wei & zhang, 2008 ownership structure, cash flow, and capital investment_evidence from east...

TRANSCRIPT

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 1/15

Ownership structure, cash flow, and capital investment:

Evidence from East Asian economies before the financial crisis☆

K.C. John Wei a ,⁎, Yi Zhang b

a Department of Finance, Hong Kong University of Science and Technology, Clearwater Bay, Kowloon, Hong Kong

b Department of Finance, Guanghua School of Management, Peking University, Beijing 100871, China

Received 21 August 2007; received in revised form 31 January 2008; accepted 14 February 2008

Available online 26 February 2008

Abstract

Using financial and ownership data from eight East Asian emerging markets before the Asian financial crisis, we document that

while the sensitivity of a firm's capital investment to its cash flow decreases as the cash-flow rights of its largest shareholders

increase, this sensitivity increases as the degree of the divergence between the control rights and cash-flow rights of the firm's

largest shareholders increases. We interpret the results to be consistent with the free cash-flow hypothesis, which postulates that too

much free cash flow in the hands of entrenched managers is likely to lead to overinvestment. This is particularly true for firms with

the greatest divergence between the largest shareholders' control rights and their cash-flow rights and for firms with lower

profitability.

© 2008 Elsevier B.V. All rights reserved.

JEL classification: G32; G34

Keywords: Investment-cash flow sensitivity; Capital investment; Pyramids; Voting rights; Cash-flow rights; East Asia

1. Introduction

The effect of cash flow on capital investment has been extensively studied with the role that financing constraints

play receiving the most attention. In a perfect market without asymmetric information or financial constraints, a firm's

cash flow should not affect its capital investments. Instead, capital investments should be solely determined by the

Available online at www.sciencedirect.com

Journal of Corporate Finance 14 (2008) 118 –132www.elsevier.com/locate/jcorpfin

☆ The previous versions of the paper were titled “Ownership structure, cash flow, and corporate investment: evidence from East Asian emerging

markets” and “Corporate governance, overinvestment and the Asian financial crisis”. The authors appreciate helpful comments and suggestions from

Dolly King, Yrjo Koskinen, and seminar participants at Hong Kong University of Science and Technology, Peking University, the 2005 Chinese

Finance Annual Meetings, where it was awarded the third prize for best papers, the 4th NTU International Conference on Economics, Finance and

Accounting in Taipei, the 2006 JBF Conference in Beijing, the 2006 China International Conference in Finance, where it was named the winner of the

best paper award, and the 2006 European Finance Association meetings in Zurich. The authors also wish to thank Jeffry M. Netter (the editor) and an

anonymous referee for insightful comments and suggestions and Dr. Virginia Unkefer for editorial assistance. John Wei acknowledges financial

support from an RGC Competitive Earmarked Research Grant of the Hong Kong Special Administration Region, China (HKUST6014/01H) and Yi

Zhang acknowledges financial support from the National Science Foundation of China (70603001).⁎ Corresponding author. Tel.: +852 2358 7676; fax: +852 2358 1749.

E-mail addresses: [email protected] (K.C.J. Wei), [email protected], [email protected] (Y. Zhang).

0929-1199/$ - see front matter © 2008 Elsevier B.V. All rights reserved.doi:10.1016/j.jcorpfin.2008.02.002

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 2/15

firm's investment opportunities. However, in the real market, although firms tend to invest more following increases in

their stock prices, cash flow is a better predictor than stock prices of a firm's capital investments.1

There are two competing explanations for the positive relation between cash flow and corporate investments. The

first explanation is based on the agency costs of free cash flow as suggested by Jensen (1986). Jensen shows that

managers have a tendency to overspend their free cash flow on unprofitable projects for their own private benefits. This

free cash-flow hypothesis suggests that the positive relation between cash flow and investment is basically a symptomof overinvestment . Firms tend to overinvest, not because external capital is too expensive, but because internal capital

is too inexpensive. The alternative explanation is based on asymmetric information. For example, Myers and Majluf

(1984) show that the cost of external funds is more expensive than is the cost of internal funds due to asymmetric

information problems. This asymmetric information hypothesis argues that the positive relation between cash flow and

investment is typically a symptom of underinvestment . Firms tend to pass up some positive net present value projects

because the cost of external capital is too high compared with the cost of internal capital.

The empirical results from Fazzari et al. (1988), Hoshi et al. (1991), and other follow-up studies seem to support the

asymmetric information hypothesis. These studies show that financially constrained firms tend to have higher

investment-cash flow sensitivities. Further, Lamont (1997) and Shin and Stulz (1998) document that capital invest-

ments by segments of a diversified firm depend on the cash flow from other segments. These results suggest that

because the cost of external capital is significantly more expensive than the cost of internal capital, financial constraintsare an important factor when a firm makes its investment decisions. However, Kaplan and Zingales (1997) provide both

theoretical arguments and empirical evidence that investment-cash flow sensitivities are not good indicators of

financial constraints. Whether or not investment-cash flow sensitivities are valid measures of financial constraints is

still the subject of debate.2

The existing studies on investment-cash flow sensitivities seldom consider the overinvestment argument caused by the

agency problem, which creates conflicts between managers and shareholders (Jensen and Meckling, 1976).3 Recent

studies suggest that since large shareholders have strong incentives to maximize the value of the stocks they own, large

shareholders can help to overcome this agency problem.4 However, large shareholders are also associated with negative

entrenchment effects.5 The empirical results from Morck et al. (1988) and McConnell and Servaes (1990) appear to

substantiate both the enhancement and entrenchment effects of large shareholders. They find an inverse U-shaped relation

between managerial equity ownership and firm valuation. That is, firm valuation initially increases as managerial

ownership increases. However, after a certain point, firm value starts to decrease as managerial ownership increases, because managers become entrenched and start to pursue their private benefits at the expense of outside investors.6

Hadlock (1998) argues that if the positive investment-cash flow relation is caused by a managerial preference to

overinvest internal funds, then the positive investment-cash flow sensitivity should decrease as the alignment of interests

between managers and shareholders increases. On the other hand, if the positive investment-cash flow relation is caused by

a managerial preference for underinvestment, the positive investment-cash flow sensitivity should increase as the

alignment of interests between managers and shareholders increases. Using managers' ownership data from 1975 as his

measure of the alignment of interests between managers and shareholders along with financial data from 1973–1976,

Hadlock (1998) finds an inverse U-shaped relation between managerial ownership and investment-cash flow sensitivities

for the U.S. firms in his sample. He interprets the results to be consistent with the underinvestment hypothesis caused by

asymmetric information.

In this paper, we extend Hadlock's (1998) work to use the information on both large shareholders' cash-flow rightsand the divergence between large shareholders' control rights and their cash-flow rights to disentangle the positive

1 See, for example, Fazzari et al. (1988) and Morck et al. (1990). Also see Hubbard (1998) for an excellent review of this literature.2 See, for example, Cleary (1999), Fazzari et al. (2000) and Kaplan and Zingales (2000).3 There are studies that empirically test agency problems and the overinvestment hypothesis from different angles. For example, Harvey et al.

(2004) find that debt mitigates agency problems associated with overinvestment. Dittmar et al. (2003), Pinkowitz et al. (2006), and Kalcheva and

Lins (in press) find evidence of overinvestment by entrenched managers related to cash holdings.4 For example, Shleifer and Vishny (1997, p. 754) point out, “Large shareholders thus address the agency problem in that they have both a general

interest in profit maximization, and enough control over the assets of the firm to have their interest respected ”.5 Again, Shleifer and Vishny (1997, p. 758) argue, “The large shareholders represent their own interests, which need not coincide with the

interests of other investors in the firm, or with the interests of employees and managers”.6

Stulz (1988) has formally modeled this negative effect of large shareholders on firm value, which predicts an inverse U-shaped relation betweenmanagerial ownership and firm value.

