west virginia tax institute wvu college of business & economics 10/2/2006 a.s. fleming, ph.d....

TRANSCRIPT

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 11

West Virginia Tax Institute

WVU College of Business & Economics

Scott Fleming, Ph.D. CPA CMAAssistant Professor of Accounting

College of Business & Economics

West Virginia University

office (304) 293-7896

home (304) 636-7669

cellular (304) 614-3573

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 22

West Virginia Tax Institute

WVU College of Business & Economics

Ethics: Education of Accounting Students

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 33

West Virginia Tax Institute

WVU College of Business & Economics

• Ex-WordCom chief, Bernard Ebbers, starts jail term 9/26/2006

• Fastow gets 6 years for Enron role 9/26/2006

• Panel subpoenas 5 investigators for HP hearing 9/27/2006

• Fugitive ex-Comverse Technology CEO nabbed in Namibia 9/27/2006

• Tyson Foods settles discrimination dispute 9/27/2006

• HealthSouth, investors finalize fraud settlement 9/27/2006

Highlights The Importance of Ethics

Two Days of Business Headlines…

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 44

West Virginia Tax Institute

WVU College of Business & Economics

Multi-Focus Approach To Ethics Education

In Academia Today…

Rules & Regulations

• Codes of Conduct

• SOX

• Circular 230

Post Mortem Analyses

• Enron

• WorldCom

• Global Crossing

ResearchFOCUS OF TODAY’S

DISCUSSION

• Empirical

• Case Studies

• Behavioral

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 55

West Virginia Tax Institute

WVU College of Business & Economics

Teach Consequences

Legal Outcomes and Instinctive Behavioral Actions

We Must Demonstrate And Reiterate “Right” from “Wrong”

then

In The Classroom…

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 66

West Virginia Tax Institute

WVU College of Business & Economics

Significant Change In Students’ Ethical Reasoning Scores

Does This Work?Study by Mohammad J. Abdolmohammadi (2002)*

Accounting Master Students

• Individual ethics

• Professional ethics

• Business ethics

Using pre- and post- Defining Issues Test Scores (DIT)

• Small classes saw greater benefit

• Younger students saw greater benefit

• Males saw greater benefit

Case Study Approach

* Ethical training in graduate accounting courses: Effects of intervention and gender on students’ ethical reasoning, Research on Profession Responsibility and Ethics in Accounting, Vol. 10 p. 37

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 77

West Virginia Tax Institute

WVU College of Business & Economics

Why Focus on the Behavioral Aspect?

• Ethical Dilemmas Are Caused By Actions

• These Actions May Be Instinctive, Cultural, etc.

• People May Not Know They Commit These Actions

Knowing These Behaviors and Susceptibility To These Behaviors May Prevent Dilemmas

