vinci play presentation

TRANSCRIPT

A Case for Further Internationalization

• Company snapshot • Playground industry overview • Market Identification • Final Selection • Recommendations

Presentation Outline

Company Snapshot

Legal name Babycam International trading name Vinciplay

Employees 50 Year of founding 2009

Founder Pawel Chodkowski Managing Director Piotr Nadulne

Head Offices Warsaw, Poland Production and Warehousing facilities Lowicz, Poland

Exports to 15 countries References Skanska, Sheraton, Municipality of

Radom, etc.

Exclusivity agreements

preferred by construction companies

Strategic and economically

interesting partners

Contacts, trust and quality are

important factors for

manufacturers

Niche and highly linked to the construction

sector

Cost-efficient players from

countries with low-labor cost are

increasingly eating away at incumbent

players

Long-term relationships

Mature Industry

PLAYGROUND INDUSTRY OVERVIEW

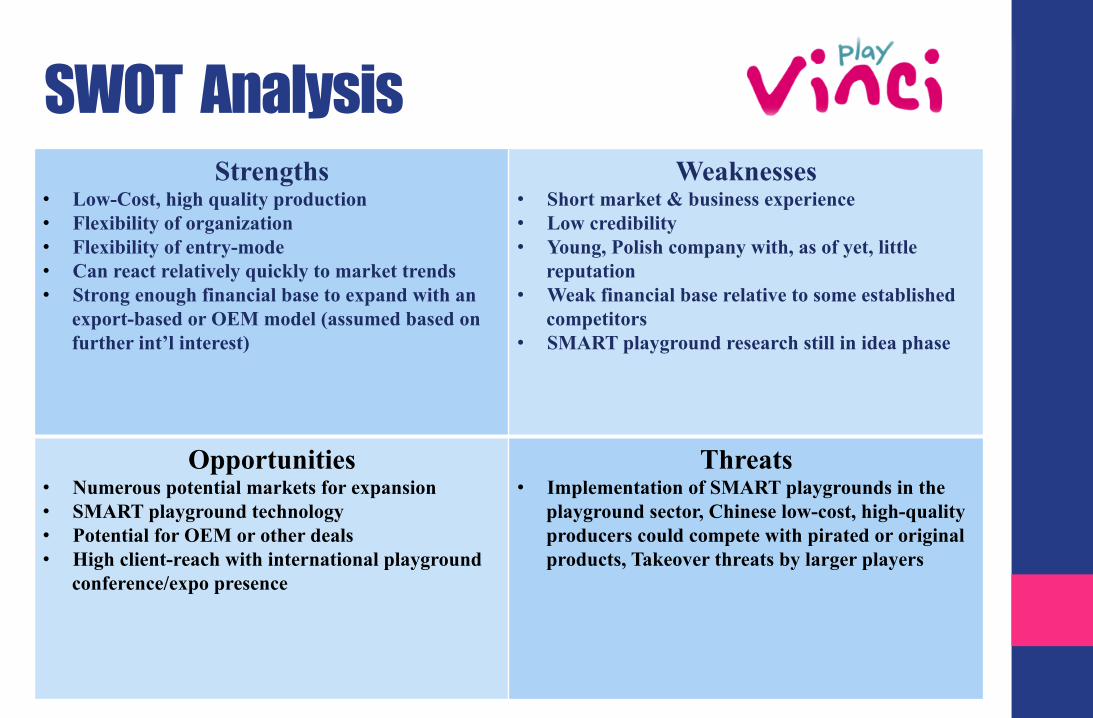

SWOT Analysis Strengths

• Low-Cost, high quality production • Flexibility of organization • Flexibility of entry-mode • Can react relatively quickly to market trends • Strong enough financial base to expand with an

export-based or OEM model (assumed based on further int’l interest)

Weaknesses • Short market & business experience • Low credibility • Young, Polish company with, as of yet, little

reputation • Weak financial base relative to some established

competitors • SMART playground research still in idea phase

Opportunities • Numerous potential markets for expansion • SMART playground technology • Potential for OEM or other deals • High client-reach with international playground

conference/expo presence

Threats • Implementation of SMART playgrounds in the

playground sector, Chinese low-cost, high-quality producers could compete with pirated or original products, Takeover threats by larger players

