volume 1: annexes - netherlands. david stower permanent secretary, ministry of water and irrigation...

TRANSCRIPT

PUBLIC-PRIVATE INFRASTRUCTURE ADVISORY FACILITY STRATEGIC REVIEW 2008

March 2009

Final Report

VOLUME 1: ANNEXES

Submitted by: Cambridge Economic Policy Associates Ltd

CONTENTS

1. Annex 1: Terms of reference for the Strategic Review 2008..............................4

2. Annex 2: List of consultations...........................................................................8

2.1. PPIAF annual meeting, Tunis, June 2008 ................................................................8

2.2. PMU headquarters, Washington DC, July 2008......................................................9

2.3. Field visits, Kenya, Uganda, India and Vietnam, Nov 2008- Jan 2009..............10

2.4. Consultations in London in person and by telephone/videoconference..........13

3. Annex 3: Market and institutional context of PPIAF ..................................... 14

3.1. Market context ...........................................................................................................14

3.2. Institutional context...................................................................................................17

4. Annex 4: Analysis of the trends in PPI by region ........................................... 21

5. Annex 5: An analysis of PPIAF’s portfolio using the suggested revised categorisation of activities ......................................................................................38

5.1. Geography...................................................................................................................38

5.2. Sector ...........................................................................................................................41

5.3. Size ...............................................................................................................................44

5.4. Activity.........................................................................................................................46

6. Annex 6: An analysis of PPIAF’s portfolio using the traditional classification 49

6.1. Geography...................................................................................................................49

6.2. Sector ...........................................................................................................................53

6.3. Size ...............................................................................................................................55

6.4. Activity.........................................................................................................................56

7. Annex 7: PPIAF governance structure............................................................58

7.1. PPIAF origins and the Charter ................................................................................58

7.2. Governance arrangements........................................................................................59

8. Annex 8: A comparison of PPIAF and other Trust Funds ............................. 61

8.1. Comparison of PMU costs with other Trust Funds.............................................62

8.2. More details on other World Bank Trust Funds ...................................................63

9. Annex 9: Proposal review process and trends in proposal approval...............78

9.1. Proposal origination and review process................................................................78

9.2. Trends in PPIAF proposal approval.......................................................................79

10. Annex 10: Outcomes and Impacts of a sample of PPIAF activities ...........82

3

11. Annex 11: Summary field visit reports .........................................................93

11.1. Kenya...........................................................................................................................93

11.2. Uganda.........................................................................................................................98

11.3. India .......................................................................................................................... 103

11.4. Vietnam .................................................................................................................... 108

1. ANNEX 1: TERMS OF REFERENCE FOR THE STRATEGIC REVIEW

2008

This annex reproduces the terms of reference for the Strategic Review 2008, as provided

to the consultants at the start of the assignment.

5

6

7

8

2. ANNEX 2: LIST OF CONSULTATIONS

2.1. PPIAF annual meeting, Tunis, June 2008

Table A2.1: List of consultations: Tunis, 2-6 June 2008

Name of Person Role and organization

Programme Council

Dianne Harris Assistant Program Manager, PIDG

Dag Larsson Senior Advisor, Private Sector Development, Norad

Johan Gely Program Manger, SECO

Lazlo Lovei Chair of Program Council and Director, Finance, Economics and Urban, World Bank

Marie Bergstrom Senior Adviser, department for Infrastructure and Economic Cooperation, SIDA

Peter Roberts DFID

Vincent Gouarne Director Sub National Finance Department, World Bank

Jyoti Shukla PPIAF program manager

Bianca Denfeld KfW

Nina Nadin Barmeier GTZ – German Technical Cooperation

Peter Kelly AusAid - Australia

Ewout de Wit DGIS, Netherlands

PPIAF PMU

James Leigland Program Leader for SNTA

Clemencia Torres de Mästle

PMU, Global knowledge management

Bhavna Bhatia Regional Program Leader for Eastern Europe & Central Asia, and South Asia

Joel Kolker Regional Program Leader for South and Eastern Africa

Lorenzo Bertolini Regional Program Leader for West and Central Africa

Paul Reddel Regional Program leader for East Asia and Pacific

Joshua Gallo Regional Program Leader for Latin America and Caribbean

Serah Njoroge Program Officer for South and Eastern Africa

PPIAF Technical Advisory Panel

Anton Eberhard TAP Member

Nasser Munjee TAP Member

Robin Simpson TAP member

Prof. Eduardo Engel TAP member

Valentine Chitalu TAP member

Others

9

Name of Person Role and organization

Gilbert Mbesherubsa Director of Infrastructure Department, AFDB

John Flora Technical Adviser of TAF

Lamin Manneh Regulatory expert, AfDB

Andrew Roberts Infrastructure Expert, ICA Secretariat

Hugh Goldsmith EIB

Catherine Revels WSP, South Asia

Johan Kruger Former CEO, INCA, SA

Chris Burke Research Fellow - Centre for Chinese Studies

2.2. PMU headquarters, Washington DC, July 2008

Table A2.2: List of consultations: Washington DC, 7- 10 July 2008

Name of Person Role and organization

Jyoti Shukla PPIAF Programme Manager

Aldo Baietti Senior financial specialist, Energy, transport and water department, World Bank

Katherine Sierra Vice President, Sustainable Development, World Bank

Christopher Gerrard Lead Evaluation Officer, IEGCG

Dana Rysankova Senior Energy Specialist, Energy, Africa, World Bank

Pankaj Gupta Sr. Financial Analyst, AFT: Energy, World Bank

Alain Labeau Program Coordinator, AFT Transport, World Bank

John Flora Technical Advisor, Technical Assistance Facility, PIDG

Pierre Guislain IFC Director, Investment Climate

Motoo Konishi Sector Manager, Sustainable Dvlpt. Sector Unit, World Bank

Bernie Sheahan Director, Advisory Services, IFC

Jonathan Walters Sector Manager; and Paul Noumba, Lead Economist, MENA Sustainable Development, World Bank

Jamal Saghir Director, Energy, Transport and Water Dept, World Bank

Junaid Ahmad Sector Manager, South Asia Sustainable Dvlpt., World Bank

Anil Bhandari Sr. Advisor, Transport, Nairobi, World Bank

Michael Haney Sr. Energy Specialist, South Asia Sustainable Dvlpt. - Energy

Patricia Veevers-Carter Program Manager, GPOBA

Kamran Khan Infrastructure Policy Advisor, East Asia Sustainable Dvlpt. - Operations and Policy, World Bank

Paul Cadario Senior Manager, Trust Fund Quality Assurance & Compliance

Ashok Subramanian Sector Manager, AFT: Water Resource Management

Jyoti and Amit PPIAF PMU

Inger Andersen Director, Africa Sustainable Dvlpt. Front Office

10

Name of Person Role and organization

Vivien Foster Lead Economist, Africa Sustainable Dvlpt. Front Office

Magdalena Manzo Senior Operations Officer, Trust Fund Operations

Dara M. Lengkong Trust Fund Operations

Nigel Twose Director, IDA/IFC Secretariat

Dianne Rudo TAP Member

Carol Bonney Sr. Resource Management Officer

Ajay Kumar Sr. Transport Economist, World Bank

Pierre Pozzo di Borgo Sr. Transport Specialist, World Bank

2.3. Field visits, Kenya, Uganda, India and Vietnam, Nov 2008- Jan 2009

2.3.1. Kenya

Table A2.3: List of consultations in Kenya, 24-26 November 2008

Name of Person Role and Organisation

Joel Kolker Regional program leader for South and Eastern Africa, PPIAF

Serah Njoroge Program officer for South and Eastern Africa, PPIAF

Mrs Esther Koimett Investment secretary, Ministry of Finance

Richard J Muiru Chief engineer ( Electrical ), Ministry of Energy

Patrick M Nyoike Permanent secretary, Ministry of Energy

Anil Bhandari Senior transport advisor, World Bank

Vishal Agarwal Head of infrastructure finance in SS Africa, PricewaterhouseCoopers

Elly Aguko Senior manager (projects), K- Rep Bank

J Kimani Engineer, Athi Water Services Board

Leonard M Mbugua Chairman, Kiamumbi Multipurpose Cooperative Society

Eng. David Stower Permanent secretary, Ministry of Water and Irrigation

Eng. Lawrence N Simitu Director of water services, Ministry of Water and Irrigation

Eng, R K Gaita Director of irrigation, drainage and water storage, Ministry of Water and Irrigation

James K Yatich Acting director, land reclamation department, Ministry of Water and Irrigation

Eng. Joseph K Njoroge Managing director, Kenya Power and Lighting Co Ltd

David Mwangi Chief manager, planning, research and performance monitoring, Kenya Power and Lighting Co Ltd

