what insurance innovation means for corporations3b104b0c-0cad-405a... · the digital society is the...

TRANSCRIPT

What insurance innovation means for corporations

Dr. Jeffrey Bohn, Head, Swiss Re Institute

May 2019

2

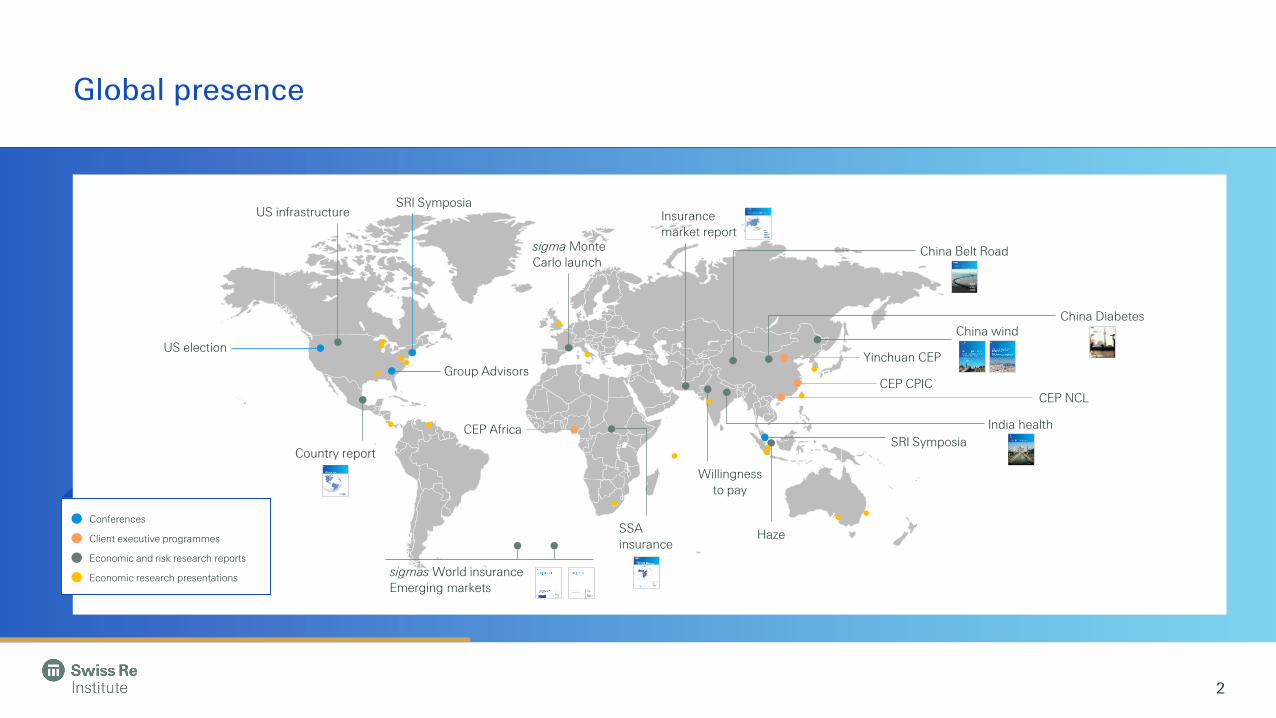

Global presence

Conferences

Client executive programmes

Economic and risk research reports

Economic research presentations

US election

US infrastructure

Country report

Group Advisors

SRI Symposia

sigma MonteCarlo launch

sigmas World insuranceEmerging markets

CEP Africa

SSAinsurance

Insurancemarket report

Willingnessto pay

India health

China Belt Road

China Diabetes

Yinchuan CEP

China wind

CEP CPICCEP NCL

Haze

SRI Symposia

Swiss Re Institute: Background and Partnerships

Strategic

Tactical

Opportunistic

University of Washington

Drivers of innovation

4

The Digital Society is the result of many technology trends

Semiconductors enabled cheap and abundant computation

The internet enabled cheap and abundant connectivity

Big data creates cheap and abundant information

IoT & 5G enables cheap, abundant, and connected sensors

…

Distributed ledger technology enables decentralized transaction authentication

AI enables cheap and abundant predictions

In digital societies, if data is the oil, Machine Intelligence is the refinery

Data is the new oil: The crude product multiplies in value after refinement

Generate & collect

Organise & curate

Analyse & transform

Deliver& multiply value

Platforms (eg. Smart City)

IoT 5G Connectivity Big Data Cloud computing Human + Artificial Intelligence Autonomous systemsRobotics

Innovation drivers from the InsurTech perspective

7

Next-generation online insurance portals

10%

Cloud computing8%

Drones, aerial and digital Imagery 9%

Others

Telematics and connected car7%

2%

8%External third-party marketplaces

4%

Location Intelligence22%

Internet of Things (IoT)

11%

19%

AI / Machine learning / roboadvisors

Advanced analytics solutions

Note: Data relate to a sample of 300 of the best-known and well-funded InsurTech start-ups.

