what is the financial justification for your gift planning program? richard w. lawrence executive...

TRANSCRIPT

What is the Financial Justification for Your

Gift Planning Program?

Richard W. Lawrence

Executive Vice President & Chief Operating Officer

Kristen L. Dugdale

Vice President, Gift Planning

Current Environment

Budgets are tight and likely to remain so

Pressure to raise current funds

Deferred gift activities might be “deferred”

Gift planning directors might have to defend program budget

Gift Planning’s Measurement Problem

Hard to quantify means it is hard to manage Other development efforts are more quantifiable “Dollars in the door” seems more tangible—easier to

measure Yet, significant dollars come from planned gifts,

especially bequests

What Might Leadership Be Thinking?

How do I allocate development resources? How integral is the gift planning staff to the success of

outright and campaign giving? What is the cost/benefit relationship of deferred gifts? If we cut X in annual giving or major gifts, we know the

likely result. If we cut gift planning, there is no immediate loss, right?

Director of Gift Planning Challenges

You might be fortunate to have leadership that strongly supports gift planning

Current environment will bring scrutiny How do you advocate to keep or to augment resources?

Qualitative case Quantitative case

Do you speak your leadership’s “language”?

Case Study

University of Colorado Foundation

A For-Profit Lens On a Non-Profit Activity

What Is Our Cost to Raise a Dollar?

Efficiency of Various Business Units

Simple Formulas Don’t Work for Gift Planning

The Planned Gift Measurement Problem

Most planned gifts have an associated time deferral element

Most planned gifts have undetermined gift value Many planned gifts are revocable

We gain the greatest insight by linking today’s gift planning activities to some measure of the

value that they create

We gain the greatest insight by linking today’s gift planning activities to some measure of the

value that they create

Present Value Formula

1

(1 + r ) n( )P

Present Value of $100,000

Rate of Discount In 5 Years In 25 Years

5% $78,370 $29,533

7% $71,327 $18,426

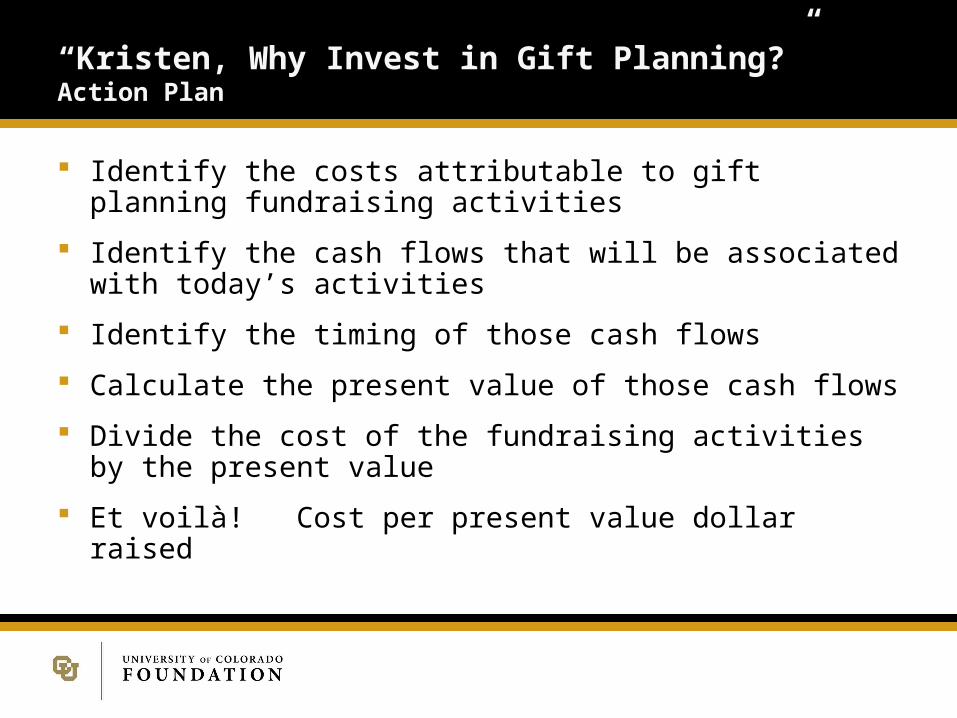

“Kristen, Why Invest in Gift Planning?”Action Plan

Identify the costs attributable to gift planning fundraising activities

Identify the cash flows that will be associated with today’s activities

Identify the timing of those cash flows

Calculate the present value of those cash flows

Divide the cost of the fundraising activities by the present value

Et voilà! Cost per present value dollar raised

The Process

Set the broad gift planning fundraising goal Divide the goal into gift types For each gift type, determine assumptions for

horizon and investment return Calculate a future value for each type and discount

it to present value Determine the costs associated with raising the gifts

and divide them by the present values Et voilà!