Eng. John Ombini Chief manager, distribution, Kenya Power and Lighting Co Ltd

Paivi Koljonen Lead energy specialist, World Bank

Taz Chaponda Associate director, Prosperity Capital Management Ltd

Eng. Gakubia CEO, Water Regulatory Board

11

Name of Person Role and Organisation

Joseph Nduva Muli Managing director, Kenya Railways Corporation

Eng. Joster I Onyango General manager (Concession), Kenya Railways Corporation

George Muhoho Managing director, Kenya Airports Authority

2.3.2. Uganda

Table A2.4: List of consultations in Uganda, 25-26 November 2008

Name of Person Role and Organisation

David Ssebabi Director, Privatisation and Utility Sector Reform Program

Joselyn Ategeka Legal Officer, Privatisation and Utility Sector Reform Program

Mona Batabara Muguma African Alliance

G T Itazi Director, Ministry of Works and Transport

C Okelo Principal Transport Economist, Ministry of Works and Transport

Name not available Kampala City Council

David Luyimbazi Director Planning, National Roads Authority

Patrick Mwesige Director of Finance and Administration, Electricity Regulatory Authority

Eng. Semitala Norbert Director of Technical Regulation, Electricity Regulatory Authority

Eric Kenneth Lokolong Senior Compliance Officer (Legal), Capital Markets Authority

Angela Kiryabwire Kanyima

Director, Legal and Compliance, Capital Markets Authority

Dr. William Muhairwe Managing Director, National Water and Sewerage Corporation

Alfred Okot Okidi Chief Manager of Finance and Accounts Division, NWSC

Rob Rudy Pro-Poor Growth Adviser, DFID

Kajuna Benon Assistant Commissioner, Planning, Ministry of Works and Transport

Okelo Cipriano Transport Economist, Ministry of Works and Transport

2.3.3. India

Table A2.5: List of consultations in India, 3-5 December 2008

Name of person Role and organisation

Beneficiaries/ government representatives

Dr Arvind Mayaram Additional Secretary, Government of India, formerly in the Ministry of Finance, PPPs.

Ashish Khundra Officer on Special Duty to Minister of External Affairs; formerly in Delhi Jal Board

Aparna Bhatia Joint Director – PPP, Department of Economic Affairs

Gajendra Haldea Adviser to Deputy Chairman, Planning Commission

Dr Pramod Deo Chairman, Central Electrical Regulatory Commission (CERC)

12

Alok Kumar Secretary

P. K. Srivastava Joint Secretary, Ministry of Urban Development

Vinayak Chatterjee Confederation of Indian Industries; Chairman, Feedback Ventures Pvt Limited

Manu Srivastave Secretary Urban Development, Government of Maharashtra

Donors

Stephen Young Senior Infrastructure & Urban Development Adviser, DFID

Anouj Mehta Senior Infrastructure Finance Specialist, PPPs, Asian Development Bank, India Resident Mission

PPIAF Consultants

Anish De

Puneet Chitkara

Vibhuti Garg

CEO, Mercados Energy Markets India Pvt Ltd.

Manager

Consultant

Amrit Pandurangi Partner, PWC

Akanksha Chaurey Director, Decentralised Energy Solutions, TERI

Amit Kapur Partner, J.Sagar Associates

NGO - PPIAF beneficiaries

Udai S Mehta

Sharad Shrivastava

CUTS – Centre for Competition, Investment & Economic Regulation

Assistant Manager, CIRC

Anjali Garg Fellow & Area Convenor; TERI

2.3.4. Vietnam

Table A2.6: List of consultations in Vietnam, January 2009

Name of person Role and organisation

Dr Pham Ngoc Thai Deputy Director, Department of Technical Infrastructure, Ministry of Construction, Hanoi

Mr Tran Huang Tuan Director, Transport Management and Operations Centre ( TRAMOC), Hanoi

Mr Nguyen Hoang Hai Deputy Director, TRAMOC, Hanoi

Mr Nguyen Manh Hung Director, Hanoi Department of Transport

Mr Dinh Quang Hiep Director, Bac Ninh Water and Sewerage Company, Bac Ninh

Mr Tam General Director, Lim DBL Contractor, Lim

Mr Paul Coleman Partner in charge of advisory services, PwC Hanoi

Mrs Dinh Quynh Van Partner in charge of PwC Hanoi office and tax services, Hanoi

Mr Paul Reddel PPIAF Regional Program Leader, East Asia and Pacific, Manila

13

Name of person Role and organisation

Ms Hope Gerochi PPIAF Program Officer, Manila

Mr Nguyen Quang Vinh Operation Officer, Urban Sustainable Development Program, World Bank, Hanoi

Mr Richard Spencer Energy Sector Coordinator, World Bank, Hanoi

Mrs Beatriz Arizu de Jablonski

TTL PPIAF energy sector projects in Vietnam, World Bank

Mr Nguyen Vu Quang Deputy Director General, Electricity Regulatory Authority of Vietnam ( ERAV), Hanoi

Mr Vuong Quang San General Director, Saigon Water Corporation, (SAWACO), HCMC

Ms Le Anh Dao Corporate Office Vice manager, SAWACO, HCMC

Mr Ly Chung Dan Vice General Director, SAWACO, HCMC

Mr Tran Van Thinh General Director, Saigon Environmental Technology and Construction Company (SENCO), HCMC

Simon Calvert Consultant on DBL projects, director PwC – email

Robert G. Fitzgibbons Consultant for energy regulatory licensing projects – email

Roland Liemburger Consultant for NRWater projects in Hanoi and HCMC - email

William B. Kingdom TTL water and sanitation projects, World Bank – email

2.4. Consultations in London in person and by telephone/videoconference

Table A2.7: List of consultations: By telephone and others, June 2008 to March 2009

Name of Person Role and organization

John Hodges PIDG

William Cobbett Cities Alliance

Kameel Virjee WSP (Nairobi)

Michael Jordan Reviewer - PPIAF 2004

Tracey Osbourne PPIAF Communications Manager

Jan van Renselaar DGIS, Netherlands

Joanna Masic

Georges Heines

Ricardo Loi

Asian Development Bank

Engin Goksu European Bank for Reconstruction and Development

Misa Andriamihaja Philippe G

African Development Bank

14

3. ANNEX 3: MARKET AND INSTITUTIONAL CONTEXT OF PPIAF

In this annex, we consider both the high-level “market” and “institutional” contexts

within which the PPIAF program is taking place. In market context, we set out the

broad market impediments to privately financed infrastructure in PPIAF’s chosen areas

of operations. By institutional, we are primarily referring to the bilateral and multi-lateral

aid architecture through which PPIAF operates. The specific details of the institutional

location of PPIAF is set out in the main Inception Report.

3.1. Market context

In this sub-section, we explore the market context within which PPIAF operates. We

begin by summarising the main high level impediments to private sector participation in

infrastructure.

3.1.1. High level impediments to PPI

Although the specific constellation of impediments differs by region, country, sector and

even project, we would argue that impediments to the successful financial closure of

projects can be grouped into the following distinct, but inter-related themes:

• poor project fundamentals – in terms of the underlying economics and design

of the project, particularly as regards risk allocation;

• under-developed enabling environment – in terms of PPP and other

necessary laws, and the institutional structures necessary for private sector

participation; and

• lack of stakeholder commitment and/ or capacity – in other words, the

necessary motivations and capabilities of governments, project sponsors and to

some extent, donors.

These relationships might be set out figuratively as shown in Figure A3.1:

15

Figure A3.1: High level barriers template

Poor project fundamentals

In considering fundamentals, the aim is to analyse the project on a standalone basis.

Project fundamentals determine the bankability of a project from the perspectives of

investors and lenders. To attract the appropriate finance the project must (i) be able to

provide overall equity returns and debt margins, commensurate with the risks faced by

investors and lenders and (ii) commercial, financial and political risks must have been

either mitigated, or allocated to the party best able to manage them, or else appropriately

shared.

The principal barrier which can affect the required rate of return is a lack of

affordability in that the project’s revenue generation from direct or ultimate user charges

falls well short of the project’s costs, i.e. there is a funding gap; which is often not

addressed due to a lack of government and / or donor subsidies to fill the gap.

The principal project risks, and subsequent allocations, that cause the most problems are:

• Commercial: such as limited or lack of solvency among government purchasers

of private sector services (e.g. the sale of private power to national utilities which

are often highly indebted and are unable to set and collect cost reflective tariffs).

• Financial: such as currency mismatches between local currency revenues and

foreign exchange financing; where local currency financing is available, an

inability to hedge local interest rates and extend tenors can be highly problematic.

• Political / country: a lack of truly independent regulators who can stand up to

governments and customers means that many longer term arrangements – even

concessions – can be subject to regulatory risk that is often extremely difficult to

mitigate without considerable government or even multilateral commitment.

As the model suggests there are various overlaps between issues that are purely to do

with the project’s design, and those which are to do with other issues. As we will go to

discuss, an inability to recognise the problems set out above due to limited capacity will

contribute to the problems of design, whereas gaps in the enabling environment – such

Project

Fundamentals

Commitment

& Capacity

Enabling

Environment

16

as underdeveloped financial markets – give rise to a number of major project risks (eg

refinancing risk).