119 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 3/15

enhancement effect from the negative entrenchment effect of large shareholders. Using the information on both control

rights and cash-flow rights more effectively distinguishes between the two competing explanations for why cash flow

affects capital investment than does using the information on managerial cash-flow rights alone. Further, the existing

literature suggests that while the positive enhancement effect is related to the cash-flow rights of large shareholders, the

negative entrenchment effect is more associated with the control rights of large shareholders. However, as pointed out

by Claessens et al. (2002), it is difficult to separate the incentive effect from the entrenchment effect of largeshareholders using U.S. firms, since stocks in U.S. firms are widely held and there is little divergence between control

rights and cash-flow rights. In contrast, in East Asian emerging economies, many firms are owned and controlled by

single large shareholders via pyramid ownership structures. Many of the firms in these pyramid structures exhibit high

ownership concentration and high levels of divergence between the control rights and cash-flow rights of large

shareholders.7 Thus, East Asian corporations provide an excellent sample with which to study the effect of the

separation between the cash-flow rights and control rights of large shareholders on corporate investment.

The implication of Hadlock's (1998) results suggests that, if firms typically overinvest their internal capital, the

investment-cash flow sensitivity should decrease as the cash-flow rights of the large shareholders increase and this

sensitivity should increase as the divergence between the control rights and cash-flow rights of the large shareholders

increases. On the other hand, if asymmetric information typically raises the cost of external funds, we expect to observe

the opposite results. If the capital market is perfect and the availability of internal funds does not affect investment choices, then managerial ownership structures should not have any effect on the relation between cash flow and

corporate investment.

Using financial and ownership data from eight East Asian emerging markets during 1993–1996, our empirical

results support the overinvestment hypothesis caused by the agency costs of free cash flow. More specifically, the

investment-cash flow sensitivity is negatively related to the cash-flow rights of the largest shareholders, while this

sensitivity is positively associated with the divergence between the control rights and cash-flow rights of the largest

shareholders, especially among firms with lower returns on assets (ROA). Our results not only support the

overinvestment hypothesis, but also provide evidence for the positive enhancement effect related to the cash-flow

rights and the negative entrenchment effect associated with the control rights of the largest shareholders on corporate

investment. Our results complement those of Claessens et al. (2002), Lins (2003), and Joh (2003). These studies show

that firm valuation is negatively associated with the separation of cash-flow ownership from control.

Moreover, our evidence of overinvestment by East Asian corporations immediately before the Asian financial crisismay contribute to our understanding of this devastating financial crisis that began with the devaluation of the Thai baht

on July 2, 1997. Weak corporate governance, especially the divergence between the control rights and cash-flow rights

of large shareholders, has been cited as one of the causes of the crisis. Several studies have examined the impact of

corporate governance on firm performance during the East Asian financial crisis of 1997–1998. Johnson et al. (2000)

find that measures of corporate governance, particularly the effectiveness of protections for minority shareholders,

explain the extent of the exchange rate depreciation and the stock market decline during the crisis better than do

standard macroeconomic measures. Mitton (2002) finds that corporate governance and disclosure are positively related

to firm performance during the time of the crisis (1997–1998). Lemmon and Lins (2003) also offer similar results.

The rest of this paper is organized as follows. Section 2 discusses our hypothesis development. Section 3 describes

our data and empirical specifications. Section 4 reports our baseline results, while Section 5 presents the robustness

checks. Section 6 concludes the paper.

2. Hypothesis development

2.1. The overinvestment hypothesis resulting from the agency costs of free cash flow

The overinvestment hypothesis proposed by Jensen (1986) argues that managers have a tendency to overinvest

internally generated funds. Hadlock (1998) further argues that if the positive investment-cash flow relation is caused by a

7 See La Porta et al. (1999) and Claessens et al. (2000) for detailed discussions of ownership structures around the world and Asian firms,

respectively. Also see Claessens et al. (2002) for evidence on the incentive and entrenchment effects of the largest shareholders on firm value in East Asian corporations.

120 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 4/15

managerial preference to overinvest internal funds, there should be a negative relation between the investment-cash flow

sensitivity and the alignment of interests between managers and shareholders. In East Asia, ownership is concentrated as

opposed to being diffused as in the U.S. In addition, in East Asian economies, many firms are owned and controlled by

single large shareholders via pyramid ownership structures. In these economies, the nature of agency problems shifts

away from the conflicts of interest between managers and shareholders to the conflicts of interest between controlling

owners or large shareholders (who happen to be managers in most cases) and minority shareholders.In this case, there are two effects on the overinvestment problem: the enhancement effect related to cash-flow rights

and the entrenchment effect associated with the control rights of large shareholders ( Claessens et al., 2002). The

overinvestment problem is alleviated when large shareholders have a high level of cash-flow rights, since their interests

are more aligned with those of minority shareholders. Conversely, the overinvestment problem is aggravated when there

is a high level of divergence between the control rights and cash-flow rights of large shareholders, since their interests are

less aligned with those of minority shareholders. The above discussion leads to the following testable hypothesis:

Hypothesis 1. If large shareholders have a preference for overinvestment resulting from the agency costs of free cash

flow, the investment-cash flow sensitivity decreases as the level of large shareholders' cash-flow rights increases, while

this sensitivity increases as the degree of divergence between large shareholders' control rights and their cash-flow

rights increases.

2.2. The underinvestment hypothesis resulting from asymmetric information problems in the capital markets

There is an alternative view based on asymmetric information problems. Myers and Majluf (1984) show how a firm

may underinvest in the presence of asymmetric information problems in the capital markets. Hadlock (1998) further

suggests that if the positive investment-cash flow sensitivity is caused by a managerial preference for underinvestment,

there should be a positive relation between the investment-cash flow sensitivity and the alignment of interests between

managers and shareholders.8 We can extend Hadlock's argument to infer that the underinvestment problem is aggravated

when large shareholders have a high level of cash-flow rights or when there is little divergence between the control rights

and cash-flow rights of large shareholders. The above discussion leads to the following testable hypothesis.

Hypothesis 2. If large shareholders have a preference for underinvestment resulting from asymmetric information problems in the capital markets, the investment-cash flow sensitivity increases as large shareholders' cash-flow rights

increase and decreases as the divergence between large shareholders' control rights and cash-flow rights increases.

3. Data description and empirical specification

3.1. Sample selection

We start with all firms in East Asia from 1991–1996 that appeared on the Worldscope tape. Regarding ownership

data, we focus on ultimate ownership. We use ownership data assembled by Claessens et al. (2000).9 Claessens et al.

(2000) collected 1996 data on the ownership of corporations in Hong Kong, Indonesia, Japan, Korea, Malaysia, the

Philippines, Singapore, Taiwan, and Thailand. Their main source was Worldscope, supplemented by other sources that describe ownership structures. From a complete sample of 5284 publicly listed corporations in the nine East Asian

countries, ownership data were collected for 2980 firms. The procedure of identifying ultimate owners is similar to the

one used by La Porta et al. (1999). An ultimate owner is defined as the shareholder who has the determining voting rights

of the company and is not controlled by anybody else. If a company does not have an ultimate owner, it is classified as

widely held. To economize on the data collection task, the ultimate owners' voting right level is set at 50% and not traced

any further once the level exceeds 50%. Although a firm can have more than one ultimate owner, we focus on the largest

ultimate owner. As our definition of ownership relies on both cash-flow rights and voting control rights, the cash-flow

8 Dybvig and Zender (1991) show that the underinvestment problem is alleviated when large shareholders have few cash-flow rights.9

The dataset is also used by Claessens et al. (2002) and Fan and Wong (2002). We thank Joseph Fan and Larry Lang for their generousness in providing us with their ownership data.

121 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 5/15

rights that support the control by ultimate owners are further identified. Firm-specific information on pyramid ownership

structures and crossholdings is used to draw the distinction between cash-flow rights and control rights.