The Numerous Variables

Goal Split of the Gift Types Horizon Assumptions Investment & Payout Assumptions Discount Rate

Set the Goal

Our gift planning goal for Fiscal Year 2008 was $15.6 million in face value terms (revocable and irrevocable gifts)

The goal was based generally on an average of the amounts raised over the previous 10 years

The goal did not include realized bequest expectancies or life income gift maturities

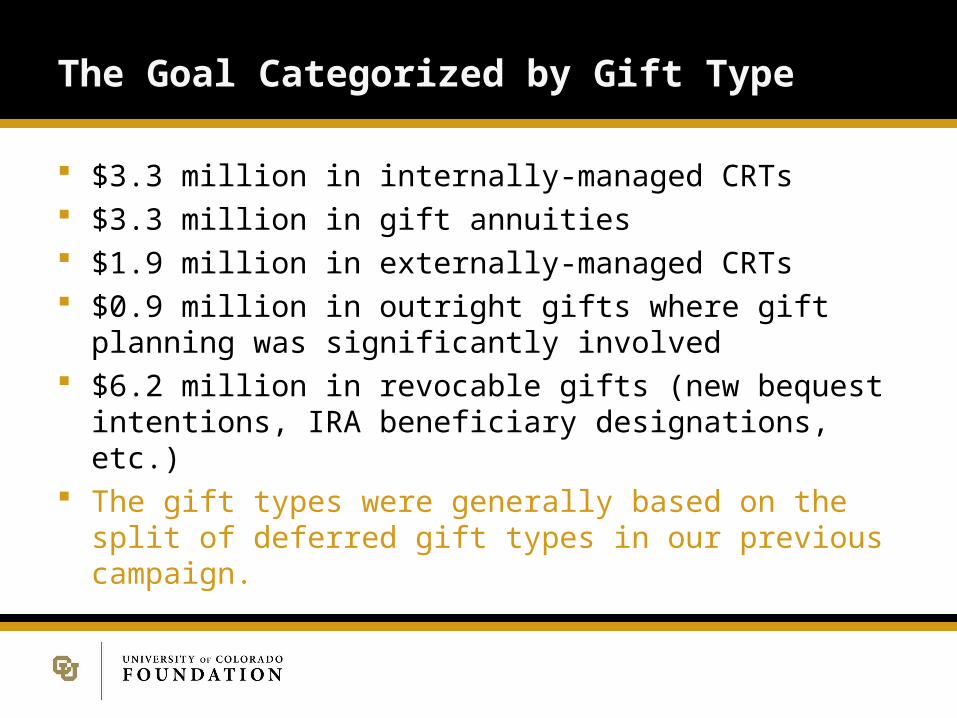

The Goal Categorized by Gift Type

$3.3 million in internally-managed CRTs $3.3 million in gift annuities $1.9 million in externally-managed CRTs $0.9 million in outright gifts where gift planning was

significantly involved $6.2 million in revocable gifts (new bequest intentions,

IRA beneficiary designations, etc.) The gift types were generally based on the split of

deferred gift types in our previous campaign.

