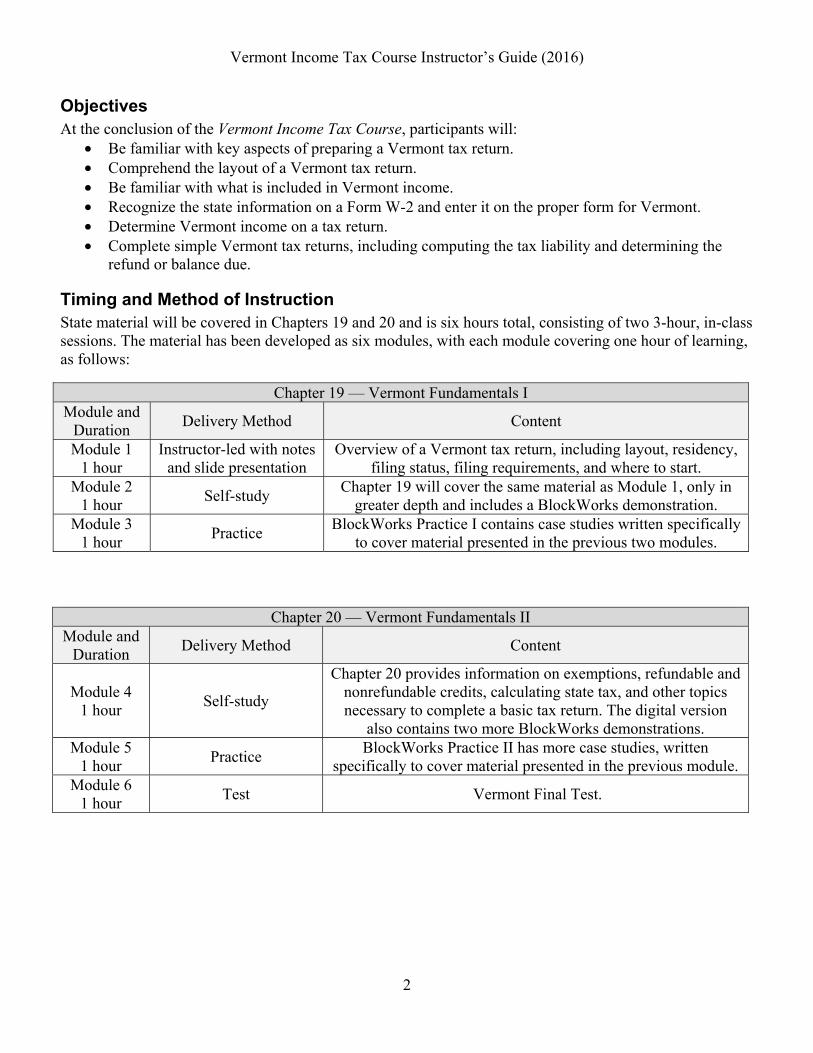

Objectives At the conclusion of the Vermont Income Tax Course, participants will:

• Be familiar with key aspects of preparing a Vermont tax return. • Comprehend the layout of a Vermont tax return. • Be familiar with what is included in Vermont income. • Recognize the state information on a Form W-2 and enter it on the proper form for Vermont. • Determine Vermont income on a tax return. • Complete simple Vermont tax returns, including computing the tax liability and determining the

refund or balance due.

Timing and Method of Instruction State material will be covered in Chapters 19 and 20 and is six hours total, consisting of two 3-hour, in-class sessions. The material has been developed as six modules, with each module covering one hour of learning, as follows:

Chapter 19 — Vermont Fundamentals I Module and

Duration Delivery Method Content

Module 1 1 hour

Instructor-led with notes and slide presentation

Overview of a Vermont tax return, including layout, residency, filing status, filing requirements, and where to start.

Module 2 1 hour

Self-study Chapter 19 will cover the same material as Module 1, only in

greater depth and includes a BlockWorks demonstration. Module 3

1 hour Practice

BlockWorks Practice I contains case studies written specifically to cover material presented in the previous two modules.

Chapter 20 — Vermont Fundamentals II Module and

Duration Delivery Method Content

Module 4 1 hour

Self-study

Chapter 20 provides information on exemptions, refundable and nonrefundable credits, calculating state tax, and other topics necessary to complete a basic tax return. The digital version

also contains two more BlockWorks demonstrations. Module 5

1 hour Practice

BlockWorks Practice II has more case studies, written specifically to cover material presented in the previous module.

Module 6 1 hour

Test Vermont Final Test.

Vermont Income Tax Course Instructor’s Guide (2016)

3

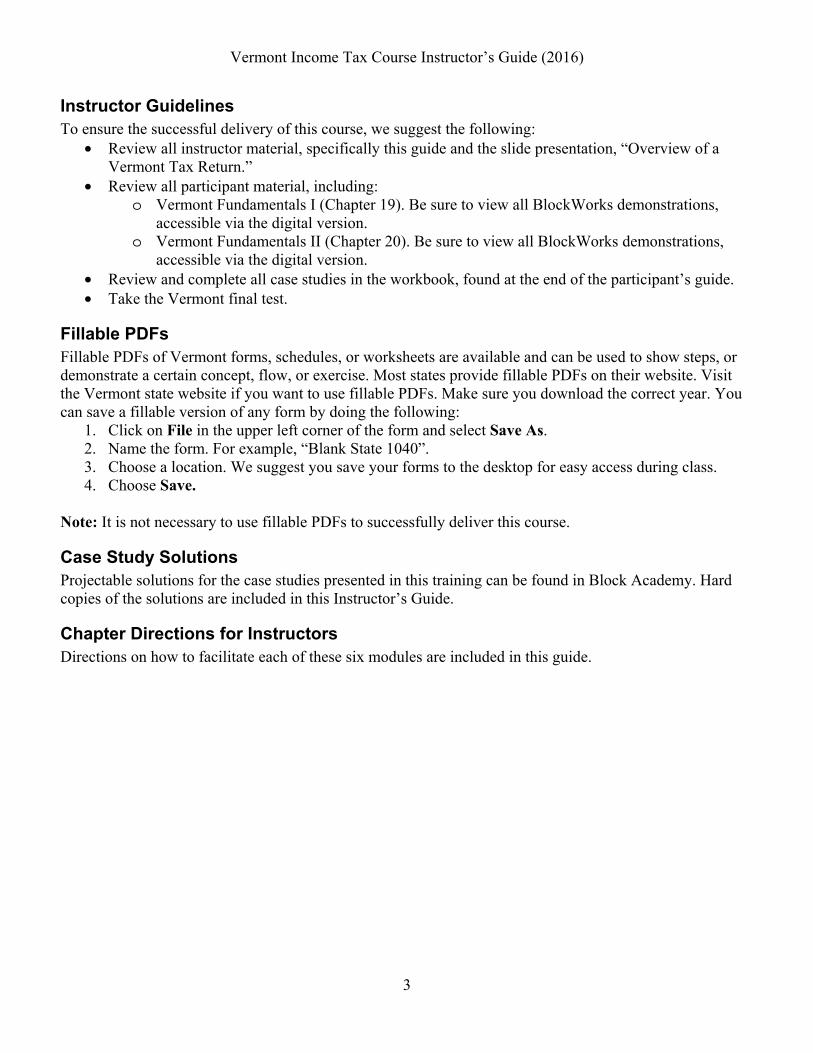

Instructor Guidelines To ensure the successful delivery of this course, we suggest the following:

• Review all instructor material, specifically this guide and the slide presentation, “Overview of a Vermont Tax Return.”

• Review all participant material, including: o Vermont Fundamentals I (Chapter 19). Be sure to view all BlockWorks demonstrations,

accessible via the digital version. o Vermont Fundamentals II (Chapter 20). Be sure to view all BlockWorks demonstrations,

accessible via the digital version. • Review and complete all case studies in the workbook, found at the end of the participant’s guide. • Take the Vermont final test.

Fillable PDFs Fillable PDFs of Vermont forms, schedules, or worksheets are available and can be used to show steps, or demonstrate a certain concept, flow, or exercise. Most states provide fillable PDFs on their website. Visit the Vermont state website if you want to use fillable PDFs. Make sure you download the correct year. You can save a fillable version of any form by doing the following:

1. Click on File in the upper left corner of the form and select Save As. 2. Name the form. For example, “Blank State 1040”. 3. Choose a location. We suggest you save your forms to the desktop for easy access during class. 4. Choose Save.

Note: It is not necessary to use fillable PDFs to successfully deliver this course.

Case Study Solutions Projectable solutions for the case studies presented in this training can be found in Block Academy. Hard copies of the solutions are included in this Instructor’s Guide.

Chapter Directions for Instructors Directions on how to facilitate each of these six modules are included in this guide.

Vermont Income Tax Course Instructor’s Guide (2016)

4

Chapter 19

Vermont Fundamentals I

Hour 1, Instructor-Led

Classroom Supplies • Instructor slide presentation, “Overview of a Vermont Tax Return.”

Objectives At the conclusion of this chapter, participants will be familiar with:

• The course map for the next six hours of classroom instruction. • The learning objectives for the Vermont Income Tax Course. • The basic structure of the Vermont tax return. • How to determine residency, filing requirements, and filing statuses for Vermont taxpayers. • Basic concepts regarding additional adjustments, exclusions, credits, refundable credits, and

payments as they pertain to Vermont.

Instructor Guidelines The following notes are intended to guide a discussion of Vermont income tax preparation in conjunction with the instructor slide presentation, “Overview of a Vermont Tax Return.” To ensure successful delivery of this material, we suggest the following:

• Go through the slide presentation once without reading the notes. • Read through the notes to become familiar with cues to move to the next slide, as well as

suggestions for questions to ask, and discussions to encourage. • Add comments or best practices you need to cover. • Review all Check for Understanding material to ensure you are comfortable reviewing the questions

and discussing the correct answers. • Practice with the slide presentation and the suggested script for the first hour of Chapter 19 to

become familiar with the timing and flow of the material. The students can follow along in Chapter 19; Vermont Fundamentals I. Chapter 19 is available digitally and will be accessed in the next session. Both the printed version and the digital version are designed to provide more in-depth coverage of the material presented in the slide presentation. The digital version also has BlockWorks demonstration videos. Encourage your students to take notes while following along, and be conscious of your time. You only have an hour — spend it wisely! Let’s get started!

Vermont Income Tax Course Instructor’s Guide (2016)

5

Welcome Say: Welcome to Vermont state tax training! We’re going to depart from federal taxes for a bit and focus just on Vermont state taxes and how to prepare them correctly. NEXT SLIDE

Course Map Say: This six-hour course covers Chapters 19 and 20. Each chapter is three modules of one hour each. Chapter 19:

• Hour 1 is instructor-led, and we’ll review some of the key elements in determining whether a Vermont return is required.

• Hour 2 is self-study. You’ll be dismissed to your computer to further review and expand on the topics we’ve discussed.

• Hour 3 is case studies. You’ll spend the rest of today’s session working on one or more state returns in BlockWorks® Professional Tax Software to practice the concepts and input required to complete the Vermont return.

