welcome to the transamerica retirement industry speakers

TRANSCRIPT

Transamerica. Master Retirement.®POWER CHOICE FREEDOM

WELCOME TO THETransamerica Retirement Industry Speakers Bureau

For Audio please call: (877) 509-7551

Conference ID: 62822935

For TPA Use Only. Not For Public Distribution.

This program will begin at 9am PST ---Please Stand by----

Transamerica. Master Retirement.®POWER CHOICE FREEDOM

WELCOME TO THETransamerica Retirement Industry Speakers Bureau

Hosted by:

Deb RubinVice President & Head of TPA Channel Distribution

For TPA Use Only. Not For Public Distribution.

TPA Channel Distribution

Transamerica Retirement ServicesTransamerica Retirement Services

Transamerica is on the move!

• Innovative Products and Services

• Both Group Annuity and True NAV Products

• Multiple Employer Plans

• PASS Services

• Proactive Fiduciary SupportProactive Fiduciary Support

• Fiduciary Warranty

• More to come….

For TPA Use Only. Not For Public Distribution. 3Footnotes appear on slide

About Transamerica Retirement ServicesAbout Transamerica Retirement Services

• Transamerica was honored as a Top Retirement Plan Provider and earned 43 “Best in Class” Cups from PLANSPONSOR® Magazine in their annual 2009 DefinedPLANSPONSOR Magazine in their annual 2009 Defined Contribution Survey

• Transamerica was named a Top Performer in Chatham Partners’ 2009 Client Satisfaction Analysis, and received a e s 009 C e Sa s ac o a ys s, a d ece ed38 “Best in Class” Ratings

• Transamerica ranked as a Top Provider in The Boston Research Group’s 2009 401(k) Advisor Satisfaction Studyp ( ) y

• Transamerica earned DALBAR communication seals in 2009 for both participant and sponsor Web sites

T i d 2009 G ld A d f th P fit• Transamerica earned a 2009 Gold Award from the Profit Sharing/401(k) Council of America for participant education – the RECOVER Plan

For TPA Use Only. Not For Public Distribution. 4Footnotes appear on slide

Housekeeping NotesHousekeeping Notes

• All lines will be muted

• CE – Self-Reporting with ASPPA and NIPA

• Q&A Session post presentation

• Call recorded – If interested in copy please send request to [email protected]

