what entrepreneurs are up to - babson college entrepreneurs are up to 2008 national entrepreneurial...

TRANSCRIPT

G lo ba l E n t r E p r E n E u r s h i p m o n i to r2008 national Entrepreneurial assessment for the united states of america

What Entrepreneurs Are Up To

Abdul Ali • I. Elaine Allen • Candida Brush • William D. Bygrave • Julio De Castro

Julian Lange • Heidi Neck • Joseph Onochie • Ivory Phinisee • Edward Rogoff • Albert Suhu

Executive Report

1

Globa l En t rep reneursh ip Mon i to r

2008 National Entrepreneurial Assessment for the United States of America

Executive Report

Abdul Ali, I. Elaine Allen, Candida Brush, William D. Bygrave,

Julio De Castro, Julian Lange, Heidi Neck, Joseph Onochie,

Ivory Phinisee, Edward Rogoff, Albert Suhu

What Entrepreneurs Are Up To

2

3

Globa l En t rep reneursh ip Mon i to r

What Entrepreneurs Are Up To

2008 National Entrepreneurial Assessment for the United States of America

Executive Report

The authors thank the Consortium of GEM National Teams who participated

in 2008: Angola, Argentina, Belgium, Bolivia, Bosnia and Herzegovina, Brazil,

Chile, Colombia, Croatia, Denmark, Dominican Republic, Ecuador, Egypt,

Finland, France, Germany, Greece, Hungary, Iceland, India, Iran, Ireland,

Israel, Italy, Jamaica, Japan, Latvia, Macedonia, Mexico, Netherlands, Norway,

Peru, Republic of Korea, Romania, Russia, Serbia, Slovenia, South Africa, Spain,

Turkey, United Kingdom, United States, and Uruguay.

Although GEM data were used in the preparation of this report, their

interpretation and use are the sole responsibility of the authors.

© 2009 by Babson College, Baruch College, Abdul Ali, I. Elaine Allen, Candida

Brush, William D. Bygrave, Julio De Castro, Julian Lange, Heidi Neck,

Joseph Onochie, Ivory Phinisee, Edward Rogoff, Albert Suhu and the Global

Entrepreneurship Research Association (GERA).

4

List of Tables 5

List of Figures 5

Executive Summary and Key Findings of the GEM 2008 U.S. Report 7

Introduction 9About GEM 9GEM Data Collection: The Adult Population Survey 10Defining Entrepreneurship 10GEM Website and Data Availability 11

GEM Terminology 12

Part 1 Why Do People Start Businesses In The United States? The Nature Of Start-Ups 14Why Do People Start Businesses in the United States? 21

Part 2 International Comparison: The United States and other Countries 24Activity 25Attitudes 31Aspirations 34

Part 3 Who Starts A Business? 35Women’s Entrepreneurship 35Immigrant Entrepreneurship 37

Part 4 How Do People Start Businesses? 46Financing 46Innovation 47Social Entrepreneurship 52

Part 5 Public Policy In the United States 55

Appendix 62

GEM Sponsors 63

Contacts 64

About the Authors 65

Table of Contents

55

List of TablesTable 1A Prevalence Rates in Percentage of Entrepreneurial Activity and Business Owner-Managers

Across GEM Countries in 2008, for the 18-99 Age Group, by Phase of Economic Development 26

Table 2 Start-Up Motivation, 2008 35Table 3 Prevalence Rates in Percentage of Entrepreneurial Activity for Immigrant

and Non-Immigrant Ethnic Groups 38Table 4 Social Entrepreneurship by Age 53Table 5 Recession Duration, Depth and Diffusion 59Table 6 U.S. Growth Rates by Industry 59Table 7 Change in U.S. Employment, Business Establishments and Firms* 59Table 8 U. S. Dynamism 61Table 1B Prevalence Rates in Percentage of Entrepreneurial Activity and Business Owner-Managers

Across GEM Countries in 2008, for the 18-64 Age Group, by Phase of Economic Development 62

List of FiguresModel 1 The GEM Conceptual Model 9Model 2 The Entrepreneurial Process and GEM Operational Definitions 10Figure 1 U.S. Entrepreneurial Prevalence 14Figure 2 U.S. Early-Stage Entrepreneurial Trends (18-99 Age Group) 15Figure 3 Expects to Start-Up a Business in Three Years (18-99 Age Group) 15Figure 4 GEM 2008 U.S. Entrepreneurial Prevalence Rates by Age Group 16Figure 5 Age Distribution Per Year, TEA 17Figure 6 Age Distribution Per Year, Established Businesses 17Figure 7 Total Early-Stage Education Levels by Year 18Figure 8 Percentage Distribution of Entrepreneurs by Education Levels (TEA) 18Figure 9 Percentage Distribution of Entrepreneurs by Education (Established Businesses) 19Figure 10 Entrepreneurs by Income Segments (TEA) 20Figure 11 Entrepreneurs by Income Segments (Established Business Owners) 20Figure 12 Respondent Perceives Good Opportunities in the Next Six Months (18-99 Age Group) 21Figure 13 Respondent Has Knowledge to Start a Business (18-99 Age Group) 22Figure 14 Fear of Failure Prevents Start-Up (18-99 Age Group) 22Figure 15 Current Start-Up Jobs 23Figure 16 Expected Jobs from Start-Up in Five Years 23Figure 17 Early-Stage Entrepreneurial Activity (TEA) for 43 Nations in 2008,

by Phase of Economic Development, Showing 95% Confidence Intervals 25Figure 18 Sector Distribution Early-Stage Entrepreneurial Activity (18-64 Age Group) 27Figure 19 Sector Distribution Established Businesses (18-64 Age Group) 28Figure 20 Early-Stage Entrepreneurial Activity for Separate Age Groups, 2008 29Figure 21 Early-Stage Entrepreneurial Activity Rates by Gender, 2008 (18-64 Age Group) 30Figure 22 Early-Stage Entrepreneurial Activity (TEA) Rates for 2001-2008 (18-64 Age Group) 30Figure 23 Necessity-Driven TEA Rates for 2001-2008 (18-64 Age Group) 31

Table of Contents

66

Figure 24 Perceived Opportunities for Starting a Business, 2001–2008 32Figure 25 Fear of Failure Among Those Who Perceive Good Start-Up Opportunities, 2001–2008 32Figure 26 Perceived Skills and Knowledge to Start a New Business, 2001–2008 33Figure 27 Intentions to Start a New Business in the Next Three Years, 2002–2008 33Figure 28 High-Growth Expectation Early-Stage Entrepreneurial Activity by Country 34Figure 29 Perceptions of Good Opportunities, Female vs. Male, 2008 36Figure 30 Fear of Failure Rates, Female vs. Male, 2008 36Figure 31 Personally Knows an Entrepreneur Rates, Female vs. Male, 2008 37Figure 32 Personally Knew Entrepreneur in the Past Two Years 39Figure 33 Perceive Good Opportunities for Start-Ups in Six Months 40Figure 34 Have Knowledge to Start a Business 40Figure 35 Fear of Failure Prevents Start-Up Effort 41Figure 36 Expect to Launch Start-Up in Three Years 41Figure 37 Shut Down Business in the Past 12 Months 42Figure 38 Immigrants Personally Knew Entrepreneur in Past Two Years 42Figure 39 Immigrants Perceive Good Opportunities for Start-Ups in Six Months 43Figure 40 Immigrants Have Knowledge to Start a Business 43Figure 41 Fear of Failure Prevents Start-Up Effort by Immigrants 44Figure 42 Immigrants Expect to Launch Start-Up in Three Years 44Figure 43 Immigrants Shut Down Business in Past 12 Months 45Figure 44 Percentage of Business Entities with New Products: Customer Unfamiliarity 48Figure 45 Percentage of Business Entities with New Products: Competitive Offerings 48Figure 46 Percentage of Business Entities Active in Medium- or High-Technology Sector 50Figure 47 Percentage of Business Entities Using Various Types of Technology in 2008 50Figure 48 Percentage of Business Entities Spending on Technology in 2008 51Figure 49 Percentage of Entrepreneurs Self-Identifying as Social Entrepreneurs 52Figure 50 Social Entrepreneurship and Gender 53Figure 51 Perception of Social Opportunities in Six Months 54Figure 52A U.S. 2008 Entrepreneurial Trends with Real GDP 57Figure 52B Percent Change: U.S. Real GDP and Key Components 58Figure 53 GEM U.S. National Expert Survey – Mean Response for New Firm Entrepreneurship Opportunity 60Figure 54 GEM U.S. National Expert Survey – Mean Response for Available Funding 61

Table of Contents

77

Executive Summary and Key Findings of the GEM 2008 U.S. Report

One of the great advantages of a research program such as GEM is that it systematically examines entrepreneurship issues through annual surveys, allowing for examination of the characteristics of entrepreneurship, actions and qualities of individual entrepreneurs and factors in the environment impacting entrepreneurship in diverse economic conditions. The global economic crisis that started in 2007 presents a different set of economic conditions than in the prior periods of GEM examination. As such, this 2008 report is particularly important, because it begins to tell the story of entrepreneurial behavior in times of economic distress. However, a note of caution is warranted.

This year’s report examines entrepreneurial activity for those in the 18-99 age group. Traditionally, GEM has examined entrepreneurial behavior for those in the 18-64 age group. Given growing evidence of entrepreneurial behavior past the age of 64, and the likelihood that all GEM countries will move to this new convention, the GEM U.S. team decided to make this change immediately in order to have a fuller picture of entrepreneurship in the United States. When appropriate, comparing the United States to other GEM countries, this report uses data from the 18-64 age group. The data on entrepreneurial activity in the United States in 2008 show some positive signs.

