webinar slides: eye on washington - quarterly business tax update, 2016 q3

TRANSCRIPT

1 #cbizmhmwebinar

Eye on Washington: Quarterly Tax Update (3rd Quarter 2016) Steve Henley and Bill Smith October 27 and November 2, 2016

2 #cbizmhmwebinar

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent

accounting firms

MHM (Mayer Hoffman McCann P.C.) is an independent CPA firm that provides audit, review and attest services, and works closely with CBIZ, a business consulting, tax and financial services provider. CBIZ and MHM are members of Kreston International Limited, a global network of independent accounting firms.

3 #cbizmhmwebinar

Before We Get Started…

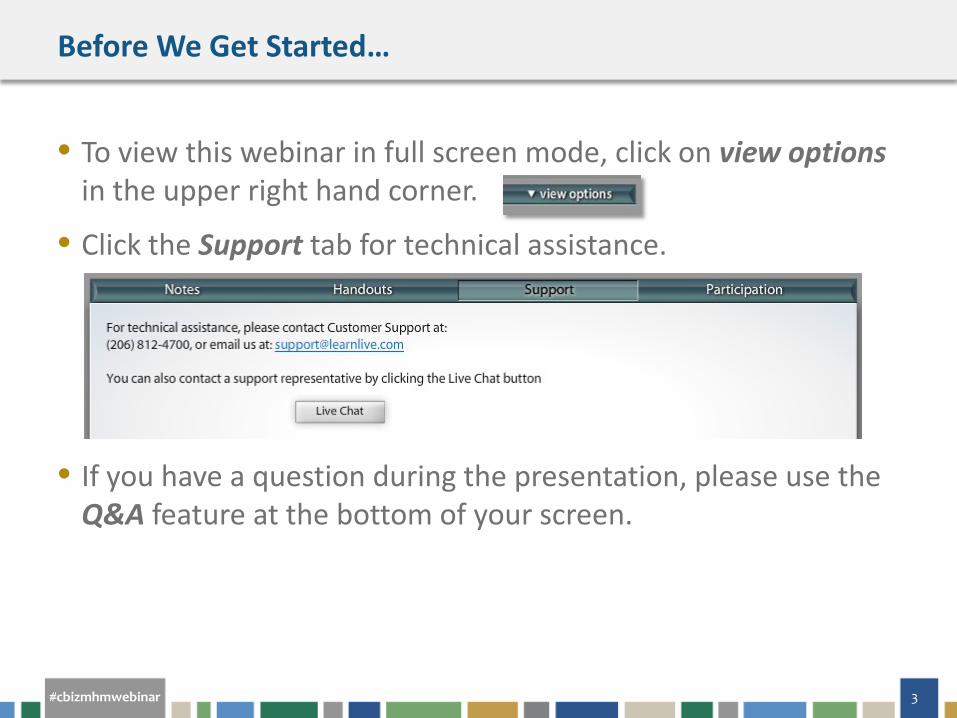

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

4 #cbizmhmwebinar

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

5 #cbizmhmwebinar

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

6 #cbizmhmwebinar

Presenters

Steve has 30 years experience in serving the tax needs of clients in a

variety of industries including retail, distribution and manufacturing,

services, technology and communications. In serving as lead tax

engagement executive, Steve’s focus is identifying and executing value

creating strategies to meet the needs of his clients in a variety of

technical areas, such as revenue recognition, acceleration of deductions,

research and experimentation credits, state and local tax minimization,

M&A tax structures, international tax planning and tax implications of

compensation programs.

770.858.4443 • [email protected]

Stephen C. Henley, CPA National Tax Practice Leader

7 #cbizmhmwebinar

Bill Smith is a managing director in the CBIZ National Tax Office. Bill

monitors federal tax legislation and consults nationally on a broad range

of foreign and domestic tax services for businesses and individuals. He is

frequently sought after by a myriad of media outlets to comment on the

changing tax environment and its effects on companies and individuals.

He has authored numerous tax articles, edits the CBIZ MHM InTouch

newsletter and federal Tax Alerts, and lectures on a broad range of tax

topics across the country.

301.907.2412 • [email protected] William M. Smith, Esq. Managing Director,

CBIZ National Tax Office

Presenters

8 #cbizmhmwebinar

Agenda

Legislative

02

01

03

04

Administrative

Judicial

Questions

9 #cbizmhmwebinar

LEGISLATIVE UPDATE

10 #cbizmhmwebinar

President

Source: www.politico.com May 2015

11 #cbizmhmwebinar

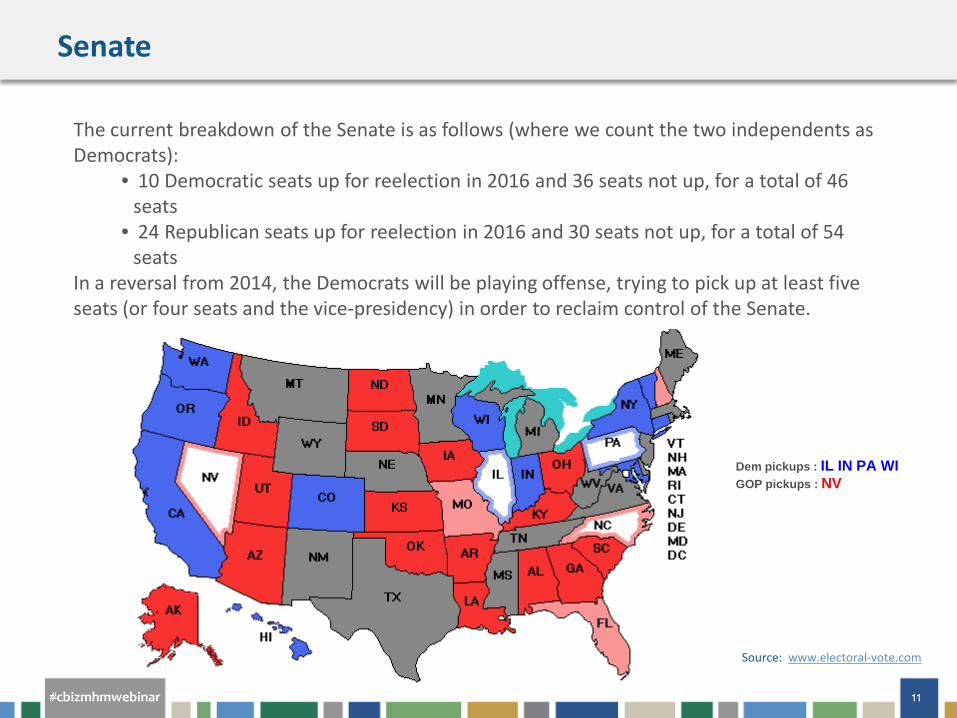

Senate

The current breakdown of the Senate is as follows (where we count the two independents as Democrats):