NEXT SLIDE

Chapter 20: • Hour 1 is self-study again. This time, you’ll dive deeper and learn about additional elements that go

into the Vermont return.

• Hour 2 gives you more BlockWorks practice, with case studies designed to allow you to enter those additional elements you might find on a typical Vermont return.

• Hour 3 is your final test for Vermont tax returns. This will consist of a case study entered into BlockWorks, and multiple-choice questions.

Say (transition): Just like the federal ITC materials, this course will prepare you to complete Vermont returns for many of the taxpayers that you might expect to see in the coming season. We will focus on clients who file federal Forms 1040EZ and 1040A only. It is expected that you will be ready to prepare Vermont returns for Vermont full-year residents. You will gain a basic understanding of how to identify returns that will involve part-year residents or nonresidents, but, as with more complex federal returns, clients who are not full-year residents of Vermont should be referred to a more experienced Tax Professional. NEXT SLIDE

Vermont Income Tax Course Instructor’s Guide (2016)

6

Objectives Say: At the end of your six hours of state training, you will:

• Understand how to prepare a basic Vermont resident tax return for a federal Form 1040EZ or Form 1040A taxpayer.

• Know how to complete a basic Vermont resident tax return in BlockWorks.

NEXT SLIDE

Agenda Say: For the next hour, I’m going to give you an overview of some of the key concepts needed to begin preparing Vermont state returns. At the conclusion of this session, you will be familiar with:

• The structure of a Vermont base tax form for residents.

• How to determine a taxpayer’s Vermont residency status.

• The rules that determine whether a taxpayer is required to file a Vermont tax return.

• The filing status requirements and options for a Vermont taxpayer.

• Additional information regarding a Vermont tax return, including any adjustments, exclusions, deductions, credits, refundable credits, and payments.

Say (transition): We’re going to start with Form IN-111 Vermont Income Tax Return, the base form for a resident of Vermont. NEXT SLIDE

Form IN-111 Overview Say: This form is used by residents, part-year residents and nonresidents of Vermont. Say: Let’s take a look at the copy of the form you have in your participant’s guide.

• Page 1 o Page 1 begins with taxpayer’s and spouse’s (if applicable) personal information. This

includes name, SSN, and address information. Also included is a checkbox to indicate if recomputed federal return information is used.

o Next, boxes are provided to indicate if the return being filed is an amended return, if the taxpayer or their spouse/partner died during the year.

o Following is space to enter the filer’s Vermont School District Code and “911 street address”.

o The next section is for tax filing information. Boxes are provided to check the appropriate filing status. The number of exemptions claimed on the federal return is also entered here.

o The next section, titled “Taxable Income”, begins with federal adjusted gross income. The taxpayer’s federal adjusted gross income is entered on line 10 of Form IN-111. Federal taxable income is entered on line 11 of Form IN-111. Boxes are provided to check if the federal AGI or federal taxable income is a loss.

Vermont Income Tax Course Instructor’s Guide (2016)

7

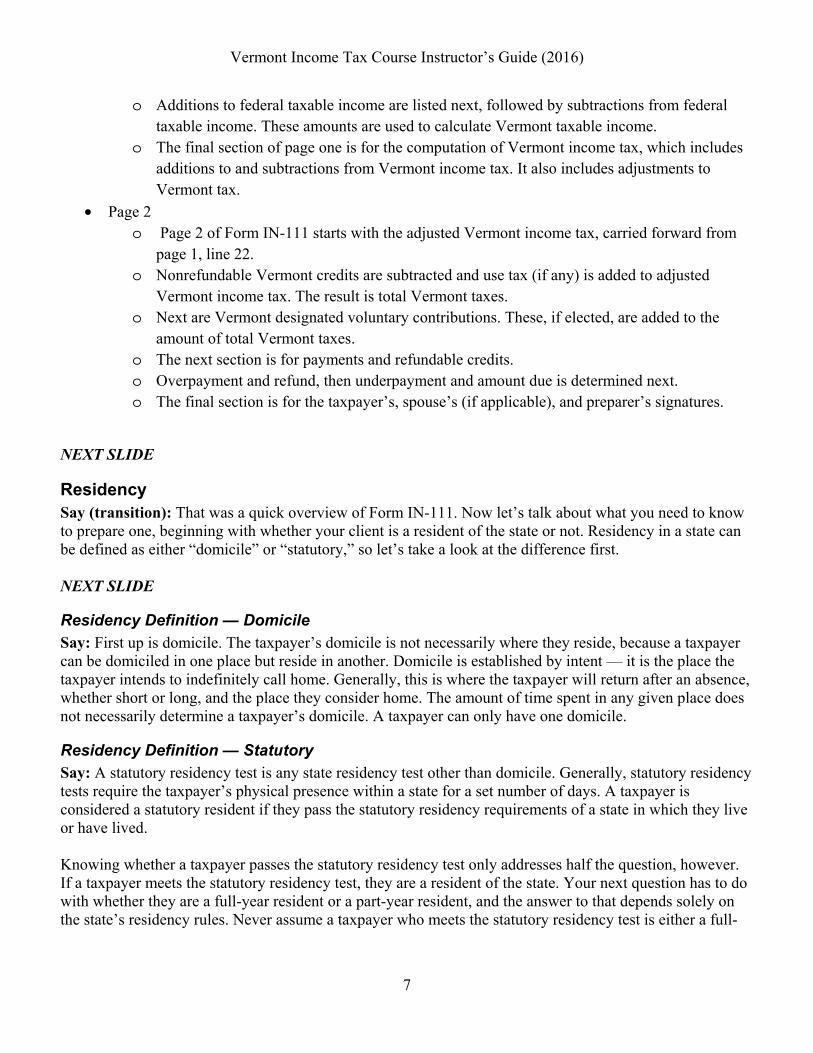

o Additions to federal taxable income are listed next, followed by subtractions from federal taxable income. These amounts are used to calculate Vermont taxable income.

o The final section of page one is for the computation of Vermont income tax, which includes additions to and subtractions from Vermont income tax. It also includes adjustments to Vermont tax.

• Page 2 o Page 2 of Form IN-111 starts with the adjusted Vermont income tax, carried forward from

page 1, line 22. o Nonrefundable Vermont credits are subtracted and use tax (if any) is added to adjusted

Vermont income tax. The result is total Vermont taxes. o Next are Vermont designated voluntary contributions. These, if elected, are added to the

amount of total Vermont taxes. o The next section is for payments and refundable credits. o Overpayment and refund, then underpayment and amount due is determined next. o The final section is for the taxpayer’s, spouse’s (if applicable), and preparer’s signatures.

NEXT SLIDE

Residency Say (transition): That was a quick overview of Form IN-111. Now let’s talk about what you need to know to prepare one, beginning with whether your client is a resident of the state or not. Residency in a state can be defined as either “domicile” or “statutory,” so let’s take a look at the difference first. NEXT SLIDE

Residency Definition — Domicile Say: First up is domicile. The taxpayer’s domicile is not necessarily where they reside, because a taxpayer can be domiciled in one place but reside in another. Domicile is established by intent — it is the place the taxpayer intends to indefinitely call home. Generally, this is where the taxpayer will return after an absence, whether short or long, and the place they consider home. The amount of time spent in any given place does not necessarily determine a taxpayer’s domicile. A taxpayer can only have one domicile.

Residency Definition — Statutory Say: A statutory residency test is any state residency test other than domicile. Generally, statutory residency tests require the taxpayer’s physical presence within a state for a set number of days. A taxpayer is considered a statutory resident if they pass the statutory residency requirements of a state in which they live or have lived. Knowing whether a taxpayer passes the statutory residency test only addresses half the question, however. If a taxpayer meets the statutory residency test, they are a resident of the state. Your next question has to do with whether they are a full-year resident or a part-year resident, and the answer to that depends solely on the state’s residency rules. Never assume a taxpayer who meets the statutory residency test is either a full-

Vermont Income Tax Course Instructor’s Guide (2016)

8

year or part-year resident of any given state. They are simply a resident. Proper understanding and application of Vermont’s residency rules will help you determine whether they are a full-year resident or a part-year resident. A taxpayer can be a statutory resident of one state and be domiciled in another. Vermont statutory residents maintain a permanent home in Vermont, and are present in Vermont for more than 183 days of the taxable year. Say (transition): Now that you are familiar with the difference between domicile and statutory residency, let’s take a look at the rules as they apply to Vermont. NEXT SLIDE

Full-Year Resident Say: A full-year resident of Vermont is domiciled in the state or maintains a permanent place of abode within the state, and is present in the state for more than a total of 183 days of the tax year. Generally, a home (whether inside or outside of Vermont) is not permanent if it is maintained only during a temporary or limited period for the accomplishment of a particular purpose, such as a temporary job assignment. Likewise, a home used only for vacations is not a permanent home. Say: Full-year residents of Vermont complete Form IN-111. Say (transition): Let’s move on. A full discussion of part-year residents and nonresidents is beyond the scope of this course. However, it’s important to understand what the rules are for those residency statuses, so let’s take a look at them now. NEXT SLIDE

Part-Year Resident Say: A part-year resident is a taxpayer who is domiciled in Vermont during only part of the year, for less than 183 days, with the intent of establishing a domicile and residing in the state indefinitely. A part-year resident qualifies for residency in the state for only part of the tax year. Also, a part-year resident is an individual who moves out of Vermont during the year with the intent of establishing a domicile in a new location.

Nonresident Say: A taxpayer is considered a nonresident when they do not qualify for residency in Vermont during any part of the tax year. The nonresident is not domiciled in Vermont, nor maintains a permanent place of abode in Vermont, where the individual is present in the state for more than 183 days of the tax year. Say: Nonresidents of Vermont will file IN-111 and Schedule IN-113, Income Adjustment Calculations, if they meet Vermont filing requirements.

Vermont Income Tax Course Instructor’s Guide (2016)

9

Say: As stated earlier, part-year resident returns and nonresident returns are more complex than resident returns and are beyond the scope of this course. In the event you believe you are helping a taxpayer who qualifies as a part-year resident or a nonresident, refer them to a more experienced Tax Professional for assistance. NEXT SLIDE

Check for Understanding For this exercise, each example is on its own slide. These questions and answers do not appear in the participant’s guide. Confirm that students understand the difference between domicile and statutory residency, if both apply in your state. Using open discussion with the class, determine the residency status of the following individuals: Example 1: Mary considers Vermont home, the place to which she would return after an absence, even a long one. [Resident] Example 2: Jonathan spends more than 183 days in Vermont but doesn’t maintain a permanent home in the state. [Nonresident] Example 3: Ethan is not domiciled in Vermont, but he spends more than 183 days in Vermont and maintains a permanent home in the state. [Resident] Example 4: Jerri has always considered Vermont home and intends to retire there one day. In the meantime, she maintains a permanent home in New Mexico and spends less than 30 days in Vermont visiting family. [Nonresident] Example 5: Louise lived and worked in Vermont until May, when she accepted a job with another company and moved to South Carolina. Louise does not plan to return to Vermont. [Part-year resident] Say (transition): Great discussion and great job on the residency requirements! When it comes to military taxpayers and their spouses, however, different rules apply. Let’s look at those now. NEXT SLIDE

Military Servicemembers Say: If the taxpayer’s home of record (domicile) was Vermont when they entered the service, they will remain a resident of Vermont for income tax purposes, regardless of where they are assigned, unless they submit a notice of intent to change their home of record (domicile) to the military. Say: Alternatively, if their home of record (domicile) was outside of Vermont when they entered the service, they do not become a resident of this state when they’re assigned to a duty station here. They remain a nonresident for income tax purposes. More details, including any special rules for Vermont are included in your participant’s guide.