For the 18-99 age group, the GEM 2008 U.S. data set shows a slight increase in TEA (Total Entrepreneurial Activity) compared to 2007 (8.7% vs. 8.3%), and while the TEA for men shows a slight decrease (9.8% to 10.7%), the TEA for women shows a marked increase (7.5% to 6.1%). Another interesting point is that the size of the ventures entrepreneurs are thinking about is changing: From 2007 to 2008, the number of jobs entrepreneurs expected to create from their start-ups decreased in all categories (no jobs, 1-5 jobs, 6-19 jobs), except in the category of 20+ jobs. Opportunity continues to be the main driver for entrepreneurs in the United States; 87% started their businesses due to an opportunity, opposed to 13% who started their businesses out of necessity.

One important trend to note is the change in the age distribution of entrepreneurs. For the total entrepreneurship and the established firms measures, the results indicate a marked reduction (around 8% to 9%) in entrepreneurial activity for individuals in the 18-44 age group and an increase of a similar amount in the 45-99 age group. While previous reports pointed toward this trend, this year’s data indicate the need to follow this trend closely because of the possible implications it could have for entrepreneurial behavior in the United States.

The results of this year’s survey indicate that the United States continues to be at or near the top of the group of innovation-driven economies in terms

of early-stage entrepreneurial activities. Looking at particular sectors of entrepreneurial activity, U.S. activity is more concentrated in the business services sector and less concentrated in the transforming sector than the activities of other countries in the innovation-economy group, for both early-stage and established firms. This indicates a continuation of the trend toward a business service-economy and away from a manufacturing-economy.

Also significant this year are the changes with respect to fear of failure. While fear of failure has increased appreciably in the United States and in the rest of the GEM countries, perceived opportunity has declined in the United States and in the other innovation-driven countries. It is important to note, however, that the decrease in perceived opportunity is only off its high levels of 2007. Thus, perceived opportunity is still substantial despite a greater fear of failure. This contrasts with the marked decrease across-the-board in GEM countries for individuals who expect to start a business in the next three years.

When comparing women and men entrepreneurs, two of the most striking differences are the amount of funding available and the type of business started. Women start ventures with eight-times less funding than their male counterparts. Moreover, men and women differ on the businesses they start. Men are more likely to start business-service businesses than consumer-oriented businesses (47% vs. 24%), while women are more likely to start a consumer-oriented rather than a service-oriented business (52% vs. 26%). However, for established businesses, roughly one-third of businesses started by men and women are consumer-oriented and service businesses. Finally, men are substantially more motivated than women by opportunity (93% vs. 68%) as opposed to necessity (5% vs. 21%), and in the realm of established business, women entrepreneurs have reported greater fear of failure and lower perceptions that business success leads to higher status than male entrepreneurs.

The data sets on ethnicity and immigration are consistent with those of previous years. African Americans have higher levels of start-up activities than whites (13.9% vs. 8.4%) while having significantly lower rates of established ventures (8.1% vs. 1.8%), whereas the activities of non-Mexican Hispanics are near those of whites for start-ups (8.6% vs. 8.4%), but for established firms are lower (5.5% vs. 8.1%). With few exceptions, this pattern continues when breaking the data down by immigration status.

In terms of financing, the number of adults reporting that they had invested in someone else’s business increased (to 5%), as did the amount they financed ($17,500); yet those numbers are countered by the precipitous decline in SBA lending. In terms of technology, the 2008 survey data indicate that while

88

early-stage entrepreneurs continue to be cautious when it comes to developing technology products, the number of entrepreneurs involved in the technology sector—either by starting an internet business and/or using web marketing or being willing to spend more than $1,000 on new technology—all increased in 2008.

With respect to social entrepreneurship, largely driven by women entrepreneurs, the survey data indicate a market change away from mostly economic goals (2007) toward a combination of economic and social goals (2008). The most popular sectors for social entrepreneurs are healthcare, education, urban development and the environment.

The trends highlighted earlier with respect to age distribution and entrepreneurial behaviors are prevalent in social entrepreneurship activities, with an increase in later-in-life social entrepreneurs. Finally, in the opinion of the national experts, there is a decline in both the perception of good opportunities and in the availability of funding for entrepreneurs.

99

Introduction

AboUt GEM

Although it is widely acknowledged that entrepreneurship is one of the most important forces shaping the changes in the economic landscape, the understanding of the relationship between entrepreneurship and national growth is far from complete. There is a lack of cross-national harmonized data sets on entrepreneurship. Since 1997, the Global Entrepreneurship Monitor (GEM) research program has contributed to increasing knowledge in this area by collecting relevant harmonized data on an annual basis. GEM focuses on three main objectives:

• To measure differences in the level of entrepreneurial activity between countries

• To uncover factors determining national levels of entrepreneurial activity

• To identify policies that may enhance national levels of entrepreneurial activity

Traditional analyses of economic growth and competitiveness have tended to neglect the role played by new and small firms in the economy. GEM takes

a comprehensive approach and considers the degree of involvement in entrepreneurial activity within a country. GEM views national economic growth and the aggregate level of economic activity in a country as being associated with newer and smaller firms as well as established firms, but its focus lies on early-stage entrepreneurial activity. Small and newer firms generate innovations, fill market niches, and increase competition, thereby contributing to resource reallocation in economic activity. By considering the complementary nature of economic activity among different groups of firms, GEM links a nation’s economic activity to the interplay of established and new and smaller firms, allowing a clearer understanding of why entrepreneurship is vital to the whole economy. Figure 1 presents the conceptual framework that guides GEM data collection. The GEM model maintains that established business activity at the national level varies with General National Framework Conditions (GNFC), while entrepreneurial activity varies with Entrepreneurial Framework Conditions (EFC). GEM’s unique contribution is its cross-national data sets that enable detailed study of the lower half of the conceptual framework. In the framework, EFCs reflect major features of an economy and host society that are expected to impact the entrepreneurial sector but are not captured in the General National Framework Conditions.i

Model 1. The GEM Conceptual Model

Social, Cultural,Political Context

General National Framework Conditions

Entrepreneurial Framework Conditions

Micro, Small and Medium Firms(Secondary Economy)

Entrepreneurial Opportunities

EntrepreneurialCapacity

•Skills

NewEstablishments

Early-stageEntrepreneurial Activity

MajorEstablished Firms(Primary Economy)

National Economic Growth(Jobs andTechnicalInnovation)

10

Model 2. The Entrepreneurial Process and GEM Operational Definitions

Introduction

GEM DAtA CollECtioN: thE ADUlt PoPUlAtioN SUrvEy

GEM takes a broad view of entrepreneurship and focuses on the role played by individuals in the entrepreneurial process. A key GEM indicator is the prevalence rate of early-stage entrepreneurial activity (also known as the TEA index), represented by the shaded box in Model 2.

DEfiNiNG ENtrEPrENEUrShiP

Entrepreneurship is a complex phenomenon that spans a variety of contexts. The varied definitions in entrepreneurship literature reflect this complexity. In line with its objectives, GEM takes a broad view of entrepreneurship and focuses on the role played by individuals in the entrepreneurial process. Unlike most entrepreneurship data sets that measure newer and smaller firms, GEM data studies the behavior of individuals with respect to starting and managing a business. This differentiates GEM data from other data sets, most of which record firm-level data on (new) firm registrations (see Model 2). New firms are most often started by individuals, and individuals typically determine the entrepreneurial attitude of established businesses, regardless of size. From the start of the project in 1999, GEM has viewed entrepreneurship as a process and has considered people in entrepreneurial activity in different phases, from the very early phase when businesses are in gestation to the established phase and possibly discontinuation of the business.

An individual entrepreneur who has succeeded in maintaining a business has gone through a process, and the characteristics of his or her actions are a very useful way to study entrepreneurial behavior. The entrepreneurial process starts before the firm is operational. Someone who is just starting a venture and trying to make it in a very competitive market is an entrepreneur despite not having high-growth aspirations. On the other hand, an established business owner may have been in business for

quite a number of years and still be innovative, competitive and growth-minded; this person is also an entrepreneur. GEM provides an umbrella under which a wide variety of entrepreneurial characteristics—such as motivations, innovativeness, competitiveness and high-growth aspirations—can be systematically and rigorously studied.

Within this context, the GEM data collection covers the life cycle of the entrepreneurial process and looks at individuals at the point when they commit resources to start a business they expect to own themselves (nascent entrepreneurs); when they currently own and manage a new business that has paid salaries for more than three months but not more than 42 months (new business owners); and when they own and manage an established business that has been in operation for more than 42 months (established business owners). Model 2 summarizes the entrepreneurial process and GEM operational definitions.

For GEM, the payment of any wages for more than three months to anyone, including the owners, is considered to be the “birth event” of actual businesses. Thus, the distinction between nascent entrepreneurs and new business owners depends on the age of the business. Businesses that have paid salaries and wages for more than three months and less than 42 months may be considered new. The cutoff point of 42 months has been made on a combination of theoretical and operational grounds.ii The prevalence rate of nascent entrepreneurs and new business owners taken together may be viewed as an indicator of early-stage entrepreneurial activity in a country. It represents dynamic new firm activity; even if a

Potentialentrepreneur:opportunities,knowledge, and skills

Nascententrepreneur:involved in settingup a business

Owner-managerof a new business(up to3.5 years old)

Owner-managerof an establishedbusiness (morethan 3.5 years old)

Conception Firm birth Persistence

Early-Stage Entrepreneurial Activity (TEA)

Introduction

11

Introduction

fair share of nascent entrepreneurs do not succeed in getting the business started, their actions may have an effect on the economy since they can put pressure on incumbent firms to perform better.

Business owners who have paid salaries and wages for more than 42 months are classified as “established business owners.” Their businesses have survived the liability of newness. High rates of established business ownership may indeed indicate positive conditions for firm survival. However, this is not necessarily the case. If a country exhibits a high degree of established entrepreneurship combined with a low degree of early-stage entrepreneurial activity, this indicates a low level of dynamism in entrepreneurial activity.

