wade leach, senior vice president commercial, ati specialty … · 2018-04-14 · freight ton miles...

TRANSCRIPT

© 2015 ATI. All Rights Reserved. ® Registered Trademark of ATI Properties Inc.

Wade Leach, Senior Vice President Commercial, ATI Specialty Materials October 5, 2015

© ATI 2015. All Rights Reserved. 2

Forward Looking Statements

This presentation contains forward-looking statements. Actual results may differ materially from results anticipated in

the forward-looking statements. These and additional risk factors are described from time to time in the Company’s

filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended

December 31, 2014.

© 2015 ATI. All Rights Reserved. ® Registered Trademark of ATI Properties Inc.

Wade Leach, Senior Vice President Commercial, ATI Specialty Materials October 5, 2015

© ATI 2015. All Rights Reserved. 4

Traffic (RPMs)

Market Drivers

0

20

40

60

80

100

120

140

160

180

200

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Commercial Aerospace Market Forecast

Passenger Miles

Freight Miles

Reve

nue

Pass

enge

r Mile

s (Bi

llion

s)

Frei

ght T

on M

iles (

Billi

ons)

History Forecast

Source: Airline Monitor, IATA, ICAO

© ATI 2015. All Rights Reserved. 5

Capacity (ASMs)

Traffic (RPMs)

Market Drivers

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1990 1995 2000 2005 2010 2015 2020

Available Seat Miles (ASMs) Market Forecast

Avai

labl

e Se

at M

iles (

Billi

ons)

History Forecast

Source: Airline Monitor

© ATI 2015. All Rights Reserved. 6

-30

-20

-10

0

10

20

30

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2000 2002 2004 2006 2008 2010 2012 2014

Global Commercial Airline Profitability

% re

venu

es

US$

bill

ion

Market Drivers

Airline Profitability

Traffic (RPMs)

Capacity (ASMs)

Source: IATA Economics

EBIT Margin

Net post-tax profit

© ATI 2015. All Rights Reserved. 7

Airline Profitability

Fuel Costs

Traffic (RPMs)

Market Drivers

Capacity (ASMs)

Jet Fuel Price and Crude Oil Price

Source: Platts, IATA

© ATI 2015. All Rights Reserved. 8

Fuel Costs

Traffic (RPMs)

Market Drivers

Capacity (ASMs)

