walloon spin-offs

TRANSCRIPT

28

SPECIAL ECONOMY

Walloon spin-offs Who are they?

To what economic impact?

WHAT IS THE NUMBER OF ACTIVE SPIN-OFFS IN WALLONIA? HOW MANY OF

THEM HAVE BEEN CREATED IN RECENT YEARS? WHAT ARE THEIR ORIGINS

AND IN WHICH BUSINESS SECTORS DO THEY OPERATE? HOW MANY JOBS

HAVE BEEN CREATED BY THESE STRUCTURES? HOW ARE THESE SPIN-

OFFS DISTRIBUTED AMONG MICRO-, SMALL-, MEDIUM- AND LARGE-SIZED

COMPANIES? WHO ARE THE

CHAMPIONS? AND WHAT IS

THEIR DYNAMIC IN TERMS

OF JOB GROWTH?

by Benoît PETRE

A spin-off is a company that aims

to commercially exploit products,

processes or know-how developed

within an higher education research

department. These structures are important

as Wallonia seeks to reorient its economy

towards the production of high value added

goods and services

Our list of Walloon spin-offs was compiled

from two different sources. The first consists

of official listings sent by certain universities

themselves (Université de Mons, Université

Catholique de Louvain and Université de

Liège). An alternative method was used

for other higher education institutions

(Université libre de Bruxelles, Université de

Namur and High Schools).

This information is then correlated with that of

the LIEU system, a public body which deals, in

particular, with the coordination of university

administrations in charge of spin-offs.

A database was established from the

annual accounts submitted by the spin-offs

identified above to the Central Balance

Sheet Office between 2004 and 2013. The

accounts of majority owned subsidiaries

active in Wallonia have been consolidated

with those of their parent company.

This research identified 192 active spin-

offs over the period 2004-2013. Of these

150 were active in 2013(1). Of these,

150 were active in 2013. The spin-offs

generated more than €246 millions of

added value(2) and 2679 jobs (FTE). Half

of these jobs came from spin-offs active

in one of the following three sectors:

computer programming & consultancy;

manufacture of pharmaceutical products;

and manufacture of computer, electronic

and optical products. The spin-offs from the

UCL and ULG alone account for 78% of total

employment generated by these operations

in 2013 compared with 12% for the ULB and

4% for UNamur and UMons.

The evolution of added value and jobs

created between 2004 and 2013 is illustrated

in Graphic 01. Both have seen a steady

growth during the reporting period,

despite an often challenging external

economic environment in Europe, increasing

employment by 80% and added value by

108%. As well as this solid performance from

existing spin-offs, another 90 (74 still being

active in 2013) new operations were also

registered between 2004-2013.

The Walloon spin-offs are relatively

heterogeneous from the perspectives

of size and age. This is illustrated in

Graphic 02. The spin-offs active in 2013 are

primarily micro (66%) or small enterprises

(25%). Medium-size companies account for

only 6% of all active spin-offs in 2013. And

only one spin-off, namely IBA (493 jobs) can

be considered as a large company.

In terms of age, spin-offs are predominantly

young, with half of them under 10 years old.

Nevertheless, one spin-off in five was more

than 20 years old in 2013. The oldest spin-

off, Slegten, celebrated its 66th anniversary

this year.

(1) 2013isthemostrecentyearintermsofavailablefinancialstatementssincetheyaregenerallygivenwithanoffsetyear.Theannualaccounts2014willonlybepresentedin2015.

(2) Theaddedvalueproducedbyacompanyrepresentsthewealthgeneratedbyit.Itisequivalenttothedifferencebetweentheturn-overofthelatter,thatistosay,theproductofitssales,anditsintermediateconsumptionexpenses,thatistosaywhatitbuysfromitsproviders.Thiswealthwillbedistributedamongworkersaswagesas,theownersofthecompany’scapitalthroughdividendsandthestateintheformoftaxesandduties.

KEY-FIGURES (2013) Total (150 spin-offs)

Average Median

Jobs (ETP) 2.679 18 4

Added value (k€) 246.000 1.643 244

Age (year) 0-66 11 10

DYNAM!SME 01-02/2015

29

This heterogeneity has the consequence

that a relatively small number of them are

responsible for the majority of employment,

net job creation and total added value

created. This is illustrated in Graphic 03.

