views on business structure - oecd.org - oecd · views on business structure: the example of...

TRANSCRIPT

Views on business structure:

The example of ship-building/repair activities

www.forumokretowe.org.pl

Jerzy Czuczman

Sławomir Skrzypiński

Set-up:

- business recovery

- opportunities perceived

- challenges faced

- shifting into offshore

POLAND – case study

Start with an earthquake ….

1990

TRANSFORMATION

LOW COST

LEADER

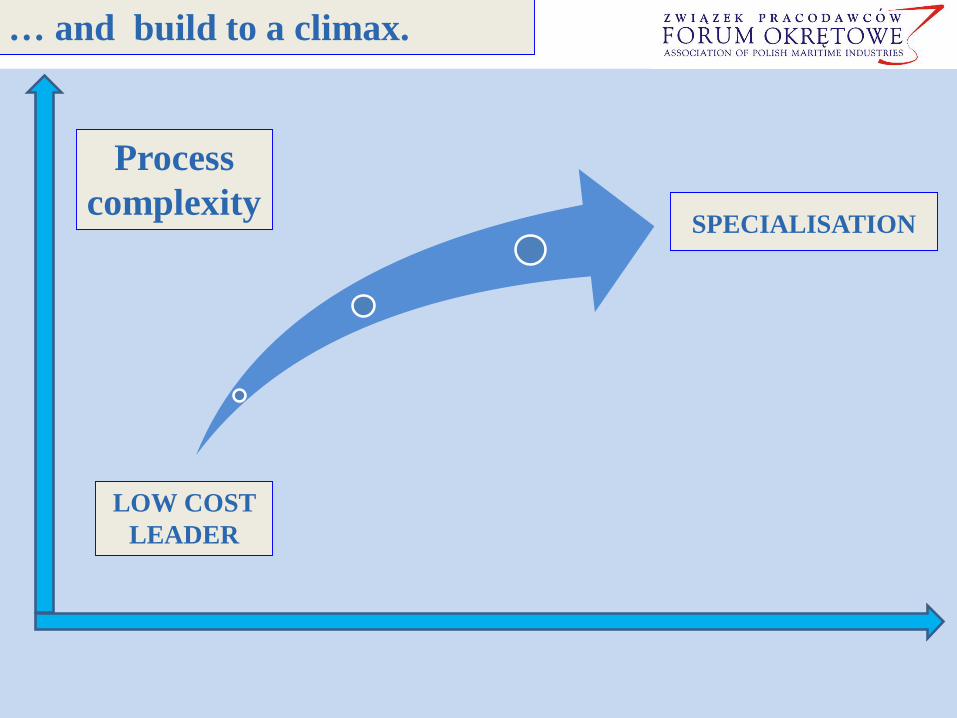

… and build to a climax.

SPECIALISATION

Process

complexity

http://ec.europa.eu/enterprise/sectors/maritime/files/fn97616_ecorys_final_report_on_shipbuilding_competitiveness_en.pdf

