welcome!. understanding & using plan design charles lockwood

Post on 20-Dec-2015

214 views

TRANSCRIPT

Welcome!

Understanding & Using Plan Design

Charles Lockwood

September 12, 2008

Charles Lockwood

ASC Institute, LLC

Highlands Ranch, CO

ERISA Workshop 2008ERISA Workshop 2008

ASCi

All qualified plans must be restated to comply with

current laws All pre-approved plans must be restated by April 30, 2010

Baby boomers are getting closer to retirement and looking for plan design options to help save more for retirement

Some ERs are trying to minimize fiduciary risk by eliminating investment risk on EEs

DB plans and hybrid plans (e.g., cash balance plans and new DB/k plans) will become more popular options

Importance of Plan Design Importance of Plan Design

ASCi

Each client has specific objectives in implementing and maintaining a retirement program Who is the plan for? Do HCEs want to maximize benefits? What are employee demographics? Does ER want to provide a guaranteed benefit? How much does employer want to spend?

Identify objectives and match them to plan design

Unique plan designs may fit unique needs

Plan Design – Traditional vs. UniquePlan Design – Traditional vs. Unique

ASCi

Rott ‘n Gumm Dentistry has a 401(k) plan with a 50% match on deferrals up to 6% of comp. The plan has failed the ADP test and Rott ‘n Gumm has had to make corrective distributions in each of the last 3 years

Plan Design Case StudyPlan Design Case Study

Dr. Rott, Dr. Gumm, and Dr. DeKay would like to maximize their contributions

Drs. Rott, Gumm and DeKay do not want to receive any more corrective distributions

Drs. Rott, Gumm and DeKay are happy with their current service providers

ASCi

Improving ADP ResultsImproving ADP Results Improve participation

Matching contributions = discretionary or fixed

Plan design Loans Hardships Participant-direction

Better communication Employee meetings

Avoid ADP testing altogether = safe harbor 401(k) plan

Automatic enrollment

ASCi

Basic matching contribution formula 100% of deferrals up to 3% of compensation

50% of deferrals between 3% and 5% of compensation

Enhanced matching contribution formula aggregate match which equals basic match at

each level of compensation

e.g., 100% of deferrals up to 4% of comp

Safe Harbor MatchSafe Harbor Match

ASCi

3% of compensation

Satisfies top heavy minimum requirements

May have other contributions (e.g., cross-tested formula)

Safe Harbor EmployerSafe Harbor Employer

ASCi

Required every year

30 - 90 days prior to beginning of plan year

New employees -- date of eligibility

New plan -- first day of plan year

May provide “maybe” notice with respect to 3% nonelective safe harbor contribution

Participant NoticeParticipant Notice

ASCi

EE Comp. DeferralsSafe Harbor

Match

Dr. Rott $230,000 $15,500 $9,200

Dr. Gumm $230,000 $15,500 $9,200

Dr. DeKay $230,000 $15,500 $9,200

NHCE 1 $80,000 $4,000 $3,200

NHCE 2 $65,000 $0 $0

NHCE 3 $47,000 $2,000 $1,880

NHCE 4 $42,000 $0 $0

NHCE 5 $42,000 $0 $0

NHCE 6 $39,000 $0 $0

NHCE 7 $30,000 $0 $0

NHCE 8 $25,000 $0 $0

Totals $1,060,000 $52,500 $32,680

* Safe harbor match = 100% of deferrals up to 4% of comp = must be 100% vested and cannot be subject to last day/ 1,000 HOS allocation condition

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

EE Comp. DeferralsSafe Harbor

Match Total

Dr. Rott $230,000 $15,500 $9,200 $24,700

Dr. Gumm $230,000 $15,500 $9,200 $24,700

Dr. DeKay $230,000 $15,500 $9,200 $24,700

NHCE 1 $80,000 $4,000 $3,200 $7,200

NHCE 2 $65,000 $0 $0 $0

NHCE 3 $47,000 $2,000 $1,880 $3,880

NHCE 4 $42,000 $0 $0 $0

NHCE 5 $42,000 $0 $0 $0

NHCE 6 $39,000 $0 $0 $0

NHCE 7 $30,000 $0 $0 $0

NHCE 8 $25,000 $0 $0 $0

Totals $1,060,000 $52,500 $32,680 $85,180

Could Rott n’ Gumm make an additional matching contribution without subjecting the plan to ADP/ACP testing?

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

EE Comp. DeferralsSafe Harbor

MatchDiscret.Match

Dr. Rott $230,000 $15,500 $9,200 $9,200

Dr. Gumm $230,000 $15,500 $9,200 $9,200

Dr. DeKay $230,000 $15,500 $9,200 $9,200

NHCE 1 $80,000 $4,000 $3,200

NHCE 2 $65,000 $0 $0

NHCE 3 $47,000 $2,000 $1,880

NHCE 4 $42,000 $0 $0

NHCE 5 $42,000 $0 $0

NHCE 6 $39,000 $0 $0

NHCE 7 $30,000 $0 $0

NHCE 8 $25,000 $0 $0

Totals $1,060,000 $52,500 $32,680

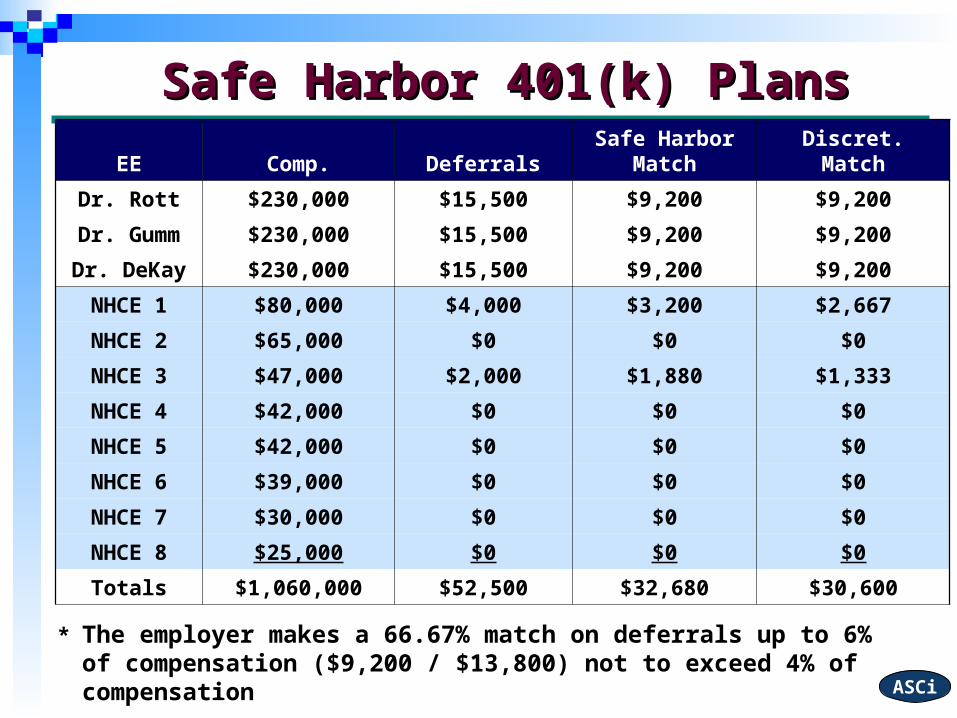

* Plan provides for safe harbor match with additional discretionary matching contribution on deferrals up to 6% of compensation not to exceed 4% of compensation

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

EE Comp. DeferralsSafe Harbor

MatchDiscret.Match

Dr. Rott $230,000 $15,500 $9,200 $9,200

Dr. Gumm $230,000 $15,500 $9,200 $9,200

Dr. DeKay $230,000 $15,500 $9,200 $9,200

NHCE 1 $80,000 $4,000 $3,200 $2,667

NHCE 2 $65,000 $0 $0 $0

NHCE 3 $47,000 $2,000 $1,880 $1,333

NHCE 4 $42,000 $0 $0 $0

NHCE 5 $42,000 $0 $0 $0

NHCE 6 $39,000 $0 $0 $0

NHCE 7 $30,000 $0 $0 $0

NHCE 8 $25,000 $0 $0 $0

Totals $1,060,000 $52,500 $32,680 $30,600

* The employer makes a 66.67% match on deferrals up to 6% of compensation ($9,200 / $13,800) not to exceed 4% of compensation

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

Is plan subject to ACP test?

No!

May plan impose vesting schedule on additional matching contributions? Yes!

May plan impose allocation conditions on additional match? No!

Must plan provide top-heavy minimum contribution? No! SH plan is exempt from top-heavy if ONLY contributions are SH contributions

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

EE Comp. DeferralSH

MatchDiscret.Match

FixedMatch Total

Dr. Rott $230,000 $15,500 $9,200 $7,500 $13,800 $46,000

Dr. Gumm $230,000 $15,500 $9,200 $7,500 $13,800 $46,000

Dr. DeKay $230,000 $15,500 $9,200 $7,500 $13,800 $46,000

NHCE 1 $80,000 $4,000 $3,200 $2,174 $4,000 $13,374

NHCE 2 $65,000 $0 $0 $0 $0 $0

NHCE 3 $47,000 $2,000 $1,880 $1,087 $2,000 $6,967

NHCE 4 $42,000 $0 $0 $0 $0 $0

NHCE 5 $42,000 $0 $0 $0 $0 $0

NHCE 6 $39,000 $0 $0 $0 $0 $0

NHCE 7 $30,000 $0 $0 $0 $0 $0

NHCE 8 $25,000 $0 $0 $0 $0 $0

Totals $1,060,000 $52,500 $32,680 $25,761 $47,400 $158,341

* Plan provides for 100% fixed match on deferrals up to 6% of comp. To maximize contributions, ER makes a 54.35% discretionary match on deferrals up to 6% of comp ($7,500 / $13,800)

Safe Harbor 401(k) PlansSafe Harbor 401(k) Plans

ASCi

Scary NewsScary News Only 43% of private sector workers are

covered by a retirement plan

Only 60% of workers over age 40 who are eligible for 401(k) plans actually participate

Average A/B of EEs in plans age 60 and above is $141,000 (which will provide annuity of $12,203 for male and $11,172 for female commencing at age 65)

Only 44% of families nearing retirement have IRAs with average balance of $60,000

ASCi

Automatic EnrollmentAutomatic Enrollment Congress/IRS are encouraging 401(k) plans

to add automatic enrollment features

35

86

19

75

13

80

0

10

20

30

40

50

60

70

80

90

Females Hispanics Under $20K

Without autoenrollmentWith autoenrollment

Actual results from employees between 3 and 15 months tenure. Study by Professor Brigitte Madrian, University of Pennsylvania’s Wharton School and Dennis Shea, United Health Group

ASCi

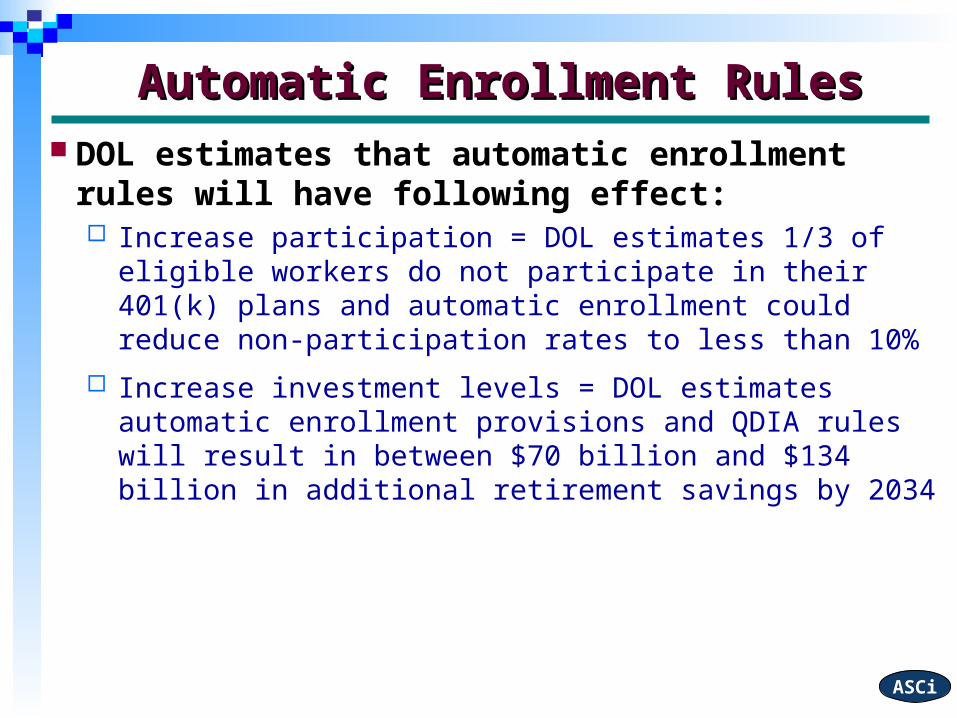

DOL estimates that automatic enrollment rules will have following effect: Increase participation = DOL estimates 1/3 of

eligible workers do not participate in their 401(k) plans and automatic enrollment could reduce non-participation rates to less than 10%

Increase investment levels = DOL estimates automatic enrollment provisions and QDIA rules will result in between $70 billion and $134 billion in additional retirement savings by 2034

Automatic Enrollment RulesAutomatic Enrollment Rules

ASCi

Beginning in 2006 – ERs were permitted to add Roth features to 401(k) plans

Advantages of Roth Deferrals Must pay taxes currently but can take qualified distribution without

taxation (including earnings) Must leave Roth Deferrals in plan for at least 5 years and must take

distribution as qualified distribution (e.g., death, disability, age 59½)

Response has been fairly lukewarm Difficult to explain to NHCEs and administrative problems May be renewed interest in Roth contributions

What About Roth Deferrals?What About Roth Deferrals?

