vietnam healthcare-market-overview-webinar-presentation (1)

TRANSCRIPT

Vietnam Healthcare Market Overview

10 December 2015

Australia Unlimited

Today’s webinar agenda

Introduction of speakers

The shift in ASEAN market – AEC & TPP impact

Vietnam healthcare market overview

Outline opportunities in hospital sector

Introduction to Medical Science & Health Services Mission to

Vietnam – July 2016

Q & A

2

Australia Unlimited

Introduction

Ms Janelle Casey – Senior Trade Commissioner, Austrade

Vietnam

Mr Dong Pham – Vice Chairman, Vietnam Private Hospital

Association

Ms Minh Cao – Business Development Manager, Austrade

Vietnam

Ms Milena Bliss – Senior Trade Adviser – International Health,

Sydney Australia

3

Why Vietnam

Australia Unlimited

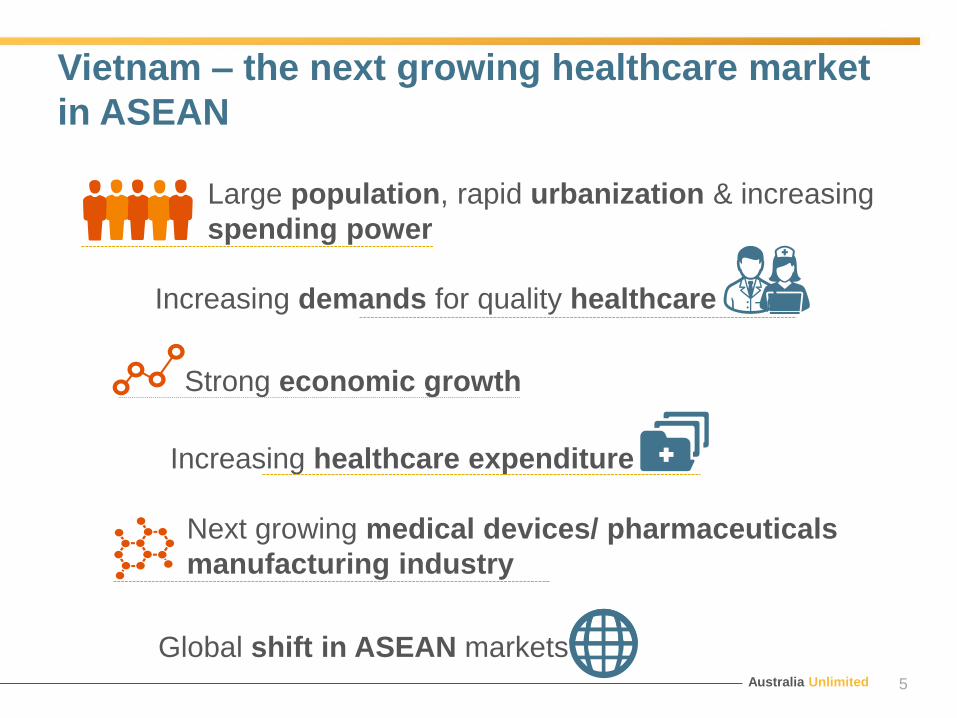

Vietnam – the next growing healthcare market

in ASEAN

5

Large population, rapid urbanization & increasing

spending power

Increasing demands for quality healthcare

Strong economic growth

Increasing healthcare expenditure

Next growing medical devices/ pharmaceuticals

manufacturing industry

Global shift in ASEAN markets

Australia Unlimited 6

The shift in ASIAN market: impacts from AEC & TPP

Australia Unlimited

Opportunities in Vietnam

