webinar slides: eye on washington quarterly business tax update, 2015 q4

TRANSCRIPT

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Eye on Washington: Quarterly Tax Update (4th Quarter) Steve Henley and Bill Smith Jan 26, 27, and 28

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

*MHM is an independent CPA firm providing audit, review and attest services, and works closely with CBIZ, a business consulting, tax and financial services provider.

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

CBIZ & MHM 6

Presenters

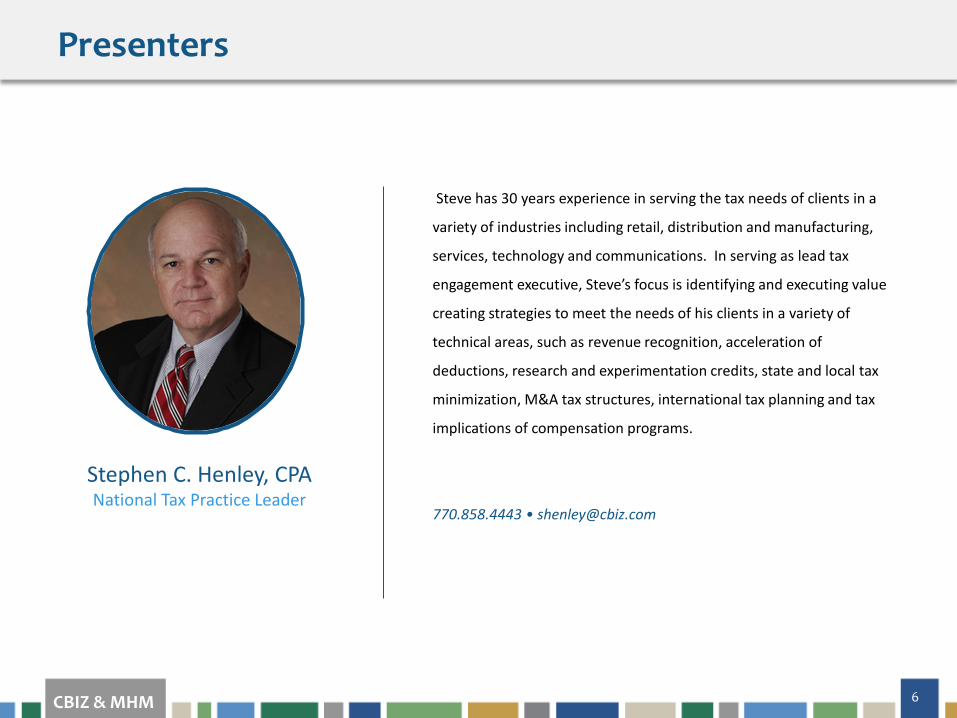

Steve has 30 years experience in serving the tax needs of clients in a

variety of industries including retail, distribution and manufacturing,

services, technology and communications. In serving as lead tax

engagement executive, Steve’s focus is identifying and executing value

creating strategies to meet the needs of his clients in a variety of

technical areas, such as revenue recognition, acceleration of

deductions, research and experimentation credits, state and local tax

minimization, M&A tax structures, international tax planning and tax

implications of compensation programs.

770.858.4443 • [email protected]

Stephen C. Henley, CPA National Tax Practice Leader

#cbizmhmwebinar 7

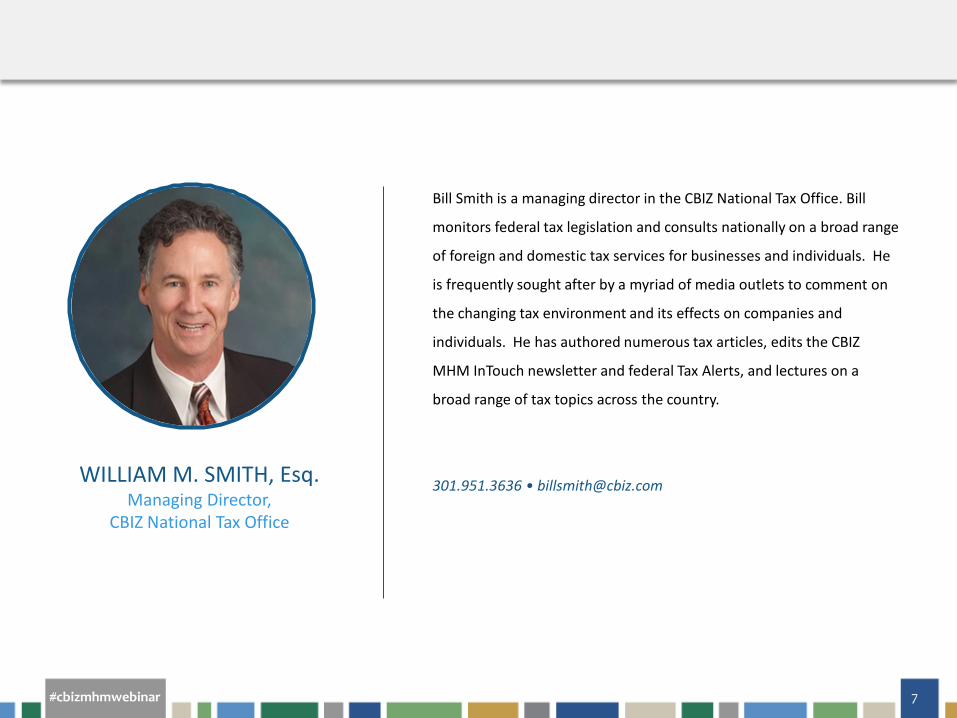

Bill Smith is a managing director in the CBIZ National Tax Office. Bill

monitors federal tax legislation and consults nationally on a broad range

of foreign and domestic tax services for businesses and individuals. He

is frequently sought after by a myriad of media outlets to comment on

the changing tax environment and its effects on companies and

individuals. He has authored numerous tax articles, edits the CBIZ

MHM InTouch newsletter and federal Tax Alerts, and lectures on a

broad range of tax topics across the country.

301.951.3636 • [email protected] WILLIAM M. SMITH, Esq. Managing Director,

CBIZ National Tax Office

#cbizmhmwebinar 8

Agenda

Legislative

02

01

03

04

Administrative

Cases

Questions

#cbizmhmwebinar 9

LEGISLATIVE UPDATE

#cbizmhmwebinar 10

Committees and House Leadership

• House of Representatives • Speaker is former Ways and Means Chairman Paul Ryan

(R – Wis.) • Chairman Ways and Means: Kevin Brady (R – Tex.)