GEM WEbSitE AND DAtA AvAilAbility

GEM is a consortium of national teams participating in the Global Entrepreneurship Research Association. Thanks to the effort and dedication of hundreds of entrepreneurship scholars as well as policy advisors around the globe, the GEM consortium consists of a unique network building a unique data set. Contact details and national teams’ micro-sites can be found on www.gemconsortium.org, which also contains a selection of GEM data. The GEM website provides an updated list of the growing number of peer-reviewed scientific articles based on GEM data.

Introduction

12

GEM Terminology

Nascent entrepreneur A nascent entrepreneur is one who is actively planning a new venture. Such an entrepreneur has done something during the previous 12 months to help start a new business that he or she will own, at least in part. Activities such as organizing the start-up team, looking for equipment, saving money for the start-up, or writing a business plan would all be considered active commitments to starting a business. Wages or salaries will have been paid for no more than three months; nascent entrepreneurs are often still employed full-time elsewhere.

New firm entrepreneur A new firm entrepreneur is an entrepreneur who, at least in part, owns and manages a new business that is between four and 42 months old and has not paid salaries for longer than this period.

Established business owner In addition to those individuals who are currently involved in the early stages of a business, there are also many individuals who have set up businesses that they have continued to own and manage for a longer time. These individuals are included in the established business owner index, which captures the percentage of individuals in a population who have set up businesses that they continue to own and manage and who have paid wages or salaries for more than 42 months.

New business ownership rate Percentage of the 18-99 age group who are currently owner-managers of new businesses, i.e., owning and managing a running business that has paid salaries, wages or any other payments to the owners for more than three months but not more than 42 months.

Dynamism As used in this report, dynamism is defined as the ratio of early-stage entrepreneurship to established business ownership. This ratio shows the relative activity levels among early-stage entrepreneurs compared to the prevalence of established business owners. Low levels of dynamism indicate a less entrepreneurial environment.

Total early-stage entrepreneurial activity (TEA Rate)

As its name implies, total early-stage entrepreneurial activity refers to the total rate of early-stage entrepreneurial activity among the adult population aged 18–64 years, inclusive. In some instances, this rate is less than the combined percentages for nascent and new firm entrepreneurs. This is because, in circumstances where a respondent qualifies as both a nascent and a new firm entrepreneur, he or she is counted only once.

Overall entrepreneurial activity rate Percentage of the 18-99 age group who are currently engaged in early-stage entrepreneurial activity or owner-manager of an established business (as defined above).

Business discontinuation rate Percentage of the 18-99 age group who have, in the past 12 months, discontinued a business, either by selling, shutting down or otherwise discontinuing an owner-management relationship with the business. Note: This is not a measure of business failure rates.

Fear of failure rate Percentage of the 18-99 age group with positive perceived opportunities (individuals involved in any stage of entrepreneurial activity excluded) who indicate that fear of failure would prevent them from setting up a business.

Entrepreneurial intention Percentage of the 18-99 age group (individuals involved in any stage of entrepreneurial activity excluded) who intend to start a business within three years.

Perceived capabilities Percentage of the 18-99 age group (individuals involved in any stage of entrepreneurial activity excluded) who believe they have the required skills and knowledge to start a business.

13

GEM National Expert Survey* (NES): National Framework Conditions

1. Financial Support (availability of financial resources, equity and debt for new and growing firms including grants and subsidies)

2. Government Policies (the extent to which government policies concerning taxes, regulations and their applications are size neutral and/or whether these polices discourage or encourage new and growing firms)

3. Government Programs (the presence of direct programs to assist new and growing firms at all levels of government: national, regional and municipal)

4. Education and Training (the extent to which training in starting or managing small, new or growing business features in the educational and training system and the quality, relevance and depth of such education and training in creating or managing small, new or growing businesses)

5. Research and Development Transfer (the extent to which national research and development leads to new commercial opportunities and whether or not R&D is available for new, small and growing firms)

6. Commercial and Professional Infrastructure (the influence of commercial, accounting and other legal services and institutions that allow or promote new, small or growing businesses)

7. Market Openness/Barriers to Entry (the extent to which commercial arrangements are prevented from undergoing constant change and re-deployment, preventing new, smaller and growing firms from competing and replacing existing suppliers, subcontractors and consultants)

8. Access to Physical Infrastructure (access to physical resources—communication, utilities, transportation, land or space—at a price that does not discriminate against new, small or growing firms)

9. Cultural and Social Norms (the extent to which existing social and cultural norms encourage, or do not discourage, individual actions that may lead to new ways of conducting business or economic activities and, in turn, lead to greater dispersion in wealth and income)

GEM Terminology

*over the few years, there have been various terms used interchangeably to define the GEM national “interviewees.” terms include: key informant (K), expert informants, expertrespondents and national experts. Despite these variations in terminology, the role and methods have remained unchanged. Going forward, National Expert Survey (NES) is the term of choice. for more information on the National Expert Survey, visit: http://www.gemconsortium.org/about.aspx?page=re_expert_surveys

14

Entrepreneurial Activity

The estimated prevalence rates from the GEM 2008 Adult Population Survey (APS) are shown in Figure 1. The figure makes distinctions among the population by gender, stage of entrepreneurial activity and

reason for starting the venture in order to provide a broad and detailed profile. The group with the highest rate of entrepreneurial activity in the United Sates is males involved in early-stage businesses followed closely by males involved in established businesses.

Part 1 Why Do People Start Businesses in the United States? The Nature of Start-Ups

0%

2%

4%

6%

8%

10%

12%

14%

Nascent New Business TotalEntrepre-

neurialActivity

TotalEntrepre-

neurialActivity

MALE

TotalEntrepre-

neurialActivity

FEM

EstablishedBusinesses

(EST)

EstablishedBusinesses MALE

EstablishedBusinesses

FEMALE

TotalEntrepre-

neurialActivity

Opportunity

TotalEntrepre-

neurialActivity

Necessity

Stage and Type of Prevalence Rates

Figure 1. U.S. Entrepreneurial Prevalence

Source: GEM U.S. 2008 Adult Population Survey (APS)

1Changes in the GEM questionnaire and in the U.S. survey methodology have improved the estimation procedure particularly for the established businesses in 2008. these changes reveal that previous years’ established business prevalence rates may have contained a downward bias. this downward bias was corrected in the 2008 survey methodology.

The data on entrepreneurial behavior in the United States show a number of positive signs. The established business ownership rate (combined male and female) is 7.7%. The established businesses are those businesses that are older than 42 months. These data sets provide some support for the staying power of new businesses. Businesses that make it to 42 months are most likely to sustain long-term viability. Moreover, while the TEA for males shows a decline (10.7% to 9.8%), the TEA for women shows a marked increase (6.1% to 7.5%), which although not strong enough to overcome the decline in males, indicates the gap between genders may be closing, and the increase in women starting businesses could be a way for the United States to overcome decline. The section on women entrepreneurs addresses this topic in more depth.

The United States continues with the trend of businesses being started by entrepreneurs that recognize an opportunity rather than businesses being started out of necessity (87% vs. 13%). Given the 2008/09 financial crises and its possible impact on likely entrepreneurs, it will be important to analyze these variables in next year’s report to assess any possible changes to the trend.

Figure 2 presents historical prevalence rates of early-stage entrepreneurial activity using the same groupings as used in the previous figure (gender, stage of entrepreneurial activity and reason for starting the venture).1 The total early-stage entrepreneurial activity among the adults in the 18-99 age group was estimated to have increased in the United States to 8.7% in 2008 from 8.3% in 2007. Figure 2 illustrates that three groups of activity peaked in 2005 and began their declines in the following year: Total early-stage activity, male early-stage activity and early-stage opportunity entrepreneurial activity.

Figure 3 shows the three year projections for starting businesses by both entrepreneurs and non-entrepreneurs in the United States for each year for the period 2002 to 2008. The decline in the expectations to start-up a business in 3 years is significant and Figure 3 illustrates that it dips from around 65% in 2005 to a little over 50% in 2008. This is important because fewer people are expecting to start new ventures in the future. Figure 3 illustrates that the long term outlook was also significantly less optimistic overall for all three groups – Early-stage entrepreneurs, Established business owner entrepreneurs and non-entrepreneurs – in 2008 compared to all prior years going back to 2002. Surely the economic recession played a major role in these less optimistic expectations in 2008.

15

Figure 2. U.S. Early-Stage Entrepreneurial Trends (18-99 Age Group)

Figure 3. Expects to Start-Up a Business in Three Years (18-99 Age Group)

Why do People Start Businesses in the United States? The Nature of Start-Ups

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2001 2002 2003 2004 2005 2006 2007 2008

Years

Perc

enta

ge E

ntre

pren

euria

l Act

ivity

Total Early-Stage Entrepreneurial Activity Male Entrepreneurial Activity

Female Entrepreneurial Activity Opportunity Entrepreneurial ActivityNecessity Entrepreneurial Activity Disconnect Activity

0%

10%

20%

30%

40%

50%

60%

70%

80%

2002 2003 2004 2005 2006 2007 2008

Perc

enta

ge W

ithin

Eac

h Ca

tego

ry

Early-StageEstablishedNo Business

Source: GEM U.S. 2002-2008 Adult Population Survey (APS)

Source: GEM U.S. 2002-2008 Adult Population Survey (APS)

Given the importance of new ventures and start-ups for the U.S. economy, this is a serious concern and one that has to be paid attention to in the future. It will be important to watch whether the total early-stage and established business entrepreneurs continue to follow the declining trends that started in 2007 for early-stage entrepreneurs and continued in 2008 for all entrpreneurs.

Figure 2 also shows that the early-stage business discontinuation rate began to increase in 2007 at the start of the U.S. recession. The GEM data for 2008 were collected in the first half of the year, making it likely that the prevalence rates have changed significantly during the last half of 2008 and for 2009. We may want to see how the early-stage discontinuation rate changes in 2009 compared to 2008.

