warrants and convertibles 1 francesca cornelli fall 1999 [email protected]

TRANSCRIPT

Warrants and Convertibles2

OUTLINE

Warrants: how to value a warrant

Convertible Bonds: Main features How to value a convertible bond Why issue convertible bonds?

Warrants and Convertibles3

WARRANTS

Warrants are similar to standard traded call options. The holder has the right to buy stock at the exercise price on or before the maturity date. There are, however, important differences.

When a warrant is issued, the purchase price is received by the company

When a warrant is exercised, the exercise price is received by the company

When a warrant is exercised, new shares are issued by the company.

Warrants and Convertibles4

VALUING WARRANTS

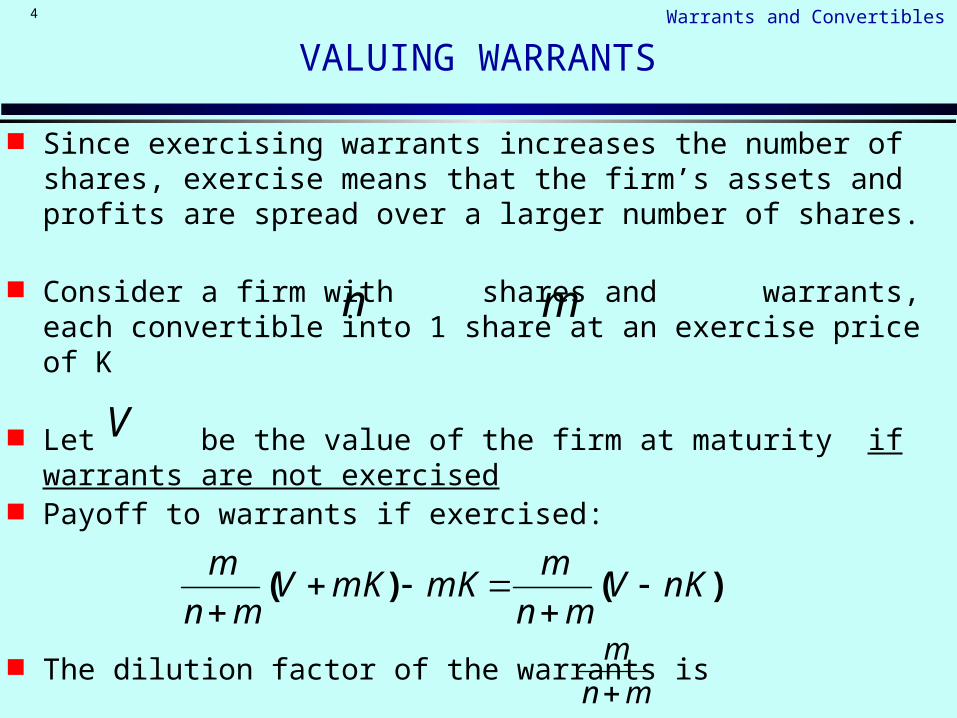

Since exercising warrants increases the number of shares, exercise means that the firm’s assets and profits are spread over a larger number of shares.

Consider a firm with shares and warrants, each convertible into 1 share at an exercise price of K

Let be the value of the firm at maturity if warrants are not exercised

Payoff to warrants if exercised:

The dilution factor of the warrants is

n m

V

)()( nKVmn

mmKmKV

mn

m

mn

m

Warrants and Convertibles5

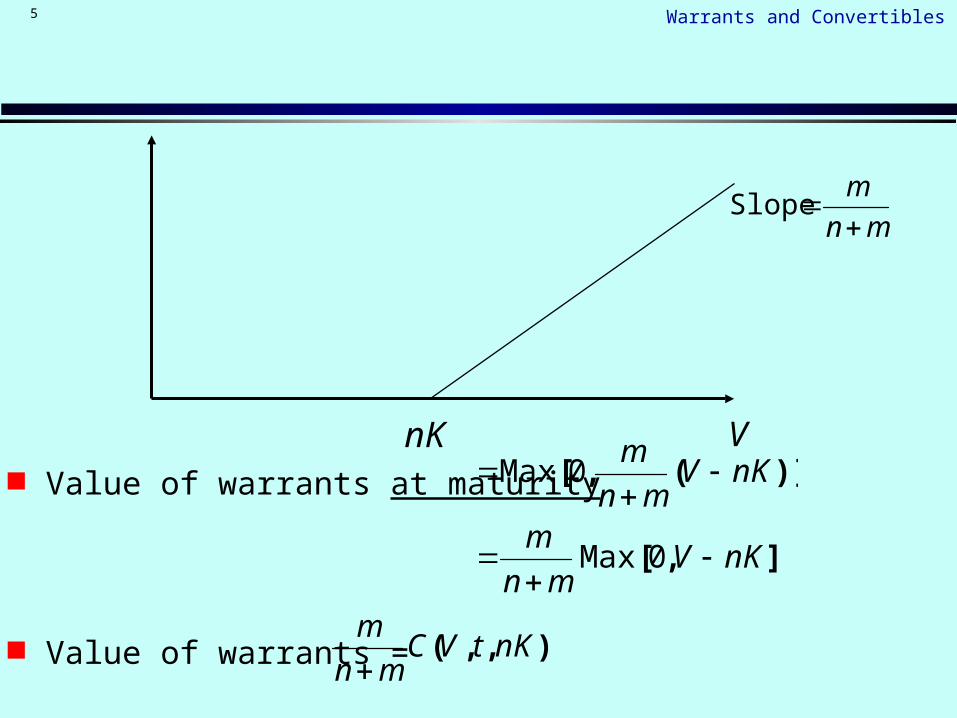

VnK

mn

m

Slope

Value of warrants at maturity

Value of warrants =

],[

)](,[

nKVmn

m

nKVmn

m

0Max

0Max

),,( nKtVCmn

m

Warrants and Convertibles6

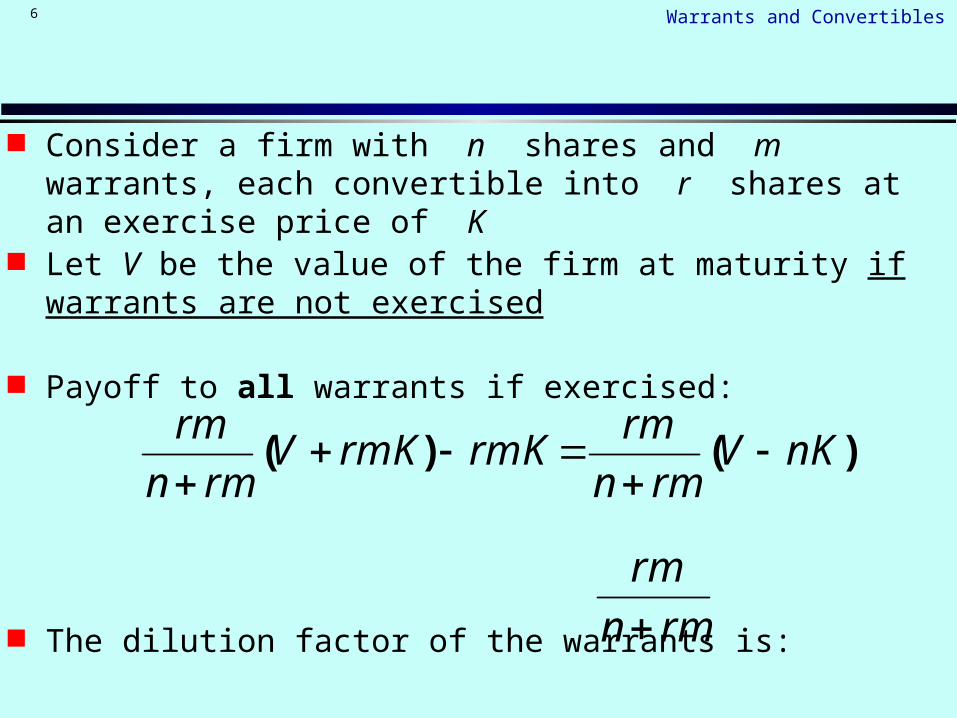

Consider a firm with n shares and m warrants, each convertible into r shares at an exercise price of K

Let V be the value of the firm at maturity if warrants are not exercised

Payoff to all warrants if exercised:

The dilution factor of the warrants is:

)()( nKVrmn

rmrmKrmKV

rmn

rm

rmn

rm

Warrants and Convertibles7

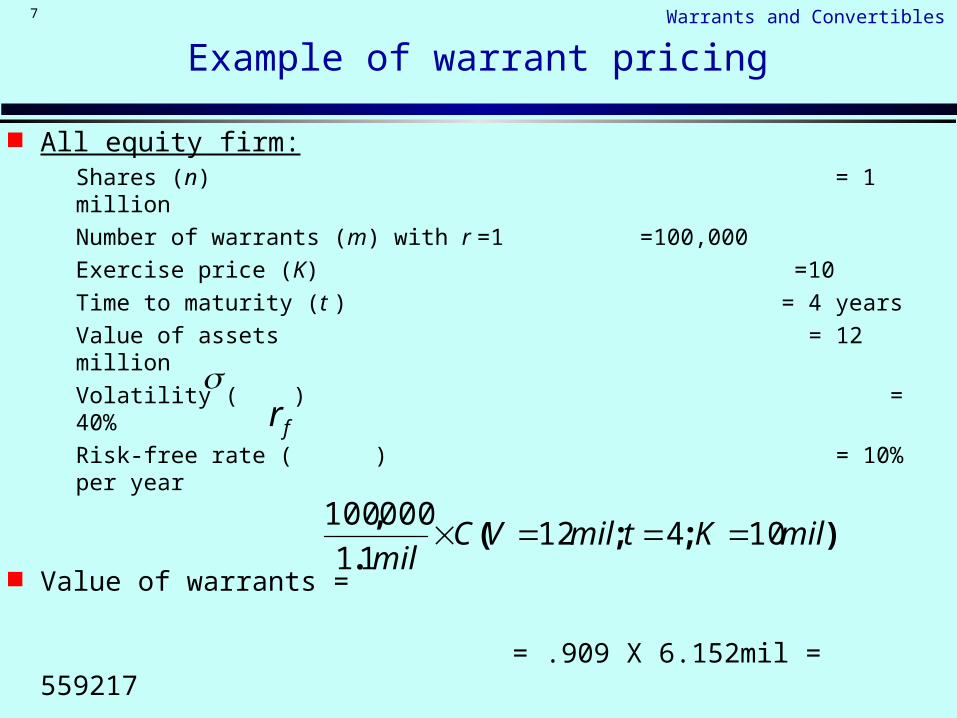

Example of warrant pricing

All equity firm: Shares (n) = 1 million Number of warrants (m) with r =1 =100,000 Exercise price (K) =10 Time to maturity (t ) = 4 years Value of assets = 12 million Volatility ( ) = 40% Risk-free rate ( ) = 10% per year

Value of warrants =

= .909 X 6.152mil = 559217

fr

);;(.