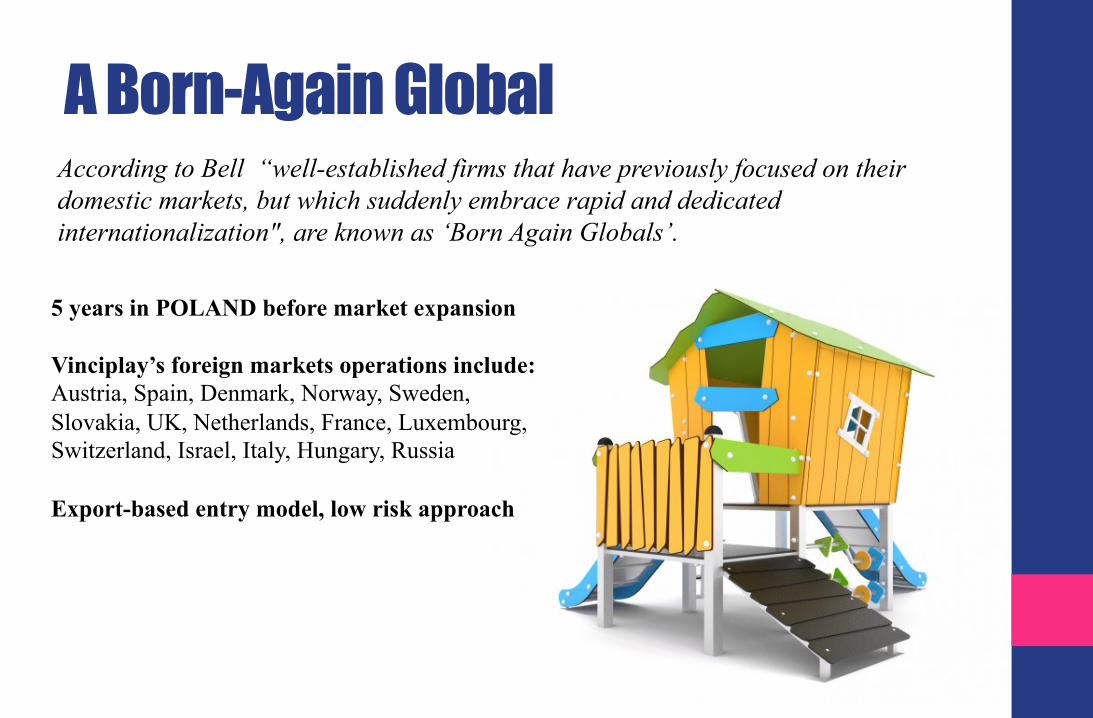

A Born-Again Global According to Bell “well-established firms that have previously focused on their domestic markets, but which suddenly embrace rapid and dedicated internationalization", are known as ‘Born Again Globals’.

5 years in POLAND before market expansion

Vinciplay’s foreign markets operations include: Austria, Spain, Denmark, Norway, Sweden, Slovakia, UK, Netherlands, France, Luxembourg, Switzerland, Israel, Italy, Hungary, Russia Export-based entry model, low risk approach

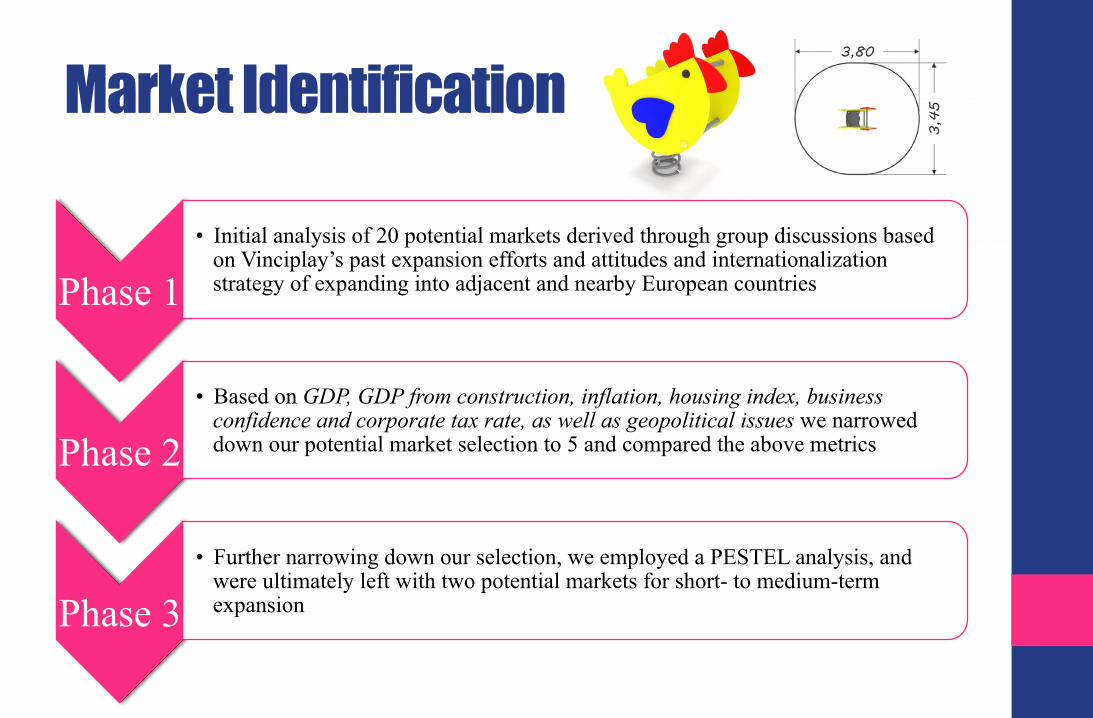

Market Identification

Phase 1 • Initial analysis of 20 potential markets derived through group discussions based

on Vinciplay’s past expansion efforts and attitudes and internationalization strategy of expanding into adjacent and nearby European countries

Phase 2 • Based on GDP, GDP from construction, inflation, housing index, business

confidence and corporate tax rate, as well as geopolitical issues we narrowed down our potential market selection to 5 and compared the above metrics

Phase 3 • Further narrowing down our selection, we employed a PESTEL analysis, and

were ultimately left with two potential markets for short- to medium-term expansion