16

Figure 4. GEM 2008 U.S. Entrepreneurial Prevalence Rates by Age Group

Why do People Start Businesses in the United States? The Nature of Start-Ups

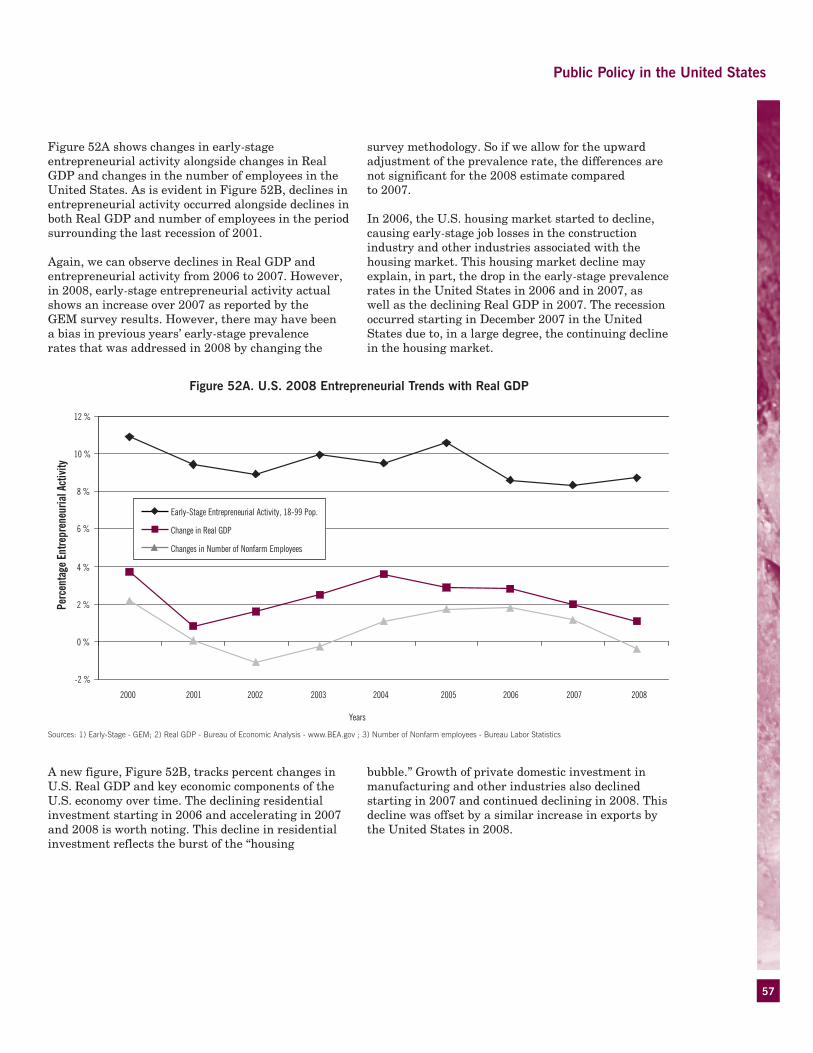

The estimated rate for dynamism for the U.S. 18-99 age group in 2008 using GEM data is 1.3. The ratio of total early-stage activity (TEA) to the total established business prevalence rate measures dynamism in an economy. Table 8 in the Public Policy section at the end of this report provides historical data on the dynamism rate for the United States from 2001 through 2008.

Entrepreneurial Activity and Age Distribution

The results for age distribution for early-stage and established business owners in the United States in 2008 indicate that younger adults in the 18-44 age range have higher prevalence rates in early-stage activity, while older adults in the 45-99 age

range have higher prevalence rates in established business activity (Figure 4). Furthermore, an in-depth examination of age distribution by comparing the 2007 data and determining the percentages per age group for both TEA (Figure 5) and for established businesses (Figure 6) yields some interesting results. With respect to the TEA, the data indicate marked decreases in the activity rate for the 18-24 age group (10.5% vs. 14%) and the 35-44 age group (20.2% vs. 25.1%), but increases in the older age groups (45-54 years, 27.7% vs. 21.8%; 55-64 years, 10.5% vs. 9.5%; 65-99 years, 4.3% vs. 3.4%). This indicates a shifting pattern of entrepreneurial activity. The share distribution of the TEA for the 18-44 age range decreased by 8% while the share distribution of the TEA for the 45-99 age range increased by 7.8% for 2008 compared to 2007.

0%

2%

4%

6%

8%

10%

12%

14%

16%

Early-Stage Established Business

Perc

enta

ge o

f Adu

lt Po

pula

tion

in A

ge G

roup

18-24 YRS25-34 YRS35-44 YRS45-54 YRS55-64 YRS65-99 YRS

Source: GEM U.S. 2008 Adult Population Survey (APS)

As illustrated in Figure 6, this pattern is similar for established firms, decreasing for the 18-24 age group (1.9% vs. 3.4%) and the 35-44 age group (14.6% vs. 23.9%), while it has increased for the older age groups (45-54 years, 37.5% vs. 30.7%; 65-99 years, 11.1% vs. 8.0%). The share distribution of the established business owner decreased a total 9.6% for the 18-44 age group while it increased 9.6% for the 45-99 age group in 2008 compared to 2007.

The results of the comparison between 2008 and 2007 indicate a significant shift in early-stage and established business owners’ share of entrepreneurial activity by age with increases for older age groups and decreases for younger age groups of around 8% for the TEA and 9.5% for the established businesses. This is clearly an area to examine in the future (to determine if this is a temporary or more permanent change) as well as the possible relationship between this shift and the economic situation of 2008. The strength of the current information in Figures 5 and 6 is, however, strong enough to provide significant food for thought.

17

Why do People Start Businesses in the United States? The Nature of Start-Ups

Figure 5. Age Distribution Per Year, TEA

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008

18-24 YRS25-34 YRS35-44 YRS45-54 YRS55-64 YRS65-99 YRS

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Figure 6. Age Distribution Per Year, Established Businesses

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008

18-24 YRS25-34 YRS35-44 YRS45-54 YRS55-64 YRS65-99 YRS

Entrepreneurial Activity and Education

Historical GEM data and information from a significant number of other sources indicate that education is an important determinant of the supply of entrepreneurs in societies. Figure 7 measures the distribution of general education levels for early-stage entrepreneurs. The results in Figures 7-9 with respect

to education indicate changes in level of education and entrepreneurial activity for both the TEA and EST indicators. For 2008, the results indicate that for the TEA, 71.4% of entrepreneurs had post-secondary or graduate education (post-secondary, 25.8%; graduate education, 45.8%), and for the established business measures, 76.4% of entrepreneurs had post-secondary or graduate education (post-secondary,

18

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Figure 7. Total Early-Stage Education Levels by Year

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 2008

Some SecondarySecondary DegreePost-SecondaryBachelors Degree or Higher

Figure 8. Percentage Distribution of Entrepreneurs by Education Levels (TEA)

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007 2008

Some Secondary

Secondary Degree

Post-Secondary

Bachelors Degree or Higher

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

25.6%; graduate education, 51.8%). This surprising result, combined with a large drop in the percentage of entrepreneurs with secondary degrees from 2007 to 2008 for both the TEA (38.2% to 17.1%) and established business measures (20.5% to 13.8 %), requires further assessment to determine the reasons behind this shift and to determine whether it is a temporary or permanent phenomenon.

This change may reflect the current economic crisis, with more educated workers opting to start their own firms. However, more data are needed to determine whether this is the case. Nevertheless, a trend to observe is the percentage increase of entrepreneurs with graduate education for both the TEA and the established business measures (Figures 8 and 9). For both measures, the increase of percentages of entrepreneurs with graduate education has been both consistent and significant.

Why do People Start Businesses in the United States? The Nature of Start-Ups

19

Figure 9. Percentage Distribution of Entrepreneurs by Education (Established Businesess)

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007 2008

Some Secondary

Secondary Degree

Post-Secondary

Bachelors Degree or Higher

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Entrepreneurial Activity and Income Distribution

Finally, this report looks at distributions for different phases of U.S. entrepreneurial activity based on the income classification of entrepreneurs. The classifications for income are high, medium and low. High, medium and low represent the percentages of entrepreneurs that rank in the upper, middle or lower third of the income levels for the U.S. 18-99 age group for each year from 2003 to 2008. The results for those entrepreneurs in the total early-stage (TEA) and established business ownership (EST) phases of entrepreneurship are contained in Figures 10 and 11, respectively. Figure 10 illustrates that in the earlier

years, 2003–2004, the early-stage entrepreneurs had the highest percentage of entrepreneurial activity from the high-income U.S. population. Participation of the low- and middle-income early-stage entrepreneurs increased relative to the high-income early-stage entrepreneurs in 2005. In 2008, 31.8% of early-stage entrepreneurs are estimated to be in the lowest third income category, 36.8% are in the middle third and 31.3% are estimated to be in the highest third income category for early-stage entrepreneurial activity. Those numbers are consistent with and show little variation from data from the previous year, 2007. The middle-income category has maintained the highest distribution for activity in the early-stage phase from 2005 to 2008.

Why do People Start Businesses in the United States? The Nature of Start-Ups

20

0%

10%

20%

30%

40%

50%

60%

70%

80%

2003 2004 2005 2006 2007 2008

Lowest 33rd Percentile

Middle 33rd Percentile

Upper 33rd Percentile

Figure 11. Entrepreneurs by Income Segments (EST)

Source: GEM U.S. 2003-2008 Adult Population Survey (APS)

Figure 11 illustrates that the established business owners have the highest number of entrepreneurs in the high-income category for each year from 2003 to 2008. As was the case for the early-stage entrepreneurs, the low- and medium-income categories gained shares of the percentage of activity for the established business entrepreneurs, but the

high-income category declined in 2003 and 2004. However, the low-income category of entrepreneurs has been declining in percentage distributions since 2006 in the established business phase, whereas the middle-income category of entrepreneurs has increased its distribution in 2008 in the established business phase.