For TPA Use Only. Not For Public Distribution. 5

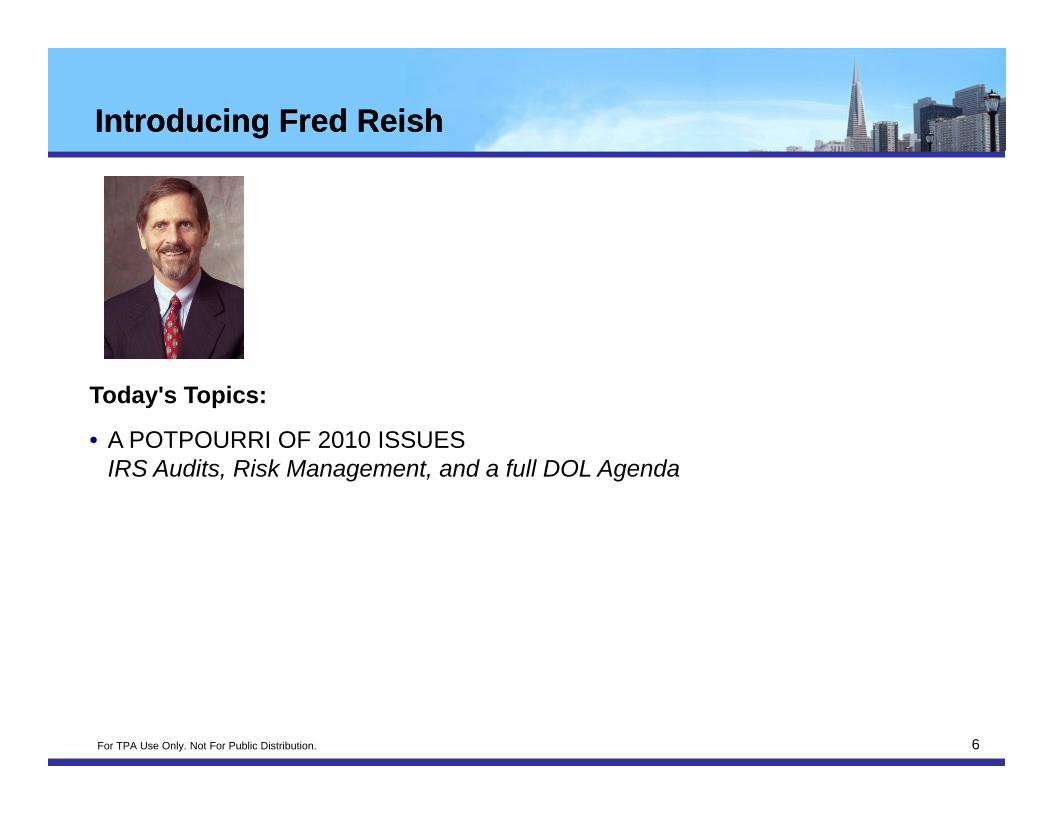

Introducing Fred ReishIntroducing Fred Reish

Today's Topics:

• A POTPOURRI OF 2010 ISSUES IRS Audits, Risk Management, and a full DOL Agenda

For TPA Use Only. Not For Public Distribution. 6

A POTPOURRI OF 2010 ISSUES:A POTPOURRI OF 2010 ISSUES:IRS Audits, Risk Management

d A F ll DOL A dand A Full DOL Agenda

presented by

FFREDRED RREISHEISH,, ESQESQFFREDRED RREISHEISH,, ESQESQ..REISH & REICHER

April 13 2010April 13, 2010

Th IRS h i iti t d l LESE f t j t

IRS AuditsIRS AuditsThe IRS has initiated several LESE enforcement projects(Learn, Educate, Self-Correct and Enforce) and hascompleted and reported on two of those projects.

The LESE Project #1 involved examinations of definedcontribution plans with less than $250,000 in assets.C i di d b th IRSCommon issues discovered by the IRS were:

• Failure to secure adequate bonding per ERISA.

• Failure to timely amend to comply with current lawand regulatory guidance.

8

continued . . .

IRS AuditsIRS Audits• Failure to timely file Forms 1099-R.

• Failure to allocate contributions and forfeitures perFailure to allocate contributions and forfeitures perplan terms.

• Failure to make top heavy minimum contributions.p y

• Failure to obtain joint and survivor annuity waivers.

• Failure to include deemed distributions in income.

9

LESE P j t #4 i l d i ti f 401(k) l

IRS AuditsIRS AuditsLESE Project #4 involved examinations of 401(k) planscovering from three to eight participants, which wereexpected to be subject to the top heavy rules. Commonfailures discovered by the IRS were:

• Failure to secure adequate bonding per ERISA.q g p

• Failure to satisfy the IRS §416 top heavyrequirements.

10

continued . . .

IRS AuditsIRS Audits• Failure to deposit elective deferrals timely into the

plan.

• Failure to properly recognize and distribute excesscontributions timely.

• Failure to properly cover all eligible employees perIRC §410.

11

Th IRS h t bli h d 401(k) l h kli t f

IRS Checklist for Reviewing PlansIRS Checklist for Reviewing PlansThe IRS has established a 401(k) plan checklist forreviewing the operation of retirement plans. Thechecklist is designed for plan sponsors, but it also givesg p p , gTPAs a good idea of the probable audit areas in thefeature. Some of the questions are:

• Has your plan document been updated with thepast few years?

• Are the plan’s operations based on the terms ofthe plan document?

12

continued . . .

