view

TRANSCRIPT

WA Marketing & Business Networking Congress – Perth

7 June 2006

“Positioned for Success”Trevor Amery

Chairman, Subaru (Aust) Pty Ltd

Agenda

•Background

•Positioning- Strategic

- Operational

•“Success?”

Background

•Subaru commenced in Australia in 1973•Disparate Niche Products•Rural Sales Bias•Inferiority Complex•Complex Range•Over Dealerised•“Endaka”•Competitive Motor Vehicle Market

•53 Brands / Marques•4 Local Manufacturers Market Share

- Toyota 20.5%- Holden 17.7%- Ford 13.1%- Mitsubishi 6.3%

5 7 .6 %•49 Marques compete in 42.4% of market

- Average 8,551 units each•Over 800 models / variants•Total Volume 988,269 units

VFACTS: 2005

Background

“Positioning”

Strategic

Customer, Dealers, Employees, FHI, Tomen & Inchcape

•Position Subaru as the pre-eminent Japanese automotive brand in the Australian marketplace

•Position Subaru as the All-Wheel Drive brand

•Position Subaru Australia as the pre-eminent distributor of Subaru product in the world

•Manage the Subaru brand to optimise the value for all stakeholders

CUSTOMER

• Grow Brand• Real Time• Experiences

RETAIL

• Create Brand• Build Network• Quality Sales• CRM

MARKETER

Helped Network sell cars

ADVERTISER

Sold cars to Dealers

IMPORTER

M o v e c lo s e r t o t h e C u s t o m e rStrategic

SUBARUBRAND IMAGE

StrategicPrice

Post PurchaseExperience

Ease ofOwnership

PurchaseExperience/

Process

Psychographics- Demographics

Product /Features

K e y B e n c h m a r k sStrategic

•Product Positioning•Product Planning•Marketing Consistency•Dealership Presentation

• Training- Skill- Attitude

• Presentation

Operational

•Rationalise Dealer Network•Rationalise Model Range•Marketing focused on the Consumer

Benefits of our Differences•Go Rallying•Web Strategy•RRP Integrity

O r d e r t o D e liv e r y C y c leOperational

Production Order 0

Proc. & Production 58 58

Shipping 21 79

Wharf to Compound 2 81

Landed – Wholesale 78 159

Wholesale - Retail 59 218

1995 - DAYS IN PROCESS

“Success?”

(

00

0’

)RetailedUnits

s

96

40

35

30

25

20

15

10

5

0

97 98 99 00 01 02 03 04 05

FWD vs AWD

FWD

AWD

1 9 9 6 - 2 0 0 5

unprecedented ten consecutive championships

P o s s u m B o u r n e 1996 - 2002

C o d y C r o c k e r 2003 - 2005

AU S TR ALIAN R ALLYC H AM P IO N

40

35

30

25

20

15

10

5

0

96 97 99 01 02 04 05

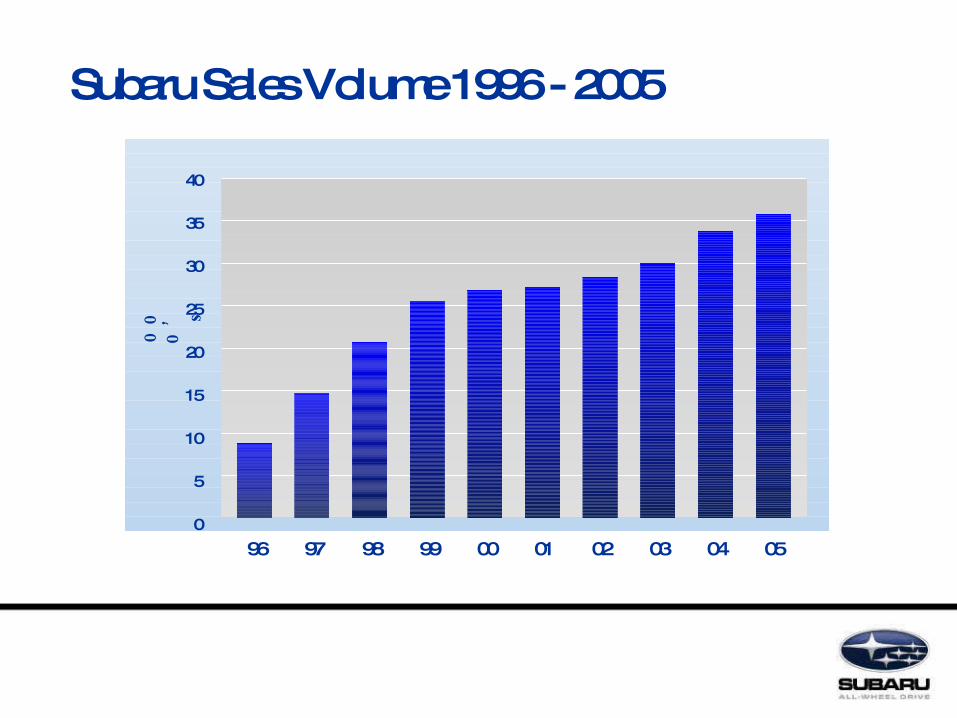

Subaru Sales Volume 1996 - 2005

98 00 03

00

0’ s

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1.500

1,000

500

0

99 00 01 02 03 04 05

Subaru Sales Volume $50k Plus

4.0

3.5

3.0

2.5

2.0

1.5

1.0

.5

0

Subaru Market Share

96 97 99 01 02 04 0598 00 03 YTD Mar 06

%

1995 180 7,910 44

2005 109 36,044 331

New Vehicle Dealerships Volume Average Sales Volume pa

Dealership Throughput

Note: 40 Dealerships achieve > 70% of National Volume

+752.3%

Subaru Melbourne – Docklands

Subaru Mt Gravatt

80

70

60

50

40

30

20

10

0

% of current drivers who would consider repurchasing brand (based on 12mth database and no 20k filter in demographic)

Peu

ge

ot

Su

baru

Ho

lde

n

BM

W

To

yota

Ho

nd

a

Mazd

a

Fo

rd

Vo

lvo

Nis

san

Saab

La

nd

Ro

ver

Vo

lkswag

en

Hyu

nd

ai

Merce

des

Mits

ub

ishi

48

71

65 65

59

52 5147 48

44

3033

56

33

4342

52

68

59 61 61

51

4549

28

4744

32

41

33

4643

Jan 04 -Dec 04

Jul 05 - Jan 06

SOURCE: Panorama

New Car Brand Loyalty:

Order to Delivery Cycle

Production Order 0 0

Proc. & Production 58 58 55 55

Shipping 21 79 13 68

Wharf to Compound 2 81 2 70

Landed – Wholesale 78 159 8 78

Wholesale - Retail 59 218 34 112

1995 2005 Days in Process Days in Process

20

0

-20

-40

-60

-80

-100

-120

-140

94 97 99 01 02 04 0598 00 03

Mill

ions

Subaru Australia - Working Capital

95 96

Volume MarketUnits Share

Volume and Market Share 2005

Japan (excl mini cars)

Japan (inc mini cars)

USA

Australia

Canada

Switzerland

Germany

UK

108,649

258,217

196,002

36,044

15,966

9,401

10,132

8,926

2.8%

4.4%

1.1%

3.6%

1.0%

3.6%

0.3%

0.4%

40

30

25

20

15

10

597 99 01 02 04 0598 00 0396

Subaru Australia v Peers

Australia

Germany

UKSwitzerland

Canada

FHI: Retail Sales (000’s)

97 99 01 02 04 0598 00 03

$

95 96

Subaru Australia - PBT

Thank you for your interest.