visa inc. overvie · visa inc. overview august 2010 ... 2008. visa confidential. a 50-year history...

TRANSCRIPT

Visa Inc. OverviewAugust 2010

DisclaimerThe following materials and management’s discussion of them may contain “forward- looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements can be identified by the terms “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will” and similar expressions that are intended to identify forward-looking statements. In addition, any underlying assumptions are forward-looking statements. Such forward- looking statements include but are not limited to statements regarding certain of Visa’s goals and expectations with respect to adjusted earnings per share, revenue, adjusted operating margin and free cash flow and the growth rate in those items, as well as other measures of economic performance.By their nature, forward-looking statements: (i) speak only as of the date they are made, (ii) are not guarantees of future performance or results and (iii) are subject to risks, uncertainties and assumptions that are difficult to predict or quantify. Therefore, actual results could differ materially and adversely from those forward-looking statements as a result of a variety of factors, including all the factors detailed from time to time in Visa’s reports filed with the U.S. Securities Exchange Commission, including Visa’s quarterly reports on Form 10-Q and its annual report on Form 10-K. You are cautioned not to place undue reliance on such statements, which speak only as of the date of this presentation. Unless required to do so under U.S. federal securities laws or other applicable laws, we do not intend to update or revise any forward-looking statements.

2

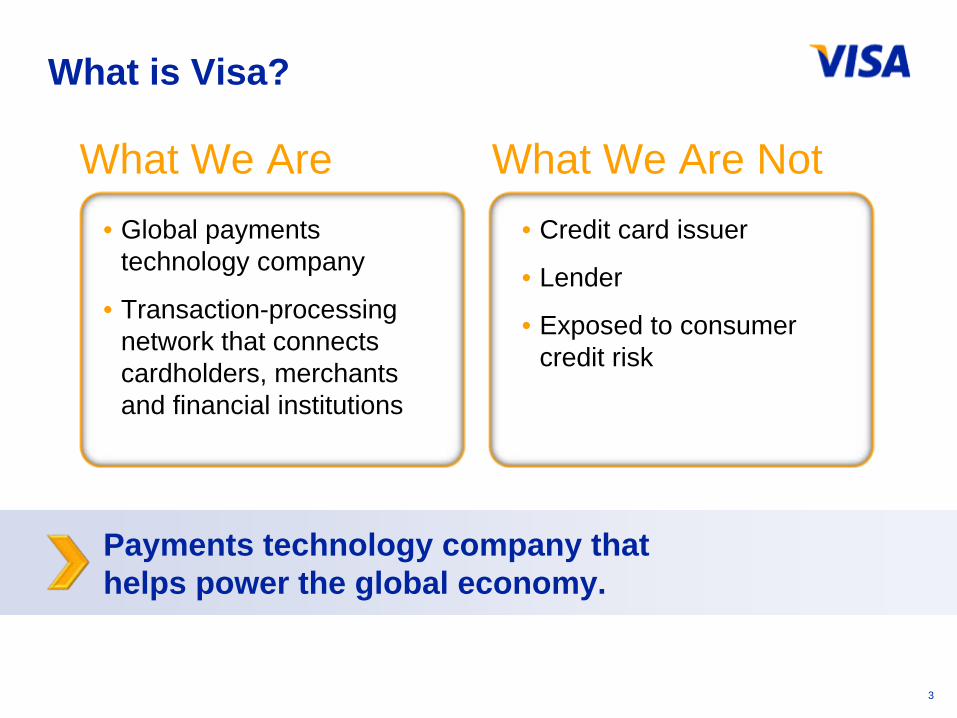

What We Are Not

Payments technology company that helps power the global economy.

What is Visa?