• 10 Democratic seats up for reelection in 2016 and 36 seats not up, for a total of 46 seats

• 24 Republican seats up for reelection in 2016 and 30 seats not up, for a total of 54 seats

In a reversal from 2014, the Democrats will be playing offense, trying to pick up at least five seats (or four seats and the vice-presidency) in order to reclaim control of the Senate.

Dem pickups : IL IN PA WI GOP pickups : NV

Source: www.electoral-vote.com

12 #cbizmhmwebinar

House

As is the case every two years, all 435 seats in the House of Representatives will be contested this November. Republicans currently* hold 247 seats, Democrats 188. With 218 seats required for control, Democrats must gain 30 seats to take the gavel from Paul Ryan.

Source: www.270towin.com September 2016

13 #cbizmhmwebinar

House

In an appearance before the Economic Club of New York on September 19, House Speaker Paul Ryan (R-Wis.) warned that Democrats and Republicans remain far apart on overhauling the U.S. tax system. “The experience I had when I was Ways and Means chair with your party [Democrats] was not a pleasant one, and I don't know if that's going to change. We'll see,” Ryan said.

14 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

15 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

16 #cbizmhmwebinar

Average Effective Tax Rate By Industry (Washington Post Oct. 4)

17 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

18 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

19 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

20 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

21 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

22 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

23 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

24 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

25 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

26 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

27 #cbizmhmwebinar

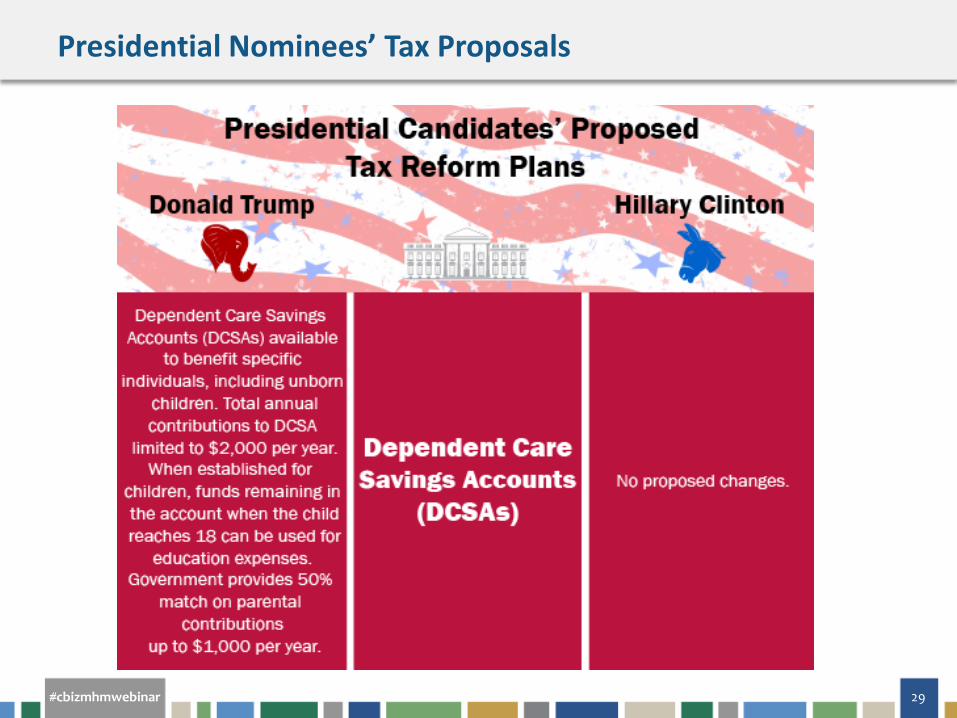

Presidential Nominees’ Tax Proposals

28 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

29 #cbizmhmwebinar

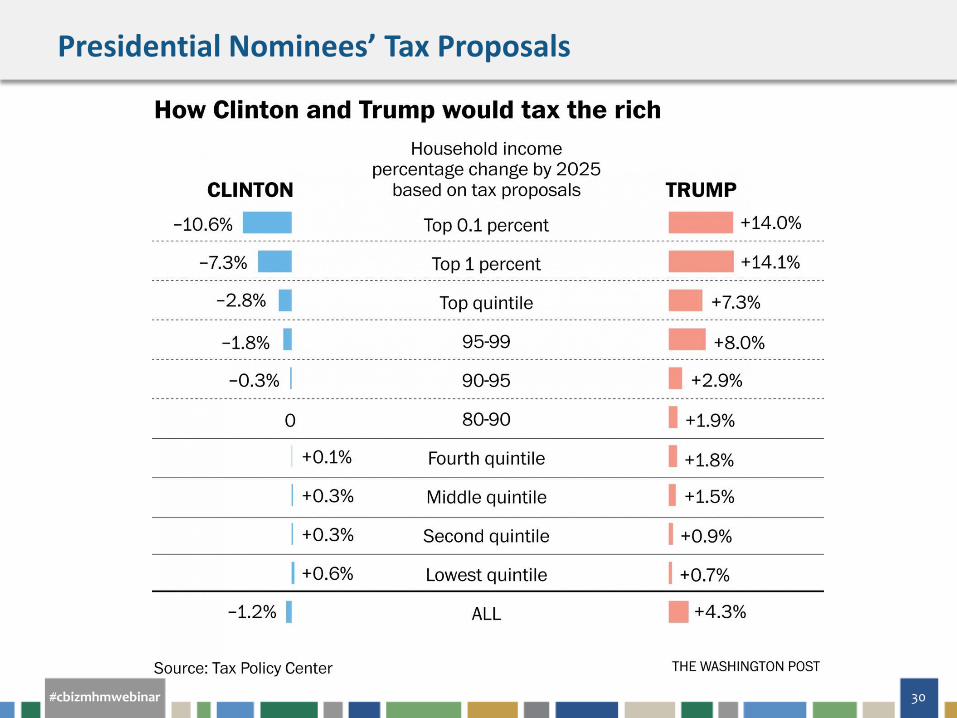

Presidential Nominees’ Tax Proposals

30 #cbizmhmwebinar

Presidential Nominees’ Tax Proposals

31 #cbizmhmwebinar

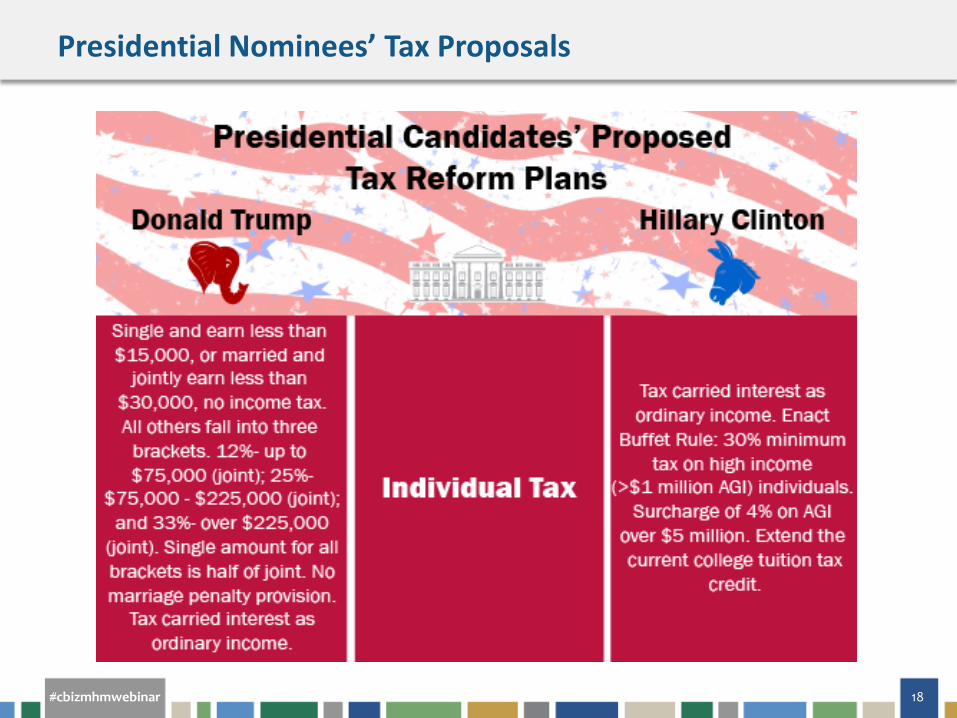

Tax Policy Center Updated Analysis October 11, 2016

• Trump Plan • By 2025, about 51% of the benefits of Trump's tax plan