Airline Profitability

Economic Turmoil

© ATI 2015. All Rights Reserved. 9

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Military Aircraft

Regionals

Airbus

Boeing

# of

Airc

raft

B787 A350

C-Series A320neo

MRJ B737max

E2-Jets A330neo B777x

C919

2010-2019 CAGR = 7.8%

Aircraft Build Rates

Source: Airline Monitor and Forecast International

© ATI 2015. All Rights Reserved. 10

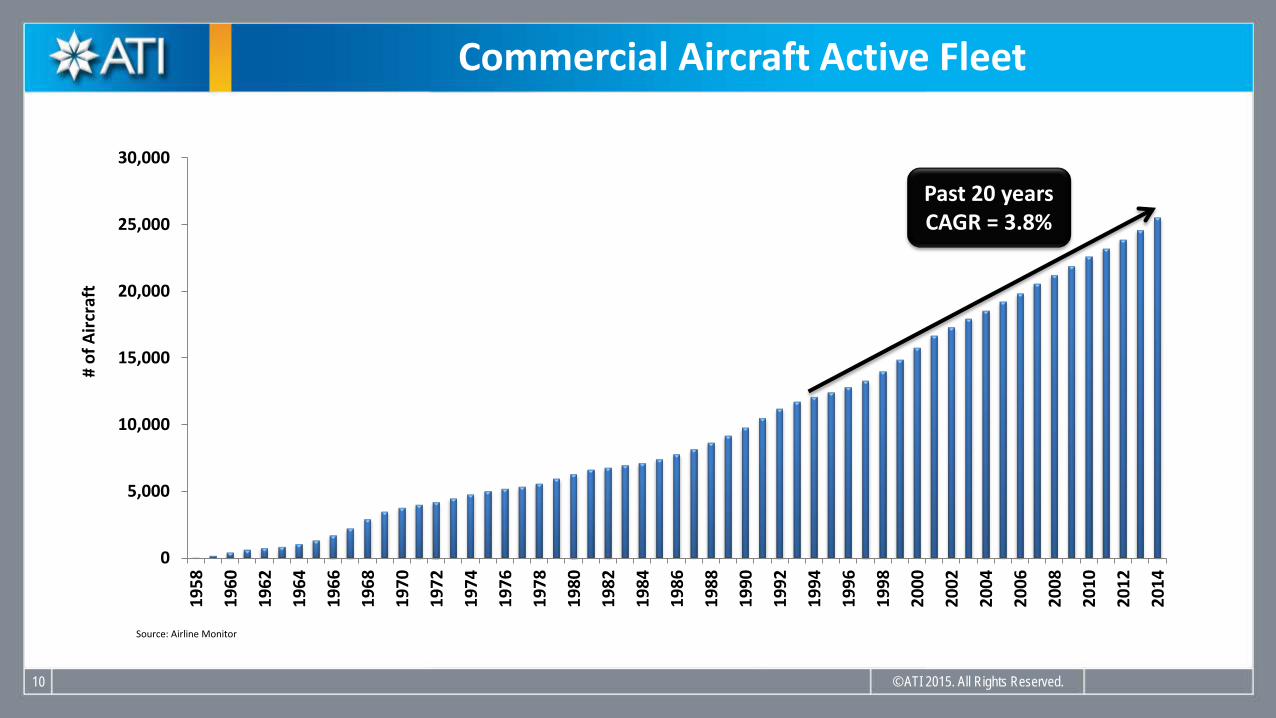

0

5,000

10,000

15,000

20,000

25,000

30,000

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

# of

Airc

raft

Past 20 years CAGR = 3.8%

Commercial Aircraft Active Fleet

Source: Airline Monitor

© ATI 2015. All Rights Reserved. 11

0%

2%

4%

6%

8%

10%

12%

14%

16%

1960 1965 1970 1975 1980 1985 1990 1995 2000

% w

eigh

t of t

itani

um

B777

A330/A340

B737 B757

B727 A300 B767

B747

Historical Titanium Usage in Commercial Aircraft

Source: Roskill Economics of Titanium Note: Titanium content per Airframe (engine not included)

© ATI 2015. All Rights Reserved. 12

0

10,000

20,000

30,000

40,000

50,000

60,000

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

# of

Airc

raft

Past 20 years CAGR = 3.8%

Next 20 years CAGR = 3.6%

Commercial Aircraft Active Fleet

Source: Airline Monitor

Aircraft Fleet to double in the next 20 years

© ATI 2015. All Rights Reserved. 13

Next Generation Titanium Usage in Commercial Aircraft

Source: Roskill Economics of Titanium, Goldman Sachs Note: Titanium content per Airframe (engine not included)

0%

2%

4%

6%

8%

10%

12%

14%

16%

1960 1970 1980 1990 2000 2010 2020

% w

eigh

t of t

itani

um

B787 A350

A380 B777

A330/A340

B737

B767

B757 B747

B727 A300

B777x?

B737Max A320Neo

© ATI 2015. All Rights Reserved. 14

Corrosion Resistance

Space Limitation

Heat Resistance

Weight Savings

Why Titanium?

Titanium Historic Advantages:

© ATI 2015. All Rights Reserved. 15

Passenger Comfort

Improved Maintenance

Increased Operating Efficiency

Trend of Titanium in Airframes

Rise of Composite & Titanium Airframes

© ATI 2015. All Rights Reserved. 16

Near-net products that improve buy-to-fly ratios

Engineering new alloys

Additive Manufacturing

Globalization of supply chain

Vertical integration

Expanding capacity

How is the industry answering the challenge?

Relentless Innovation ®