weekly market revie · 2014-11-25 · moody’s affirmed saudi-based islamic development bank’s...

TRANSCRIPT

Weekly Market Review 26th October 2014 - 1st November 2014

CONTENTS

International Equity Markets

GCC Equity

Currencies

Commodities

Interest Rates

Equity Markets - Top Most & Bottom Most

Commodity Markets - Top Most & Bottom Most

US Fed confirmed on Oct 29, it will end its monthly asset purchase program while maintaining pledge to keep interest rates low for a “considerable time”

US consumer spending fell 0.2% in Sept after rising 0.5% in Aug, first decline since January

Thomson Reuters/University of Michigan's consumer sentiment index rose to 86.9 from 84.6 in Sept

Wages and salaries in US rose 0.8% in 3Q2014, the largest increase in more than six years

Euro zone inflation inched up by 0.4% in Oct, meeting expectations and dimming chances of any new ECB action

Unemployment remained unchanged at 11.5% in September

ECB failed 25 of the 130 Euro zone banks in 2013 health checks, but said that most have repaired their finances

Ifo’s business climate index for Germany fell to 103.2 from 104.7 in Sept, its lowest level in almost two years

GfK's UK consumer confidence index fell to -2 in Oct from -1 in Sept

Nielsen Global Consumer Confidence Index rose 1 point in 3Q2014 to 98. India remained the most bullish consumer market, while Italy became the most pessimistic

Bank of Japan (BoJ) announced it would expand its asset-buying program by as much as 33%, by not just only buying more government bonds but also stocks and real-estate funds

BoJ cut its growth forecast for the fiscal year to March to 0.5% from earlier 1%

Core inflation forecast was cut to 1.2% from earlier 1.3% for 2014-15 and to 1.7% from 1.9% for 2016-17

Japan household spending fell 5.6% YoY while it grew 1.5% MoM in Sept

China’s manufacturing further slowed as official PMI came at 50.8 in October vs. 51.1 in September

HSBC Russia manufacturing PMI fell to 50.3 from 50.4 in September as demand for Russian exports fell

Brazil’s central bank surprisingly raised its benchmark Selic rate by 25 bps to 11.25%

Argentina’s industrial output shrank 1.7% YoY in Sept, marking the 14th consecutive monthly decline

S&P 500 – 1 year performance Euro Stoxx 600 – 1 year performance

Source: Bloomberg, Mashreq Private Banking

INTERNATIONAL EQUITY MARKETS

Last Close Change 5 Day % YTD %

S&P 500 2,018.05 53.47 2.72 9.18

DJI 17,390.52 585.11 3.48 4.91

Nasdaq Comp 4,630.74 147.03 3.28 10.87

Euro Stoxx 600 336.80 9.63 2.94 2.60

FTSE 100 6,546.47 157.74 2.47 -3.00

Dax 9,326.87 339.07 3.77 -2.36

CAC 40 4,233.09 104.19 2.52 -1.46

Nikkei 225 16,413.76 1,122.12 7.34 0.75

Hang Seng 23,998.06 695.86 2.99 2.97

Brazil - Bovespa 54,628.60 2,687.87 5.17 6.06

Russia - Micex 1,488.47 108.08 7.83 -1.04

BSE Sensex 27,865.83 1,014.78 3.78 31.62

Shanghai Comp 2,420.18 117.90 5.12 14.38

Source: Bloomberg, Mashreq Private Banking

Amanat Holdings’ AED1.375bn IPO had been fully covered within a week since the subscriptions opened

Majid Al Futtaim is set to invest $683mn in the construction of a mall in Egypt which will include over 420 stores

Dubai-based Emaar properties reported a 37.4% YoY rise in its operating profit to AED2,489mn

National Bank of Abu Dhabi’s 3Q2014 net profit rose 32% YoY to AED1.37bn. Profit was down 3.7% QoQ

Emirates Integrated Telecom. Co. reported a 17.8% YoY rise in 3Q2014 net profit to QR558.7mn

Mashreq Bank’s 3Q2014 profit attributable to owners rose 26.1% YoY to AED596.8mn

Emaar Malls Group reported AED321.2mn net profit in 3Q2014 vs. AED206.97mn net profit in 3Q2013

