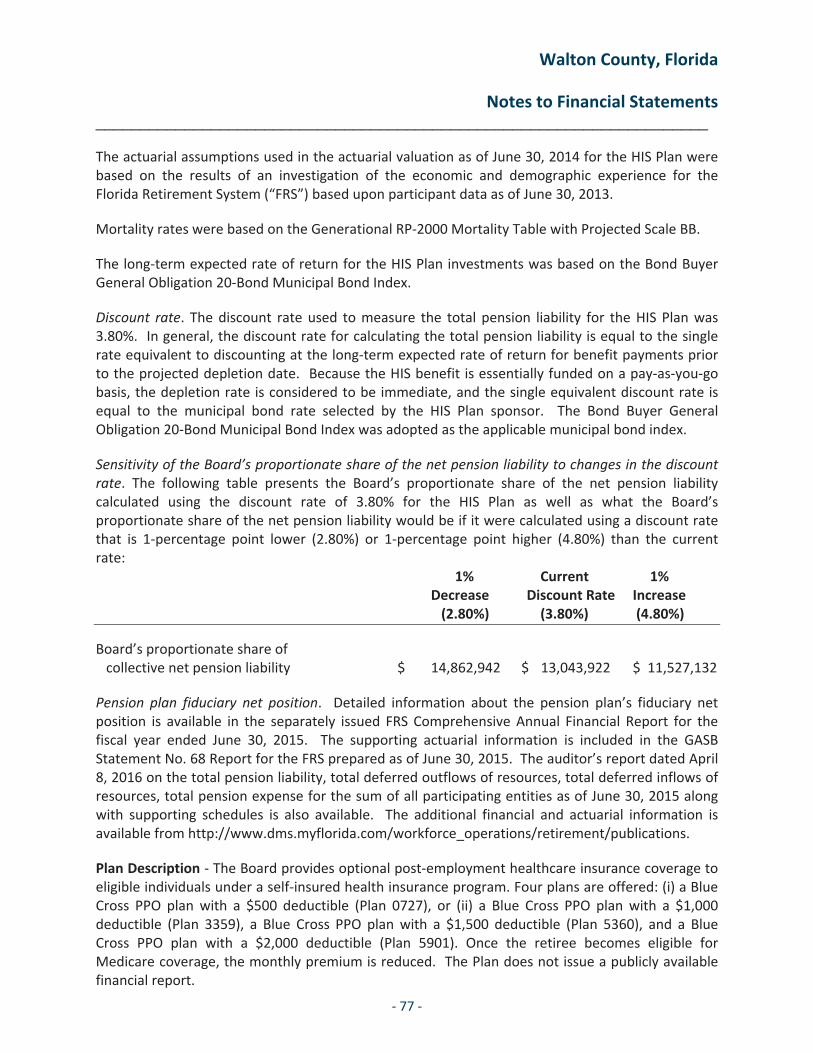

walton county, florida - flauditor.gov rpts/2015 walton county.pdf · 30-09-2015 · and fairness...

TRANSCRIPT

WALTON COUNTY, FLORIDA

COMPREHENSIVE ANNUAL FINANCIAL REPORT

for the fiscal year ended

September 30, 2015

Prepared by the Office of the Clerk of Circuit Court and County Comptroller

WALTON COUNTY, FLORIDA

PRINCIPAL OFFICERS

BOARD OF COUNRY COMMISSIONERS

Bill Imfeld Chair – District 3 Cindy Meadows Vice-Chair – District 5 Bill Chapman Commissioner – District 1 Cecilia Jones Commissioner – District 2 Sara Comander Commissioner – District 4 Tax Collector Sheriff Rhonda Skipper Michael A. Adkinson, Jr. Property Appraiser Supervisor of Elections Patrick Pilcher Bobby Beasley

Clerk of the Circuit Court Alex Alford

INTRODUCTORY SECTION

TABLE OF CONTENTS

LETTER OF TRANSMITTAL

CERTIFICATE OF ACHIEVEMENT FOR EXCELLENCE IN FINANCIAL REPORTING

ORGANIZATIONAL CHART

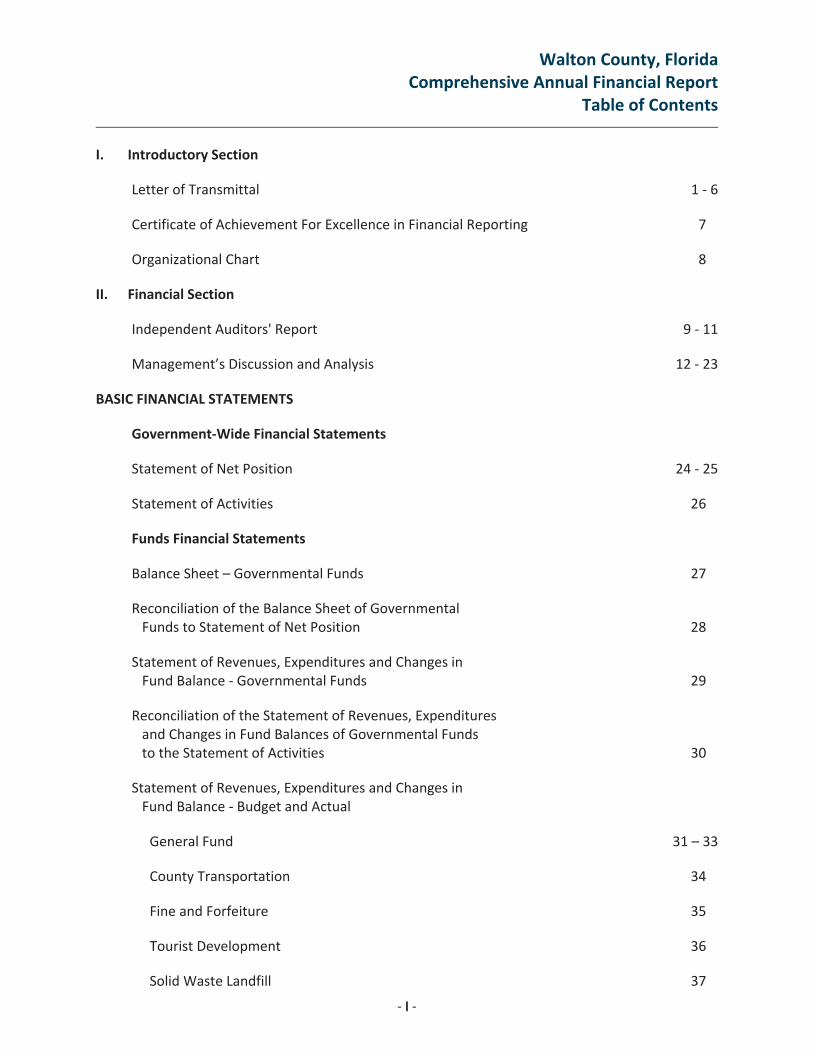

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

II

I. Introductory Section

Letter of Transmittal 1 6

Certificate of Achievement For Excellence in Financial Reporting 7

Organizational Chart 8

II. Financial Section

Independent Auditors' Report 9 11

Management’s Discussion and Analysis 12 23

BASIC FINANCIAL STATEMENTS

Government Wide Financial Statements

Statement of Net Position 24 25

Statement of Activities 26

Funds Financial Statements

Balance Sheet – Governmental Funds 27

Reconciliation of the Balance Sheet of GovernmentalFunds to Statement of Net Position 28

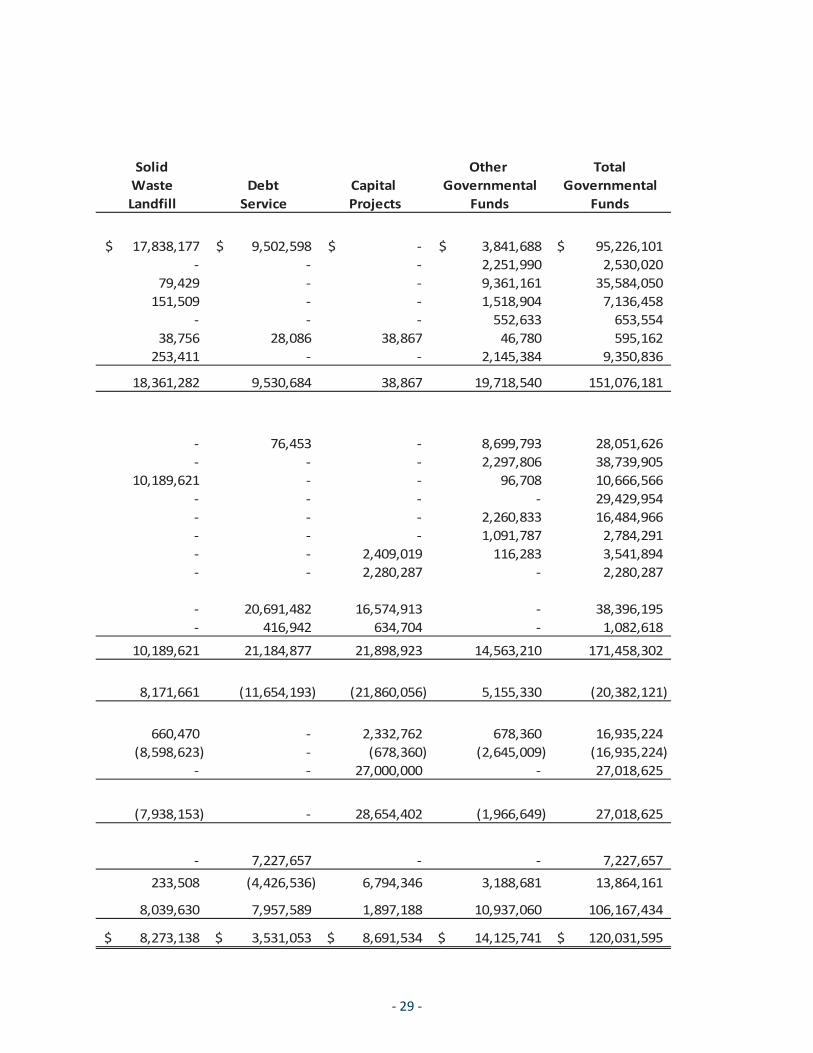

Statement of Revenues, Expenditures and Changes inFund Balance Governmental Funds 29

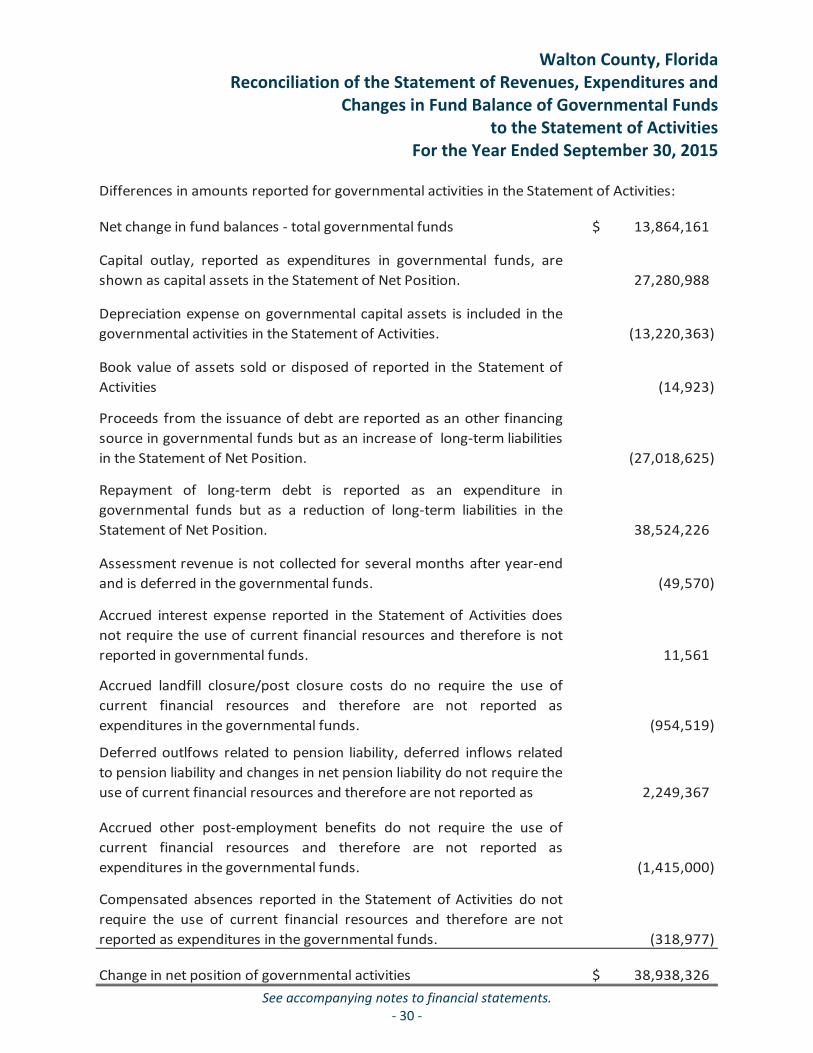

Reconciliation of the Statement of Revenues, Expendituresand Changes in Fund Balances of Governmental Fundsto the Statement of Activities 30

Statement of Revenues, Expenditures and Changes inFund Balance Budget and Actual

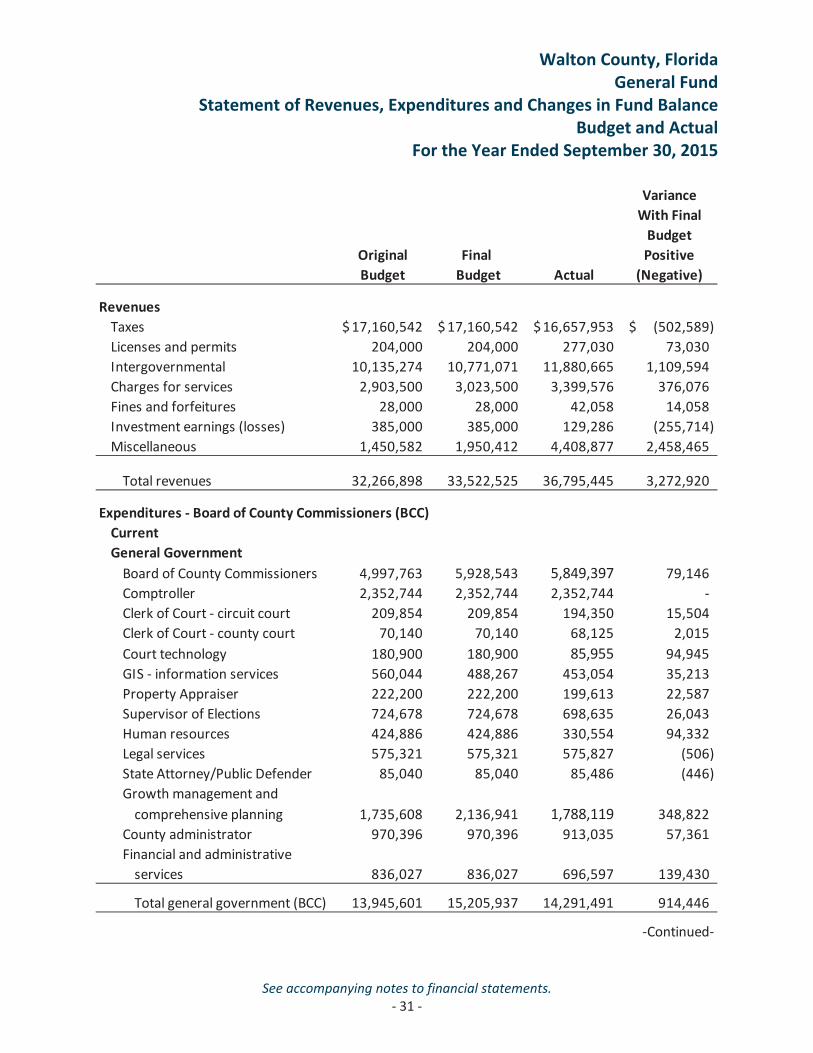

General Fund 31 – 33

County Transportation 34

Fine and Forfeiture 35

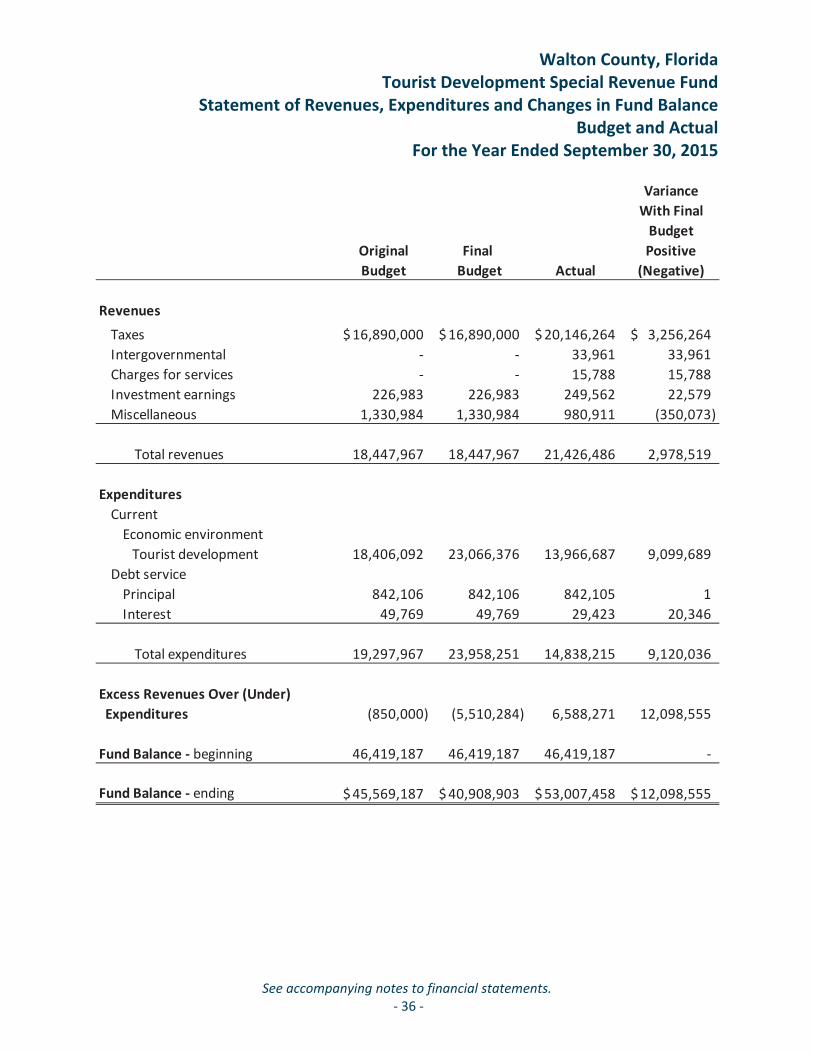

Tourist Development 36

Solid Waste Landfill 37

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

IIII

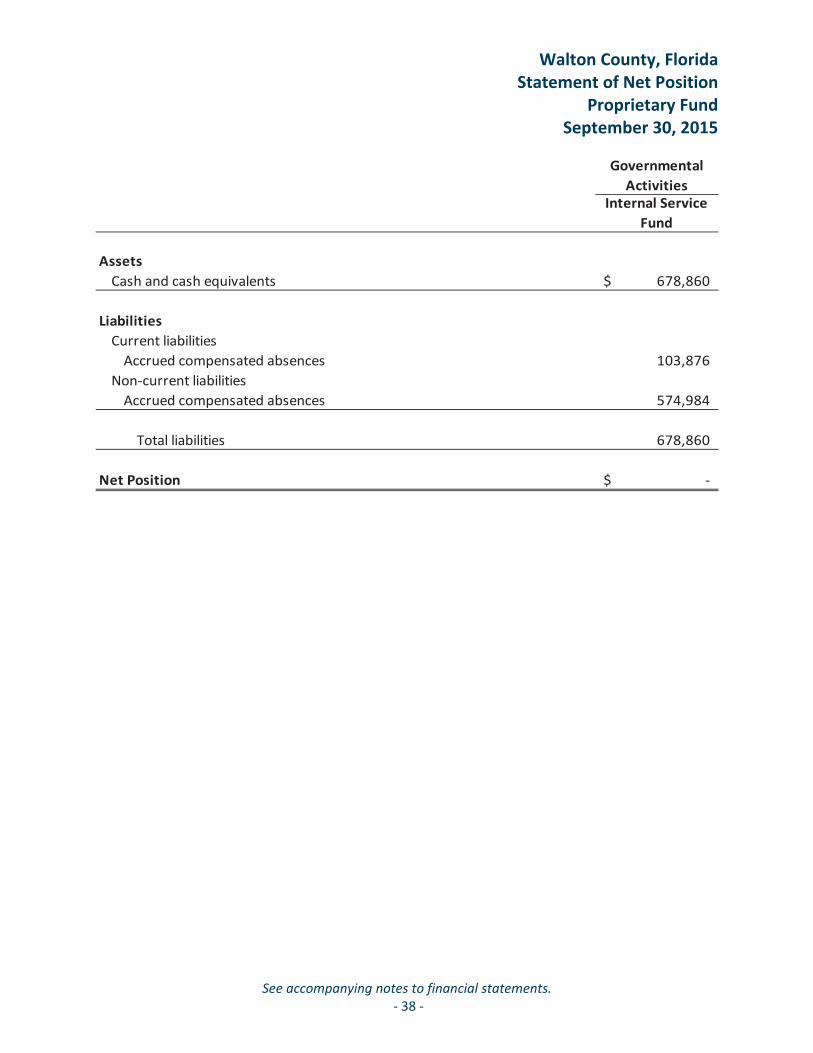

Statement of Net Position – Proprietary Fund 38

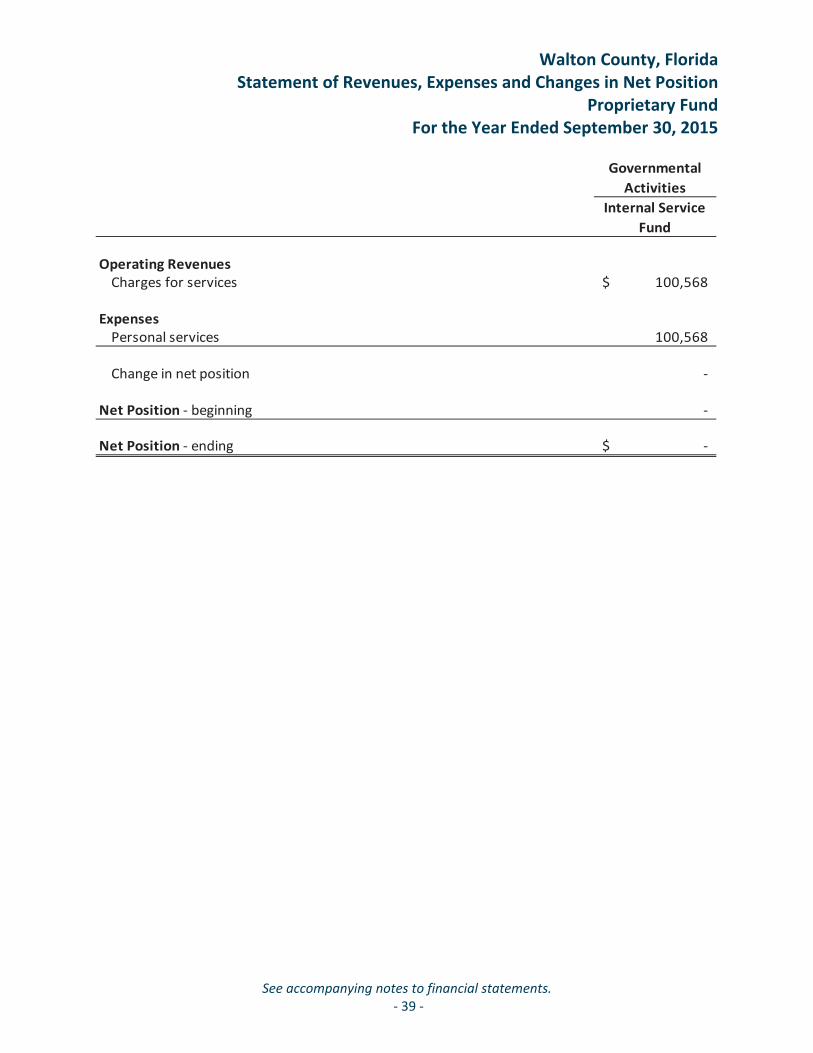

Statement of Revenues, Expenses and Changes in Net Position –Proprietary Fund 39

Statement of Cash Flows – Proprietary Fund 40

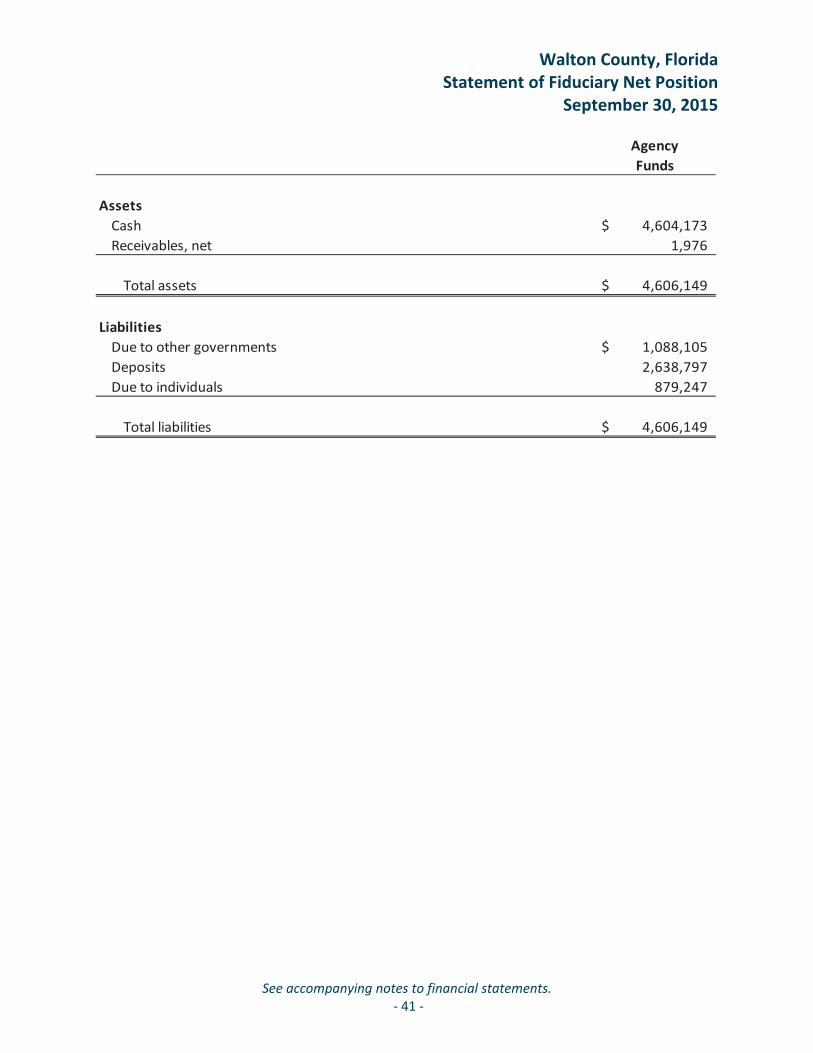

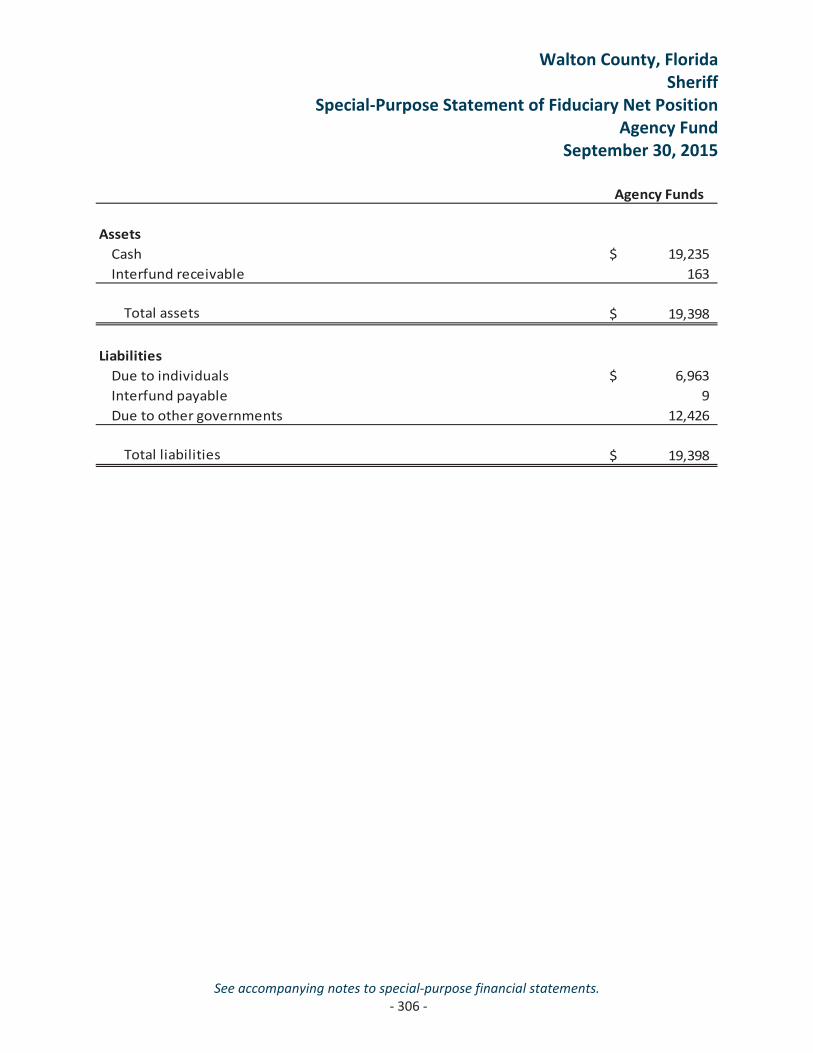

Statement of Fiduciary Net Position – Agency Funds 41

Notes to Financial Statements 42 84

REQUIRED SUPPLEMENTARY INFORMATION

Post Employment Benefits Plan Schedule of Funding Progress 85

Schedule of Employer’s Proportionate Share of the Net Pension Liability –Florida Retirement Systems Pension Plan 86

Schedule of Employer Contributions – Florida Retirement Systems Pension Plan 87

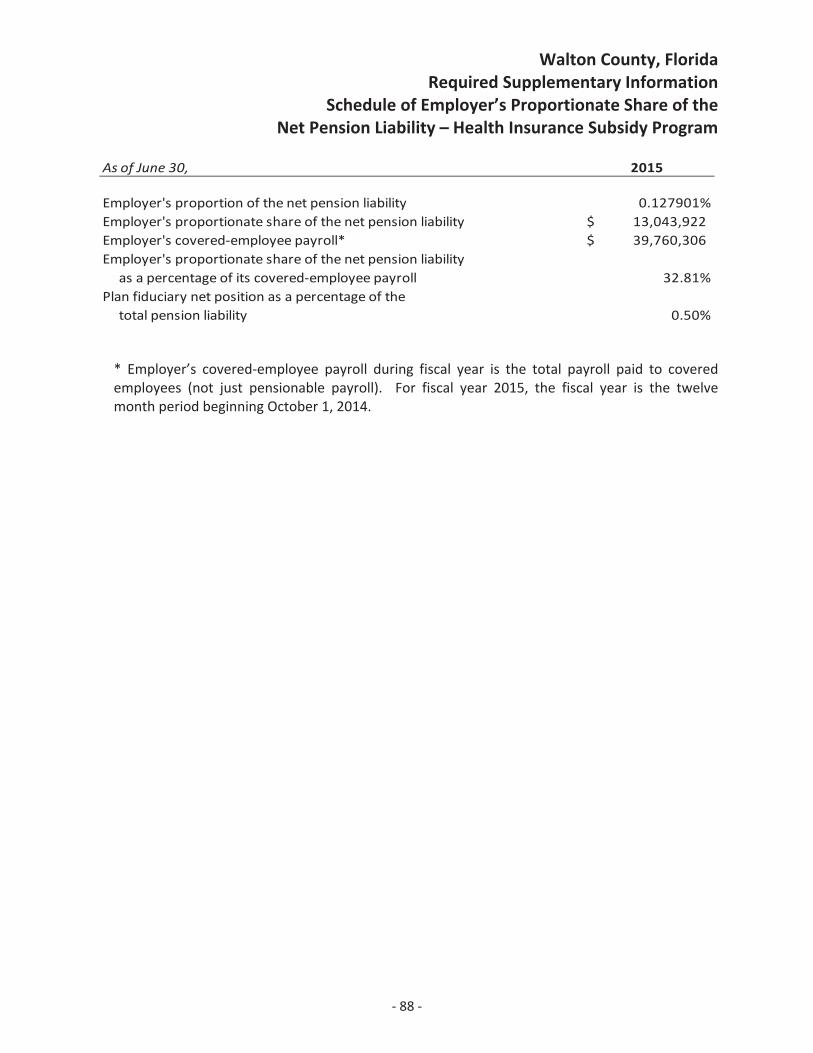

Schedule of Employer’s Proportionate Share of the Net Pension Liability –Health Insurance Subsidy Program 88