Vermont Income Tax Course Instructor’s Guide (2016)

10

Say: If the spouse of a nonresident servicemember is also a nonresident of Vermont, they may not have to pay tax on income earned while living and working here. There are specific guidelines regarding this in the Military Spouses Residential Relief Act (MSRRA), which we’ll look at again a bit later. Whether the taxpayer or the spouse qualifies as a nonresident, the result is a more complicated tax return. If you believe you have a taxpayer (and spouse, if applicable) in this situation, you should refer them to a more experienced Tax Professional. NEXT SLIDE

Filing Requirements Say: Now that we know who is a resident and who is not, we need to determine whether they’re required to file a Vermont tax return. NEXT SLIDE

Full-year Residents Say: Full-year residents must report federal adjusted gross income and federal taxable income. Full-year residents are required to file a Vermont IN-111, if they are required to file a federal income tax return and earned or received more than $100 in Vermont income. Say: An active-duty military servicemember whose home of record is Vermont must file a Vermont tax return, even if they were outside of Vermont all year.

Part-Year Residents Say: Part-year residents are required to file a tax return if:

• They were required to file a federal income tax return and, • Earned or received more than $100 in Vermont income. • Earned or received Vermont gross income of more than $1,000 as a nonresident, during the time

they were not a resident.

Nonresidents Say: Nonresidents are required to file a tax return if they are required to file a federal income tax return and

• Earned or received net income of more than $100 in Vermont income. • Earned or received gross income of more than $1,000 as a nonresident.

Say: Active-duty military servicemembers whose home of record is a state other than Vermont are not required to file a Vermont tax return for income earned while stationed in Vermont unless they have received income from Vermont other than military pay. Say (transition): There are a few other things that might determine whether a taxpayer files a Vermont tax return or not. Let’s take a look at those now. NEXT SLIDE

Vermont Income Tax Course Instructor’s Guide (2016)

11

Filing Even When Not Required Say: The taxpayer should also file a return to receive a refund or credit, even if their income is equal to or below the filing threshold, if any of the following are true:

1. The taxpayer has Vermont income tax withheld. 2. The taxpayer paid Vermont estimated taxes. 3. The taxpayer is eligible for a Vermont refundable credit.

NEXT SLIDE

Federal Preemption Say: There are situations in which state laws are overridden by federal laws. These federal laws generally prevent state taxation of certain types of income. There are three main situations where this occurs; however, this list is not exhaustive.

• Nonresident retirement.

• Military Spouses Residency Relief Act (MSRRA).

• Railroad retirement benefits.

Say: Because these federal preemptions might reduce the amount of income taxable to Vermont, they can also affect whether the taxpayer is required to file a Vermont tax return, so let’s take a closer look at each of them.

NEXT SLIDE

Nonresident Retirement Say: As this has to do with nonresident income, this is presented for your awareness only. Say: For nonresidents of Vermont, retirement income, pension income, and annuity income are not subject to Vermont income tax, regardless of where the taxpayer worked in prior years to earn the pension. For example, a full-year Indiana resident who spends three months of the year in Vermont and the remainder in Indiana, and who receives a pension, is not liable for Vermont income tax on that income. The same is true of anyone who worked to earn their pension in Vermont but is now a resident elsewhere, as they are now considered a nonresident of Vermont.

Military Spouses Residency Relief Act (MSRRA) Say: The MSRRA allows military spouses, under specified conditions, to maintain one “state of domicile” for the purposes of residency, voting, and taxation. A military spouse is exempt from paying state income taxes in the state in which they are working if they are covered under the MSRRA. Say: This information is presented for your awareness only. If you have a taxpayer who you believe qualifies for the MSRRA, refer them to a more experienced Tax Professional.

Vermont Income Tax Course Instructor’s Guide (2016)

12

Railroad Retirement Benefits Say: Railroad retirement benefits paid by the Railroad Retirement Board will not be subject to state tax. Thus, any time there is a possibility that these benefits are included in an amount brought from the federal return (such as federal adjusted gross income), they must be subtracted. If the state tax return doesn’t begin with any figure from the federal return, railroad retirement benefits will not be added, nor will they be taxed in any way, on the state return. Say (transition): We’re going to move to filing statuses next, but first, does anyone have any questions regarding filing requirements? Discuss and answer questions before moving on. NEXT SLIDE

Filing Status Say: Vermont filing status is, in general, the same as the filing status used on the federal income tax return. There are two exceptions, discussed later. NEXT SLIDE Say: Vermont filing statuses are:

• Single. • Head of household. • Married filing jointly. • CU (Civil Union) partner filing jointly. • Qualifying widow(er) with dependent children. • Married filing separately. • CU (Civil Union) partner filing separately.

NEXT SLIDE Say: There are situations where the federal tax information may be required to be recomputed for Vermont purposes:

• Civil Union – status available to same sex couples that have a valid civil union certificate. • Vermont Resident with a non-Vermont resident spouse who has no Vermont income – If they elect

to file married filing jointly, MFJ, Schedule IN-113 cannot be used to apportion income of the nonresident spouse. (See Vermont Technical Bulletin 55).

Say: Federal tax information is required to be recomputed for Vermont purposes when:

• Civil union filing jointly – must recompute both partner’s federal returns as if it was a married filing jointly return.

• Civil union filing separately – must recompute two (2) federal returns as if they were married filing separate returns.

• Taxpayer with a nonresident spouse who has no Vermont income and who elects to file MFS, for Vermont purposes, must recompute their federal return as two MFS returns.

Vermont Income Tax Course Instructor’s Guide (2016)

13

Check the box in the “taxpayer information” section of Form IN-111 and attach the recomputed returns to Form IN-111. Also attach the original federal return. NEXT SLIDE

Standard Deduction or Itemized Deductions Say: Vermont starts with federal taxable income from the federal tax return. If applicable, Vermont starts with the amount from the recomputed federal return. Adjusted gross income from the federal return is entered on Form IN-111, line 10. The federal taxable income or recomputed amount is entered on Form IN-111, line 11. Since the Vermont income tax return begins with federal taxable income, taxpayers do not have separate standard or itemized deductions. Deductions and exemptions are claimed on the federal income tax return. No additional amounts are claimed on the Vermont return. NEXT SLIDE

Exemptions Say: The number of exemptions claimed on the federal return (or recomputed federal return) is entered on Form IN-111, line 9. NEXT SLIDE

Check for Understanding Say: We’ve covered quite a lot already, so let’s see what you remember.

• A resident of Vermont who meets the filing requirements or is claiming a refund will file their tax return on what form? [IN-111]

• What is the definition of domicile? [It is the place the taxpayer intends to indefinitely call home; generally where the taxpayer will return after an absence, whether short or long; the place they consider home.]

• What is the definition of the statutory residency test? [Any residency test other than domicile. Generally, statutory residency tests require the taxpayer’s physical presence within a state for a set number of days.]

• What is the income threshold for a taxpayer filing married filing joint? [$100 Vermont income or $1,000 gross income.] Single? [$100 of Vermont income or $1,000 gross income]

• If an individual’s income is over the threshold and they’re claimed as a dependent on someone else’s return, are they required to file a tax return? [Same as federal; yes, if earned and unearned income exceeds certain levels]

• What is the standard deduction for a couple filing married filing joint? [Vermont does not have a standard deduction. The federal standard deduction for a couple MFJ is $12,600.]

Vermont Income Tax Course Instructor’s Guide (2016)

14

• What is the personal exemption amount? [Vermont does not have a personal exemption amount. The federal personal exemption is $4,000 each for the taxpayer and spouse]. What about a taxpayer over 65? [Federal, $4,000] Blind? [Federal, $4,000]

Whew! All of this will be recapped in your self-study session coming up when we’re done here. NEXT SLIDE Say (transition): The rest of the hour will be spent quickly covering the rest of the Vermont return. You’ll get more information in your self-study session, and you’ll have an opportunity to practice in BlockWorks using case studies specifically written for this class.

Vermont defined income Say: Vermont statutes state that the income of a resident individual is the individual’s adjusted gross income for the taxable year, less the following (to the extent the income is included in federal AGI):

• Income exempt from state tax under U.S. laws. • Military pay for full-time active duty with U.S. Armed Services earned outside of Vermont.

o Additionally, the first $2,000 of military pay for unit training in the state (National Guard and U.S. Reserve personnel).

• Funds received through federal Armed Forces Educational Loan Repayment Program. • Amount paid by Vermont to a family for the support of an eligible person with a developmental

disability, to the extent the amount is included in federal AGI. • Other amounts paid by Vermont, to the extent the amounts are included in the federal AGI.

Say: The determination of Vermont taxable income starts with federal taxable income from the federal income tax return. If the individual is claiming a Vermont filing status different from the one claimed on their federal return (discussed above), use the taxable income amount from the recomputed federal return. NEXT SLIDE

Additions Say: Vermont additions to federal taxable income include some items that will not apply to federal 1040A or 1040EZ filers. Vermont additions include:

• Income from non-Vermont state and local obligations, Schedule IN-112, VT Tax Adjustments and Credits.

• Bonus depreciation allowed under federal law. • Addback of state and local income taxes, Schedule IN-155, Federal Itemized Deductions Addback. • Addback of itemized deductions, Schedule IN-155, Federal Itemized Deductions Addback.

The sum of federal taxable income with additions is entered on line 13. If this result is a loss (a negative number), enter the amount on line 13, on IN-111, and check the box provided to indicate loss. NEXT SLIDE

Vermont Income Tax Course Instructor’s Guide (2016)

15

Subtractions Say: Vermont subtractions from federal taxable income include:

• Interest income from U.S. obligations. • Capital gains exclusion, Schedule IN-153, Capital Gain Exclusion Calculation. • Adjustment for prior years’ bonus depreciation.

Total subtractions are summed and entered on line 14d. Vermont taxable income is calculated as follows, and is entered on line 15:

• Federal taxable income with additions, (line 13). • Less total subtractions, (line14d).

NEXT SLIDE

Taxes Say: Taxpayers with Vermont taxable income of:

• $75,000 or less, use VT Tax Tables to calculate tax, based on income, and filing status. • More than $75,000, use the VT Tax Rate Schedule to calculate tax.

There are adjustments to Vermont income tax from, Schedule IN-112 VT Tax Adjustments and Credits, and Schedule IN-113, Income Adjustment Calculations. After appropriate adjustments are applied, the adjusted Vermont income tax is entered on line 22. Say: Vermont income tax on Vermont taxable income is subject to the following, effective January 1, 2015: Taxpayers with federal AGI greater than $150,000 must pay a minimum Vermont tax of 3% of their federal AGI (less interest from U.S. obligations).