IRS Checklist for Reviewing PlansIRS Checklist for Reviewing Plans• Is the plan’s definition of compensation for all

deferrals and allocations used correctly?

• Were all eligible employees identified and given• Were all eligible employees identified and giventhe opportunity to make an elective deferralelection?

• Have you timely deposited employee electivedeferrals?

• Do participant loans conform to the requirementsp p qof the plan document and IRC §72(p)?

• Were hardship distributions made properly?

13

DisclosuresDisclosuresThe trend is towards full disclosure—at both the planand participant level.

• disclosure to fiduciaries and participants

• disclosure by providers and advisersdisclosure by providers and advisers

• disclosure of costs

• disclosure of compensation and revenue sharing (“direct” and “indirect”)

14

Th fid i

Disclosures: Fiduciary IssuesDisclosures: Fiduciary Issues

Is the compensation reasonable?

The fiduciary concerns:

Is the compensation reasonable?

Are the costs reasonable?

Are there conflicts of interest?

15

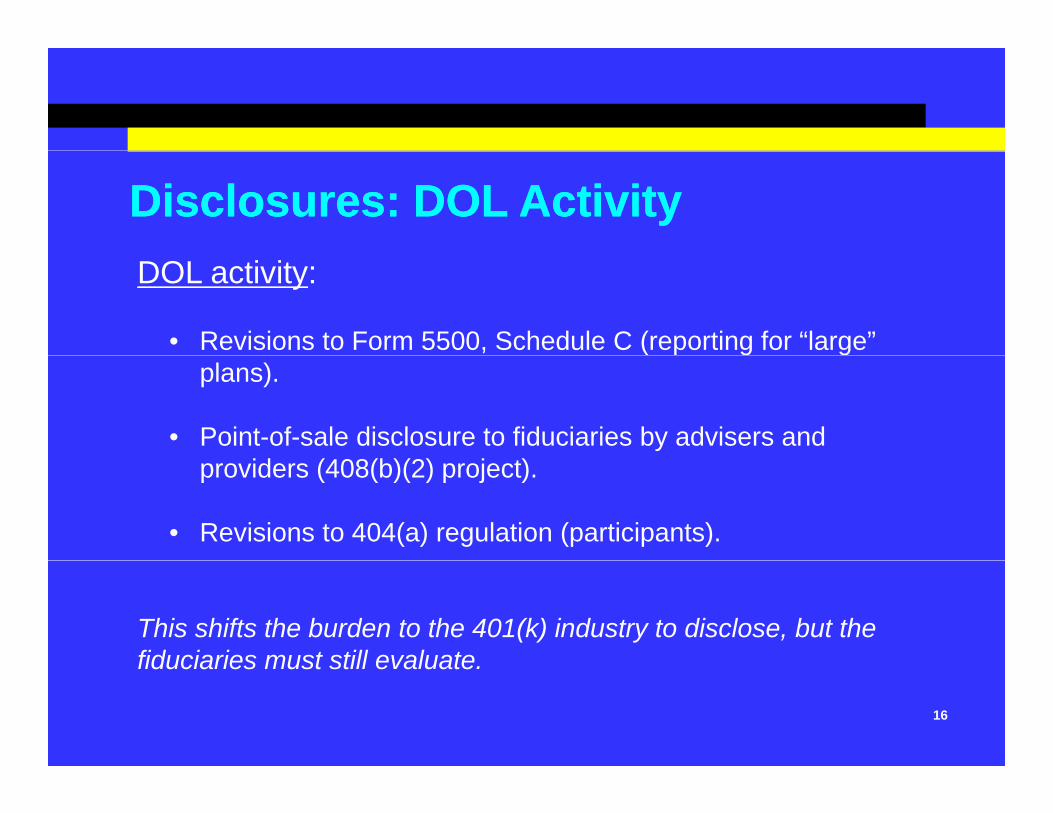

Disclosures: DOL ActivityDisclosures: DOL ActivityDOL activity:

• Revisions to Form 5500, Schedule C (reporting for “large” plans).