Schedule of Employer Contributions – Health Insurance Subsidy Program 89

COMBINING AND INDIVIDUAL FUND STATEMENTS AND SCHEDULES

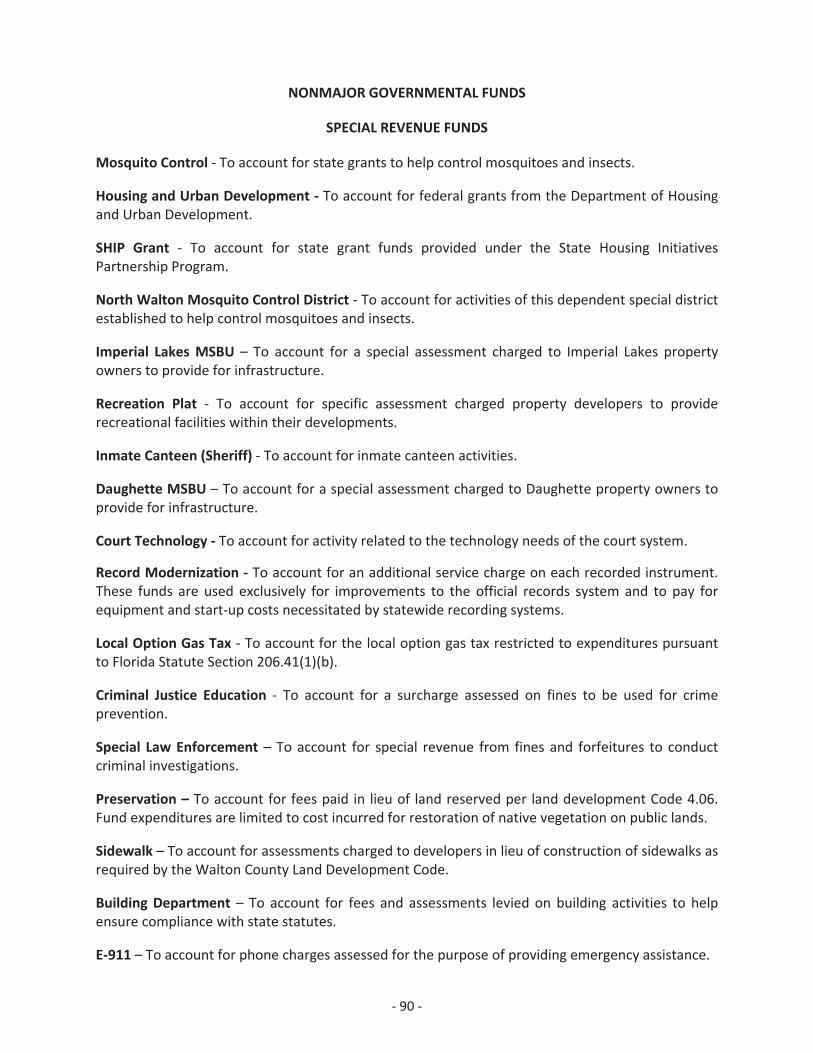

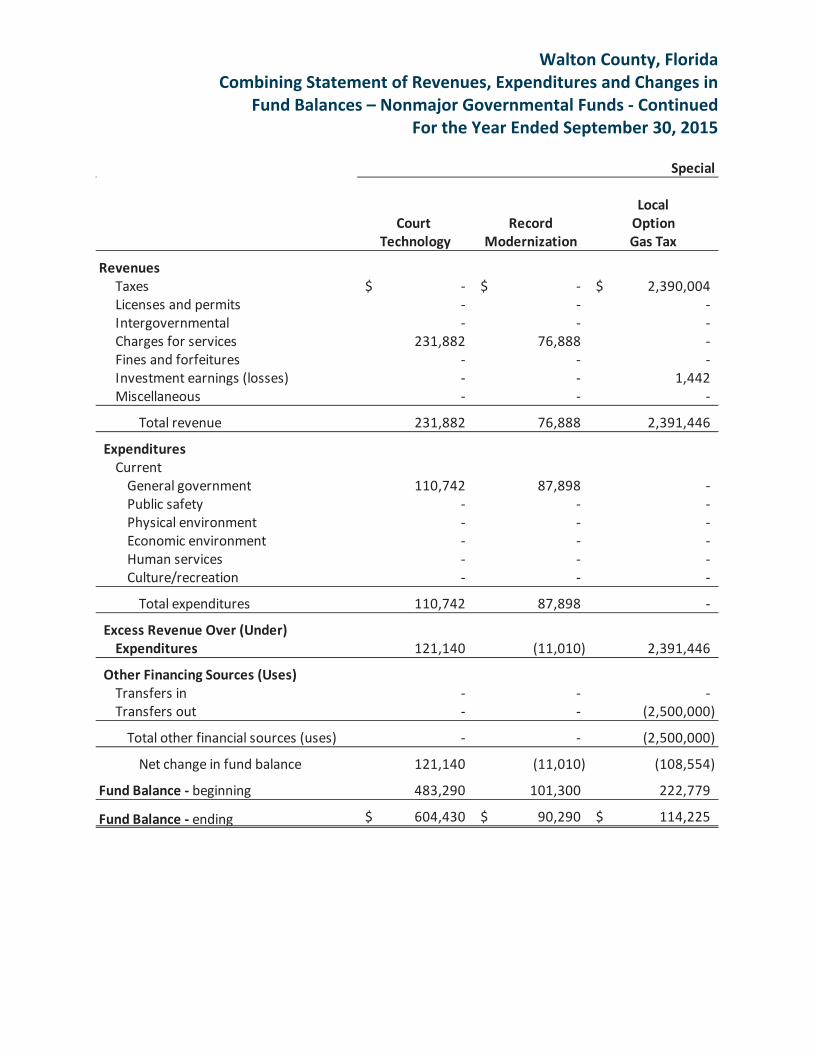

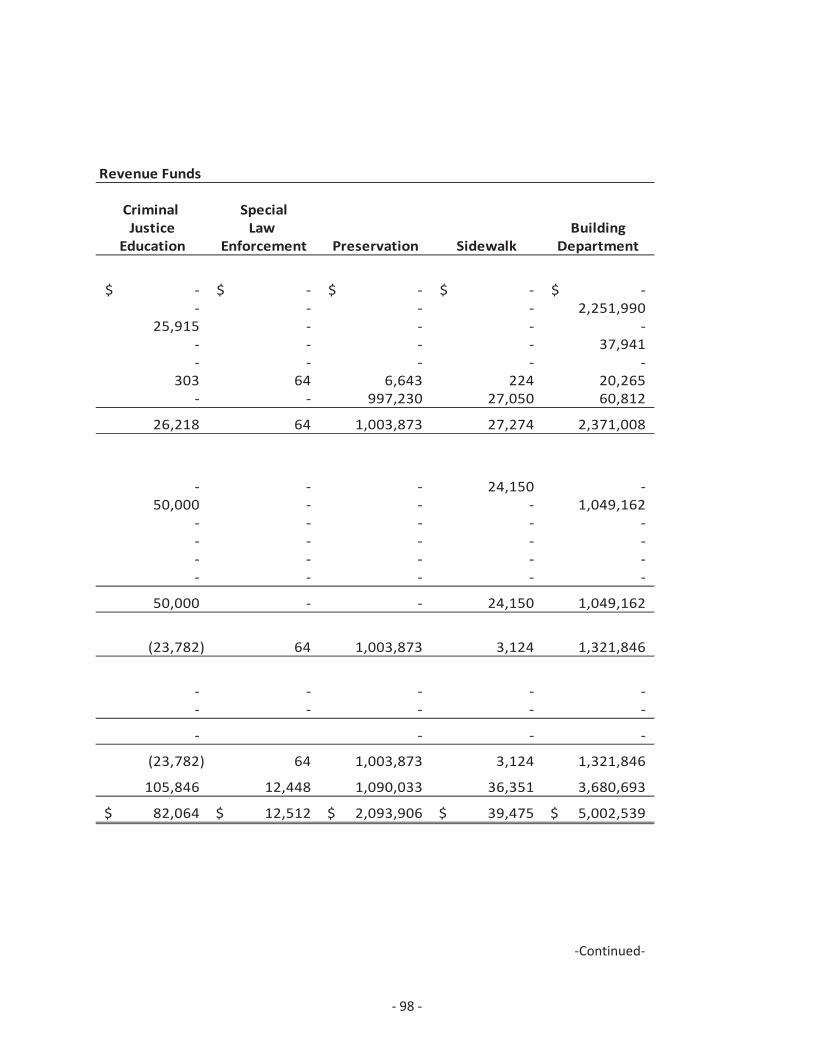

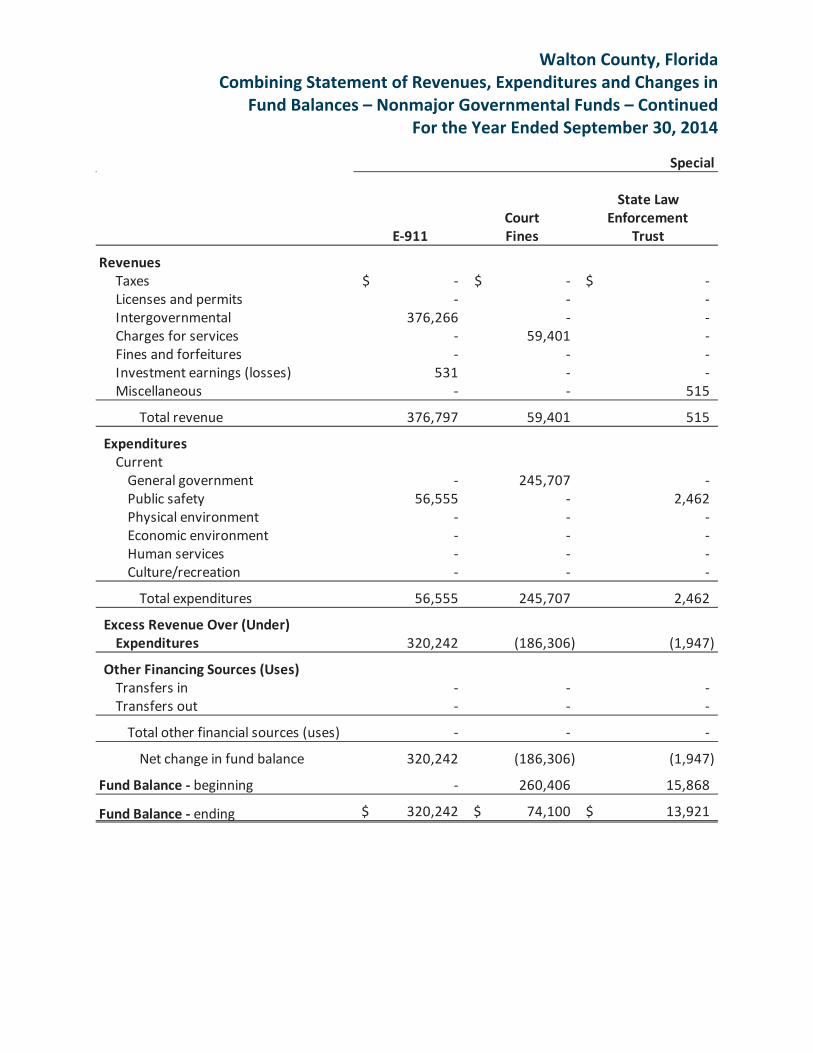

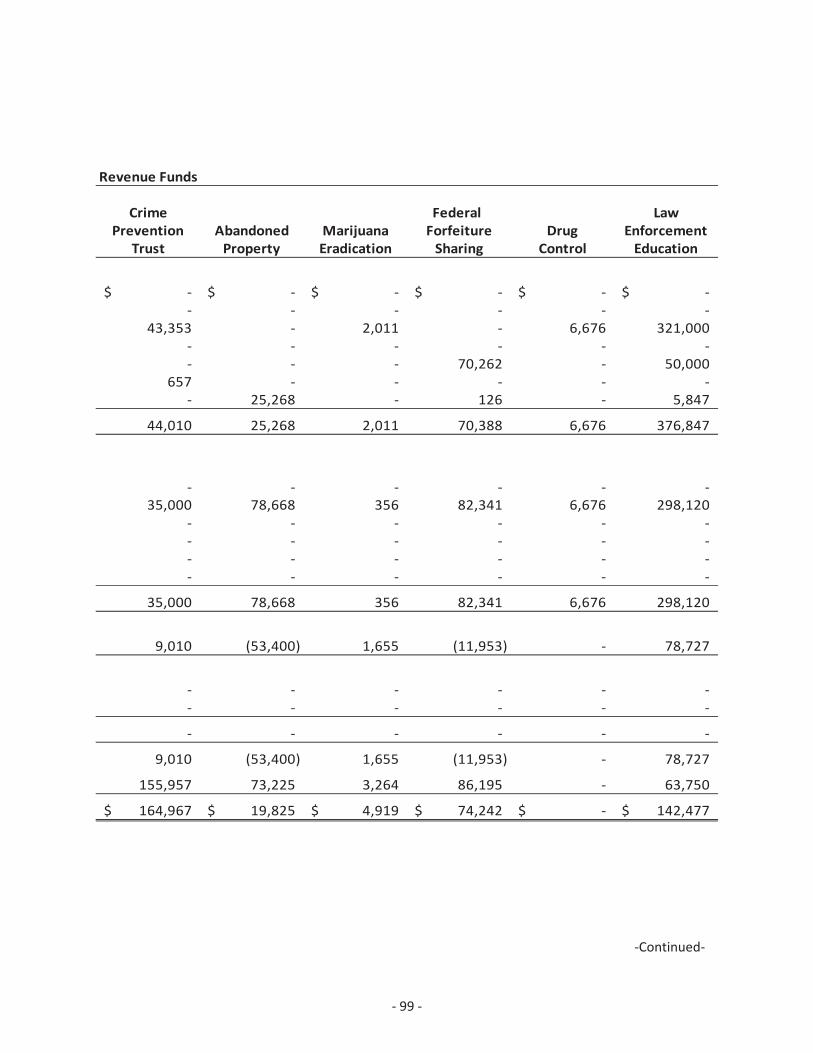

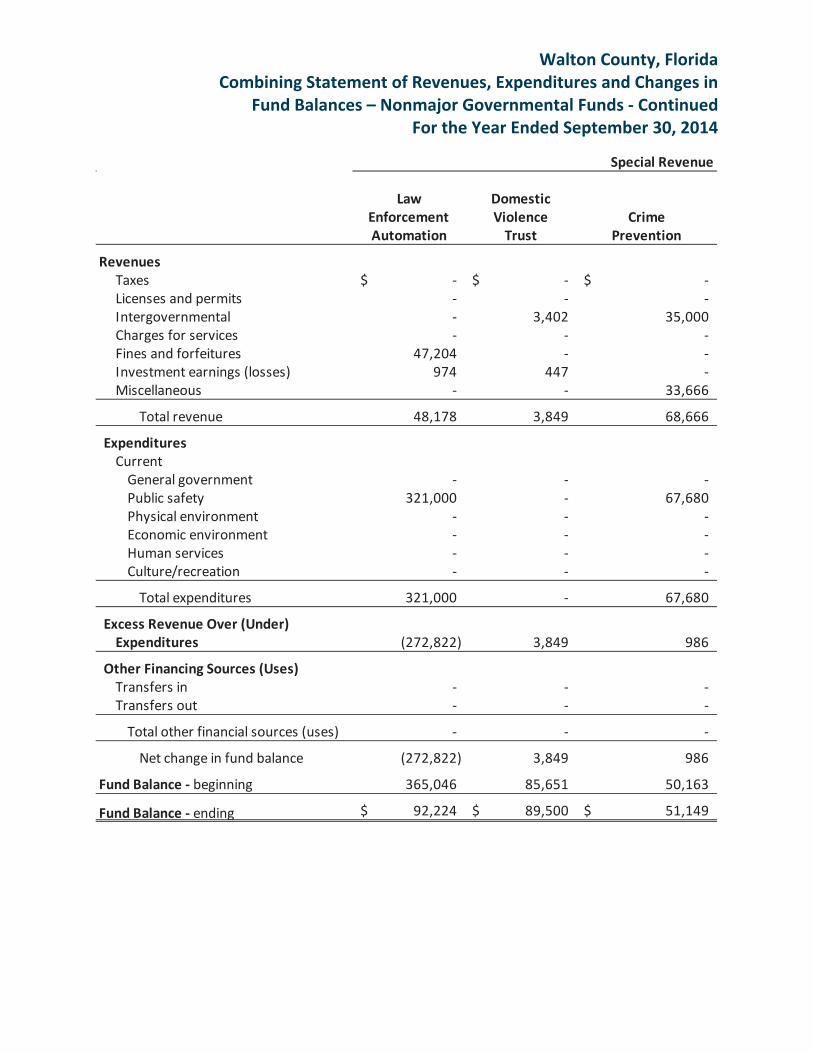

Description of Nonmajor Governmental Funds 90 91

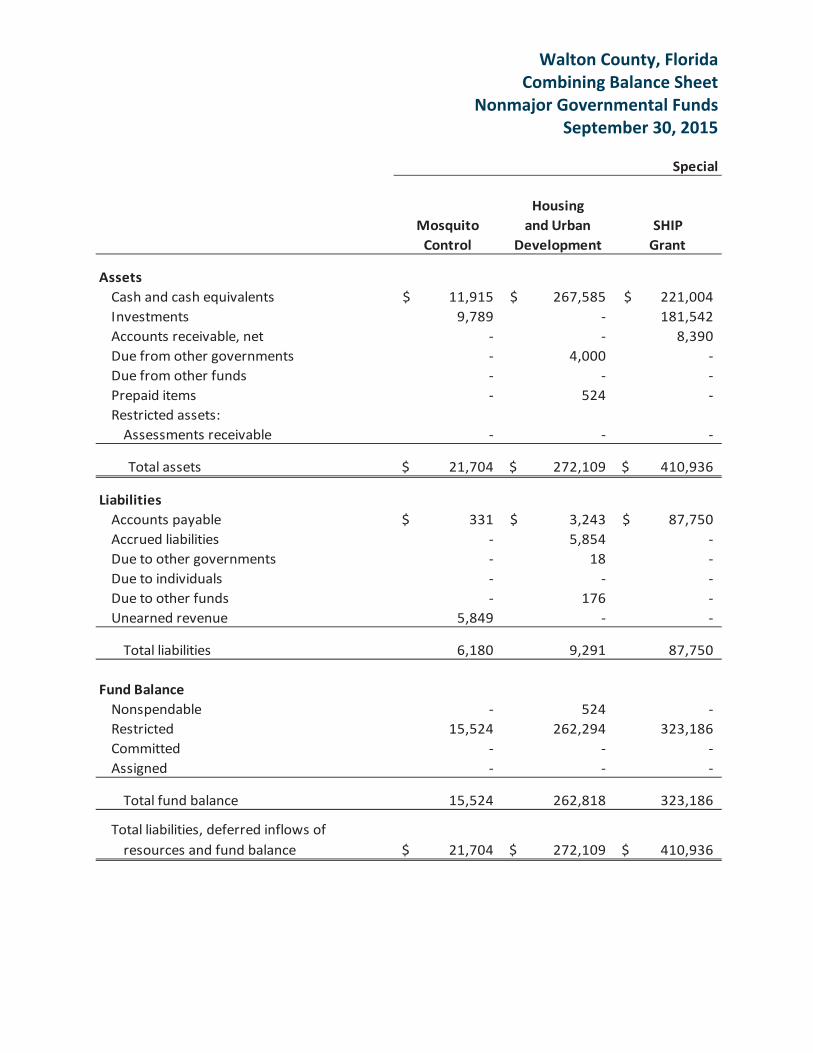

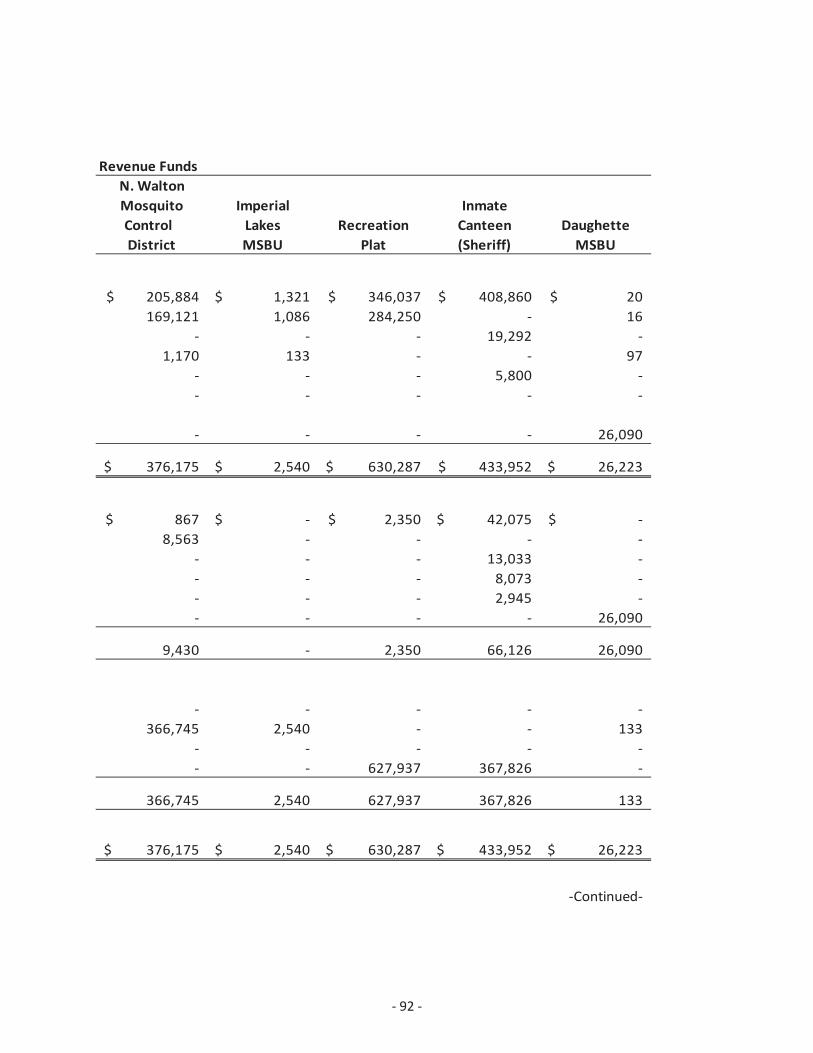

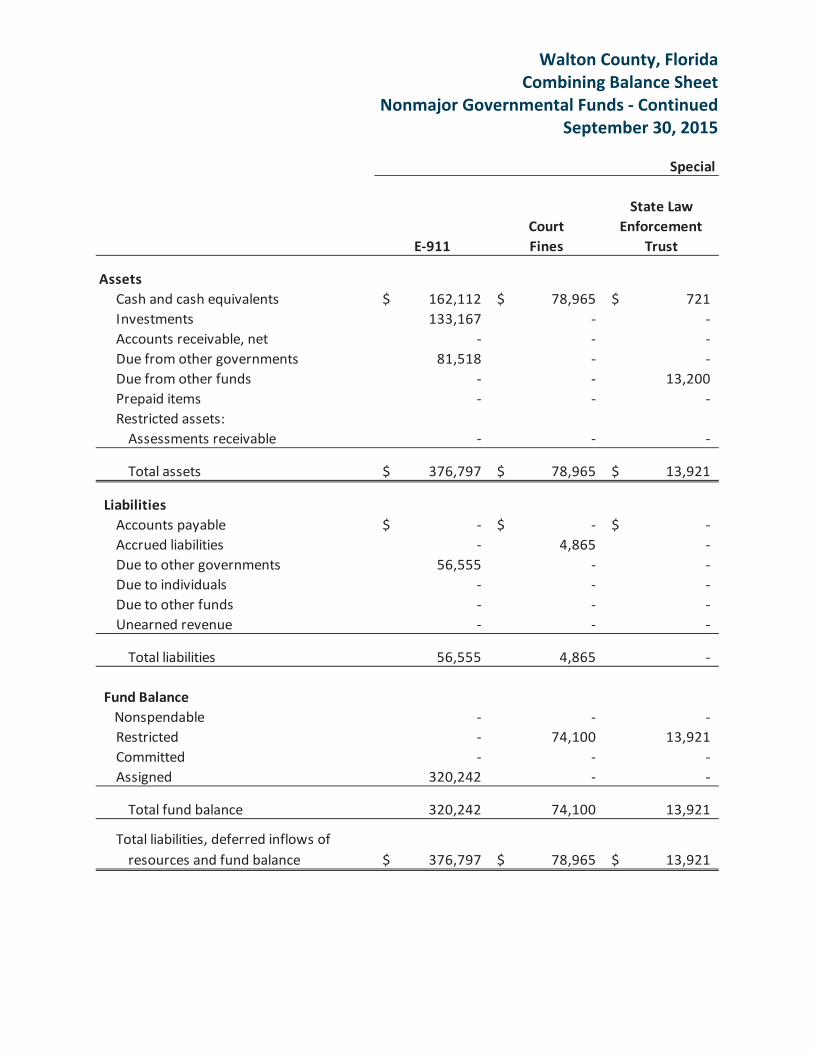

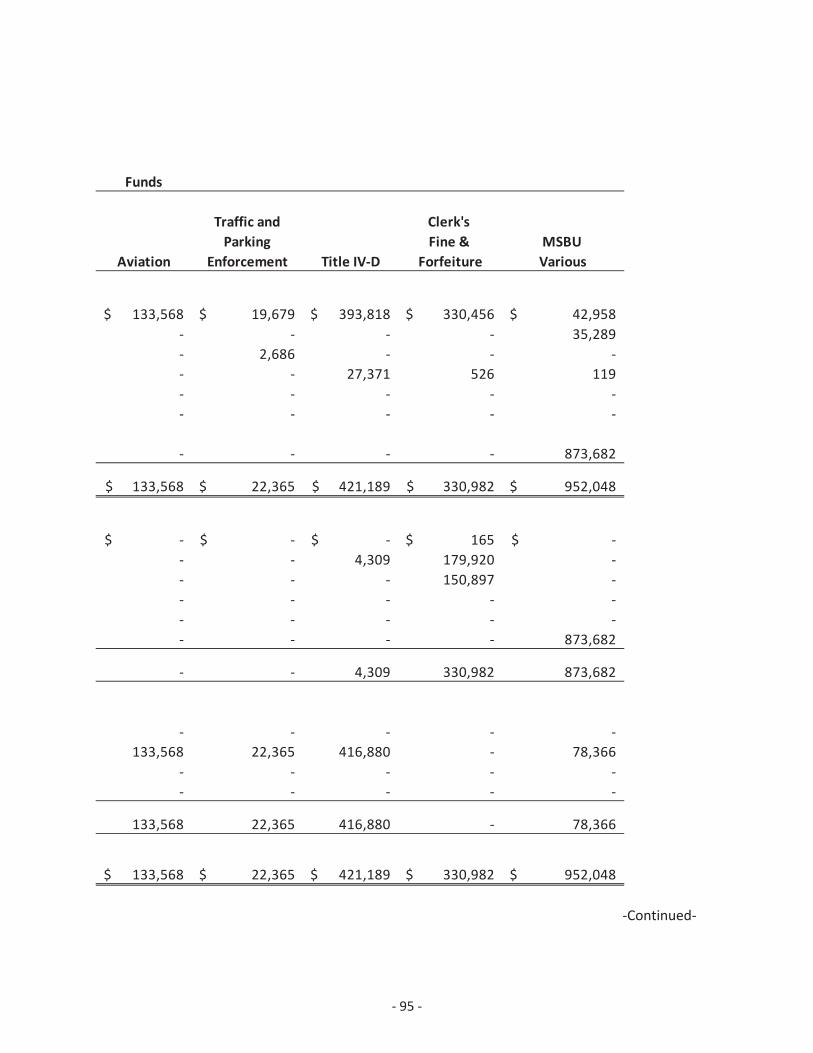

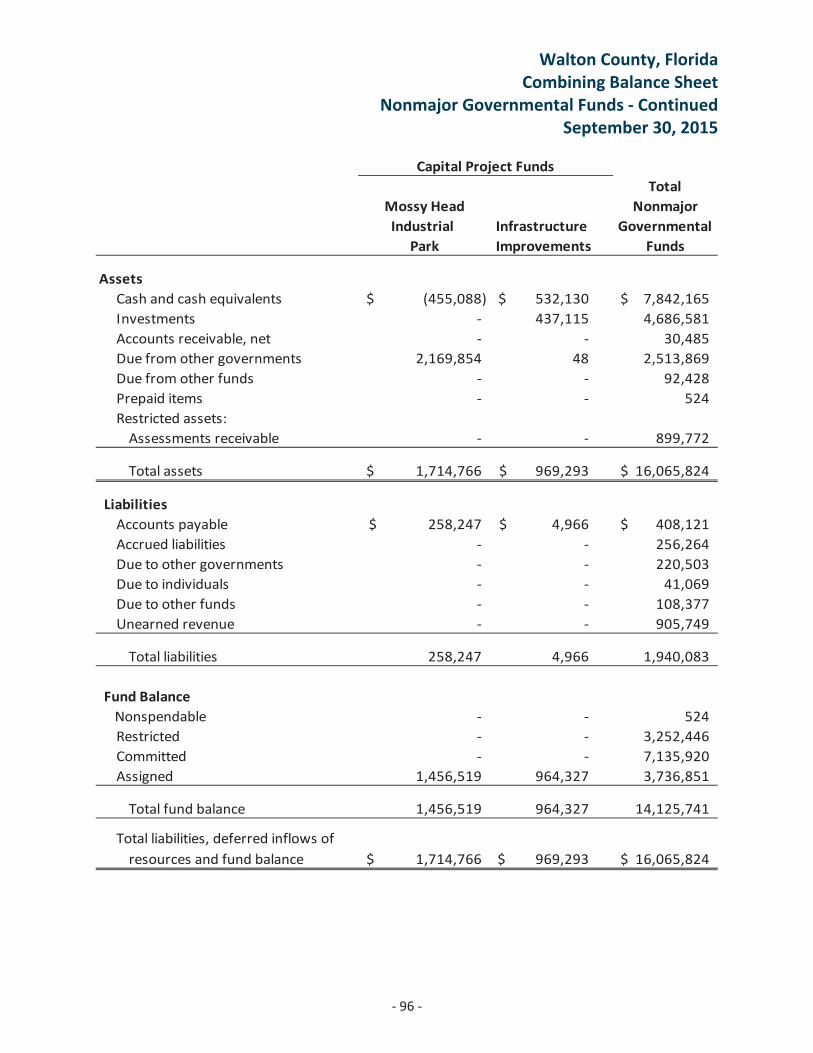

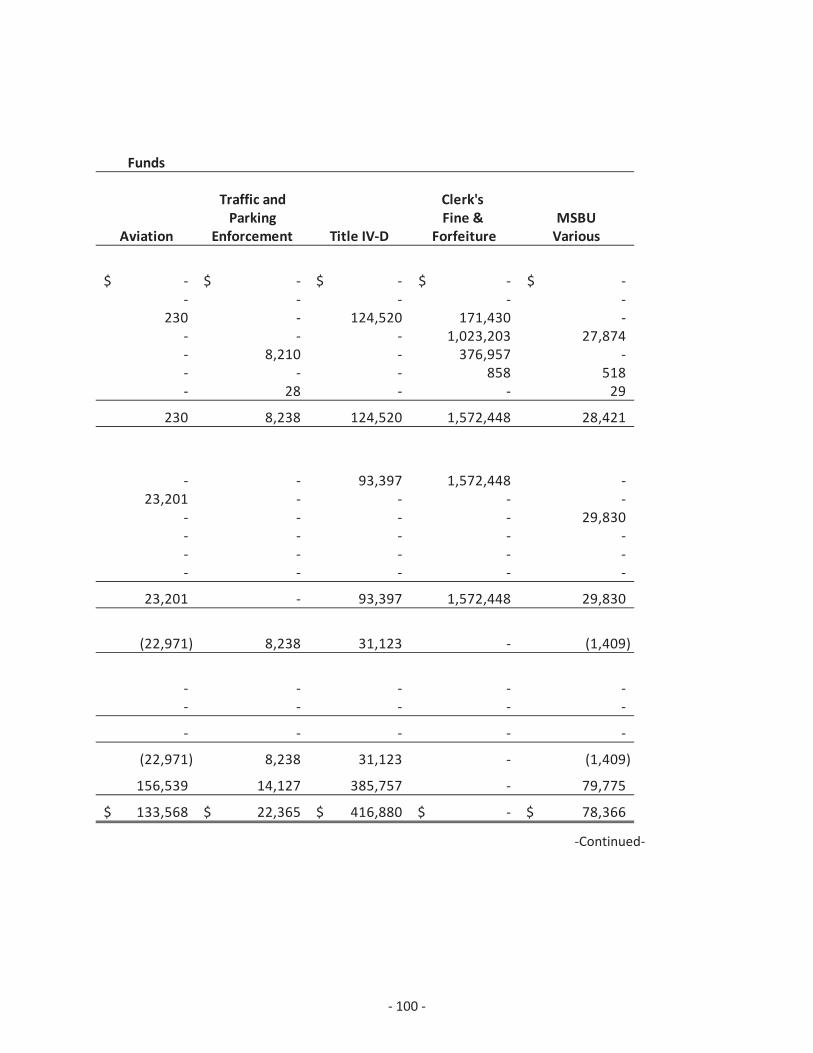

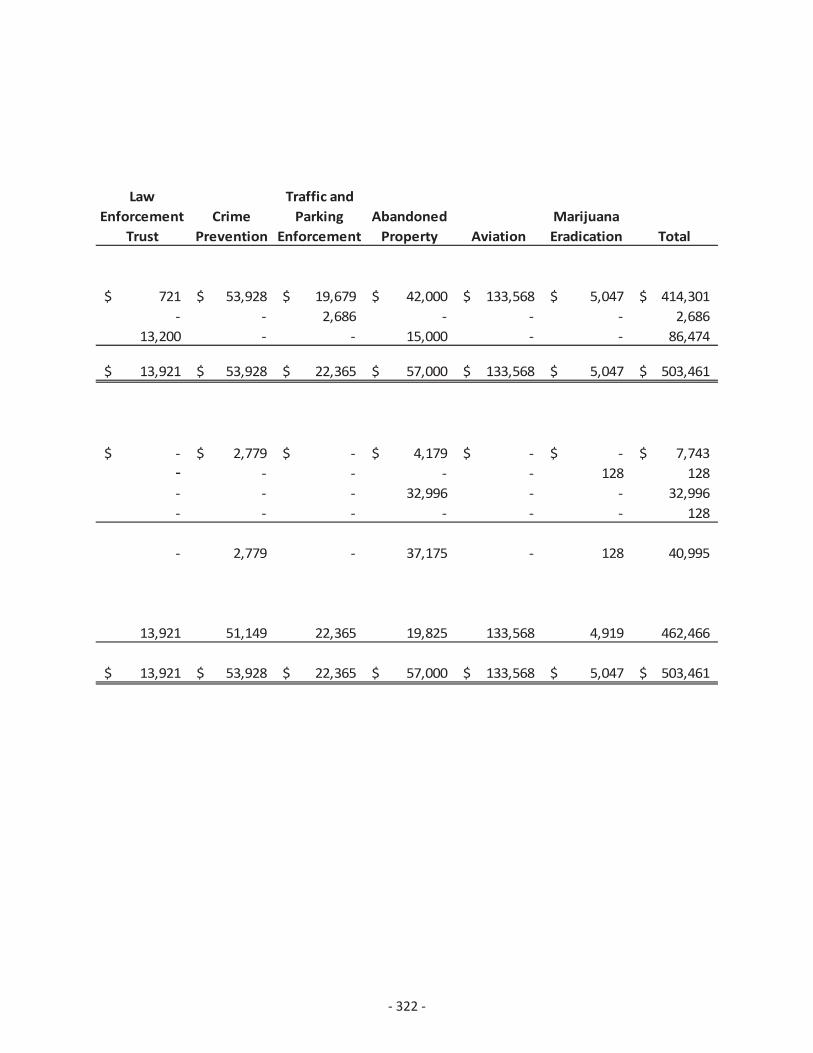

Combining Balance Sheet – Nonmajor Governmental Funds 92 96

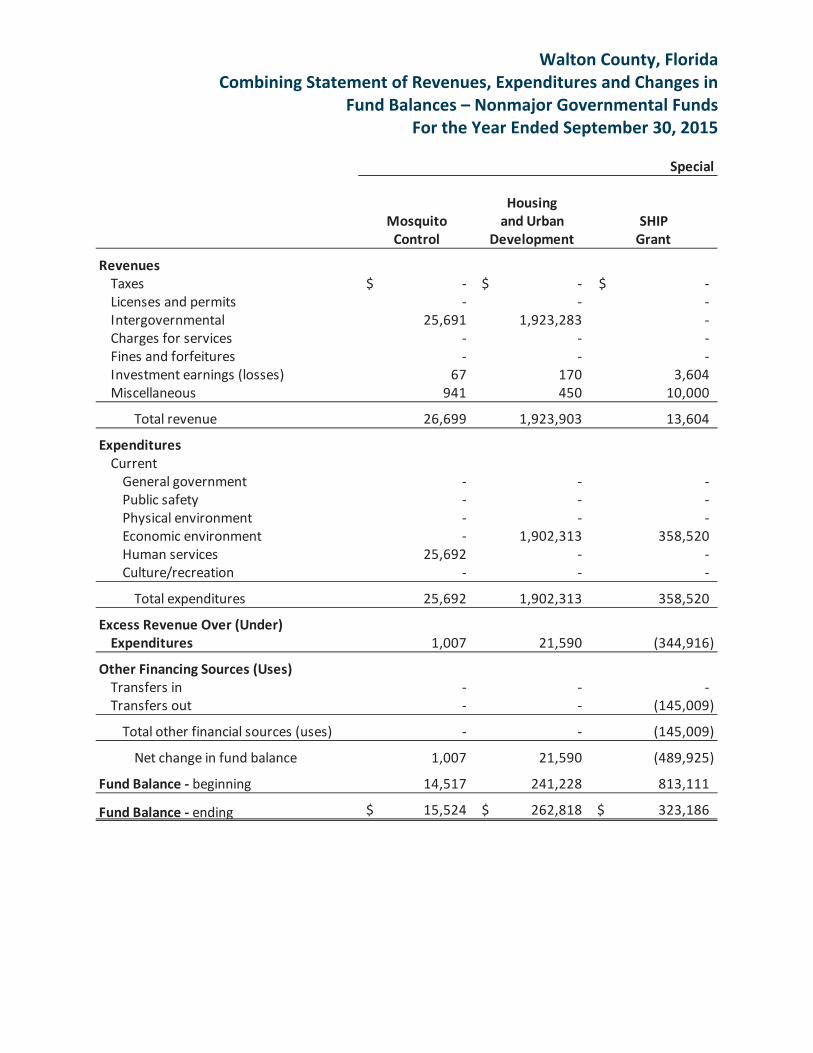

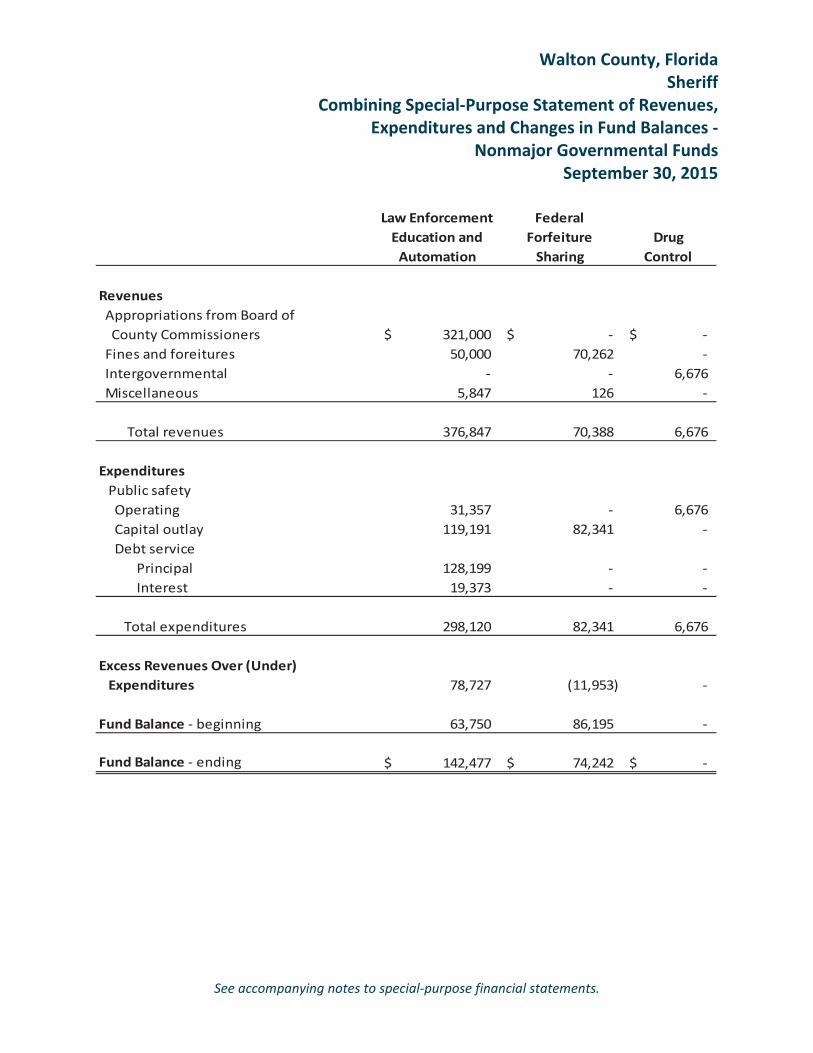

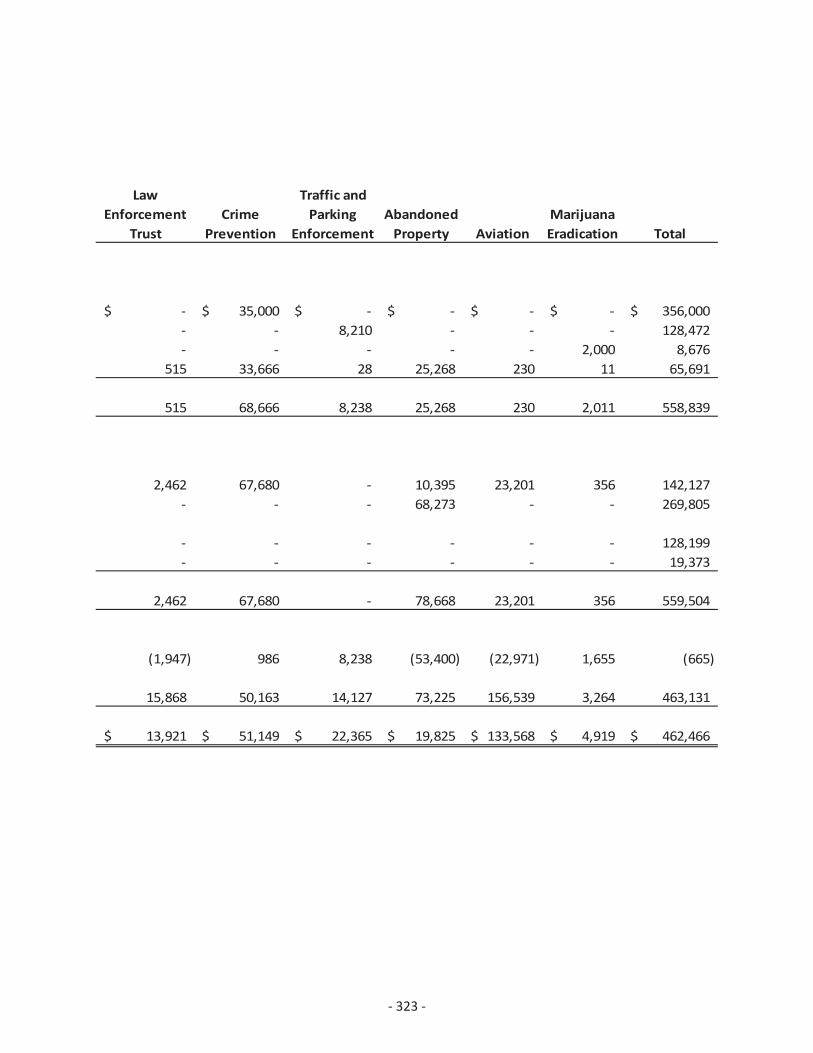

Combining Statement of Revenues, Expenditures and Changesin Fund Balance – Nonmajor Governmental Funds 97 101