,milKtmilVC

mil10412

11

000100

Warrants and Convertibles8

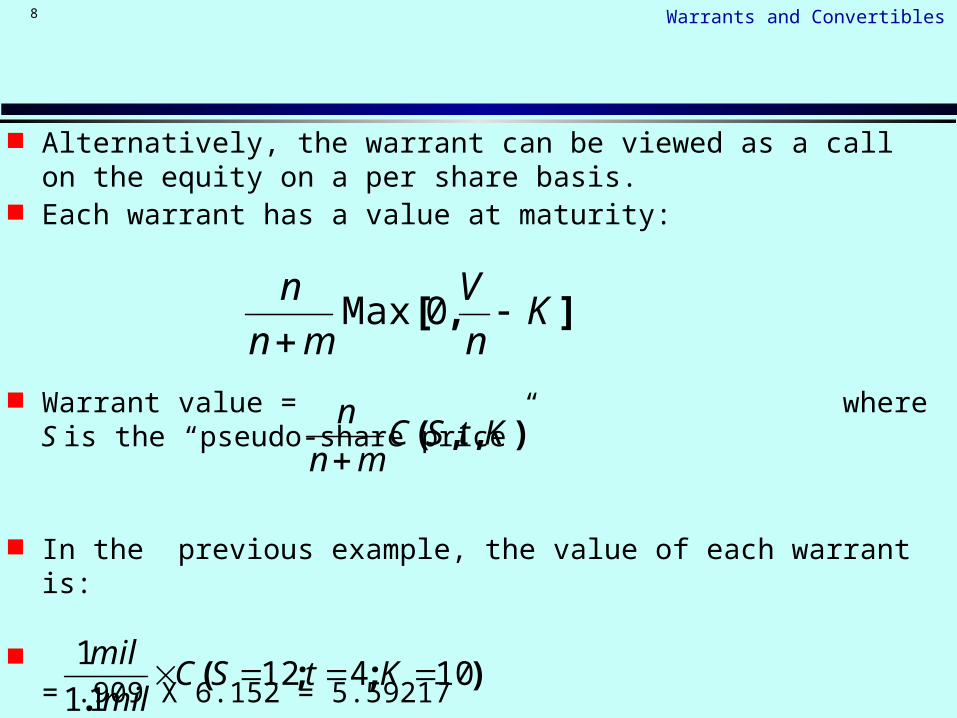

Alternatively, the warrant can be viewed as a call on the equity on a per share basis.

Each warrant has a value at maturity:

Warrant value = where S is the “pseudo-share price”

In the previous example, the value of each warrant is:

= .909 X 6.152 = 5.59217

],[ Kn

V

mn

n

0Max

),,( KtSCmn

n

);;(.

1041211

1 KtSC

mil

mil

Warrants and Convertibles9

CONVERTIBLE BONDS

Convertible bonds are bonds that can be converted into a specified number of shares at the bondholder discretion

A convertible bond is a package of an ordinary bond and a warrant

Warrants and Convertibles10

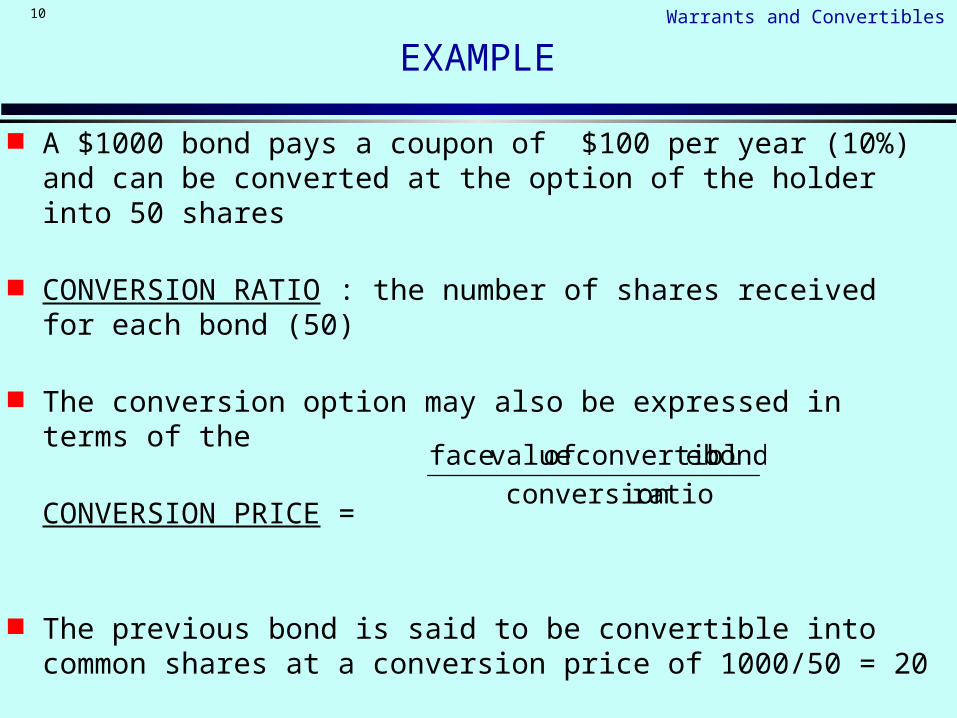

EXAMPLE

A $1000 bond pays a coupon of $100 per year (10%) and can be converted at the option of the holder into 50 shares

CONVERSION RATIO : the number of shares received for each bond (50)

The conversion option may also be expressed in terms of the

CONVERSION PRICE =

The previous bond is said to be convertible into common shares at a conversion price of 1000/50 = 20