ASCi

Under PPA – beginning in 2008, EEs can roll from 401(k) plan to Roth IRA Must pay income tax at time of rollover

AGI restrictions still apply (i.e., must have AGI below $100,000) Post-2008 rollover may be accomplished by direct rollover or 60-

day rollover Plan Administrator of distributing plan is not responsible for

ensuring that EE is eligible to make a rollover to a Roth IRA No mandatory 20% withholding and early withdrawal penalty tax

does not apply

Conversion to Roth IRAConversion to Roth IRA

ASCi

PPA allows conversion beginning in 2010 for all taxpayers AGI limits no longer apply = HCEs can convert

existing IRAs to Roth IRAs

Income taxes due on conversion can be spread over 2 years (e.g., 2011 and 2012)

Conversions in subsequent years are included in income during tax year in which conversion is completed

Conversion to Roth IRAConversion to Roth IRA

ASCi

May want to begin taking action to maximize Roth conversion opportunity (and reduced taxation) in 2010

If possible = open up Roth IRA now to begin 5-year clock If available = make contributions to traditional IRA to prepare

for conversion If cannot make deductible contributions = make after-tax

contributions to traditional IRA and convert in 2010 Rollover from qualified plan to traditional IRA and then convert

= amend plan to allow for in-service distribution

Conversion to Roth IRAConversion to Roth IRA

ASCi

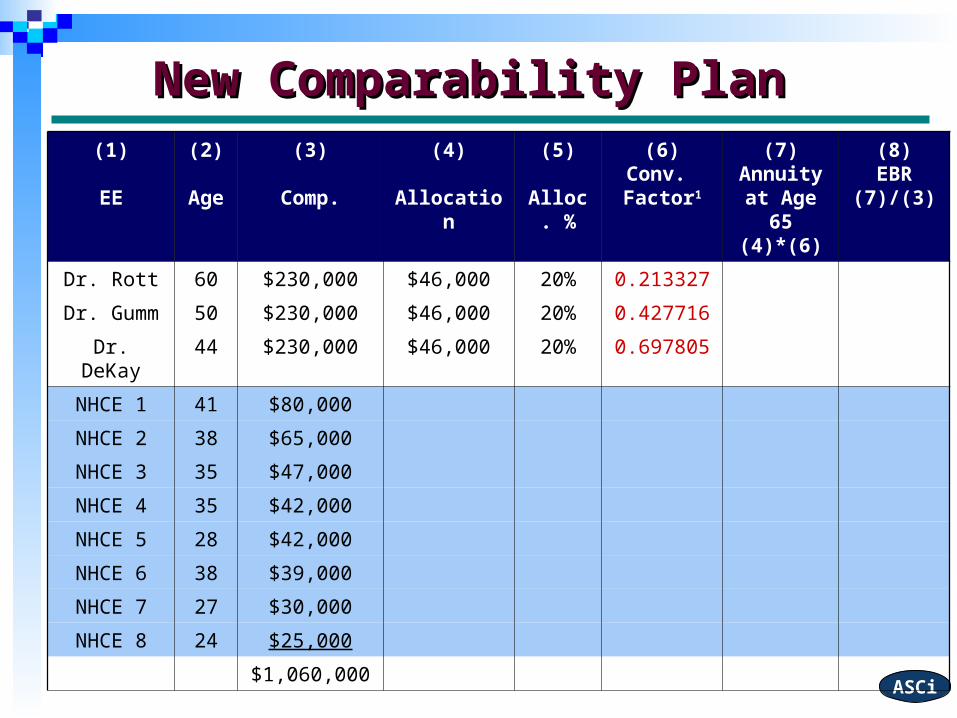

Have become very popular = based on concept of “cross-

testing”

Permits substantial disparity in contribution for older employees

Must be tested for discrimination using general nondiscrimination test

IRS has issued regulations requiring a minimum 5% contribution for NHCEs in a “cross-tested” plan

New Comparability PlanNew Comparability Plan

ASCi

EE Age Comp

Dr. Rott 60 $230,000

Dr. Gumm 50 $230,000

Dr. DeKay 44 $230,000

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000

Dr. Gumm 50 $230,000

Dr. DeKay 44 $230,000

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20%

Dr. Gumm 50 $230,000 $46,000 20%

Dr. DeKay 44 $230,000 $46,000 20%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

Factor used to convert contribution to equivalent benefit rate (EBR) at NRA

Conversion factor: Project contribution to NRA at applicable interest rate (e.g.,

8.5%) = Contribution * 1.085^N where N is years to NRA

Convert projected benefit to life annuity at age 65 based on applicable interest rate and mortality table (e.g., 8.5% and UP 1984 table) = 7.9486 annuity factor

Example = Dr. Rott (age 45) has a conversion factor of 0.643138 (1.085^20 / 7.9486)

Conversion FactorConversion Factor

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20% 0.213327

Dr. Gumm 50 $230,000 $46,000 20% 0.427716

Dr. DeKay 44 $230,000 $46,000 20% 0.697805

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

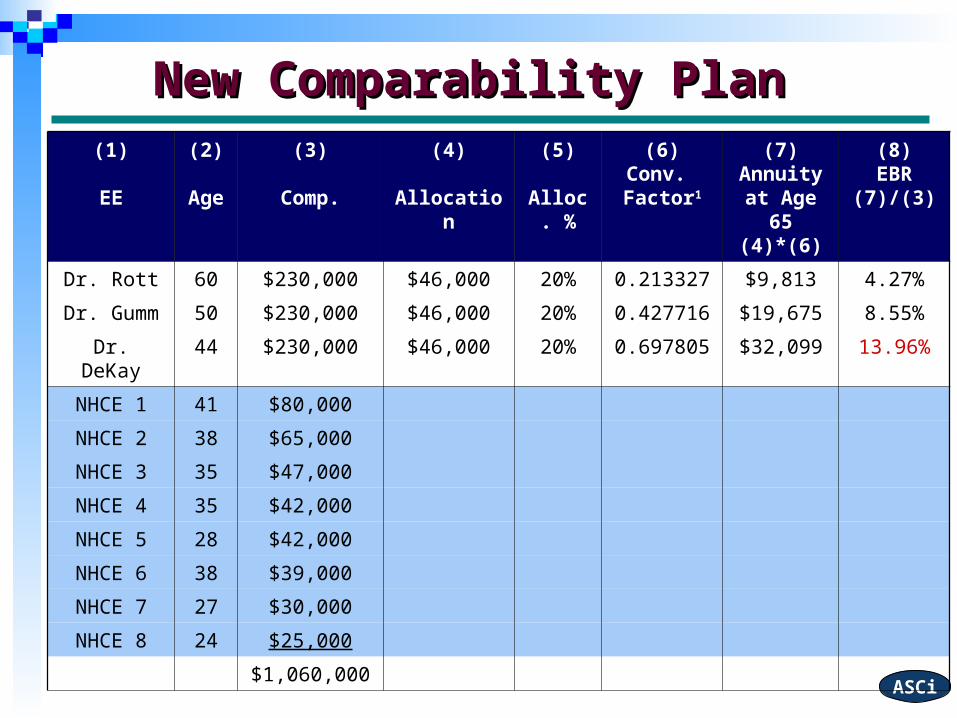

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813 4.27%

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675 8.55%

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099 13.96%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813 4.27%

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675 8.55%

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099 13.96%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813 4.27%

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675 8.55%

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099 13.96%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000 $978 3.91% 3.567210 3,489 13.96%

$1,060,000

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813 4.27%

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675 8.55%

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099 13.96%

NHCE 1 41 $80,000 $3,128 3.91% 0.891298 2,788 3.49%

NHCE 2 38 $65,000 $2,542 3.91% 1.138446 2,894 4.45%

NHCE 3 35 $47,000 $1,838 3.91% 1.454124 2,673 5.67%

NHCE 4 35 $42,000 $1,642 3.91% 1.454124 2,388 5.67%

NHCE 5 28 $42,000 $1,642 3.91% 2.574007 4,227 10.06%

NHCE 6 38 $39,000 $1,525 3.91% 1.138446 1,736 4.45%

NHCE 7 27 $30,000 $1,173 3.91% 2.792797 3,276 10.92%

NHCE 8 24 $25,000 $978 3.91% 3.567210 3,489 13.96%

$1,060,000 $148,473

New Comparability PlanNew Comparability Plan

ASCi

Gateway test = to use “cross-testing” for discrimination testing, plan must satisfy one of “gateway” tests: All benefiting NHCEs must receive at least 5% allocation (based on

§415(c) compensation) OR Lowest allocation to any NHCE must be at least 1/3 of highest allocation

to any HCE (based on any definition of §414(s) compensation)

Example. If highest HCE rate is 12%, lowest NHC rate must be 4%. If highest HCE rate is 18%, lowest NHC rate must be 5%.

Minimum Gateway RequirementsMinimum Gateway Requirements

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

(6)Conv. Factor1

(7)Annuity at Age

65(4)*(6)

(8)EBR

(7)/(3)

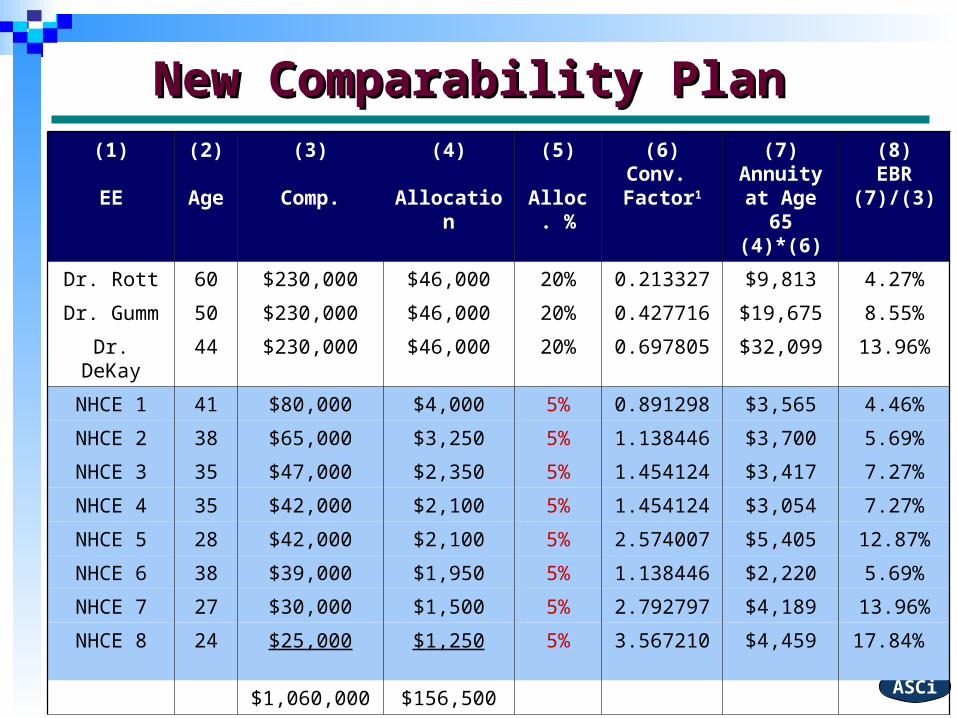

Dr. Rott 60 $230,000 $46,000 20% 0.213327 $9,813 4.27%

Dr. Gumm 50 $230,000 $46,000 20% 0.427716 $19,675 8.55%

Dr. DeKay 44 $230,000 $46,000 20% 0.697805 $32,099 13.96%

NHCE 1 41 $80,000 $4,000 5% 0.891298 $3,565 4.46%

NHCE 2 38 $65,000 $3,250 5% 1.138446 $3,700 5.69%

NHCE 3 35 $47,000 $2,350 5% 1.454124 $3,417 7.27%

NHCE 4 35 $42,000 $2,100 5% 1.454124 $3,054 7.27%

NHCE 5 28 $42,000 $2,100 5% 2.574007 $5,405 12.87%

NHCE 6 38 $39,000 $1,950 5% 1.138446 $2,220 5.69%

NHCE 7 27 $30,000 $1,500 5% 2.792797 $4,189 13.96%

NHCE 8 24 $25,000 $1,250 5% 3.567210 $4,459 17.84%

$1,060,000 $156,500

New Comparability PlanNew Comparability Plan

ASCi

(1)

EE

(2)

Age

(3)

Comp.