Dubai Properties expects to complete the AED800mn Dubai Wharf project by 1Q2017

Fitch affirmed Tourism Development & Inv. Co.’s long & short-term Issuer Default rating with a Stable outlook

Saudi Arabia’s Petro Rabigh seeks about $8bn of loans to fund expansion which includes $2-2.5bn 16-yr bank loans

Saudi Telecom’s BoD approved the distribution of SR2bn dividend for 3Q2014

Moody’s affirmed Saudi-based Islamic Development Bank’s Credit Rating at ‘Aaa’ with a Stable outlook

Saudi-based SEDCO Capital, plans to arrange a club investment of up to $300mn in European real estate

Jindal Steel & Power to double Sohar plant’s steel making capacity, with an estimated investment of around $2bn

Qatar-based Barwa Real Estate Group plans to build a QR500mn mall consisting of about 650 retails shops in Doha

Qatar’s capital market regulator reduced the minimum capital requirement for SMEs wanting to be listed on venture market, expected to be operational by early 2015, to QR2mn from QR5mn

Kuwait-based Burgan Bank received regulatory approval to launch $74.8mn rights issue by the end of 2014

National Bank of Bahrain posted a 9M2014 net profit of BHD42.2mn, up 5.2% YoY. NII rose 3.9% YoY to BHD45.3mn

Bahrain Telecommunications Co. posted a 40% rise in its 3Q2014 net profit to BHD15.99mn

Last Close Change 5 Day % YTD %

Dubai 4,545.39 -27.66 -0.60 34.89

Abu Dhabi 4,861.45 31.62 0.65 13.31

Saudi Tadawul 10,034.92 -130.41 -1.28 17.57

Qatar Index 13,498.86 33.17 0.25 30.05

Kuwait Index 7,361.61 -53.14 -0.72 -2.49

Oman MSM 30 6,974.62 -35.09 -0.50 2.05

Bahrain All Share 1,444.13 7.09 0.49 15.64

Egypt EGX 30 9,115.63 318.34 3.62 34.39

Istanbul 100 Index

80,579.66 1,162.53 1.46 18.85

Source: Bloomberg, Mashreq Private Banking

DFMGI – 1 year performance Saudi Tadawul – 1 year performance

GCC EQUITIES

Source: Bloomberg, Mashreq Private Banking

The euro depreciated 1.15% in the week to 1.2525 per dollar, as the European Central Bank stepped up its stimulus efforts, buying covered bonds last week and saying it will expand into asset-backed securities in November

Japanese Yen tumbled 3.85% in the week to 112.32 per dollar, its weakest level in almost seven years, after Bank of Japan said it plans to expand the monetary base by Yen 80tn a year, up from a previous Yen 60tn to Yen 70tn

The pound fell 0.6% in the week for a 2nd week to 1.5995 per dollar, dropping for a fourth month, as traders pushed back expectations for when the Bank of England will raise interest rates amid signs of a slowing economic recovery

The Canadian dollar fell 0.31% in the week to 1.1266 per dollar after a report showed the economy shrank 0.1% in August to an annualized Canadian dollar 1.63tn

Brazil’s real declined 0.16% in the week to 2.4778 per dollar as the budget deficit widened to BRL69.4bn in October. The shortfall was the biggest since the series of data began in December 2001

India’s rupee weakened 0.14% in the week to 61.365 per dollar as the dollar got a boost after the US Federal Reserve struck a more hawkish tone than expected at its policy meeting

Russia’s ruble was down 2.87% in the week to 43.0095 per dollar, the most since 2011 after a larger-than-forecast increase of Russia’s key interest rate failed to ease concern that the economy will remain hobbled by sanctions and capital flight