Under-developed enabling environment

We would seen the enabling environment constituting the laws and regulations, economic

institutions and established PPP processes, which create conditions conducive to the

development of not just PPP “projects”, but also markets which are needed for other

supporting activities such as finance.

Critical aspects of the enabling environment for PSP infrastructure are typically:

• Legal: a basic Build-Operate-Transfer (BOT) or other laws, which inter alia,

define the roles of the contracting parties, and those bodies required to approve

any PSP investment.

• Institutional: capabilities to develop and take projects to market or – at a

minimum – an ability to negotiate with investors making unsolicited approaches.

• Process: – clearly understood PPP processes where the responsibility of each

part of government are clearly set out, from those initiating projects through to

those responsible for ensuing that investors are treated respectfully.

Naturally, establishing such a favourable environment cannot be achieved without both

commitment and capacity, which overlaps with our third core area.

Capacity and commitment

This is a much wider and nuanced set of issues, which is not just limited to the host

countries, particularly where commitment is considered. The bullet point above on

institutional capabilities clearly overlaps with this third area, at least as far as capacity is

concerned. However, the capacity itself, is a necessary but not sufficient condition for

success; without the necessary discipline and commitment, private investment is unlikely

to occur. From government perspective, the commitment involves being prepared to

support private sector investment – and all that entails – even when certain aspects of it

may be politically unpopular – for instance, when tariff increase justifiably required. All

too often, rather than commitment and discipline rent seeking and more blatant forms of

corruption amongst officials and politicians are often observed.

However, those taking such short-cuts are often the investors themselves who are only

too happy to offer bribes and other forms of inducements in order that they achieve their

objectives. As such, there can also be a lack of commitment by some investors to fair

competition for project opportunities.

Finally, the role of donors can also often be prejudicial to the successful completion of

projects. Many lack the technical understanding of what PSP requires, whilst others are

easily swayed by interest groups with a minority interest, rather than being committed to

the successful completion of the project. Unrealistic social, environmental and gender

requirements, far in excess of those required in the developed world, have arguably

distorted and delayed donor investment and lending decisions. This has led to frustration

17

on the part of some governments and a greater temptation to respond favourably to

unsolicited approaches from, for instance, companies from developing counties who are

less concerned about such issues.

3.2. Institutional context

As well as the “market side” of infrastructure context within which PPIAF operates, it is

also important to consider the institutional context. Indeed, the terms of reference, in

paragraph11(iii), asks for an assessment of:

“PPIAF’s place in the international aid architecture including its impact on the programs of its donors,

other major development partners and other global programs.”

This sub-section is an initial contribution to this assessment and is largely based on

knowledge gained in earlier PIDG work, the DFID PSI review, internet research and

interviews in Phase 1 of this study.

PPIAF, particularly from 1999 to 2005, operated in a context of declining donor interest

in investment in economic infrastructure, combined with the post-1997 withdrawal of

private sector operators and project finance from many emerging markets. In this sense,

PPIAF was for a long time, an unfashionable but important champion of policy based

analytical work to specifically enable PPI and more generally, the crucial importance of

infrastructure to economic growth and poverty reduction. Views have, however, moved

on and the World Bank Group – having led the flight away from infrastructure – has

now moved back to being a lead investor and advocate. However the channels and

modalities are different and more complex than before.

Recent increases in global aid volumes, as defined by OECD DAC, have been driven by

debt relief; high profile post war reconstruction and prioritising of social sectors (which

now officially includes water and sanitation). Even for Sub-Saharan Africa, sector aid for

infrastructure fell from 29% of total aid flows in the early 1990s to 19% in 2000 – 2004;

moreover only two donors – Japan and US - together account for over 80 % of bilateral

infrastructure programs. For multi-laterals, IDA and EC dominate with nearly a third

each, although more recently the AfDB and ADB have raised their financing profile.

3.2.1. Aid Architecture

In general, the last five or so years have seen a proliferation of aid channels, a growing

number of new infrastructure sector participants - countries like China, Russia and India;

civil society and private sector foundations; and a massive rise in special purpose

programs or institutions - plus fragmentation and significant earmarking of aid

contributions. The latter include the rise of “vertical” global or regional, multi-donor

trust funds. The very lack of coherence has fuelled the aid effectiveness debate and

attempts to implement the 2005 Paris Declaration. In September 2008, a major High

Level Forum on this topic was held in Accra; and the resulting Accra Agenda for Action

aims to accelerate progress towards making aid more effective. The Agenda is complex

and political but includes extended principles on broadening ownership in development

policy, particularly at the country level, greater use of in-country systems, untying aid and

18

increasing predictability plus greater transparency. On technical assistance and capacity

building, the AAA concludes that: “Donors support for capacity building will be

demand-driven and designed to support country ownership.” Apart from recognition of

the fragmentation dangers associated with global funds, there is little on specific reform

of aid architecture.

PPIAF is one of a number of Trust Funds locate in the Bank. Other infrastructure

related Trust Funds are the Cities Alliance (CA), ESMAP, Water & Sanitation

Programme (WSP) and the Global Partnership for Output-Based-Aid. Donors are

recently reporting pledges of over $ 6 billion to the Climate Trust Funds, a pair of

investment instruments to provide scaled up funding to mitigate increases in greenhouse

gas emissions and adapt to climate change. The two Trust Funds cover the Clean

Technology Fund and the Strategic Climate Fund, the latter being broader and more

flexible and aimed to test innovative approaches. Interestingly the funds will be

administered and executed through a partnership or the World Bank Group and other

multi-laterals Developing countries will have an equal voice in the governance structures

and decisions on use of finds will be made by consensus. The first annual Partnership

Forum will have a very wide stakeholder base.

Based on the latest available “2006 Trust Funds Annual Report” from the World Bank,

there were some 929 active trust funds variously hosted at end June 2006. Annual

disbursements were US$4.4 billion and funds held around US$10.3 billion. Some 80% of

funds were from sovereign governments and under 1 % from private sources. There are

three types:

• funds supervised on behalf of donors;

• funds where the Bank acts only as financial intermediary; and

• funds used to “scale up” Bank activities.

PPIAF is in the latter category: this is the smallest of the three, adding only to some 6 %

of disbursements in 2006, but growing rapidly. Supervised funds added to 47 % and

included debt relief and reconstruction; fiscal agency funds totalled 38 % and included

majors like GEF, GFATM and CGIAR.

Of the 929 funds, IBRD operates 95% by disbursement value and the IFC 5 %( or 15),

with MIGA having a nominal residual share. In terms of infrastructure related funds or

programs size, PPIAF is at the larger end. In FY 2006, it spent US$17 million, the same

as FIAS but less than WSP (US$18 million); ESMAP spent US$5 million, Cities Alliance

some US$9 million and SSATP around US$4 million. Outside the segment, CGAP also

spent some US$ 9 million but GFATM disbursed US$1.32 billion. Interestingly, the IFC

is reported as spending US$75 million on technical assistance, from all sources, mainly on

advisory services.

3.2.2. IFC

In PPIs in infrastructure, the IFC will be increasingly important. Traditionally the IBRD

and the IFC have co-existed rather than proactively co-operated; they have different

19

cultures, procurement and safeguards. Under the new President and pressure from

donors following the IDA 15 replenishment, IBRD/ IDA and IFC will be incentivised

to work closer. Our consultations also suggested a greater degree of strategic and

operational cooperation within the World Bank Group going forward, which should

have positive implications for PPIAF.

Under IDA 15, some US$1.75 billion went to the IFC and there is a joint IFC / IDA

secretariat. Some 50% of IFC investment should be in “frontier” states. There is a move

to match IFC investments with IDA credits or sequence. In the IFC, infrastructure is one

of five advisory business lines and the TA Trust Funds program largely supports project

development activities and private sector development. In FY 2006, they managed a total

of US$134 million in technical assistance often sourced from IFC retained earnings; this

was centralised and then pooled regionally. The IFC Technical Assistance Trust Funds

Program is collectively sponsored by 23 donor countries and spends between US$15 to

US$20 million per year; this compares to around US$65 million per year from IFC

profits. Infrastructure is running at 30% of all technical approvals (including DevCo).

3.2.3. Overlap or Co-operation?

The PPIAF global enabling environment niche for PPI appears to have been well

regarded respected and there are no major competing initiatives. Of the original core

activities allowed by the Charter, only pioneering transactions support is part of the remit

of a number of regional and other (PIDG or IFC or DFI) project development and

investment facilities. The PPIAF program council represents around 15 donors and

covers all those with a continuing infrastructure interest; partnerships are also being

proactively pursued with emerging new players, like revitalised AfDB and the Africa

Infrastructure Forum. China and India are also a focus. The SNTA window is

complementary and reinforces the PPIAF platform compared to other initiatives. PPIAF

is also now an observer at PIDG.

In terms of other Bank Group technical assistance programs, apart from the IFC, the

potential overlap with FIAS seems well managed unless there is a bigger move into

directly productive agriculture or industry; here reference would also have to given to

water and sanitation programs. PPIAF client definitions have also been softened to

include commercial public sector only operations, at national and local levels.

