what is gst ?

TRANSCRIPT

- Infosoft Technologies

Salient Features

• Registration threshold proposed - Rs 4 Lakh for NE states + Sikkim & Rs 9 Lakh for Rest of India

• liability to pay tax after crossing the threshold of Rs 5 Lakh for NE states + Sikkim and Rs 10 Lakhs for Rest of India

• 7-8 million businesses are likely to be registered under GST.

• Small dealers with turnover below Rs 50 Lakh have the option of adopting the Composition scheme and pay flat ~1 to 4% tax on turnover

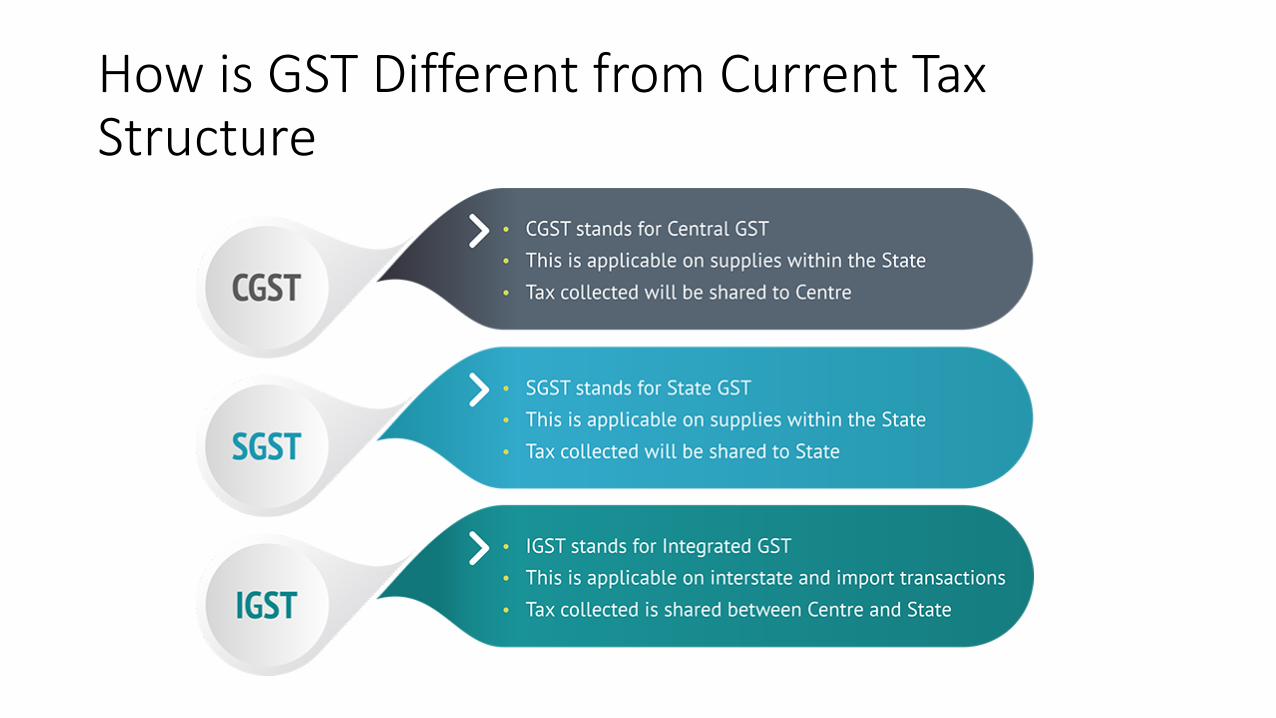

How is GST Different from Current Tax Structure

Taxes subsumed under GST

Dual GST

• Dual GST has been chosen as the apt model wherein tax would be jointly levied by both Centre and the states on supply of goods and services.• SGST: State GST• CGST: Central GST• IGST: Integrated GST

• On intra-state transactions CGST+SGST will be applicable and on Interstate transactions, IGST will be applicable.

GST Rates

• There are likely to be 3 sets of rates as below:

• Merit Rate

• Standard Rate

• De-Merit Rate

• There is also likely to be a lower rate for precious metals and zero-rate for essential goods.

Taxes Subsumed:

Subsumed in GST Not subsumed in GSTCentral Excise Basic Customs dutyService Tax Alcohol for human consumptionVAT / Sales Tax Petrol / Diesel / Aviation fuel / Natural Gas*Entertainment Tax Stamp duty and Property taxLuxury Tax Toll taxTaxes on lottery

Electricity DutyOctroi and Entry TaxPurchase tax

*To be included only at a later notified date

ITC Utilization

Input Tax Credit Set-off against liability of

CGST CGST and IGST (in that order)

SGST SGST and IGST (in that order)

IGST IGST, CGST, SGST (in that order)

Please note that CGST and SGST cannot be set off against one another

IT Infrastructure

• Goods and Service Tax Network or GSTN is a Not for Profit Sec 25/Section 8 company incorporated under the public-private partnership(private companies, central and state government are the stakeholders) to roll out the IT backbone (Backend and Frontend) and portal for meeting all the e-filing requirements of GST. This would be the nodal agency which would control all the processes, forms, and also the data of all the trade that happens in the country

GST Council

• The council to be formed within 60 days of getting presidential assent, would consist of 2/3rd representation of states and 1/3rd representation of Centre. The GST Council will take all decisions regarding tax rates, dispute resolution, exemptions and so on. Recommendations of the GST Council (75% votes) will be binding on the Centre and states.