• Senate • Orrin Hatch (R – Utah), Chairman of Senate Finance

committee

#cbizmhmwebinar 11

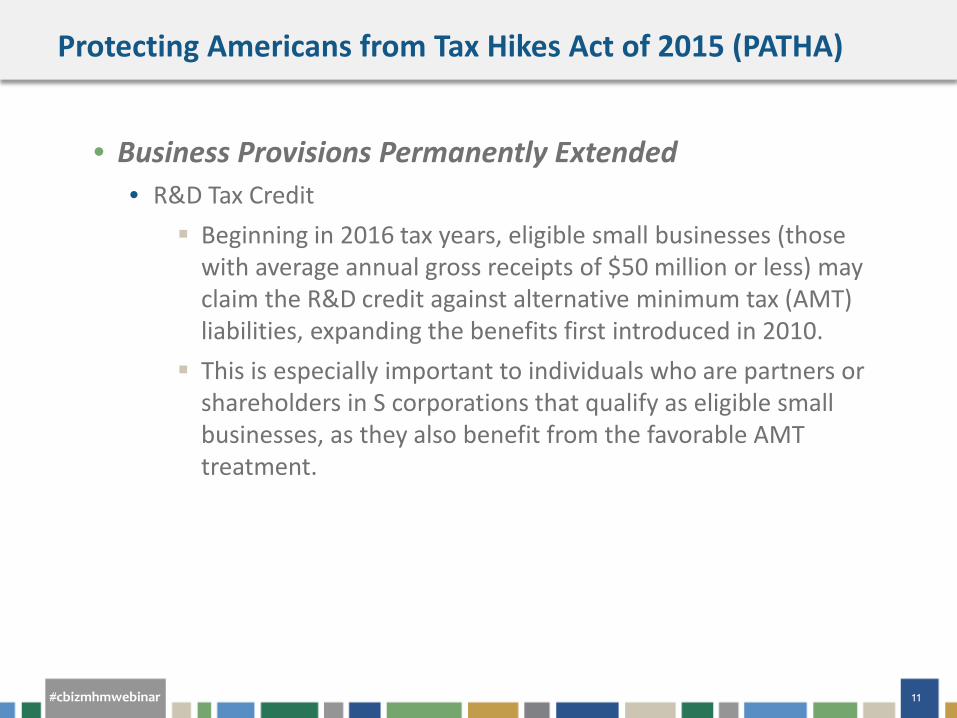

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Permanently Extended • R&D Tax Credit

Beginning in 2016 tax years, eligible small businesses (those with average annual gross receipts of $50 million or less) may claim the R&D credit against alternative minimum tax (AMT) liabilities, expanding the benefits first introduced in 2010.

This is especially important to individuals who are partners or shareholders in S corporations that qualify as eligible small businesses, as they also benefit from the favorable AMT treatment.

#cbizmhmwebinar 12

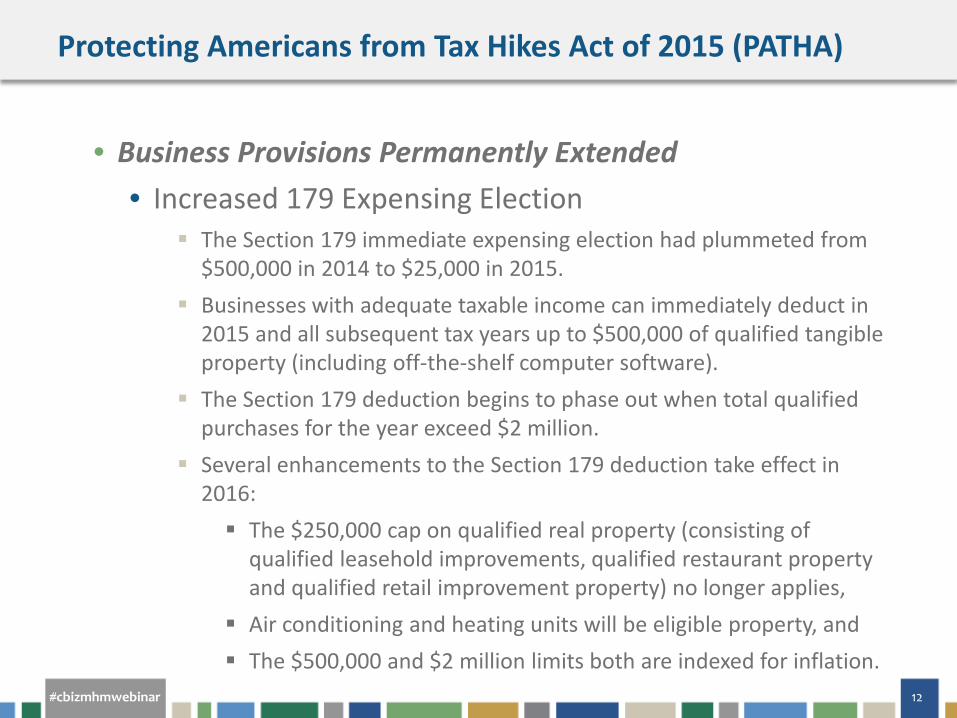

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Permanently Extended • Increased 179 Expensing Election

The Section 179 immediate expensing election had plummeted from $500,000 in 2014 to $25,000 in 2015.

Businesses with adequate taxable income can immediately deduct in 2015 and all subsequent tax years up to $500,000 of qualified tangible property (including off-the-shelf computer software).

The Section 179 deduction begins to phase out when total qualified purchases for the year exceed $2 million.

Several enhancements to the Section 179 deduction take effect in 2016: The $250,000 cap on qualified real property (consisting of

qualified leasehold improvements, qualified restaurant property and qualified retail improvement property) no longer applies,

Air conditioning and heating units will be eligible property, and The $500,000 and $2 million limits both are indexed for inflation.