The Investment Climate Facility (ICF) for Africa is a new public-private partnership

based in Dar Es Salaam which aims to remove real and perceived constraints on the

investment and business climate. One of its eight themes is facilitating infrastructure. It

covers the 24 African countries that have signed up for the Africa peer review

mechanism under NEPAD. It is time limited to seven years; a budget of US$120 million

is anticipated for the first five years; DFID, the IFC and the EC plus the Netherlands are

the start up donors. Corporate investors – at US$2.5 million each – include Celtel,

Microsoft, Anglo, Shell, SAB Miller , Unilever and Standard Bank .

There is a thin line between overlap and co-operation, particularly when most bilateral

and multi-lateral institutions actively seek “leverage.” A possible partner could be FIRST,

the global financial sector capacity initiative that was outsourced, but is now hosted by

20

the Bank. GPOBA and CA co-operation is already advanced; PPIAF is also looking to

extend links with EBRD and the EIB.

DFID have developed a portfolio of some 15 PSI initiatives including many of those

mentioned above. It was a lead champion and remains a major financier of PPIAF; many

of the European donors are also active in other initiatives, both PIDG and non-PIDG,

or small scale sector specific programs. The PPPUE predates PPIAF and was a policy

based urban technical assistance vehicle operated by UNDP but funded by DFID; there

was attempts to merge it with PPIAF but eventually DFID exited from funding in

around 2005 and PPPUE appears to have ceased to operate.

PPIAF is seen by contributing donors as addressing a continuing market failure and has

influenced the design of other programs via its relatively low cost, increasingly

decentralised business model. After a decade there is increasing pressure to demonstrate

development outcomes and impacts; IFC have embraced this different M & E reporting

framework and use it positively to secure grants. Internally PPIAF has been and

continues to be very important for the Bank in its analytical and knowledge agenda; it

also allows it buy-in skills and expertise it does not have or has lost. The wider and

deeper use of PP infrastructure solutions is a major pillar of the Bank’s SIAP 2009-11,

this envisages significant increases in Bank / IFC and MIGA infrastructure financing.1

1 SIAP envisages scale up of Bank Group infrastructure financing from around $ 41 billion in 2004 -07 , to

between $ 59 to $ 72 billion over 2008-11.

21

4. ANNEX 4: ANALYSIS OF THE TRENDS IN PPI BY REGION

This Annex summarises the PPI activity, both in terms of number and value of projects,

across regions in the period 1996-2007. The broad objective of this exercise is to get an

idea of PPI activity by region/ sector, and map that to the extent possible with the

PPIAF activities, to understand the linkages between the two. However, as set out in

Figure A4.1., our initial analysis of PPI activity over years, say in Sub Saharan Africa

(excluding Republic of South Africa), which is a main focus of PPIAF activities, does not

particularly show any trends. PPI activity has fallen since it’s peak in 2001but recovered,

albeit to a lower peak, in 2005.

Figure A4.1.: PPI spend in SSA

PPI spend in SSA, excluding RSA ($m)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2000 2001 2002 2003 2004 2005 2006

PPI spend in SSA ($m)

PPI spend in SSA ($m)

The rest of this section presents the PPI information in summary tabular form by region.

Table A6.1. shows PPI activity in Sub-Saharan Africa (excluding South Africa), Table

A6.2. South Asia, Table A6.3. East Asia and Pacific, Table A6.4 Middle East and North

Africa, and Table A6.5. Europe and Central Asia and finally, Table A6.6 Latin America

and Caribbean.

22

Table A4.1: PPI projects and investments (in US $) in Sub-Saharan Africa 1996-2007 (excluding projects in Republic of South Africa )

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • More than a third of PPI investment in energy during this period took place before 2000.

• Since then, investment has been erratic, with 2001, 2003 and 2005 all seeing investments of more than $1b.

• Only a fifth of projects have involved investments of more than $150m.

• Nigeria and Mozambique together account for one-third of sector investment, although the latter is mostly in the gas sub-sector.

• Almost 63% of investments have been greenfield.

66 7,395

Electricity generation

• Projects involving electricity generation involved, on average, and investment of almost $90m. 84% of investments have been through greenfield projects.

• More than a third of investments have been made in Nigeria. Kenya, with nine percent of investments, closed greenfield projects and the KenGen divestiture.

• Investment in Tanzania and Zimbabwe amounted to almost 30%.

• Almost half of electricity generation investments took place before 2000; this has been erratic since. Larger scale IPPs were mostly undertaken during the 1990s.

43 3,837

Electricity distribution / transmission

• There has been very little investment since 2000, with the exception of the Umeme Concession in 2005. 78 % of investments came through divestitures.

• The average project involved an investment of $51m, although projects involving some transmission network investment were larger.

• Zambia accounts for two-thirds of investment in networks, while Uganda received 20%. Around 12% was the 1999 Electa project in Cape Verde

8 411

Integrated electricity generation and distribution/ transmission

• Virtually all (99%) integrated projects took place between 1999 and 2001, and all were made on a concession basis.

• Integrated projects tended to be much larger, on average, than separate network or generation projects.

• The largest commitment, accounted for 42% of investments in integrated projects, was the 2001 AES Sonel Concession in Cameron.

11 1,268

Gas distribution / transmission

• Two projects, accounting for 95% of gas sector investments, took place in 2003 and 2005: the Mozambique-South Africa Gas Pipeline BOO, worth $1.2bn, and the West African Gas Pipeline, worth $590m. All four projects were greenfield.

• While the average gas sector project involved an investment of almost $470m, projects with

4 1,879

23

Sector / subsector

Observations Total no. of projects

Value of commitments

grater transmission network components were larger. TRANSPORT • Three quarters of transport investment occurred in the years 2003-07, with about 50%

in 2005 alone.

• More than 85% of investments were concessions, with the majority of others coming through greenfield projects.

• More than half of transport investments took place in Nigeria, with Mozambique and Kenya accounting for another quarter.

• Nearly three quarters of projects were less than $75m in value, with just 11% grater than $150m.

66 5,139

Ports • 60% of transport investments took place in the sea-port sector, with Nigeria accounting for 78% these.

• Three-quarters of investments took place in 20 projects in 2005 alone.

• 32 projects were Concessions, accounting for 90% of investments.

42 3,079

Airports • 85% of investments were through greenfield projects, in particular the 2006 Murtala Muhammed Terminal ROT project in Nigeria, accounting for three-quarters of sub-sector investment.

5 261

Rail • 23% of transport investments took place in the rail sector, with the $404m Kenya-Uganda rail Concession in 2006 accounting for a third of these.

• Three-quarters of investments overall have taken place between 2003-07.

• More than 90% of investments involved an element of rehabilitation, in particular based on freight traffic in Franco-phone West Africa.

17 1,223

Roads/bridges • The 1999 Abidjan Lagoon Toll Bridge BOT and 1997 Mozambique-South Africa N4 Toll Road Concession were the sum of sub-sector investments.

• There have been no new PPI investments since 2000.

2 576

WATER & SANITATION

• All projects other than the 2007 Omdurman Water Treatment Plant BOT in Sudan were management/ lease contracts. Ten of the fifteen involved no new investment. Five projects have taken place between 2003 and ’07.

15 178

Full network • There has been a relatively consistent stream of discrete network projects over the period in Anglophone and Francophone countries.

13 57

Bulk water supply / treatment

• In addition to the Sudanese plant, the other project was a lease contract for a sewerage treatment plant in Namibia.

2 121

24

Sector / subsector

Observations Total no. of projects

Value of commitments

TELECOMS • 39% of investments took place between 1996 and ’99, with another third in 2001 alone. Although only 11% has taken place since 2003, this still amounts to $2.3bn.

141 21,225

Fixed access and long distance only

• 70% of fixed line only investment was made before 2000.

• Sudan, Ghana, Nigeria and, in particular, Cote D’Ivoire account for 95% of fixed network investments.

22 2,060

Some element of mobile.

• 14 projects took place in 2001 alone, amounting to almost $6.9bn. Around $775m was invested between 2003 and ’05, compared to more than a billion dollars in 2006 alone.

• Almost half of investments took place in Nigeria.

102 19,166

25

Table A4.2: PPI projects and investments (in US $) in South Asia 1996-2007

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • Majority of activity in the energy sector is in electricity generation.

• A little less than half of the projects have been relatively small in size (<$75m), with 41% of the projects being large (>$150m)

• 42% of the activity in this sector has taken place before 2000 i.e. 1996 to 1999

• Majority of the projects have been Greenfield projects (86%)

100 22,348

Electricity generation

• Three-fourths of the electricity generation projects have been in India.

• Less than half (43%) of the projects took place prior to 2000 (i.e. in the 4 year period 1996-1999), with the balance taking place in the 8 year period from 2000-07. In terms of investment commitments as well, the projects from 1996-99 accounted for 43% of the total investment commitments over the concerned period.

• Majority of the electricity generation projects are Greenfield, with 3 divestures only – 2 in India and 1 in Pakistan.