0%

10%

20%

30%

40%

50%

60%

70%

2003 2004 2005 2006 2007 2008

Lowest 33rd Percentile

Middle 33rd Percentile

Upper 33rd Percentile

Figure 10. Entrepreneurs by Income Segments (TEA)

Source: GEM U.S. 2003-2008 Adult Population Survey (APS)

Why do People Start Businesses in the United States? The Nature of Start-Ups

21

Why Do PEoPlE StArt bUSiNESSES iN thE UNitED StAtES?

Whether or not individuals start a new business depends on a complex series of factors. Intentions and perceptions are important determinants in the decision making process. Entrepreneurs who aspire to create jobs are of special interest in this troubled economic period. The intention to create jobs is an integrated measure of both an entrepreneur’s ability as a manager and of his/her perception of characteristics in the environment being conducive to entrepreneurial activity. Individual perceptions of skills and fear of failure also play important roles in the number and types of entrepreneurs entering the marketplace.

Attitudes and Perceived Opportunities for Starting a Business

A different picture emerges when differentiating between early-stage (TEA) and the non-early-stage (non-TEA) populations. Figure 12 indicates that in 2008, we see the highest percentage of good opportunities to start a business in six months for the non-early-stage population and the lowest percentage of positive responses for the early-stage entrepreneurs. This trend of less optimism in 2008 is also seen for start-ups of new businesses in three years by early-stage entrepreneurs and by established business entrepreneurs as well as the non-early-stage respondents.

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005 2006 2007 2008

Perc

enta

ge Ye

s

Non TEA TEA

Figure 12. Respondent Perceives Good Opportunities in the Next Six Months (18-99 Age Group)

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

The perception of good opportunities for starting new businesses in the United States in six months during the 2001—2007 period ranged from 61.1% to 72.5% (post-9/11) for early-stage entrepreneurs and from 21.1% to 30.3% for the rest of the population. Those involved in early-stage entrepreneurship were twice as optimistic about the opportunities to start a business in the near term for the 2001–2007 period.

Attitude and Perceptions of Knowledge and Skills to Start a Business

Figure 13 shows that there is a very high perception by early-stage entrepreneurs concerning their skills and knowledge to start and manage a business in the United States. The last two years, 2007 and 2008, however, have dipped below 90% for the early-stage entrepreneurs, perhaps indicative of the recession and financial crisis in the United States. Half of the non-early-stage entrepreneurs feel they have the knowledge to run a business over the 2001–2008 period.

Why do People Start Businesses in the United States? The Nature of Start-Ups

22

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005 2006 2007 2008

Perc

enta

ge Ye

s

Non TEA TEA

Figure 13. Respondent Has Knowledge to Start a Business (18-99 Age Group)

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Attitude and Perceptions of Fear of Failure

Figure 14 illustrates the fear of failure as a consideration in starting or running a business. In 2008, there is an increase in the fear of failure to start a business for the overall U.S. population compared

to 2007. When examining the strength of the entrepreneurial ethos in the United States, scholars have centered on the notion that less concern for fear of failure would be a key driver of entrepreneurial behavior in the United States.

Aspirations and Expected Jobs from Start-Up

Figure 15 shows the historical number of jobs created during the start-up phase of entrepreneurship. The start-up phase includes the nascent and new business entrepreneur. From 2001 to 2006, the number of start-up businesses with no current jobs hovered around 80%. In 2007, based on the GEM data, there was a substantial decrease to 50% for the current

number of startups with no jobs. One definition of a high-growth entrepreneur is one that expects to create 20 or more jobs in five years. In 2007, we see over 10% of the start-up businesses with 20+ current jobs and over 8% in 2008. Figure 16 shows job creation numbers for start-up businesses expected in five years. The aspirations are that about 25% of the start-up businesses expect to create 20 or more jobs in five years in 2008, compared to less than 20% in 2007.

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008

Perc

enta

ge Ye

s

Non TEA TEA

Figure 14. Fear of Failure Prevents Start-Up (18-99 Age Group)

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Why do People Start Businesses in the United States? The Nature of Start-Ups

23

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 2008

No Jobs

1-5 Jobs

6-19 Jobs

20+ Jobs

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008

No Jobs

1-5 Jobs

6-19 Jobs

20+ Jobs

Figure 15. Current Start-Up Jobs

Figure 16. Expected Jobs from Start-Up in Five Years

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Source: GEM U.S. 2001-2008 Adult Population Survey (APS)

Why do People Start Businesses in the United States? The Nature of Start-Ups

24

Part 2 International Comparison: The United States and Other Countries

GEM PArtiCiPAtiNG CoUNtriES iN 2008

Forty-three countries participated in the GEM project in 2008. For more appropriate comparisons, the countries are grouped by similar stages of economic development: factor-driven countries, efficiency-driven countries and innovation-driven countries. These groupings are based on the World Economic Forum’s 2008-2009 Global Competitiveness Report (Porter and Schwab, 2008) and are as follows:

Factor-Driven Economies

Angola, Bolivia, Bosnia and Herzegovina,* Colombia,* Ecuador,* Egypt, India, Iran*

Efficiency-Driven Economies

Argentina, Brazil, Chile, Croatia,** Dominican Republic, Hungary,** Jamaica, Latvia, Macedonia, Mexico, Peru, Romania, Russia, Serbia, South Africa, Turkey, Uruguay

Innovation-Driven Economies

Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Israel, Italy, Japan, Republic of Korea, Netherlands, Norway, Slovenia, Spain, United Kingdom, United States

*Transition country: from factor-driven to efficiency-driven

**Transition country: from efficiency-driven to innovation-driven

25

0%

5%

10%

15%

20%

25%

30%

35%

Bosn

ia a

nd H

erzo

govi

na Iran

Indi

aEg

ypt

Ecua

dor

Ango

laCo

lom

bia

Boliv

iaRu

ssia

Rom

ania

Turk

eyLa

tvia

Hung

ary

Croa

tiaSe

rbia

Sout

h Af

rica

Urug

uay

Braz

ilM

exic

oCh

ileM

aced

onia

Jam

aica

Arge

ntin

aDo

min

ican

Rep

ublic

Peru

Belg

ium

Ger

man

yDe

nmar

kIta

lyN

ethe

rland

sJa

pan

Fran

ceUn

ited

King

dom

Slov

enia

Isra

elSp

ain

Finl

and

Irela

ndN

orw

ayG

reec

eRe

publ

ic o

f Kor

eaIc

elan

dUn

ited

Stat

es

Factor-Driven Economies

Efficiency-Driven Economies Innovation-Driven Economies

Perc

enta

ge o

f Ad

ult

Popu

latio

n be

twee

n 18

-64

Age

Gro

up

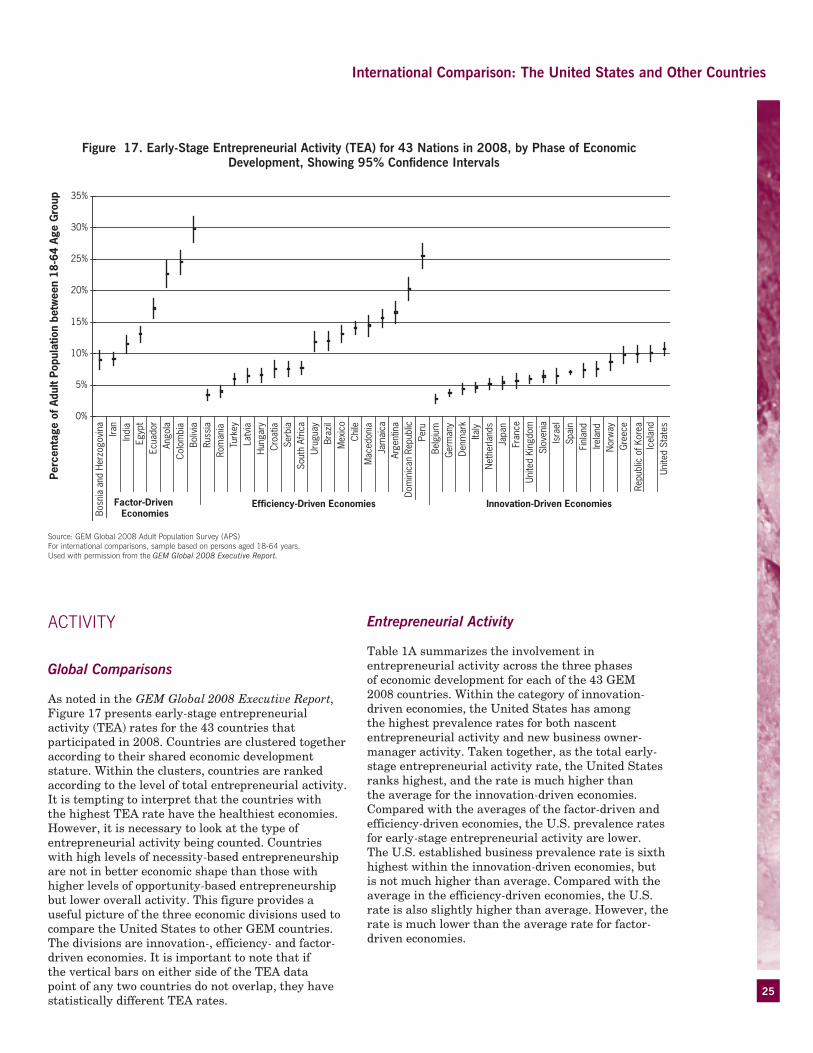

Figure 17. Early-Stage Entrepreneurial Activity (TEA) for 43 Nations in 2008, by Phase of Economic Development, Showing 95% Confidence Intervals

Source: GEM Global 2008 Adult Population Survey (APS)for international comparisons, sample based on persons aged 18-64 years.Used with permission from the GEM Global 2008 Executive Report.