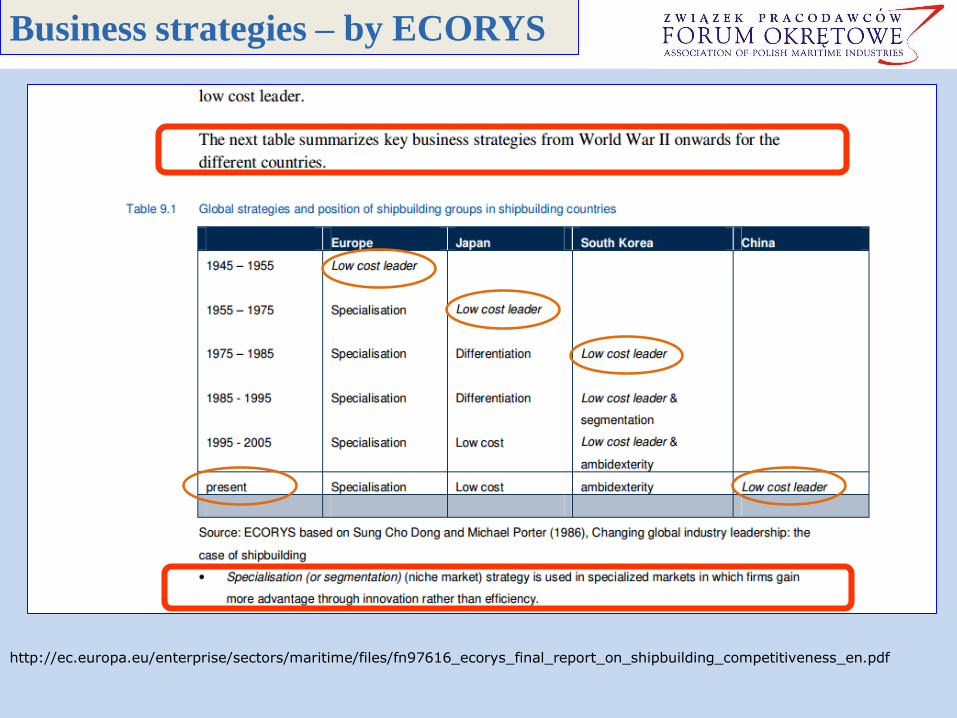

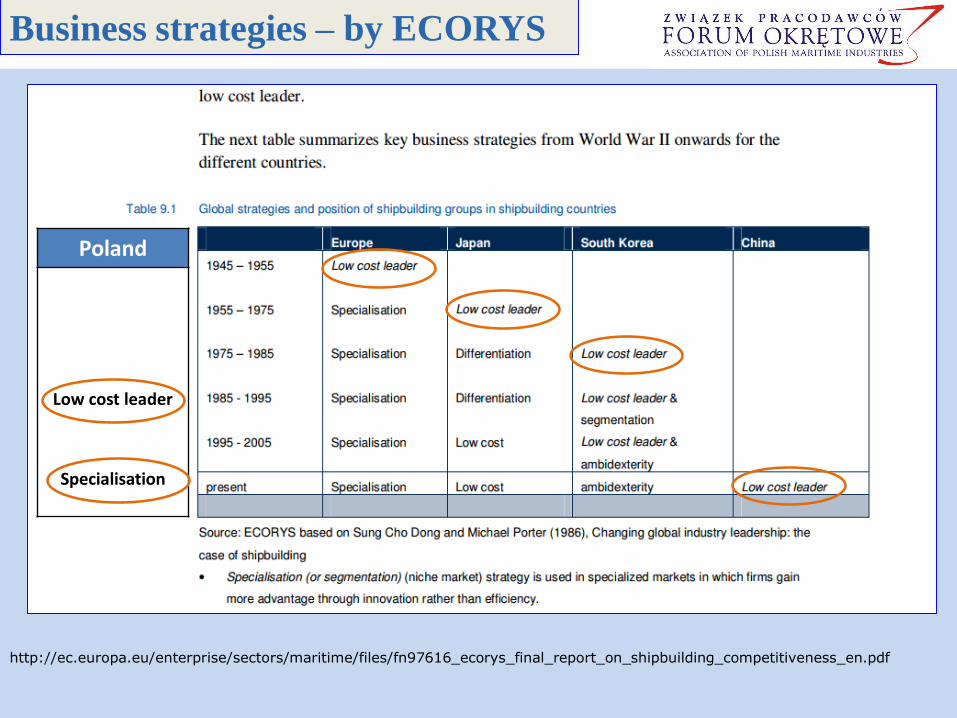

Business strategies – by ECORYS

http://ec.europa.eu/enterprise/sectors/maritime/files/fn97616_ecorys_final_report_on_shipbuilding_competitiveness_en.pdf

Business strategies – by ECORYS

Poland

Low cost leader

Specialisation

But the „way” was NOT like a „high way”