• 80% of the projects are thermal power with the remainder being hydro/ wind.

87 20,056

Electricity distribution / transmission

• PSP in this sub sector limited to India (missing data?)

• Projects have been a mix of Greenfield, concessions and divestures- with the latter being the largest share of projects.

9 1,308

Integrated electricity generation and distribution/ transmission

• Karachi Electric Supply Company (KESC) is the only divesture of a vertically integrated electricity utility in the South Asia region with 73% private ownership.

1 342

Gas distribution / transmission

• Natural gas forms a small proportion of total energy projects, with 1 relatively large project in India and the remaining 2 being fairly small projects (<$75K)

3 641

TRANSPORT • Again, majority of the activity has been in India – 116 of the 123 projects, $12,536m of the total $13,176m

• The roads sector has been most active, with 92 projects, followed by ports and airports at 21 and 7 respectively. Overall figures point to a large number of small projects in the roads sector and fewer number of projects in the airports sector, but involving high investment commitments.

• Post 2004 has been the relatively more intensive period with investment commitments exceeding $1,000m p.a. (prior to 2004, investment commitments have been in the early

123 13,176

26

Sector / subsector

Observations Total no. of projects

Value of commitments

hundred millions). The year 2007 has seen a huge escalation with total investment commitments equalling $7,289m (peak of 45 projects in this year).

• Majority of the projects have been concessions and Greenfield, with management contracts being very few.

Ports • Approximately half of the port projects have been medium to small in size (<$150m), with the largest port project being $440m.

• Majority of the projects are in India, having achieved financial close post 2000. (No project outside of India in South Asia has achieved financial close in this sector).

• Majority of the projects have been Greenfield, with only one management contract.

21 3,056

Airports • 7 projects over the period, with 5 in India – large projects are the concessions (BOT including rehabilitation) of the two big city airports- Delhi and Mumbai. These two projects on their own account for $2,538m of investment commitments.

7 3,301

Rail • Very little PSP activity – all 3 projects in India. 3 218

Roads/bridges • Most successful transport sector with a lot of activity in India and some in Bangladesh.

• The year 2006 saw a number of projects achieving financial close (37)

• Bulk of the projects were medium to small scale in nature with approximately 13 projects exceeding investment commitments of $150m.

92 6,600

WATER & SANITATION

• Mostly small sized projects; all in India

9 255

Utility • 1 management and lease contract in India 1 0

Bulk water supply/ treatment

• A mix of Greenfield projects and management contracts, with one concession 8 255

TELECOMS • PSP activity is more widespread covering more South Asian countries apart from India such as Nepal, Bhutan, Maldives, and Afghanistan.

• All Greenfield projects except for 1 divesture in Sri Lanka.

• Mostly very large projects (27 of 42 exceed $150m in total investment commitments). Large projects often include both fixed line, mobile access and long distance.

• 1996-1999 saw a lot of activity in this sector

42 25,024

Fixed • Most of the larger projects were pre- 2000. 12 2,328

Mobile • Most projects are for mobile access. 30 22,694

27

Table A4.3: PPI projects and investments (in US $) in East Asia and the Pacific 1996-2007

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • China accounts for more than two-fifths of energy investment in the period, more than 60 percent of which came before between 1996 and 1999.

• Indonesia, Malaysia, Philippines and Thailand are significant others.

• More than half of projects took place between 1996-1999.

• Just under two-thirds of projects have been less than $75m in value, while less than a quarter has been more than $150m.

• Almost all projects are in electricity and natural gas. Projects in the former have been, on average, almost six times as large than in the former.

395 65,702

Electricity generation

• Almost 88% of energy sector PPI investment took place in electricity generation, with around 43% small projects and 39% large.

• The average investment in these projects was $265m.

• More than two-thirds of the generating projects over the period were closed in 1996 and 1997.

• 90% of Vietnam’s energy sector projects were in electricity generation, while China engaged in nearly 100 over the period.

• More than three-quarters of generation projects were greenfield, with the rest mostly divestitures.

217 57,586

Integrated electricity generation and distribution/ transmission

• The average size of these integrated projects was less than $65m, with five of them being small and only one large project.

• All but one of the projects was a partial divestiture.

• All but one of these projects took place in China, the other being the Shoreline concession in Tonga.

8 525

Electricity distribution / transmission

• The only electricity distribution project was the 2003 Subic Bay Power Distribution project in the Philippines, a Rehabilitate, Operate and Transfer (ROT) concession worth $7m.

1 78

Gas distribution / transmission

• Almost all (161) of the natural gas sector projects took place in China. None of them were in Pacific Island countries.

• More than three-quarters of these projects were greenfield, mostly on a BOT basis.

• Greenfield and divestiture gas transmission projects were, on average, comfortably larger than half a billion dollars.

169 7,513

TRANSPORT • PPI investment in transport was restricted to the East and South East Asian economies rather than the Pacific region.

246 54,663

28

Sector / subsector

Observations Total no. of projects

Value of commitments

• There was steady PPI investment in transport over the twelve years, albeit with more than a quarter in 1996 and 1997.

• Two-thirds of transport investment has occurred in China, with a fifth in Malaysia and almost ten percent in Indonesia.

• Around 43% of projects are small, with around 47% grater than $150m. Ports • Almost 60% of port projects were greenfield investment. More than half of projects were

prepared on a BOT basis.

• 83% of port investment occurred in China.

64 14,235

Airports • Cambodia, Malaysia, Philippines and Thailand together accounted for 41% of airport investment, with China the rest.

• More than 80% of this investment was in combined runway/terminal projects, most of which were divestitures.

23 4,020

Rail • Railroad projects are comfortably the largest in the transport sector, amounting on average to almost $630m.

• Malaysia and China account for virtually all rail investment.

• Around 60% of this investment was in greenfield projects, and around 70% on a BOT or BROT basis.

• More than half of the investment over the period occurred in 1996-97, although 2006 saw a sharp upswing.

16 10,076

Roads/bridges • Road projects account for nearly half of PPI investment over the period, over a third of which is accounted for by Indonesia and Malaysia, but 60% by China.

• Two-thirds of road projects are Greenfield.

• Road building dramatically picked up between 2005 and 2007, during which time two-fifths, of investment over the period as a whole. Took place.

143 26,332

WATER & SANITATION

• Water-sector investment has been erratic, with more than a third of investment occurring in 1997 alone.

• This investment has been fairly even distributed across China, the Philippines and Malaysia.

• Only 16% of investment has been in greenfield projects; 80% has been in divestitures.

270 23,042

Utility network • Three-quarters of investment has been in water utilities of which around half has included sewerage.

• The majority of this took place in Malaysia and the Philippines.

49 17,446

29

Sector / subsector

Observations Total no. of projects

Value of commitments

• The average investment in water utilities was more than $350m, fourteen times the average treatment plant investment. The average utility concession is $462m.

Treatment plant • China accounted for more than three-quarters of investment in treatment facilities was made in China, equating to 92% of projects.

• Half of investments arose through management/ lease contracts.

221 5,597

TELECOMS • Around sixty percent of PPI investment in telecoms occurred before 2000, with no new projects recorded since 2004.

• Around 95% of this is accounted for investments in China and Indonesia.

• The average project in the sector was almost $1bn.

25 24,497

Fixed and long • All fixed and long telecoms investment has taken place in China and Indonesia over three separate years: 1996, 2001 and 2002

• Nearly three-quarters of investment was made before 2000.

7 7,720

Mobile or mobile combined

• Almost 70% of investments were made in projects involving mobile phones in at least some form.

• Countries other than China and Indonesia have been subject to these investments, including Lao, Thailand and Vietnam.

18 17,227

30

Table A4.4: PPI projects and investments (in US $) in Middle East and North Africa 1996-2007

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • Annual PPI investment in energy has fallen since a high $4.6bn in 1997. Nearly half of the investment in the period was between 1997-1999.

• Half of all energy investment occurred in Morocco, with around a fifth in Algeria and 14% in Oman. The average project size was larger in these counties also, particularly Morocco and Algeria.

• Around 71% of projects were greater than $150m in size.

• Investments were split evenly between Greenfield projects and concessions.

28 14,161

Electricity generation

• More than half of all energy sector projects took place in electricity generation, nearly 80% of electricity generation projects were greenfield.

• The only divestiture was worth $1.5bn.

• The average project investment was almost $370m.

• Investments in generating capacity were fairly evenly split between Algeria, Morocco, Egypt and Oman.

• 46% of investments took place between the years 2004-2007.

20 7,363

Integrated electricity generation and distribution/ transmission

• One integrated project took place in the period, the 2001 Salah Power ROT Concession in Oman.

1 270

Electricity distribution / transmission

• Four projects worth a total of more than $5.1bn took place between 1997 and 2001. All of these were ROT Concessions in Morocco.

4 5,107

Gas distribution / transmission

• Three projects worth $1.420bn were undertaken in Algeria, Tunisia and Egypt.

• The 2006 Algerian greenfield Medgaz Pipeline project is worth nearly $1.2bn.