Phase 1 Phase 2 Germany

Sweden

Switzerland

China

United States

Latvia

Lithuania

Estonia

Azerbaijan

Russia

Mexico

Portugal

Japan

Turkey

Kazakhstan

Italy

South Korea

• Germany • Italy • Turkey • United States • Estonia • Lithuania • Latvia

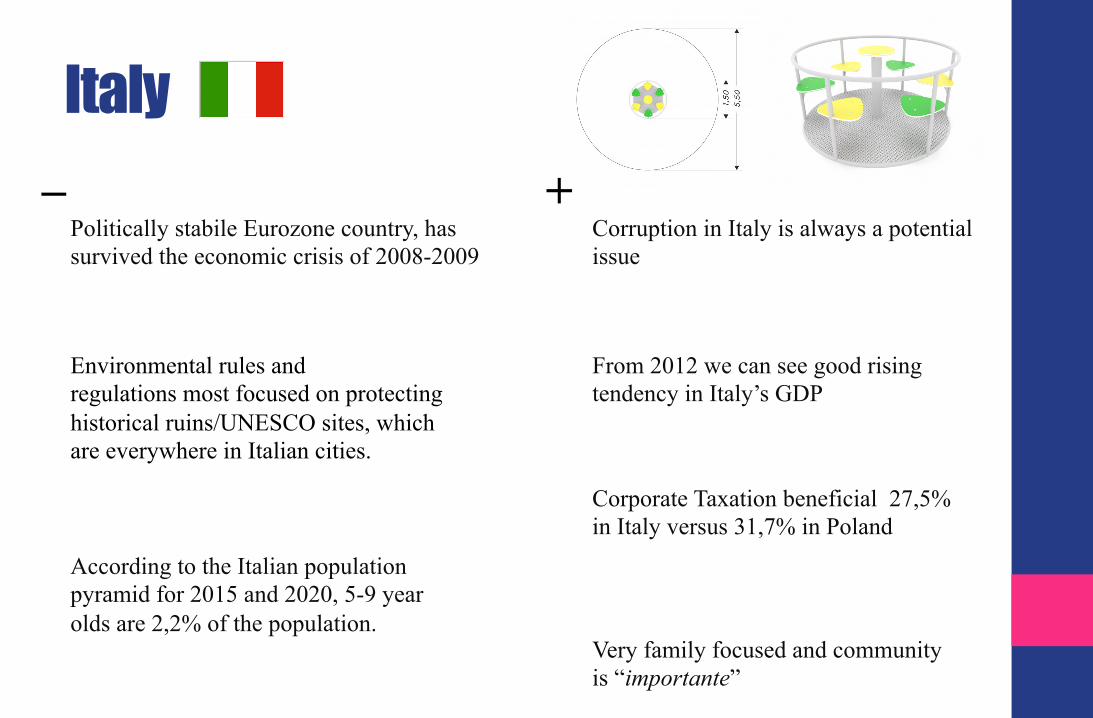

Italy

Politically stabile Eurozone country, has survived the economic crisis of 2008-2009

Corruption in Italy is always a potential issue

From 2012 we can see good rising tendency in Italy’s GDP

Corporate Taxation beneficial 27,5% in Italy versus 31,7% in Poland

Very family focused and community is “importante”

Environmental rules and regulations most focused on protecting historical ruins/UNESCO sites, which are everywhere in Italian cities.

According to the Italian population pyramid for 2015 and 2020, 5-9 year olds are 2,2% of the population.

+ _

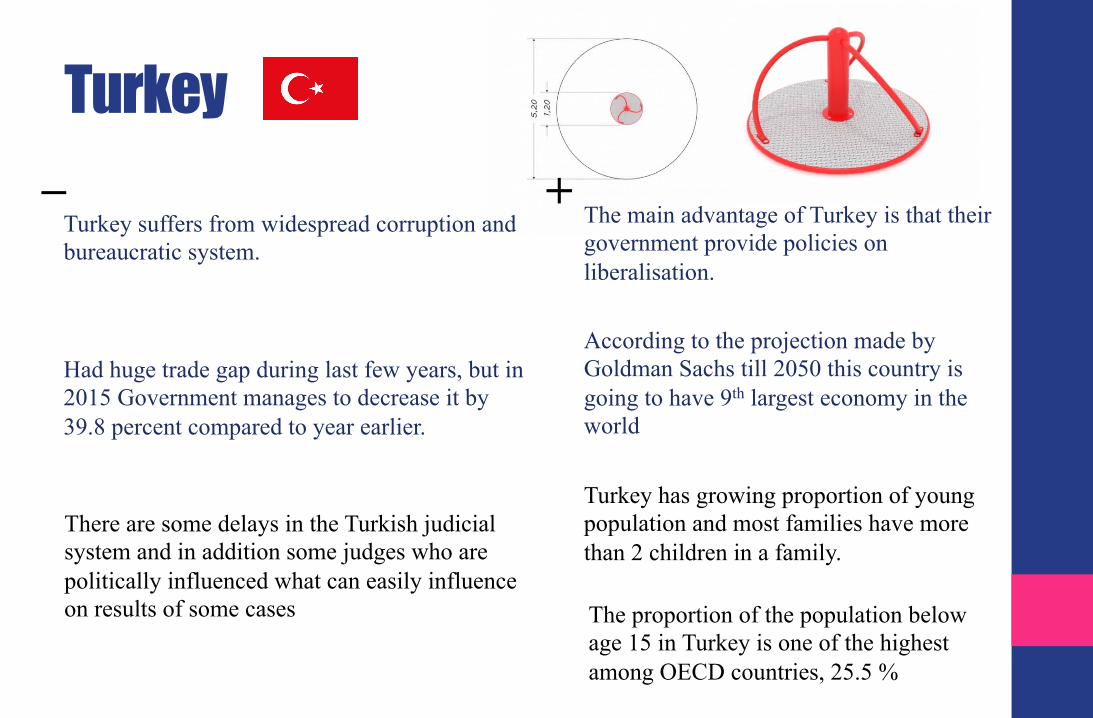

Turkey The main advantage of Turkey is that their government provide policies on liberalisation.

Turkey suffers from widespread corruption and bureaucratic system.