3

What We Are• Credit card issuer

• Lender

• Exposed to consumer credit risk

• Global payments technology company

• Transaction-processing network that connects cardholders, merchants and financial institutions

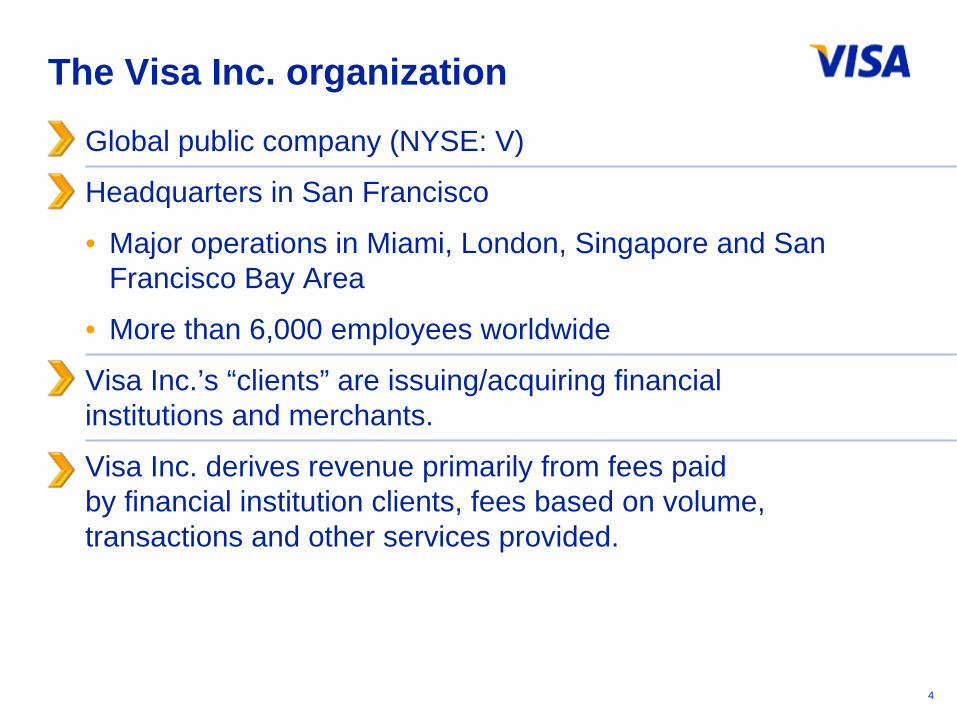

The Visa Inc. organization

Global public company (NYSE: V)

Headquarters in San Francisco

• Major operations in Miami, London, Singapore and San Francisco Bay Area

• More than 6,000 employees worldwide

Visa Inc.’s “clients” are issuing/acquiring financial institutions and merchants.

Visa Inc. derives revenue primarily from fees paid by financial institution clients, fees based on volume, transactions and other services provided.

4

1958 1976 1987 1997 2008

Visa Confidential

A 50-year history

5

Bank of America launches BankAmericard, the first general purpose card program, in California

National BankAmericard Inc., an association of financial institutions, changes its name to Visa and introduces the first debit card

Visa introduces multi-currency clearing and settlement, increasing transaction efficiency

Total payments volume passes US$1 trillion globally

Visa lists on the New York Stock Exchange under the ticker symbol “V” and raises US$19.7 billion in the largest initial public offering in U.S. history

2008U.S. debit payments volume eclipsed that of credit for the first time in the quarter ending December 31, 2008