Schedules of Revenues, Expenditures and Changes in FundBalance Budget and Actual – Debt Service Fund, Capital ProjectsFund and Budgeted Nonmajor Governmental Funds

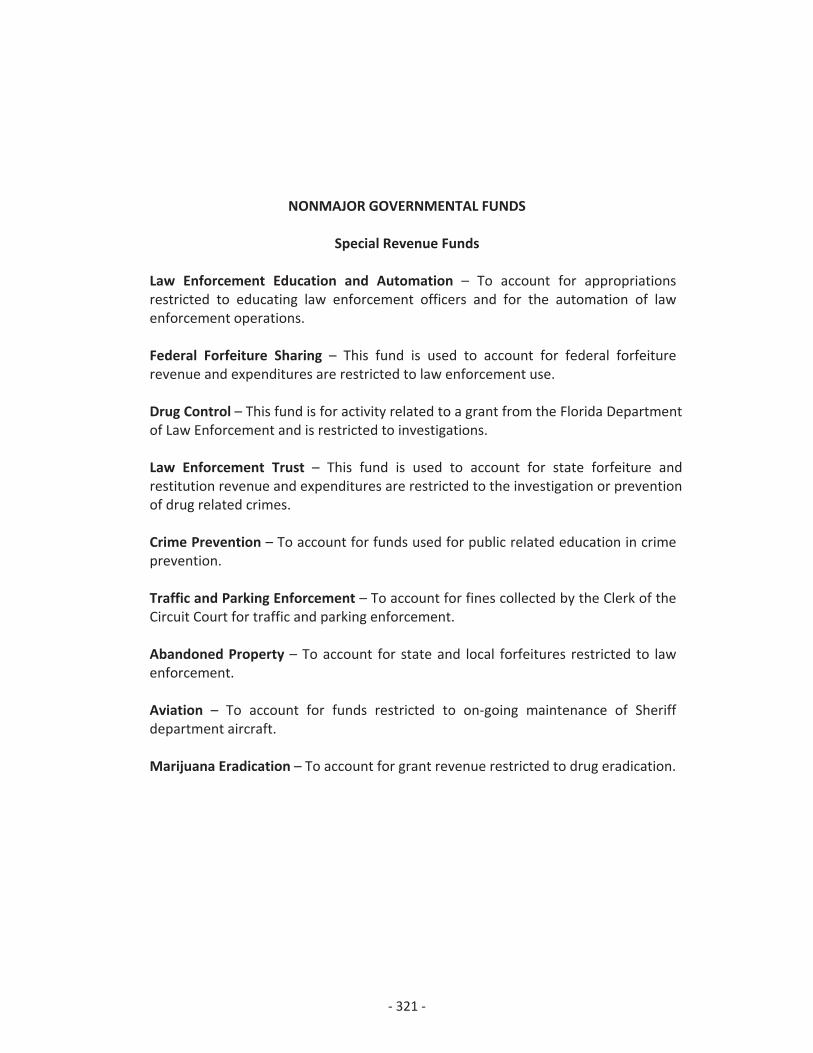

Nonmajor Governmental Funds:

Special Revenue Funds:

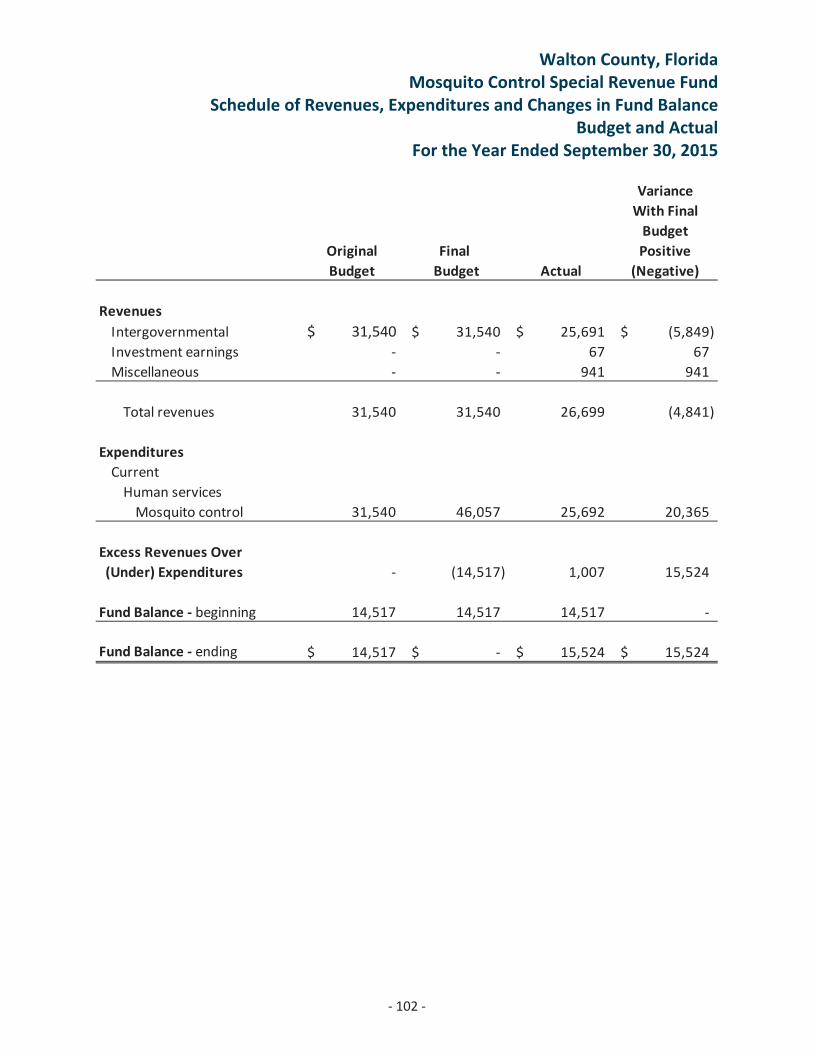

Mosquito Control 102

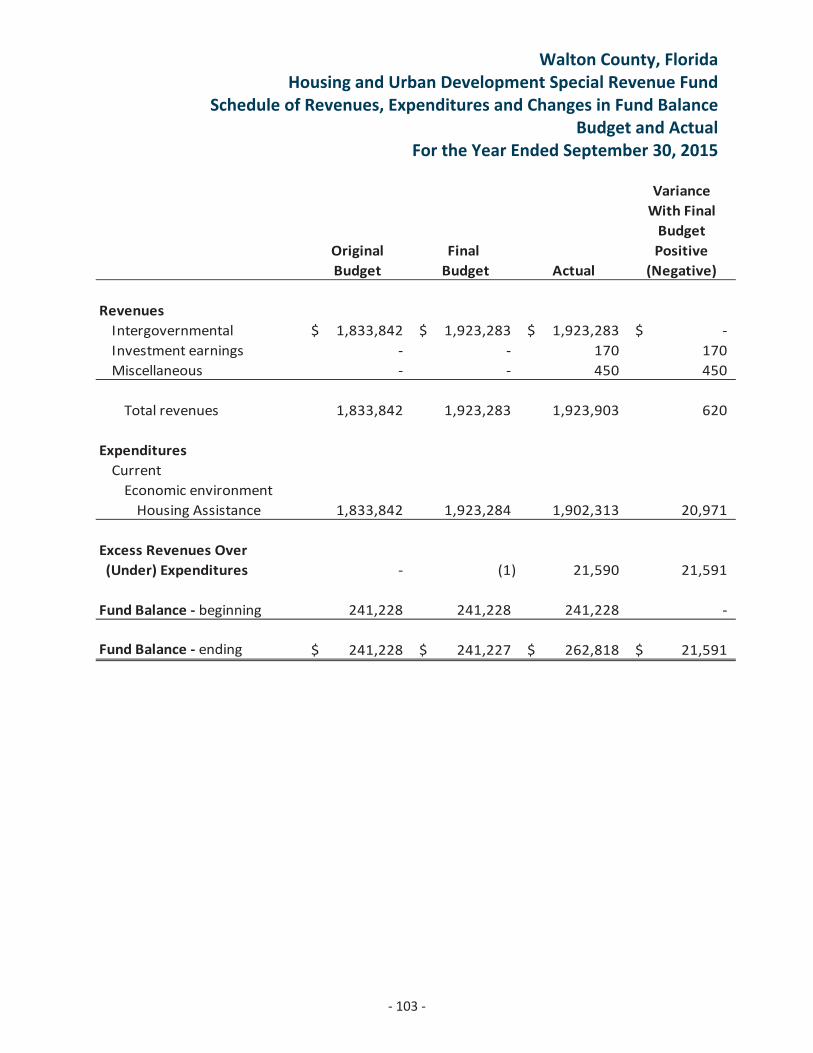

Housing and Urban Development 103

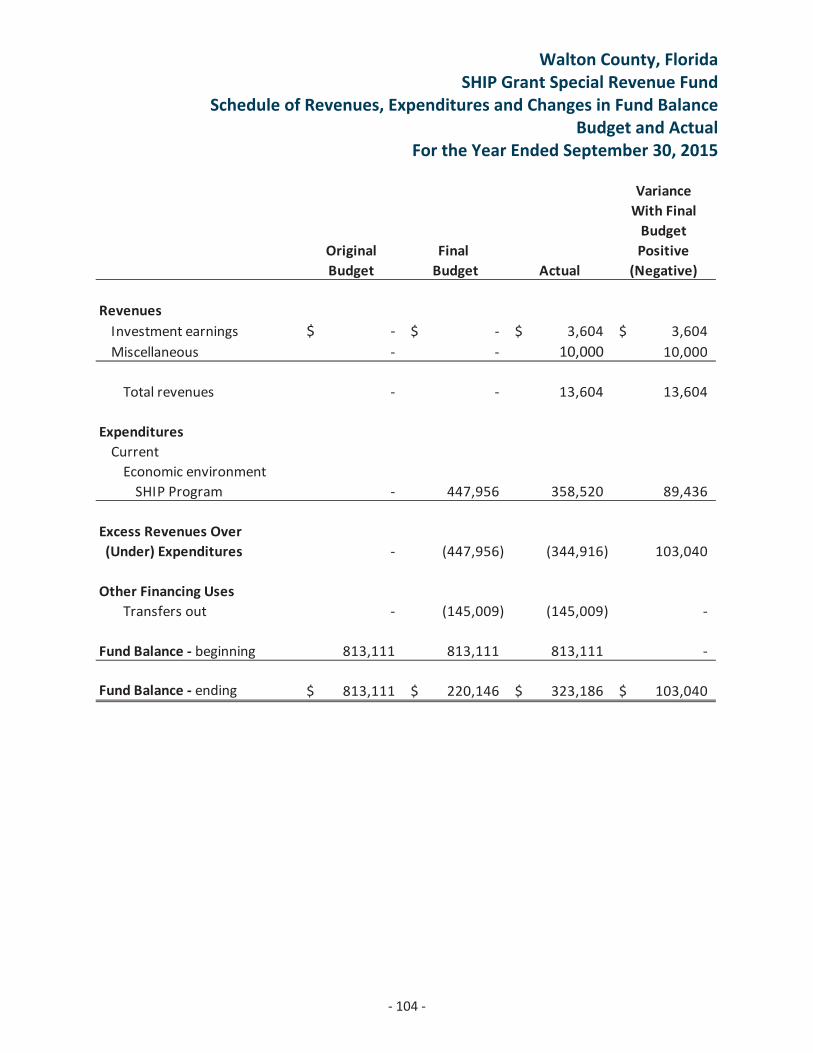

SHIP Grant 104

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

IIIIII

North Walton Mosquito Control 105

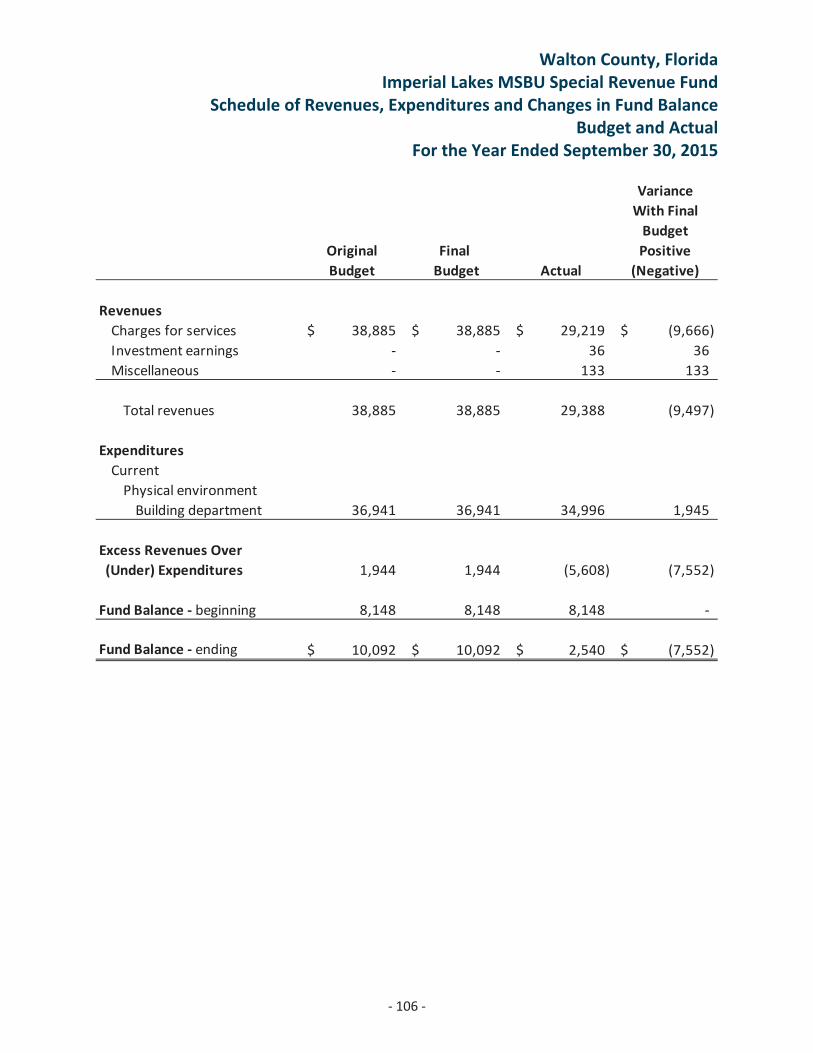

Imperial Lakes MSBU 106

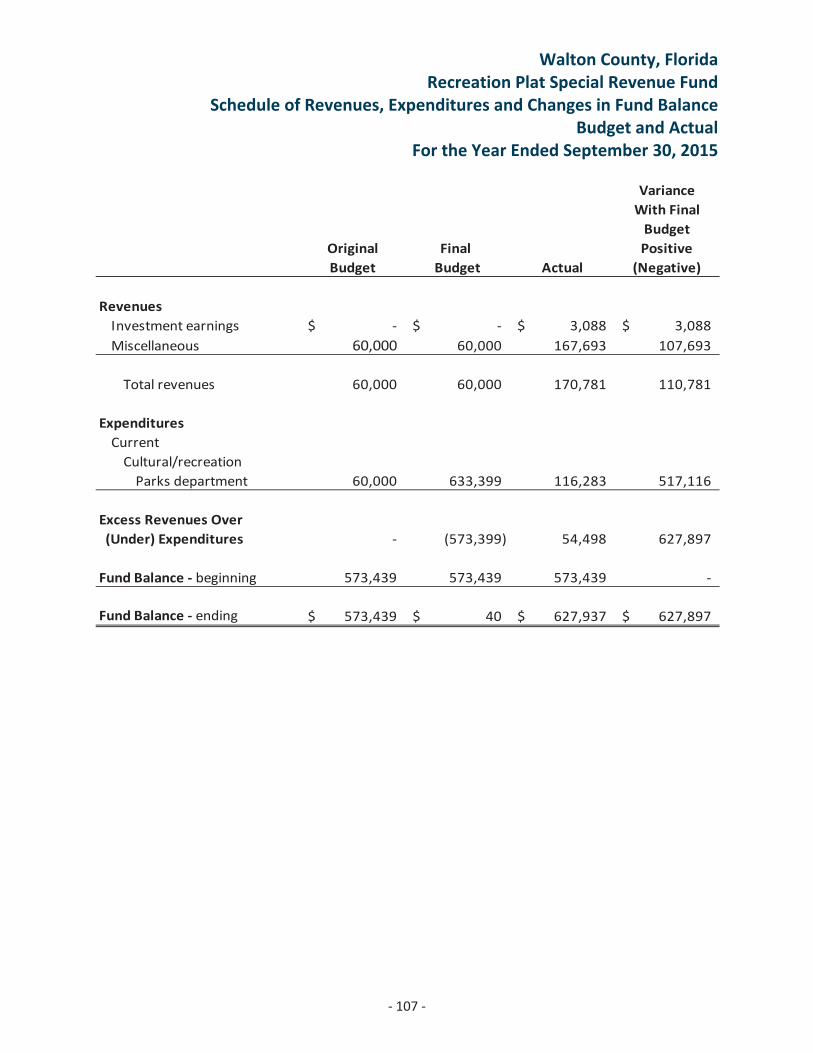

Recreation Plat 107

Daughette MSBU 108

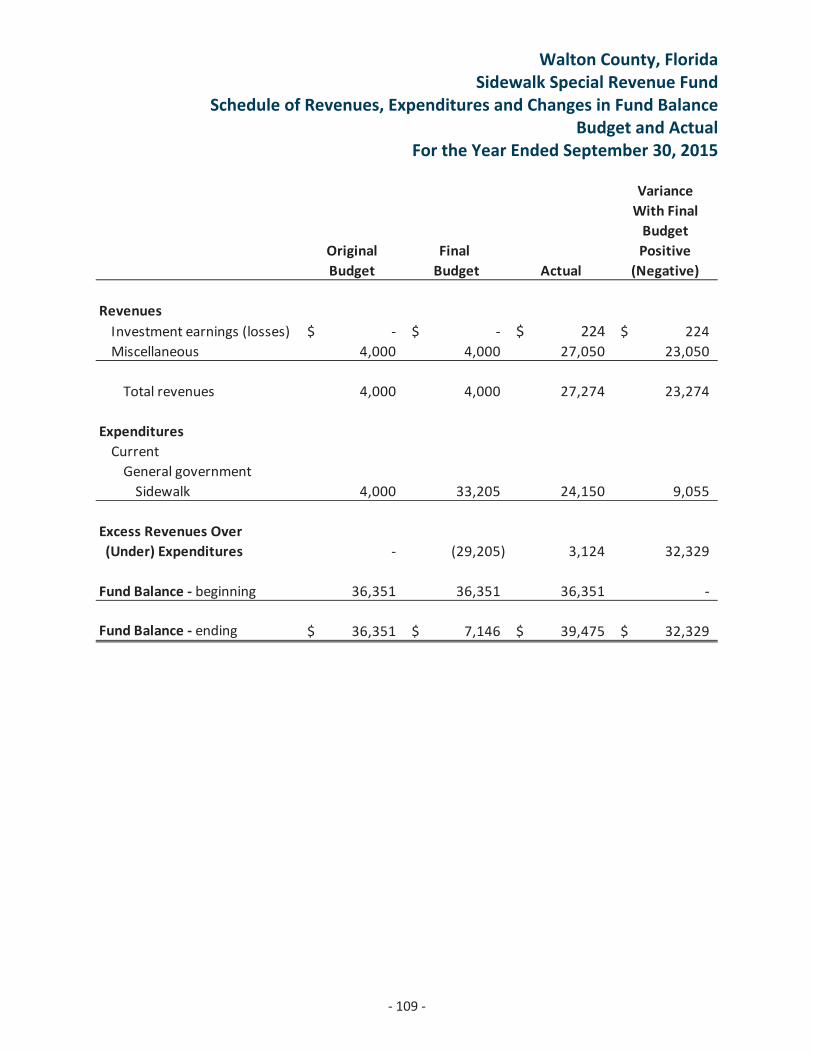

Sidewalk 109

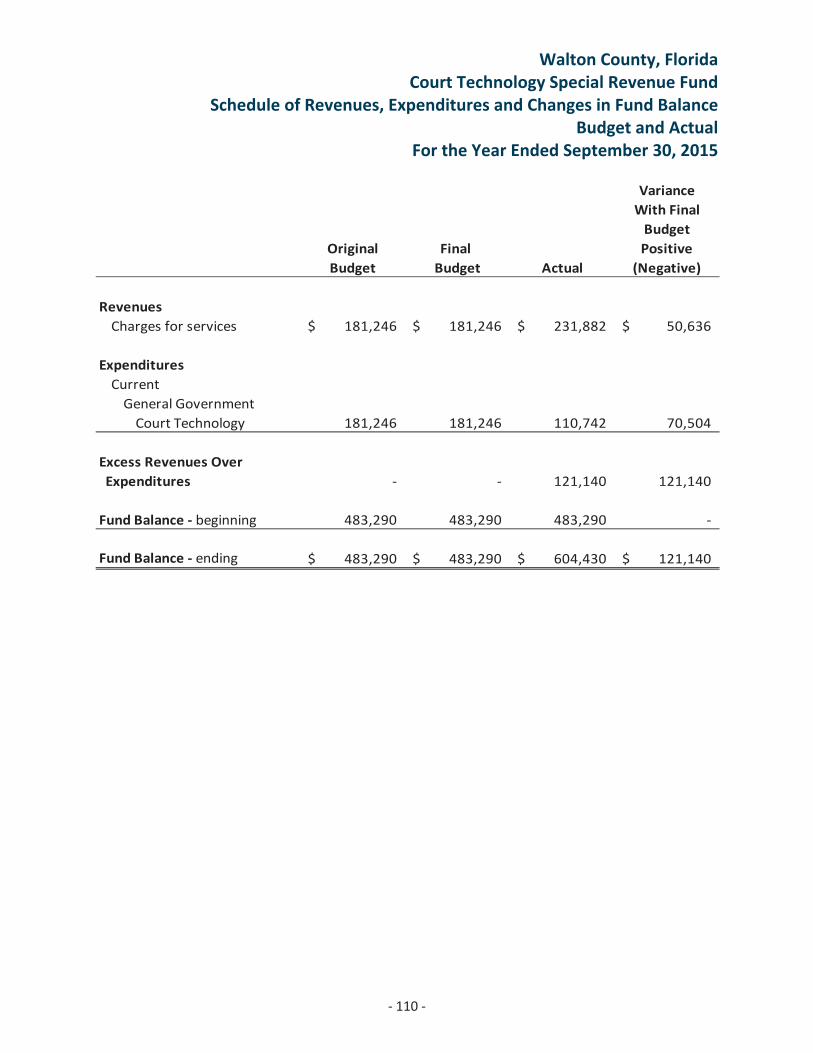

Court Technology 110

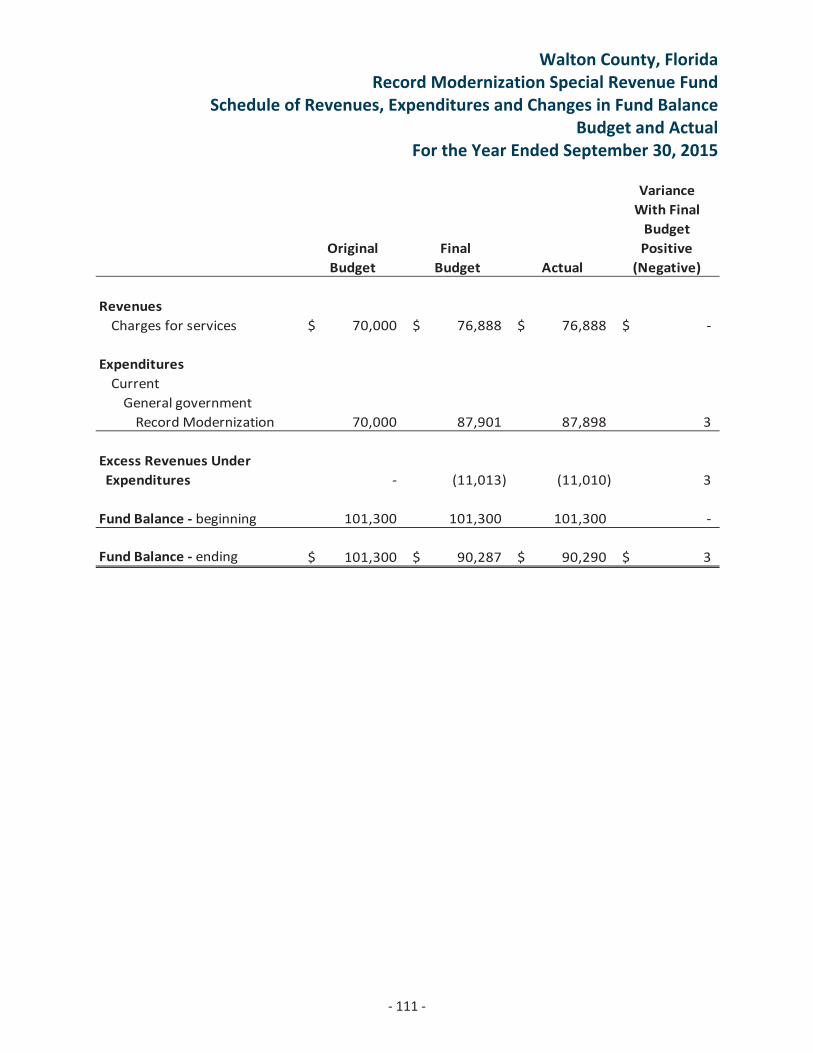

Record Modernization 111

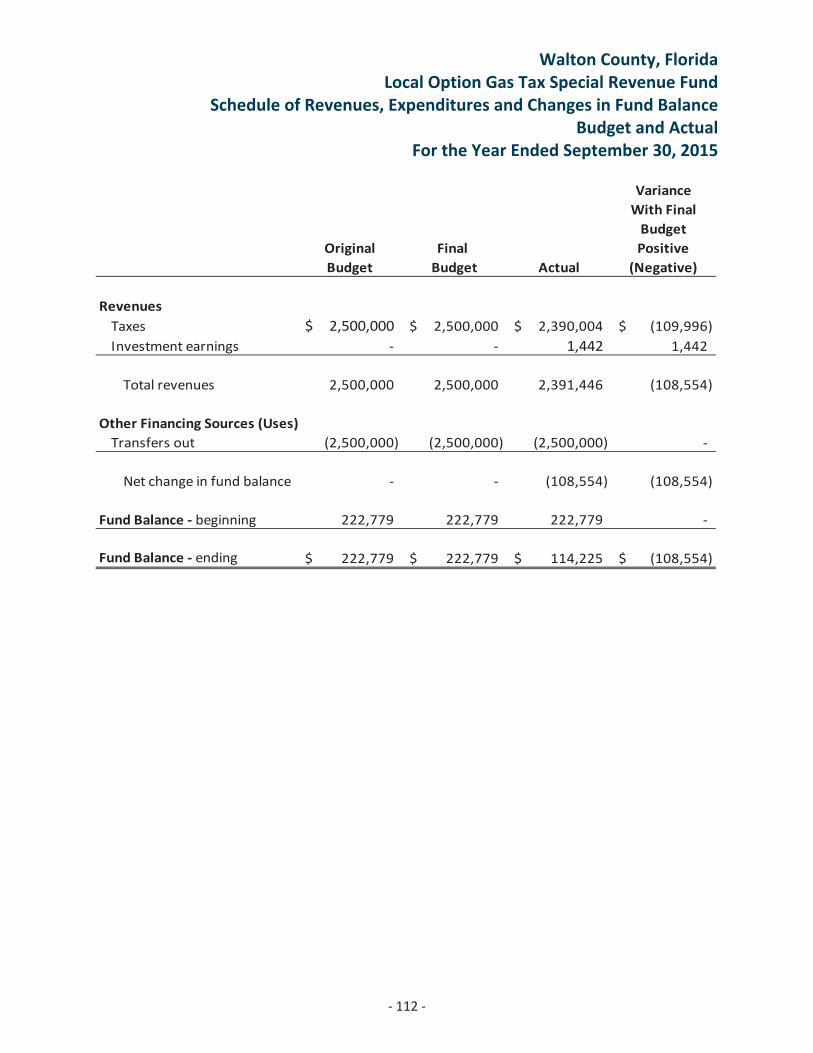

Local Option Gas Tax 112

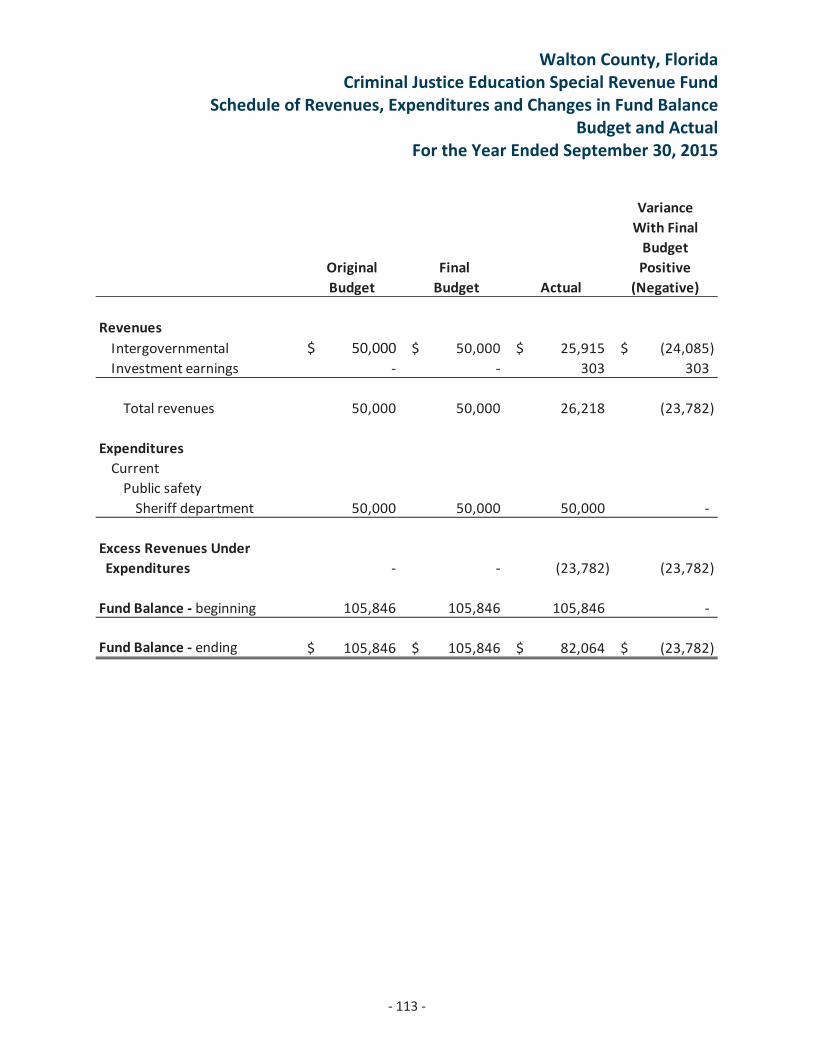

Criminal Justice Education 113

Building Department 114

E 911 115

Court Fines 116

Crime Prevention Trust 117

Title IV D 118

Clerk’s Fine & Forfeiture 119

MSBU Various 120

Mossy Head Industrial Park Capital Projects Fund 121

Infrastructure Improvements Capital Projects Fund 122

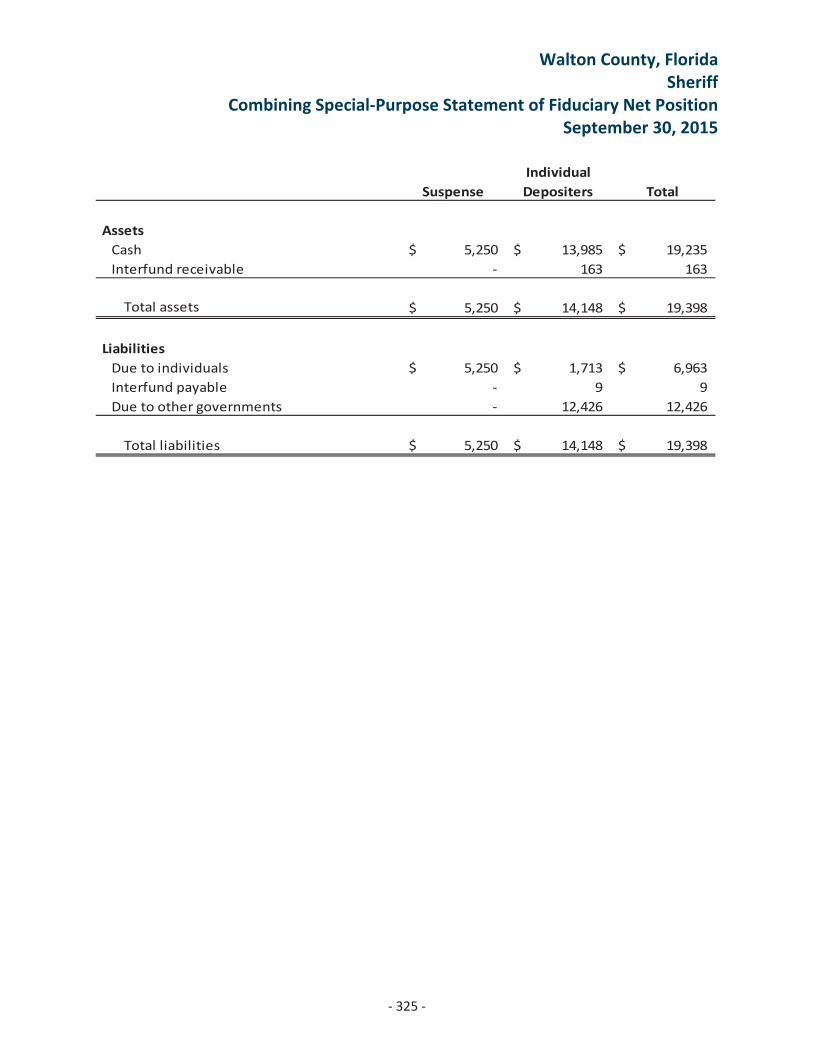

Fiduciary Funds:

Description of Fiduciary Funds 123

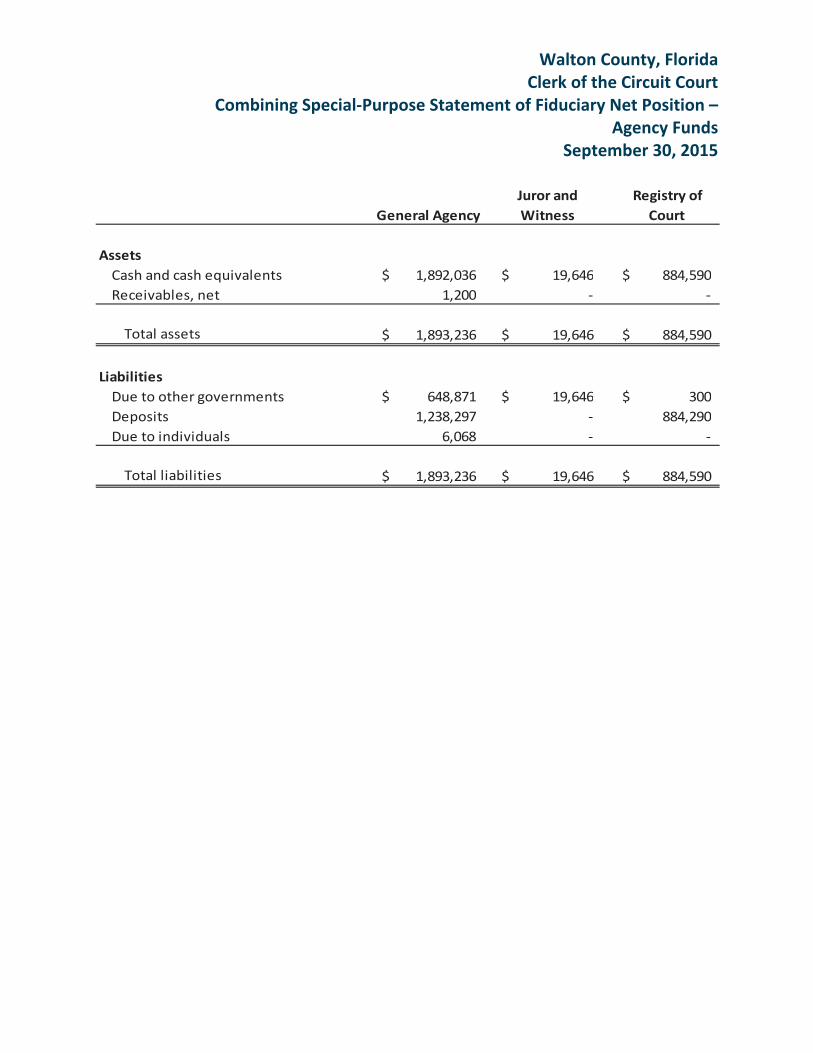

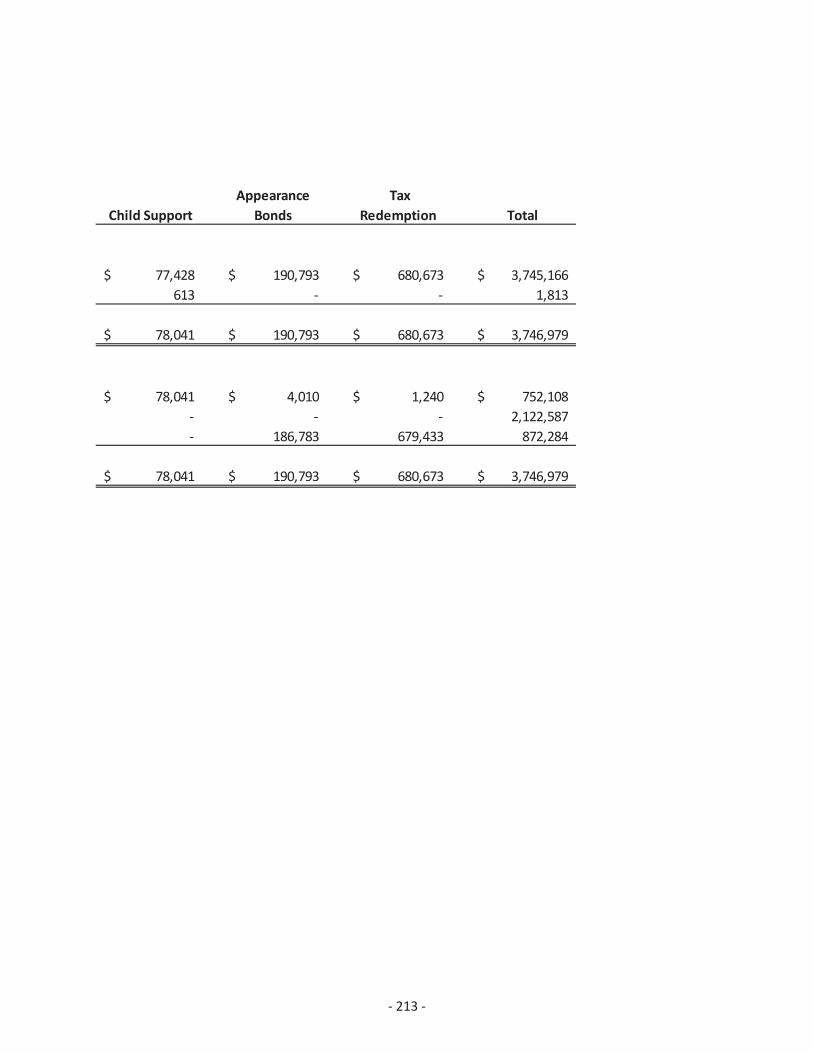

Combining Statement of Fiduciary Net Position Agency Funds 124 125

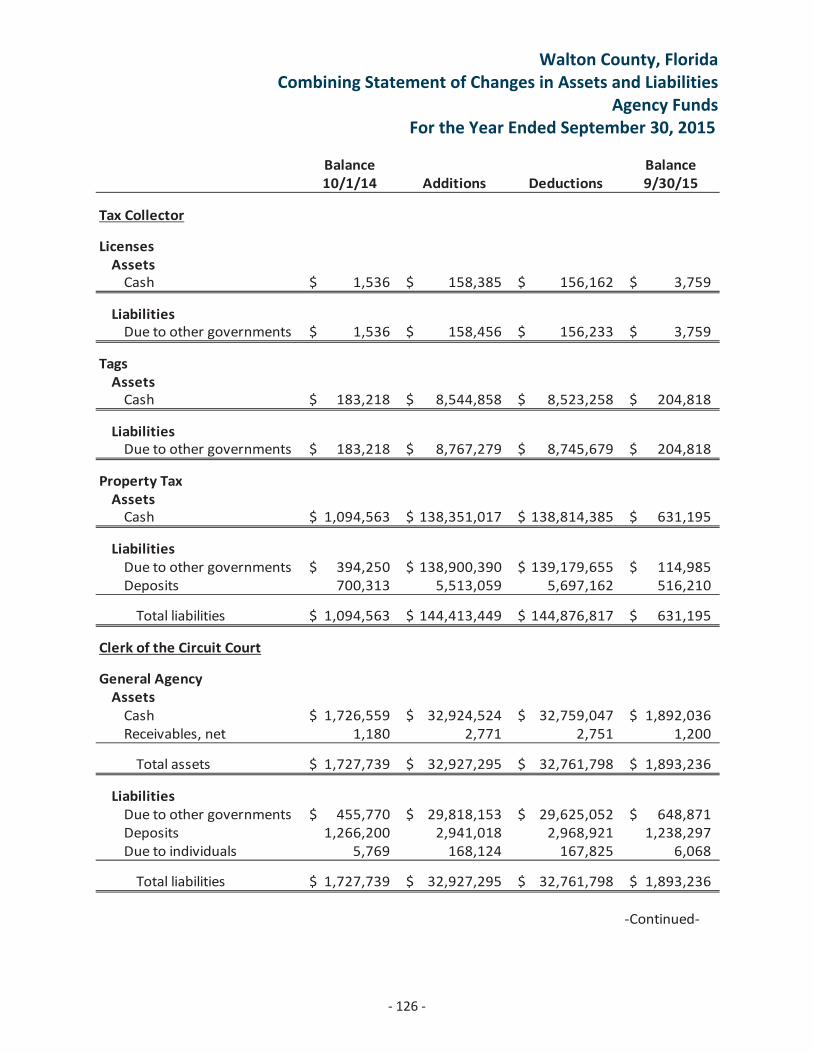

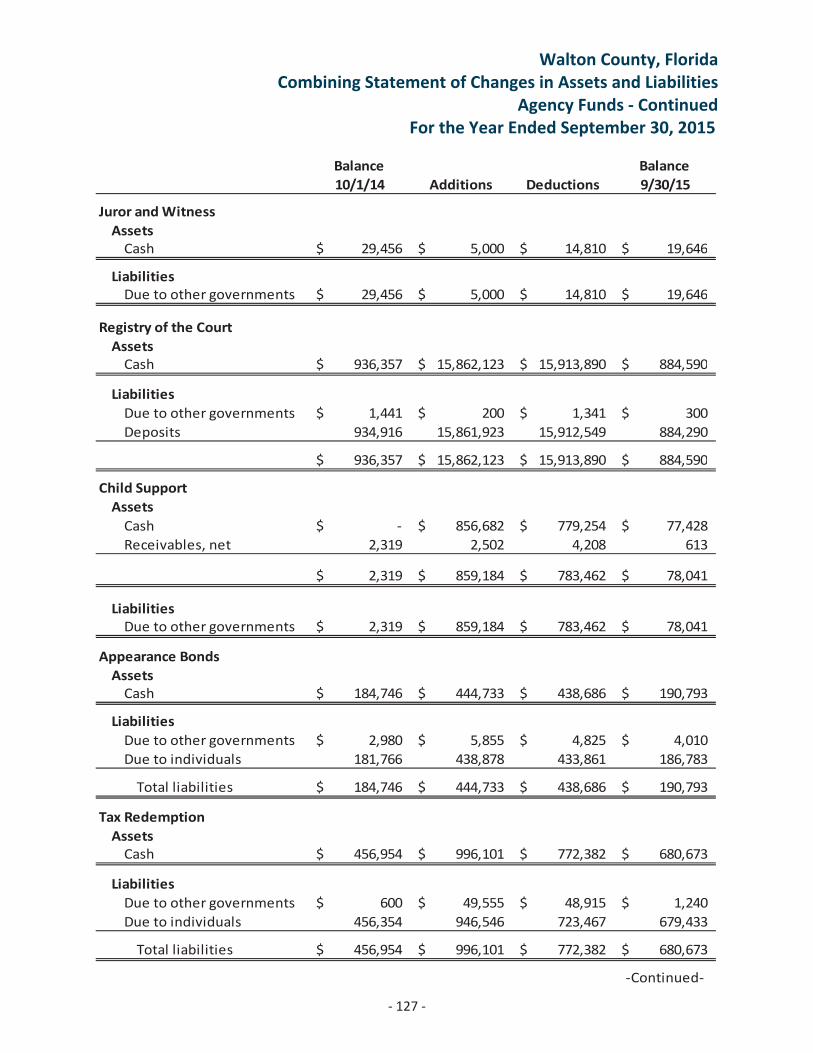

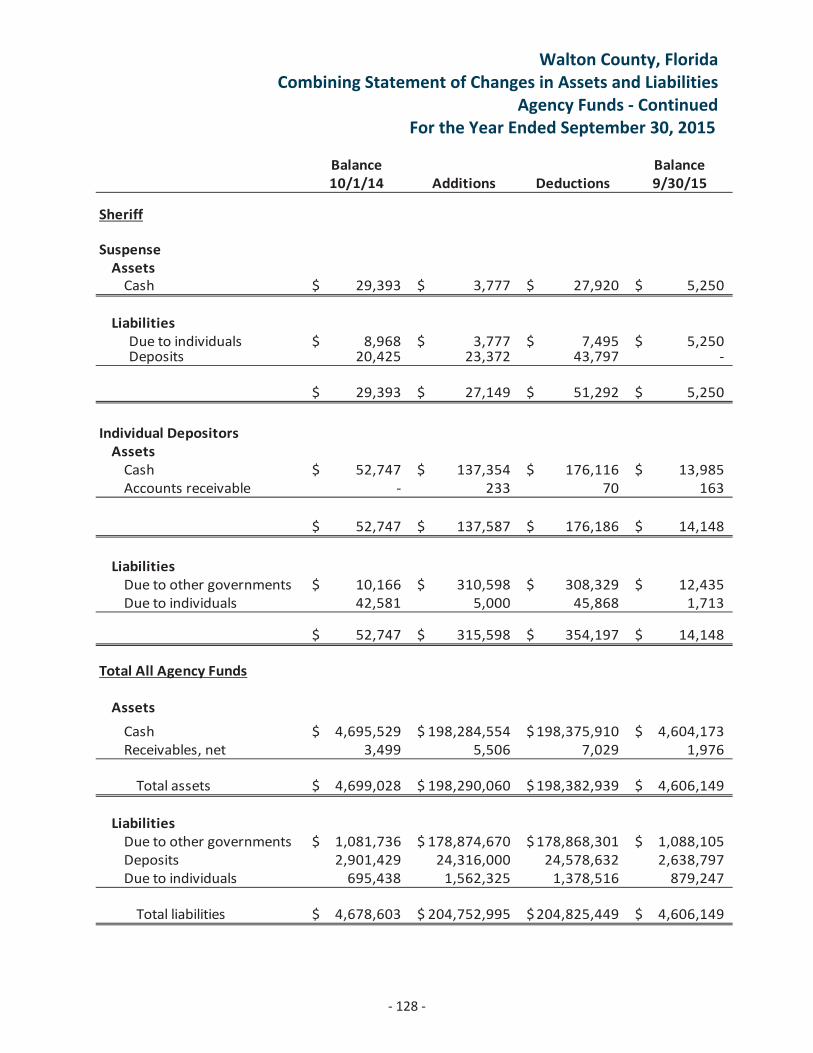

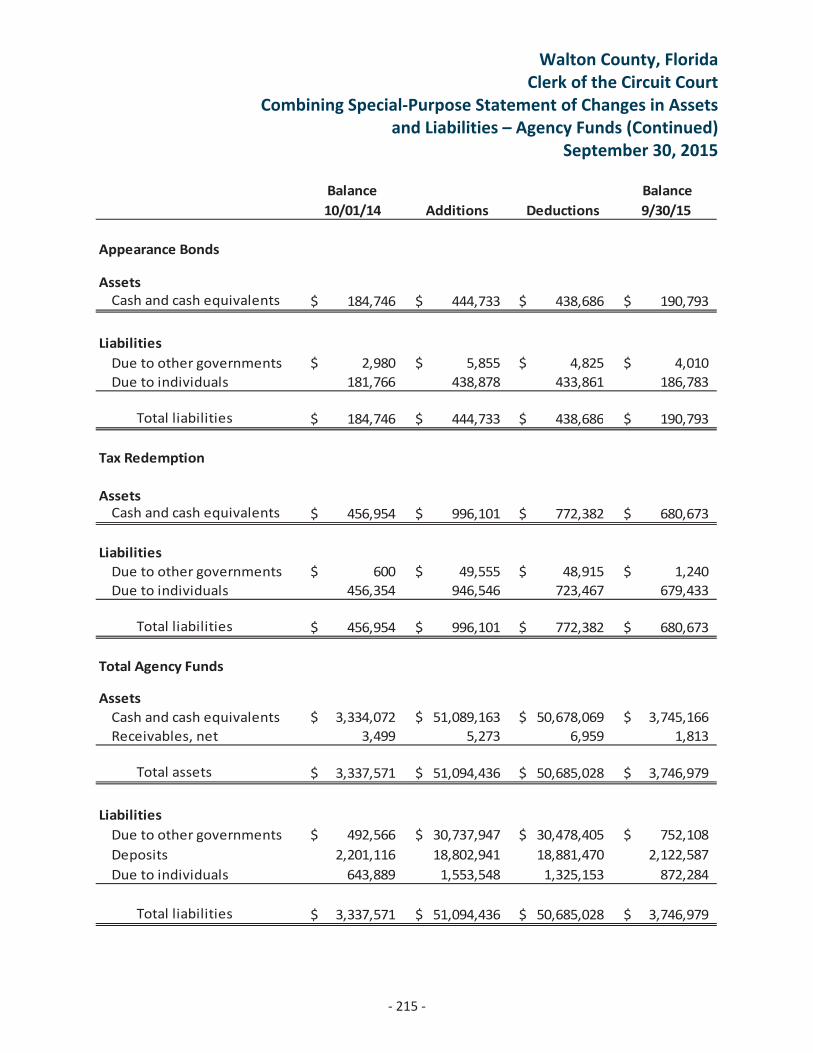

Combining Statement of Changes in Assets and LiabilitiesAgency Funds 126 128

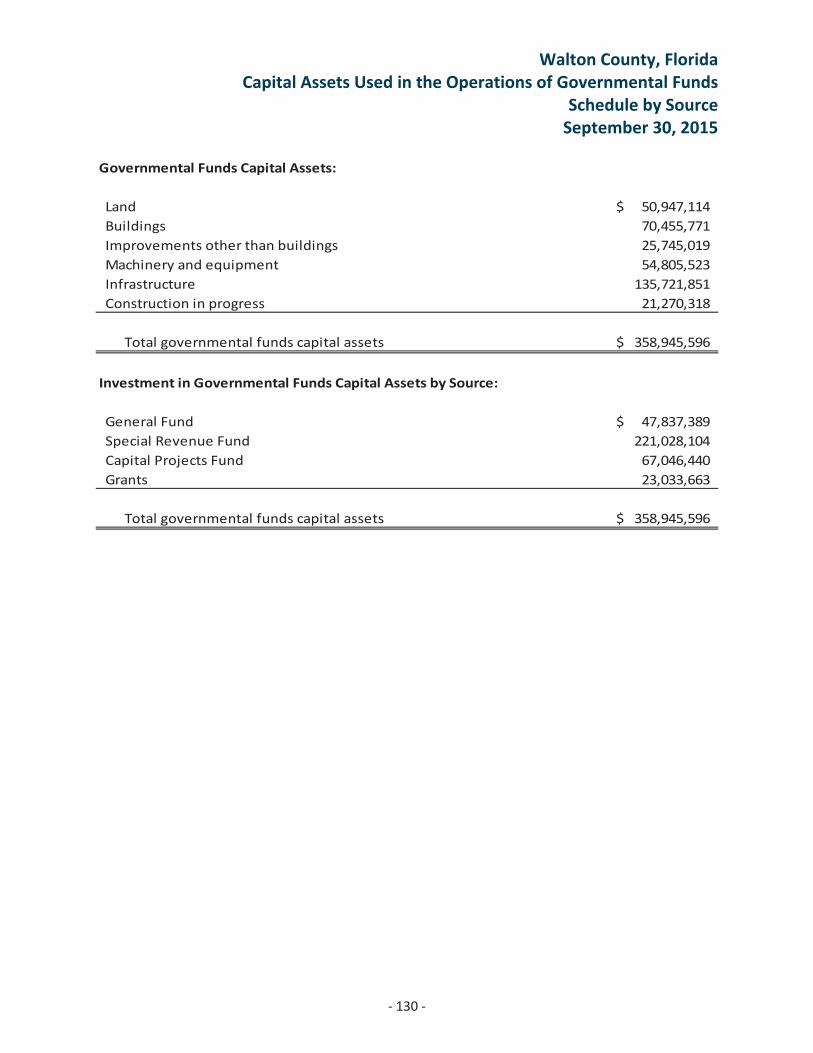

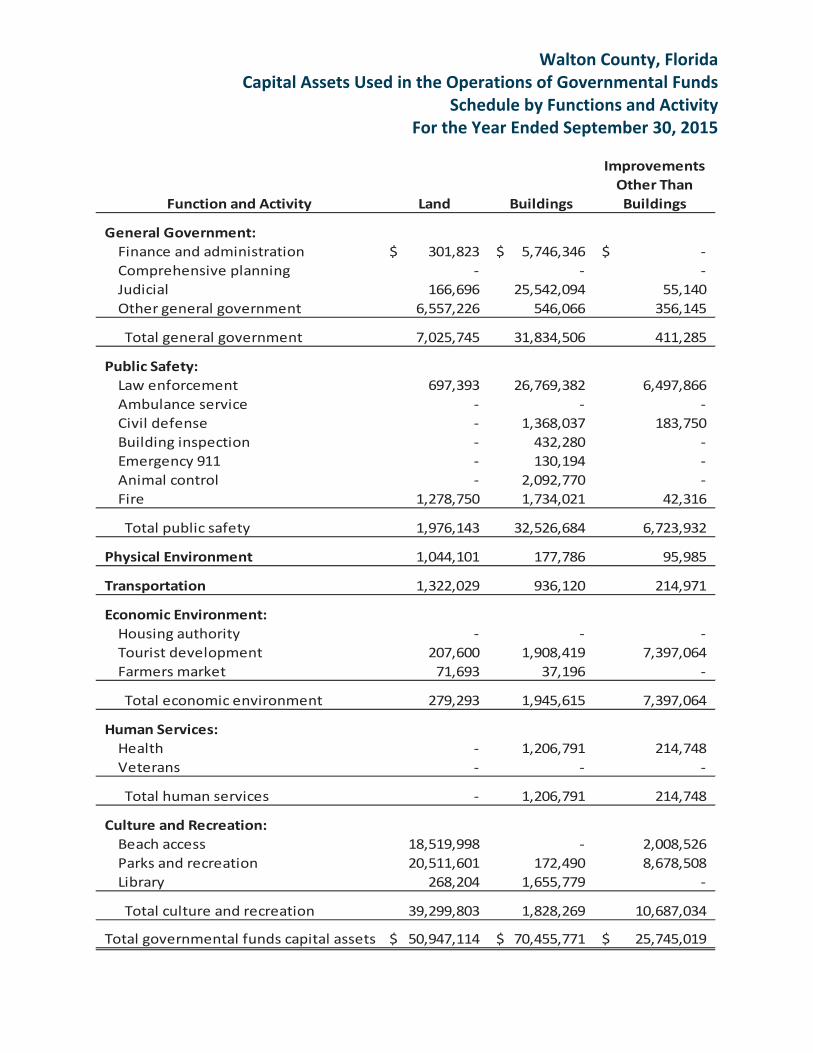

Capital Assets Used in the Operation of Governmental Funds

Capital Asset Schedules Description 129

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

IVIV

Schedule by Source 130

Schedule by Function and Activity 131

Schedule of Changes by Function and Activity 132

III. Statistical Section

Descriptions 133

Financial Statement Information

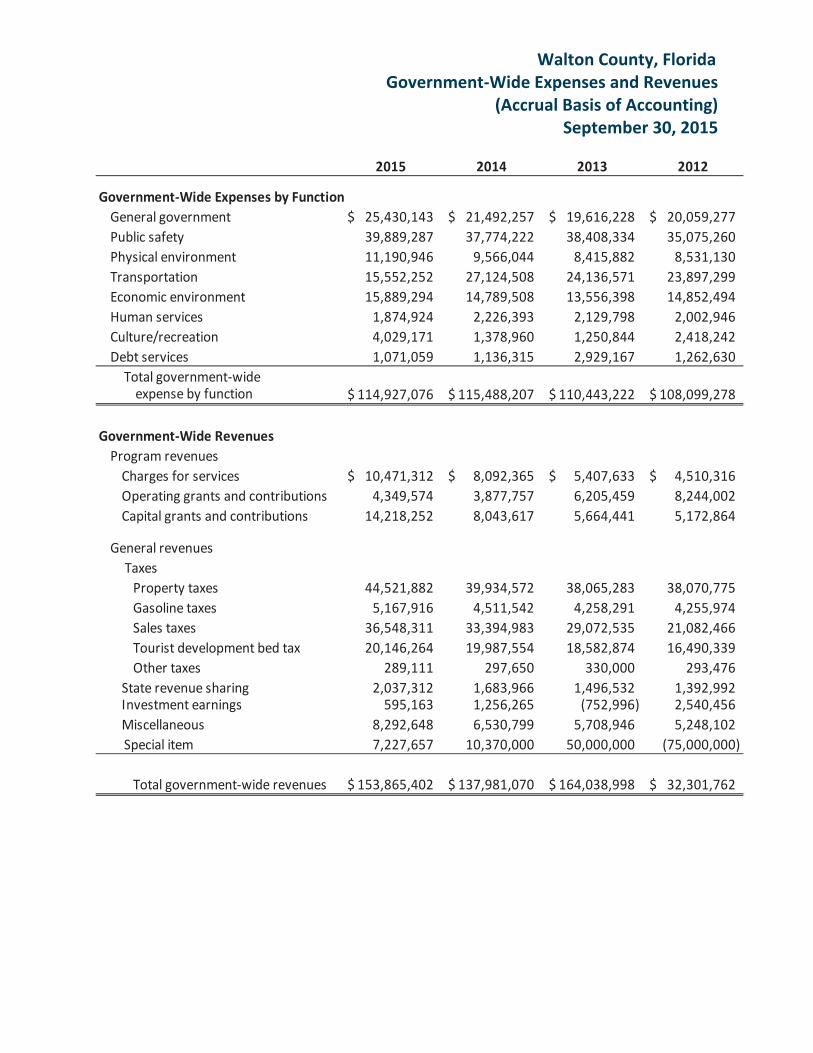

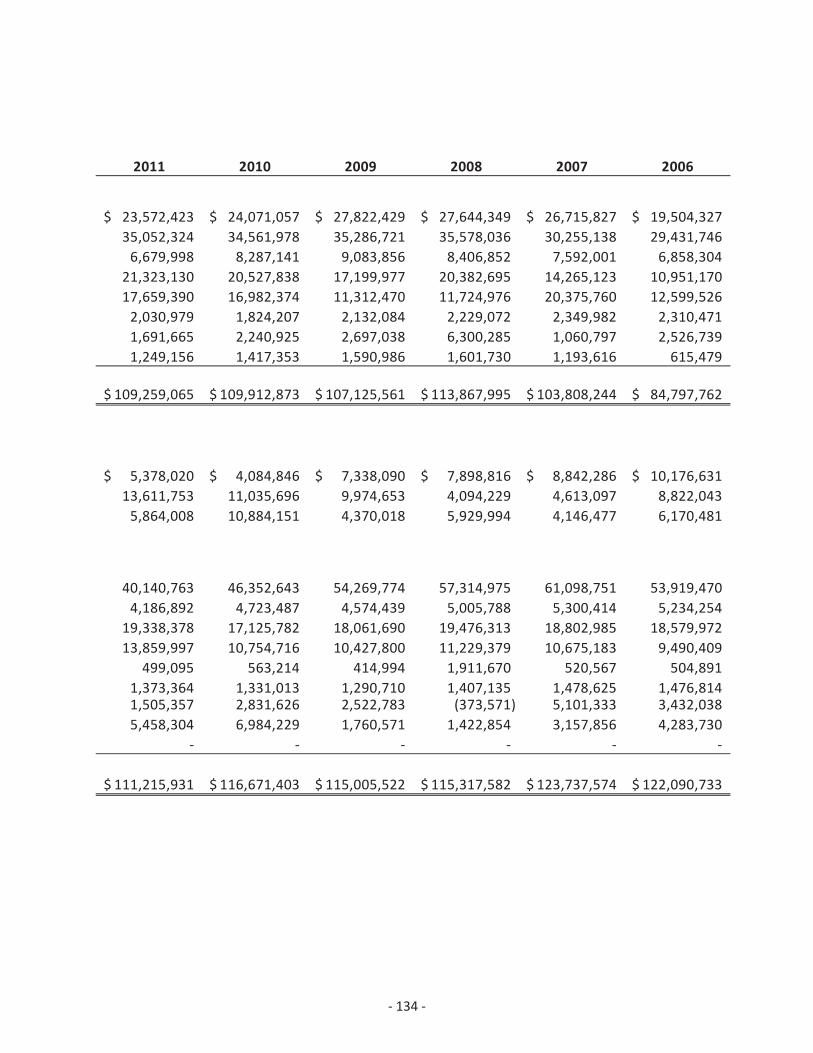

Government Wide Expenses and Revenues 134

General Governmental Expenditures by Function 135

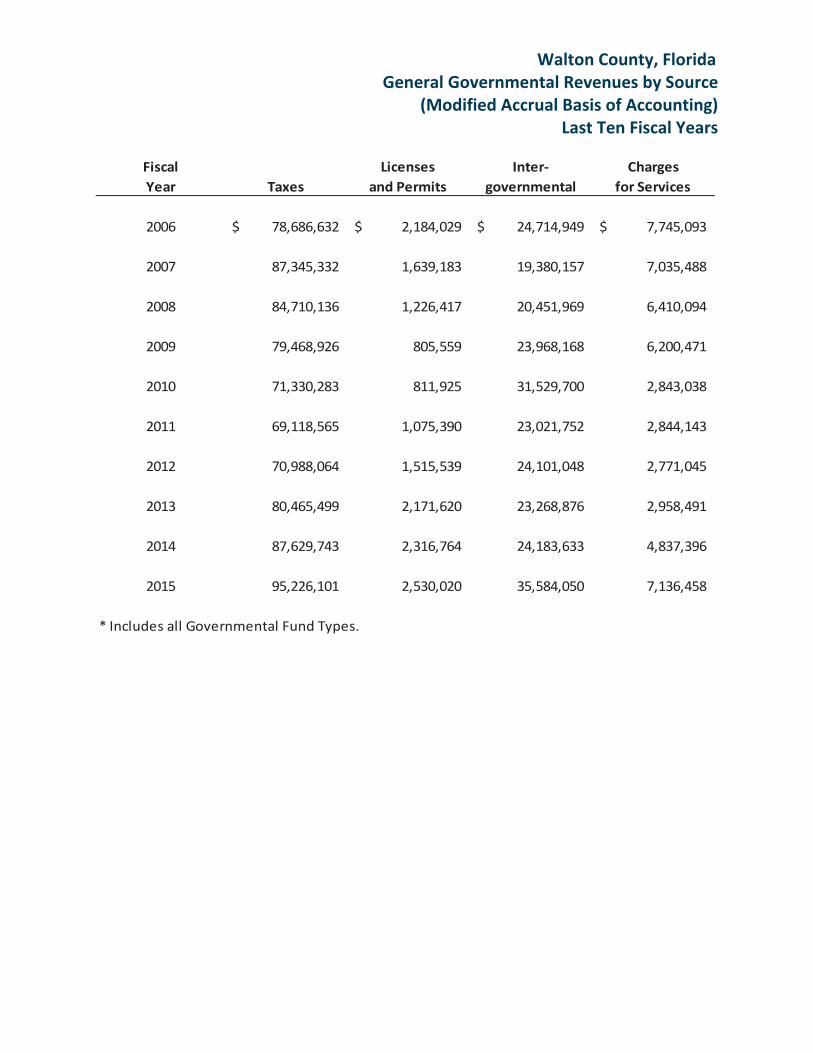

General Governmental Revenues by Source 136