We see that the spin-offs belonging to

the top 10% of their respective category

(employment, net job creation and added

value) accounts for around 2/3 of aggregate

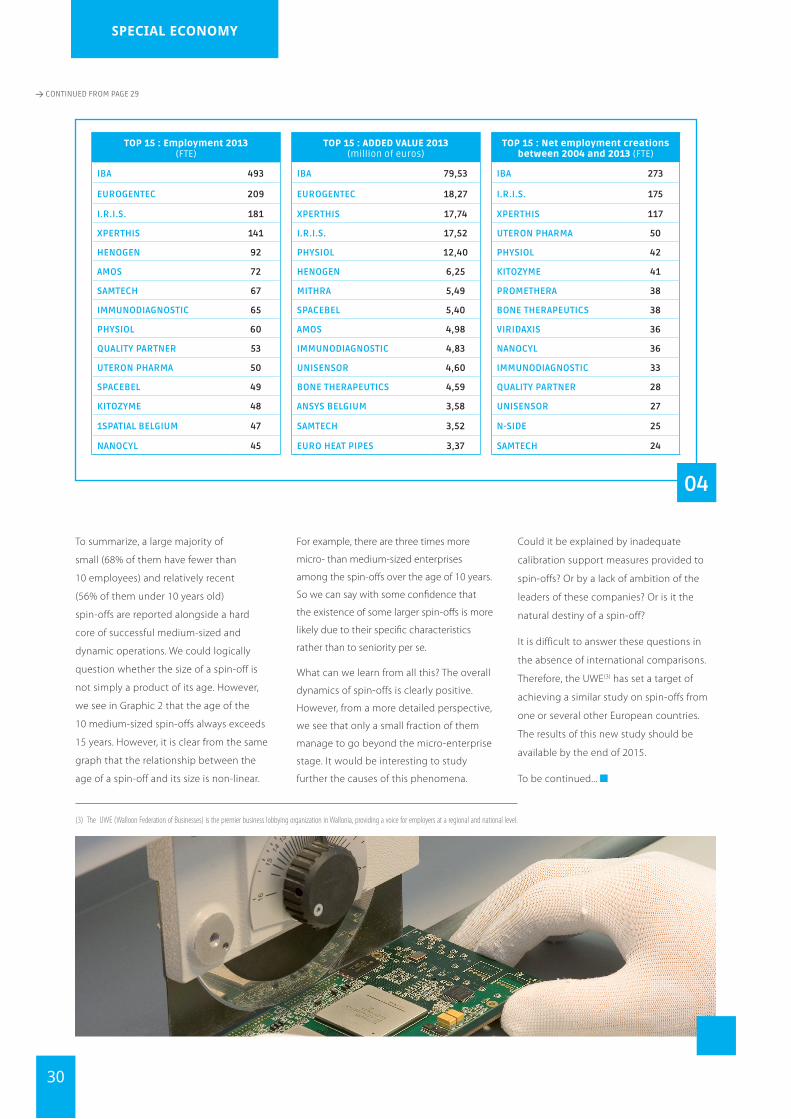

performance. A list of these fifteen spin-offs

that have distinguished themselves in a

particular area is shown in Table 04 (page 30)

The research also confirms that a spin-off

which excels in one area (employment,

net job creation and value added) is

typically very well placed in the other two

also. For example, IBA, IRIS, Xperthis and

Immunodiagnostic Systems feature in the

top 15 for each area. While this finding may

seem tautological, a spin-off cannot be

large without having experienced a period

of growth, it is important. Indeed, this

means that the positive dynamics in terms

of employment and added value created

by all the spin-offs between 2004 and 2013

is predominantly the result of just 15-20

spin-offs.