According to the projection made by Goldman Sachs till 2050 this country is going to have 9th largest economy in the world

+ _

Had huge trade gap during last few years, but in 2015 Government manages to decrease it by 39.8 percent compared to year earlier.

Turkey has growing proportion of young population and most families have more than 2 children in a family. The proportion of the population below age 15 in Turkey is one of the highest among OECD countries, 25.5 %

There are some delays in the Turkish judicial system and in addition some judges who are politically influenced what can easily influence on results of some cases

Baltics

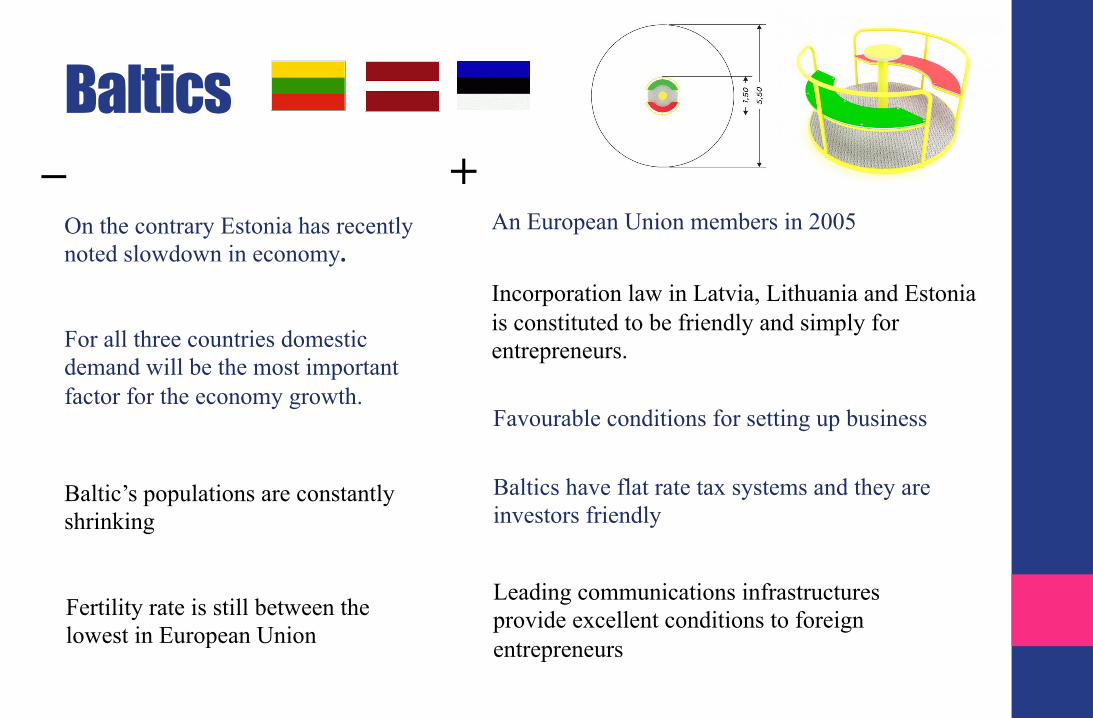

Incorporation law in Latvia, Lithuania and Estonia is constituted to be friendly and simply for entrepreneurs.

An European Union members in 2005

+ _ On the contrary Estonia has recently noted slowdown in economy.

Favourable conditions for setting up business

Baltics have flat rate tax systems and they are investors friendly

For all three countries domestic demand will be the most important factor for the economy growth.

Baltic’s populations are constantly shrinking

Leading communications infrastructures provide excellent conditions to foreign entrepreneurs

Fertility rate is still between the lowest in European Union

USA

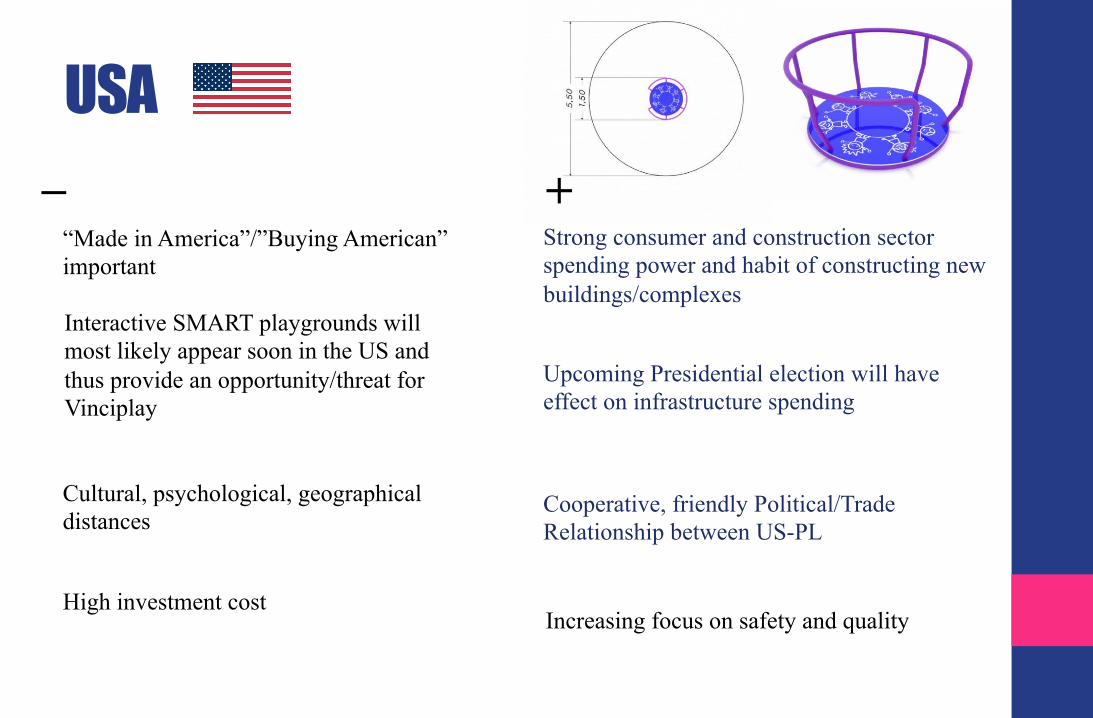

Strong consumer and construction sector spending power and habit of constructing new buildings/complexes