Schedule of Net Position and Changes in Net Position 137

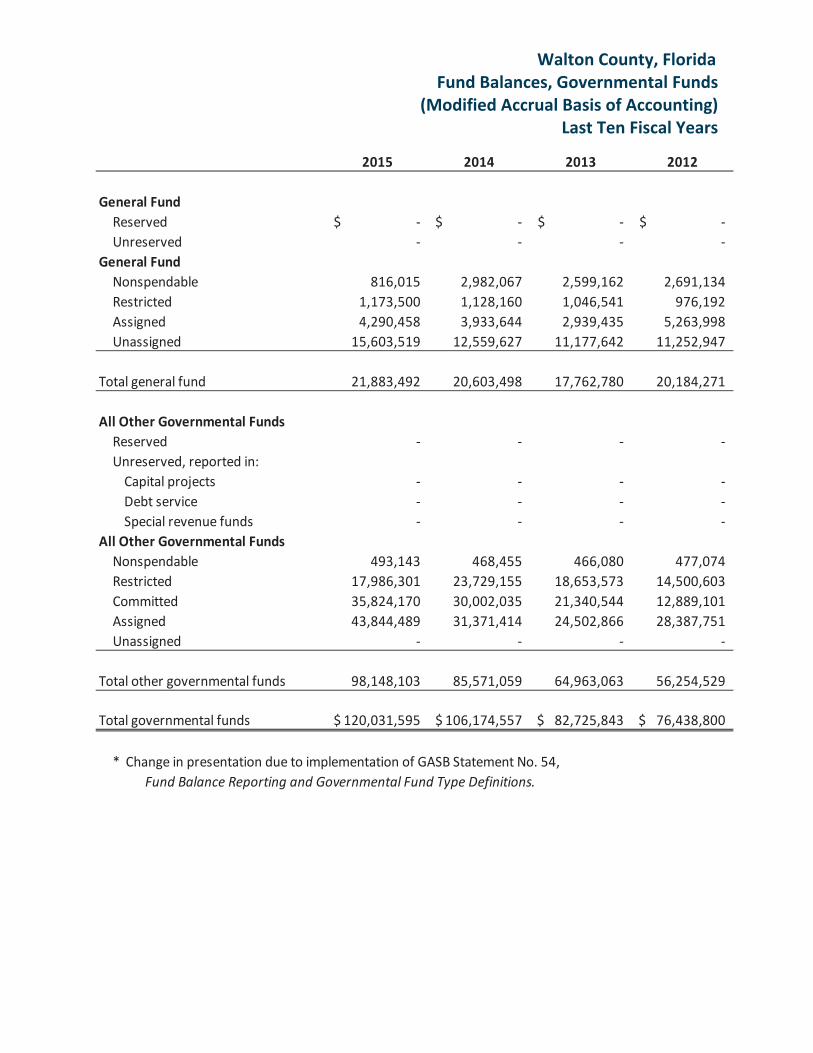

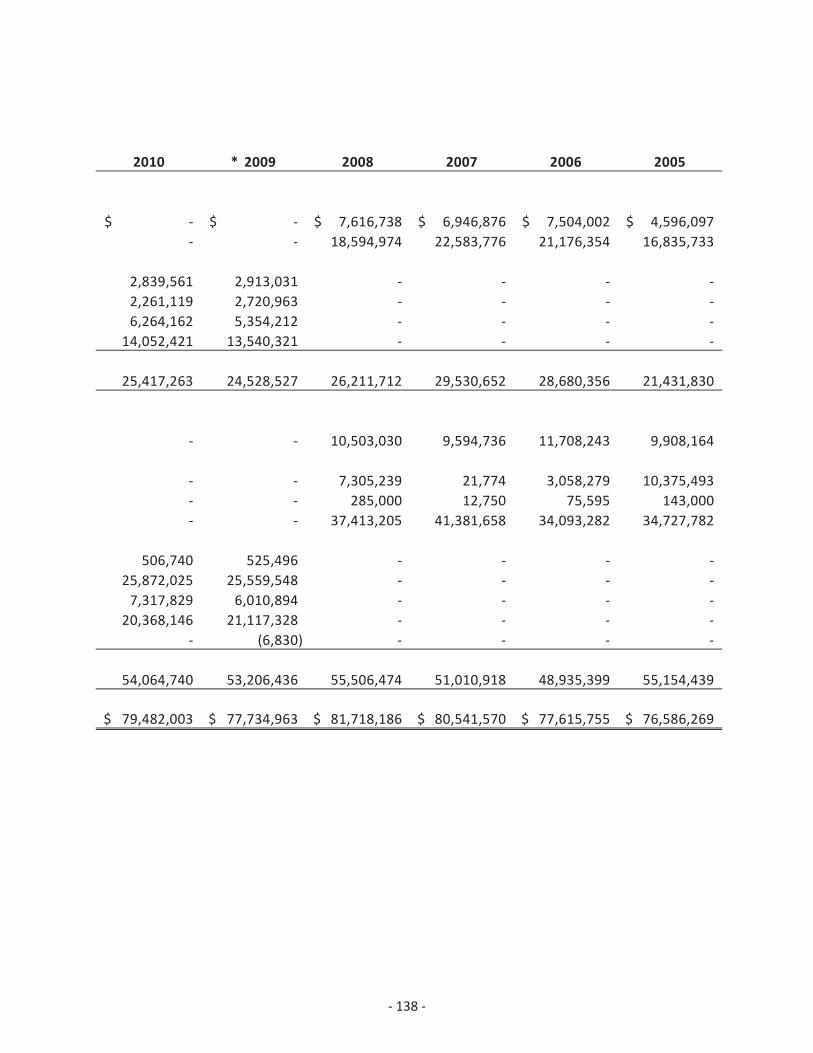

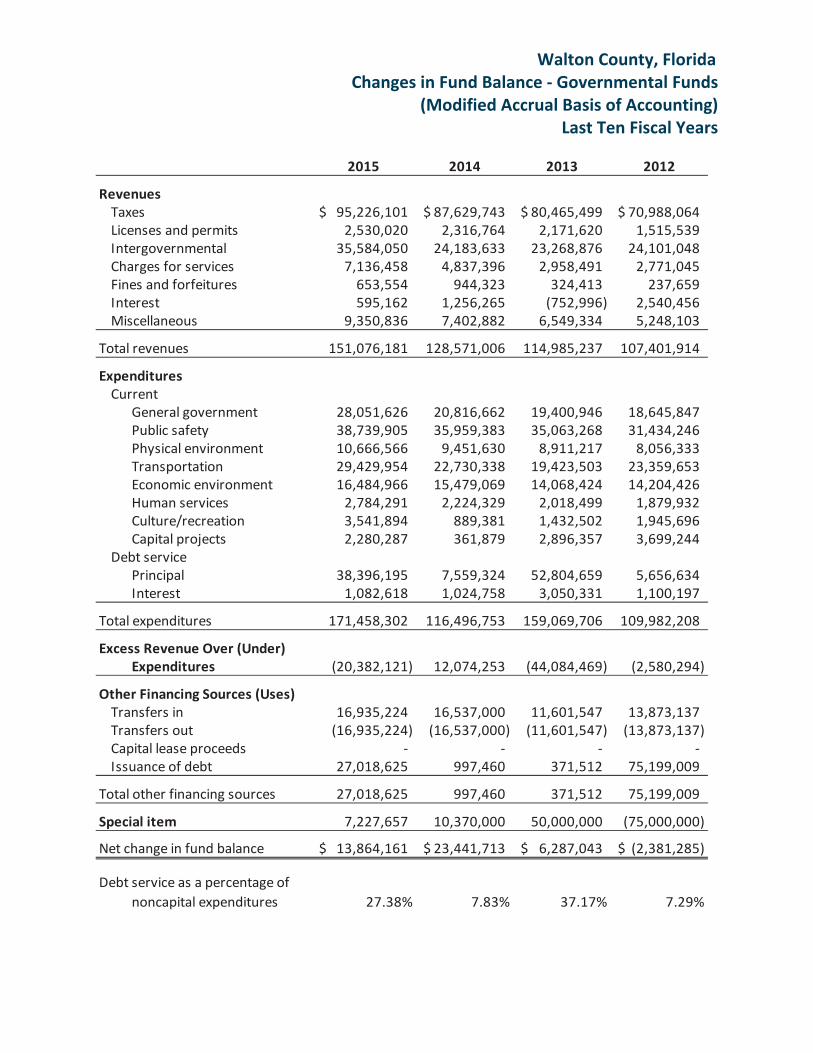

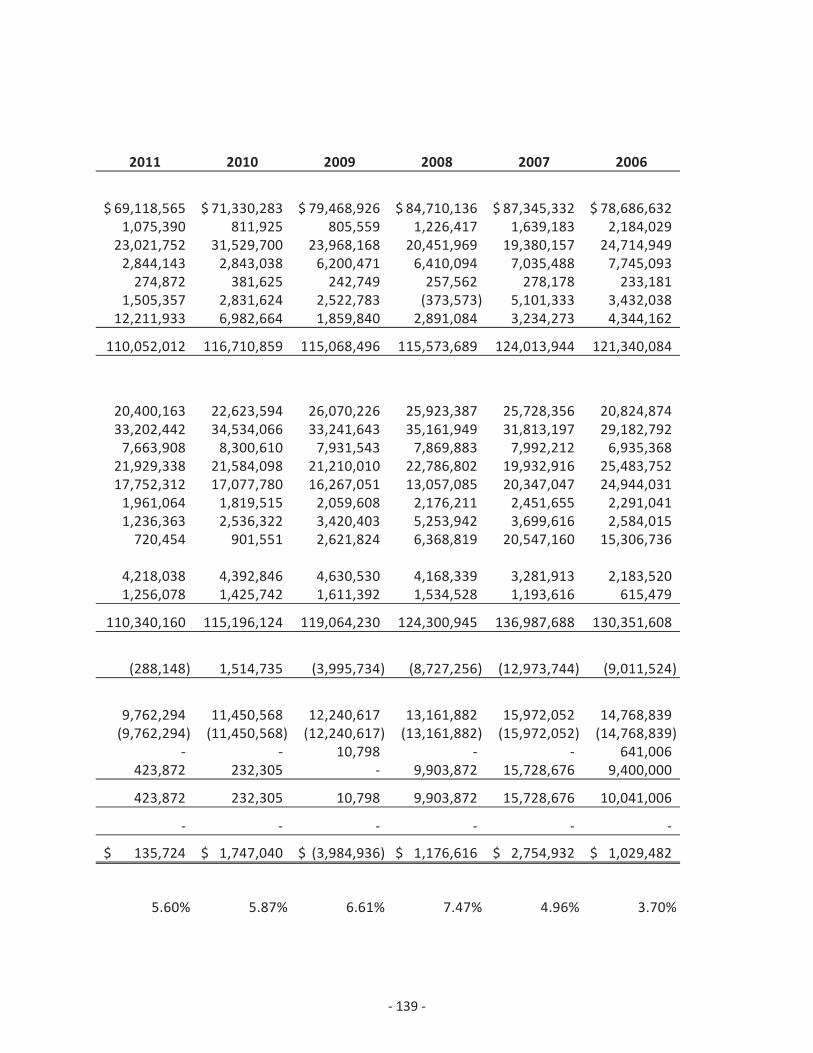

Fund Balances, Governmental Funds 138

Changes in Fund Balance – Governmental Funds 139

Other Information

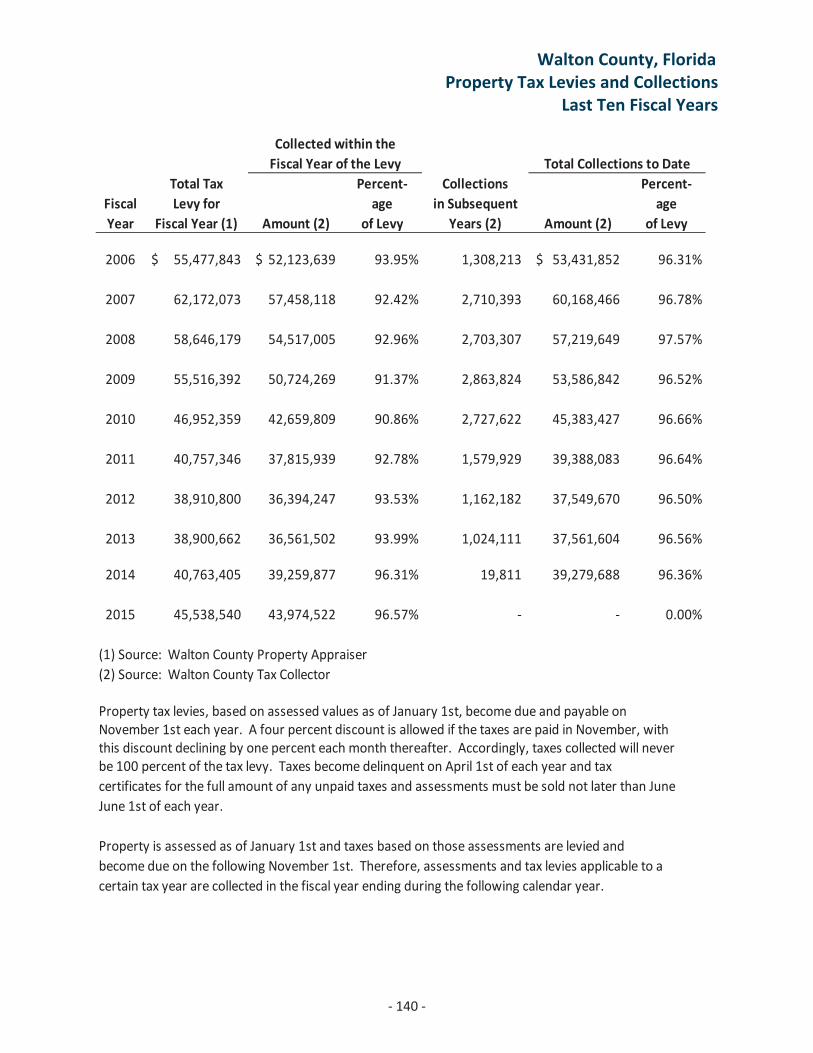

Property Tax Levies and Collections 140

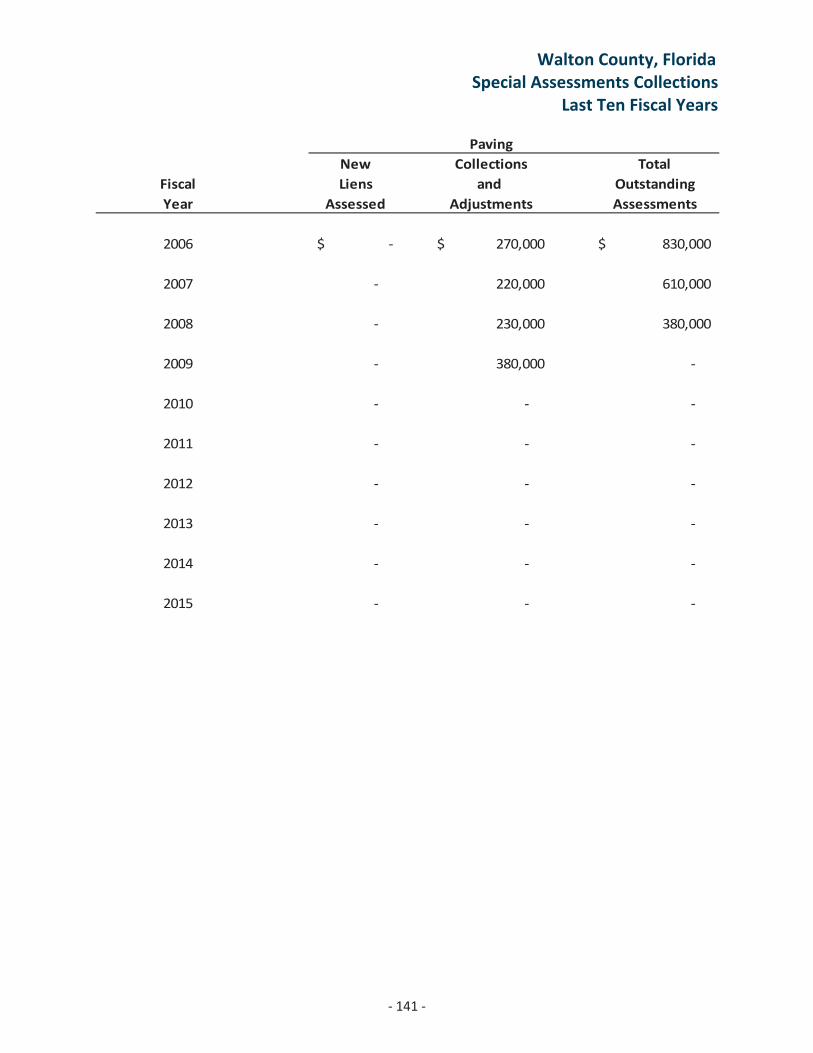

Special Assessments Collections 141

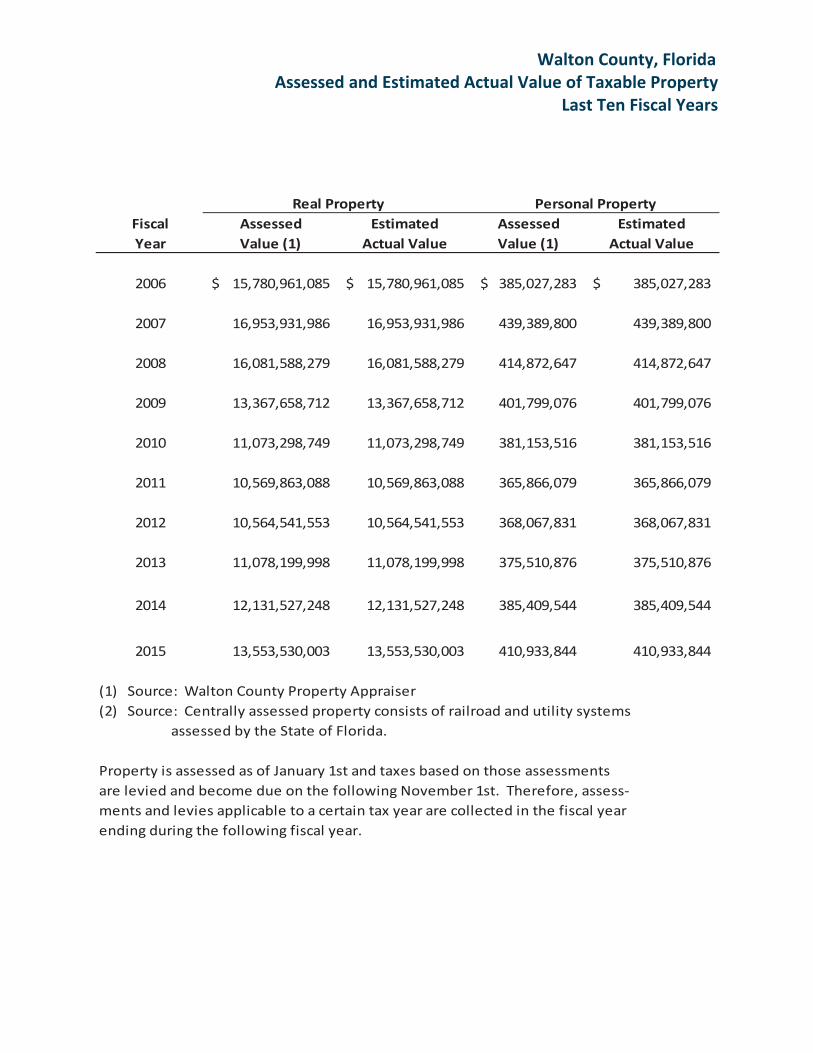

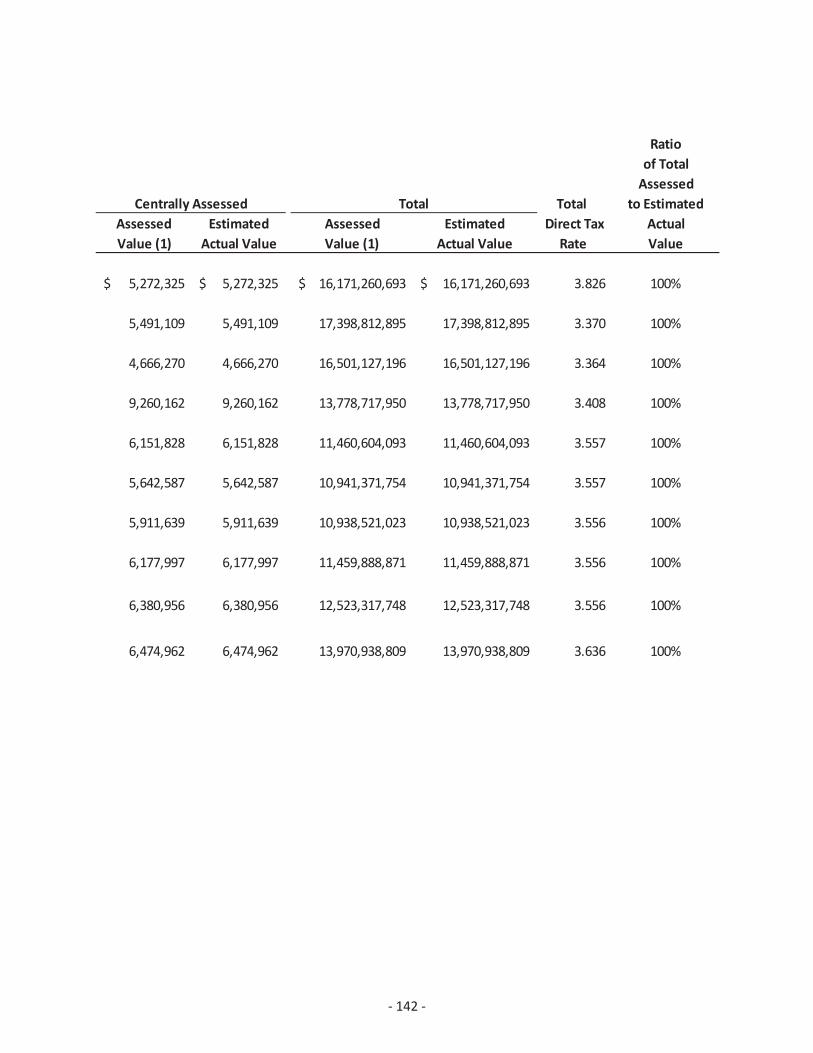

Assessed and Estimated Actual Value of Taxable Property 142

Property Tax Rates – Direct and Overlapping Governments 143

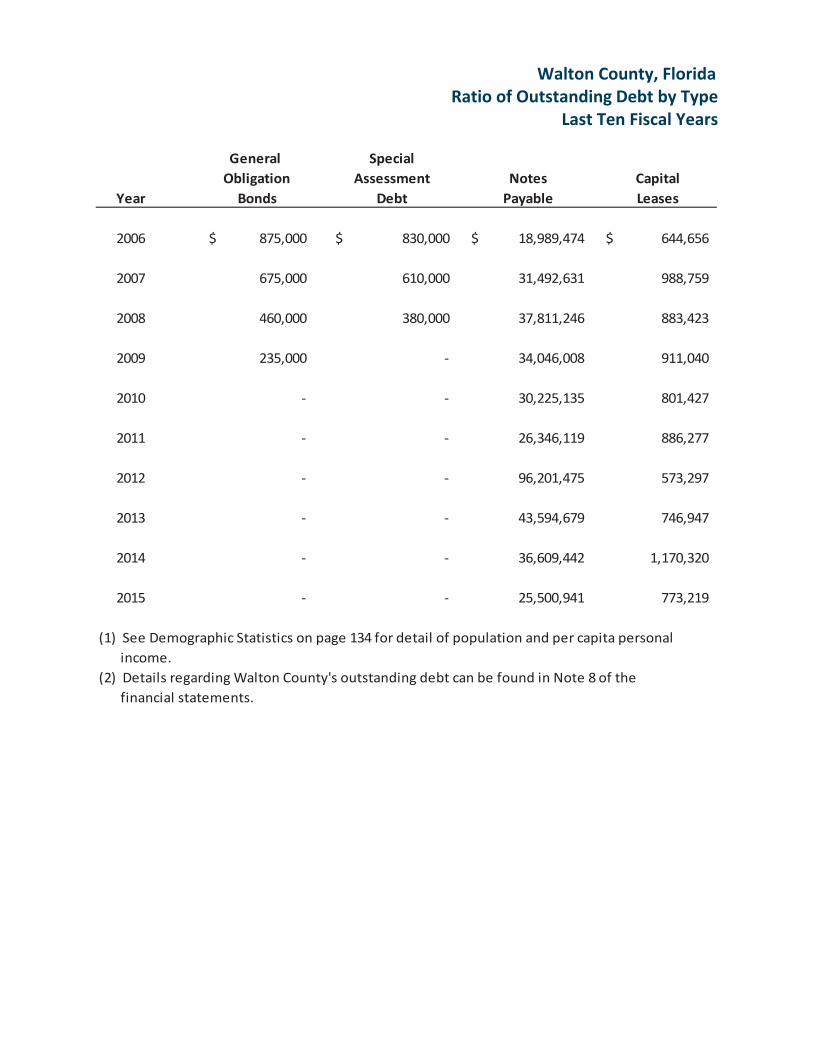

Ratio of Outstanding Debt by Type 144

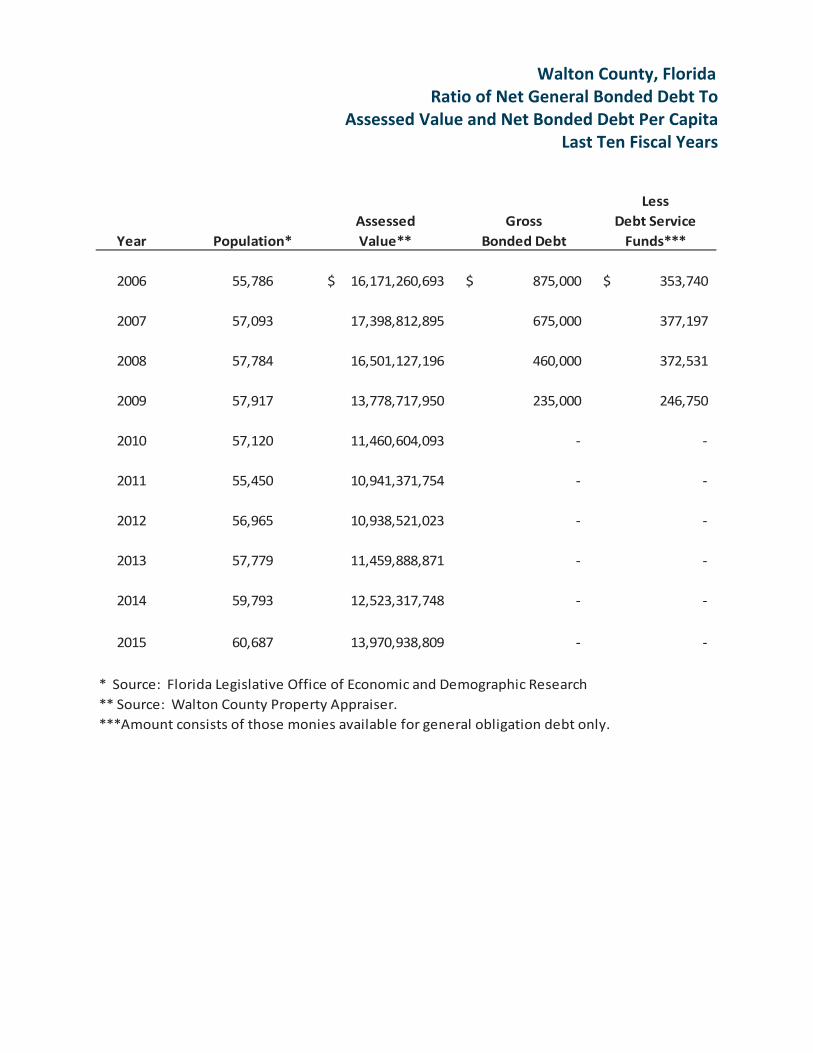

Ratio of Net General Bonded Debt to Assessed Value andNet Bonded Debt Per Capita 145

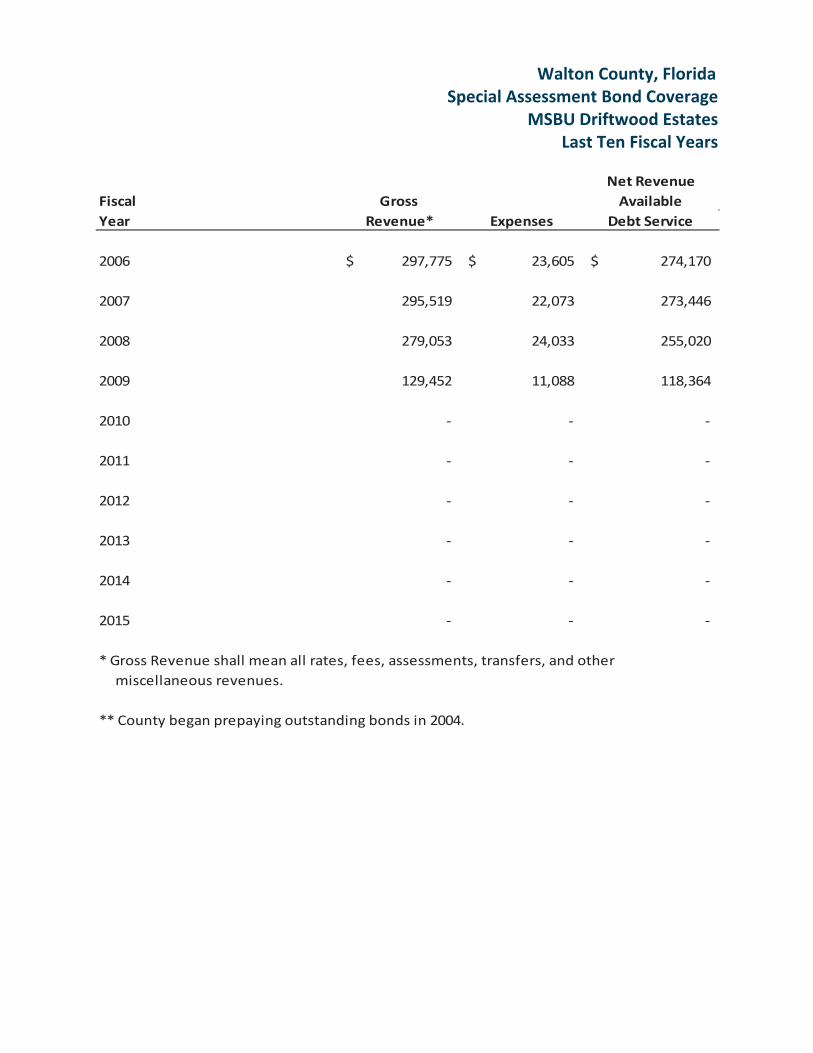

Special Assessment Bond Coverage – MSBU Driftwood Estates 146

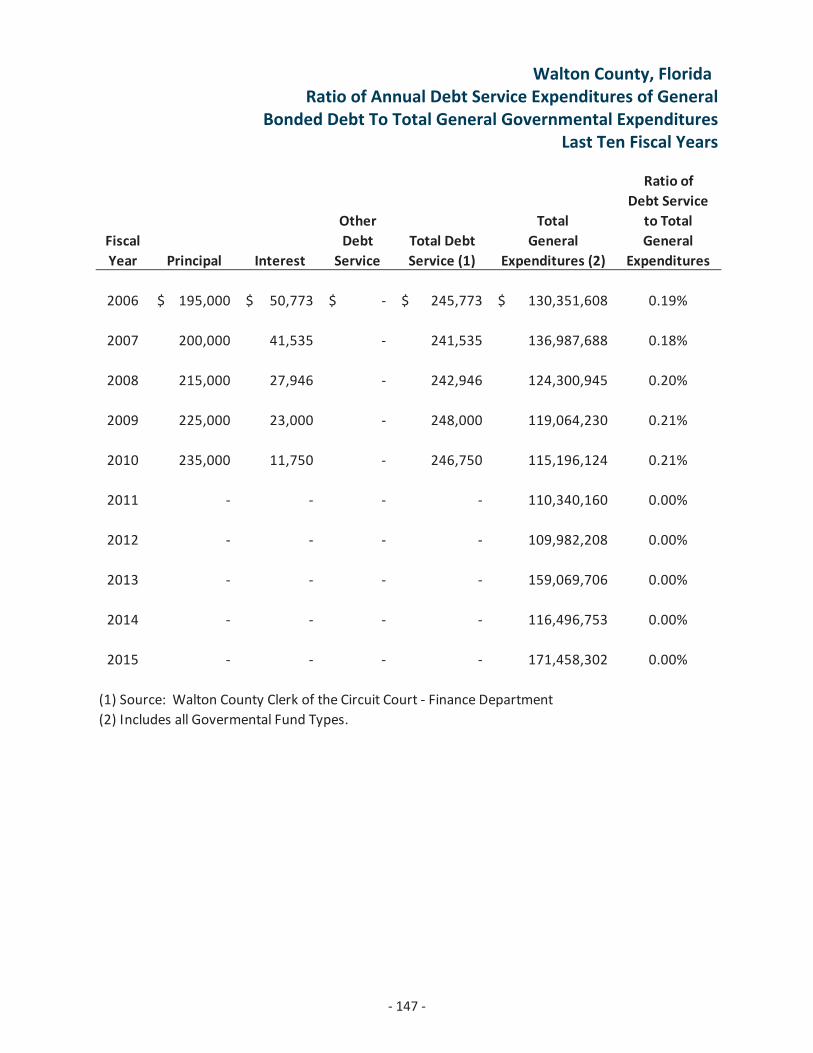

Ratio of Annual Debt Service Expenditures of General BondedDebt to Total General Governmental Expenditures 147