In our analysis, we use a subset of these firms. First, we exclude from the sample all Japanese firms. Most Japanese

firms have dispersed ownership structures, and ownership and management are separated far more often in Japan than

in other East Asian economies. The most important shareholders in most Japanese firms are widely held financial

institutions, again unlike in many other economies in the region. These financial institutions and their affiliated firmsoften work together to influence the governance of their corporations. Thus, including Japan in our sample would be

less useful for disentangling the incentive and entrenchment effects of concentrated ownership and control. Second, we

follow the literature to exclude firms that operate in financial industries (SIC 6000–6999) and regulated utilities (SIC

4900–4999), since their investment behavior should be different from the investment behaviors of other industries. We

then merge the ownership data with the Worldscope financial data.

We use the Worldscope database instead of the PACAP database, because PACAP does not provide firms' capital

expenditures. Though capital expenditures could be inferred from other accounting data, different accounting standards

in each country would lead to incomparable measures of capital expenditures. There are many firms with missing

capital expenditures in the Worldscope database. We dropped these firm-years from our sample. We also dropped firm-

years with missing values on variables such as assets, lagged assets, lagged Tobin's Q, and lagged sales. The merger of

the 1996 ownership data with the 1993–

1996 financial data requires us to assume that the ownership and controlstructures of the firms did not change substantially during that period. This is a reasonable assumption, since the

economic and political conditions were relatively stable during our sample period. These sample selection criteria

result in a final sample of 2555 firm-years from 994 corporations in eight East Asian economies over the period of

1993–1996.10 To include as many observations as possible, we use unbalanced panel data in our analyses, although we

also analyze a smaller balanced panel dataset in the robustness checks. Broken down by economies, the sample covers

458 firm-years for 193 firms from Hong Kong, 288 firm-years for 101 firms from Indonesia, 477 firm-years for 202

firms from Korea, 390 firm-years for 127 firms from Malaysia, 133 firm-years for 60 firms from the Philippines, 397

firm-years for 143 firms from Singapore, 194 firm-years for 91 firms from Taiwan, and 218 firm-years for 77 firms

from Thailand.

3.2. Summary statistics of ownership structures

Panel A of Table 1 documents the largest shareholders' control rights, cash-flow rights, and the difference between

control rights and cash-flow rights in eight East Asian economies. The definition of cash-flow rights and control rights

follows Claessens et al. (2000) and Claessens et al. (2002). The mean of the largest shareholders' control rights is

29.31% and the median is 28.00%. The mean of the largest shareholders' cash-flow rights is 24.44% and the median is

24.00%. The mean of the difference between control rights and cash-flow rights is 4.88%. This is not a large difference

because over half the firms in the sample do not exhibit a separation between control rights and cash-flow rights. A

quarter of the firms have a difference between control rights and cash-flow rights that is larger than 9%. The maximum

of the difference between control rights and cash-flow rights is 38%. This shows that the difference between control

rights and cash-flow rights of the largest shareholders is very significant in over a quarter of East Asian corporations.

3.3. Summary statistics of firm characteristics

Panel B of Table 1 presents summary statistics of firm characteristics for the entire sample and for sub-samples

based on the largest shareholders' cash-flow rights quartiles. We note that investment, cash flow, and asset size vary

significantly across quartiles based on the largest shareholders' cash-flow rights. However, interpreting the variations

in the summary statistics on the reported variables across cash-flow quartiles as evidence for or against the presence of

underinvestment or overinvestment may be problematic or premature. We do not make any inferences directly based on

these summary statistics.

10

The two extreme percentiles of firm-year observations of cash flow/assets, investment/assets, and lagged sales/assets are eliminated from thesample. Our results remain unchanged without this elimination procedure.

122 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 6/15

3.4. Empirical specification

To investigate the role of ownership structures on investment-cash flow sensitivities, we use the same basic

approach as Fazzari et al. (1988) and others. These authors regress investment on Tobin's Q, cash flow, and other control variables. They interpret differences in the investment-cash flow relationship between different groups of firms

as evidence of financial constraints. Hadlock (1998) interacts cash flow with managerial cash-flow rights to examine

the managerial enhancement effect on investment. To examine the managerial entrenchment effect on investment, we

interact cash flow with “the difference between the largest shareholders' control rights and their cash-flow rights”

(denoted as “Divergence” or “Control minus ownership”). Based on the discussion above, we use the following

regression model to perform our tests:

I it

Ai;t 1

¼ b0 þ b1Qi;t 1 þ b2

CFit

Ai;t 1

þ b3

CFit

Ai;t 1

Cashright i;t 1 þ b4

CFit

Ai;t 1

Divergencei;t 1 þ BY it þ eit ; ð1Þ

where I is investment, A is assets, Q is a measure of Tobin's Q, CF is cash flow, Cashright is the largest shareholder's

cash-flow rights, Divergence is the largest shareholder's control rights minus his/her cash-flow rights, and Y is a set of

Table 1

Summary statistics

Panel A: control rights and cash-flow rights of the largest ultimate owners

# of firms Mean SE Minimum 1st quartile Median 3rd quartile Maximum

Control rights (%)

974 29.31 12.33 0.00 22.00 28.00 36.00 63.00

Cash-flow rights (%)

974 24.44 12.40 0.00 15.00 24.00 32.00 59.00

The difference between control rights and cash-flow rights (%)

974 4.88 7.61 0.00 0.00 0.00 9.00 38.00

Panel B: summary statistics of relevant variables

Variable All firms Quartile 1 Quartile 2 Quartile 3 Quartile 4

Investment/Assets (%) 6.52 6.63⁎⁎ 7.11⁎⁎ 5.45⁎⁎ 7.14⁎⁎

Tobin's Q 1.30 1.22 1.31 1.32 1.37⁎⁎

Cash flow/Assets (%) 8.04 6.26⁎⁎ 8.05 8.28⁎⁎ 9.74⁎⁎

Sales/Assets (%) 67.10 67.60 70.30⁎⁎ 59.50⁎⁎ 68.90

Market cap (in million $) 201.20 243.50 222.53 198.50⁎⁎ 137.80⁎⁎

Total assets (in million $) 284.10 449.00⁎⁎ 298.60⁎⁎ 249.90⁎⁎ 185.80⁎⁎

Debt ratio (%) 28.10 31.70⁎⁎ 27.20 25.60 27.60⁎⁎

ROA (%) 5.48 4.95⁎⁎ 5.70 5.20⁎⁎ 6.51⁎⁎

Current ratio ($) 1.33 1.31 1.34 1.34 1.33

Number of observations 2555 643 621 699 592

Panel A of this table reports ownership structures (in percent) of the largest ultimate owners in East Asian firms. To be included in the sample, a firm

must have at least one year of capital expenditures and other financial data in the Worldscope database between 1993 and 1996 and have lagged

financial data as well. The ultimate ownership data is obtained from Claessens et al. (2000). Cash-flow rights and control rights are based on common

stock ownership. There are a total of 974 firms for the 1996 in the sample. Panel B reports summary statistics of relevant variables. All reported

figures are the medians and are calculated over the complete set of firm-years from 1993 to 1996. “Investment/Assets” is capital expenditures over

assets. “Tobin's Q” is the market value of equity plus assets minus the book value of equity over assets. “Cash flow/Assets” is operating cash flow

over assets. “Sales/Assets” is sales over assets in the previous year. “Market cap” is the market value of equity. “Total assets” is the total assets of the

firm. “Debt ratio” is total debt over asset. ROA is operating income over assets. Current ratio is current assets over current liabilities. Firms with the

cash-flow rights of the largest ultimate owners at or below the 25th percentile is classified as Quartile 1 firms, above the 25th percentile and below the

50th percentile as Quartile 2 firms, at or above the 50th percentile and at or below 75th percentile as Quartile 3 firms, and above the 75th percentile as

Quartile 4 firms. ⁎ and ⁎⁎ denote the median difference of the corresponding variable between the current ownership quartile and the next larger

ownership quartile at the 10% and 5% significant levels, respectively, using a Wilcoxon Rank-Sum test. In the Quartile 4 column, this denotes the test

of the difference between Quartile 4 and Quartile 1.