Last Close Change 5 Day % YTD %

EUR/USD 1.2525 -0.0146 -1.15 -8.86

GBP/USD 1.5995 -0.0095 -0.59 -3.39

AUD/USD 0.8798 0.0005 0.06 -1.33

USD/JPY 112.3200 4.1600 3.85 6.66

USD/CHF 0.9626 0.0107 1.12 7.81

USD/CAD 1.1266 0.0035 0.31 6.05

USD/BRl 2.4778 0.0039 0.16 4.90

USD/RUB 43.0095 1.2010 2.87 30.85

USD/INR 61.3650 0.0837 0.14 -0.70

USD/CNY 6.1130 -0.0035 -0.06 0.97

DXY Index 86.9170 1.1850 1.38 8.60

EUR/USD – 1 year performance GBP/USD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

CURRENCIES

Source: Bloomberg, Mashreq Private Banking

Gold fell 4.7% in the week and posted a second consecutive monthly loss as the dollar strengthened after the Bank of Japan unexpectedly boosted stimulus and the Federal Reserve ended asset purchases in the week

Brent crude lost 0.3% in the week to $85.86 per barrel and fell 9.3% in the month, the biggest monthly decline since May 2012 as OPEC boosted production to a 14-month high amid a global surplus

Nickel futures on LME gained 5.13% in the week as worries about declining ore stocks in China set off a buying spree that, traders said, included purchases by consumers

Soybean futures rose 7.1% in the week on CBoT after surges in US export sales and strong demand for the oilseeds. Speculations that drought in Brazil will reduce planting also helped prices

Cocoa for delivery in December on the US ICE Futures exchange dropped 5% in the week as a stronger US dollar weighed on the market amid an influx of supplies from the top-growing region and worries about demand

Palm oil futures gained 4.37% in the week as leading industry analysts becomes more bullish on palm prices, due to seasonally weakening output caused by dry spells earlier in Malaysia, as well as the ongoing drought in the palm-growing region of Indonesia’s Kalimantan

Last Close Change 5 Day % YTD %

Gold spot 1,173.48 -57.42 -4.66 -2.67

Silver spot 16.16 -1.04 -6.06 -16.99

Copper-CMX 304.70 0.60 0.20 -9.25

Brent - ICE 85.86 -0.27 -0.31 -19.25

WTI - Nymex 80.54 -0.47 -0.58 -13.14

S&P GSCI Spot Index

539.59 2.49 0.46 -14.66

Baltic Dry Index 1,428.00 236.00 19.80 -37.29

WTI Crude – 1 year performance GOLD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

COMMODITIES

Source: Bloomberg, Mashreq Private Banking

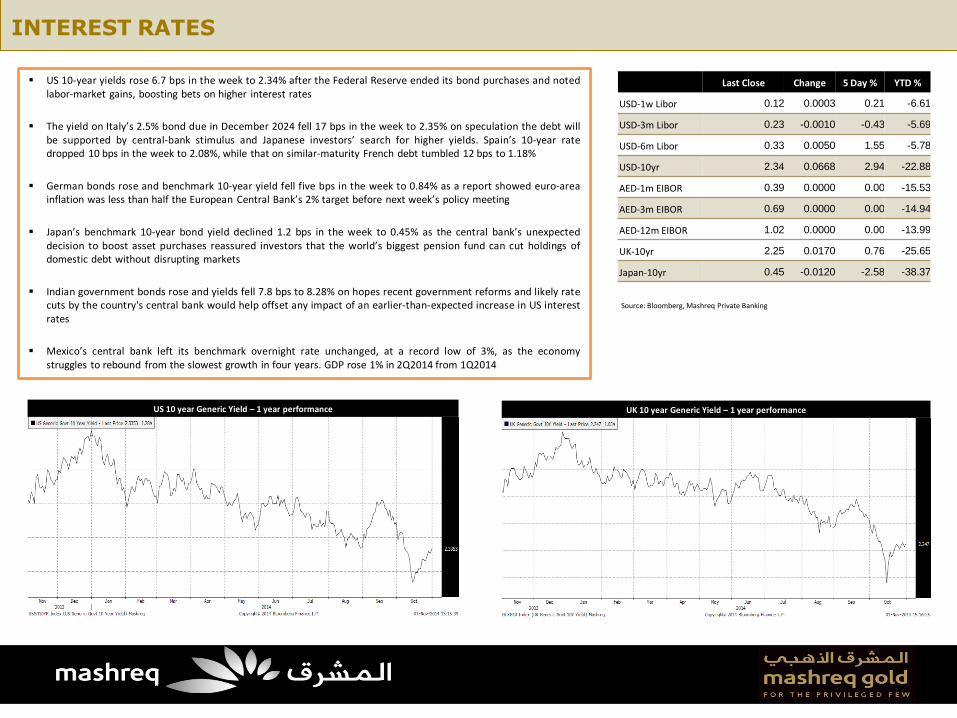

US 10-year yields rose 6.7 bps in the week to 2.34% after the Federal Reserve ended its bond purchases and noted labor-market gains, boosting bets on higher interest rates