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 88

West Virginia Tax Institute

WVU College of Business & Economics

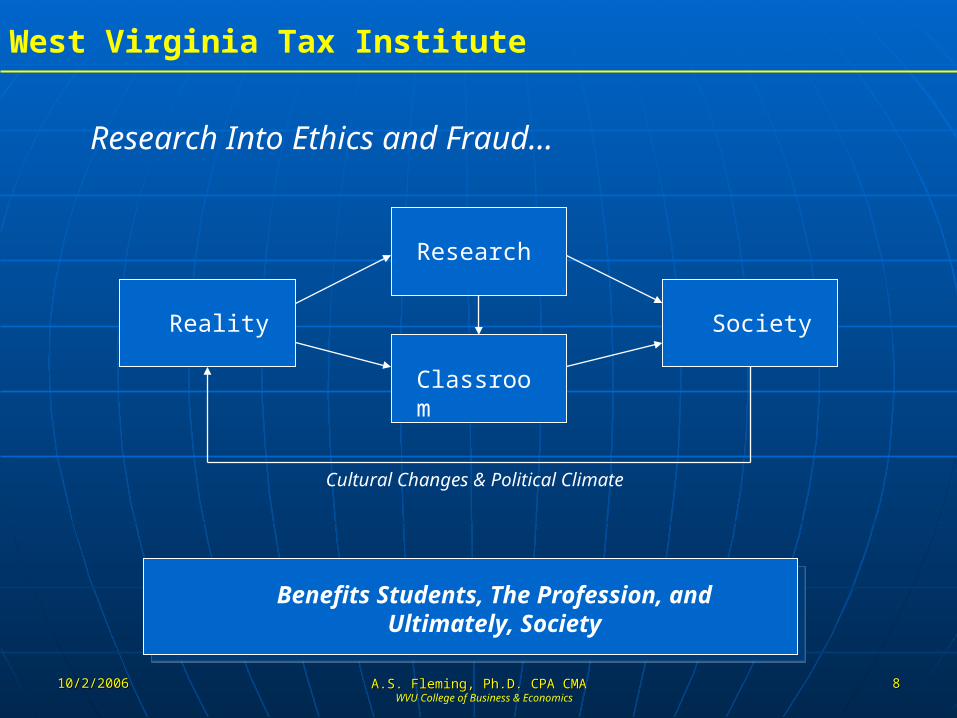

Benefits Students, The Profession, and Ultimately, Society

Research Into Ethics and Fraud…

Reality

Classroom

Research

Society

Cultural Changes & Political Climate

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 99

West Virginia Tax Institute

WVU College of Business & Economics

Divided Fiduciary Responsibilities…

Common Theme: Behaviors in Judgment and Decision Making

Tax Practitioner

The Client

Auditor The Public

Accountant The Firm

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1010

West Virginia Tax Institute

WVU College of Business & Economics

Prospect Theory…

Developed As An Alternative To Expected Utility Theory

Developed By Daniel Kahneman & Amos Tversky, 1979Prospect Theory: An Analysis of Decision under Risk, Econometrica, V. 47-2, 263-292

Example 1: Which Would You Choose?

Option A

80% chance for $4,000

Option B

100% chance for $3,000

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1111

Davis Health System

WVU College of Business & Economics

80 % of the Subjects Chose Option B (76/95), While 20% Chose Option A (19/95)

Why?

Expected Utility Theory

Option A: $4,000 x 0.80 = $3,200

Prospect Theory

Option B: $3,000

Each Theory Points To A Different Solution…

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1212

West Virginia Tax Institute

WVU College of Business & Economics

Now, Add “Framing”…

Tversky & Kahneman (1986) Rational Choice and the Framing of Decision, The Journal of Business, V. 59-4, part 2, S251-S278

Example 2: Option A

Sure gain of $240

Option B

25% chance to gain $1000

And 75% chance to gain $0

EU Value: $240 $250

Results: 84% 16%

Similar Results In A “Gain” Situation

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1313

West Virginia Tax Institute

WVU College of Business & Economics

What About “Framing” In A Loss Situation?

Tversky & Kahneman (1986) Rational Choice and the Framing of Decision, The Journal of Business, V. 59-4, part 2, S251-S278

Example 3: Option A

Sure loss of $750

Option B

75% chance to lose $1000

And 25% chance to lose $0

EU Value: -$750 -$750

Results: 13% 87%

Subjects Are Risk Seeking In Loss Situation

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1414

West Virginia Tax Institute

WVU College of Business & Economics

People Are Risk Seeking in a Loss Situation, And Risk Averse in a Gain Situation

Prospect Theory…

People Underweight Outcomes That Are Probable in Comparison To Outcomes That Are Certain

GainsLosses

Value

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1515

West Virginia Tax Institute

WVU College of Business & Economics

Accounting Research…

Taxpayers’ Prepayment Positions and Tax Return Preparation Fees

Jackson, Shoemaker, Barrick, & Burton (2005), Contemporary Accounting Research, Vol. 22-2 p. 409

Findings: Tax return preparation fees are higher for taxpayers in positive prepayment positions than for taxpayers in negative prepayment positions

Consistent with Prospect Theory:

1) Positive relation to statement above

2) Stronger for taxpayers who receive refunds that are less than fees than it is for taxpayers who receive refunds that are greater than fees

3) Stronger for taxpayers in negative prepayment positions than for taxpayers in positive prepayment positions

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1616

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

A Note on the Relation between Frames, Perceptions, and Taxpayer Behavior

Jackson & Hatfield (2005), Contemporary Accounting Research, Vol. 22-1 p. 145

• Taxpayer frames have a direct effect on taxpayer behavior

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1717

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

Capital Budgeting with Taxes under Uncertainty and Irreversibility

Niemann & Sureth (2005), Jahrbücher für Nationalökonomie und Statistik , Vol. 225-1 p. 77

• Proving neutral tax systems under risk aversion

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1818

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

An empirical investigation into alternative theories explaining taxpayer behavior

Flynn (2003), Drexel University, 173 pages, AAT 3087154

• Initial results do not support house money effect, the breakeven effect, or prospect theory, but shows subjects are inherently conservative

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 1919

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

Tax Evasion and Equity Theory: An Investigative Approach

King & Sheffrin (2002), International Tax & Public Finance, Vol. 9-4, pg. 505

• Control questions are consistent with prospect theory, but general results are consistent with expected utility theory

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2020

West Virginia Tax Institute

WVU College of Business & Economics

Confirmation Bias Can Result in Inaccurate Assessments of Authoritative Support and Lead

To Overly Aggressive Recommendations

Confirmation Bias…

The Influence of Client Preferences on Tax Professionals’ Search for Judicial Precedents, Subsequent Judgments and Recommendations