123 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 7/15

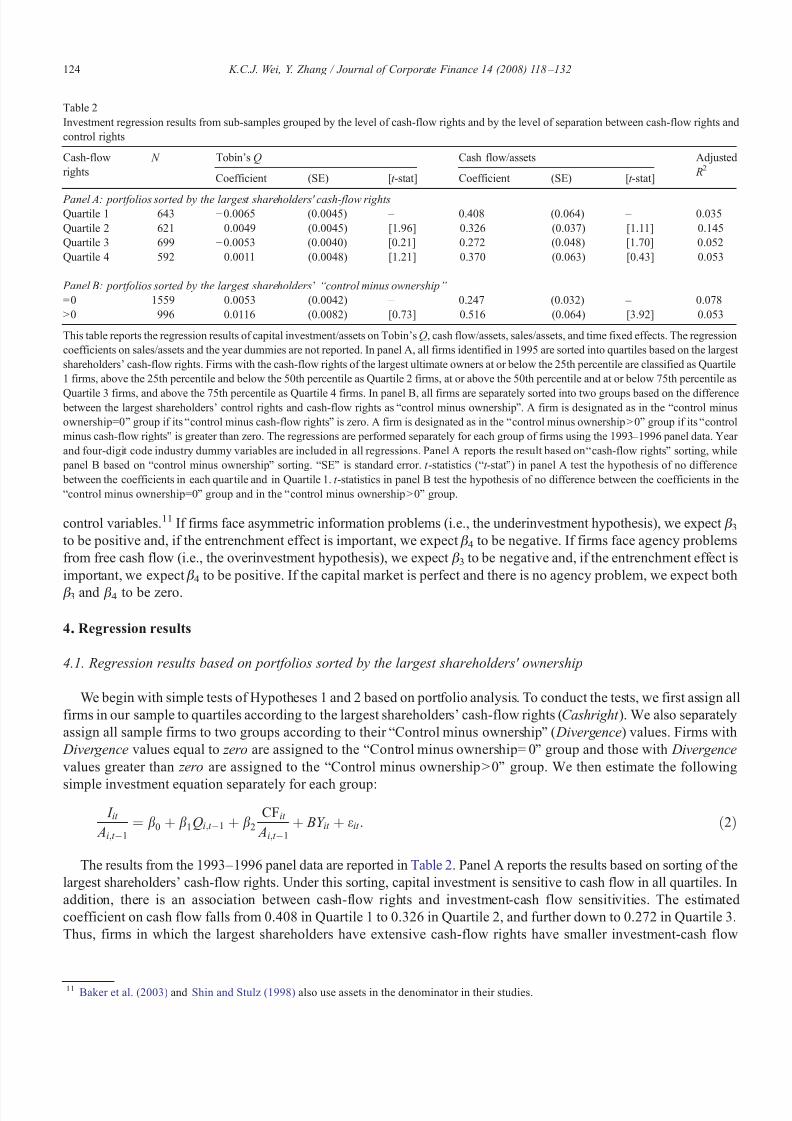

control variables.11 If firms face asymmetric information problems (i.e., the underinvestment hypothesis), we expect β 3to be positive and, if the entrenchment effect is important, we expect β 4 to be negative. If firms face agency problems

from free cash flow (i.e., the overinvestment hypothesis), we expect β 3 to be negative and, if the entrenchment effect is

important, we expect β 4 to be positive. If the capital market is perfect and there is no agency problem, we expect both

β 3 and β 4 to be zero.

4. Regression results

4.1. Regression results based on portfolios sorted by the largest shareholders' ownership

We begin with simple tests of Hypotheses 1 and 2 based on portfolio analysis. To conduct the tests, we first assign all

firms in our sample to quartiles according to the largest shareholders' cash-flow rights (Cashright ). We also separately

assign all sample firms to two groups according to their “Control minus ownership” ( Divergence) values. Firms with

Divergence values equal to zero are assigned to the “Control minus ownership= 0” group and those with Divergence

values greater than zero are assigned to the “Control minus ownershipN0” group. We then estimate the following

simple investment equation separately for each group:

I it

Ai;t 1

¼ b0 þ b1Qi;t 1 þ b2

CFit

Ai;t 1

þ BY it þ eit : ð2Þ

The results from the 1993–1996 panel data are reported in Table 2. Panel A reports the results based on sorting of the

largest shareholders' cash-flow rights. Under this sorting, capital investment is sensitive to cash flow in all quartiles. In

addition, there is an association between cash-flow rights and investment-cash flow sensitivities. The estimated

coefficient on cash flow falls from 0.408 in Quartile 1 to 0.326 in Quartile 2, and further down to 0.272 in Quartile 3.

Thus, firms in which the largest shareholders have extensive cash-flow rights have smaller investment-cash flow

11 Baker et al. (2003) and Shin and Stulz (1998) also use assets in the denominator in their studies.

Table 2

Investment regression results from sub-samples grouped by the level of cash-flow rights and by the level of separation between cash-flow rights and

control rights

Cash-flow

rights

N Tobin's Q Cash flow/assets Adjusted

R2

Coefficient (SE) [t -stat] Coefficient (SE) [t -stat]

Panel A: portfolios sorted by the largest shareholders' cash-flow rightsQuartile 1 643 −0.0065 (0.0045) – 0.408 (0.064) – 0.035

Quartile 2 621 0.0049 (0.0045) [1.96] 0.326 (0.037) [1.11] 0.145

Quartile 3 699 −0.0053 (0.0040) [0.21] 0.272 (0.048) [1.70] 0.052

Quartile 4 592 0.0011 (0.0048) [1.21] 0.370 (0.063) [0.43] 0.053

Panel B: portfolios sorted by the largest shareholders' “ control minus ownership”

=0 1559 0.0053 (0.0042) – 0.247 (0.032) – 0.078

N0 996 0.0116 (0.0082) [0.73] 0.516 (0.064) [3.92] 0.053

This table reports the regression results of capital investment/assets on Tobin's Q, cash flow/assets, sales/assets, and time fixed effects. The regression

coefficients on sales/assets and the year dummies are not reported. In panel A, all firms identified in 1995 are sorted into quartiles based on the largest

shareholders' cash-flow rights. Firms with the cash-flow rights of the largest ultimate owners at or below the 25th percentile are classified as Quartile

1 firms, above the 25th percentile and below the 50th percentile as Quartile 2 firms, at or above the 50th percentile and at or below 75th percentile as

Quartile 3 firms, and above the 75th percentile as Quartile 4 firms. In panel B, all firms are separately sorted into two groups based on the difference between the largest shareholders' control rights and cash-flow rights as “control minus ownership”. A firm is designated as in the “control minus

ownership=0” group if its “control minus cash-flow rights” is zero. A firm is designated as in the “control minus ownershipN0” group if its “control

minus cash-flow rights” is greater than zero. The regressions are performed separately for each group of firms using the 1993–1996 panel data. Year

and four-digit code industry dummy variables are included in all regressions. Panel A reports the result based on “cash-flow rights” sorting, while

panel B based on “control minus ownership” sorting. “SE” is standard error. t -statistics (“t -stat ”) in panel A test the hypothesis of no difference

between the coefficients in each quartile and in Quartile 1. t -statistics in panel B test the hypothesis of no difference between the coefficients in the

“control minus ownership=0” group and in the “control minus ownershipN0” group.

124 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 8/15

sensitivities than do firms in which the largest shareholders have limited cash-flow rights. A formal test shows that the

difference in the estimated coefficient on cash flow is statistically significant between Quartile 1 and Quartile 3 at the

10% level with a t -statistic of 1.70. The results imply that the overinvestment problem is alleviated in firms in which the

largest shareholders have extensive cash-flow rights, which is consistent with the overinvestment hypothesis suggested

by the agency problems of free cash flow. However, the estimated coefficient on cash flow in Quartile 4 increases to

0.370 from 0.272 in Quartile 3. This may suggest that the entrenchment effect appears to become more significant asthe largest shareholders' control rights increase along with their cash-flow rights. However, we need to examine the

cash-flow rights and control rights simultaneously to disentangle the two effects.