“Made in America”/”Buying American” important Interactive SMART playgrounds will most likely appear soon in the US and thus provide an opportunity/threat for Vinciplay

+ _

Upcoming Presidential election will have effect on infrastructure spending

Cooperative, friendly Political/Trade Relationship between US-PL

Cultural, psychological, geographical distances

High investment cost Increasing focus on safety and quality

Germany + _

Increases in public investment in infrastructure Economic activity has not been stable

Business investments have disappointed The federal government has made EUR 600 million available for further urban development over the period 2014-2015

Since 2002 Germany has an aging population.

The population will fall to 65 million people

High standard of living and social security

Largest population in the EU

Germany and Poland having strong trading relations

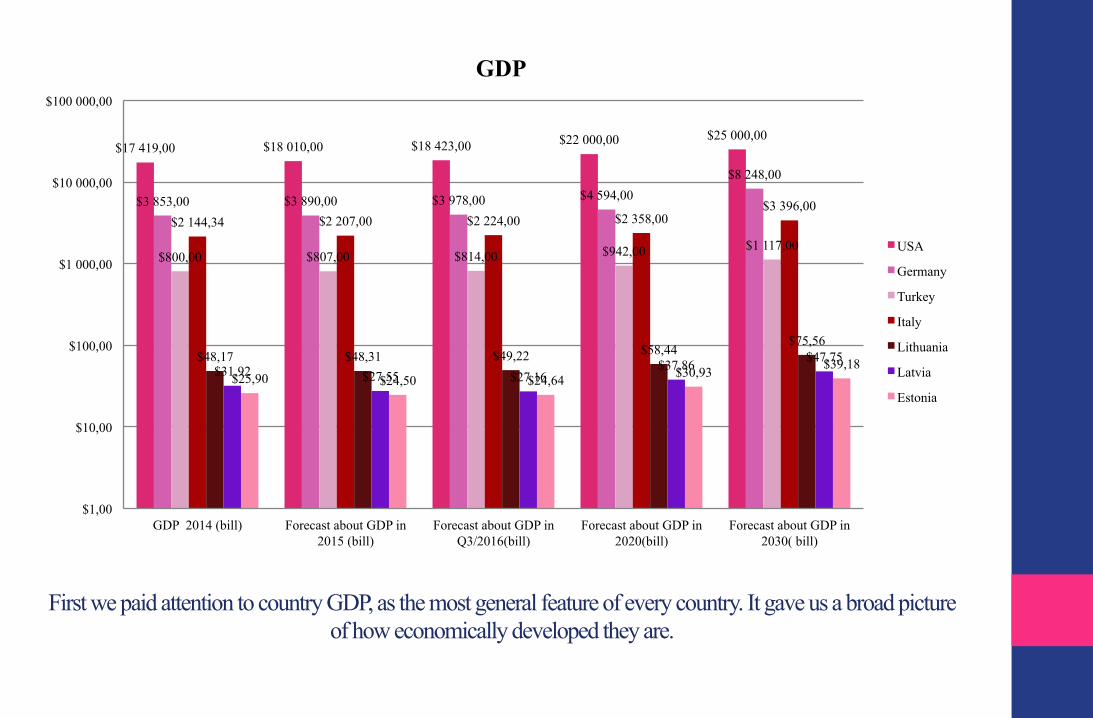

First we paid attention to country GDP, as the most general feature of every country. It gave us a broad picture of how economically developed they are.

$17 419,00 $18 010,00 $18 423,00 $22 000,00 $25 000,00

$3 853,00 $3 890,00 $3 978,00 $4 594,00 $8 248,00

$800,00 $807,00 $814,00 $942,00 $1 117,00

$2 144,34 $2 207,00 $2 224,00 $2 358,00 $3 396,00

$48,17 $48,31 $49,22 $58,44 $75,56

$31,92 $27,55 $27,16 $37,86 $47,75

$25,90 $24,50 $24,64 $30,93 $39,18

$1,00

$10,00

$100,00

$1 000,00

$10 000,00

$100 000,00

GDP 2014 (bill) Forecast about GDP in 2015 (bill)

Forecast about GDP in Q3/2016(bill)

Forecast about GDP in 2020(bill)

Forecast about GDP in 2030( bill)