Import of services for physicians

Next in production of and R&D pharmaceutical and medical devices

Manufacturing base for medical devices

AEC OBJECTIVES

Free flow of Goods

Free Flow of

Services

Free Flow of Investment

Free Flow of Capital

Free flow of skilled

labor

AEC impacts to healthcare industry

7

Source: BMI, Frost & Sullivan

Harmonised requirements

for inter-ASEAN licensing &

permits for practice

Removed or lowered tariff /

tax rates

Expansion & exporting of

services such as medical &

technical expertise

Expansion of

pharmaceutical & medical

device manufacturers &

distributors

Easier medical business

expansion & transfer of

capital

Australia Unlimited

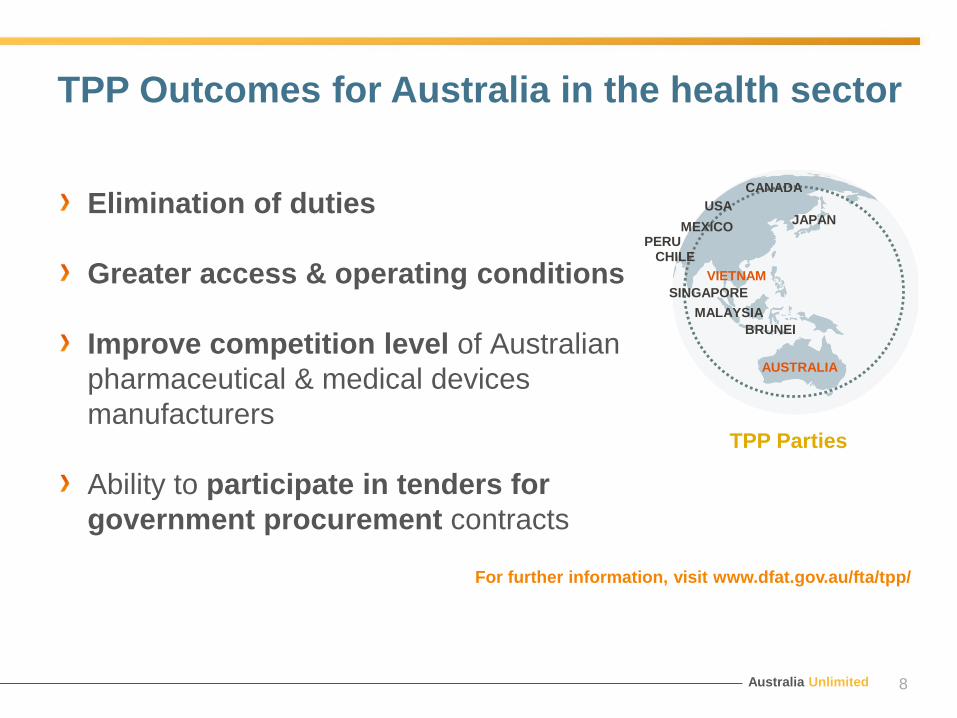

TPP Outcomes for Australia in the health sector

8

Elimination of duties

Greater access & operating conditions

Improve competition level of Australian

pharmaceutical & medical devices

manufacturers

Ability to participate in tenders for

government procurement contracts

For further information, visit www.dfat.gov.au/fta/tpp/

SINGAPORE

MEXICO

TPP Parties

JAPAN

VIETNAM

MALAYSIA

BRUNEI

AUSTRALIA

CANADA

USA

PERUCHILE

VIETNAM HEALTHCARE

MARKET

Australia Unlimited

Year 2014

Vietnam – the next healthcare market in ASEAN