In summary, the results in panel A of Table 2 show that there is a U-shaped relationship between investment-cash

flow sensitivities and the cash-flow rights of the largest shareholders, which is opposite to the finding by Hadlock

(1998) in U.S. firms. This perhaps suggests that the overinvestment hypothesis is more appropriate in describing

investment activities in East Asian countries than the underinvestment hypothesis is.

Panel B of Table 2 reports the results based on the “control minus ownership” sorting. The results indicate that there

is indeed a strong relationship between “Control minus ownership” and the effect of cash flow on investment. The

estimated coefficient on cash flow increases from 0.247 in the “Control minus ownership = 0” group to 0.516 in the

“Control minus ownershipN0” group. Thus, firms that have a separation between the largest shareholders' control

rights and their cash-flow rights have more than double the sensitivity of investment to cash flow than do firms that have no such separation. A formal test shows that the difference in the estimated coefficients on cash flow is

statistically significant between the two groups at the 1% level with a t -statistic of 3.92. These results imply that the

overinvestment problem is aggravated in firms with a separation between the largest shareholders' control rights and

their ownership, which is also consistent with the overinvestment hypothesis.

4.2. Baseline regression results

The results from the portfolio analyses in the last sub-section support the overinvestment hypothesis. In this section,

we use the entire sample for a formal test of our hypotheses. Since the ownership data are collected from 1996, we use

the 1993–1996 panel data. The regression results from Eq. (1) are reported in Table 3. Model 1 of Table 3 reports the

estimates from a standard investment-cash flow regression. The estimated coefficient on lagged sales/assets is positive

Table 3

Regression of investment on Tobin's Q, cash flow, and the largest shareholders' ownership structures

Independent variable Model 1 Model 2 Model 3 Model 4

Intercept 0.066⁎⁎ 0.069⁎⁎ 0.065⁎⁎ 0.067⁎⁎

(7.39) (7.63) (8.11) (7.43)

Sales 0.015 0.016 0.017 0.017

(0.32) (0.36) (0.37) (0.38)

Tobin's Q 0.007⁎ 0.007⁎ 0.006⁎ 0.007⁎

(1.89) (1.92) (1.67) (1.72)

Cash flow 0.316⁎⁎ 0.540⁎ 0.426⁎⁎ 0.426⁎⁎

(10.57) (5.73) (4.05) (4.05)Cash flow×Cash-flow rights −0.955⁎⁎ −0.633

(−2.50) (−1.57)

Cash flow × (Control minus ownership) 1.340⁎⁎ 1.097⁎⁎

(3.07) (2.37)

Country and industry dummies Yes Yes Yes Yes

Adjusted R2 0.071 0.064 0.064 0.061

Number of observations 2555 2555 2555 2555

This table reports fixed-effect regression results of capital investment on Tobin's Q, cash flow, interactions of cash flow with the largest shareholders'

cash-flow rights and with the difference between the largest shareholders' control rights and cash-flow rights (denoted as “control minus ownership”),

controls, the country dummies, and the four-digit industry code dummies in 1993–1996. “Investment ” is defined as capital expenditures over assets.

“Sales” is the total sales over assets in the previous year. “Tobin's Q” is defined as the market value of equity plus assets minus the book value of

equity over assets. “Cash flow” is operating cash flow over assets. “Cash-flow right ” is the largest shareholders' cash-flow rights. “Control minus

ownership”

is the difference between the largest shareholders' control rights and cash-flow rights. Firm fixed effects and year dummy variables areincluded in all regressions. t -statistics are in parentheses. ⁎ and ⁎⁎ denote significance at the 10% and 5% levels, respectively.

125 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 9/15

but insignificant. Both coefficients on lagged Tobin's Q and on cash flow have the expected positive signs and are

significant, which is also consistent with previous studies that use U.S. data (e.g., Fazzari et al., 1988).

Model 2 includes a term that interacts cash flow with the largest shareholders' cash-flow rights (Cash flow × Cash-

flow rights). The coefficient of interest in this case is the coefficient on the interaction term (β 3 in Eq. (1)). The

estimated coefficient on Cash flow × Cash-flow rights is −0.955, which is negative and significant at the 5% level with

a t -statistic of −

2.50. This result shows that the sensitivity of investment to cash flow falls rapidly as the largest shareholders' cash-flow rights increase. This result strongly supports the overinvestment hypothesis that is heightened

by the largest shareholders' enhancement effect on investment.

Model 3 includes a term that interacts cash flow with “Control minus ownership” (Cash flow×(Control minus

ownership)). The coefficient of interest in this case is the coefficient on the interaction term (β 4 in Eq. (1)). The coefficient

on Cash flow×(Control minus ownership) is 1.34, which is positive and significant at the 1% level with a t -statistic of

3.07. This implies that the sensitivity of investment to cash flow increases rapidly as the degree of separation between the

largest shareholders' ownership and their control rights increases. This result is also consistent with the overinvestment

hypothesis that is heightened by the largest shareholders' entrenchment effect on investment.

Model 4 reports results from our full model by interacting cash flow with both cash-flow rights and “Control minus

ownership”. We use this specification as our baseline specification for any comparisons below. The coefficients of

interest in this case are the coefficients on the interaction terms (β 3 and β 4 in Eq. (1)). The coefficient on Cashflow×Cash-flow rights is −0.633, which is negative and close to significant at the 10% level. The coefficient on Cash

flow×(Control minus ownership) is 1.097, which is positive and significant at the 5% level with a t -statistic of 2.37.

The results demonstrate that the sensitivity of investment to cash flow simultaneously decreases as the largest

shareholders' cash-flow rights increase and it increases as the degree of separation between the largest shareholders'

ownership and their control rights increases. The results are consistent with the overinvestment hypothesis, which is

heightened by the largest shareholders' enhancement and entrenchment effects on investment. This suggests that using

East Asian firms allows us to detect both the enhancement and entrenchment effects of the largest shareholders on

investment. These effects are difficult to identify in typical U.S. firms.

Overall, the results in Table 3 support the overinvestment hypothesis caused by the agency costs of free cash flow using

our East Asian sample. They do not support the underinvestment hypothesis caused by asymmetric information problems

as documented by Hadlock (1998) on a U.S. sample. Our results and approach offer a much clearer picture of the impact of

ownership structures on the investment-cash flow sensitivity than previous studies have been able to show. In particular,we disentangle the enhancement effect from the entrenchment effect on investment. When large shareholders care more

about shareholder value, the agency costs of free cash flow are less severe and the overinvestment problem also becomes

less severe. On the other hand, when the degree of separation between ownership and control rights is great, the

overinvestment problem is aggravated.

5. Robustness checks and additional tests

5.1. Alternative requirements for panel data

To work with a large sample, we use an unbalanced panel dataset in the above analyses. More specifically, we

include all firms in the sample that have at least one firm-year in the span of 1993 –1996, provided that all the datarequired for analysis are available. This sampling procedure might bias our results. In this section, we examine whether

our results are robust to the requirement of specific numbers of firm-years for a firm to be included in the sample.

First, we exclude firms with only one firm-year observation in 1993–1996. Column 1 of Table 4 reports the

estimated coefficients based on this reduced sample of 2292 firm-years. The results remain almost unchanged. We then

further exclude firms with only one or two firm-year observations. Column 2 of Table 4 reports estimated coefficients

based on this further reduced sample of 1786 firm-years. The results change slightly. The coefficient on Cash

flow× Cash-flow rights becomes significant at the 10% level and the significance of the coefficient on Cash

flow×(Control minus ownership) reduces to the 10% level. Finally, we include only firms with all four firm-year

observations. Column 3 of Table 4 reports the estimated coefficients based on this balanced panel data sample of only

1408 firm-years. The coefficients on all variables do change, but the signs on all variables remain the same. The

coefficient on Cash flow × Cash-flow rights improves to become significant at the 5% level. In sum, our results remain

virtually unchanged or are even stronger when we impose more stringent restrictions on firm-year observations.