• Vermont income tax is the higher of either: 1. 3% of federal AGI (less interest from U.S. obligations). 2. Tax calculated using the applicable tax table or schedule.

NEXT SLIDE

Nonrefundable Credits Say: Vermont nonrefundable credits are subtracted from the adjusted Vermont income tax amount carried forward from line 22. Nonrefundable Vermont credits include:

• Credit for Income Tax Paid to Another State or Canadian Province, Schedule IN-117. • Vermont tax credits, Schedule IN-112, VT Tax Adjustments and Credits, or Schedule IN-119, VT

Economic Incentive Income Tax Credits. • Total nonrefundable Vermont credits are summed on line 25. This amount is subtracted from the

adjusted Vermont income tax, reducing the Vermont income tax liability. Next, use tax (if any) is added. The result, total Vermont taxes is entered on line 28. NEXT SLIDE

Vermont Income Tax Course Instructor’s Guide (2016)

16

Voluntary Contributions Say: The total of Vermont taxes and voluntary contributions is summed and entered on line 30. Designated Vermont voluntary contributions that may be elected by the taxpayer include:

• Nongame Wildlife Fund. • Children’s Trust Fund. • Vermont Veterans’ Fund • Green Up Vermont.

Things to Remember About Voluntary Designated Contributions in Vermont • The amount of voluntary contributions elected by the taxpayer is added to the total Vermont tax

liability.

• In effect, if the contribution is made on a return with a refund, the refund amount will be reduced by the amount of the contribution.

• In effect, if the contribution is made on a return with a balance due, the amount will be added to the balance due, increasing the amount to be remitted with the return.

• The taxpayer should not send a separate check for the charity with their balance-due tax return. Checks should be made out to the taxing authority as outlined in the instructions. The state will forward the funds to the specified charity. The taxpayer may, of course, write a separate check and mail it directly to the charity.

• Contributions are generally tax-deductible in the year following the year of contribution.

NEXT SLIDE

Payments and Refundable Credits Say: Vermont income tax payments and refundable credits are summed, and the total amount is entered on line 31h, total payments and credits. Sources of Vermont income tax payments include:

• Vermont income tax withheld from Forms W-2, 1099 and other information documents. • Vermont estimated tax payments, refund amounts applied from a prior year, and any extension

payments made. Vermont refundable credits include, but are not limited to, amounts carried from various Vermont forms and schedules, such as:

• Earned Income Tax Credit, Schedule IN-112. • Renter Rebate, Form PR-141. • Vermont real estate withholding, Form RW-171. • Low Income Child and Dependent Care Credit.

Any overpayment of tax is entered on line 32. The amount of tax underpaid, if any, is entered on line 35. NEXT SLIDE

Vermont Income Tax Course Instructor’s Guide (2016)

17

Questions Say: This concludes the instructor-led part of your state training. Are there any questions before we move forward? NEXT SLIDE

What’s Next? Say: Here we have the course map again. As you can see, we have completed Module 1 of Chapter 19. Next is a self-study portion that will review and expand on these topics. This will take you approximately one hour. Take your time and read the materials carefully. View all of the embedded videos, as they will further clarify some of what you’re reading, as well as provide BlockWorks demonstrations designed to help you with your case studies. Remember that your participant’s guide will be a primary resource for you as you take your test, so use it to take plenty of notes. Feel free to let me know if you have questions on anything you read. When you have completed the self-study portion, you will move on to the case studies included in your book.

Vermont Income Tax Course Instructor’s Guide (2016)

18

Hour 2, Self-Study

Classroom Supplies • The digital version of Vermont Income Tax Course can be found in Block Academy. • Ear buds for each student. • Computers (ideal ratio of 1:1).

Objectives At the conclusion of this chapter, participants will be able to:

• Accurately define Vermont residency, filing requirements, and filing statuses. • Explain where to find Vermont forms in BlockWorks.

Instructor Focus Explain that this chapter is completed at the computer. Demonstrate how to find and open the digital version of Vermont Income Tax Course. Inform the students that there are BlockWorks demonstration videos embedded in the material. Remind the students that this material is included in their printed participant’s guide (Chapter 19) and should be used for reference and notes. Assist students, as needed, to get them started. Be available if any student has questions.

Closing At the end of the hour, request students close the digital version of Vermont Income Tax Course and move on to BlockWorks Practice I.

Vermont Income Tax Course Instructor’s Guide (2016)

19

Hour 3, BlockWorks Practice I

Classroom Supplies Access to BlockWorks.

Objectives At the conclusion of this chapter, participants will be able to complete simple Vermont returns in BlockWorks. Note: Due to the complexity and variety of local taxes, this course does not attempt to address them. All case studies and solutions are based on state tax only.

Instructor Focus Explain that this hour will be devoted to BlockWorks practice. Demonstrate how to open a shell return in BlockWorks. Remind the students to write down the new social security number assigned to the case study. Inform the students that the case studies can be found in their workbook. They will complete case studies 1 – 3 only in this session. Remind students they should clear any critical (red) diagnostics and review all other diagnostics before considering their return complete. Note: All shell returns have been entered as paper returns. To eliminate most of the critical (red) diagnostics, students should change the state return to paper as well. Assist students, as needed, to get them started. Be available if any student has questions. Stay alert for common issues and, if necessary, address them to the class as a whole.

Closing Provide the solutions for the case studies (included in this guide at the end of this chapter). Ask if there are any questions. Inform the participants that there is no assigned homework, but encourage them to visit the Vermont website and review Chapter 20 in their participant’s guide. Challenge them to complete their case studies on paper for additional practice. Tax tables (if required) can be found at the end of Chapter 20.

Vermont Income Tax Course Instructor’s Guide (2016)

20

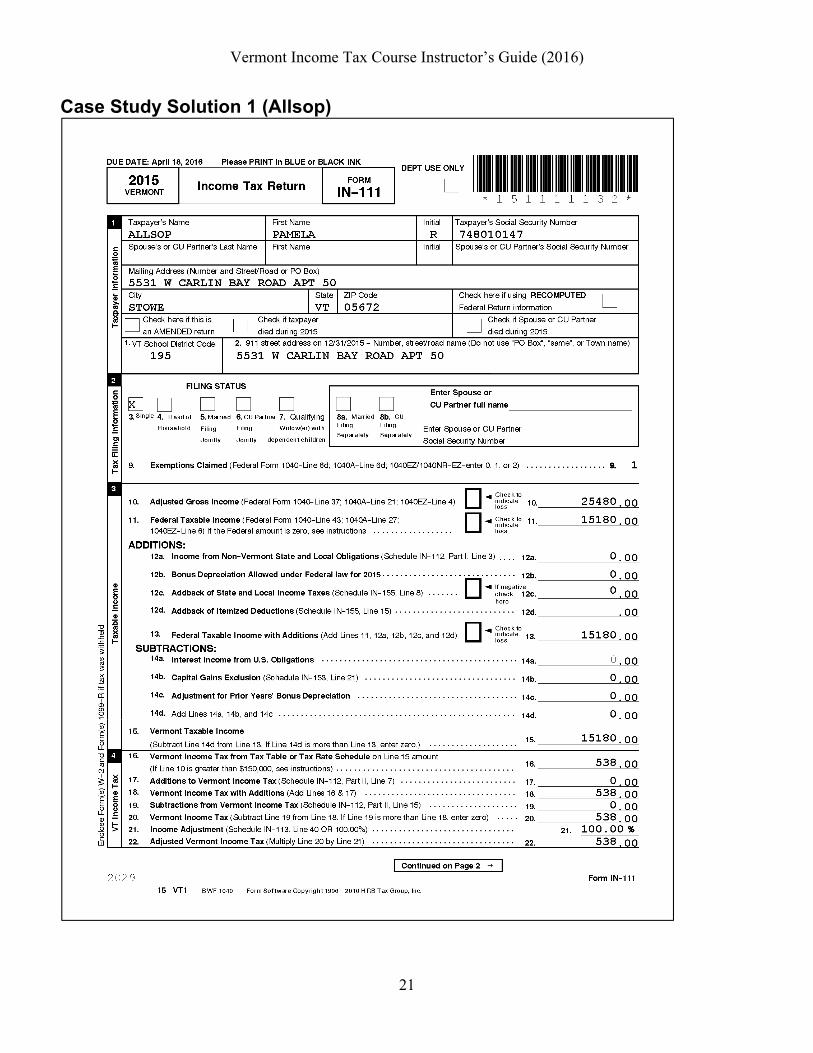

Case Study Solution 1 (Allsop)

Vermont Income Tax Course Instructor’s Guide (2016)

21

Case Study Solution 1 (Allsop)

Vermont Income Tax Course Instructor’s Guide (2016)

22

Case Study Solution 1 (Allsop)

Vermont Income Tax Course Instructor’s Guide (2016)

23

Case Study Solution 1 (Allsop)

Vermont Income Tax Course Instructor’s Guide (2016)

24

Case Study Solution 1 (Allsop)

1. Is Pamela required to file a federal income tax return? If she is not required to file, is there any benefit for her to file anyway? Yes, the federal return is required because the income exceeds the filing requirement threshold.

2. If Pamela is not required to file a federal return, is she required to file a Vermont return? If she is not required to file, is there any benefit for her to file anyway? Yes, because the federal return is required, this means that the Vermont return is also required.

3. Review Form IN-111. Read the header information. Be sure that your School District Code appears. Notice that the choices for filing status are different than for the federal return. On line 9 should be the number of exemptions claimed on the federal return. Are there differences in the filing status options versus the federal filing statuses? Yes, there are also statuses for CU Partner Filing Jointly and CU Filing Separately.

4. What is on line 10? $25,480, which is her federal AGI. What is on line 11? $15,180, which is her federal taxable income. How did the information on these two lines flow to the VT IN-111? These flow automatically in BlockWorks from the federal return that must be prepared thoroughly before starting the Vermont return, so that all of the applicable information will flow to the state return. Are there any amounts on line 12 or 14? No. She has no additions to or subtractions from federal taxable income. What is on line 15? $15,180, her Vermont taxable income. What is on line 16? $538, the amount of her Vermont income tax, taken from the Tax Table. Review the Tax Table at the end of Chapter 20 to validate the calculated amount of the tax. Is there an amount on line 17 or 19? No, there are not amounts here because Pamela does not have any additions to or subtractions from Vermont income tax. What is on line 25? Zero. Pamela has no Vermont tax credits. What is on line 28? $538, Total Vermont Taxes. What is on line 29? Pamela is making a voluntary contribution of $15. What is on line 30? $553, the amount of the contribution added to the amount of the Vermont tax. What is on line 31a? $806, the amount of Pamela’s Vermont Tax Withheld. How did this information flow to the VT IN-111? This flows automatically through BlockWorks from the input into the federal W2 screen. This is the amount from box 17. What is on lines 32 and line 34? $253. This is the amount of the Overpayment on line 32, which is the same as what is on line 34 for the Refund Amount.