… it was more like THAT way……

So, let’s take a view

on business structure

0

100

200

300

400

500

600

700

% p

er y

ear

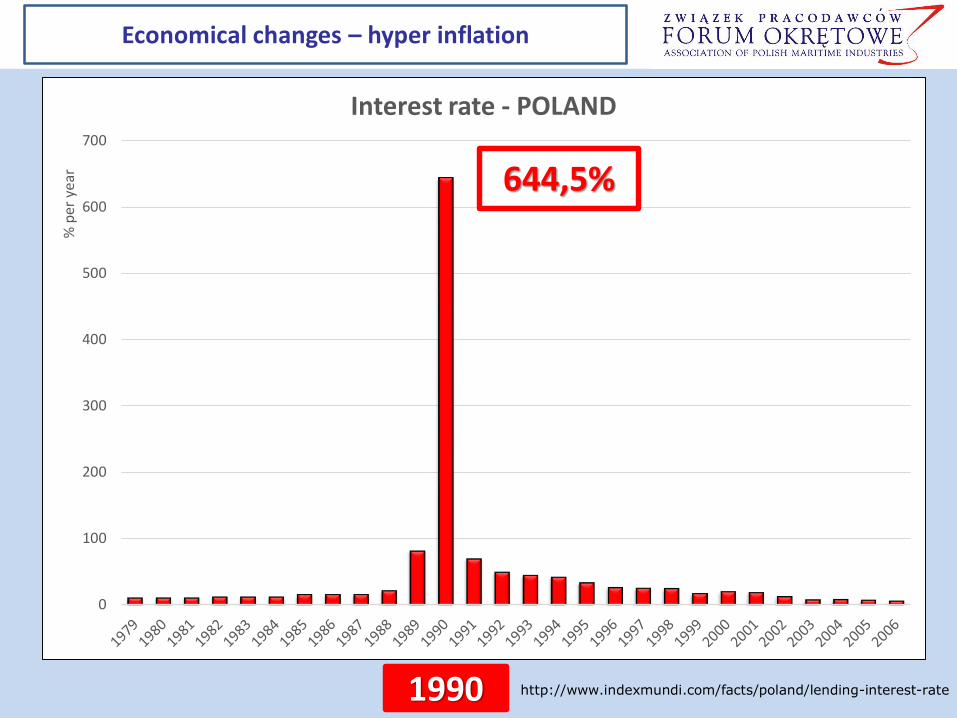

Interest rate - POLAND

644,5%

1990

Economical changes – hyper inflation

http://www.indexmundi.com/facts/poland/lending-interest-rate

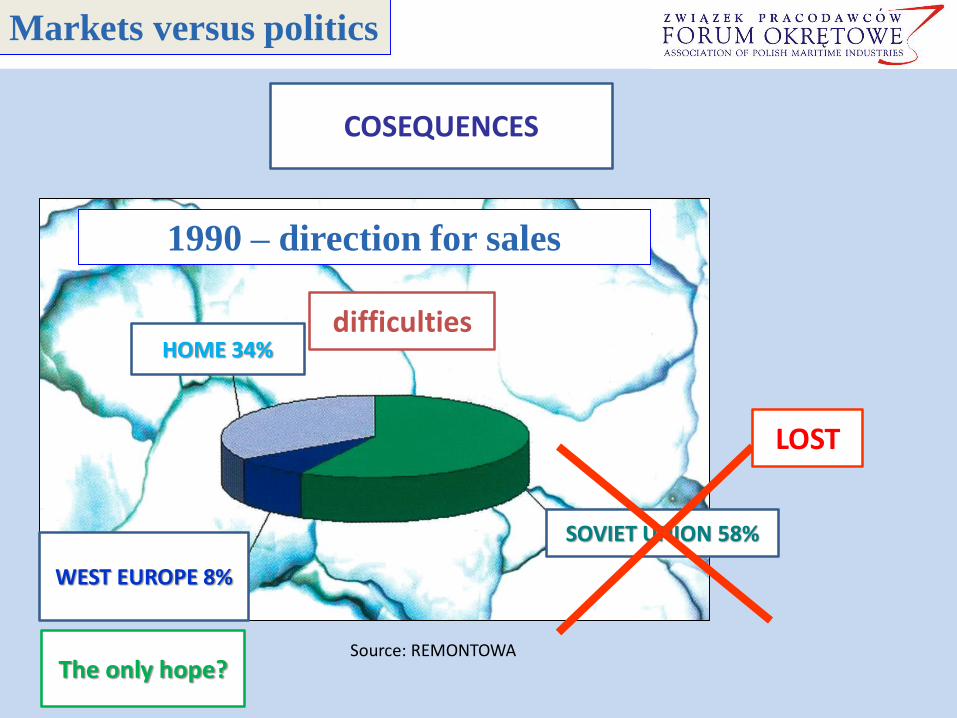

Markets versus politics

HOME 34%

WEST EUROPE 8%

SOVIET UNION 58%

Source: REMONTOWA

1990 – direction for sales

COSEQUENCES

LOST

difficulties

The only hope?

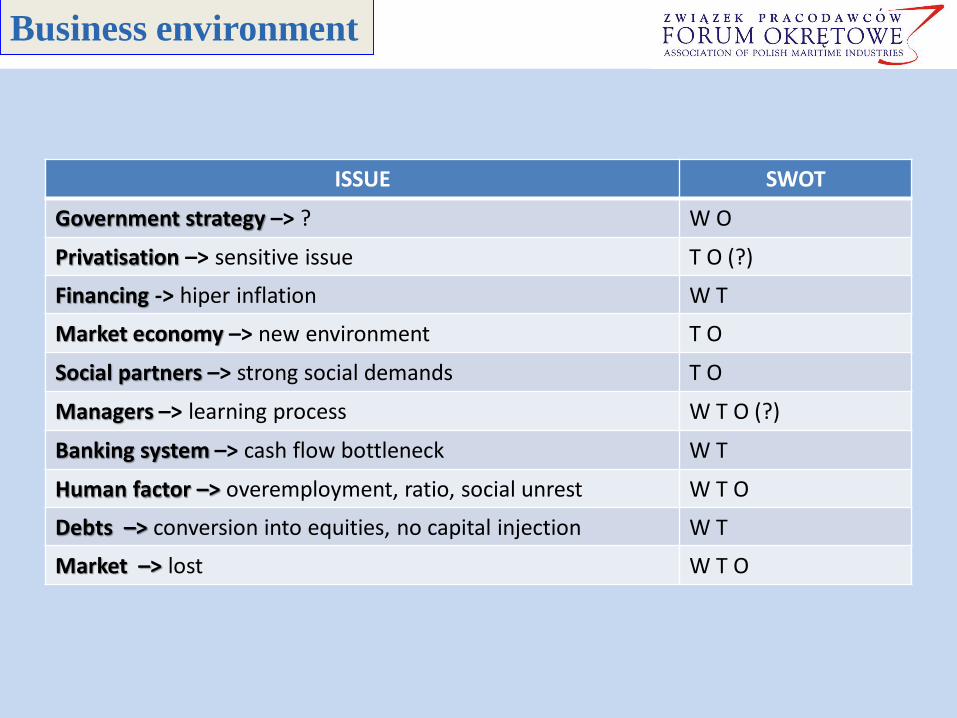

ISSUE SWOT

Government strategy –> ? W O

Privatisation –> sensitive issue T O (?)

Financing -> hiper inflation W T

Market economy –> new environment T O

Social partners –> strong social demands T O

Managers –> learning process W T O (?)