would accrue to the wealthiest percentile, saving $317,000 on average each year, increasing their incomes by more than 14%.

• Less affluent taxpayers would also benefit, but less so. A typical family would save a little less than $1,100 a year in taxes -- an increase of 1.5%.

• Families with single parents or multiple children, however, could pay more in taxes under Trump's plan.

• If the government borrowed all of the money to pay for Trump's tax plan, the deficits and the cost of interest would increase the national debt by $7.2 trillion. (Cost of Romney's tax plan four years ago was about $5 trillion)

32 #cbizmhmwebinar

NYU Professor Lily Batchelder – September 24, 2016

• Trump Plan • More than half of America's single parents and one-fifth of

its families with children could see their federal income taxes go up.

• The analysis comes from Lily Batchelder, a professor at NYU's law school who focuses on tax policy and worked for President Obama's National Economic Council. She previously served as a tax specialist for the Obama administration and the Senate Finance Committee.

• Says she conducted this study entirely independent of the campaign.

• The Trump campaign called the findings "pure fiction"

33 #cbizmhmwebinar

Tax Policy Center Updated Analysis October 11, 2016

• Clinton Plan • By 2025, 93% of the new revenue would come from the

richest 1%. This group would pay close to $164,000 more each year on average and reduce their incomes by an average of 7.3%.

• Almost 2/3 would come from the richest 0.1%, who would pay an average of $1.1 million more each year, reducing their incomes by almost 11%.

• Most of the benefits would go to working and middle-class families. For families with children under the age of 5, Clinton would double the maximum yearly value of the child tax credit from $1,000 to $2,000 for each child.

• Clinton's plan would raise $1.4 trillion in new federal revenue over a decade.

34 #cbizmhmwebinar

Tax Foundation Analysis October 12, 2016

• Clinton Plan • Constrain economic growth, leading to lower wages and

about 697,000 fewer jobs • Increase federal revenue by $663 billion over 10 years • The lower number stems from the group's use of “dynamic

scoring,” which seeks to account for changes in economic behavior that would result from changes to the tax code.

• On a “static” basis Clinton's plan would raise $1.4 trillion in new federal revenue over a decade, the study found. That amount matches the overall estimate for Clinton's plan that another group, the Tax Policy Center, released Oct. 11.