6

Visa Inc. Operates the

world’s largest retail electronic

payments network1

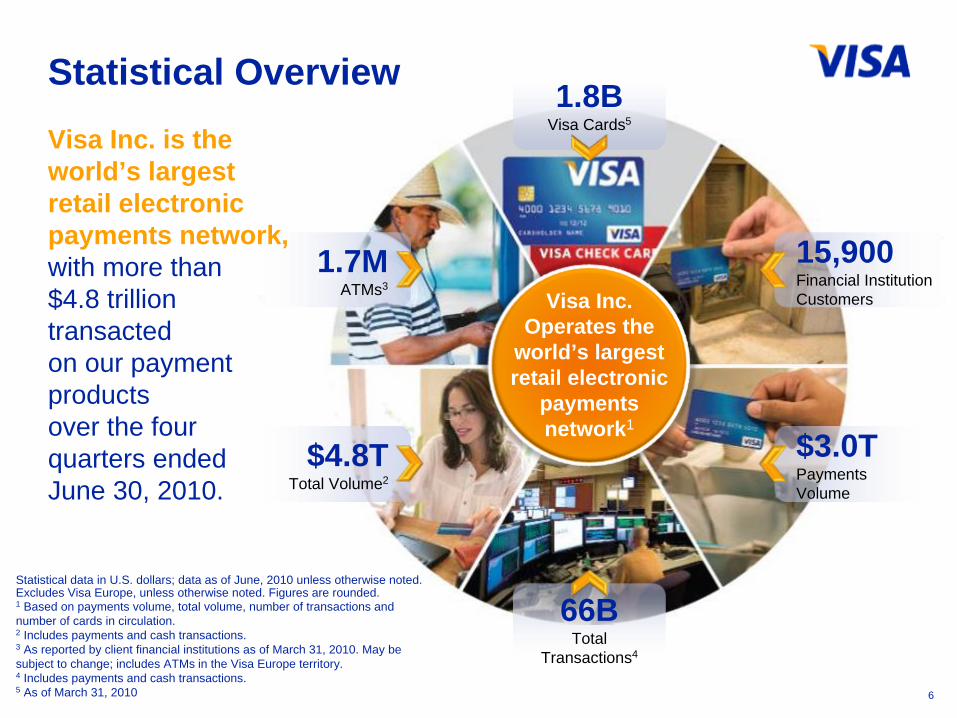

$4.8TTotal Volume2

$3.0TPayments Volume

66BTotal

Transactions4

1.8BVisa Cards5

1.7MATMs3

15,900Financial Institution Customers

Statistical OverviewVisa Inc. is the world’s largest retail electronic payments network, with more than $4.8 trillion transacted on our payment products over the four quarters ended June 30, 2010.

Statistical data in U.S. dollars; data as of June, 2010 unless otherwise noted.Excludes Visa Europe, unless otherwise noted. Figures are rounded.1 Based on payments volume, total volume, number of transactions and number of cards in circulation.2 Includes payments and cash transactions.3 As reported by client financial institutions as of March 31, 2010. May be subject to change; includes ATMs in the Visa Europe territory.4 Includes payments and cash transactions.5 As of March 31, 2010

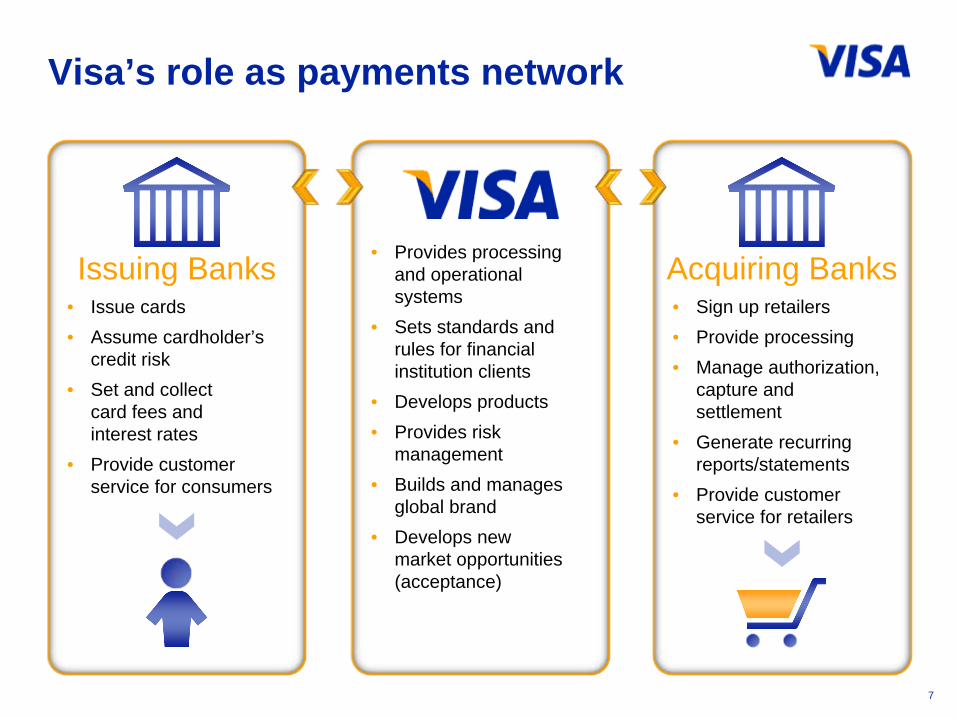

• Provides processing and operational systems

• Sets standards and rules for financial institution clients

• Develops products• Provides risk

management• Builds and manages

global brand• Develops new

market opportunities (acceptance)