126 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 10/15

Since the East Asian financial crisis took place in mid 1997, the year 1996, which is just prior to the crisis, may bedifferent from other years, and thus may influence our results. To test this possibility, we run the baseline regression

with the panel data from 1992–1995. The results (unreported) are similar to those on data from 1993–1996. Though

not reported, we also run a country-by-country analysis. The results are consistent with the whole sample analysis in

general (with correct signs for a majority of countries), but are weaker due to fewer observations.

5.2. Robustness checks: different sets of control variables

Our results in Table 3 may be sensitive to the exclusion or inclusion of certain control variables. In this section, we

report robustness checks to validate our results. First, sales are highly correlated with Tobin's Q, which may explain

why the coefficient on Tobin's Q is not large in Model 1 of Table 3. Model 1 of Table 5 reports the estimated

coefficients excluding sales from our baseline result reported in Model 4 of Table 3. After excluding sales, thecoefficient on Tobin's Q is positive and significant, but it does not change much. The other coefficients also do not

change much. Our results continue to support the overinvestment hypothesis caused by the agency costs of free cash

flow when excluding sales from the regression. We also replace sales/assets with sales growth in the regression. The

result (unreported) is essentially the same.

Second, it is possible that the investment-Tobin's Q relationship is not monotonic. Models 2 and 3 in Table 5 report

the results with the squared term of Tobin's Q included. Model 2 excludes sales, while Model 3 includes sales. The

results from both Models 2 and 3 indicate that the inclusion of the squared Tobin's Q does not change the coefficient on

Cash flow×Cash-flow rights or the coefficient on Cash flow×(Control minus ownership) too much except that the

former becomes significant at the 10% level, compared with our baseline result in Model 4 of Table 3.

Third, a potential explanation for our results in Table 3 is that the largest shareholders' ownership may be a proxy for

omitted variables that affect the investment-cash flow sensitivity. It is possible that the results reflect a negative

correlation between firm size and the largest shareholders' ownership. To control for this possibility, we include a term

Table 4

Regression of investment on Tobin's Q, cash flow, and the largest shareholders' ownership structures: alternative sample size

Independent variable At least 2 firm-years At least 3 firm-years 4 firm-years only

(Column 1) (Column 2) (Column 3)

Intercept 0.065⁎⁎ 0.064⁎⁎ 0.060⁎⁎

(7.33) (6.76) (5.70)Sales 0.002 −0.000 −0.001

(0.38) (−0.02) (−0.26)

Tobin's Q 0.007⁎ 0.008⁎ 0.011⁎⁎

(1.72) (1.84) (2.23)

Cash flow 0.426⁎⁎ 0.473⁎⁎ 0.576⁎⁎

(4.05) (3.99) (4.14)

Cash flow×Cash-flow rights −0.633 −0.864⁎ −1.29⁎⁎

(−1.57) (−1.87) (−2.37)

Cash flow × (Control minus ownership) 1.097⁎⁎ 1.170⁎⁎ 1.240⁎⁎

(2.37) (2.33) (2.18)

Country and industry dummies Yes Yes Yes

Adjusted R2 0.061 0.059 0.056

Number of observations 2292 1786 1408

This table reports fixed-effect regression results of capital investment on Tobin's Q, cash flow, interactions of cash flow with cash-flow rights and

with “control minus ownership” controls, the country dummies, and the four-digit industry code dummies for the 1993–1996 panel data.

“Investment ” is defined as capital expenditures over assets. “Sales” is the total sales over assets in the previous year. “Tobin's Q” is defined as the

market value of equity plus assets minus the book value of equity over assets. “Cash flow” is operating cash flow over assets. “Cash-flow right ” is the

largest shareholders' cash-flow rights. “Control minus ownership” is the difference between the largest shareholders' control rights and cash-flow

rights. Column 1 reports the unbalanced panel data regression results when the sample includes 731 firms for a total of 2292 firm-years with each firm

having at least two firm-years. Column 2 reports the unbalanced panel data regression results when the sample includes 478 firms for a total of 1786

firm-years with each firm having at least three firm-years. Column 3 reports the balanced panel data regression results with 352 firms for a total of

1408 firm-years with each firm having all four firm-years. Firm fixed effects and year dummy variables are included in all regressions. t -statistics are

in parentheses. ⁎ and ⁎⁎ denote significance at the 10% and 5% levels, respectively.

127 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 11/15

interacting cash flow with the logarithm of the firm's book value of assets (Cash flow × Ln(Size)). The result is given in

Model 4 of Table 5. The coefficient on Cash flow×Cash-flow rights changes very little from −0.633 to −0.677, but it

becomes significant at the 10% level. The coefficient on Cash flow × (Control minus ownership) changes from 1.097 to

1.078 and is still highly significant. The coefficient on Cash flow×Ln(Size) is negative but insignificant.

In addition, it is possible that our results reflect a positive correlation between a firm's growth potential and the

largest shareholder's ownership. To control for this possibility, we include a term interacting cash flow with the firm's

Tobin's Q (Cash flow×Tobin's Q) in addition to the term interacting cash flow with firm size (Cash flow×Ln(Size)).

In Model 5, the coefficient on Cash flow×Tobin's Q is negative but it is insignificant. The coefficients on Cash

flow× Cash-flow rights and Cash flow × (Control minus ownership) change very little, compared with the results from

Model 4. The results from both Models 4 and 5 indicate that our conclusion about the overinvestment hypothesiscaused by the agency costs of free cash flow is robust to the inclusion of cash flow interacted with firm size and with

Tobin's Q.

In sum, the results in Table 5 indicate that our overinvestment conclusion is robust to a number of alternative

specifications with different sets of control variables that may affect our results. That is, our results supporting the

overinvestment hypothesis caused by the agency costs of free cash flow, which are heightened with the enhancement

and entrenchment effects of the largest shareholders' ownership structures, are very robust to various empirical

specifications.

5.3. Comparison of overinvestment problems between low ROA and high ROA groups

The overinvestment problem should be a more important issue in firms with a lower return on investment than in

firms with a higher return on investment. To test this hypothesis, we classify all firms into two groups. The low ROA

Table 5

Regression of investment on Tobin's Q, cash flow, and the largest shareholders' ownership structures: robustness checks

Independent variable Model 1 Model 2 Model 3 Model 4 Model 5

Intercept 0.068⁎⁎ 0.063⁎⁎ 0.062⁎⁎ 0.068⁎⁎ 0.058⁎⁎

(8.18) (7.52) (6.86) (7.47) (5.28)

Sales 0.002 0.017 0.002(0.35) (0.38) (0.34)

Tobin's Q 0.007⁎ 0.008⁎⁎ 0.008⁎⁎ 0.012⁎ 0.012⁎⁎

(1.74) (2.07) (2.06) (1.72) (2.32)

Tobin's Q squared 0.0012⁎⁎ 0.0012⁎⁎

(2.36) (2.63)

Cash flow 0.427⁎⁎ 0.422⁎⁎ 0.422⁎⁎ 0.444⁎⁎ 0.506⁎⁎

(4.06) (4.02) (4.02) (4.13) (4.42)

Cash flow×Cash-flow rights −0.632 −0.700⁎ −0.701⁎ −0.677⁎ −0.678⁎

(−1.56) (−1.73) (−1.73) (−1.66) (−1.66)

Cash flow×(Control minus ownership) 1.095⁎⁎ 1.160⁎⁎ 1.164⁎⁎ 1.078⁎⁎ 1.040⁎⁎

(2.37) (2.51) (2.54) (2.32) (2.24)

Cash flow×Ln(Size) −0.036 −0.042

(−0.84) (−0.99)

Cash flow×Tobin's Q −

0.024(−1.56)

Year and industry dummies Yes Yes Yes Yes Yes

Adjusted R2 0.062 0.053 0.052 0.056 0.055

Number of observations 2555 2555 2555 2555 2555

This table reports robustness checks for the fixed-effect regressions of investment on Tobin's Q, cash flow, interactions of cash flow with cash-flow

rights and with “control minus ownership”, controls, the country dummies, and the four-digit industry code dummies for the 1993 –1996 panel data.