• Point-of-sale disclosure to fiduciaries by advisers and providers (408(b)(2) project).

• Revisions to 404(a) regulation (participants).

This shifts the burden to the 401(k) industry to disclose, but the fiduciaries must still evaluate

16

fiduciaries must still evaluate.

Schedule C for 2009Schedule C for 2009

Applies only to large plans—generally 100 ormore participants; and

Service providers who receive at least $5,000 incompensation during the plan year.

17

Schedule C for 2009 Form 5500Schedule C for 2009 Form 5500The new Schedule C for 2009 plan years requiresreporting by plan sponsors of direct and indirectrevenues received by service providers

Direct compensation.

revenues received by service providers.

Indirect compensation: eligible and ineligible.

18

F li ibl i di t ti itt di l

Schedule CSchedule CFor eligible indirect compensation, written disclosures must be given that describe:

the existence of the indirect compensation;

the service provided;

the amount (or estimate) of the compensation ora description of the formula used; and

the identity of the parties paying and receiving thecompensation.

19

Schedule CSchedule C

Part I Service Provider Information (see instructions)

You must complete this Part, in accordance with the instructions, to report the information required for each person whoreceived, directly or indirectly, $5,000 or more in total compensation (i.e., money or anything else of monetary value) inconnection with services rendered to the plan or the person’s position with the plan during the plan year. If a personp p p p g p y preceived only eligible indirect compensation for which the plan received the required disclosures, you are required toanswer line 1 but are not required to include that person when completing the remainder of this Part.

1 Information on Persons Receiving Only Eligible Indirect Compensation

a Check “Yes” or “No” to indicate whether you are excluding a person from the remainder of this Part because theyy g p yreceived only eligible indirect compensation for which the plan received the required disclosures (see instructions for definitionsand conditions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

b If you answered line 1a “Yes,” enter the name and EIN or address of each person providing the required disclosures forthe service providers who received only eligible indirect compensation. Complete as many entries as needed (seeinstructions).

(b) Enter name and EIN or address of person who provided you disclosure on eligible indirect compensation

20Note regarding Schedule A.

Schedule CSchedule C

2. Information on Other Service Providers Receiving Direct or Indirect Compensation. Except for those persons for whom youanswered “yes” to line 1a above, complete as many entries as needed to list each person receiving, directly or indirectly,$5,000 or more in total compensation (i.e., money or anything else of value) in connection with services rendered to theplan or their position with the plan during the plan year. (See instructions).

(a) Enter name and EIN or address (see instructions)

(b) (c) (d) (e) (f) (g) (h)

Service Code(s)

Relationship to employer,

employee organization,

or person known to be

Enter direct compensation

paid by the plan. If none,

enter -0-.

Did service provider receive

indirect compensation? (sources other

than plan or plan

Did indirect compensatio

n include eligible indirect

compensatio

Enter total indirect

compensation received by

service provider excluding eligible

Did the service

provider give you a formula instead of an amount or an

a party-in-interest

sponsor) n for which the plan

received the required

disclosures?

indirect compensation for

which you answered “Yes” to element (f). If none, enter -0-.

estimated amount?