Cloyd & Spilker (1999), The Accounting Review, Vol. 74-3 p. 299-322

Findings: Subjects’ information searches emphasized cases with conclusions consistent with the client’s desired outcome over cases inconsistent with the clients desired outcome

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2121

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

The Influence of Biased Tax Research Memoranda on Supervisors' Initial Judgments in the Review Process

Barrick, Cloyd, & Spilker (2004), Journal of the American Taxation Association, Vol. 26-1 p. 1

• Supervisors are more persuaded by an unbiased memo for non-appropriate positions

• Supervisors are also more persuaded by a biased memo for appropriate positions

• Supervisors act to correct confirmation bias by requesting more rework of staff who prepare biased memos than of staff who prepare unbiased memos

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2222

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

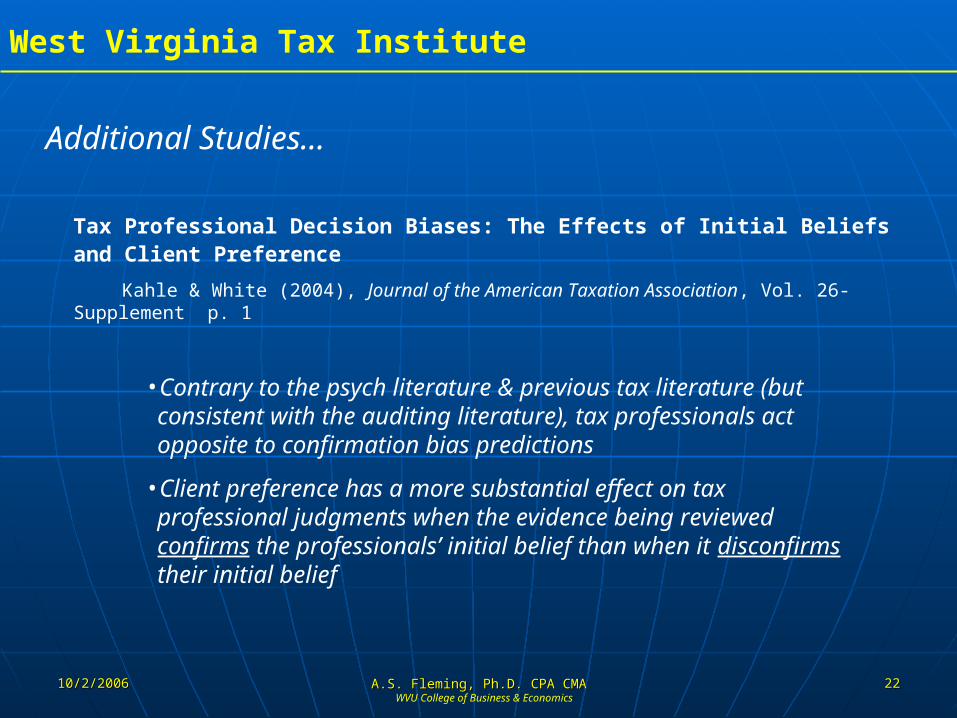

Tax Professional Decision Biases: The Effects of Initial Beliefs and Client Preference

Kahle & White (2004), Journal of the American Taxation Association, Vol. 26-Supplement p. 1

• Contrary to the psych literature & previous tax literature (but consistent with the auditing literature), tax professionals act opposite to confirmation bias predictions

• Client preference has a more substantial effect on tax professional judgments when the evidence being reviewed confirms the professionals’ initial belief than when it disconfirms their initial belief

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2323

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

The effect of staff accountant objectivity in the review and decision process: A tax setting

Hatfield (2001), Journal of the American Taxation Association, Vol. 23-1 p. 61

• Objectivity judgments made by partner / manager level accountants are influenced by whether the staff accountant’s research report confirms their initial opinion

• This affects the manner in which the report is incorporated into a client recommendation

• Preference for client-favorable outcomes is found to affect the weight given to staff accountant research reports

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2424

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

Confirmation bias in tax information search: A comparison of law students and accounting students

Cloyd & Spilker (2000), Journal of the American Taxation Association, Vol. 22-2 p. 60

• Law students and accounting students are victims of confirmation bias (in examining information search behaviors)

• Law students are less prone to the bias in certain situations

• The nature of academic training influences the extent to which researchers are subject to confirmation bias

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2525

West Virginia Tax Institute

WVU College of Business & Economics

Game Theory…

Developed By John von Neumann & Oskar MorgensternTheory of Games and Economic Behavior (1944)

Organized By John Nash (1950)

Prisoner’s Dilemma…

confess don’t

confess 10 10 0 20

don’t 20 0 1 1

Fastow

Skilling

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2626

West Virginia Tax Institute

WVU College of Business & Economics

Solution…

confess don’t

confess 10 10 0 20

don’t 20 0 1 1

Fastow

Skilling

The Nash Equilibrium Solution is Confess / Confess

Suppose you are Andy Fastow. If you know the consequences, then you can reason that Skilling can do one of two things: confess or keep quiet.