Total healthcare spending

90% Medical devices are imported

Hospitals

Year 2020e

91million 97million

Large & fast growing Population

33.6% 36.9%

URBAN RATE19.5%

24.9%

4.9%

5.2%

13.3%

32.3%

Consumables

Diagnostic Imaging

Dental products

Orthopedics &prosthetics

Patient aids

Others

22.3%

25.4%

5.0%

5.9%

12.0%

29.3%

US$13billion

Year 2015

Year 2015 Year 2020e

Year 2015 Year 2020e

Growing at 13.4%

Growing at 1.05%

Year 2014 Year 2020e

1,090 1,204

200175

Public

Private

7.9 Doctors per 10,000 habitants

25.1 Hospital beds per 10,000

habitants

10

US$24billion

Pharmaceuticals market value

US$3.8billion

US$7.3billion

Growing at 14.1%

Year 2014 Year 2019e

5.8% GDP – highest in ASEAN

4th largest in ASEAN

14th largest in the world

Source: BMI, Frost & Sullivan, World Bank

Australia Unlimited

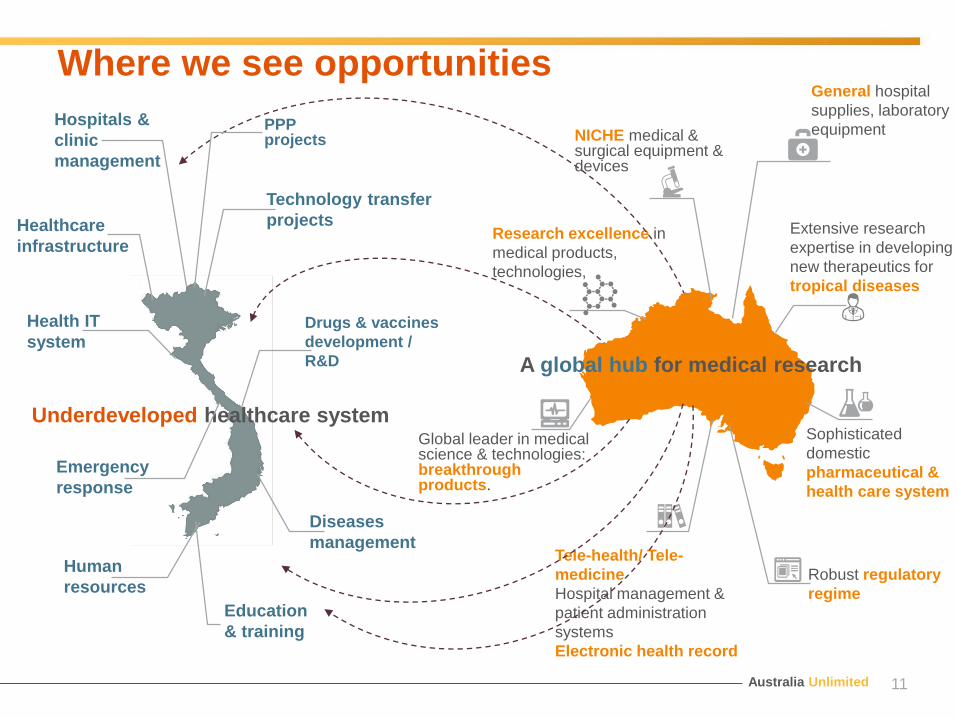

Where we see opportunities

11

Tele-health/ Tele-

medicine

Hospital management &

patient administration

systems

Electronic health record

Research excellence in

medical products,

technologies,

Robust regulatory

regime

Sophisticated

domestic

pharmaceutical &

health care system

Global leader in medical science & technologies: breakthrough products.