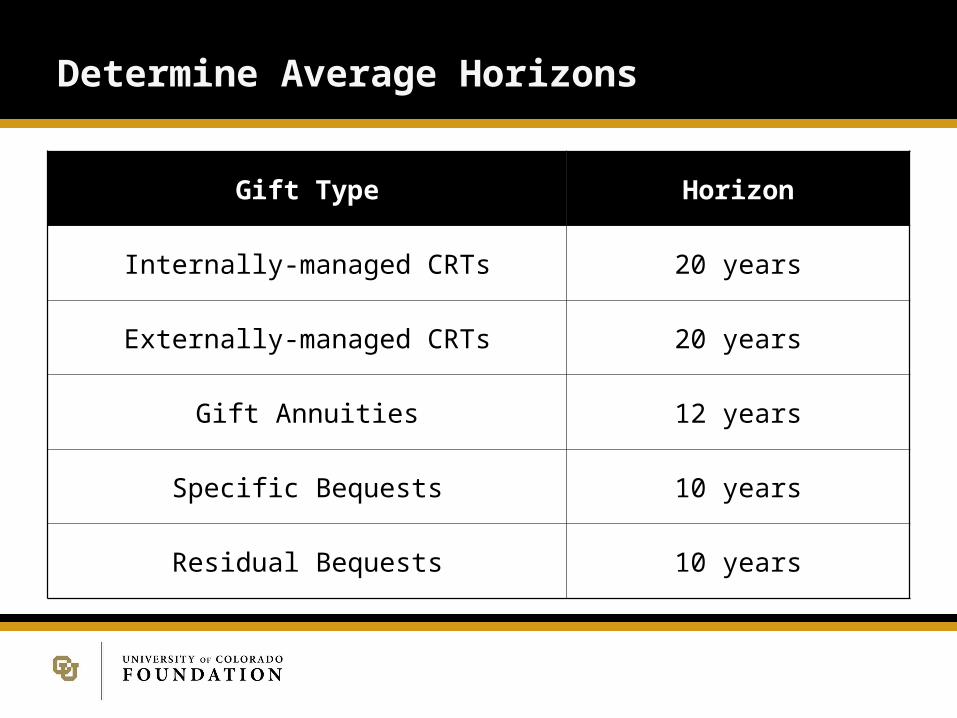

Determine Average Horizons

Gift Type Horizon

Internally-managed CRTs 20 years

Externally-managed CRTs 20 years

Gift Annuities 12 years

Specific Bequests 10 years

Residual Bequests 10 years

Horizon assumptions predicated on facts

Trust & Annuity horizon assumptions were determined by averaging the remaining horizons of every trust and/or annuity in our current program (15 years for trusts, 12 years for annuities).

Is the horizon to short, as we did not look at original gift dates? Is the horizon to long, as we did not allow for the possibility of earlier than

expected terminations? Because of these variables, we added 5 years to the assumption for trusts &

3 years to gift annuities Horizons = 20 Years for trusts; 15 years for annuities. In the case of gift annuities, we also considered the ACGA suggested rate

for a 75 year-old.

Horizon assumptions for bequests

Made an assumption that specific & residual bequests would be split 50/50.

Applied an annual total return to residual bequests of 3%.

Compared the gift date of recorded bequests in our system to the realization date (if any), and averaged all for a period of 4 years.

Conservatively added to that term by using 10 years.

Chose not to discount bequests based on their revocability.

NCPG’s Survey of Donors conducted in 1992, and updated in 2000.

92% of donors did not take charity out of the will. 86% did not change the amount to charity. Of those who did change the amount, 1/10 did so to

increase the amount. Only 1/100 decreased the amount & others made

changes for “mechanical reasons”. Results reaffirmed in 2000 survey.

Determine Payout Rates and Projected Investment Returns

Gift Type Payout RateInvestment

Return

Internally-managed CRTs 7% 9%

Externally-managed CRTs 7% 9%

Gift Annuities 7.1% 9%

Specific Bequests n/a n/a

Residual Bequests n/a 3%

Determine a Discount Rate

Should we use the endowment rate of return to discount the value of a future gift to the university?

Or use the Higher Education Price Index?

Or pick a rate in the middle?

We decided to use a 7% discount rateWe decided to use a 7% discount rate

Calculate the Present Value of Gifts

Grow each gift type out to its estimated future value (net of payments and costs)

