web chapter 27 finance companies. copyright ©2015 pearson education, inc. all rights reserved.27-1...

TRANSCRIPT

Web Chapter 27

Finance Companies

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-2

Chapter Preview

• Suppose you need to buy a car, but don’t have the $20,000 handy. Most dealers will help arrange financing for you, using a finance company. Along with consumer loans, finance companies are involved in lease finance and other business services.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-3

Chapter Preview

• In this chapter, we examine how finance companies evolved and what they do. Topics include: ─ History of Finance Companies─ Purpose of Finance Companies─ Risk of Finance Companies─ Types of Finance Companies─ Regulation of Finance Companies─ Finance Company Balance Sheet

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-4

History of Finance Companies

• Finance companies date back to the 1800s when retailers started offering installment credit.

• Autos loans really developed the industry, since banks didn’t offer car loans in the early 1990s.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-5

History of Finance Companies

• By the beginning of 2013, banks held $1,191 billion in consumer loans, while finance companies held $804 billion.

• Finance companies moved into business financing (lease financing, etc.)

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-6

Purpose of Finance Companies

• Issue commercial paper and use the proceeds to make loans.

• Largely unregulated, some states limit the size of a loan contract to a consumer borrower.

• Service both consumers and businesses with tailored products (usually not offered by banks).

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-7

Risk in Finance Companies

• Default risk is the greatest risk, and finance companies often lend to those who can’t get financing otherwise.

• Liquidity risk can be an issue, as their assets (loans) are not easily sold. A need for cash can cause problems.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-8

Risk in Finance Companies

• Roll over risk refers to the need to continue to borrow in the commercial paper market.

• Interest rate risk is also present. Assets are medium-term loans, funded by short-term commercial paper.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-9

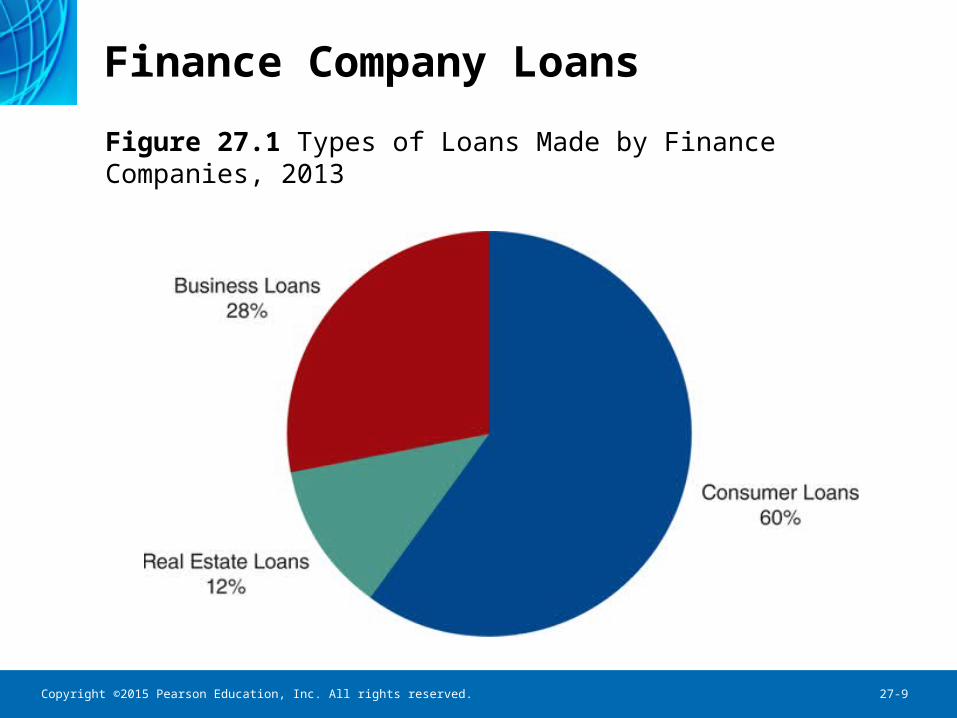

Finance Company Loans

Figure 27.1 Types of Loans Made by Finance Companies, 2013

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-10

Types of Finance Companies

• Business Finance Companies offer loans secured by accounts receivable and other business.

• They also factor accounts receivable - giving companies, say, 90% of the book value of A/R.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-11

Types of Finance Companies

• They also specialize in leasing, often buying the asset and then lease it back to the company. Possible tax play.

• Floor plans help, for example, car dealers pay for all the cars on their lot.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-12

Business Finance Company Loans

Figure 27.2 Types of Business Loans Made by Finance Companies (end of 2013)

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-13

Business Finance Company Loans

Figure 27.3 Finance Company Business Loans, 1994–2013

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-14

Consumer Finance Companies

• Consumer finance companies offer consumer loans to for furniture, home improvements, etc.

• Consumers often can’t get credit elsewhere.• Two exceptions are home equity loans and

retail credit cards.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-15

Consumer Finance Companies

• A home equity loans can reduce borrowing costs:

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-16

Sales Finance Companies

A sales finance company is owned by the manufacturer to promote its sales. •If you want to buy a GM car, GMAC will be happy to assist with the financing. •Also known as captive finance companies.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-17

Regulation

• Since there are no depositors or government insurance, regulation is limited.

• Regulation is typically designed to protect consumers. For example, Regulation Z requires the disclosure of the APR on loans.

• Usury laws limit the interest rate that can be charged.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-18

Regulation

• State and federal regulation limit ability to collect on delinquent or defaulted loans.

• Few regulations in the business loan market.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-19

Finance Company Balance Sheet

Table 27.1 Consolidated Finance Company Balance Sheet, 2012

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-20

Finance Company Balance Sheet

• Assets. ─ Primary asset is their loan portfolio─Must maintain a contra-asset account reserve

for loan losses to charge off expected loan defaults

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-21

Finance Company Balance Sheet

• Liabilities. ─ Equity (about 12% of assets)─ Loans ─ Active in the commercial paper market─ Captive finance companies can borrow directly

from their parent company

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-22

Finance Company Balance Sheet

• Income. Their income comes from several sources:─ Interest income from their loan portfolio─ Loan origination fees─ Credit insurance premiums─ Some have also expanded into income tax

preparation services

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-23

Finance Company Balance Sheet: Growth in Assets

Figure 27.4 Growth of Finance Company Assets, 1980–2012

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-24

Chapter Summary

• History and Purpose: the history and background of these companies was presented - essentially, how they filled the void left by banks.

• Risk: the essential risks faced by finance companies was covered: roll over and interest rate risk.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-25

Chapter Summary

• Types: the basic classification of finance companies was reviewed, primarily by the type of customer served.

• Regulations: other than consumer protections laws, we discussed why finance companies aren’t heavily regulated.

Copyright ©2015 Pearson Education, Inc. All rights reserved. 27-26

Chapter Summary

• Balance Sheet: we reviewed the breakdown of the assets and liabilities held by these companies.