5. Return to input. Change the amount of Pamela’s contribution to $300. Preview the return. How does this change Pamela’s return? Now, the $300 is added to the Total Vermont Taxes amount of $538, resulting in the Total of Vermont Taxes and Voluntary Contributions to now be $838 on line 30. When we compare this to Pamela’s Vermont tax withheld, she now has a balance due.

6. What is Pamela’s refund or balance due for Vermont? A balance due of $32.

Vermont Income Tax Course Instructor’s Guide (2016)

25

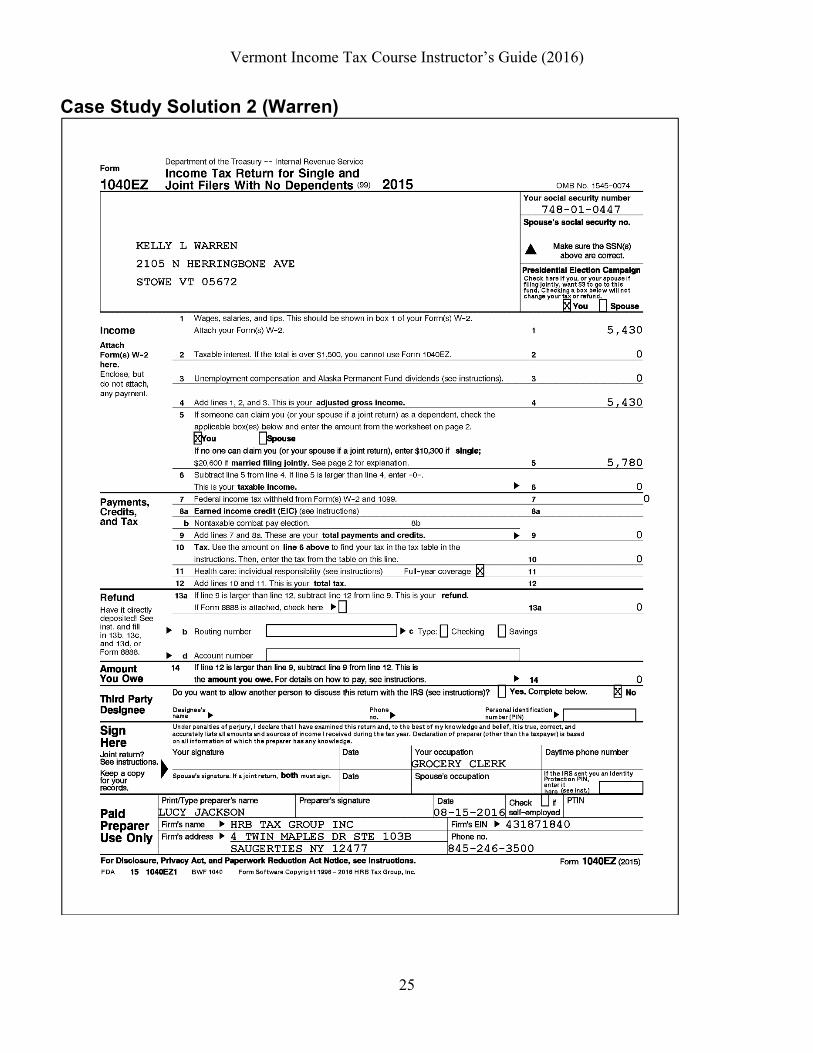

Case Study Solution 2 (Warren)

Vermont Income Tax Course Instructor’s Guide (2016)

26

Case Study Solution 2 (Warren)

Vermont Income Tax Course Instructor’s Guide (2016)

27

Case Study Solution 2 (Warren)

Vermont Income Tax Course Instructor’s Guide (2016)

28

Case Study Solution 2 (Warren)

1. Is Kelly required to file a federal income tax return? If she is not required to file, is there any benefit for her to file anyway? No, the federal return is not required because the income is less than the filing requirement threshold for a dependent. Since she has had no federal withholding, there is no benefit for her to file a federal tax return.

2. If Kelly is NOT required to file a federal return, is she required to file a Vermont return? If she is not required to file, is there any benefit for her to file anyway? No, because the federal return is not required, this means that the Vermont return is not required. However, because she had Vermont withholding she will want to file in order to get a refund of the taxes withheld.

3. Review Form IN-111. Read the header information. Be sure that your School District Code appears. Notice that the choices for filing status are different than for the federal return. On line 9 should be the number of exemptions claimed on the federal return. Are there difference in the filing status options versus the federal filing statuses? Yes, there are also statuses for CU Partner Filing Jointly and CU Filing Separately.

4. What is on line 10? $5,430, which is her federal AGI. What is on line 11? Zero, because she had no federal taxable income. How did the information on these two lines flow to the VT IN-111? These flow automatically in BlockWorks from the federal return that must be prepared thoroughly before starting the Vermont return, so that all of the applicable information will flow to the state return. Are there any amounts on line 12? The rest of her return is all zeros until we get to line 29. What is on line 29? $30 for the voluntary contribution. What is on line 30? $30, Total of Vermont Taxes and Voluntary Contributions. What is on line 31a? $164, the amount of the Vermont Tax Withheld. How did this information flow to the VT IN-111? This flows automatically from the federal W2 input screen. What is on lines 32 and line 34? On line 34 is $134. Since the $30 contribution was subtracted from the tax withheld, this is the remaining amount of her overpayment.

5. Is Kelly eligible for the Lifeline credit? No, because she is a dependent.

6. Why wasn’t Form 1098-T entered on Kelly’s tax return? Since her parents are claiming her, and they paid her education expenses, they will be taking the education credits on their return.

7. What is Kelly’s refund or balance due for Vermont? A refund of $134.

Vermont Income Tax Course Instructor’s Guide (2016)

29

Case Study Solution 3 (Andrews)

Vermont Income Tax Course Instructor’s Guide (2016)

30

Case Study Solution 3 (Andrews)

Vermont Income Tax Course Instructor’s Guide (2016)

31

Case Study Solution 3 (Andrews)

Vermont Income Tax Course Instructor’s Guide (2016)

32

Case Study Solution 3 (Andrews)

Vermont Income Tax Course Instructor’s Guide (2016)

33

Case Study Solution 3 (Andrews)

Vermont Income Tax Course Instructor’s Guide (2016)

34

Case Study Solution 3 (Andrews)

1. Are the Andrewses required to file a federal income tax return? If they are not required to file, is there any benefit for them to file anyway? Yes, the federal return is required because the income exceeds the filing requirement threshold.

2. If they are NOT required to file a federal return, are they required to file a Vermont return? If they are not required to file, is there any benefit for them to file anyway? Yes, because the federal return is required, the Vermont return is also required.

3. Review Form IN-111. Read the header information. Be sure that your School District Code appears. Notice that the choices for filing status are different than for the federal return. On line 9, should be the number of exemptions claimed on the federal return. Are there differences in the filing status options versus the federal filing statuses? Yes, there are also statuses for CU Partner Filing Jointly and CU Filing Separately.

4. What is on line 10? $33,360, which is their federal AGI. What is on line 11? $12,760, which is their Federal Taxable Income. How did the information on these two lines flow to the VT IN-111? These flow automatically in BlockWorks from the federal return that must be prepared thoroughly before starting the Vermont return, so that all of the applicable information will flow to the state return. Are there any amounts on line 12? Yes, $300, which is the amount of the munibond interest for the New York bonds. Since this munibond interest is not taxable for federal, this must be added to federal taxable income for Vermont tax purposes. Are there any amounts on line 14? Yes, $18. This is the amount of the U.S. savings bond interest that is included in federal taxable income, but may not be taxed by Vermont, and therefore this amount must be subtracted from federal taxable income. What is on line 15? $13,042 is the amount of Vermont Taxable Income. This is the result of taking the federal taxable income and then adding and subtracting the appropriate amounts. What other form or forms have been added to this return? VT IN-112 Pg 1 and Pg 2. Review this form. This form contains a considerable amount of information that can affect the Vermont return. Study it and become familiar with what is included on this form. Return to VT IN-111 Pg 1. What is on line 16? $463, Vermont Income Tax. This is taken from the Tax Tables. The Tax Tables are located at the end of Chapter 20. Verify the tax amount for the Andrewses on the table. Is there an amount on line 17 or 19? No, there are no additions to or subtractions from Vermont tax. What is on line 25? Zero. The Andrewses do not have any Vermont Credits. What is on line 28? $463, the Total Vermont Taxes. What is on line 29? The Andrewses have not opted to make a voluntary contribution. What is on line 30? Total of Vermont Taxes and Voluntary Contributions is $463. What is on line 31a? $1,181, Vermont Tax Withheld. How did this information flow to the VT IN-111? This flows automatically in BlockWorks from the entries made in the federal W2 input screen. This amount comes from box 17. What is on lines 32 and 34? $718 is the amount of the Overpayment on line 32. This is the same as the refund amount on line 34.

Vermont Income Tax Course Instructor’s Guide (2016)

35

5. Return to input and select the 1099-INT. Change the munibond allocation to 100% Vermont. Preview the return. What has changed? There is no longer $300 on line 12 for additions to federal taxable income. Since the munibond interest is now from Vermont bonds, this income will not be taxable to Vermont. This changes the calculations of Vermont taxable income and Vermont tax.

6. What is the Andrewses’ refund or balance due for Vermont? A refund of $728.

Vermont Income Tax Course Instructor’s Guide (2016)

36

Chapter 20

Vermont Fundamentals II

Hour 1, Self-Study

Classroom Supplies • The digital version of Vermont Income Tax Course can be found in Block Academy. • Ear buds for each student. • Computers (ideal ratio of 1:1).

Objectives At the conclusion of this chapter, participants will be able to:

• Identify various adjustments, exclusions, deductions, and credits particular to Vermont. • Find and complete various Vermont forms in BlockWorks.

Instructor Focus Explain that this chapter is completed at the computer. Demonstrate how to find and open the digital version of Vermont Income Tax Course. Inform the students that there are BlockWorks demonstration videos embedded in the material. Remind the students that this material is included in their printed participant’s guide (Chapter 20) and should be used for reference and notes. Assist students, as needed, to get them started. Be available if any student has questions.

Closing At the end of the hour, request students close the digital version of Vermont Income Tax Course and move on to BlockWorks Practice II.

Vermont Income Tax Course Instructor’s Guide (2016)

37

Hour 2, BlockWorks Practice II

Classroom Supplies Access to BlockWorks.

Objectives At the conclusion of this chapter, participants will be able to find and complete more forms common to basic Vermont returns in BlockWorks. Note: Due to the complexity and variety of local taxes, this course does not attempt to address them. All case studies and solutions are based on state tax only.