• Issue cards• Assume cardholder’s

credit risk• Set and collect

card fees and interest rates

• Provide customer service for consumers

Issuing Banks• Sign up retailers• Provide processing• Manage authorization,

capture and settlement

• Generate recurring reports/statements

• Provide customer service for retailers

Acquiring Banks

Visa’s role as payments network

7

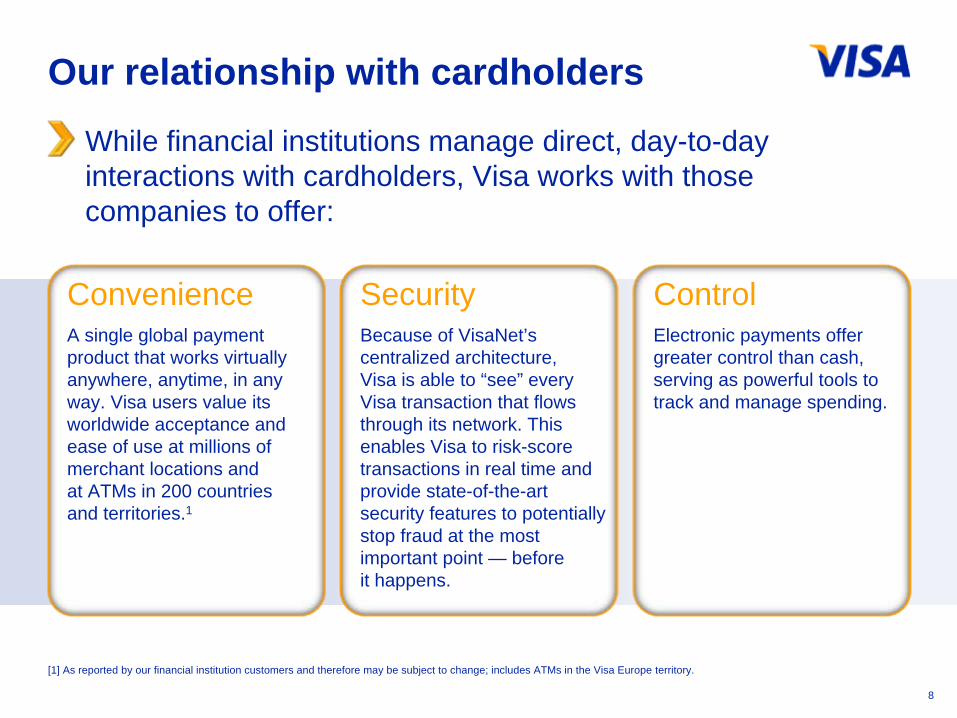

Our relationship with cardholders

While financial institutions manage direct, day-to-day interactions with cardholders, Visa works with those companies to offer:

ConvenienceA single global payment product that works virtually anywhere, anytime, in any way. Visa users value its worldwide acceptance and ease of use at millions of merchant locations and at ATMs in 200 countries and territories.1

SecurityBecause of VisaNet’s centralized architecture, Visa is able to “see” every Visa transaction that flows through its network. This enables Visa to risk-score transactions in real time and provide state-of-the-art security features to potentially stop fraud at the most important point — before it happens.

ControlElectronic payments offer greater control than cash, serving as powerful tools to track and manage spending.

[1] As reported by our financial institution customers and therefore may be subject to change; includes ATMs in the Visa Europe territory.