#cbizmhmwebinar 13

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

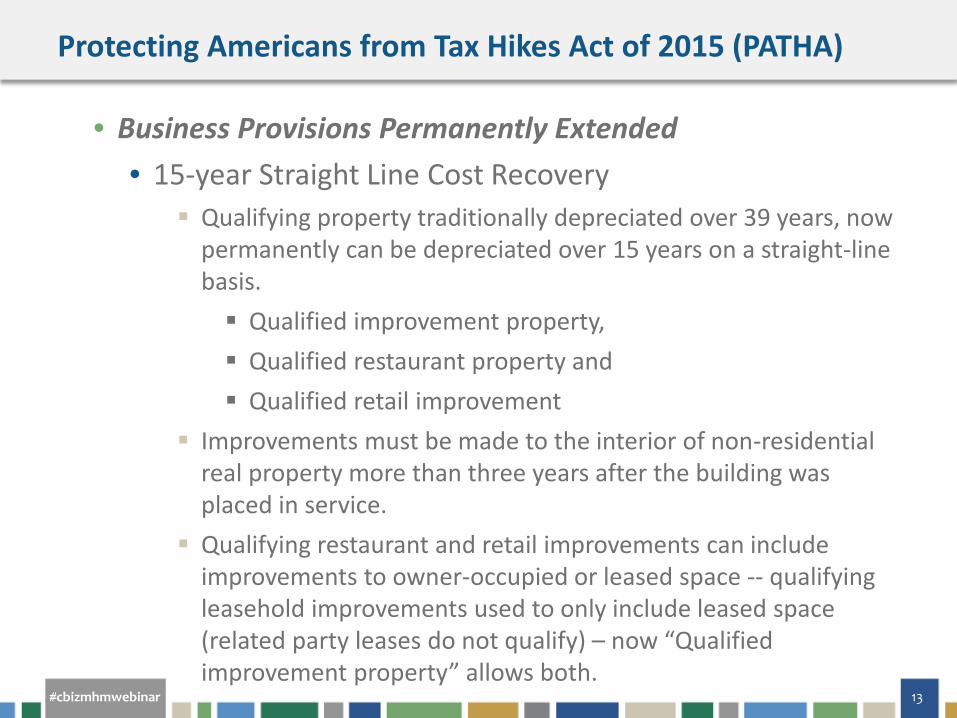

• Business Provisions Permanently Extended • 15-year Straight Line Cost Recovery

Qualifying property traditionally depreciated over 39 years, now permanently can be depreciated over 15 years on a straight-line basis. Qualified improvement property, Qualified restaurant property and Qualified retail improvement

Improvements must be made to the interior of non-residential real property more than three years after the building was placed in service.

Qualifying restaurant and retail improvements can include improvements to owner-occupied or leased space -- qualifying leasehold improvements used to only include leased space (related party leases do not qualify) – now “Qualified improvement property” allows both.

#cbizmhmwebinar 14

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Permanently Extended • Other provisions

100 percent exclusion of gain from the sale of qualified small business stock held by non-corporate taxpayers for more than 5 years Also, the gain will no longer be treated as an AMT

preference item Reduction of the recognition period for built-in gains of S

corporations from 10 to 5 years Basis adjustment to stock of S corporations making charitable

contributions of appreciated property Enhanced charitable deduction for contributions of food

inventory Subpart F exception for active financing income.

#cbizmhmwebinar 15

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

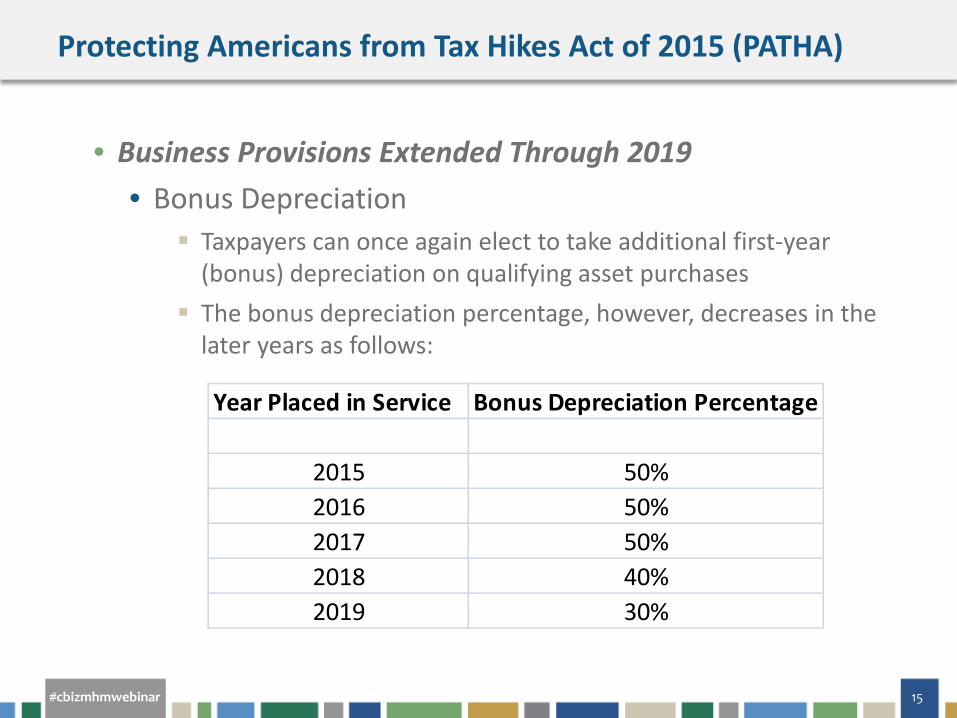

• Business Provisions Extended Through 2019 • Bonus Depreciation

Taxpayers can once again elect to take additional first-year (bonus) depreciation on qualifying asset purchases

The bonus depreciation percentage, however, decreases in the later years as follows:

Year Placed in Service Bonus Depreciation Percentage

2015 50%2016 50%2017 50%2018 40%2019 30%

#cbizmhmwebinar 16

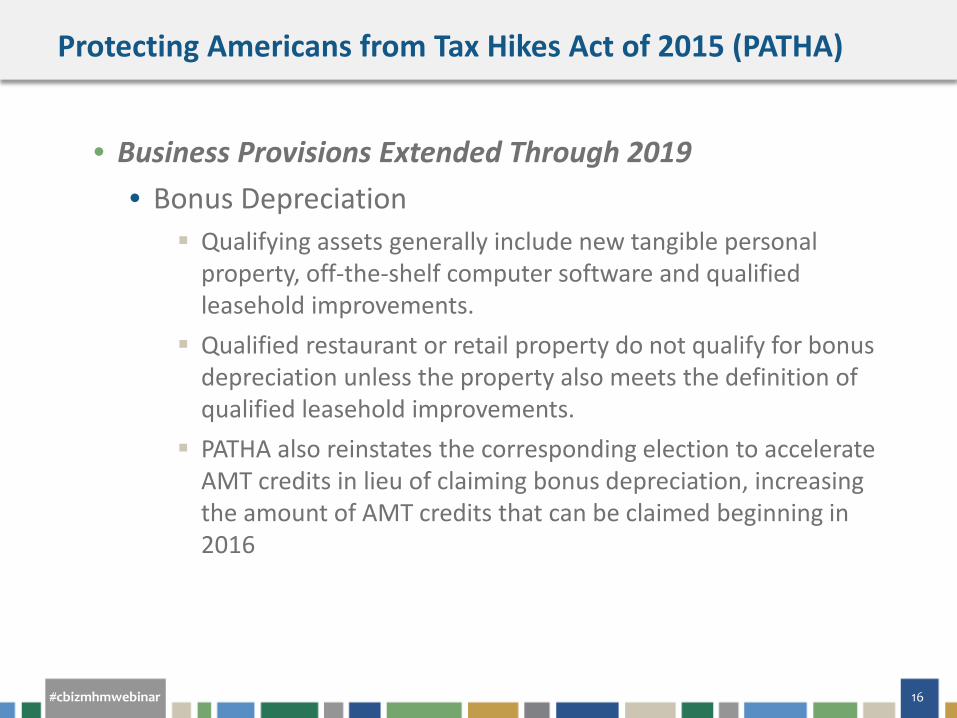

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Extended Through 2019 • Bonus Depreciation

Qualifying assets generally include new tangible personal property, off-the-shelf computer software and qualified leasehold improvements.