Banking system –> cash flow bottleneck W T

Human factor –> overemployment, ratio, social unrest W T O

Debts –> conversion into equities, no capital injection W T

Market –> lost W T O

Business environment

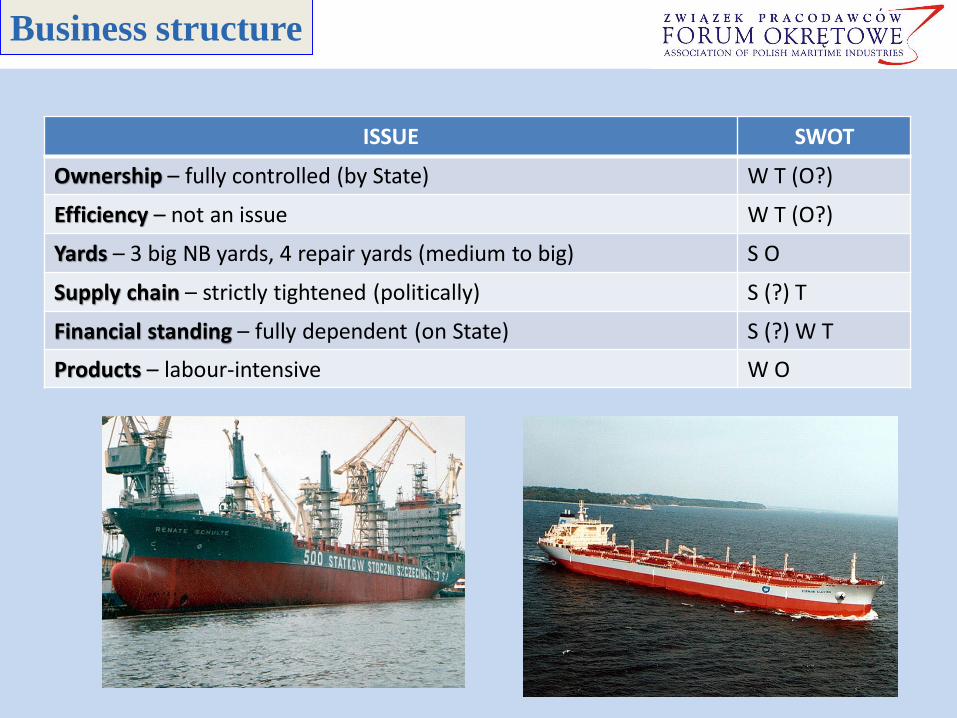

ISSUE SWOT

Ownership – fully controlled (by State) W T (O?)

Efficiency – not an issue W T (O?)

Yards – 3 big NB yards, 4 repair yards (medium to big) S O

Supply chain – strictly tightened (politically) S (?) T

Financial standing – fully dependent (on State) S (?) W T

Products – labour-intensive W O

Business structure

Description Fast movingNew ideas,

Best technical equipment

„only” repair yard not a NB yard,

left of „public interest”

Products Containers,

introducing new products

Containers, introducing new

productsIntensive search

Ownership structure

Management buy-out

Struggling for management buy-out

Assets being released Involve employees

Managerialstructure

Dramatic shiftEfficiency under

controlNot efficient Strongly centralised

Business cases

19901996

„Golden Age”- ?

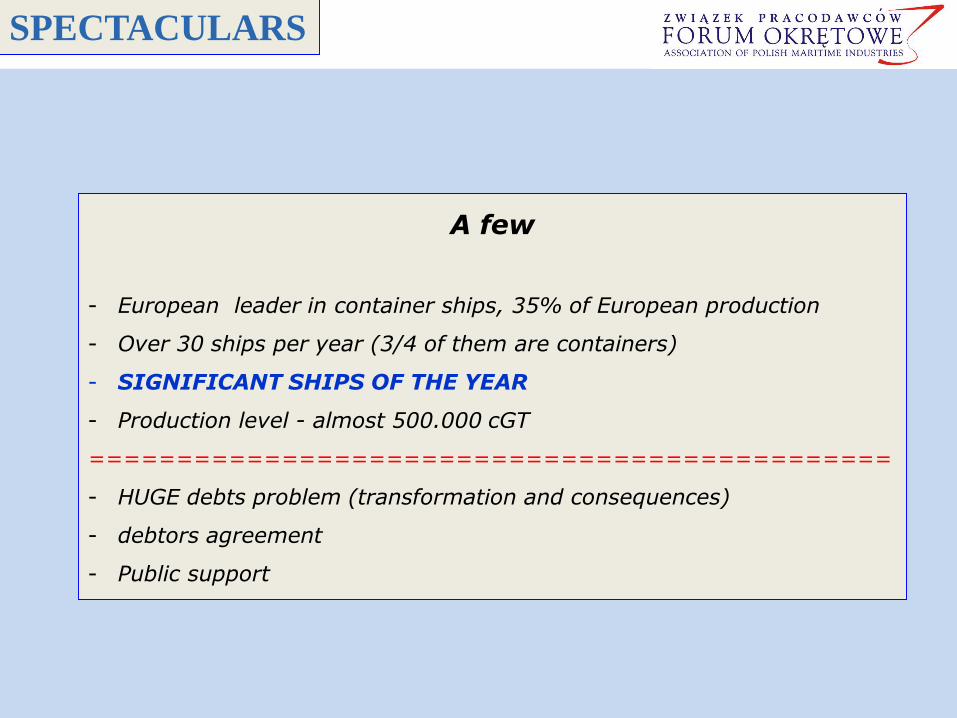

SPECTACULARS

A few

- European leader in container ships, 35% of European production

- Over 30 ships per year (3/4 of them are containers)

- SIGNIFICANT SHIPS OF THE YEAR

- Production level - almost 500.000 cGT

==============================================

- HUGE debts problem (transformation and consequences)