ACtivity

Global Comparisons

As noted in the GEM Global 2008 Executive Report, Figure 17 presents early-stage entrepreneurial activity (TEA) rates for the 43 countries that participated in 2008. Countries are clustered together according to their shared economic development stature. Within the clusters, countries are ranked according to the level of total entrepreneurial activity. It is tempting to interpret that the countries with the highest TEA rate have the healthiest economies. However, it is necessary to look at the type of entrepreneurial activity being counted. Countries with high levels of necessity-based entrepreneurship are not in better economic shape than those with higher levels of opportunity-based entrepreneurship but lower overall activity. This figure provides a useful picture of the three economic divisions used to compare the United States to other GEM countries. The divisions are innovation-, efficiency- and factor-driven economies. It is important to note that if the vertical bars on either side of the TEA data point of any two countries do not overlap, they have statistically different TEA rates.

Entrepreneurial Activity

Table 1A summarizes the involvement in entrepreneurial activity across the three phases of economic development for each of the 43 GEM 2008 countries. Within the category of innovation-driven economies, the United States has among the highest prevalence rates for both nascent entrepreneurial activity and new business owner-manager activity. Taken together, as the total early-stage entrepreneurial activity rate, the United States ranks highest, and the rate is much higher than the average for the innovation-driven economies. Compared with the averages of the factor-driven and efficiency-driven economies, the U.S. prevalence rates for early-stage entrepreneurial activity are lower. The U.S. established business prevalence rate is sixth highest within the innovation-driven economies, but is not much higher than average. Compared with the average in the efficiency-driven economies, the U.S. rate is also slightly higher than average. However, the rate is much lower than the average rate for factor-driven economies.

International Comparison: The United States and Other Countries

26

NASCENT ENTREPRENEURIAL ACTIVITY (%)

NEW FIRM ENTREPRENEURS (%)

EARLY-STAGE ENTREPRENEURIAL ACTIVITY (%)

ESTABLISHED ENTREPRENEURS (%)

BUSINESS DISCONTINUATION RATE (%)

EARLY-STAGE OPPORTUNITY RATE (%)

EARLY-STAGE NECESSITY RATE (%)

Factor-Driven Economies

Angola 19.9 3.8 23.1 5.7 22.3 11.4 7.6

Bolivia 17.0 13.6 28.8 20.3 10.7 20.3 8.3

Bosnia and Herzegovina 5.0 2.0 7.0 7.5 4.0 3.8 3.1

Colombia 12.6 10.7 22.4 12.9 6.5 12.7 9.3

Ecuador 8.7 9.1 17.2 11.9 5.9 12.1 4.9

Egypt 7.9 5.5 13.1 8.0 6.3 10.5 2.4

India 6.1 4.3 10.1 15.8 11.9 7.1 2.2

Iran 5.4 3.1 8.5 6.2 8.6 5.4 2.6

Average 10.6 7.1 17.0 11.8 8.9 11.1 5.2

Efficiency-Driven Economies

Argentina 6.9 6.8 13.3 12.8 8.9 8.0 5.1

Brazil 3.0 9.3 12.0 14.6 3.5 8.1 4.0

Chile 7.3 5.1 12.3 6.6 5.4 8.8 3.0

Croatia 3.6 2.0 5.5 3.9 2.5 3.9 1.6

Dominican Republic 10.1 8.5 17.6 7.1 9.7 12.1 5.4

Hungary 3.9 2.8 6.6 5.4 1.1 4.4 1.9

Jamaica 7.4 5.8 12.9 14.2 7.5 6.6 6.0

Latvia 3.9 2.7 6.5 3.0 1.8 4.9 1.3

Macedonia 5.6 6.7 12.0 9.7 4.7 5.7 5.9

Mexico 8.4 3.5 11.7 4.7 13.2 9.0 1.5

Peru 19.7 6.8 25.6 8.3 10.4 17.0 8.0

Romania 1.9 1.2 3.1 1.9 1.8 1.6 1.0

Russia 1.7 2.0 3.5 1.1 1.1 2.5 0.7

Serbia 2.9 2.8 5.6 8.3 3.3 3.5 1.8

South Africa 5.2 2.0 7.1 2.6 5.2 5.6 1.4

Turkey 3.2 3.0 6.0 4.8 4.0 3.5 2.3

Uruguay 6.0 3.3 9.2 6.6 7.5 5.9 2.3

Average 6.0 4.2 10.0 6.7 5.7 6.6 3.0

Innovation-Driven Economies

Belgium 2.0 0.9 2.9 2.7 1.5 2.4 0.3

Denmark 2.3 2.2 4.4 4.4 1.9 4.1 0.3

Finland 4.1 3.3 7.4 9.1 2.0 6.1 0.9

France 2.8 1.4 4.2 2.0 2.4 3.5 0.4

Germany 2.4 1.5 3.8 4.0 1.8 2.7 1.0

Greece 5.2 4.6 9.9 12.6 2.9 6.7 3.1

Iceland 6.5 3.6 10.0 7.1 3.4 8.2 0.5

Ireland 3.3 4.3 7.6 9.0 3.6 5.7 1.4

Israel 2.8 2.5 5.1 4.3 2.7 3.6 1.1

Italy 2.0 2.7 4.6 6.5 1.8 3.6 0.7

Japan 2.1 1.5 3.5 7.8 2.5 2.6 0.8

Republic of Korea 3.6 6.5 10.0 12.9 4.7 5.8 4.1

Netherlands 1.7 2.3 4.0 5.8 1.3 3.2 0.4

Norway 3.9 3.2 6.9 7.6 3.5 5.8 0.5

Slovenia 4.1 2.4 6.4 5.6 1.3 5.6 0.8

Spain 3.3 3.9 7.0 9.1 1.3 5.6 1.0

United Kingdom 2.3 2.2 4.4 4.4 2.0 3.5 0.6

United States 4.8 4.0 8.7 7.7 4.1 7.2 1.0

Average 3.2 3.2 6.3 7.4 2.0 5.0 1.0

GEM Average 6.0 4.4 10.2 7.1 5.4 6.7 3.1

Table 1A. Prevalence Rates in Percentage of Entrepreneurial Activity and Business Owner-Managers Across GEM Countries in 2008, for the 18-99 Age Group,* by Phase of Economic Development

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-99 years.*for the age group 18-64 see table 1b in the Appendix.

International Comparison: The United States and Other Countries

27

Entrepreneurial Motivations

The opportunity-driven early-stage entrepreneurial activity rate is the highest in the United States, much higher than the average within the category. The rate is slightly higher than the average of efficiency-driven economies but lower than the average of factor-driven countries. The necessity-driven early-stage entrepreneurial activity rate in the United States is slightly higher than the average for innovation-driven economies but is lower than the averages of both efficiency-driven and factor-driven economies.

Discontinuing Business

The U.S. business discontinuation rate is second highest among innovation-driven countries and is much higher than the average, possibly indicating a propensity to terminate business experiments that are not viable. The U.S. rate, however, is much lower than the averages of both efficiency-driven and factor-driven economies.

Sector Distributions

As shown in Figures 18 and 19, the distribution by industry sector of early-stage entrepreneurial activity and established business owner-managers follows an expected pattern across the three phases of economic development. Extraction businesses (farming, forestry, fishing and mining) are expected to be more prevalent in factor-driven economies. Transforming businesses (manufacturing and construction) are expected to be more prevalent in efficiency-driven economies. Business services should be more prevalent in innovation-driven economies. Furthermore, the proportion of consumer-oriented businesses should decline for each higher phase of economic development. Countries with poorly developed transportation and commercial infrastructure tend to have higher proportions of consumer-oriented businesses. The United States has a noticeably smaller proportion of consumer-oriented businesses than the averages of each of the three phases of development for both early-stage entrepreneurial activity and established business owner-managers. In both figures, the proportion of the business services sector is much larger than the averages of the three phases of economic development.

0% 20% 40% 60% 80% 100%

Factor-Driven Economies

Efficiency-Driven Economies

Innovation-Driven Economies

United States

Extractive Transforming Business Services Consumer-Oriented

Figure 18. Sector Distribution Early-Stage Entrepreneurial Activity (18-64 Age Group)

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

International Comparison: The United States and Other Countries

28

International Comparison: The United States and Other Countries

0% 20% 40% 60% 80% 100%

Factor-Driven Economies

Efficiency-Driven Economies

Innovation-Driven Economies

United States

Extractive Transforming Business Services Consumer-Oriented

Figure 19. Sector Distribution Established Businesses (18-64 Age Group)

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

Age and Gender Structure

As shown in Figure 20, the shapes of the age distributions are very similar across the averages of the three economic phases of development for early-stage entrepreneurial activity, with the 25-34 range having the highest prevalence rate. The U.S. age distribution also follows a similar age pattern, but with approximately equal prevalence rates across the 35-44 range and the 25-34 range. This indicates that unlike the global averages, in the United States there is a higher rate of entrepreneurial activity in the 35-44 age group relative to the 25-34 age group.