Source: Swiss Re Institute, based on information from company websites and media reports.

Technology areas that InsurTech start-ups are focusing on (% share by number of start-up investments), 2014-2016

Threats

8

Threat: Algorithmic risk– especially critical given increasing dependence on enterprise-wide software systems

• Algorithmic risk on the rise due to the following trends for software systems:

– Complexity

– Connectivity

– Ubiquity

– Interoperability (or lack thereof– particularly with respect to legacy systems)

• Trend exacerbated due to…

– Lack of software engineering standards & benchmarks

– Shortage of system architects

– Increased incidence of “algorithmic malpractice”

– Dependence on compiled components

• Primary threats from algorithmic risk

– System operational fragility i.e., risk of failure

– System vulnerability i.e., risk of cyber attack

Threat: Cyber risk

10

Accidental breaches of security

Unauthorized & deliberate breach of computer security to access systems– both internal & external

Human error leading to vulnerabilities (e.g., IT operational issues, poor capacity planning, integration issues, system integrity, etc.)

Threat & opportunity: Agile data analytics

Software talent (particularly in machine intelligence) is in short supply requiring higher throughput

Less than 5% of data analyst work generates ROI

Data driven organizations are outcompeting rest

Augmented intelligence & intelligent automation require more agile development processes

Opportunities

12

Insurance & resilience opportunities arising from innovation

• New business models

– Resilience or risk as a service

– Insurance is bundled with product

– Insurance economics modified increasing possibilities for protection

• Customized insurance protection

– Parametric

– Usage-based

– Dynamic pricing

– Specialized– insurance can be integrated into business value chains & processes in new ways

• Resilience as a service

– Resilience certification (e.g., algorithmic or system robustness)

– Resilience monitoring

– Data analytics to reinforce insurance (measure & manage delays, interruptions, chain breaks, etc.)

14

Transformative business models (e.g., distributed ledger technology (DLT))

Internal improvements

Enhancement ofinsurance value-chain New value-chains

End-customer driven initiatives

New players creating a DLT-based alternative value-

chain or market for distribution of re/insurance

services

End-customers in non-insurance verticals

organizing DLT cooperatives for aggregation of shared

services including insurance

Organizing members of existing insurance value-

chain into a DLT cooperative for driving data

standardization, aggregated data access and shared

processes

Enhancing internal business process

efficiencies by hosting shared services on internal

DLT platforms

End-customer

Capital Insurer

Broker Reinsurer

End-customer

End-customer

End-customer

Service

Insurance

Service

End-customer

Capital

new player

new player

Incremental efficiency gains

Business model disruption

15

DLT, IoT & MI is accelerating commercial supply chain digitization (e.g. Marine Trade, Trade Finance, Automotive, Food) and generating data at scaleFour quadrants depict differences in nature of data subjects, risk patterns and regulations

Commercial Property

Personal Property

Casualty

Life and Health

Commercial Lines

Property People Liability▪ Asset-centric▪ Lower data regulation▪ End-insured specific risk

events shared through DLT

▪ People-centric▪ High data regulation▪ End-insured specific risk

events hard to access

▪ High-volume▪ New risk patterns discovered

through research▪ High data sensitivity

▪ Low-volume▪ New risk patterns discovered

thru specialty▪ Low data sensitivity

Personal Lines

Urban Air MobilityUrban Air Mobility

Platform Data

Risk Intelligence Cockpit: Example for delivering resilience as a serviceEnrich big data sets with SR risk knowledge in order to power next-generation solutions

16

Resilience

Digital Distribution

Event-driven Risk Servicing

Risk-as-a-Service

Decentralised sources

Data harvesting engine with a repeatable framework that aggregates diverse

external data lakes and enriches with Swiss Re historic risk data to deliver resilient

applications

Risk Intelligence Cockpit

Urban Air Mobility

Centralised sources

Zhuhai /

Legal notice

©2019 Swiss Re. All rights reserved. You are not permitted to create any modifications or derivative works of this presentation or to use it for commercial or other public purposes without the prior written permission of Swiss Re.

The information and opinions contained in the presentation are provided as at the date of the presentation and are subject to change without notice. Although the information used was taken from reliable sources, Swiss Re does not accept any responsibility for the accuracy or comprehensiveness of the details given. All liability for the accuracy and completeness thereof or for any damage or loss resulting from the use of the information contained in this presentation is expressly excluded. Under no circumstances shall Swiss Re or its Group companies be liable for any financial or consequential loss relating to this presentation.