Bond Coverage 148

Demographic Statistics 149

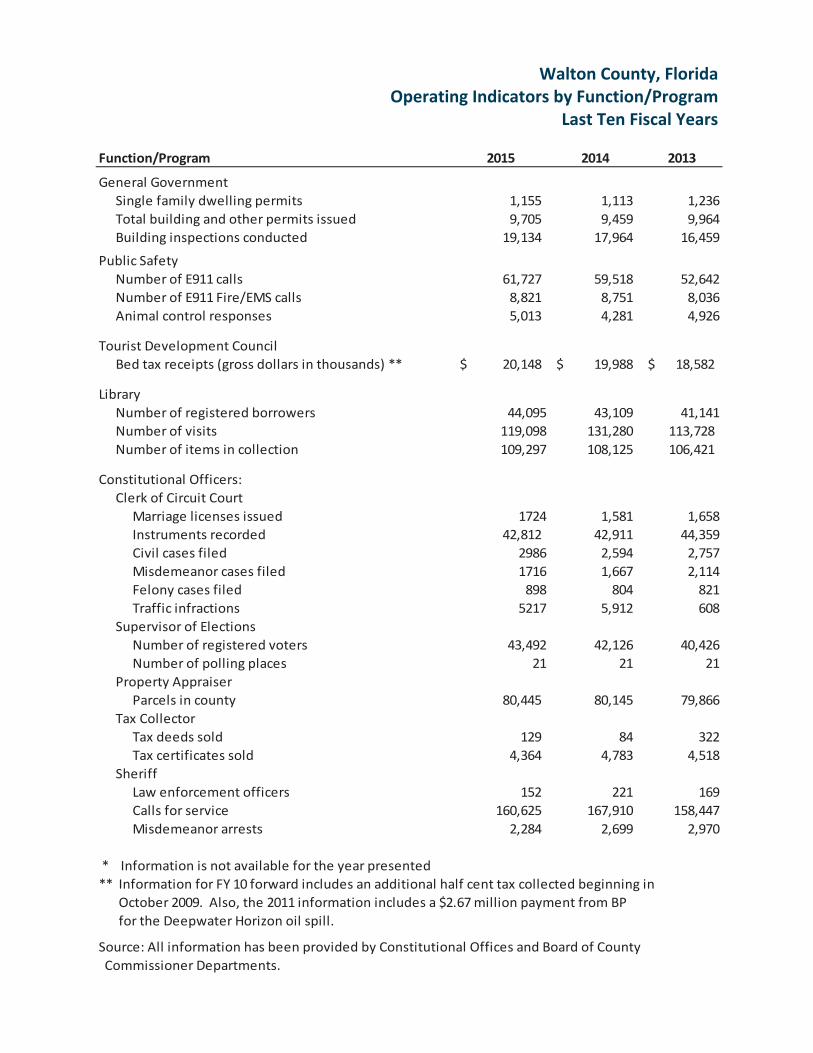

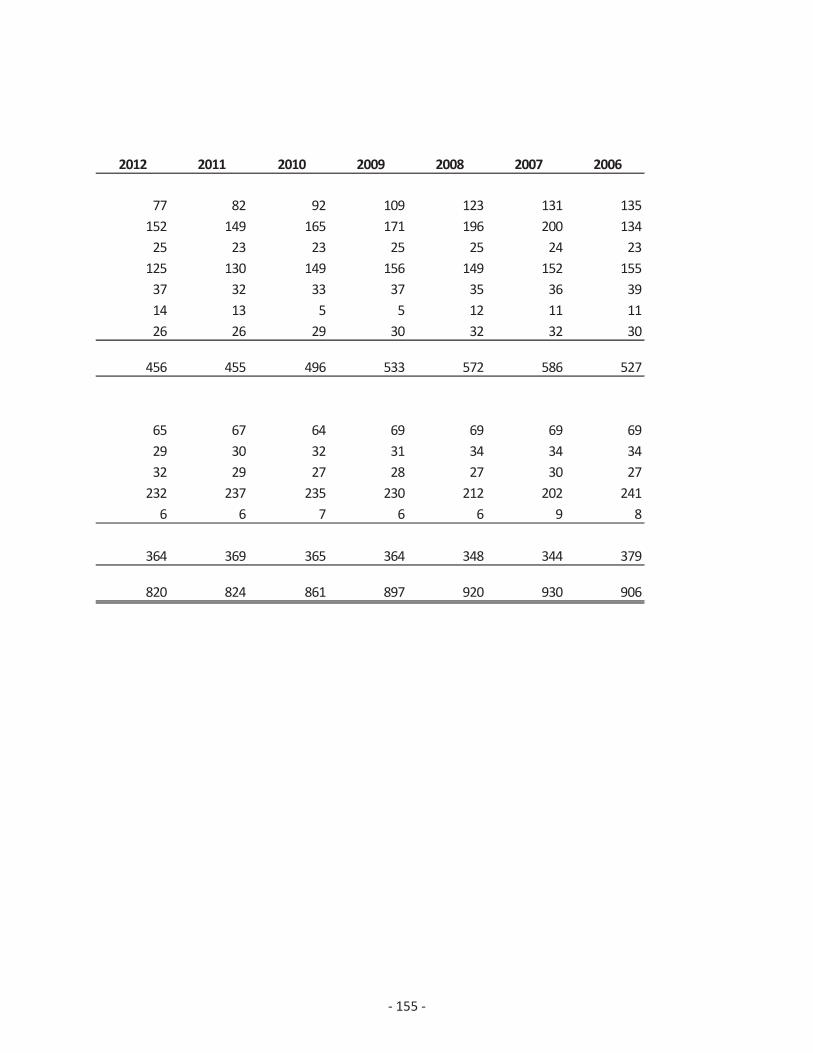

Operating Indicators by Function/Program 150

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

VV

Principal Employers 151

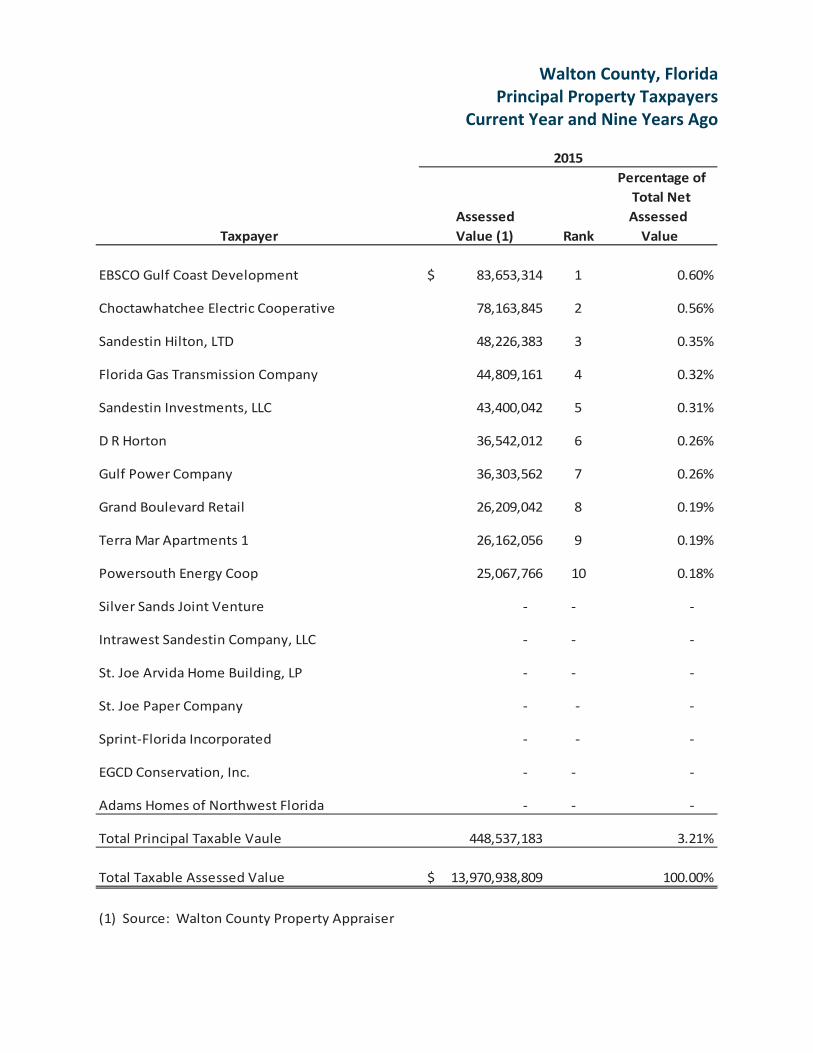

Principal Property Taxpayers 152

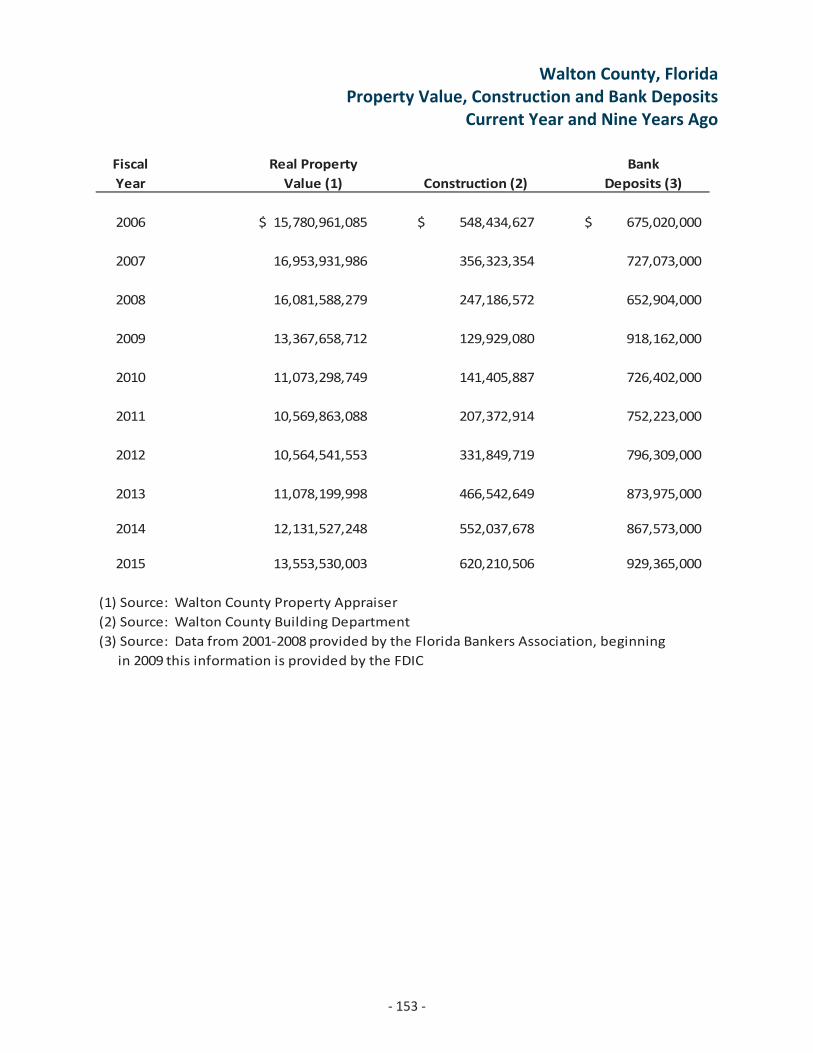

Property Value, Construction and Bank Deposits 153

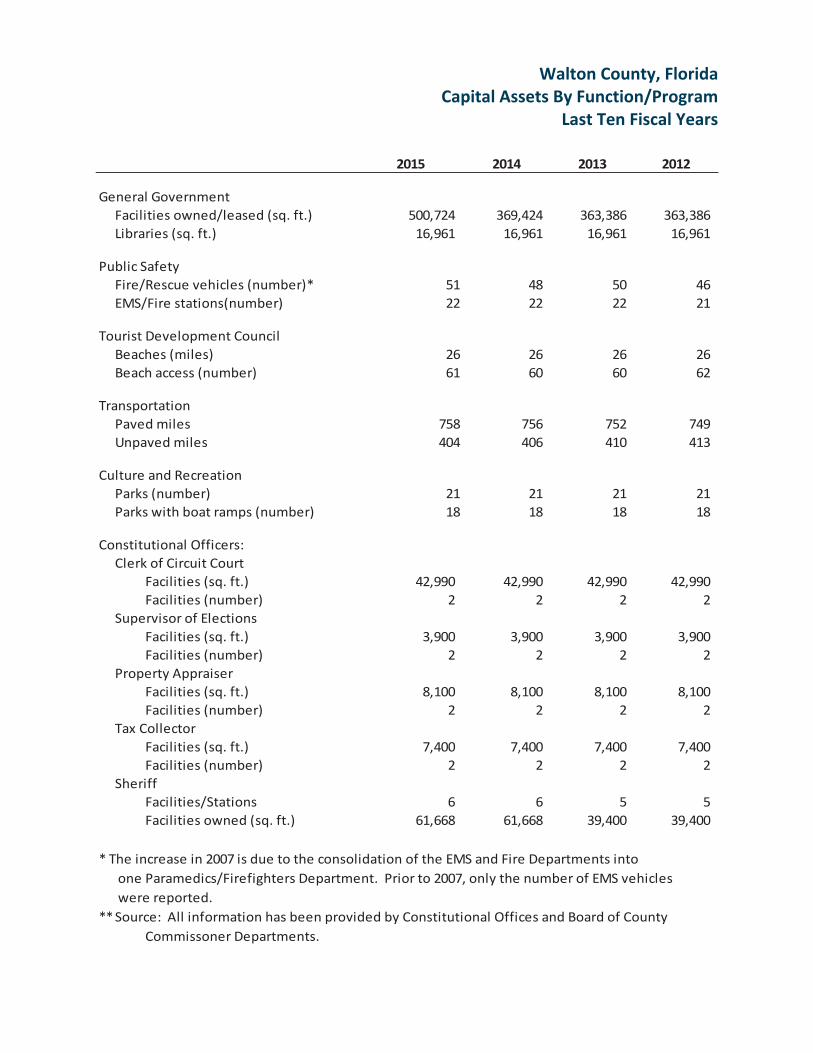

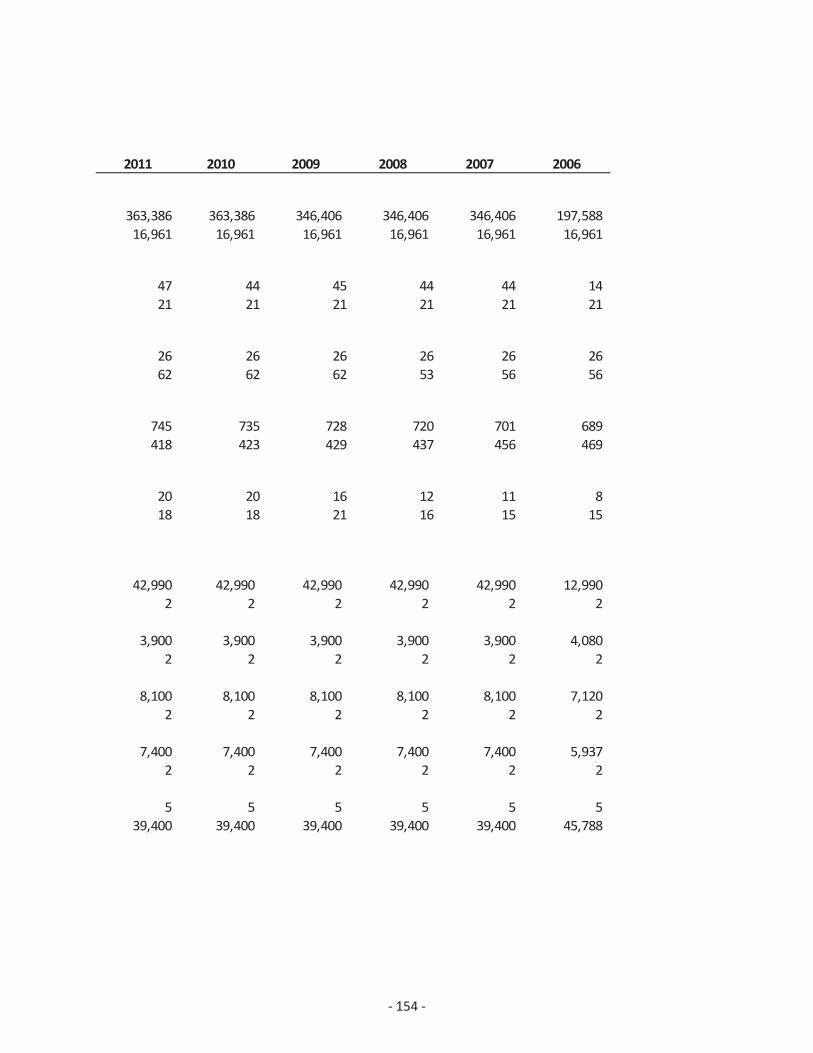

Capital Assets by Function/Program 154

Full time Equivalent Government Wide Employees by Function 155

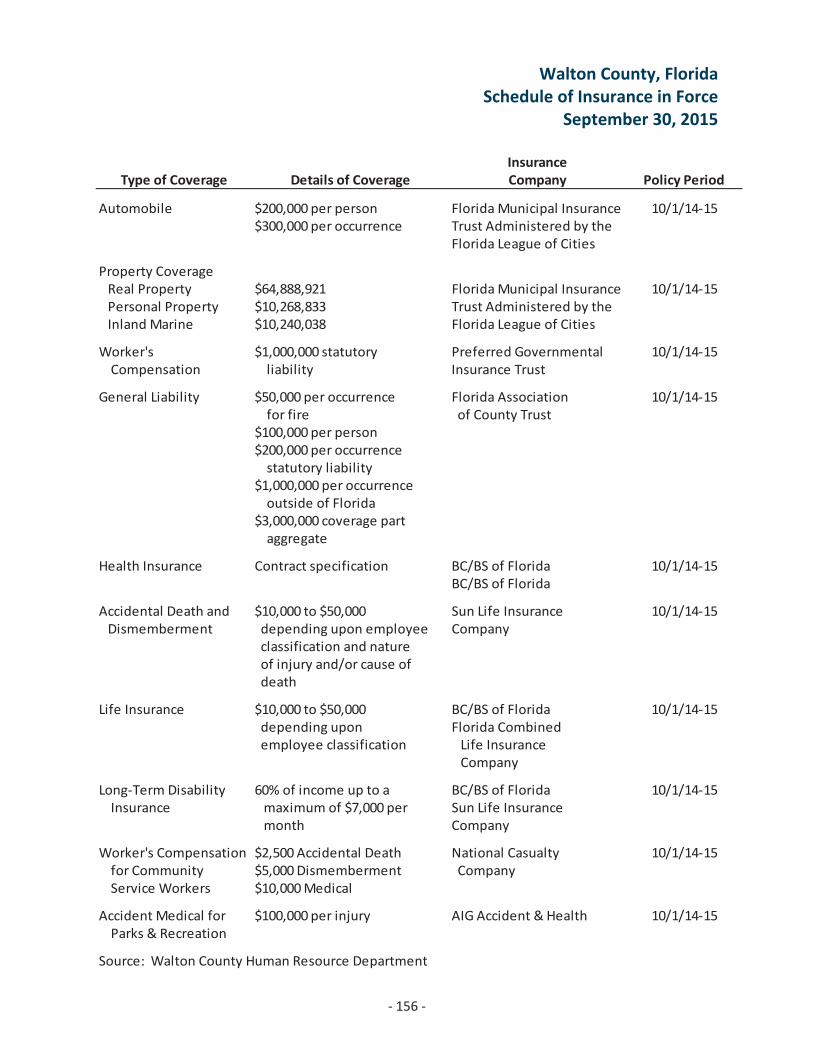

Schedule of Insurance in Force 156

IV. Compliance Section

Independent Auditors’ Reports 157 – 160

Schedule of Expenditures of Federal Awards and State FinancialAssistance 161 163

Notes to Schedule of Expenditures of Federal Awards and StateFinancial Assistance 164 165

Schedule of Findings and Questioned Costs 166 170

Summary Schedule of Prior Audit Findings for Federal Awards 171

Summary Schedule of Prior Audit Findings for State FinancialAssistance 172

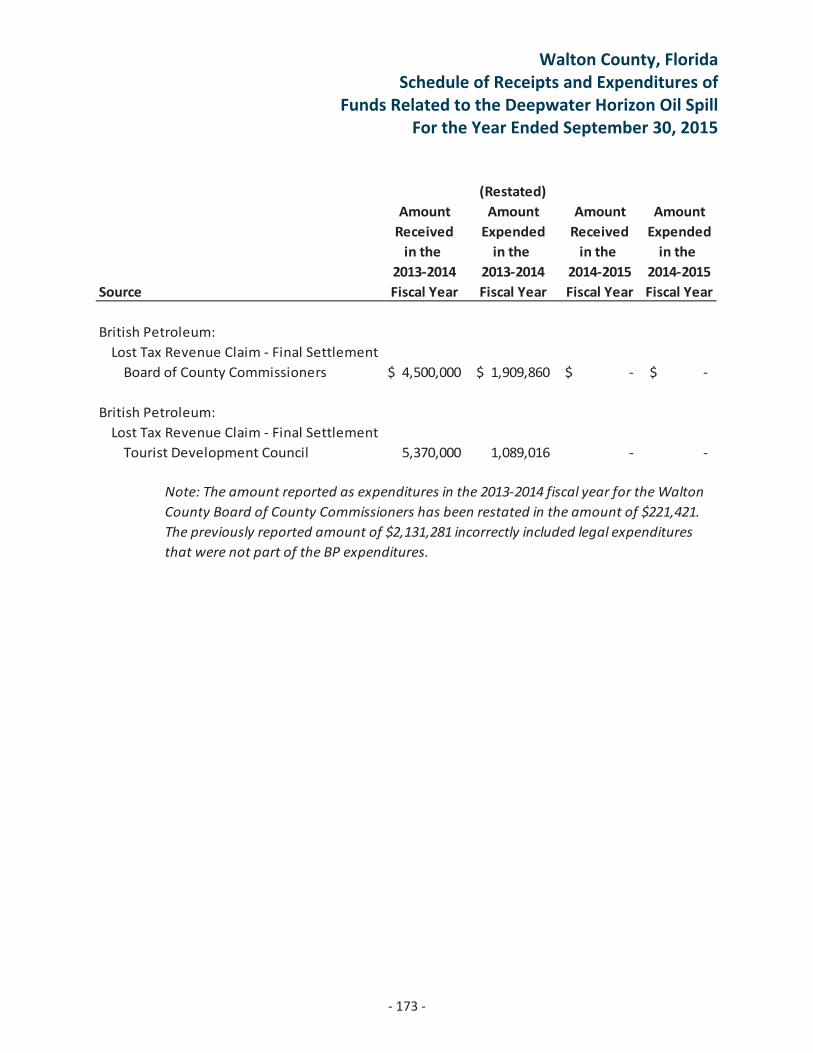

Schedule of Receipts and Expenditures of Funds Related to theDeepwater Horizon Oil Spill 173

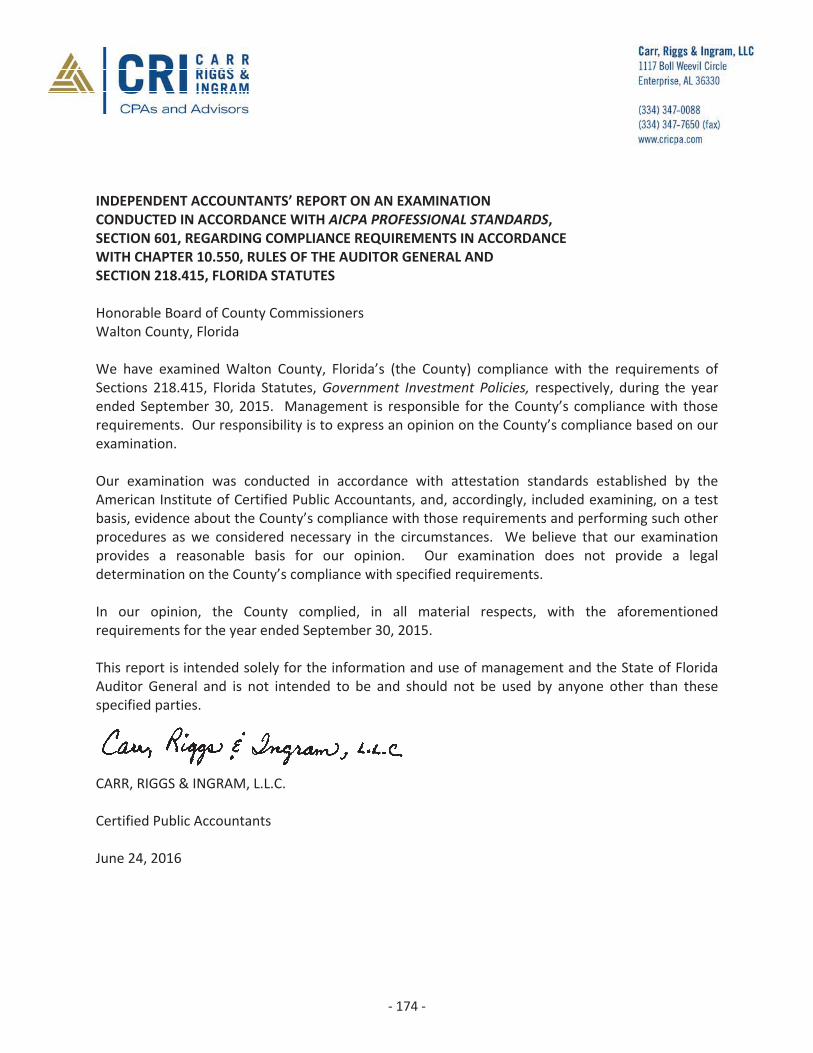

Independent Accountants’ Report on an Examination Conducted inAccordance with AICPA Professional Standards, Section 601, RegardingCompliance Requirements in Accordance with Chapter 10.550, Rulesof the Auditor General and Section 218.415, Florida Statutes 1742

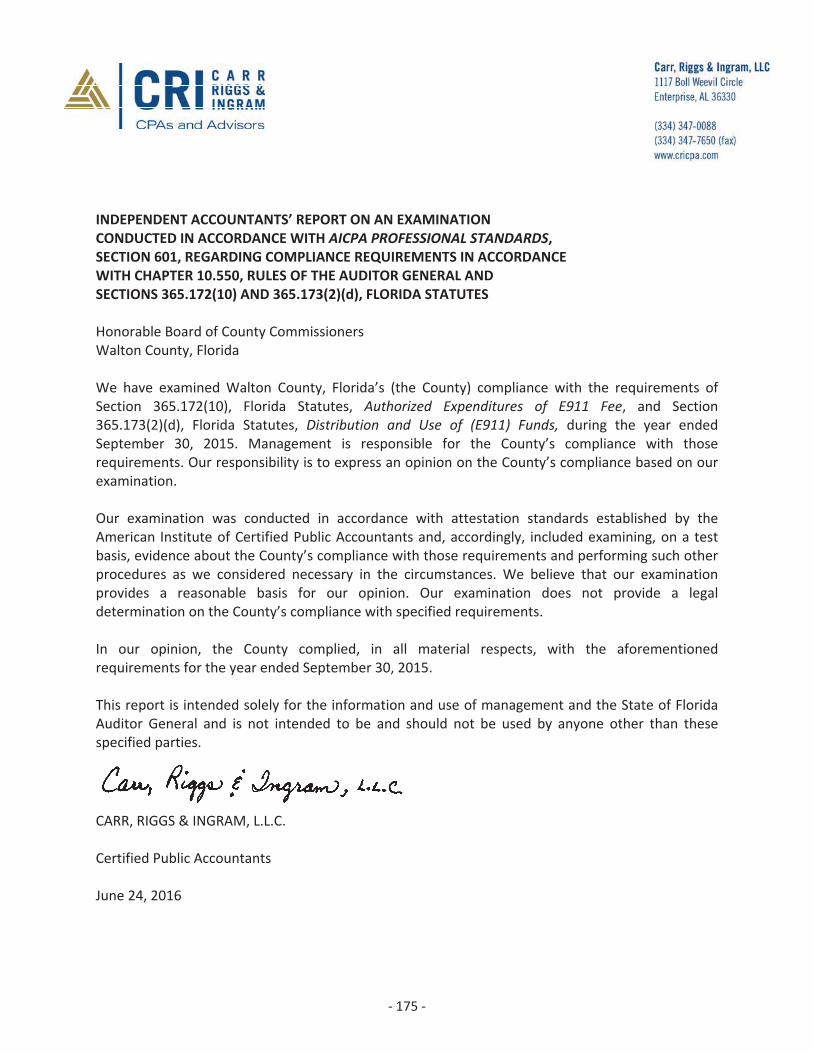

Independent Accountants’ Report on an Examination Conducted inAccordance with AICPA Professional Standards, Section 601, RegardingCompliance Requirements in Accordance with Chapter 10.550, Rulesof the Auditor General and Sections 365.172(10) and 365.173(2)(d),Florida Statutes 175

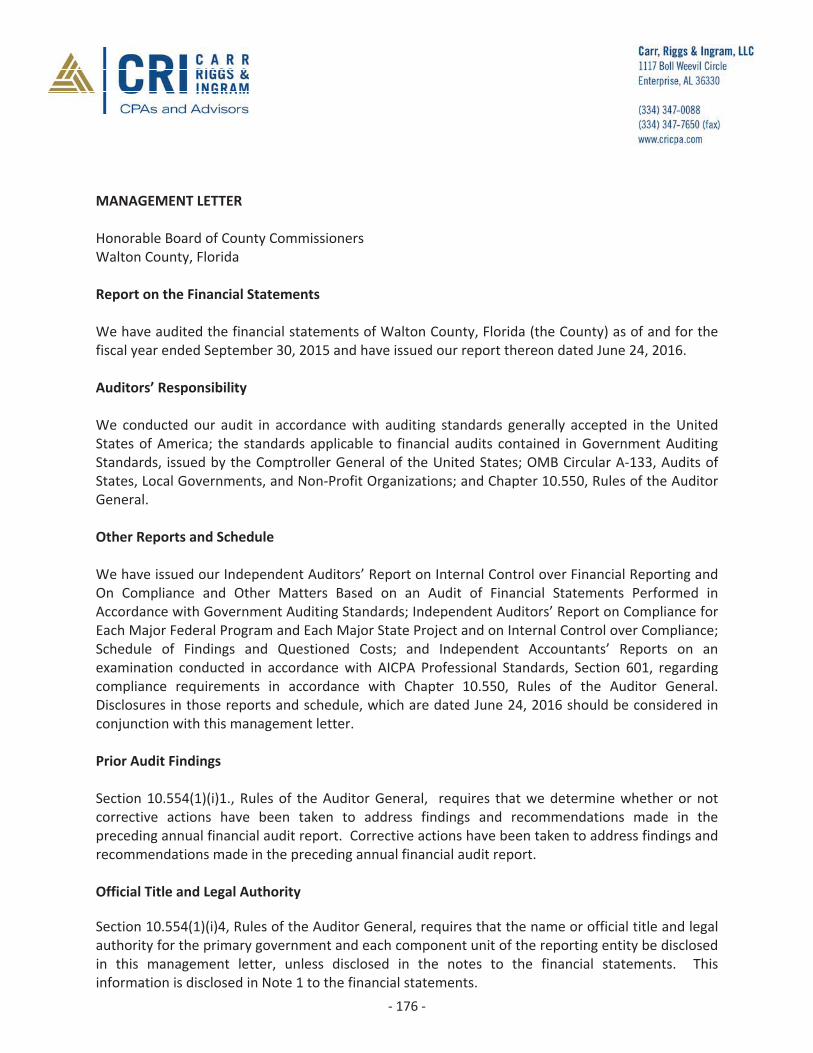

Management Letter 176 180

Management’s Response and Corrective Action Plan 181 182

Walton County, FloridaComprehensive Annual Financial Report

Table of Contents

VIVI

V. Financial Statements and Compliance Reports For Constitutional Officers

Clerk of the Circuit Court 183 220

Property Appraiser 221 242

Tax Collector 243 271

Supervisor of Elections 272 297

Sheriff 298 331

1

June 24, 2016

To the Honorable Members of the Board of County Commissioners and Citizens of Walton County:

We are pleased to present the Comprehensive Annual Financial Report (CAFR) of Walton County, Florida for the fiscal year ended September 30, 2015. This report was prepared in accordance with generally accepted accounting principles by the Clerk of Courts & County Comptroller. Responsibility for both the accuracy of the presented data, and the completeness and fairness of the presentation, including all disclosures, rests with the Clerk of Courts & County Comptroller as Chief Financial Officer of Walton County.

The Clerk of Courts & County Comptroller, through the Finance Department, is responsible for establishing and maintaining internal controls to provide reasonable, but not absolute assurance regarding the safeguarding of assets against loss from unauthorized use or disposition, the reliability of financial records for preparing financial statements, and maintaining accountability for assets. The concept of reasonable assurance recognizes that the cost of a control should not exceed the benefits likely to be derived, and the evaluation of costs and benefits requires estimates and judgments by management. It is within this framework that we believe the County’s internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions.

We believe the data as presented is accurate in all material respects; that it is presented in a manner designed to fairly set forth the financial position and results of operations of the County as measured by the financial activity of its various funds, and that all disclosures necessary to enable the user of these financial statements to gain a thorough understanding of the County’s financial activity have been included.

Chapter 218.39 of the Florida Statutes requires a financial audit of all counties in the state be performed by independent certified public accountants. This requirement has been met for the fiscal year ended September 30, 2015 and the independent auditors’ report has been included in the financial section of this report. In addition to meeting the requirements set forth in state statutes, the audit was also designed to meet the requirements of the federal 1996 Single Audit Act Amendments and the related OMB Circular A-133. The standards governing single audit engagements require the independent auditor to report on the government’s internal controls and compliance with legal requirements with special emphasis on the administration of federal awards. Information related to the single audit, including schedules of federal awards and state financial assistance and independent auditors’ reports on the internal control structure and compliance with requirements applicable to federal financial assistance, are included in the compliance section of this report.

2

Governmental accounting and auditing principles require that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in combination with it. Walton County’s MD&A can be found immediately following the independent auditors’ report.

County Organization. Walton County encompasses 1,066 square miles with a population of 60,687. There are three incorporated cities within Walton County: DeFuniak Springs, Freeport, and Paxton.

The County provides a number of services to its citizens, including police and fire protection, emergency medical services, health and social services, and cultural and recreation programs. Walton County operates under a commission/administrator form of government with a governing board consisting of five county commissioners who are elected by the citizens of Walton County from at-large districts for staggered four-year terms. Each commission member must meet district residency requirements. In addition to the Board of County Commissioners, there are five elected constitutional officers: The Clerk of the Circuit Court & County Comptroller, Property Appraiser, Sheriff, Supervisor of Elections, and Tax Collector. The Walton County Board of County Commissioners exercises varying degrees of budgetary control, but not administrative control, over the activities of the constitutional officers. The Property Appraiser, Sheriff, and Supervisor of Elections operate their respective offices as budget officers with funding provided by the Board of County Commissioners in the form of operating subsidies. In return, each budget officer is responsible for the collection of revenues within their jurisdictional area, and for the subsequent remittance of such collection to the Board. The Clerk of Courts & County Comptroller and the Tax Collector operate as fee officers. Fee officers are authorized to retain revenues generated within their offices for the purpose of defraying the cost of operations. All excess fees available at the end of the fiscal year are remitted back to the Board of County Commissioners, except for the excess fees received by the court system which are remitted to the Florida Department of Revenue.

Formal budgetary integration is employed as a management control device during the year. Constitutional officers funded by the Board and all county departments must submit their budget requests to the Office of Management and Budget (OMB) by June 1st of each year. After budget workshops are conducted with each department and constitutional officers, a proposed budget is submitted to the public by Board resolution and public hearings are held to obtain comments from the citizenry. A last public hearing is then held and the final budget is adopted. Walton County follows the laws of Florida regarding the control, adoption and amendment of the budget during each fiscal year; however, the County Administrator approves all departmental budgetary changes by means of a signed budget transfer form. The Board of County Commissioners approves all motions made for inter-divisional transfers and increases in the total budget for a division that occurs due to unanticipated grants or after a public hearing for special expenditures that need to be made from reserves.

Local Economy. Located in the Panhandle of Florida, tourism and its related industries continue to fuel the local economy; however, the County realizes the need to broaden economic opportunities by attracting more diversified businesses and jobs. While the majority of Walton County citizens are employed in the service or government sector, the need for employment diversity has never been more critical than it is now. The opening of the Mossy Head Industrial Park in 2013-14 has added to our employment base and offers our citizens more employment options. Several tenants have or will open a location in the industrial park, including Love’s Travel Stops and Country stores, Empire Truck Sales, and Southern Tire Mart. Ultimately, Walton County’s high quality of living serves as a great attraction for both individuals and their families. Our commitment to responsible growth furthers that opportunity.

3

While the economy continues to grow at a modest rate, there were some bright spots from our local economy. The September 2015 unemployment rate for Walton County was 4.5% which is 10% below the federal and state unemployment rate.

The beaches of South Walton are an integral part of the local economy generating approximately $568 million in local income annually according to research conducted for the Walton County Tourist Development Council (TDC). Visitors to Walton County are primarily drawn here by our world class beaches and by the abundance of choices in both retail and dining. The number of visitors to our area has continued to increase over the years, tourist development taxes (TDT) collected for 2015 topped the $20 million mark for the first time. This was achieved despite the fact that the tax rate dropped 11.1% to 4% on October 1, 2014. The increase in collections can be attributed to aggressive marketing of the destination by the TDC and an increase in enforcement activities by the office of the Walton County Clerk of Courts. We expect TDT collections in 2016 to be slightly higher as the economy continues to improve and fuel prices remain low.

In the last decade, the real estate market has been our hardest hit sector. However, there are signs that real estate market has begun to stabilize. Real property values dropped 0.05% in 2012, increased 4.86% in 2013, increased 9.51% in 2014, and increased 11.72% in 2015. Overall, real property values have decreased 14.12% in the last ten years. We expect an increase in 2016 as the economy begins to level off and home inventories begin to move. The biggest concern for our citizenry in recent times has been the rate of foreclosure. Over the last year, foreclosure case filings in Walton County dropped by 34% from 2015. We anticipate an increase in 2016.

Long-term financial planning. Walton County has obtained 315 acres of land in the Mossy Head area that is in a prime location that bordering Interstate 10 to the south and State Road 285 and US Highway 90 to the north. Additionally, the CSX rail line has a main track which runs along the entire northern boundary. The site has sufficient land to accommodate larger operations which few sites within a fifty mile radius have available. The intended use of this property has been to develop a mixed-use commercial/industrial park and to supply employment opportunities for the substantial population growth that is predicted for the northern part of the county. Specific businesses that will be targeted include manufacturing and distribution, and research and development companies.

In 2014, Love’s Truck Stops became the first company to purchase and open a business in the Mossy Head Industrial Park. Subsequently, several other business have invested in the property at the site including Brigman Properties, Empire Truck Service and Sales, and Southern Tire Mart. Walton County will continue to target specific businesses to include manufacturing and distribution, and research and development companies.

Full development of the commerce park cannot occur without sufficient facilities to treat and dispose/reuse the wastewater generated by the occupants. In fiscal year 2014, a project was completed connecting an underutilized package plant at the Dixie RV Superstore, southwest of the Industrial Park, to the underutilized package plant at the Mossy Head School, northeast of the Park. Water and wastewater infrastructure traverses the Park and allows for wastewater flows to be shifted back and forth between the two package plants providing additional capacity and allow current and prospective tenants to access water and wastewater infrastructure up to a certain capacity.

In 2014, the State of Florida approved a budget appropriation that will greatly benefit the marketability of the Industrial Park. The $3 million was appropriated for infrastructure costs at the site including roadway infrastructure and associated storm-water management facilities,

4

expansion of water and wastewater infrastructure, underground utilities for the site, and a landscaped entrance area into the Park. Additionally, a 250,000 gallon per day packaged concrete wastewater treatment facility was constructed at the park. As the current wastewater system reaches capacity, the new facility will allow Walton County to link Mossy Head Industrial Park to the existing water sewer system and serve the Mossy Head Industrial Park, Mossy Head Elementary School, residential areas and commercial facilities in the Mossy Head area.

Ultimately, development of this park will diversify the County’s economic base from the tourism oriented jobs in the southern part of the county and provide employment opportunities that will improve the standard of living for all residents of Walton County.

Relevant financial policies. For fiscal year 2015 (2014 millage rate), the Walton County Board of County Commissioners (Board) adopted a budget that showed no increase in the general county millage rate. The Board’s adopted millage rate of 3.556 mills is a decrease of 28.35% from the 2004 general county millage rate.

The Board moved quickly to control spending during the 2015 budgeting process due to a slight increase in projected revenues. Several departments are still being looked at for consolidation and a hiring freeze continues from past years on a limited basis. Additionally, merit increases were eliminated. The 2016 budget will continue the trend of past budgets with minimal growth projected in both revenues and expenses.

The Walton County Investment Committee monitors the County’s investment portfolio in accordance with the County’s written investment policy. Investment earnings are used to offset any projected revenue shortfalls in the budget. In 2015, Walton County’s investment portfolio had a rate of return of 0.54%.

In 2012, the State of Florida Department of Transportation (FLDOT) offered Walton County $102 million if the County contributed $75 million for the four-laning of the Clyde B. Wells Bridge on US Highway 331. Additionally, the FLDOT agreed to four-lane the rest of US Highway 331 to Interstate 10 if the $75 million match was made. The Board of County Commissioners decided to hold a referendum on increasing the sales tax in Walton County by a half-cent. In May of 2012, the voters of Walton County approved the half-cent sales tax increase. Funding was then secured for the match and the monies were transferred to the State of Florida.

After receiving bids much lower than expected for the bridge construction, the State of Florida refunded $50 million to Walton County. These monies were immediately used to pay down the $75 million loan and the remaining $25 million was refinanced at a much lower rate. In 2015, the State of Florida refunded an additional $7,227,657 which when combined with sales tax collections enabled Walton County to pay off the loan on August 26, 2015. The half-cent sales tax was allowed to sunset on December 31, 2015.

Major initiatives. The four-laning of U.S. Highway 331 has been a priority of the County Commissioners for a number of years. Safety concerns are paramount as this roadway is the only north-south hurricane evacuation route in Southern Walton County. However, due to the high cost of construction, the project will be completed in segments. The first segment expanded U.S. Highway 331 to four lanes between the U.S. Highway 98 intersection and the southern end of the Clyde B. Wells Bridge at Choctawhatchee Bay. Safety and drainage improvements, new sidewalks and bicycle lanes, and new traffic signals were also included in this project. Total cost of this segment of the project was $21 million. Funding for this 2.093 mile segment was provided by the Florida Department of Transportation.

5

Segment two is the construction of a two-lane addition to the Clyde B. Wells Bridge over Choctawhatchee Bay. Construction began in February of 2014 with an estimated completion date of March 2018. Total cost of this segment is projected to be $118 million. Funding for this 2.274 mile addition will be provided by multiple sources. Walton County contributed $17.8 million to this project through a bank financing arrangement and the remaining $100 million will be provided by the Florida Department of Transportation.

Segment three is the construction of two additional lanes from just north of the Clyde B. Wells Bridge to just south of State Road 20. Construction is scheduled to begin this year and should be completed in 2015. Total cost of this segment is projected to be over $100 million which also includes design, right-of-way acquisition and mitigation expenses. Funding for this 4.697 mile segment will be provided by the Florida Department of Transportation.

Segment four totaling 4.961 miles is the construction of two additional lanes from State Road 20 to Owl’s Head Road. The timetable for final construction of this segment has yet to be determined. Funding for this segment will be provided by the Florida Department of Transportation.

Segment five totaling 4.204 miles is the construction of two additional lanes from Owl’s Head Road to Edgewood Circle. This project will be constructed in two phases with the first phase completed in 2013 and the second phase to begin construction in 2014. Total cost of this segment is projected to be over $70 million which also includes design, right-of-way acquisition and mitigation expenses. Walton County was awarded a Local Agency Participation Grant which funded $6.924 million of the construction cost with a local match of $2.672 million. The remaining funding will be provided by the Florida Department of Transportation.

Segment six totaling 4.673 miles is the construction of two additional lanes from Edgewood Circle to Interstate 10. Total cost of this segment is projected to be over $90 million which would include design, right-of way acquisition and mitigation expenses. The timetable for construction of this segment has yet to be determined but funding will be provided by the Florida Department of Transportation.

Due to the widening of U.S. Highway 331, the United Fire station building and property was sold in 2014 to the FLDOT for $500,000. Construction then began on a new fire station located three miles south of the original building on a five acre parcel being sub-let from the FLDOT for $300 per year through 2049. Construction of the new United Fire Station was completed in the spring of 2015. The only building construction planned for 2016 is an 1800 square foot addition to the county administration building slated to be completed in the summer of 2016.

In 2009, the permitting process began on the restoration of the 12.9 mile stretch of beaches at Seagrove, Blue Mountain, Inlet, and Dune Allen. The permitting process for this federal project can take several years to complete and is anticipated to begin in 2016 or 2017. The approximate cost of this restoration is estimated to be between $60 and $70 million. The restoration will be paid for with tourist development taxes and federal and state funds should they become available.

Awards. The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to Walton County, Florida for its comprehensive annual financial report for the fiscal year ended September 30, 2014. This was the fourteenth consecutive year that Walton County has received this prestigious award. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual

6

financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program’s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate.

Acknowledgements. This Comprehensive Annual Financial Report is a result of the tremendous effort and dedication given by the Finance Department of the Clerk of Courts & County Comptroller of Walton County. Your hard work is evident in this report. Thank you!

We would also like to thank the staff of the Office of Management and Budget for their cooperation and assistance during this process.

Finally, we would like to thank the accounting firm of Carr, Riggs & Ingram, LLC and specifically Hilton Galloway and Keith Hundley for their contribution to the publication of this document.