(4)

Allocation

(5)

Alloc. %

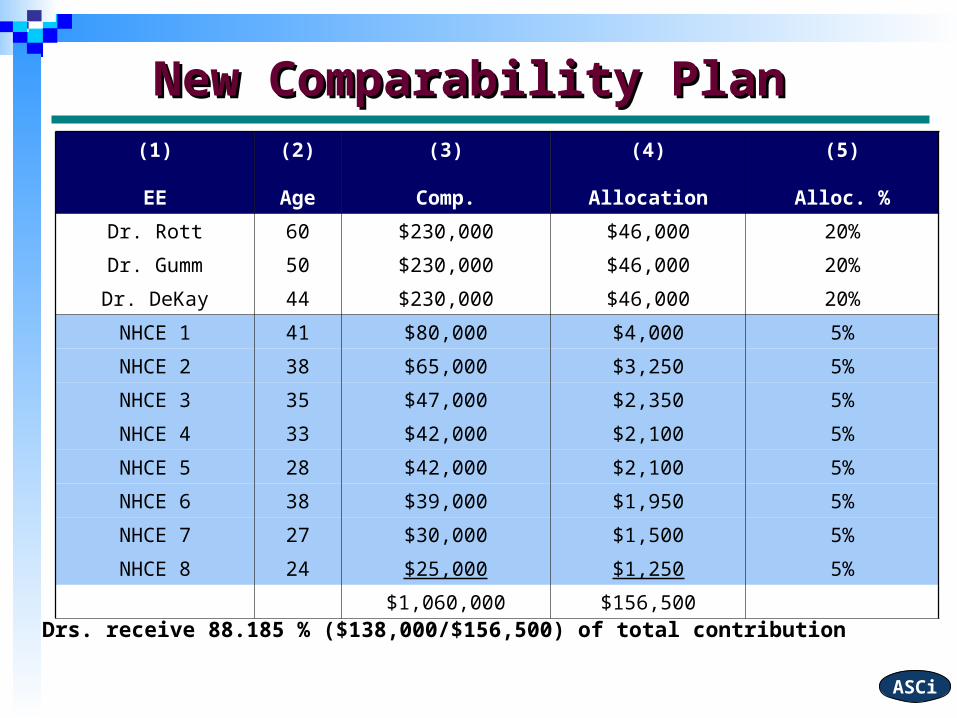

Dr. Rott 60 $230,000 $46,000 20%

Dr. Gumm 50 $230,000 $46,000 20%

Dr. DeKay 44 $230,000 $46,000 20%

NHCE 1 41 $80,000 $4,000 5%

NHCE 2 38 $65,000 $3,250 5%

NHCE 3 35 $47,000 $2,350 5%

NHCE 4 33 $42,000 $2,100 5%

NHCE 5 28 $42,000 $2,100 5%

NHCE 6 38 $39,000 $1,950 5%

NHCE 7 27 $30,000 $1,500 5%

NHCE 8 24 $25,000 $1,250 5%

$1,060,000 $156,500Drs. receive 88.185 % ($138,000/$156,500) of total contribution

New Comparability PlanNew Comparability Plan

ASCi

EE Age Comp. DeferSH ER

ContribER

ContribTotal

ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000

Dr. Gumm 50 $230,000

Dr. DeKay 44 $230,000

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age Comp. DeferSH ER

ContribER

ContribTotal

ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000 $15,500

Dr. Gumm 50 $230,000 $15,500

Dr. DeKay 44 $230,000 $15,500

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age Comp. DeferSH ER

ContribER

ContribTotal

ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000 $15,500 $6,900 $23,600 $30,500 13.26%

Dr. Gumm 50 $230,000 $15,500 $6,900 $23,600 $30,500 13.26%

Dr. DeKay 44 $230,000 $15,500 $6,900 $23,600 $30,500 13.26%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age Comp. DeferSH ER

ContribER

ContribTotal

ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 2.80%

Dr. Gumm 50 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 5.61%

Dr. DeKay 44 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 9.15%

NHCE 1 41 $80,000

NHCE 2 38 $65,000

NHCE 3 35 $47,000

NHCE 4 35 $42,000

NHCE 5 28 $42,000

NHCE 6 38 $39,000

NHCE 7 27 $30,000

NHCE 8 24 $25,000

$1,060,000

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age Comp. DeferSH ER

ContribER

ContribTotal ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 2.80%

Dr. Gumm 50 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 5.61%

Dr. DeKay 44 $230,000 $15,500 $6,900 $23,600 $30,500 13.26% 9.15%

NHCE 1 41 $80,000 $1,000 $2,400 $1,136 $3,536 4.42% 3.89%

NHCE 2 38 $65,000 $0 $1,950 $923 $2,873 4.42% 4.98%

NHCE 3 35 $47,000 $0 $1,410 $667 $2,077 4.42% 6.35%

NHCE 4 35 $42,000 $0 $1,260 $596 $1,856 4.42% 6.35%

NHCE 5 28 $42,000 $0 $1,260 $596 $1,856 4.42% 11.25%

NHCE 6 38 $39,000 $0 $1,170 $554 $1,724 4.42% 4.98%

NHCE 7 27 $30,000 $0 $900 $426 $1,326 4.42% 12.20%

NHCE 8 24 $25,000 $0 $750 $355 $1,105 4.42% 15.60%

$1,060,000 $47,500 $31,800 $76,053 $107,853

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age Comp. DeferTotal ERContrib

Alloc. %

Dr. Rott 60 $230,000 $15,500 $30,500 13.26%

Dr. Gumm 50 $230,000 $15,500 $30,500 13.26%

Dr. DeKay 44 $230,000 $15,500 $30,500 13.26%

NHCE 1 41 $80,000 $1,000 $3,536 4.42%

NHCE 2 38 $65,000 $0 $2,873 4.42%

NHCE 3 35 $47,000 $0 $2,077 4.42%

NHCE 4 35 $42,000 $0 $1,856 4.42%

NHCE 5 28 $42,000 $0 $1,856 4.42%

NHCE 6 38 $39,000 $0 $1,724 4.42%

NHCE 7 27 $30,000 $0 $1,326 4.42%

NHCE 8 24 $25,000 $0 $1,105 4.42%

$1,060,000 $47,500 $107,853

Drs. receive 84.84% ($91,500/$107,853) of total contribution plus deferrals

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

Plan document issues = more limited under prototype plans

Turnover / hiring practices

Excluding family members

Failure of average benefits test = automatic enrollment

Not enough time to accumulate sufficient retirement savings

Potential IssuesPotential Issues

When to Recommend DB/DC Combo & Cash Balance Plans

Charles Lockwood

ASCi

Can provide substantially greater benefit to

older employees (generally over 40 years old)

Especially useful for sole proprietors (or employers with very few EEs)

Benefit is guaranteed at retirement = employer bears investment risk

Entire normal cost is deductible = no limit unless combine with defined contribution plan

Why Do DB Plans Make Sense?Why Do DB Plans Make Sense?

ASCi

Age Maximum Accrual

37 $35,073

38 $37,178

39 $39,409

40 $41,773

41 $44,279

42 $46,936

43 $49,752

44 $52,738

45 $55,902

46 $59,256

47 $62,811

48 $66,580

49 $70,575

50 $74,809

Age Maximum Accrual

51 $79298

52 $84,056

53 $89,099

54 $94,445

55 $100,112

56 $106,118

57 $112,485

58 $119,235

59 $126,389

60 $133,972

61 $142,010

62 $150,531

63 $159,563

64 $169,136

Maximum benefit accrual for first year of plan assuming normal retirement age of 65, 6% interest assumption and ’94 GAR mortality table

Benefit Accruals Under a DB PlanBenefit Accruals Under a DB Plan

ASCi

Code §415 limits how much an EE may receive under a

qualified plan

DC plan limit = lesser of $45,000 or 100% of compensation

DB plan limit = based on maximum annual benefit that can be provided at retirement

Under EGTRRA = DB limit is the lesser of 100% of 3 year high average compensation or $185,000

Code 415 LimitsCode 415 Limits

ASCi

EE Age Comp. Accrual

Dr. Rott 60 $230,000 $133,972

Dr. Gumm 50 $230,000 $72,472

Dr. DeKay 40 $230,000 $41,728

NHCE 1 50 $80,000 $28,498

NHCE 2 48 $65,000 $20,608

NHCE 3 40 $47,000 $9,349

NHCE 4 39 $42,000 $7,881

NHCE 5 35 $42,000 $6,042

NHCE 6 35 $39,000 $5,791

NHCE 7 27 $30,000 $2,863

NHCE 8 24 $25,000 $2,003

$1,060,000 $331,207

Plan formula = 8.09% x YOP (up to 5) -- age 65 NRA, 6% interest, 94 GAR mortality table

Sample Defined Benefit PlanSample Defined Benefit Plan

ASCi

Cover enough EEs in both plans to pass

coverage and Code §401(a)(26) Can be maintained separately without combined testing

No cross-participation allows plan to avoid 25% combined deduction limit DB plan can always deduct “normal cost” and DC plan

can deduct up to 25% of total comp If have cross-participation = no deduction in DC plan to

DB/DC contribution exceeds 25% of compensation New rules allow plan to deduct up to 6% of

compensation in DC plan

DB Carve-OutDB Carve-Out

ASCi

EE Age Comp. DC Contribution DB Accrual

Dr. Rott 60 $230,000 $0 $133,972

Dr. Gumm 50 $230,000 $0 $72,472

Dr. DeKay 40 $230,000 $46,000 $0

NHCE 1 50 $80,000 $4,891 $0

NHCE 2 48 $65,000 $3,974 $0

NHCE 3 40 $47,000 $0 $9,349

NHCE 4 39 $42,000 $0 $7,881

NHCE 5 35 $42,000 $0 $6,042

NHCE 6 35 $39,000 $0 $5,791

NHCE 7 27 $30,000 $1,834 $0

NHCE 8 24 $25,000 $1,529 $0

$1,060,000 $57,228 $235,507• Both plans satisfy coverage / nondiscrimination• DB plan satisfies 401(a)(26)• No deduction problem = no cross participation

DB/DC CombinationDB/DC Combination

ASCi

Different contributions for EEs based on age Hard to communicate to employees = younger

employees don’t appreciate life annuity at age 65

Plans can become underfunded or overfunded Can limit possibility by using appropriate investment vehicle

Must have enrolled actuary to determine funding and to sign Schedule B of Form 5500

Problems with DB PlansProblems with DB Plans

ASCi

Defined benefit plan that looks and acts like a defined contribution plan

DB characteristics Contribution is based on actuarial funding concepts = employer

bears risk of gain or loss

DB 415 limits apply = permits greater contributions than DC plan

Subject to PBGC coverage

Must file a Schedule B with Form 5500

Subject to QJSA rules

Cash Balance PlansCash Balance Plans

ASCi

DC characteristics

Benefit expressed as a hypothetical account balance

Benefit and interest credited to the account each year = must be defined in plan document Plan looks like DC plan because benefit is determined

like a “contribution” to a DC plan Plan is a DB-plan because benefit is determined based

on value at NRA using an assumed interest credit

Cash Balance PlansCash Balance Plans

ASCi

Advantages Participants receive a DC-type statement showing value of

hypothetical account Participants do not have the ability to direct investment of

their “account”

Distribution option generally will be a lump sum Need clarification from Congress/IRS on whipsaw issue which

forces plan to use lower that desired interest credits

Allows a more equitable sharing of costs among HCEs

Cash Balance PlansCash Balance Plans

ASCi

Business has stable income to meet continuing

funding obligation

Targeted group (e.g., owner) is age 50 or older with compensation > $230,000

Owners want to maximize contribution at a level above what is available in DC plan

ER has existing new comparability plan with “room” under the maximum deduction limit