• Tax Foundation described as “right-leaning”

35 #cbizmhmwebinar

Democratic Party Platform DRAFT – July 1: Tax Provisions

• Claw back tax breaks for companies that ship jobs overseas • Eliminate tax breaks for big oil and gas companies • Crack down on inversions and other methods companies use

to dodge their tax responsibilities • Make sure tax code rewards businesses that make investments

and provide good-paying jobs here in the United States, not businesses that walk out on America

• End deferrals so that American corporations pay U.S. taxes immediately on foreign profits and can no longer escape paying their fair share of United States taxes by stashing profits abroad

• Use the revenue raised from fixing the corporate tax code to reinvest in rebuilding America and ensuring economic growth that will lead to millions of good-paying jobs

36 #cbizmhmwebinar

Democratic Party Platform DRAFT – July 1: Tax Provisions

• Ask those at the top to contribute to our country’s future by establishing a multimillionaire surtax to ensure millionaires and billionaires pay their fair share

• Shut down the “private tax system” for those at the top, immediately close egregious loopholes like those enjoyed by hedge fund managers

• Restore fair taxation on multimillion dollar estates • Ensure millionaires can no longer pay a lower rate than their

secretaries • Offer tax relief to middle-class families—not those at the top

37 #cbizmhmwebinar

House Republicans Tax Reform Proposals – June 24

SIMPLICITY AND FAIRNESS • Save time and money by making it so that most Americans

can do their taxes on a form as simple as a postcard. • Consolidate the system down to three tax brackets, and

lower the top individual income tax rate to 33 percent. • Simplify tax filing for families by creating a larger standard

deduction and a larger child and dependent tax credit. • Make it easier to pay for college by streamlining the maze of

education tax benefits.

38 #cbizmhmwebinar

House Republicans Tax Reform Proposals – June 24

• Eliminate the alternative minimum tax so you don’t have to do your taxes twice a year.

• Reward work by improving the EITC. • Encourage charitable giving by providing a real tax incentive. • Help families plan for retirement by reforming savings

provisions. • Stop overtaxing “Made in America” products so that our

manufacturers can compete. • Repeal the death tax so that the loss of a family member will

no longer be taxable.

39 #cbizmhmwebinar

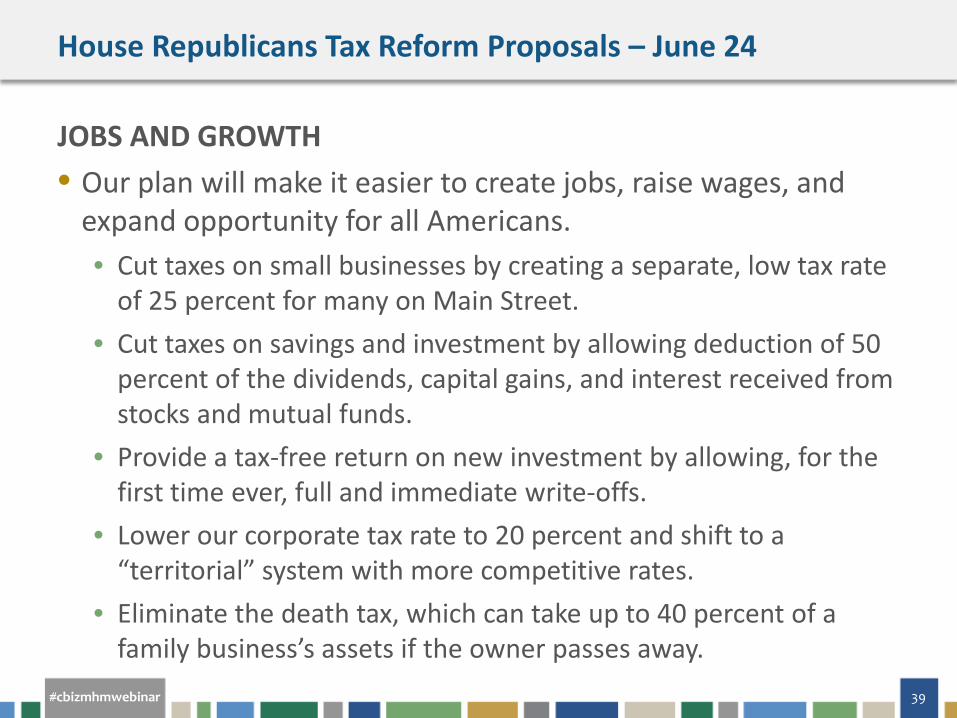

House Republicans Tax Reform Proposals – June 24

JOBS AND GROWTH • Our plan will make it easier to create jobs, raise wages, and

expand opportunity for all Americans. • Cut taxes on small businesses by creating a separate, low tax rate

of 25 percent for many on Main Street. • Cut taxes on savings and investment by allowing deduction of 50

percent of the dividends, capital gains, and interest received from stocks and mutual funds.

• Provide a tax-free return on new investment by allowing, for the first time ever, full and immediate write-offs.

• Lower our corporate tax rate to 20 percent and shift to a “territorial” system with more competitive rates.

• Eliminate the death tax, which can take up to 40 percent of a family business’s assets if the owner passes away.

40 #cbizmhmwebinar

House Republicans Health Reform Proposals – June 21

• Repeal the Affordable Care Act (About 20 million adults have gained coverage under the ACA: Department of Health and Human Services – March 2016)

• Replace it by • Providing tax credits to help people buy insurance • Letting them purchase coverage across state lines, and • Providing $25 billion for state-run high-risk pools to aid people

priced out of coverage • Americans should have a chance to buy health insurance regardless

of whether they are sick, and • The government should have a role in setting some regulations and

helping people pay for getting insurance • No estimate of the cost or savings of major components • No estimate of how many people covered compared to ACA.