21

F il t P id I f ti

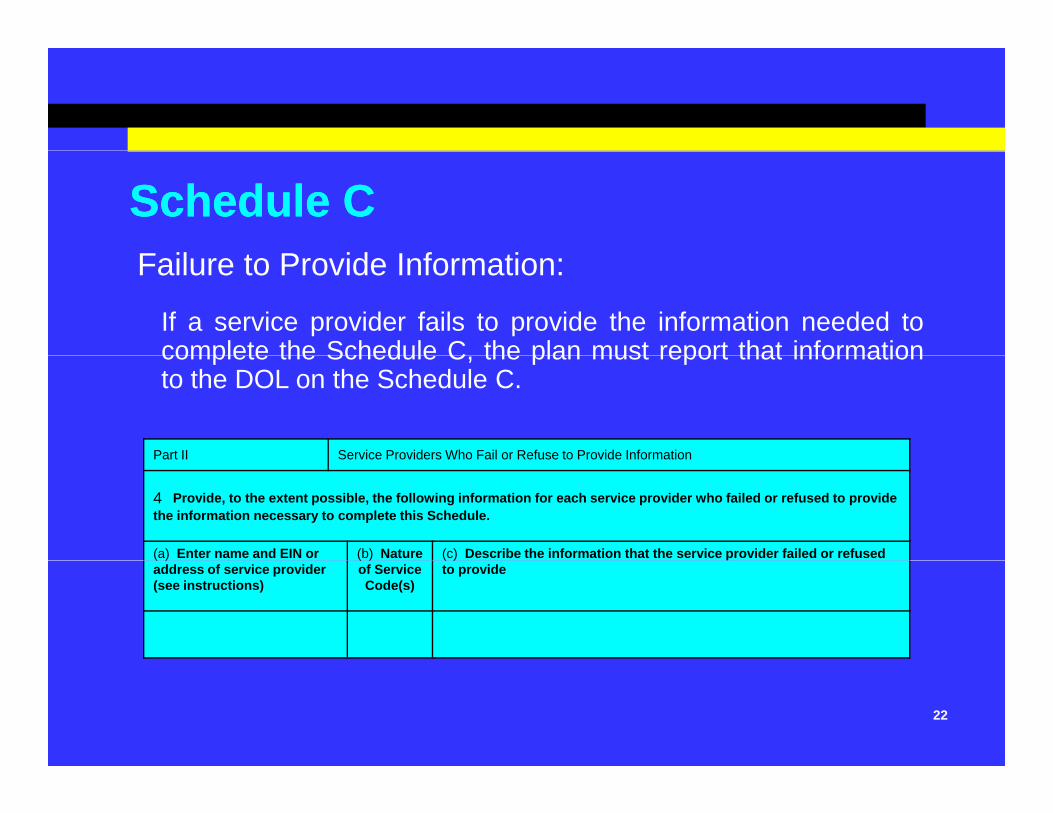

Schedule CSchedule CFailure to Provide Information:

If a service provider fails to provide the information needed tocomplete the Schedule C the plan must report that informationcomplete the Schedule C, the plan must report that informationto the DOL on the Schedule C.

Part II Service Providers Who Fail or Refuse to Provide InformationPart II Service Providers Who Fail or Refuse to Provide Information

4 Provide, to the extent possible, the following information for each service provider who failed or refused to provide the information necessary to complete this Schedule.

(a) Enter name and EIN or (b) Nature (c) Describe the information that the service provider failed or refused ( )address of service provider (see instructions)

( )of Service Code(s)

( )to provide

22

Disclosures: 408(b)(2) RegulationDisclosures: 408(b)(2) Regulation

The DOL sent, on March 3, a new 403(b) regulation tothe Office of Management and Budget. In the ordinary

th OMB ill t i l t M l Jcourse, the OMB will act in late May or early June.

The regulation will have a delayed effective date—g yperhaps January 1, 2011, or even 12 months after theregulation is issued.

23

Note regarding existing clients.