• Both other projects took place in 1998.

3 1,420

TRANSPORT • Almost a third of transport investments took place in 2007, with three projects in Algeria, Jordan and Tunisia.

32 5,406

Ports • 45% of seaport investments were made in Egypt, with more than 17% in Djibouti and a quarter shared between Morocco and Oman.

• Two-thirds of investments were made between 2002 and 2006.

• Almost 80% of investments were concessions.

17 2,855

31

Sector / subsector

Observations Total no. of projects

Value of commitments

Airports • Two large airport concessions in 1997, Queen Alia International Airport in Jordan and Enfidha and Monastir International Airports in Tunisia, accounted for three quarters of all sectoral investment in the period.

• Much of the remaining airport investment was closed in 2001 in Egypt and Oman, including the greenfield Borg El Arab Airport.

12 2,103

Rail • Rail investment in the period took place in two projects: the Algiers Metro lease contract in 2007 and the Aqaba BROT rail concession in 1999.

2 343

Roads/bridges • The sole road PPI during the period was the greenfield Dongying Yellow River Roadway Bridge BROT in 2001.

1 104

WATER & SANITATION

• Of the 14 projects in the sector since 1996, nine have been since 2005.

• A majority of investments and projects undertaken were in Algeria.

14 1,082

Utility network • Utility projects were spread between Algeria, Jordan, Lebanon, Oman and the Palestinian territories.

* Investment values are unavailable for several utility projects.

8 0*

Treatment plant • The two largest water and sanitation projects were greenfield BOT desalination plants in Algeria.

6 1,082

TELECOMS • More than half of telecoms projects were undertaken between 2003-2006.

• North Africa was the focus of investment: Egypt and Morocco accounted for 57% of commitments, with Algerian and Tunisia also prominent.

35 29,900

Fixed and long • Projects with no mobile phone element were concentrated in Algeria and Egypt. 6 1,501

Mobile or mobile combined

• 95% of investments involved some mobile phone element in the project.

• Combined projects, i.e. those involving fixed and long distance access as well as mobile telephony, were, on average, two to three times the size of those involving just the latter.

29 28,399

32

Table A4.5: PPI projects and investments (in US $) in Europe and Central Asia 1996-2007

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • More than half of investments took place between 2002 and 2006.

• Around 62% of investments were divestitures, with less than a quarter greenfield.; 22% of investments were made in Turkey, with 57% in EU accession countries.

151 33,343

Electricity generation

• Almost half of energy investment was made in projects with some element of increased generating capacity.

• Almost 80% of greenfield projects were electricity generation (e.g. IPPs).

• Turkey accounts for a third of generation investments, with Bulgaria, Kazakhstan and Poland between them accounting for another 38%.

• The average generation project was around $200m in size.

80 15,944

Integrated electricity generation and distribution/ transmission

• The only completely integrated projects in the electricity sector were late 1990s divestitures in Estonia and Ukraine.

2 0

Electricity distribution / transmission

• Three-quarters of investments took place between 2002 and 2006.

• Projects involved an investment of, on average, just over $100m.

• Bulgaria accounts for a quarter of all network investments, with another half in the other EU accession countries. Macedonia and Azerbaijan received 9% each.

• More than 90% of investments were divestitures.

42 4,289

Gas distribution / transmission

• Almost 40% of energy investments were made in gas sectors.

• Outside of the EU, Croatia received 29% of gas sector investments, Russia 13%, Belarus 4% and Turkey 15%.

• Investments, on average, were almost half a billion dollars in size.

• Projects involving some element of transmission infrastructure were almost $1.25bn in size.

• Gas projects accounted for 20% of greenfield projects.

27 13,109

TRANSPORT • There has been a sharp pick-up in PPI investment in transport between 2004-07, with 78% of investments over the period falling into these years.

• Around two-thirds of this was split between Turkey and Hungary, with Croatia and Poland also prominent.

• 43% of funds were invested through concession arrangements, with over a quarter in greenfield projects and a quarter management/ lease contracts.

61 17,589

33

Sector / subsector

Observations Total no. of projects

Value of commitments

• The average project was worth around $300m; 43% of projects are smaller than $75m and 33% greater than $150m, implying a skewed distribution.

Ports • Despite no PPI investment in ports in 2001, more than $1.5bn was subsequently invested in the following six years.

• 61% of investment took place in Turkey, with the rest split between Poland, Latvia and Jordan.

• More than have of the investments in ports were concluded through concession agreements, with more than a third Greenfield.

19 2,091

Airports • The average size of contract was almost $360m.

• Virtually all (87%) investment has taken place since 2005.

• Hungary and Turkey accounted for more than 80% of airport investment.

• Around half of airport deals were management/ lease contracts, with 41% concessions and only 10% Greenfield.

27 9,666

Rail • There have been far fewer rail projects, and as a result investment has been much more erratic over time, with 97% of investment being accounted for by two projects, one which was cancelled in Estonia and the Shar-Ust-Kamenogorsk Railway Concession in Kazakhstan.

7 530

Roads/bridges • Two-thirds of road investment occurred between 2004 and 2007, all taking place in Croatia, Hungary and Poland.

• Almost 60% of investment was Greenfield.

8 5,302

WATER & SANITATION

• More than a quarter of water sector investment took place before 2000 in the period, although this has subsequently picked up, with $1.9bn investments between 2003-07.

• More than a quarter of investments took place in Russia, with Romania and Turkey together accounting for almost 40%.

75 5,274

Utility network • Around 40% of investment during the period took place in the year 2000, with another third being secured between 2005 and 2007.

• The average utility network investment was $53m, with a third of investment overall taking place in Romania.

67 3,449

Treatment plant • 58% of investment in treatment plants during the period took place before 2000.

• The average treatment plant project involved an investment of $230m.

• Have of all investments in treatment plants took place in Turkey, with a further third in Russia.

8 1,825

TELECOMS • More than two-thirds of telecoms investment took place before 2000, although there 151 69,736

34

Sector / subsector

Observations Total no. of projects

Value of commitments

was more than $12.5bn between 2005 and 2007.

• 16% of investments have taken place in Turkey, with around half in the EU accession countries (including nearly $2bn in Poland).

Fixed and long • Three quarters of fixed line projects took place between 1996 and 1999.

• 37% of investments took place in Poland, with 18% in Turkey.

39 17,953

Mobile or mobile combined

• 54% of projects were closed before 2000.

• 42% of investment has taken place in EU accession countries, with Ukraine, Turkey, Serbia and Russia together accounting for 37%.

112 51,784

35

Table A4.6: PPI projects and investments (in US $) in Latin America and the Caribbean 1996-2007

Sector / subsector

Observations Total no. of projects

Value of commitments

ENERGY • Almost 70% of investments in Energy came before 2000. While only 7% of investments were made between 2004 and 2006, this amounted to $7.7bn.

• 58% of investments were made in Brazil, with 23% in Argentina, Colombia and Mexico. 64% of investment in Brazil was in 1996-98.

• Investments were made through more than $49bn in Greenfield projects, almost $56bn in divestitures and $1.2bn in concessions.

• The average investment was more than $285m per project, with 39% of projects smaller than $75m, and 46% greater than $150m.

372 106,307

Electricity generation

• Investments in electricity generation have been relatively spread over the period but have still clearly fallen since the 1990s, with 57% 1996-99, 34% 2000-03 and 8% 2004-06.

• Less than half of investments in projects involving new generating capacity were made in Brazil, with Argentina and Mexico sharing 23%, and 22% in Peru, Colombia, Chile and the Dominican Republic.

• Two-thirds of investment was Greenfield.

• Generation projects involving network investment, gas transmission or electricity distribution, were, on average, four times the size of generating only projects.

213 49,279

Integrated electricity generation and distribution/ transmission

• 93% of investments in integrated electricity infrastructure were made in 1996-97, and were all divestitures.

• Integrated projects were worth, on average, $685m, virtually all in Brazil.

12 8,215

Electricity distribution / transmission

• Despite encouraging signs in 2006, with almost $2.3bn invested, 72% of sector investment took place in the years 1996-98. More than 80% of regional electricity network investment consisted of divestitures.

• Three quarters of network investments were made in Brazil, with another 11% in Argentina.

• The average project was worth nearly $390m, and was much larger for projects involving distribution elements.

85 32,890

Gas distribution / transmission

• 80% of gas investment over the period was in 1996-98. Between 2004 and 2006, there was just $181m PPI investment.

• Brazil accounts for 37% of investments, with Bolivia picking up 20%.

• Gas transmission projects involved investment, on average, of $378m, compared with $169m

62 15,922

36

Sector / subsector

Observations Total no. of projects

Value of commitments

for distribution projects.

• 70% of investments were Greenfield, with a further 27% divestitures.