41 #cbizmhmwebinar

ADMINISTRATIVE UPDATE

42 #cbizmhmwebinar

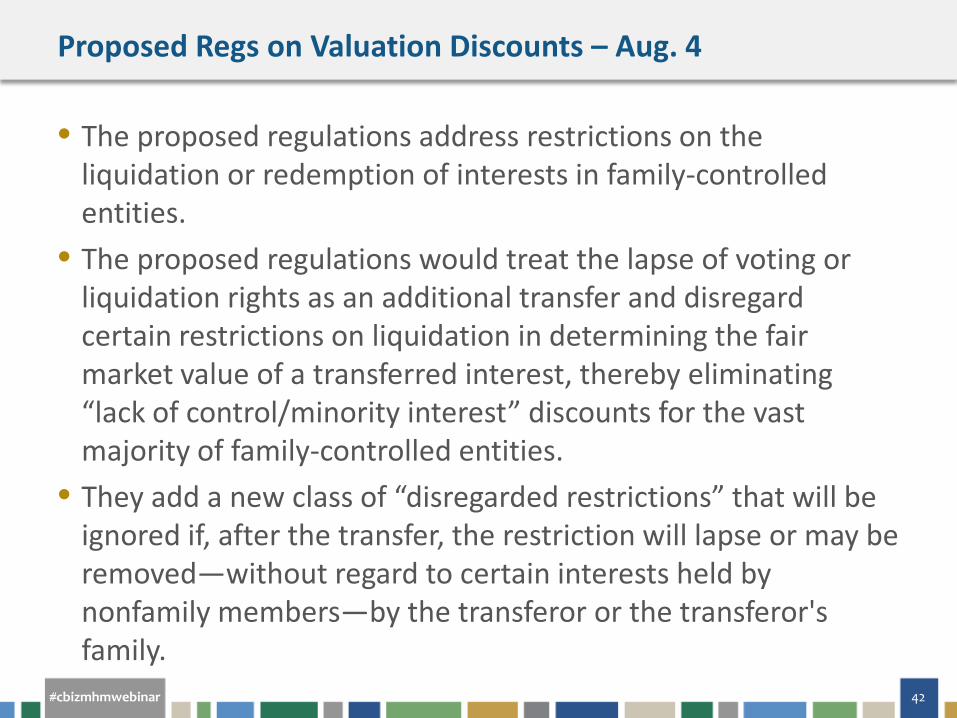

Proposed Regs on Valuation Discounts – Aug. 4

• The proposed regulations address restrictions on the liquidation or redemption of interests in family-controlled entities.

• The proposed regulations would treat the lapse of voting or liquidation rights as an additional transfer and disregard certain restrictions on liquidation in determining the fair market value of a transferred interest, thereby eliminating “lack of control/minority interest” discounts for the vast majority of family-controlled entities.

• They add a new class of “disregarded restrictions” that will be ignored if, after the transfer, the restriction will lapse or may be removed—without regard to certain interests held by nonfamily members—by the transferor or the transferor's family.

43 #cbizmhmwebinar

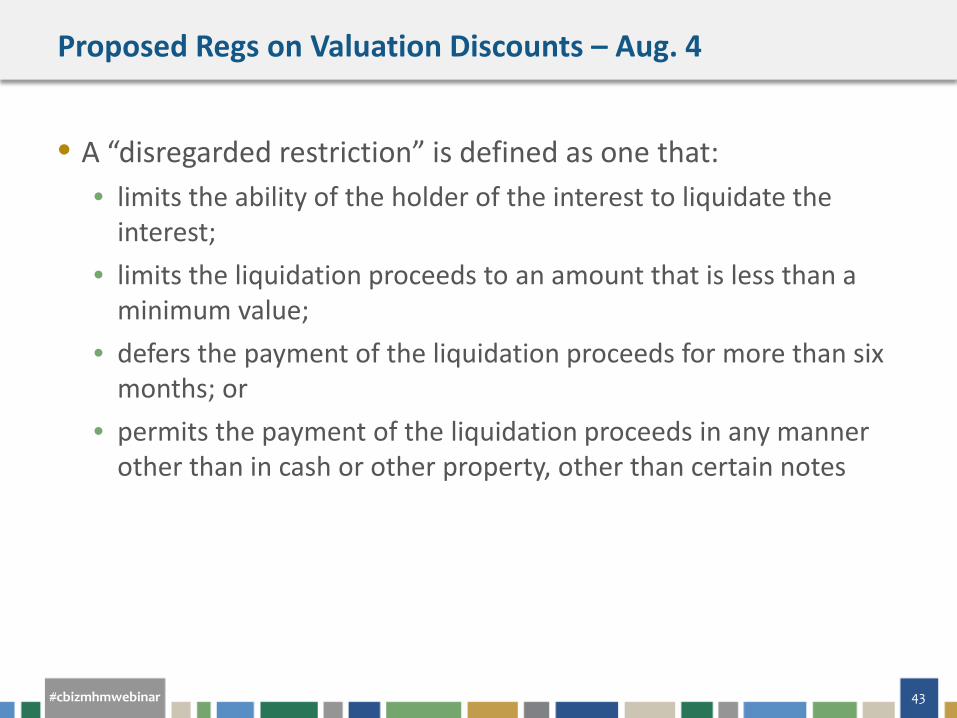

Proposed Regs on Valuation Discounts – Aug. 4

• A “disregarded restriction” is defined as one that: • limits the ability of the holder of the interest to liquidate the

interest; • limits the liquidation proceeds to an amount that is less than a

minimum value; • defers the payment of the liquidation proceeds for more than six

months; or • permits the payment of the liquidation proceeds in any manner

other than in cash or other property, other than certain notes

44 #cbizmhmwebinar

Proposed Regs on Valuation Discounts – Aug. 4

• On September 29, a group of Republican Senate lawmakers have asked Treasury Secretary Jack Lew not to move forward with Code Sec. 2704 proposed regulations.

• "The proposed regulations eliminate or greatly reduce the discounts for lack of control and lack of marketability for family farms and businesses and will thus discourage families from continuing to operate and build their businesses," the GOP lawmakers wrote. "If finalized in their current form, it will significantly increase the estate tax burden on family businesses."

• Lawmakers added that, under the proposed regulations, family-owned businesses would be at a greater disadvantage relative to other types of businesses.