GDP

USA

Germany

Turkey

Italy

Lithuania

Latvia

Estonia

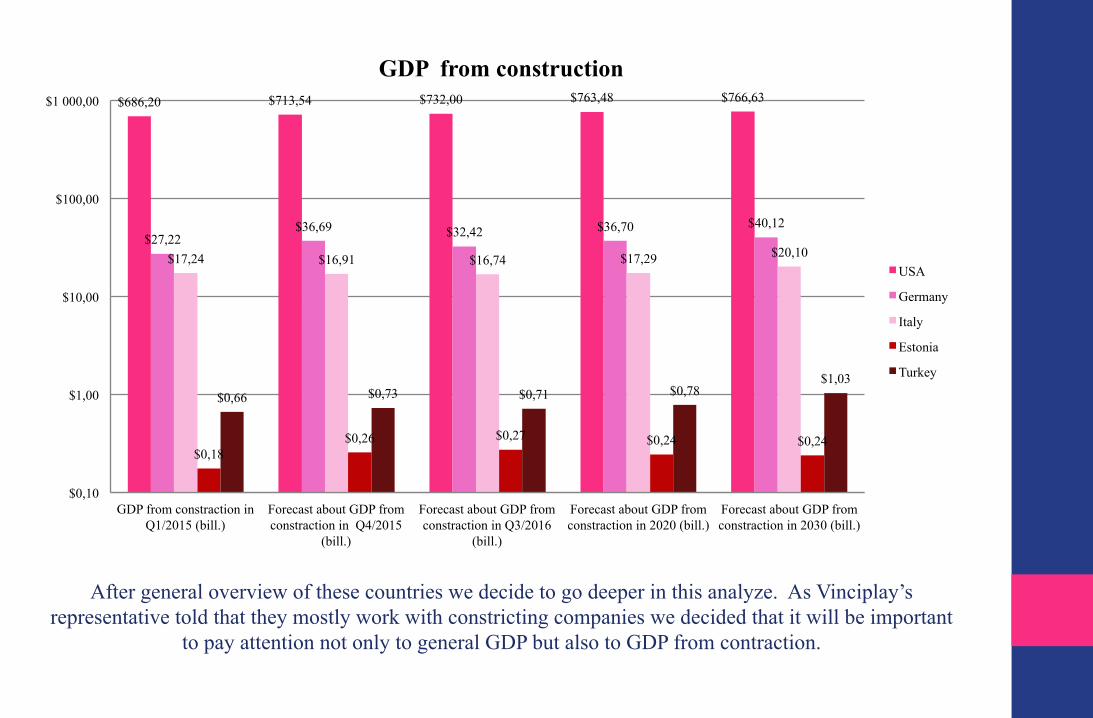

After general overview of these countries we decide to go deeper in this analyze. As Vinciplay’s representative told that they mostly work with constricting companies we decided that it will be important

to pay attention not only to general GDP but also to GDP from contraction.

$686,20 $713,54 $732,00 $763,48 $766,63

$27,22 $36,69 $32,42 $36,70 $40,12

$17,24 $16,91 $16,74 $17,29 $20,10

$0,18 $0,26 $0,27 $0,24 $0,24

$0,66 $0,73 $0,71 $0,78 $1,03

$0,10

$1,00

$10,00

$100,00

$1 000,00

GDP from constraction in Q1/2015 (bill.)

Forecast about GDP from constraction in Q4/2015

(bill.)

Forecast about GDP from constraction in Q3/2016

(bill.)

Forecast about GDP from constraction in 2020 (bill.)

Forecast about GDP from constraction in 2030 (bill.)