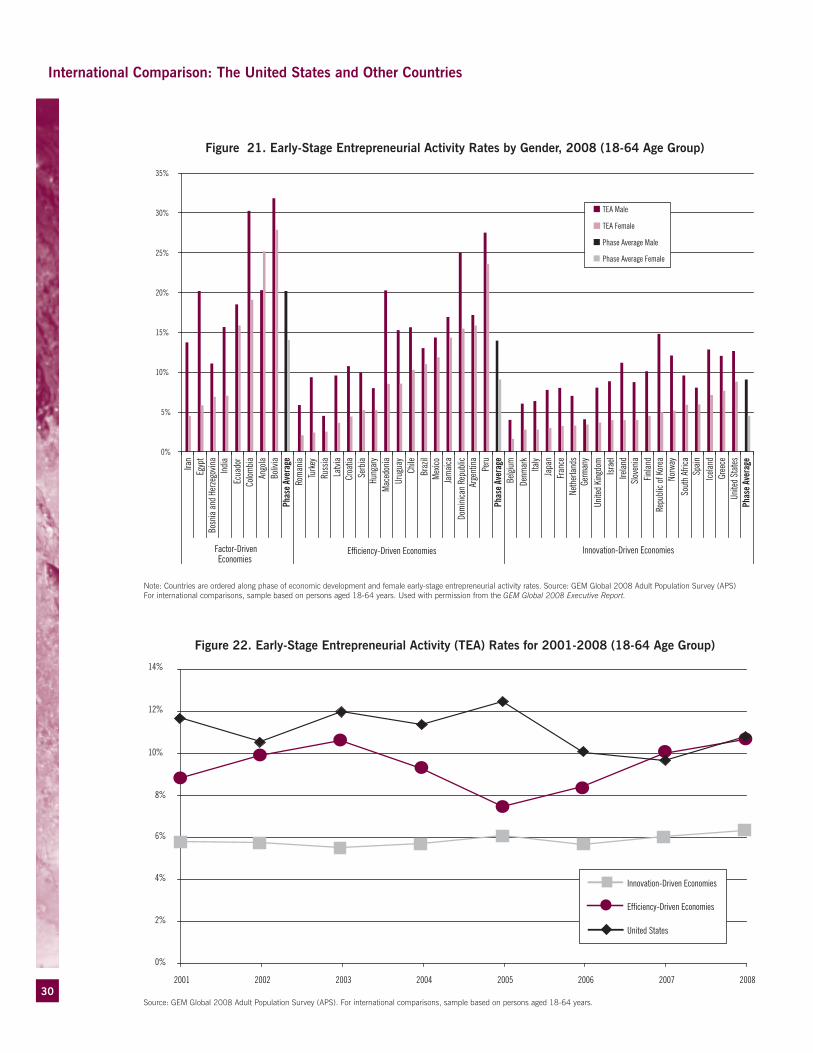

Figure 21 displays the differences in female and male participation for each country, grouped by phase of economic development with increasing female participation rate. The gap in the average ratio of male to female participation increases across the phases—with lows of 1.4 males to females in factor-driven economies and 1.5 males to females in efficiency-driven economies—to twice as many males involved in early-stage entrepreneurial activity than women in innovation-driven countries. The gap is smaller in the United States, on the other hand, with more women involved in early-stage entrepreneurial activity relative to the average rate in innovation-driven countries.

29

International Comparison: The United States and Other Countries

0%

5%

10%

15%

20%

25%

Factor-DrivenEconomies

Efficiency-DrivenEconomies

Innovation-DrivenEconomies

United States

Perc

enta

ge o

f Adu

lt Pp

opul

atio

n in

Age

Gro

up

18-24 YRS

25-34 YRS

35-44 YRS

45-54 YRS

55-64 YRS

Figure 20. Early-Stage Entrepreneurial Activity for Separate Age Groups, 2008

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

Trend in Early-Stage Entrepreneurial Activity 2001–2008

Figure 22 is a chart of the average annual TEA rates from 2001 to 2008 for the United States and a subset of GEM efficiency-driven and innovation-driven countries. The TEA rates for innovation-driven economies have been stable at around a 6% rate since 2001. The TEA rate for efficiency-driven economies has been more volatile, but on average has been higher than the rate for innovation-driven economies. The U.S. TEA rate has been substantially higher than the average TEA rate for innovation-

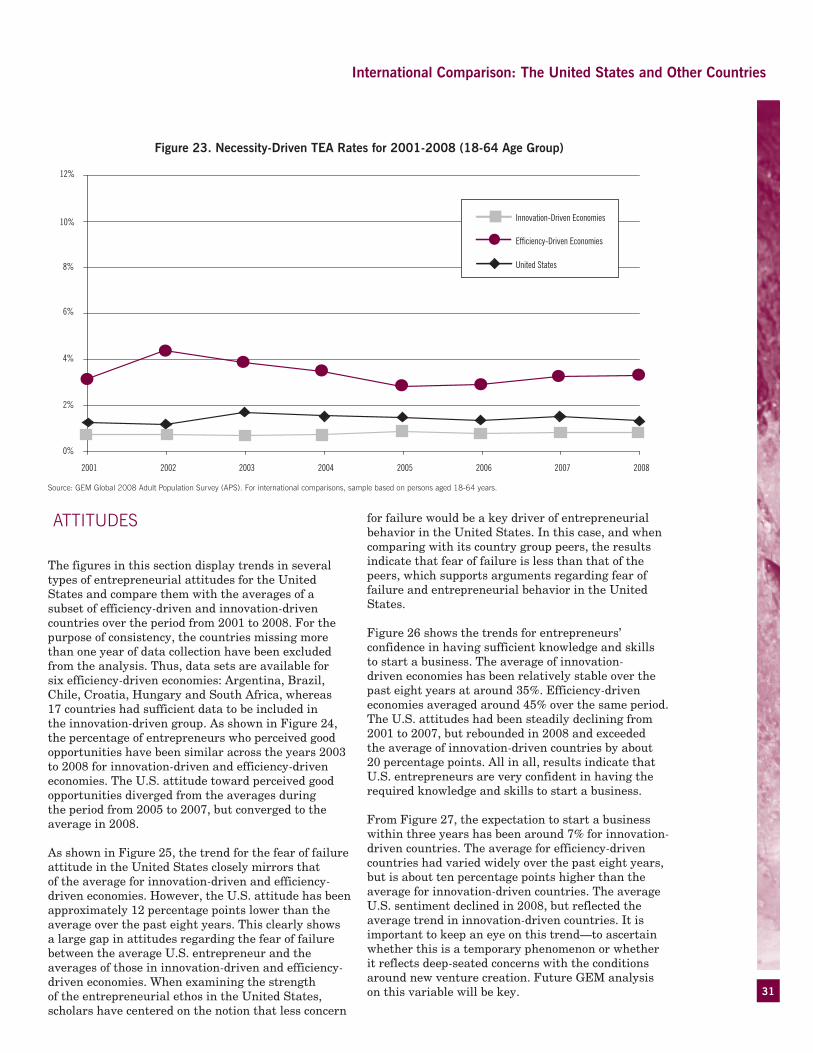

driven economies. In the past two years, the U.S. rate has fallen to a level comparable to the average TEA rate for efficiency-driven economies. Figure 23 shows the trends in necessity-driven TEA rates from 2001 to 2008 for the United States and a subset of GEM efficiency-driven and innovation-driven countries. Similarly, the average for innovation-driven economies has been stable at a rate under 1% since 2001, while the rate for the efficiency-driven countries has averaged around 3%. On the other hand, although the U.S. necessity-driven TEA rate has been stable, it is slightly higher than the average for innovation-driven economies but lower than the average for efficiency-driven economies.

30

0%

2%

4%

6%

8%

10%

12%

14%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

Figure 22. Early-Stage Entrepreneurial Activity (TEA) Rates for 2001-2008 (18-64 Age Group)

International Comparison: The United States and Other Countries

Note: Countries are ordered along phase of economic development and female early-stage entrepreneurial activity rates. Source: GEM Global 2008 Adult Population Survey (APS)for international comparisons, sample based on persons aged 18-64 years. Used with permission from the GEM Global 2008 Executive Report.

Figure 21. Early-Stage Entrepreneurial Activity Rates by Gender, 2008 (18-64 Age Group)

0%

5%

10%

15%

20%

25%

30%

35%

Iran

Egyp

tBo

snia

and

Herze

govin

aIn

dia

Ecua

dor

Colom

bia

An

gola

Boliv

iaPh

ase

Aver

age

Rom

ania

Turk

ey

Russ

ia

Latv

ia

Croa

tia

Serb

ia Hu

ngar

y

M

aced

onia

Urug

uay

Chile

Br

azil

Mex

ico

Jam

aica

Dom

inica

n Re

publi

c Ar

gent

ina

Peru

Phas

e Av

erag

e Be

lgium

De

nmar

k

Ita

ly

Japa

n

Fran

ce

Neth

erlan

ds

Germ

any

Unite

d Ki

ngdo

m

Isr

ael

Irelan

d

Sl

oven

ia

Fin

land

Repu

blic o

f Kor

eaNo

rway

So

uth

Afric

a

Spain

Ice

land

Gree

ce

Unite

d St

ates

Phas

e Av

erag

e

Factor-DrivenEconomies

Efficiency-Driven Economies Innovation-Driven Economies

TEA Male

TEA Female

Phase Average Male

Phase Average Female

31

0%

2%

4%

6%

8%

10%

12%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

Figure 23. Necessity-Driven TEA Rates for 2001-2008 (18-64 Age Group)

International Comparison: The United States and Other Countries

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

AttitUDES

The figures in this section display trends in several types of entrepreneurial attitudes for the United States and compare them with the averages of a subset of efficiency-driven and innovation-driven countries over the period from 2001 to 2008. For the purpose of consistency, the countries missing more than one year of data collection have been excluded from the analysis. Thus, data sets are available for six efficiency-driven economies: Argentina, Brazil, Chile, Croatia, Hungary and South Africa, whereas 17 countries had sufficient data to be included in the innovation-driven group. As shown in Figure 24, the percentage of entrepreneurs who perceived good opportunities have been similar across the years 2003 to 2008 for innovation-driven and efficiency-driven economies. The U.S. attitude toward perceived good opportunities diverged from the averages during the period from 2005 to 2007, but converged to the average in 2008.

As shown in Figure 25, the trend for the fear of failure attitude in the United States closely mirrors that of the average for innovation-driven and efficiency-driven economies. However, the U.S. attitude has been approximately 12 percentage points lower than the average over the past eight years. This clearly shows a large gap in attitudes regarding the fear of failure between the average U.S. entrepreneur and the averages of those in innovation-driven and efficiency-driven economies. When examining the strength of the entrepreneurial ethos in the United States, scholars have centered on the notion that less concern

for failure would be a key driver of entrepreneurial behavior in the United States. In this case, and when comparing with its country group peers, the results indicate that fear of failure is less than that of the peers, which supports arguments regarding fear of failure and entrepreneurial behavior in the United States.