Candidate for Cash Balance PlanCandidate for Cash Balance Plan

ASCi

EE Age

Comp. DeferTotal ERContrib

Alloc. %EBR

Dr. Rott 60 $230,000 $15,500 $30,500 13.26% 2.80%

Dr. Gumm 50 $230,000 $15,500 $30,500 13.26% 5.61%

Dr. DeKay 44 $230,000 $15,500 $30,500 13.26% 9.15%

NHCE 1 41 $80,000 $4,800 $3,536 4.42% 3.89%

NHCE 2 38 $65,000 $4,000 $2,873 4.42% 4.98%

NHCE 3 35 $47,000 $0 $2,077 4.42% 6.35%

NHCE 4 35 $42,000 $2,000 $1,856 4.42% 6.35%

NHCE 5 28 $42,000 $0 $1,856 4.42% 11.25%

NHCE 6 38 $39,000 $0 $1,724 4.42% 4.98%

NHCE 7 27 $30,000 $1,000 $1,326 4.42% 12.20%

NHCE 8 24 $25,000 $2,500 $1,105 4.42% 15.60%

$1,060,000 $60,800 $107,853

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

ASCi

EE Age

Comp. DeferTotal ERContrib

Alloc. % EBR

Dr. Rott 60 $230,000 $15,500 $30,500 13.26% 2.80%

Dr. Gumm 50 $230,000 $15,500 $30,500 13.26% 5.61%

Dr. DeKay 44 $230,000 $15,500 $30,500 13.26% 9.15%

NHCE 1 41 $80,000 $4,800 $3,536 4.42% 3.89%

NHCE 2 38 $65,000 $4,000 $2,873 4.42% 4.98%

NHCE 3 35 $47,000 $0 $2,077 4.42% 6.35%

NHCE 4 35 $42,000 $2,000 $1,856 4.42% 6.35%

NHCE 5 28 $42,000 $0 $1,856 4.42% 11.25%

NHCE 6 38 $39,000 $0 $1,724 4.42% 4.98%

NHCE 7 27 $30,000 $1,000 $1,326 4.42% 12.20%

NHCE 8 24 $25,000 $2,500 $1,105 4.42% 15.60%

$1,060,000 $60,800 $107,853

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

Deductible limit = 25% * $1,060,000 = $265,000Total deductible contrib. = $107,853 (deferrals always deductible)Remaining deductible amount = $157,147

ASCi

EE Age Comp. DeferTotal ERContrib

Alloc. %EBR

Additional

Benefit

Dr. Rott 60 $230,000 $15,500 $30,500 13.26% 2.80% $40,000

Dr. Gumm 50 $230,000 $15,500 $30,500 13.26% 5.61% $40,000

Dr. DeKay 44 $230,000 $15,500 $30,500 13.26% 9.15% $40,000

NHCE 1 41 $80,000 $4,800 $3,536 4.42% 3.89%

NHCE 2 38 $65,000 $4,000 $2,873 4.42% 4.98%

NHCE 3 35 $47,000 $0 $2,077 4.42% 6.35%

NHCE 4 35 $42,000 $2,000 $1,856 4.42% 6.35%

NHCE 5 28 $42,000 $0 $1,856 4.42% 11.25%

NHCE 6 38 $39,000 $0 $1,724 4.42% 4.98%

NHCE 7 27 $30,000 $1,000 $1,326 4.42% 12.20%

NHCE 8 24 $25,000 $2,500 $1,105 4.42% 15.60%

$1,060,000 $60,800 $107,853

New Comp / SH 401(k) PlanNew Comp / SH 401(k) Plan

Deductible limit = 25% * $1,060,000 = $265,000Total deductible contrib. = $107,853 (deferrals always deductible)Remaining deductible amount = $157,147

ASCi

Cash balance plan is DB plan

Subject to DB 415 limit and funding rules

Combined plans must satisfy minimum gateway requirement 7.5% gateway applies to DC/DB plans

Cash balance plan must satisfy Code §401(a)(26) Must provide at least 40% of employees with at least 0.5%

NAR

Combined plans are subject to 25% deduction limit

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

ASCi

Gateway for DB/DC PlansGateway for DB/DC Plans

Highest HCE ANAR ANAR for NHCEs

Less than 15% At least 1/3 of the HCE rate

15% to 25% 5%

25% - 30% 6%

30-35% 7%

Above 35% 7½%

To satisfy the minimum gateway for DB/DC combination plans, each NHCE must have an aggregate normal allocation rate (ANAR) that meets following requirements:

ASCi

Cash balance plan is DB plan

Subject to DB 415 limit and funding rules

Combined plans must satisfy minimum gateway requirement 7.5% gateway applies to DC/DB plans

Cash balance plan must satisfy Code §401(a)(26) Must provide at least 40% of employees with at least 0.5%

NAR

Combined plans are subject to 25% deduction limit

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15%

NHCE 1 41 $80,000 $4,800 $6,000

NHCE 2 38 $65,000 $4,000 $4,875

NHCE 3 35 $47,000 $0 $3,525

NHCE 4 35 $42,000 $2,000 $3,150

NHCE 5 28 $42,000 $0 $3,150

NHCE 6 38 $39,000 $0 $2,925

NHCE 7 27 $30,000 $1,000 $2,250

NHCE 8 24 $25,000 $2,500 $1,875

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Plan satisfies minimum gateway = NHCEs receive 7.5% allocation in DC plan

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15%

NHCE 1 41 $80,000 $4,800 $6,000 6.69%

NHCE 2 38 $65,000 $4,000 $4,875 8.54%

NHCE 3 35 $47,000 $0 $3,525 10.91%

NHCE 4 35 $42,000 $2,000 $3,150 10.91%

NHCE 5 28 $42,000 $0 $3,150 19.31%

NHCE 6 38 $39,000 $0 $2,925 8.54%

NHCE 7 27 $30,000 $1,000 $2,250 20.95%

NHCE 8 24 $25,000 $2,500 $1,875 26.75%

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Convert DC allocation to EBRs using applicable interest rate (8.5%) and applicable mortality table (UP-1984)

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

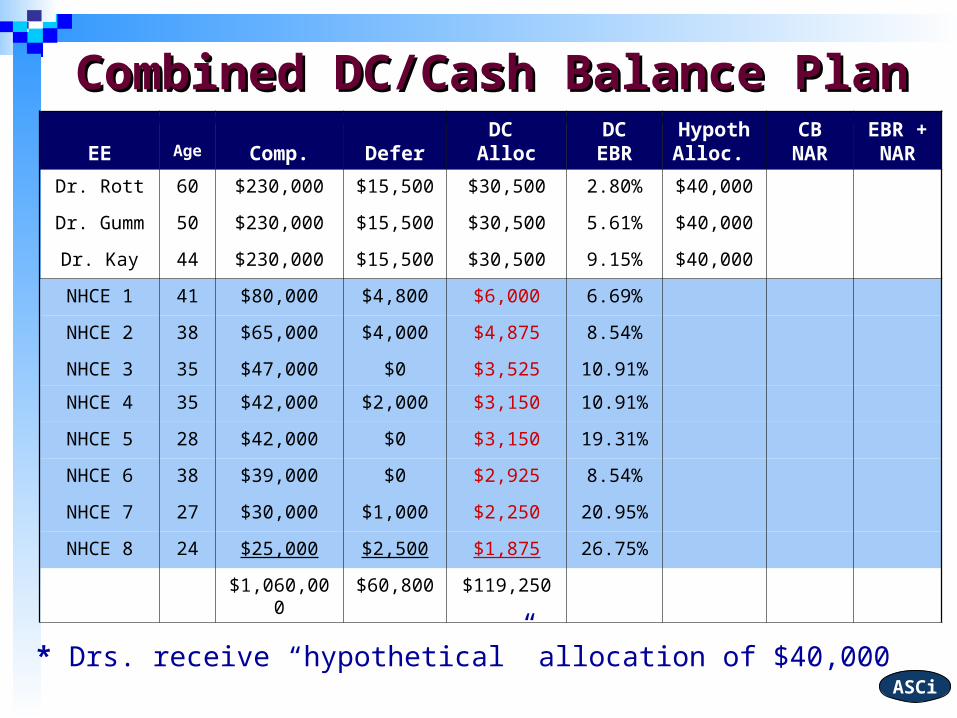

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000

NHCE 1 41 $80,000 $4,800 $6,000 6.69%

NHCE 2 38 $65,000 $4,000 $4,875 8.54%

NHCE 3 35 $47,000 $0 $3,525 10.91%

NHCE 4 35 $42,000 $2,000 $3,150 10.91%

NHCE 5 28 $42,000 $0 $3,150 19.31%

NHCE 6 38 $39,000 $0 $2,925 8.54%

NHCE 7 27 $30,000 $1,000 $2,250 20.95%

NHCE 8 24 $25,000 $2,500 $1,875 26.75%

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Drs. receive “hypothetical” allocation of $40,000

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83%

NHCE 1 41 $80,000 $4,800 $6,000 6.69%

NHCE 2 38 $65,000 $4,000 $4,875 8.54%

NHCE 3 35 $47,000 $0 $3,525 10.91%

NHCE 4 35 $42,000 $2,000 $3,150 10.91%

NHCE 5 28 $42,000 $0 $3,150 19.31%

NHCE 6 38 $39,000 $0 $2,925 8.54%

NHCE 7 27 $30,000 $1,000 $2,250 20.95%

NHCE 8 24 $25,000 $2,500 $1,875 26.75%

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Hypothetical allocation is converted to Normal Accrual Rate (NAR) using plan’s assumptions = 5% interest rate and ’94 GAR mortality table

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69%

NHCE 2 38 $65,000 $4,000 $4,875 8.54%

NHCE 3 35 $47,000 $0 $3,525 10.91%

NHCE 4 35 $42,000 $2,000 $3,150 10.91%

NHCE 5 28 $42,000 $0 $3,150 19.31%

NHCE 6 38 $39,000 $0 $2,925 8.54%

NHCE 7 27 $30,000 $1,000 $2,250 20.95%

NHCE 8 24 $25,000 $2,500 $1,875 26.75%

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* DC EBR and CB NAR are added together to get benefit rate subject to rate group test

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $0

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $0

NHCE 3 35 $47,000 $0 $3,525 10.91% $0

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $0

NHCE 5 28 $42,000 $0 $3,150 19.31% $0

NHCE 6 38 $39,000 $0 $2,925 8.54% $0

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $0

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $0

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $0

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $0

NHCE 3 35 $47,000 $0 $3,525 10.91% $0

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $0

NHCE 5 28 $42,000 $0 $3,150 19.31% $0

NHCE 6 38 $39,000 $0 $2,925 8.54% $0

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $0

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $0

$1,060,000 $60,800 $119,250

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

Plan fails 401(a)(26) = must have at least 40% of employees receiving “meaningful benefit” which IRS has defined as .5% accrual

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $300

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $300

NHCE 3 35 $47,000 $0 $3,525 10.91% $300

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $300

NHCE 5 28 $42,000 $0 $3,150 19.31% $300

NHCE 6 38 $39,000 $0 $2,925 8.54% $300

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $300

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $300

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

*NHCEs receive hypothetical allocation of $300

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $300 0.10%

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $300 0.28%

NHCE 3 35 $47,000 $0 $3,525 10.91% $300 0.15%

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $300 0.15%

NHCE 5 28 $42,000 $0 $3,150 19.31% $300 0.22%

NHCE 6 38 $39,000 $0 $2,925 8.54% $300 0.28%

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $300 0.54%

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $300 0.75%

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

*Cash balance plan satisfies Code §401(a)(26) = 5/11 (45%) of EEs receive meaningful benefits

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $300 0.10% 6.79%

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $300 0.28% 8.86%

NHCE 3 35 $47,000 $0 $3,525 10.91% $300 0.15% 11.06%

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $300 0.15% 11.06%

NHCE 5 28 $42,000 $0 $3,150 19.31% $300 0.22% 19.53%

NHCE 6 38 $39,000 $0 $2,925 8.54% $300 0.28% 8.82%

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $300 0.54% 21.49%

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $300 0.75% 27.50%

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Plan satisfies nondiscrimination on basis of combined DC EBRs and CB NARs

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

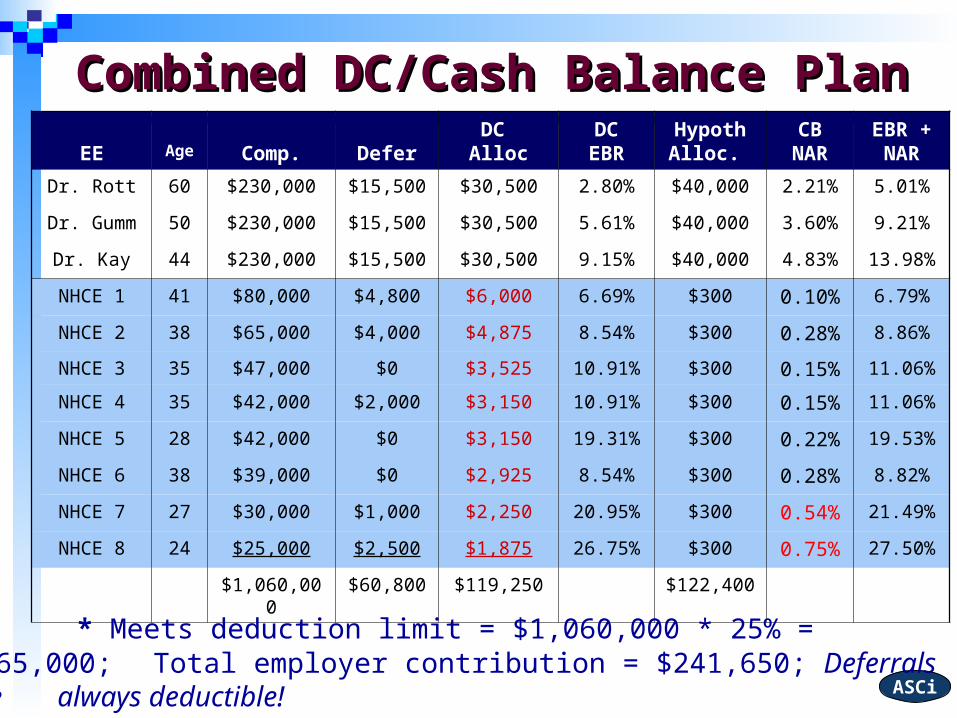

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $300 0.10% 6.79%

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $300 0.28% 8.86%

NHCE 3 35 $47,000 $0 $3,525 10.91% $300 0.15% 11.06%

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $300 0.15% 11.06%

NHCE 5 28 $42,000 $0 $3,150 19.31% $300 0.22% 19.53%

NHCE 6 38 $39,000 $0 $2,925 8.54% $300 0.28% 8.82%

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $300 0.54% 21.49%

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $300 0.75% 27.50%

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Meets deduction limit = $1,060,000 * 25% = $265,000; Total employer contribution = $241,650; Deferrals are always deductible!