Alex AlfordClerk of Courts & County Comptroller

7

8

Walton County, FloridaOrganizational Chart

Board of County

Commissioners

County Attorney

CountyAdministrator

Deputy County Administrator (Operations)

Public Safety

Probation Emergency Response

Risk Management and Safety

Public Works

Public Works Department Shop/Fleet

Facilities Maintenance Landfill

Environmental Soil Conservation

Mosquito Control

Community Development

Building Planning and Development

CodeCompliance

Parks and Recreation

Deputy County Administrator

(Administration)

Administration and

BCC SupportHR

Public Information Technology

Finance/OMB Purchasing

Grants GIS/IT

Library Extension Services

Discretionary MSBU’s

HUD Veterans

TouristDevelopment

Director

FINANCIAL SECTION

INDEPENDENT AUDITORS’ REPORT

MANAGEMENT’S DISCUSSION AND ANALYSIS

BASIC FINANCIAL STATEMENTS

COMBINING AND INDIVIDUAL FUND STATEMENTS

9

INDEPENDENT AUDITORS' REPORT

Honorable Members of theBoard of County CommissionersWalton County, Florida

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, thediscretely presented component unit, each major fund, the aggregate remaining fund information,and the proprietary and fiduciary fund types of Walton County, Florida (the “County”), as of and forthe year ended September 30, 2015, and the related notes to the financial statements, whichcollectively comprise the County’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statementsin accordance with accounting principles generally accepted in the United States of America; thisincludes the design, implementation, and maintenance of internal control relevant to thepreparation and fair presentation of financial statements that are free from material misstatement,whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States. Those standards require that weplan and perform the audit to obtain reasonable assurance about whether the financial statementsare free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor’s judgment,including the assessment of the risks of material misstatement of the financial statements, whetherdue to fraud or error. In making those risk assessments, the auditor considers internal controlrelevant to the entity’s preparation and fair presentation of the financial statements in order todesign audit procedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we expressno such opinion. An audit also includes evaluating the appropriateness of accounting policies usedand the reasonableness of significant accounting estimates made by management, as well asevaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinions.

10

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, the discretely presented componentunit, each major fund, the aggregate remaining fund information, the proprietary fund type and thefiduciary fund type of the County, as of September 30, 2015 and the respective changes in financialposition and where applicable, cash flows thereof, and the respective budgetary comparison for theGeneral Fund, County Transportation Fund, Fine and Forfeiture Fund, Tourist Development Fundand Solid Waste Landfill Fund thereof for the year then ended in conformity with accountingprinciples generally accepted in the United States of America.

Emphasis of a Matter

Change in Accounting Principle

As discussed in note 1 to the financial statements, the Board adopted the provisions ofGovernmental Accounting Standards Board (GASB) Statement No. 68, Accounting and FinancialReporting for Pensions an amendment to GASB Statement No. 27, GASB Statement No. 69,Government Combinations and Disposals of Government Operations, and GASB Statement No. 71,Pension Transition for Contributions Made Subsequent to the Measurement Date an amendmentof GASB Statements No. 68, during the year ended September 30, 2015. Our opinion is notmodified with respect to these matters.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that themanagement’s discussion and analysis, on pages 12 through 23, post employment benefits planschedule of funding progress on page 85, schedule of employer’s proportionate share of the netpension liability – Florida Retirement Systems Pension Plan, schedule of employer contributions –Florida Retirement Systems Pension Plan, schedule of employer’s proportionate share of the netpension liability – Health Insurance Subsidy Program and schedule of employer contributions –Health Insurance Subsidy Program, on pages 86 through 89, be presented to supplement the basicfinancial statements. Such information, although not a part of the basic financial statements, isrequired by the Governmental Accounting Standards Board, who considers it to be an essential partof financial reporting for placing the basic financial statements in an appropriate operational,economic, or historical context. We have applied certain limited procedures to the requiredsupplementary information in accordance with auditing standards generally accepted in the UnitedStates of America, which consisted of inquiries of management about the methods of preparing theinformation and comparing the information for consistency with management’s responses to ourinquiries, the basic financial statements, and other knowledge we obtained during our audit of thebasic financial statements. We do not express an opinion or provide any assurance on theinformation because the limited procedures do not provide us with sufficient evidence to expressan opinion or provide any assurance.

11

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the County’s basic financial statements. The introductory section, combiningand individual non major fund financial statements and schedules, capital assets used in theoperation of governmental funds schedules and statistical sections are presented for purposes ofadditional analysis and are not a required part of the basic financial statements. The accompanyingschedule of expenditures of federal awards and state financial assistance is presented for purposesof additional analysis as required by the U.S. Office of Management and Budget Circular A 133,Audits of States, Local Governments and Non Profit Organizations, and the Florida Single Audit Act;and the schedule of receipts and expenditures of funds related to the Deepwater Horizon oil spill isrequired by Chapter 10.550, Local Governmental Audits, Rules of the Auditor General of the State ofFlorida, and neither schedule is a required part of the basic financial statements.

The combining and individual nonmajor fund financial statements and schedules, capital assetsused in the operation of governmental funds schedules, the schedule of expenditures of federalawards and state financial assistance, and the schedule of receipts and expenditures of fundsrelated to the Deepwater Horizon oil spill are the responsibility of management and were derivedfrom and relate directly to the underlying accounting and other records used to prepare the basicfinancial statements. Such information has been subjected to the auditing procedures applied in theaudit of the basic financial statements and certain additional procedures, including comparing andreconciling such information directly to the underlying accounting and other records used toprepare the basic financial statements or to the basic financial statements themselves, and otheradditional procedures in accordance with auditing standards generally accepted in the UnitedStates of America. In our opinion, the combining and individual nonmajor fund financial statementsand schedules, capital assets used in the operation of governmental funds schedules, the scheduleof expenditures of federal awards and state financial assistance, and the schedule of receipts andexpenditures of funds related to the Deepwater Horizon oil spill are fairly stated in all materialrespects in relation to the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing proceduresapplied in the audit of the basic financial statements and, accordingly, we do not express an opinionor provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated June 24,2016 on our consideration of the County’s internal control over financial reporting and on our testsof its compliance with certain provisions of laws, regulations, contracts, and grant agreements andother matters. The purpose of that report is to describe the scope of our testing of internal controlover financial reporting and compliance and the results of that testing, and not to provide anopinion on internal control over financial reporting or on compliance. That report is an integral partof an audit performed in accordance with Government Auditing Standards in considering theCounty’s internal control over financial reporting and compliance.

CARR, RIGGS & INGRAM, L.L.C.Certified Public AccountantsJune 24, 2016

12

Management’s Discussion and Analysis

The County’s management discussion and analysis presents an overview of the County’s financialactivities for the two fiscal years ended September 30, 2014 and September 30, 2015. Please readit in conjunction with the Letter of Transmittal, beginning on page 1, and the County’s financialstatements.

Financial Highlights

In fiscal year 2015, Walton County implemented Governmental Accounting Standards BoardStatement 68, “Accounting and Financial Reporting for Pensions.” Accordingly, the 2014amounts presented have been restated, resulting in a decrease in the ending fiscal year2014 net position from governmental activities of $37,086,830.

Walton County’s primary government assets exceeded liabilities (net position) by$254,156,237 for fiscal year 2015 as compared to $215,217,911 for fiscal year 2014, asrestated. Unrestricted net position may be used to meet the County’s ongoing obligationsto citizens and creditors. Walton County’s unrestricted net position at September 30, 2015,amounted to $49,593,608, an increase of $44,253,128.

The County’s total primary government net position for the 2015 fiscal year increased$38,938,326 over fiscal year 2014, as restated.

The County’s governmental funds reported a combined ending fund balance of$120,031,595 at September 30, 2015, an increase of $13,864,161 in comparison with theprior year.

At September 30, 2015, the General Fund balance was $21,883,492 (of which $15,603,519was unassigned), an increase of $1,279,994 from 2014.

The County’s outstanding notes payable and other long term debt decreased by$11,108,501 during fiscal year 2015.

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the County’s basic financialstatements. The County’s basic financial statements consist of government wide financialstatements, fund financial statements, and notes to the financial statements. This report alsocontains additional supplementary information following the basic financial statements themselves.

Government wide Financial Statements

Government wide financial statements, which consist of the Statement of Net Position and theStatement of Activities, are designed to provide readers with a broad overview of the County’sfinances in a manner similar to a private sector business. The Statement of Net Position presentsinformation on the County’s assets plus deferred outflows less its liabilities and deferred inflows atSeptember 30, 2015. The difference between these assets and deferred outflows and liabilities anddeferred inflows is reported as net position. Over time, increases or decreases in net position may

13

serve as a useful indicator of whether the financial position of the County is improving ordeteriorating.

The Statement of Activities presents information showing how the County’s net position changedduring the fiscal year. All changes in net position are reported as soon as the underlying eventgiving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues andexpenses are reported in this statement for some items that will only result in cash flows in futurefiscal periods (such as uncollected taxes or earned but unused vacation leave).

Governmental activities of the County include general government, public safety, physicalenvironment, transportation, economic environment, human services, culture and recreation, andinterest on long term debt.

The government wide financial statements include both the County itself (known as the primarygovernment) and Florida Community Services Corporation, a legally separate component unitformed to acquire and improve existing water distribution facilities in southern Walton County.

The government wide financial statements begin on page 24.

Fund Financial Statements

A fund is a grouping of related accounts used to maintain control over resources that have beensegregated for specific activities or objectives. The County, like other state and local governments,uses fund accounting to ensure and demonstrate compliance with finance related legalrequirements. All funds of the County can be divided into three categories: governmental,proprietary (internal service), and fiduciary funds.

Governmental Funds

Governmental funds account for essentially the same functions reported as governmental activitiesin the government wide financial statements. However, unlike the government wide financialstatements, governmental fund financial statements focus on near term inflows and outflows ofspendable resources, as well as on balances of spendable resources available at the end of the fiscalyear. Such information may be useful in evaluating a government’s near term financingrequirements.

Because the focus of governmental funds is narrower than that of government wide financialstatements, it is useful to compare the information presented for governmental activities in thegovernment wide financial statements. By doing so, readers may better understand the long termimpact of the government’s near term financing decisions. Both the governmental fund balancesheet and the governmental fund statement of revenues, expenditures, and changes in fundbalances provide reconciliation to facilitate this comparison between governmental funds andgovernmental activities.

The County maintains 42 individual governmental funds. Information is presented separately in thegovernmental funds balance sheet and in the governmental funds statement of revenues,expenditures, and changes in fund balances for the General, County Transportation, Fine andForfeiture, Tourist Development Council, Solid Waste Landfill, Debt Service, and Capital Projects

14

funds, all of which are considered to be major funds. Data from the other 35 governmental fundsare combined into a single, aggregated presentation. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements in the supplementaryinformation section of this report.

The County adopts an annual appropriated budget for each of its governmental funds. A budgetarycomparison statement has been provided for the major funds to demonstrate budgetarycompliance.

The government funds financial statements begin on page 27.

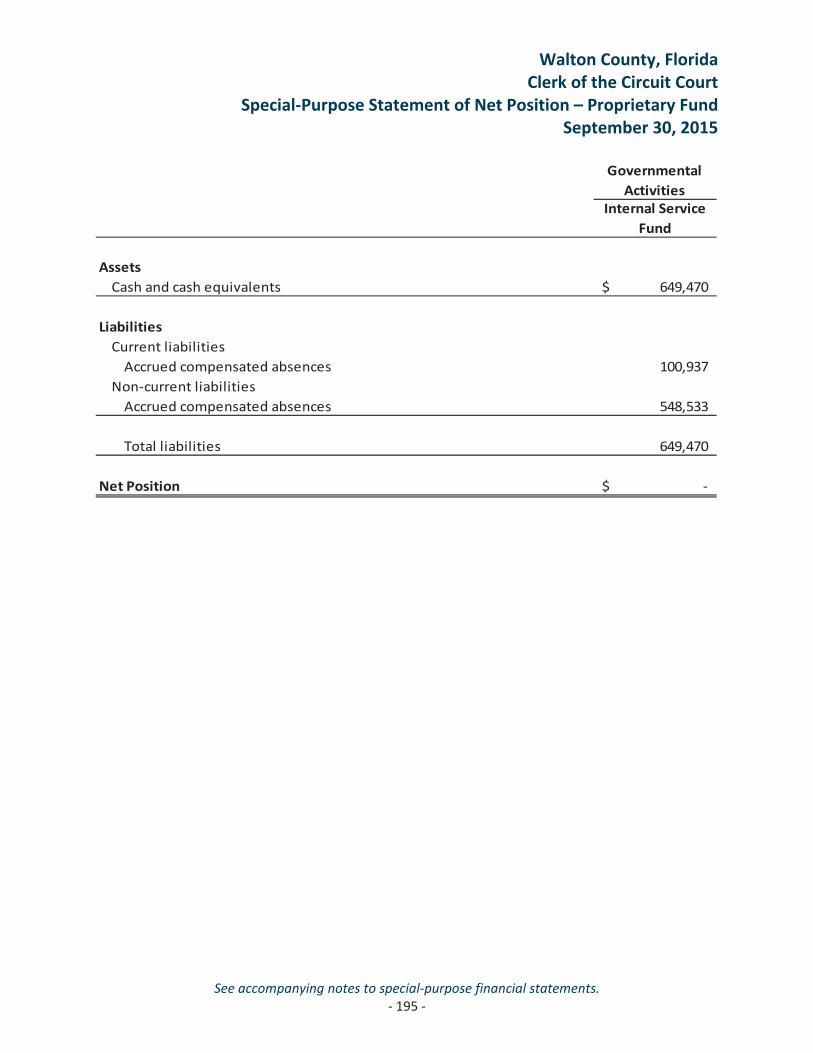

Proprietary Funds

The County maintains and presents one type of proprietary fund, an internal service fund, startingon page 38.

The County uses the internal service fund to report funded and accrued compensated absences.

Fiduciary Funds

Fiduciary funds are used to account for resources held for the benefit of parties outside thegovernment. Fiduciary funds are not included in the government wide financial statementsbecause the resources of these funds are not available to support the County’s own operations.

Notes to the Financial Statements

The notes provide additional information that is essential to a full understanding of the dataprovided in the government wide and fund financial statements. The notes to the financialstatements can be found beginning on page 42 of this report.

Other Information

This report presents certain required supplementary information on pages 85 to 89 concerningWalton County’s progress in funding its obligation to provide pensions and other post employmentbenefits to its employees.

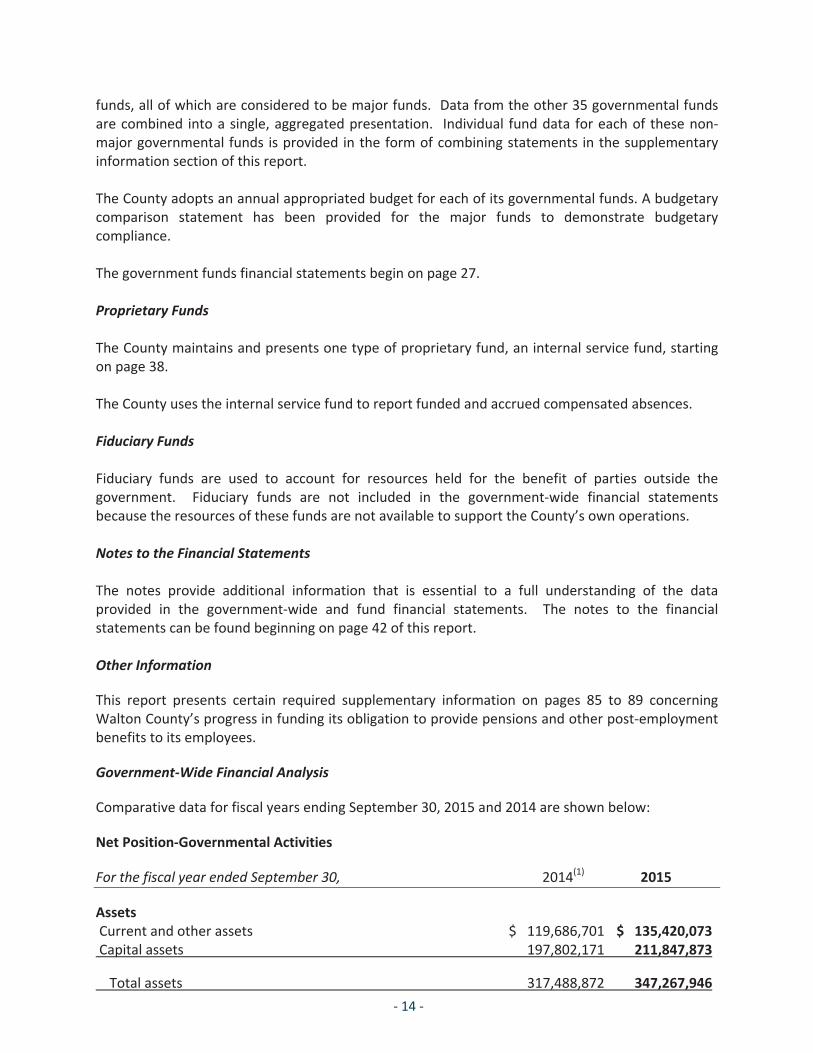

Government Wide Financial Analysis

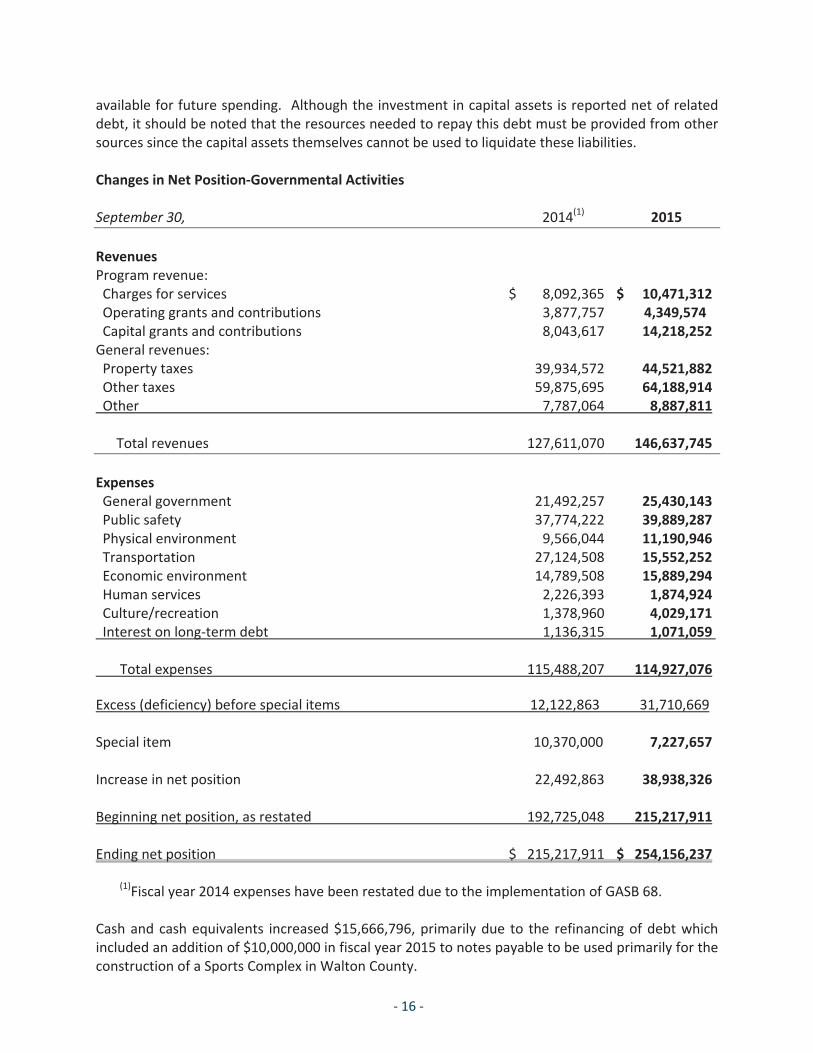

Comparative data for fiscal years ending September 30, 2015 and 2014 are shown below:

Net Position Governmental Activities

For the fiscal year ended September 30, 2014(1) 2015

AssetsCurrent and other assets $ 119,686,701 $ 135,420,073Capital assets 197,802,171 211,847,873

Total assets 317,488,872 347,267,946

15

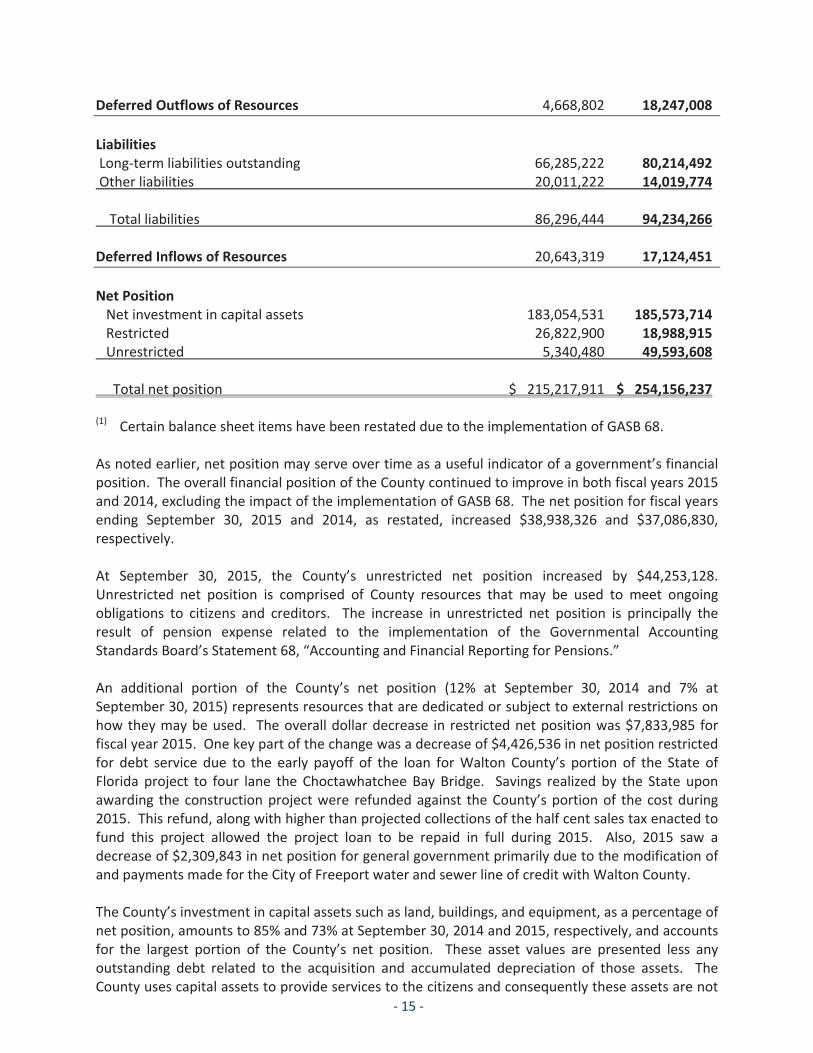

Deferred Outflows of Resources 4,668,802 18,247,008

LiabilitiesLong term liabilities outstanding 66,285,222 80,214,492Other liabilities 20,011,222 14,019,774

Total liabilities 86,296,444 94,234,266

Deferred Inflows of Resources 20,643,319 17,124,451

Net PositionNet investment in capital assets 183,054,531 185,573,714Restricted 26,822,900 18,988,915Unrestricted 5,340,480 49,593,608

Total net position $ 215,217,911 $ 254,156,237

(1) Certain balance sheet items have been restated due to the implementation of GASB 68.

As noted earlier, net position may serve over time as a useful indicator of a government’s financialposition. The overall financial position of the County continued to improve in both fiscal years 2015and 2014, excluding the impact of the implementation of GASB 68. The net position for fiscal yearsending September 30, 2015 and 2014, as restated, increased $38,938,326 and $37,086,830,respectively.

At September 30, 2015, the County’s unrestricted net position increased by $44,253,128.Unrestricted net position is comprised of County resources that may be used to meet ongoingobligations to citizens and creditors. The increase in unrestricted net position is principally theresult of pension expense related to the implementation of the Governmental AccountingStandards Board’s Statement 68, “Accounting and Financial Reporting for Pensions.”

An additional portion of the County’s net position (12% at September 30, 2014 and 7% atSeptember 30, 2015) represents resources that are dedicated or subject to external restrictions onhow they may be used. The overall dollar decrease in restricted net position was $7,833,985 forfiscal year 2015. One key part of the change was a decrease of $4,426,536 in net position restrictedfor debt service due to the early payoff of the loan for Walton County’s portion of the State ofFlorida project to four lane the Choctawhatchee Bay Bridge. Savings realized by the State uponawarding the construction project were refunded against the County’s portion of the cost during2015. This refund, along with higher than projected collections of the half cent sales tax enacted tofund this project allowed the project loan to be repaid in full during 2015. Also, 2015 saw adecrease of $2,309,843 in net position for general government primarily due to the modification ofand payments made for the City of Freeport water and sewer line of credit with Walton County.

The County’s investment in capital assets such as land, buildings, and equipment, as a percentage ofnet position, amounts to 85% and 73% at September 30, 2014 and 2015, respectively, and accountsfor the largest portion of the County’s net position. These asset values are presented less anyoutstanding debt related to the acquisition and accumulated depreciation of those assets. TheCounty uses capital assets to provide services to the citizens and consequently these assets are not

16

available for future spending. Although the investment in capital assets is reported net of relateddebt, it should be noted that the resources needed to repay this debt must be provided from othersources since the capital assets themselves cannot be used to liquidate these liabilities.

Changes in Net Position Governmental Activities

September 30, 2014(1) 2015

RevenuesProgram revenue:Charges for services $ 8,092,365 $ 10,471,312Operating grants and contributions 3,877,757 4,349,574Capital grants and contributions 8,043,617 14,218,252General revenues:Property taxes 39,934,572 44,521,882Other taxes 59,875,695 64,188,914Other 7,787,064 8,887,811

Total revenues 127,611,070 146,637,745

ExpensesGeneral government 21,492,257 25,430,143Public safety 37,774,222 39,889,287Physical environment 9,566,044 11,190,946Transportation 27,124,508 15,552,252Economic environment 14,789,508 15,889,294Human services 2,226,393 1,874,924Culture/recreation 1,378,960 4,029,171Interest on long term debt 1,136,315 1,071,059

Total expenses 115,488,207 114,927,076

Excess (deficiency) before special items 12,122,863 31,710,669

Special item 10,370,000 7,227,657

Increase in net position 22,492,863 38,938,326

Beginning net position, as restated 192,725,048 215,217,911

Ending net position $ 215,217,911 $ 254,156,237

(1)Fiscal year 2014 expenses have been restated due to the implementation of GASB 68.

Cash and cash equivalents increased $15,666,796, primarily due to the refinancing of debt whichincluded an addition of $10,000,000 in fiscal year 2015 to notes payable to be used primarily for theconstruction of a Sports Complex in Walton County.

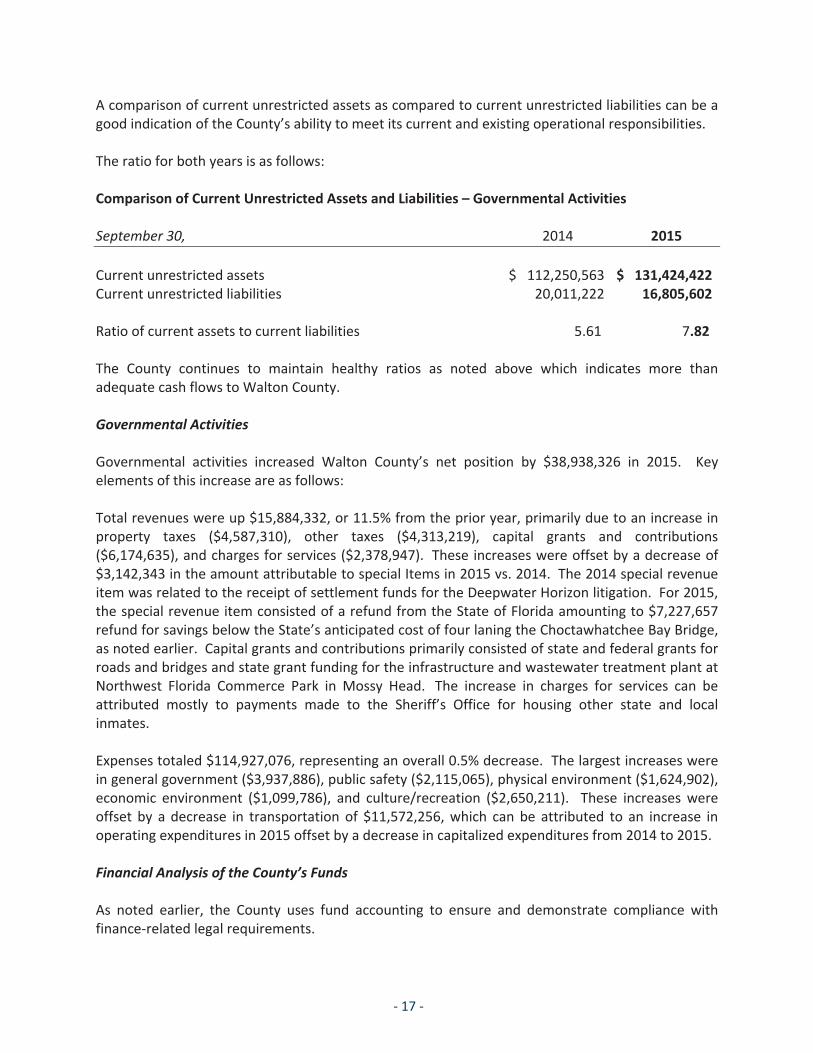

17

A comparison of current unrestricted assets as compared to current unrestricted liabilities can be agood indication of the County’s ability to meet its current and existing operational responsibilities.

The ratio for both years is as follows:

Comparison of Current Unrestricted Assets and Liabilities – Governmental Activities

September 30, 2014 2015

Current unrestricted assets $ 112,250,563 $ 131,424,422Current unrestricted liabilities 20,011,222 16,805,602

Ratio of current assets to current liabilities 5.61 7.82

The County continues to maintain healthy ratios as noted above which indicates more thanadequate cash flows to Walton County.

Governmental Activities

Governmental activities increased Walton County’s net position by $38,938,326 in 2015. Keyelements of this increase are as follows:

Total revenues were up $15,884,332, or 11.5% from the prior year, primarily due to an increase inproperty taxes ($4,587,310), other taxes ($4,313,219), capital grants and contributions($6,174,635), and charges for services ($2,378,947). These increases were offset by a decrease of$3,142,343 in the amount attributable to special Items in 2015 vs. 2014. The 2014 special revenueitem was related to the receipt of settlement funds for the Deepwater Horizon litigation. For 2015,the special revenue item consisted of a refund from the State of Florida amounting to $7,227,657refund for savings below the State’s anticipated cost of four laning the Choctawhatchee Bay Bridge,as noted earlier. Capital grants and contributions primarily consisted of state and federal grants forroads and bridges and state grant funding for the infrastructure and wastewater treatment plant atNorthwest Florida Commerce Park in Mossy Head. The increase in charges for services can beattributed mostly to payments made to the Sheriff’s Office for housing other state and localinmates.

Expenses totaled $114,927,076, representing an overall 0.5% decrease. The largest increases werein general government ($3,937,886), public safety ($2,115,065), physical environment ($1,624,902),economic environment ($1,099,786), and culture/recreation ($2,650,211). These increases wereoffset by a decrease in transportation of $11,572,256, which can be attributed to an increase inoperating expenditures in 2015 offset by a decrease in capitalized expenditures from 2014 to 2015.

Financial Analysis of the County’s Funds

As noted earlier, the County uses fund accounting to ensure and demonstrate compliance withfinance related legal requirements.

18

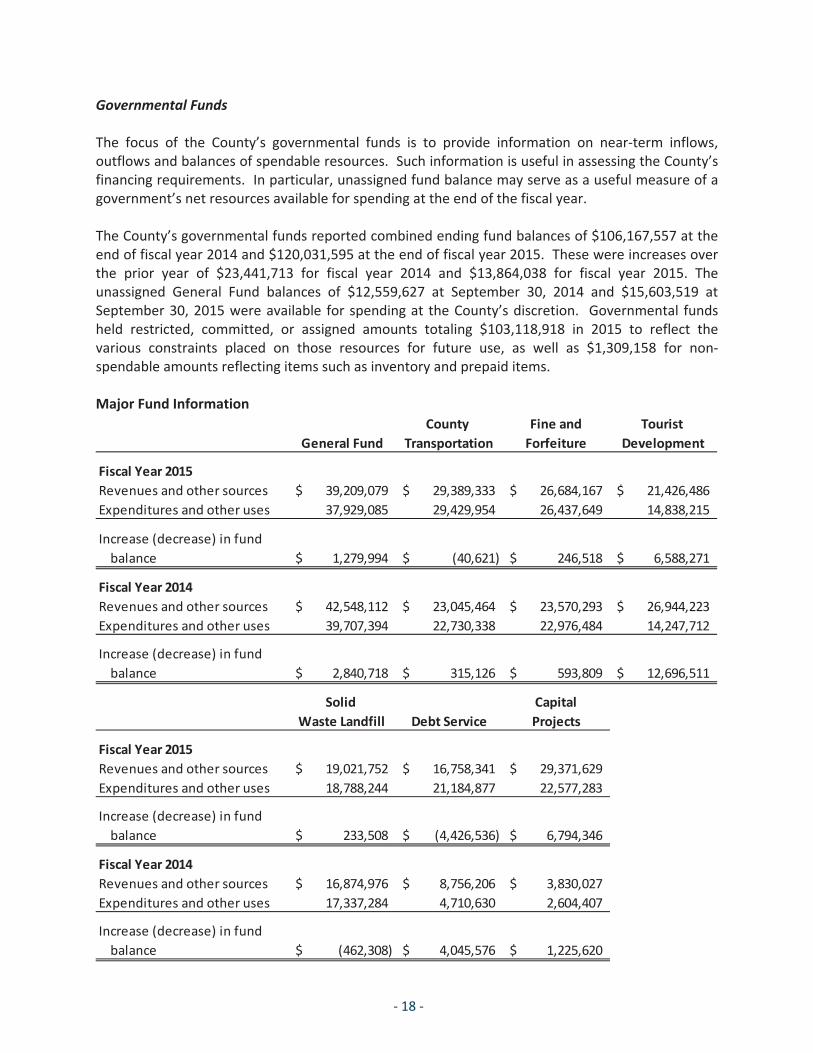

Governmental Funds

The focus of the County’s governmental funds is to provide information on near term inflows,outflows and balances of spendable resources. Such information is useful in assessing the County’sfinancing requirements. In particular, unassigned fund balance may serve as a useful measure of agovernment’s net resources available for spending at the end of the fiscal year.

The County’s governmental funds reported combined ending fund balances of $106,167,557 at theend of fiscal year 2014 and $120,031,595 at the end of fiscal year 2015. These were increases overthe prior year of $23,441,713 for fiscal year 2014 and $13,864,038 for fiscal year 2015. Theunassigned General Fund balances of $12,559,627 at September 30, 2014 and $15,603,519 atSeptember 30, 2015 were available for spending at the County’s discretion. Governmental fundsheld restricted, committed, or assigned amounts totaling $103,118,918 in 2015 to reflect thevarious constraints placed on those resources for future use, as well as $1,309,158 for nonspendable amounts reflecting items such as inventory and prepaid items.

Major Fund InformationCounty Fine and Tourist

General Fund Transportation Forfeiture Development

Fiscal Year 2015Revenues and other sources 39,209,079$ 29,389,333$ 26,684,167$ 21,426,486$Expenditures and other uses 37,929,085 29,429,954 26,437,649 14,838,215

Increase (decrease) in fundbalance 1,279,994$ (40,621)$ 246,518$ 6,588,271$

Fiscal Year 2014Revenues and other sources 42,548,112$ 23,045,464$ 23,570,293$ 26,944,223$Expenditures and other uses 39,707,394 22,730,338 22,976,484 14,247,712

Increase (decrease) in fundbalance 2,840,718$ 315,126$ 593,809$ 12,696,511$

Solid CapitalWaste Landfill Debt Service Projects

Fiscal Year 2015Revenues and other sources 19,021,752$ 16,758,341$ 29,371,629$Expenditures and other uses 18,788,244 21,184,877 22,577,283

Increase (decrease) in fundbalance 233,508$ (4,426,536)$ 6,794,346$

Fiscal Year 2014Revenues and other sources 16,874,976$ 8,756,206$ 3,830,027$Expenditures and other uses 17,337,284 4,710,630 2,604,407

Increase (decrease) in fundbalance (462,308)$ 4,045,576$ 1,225,620$

19

General Fund

The General Fund is the chief operating fund of the County. It accounts for many of the County’score services, such as planning, recreation, library services, and fire rescue services. At September30, 2015, the total fund balance in the General Fund was $21,883,492 of which $15,603,519 wasunassigned. As a measure of the General Fund’s liquidity, it may be useful to compare bothunassigned fund balance and total fund balance to total fund expenditures. Unassigned fundbalance represents 47.40% of total 2015 expenditures, while total fund balance is 66.48% of thesame amount. For fiscal year 2014, unassigned fund balance represented 37.42% of totalexpenditures, while total fund balance was 61.38% of the same amount. The increase in unassignedfund balance to total fund expenditures in fiscal year 2015 can be attributed to an adjustment madeto nonspendable fund balance resulting from the modification and repayment of the City ofFreeport water and sewer line of credit with Walton County.