GDP from construction

USA

Germany

Italy

Estonia

Turkey

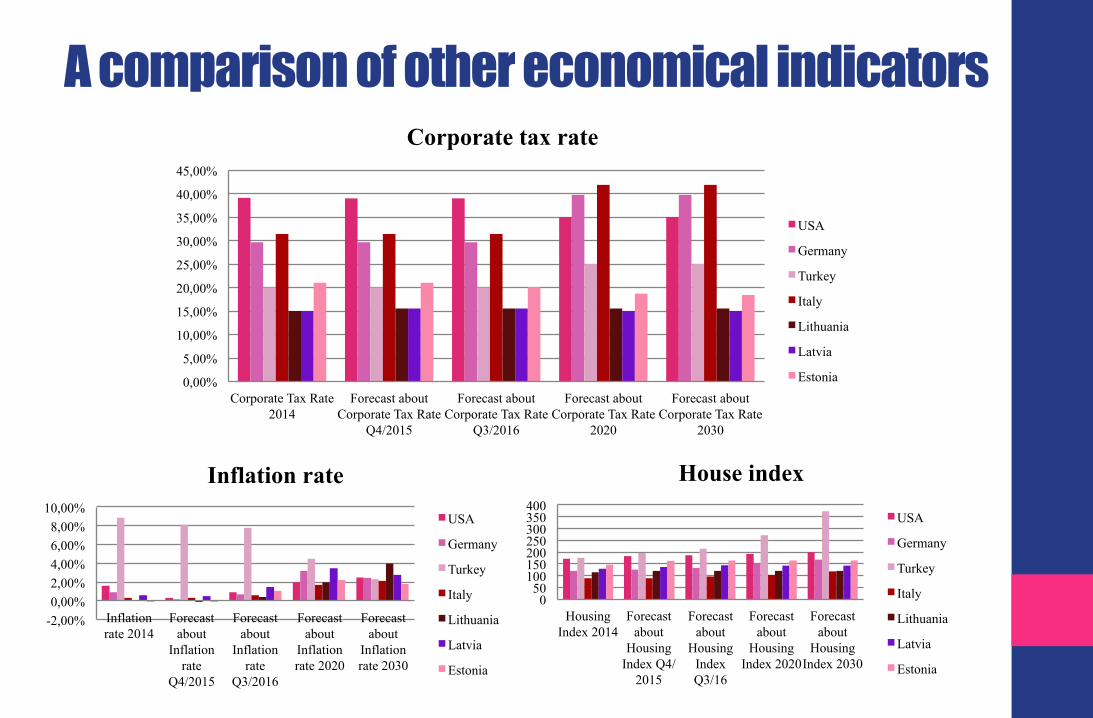

A comparison of other economical indicators

-2,00% 0,00% 2,00% 4,00% 6,00% 8,00%

10,00%

Inflation rate 2014

Forecast about

Inflation rate

Q4/2015

Forecast about

Inflation rate

Q3/2016

Forecast about

Inflation rate 2020

Forecast about

Inflation rate 2030

Inflation rate

USA

Germany

Turkey

Italy

Lithuania

Latvia

Estonia

0 50

100 150 200 250 300 350 400

Housing Index 2014

Forecast about

Housing Index Q4/

2015

Forecast about

Housing Index Q3/16

Forecast about

Housing Index 2020

Forecast about

Housing Index 2030

House index

USA

Germany

Turkey

Italy

Lithuania

Latvia

Estonia

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

45,00%

Corporate Tax Rate 2014

Forecast about Corporate Tax Rate

Q4/2015

Forecast about Corporate Tax Rate

Q3/2016

Forecast about Corporate Tax Rate

2020

Forecast about Corporate Tax Rate

2030

Corporate tax rate

USA

Germany

Turkey

Italy

Lithuania

Latvia

Estonia

Germany Phase 3 • 5+1 Porter’s analysis • Recomendations • Quastions to potential partners • PPP

• Am lot of big players are active • The new company needs a “German” profile • The relative maturity of the playground market • A niche market, which may hamper transparency and knowledge about operating

Threat of New Entrants: Medium

Intensity of Rivalry: High

• Polish companies are perceived of manufacturing lower quality good by German customers

• Significant customer loyalty to local and German manufacturer • price is a very sensitive topic, and especially for organizations with budget restraints

Bargaining Power of Buyers: High

Threat of Substitutes: Medium

• The power of suppliers of standardized goods is low • Some suppliers may be pressed for exclusivity

Bargaining Power of Suppliers: Medium

Complementary Products: Weak

Small local and large global players in this industry SMART playgrounds are being researched by incumbents Offer high quality products as Germans are very quality and reputation conscious In the German playground industry, wood is preferred compared to steel Playground equipment manufacturers are selling equipment worldwide and may transfer and apply learning benefits to the German market

Entertainment centres for kids, e.g. parks, water parks, playing indoor or outdoor, malls, arcades New toys and devices

No noteworthy complementary factors

• Partners from trade fairs (November 2015 – indefinitely) • Partners from the construction industry (specifically Public-Private

Partnerships) (November 2015 – Indefinitely) • Municipalities & government entities (June 2016 - Indefinitely)

Contact:

Recommendations

• CSR • Wooden playgrounds

Aditionally:

• Email and call • Physical meeting

How:

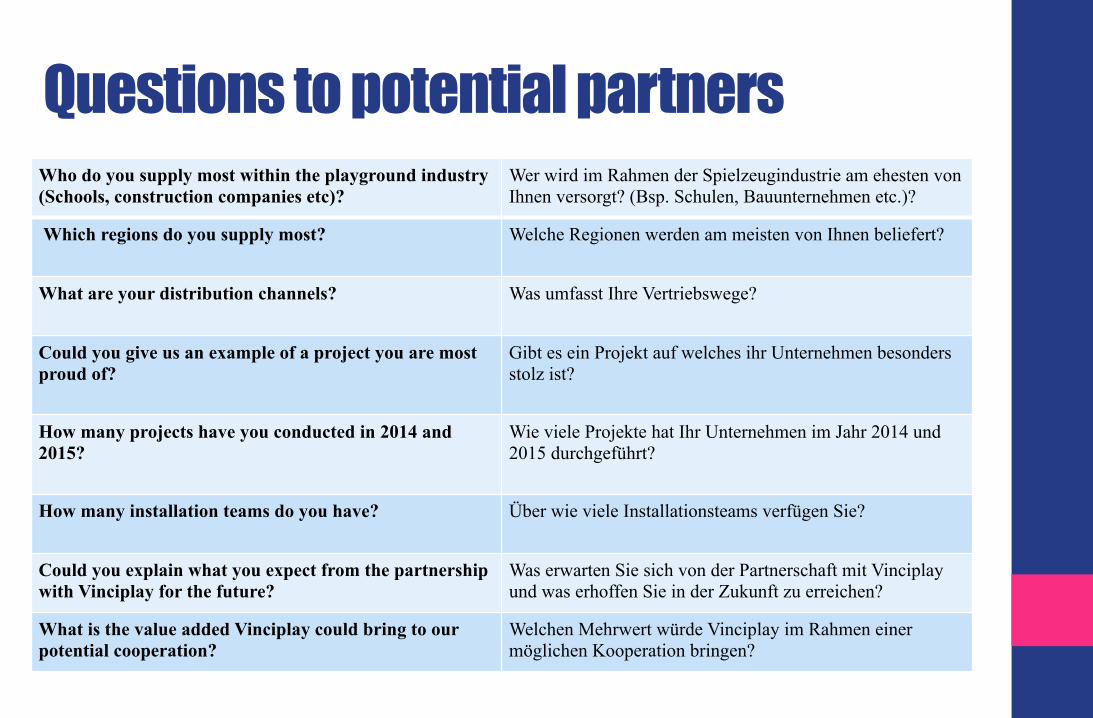

Questions to potential partners Who do you supply most within the playground industry (Schools, construction companies etc)?

Wer wird im Rahmen der Spielzeugindustrie am ehesten von Ihnen versorgt? (Bsp. Schulen, Bauunternehmen etc.)?