ratio conversion

bond econvertibl of valueface

Warrants and Convertibles11

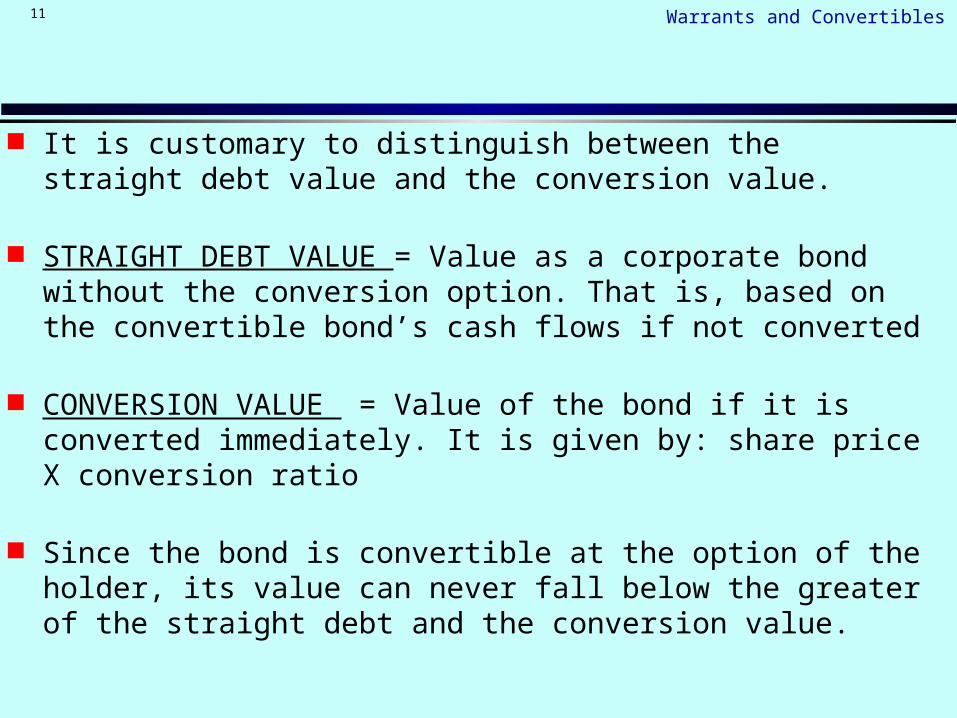

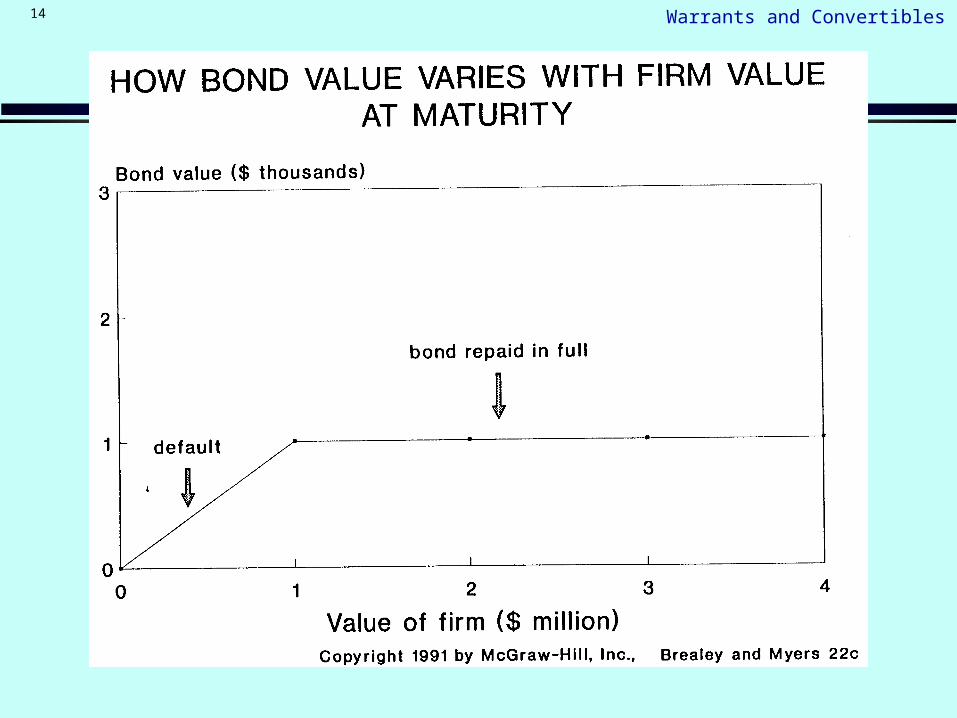

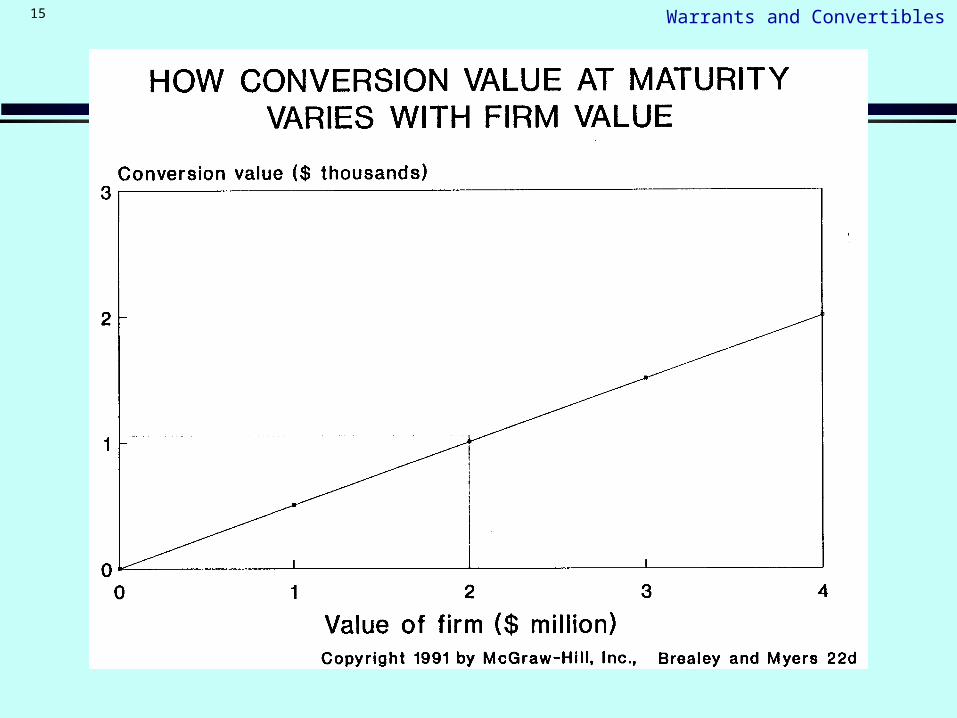

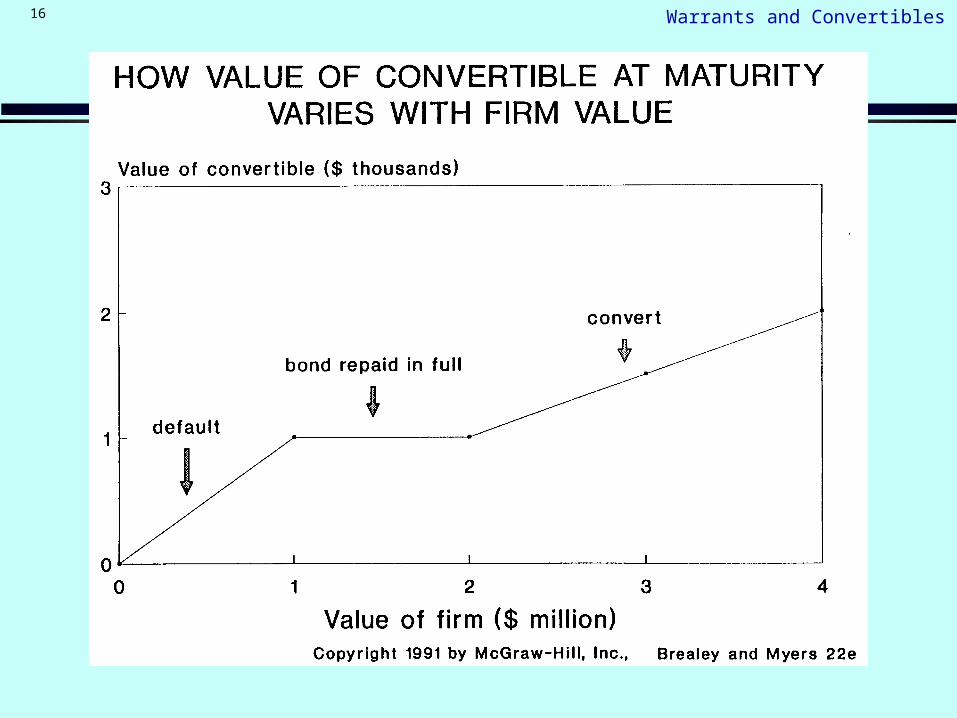

It is customary to distinguish between the straight debt value and the conversion value.

STRAIGHT DEBT VALUE = Value as a corporate bond without the conversion option. That is, based on the convertible bond’s cash flows if not converted

CONVERSION VALUE = Value of the bond if it is converted immediately. It is given by: share price X conversion ratio

Since the bond is convertible at the option of the holder, its value can never fall below the greater of the straight debt and the conversion value.

Warrants and Convertibles12

EXAMPLE

XYZ Convertible Bond

Maturity = 10 years Coupon rate = 10% Conversion ratio = 50 Face value = 1000