Instructor Focus Explain that this hour will be devoted to BlockWorks practice. Demonstrate how to open a shell return in BlockWorks. Remind the students to write down the new social security number assigned to the case study. Inform the students that the case studies can be found in their workbook. They will complete case studies 4 – 6 in this session. Remind students they should clear any critical (red) diagnostics and review all other diagnostics before considering their return complete. Note: All shell returns have been entered as paper returns. To eliminate most of the critical (red) diagnostics, students should change the state return to paper as well. Assist students, as needed, to get them started. Be available if any student has questions. Stay alert for common issues and, if necessary, address them to the class as a whole.

Closing Provide the solutions for the case studies (included in this guide at the end of this chapter). Ask if there are any questions thus far. Inform the participants that their final test is next. Encourage them to continue to visit the Vermont website and review their participant’s guide and any notes they have. Challenge them to complete their case studies on paper for additional practice. Tax tables (if required) can be found at the end of Chapter 20.

Vermont Income Tax Course Instructor’s Guide (2016)

38

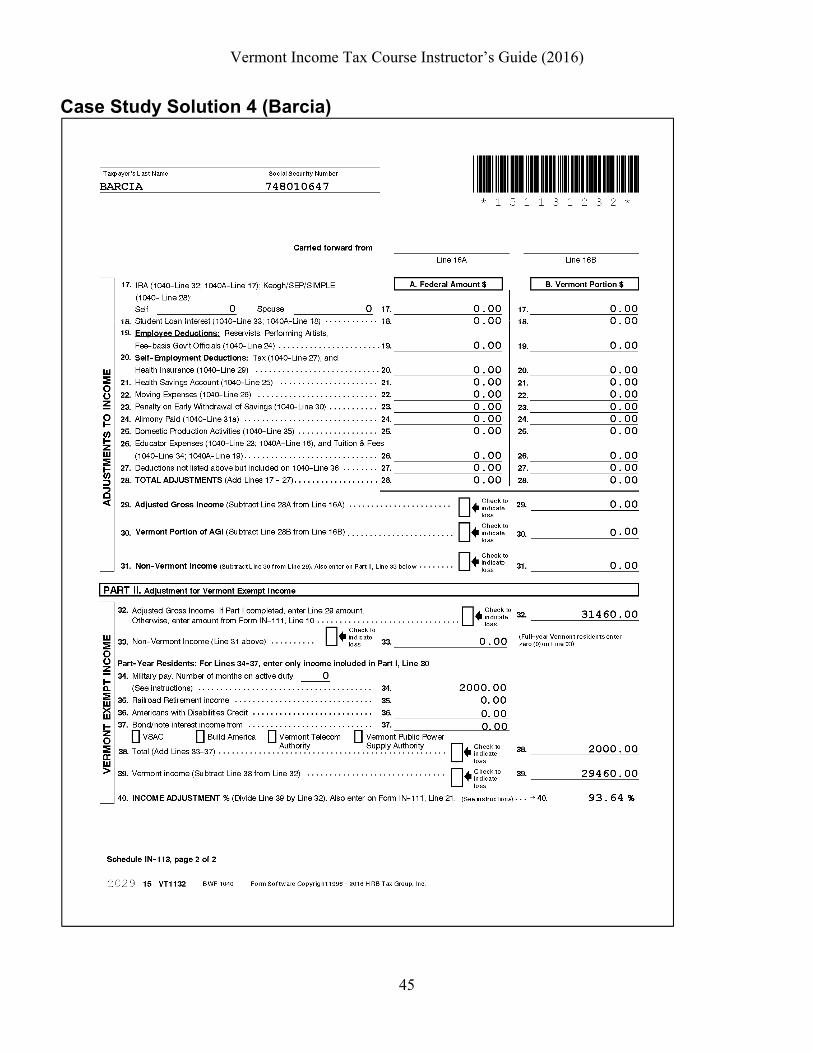

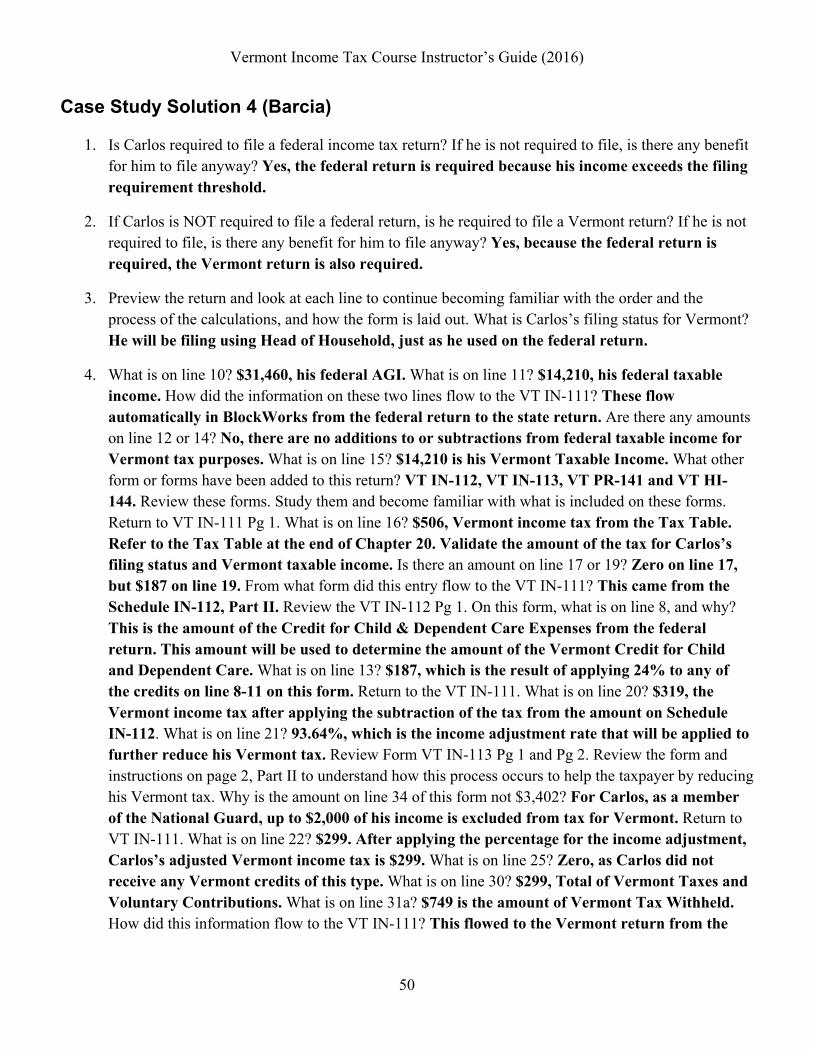

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

39

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

40

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

41

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

42

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

43

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

44

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

45

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

46

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

47

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

48

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

49

Case Study Solution 4 (Barcia)

Vermont Income Tax Course Instructor’s Guide (2016)

50

Case Study Solution 4 (Barcia)

1. Is Carlos required to file a federal income tax return? If he is not required to file, is there any benefit for him to file anyway? Yes, the federal return is required because his income exceeds the filing requirement threshold.

2. If Carlos is NOT required to file a federal return, is he required to file a Vermont return? If he is not required to file, is there any benefit for him to file anyway? Yes, because the federal return is required, the Vermont return is also required.

3. Preview the return and look at each line to continue becoming familiar with the order and the process of the calculations, and how the form is laid out. What is Carlos’s filing status for Vermont? He will be filing using Head of Household, just as he used on the federal return.

4. What is on line 10? $31,460, his federal AGI. What is on line 11? $14,210, his federal taxable income. How did the information on these two lines flow to the VT IN-111? These flow automatically in BlockWorks from the federal return to the state return. Are there any amounts on line 12 or 14? No, there are no additions to or subtractions from federal taxable income for Vermont tax purposes. What is on line 15? $14,210 is his Vermont Taxable Income. What other form or forms have been added to this return? VT IN-112, VT IN-113, VT PR-141 and VT HI-144. Review these forms. Study them and become familiar with what is included on these forms. Return to VT IN-111 Pg 1. What is on line 16? $506, Vermont income tax from the Tax Table. Refer to the Tax Table at the end of Chapter 20. Validate the amount of the tax for Carlos’s filing status and Vermont taxable income. Is there an amount on line 17 or 19? Zero on line 17, but $187 on line 19. From what form did this entry flow to the VT IN-111? This came from the Schedule IN-112, Part II. Review the VT IN-112 Pg 1. On this form, what is on line 8, and why? This is the amount of the Credit for Child & Dependent Care Expenses from the federal return. This amount will be used to determine the amount of the Vermont Credit for Child and Dependent Care. What is on line 13? $187, which is the result of applying 24% to any of the credits on line 8-11 on this form. Return to the VT IN-111. What is on line 20? $319, the Vermont income tax after applying the subtraction of the tax from the amount on Schedule IN-112. What is on line 21? 93.64%, which is the income adjustment rate that will be applied to further reduce his Vermont tax. Review Form VT IN-113 Pg 1 and Pg 2. Review the form and instructions on page 2, Part II to understand how this process occurs to help the taxpayer by reducing his Vermont tax. Why is the amount on line 34 of this form not $3,402? For Carlos, as a member of the National Guard, up to $2,000 of his income is excluded from tax for Vermont. Return to VT IN-111. What is on line 22? $299. After applying the percentage for the income adjustment, Carlos’s adjusted Vermont income tax is $299. What is on line 25? Zero, as Carlos did not receive any Vermont credits of this type. What is on line 30? $299, Total of Vermont Taxes and Voluntary Contributions. What is on line 31a? $749 is the amount of Vermont Tax Withheld. How did this information flow to the VT IN-111? This flowed to the Vermont return from the

Vermont Income Tax Course Instructor’s Guide (2016)