Extensive research

expertise in developing

new therapeutics for

tropical diseases

A global hub for medical research

Underdeveloped healthcare system

PPP projects

Healthcare

infrastructure

Technology transfer

projects

Drugs & vaccines

development /

R&D

Emergency

response

Diseases

management

Human

resources

Health IT

system

Hospitals &

clinic

management

Education

& training

NICHE medical & surgical equipment & devices

General hospital

supplies, laboratory

equipment

Australia Unlimited

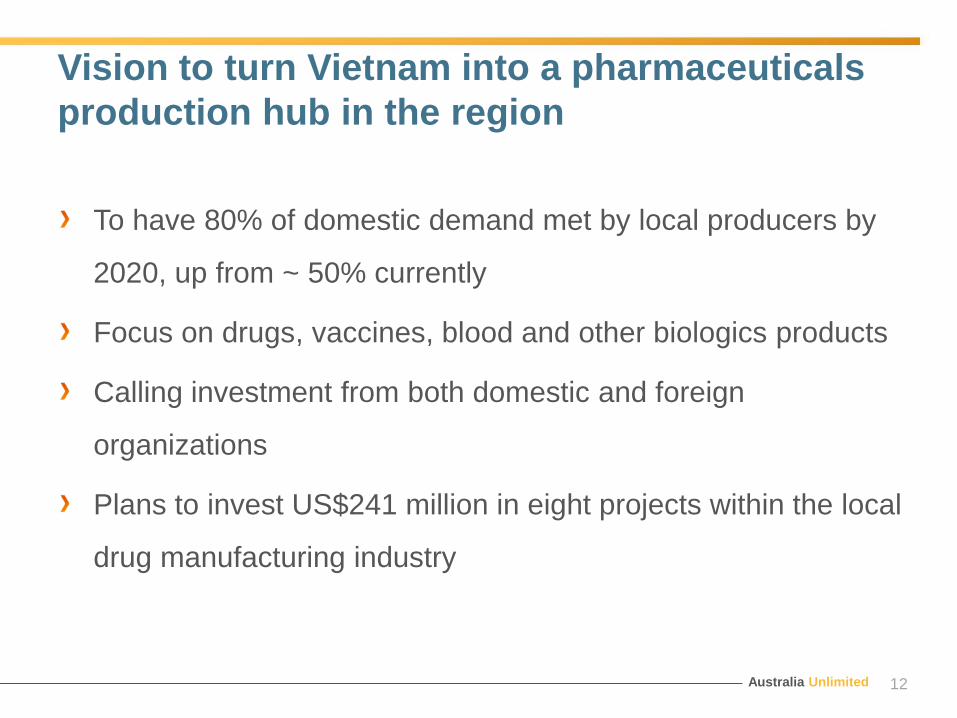

Vision to turn Vietnam into a pharmaceuticals

production hub in the region

To have 80% of domestic demand met by local producers by

2020, up from ~ 50% currently

Focus on drugs, vaccines, blood and other biologics products

Calling investment from both domestic and foreign

organizations

Plans to invest US$241 million in eight projects within the local

drug manufacturing industry

12

Australia Unlimited

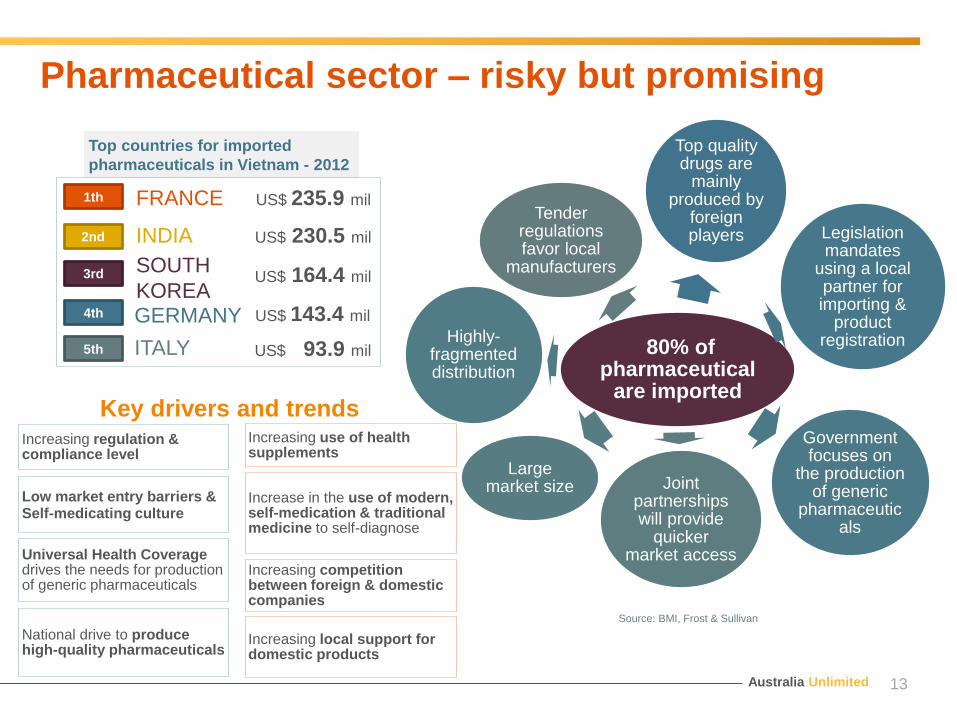

Pharmaceutical sector – risky but promising

13

Top countries for imported

pharmaceuticals in Vietnam - 2012

80% of pharmaceutical

are imported

Top quality drugs are

mainly produced by

foreign players Legislation

mandates using a local partner for importing &

product registration

Government focuses on

the production of generic

pharmaceuticals

Highly-fragmented distribution

Large market size Joint

partnerships will provide

quicker market access

Tender regulations favor local

manufacturers

Increasing regulation & compliance level

Low market entry barriers & Self-medicating culture

Universal Health Coverage drives the needs for production of generic pharmaceuticals

National drive to produce high-quality pharmaceuticals

Key drivers and trends

FRANCE1th

2nd INDIA

US$ 235.9 mil

US$ 230.5 mil

3rd SOUTH

KOREAUS$ 164.4 mil

4th GERMANY US$ 143.4 mil

5th ITALY US$ 93.9 mil

Increasing use of health supplements

Increase in the use of modern, self-medication & traditional medicine to self-diagnose