- debtors agreement

- Public support

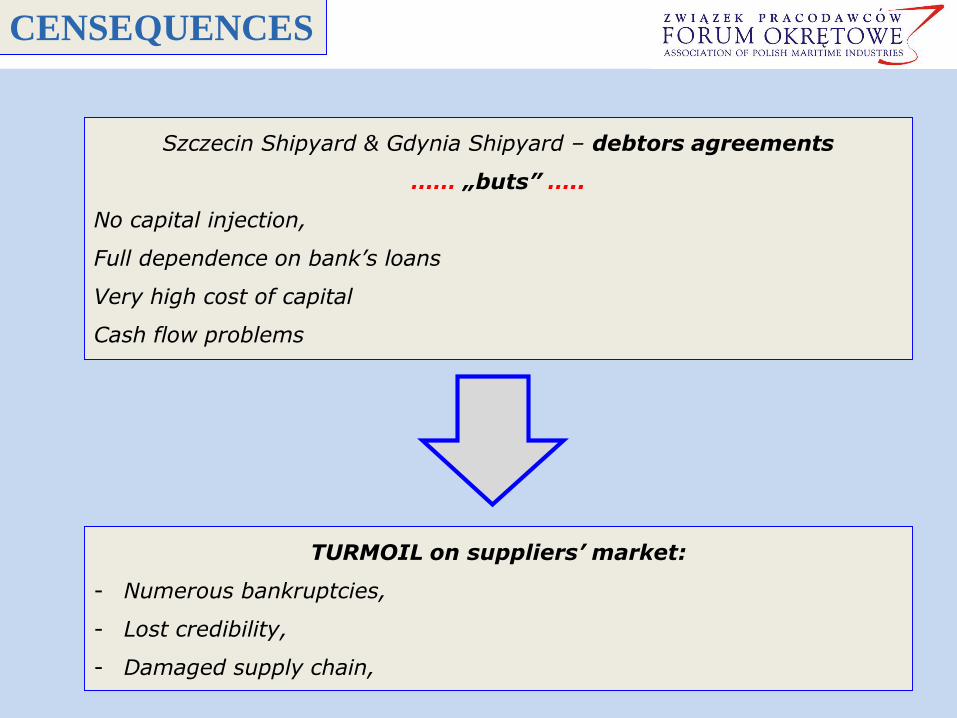

CENSEQUENCES

TURMOIL on suppliers’ market:

- Numerous bankruptcies,

- Lost credibility,

- Damaged supply chain,

Szczecin Shipyard & Gdynia Shipyard – debtors agreements

…… „buts” …..

No capital injection,

Full dependence on bank’s loans

Very high cost of capital

Cash flow problems

PRODUCTS

Containers:

2000TEU – ab.34 mln EUR 3,35 eur/kg

Cars:Fiat 126p - ab. 9400 zł4,61 eur/kg

Ford Mondeo 1,6 ab. 27.000DEM, 10,50 eur/kg

OBSERVATIONS

INTERNAL

- Low hour rate,

- Labour-intensive product

- LOW COST LEADER

EXTERNAL

- Poland negotiate OECD agreement

- cup of 600.000 cGT imposed on Poland

- cGT „cup policy” brought no success

- administrative way of controlling market brought no results

- supply-demand factors runs their own way

19901996

2001

No spectaculars

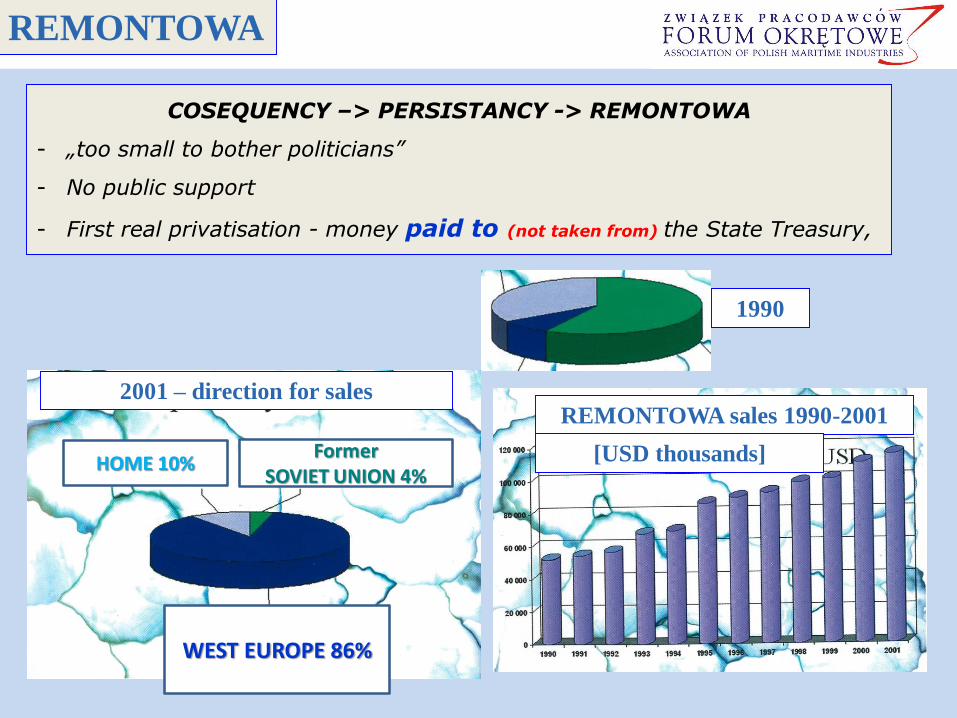

COSEQUENCY –> PERSISTANCY -> REMONTOWA

- „too small to bother politicians”

- No public support

- First real privatisation - money paid to (not taken from) the State Treasury,

REMONTOWA

2001 – direction for sales

Former SOVIET UNION 4%

HOME 10%

WEST EUROPE 86%

REMONTOWA sales 1990-2001

[USD thousands]

1990

19901996

2002

2001„checking”