Qualified restaurant or retail property do not qualify for bonus depreciation unless the property also meets the definition of qualified leasehold improvements.

PATHA also reinstates the corresponding election to accelerate AMT credits in lieu of claiming bonus depreciation, increasing the amount of AMT credits that can be claimed beginning in 2016

#cbizmhmwebinar 17

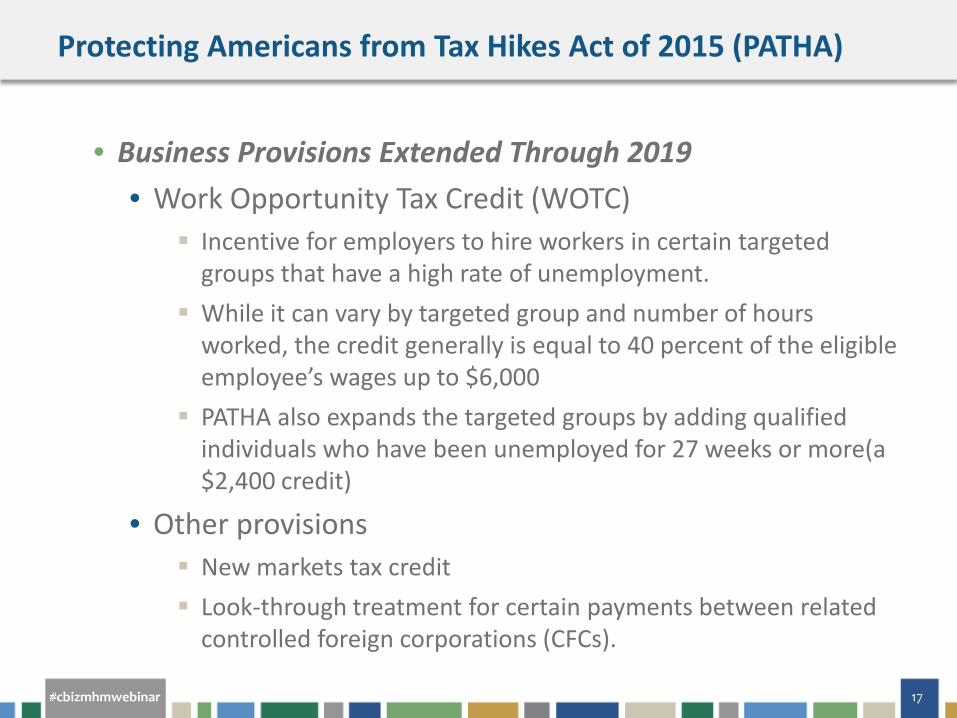

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Extended Through 2019 • Work Opportunity Tax Credit (WOTC)

Incentive for employers to hire workers in certain targeted groups that have a high rate of unemployment.

While it can vary by targeted group and number of hours worked, the credit generally is equal to 40 percent of the eligible employee’s wages up to $6,000

PATHA also expands the targeted groups by adding qualified individuals who have been unemployed for 27 weeks or more(a $2,400 credit)

• Other provisions New markets tax credit Look-through treatment for certain payments between related

controlled foreign corporations (CFCs).

#cbizmhmwebinar 18

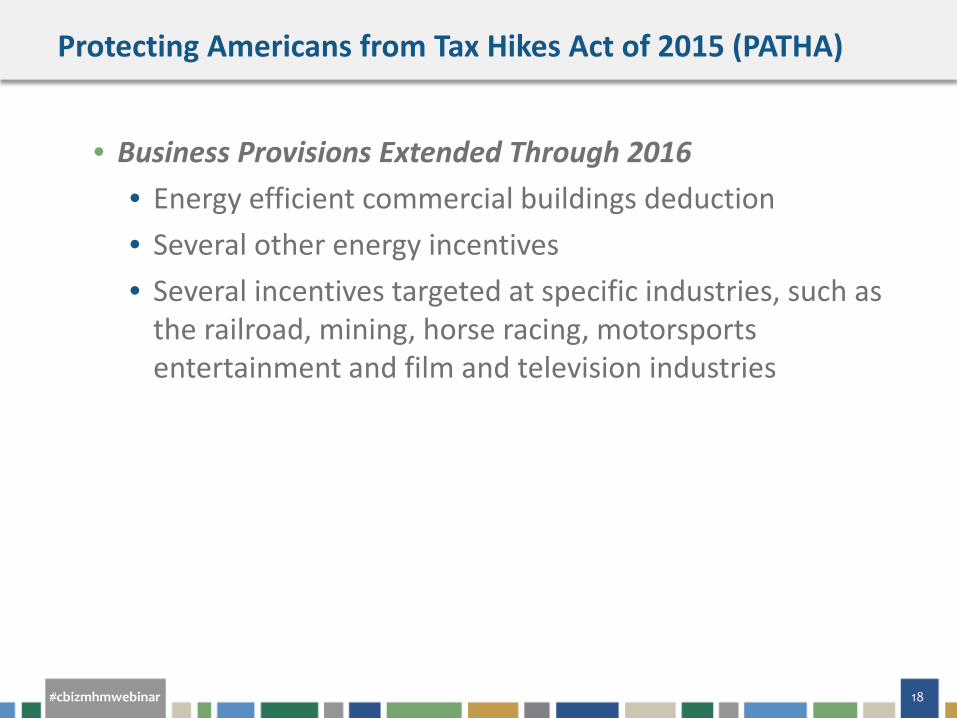

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Business Provisions Extended Through 2016 • Energy efficient commercial buildings deduction • Several other energy incentives • Several incentives targeted at specific industries, such as

the railroad, mining, horse racing, motorsports entertainment and film and television industries