The regression also includes the four-digit industry dummies. “Investment ” is defined as capital expenditures over assets. “Sales” is the total sales

over assets in the previous year. “Tobin's Q” is defined as the market value of equity plus assets minus the book value of equity over assets. “Cash

flow” is operating cash flow over assets. “Cash-flow right ” is the largest shareholders' cash-flow rights. “Control minus ownership” is the difference

between the largest shareholders' control rights and cash-flow rights. “Ln(Size)” is the natural logarithm of assets. t -statistics are in parentheses. Firm

fixed effects and year dummy variables are included in all regressions. ⁎ and ⁎⁎ denote significance at the 10% and 5% levels, respectively.

128 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 12/15

group contains firms with a four-year (1993–1996) average ROA of less than 0.05, while the high ROA group contains

firms with a four-year average ROA of greater than or equal to 0.05.12 The results are reported in Table 6. For the low

ROA group, the coefficient on Cash flow× Cash-flow rights is negative and significant at the 10% level. The

coefficient on Cash flow×(Control minus ownership) is positive and significant at the 5% level with a t -statistic of

2.44. The results demonstrate that in firms with a low ROA, the sensitivity of investment to cash flow simultaneously

decreases with the largest shareholders' cash-flow rights and increases with the degree of separation between the largest

shareholders' ownership and their control rights. The results are consistent with the overinvestment hypothesis. In the

high ROA group, the coefficient on Cash flow×Cash-flow rights is negative but not significant. The coefficient on

Cash flow × (Control minus ownership) is positive but not significant. This suggests that the overinvestment problemcaused by the agency costs of free cash flow is more severe in firms with lower returns on investments. 13

Table 6

Regression of investment on Tobin's Q, cash flow, and the largest shareholders' ownership structures: low ROA group versus high ROA group

Independent variable Low ROA group High ROA group

(Column 1) (Column 2)

Intercept 0.066⁎⁎ 0.042⁎⁎

(4.07) (2.11)Sales 0.001 0.018

(0.16) (1.03)

Tobin's Q 0.013 0.009

(1.52) (1.26)

Cash flow 0.646⁎⁎ 0.589⁎⁎

(2.67) (3.14)

Cash flow×Cash-flow rights −1.190⁎ −0.822

(−1.73) (−1.43)

Cash flow × (Control minus ownership) 1.910⁎⁎ 0.239

(2.44) (0.35)

Cash flow×Ln(Size) −0.023 −0.024

(−1.64) (−0.56)

Cash flow×Tobin's Q −0.035 −0.015

(−0.52) (−0.86)

Country and industry dummies Yes Yes

Adjusted R2 0.058 0.048

Number of observations 1155 1400

This table reports fixed-effect regression results of capital investment on Tobin's Q, cash flow, interactions of cash flow with cash-flow rights and

with “control minus ownership”, controls, the country dummies, and the four-digit industry code dummies for the two groups classified based on

returns on assets (ROA). The 1993–1996 panel data is used. “Investment ” is defined as capital expenditures over assets. “Sales” is the total sales over

assets in the previous year. “Tobin's Q” is defined as the market value of equity plus assets minus the book value of equity over assets. “Cash flow” is

operating cash flow over assets. “Cash-flow right ” is the largest shareholders' cash-flow rights. “Control minus ownership” is the difference between

the largest shareholders' control rights and cash-flow rights. Column 1 reports the regression results for the low ROA firms with an average four-year

ROA of less than 0.05. The low ROA group includes 456 firms for a total of 1155 firm-years. Column 2 reports the regression results for the high

ROA firms with a four-year average ROA of greater than or equal to 0.05. The high ROAgroup includes 538 firms for a total of 1400 firm-years. Firm

fixed effects and year dummy variables are included in all regressions. t -statistics are in parentheses. ⁎ and ⁎⁎ denote significance at the 10% and 5%

levels, respectively.

12 We also use different ROA cut-off points to classify firms into low and high ROA groups. The results are essentially similar to those reported in

Table 6.13 Previous research has documented that large shareholders in general and the separation of ownership and control rights in particular are usually

associated with family ownership. It is possible that investment behavior is different between large shareholders in a family and large shareholders

not in families. To test this hypothesis, we divide the sample into two groups: firms with family owners as the largest shareholder (about 70% of our

sample) and firms with non-family owners (including the state, or widely held corporations and financial institutions) as the largest shareholders.

The unreported results suggest that overinvestment caused by the agency costs of free cash flow is more severe in firms with family owners than infirms with non-family owners as the largest shareholders.

129 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 13/15

5.4. Discussion of endogeneity issues

The empirical tests conducted above implicitly assume that the levels of the largest shareholders' ownership and

control rights are exogenously set. An issue that might arise is the possibility of a reverse causality in terms of the

impact of the divergence between ownership and control rights on the investment-cash flow sensitivity. Suppose that

the largest shareholder faces an asymmetric information problem. He/she might then decrease his/her cash-flow rights, but increase the level of the divergence between his/her control rights and cash-flow rights.

On the contrary, suppose that the largest shareholder faces the free cash-flow problem. He/she might then increase

his/her cash-flow rights, but decrease the level of the divergence between his/her control rights and cash-flow rights.

We could then find that as the level of cash-flow rights becomes larger and/or the divergence becomes smaller, the

investment-cash flow sensitivity decreases. Hence, this result would not tell us much about the possible entrenchment

effect of the separation between ownership and control. However, it seems unlikely that firms can change their cash-

flow rights and control rights quickly and frequently in light of temporary free cash flow or asymmetric information

problems. In fact, La Porta et al. (1999) report that the ownership structures of the top 20 to 30 East Asian firms are

relatively stable over time. As a result, the endogeneity issue would not be important in this case.

6. Conclusions

The high degree of separation between control rights and cash-flow rights in East Asian corporations provides an

excellent sample with which to study investment-cash flow sensitivities in differentiating the agency costs of free cash

flow from asymmetric information problems in capital markets. This separation may be impossible to detect in U.S.

corporations. We find that the investment-cash flow sensitivity decreases with increases in the cash-flow rights of the

largest shareholders but it increases with the degree of divergence between the control rights and cash-flow rights of the

largest shareholders. All these results are consistent with the overinvestment hypothesis caused by the agency costs of

free cash flow, but are inconsistent with the underinvestment hypothesis caused by asymmetric information problems.

Furthermore, our results also demonstrate the enhancement and entrenchment effects of the largest shareholders'

ownership and control on corporate investment.

Our study contributes to the debate on whether the positive association between cash flow and investment is due to

the largest shareholders' preferences to overinvest or to underinvest. The previous literature does not provide a goodinstrument to differentiate between these two explanations. We believe that using the largest shareholders' cash-flow

rights and their control rights provides a better instrument in distinguishing between these two explanations than does

using managerial cash-flow rights alone. The reason is simple. While it is not clear how we can separate the

entrenchment effect from the enhancement effect based on the largest shareholders' cash-flow rights alone, the degree

of divergence between the largest shareholders' control rights and their cash-flow rights in East Asian corporations

does provide an excellent measure of the largest shareholders' entrenchment.