EVOLUTION OF TOTAL ADDED VALUE AND TOTAL EMPLOYMENT IN WALLOON SPIN-OFFS In full-time equivalent (FTE) or millions of euros (2004-2013)

01

DISTRIBUTION OF PIN-OFFS PER AGE AND EMPLOYMENT* - 150 ACTIVE SPIN-OFFS IN 2013*The results are similar with the added value as its correlation with employment is strong (R-squared = 85%)

02

DISTRIBUTION OF EMPLOYMENT, OF THE ADDED VALUE AND OF THE NET JOB CREATIONS IN THE SPIN-OFFS

03

0

500

1000

1500

2000

2500

3000

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Millions

Total added value (left) Total employment (right)

0 1-5 6-10 11-20 21-50 51-100 > 100

>21 3 3 2 5 4 4

16-20 1 1 3 2 2

11-15 7 10 3 6 7 2

6-10 9 11 11 9 2

>5 16 21 3 1 2

top 1562%

13538%

Répartition de l'emploi dans les spin‐offs en 2013

top 1568%

10232%

Répartition de la valeur ajoutée dans les spin‐offs dont la valeur ajoutée est positive en 2013

top 1564%

13536%

Répartition des création net d'emploi sur la période 2004‐2013Distribution of

employment in the spin-offs in 2013

Distribution of the added value in the spin-offs** in 2013 Distribution of the

net job creations in the period

2004-2013

FTE

AG

E

** Only the spin-offs whose added value is positive in 2013 (113 spin-offs).

> CONTINUED ON PAGE 30

Mill

ions

€

30

SPECIAL ECONOMY

To summarize, a large majority of

small (68% of them have fewer than

10 employees) and relatively recent

(56% of them under 10 years old)

spin-offs are reported alongside a hard

core of successful medium-sized and

dynamic operations. We could logically

question whether the size of a spin-off is

not simply a product of its age. However,

we see in Graphic 2 that the age of the

10 medium-sized spin-offs always exceeds

15 years. However, it is clear from the same

graph that the relationship between the

age of a spin-off and its size is non-linear.

For example, there are three times more

micro- than medium-sized enterprises

among the spin-offs over the age of 10 years.

So we can say with some confidence that

the existence of some larger spin-offs is more

likely due to their specific characteristics

rather than to seniority per se.

What can we learn from all this? The overall

dynamics of spin-offs is clearly positive.

However, from a more detailed perspective,

we see that only a small fraction of them

manage to go beyond the micro-enterprise

stage. It would be interesting to study

further the causes of this phenomena.

Could it be explained by inadequate

calibration support measures provided to

spin-offs? Or by a lack of ambition of the

leaders of these companies? Or is it the

natural destiny of a spin-off?

It is difficult to answer these questions in

the absence of international comparisons.

Therefore, the UWE(3) has set a target of

achieving a similar study on spin-offs from

one or several other European countries.

The results of this new study should be

available by the end of 2015.

To be continued...

TOP 15 : Employment 2013 (FTE)

TOP 15 : ADDED VALUE 2013 (million of euros)

TOP 15 : Net employment creations between 2004 and 2013 (FTE)

IBA 493 IBA 79,53 IBA 273

EUROGENTEC 209 EUROGENTEC 18,27 I.R.I.S. 175

I.R.I.S. 181 XPERTHIS 17,74 XPERTHIS 117

XPERTHIS 141 I.R.I.S. 17,52 UTERON PHARMA 50

HENOGEN 92 PHYSIOL 12,40 PHYSIOL 42

AMOS 72 HENOGEN 6,25 KITOZYME 41

SAMTECH 67 MITHRA 5,49 PROMETHERA 38

IMMUNODIAGNOSTIC 65 SPACEBEL 5,40 BONE THERAPEUTICS 38

PHYSIOL 60 AMOS 4,98 VIRIDAXIS 36

QUALITY PARTNER 53 IMMUNODIAGNOSTIC 4,83 NANOCYL 36

UTERON PHARMA 50 UNISENSOR 4,60 IMMUNODIAGNOSTIC 33

SPACEBEL 49 BONE THERAPEUTICS 4,59 QUALITY PARTNER 28

KITOZYME 48 ANSYS BELGIUM 3,58 UNISENSOR 27

1SPATIAL BELGIUM 47 SAMTECH 3,52 N-SIDE 25

NANOCYL 45 EURO HEAT PIPES 3,37 SAMTECH 24

04

> CONTINUED FROM PAGE 29

(3) TheUWE(WalloonFederationofBusinesses)isthepremierbusinesslobbyingorganizationinWallonia,providingavoiceforemployersataregionalandnationallevel.