Current market price of XYZ convertible bond = $950 Current market price of XYZ stock = $17

Conversion price = Conversion value =

20501000 /8501750

Warrants and Convertibles13

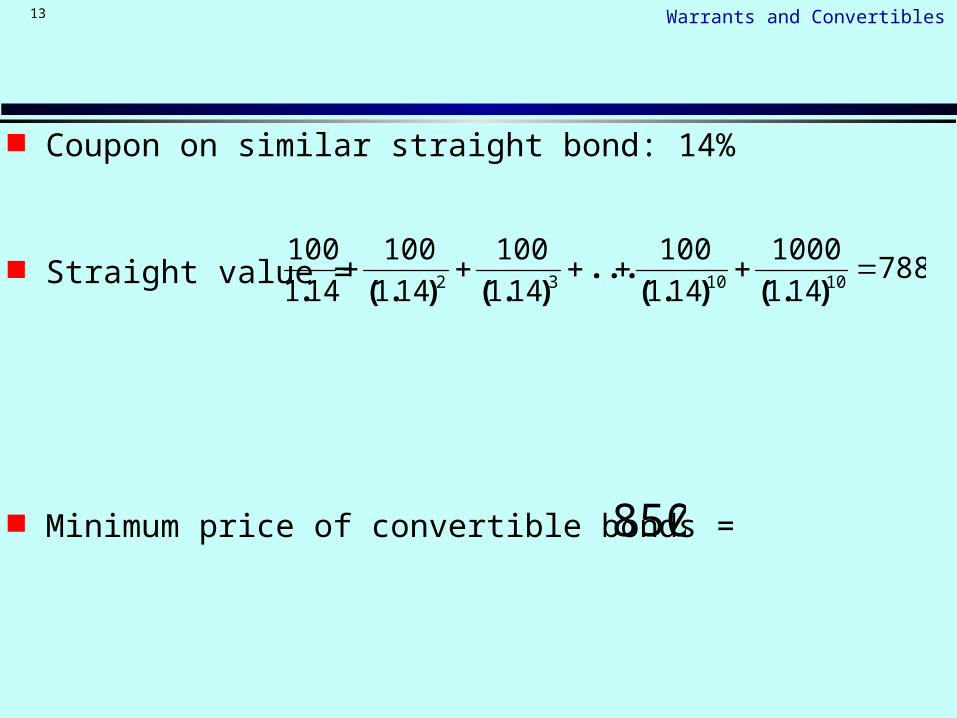

Coupon on similar straight bond: 14%

Straight value =

Minimum price of convertible bonds =

788141

1000

141

100

141

100

141

100

141

100101032

).().(

...).().(.

850

Warrants and Convertibles14

Warrants and Convertibles15

Warrants and Convertibles16

Warrants and Convertibles17

CONVERTIBLE BOND VALUATION

Existing shares = 45.2 mil. Current share price = 31

Convertible bonds = 130,500 Face value = 1000 per bond Conversion price = 38.131 (per new share) Conversion ratio = 26.225 (shares per conv. bond)

The fraction of equity convertible bondholders possess if they convert is:

esconvertibl of No. ratio conversion shares old of No.

esconvertibl ofnumber ratio conversion

%.,..