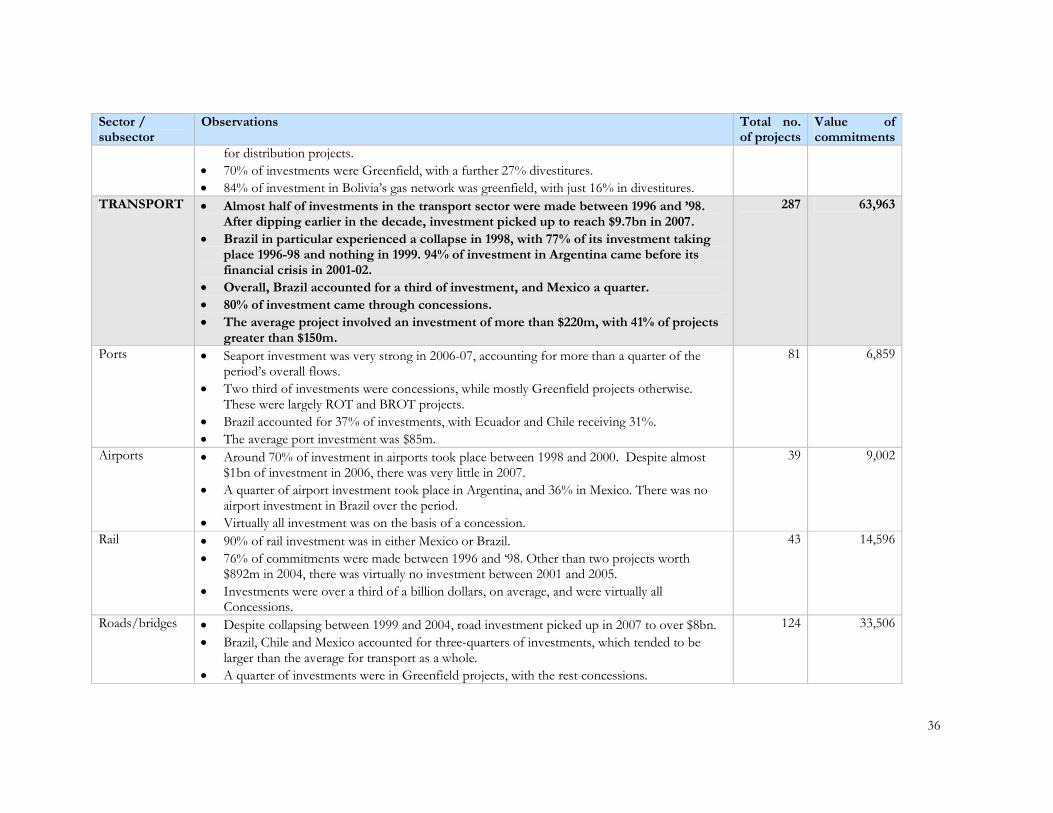

• 84% of investment in Bolivia’s gas network was greenfield, with just 16% in divestitures. TRANSPORT • Almost half of investments in the transport sector were made between 1996 and ’98.

After dipping earlier in the decade, investment picked up to reach $9.7bn in 2007.

• Brazil in particular experienced a collapse in 1998, with 77% of its investment taking place 1996-98 and nothing in 1999. 94% of investment in Argentina came before its financial crisis in 2001-02.

• Overall, Brazil accounted for a third of investment, and Mexico a quarter.

• 80% of investment came through concessions.

• The average project involved an investment of more than $220m, with 41% of projects greater than $150m.

287 63,963

Ports • Seaport investment was very strong in 2006-07, accounting for more than a quarter of the period’s overall flows.

• Two third of investments were concessions, while mostly Greenfield projects otherwise. These were largely ROT and BROT projects.

• Brazil accounted for 37% of investments, with Ecuador and Chile receiving 31%.

• The average port investment was $85m.

81 6,859

Airports • Around 70% of investment in airports took place between 1998 and 2000. Despite almost $1bn of investment in 2006, there was very little in 2007.

• A quarter of airport investment took place in Argentina, and 36% in Mexico. There was no airport investment in Brazil over the period.

• Virtually all investment was on the basis of a concession.

39 9,002

Rail • 90% of rail investment was in either Mexico or Brazil.

• 76% of commitments were made between 1996 and ‘98. Other than two projects worth $892m in 2004, there was virtually no investment between 2001 and 2005.

• Investments were over a third of a billion dollars, on average, and were virtually all Concessions.

43 14,596

Roads/bridges • Despite collapsing between 1999 and 2004, road investment picked up in 2007 to over $8bn.

• Brazil, Chile and Mexico accounted for three-quarters of investments, which tended to be larger than the average for transport as a whole.

• A quarter of investments were in Greenfield projects, with the rest concessions.

124 33,506

37

Sector / subsector

Observations Total no. of projects

Value of commitments

WATER & SANITATION

• More than three-quarters of investments in the water sector were made between 1996 and 2000, including over $6bn in 1999. Annual investments have not totalled more than $1bn since 2001.

• Brazil, Chile and Argentina account for 72% of investments.

• 37% of investments were divestitures, with 53% concessions.

• More than three-quarters of projects were worth less than $75m, with the average project just over $100m.

166 17,003

Utility network • The average utility investment was almost three times the size of investments in treatment plants.

• 87% of investments took place before 2002.

• 78% of investments were made in Argentina, Brazil and Chile.

• 41% of investments were concessions, with 59% divestitures.

130 15,364

Treatment plant • Half of the investments in treatment plants were made between 2004 and ’07, following two years of zero investment.

• Investment is highly concentrated in Mexico (62%), and 95% of the total were in greenfield projects.

36 1,638

TELECOMS • 83% of telecoms investment took place between 1886 and ’98, with $76bn in 1998 alone. In contrast, there has been only $1.3bn since 2002.

• 61% of investments were divestitures, and 78% took place in Brazil.

96 117,484

Fixed and long • Virtually all investment in telecoms with no mobile phone element took place in the 1990s. 36 36,578

Mobile or mobile combined

• Since 2001, in which $12.5bn was invested in projects with some mobile phone component, there has been less than $1bn investment in total.

60 80,906

38

5. ANNEX 5: AN ANALYSIS OF PPIAF’S PORTFOLIO USING THE

SUGGESTED REVISED CATEGORISATION OF ACTIVITIES

In this annex, we present an analysis of the PPIAF portfolio by geography, sector,

intervention size, and activity focus as a means to consider the extent to which PPIAF

activities are relevant to the current market context and needs.

5.1. Geography

Figure A5.1 below presents the percentage share of total annual PPIAF spend for each

region (including global activities) for the period 2000-08. As can be seen from the figure,

the SSA region has on average received over 22% of total PPIAF annual spend since 2000,

with its share in 2007 and 2008 being the highest (44% and 45% respectively). This has

commensurately resulted in a relative reduction in PPIAF expenditure in the LAC and EAP

regions in recent years. Overall, the MENA region has received the smallest share of PPIAF

activities (4%), but has shown some growth in recent years.

Figure A5.1: Percentage share of total PPIAF spend per year by regions, FY2000-2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Percentage of PPIAF interventions by value

EAP ECA Global LAC MENA SAR SSA

The changing trend in regional focus over the period 2000-08 is further highlighted in Figure

A5.2 below.2 As evident, an increasing number of projects (in terms of percentage share in

total value) are being undertaken in the SSA region. The EAP, SAR and LAC regions exhibit

a declining trend. ECA and Global projects are not depicted in the graph below as the trend

line appears fairly constant.

2 For simplicity, we have calculated and presented the linear trend over time.

39

Figure A5.2: Trend in PPIAF interventions by region, 2000-2008

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Linear (SSA) Linear (EAP) Linear (SAR) Linear (LAC) Linear (MENA)