45 #cbizmhmwebinar

JUDICIAL UPDATE

46 #cbizmhmwebinar

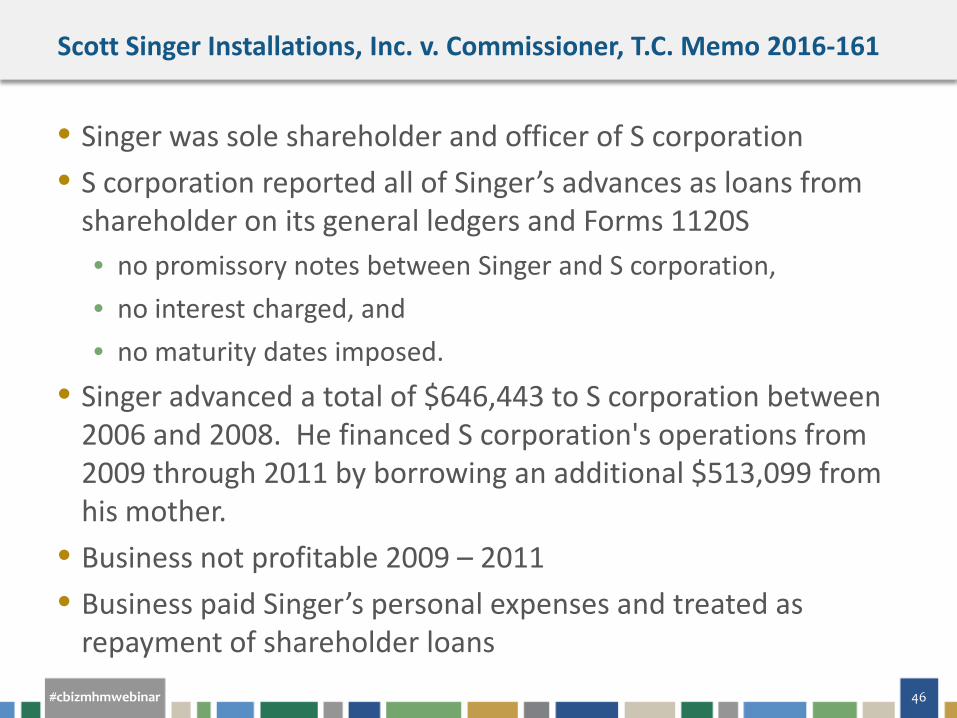

Scott Singer Installations, Inc. v. Commissioner, T.C. Memo 2016-161

• Singer was sole shareholder and officer of S corporation • S corporation reported all of Singer’s advances as loans from

shareholder on its general ledgers and Forms 1120S • no promissory notes between Singer and S corporation, • no interest charged, and • no maturity dates imposed.

• Singer advanced a total of $646,443 to S corporation between 2006 and 2008. He financed S corporation's operations from 2009 through 2011 by borrowing an additional $513,099 from his mother.

• Business not profitable 2009 – 2011 • Business paid Singer’s personal expenses and treated as

repayment of shareholder loans

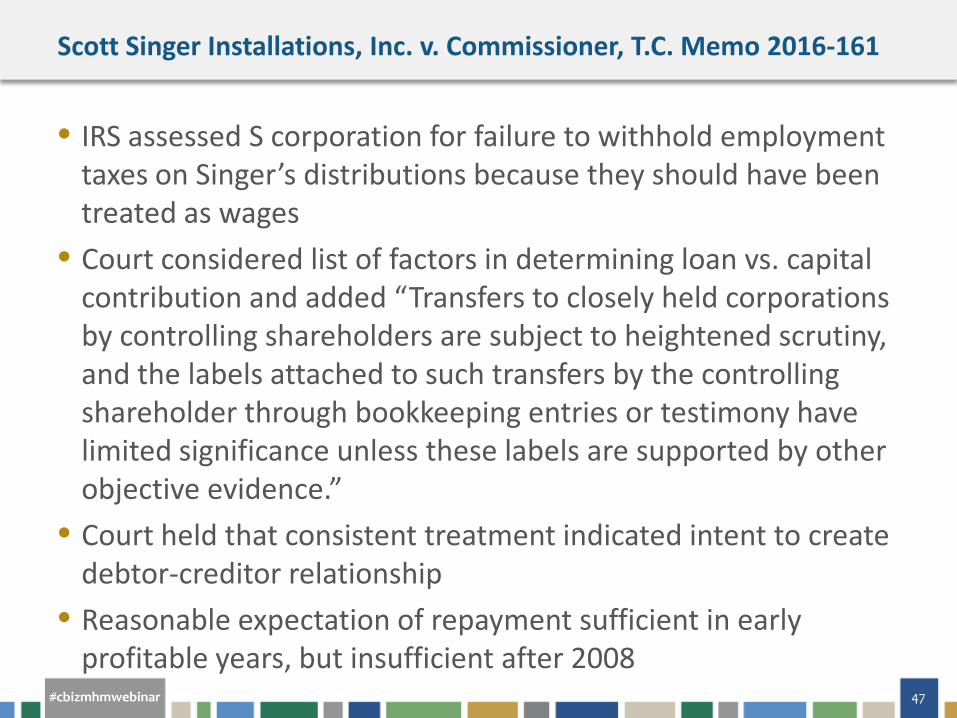

47 #cbizmhmwebinar

Scott Singer Installations, Inc. v. Commissioner, T.C. Memo 2016-161

• IRS assessed S corporation for failure to withhold employment taxes on Singer’s distributions because they should have been treated as wages

• Court considered list of factors in determining loan vs. capital contribution and added “Transfers to closely held corporations by controlling shareholders are subject to heightened scrutiny, and the labels attached to such transfers by the controlling shareholder through bookkeeping entries or testimony have limited significance unless these labels are supported by other objective evidence.”

• Court held that consistent treatment indicated intent to create debtor-creditor relationship

• Reasonable expectation of repayment sufficient in early profitable years, but insufficient after 2008

48 #cbizmhmwebinar

• In EOW for 1st Quarter 2014 we reported on the Shea Homes case, which was affirmed by the 9th Cir. On August 24

• Developer of planned residential communities purchased land, constructed infrastructure and amenities as common improvements, and constructed homes.