ASCi

EE Age Comp. Defer

DC Alloc

DCEBR

HypothAlloc.

CBNAR

EBR +NAR

Dr. Rott 60 $230,000 $15,500 $30,500 2.80% $40,000 2.21% 5.01%

Dr. Gumm 50 $230,000 $15,500 $30,500 5.61% $40,000 3.60% 9.21%

Dr. Kay 44 $230,000 $15,500 $30,500 9.15% $40,000 4.83% 13.98%

NHCE 1 41 $80,000 $4,800 $6,000 6.69% $300 0.10% 6.79%

NHCE 2 38 $65,000 $4,000 $4,875 8.54% $300 0.28% 8.86%

NHCE 3 35 $47,000 $0 $3,525 10.91% $300 0.15% 11.06%

NHCE 4 35 $42,000 $2,000 $3,150 10.91% $300 0.15% 11.06%

NHCE 5 28 $42,000 $0 $3,150 19.31% $300 0.22% 19.53%

NHCE 6 38 $39,000 $0 $2,925 8.54% $300 0.28% 8.82%

NHCE 7 27 $30,000 $1,000 $2,250 20.95% $300 0.54% 21.49%

NHCE 8 24 $25,000 $2,500 $1,875 26.75% $300 0.75% 27.50%

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Beginning in 2007 – deductible amount increases to $328,600; $1,060,000 * 25% = $265,000 + $63,600 (6% of comp)

ASCi

EE Age Comp. Defer

DC Alloc

HypothAlloc.

Dr. Rott 60 $230,000 $15,500 $30,500 $40,000

Dr. Gumm 50 $230,000 $15,500 $30,500 $40,000

Dr. Kay 44 $230,000 $15,500 $30,500 $40,000

NHCE 1 41 $80,000 $4,800 $6,000 $300

NHCE 2 38 $65,000 $4,000 $4,875 $300

NHCE 3 35 $47,000 $0 $3,525 $300

NHCE 4 35 $42,000 $2,000 $3,150 $300

NHCE 5 28 $42,000 $0 $3,150 $300

NHCE 6 38 $39,000 $0 $2,925 $300

NHCE 7 27 $30,000 $1,000 $2,250 $300

NHCE 8 24 $25,000 $2,500 $1,875 $300

$1,060,000 $60,800 $119,250 $122,400

Combined DC/Cash Balance PlanCombined DC/Cash Balance Plan

* Drs. receive 87.52% of ER contribution + deferrals

ASCi

Pension Protection ActPension Protection Act No age discrimination if benefit is equal to

or greater than that of any similarly situated, younger participant

May provide interest credits not greater than a market rate of return

Can provide lump sum distribution equal to hypothetical account balance Eliminates “whipsaw” problem

Must provide 100% vesting after 3 YOS

Understanding the Need for Plan Corrections (VCP)

Charles Lockwood

ASCi

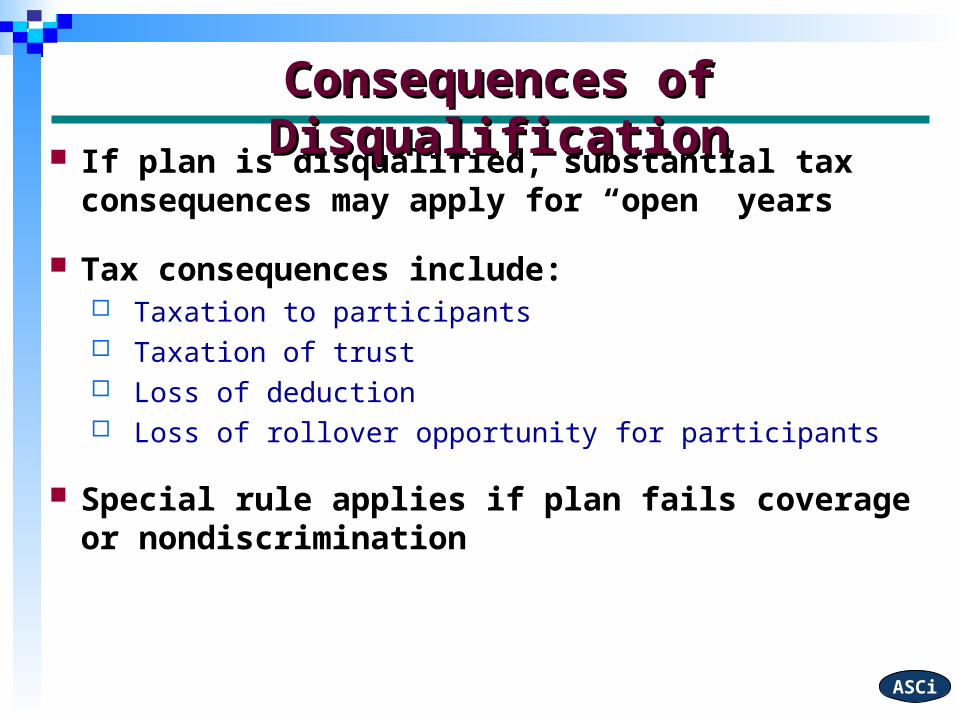

If plan is disqualified, substantial tax

consequences may apply for “open” years

Tax consequences include: Taxation to participants Taxation of trust Loss of deduction Loss of rollover opportunity for participants

Special rule applies if plan fails coverage or nondiscrimination

Consequences of DisqualificationConsequences of Disqualification

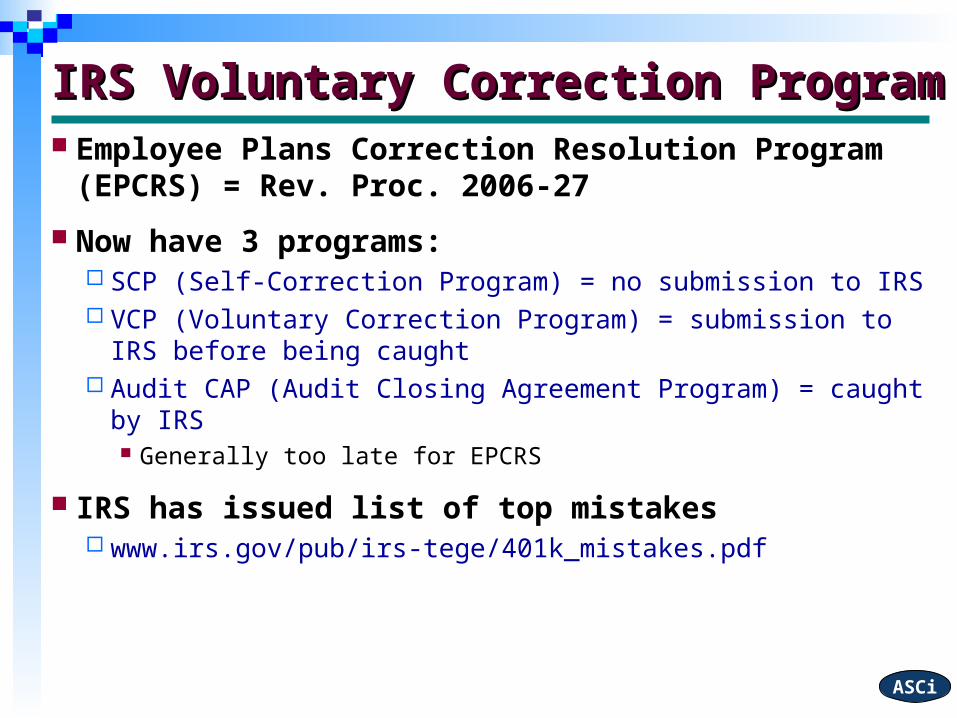

ASCi

Employee Plans Correction Resolution

Program (EPCRS) = Rev. Proc. 2006-27

Now have 3 programs: SCP (Self-Correction Program) = no submission to IRS VCP (Voluntary Correction Program) = submission to

IRS before being caught Audit CAP (Audit Closing Agreement Program) = caught

by IRS Generally too late for EPCRS

IRS has issued list of top mistakes www.irs.gov/pub/irs-tege/401k_mistakes.pdf

IRS Voluntary Correction ProgramIRS Voluntary Correction Program

ASCi

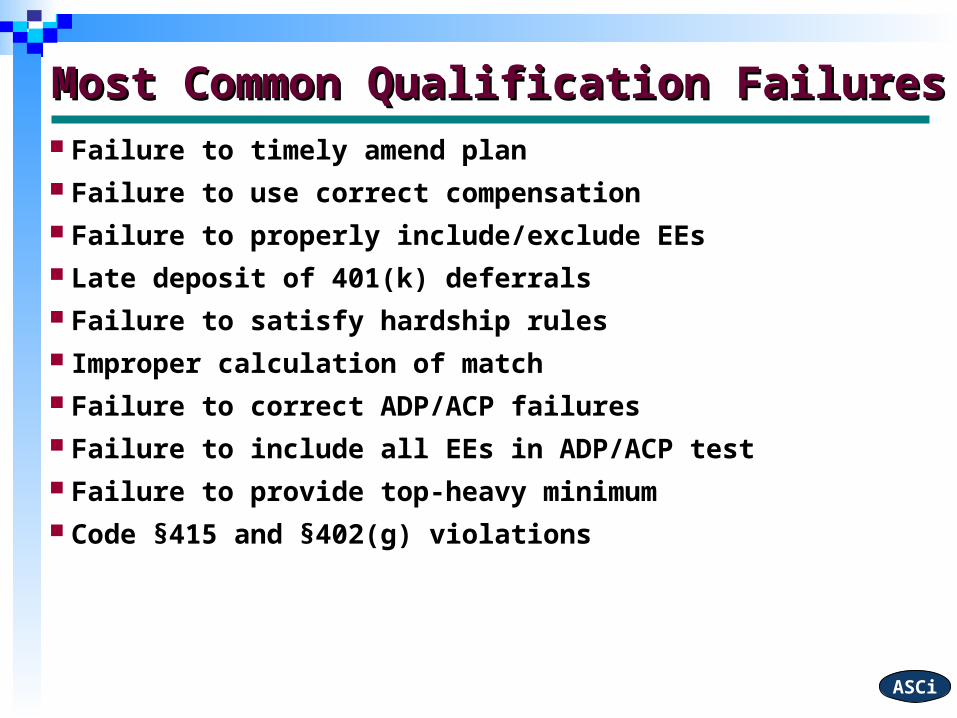

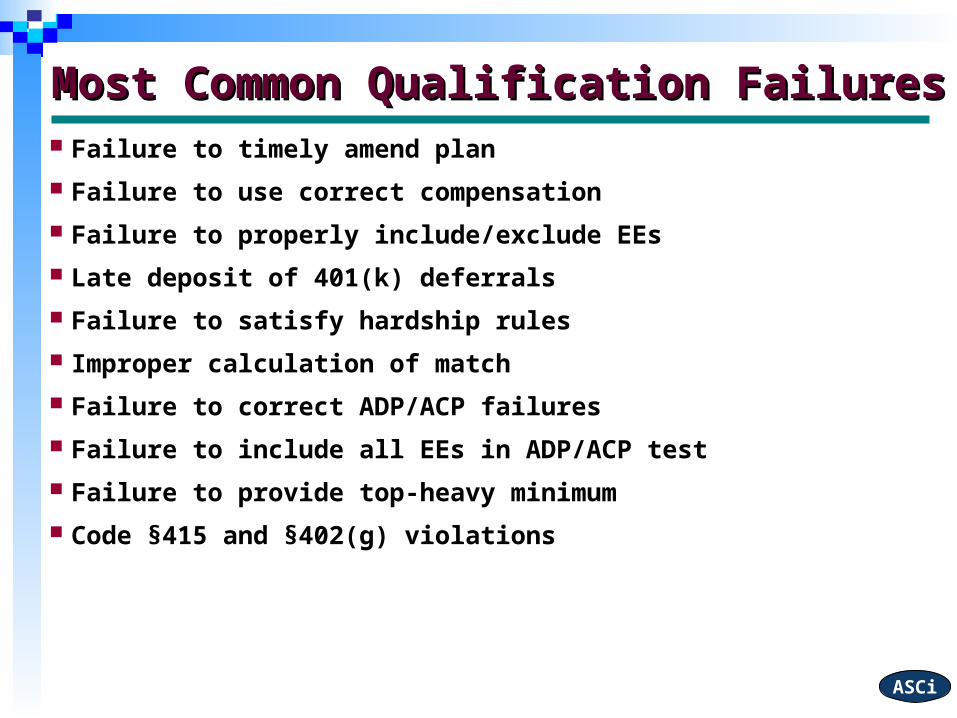

Failure to timely amend plan Failure to use correct compensation Failure to properly include/exclude EEs Late deposit of 401(k) deferrals Failure to satisfy hardship rules Improper calculation of match Failure to correct ADP/ACP failures Failure to include all EEs in ADP/ACP test Failure to provide top-heavy minimum Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