51

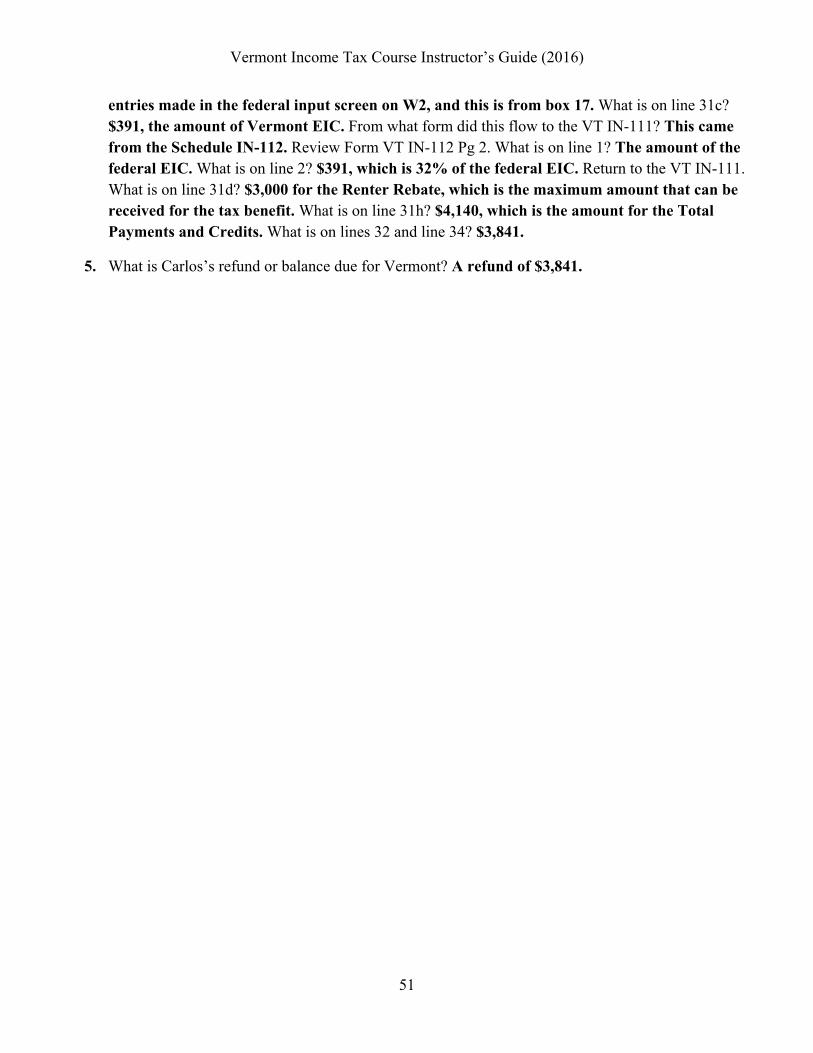

entries made in the federal input screen on W2, and this is from box 17. What is on line 31c? $391, the amount of Vermont EIC. From what form did this flow to the VT IN-111? This came from the Schedule IN-112. Review Form VT IN-112 Pg 2. What is on line 1? The amount of the federal EIC. What is on line 2? $391, which is 32% of the federal EIC. Return to the VT IN-111. What is on line 31d? $3,000 for the Renter Rebate, which is the maximum amount that can be received for the tax benefit. What is on line 31h? $4,140, which is the amount for the Total Payments and Credits. What is on lines 32 and line 34? $3,841.

5. What is Carlos’s refund or balance due for Vermont? A refund of $3,841.

Vermont Income Tax Course Instructor’s Guide (2016)

52

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

53

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

54

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

55

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

56

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

57

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

58

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

59

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

60

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

61

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

62

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

63

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

64

Case Study Solution 5 (Granger)

Vermont Income Tax Course Instructor’s Guide (2016)

65

Case Study Solution 5 (Granger)

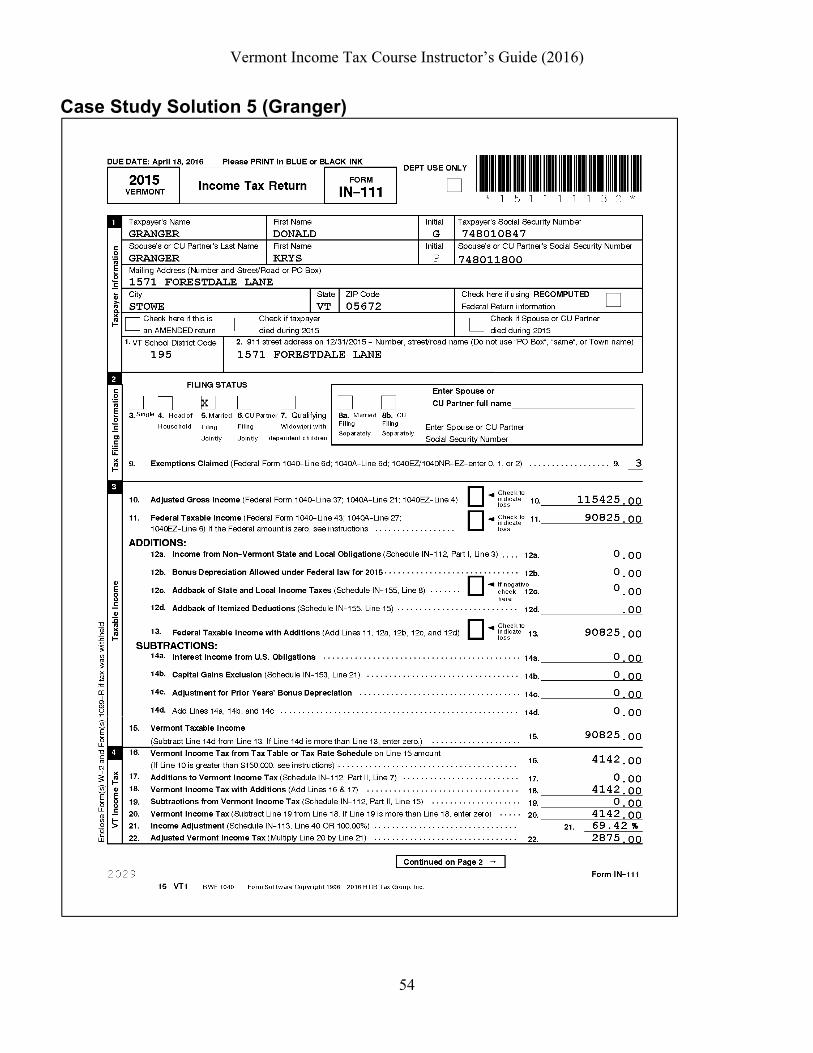

1. Are the Grangers required to file a federal income tax return? If they are not required to file, is there any benefit for them to file? Yes, the federal return is required because their income exceeds their filing requirement threshold.

2. If they are NOT required to file a federal return, are they required to file a Vermont return? If they are not required to file, is there any benefit for them to file anyway? Yes, because the federal return is required, the Vermont return is also required.

3. Preview the return, looking at each line to continue to become familiar with the ordering, the process of the calculations, and how the form is laid out.

4. What is on line 10? $115,425, which is their federal AGI. What is on line 11? $90,825, which is their federal taxable income. Are there any amounts on line 12 or 14? No, there are not additions to or subtractions from federal taxable income for Vermont purposes. What is on line 15? $90,825 is their Vermont Taxable Income. What other form or forms have been added to this return? VT IN-112, VT IN-113, VT HS-122, VT HI-144, and VT IN-116. Review these forms. Study them and become familiar with what is included on these forms. Return to VT IN-111 Pg 1. What is on line 16? $4,142, their Vermont income tax. Is there an amount on line 17 or 19? No, there are no additions to or subtractions from Vermont income tax. What is on line 21? 69.42%, for the income adjustment. Review Form VT IN-113 Pg 1 and Pg 2. Review the form and instructions on page 2, Part II to understand how this process occurs to help the taxpayer by reducing his Vermont tax. Return to VT IN-111. What is on line 25? $500, for Vermont Tax Credits. This comes from Schedule IN-112 Part IV. Review IN-112 Pg 2. Why is the amount on line 1 not $700? The maximum contribution allowable for the credit is $5,000. Return to VT IN-111. What is on line 28? $2,375, Total Vermont tax, which includes the reduction due to the $500 Tax Credit. What is on line 31a? $2,172, the amount of the Vermont tax withheld. What is on line 35? $203, which is the result of subtracting line 31h from line 30.

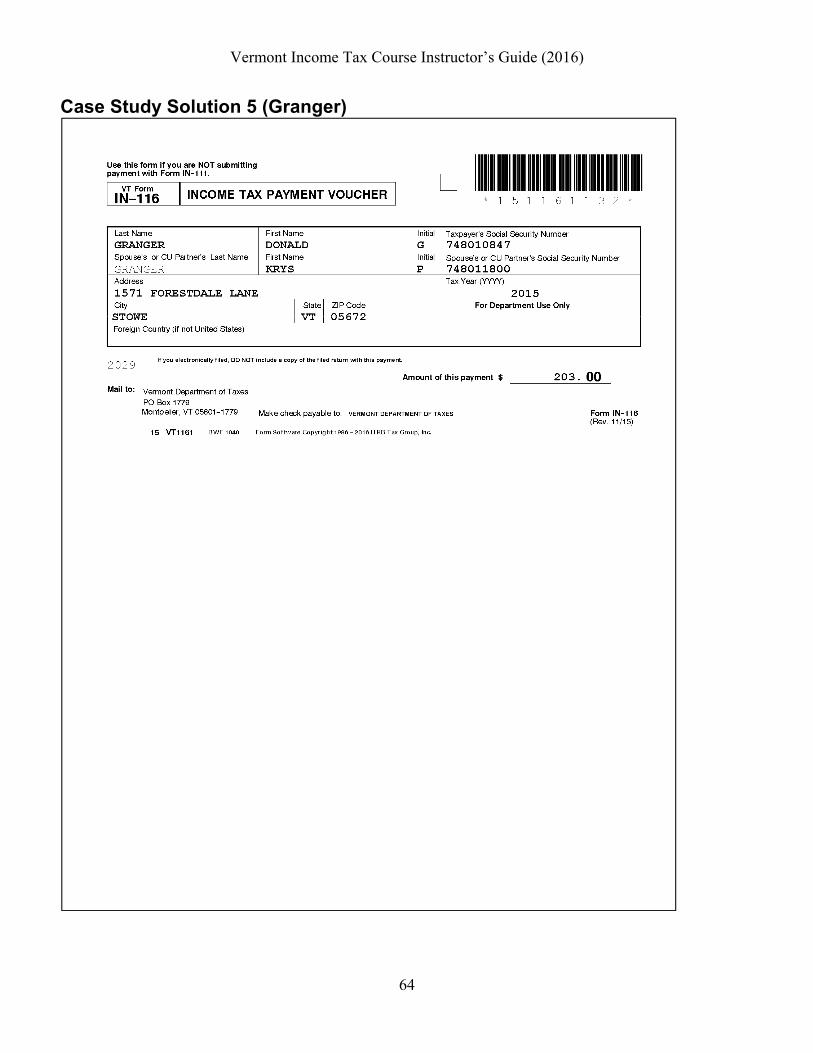

5. What is the Grangers’ refund or balance due for Vermont? A balance due of $203.

Vermont Income Tax Course Instructor’s Guide (2016)

66

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

67

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

68

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

69

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

70

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

71

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

72

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

73

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

74

Case Study Solution 6 (Williams)

Vermont Income Tax Course Instructor’s Guide (2016)

75

Case Study Solution 6 (Williams)

1. Are the Williamses required to file a federal income tax return? If they are not required to file, is there any benefit for them to file? Yes, the federal return is required because their income exceeds the filing requirement threshold.

2. If they are NOT required to file a federal return, are they required to file a Vermont return? If they are not required to file, is there any benefit for them to file anyway? Yes, because the federal return is required, the Vermont return is also required.

3. Preview the return looking at each line to continue to become familiar with the ordering, the process of the calculations, and how the form is laid out. What else do you notice regarding additional line items that are on their Vermont return? There are amounts on line 12a, 14a, and line 27.