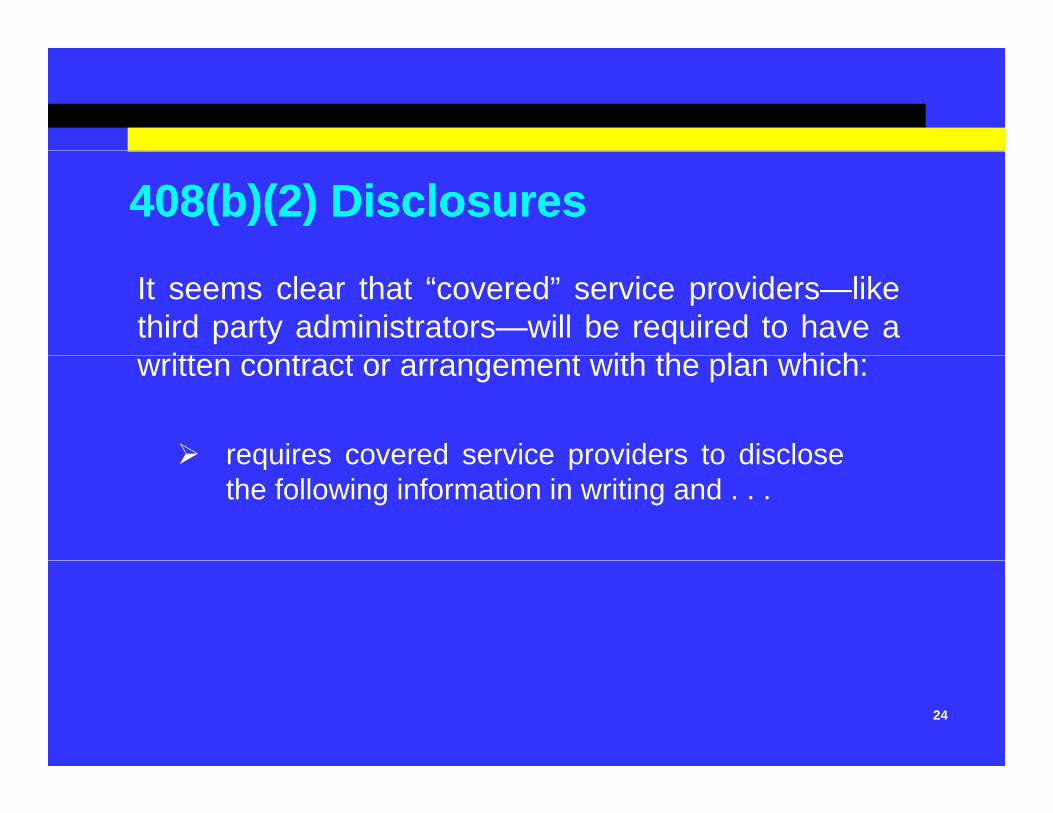

408(b)(2) Disclosures408(b)(2) Disclosures

It seems clear that “covered” service providers—likethird party administrators—will be required to have a

itt t t t ith th l hi hwritten contract or arrangement with the plan which:

requires covered service providers to discloserequires covered service providers to disclosethe following information in writing and . . .

24

408(b)(2) Disclosures408(b)(2) Disclosures

. . . includes a representation that, before thearrangement was entered into, information wasgiven to the “responsible plan fiduciary” following:

• a list of the services provided, and• for each service,

the compensation—direct or indirect—to be received andbe received, andthe manner of receipt.

• information about potential conflicts of interest.

25

p

Where do we go from here?Where do we go from here?

• Increase focus on compliance and risk management.

• Benefit of transparency.

• Risk management through well-drafted agreements.

26

ExamplesExamples

Disclose all indirect cash payments (materiality)

Disclose all other items of material value

Di l i l fliDisclose material conflicts

Limit fiduciary statusy

27

Disclosures to ParticipantsDisclosures to Participants

“Fiduciary Requirements for Disclosure in Participant-Directed Individual Account Plans”

DOL Work Plan for 2009-2010:

“The rulemaking will ensure that the participants andbeneficiaries in participant directed individual

Individual Account Plans

beneficiaries in participant-directed individualaccount plans are provided the information theyneed, including information about fees andexpenses to make informed investment decisions ”expenses, to make informed investment decisions.

28

Disclosures to ParticipantsDisclosures to Participants

Provider burden for compliance

Issues and Outcomes:

Provider burden for compliance.

Possible “push-back” by participants.

Impact on participant education.

29

Additional GuidanceAdditional GuidanceThe DOL is working on guidance to expand thedefinition of fiduciary:

The Department’s EBSA plans to publish aproposed regulation in June 2010 to amend theproposed regulation in June 2010 to amend thecurrent regulatory definition of “fiduciary” to includemore persons, such as pension consultants, asfiduciariesfiduciaries.