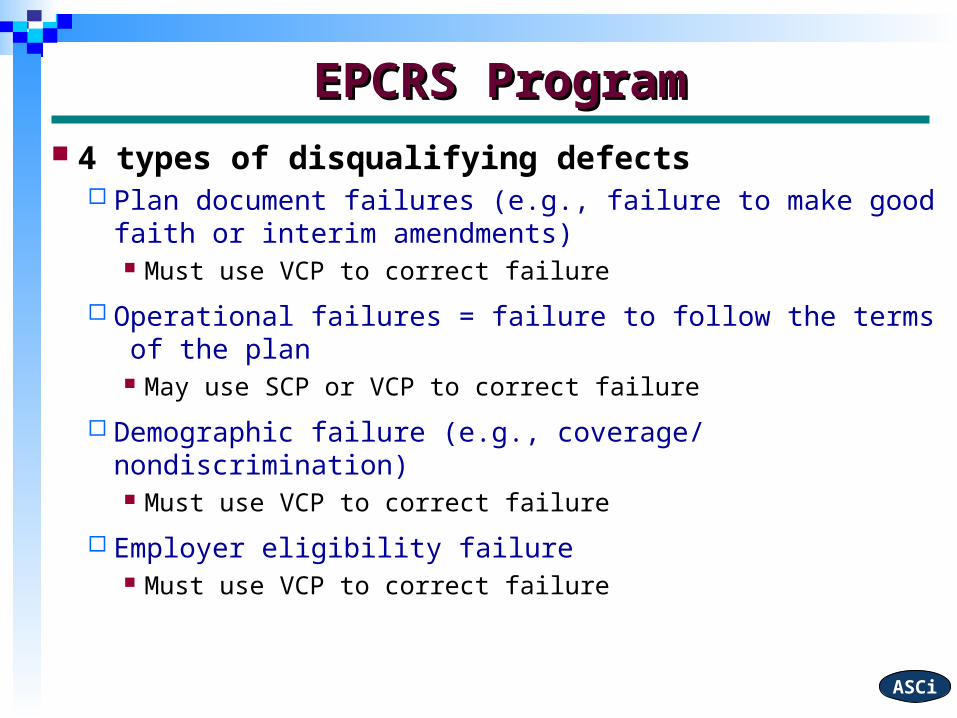

4 types of disqualifying defects Plan document failures (e.g., failure to make good faith

or interim amendments) Must use VCP to correct failure

Operational failures = failure to follow the terms of the plan May use SCP or VCP to correct failure

Demographic failure (e.g., coverage/ nondiscrimination) Must use VCP to correct failure

Employer eligibility failure Must use VCP to correct failure

EPCRS ProgramEPCRS Program

ASCi

Established practices and procedures

Operational problem

General correction principles used

Change administrative procedures

Significant failure – two years Special rule for mergers/acquisitions

Insignificant failure – no limit

Maintain adequate records

No fee

SCPSCP

ASCi

Plan sponsor submits VCP paperwork

Plan sponsor identifies failures

Plan sponsor proposes correction

Plan sponsor pays user fee

IRS issues a compliance statement

Plan sponsor corrects within 150 days of compliance statement

Plan not examined

VCPVCP

ASCi

VCP FeesVCP Fees

Number of participants VCP fee

20 or fewer $750

21-50 $1,000

51-100 $2,500

101-500 $5,000

501-1,000 $8,000

1,001-5,000 $15,000

5,001-10,000 $20,000

Over 10,000 $25,000

ASCi

Plan sponsor is under examination

Plan sponsor enters closing agreement

Plan sponsor makes correction

Plan sponsor pays sanction Negotiated % of maximum payment amount (MPA)

for open years Tax on trust Income tax due to loss of employer deductions Income tax due to inclusion of income for participants

Audit CAPAudit CAP

ASCi

Failure to timely amend plan Failure to use correct compensation Failure to properly include/exclude EEs Late deposit of 401(k) deferrals Failure to satisfy hardship rules Improper calculation of match Failure to correct ADP/ACP failures Failure to include all EEs in ADP/ACP test Failure to provide top-heavy minimum Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

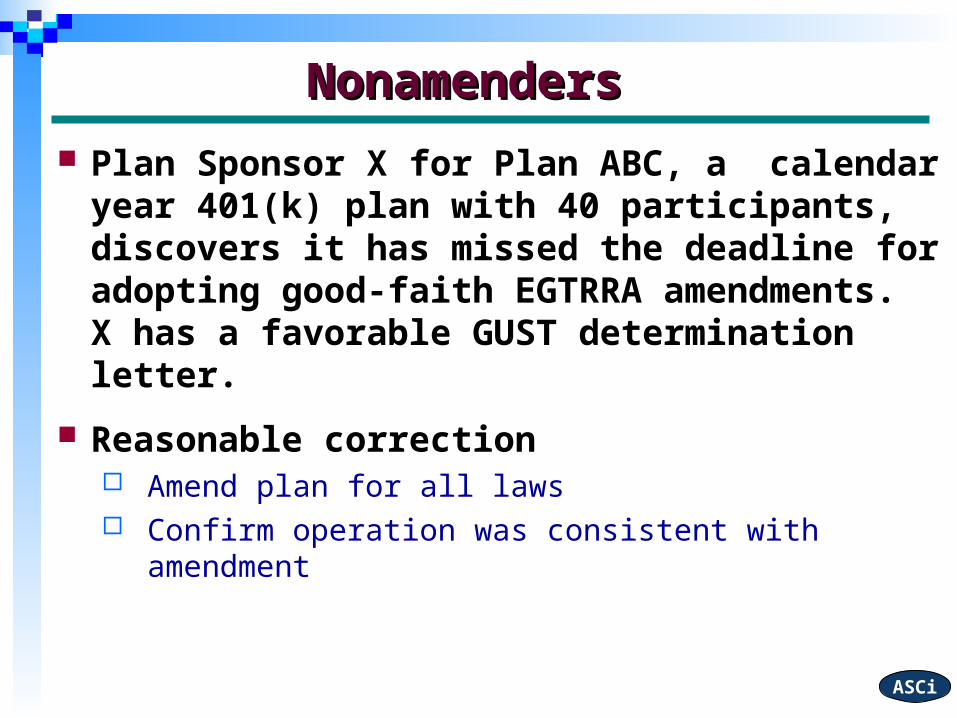

Plan Sponsor X for Plan ABC, a calendar year 401(k) plan with 40 participants, discovers it has missed the deadline for adopting good-faith EGTRRA amendments. X has a favorable GUST determination letter.

Reasonable correction Amend plan for all laws Confirm operation was consistent with

amendment

NonamendersNonamenders

ASCi

SCP – not available

VCP – available Normally $1,000 fee

If “good faith amendments” or interim amendments only, fee is $375

Audit CAP – Amend plan, pay negotiated % of MPA

NonamendersNonamenders

ASCi

Compensation DefinitionsCompensation Definitions

Code §415 = gross

Top-heavy = gross

Highly compensated employees = gross

Deductions = gross

Allocations or benefits = Plan Compensation (as defined in AA §5-2)

Testing compensation = any Code §414(s) definition of compensation

ASCi

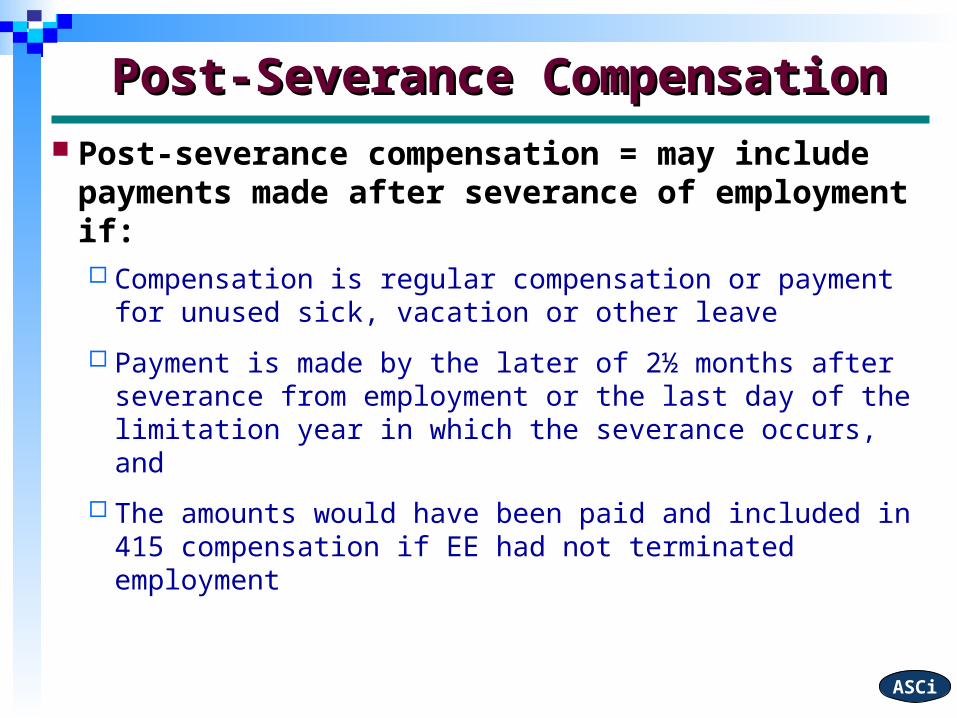

Post-severance compensation = may

include payments made after severance of employment if: Compensation is regular compensation or payment

for unused sick, vacation or other leave

Payment is made by the later of 2½ months after severance from employment or the last day of the limitation year in which the severance occurs, and

The amounts would have been paid and included in 415 compensation if EE had not terminated employment

Post-Severance CompensationPost-Severance Compensation

ASCi

Severance pay is not included as 415

compensation May not defer on severance payments

Plan may exclude post-severance compensation Plan would be subject to 414(s) testing

Raises issues regarding application of ADP/ACP test

Post-Severance Compensation Post-Severance Compensation

ASCi

415 amendment = required (interim) As interim amendment = RAP expires as of due

date for filing tax return for tax year beginning after 7/1/07

Amendment date for calendar year ER = 9/15/09 (if file for corporate extension)

Concern is possible cut-back if apply compensation definition retroactively to 1/1/08 Amend plan before anyone accrues benefit for 2008

Plan AmendmentPlan Amendment

ASCi

Failure to timely amend plan

Failure to use correct compensation

Failure to properly include/exclude EEs

Late deposit of 401(k) deferrals

Failure to satisfy hardship rules

Improper calculation of match

Failure to correct ADP/ACP failures

Failure to include all EEs in ADP/ACP test

Failure to provide top-heavy minimum

Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

401(k) plan with 8 participants

Employee Y (a former participant) was rehired on March 1, 2008

Employee Y was not permitted to make deferrals until January 1, 2009

Employee Y was an NHCE with compensation of $75,000

The NHCE ADP for 2008 was 8% and the HCE ADP was 10%

Exclusion of Eligible EmployeeExclusion of Eligible Employee

ASCi

Reasonable correction Make QNEC to compensate for missed deferral

opportunity QNEC = 50% of employee’s missed deferral Missed deferral = ADP of employee’s group for plan year

of exclusion by employee’s compensation for that year Make up any matching contributions based on actual

amount of missed deferral (not 50%) 8% x $75,000 x 50% x 10/12 = $2,500 plus earnings

What if ER fails to follow EE’s election? Rev. Proc. 2008-50 = 50% of amount elected

Exclusion of Eligible EmployeeExclusion of Eligible Employee

ASCi

Failure to timely amend plan

Failure to use correct compensation

Failure to properly include/exclude EEs

Late deposit of 401(k) deferrals

Failure to satisfy hardship rules

Improper calculation of match

Failure to correct ADP/ACP failures

Failure to include all EEs in ADP/ACP test

Failure to provide top-heavy minimum

Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

Top-10 DOL ViolationsTop-10 DOL Violations Failure to timely deposit deferrals Failure to make required contributions Improper valuation of plan assets Improper distributions Orphaned plans Adverse actions against EEs trying to

enforce plan rights Failure to put assets in plan's name Prohibited transactions Failure to have established procedures Improper allocation of expenses