Increasing competition between foreign & domestic companies

Increasing local support for domestic products

Source: BMI, Frost & Sullivan

Australia Unlimited

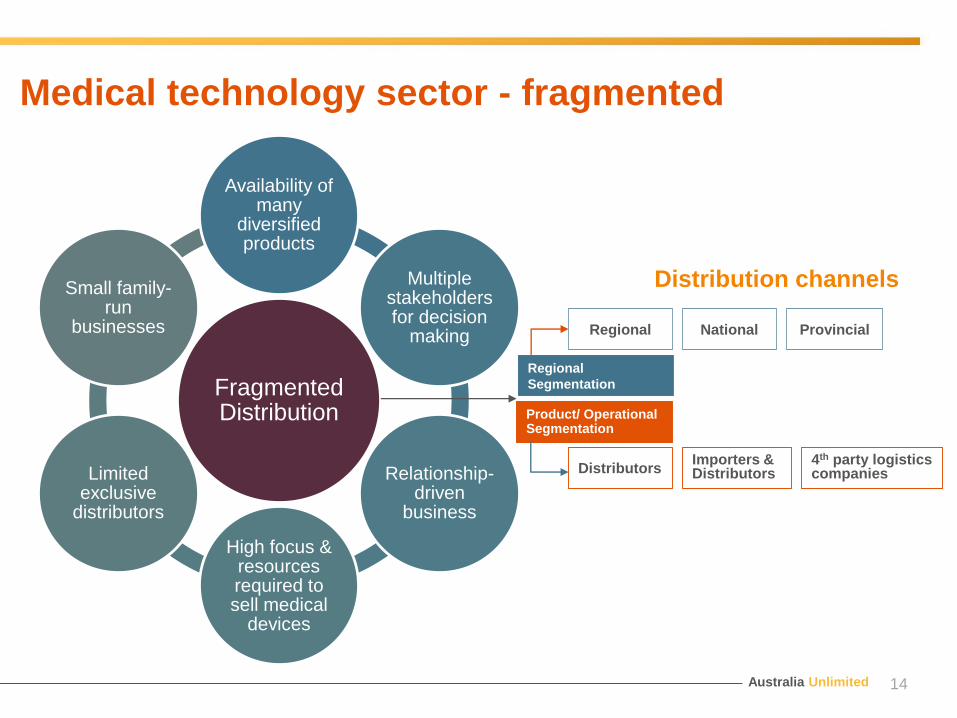

Medical technology sector - fragmented

14

Fragmented Distribution

Availability of many

diversified products

Multiple stakeholders for decision

making

Relationship-driven

business

High focus & resources required to sell medical

devices

Limited exclusive

distributors

Small family-run

businesses

Distribution channels

Regional

Segmentation

Regional Provincial

Product/ Operational Segmentation

DistributorsImporters & Distributors

4th party logistics companies

National

Australia Unlimited

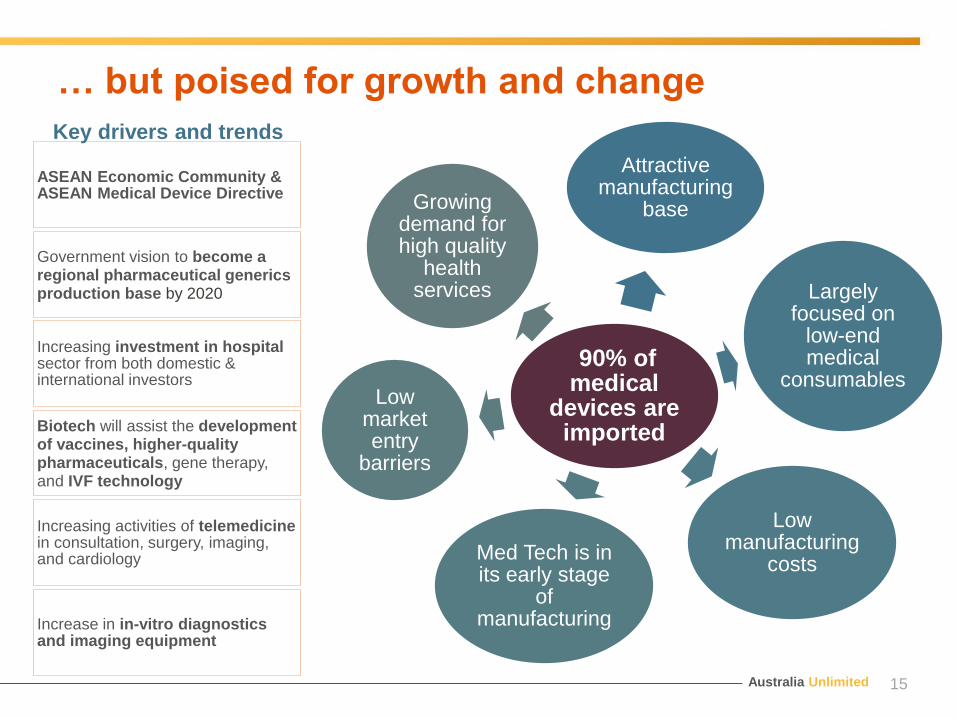

… but poised for growth and change

15

ASEAN Economic Community &ASEAN Medical Device Directive

Government vision to become a regional pharmaceutical generics production base by 2020

Increasing investment in hospital sector from both domestic & international investors

Biotech will assist the development of vaccines, higher-quality pharmaceuticals, gene therapy, and IVF technology

Increasing activities of telemedicine in consultation, surgery, imaging, and cardiology

Increase in in-vitro diagnostics and imaging equipment

Key drivers and trends

90% of medical

devices are imported

Attractive manufacturing

base

Largely focused on

low-end medical

consumables

Low manufacturing

costsMed Tech is in its early stage

of manufacturing

Low market entry

barriers

Growing demand for high quality

health services

Hospital sector

Mr The Dong Pham

Vice Chairman

Vietnam Private Hospital Association

Australia Unlimited

Developing public hospital sector is a priority

Market drivers

Healthcare expenditure is ~ 6% of GDP, highest in ASEAN region

Financial resources from WHO to develop

healthcare infrastructure

Government reducing barriers to new

hospital set-ups

2011–2015 eHealth Plan to improve health

IT applications

Aging society with decreasing birth rates

Collaboration between local manufacturers and

foreign companies for local generics or low-

end medical devices

Collaboration with distributors for joint ventures

to move the distributor up the value chain

Expansion or joint ventures in both urban and rural

areas; data warehousing to increase efficiency &

data tracking between vendors and hospitals

Systems adoption to link up private and

public hospital information systems.

Aged care services or IVF specialty clinics or

products.