30

Participant Investing and Target Participant Investing and Target Date FundsDate FundsDate FundsDate FundsBecause of large losses by target date funds in 2008,the DOL and SEC held a joint hearing on June 18the DOL and SEC held a joint hearing on June 18,2009, on the subject of target date funds.

It is contemplated that the agencies will issue reportsor findings based on those hearings—and possiblyfollow up with guidance.follow up with guidance.

31

Participant Investing and Target Participant Investing and Target Date FundsDate FundsOutcome and Issues:

Date FundsDate Funds

• Better disclosure to plan sponsors and participants.

• Query regarding “labeling?”

• Fiduciary proposal by Senator Kohl.

• Selection and monitoring: like any other investment.g y

“to” and “through.”

last 10 years.

32

Participant Investment AdviceParticipant Investment Advice“Prohibited Transaction Exemption for Provision of InvestmentAdvice to Participants in Individual Account Plans”

“In order to qualify as an “eligible investment advicearrangement,” the arrangement must either providethat any fees received by the adviser do not varydepending on the basis of any investment optionsselected, or use a computer model under aninvestment advice program that meets the criteria setforth in section 408(g) in adviser connection with theforth in section 408(g) in adviser connection with theprovision of investment advice.

33

O t d I

Participant Investing and AdviceParticipant Investing and AdviceOutcome and Issues:

• Proposed regulation.

• Fiduciary status and level fees.

• Investment education: DOL Interpretive Bulletin 96-1.

• Products that “deliver” fiduciaries.

• Target date funds and risk-based funds.g

• IRAs.

34

Lifetime Income DisclosureLifetime Income DisclosureUnder the proposal, defined contribution plans subjectto ERISA would be required to include “annuityequivalents” on benefit statements provided toequivalents on benefit statements provided toemployees. An annuity equivalent would be themonthly annuity payment that would be made if theemployee’s total account balance were used to buy alife annuity that commenced payments at the plan’snormal retirement age (generally 65).g (g y )

Description of S 2832 from Office of Senator Bingaman

35

Description of S. 2832 from Office of Senator Bingaman.

Lifetime IncomeLifetime Income

The DOL and Treasury Departments have expresseda common interest in that issue and have developed

t f i f ti RFI t b d t tha request for information—or RFI—to be posed to theprivate sector.

36

Benefit Adequacy and Lifetime Benefit Adequacy and Lifetime IncomeIncomeOutcomes and Issues:

IncomeIncome

Gap analysis.

Emerging issue: Need for “solution ”Emerging issue: Need for solution.

Developments with GMWBs and GIFL.

• benefit base

• guaranteed income

37

FRED REISH, ESQ.11755 Wilshire Boulevard, 10th Floor Los Angeles, CA 90025-1539

(310) 478 5656 (310) 478 5831 [fax] (310) 776 7822 [direct fax](310) 478-5656 (310) 478-5831 [fax] (310) 776-7822 [direct fax][email protected] • www.linkedin.com/in/fredreish

www.reish.com/practice_areas/empbenefits.cfm

Q&A SessionQ&A Session

Q ti ???Questions???

For TPA Use Only. Not For Public Distribution. 39

Next TPA Administrator Training InstituteNext TPA Administrator Training Institute

Next Administrators Training Institute will be held in May

• Form 5500 Tools:

• Schedules (A, C, D)

• Activity Statement Review

• Audit Package Process

Be on the look out for the invitation!Be on the look out for the invitation!

For a copy of today’s presentation, and/or to request contact information for your Transamerica Sales Representative, please send request to

TPAServices@transamerica com

For TPA Use Only. Not For Public Distribution. 40

Transamerica. Master Retirement.®POWER CHOICE FREEDOM

Thank You.Be sure to join us at our nextBe sure to join us at our next

Transamerica Retirement Industry Speakers Bureau

For TPA Use Only. Not For Public Distribution.