#cbizmhmwebinar 19

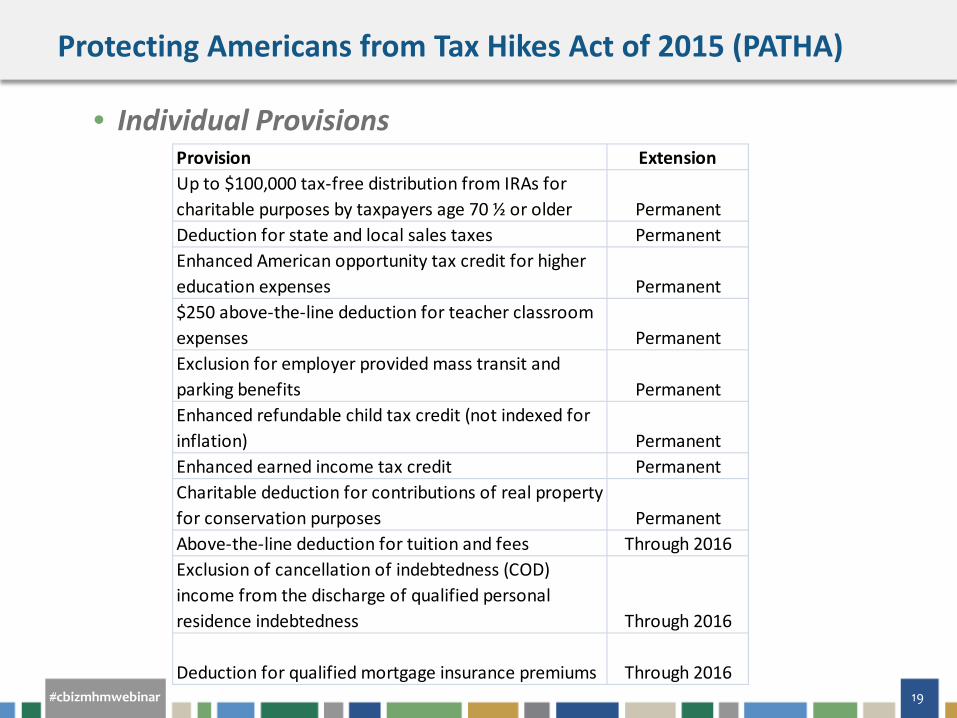

Protecting Americans from Tax Hikes Act of 2015 (PATHA)

• Individual Provisions

Provision ExtensionUp to $100,000 tax-free distribution from IRAs for charitable purposes by taxpayers age 70 ½ or older PermanentDeduction for state and local sales taxes PermanentEnhanced American opportunity tax credit for higher education expenses Permanent$250 above-the-line deduction for teacher classroom expenses PermanentExclusion for employer provided mass transit and parking benefits PermanentEnhanced refundable child tax credit (not indexed for inflation) PermanentEnhanced earned income tax credit PermanentCharitable deduction for contributions of real property for conservation purposes PermanentAbove-the-line deduction for tuition and fees Through 2016Exclusion of cancellation of indebtedness (COD) income from the discharge of qualified personal residence indebtedness Through 2016

Deduction for qualified mortgage insurance premiums Through 2016

#cbizmhmwebinar 20

Cadillac Tax (FY 2016 Omnibus)

• 40% non-deductible excise tax on high-cost, employer-sponsored health coverage -- originally set to start in 2018 -- for health benefits exceeding $10,200 self-only coverage and $27,500 for all others • Self-funded and fully insured • Retiree coverage • Applies to employer and employee premium contributions • Applies to Flex accounts and HSAs

• FY 2016 Omnibus delays implementation to 2020, and makes the tax deductible against income

#cbizmhmwebinar 21

Medical Device Excise Tax (FY 2016 Omnibus)

• Starting in 2013, ACA imposes an excise tax on any manufacturer, producer or importer of certain medical devices equal to 2.3 percent of the price for which the medical device is sold.

• A taxable medical device means any "device"—as defined in section 201(h) of the Federal Food Drug and Cosmetic Act (FDC Act or FFDCA))—intended for humans.

• FY 2016 Omnibus imposes a moratorium on the excise tax for sales in 2016 and 2017

#cbizmhmwebinar 22

New Partnership Audit Rules (Effective 2018)

• 2014 GAO report: • IRS audited less than 1 percent of the 2012 income tax returns of

large partnerships (i.e., those with greater than $100 million in assets), essentially the same audit rate as individual income tax returns.

• By contrast, over 27 percent of large C corporations were audited. • The disparity in the audit rates is caused by the increased burden on

the IRS when auditing partnerships under the current TEFRA rules, where the audit adjustments are assessed against the individual partners of the partnership.

• The assessment of an adjustment against a C corporation simply is made against one taxpayer — the corporation.

• The new legislation (Bipartisan Budget Act of 2015) attempts to ease the administrative burden for both the IRS and taxpayers by simplifying the administrative procedures of conducting a partnership examination

#cbizmhmwebinar 23

New Partnership Audit Rules (Effective 2018)

• Applies to all partnerships, except for certain qualifying partnerships that affirmatively elect out of the new rules for that particular tax year.

• New terms: • If the IRS determines that adjustments are required for

the partnership tax year (the "reviewed year"), the partnership is required to pay any "imputed underpayment" with respect to the adjustment in the year in which the adjustment is finalized (the "adjustment year").

• The imputed underpayment is generally determined at maximum corporate or individual rate

#cbizmhmwebinar 24

New Partnership Audit Rules (Effective 2018)

• An adjustment that results in an overpayment generally is taken into account by the partnership in the adjustment year • This may create a disparity because this treatment appears to

treat the adjustment as ordinary income, regardless of its original character.

• Generally speaking, audit adjustments of income, gain, loss, deduction, or credit of the partnership will be applied at the partnership level.

• Accordingly, the assessment and collection of any taxes, interest, and penalties relating to an adjustment also will be applied at the partnership level.

• Each partnership that does not elect out of the new regime to designate a partner as the partnership's representative.

#cbizmhmwebinar 25

New Partnership Audit Rules (Effective 2018)

• A partnership can avoid of the new rules for a tax year in one of two ways: • If the partnership issues 100 or fewer Schedule K-1s for the

tax year and each of the partners is an individual, a C corporation, any foreign entity that would be treated as a C corporation were it domestic, an S corporation, or an estate of a deceased partner • The partnership can make an election with a timely filed

return for such taxable year • For partners that are S corporations, the number of

Schedule K-1s issued by the S corporation partner to its shareholders counts toward the "100 or fewer Schedule K-1s" requirement

#cbizmhmwebinar 26

New Partnership Audit Rules (Effective 2018)

• A partnership can avoid of the new rules for a tax year in one of two ways: • If the partnership receives a notice of final partnership

adjustment ("NFPA"), an election must be made by the partnership no later than 45 days after the date of the NFPA

• IRS to provide mechanism for making election • Partnership must furnish to each partner for the reviewed

year and to the IRS a statement of the partner's share of any adjustment to income, gain, loss, deduction, or credit (as determined in the NFPA)

• Partner includes his share of all adjustments from NFPA in his tax for the year the statement is furnished

#cbizmhmwebinar 27

New Partnership Audit Rules (Effective 2018)

• The IRS required to provide a mechanism whereby partners (instead of the partnership) who were partners in the year to which the changes relate (the reviewed year) can pay their share of the tax deficiencies by amending past returns. • Beneficial if the partner's tax liability is less than his share of the partnership's

deficiency.

• Partnership must pay the imputed underpayment amount by the due date of the partnership's tax return (without regard to extensions of time to file) for the adjustment year. • No deduction is allowed to the partnership for the payment of such imputed

underpayment amount.

• Current partners bear burden of past years’ tax deficiencies unless partnership elects out, regardless of whether the current partners are the same as the partners in the reviewed year.