Opportunities

17

Australia Unlimited

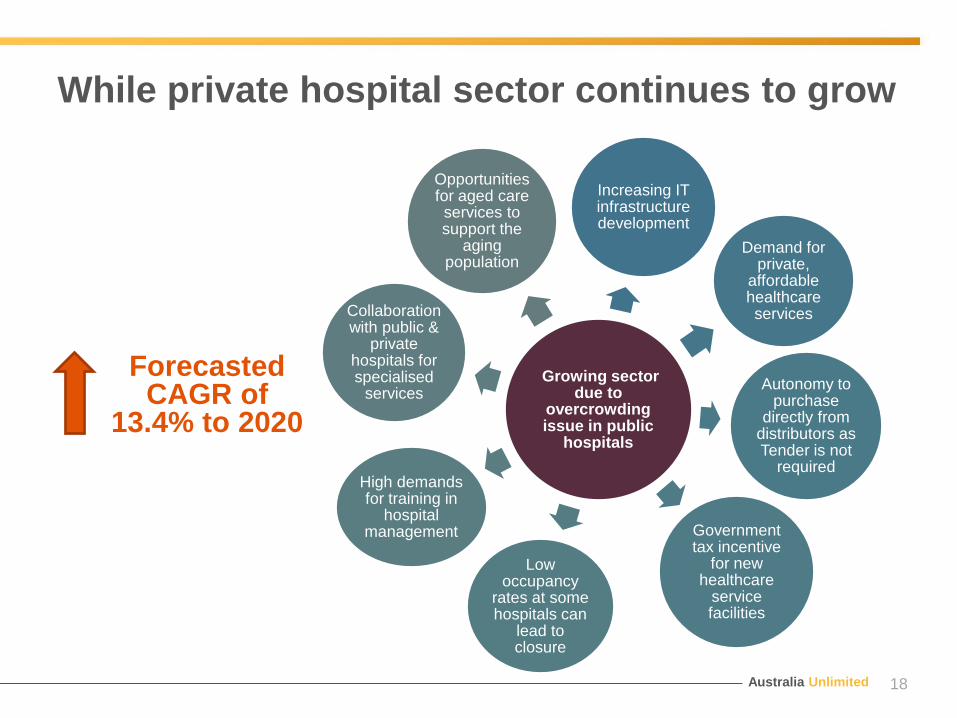

While private hospital sector continues to grow

18

Growing sector due to

overcrowding issue in public

hospitals

Increasing IT infrastructure development

Demand for private,

affordable healthcare services

Autonomy to purchase

directly from distributors as Tender is not

required

Government tax incentive

for new healthcare

service facilities

Low occupancy

rates at some hospitals can

lead to closure

High demands for training in

hospital management

Collaboration with public &

private hospitals for specialised

services

Opportunities for aged care services to support the

aging population

Forecasted CAGR of

13.4% to 2020

Australia Unlimited

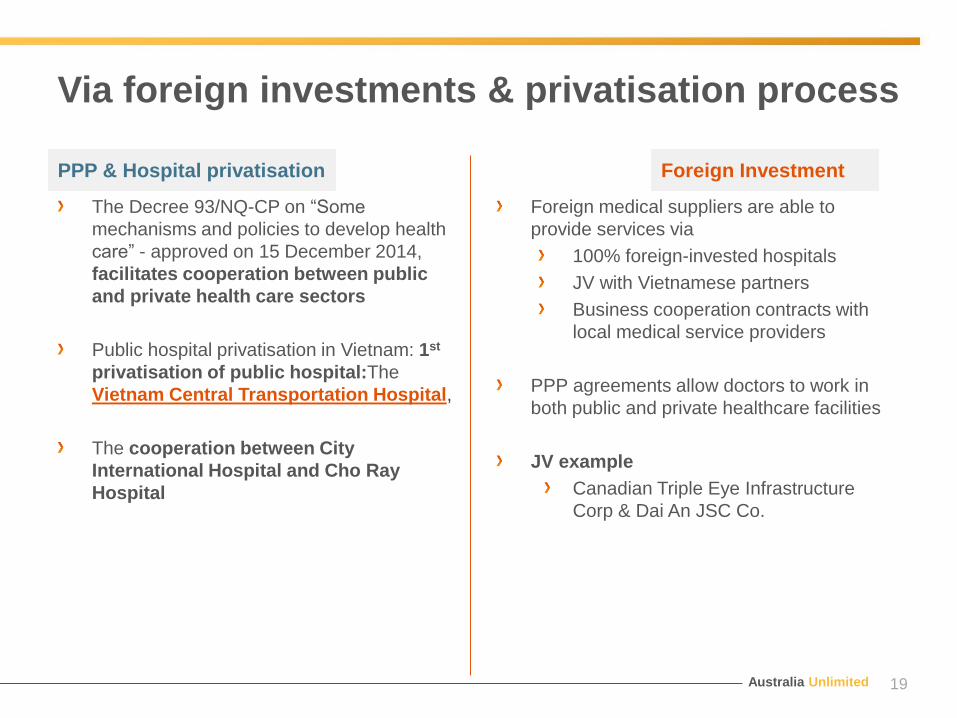

Via foreign investments & privatisation process

The Decree 93/NQ-CP on “Some

mechanisms and policies to develop health

care” - approved on 15 December 2014,

facilitates cooperation between public

and private health care sectors

Public hospital privatisation in Vietnam: 1st

privatisation of public hospital:The

Vietnam Central Transportation Hospital,

The cooperation between City

International Hospital and Cho Ray

Hospital

Foreign medical suppliers are able to

provide services via

100% foreign-invested hospitals

JV with Vietnamese partners

Business cooperation contracts with

local medical service providers

PPP agreements allow doctors to work in

both public and private healthcare facilities

JV example

Canadian Triple Eye Infrastructure

Corp & Dai An JSC Co.