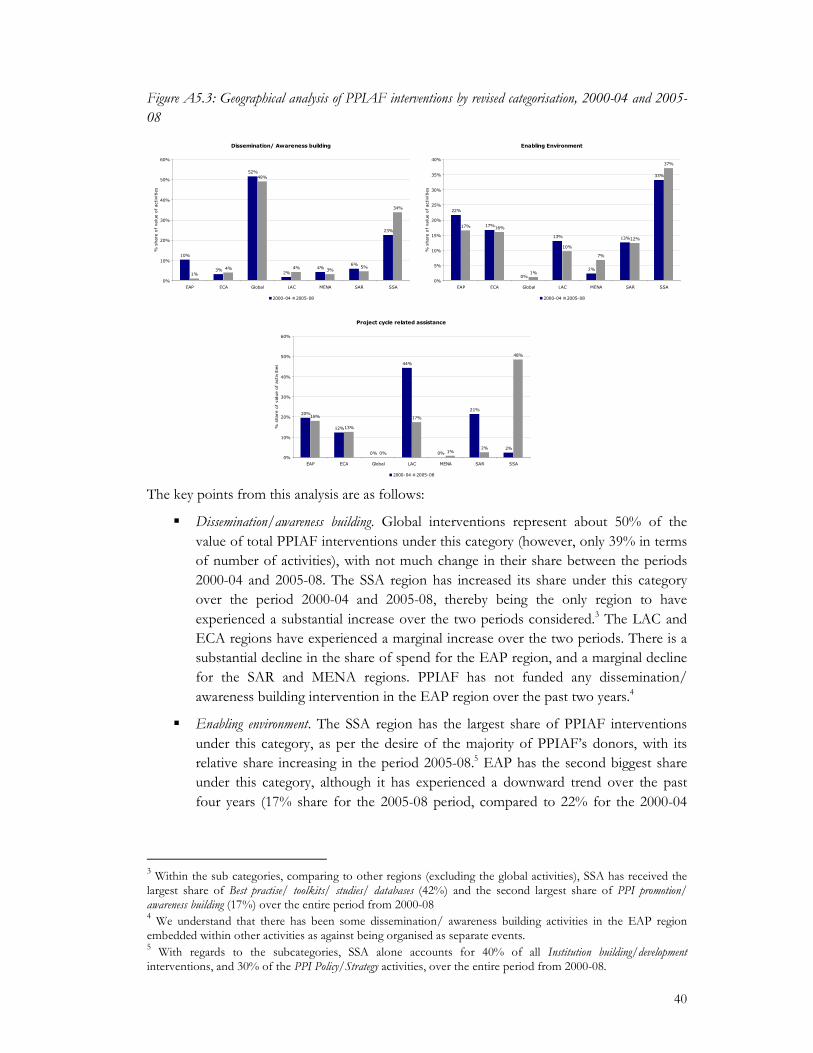

Figure A5.3 below presents a geographical analysis of the value of PPIAF interventions by

the revised categorisation. The figure considers the changing trend (if any) between the two

strategic review periods - 2000-04 and 2005-08.

40

Figure A5.3: Geographical analysis of PPIAF interventions by revised categorisation, 2000-04 and 2005-

08

The key points from this analysis are as follows:

� Dissemination/awareness building. Global interventions represent about 50% of the

value of total PPIAF interventions under this category (however, only 39% in terms

of number of activities), with not much change in their share between the periods

2000-04 and 2005-08. The SSA region has increased its share under this category

over the period 2000-04 and 2005-08, thereby being the only region to have

experienced a substantial increase over the two periods considered.3 The LAC and

ECA regions have experienced a marginal increase over the two periods. There is a

substantial decline in the share of spend for the EAP region, and a marginal decline

for the SAR and MENA regions. PPIAF has not funded any dissemination/

awareness building intervention in the EAP region over the past two years.4

� Enabling environment. The SSA region has the largest share of PPIAF interventions

under this category, as per the desire of the majority of PPIAF’s donors, with its

relative share increasing in the period 2005-08.5 EAP has the second biggest share

under this category, although it has experienced a downward trend over the past

four years (17% share for the 2005-08 period, compared to 22% for the 2000-04

3 Within the sub categories, comparing to other regions (excluding the global activities), SSA has received the

largest share of Best practise/ toolkits/ studies/ databases (42%) and the second largest share of PPI promotion/ awareness building (17%) over the entire period from 2000-08 4 We understand that there has been some dissemination/ awareness building activities in the EAP region

embedded within other activities as against being organised as separate events. 5 With regards to the subcategories, SSA alone accounts for 40% of all Institution building/development

interventions, and 30% of the PPI Policy/Strategy activities, over the entire period from 2000-08.

Dissemination/ Awareness building

10%

3%

52%

2%4%

6%

23%

1%

4%

49%

4%3%

5%

34%

0%

10%

20%

30%

40%

50%

60%

EAP ECA Global LAC MENA SAR SSA

% share of value of activities

2000-04 2005-08

Enabling Environment

22%

17%

0%

13%

2%

13%

33%

17% 16%

1%

10%

7%

12%

37%

0%

5%

10%

15%

20%

25%

30%

35%

40%

EAP ECA Global LAC MENA SAR SSA

% share of value of activities

2000-04 2005-08

Project cycle related assistance

20%

12%

0%

44%

0%

21%

2%

18%

13%

0%

17%

1%2%

48%

0%

10%

20%

30%

40%

50%

60%

EAP ECA Global LAC MENA SAR SSA

% share of value of activities

2000-04 2005-08

41

period). PPIAF enabling environment interventions in the MENA region have

increased in the period 2005-08.6

• Project/transaction support. The SSA region has experienced a considerable increase

over the two periods under consideration – from 2% over the period 2000-04 to

48% over the period 2005-08.7 The LAC and SAR regions have experienced a

decline. However, important to note is that the number of activities in this category

have been much fewer than that in the other two categories discussed above.

5.1.1. Analysis by DAC country list

As shown in Figure A5.4, the Enabling environment category has the largest share of activities

in all the four DAC list columns (between 80-87% of total on average in each DAC list

column). Activities in the Project/transaction support category have a higher share in DAC list

column 1 and 3 compared to DAC list 2 and 4. In relation to the Dissemination/awareness

building category, 53% of all PPIAF approved applications belong to countries under the

DAC list column 1.

Figure A5.4: PPIAF interventions by category and DAC list8

31 1 1

27

21

34

7

2

4

1

4

0

5

10

15

20

25

30

35

40

45

DAC 1 DAC 2 DAC 3 DAC 4

Value of interventions (US$ m

)

Dissemination/Awareness building Enabling Environment Project/transaction support

5.2. Sector

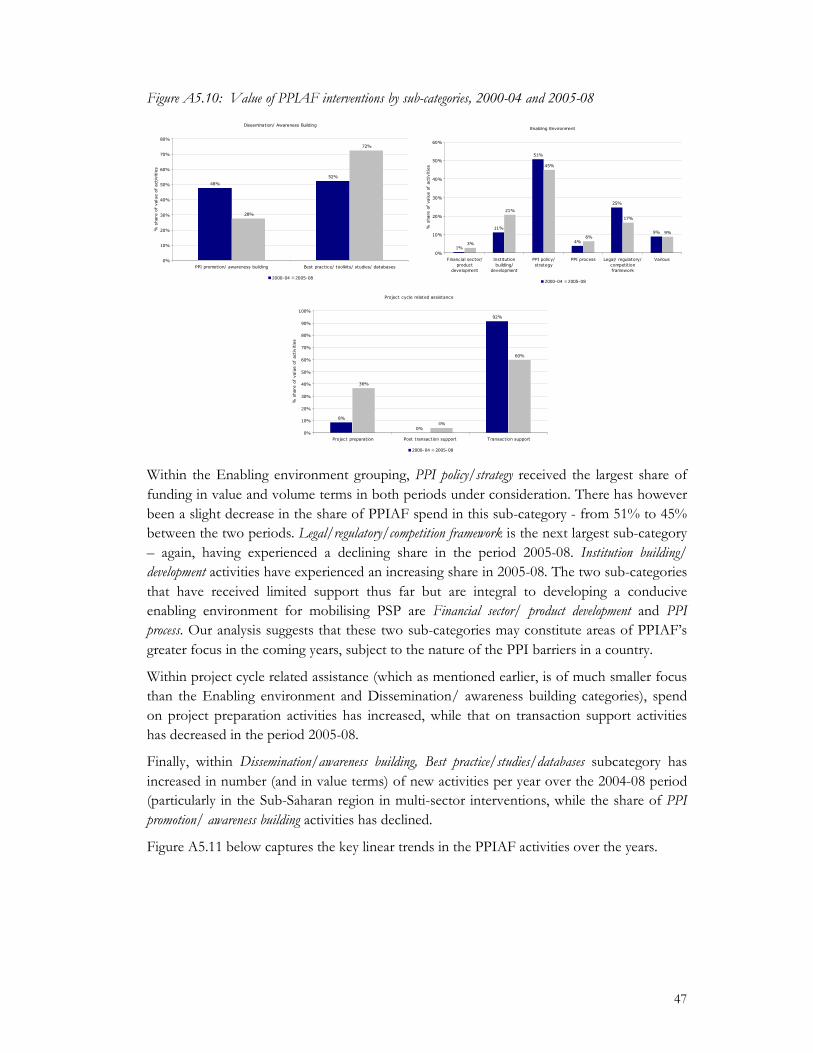

Figure A5.5 below depicts the share of activities by sector in the annual PPIAF spend.

Looking at the figure, multi-sector activities have, on average, been the largest focus (37%),

followed by the energy and W&S sectors (both 19%). The telecoms sector has received the

6 Some of the detail of the yearly trend is presented in Annex 4.

7 With regards to the subcategories, SSA accounts for all Post Transaction Support interventions and 50% of the Project Preparation activities 8 Note that this analysis does not include US$40.5m (224 interventions) that could not be classified.

42

smallest share of PPIAF activities (9%), particularly in recent years where the range of

activities undertaken has been severely restricted to direct pro-poor ones.

Figure A5.5: Total PPIAF interventions by sector, FY2000-2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

% of PPIAF intervention by value

Energy Multi-Sector Telecoms Transport W&S

Figure A5.6 below brings out the trend change in share of PPIAF spend by sector.9 As the

figure depicts, there has been an increasing focus on the transport and energy sectors, and a

declining focus on the W&S sector. Multi-sector and telecoms projects did not exhibit any

major change in trend over the period (and hence have not been presented in the figure).