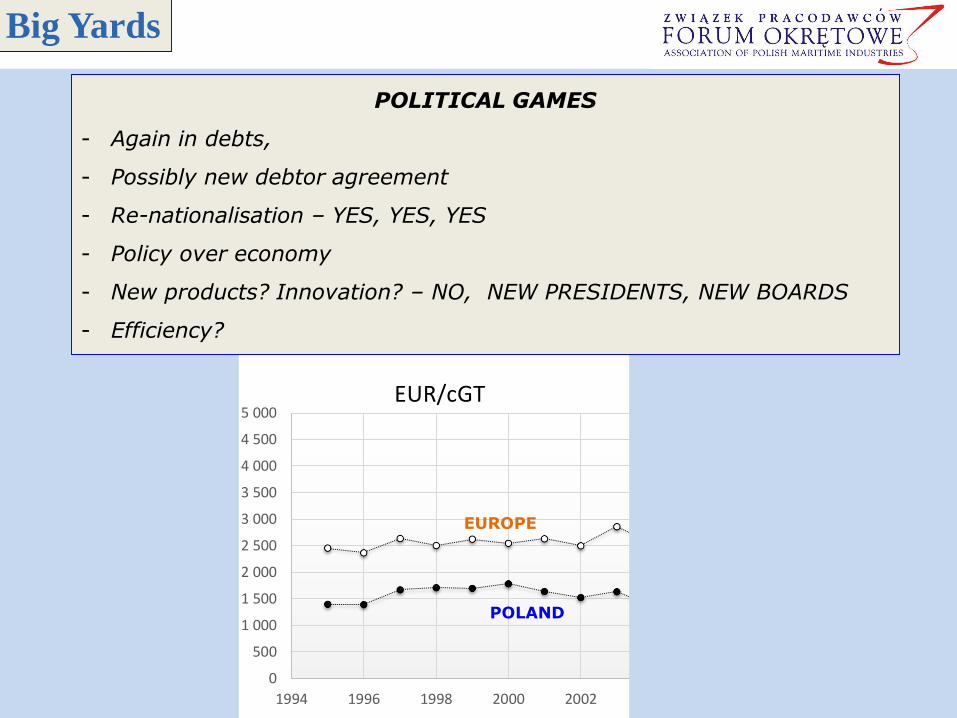

Big Yards

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

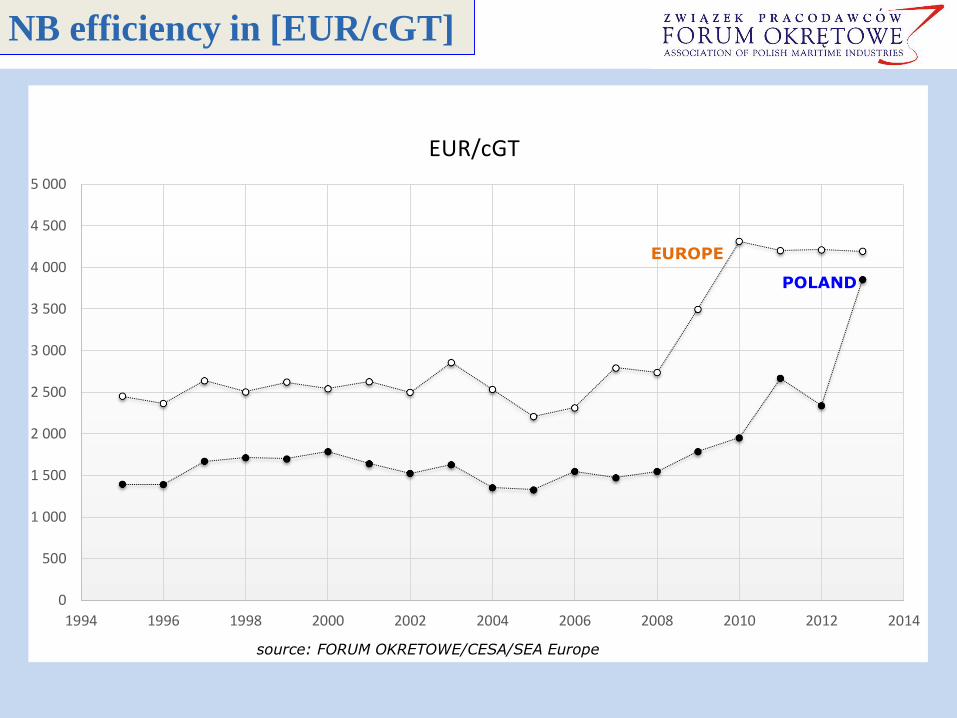

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

EUR/cGT

EUROPE

POLAND

POLITICAL GAMES

- Again in debts,

- Possibly new debtor agreement

- Re-nationalisation – YES, YES, YES

- Policy over economy

- New products? Innovation? – NO, NEW PRESIDENTS, NEW BOARDS

- Efficiency?