As detailed in Note 13 to the financial statements, $6,279,973 of the General Fund was nonspendable, restricted, committed, or assigned at September 30, 2015 to reflect prepaid items,inventory, receivables, budget commitments, and judicially controlled funds. At September 30,2014, this amount was $8,043,871. This decrease was primarily due to the adjustment referred toin the previous paragraph which reclassified $1,837,030 in nonspendable fund balance tounassigned upon modification and repayment of the City of Freeport water and sewer line of credit.For fiscal year 2014, $3,913,134 was assigned for use in the General Fund’s 2015 budget and$20,510 assigned for carry forward to complete capital projects. For fiscal year 2015, $2,419,153was assigned for the 2016 budget and $1,871,305 was assigned for carry forward to completecapital projects.

Other Major Governmental Funds

The major governmental funds table also discloses information regarding the other six majorgovernmental funds of the County.

The County Transportation Fund accounts for ad valorem, motor fuel taxes, and various grants tofinance road and bridge construction and maintenance. State statutes govern how these funds areto be used. 2015 saw an increase in intergovernmental revenues from State and Federal grantfunding, funding transferred into the County Transportation Fund from the General Fund to replacemachinery and equipment, and revenues from surplus equipment sales of aging machinery andequipment during the year. These increases were offset by a decrease in Proportionate Fair Sharerevenues recognized during 2015 and unrealized losses on the County Transportation Funds’ shareof long term investments. Operating expenditures increased $6,572,616 during 2015, mostly due towork completed on grant projects during the year and increased expenditures for capital machineryand equipment.

The Fine and Forfeiture Fund accounts for ad valorem, fines and forfeitures, special assessments,and various grants used to finance law enforcement. The increased revenues in fiscal 2015 can beattributed to a higher ad valorem allocation in fiscal year 2015 over 2014 and increased revenuesfrom housing Escambia County inmates following the flooding of the Escambia County Jail CentralBooking and Detention Facility in 2014. Increased expenditures can be attributed to operation andmaintenance of the jail facilities to house the additional inmates, and to the operation of theCorrections and Animal Control departments. During fiscal year 2014, the Corrections and Animal

20

Control Departments transferred from the Board of County Commissioners to the Sheriff’s Office.The increase in 2015 expenditures also reflects the first full year of operations of these twodepartments under the Sheriff’s Office.

The Tourist Development Council (TDC) Fund accounts for the local option tourist development taxarising from activities related to the tourist industry. Its use is governed by State statute forpromotion of the tourism industry and beach maintenance and renourishment. At the end of fiscal2014, the half cent Tourist Development Tax committed for emerging markets was allowed tosunset. The remaining portion of fund balance committed to this initiative will be utilized forcontinued expansion of the target tourism market. Even with this decrease in the tax rate (from4.5% in fiscal year 2014 down to 4% in fiscal year 2015), overall revenues from the TouristDevelopment Tax still increased slightly, reflecting the County’s continued tourism growth.Operating costs increased slightly over fiscal year 2014, resulting in the addition of $6,588,271 tothe TDC’s restricted fund balance. These funds are not available for the County to use for generalgovernment operation.

The Solid Waste Landfill Fund utilizes a one cent small county sales tax to pay for operation of alandfill and provide garbage and yard debris collection to County residences. Revenues from thissales tax increased $1,575,634 for fiscal year 2015 as a result of both overall growth and increasedtourism in the County. Revenues also increased due to a transfer in from the General Fund formachinery and equipment purchases for the Landfill during fiscal year 2015. Expendituresincreased during fiscal year 2015 due to an increase in the purchase of machinery and equipmentduring the year and increased contractual solid waste disposal costs. The balance of the fund isrestricted, committed or assigned to fund remaining costs on capital projects, acquisition of land forlandfill expansion, landfill closure costs, economic development and road paving.

Within the Solid Waste Landfill Fund, deposits are made to the fund’s other cash and cashequivalents account for the purpose of complying with federal and state laws and regulationsrelated to funding the minimum estimated landfill closure and past closure costs. This requires theCounty to annually deposit funds in an interest bearing account for the purpose of funding thesecosts. This amount is shown as a restricted asset within the fund and was $1,152,779 at September30, 2014. This was increased to $1,154,692 at September 30, 2015.

The Debt Service Fund accounts for the ½ cent sales tax enacted to repay the debt incurred for theCounty’s portion of the State of Florida’s construction project to four lane the Choctawhatchee BayBridge. Increased revenues can be attributed to the return of $7,227,657 from the State of Floridarepresenting the return of funds by the State of Florida related to the Choctawhatchee Bay Bridgeconstruction project as previously discussed. The increase in debt service expenditures during 2015can be attributed to the early payoff of the 331 bridge loan during fiscal year 2015, with theremaining fund balance consisting of surplus collections to be utilized for improvements to thebridge and approaches as allowed by the referendum ballot language and County ordinanceenacting the sales tax.

The Capital Projects Fund is used to account for financial resources used for the acquisition orconstruction of major capital facilities, other than those financed by proprietary operations. Theincreased revenues and expenditures in fiscal year 2015 were primarily due to the refinancing ofthe existing Capital Projects Line of Credit and addition of $10,000,000 to the principal amount forthe purchase of property and construction of a Sports Complex in Walton County. Property for

21

this project was purchased and design of the Sports Complex was begun in 2015. The net increasein fund balance primarily represents the remaining funds for construction of the Sports Complex.

General Fund Budgetary Highlights

Differences between the General Fund’s fiscal year 2015 original budget and final amended budgetwere an increase of $1,460,770 to Board of County Commissioner accounts. They can besummarized as follows:

$471,407 rolled forward from fiscal year 2014 for grants and projects not completed in FY 2014$334,524 for new grants and additions to capital projects received in FY 2015$316,530 received from the City of Freeport for remaining FY 15 costs after the transfer ofFreeport Fire Department to Walton County Fire Rescue$43,200 received from Greater Driftwood Estates Homeowners Association, Inc. and DriftwoodEstates Phase II Homeowners Association, Inc. as part of a cost sharing agreement with WaltonCounty for improvements to Driftwood Park$120,000 in unanticipated revenues from an increase in Planning Department fees$145,009 received from the SHIP Housing fund for prior years’ SHIP program administrativefees$10,000 brought forward from Court Innovations reserves for Mortgage Foreclosure casemanagement services$20,000 brought forward from Court Facilities Trust Fund reserves for repairs to the DeFuniakSprings Courthouse air conditioning system$100 received as a donation for the Summer Reading Program

Actual General Fund expenditures were $1,811,326 less than budgeted. The primary components ofthat difference consisted of an $843,702 reduction in personnel costs due to the delayed filling ofvacancies and $674,640 of grants and minor capital projects not completed, and $262,589budgeted but unspent on state mandated health programs.

Actual General Fund revenues were $3,272,920 more than budgeted. Per the Statement ofRevenues, Expenditures and Changes in Fund Balance, taxes received were $502,589 less thanbudgeted. Those taxes consist of Ad Valorem taxes and the Communications Services Tax. Thestatement does not consider the 5% discount ($841,578) allowance included principally for theearly prepayment of ad valorem taxes. When netted against that budgeted allowance, there isactually $338,989 more revenue than budgeted.

Intergovernmental revenues are reported as $1,109,594 greater than budgeted. This is primarilyattributable to the receipt of $878,897 more in Local Government Half Cent Sales Tax revenue and$354,226 more in State of Florida Revenue Sharing distributions than budgeted.

Revenues for Charges for Services were $376,076 greater than budgeted projections. The primaryfactors resulting in this overage were an excess in planning fees amounting to $251,192 overbudget, ambulance fee collections of $87,245 more than the budgeted amount, and fire MSBU feesof $42,100 over the projected budget.

22

Investment Earnings are reported to have been $255,714 short of projections. This primarilyrepresents unrealized losses on the investment of fund balances held throughout 2015.

Miscellaneous revenues exceeded projections by $2,458,465. This mostly consists of a surplus of$959,329 for fees in excess of expenditures returned by the Constitutional Officers, $250,343 insurplus land and equipment sales during fiscal year 2015, and $569,387 from Florida Blue forWalton County’s share of Florida Blue’s prior year health insurance profits on the Walton Countyaccount, and charges for services generated by the Constitutional Offices.

Capital Asset and Debt Administration

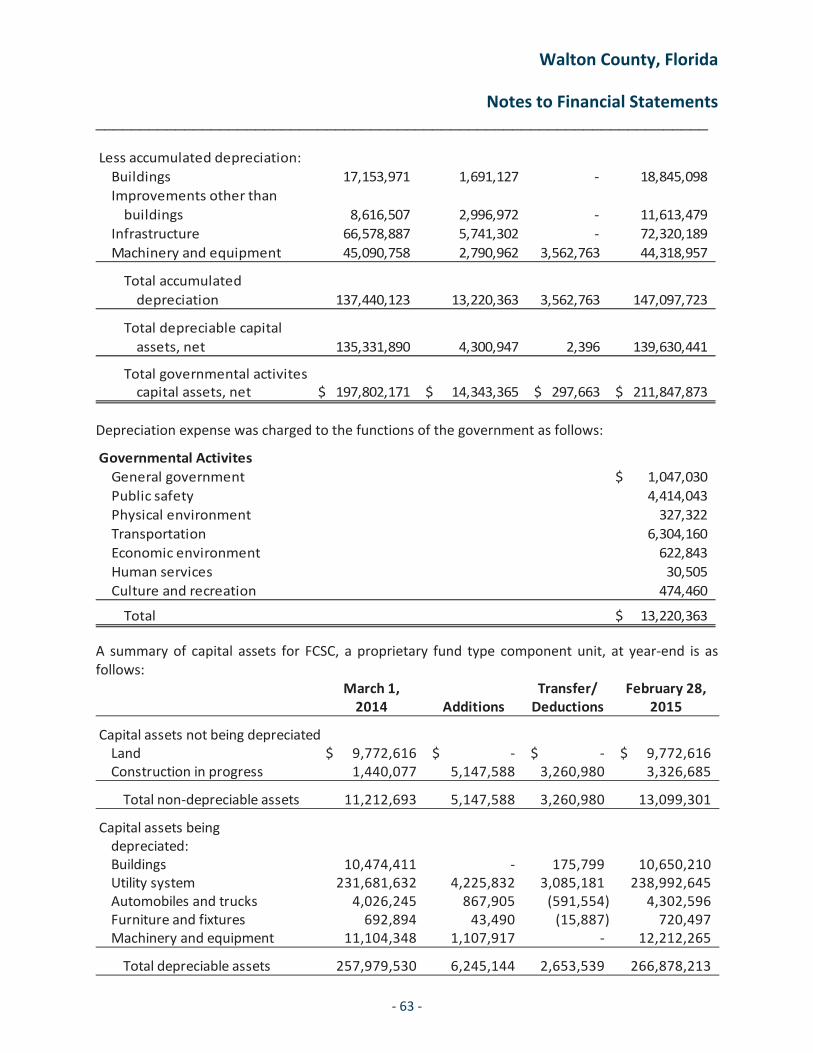

The County’s investment in capital assets for its governmental activities as of September 30, 2014amounted to $197,802,171 (net of accumulated depreciation) and at September 30, 2015amounted to $211,847,873. This investment includes capital assets subject to depreciation, such asinfrastructure, buildings, and equipment as well as capital assets not subject to depreciation such asland and construction in progress. The total increase in the County’s investment in capital assetsfor the current fiscal year was 7%.

The most significant capital asset for the County during fiscal year 2015 was infrastructure, with$2,477,917 added during the current year. Additions primarily consisted of the Mossy HeadWastewater Treatment plant, infrastructure completed at the Northwest Florida Commerce Park,and road paving completed in 2015. Construction in progress at September 30, 2015 consistedmostly of $20,350,053 for road and bridge projects, $247,718 for the Landfill building, and $126,518for a Sheriff’s Substation at the Northwest Florida Commerce Park. The net increase in equipmentof $3,623,919 is reflective of continuing efforts to replace Sheriff’s office vehicles and Public Worksequipment that were delayed for several years during the periods of lower ad valorem and salesand gas tax revenues from 2009 through 2012.

Capital Assets (Net of Depreciation)

September 30, 2014 2015

Land $ 48,448,198 $ 50,947,114Buildings 51,405,601 51,610,673Infrastructure 60,923,745 63,401,662Improvements other than buildings 16,139,897 14,131,540Construction in progress 14,022,083 21,270,318Equipment 6,862,647 10,486,566

Total $ 197,802,171 $ 211,847,873

Additional information on the County’s capital assets can be found in Note 7 on page 62 of thisreport.

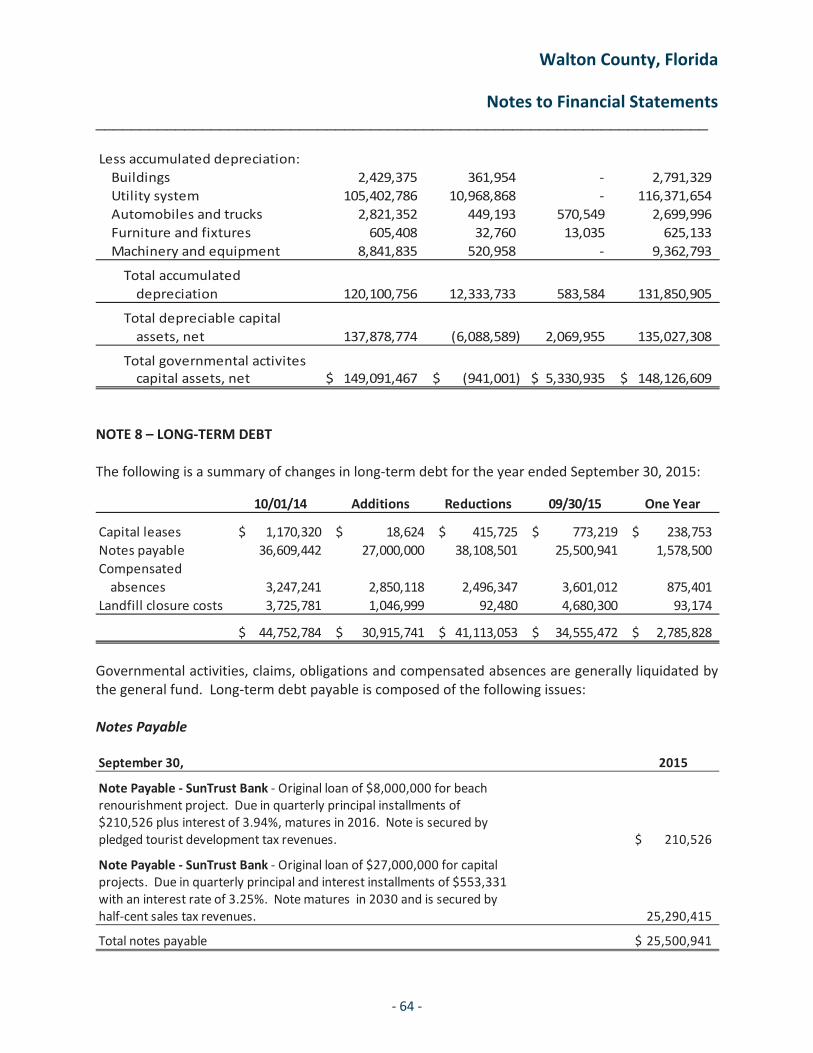

Long Term Debt

As reflected in Note 8 to the financial statements, the County had $25,500,941 in notes payable atSeptember 30, 2015, of which $1,578,500 is due for repayment during fiscal year 2016.

23

September 30, 2014 2015

Notes payableUS 331 Choctawhatchee Bridge Loan $ 20,691,482 $Capital Projects Line of Credit 14,865,329 25,290,415Beach Renourishment Loan 1,052,631 210,526

Total $ 36,609,442 $ 25,500,941

The County’s outstanding notes payable decreased in fiscal year 2015 by $11,108,501, or 30%. Thedecrease was attributable to a combination of two events. First, the capital projects notes wererefinanced to include an additional $10,000,000 in principal for the purchase of property andconstruction of a Sports Complex in Walton County. Second, the Choctawhatchee Bay Bridge loannoted earlier was paid in full during fiscal year 2015. The remaining decreases during the currentyear were attributable to normal debt service principal reductions.

Additional information on the County’s long term debt can be found in Note 8 on page 64 of thisreport.

Economic Factors and Next Year’s Budget and Rates

The unemployment rate for the County at September 30, 2015 was 4.5 percent, slightly up from 3.9percent at September 30, 2014.

Overall building permit activity continued to improve for fiscal year 2015, with 2,324 total permitsissued, including 1,155 residential permits. 2,320 permits, including 1,113 residential, were issuedfor fiscal year 2014. These figures reflect both new housing starts and commercial constructionduring the County’s fiscal year.

Walton County’s population increased 1.5% from the fiscal year ending September 30, 2014, to atotal population of 60,687.

The general ad valorem tax rate for fiscal year 2015 increased to 3.6363 mills. The additional .08mil added in FY 15 was allocated to a Capital Projects fund to be utilized for County wideinfrastructure improvements. The upcoming 2016 fiscal year tax rate remains unchanged at the2015 rate of 3.6363 mills.

Total balance brought forward into the original fiscal year 2014 budget was $10,118,994.$2,710,003 was brought forward in the General Fund and $7,408,991 from all other funds.$12,377,938 was brought forward into the original fiscal year 2015 budget, with $3,885,000brought forward from the General Fund and $8,492,938 from all other funds.

Request for Information

This financial report is designed to present users with a general overview of the County’s financesand to demonstrate the County’s accountability. If you have questions concerning any of theinformation provided in this report or need additional financial information, contact the County’sFinance Director at 176 Montgomery Circle, DeFuniak Springs, Florida 32435, or the FinanceDirector for the Clerk of the Court, P.O. Box 1260, DeFuniak Springs, Florida 32435. Additionalinformation can be found on the County’s web site: http://www.co.walton.fl.us.

Basic Financial Statements

Walton County, FloridaStatement of Net Position

September 30, 2015

See accompanying notes to financial statements.24

PrimaryGovernmentGovernmental ComponentActivities Unit

AssetsCurrent assets

Cash and cash equivalents 63,122,119$ 11,702,857$Cash designated for construction 15,864,882Investments 53,020,170 15,006,053Accounts receivable, net 2,241,811 1,919,233Accounts receivable developer agreements, net 709,724Due from other governments 12,231,968Inventory 638,028 3,347,364Prepaid items 170,326 19,238Restricted assets:Cash and cash equivalents 2,582,450Assessments receivable 899,772

Total current assets 134,906,644 48,569,351

Noncurrent assetsRestricted cashDebt service fund 5,186,245Renewal and replacement fund 922,829Customer's deposits 1,674,958

Accounts receivable developer agreements, net 567,779Loans receivable 513,429Deposits 11,330Land and other nondepreciable assets 72,217,432 13,099,301Capital assets, net of depreciation 139,630,441 135,027,308

Total noncurrent assets 212,361,302 156,489,750

Total assets 347,267,946 205,059,101

Deferred Outflows of ResourcesDeferred outflows related to pension 18,247,008Deferred losses on debt refundings 302,513

Total deferred outflows of resources 18,247,008 302,513

Continued

Walton County, FloridaStatement of Net Position Continued

September 30, 2015

See accompanying notes to financial statements.25

Primary GovernmentGovernmental ComponentActivities Unit

LiabilitiesCurrent liabilities

Accounts payable 5,537,331$ 125,956$Accrued liabilities 2,621,422 107,284Accrued interest payable 210,051Due to other governments 1,574,094Due to individuals 41,069Deposits 2,393,309Unearned revenue 1,642,498Landfill closure costs 93,174Compensated absences 875,401Payable from restricted assets:Accrued interest payable 578,935Bonds payable 1,647,000

Capital lease obligations 238,753Notes payable 1,578,500Total current liabilities 16,805,602 2,459,175

Noncurrent liabilitiesCustomer deposits 1,674,958Notes payable 23,922,441Capital lease obligations 534,466Bonds payable 29,999,445Obligation for deferred compensation 589,817Net pension liability 35,960,020Other post employment benefit obligation 9,699,000Landfill closure cost 4,587,126Compensated absences 2,725,611 204,739Total noncurrent liabilities 77,428,664 32,468,959

Total liabilities 94,234,266 34,928,134Deferred Inflows of ResourcesDeferred inflows related to pension 17,124,451

Net PositionNet investment in capital assets 185,573,714 116,782,675Restricted for:Debt service 3,531,053 6,109,074Capital projects 2,044,676General government 1,664,480Public safety 2,133,933Transportation 8,646,500Economic environment 586,004Human services 382,269

Unrestricted 49,593,608 47,541,731

Total net position 254,156,237$ 170,433,480$

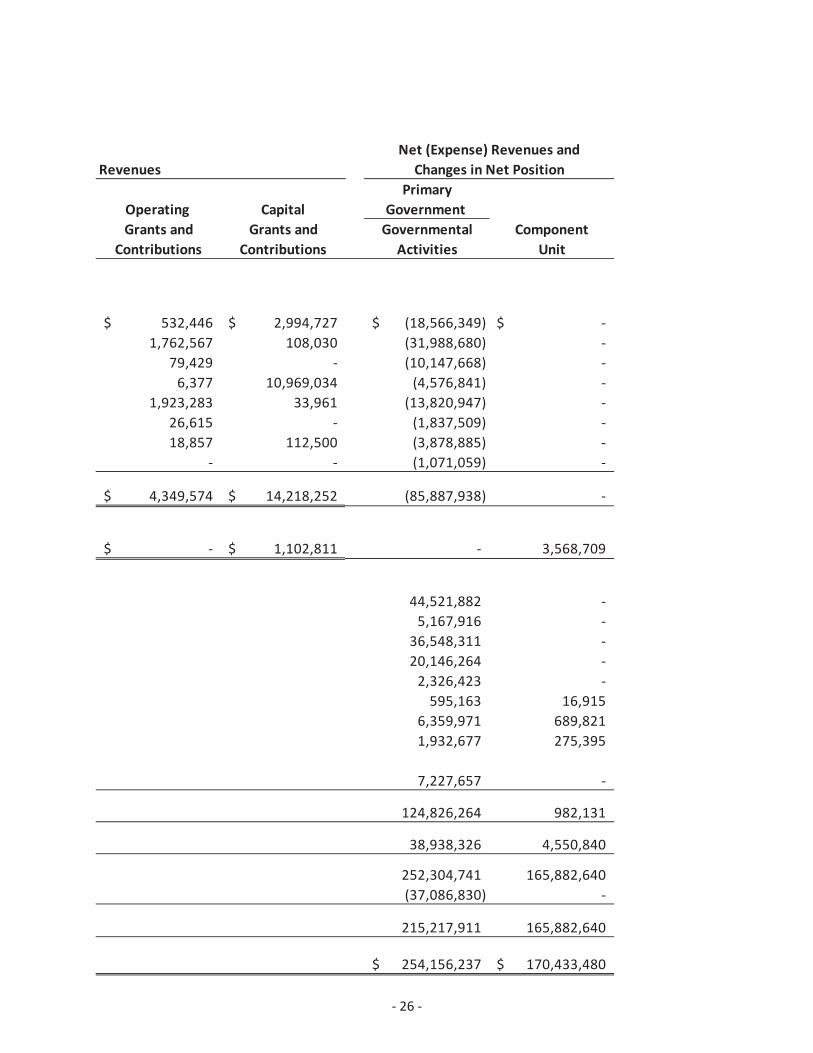

Walton County, FloridaStatement of Activities

For the Year Ended September 30, 2015

See accompanying notes to financial statements.

Program

Chargesfor

Functions/Programs Expenses Services

Primary GovernmentGovernmental Activities:General government 25,430,143$ 3,336,621$Public safety 39,889,287 6,030,010Physical environment 11,190,946 963,849Transportation 15,552,252Economic environment 15,889,294 111,103Human services 1,874,924 10,800Culture/recreation 4,029,171 18,929Interest on long term debt 1,071,059

Total primary government 114,927,076$ 10,471,312$

Component UnitFlorida Community Services Corporation 22,160,028$ 24,625,926$

General RevenuesProperty taxesGasoline taxesSales taxTourist development taxOther taxesInvestment earnings (losses)MiscellaneousGain on disposition of equipment

Special ItemContractual obligation State of Florida

Total general revenues

Change in net position

Total Net Position beginningPrior period adjustment

Net Position beginning, as restated

Total Net Position ending

26

PrimaryOperating Capital GovernmentGrants and Grants and Governmental Component

Contributions Contributions Activities Unit

532,446$ 2,994,727$ (18,566,349)$ $1,762,567 108,030 (31,988,680)

79,429 (10,147,668)6,377 10,969,034 (4,576,841)

1,923,283 33,961 (13,820,947)26,615 (1,837,509)18,857 112,500 (3,878,885)

(1,071,059)

4,349,574$ 14,218,252$ (85,887,938)

$ 1,102,811$ 3,568,709

44,521,8825,167,916

36,548,31120,146,2642,326,423595,163 16,915

6,359,971 689,8211,932,677 275,395

7,227,657

124,826,264 982,131

38,938,326 4,550,840

252,304,741 165,882,640(37,086,830)

215,217,911 165,882,640

254,156,237$ 170,433,480$

Net (Expense) Revenues andChanges in Net PositionRevenues

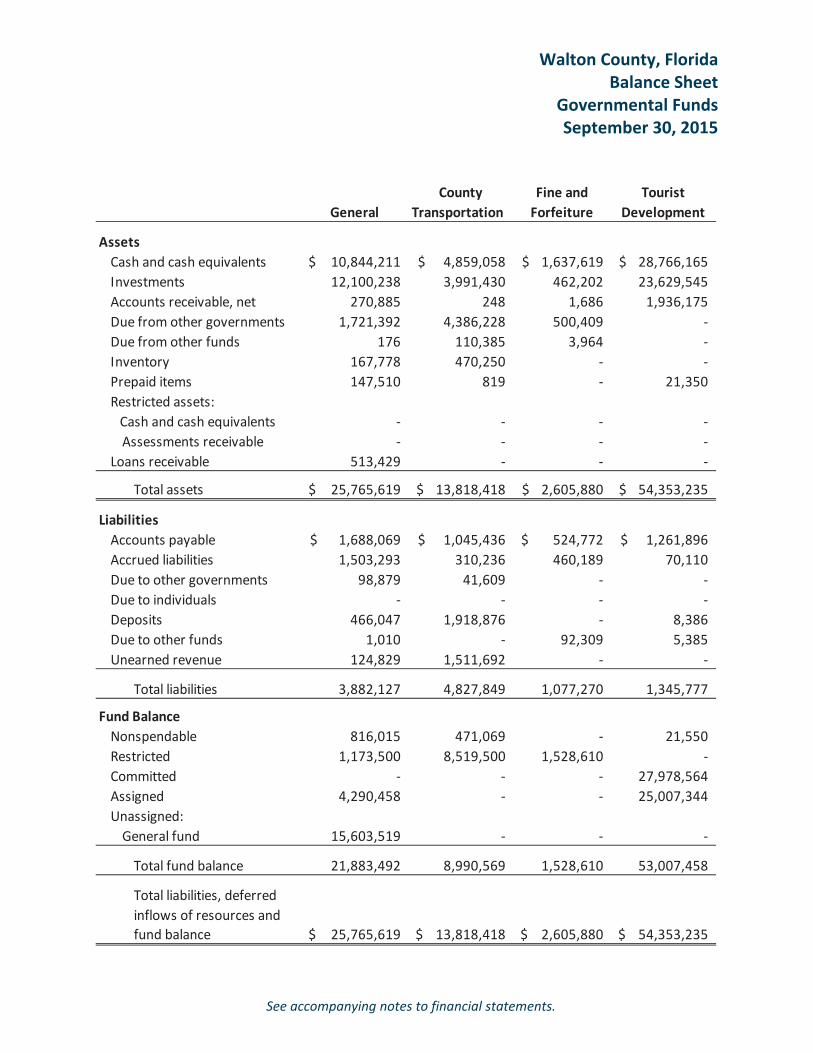

Walton County, FloridaBalance Sheet

Governmental FundsSeptember 30, 2015

See accompanying notes to financial statements.

County Fine and TouristGeneral Transportation Forfeiture Development

AssetsCash and cash equivalents 10,844,211$ 4,859,058$ 1,637,619$ 28,766,165$Investments 12,100,238 3,991,430 462,202 23,629,545Accounts receivable, net 270,885 248 1,686 1,936,175Due from other governments 1,721,392 4,386,228 500,409Due from other funds 176 110,385 3,964Inventory 167,778 470,250Prepaid items 147,510 819 21,350Restricted assets:Cash and cash equivalentsAssessments receivable

Loans receivable 513,429

Total assets 25,765,619$ 13,818,418$ 2,605,880$ 54,353,235$

LiabilitiesAccounts payable 1,688,069$ 1,045,436$ 524,772$ 1,261,896$Accrued liabilities 1,503,293 310,236 460,189 70,110Due to other governments 98,879 41,609Due to individualsDeposits 466,047 1,918,876 8,386Due to other funds 1,010 92,309 5,385Unearned revenue 124,829 1,511,692

Total liabilities 3,882,127 4,827,849 1,077,270 1,345,777

Fund BalanceNonspendable 816,015 471,069 21,550Restricted 1,173,500 8,519,500 1,528,610Committed 27,978,564Assigned 4,290,458 25,007,344Unassigned:General fund 15,603,519

Total fund balance 21,883,492 8,990,569 1,528,610 53,007,458

Total liabilities, deferredinflows of resources andfund balance 25,765,619$ 13,818,418$ 2,605,880$ 54,353,235$

27

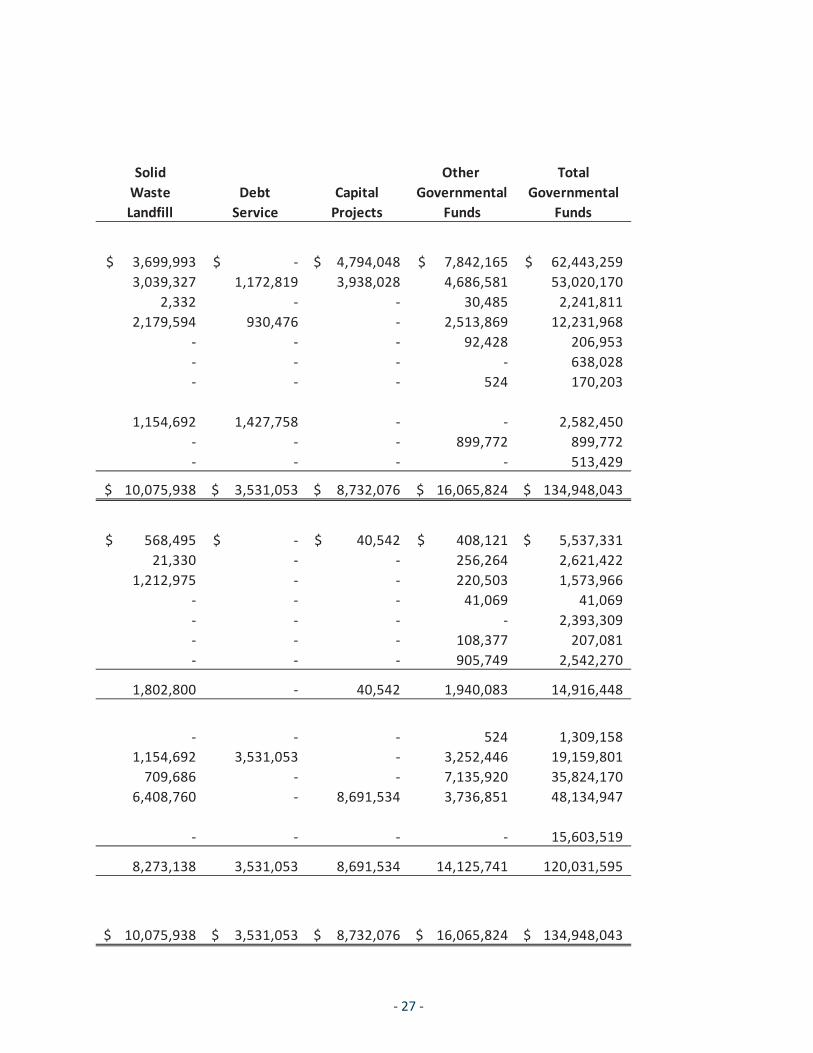

Solid Other TotalWaste Debt Capital Governmental GovernmentalLandfill Service Projects Funds Funds

3,699,993$ $ 4,794,048$ 7,842,165$ 62,443,259$3,039,327 1,172,819 3,938,028 4,686,581 53,020,170

2,332 30,485 2,241,8112,179,594 930,476 2,513,869 12,231,968

92,428 206,953638,028

524 170,203

1,154,692 1,427,758 2,582,450899,772 899,772

513,429

10,075,938$ 3,531,053$ 8,732,076$ 16,065,824$ 134,948,043$

568,495$ $ 40,542$ 408,121$ 5,537,331$21,330 256,264 2,621,422

1,212,975 220,503 1,573,96641,069 41,069

2,393,309108,377 207,081905,749 2,542,270

1,802,800 40,542 1,940,083 14,916,448

524 1,309,1581,154,692 3,531,053 3,252,446 19,159,801709,686 7,135,920 35,824,170

6,408,760 8,691,534 3,736,851 48,134,947

15,603,519

8,273,138 3,531,053 8,691,534 14,125,741 120,031,595

10,075,938$ 3,531,053$ 8,732,076$ 16,065,824$ 134,948,043$

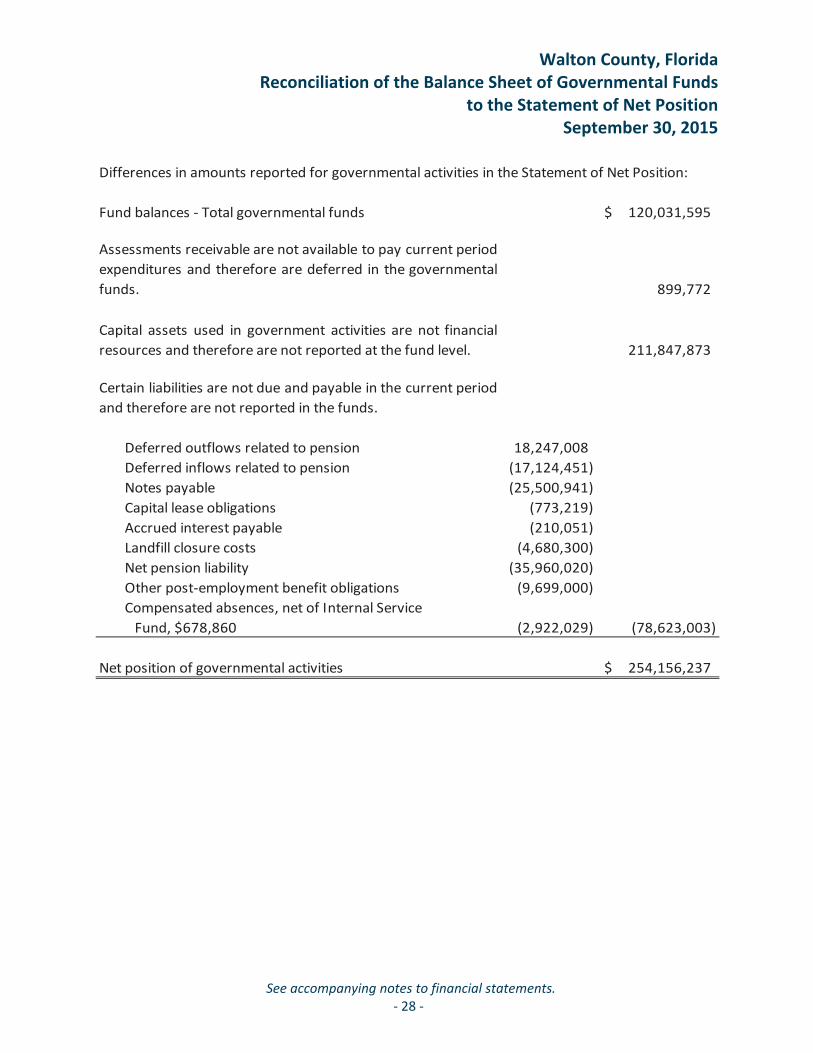

Walton County, FloridaReconciliation of the Balance Sheet of Governmental Funds

to the Statement of Net PositionSeptember 30, 2015

See accompanying notes to financial statements.28

Differences in amounts reported for governmental activities in the Statement of Net Position:

Fund balances Total governmental funds 120,031,595$

899,772

211,847,873

Deferred outflows related to pension 18,247,008Deferred inflows related to pension (17,124,451)Notes payable (25,500,941)Capital lease obligations (773,219)Accrued interest payable (210,051)Landfill closure costs (4,680,300)Net pension liability (35,960,020)Other post employment benefit obligations (9,699,000)

(2,922,029) (78,623,003)

Net position of governmental activities 254,156,237$