19

PPP & Hospital privatisation Foreign Investment

Australia Unlimited

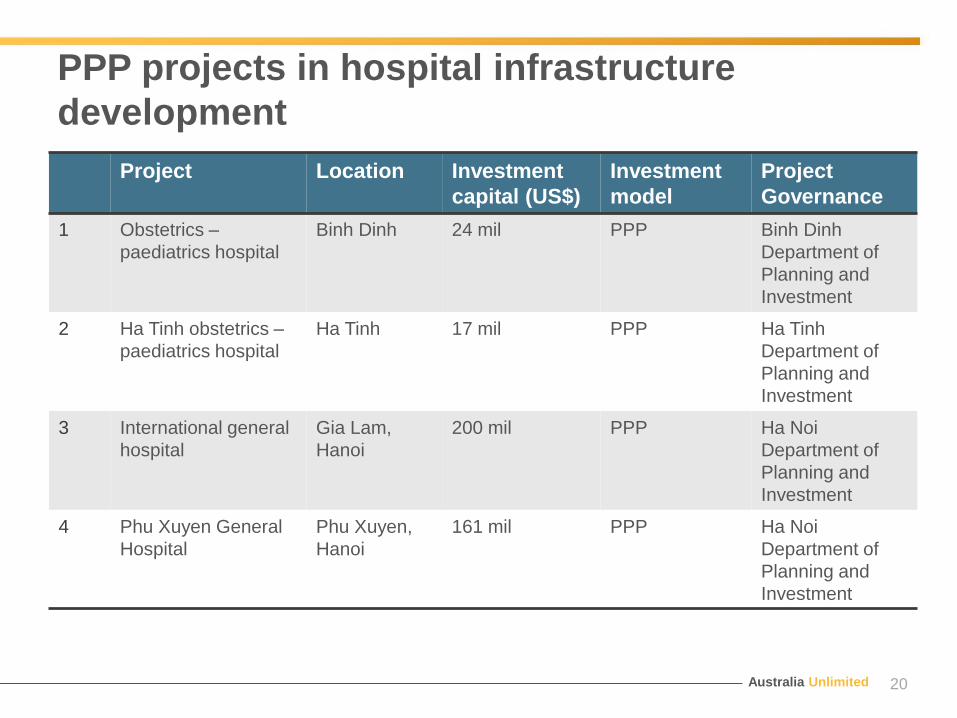

PPP projects in hospital infrastructure

development

Project Location Investment

capital (US$)

Investment

model

Project

Governance

1 Obstetrics –

paediatrics hospital

Binh Dinh 24 mil PPP Binh Dinh

Department of

Planning and

Investment

2 Ha Tinh obstetrics –

paediatrics hospital

Ha Tinh 17 mil PPP Ha Tinh

Department of

Planning and

Investment

3 International general

hospital

Gia Lam,

Hanoi

200 mil PPP Ha Noi

Department of

Planning and

Investment

4 Phu Xuyen General

Hospital

Phu Xuyen,

Hanoi

161 mil PPP Ha Noi

Department of

Planning and

Investment

20

Australia Unlimited 21

SAIGON ITO HOSPITAL GROUP

Australia Unlimited

Demands for

healthcare in

Vietnam are unmet

Long-term potentials in

medical technology

market

• Driven by the national initiative for

local drugs & medical devices

manufacturing

• AEC & TPP in place

• Strong foreign investment

Vietnam may become the

generic drugs manufacturing

hub in the region

• Government focus sector

• Low-cost production & competitive

environment

• Lower business boundaries due to AEC &

TPP

Vietnam – a market full of potentials

• Hospitals overcrowding

• Under-served rural population

• Poor adoption of technology

• High-quality drugs are mainly

imported

22

Australia Unlimited

Medical science & health services mission to Vietnam

23

Led by Professor Ian

Frazer

Opportunities to

showcase

• Products

• Equipment

• Technology

• Systems

• Services, education and

research

Obtain market insights,

first-hand market

understanding

Increase brand awareness

Chances to establish

connections with

• Industry key stakeholders

• Potential customers,

distributors and partners

• Key market players

• Education and training

institutions Site visits, business

matching activities, net

working functions,

research workshop

Leverage the Australian

government badge

Hanoi & Ho Chi Minh City

18th to 22th July 2016

Develop business &

collaboration opportunities

CONTACT AUSTRADE

In Australia: 13 28 78

In Vietnam: +84 8 3827 0600

www.austrade.gov.au/Vietnam

www.exportawards.gov.au

www.australiaunlimited.com

Disclaimer: Austrade does not endorse or guarantee the performance or suitability of any information introduced in this

presentation or accept liability for the accuracy or usefulness of information contained here within. Please use your commercial

discretion to assess the suitability of any business introduction or goods and services offered when assessing your business needs.

Austrade does not accept liability for loss associated with the use of any information and any reliance is entirely at the user’s discretion.

This presentation is copyright and cannot be reproduced without the prior permission of the Australian Trade Commission.