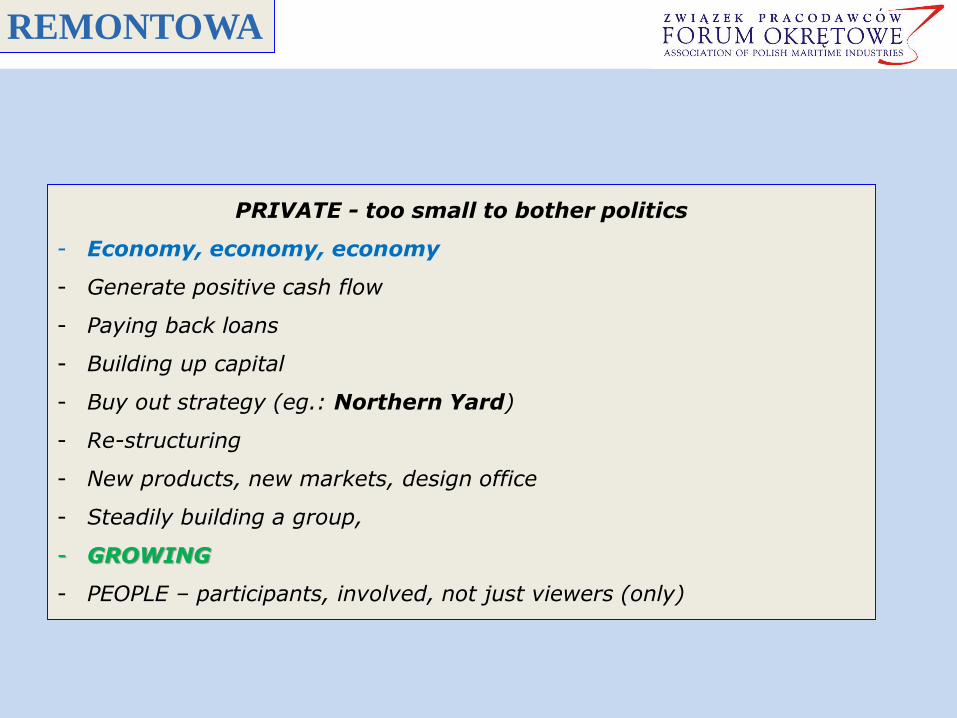

REMONTOWA

PRIVATE - too small to bother politics

- Economy, economy, economy

- Generate positive cash flow

- Paying back loans

- Building up capital

- Buy out strategy (eg.: Northern Yard)

- Re-structuring

- New products, new markets, design office

- Steadily building a group,

- GROWING

- PEOPLE – participants, involved, not just viewers (only)

19901996

2002

2001

2004

EU

2004 – joining EU

- No interim period for Polish shipbuilding/repair sector

- Low rank at negotiation table, („forgotten” sector),

- Facing all constrains, eg. free flow of people

- Any benefits for the sector ?

Source: REMONTOWA GALATEA - Buoy-Laying Vessel – 2007

19901996

2002

2001

2004

2008

Too big to fall down ? (really)?

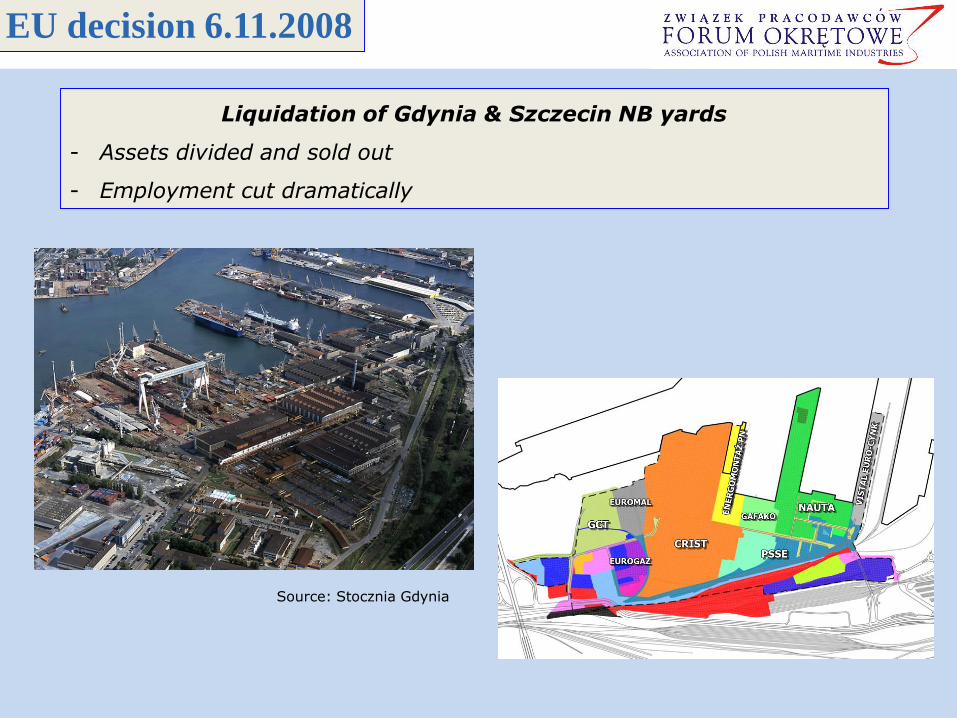

EU decision 6.11.2008

Liquidation of Gdynia & Szczecin NB yards

- Assets divided and sold out

- Employment cut dramatically

Source: Stocznia Gdynia

New business

Gdynia

- New opportunities

- New products

- Employment steadily growing

- Turnover reached „momentum”

Szczecin

- no significant success, yet ….