Business Process

• Existing dealers would be auto-migrated and given a 15-digit PAN based GSTIN with following structure.

State Code PANEntity Code

BlankCheck Digit

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

• The entity code will be applicable for taxpayers having multiple business verticals within the state.

Returns:The GST regime introduces the following changes:• The GST regime requires all businesses to mandatorily file monthly returns along with the requisite

quarterly or annual returns. Even businesses which now file returns quarterly or half-yearly (such as returns for service tax etc.) now need to file returns every month.

• There will now be ‘3 compliance events every month’ compared to 1 event today. This means, businesses will now need to comply with the requirements of filing GSTR- 1, GSTR-2 and GSTR- 3 (as mentioned below) as against filing 1 return today.

• The first compliance event (filing GSTR-1) has a due date of 10th of the subsequent month as against the deadline of 20th in the current VAT regime.

• Composition scheme will no longer be a favorable option since returns need to be filed quarterly and the details in those returns need to be filed relating to purchases, though sales would be lump sum like earlier. Another big deterrent in the scheme would be non availability of input credit to the chain below which would increase the selling price for the composite dealers. This would mean that businesses would reduce their purchases from these dealers.

• Regular Dealer: Monthly filing• GSTR-1: Upload all sale invoices (By 10th)• GSTR-2: Accept the auto-populated counterparty sales as your purchase, and add

any missing purchases (By 15th)• GSTR-3: Submit the auto-populated GSTR-3 by 20th

• Composition Dealer: Quarterly filing• GSTR-4: Submit by 18th after quarter-end• GSTR-8: Annual Return for both Regular and Composition by 31st Dec of

subsequent year.

Payments & Refunds

• Mandatory e-payment for amount > Rs 10,000

• Online: NEFT/RTGS/IMPS

• Offline: Cash/Cheque/DD/NEFT/RTGS etc.

• Challan is auto-populated, and can be downloaded

• Refund process will be automated and wherever applicable 80% refund will be granted provisionally when applied without scrutiny.

Major Impact Areas• Adoption of Technology is imperative: Unlike earlier, paper filing will not be an option.

• Access to Pan-India market: Intra-state and interstate trades would become tax neutral, and the whole of India will open up as a market for both sourcing vendors and customers without hassles of compliance.

• Cash flow planning: Input tax credit on purchase will be provided only provisionally during return filing, and will be confirmed only after corresponding sale has been uploaded and after the liability is discharged by supplier. Hence, cash flows WILL get impacted in case of mismatch.

• Easier Compliance: GST requires businesses to provide granular level of data (invoice-wise), that needs to be reported with HSN codes. The good news is that compliance is going to get easier with GST replacing most of the prevalent indirect taxes and with the support of technology.

• Branch / Supply chain re-engineering: Businesses having multi-state presence due to tax considerations (to avail concessional CST rate) need to re-plan their warehouse and branch networks and locate them nearer to markets rather than state-wise.

• Pricing strategy: Due to elimination of cascading effect, prices of products are likely to come down.

• Re-negotiate contracts: Work contracts and other multi-year supply deals have to be renegotiated to absorb GST rates.

What Next?

• With the passage of the 122nd constitutional Amendment Bill in RajyaSabha, the immediate next steps are:

• As this is a constitutional amendment, a minimum of 15 state assemblies also need to ratify the bill.

• Presidential assent to the bill and formation of GST council within the next 60 days from date of obtaining assent, is required.

• Passing of CGST and IGST Bills (probably as Money Bill) in winter session of parliament and of SGST Bill in 29 state assemblies.

• Rollout of GST Network by January 2017.• The tasks look daunting, yet achievable.

What next for all of us

• With 1st of April 2017 being the likely date for launch of GST, the taxpayer needs to take several preparatory steps in this direction. The transition will be the key for having a clean opening balance to start with.

• Input tax credit (in returns/inputs/capital goods) from current regime(CENVAT, VAT) will be carried forward to GST(CGST, SGST). Hence, it is imperative to keep the books updated. It helps companies during assessment as only at that time the number will get picked up and if trail/clarity is not available businesses will go through a lot of financial and non-financial pain.

• All the accounting and party masters in ERP need to be kept updated with statutory details filled-in, such that transition to GST is smooth.

• As always, Tally has been the pioneer in assisting businesses with understanding and adopting statutory changes. The greatly simplified solution in Tally.ERP 9 will ensure quick migration and easy handling of statutory requirements of GST.

• This note has been prepared with publicly available information, however the actual GST rates and business process are likely to undergo significant changes by the time of rollout.

Thank You..

+91 937 344 3800

+91 937 244 3800