ASCi

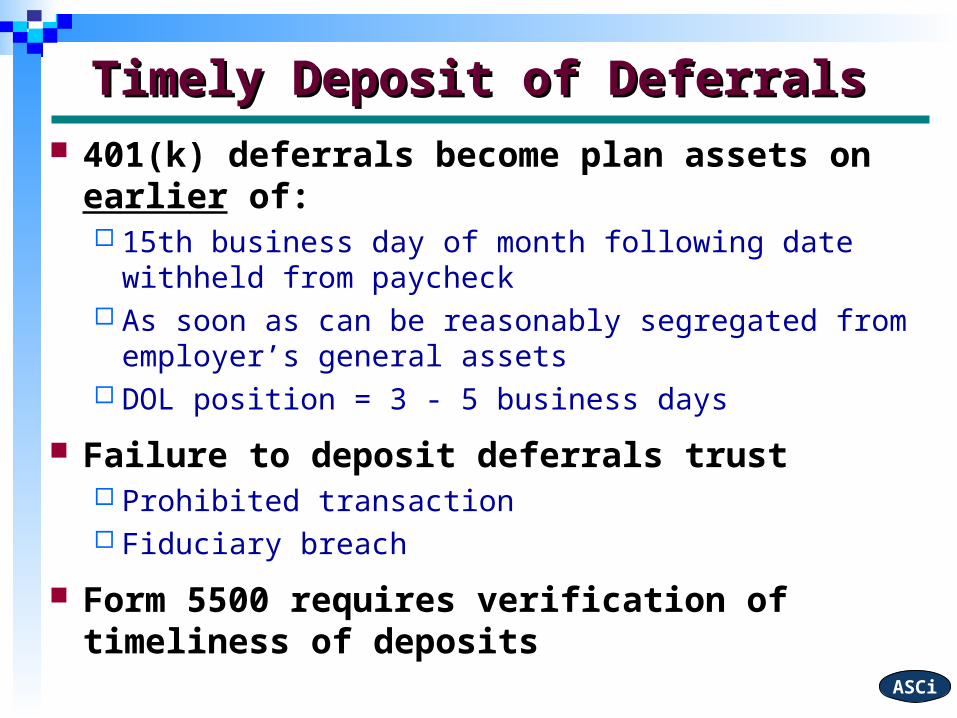

Timely Deposit of DeferralsTimely Deposit of Deferrals 401(k) deferrals become plan assets on

earlier of: 15th business day of month following date withheld

from paycheck As soon as can be reasonably segregated from

employer’s general assets DOL position = 3 - 5 business days

Failure to deposit deferrals trust Prohibited transaction Fiduciary breach

Form 5500 requires verification of timeliness of deposits

ASCi

DOL Proposed RegulationsDOL Proposed Regulations Creates safe harbor for timely deposit of

401(k) deferrals Deemed timely if deposited within 7 business

days following date amounts are withheld from paycheck

Only available if plan has fewer than 100 participants at beginning of plan year

For larger plans – timing of deferrals may be sooner than 7 days = DOL may add SH for larger plans in final regulations

SH rule also applies to deposit of loan repayments

ASCi

DOL Proposed RegulationsDOL Proposed Regulations Compliance with safe harbor rule is not

mandatory = will allow ERs to ensure satisfying plan asset rules

Small ER that remits later than 7-day limit may wish to review its systems and plan remittance procedures

Gives providers another reason to encourage ERs to remit deferrals on a timely basis

Effective when final regs are issued = DOL will apply rule until finalized

ASCi

Plan trustees are responsible for monitoring and collecting delinquent plan contributions and generally may not contract around that duty

FAB applies obligation on trustees to collect delinquent contributions Plan or service contracts should identify responsible

parties

Steps necessary to collect delinquent contributions = facts of each case Value of assets involved, the likelihood of successful

recovery, and expenses

FAB 2008-01

ASCi

Expected that new guidance will begin new round of DOL audits focusing on trustee misconduct Concern that DOL will begin/continue targeting

service providers (including TPAs) to determine whether ERs are making timely contributions

Already starting to see some specific DOL action against trustees

FAB 2008-01

ASCi

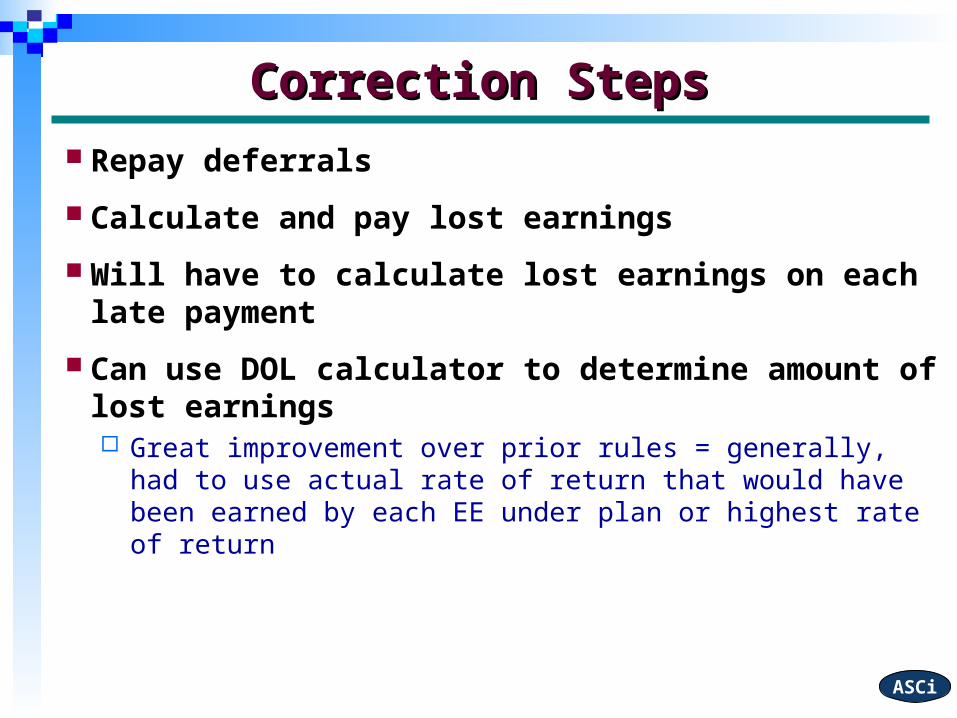

Repay deferrals

Calculate and pay lost earnings

Will have to calculate lost earnings on each late payment

Can use DOL calculator to determine amount of lost earnings Great improvement over prior rules = generally, had

to use actual rate of return that would have been earned by each EE under plan or highest rate of return

Correction StepsCorrection Steps

ASCi

DOL CalculatorDOL CalculatorCorrection Period Interest Rate

4/1/2000 - 3/31/2001 9%

4/1/2001 - 6/30/2001 8%

7/1/2001 - 12/31/2001 7%

1/1/2002 - 12/31/2002 6%

1/1/2003 - 9/30/2003 5%

10/1/2003 - 3/31/2004 4%

4/1/2004 - 6/30/2004 5%

7/1/2004 - 9/30/2004 4%

10/1/2004 - 3/31/2005 5%

4/1/2005 - 9/30/2005 6%

10/1/2005 - 6/30/2006 7%

7/1/2006 - 12/31/2007 8%

1/1/2008 - 3/31/2008 7%

Can use calculator rates = regardless of interest actually earned by plan

Based on IRS underpayment penalty rate under Code §6621

Currently 6%

Interest rate is never negative

dol.gov/ebsa/ calculator/main.html

ASCi

Form 5500 specifically asks if are a late depositor

Must answer under penalties of perjury

Recent court case = imposed $153,000 in penalties and fines and a one-year term of federal probation for false 5500 Hid fact that ER was using funds for own purpose Had repaid the amounts back to the plan “Lied” about existence of prohibited transaction

Second criminal case in last few months for false filing of Form 5500

How Should ER Answer 5500?How Should ER Answer 5500?

ASCi

Failure to timely amend plan

Failure to use correct compensation

Failure to properly include/exclude EEs

Late deposit of 401(k) deferrals

Failure to satisfy hardship rules

Improper calculation of match

Failure to correct ADP/ACP failures

Failure to include all EEs in ADP/ACP test

Failure to provide top-heavy minimum

Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

Plan does not allow for hardship distribution Retroactive amendment to permit hardship Repayment to the plan

Plan must exhaust all available distributions (including loans) prior to taking hardship distribution

Hardship DistributionsHardship Distributions

ASCi

Plan provides for 100% match on deferrals up to

6% of compensation

ER matches each payroll period

Jane earns $50,000 and defers 10% through July 1 when she stops deferring

Jane has deferred $2,500 (10% x $25,000) and received a match of $1,500 (6% x $25,000)

Is Jane entitled to an additional “true-up” contribution?

Improper Matching ContributionImproper Matching Contribution

ASCi

Failure to timely amend plan

Failure to use correct compensation

Failure to properly include/exclude EEs

Late deposit of 401(k) deferrals

Failure to satisfy hardship rules

Improper calculation of match

Failure to correct ADP/ACP failures

Failure to include all EEs in ADP/ACP test

Failure to provide top-heavy minimum

Code §415 and §402(g) violations

Most Common Qualification Failures Most Common Qualification Failures

ASCi

DOL penalties can be as high as $1,100 per day per late form Generally run in the range of $50 to $300 per day = common

to see penalties in 5 – 6 figures

IRS penalties are $25 per day up to $15,000 per late form

Reasonable correction Correction is not available through EPCRS May use DOL’s Delinquent Filer Voluntary Correction Program If Form 5500-EZ, file with IRS and include reasonable cause

statement requesting

Failure to File Form 5500Failure to File Form 5500

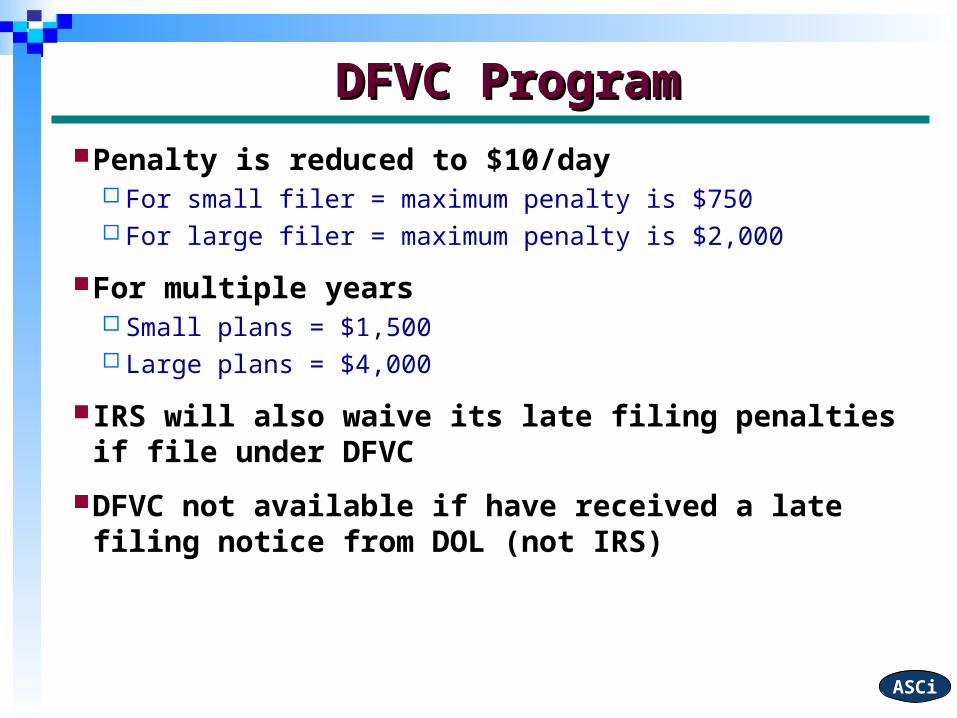

ASCi

Penalty is reduced to $10/day For small filer = maximum penalty is $750 For large filer = maximum penalty is $2,000

For multiple years Small plans = $1,500 Large plans = $4,000

IRS will also waive its late filing penalties if file under DFVC

DFVC not available if have received a late filing notice from DOL (not IRS)

DFVC ProgramDFVC Program

Opportunities in the 403(b) Market

Charles Lockwood

ASCi

IRS issued final regs on July 23, 2007

Very surprising – expected final regs by 7/1 Not effective until 2009 taxable years Not too many changes from proposed regs

403(b) plans are available for: Public schools Tax-exempt ERs under 501(c)(3) and Churches

Must be funded by: Annuity contracts issued by insurance co. Custodial accounts invested in mutual fund Retirement income accounts