,.0387

50013022526245

50013022526

mill

Warrants and Convertibles18

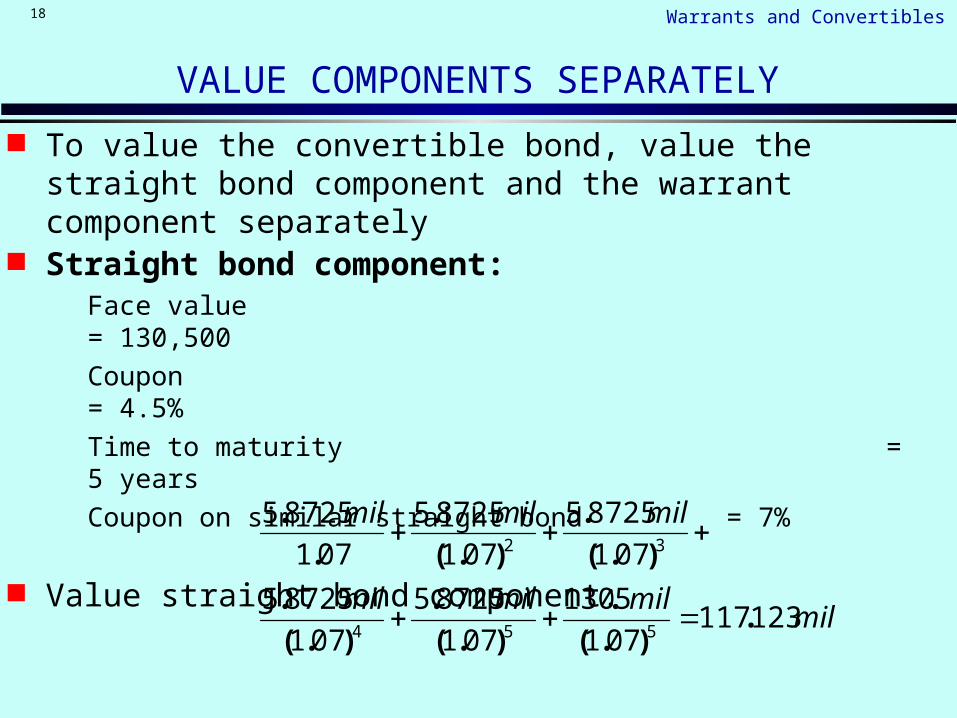

VALUE COMPONENTS SEPARATELY

To value the convertible bond, value the straight bond component and the warrant component separately

Straight bond component: Face value = 130,500 Coupon = 4.5% Time to maturity = 5 years Coupon on similar straight bond = 7%

Value straight bond component:

milmilmilmil

milmilmil

123117071

5130

071

87255

071

87255

071

87255

071

87255

071

87255

554

32

.).(

.

).(

.

).(

.

).(

.

).(

.

.

.

Warrants and Convertibles19

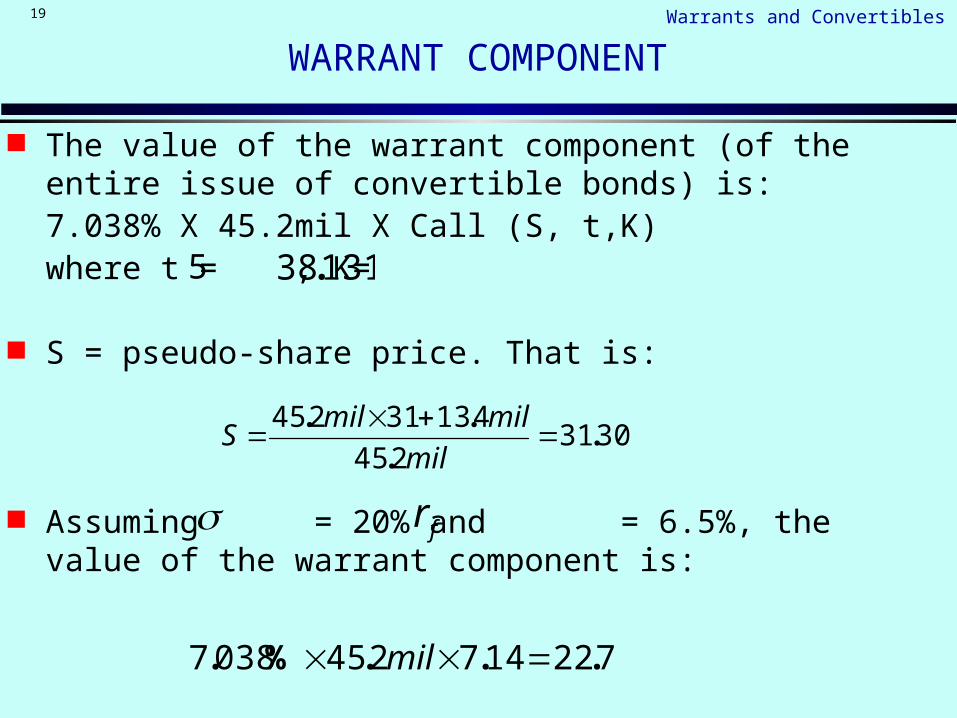

WARRANT COMPONENT

The value of the warrant component (of the entire issue of convertible bonds) is:

7.038% X 45.2mil X Call (S, t,K) where t = , K=

S = pseudo-share price. That is:

Assuming = 20% and = 6.5%, the value of the warrant component is:

5

3031245

41331245.

.

..

mil

milmilS

7221472450387 ...%. mil

fr

13138.

Warrants and Convertibles20

Valuing a convertible

The total value of the convertible bonds would be:

Straight debt component + warrant component

But the bonds were sold for 130.5mil

milmilmil 81397221117 ...