• Developer marketed the community and the life-style of the development, not just the individual home itself.

• Before the buyer and seller closed on a home, the seller was required to construct all common improvements or post a performance bond.

Shea Homes, Inc. v. Comm’r, 142 T.C. 3, aff’d Aug. 24 by 9th Cir.

49 #cbizmhmwebinar

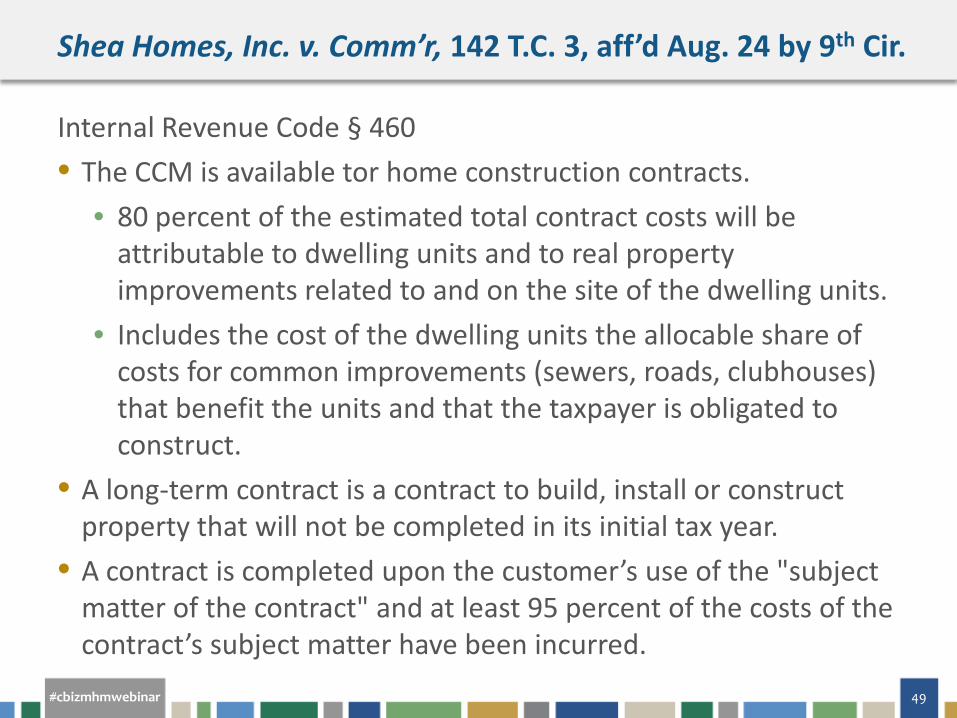

Internal Revenue Code § 460 • The CCM is available tor home construction contracts.

• 80 percent of the estimated total contract costs will be attributable to dwelling units and to real property improvements related to and on the site of the dwelling units.

• Includes the cost of the dwelling units the allocable share of costs for common improvements (sewers, roads, clubhouses) that benefit the units and that the taxpayer is obligated to construct.

• A long-term contract is a contract to build, install or construct property that will not be completed in its initial tax year.

• A contract is completed upon the customer’s use of the "subject matter of the contract" and at least 95 percent of the costs of the contract’s subject matter have been incurred.

Shea Homes, Inc. v. Comm’r, 142 T.C. 3, aff’d Aug. 24 by 9th Cir.

50 #cbizmhmwebinar

• Taxpayer: the subject matter of the contracts was the entire development, and that completion did not occur until the final road is paved and the final performance bond is released.

• IRS : each contract was completed when the home escrow closed, and common improvements to the developments were secondary items and that these costs should not be counted in applying the 95 percent threshold.

• Tax Court: the subject matter of the contract was the entire development, and the developer was obligated to provide amenities and infrastructure as part of the contract. The Court considered: • The lifestyle advertised for the developments • The amounts budgeted and incurred for indirect costs • The performance bonds securing completion of the common improvements • The obligations imposed by the CC&Rs (Covenants, Conditions and

Restrictions)

• Homeowners’ Association rules

Shea Homes, Inc. v. Comm’r, 142 T.C. 3 Shea Homes, Inc. v. Comm’r, 142 T.C. 3, aff’d Aug. 24 by 9th Cir.

51 #cbizmhmwebinar

• 9th Cir.: • The IRS “took the very crabbed view that the subject matter was limited

to the house and the lot.” “We suspect that the Commissioner was satisfied that his position on those points would win the day and, therefore, that he need not concentrate his firepower on the overall planned community development aspect of the contracts. The resulting outcome was due to his misperception rather than a Tax Court mistake.”

• Caution • Very fact specific case where the court conducted extensive analysis of

the contract laws of numerous states. • Based in part on the lack of clarity in the regulations, and similar cases

are currently working their way through the system. • Treasury has indicated that it may change the regulations

Shea Homes, Inc. v. Comm’r, 142 T.C. 3 Shea Homes, Inc. v. Comm’r, 142 T.C. 3, aff’d Aug. 24 by 9th Cir.

52 #cbizmhmwebinar

Voss v Comm’r, 2015-2 U.S.T.C. ¶50,427 (9th Cir.)