Our results are different from those reported by Hadlock (1998). Firms in both the U.S. and East Asia exhibit

strongly positive investment-cash flow sensitivities. However, our findings reveal that the reasons for the positive

investment-cash flow sensitivities are different. While Hadlock's data support the underinvestment hypothesis caused

by asymmetric information problems in U.S. corporations, we document evidence that is consistent with the

overinvestment hypothesis caused by the agency costs of free cash flow in East Asian corporations. The difference between our results and Hadlock's may be the result of differences in institutional factors. It is well known that the U.S.

economy is characterized by dispersed ownership structures, effective capital market governance, and stronger

protections of shareholders. In contrast, the East Asian economies are distinguished by family firms, state-owned firms,

pyramid and concentrated ownership structures, weak capital market governance, and expropriation of minority

shareholders by dominant shareholders. These more fundamental factors may contribute to the differences in the

agency problems that firms in the two groups of economies face. Previous literature, for example, La Porta et al. (1999)

and Claessens et al. (2002), points out that East Asia and other countries outside the U.S. or the U.K. have different

agency problems. In fact, the agency problem in the U.S. centers on the conflicts of interest between managers and

shareholders, while the agency problem in East Asia is defined by conflicts of interest between large shareholders and

minority shareholders. We provide further evidence to support their arguments that the level of divergence between the

control rights and cash-flow rights of the largest shareholders does have an entrenchment effect on corporate

overinvestment.

130 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 14/15

Since the Asian financial crisis, people have often argued that one of the major reasons for the crisis was

overinvestment by Asian corporations due to too much cheap capital flowing into the region before the crisis. They

have further argued that the overinvestment problem was caused by poor corporate governance mechanisms in these

countries, especially in regard to the significant divergence between the control rights and cash-flow rights of the

largest shareholders (see, for example, Stiglitz (1998), Greenspan (1999), Rajan and Zingales (1998), and Yellen

(1998)). However, up to today, no direct empirical evidence has been offered to support these arguments. Our paper provides evidence that these conjectures are correct. More specifically, we find that firms in East Asian emerging

economies showed the symptom of overinvestment before the Asian financial crisis (i.e., during our sample period

from 1993–1996). This is particularly true for firms with the greatest divergence between the largest shareholders'

control rights and their cash-flow rights and for firms with lower ROA.

Since the Asian financial crisis, the quality of corporate governance mechanisms in the East Asian region has been

substantially improved via government regulations, such as the requirement that independent directors serve on

company boards, and the scrutiny of shareholder rights activists. However, the problems of concentrated ownership

structures and the divergence between the largest shareholders' control rights and their cash-flow rights have not been

resolved. Whether or not the improvement in the quality of corporate governance mechanisms alone has changed the

investment behaviors of East Asian corporations is left for future research.

References

Baker, M., Stein, J.C., Wurgler, J., 2003. When does the market matter? Stock prices and the investment of equity-dependent firms. Quarterly Journal

of Economics 118, 969–1005.

Claessens, S., Djankov, S., Fan, J.P.H., Lang, L.H.P., 2002. Disentangling the incentive and entrenchment effects of large shareholders. Journal of

Finance 57, 2741–2771.

Claessens, S., Djankov, S., Lang, L.H.P., 2000. The separation of ownership and control in East Asia corporations. Journal of Financial Economics

58, 81–112.

Cleary, S., 1999. The relationship between firm investment and financial status. Journal of Finance 54, 673–692.

Dittmar, A., Mahrt-Smith, J., Servaes, H., 2003. International corporate governance and corporate cash holdings. Journal of Financial and

Quantitative Analysis 38, 111–133.

Dybvig, P.H., Zender, J.F., 1991. Capital structure and dividend irrelevance with asymmetric information. Review of Financial Studies 4, 201–219.

Fan, J.P.H., Wong, T.J., 2002. Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting andEconomics 33, 401–425.

Fazzari, S., Hubbard, R.G., Peterson, B.C., 1988. Financing constraints and corporate investment. Brookings Paper on Economic Activity 1,

141–195.

Fazzari, S., Hubbard, R.G., Peterson, B.C., 2000. Investment-cash flow sensitivities are useful: a comment on Kaplan and Zingales. Quarterly Journal

of Economics 115, 695–705.

Greenspan, A., 1999. Lessons from the global crises. Address to the World Bank Group and International Monetary Fund, September 27, 1999.

Hadlock, C.J., 1998. Ownership, liquidity, and investment. RAND Journal of Economics, 29, 487 –508.

Harvey, C., Lins, K., Roper, A., 2004. The effect of capital structure when expected agency costs are extreme. Journal of Financial Economics 74, 3–30.

Hoshi, T., Kashyap, A., Scharfstein, D., 1991. Corporate structure, liquidity, and investment: evidence from Japanese industrial groups. Quarterly

Journal of Economics 106, 33–60.

Hubbard, R.G., 1998. Capital-market imperfections and investment. Journal of Economic Literature 36, 193–225.

Jensen, M., 1986. Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review 76, 323–329.

Jensen, M., Meckling, W., 1976. The theory of firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3,

305–350.

Joh, S.W., 2003. Corporate Governance and firm profitability: evidence from Korea before the economic crisis. Journal of Financial Economics 68,

287–322.

Johnson, S., Boone, P., Breach, A., Friedman, E., 2000. Corporate governance in the Asian financial crisis. Journal of Financial Economics 58,

141–186.

Kalcheva, I., Lins, K.V., in press. International evidence on cash holdings and expected managerial agency problems. Review of Financial Studies,

forthcoming.

Kaplan, S., Zingales, L., 1997. Do investment-cash flow sensitivities provide useful measures of financing constraints? Quarterly Journal of

Economics 112, 169–216.

Kaplan, S., Zingales, L., 2000. Investment-cash flow sensitivities are not valid measures of financing constraints. Quarterly Journal of Economics

115, 707–712.

Lamont, O., 1997. Cash flow and investment: evidence from internal capital markets. Journal of Finance 52, 83–110.

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., 1999. Corporate ownership around the world. Journal of Finance 54, 471–518.

Lemmon, M.L., Lins, L.V., 2003. Ownership structure, corporate governance, and firm value: evidence from the East Asian financial crisis. Journal of Finance 58, 1445–1468.

131 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132

8/13/2019 Wei & Zhang, 2008 Ownership Structure, Cash Flow, And Capital Investment_Evidence From East Asian Economie…

http://slidepdf.com/reader/full/wei-zhang-2008-ownership-structure-cash-flow-and-capital-investmentevidence 15/15

Lins, K.V., 2003. Equity ownership and firm value in emerging markets. Journal of Financial and Quantitative Analysis 38, 159–184.

McConnell, J., Servaes, H., 1990. Additional evidence on equity ownership and corporate value. Journal of Financial Economics 27, 595 –612.

Mitton, T., 2002. A cross-firm analysis of the impact of corporate governance on the East Asian financial crisis. Journal of Financial Economics 64,

215–241.

Morck, R., Shleifer, A., Vishny, R., 1988. Management ownership and market valuation: an empirical analysis. Journal of Financial Economics 20,

293–315.

Morck, R., Shleifer, A., Vishny, R., 1990. The stock market and investment: is the market a side-show? Brookings Papers on Economic Activity 2,157–215.

Myers, S., Majluf, N., 1984. Corporate financing and investment decisions when firms have information that investors do not have. Journal of

Financial Economics 13, 187–221.

Pinkowitz, L., Stulz, R., Williamson, R., 2006. Does the contribution of corporate cash holdings and dividends to firm value depend on governance?

A cross-country analysis. Journal of Finance 61, 2725–2751.

Rajan, R.G., Zingales, L., 1998. Which capitalism? Lessons from the East Asian crisis. Journal of Applied Corporate Finance 11, 40–48.

Shin, H.H., Stulz, R.M., 1998. Are internal capital markets efficient? Quarterly Journal of Economics 113, 531–552.

Shleifer, A., Vishny, R.W., 1997. A survey of corporate governance. Journal of Finance 52, 737–783.

Stiglitz, J., 1998. The role of international financial institutions in the current global economy. Address to the Chicago Council on Foreign Relations,

February 27, 1998.

Stulz, R., 1988. Managerial control of voting rights: financing policies and the markets for corporate control. Journal of Financial Economics 20,

25–54.

Yellen, J., 1998. Lessons from the Asian crisis. Speech at Council on Foreign Relations, New York.

132 K.C.J. Wei, Y. Zhang / Journal of Corporate Finance 14 (2008) 118 – 132