8

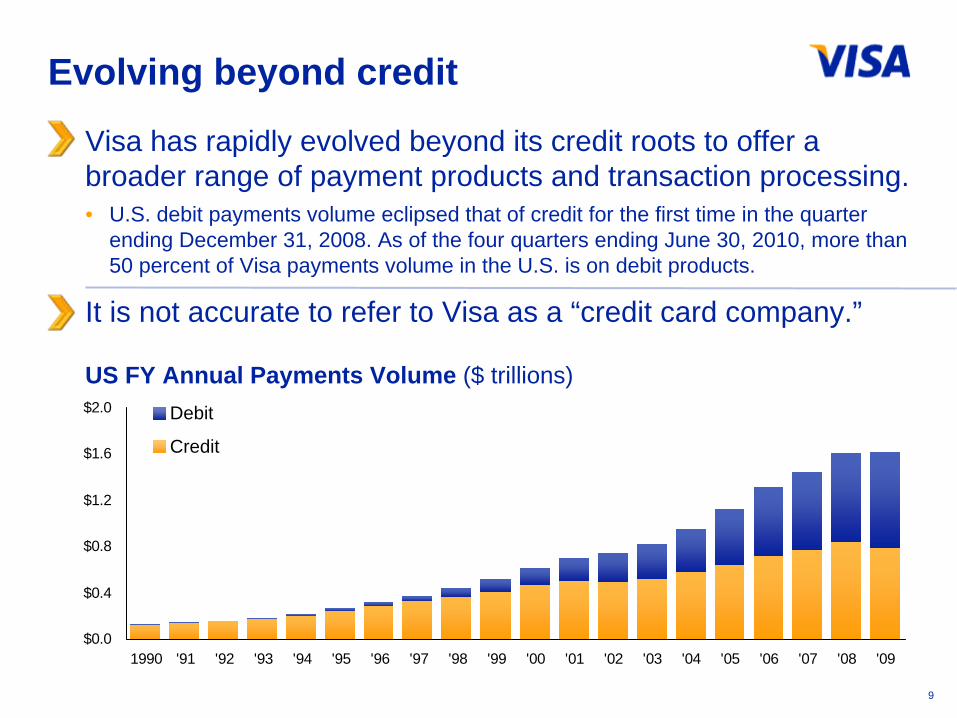

Evolving beyond credit

Visa has rapidly evolved beyond its credit roots to offer a broader range of payment products and transaction processing.• U.S. debit payments volume eclipsed that of credit for the first time in the quarter

ending December 31, 2008. As of the four quarters ending June 30, 2010, more than 50 percent of Visa payments volume in the U.S. is on debit products.

It is not accurate to refer to Visa as a “credit card company.”