Source: Stocznia Gdynia/Crist

Source: FORUM OKRĘTOWE

19901996

2002

2001

2004

2008

2014

Specialisation and shifting into offshore

Source: REMONTOWA/FORUM OKRĘTOWE

Lloyd's List events & Lloyd's Maritime Academy2010 - Green Ship of the Year

Source: Sunreef Yachts

Source: REMONTOWA

Specialisation and shifting into offshore

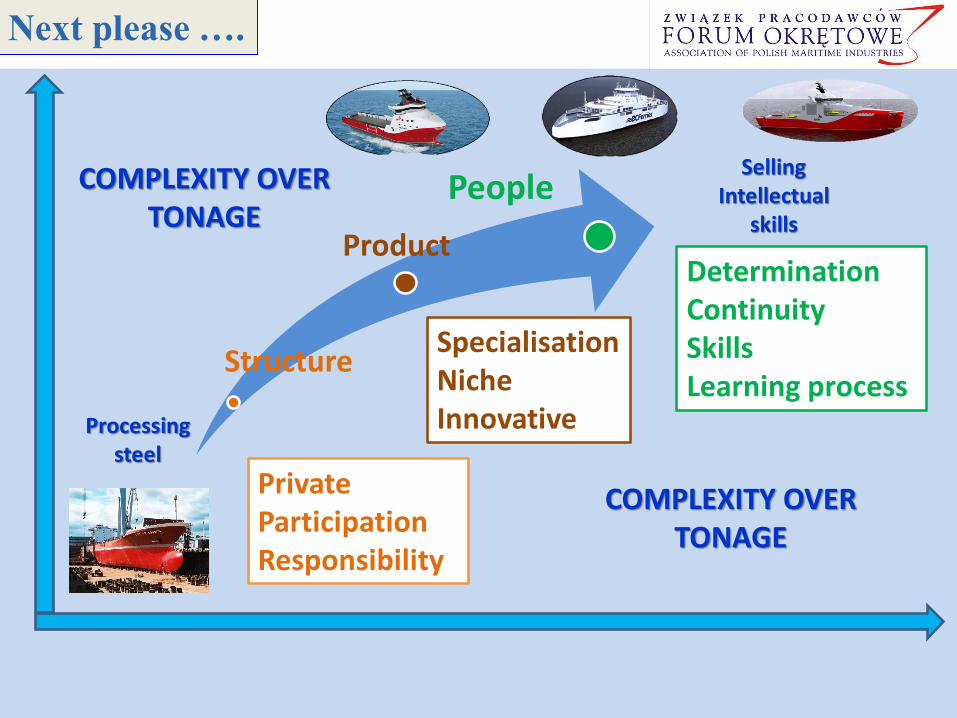

Next please ….

People

Structure

Product

PrivateParticipationResponsibility

SpecialisationNiche Innovative

DeterminationContinuitySkills Learning process

Processingsteel

Selling Intellectual

skills

COMPLEXITY OVER TONAGE

COMPLEXITY OVER TONAGE

NB efficiency in [EUR/cGT]

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

EUR/cGT

POLAND

EUROPE

source: FORUM OKRETOWE/CESA/SEA Europe

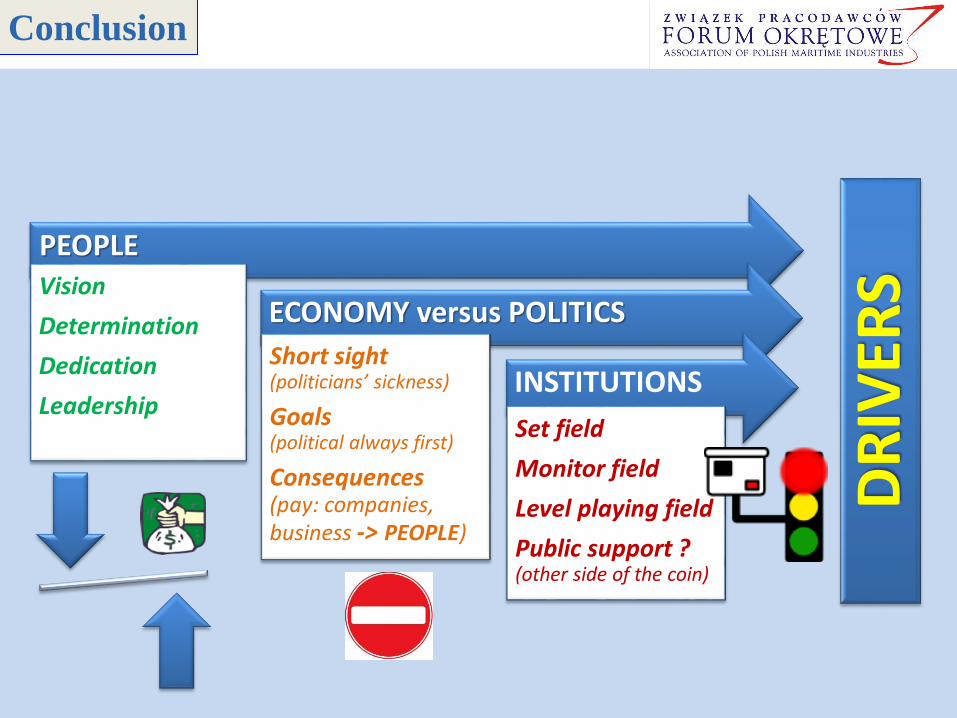

Conclusion

PEOPLEVision

Determination

Dedication

Leadership

ECONOMY versus POLITICS

Short sight (politicians’ sickness)

Goals(political always first)

Consequences(pay: companies, business -> PEOPLE)

INSTITUTIONS

Set field

Monitor field

Level playing field

Public support ? (other side of the coin)

DR

IVER

S

Thank you for your attention

www.forumokretowe.org.pl

Questions, Clarifications, Comments ?

WELCOME

Jerzy Czuczman

Sławomir Skrzypiński