Figure 26 shows the trends for entrepreneurs’ confidence in having sufficient knowledge and skills to start a business. The average of innovation-driven economies has been relatively stable over the past eight years at around 35%. Efficiency-driven economies averaged around 45% over the same period. The U.S. attitudes had been steadily declining from 2001 to 2007, but rebounded in 2008 and exceeded the average of innovation-driven countries by about 20 percentage points. All in all, results indicate that U.S. entrepreneurs are very confident in having the required knowledge and skills to start a business.

From Figure 27, the expectation to start a business within three years has been around 7% for innovation-driven countries. The average for efficiency-driven countries had varied widely over the past eight years, but is about ten percentage points higher than the average for innovation-driven countries. The average U.S. sentiment declined in 2008, but reflected the average trend in innovation-driven countries. It is important to keep an eye on this trend—to ascertain whether this is a temporary phenomenon or whether it reflects deep-seated concerns with the conditions around new venture creation. Future GEM analysis on this variable will be key.

32

International Comparison: The United States and Other Countries

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

Figure 24. Perceived Opportunities for Starting a Business, 2001-2008

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

Figure 25. Fear of Failure Among Those Who Perceive Good Start-Up Opportunities, 2001-2008

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

33

International Comparison: The United States and Other Countries

Figure 26. Perceived Skills and Knowledge to Start a Business, 2001-2008

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

Figure 27. Intentions to Start a New Business in the Next Three Years, 2002-2008

Source: GEM Global 2008 Adult Population Survey (APS). for international comparisons, sample based on persons aged 18-64 years.

30%

35%

40%

45%

50%

55%

60%

65%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2001 2002 2003 2004 2005 2006 2007 2008

Innovation-Driven Economies

Efficiency-Driven Economies

United States

34

ASPirAtioNS

Figure 28 shows the rate of high-growth expectation for early-stage entrepreneurship in GEM countries for which a sufficient sample size was available,

grouped by level of economic development. The United States has the fifth highest rate among innovation-driven countries and is above the average within the innovation-driven grouping. Compared with efficiency-driven and factor-driven countries, the U.S. rate is approximately equal to the averages of those groups.

Figure 28. High-Growth Expectations Early-Stage Entrepreneurial Activity by Country

Source: GEM Global 2008 Adult Population Survey (APS)for international comparisons, sample based on persons aged 18-64 years.Used with permission from GEM Global 2008 Executive Report.

0%

5%

10%

15%

20%

25%

30%

India

Colom

biaCh

ina

Aver

age

Mex

ico

Thail

and

Braz

ilPe

ruHu

ngar

y

Sout

h Afri

ca

Arge

ntin

aCr

oatia

Chile

Latv

iaTu

rkey

Aver

age

Spain

Gree

ceFr

ance

Finlan

dBe

lgium

Aust

ralia

Norw

ayNe

ther

lands

New

Zeala

ndSw

itzer

land

Japa

nIta

ly

Swed

enUn

ited

King

dom

Germ

any

Denm

ark

Irelan

dSl

oven

ia

Unite

d St

ates

Cana

da

Icelan

dSi

ngap

ore

Hong

Kon

g

Aver

age

Factor-Driven

Efficiency-Driven Innovation-Driven

Perc

enta

ge o

f Ear

ly-St

age

Entre

pren

eurs

Country Mean

Phase Average

International Comparison: The United States and Other Countries

35

WoMEN’S ENtrEPrENEUrShiP

It is widely acknowledged that women own 30% and are majority owners of 6.7 million of more than 23 million U.S. businesses (www.cfwbr.org). This impressive statistic includes businesses that were co-founded, acquired or inherited, but does not capture those recently launched. In comparison, the GEM 2008 data set captures those women led ventures in the nascent and early-stage and allows comparisons by gender.

As noted in Part 1, the rate of start-up activity in 2008 for women entrepreneurs was 7.5% compared to 9.8% for men, whereas in 2007 it was 7.3% for women and 12.0% for men. This suggests that the rate of women’s

entrepreneurship has been steady, but for men it has declined, effectively decreasing the gap between them. More than 50% of women started businesses are in consumer services versus 24% of those started by men, while men were more likely to launch ventures (46%) compared to women (26%). While the majority of all nascent ventures are no/low-technology, 10% of men compared to 2.6% of women are in the high-technology sector.

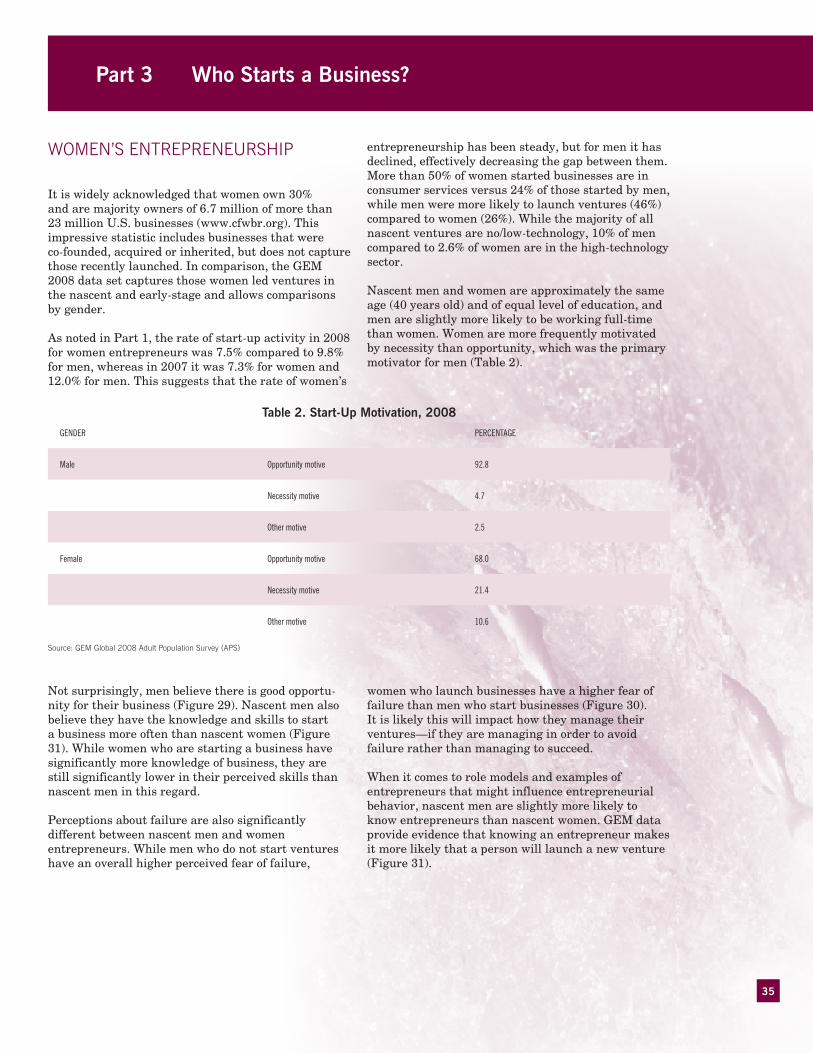

Nascent men and women are approximately the same age (40 years old) and of equal level of education, and men are slightly more likely to be working full-time than women. Women are more frequently motivated by necessity than opportunity, which was the primary motivator for men (Table 2).

Part 3 Who Starts a Business?

Table 2. Start-Up Motivation, 2008

GENDER PERCENTAGE

Male Opportunity motive 92.8

Necessity motive 4.7

Other motive 2.5

Female Opportunity motive 68.0

Necessity motive 21.4

Other motive 10.6

Source: GEM Global 2008 Adult Population Survey (APS)

Not surprisingly, men believe there is good opportu-nity for their business (Figure 29). Nascent men also believe they have the knowledge and skills to start a business more often than nascent women (Figure 31). While women who are starting a business have significantly more knowledge of business, they are still significantly lower in their perceived skills than nascent men in this regard.

Perceptions about failure are also significantly different between nascent men and women entrepreneurs. While men who do not start ventures have an overall higher perceived fear of failure,

women who launch businesses have a higher fear of failure than men who start businesses (Figure 30). It is likely this will impact how they manage their ventures—if they are managing in order to avoid failure rather than managing to succeed.

When it comes to role models and examples of entrepreneurs that might influence entrepreneurial behavior, nascent men are slightly more likely to know entrepreneurs than nascent women. GEM data provide evidence that knowing an entrepreneur makes it more likely that a person will launch a new venture (Figure 31).

36

Figure 29. Perceptions of Good Opportunities, Female vs. Male, 2008

Source: GEM U.S. 2008 Adult Population Survey (APS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Male Female

Fear of Failure/No Start-Up

Fear of Failure/ Yes Start-Up

Figure 30. Fear of Failure Rates, Female vs. Male, 2008

Source: GEM U.S. 2008 Adult Population Survey (APS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Male Female

Personally Knows an

Entrepreneur (No Start-Up)

Personally Knows an

Entrepreneur (Yes, Start-Up)

Who Starts a Business?

37

Who Starts a Business?

Source: GEM U.S. 2008 Adult Population Survey (APS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Male Female

Has Knowledge and Skill

for a Start-up (No Start-Up)

Has Knowledge and Skill

for a Start-up (Yes, Start-Up)

Figure 31. Personally Knows an Entreprenuerial Rates, Female vs. Male, 2008

The start-up circumstances for men and women vary significantly; 40% of women come from households earning less than $50,000 a year compared to 23% of men. Furthermore, 20% of nascent men come from households earning more than $150,000 a year compared to only 11% of nascent women. This is likely related to the comparatively lower plans for start-up funding, where 80% of women expect to spend less than $5,000 versus 64% of men. In considering the start-up investment, the data show that women start ventures with eight-times less funding than their male counterparts.

When it comes to expansion, slightly more nascent men expect to develop new products and services, and significantly more men are likely to apply or use new technology in their venture in the next six months.