9

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09

US FY Annual Payments Volume ($ trillions)Debit

Credit

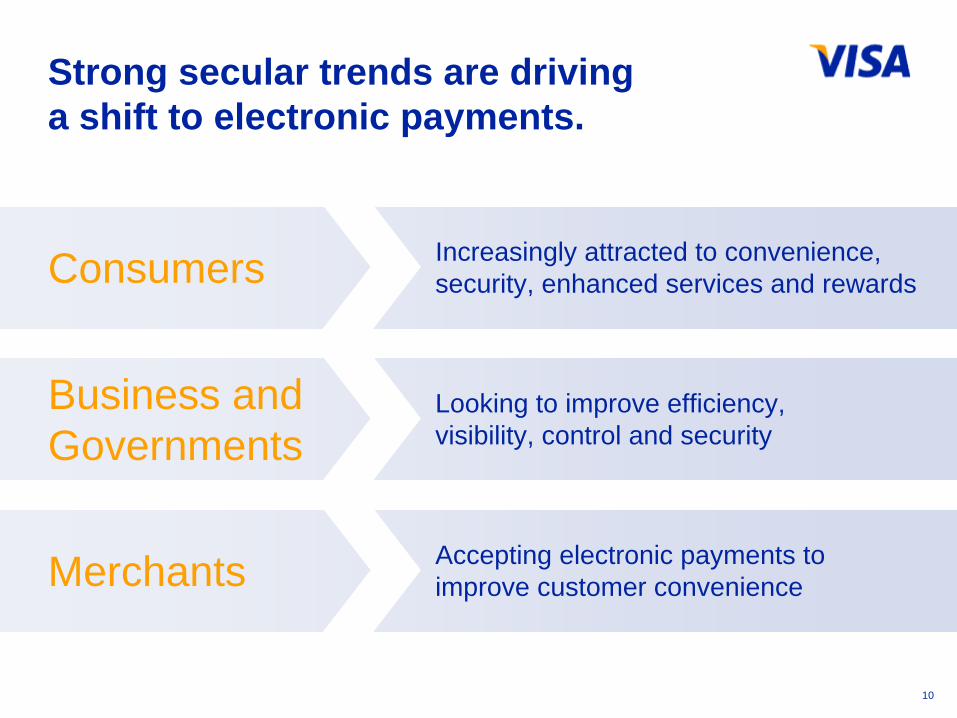

Strong secular trends are driving a shift to electronic payments.

10

Merchants

Business and Governments

Consumers Increasingly attracted to convenience, security, enhanced services and rewards

Looking to improve efficiency, visibility, control and security

Accepting electronic payments to improve customer convenience

Notes: Debit includes Interlink1 Quarter ended June 30, 20102 Prior to Q409, quick service restaurants were classified as Discretionary. Historical data is updated to reflect current definition

Source: Visa Inc. analysis through June 2010

20092001 2007 20101

25% 33%

54%

36%

56%

36%

57%41%

75% 67%46%

64%44%

64%43%

59%

Credit Debit Credit Debit Credit Debit Credit Debit

Non-Discretionary SpendNon-discretionary consumer spend is the most resilient and fastest growing part of Visa’s business

USA Region, Consumer Credit and Debit Volume

Non-Discretionary

Discretionary

Primary Merchant Segments

• Discretionary retail• Restaurants• Lodging • Airlines

• Gasoline• Bill payment• Grocery• Discount stores• Drugstores• Quick service restaurants2

48%29%

44%51%

11

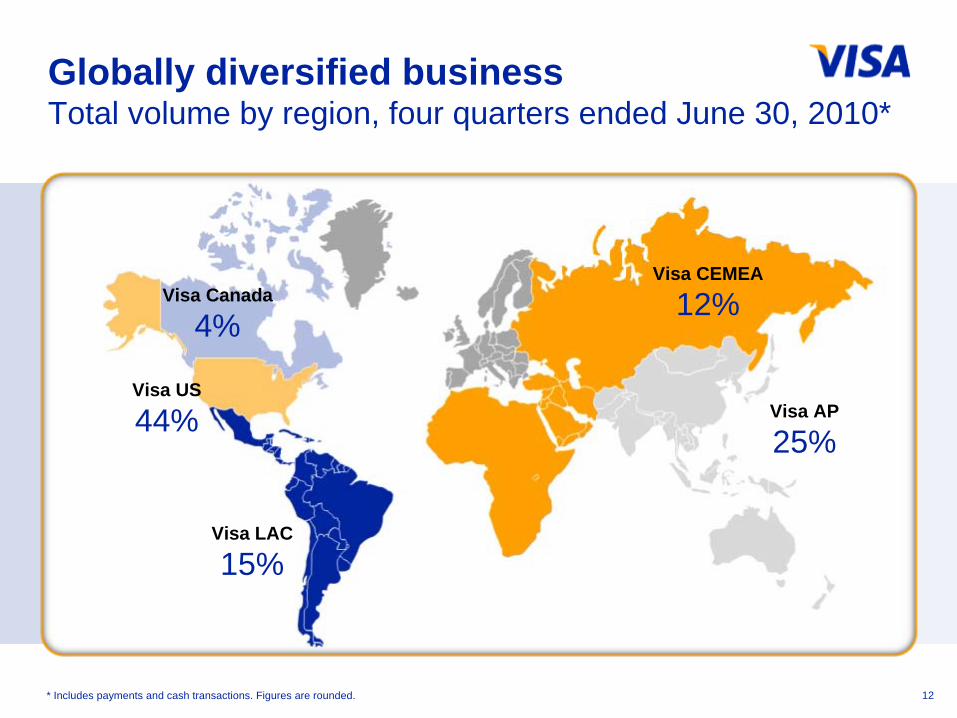

Globally diversified business Total volume by region, four quarters ended June 30, 2010*