Warrants and Convertibles21

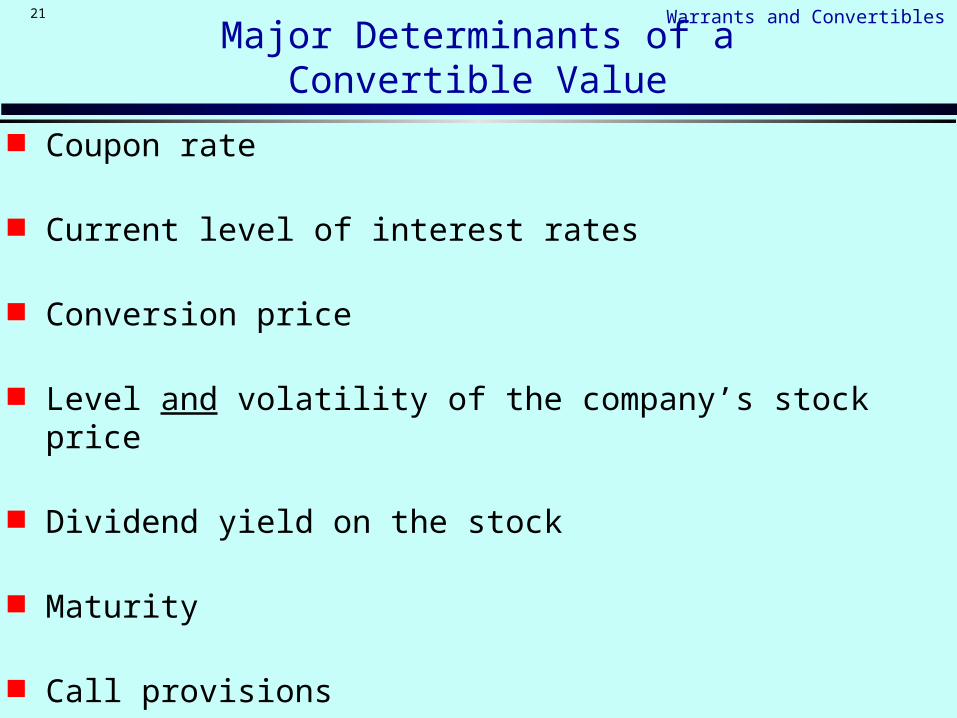

Major Determinants of a Convertible Value

Coupon rate

Current level of interest rates

Conversion price

Level and volatility of the company’s stock price

Dividend yield on the stock

Maturity

Call provisions

Warrants and Convertibles22

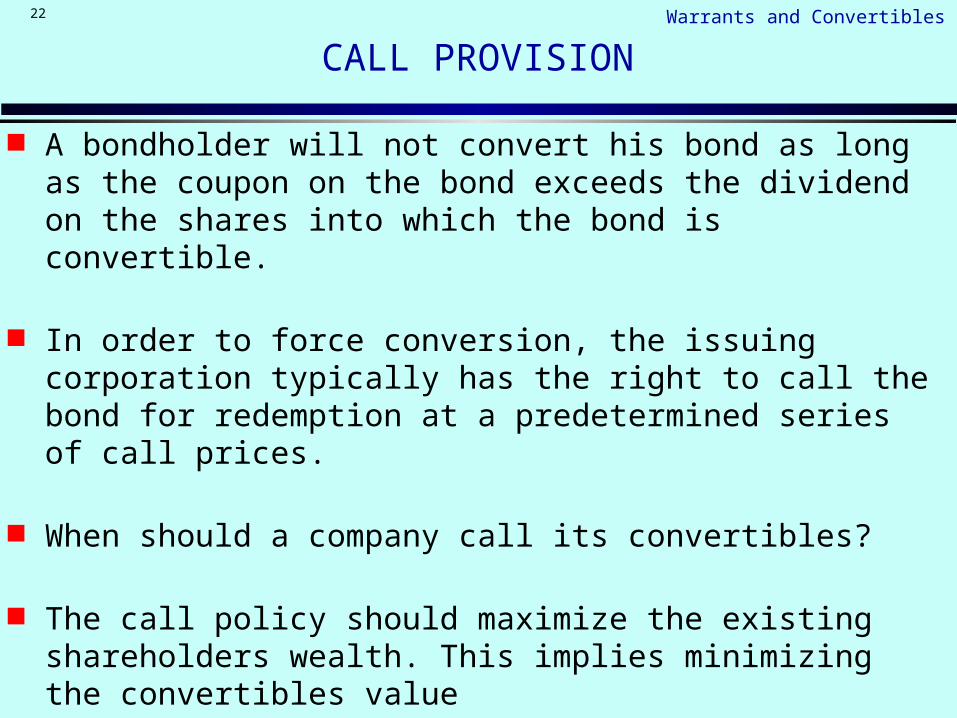

CALL PROVISION

A bondholder will not convert his bond as long as the coupon on the bond exceeds the dividend on the shares into which the bond is convertible.

In order to force conversion, the issuing corporation typically has the right to call the bond for redemption at a predetermined series of call prices.

When should a company call its convertibles?

The call policy should maximize the existing shareholders wealth. This implies minimizing the convertibles value

Warrants and Convertibles23

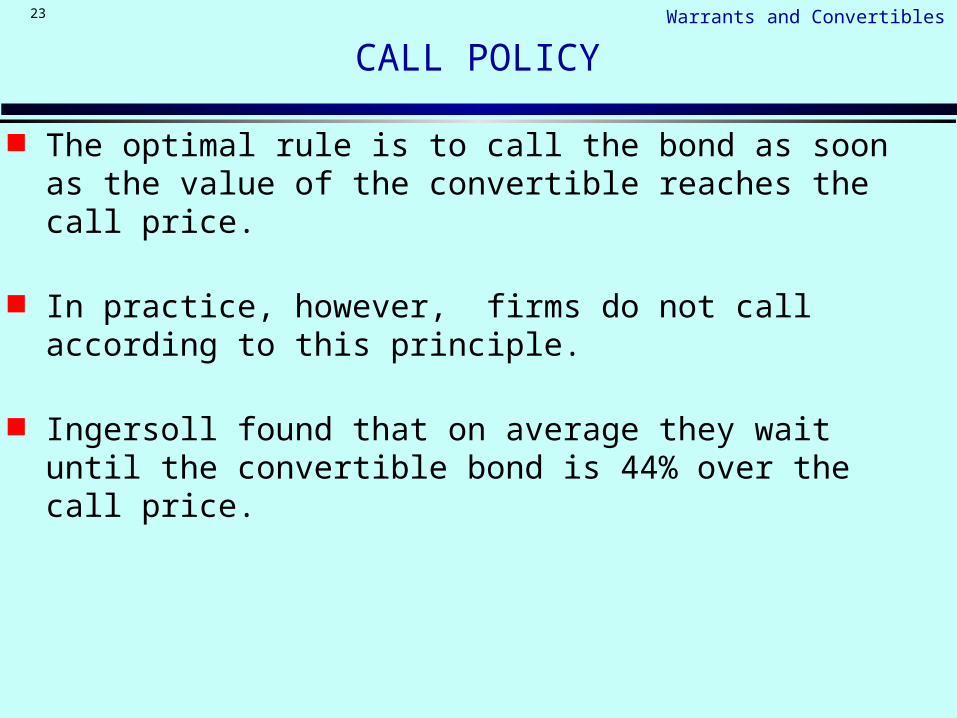

CALL POLICY

The optimal rule is to call the bond as soon as the value of the convertible reaches the call price.

In practice, however, firms do not call according to this principle.

Ingersoll found that on average they wait until the convertible bond is 44% over the call price.

Warrants and Convertibles24

Why issue convertible bonds?