4. What is on line 10? $45,263, which is their federal AGI. What is on line 11? $23,413, which is the amount of their federal taxable income. Are there any amounts on line 12 or 14? Yes, on line 12a is $105, Income from Non-Vermont State and Local Obligations. This is the interest income on the New York bonds which is not taxable on the federal return, but is for Vermont. Therefore, it must be added to federal taxable income for Vermont tax purposes. On line 14a is $14, which is the amount of interest income from U.S. obligations. This amount was taxable for federal, but is not taxable for Vermont and therefore this must be subtracted from federal taxable income for Vermont tax purposes. What is on line 15? $23,504, which is Vermont Taxable Income. This amount is the result of applying the additions to and subtractions from federal taxable income. What other form or forms have been added to this return? VT IN-112 and VT HI-144. Review these forms. Study them and become familiar with what is included on these forms. Return to VT IN-111 Pg 1. What is on line 16? $836, which is the Vermont Tax from the Tax Tables. Is there an amount on line 17 or 19? No, there are no additions to or subtractions from Vermont Income Tax. What is on line 27? $84 for the amount of the Use Tax that they owe. What is on line 30? $920, which is the combination of their Vermont income tax and their Use Tax. What is on line 31a? $1,154, the amount of their Vermont Tax Withheld. What is on line 31d, and why? Zero. Even though their federal AGI is $45,263, they are not eligible for the Renter Rebate because their household income is above $47,000. Review VT HI-144. Note that on line b is the full amount of the social security received by Greg, not just the federally taxable portion. What is on lines 32 and line 34? Their Overpayment is $234 on line 32 and the same amount is on line 34.

5. What is the Williamses’ refund or balance due for Vermont? A refund of $234.

Vermont Income Tax Course Instructor’s Guide (2016)

76

Hour 3, Final Test

Classroom Supplies Access to Block Academy.

Overview Inform participants that the test consists of completing a Vermont tax return in BlockWorks plus 20 multiple choice questions in Block Academy. Students should complete the tax return first, then the multiple choice questions, as some of the questions on the test will have to do with the tax return. The test case study (Duvall) should be entered using the information provided in the case study scenario and their student ID. There is no shell return available in BlockWorks for this test. Remind students they should clear any critical (red) diagnostics and review all other diagnostics before considering their return complete. Note: All shell returns have been entered as paper returns. To eliminate most of the critical (red) diagnostics, students should change the state return to paper as well.

Instructor Focus Demonstrate how to enroll in the test in Block Academy. Participants should do this before completing the tax return so they can go straight to the test when they are finished entering the return in BlockWorks. Inform the participants that the test case study (Duvall) is included in their workbook. Remind the participants that the test is open-book, and they may have all material available.

Closing Review the final case study with participants. Review the final test questions and answers with participants. Answer any questions. Remind the participants that the next time you meet will be to review the federal material in preparation for their final test. State material is not included in the federal final test. Suggest they complete any case studies they have not finished, and review any material that they found challenging.

Vermont Income Tax Course Instructor’s Guide (2016)

77

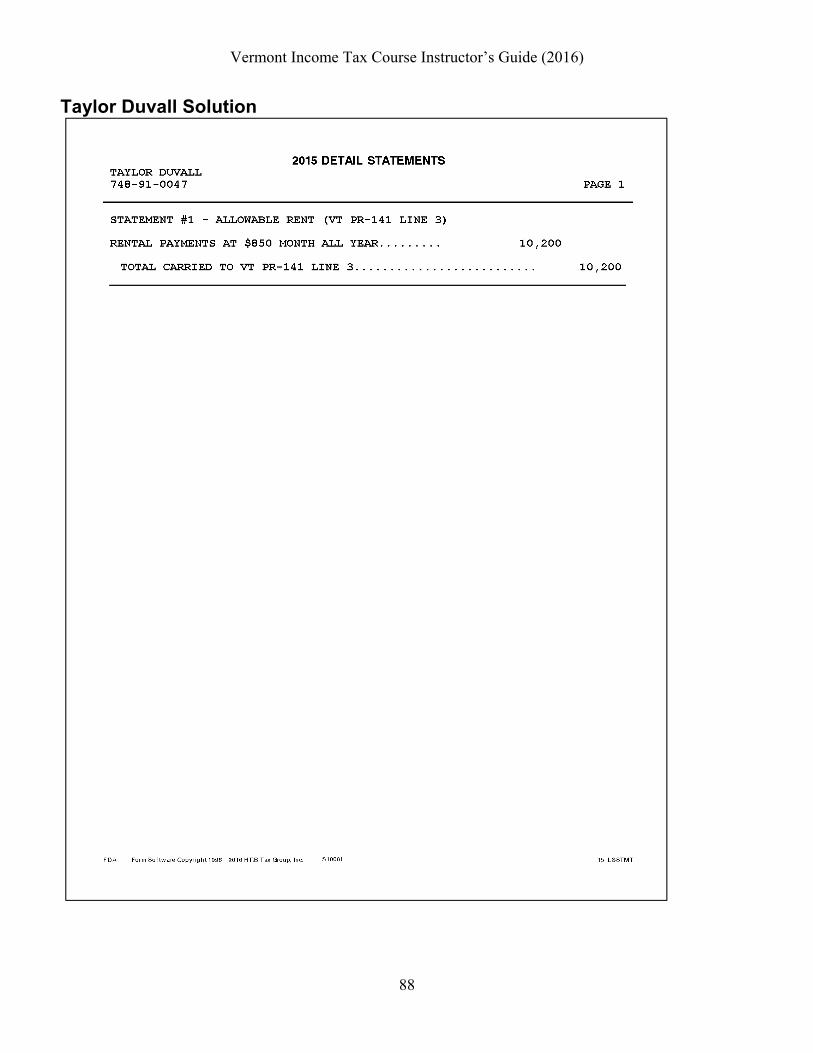

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

78

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

79

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

80

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

81

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

82

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

83

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

84

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

85

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

86

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

87

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

88

Taylor Duvall Solution

Vermont Income Tax Course Instructor’s Guide (2016)

89

Vermont State ITC – Multiple Choice Test

1. Beatrix's home was in Woodstock, Vermont from September 2013 until July 15, 2015, when she purchased a home and moved back to her childhood home in Salem, Massachusetts. Her intent was to make Massachusetts her home indefinitely. She sold her home in Vermont on July 30th. She was physically present in Vermont for a total of 184 days during the tax year. What is Beatrix's Vermont residency status for 2015?

a. Part-year resident. b. Nonresident. c. Resident, because she meets Vermont's domicile residency test. d. Resident, because she meets Vermont's statutory residency test.

2. Gunnar is an active duty member of the U.S. Army. He has been stationed at the Camp Ethan Allen

Training Site in Jericho, Vermont since September 2014. Florida was his home of record at the time he entered the military. He is serving in Vermont in compliance with military orders. Gunnar rented a studio apartment in nearby Burlington, Vermont on December 1, 2014, where he continues to live. He was physically present in Vermont a total of 328 days during the tax year. What is Gunnar's Vermont residency status?

a. Part-year resident. b. Nonresident. c. Resident, because he meets Vermont's domicile residency test. d. Resident, because he meets Vermont's statutory residency test.

3. Jocelyn's domicile is in Arkansas. She has been employed as a Baking and Pastry Arts Instructor at

the New England Culinary Institute in Montpelier, Vermont since August 25, 2014. Her contract was renewed for an additional two years. She signed a two-year lease for an apartment in Montpelier on January 1, 2015. She was physically present in Vermont for a total of eight months during the tax year. What is Jocelyn's Vermont residency status?

a. Part-year resident. b. Nonresident. c. Resident, because she meets Vermont's domicile residency test. d. Resident, because she meets Vermont's statutory residency test.

Vermont Income Tax Course Instructor’s Guide (2016)

90

4. Jedidiah's (38) domicile has been in Vermont since childhood. He has been employed as an instructor for Mahoosuc Guide Service in Newbury, Maine since November 2014. His wife, Naomi, and their children have continued to live in their Vermont home. After Jedidiah has gained enough experience, he plans to return to Vermont and start his own guide service. What is Jedidiah's Vermont residency status?

a. Part-year resident. b. Nonresident. c. Resident, because he meets Vermont's domicile residency test. d. Resident, because he meets Vermont's statutory residency test.

5. Blake (31) is single and an active duty member of the U.S. Marines. He was a Vermont resident at

the time he joined the military. He was stationed at Camp Pendleton, California until February 15, 2015, when he was deployed to Germany, then to Afghanistan to serve as an EOD tech. He spent a total of ten days in Vermont during the tax year. Blake's only income was $34,560 of active duty military pay, which includes $4,340 for his service in California. He is required to file a federal tax return. What is Blake's Vermont filing requirement?

a. Blake is required to file a Vermont resident tax return. The military pay that is included in his federal adjusted gross income is an adjustment on his Vermont return.

b. Blake is not required to file a Vermont return because none of his active duty military pay is from Vermont sources.

c. Blake is required to file a Vermont resident tax return. No adjustment is required on his Vermont return because Vermont follows the federal treatment of active duty military pay.

d. Blake is not required to file a Vermont return because the income he earned overseas is exempt from Vermont taxation and his U.S. earnings are below the Vermont filing requirement threshold for his filing status.

Vermont Income Tax Course Instructor’s Guide (2016)

91

6. Abigail Rose (22) is single and has been a student at Sweet Briar College in Sweet Briar, Virginia since September 2014. She is a Vermont resident and is claimed as a dependent on her parents' tax return. During the tax year, she was employed as a Craft Adventure Guide at Devils Backbone Brewing, near campus, and earned $4,530 in wages. She also received $390 in federally taxable U.S. Treasury Bond interest. She is required to file a federal tax return. What is Abigail Rose's Vermont filing requirement?

a. Abigail Rose is not required to file a Vermont return because she is a dependent on her parents' return.

b. Abigail Rose is required to file a Vermont resident tax return and report all of her income regardless of where it was earned or received. She may then subtract the U.S. Treasury Bond interest.

c. Abigail Rose is not required to file because her income is below the Vermont filing requirement threshold for a single taxpayer.

d. Abigail Rose is required to file. However, she is only required to report the interest income because her wages were earned outside of Vermont.

7. Radclyffe and Una are Vermont residents. Both are required to file in Vermont. They entered into a

legally recognized civil union in Vermont on January 1, 2001. They will each file their federal return using the single filing status. What is their filing status option(s) for Vermont?

a. They may choose to file using either: civil union filing jointly or civil union filing separately.

b. They must use the married filing separately status since they are in a civil union. c. They must use the married filing jointly status since they entered into a civil union in a state

that recognizes civil unions. d. They must use the same filing status as was used on their federal tax returns.

Vermont Income Tax Course Instructor’s Guide (2016)

92

8. Dwayne is an active duty servicemember. His domicile has been New Hampshire since he entered the military. He is stationed in Vermont under military orders. Dwayne's wife, Gabrielle, is a civilian employee at the base where Dwayne is stationed. Gabrielle has lived in Vermont since 2010. They married on May 15, 2015, and will be filing a joint federal return. Under the Military Spouses Residency Relief Act (MSRRA), will Gabrielle's wages at the base be subject to Vermont taxation? Why or why not?

a. Yes, Gabrielle's wages are subject to Vermont tax under MSRRA because she was still married to Dwayne at the end of the year.

b. No, under MSRRA, Gabrielle's wages will not be subject to Vermont tax because she is an employee of the U.S. government working on an active military base.