#cbizmhmwebinar 28

ADMINISTRATIVE UPDATE

#cbizmhmwebinar 29

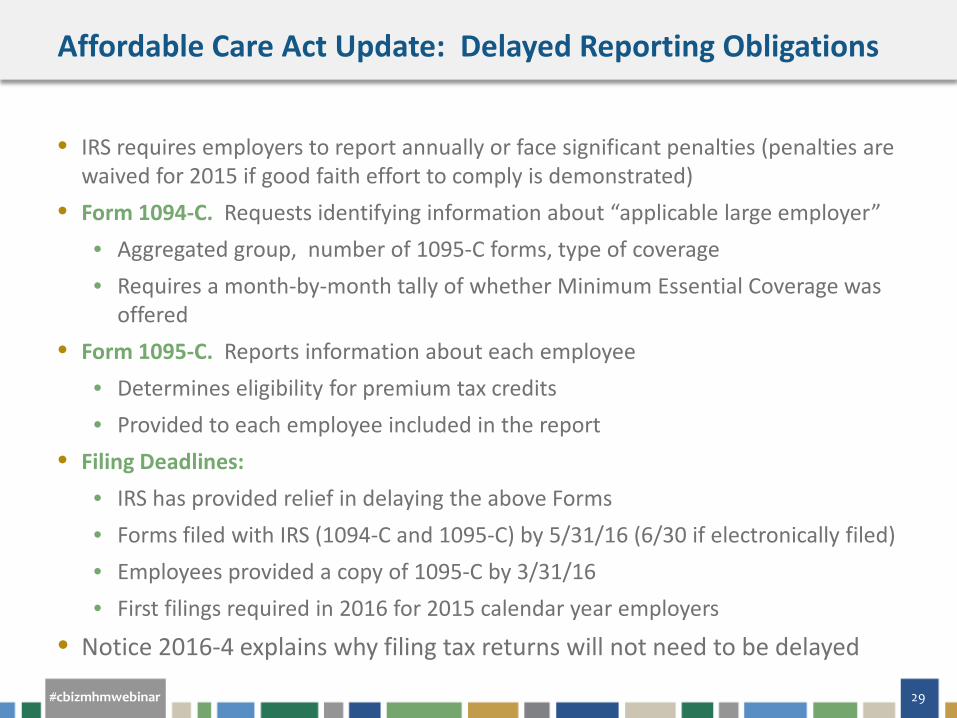

Affordable Care Act Update: Delayed Reporting Obligations

• IRS requires employers to report annually or face significant penalties (penalties are waived for 2015 if good faith effort to comply is demonstrated)

• Form 1094-C. Requests identifying information about “applicable large employer” • Aggregated group, number of 1095-C forms, type of coverage • Requires a month-by-month tally of whether Minimum Essential Coverage was

offered • Form 1095-C. Reports information about each employee

• Determines eligibility for premium tax credits • Provided to each employee included in the report

• Filing Deadlines: • IRS has provided relief in delaying the above Forms • Forms filed with IRS (1094-C and 1095-C) by 5/31/16 (6/30 if electronically filed) • Employees provided a copy of 1095-C by 3/31/16 • First filings required in 2016 for 2015 calendar year employers

• Notice 2016-4 explains why filing tax returns will not need to be delayed

#cbizmhmwebinar 30

Revised Tangible Property De Minimis Safe Harbor

• Final Tangible Property Regulations allowed qualifying businesses to elect to immediately deduct purchases of tangible property below certain dollar thresholds

• Taxpayers with an applicable financial statement (AFS), typically an audited f/s: $5,000 per invoice or item

• Taxpayers without AFS: old rules, $500 per invoice or item • Now, for these smaller taxpayers, safe harbor amount

increased to $2,500 • Beginning with 2016 tax years

#cbizmhmwebinar 31

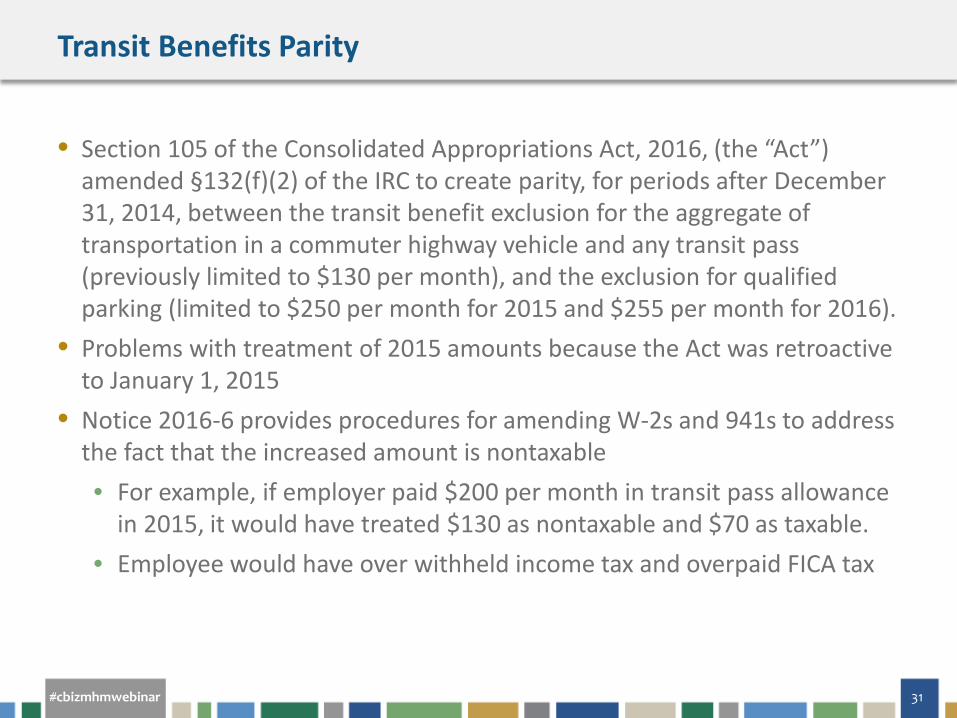

Transit Benefits Parity

• Section 105 of the Consolidated Appropriations Act, 2016, (the “Act”) amended §132(f)(2) of the IRC to create parity, for periods after December 31, 2014, between the transit benefit exclusion for the aggregate of transportation in a commuter highway vehicle and any transit pass (previously limited to $130 per month), and the exclusion for qualified parking (limited to $250 per month for 2015 and $255 per month for 2016).