The yield on Italy’s 2.5% bond due in December 2024 fell 17 bps in the week to 2.35% on speculation the debt will be supported by central-bank stimulus and Japanese investors’ search for higher yields. Spain’s 10-year rate dropped 10 bps in the week to 2.08%, while that on similar-maturity French debt tumbled 12 bps to 1.18%

German bonds rose and benchmark 10-year yield fell five bps in the week to 0.84% as a report showed euro-area inflation was less than half the European Central Bank’s 2% target before next week’s policy meeting

Japan’s benchmark 10-year bond yield declined 1.2 bps in the week to 0.45% as the central bank’s unexpected decision to boost asset purchases reassured investors that the world’s biggest pension fund can cut holdings of domestic debt without disrupting markets

Indian government bonds rose and yields fell 7.8 bps to 8.28% on hopes recent government reforms and likely rate cuts by the country's central bank would help offset any impact of an earlier-than-expected increase in US interest rates

Mexico’s central bank left its benchmark overnight rate unchanged, at a record low of 3%, as the economy struggles to rebound from the slowest growth in four years. GDP rose 1% in 2Q2014 from 1Q2014

Last Close Change 5 Day % YTD %

USD-1w Libor 0.12 0.0003 0.21 -6.61

USD-3m Libor 0.23 -0.0010 -0.43 -5.69

USD-6m Libor 0.33 0.0050 1.55 -5.78

USD-10yr 2.34 0.0668 2.94 -22.88

AED-1m EIBOR 0.39 0.0000 0.00 -15.53

AED-3m EIBOR 0.69 0.0000 0.00 -14.94

AED-12m EIBOR 1.02 0.0000 0.00 -13.99

UK-10yr 2.25 0.0170 0.76 -25.65

Japan-10yr 0.45 -0.0120 -2.58 -38.37

US 10 year Generic Yield – 1 year performance UK 10 year Generic Yield – 1 year performance