Visa LAC

15%

Visa Canada

4%

Visa US

44%

Visa CEMEA

12%

Visa AP

25%

* Includes payments and cash transactions. Figures are rounded. 12

Products Broad Set of

Products and Services

Clients Large and Diversified

Client Network

Brand Powerful,

Compelling, Memorable

Brand

Processing State-of-the-Art

Processing Capabilities

Visa’s unique competitive advantages

13

Secure

State-of-the-art processing capabilities with VisaNet

14

Reliable

ScalableFlexible

VisaNet provides cost and functional advantages.

VisaNet

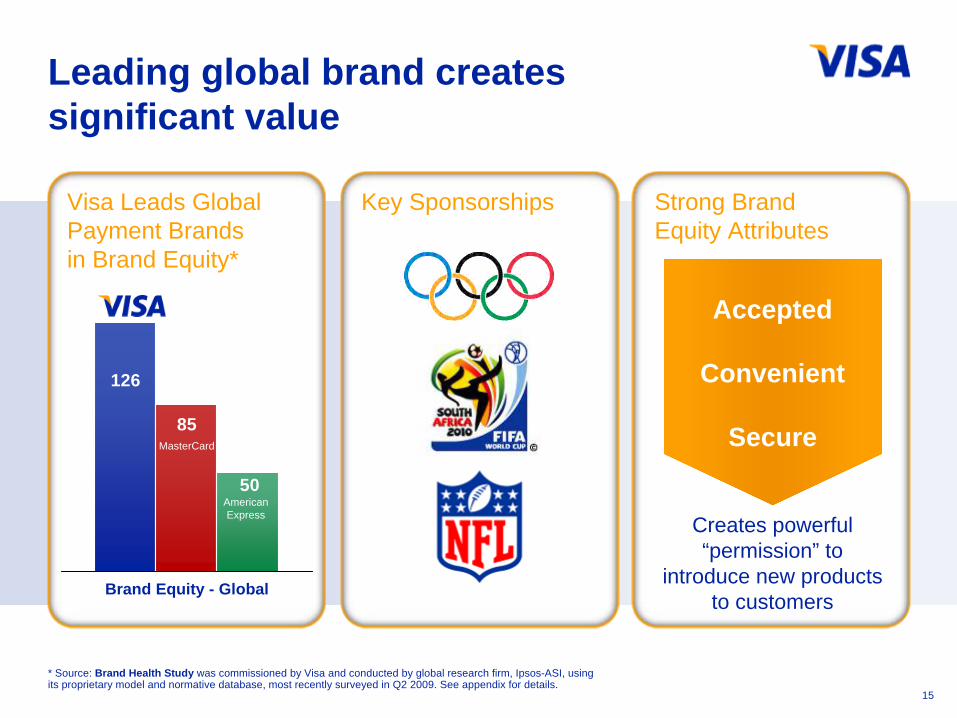

Leading global brand creates significant value

15

126

85

50

Brand Equity - Global

* Source: Brand Health Study was commissioned by Visa and conducted by global research firm, Ipsos-ASI, using its proprietary model and normative database, most recently surveyed in Q2 2009. See appendix for details.

Visa Leads Global Payment Brands in Brand Equity*

Key Sponsorships Strong Brand Equity Attributes

Accepted

Convenient

Secure

Creates powerful “permission” to

introduce new products to customers

%

MasterCard

American Express

16

March 2010World's Most Admired CompaniesVisa ranked #1 in the Consumer Credit Card and Related Services Category for the second year in a row.

April 2010Fortune 500Visa ranked #326 out of America’s 500 largest corporations and #2 within the financial services category.

May 2010Bloomberg BusinessWeekVisa ranked #26 for its accomplishments in IT services in its first year of inclusion on the list of the world’s 100 best performing tech companies of 2010.

February 2010World's Most Respected CompaniesVisa ranked #32 on this list of the most highly regarded public companies.