• Problems with treatment of 2015 amounts because the Act was retroactive to January 1, 2015

• Notice 2016-6 provides procedures for amending W-2s and 941s to address the fact that the increased amount is nontaxable • For example, if employer paid $200 per month in transit pass allowance

in 2015, it would have treated $130 as nontaxable and $70 as taxable. • Employee would have over withheld income tax and overpaid FICA tax

#cbizmhmwebinar 32

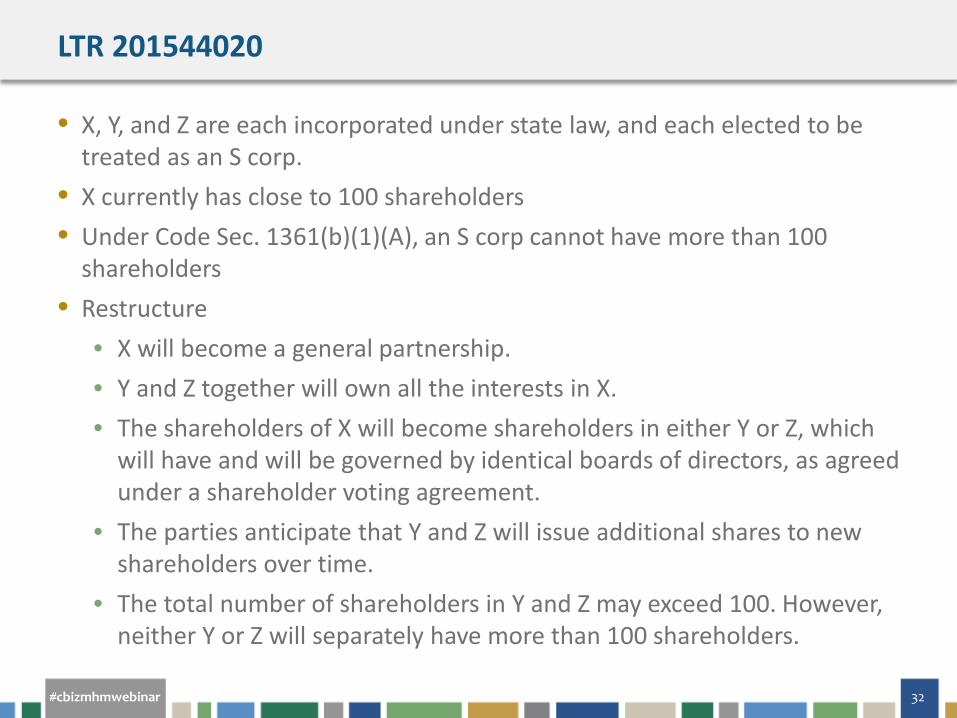

LTR 201544020

• X, Y, and Z are each incorporated under state law, and each elected to be treated as an S corp.

• X currently has close to 100 shareholders • Under Code Sec. 1361(b)(1)(A), an S corp cannot have more than 100

shareholders • Restructure

• X will become a general partnership. • Y and Z together will own all the interests in X. • The shareholders of X will become shareholders in either Y or Z, which

will have and will be governed by identical boards of directors, as agreed under a shareholder voting agreement.

• The parties anticipate that Y and Z will issue additional shares to new shareholders over time.

• The total number of shareholders in Y and Z may exceed 100. However, neither Y or Z will separately have more than 100 shareholders.

#cbizmhmwebinar 33

LTR 201544020

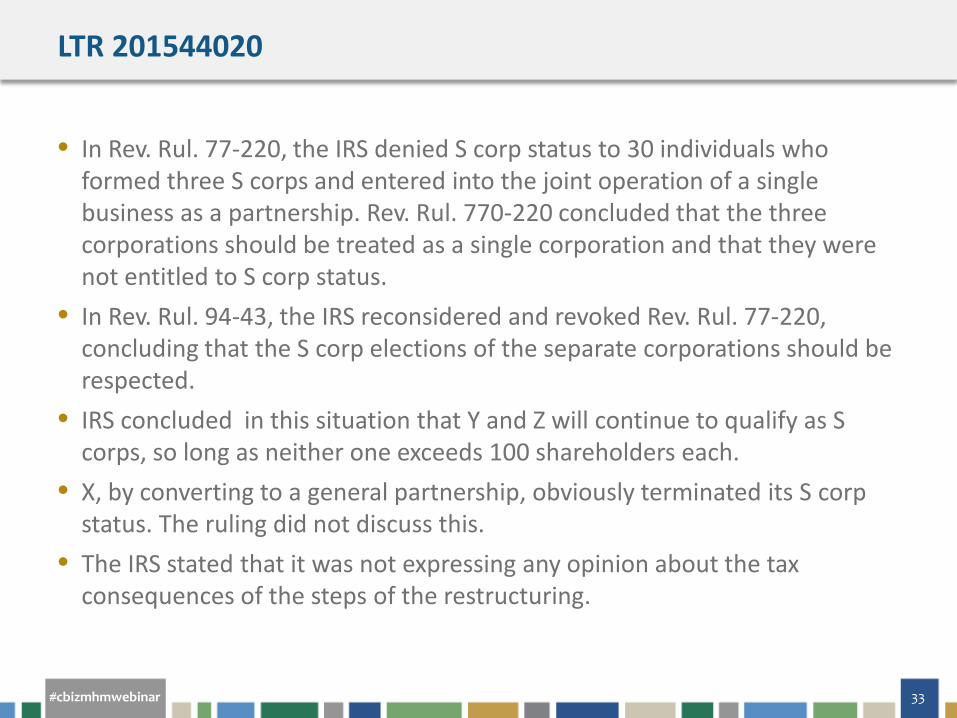

• In Rev. Rul. 77-220, the IRS denied S corp status to 30 individuals who formed three S corps and entered into the joint operation of a single business as a partnership. Rev. Rul. 770-220 concluded that the three corporations should be treated as a single corporation and that they were not entitled to S corp status.

• In Rev. Rul. 94-43, the IRS reconsidered and revoked Rev. Rul. 77-220, concluding that the S corp elections of the separate corporations should be respected.

• IRS concluded in this situation that Y and Z will continue to qualify as S corps, so long as neither one exceeds 100 shareholders each.

• X, by converting to a general partnership, obviously terminated its S corp status. The ruling did not discuss this.

• The IRS stated that it was not expressing any opinion about the tax consequences of the steps of the restructuring.

#cbizmhmwebinar 34

JUDICIAL UPDATE

#cbizmhmwebinar 35

142 T.C. No. 20 (Reported on third quarter of 2014) • The taxpayer was in the land development business -- acquired land, divided it

into parcels, divided the parcels into lots, constructed infrastructure (common improvements), and sold the parcels to builders. Many of the improvements made to the land were necessary for the builders to construct homes on the land. The taxpayer did not build homes on the land they sold.

• The taxpayer used the completed contract method (CCM) in computing its gain on the sale of the properties (before homes were built). The IRS assessed a $144 million deficiency, arguing that taxpayer should have used the percentage-of-completion (PCM) method.

• Under the PCM, a taxpayer must report income annually based on the percentage of the contract completed in that year. Under the CCM, a taxpayer can defer reporting any income, even if payments are received, until its costs reach 95 percent of the total estimated contract costs. The taxpayer deferred over $200 million a year for two years using CCM.

Howard Hughes Co., LLC v. Comm’r

#cbizmhmwebinar 36

• The Tax Court (142 T.C. No. 20 (Reported on third quarter of 2014)) • Said the contracts were not completed until all of the obligatory

improvements had been made, not at the time escrow closed; however, • The contracts were not “home construction contracts” because developer

was never obligated to build the homes • 5th Circuit Court of Appeals (2015-2 U.S.T.C. ¶50,536):

• Rejected the taxpayer’s argument that the statute only requires some causal relationship between dwelling units and the construction costs incurred.