Source: Bloomberg, Mashreq Private Banking

INTEREST RATES

Source: Bloomberg, Mashreq Private Banking

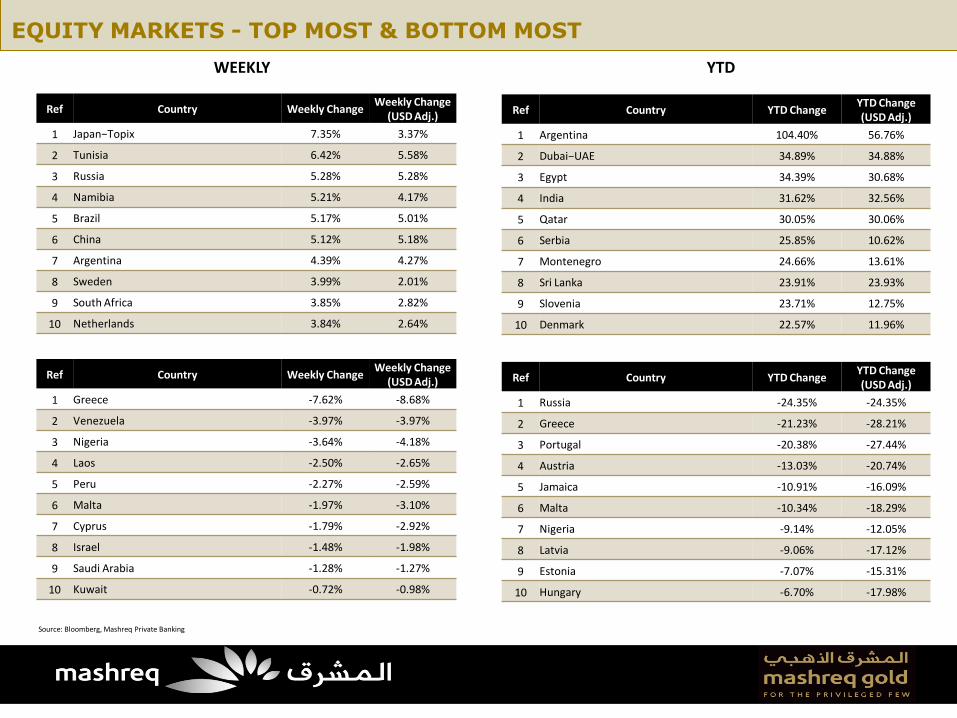

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Greece -7.62% -8.68%

2 Venezuela -3.97% -3.97%

3 Nigeria -3.64% -4.18%

4 Laos -2.50% -2.65%

5 Peru -2.27% -2.59%

6 Malta -1.97% -3.10%

7 Cyprus -1.79% -2.92%

8 Israel -1.48% -1.98%

9 Saudi Arabia -1.28% -1.27%

10 Kuwait -0.72% -0.98%

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Japan−Topix 7.35% 3.37%

2 Tunisia 6.42% 5.58%

3 Russia 5.28% 5.28%

4 Namibia 5.21% 4.17%

5 Brazil 5.17% 5.01%

6 China 5.12% 5.18%

7 Argentina 4.39% 4.27%

8 Sweden 3.99% 2.01%

9 South Africa 3.85% 2.82%

10 Netherlands 3.84% 2.64%

WEEKLY

Ref Country YTD Change YTD Change (USD Adj.)

1 Argentina 104.40% 56.76%

2 Dubai−UAE 34.89% 34.88%

3 Egypt 34.39% 30.68%

4 India 31.62% 32.56%

5 Qatar 30.05% 30.06%

6 Serbia 25.85% 10.62%

7 Montenegro 24.66% 13.61%

8 Sri Lanka 23.91% 23.93%

9 Slovenia 23.71% 12.75%

10 Denmark 22.57% 11.96%

YTD

Ref Country YTD Change YTD Change (USD Adj.)