Common misconception:

Convertible debt is a cheap source of finance:

If company does poorly no conversion

cheap debt

If company prospers conversion

sell shares at a high price

Warrants and Convertibles25

A technical point about convertibles

Suppose a firm’s assets become more volatile. How does that affect the value of a convertible?

Two effects: Bond value declines Value of conversion option increases

You can design a convertible so that these two effects cancel out.

Warrants and Convertibles26

Possible rationales for the use of convertible debt

MORAL HAZARD (Green, 1984): the value of straight debt may be reduced if the firm increases the risk of the assets. The conversion feature protects the convertible bonds.

ADVERSE SELECTION (Brennan & Schwartz, 1982): for a given coupon rate, a straight bond is more attractive to an issuer the higher the issuer’s risk. But the warrant element goes in the opposite direction. Different terms for different risks.

DELAYED EQUITY FINANCING (Stein, 1992): firms issue convertibles in the expectation that they will be able to force conversion when good news about their future prospects is revealed.

Warrants and Convertibles27

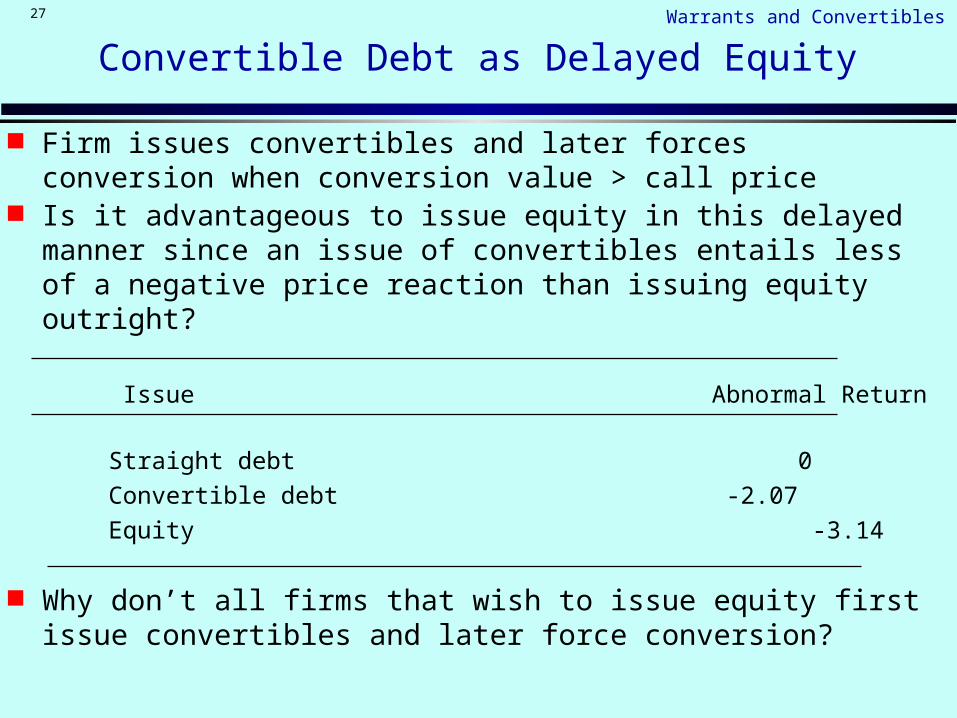

Convertible Debt as Delayed Equity

Firm issues convertibles and later forces conversion when conversion value > call price

Is it advantageous to issue equity in this delayed manner since an issue of convertibles entails less of a negative price reaction than issuing equity outright?

Issue Abnormal Return

Straight debt 0 Convertible debt -2.07 Equity -3.14

Why don’t all firms that wish to issue equity first issue convertibles and later force conversion?

Warrants and Convertibles28

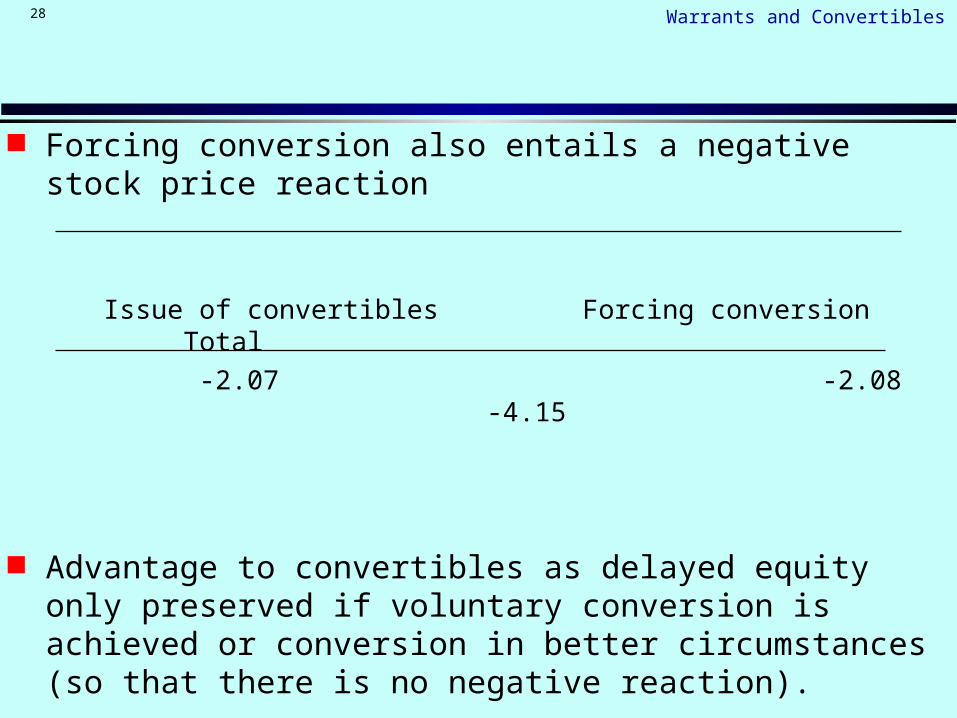

Forcing conversion also entails a negative stock price reaction

Issue of convertibles Forcing conversion Total -2.07 -2.08 -4.15

Advantage to convertibles as delayed equity only preserved if voluntary conversion is achieved or conversion in better circumstances (so that there is no negative reaction).