• The law allows costs of improvements to be included in the cost of the dwelling units, but this required that the taxpayer build dwelling units.

Howard Hughes Co., LLC v. Comm’r

#cbizmhmwebinar 37

Alterman Trust v Commr, T.C. Memo. 2015-231

• “Midco transaction”: • MidCoast courted business sellers in order to “reengineer the targets into asset

recovery businesses that purchased receivables (bad credit card debt), and used this method to defer tax”

• Alterman Corporation (AC) was C corporation operating out of Florida as nationwide trucking business, established by Father and subsequently run by three sons, each owing shares through testamentary trusts

• Health problems caused sons to sell business • Spun off all assets buyer did not want into new LLC wholly owned by AC

• After the redemption LLC had $27,463,444 of equity • LLC shares distributed to sons in same ratios as they owned AC stock • Remaining stock sold to MidCoast

• AC had sufficient funds remaining to cover its liabilities (including the putative tax liabilities) with net equity of $1,501,336.

• The redemption did not render AC insolvent, a fact acknowledged by IRS.

#cbizmhmwebinar 38

Alterman Trust v Commr, T.C. Memo. 2015-231

• Despite warranties to the contrary regarding not selling AC and maintaining at least $1.5 million of net worth for 4 years, MidCoast immediately sold AC after the transaction to the financing lender.

• Money transferred offshore • MidCoast applied for quick refund of $1.3 million on 2003 return,

subsequently filed tax return showing no liability due to interest rate swap option sales

• IRS commenced audit in 2005, disallowed deduction, assessed deficiency of $7.5 million in penalties and interest

• Subsequently determined AC had no assets • Assessed the sons’ trusts with transferee liability for entire amount • Sons did not know MidCoast had immediately sold AC until it got transferee

inquiries from IRS • In 2012 the U.S. Government indicted many of the MidCoast principals

#cbizmhmwebinar 39

Alterman Trust v Commr, T.C. Memo. 2015-231

• “Courts, including this court, have been plagued by Midco cases. Rarely do these cases present themselves for a determination of the underlying liabilities. Instead, these cases are postured so that the courts are asked to determine whether someone other than the taxpayer should be on the hook for the taxpayer's liability. They are transferee liability cases, and so are these cases.”

• “Many taxpayers have prevailed at the trial court, but many of those taxpayers have seen their victories turned to defeat on appeal. The IRS has likewise prevailed at the trial court, and its victories have uniformly survived appeal. Rarest of all is the taxpayer victory that survives appeal.”

• IRS determined that “[i]n substance, for all transactions (stock sale and redemption transaction), the shareholders received a distribution in liquidation from Alterman Corporation.”

#cbizmhmwebinar 40

Alterman Trust v Commr, T.C. Memo. 2015-231

• The IRS had to prove two separate and independent conditions: (1) that petitioners are “transferees” as defined under IRC § 6901 and (2) that an “independent basis * * * exist[s] under applicable State law (Florida Unified Fraudulent Transfer Act) for holding the * * * [transferees] liable for the [AC’s] unpaid tax.”

• The court further found that the former shareholders lacked actual or constructive knowledge that MidCoast would fail to do what it promised under the share purchase agreement. • Constructive knowledge is either the "knowledge that ordinary diligence would

have elicited" or a "more active avoidance of the truth." • Sons took reasonable steps to investigate the transaction.

• Rejected IRS’s circular flow of funds argument , finding no evidence that cash in the business had been used to fund the purchase of the shares.

• Lastly, the court found no actual or constructive fraud under Florida's Uniform Fraudulent Transfer Act (FUFTA).

#cbizmhmwebinar 41

Gemperle v Commr, TC Memo 2016-1

• Taxpayers donated a historic façade easement on their home in Chicago • Taxpayers obtained an appraisal valuing the easement at $108,000 • The taxpayers claimed a deduction for the easement on their professionally

prepared 2007 return ($69,186 for 2007, with $38,814 carried over to 2008), but failed to include the appraisal.

• They attached an incomplete Form 8283, Noncash Charitable Contributions, which clearly stated both on the form itself as well as in the instructions that an appraisal was required.

• Court agreed with IRS that the taxpayers weren't entitled to any deduction for their contribution because they failed to include a copy of a qualified appraisal with their 2007 return as required by Code Sec. 170(h)(4)(B)(iii)(I). • Conclusion was supported both by the language of the statute as well as the

underlying legislative history, which expressly states that a failure to obtain and attach an appraisal “results in disallowance of the deduction.”

• Upheld penalties, because no due diligence – Form 8283 unambiguous

#cbizmhmwebinar 42

Route 231 LLC v Commr, 4th Cir

• Partners may contribute capital to a partnership tax-free and may receive a tax-free return of previously taxed profits through distributions.

• These nonrecognition rules do not apply, however, where the transaction is found to be a disguised sale of property.

• A disguised sale can occur if: • there is a direct or indirect transfer of property (including money) by a partner

to a partnership, • there is a related direct or indirect transfer of property (including money) by the

partnership to that partner, and • when viewed together, both transfers are properly characterized as a sale or

exchange of property.

• If these conditions are met, then the transfers are to be treated either as a sale between the partnership and an outsider or as a transaction between two or more partners all of whom are acting outside of their capacities as partners.

#cbizmhmwebinar 43

Route 231 LLC v Commr, 4th Cir

• During 2005 and 2006, Virginia provided an income tax credit to encourage the preservation of natural resources equal to 50% of the fair market value of any land or interest in land in Virginia donated to an eligible agency for preservation purposes.

• A partner in a passthrough entity that held Virginia tax credits could use the credits on his own Virginia income tax returns either in proportion to his interest in the entity or as set forth in the partnership agreement.

• Any taxpayer holding Virginia tax credits could transfer or sell unused but otherwise allowable credits to another taxpayer for use on his Virginia income tax return.

#cbizmhmwebinar 44

Route 231 LLC v Commr, 4th Cir

• Route 231, LLC reported capital contributions of $8,416,000 on its 2005 federal tax return, including $3,816,000 it received from one of its members, Virginia Conservation Tax Credit FD LLLP.

• Upon audit, the said Route 231 should have reported the $3,816,000 received as gross income and not a capital contribution because it was a disguised sale

• Virginia Conservation agreed to make capital contributions “in an amount equal to the product of $0.53 for each $1.00 of [the tax credits] allocated to” it.

• Tax Court held in this and prior case that the credits were property, and that transfer of the credits was not dependent on the ongoing entrepreneurial risks of business, and so it was a disguised sale.

• 4th Circuit agreed that the credits were property, and that the transaction fell squarely within the definitions of disguised sale.

#cbizmhmwebinar 45

? QUESTIONS

#cbizmhmwebinar 46

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