1 Russia -24.35% -24.35%

2 Greece -21.23% -28.21%

3 Portugal -20.38% -27.44%

4 Austria -13.03% -20.74%

5 Jamaica -10.91% -16.09%

6 Malta -10.34% -18.29%

7 Nigeria -9.14% -12.05%

8 Latvia -9.06% -17.12%

9 Estonia -7.07% -15.31%

10 Hungary -6.70% -17.98%

EQUITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

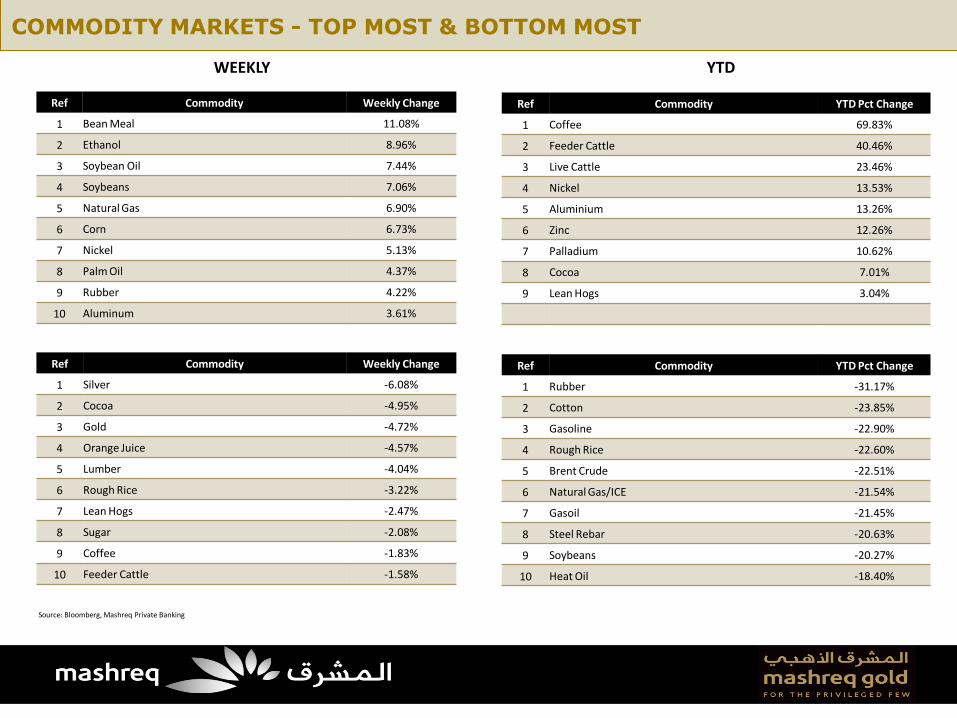

Ref Commodity Weekly Change

1 Silver -6.08%

2 Cocoa -4.95%

3 Gold -4.72%

4 Orange Juice -4.57%

5 Lumber -4.04%

6 Rough Rice -3.22%

7 Lean Hogs -2.47%

8 Sugar -2.08%

9 Coffee -1.83%

10 Feeder Cattle -1.58%

Ref Commodity Weekly Change

1 Bean Meal 11.08%

2 Ethanol 8.96%

3 Soybean Oil 7.44%

4 Soybeans 7.06%

5 Natural Gas 6.90%

6 Corn 6.73%

7 Nickel 5.13%

8 Palm Oil 4.37%

9 Rubber 4.22%

10 Aluminum 3.61%

WEEKLY

Ref Commodity YTD Pct Change

1 Coffee 69.83%

2 Feeder Cattle 40.46%

3 Live Cattle 23.46%

4 Nickel 13.53%

5 Aluminium 13.26%

6 Zinc 12.26%

7 Palladium 10.62%

8 Cocoa 7.01%

9 Lean Hogs 3.04%

YTD

Ref Commodity YTD Pct Change

1 Rubber -31.17%

2 Cotton -23.85%

3 Gasoline -22.90%

4 Rough Rice -22.60%

5 Brent Crude -22.51%

6 Natural Gas/ICE -21.54%

7 Gasoil -21.45%

8 Steel Rebar -20.63%

9 Soybeans -20.27%

10 Heat Oil -18.40%

COMMODITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

IMPORTANT NOTICE

This report was prepared by the Private Banking Unit of Mashreqbank psc (“Mashreq”) in the United Arab Emirates (“U.A.E.”). Mashreq is regulated by the Central Bank of the U.A.E. This report is provided for informational purposes and private circulation only and should not be construed as an offer to sell or a solicitation to buy any security or any other financial instrument or adopt any hedging, trading or investment strategy. Prior to investing in any product, we recommend that you consult with a professional financial advisor, taking into consideration investment objectives, financial circumstances and tax implication. While based on information believed to be reliable, we do not guarantee and make no express or implied representation as to the accuracy of this report or complete description of the securities markets or developments referred to in this report. The information, opinions, forecasts (if any), assumptions or estimates contained in this report are as of the date indicated and are subject to change at any time without prior notice. The stated price of any securities mentioned in this report is as of the date indicated and is not a representation that any transaction can be effected at this price. The risks related to investment products described in this report are not all encompassing and investors should refer to the relevant investment offer document for detailed information and applicable terms and conditions. Investment products, including treasury products, are not guaranteed by Mashreq or any of its affiliates or subsidiaries unless stated otherwise and are subject to investment risk, including loss of principal. Investment products are not government insured. Past performance is not an indicator of future performance. US persons (US Citizens; US Green Card Holders; Resident Aliens subject to US income taxes for IRS purposes) are not eligible for any of the investment products introduced by Mashreq unless stated otherwise. This report is for distribution only under such circumstances as may be permitted by applicable law. Neither Mashreq nor its officers, directors or shareholders or other persons shall be liable for any direct, indirect, incidental or other damages including loss of profits arising in any way from the information contained in this report. This report is intended solely for the use by the intended recipients and the contents shall not be reproduced, redistributed or copied in whole or in part for any purpose without Mashreq’s prior express consent.