Which regions do you supply most? Welche Regionen werden am meisten von Ihnen beliefert?

What are your distribution channels?

Was umfasst Ihre Vertriebswege?

Could you give us an example of a project you are most proud of?

Gibt es ein Projekt auf welches ihr Unternehmen besonders stolz ist?

How many projects have you conducted in 2014 and 2015?

Wie viele Projekte hat Ihr Unternehmen im Jahr 2014 und 2015 durchgeführt?

How many installation teams do you have?

Über wie viele Installationsteams verfügen Sie?

Could you explain what you expect from the partnership with Vinciplay for the future?

Was erwarten Sie sich von der Partnerschaft mit Vinciplay und was erhoffen Sie in der Zukunft zu erreichen?

What is the value added Vinciplay could bring to our potential cooperation?

Welchen Mehrwert würde Vinciplay im Rahmen einer möglichen Kooperation bringen?

Private Public Partnership Germany schools are seen to be long overdue with their renovations

Money is missing for schools to be renovated.

Due to ‘Public Private Partnership’ the renovations are made possible.

The experiment started in 2007, in Frankfurt, including 4 schools.

Hochtief, took the responsibility for the next 20 years, to be in charge of the building, renovating, and investing 250 million euros.

In return for this, the city pays the company a 13 million Euros lease payment.

Construction company needs to guarantee quality for the next 20 years (Vinciplay even offering 30 years of quality guarantee)

United States Phase 3 • 5+1 Porter’s analysis • recomendations

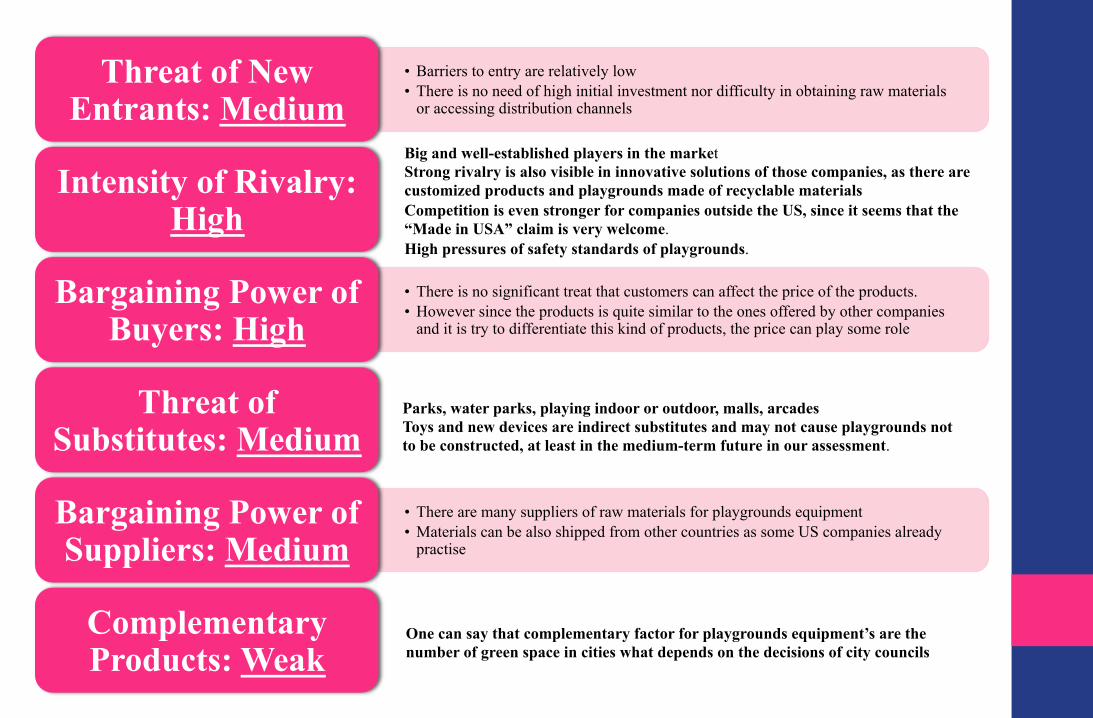

• Barriers to entry are relatively low • There is no need of high initial investment nor difficulty in obtaining raw materials

or accessing distribution channels

Threat of New Entrants: Medium

Intensity of Rivalry: High

• There is no significant treat that customers can affect the price of the products. • However since the products is quite similar to the ones offered by other companies

and it is try to differentiate this kind of products, the price can play some role

Bargaining Power of Buyers: High

Threat of Substitutes: Medium

• There are many suppliers of raw materials for playgrounds equipment • Materials can be also shipped from other countries as some US companies already

practise

Bargaining Power of Suppliers: Medium

Complementary Products: Weak

Big and well-established players in the market Strong rivalry is also visible in innovative solutions of those companies, as there are customized products and playgrounds made of recyclable materials Competition is even stronger for companies outside the US, since it seems that the “Made in USA” claim is very welcome. High pressures of safety standards of playgrounds.

Parks, water parks, playing indoor or outdoor, malls, arcades Toys and new devices are indirect substitutes and may not cause playgrounds not to be constructed, at least in the medium-term future in our assessment.

One can say that complementary factor for playgrounds equipment’s are the number of green space in cities what depends on the decisions of city councils

• Partners from trade fairs • Partners from the construction industry • Municipalities & government entities

Contact:

Recommendations

• CSR • SMART playgrounds • Assembled in U.S.A.

Aditionally:

• Email and call • Physical meeting • Warehouse (average cost 53,

815$ for 1000m2)

How:

Q & A