1) If Skilling confesses and I don’t, then I will get 20 years. If I confess also, though, I’ll only get 10 years. Confessing is the best option.

2) If Skilling keeps quiet and I also keep quiet, then I will get 1 year. If Skilling keeps quiet and I confess, though, I won’t get any jail time. Again, confessing is the best option.

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2727

West Virginia Tax Institute

WVU College of Business & Economics

Studies…

Audit Misperception, Tax Compliance, and Optimal Uncertainty

Kim (2005), Journal of Public Economic Theory, Vol. 7-3 p. 521

• Research introduces a small amount of uncertainty about the true audit probability

• Find a unique equilibrium cutoff point, such that each taxpayer evades if and only if his perceived signal falls below this cutoff

• When reducing uncertainty has no cost, the optimal uncertainty is indeterminate

• When reducing uncertainty is costly, eliminating all uncertainty can never be optimal

• Introducing a small amount of enforcement cost resolves the indeterminacy problem

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2828

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

Tax Compliance as a Coordination Game

Alm & McKee (2004), Journal of Economic Behavior & Organization, Vol. 54-3 p. 297

• Major tool of tax agencies to reduce evasion is the audit of returns

• IRS uses “discriminant index function” (DIF) to audit those who deviate about the average

• Individuals find it difficult to coordinate on the zero-compliance equilibrium

• Pre-game communication (mimicking info in a tax guide) provides a mechanism to coordinate

• The IRS can make subtle changes to the audit rule

• A DIF rule is often able to achieve high levels of compliance

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 2929

West Virginia Tax Institute

WVU College of Business & Economics

Belief Revision Model…

Developed By Einhorn and Hogarth (1987)

The Influence of Information Presentation Order on Professional Tax Judgment

Pei, Reckers, & Wyndelts (1990), Journal of Economic Psychology, Vol. 11-1 p. 119

• Study on the effects of information presentation order on tax professionals’ belief revisions about ambiguous tax treatments

• Two dimensions studied (1) judgment reasonableness, and (2) recommendation of tax treatment to client

• Both dimensions affected by presentation order

• Neither is affected by the client preference

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 3030

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies…

Tax Professionals Belief Revision: The Effects of Information Presentation Sequence, Client Preference, and Domain Experience

Pei, Reckers, & Wyndelts (1992), Decision Sciences, Jan/Feb Vol. 23-1 p. 175

• Experienced tax professionals’ belief revisions are affected by the presentation order, but unaffected by the client preference

• Inexperienced tax professionals’ belief revisions are affected by the client preference, but unaffected by the presentation order

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 3131

West Virginia Tax Institute

WVU College of Business & Economics

Additional Ethic / Psychological Areas …

Gender Biases

Recency / Primacy Effects

Group Think

Persuasive arguments explanation

Stereotypes

Non-verbal cues

Perseverance bias

Lying / deception cues

Cultural differences (domestic and international)

… And Many More

10/2/200610/2/2006 A.S. Fleming, Ph.D. CPA CMAA.S. Fleming, Ph.D. CPA CMA 3232

West Virginia Tax Institute

WVU College of Business & Economics

Additional Studies of Interest…

Hume, Larkins, Iyer (1999), On compliance with ethical standards in tax preparation, Journal of Business Ethics, Vol. 18-2 p. 229

Larkins, Hume, Garcha (1997), The validity of the randomized response method in tax ethics research, Journal of Applied Business Research, Vol. 13-3 p. 25

Schisler (1995), Equity, aggressiveness, consensus: A comparison of taxpayers and tax preparers, Accounting Horizons, Vol. 904 p. 76

Cloyd (1995), The effects of financial accounting conformity on recommendations of tax preparers, Journal of the American Taxation Association, Vol. 17-2 p. 50

Schisler (1994), An experimental examination of factors affecting tax preparers’ aggressiveness – a prospect theory approach, Journal of the American Taxation Association, Vol. 16-2 p. 124

Cuccia (1994), The effects of increased sanctions on paid tax preparers: Integrating economic and psychological factors, Journal of the American Taxation Association, Vol. 16-1 p. 41

Newberry, Reckers, & Wyndelts (1993), An examination of tax practitioner decisions: The role of preparer sanctions and framing effects associated with client condition, Journal of Economic Psychology, Vol. 14-2 p. 439

Christensen (1992), Evaluation of Tax Services: A client and preparer perspective, Journal of the American Taxation Association, Vol. 14-2 p. 60