403(b) Regulations403(b) Regulations

ASCi

ERs now responsible for administration of

plan document Individual participants no longer the target market ERs will generally be more involved in selection of

investments ER must monitor contribution limits, in-service

withdrawals and loan limits ER must enter into information sharing agreements

with providers = will result in significant consolidation of providers

ERs will be required to file full Form 5500

Changing WorldChanging World

ASCi

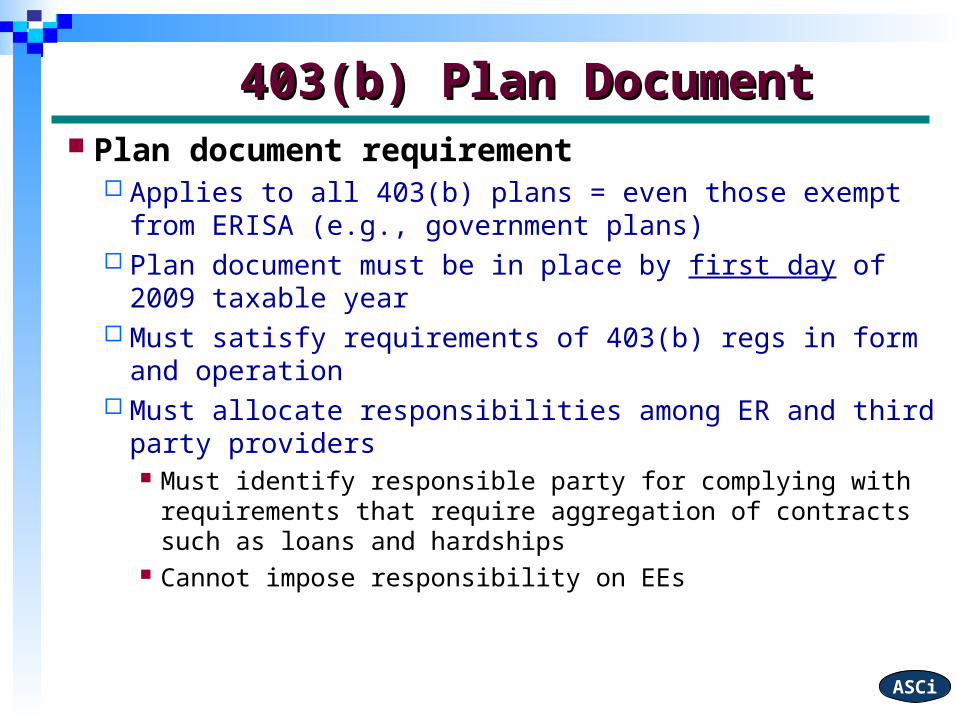

Plan document requirement

Applies to all 403(b) plans = even those exempt from ERISA (e.g., government plans)

Plan document must be in place by first day of 2009 taxable year

Must satisfy requirements of 403(b) regs in form and operation

Must allocate responsibilities among ER and third party providers Must identify responsible party for complying with

requirements that require aggregation of contracts such as loans and hardships

Cannot impose responsibility on EEs

403(b) Plan Document403(b) Plan Document

ASCi

Plan document requirement May incorporate other documents by reference,

such as annuity contract or custodial account Must not be any conflict of interest

IRS will issue model language for public school plans

May lead to IRS determination letter or pre-approved 403(b) program

May have to file full Form 5500

403(b) Plan Document403(b) Plan Document

ASCi

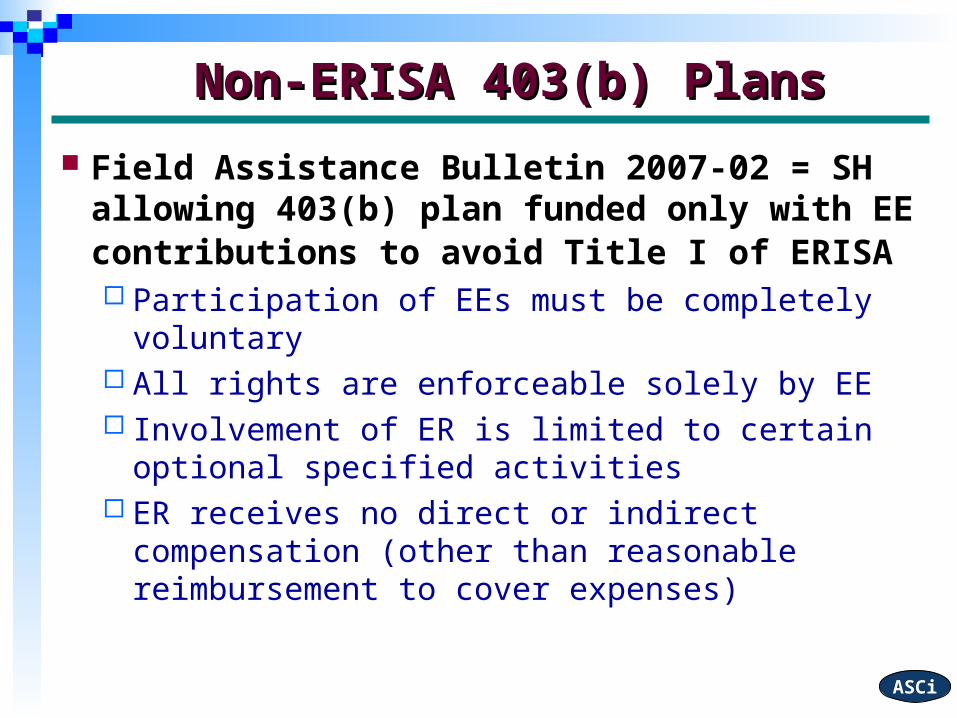

Field Assistance Bulletin 2007-02 = SH allowing 403(b) plan funded only with EE contributions to avoid Title I of ERISA Participation of EEs must be completely voluntary All rights are enforceable solely by EE Involvement of ER is limited to certain optional

specified activities ER receives no direct or indirect compensation

(other than reasonable reimbursement to cover expenses)

Non-ERISA 403(b) PlansNon-ERISA 403(b) Plans

ASCi

Allowable activities include:

requesting information concerning proposed providers and compiling such information to facilitate review and analysis by EEs

entering into salary reduction agreements and collecting/remitting amounts to providers

limiting funding media or products available to EE to a number and selection designed to afford EEs reasonable choice

Other acts may subject ER to ERISA Handling plan transfers, processing distributions, making

hardship or QDRO determinations, or administering loans

Non-ERISA 403(b) PlansNon-ERISA 403(b) Plans

ASCi

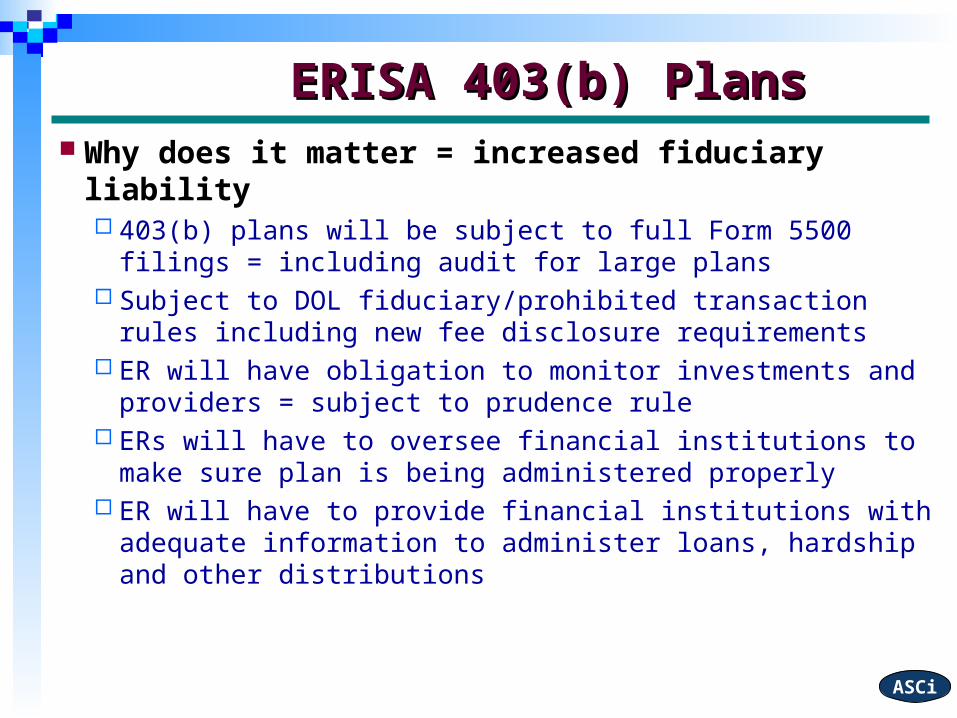

Why does it matter = increased fiduciary

liability 403(b) plans will be subject to full Form 5500 filings =

including audit for large plans Subject to DOL fiduciary/prohibited transaction rules

including new fee disclosure requirements ER will have obligation to monitor investments and

providers = subject to prudence rule ERs will have to oversee financial institutions to make sure

plan is being administered properly ER will have to provide financial institutions with adequate

information to administer loans, hardship and other distributions

ERISA 403(b) PlansERISA 403(b) Plans

ASCi

Restriction on 90-24 transfers Rev. Rul. 90-24 permitted EEs to transfer from one

contract to another contract as long as similar distribution restrictions

Final regulations allow transfers if similar distribution restrictions and ER enters into agreement with provider to share employment information (e.g., term date), hardship and loan information

Effective for exchanges occurring after September 24, 2007 = prior transfers are grandfathered (as long as no later transfer)

403(b) Regulations403(b) Regulations

ASCi

Rev. Proc. 2007-71 = model language Post-2004 orphan contracts (both pre- and post-

9/24/07) will not fail §403(b) if: ER makes reasonable, good faith effort to contact issuer

and notify them of contact information for person in charge of administering the ER’s plan or

Issuer makes reasonable, good faith effort to contact ER before making any distribution or loan to participant

For former EEs, issuer must make reasonable effort before making loan to determine if loan limits are met (e.g., other outstanding loans)

Post 9/24/07 transfers can be re-exchanged prior to July 1, 2009

403(b) Regulations403(b) Regulations

ASCi

Special rules regarding 415 excesses If 415 excess, excess amount treated as

nonqualified = remaining portion retains qualified status

Any 415 excess must be held in separate account for year of excess and following year

Clarifies that 403(b) plans are subject to QDRO rules

Life insurance prohibited

403(b) Regulations403(b) Regulations

ASCi

Tax-exempt ERs subject to same discrimination rules as qualified plans Eliminates “good-faith” standard under Notice 89-23 Church and governmental plans generally exempt

from nondiscrimination rules Are subject to compensation limit under 401(a)(17) and

universal availability

Catch-up contributions permitted under 403(b) plan Only applies after EE makes special $3,000 catch-up

for “qualified EEs” of “qualified organizations”

403(b) Regulations403(b) Regulations

ASCi

Universal availability

Replaces ADP test Eliminates ability to exclude certain EEs permitted

under Notice 89-23 EEs covered by collective bargaining agreement; EEs who make one-time election to participate in

governmental plan instead of 403(b) program; certain visiting professors; and EEs of religious order who have taken a vow of

poverty Can continue to exclude until 2010 TY

403(b) Regulations403(b) Regulations

ASCi

Ability to terminate 403(b) plans and convert to 401(k) plans

Can distribute from terminating 403(b) only if no contributions made to another 403(b) plan during 12-month period following final distribution of plan assets

Terminations can occur between July 27, 2007 and effective date of regulations

Can 403(b) plans terminate if there are orphan accounts for which ER has no information?

403(b) Regulations403(b) Regulations

ASCi

Is switching from 403(b) to 401(k) a good idea?

If plan is a non-ERISA plan = switching would require Form 5500 reporting, SPD/SMMs, additional testing

Universal availability avoids need for ADP test = ER may be able to utilize SH plan design

403(b) plans may permit greater catch-up contributions ER may be able to offer more investments and services

at lower cost in a 401(k) plan EEs will have ability to take a distribution from the plan

upon termination

403(b) Regulations403(b) Regulations

ASCi

In 2007 = estimated that 403(b) plans accounted for $735 billion in assets (roughly 17% of total DC plan market)

403(b) plans will need solutions to: Implement 403(b) plan document prior to 1/1/09 Address fiduciary concerns Ease potential administrative burdens

In a recent survey of 403(b) sponsors = 90% cited assistance with new regulatory compliance as a key need

403(b) Opportunities403(b) Opportunities

ASCi

Plan design and plan administration opportunities 403(b) plans subject to same nondiscrimination rules

as 401(k) plans ERs will need assistance in ensuring 403(b) plan is in

compliance with regulations = no longer can shift responsibility to EEs

Potential fiduciary liability will increase need for employee education

Participants with orphan accounts may need help consolidating their accounts

403(b) Opportunities403(b) Opportunities

ASCi

ERs will need help reviewing prospectuses, fees, investment performance and surrender charges Excessive fees in 403(b) plans recognized as

significant problem

Focus changes from participant-managed investments to employer-managed investments

IRS expected to substantially increase 403(b) audit activity

403(b) Opportunities403(b) Opportunities

Q & ACharles Lockwood