February 2010TrustR Brand ListVisa ranked #6 on the list of the ten most trusted brands in the U.S. and #5 among the ten most trusted and recommended global brands.

February 2010 All-American Investor Team, Institutional InvestorVisa ranked #10 overall in February 2010 with individual #1 rankings in five areas.

Visa Accolades

16

Visa payment types

Visa’s network facilitates a broad range of payment transactions.

17

Credit products draw funds from a credit line

Debit products, such as Visa Check card draw funds from a current account

Prepaid products draw funds from a pre-funded card account that can be funded from a variety of sources

Pay Later Pay Now Pay Before

Strategic initiatives to drive growth

Prepaid eCommerce

MobileMoney Transfer

18

Prepaid opportunity

Prepaid addresses consumer segments and payment sectors not served by other products• Underserved: general purpose reloadable• Government: benefits disbursement• Branch and retail: travel and gift• Corporate disbursements: incentive,

rebates, vouchers• Healthcare: health savings, healthcare

reimbursement

Visa’s position in the category is unique• Full suite of branded products• Network services, including ReadyLink,

partial authorization/balance return and auto-substantiation

• Issuer processing • Co-brands

19

Mobile opportunity

With more than 4 billion devices, mobile may be the world’s first ubiquitous technology.

218 MillioniPods

1 BillionPCs

1.6 Billion Internet Users

1.8 Billion Visa Cards

2.1 Billion TVs

4 BillionMobile Devices

Source: iPods: Apple.com (July 2009); PCs: Gartner (April 2008); Internet users: Internetworldstats.com (Dec 2008); Mobiles: International Telecommunication Union (Jan 2009), GSMA (Feb 2009)

20

Payment Value-Add

AcceptanceMoney Transfer

Mobile strategy

Visa’s mobile strategy extends Visa payment, money transfer, value-added services and acceptance capabilities to mobile channels.

Point of Sale Mobile Visa payWave payment

Remote Via IVR, SMS, mobile Internet

Alerts and NotificationsCustomer-set parameters and issuer-triggered alerts

Remittances Cross-border and domestic

Mobile AcceptanceMobile device enabled to accept Visa payments

Offers Mobile offers and discounts

21

Money-transfer opportunity

22

eCommerce opportunity

Marketplace Situation• Forrester reports global ecommerce sales are growing >20% annually

and will approach US$1 trillion by 2010• Security and convenience are key consumer concerns in the

ecommerce channel• Customer loyalty (powered by permission-based marketing) remains the

top merchant priority, making data acquisition and appropriate customer profiling highly valuable

Initiative Strategy• Increase merchant preference for Visa through value-added

products/services• Enhance cardholder value proposition of security, convenience

and reliability• Continually enhance and promote security to maintain stakeholder trust• Improve ease of cross-border transactions and enhance international

consumer and merchant experience• Continue to build upon Visa’s investment in the payment system

Sources: Visa; Forrester, “The State of Retailing Online 2008: Marketing Report,” Updated August 19, 2008 23

Global Brand Health Tracker Methodology

Appendix: Summary Purpose/Methodology Brand Health StudyPurpose: The purpose of this Visa-commissioned quantitative study is to measure the Health and Equity of the Visa brandVendor: Ipsos ASI Ltd.Method: U.S.: Telephone interviewing (random digit); Outside of U.S.: Face-to-face or telephone interviewing depending on countryDates: U.S.: Continuous interviewing from 2005 to 2009 for this report; Outside of U.S.: Interviewing waves, from 2005 to 2009 for this reportNumber of interviews: U.S.: Approx. 80-90 completes per week; Outside of U.S.: Varies by country, at least 1,000 per year per countryQualifying criteria: Those not working for conflicting interest. U.S.: adults 18+ who own at least one payment card, with a household income of at least $10,000; Outside of U.S.: Banked adults 18+Representation: Individual countries are weighted by composite measure (payment card penetration and PCE) Global Countries: U.S., Canada, Brazil, Mexico, Australia, South Korea, Japan, China, India, Russia, GCC (UAE, Saudi Arabia)

24