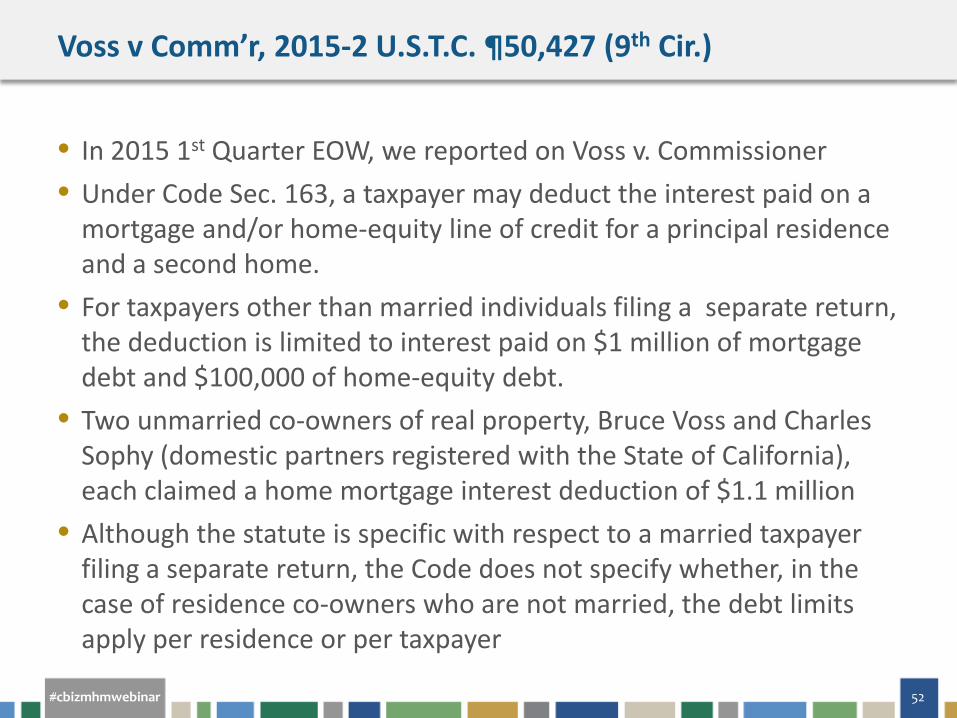

• In 2015 1st Quarter EOW, we reported on Voss v. Commissioner • Under Code Sec. 163, a taxpayer may deduct the interest paid on a

mortgage and/or home-equity line of credit for a principal residence and a second home.

• For taxpayers other than married individuals filing a separate return, the deduction is limited to interest paid on $1 million of mortgage debt and $100,000 of home-equity debt.

• Two unmarried co-owners of real property, Bruce Voss and Charles Sophy (domestic partners registered with the State of California), each claimed a home mortgage interest deduction of $1.1 million

• Although the statute is specific with respect to a married taxpayer filing a separate return, the Code does not specify whether, in the case of residence co-owners who are not married, the debt limits apply per residence or per taxpayer

53 #cbizmhmwebinar

Voss v Comm’r, 2015-2 U.S.T.C. ¶50,427 (9th Cir.)

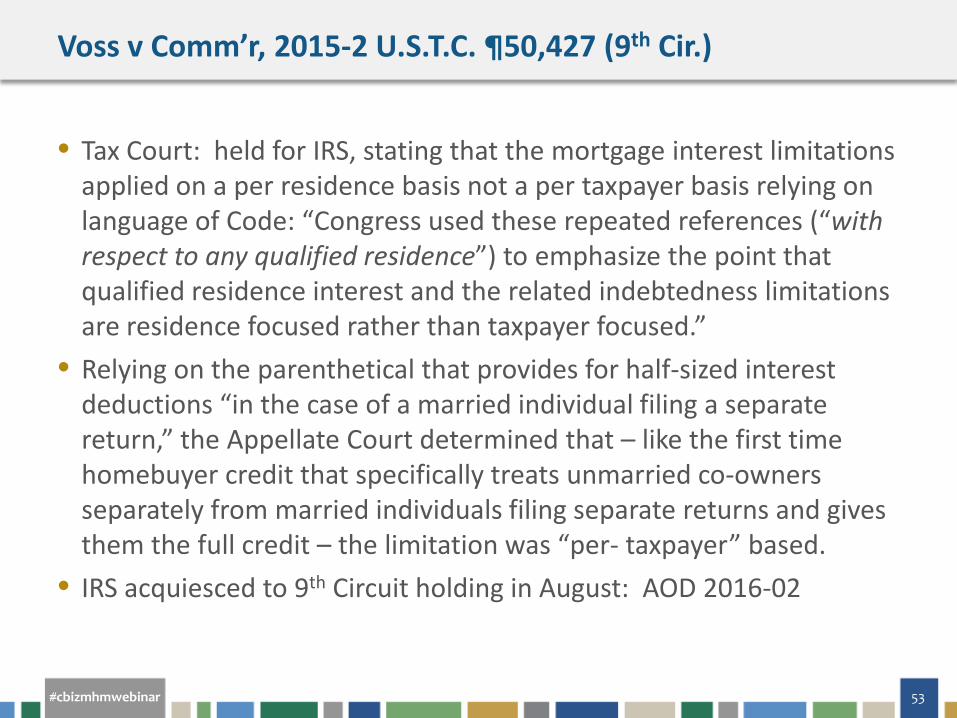

• Tax Court: held for IRS, stating that the mortgage interest limitations applied on a per residence basis not a per taxpayer basis relying on language of Code: “Congress used these repeated references (“with respect to any qualified residence”) to emphasize the point that qualified residence interest and the related indebtedness limitations are residence focused rather than taxpayer focused.”

• Relying on the parenthetical that provides for half-sized interest deductions “in the case of a married individual filing a separate return,” the Appellate Court determined that – like the first time homebuyer credit that specifically treats unmarried co-owners separately from married individuals filing separate returns and gives them the full credit – the limitation was “per- taxpayer” based.

• IRS acquiesced to 9th Circuit holding in August: AOD 2016-02

54 #cbizmhmwebinar

? QUESTIONS

55 #cbizmhmwebinar

If You Enjoyed This Webinar…

Upcoming Courses: • 11/7 & 11/22: Implementing Revenue Recognition • 11/15 & 12/1: Individual Year-End Tax Planning Tips for 2016 and Beyond

• 11/30: Accounting for Impairment under the Credit Loss Impairment Rules

• 12/6: Understanding Complex Debt and Equity Transactions

Recent Publications: • Highlights from the IRS Tax-Exempt and Government Entities Division

2017 Work Plan • Understanding the Leasing Standard: Sale and Leaseback and Other Types

of Lease Transactions • Nexus Implications for E-commerce Businesses

56 #cbizmhmwebinar

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