Apply the discount rate to determine the net present value

Add the net present values across gift types

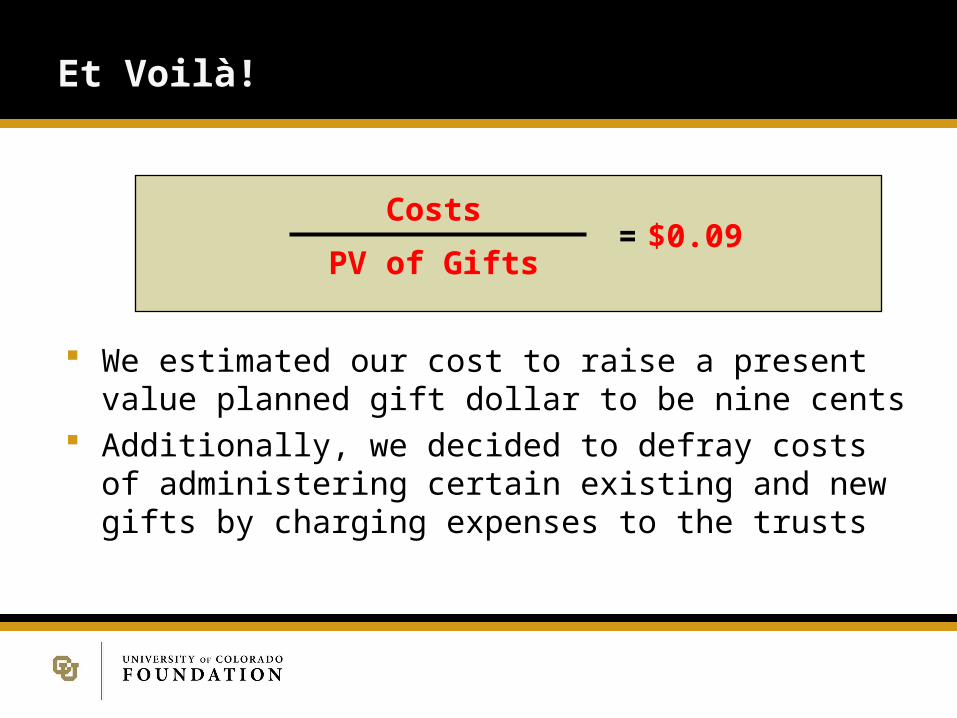

Costs

PV of Gifts= Cost per PV $ Raised

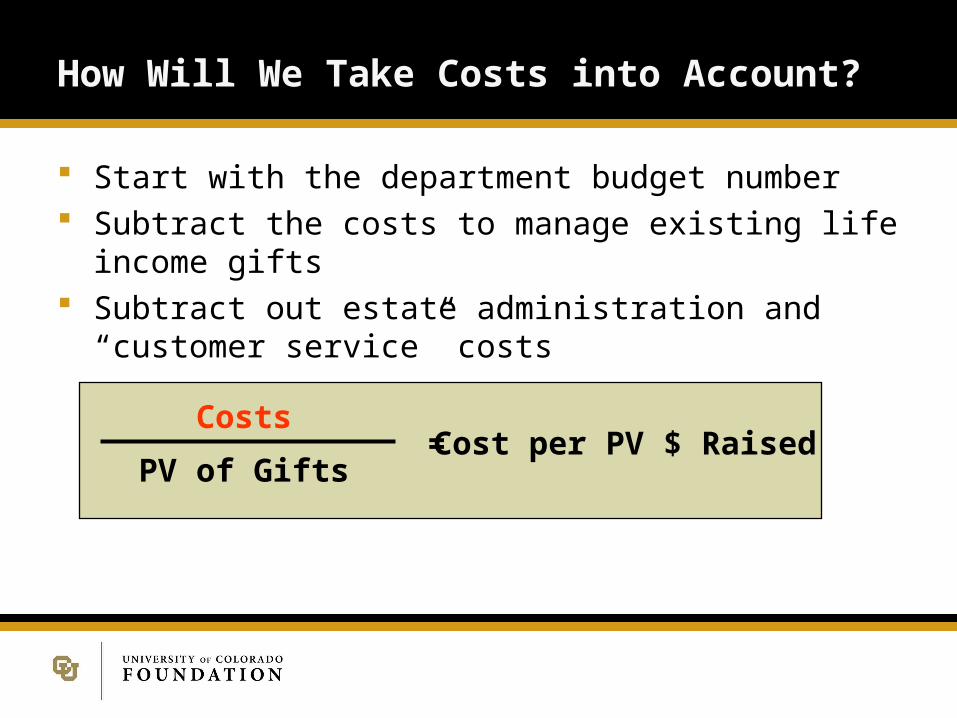

How Will We Take Costs into Account?

Start with the department budget number Subtract the costs to manage existing life income gifts Subtract out estate administration and “customer

service” costs

Costs

PV of Gifts= Cost per PV $ Raised

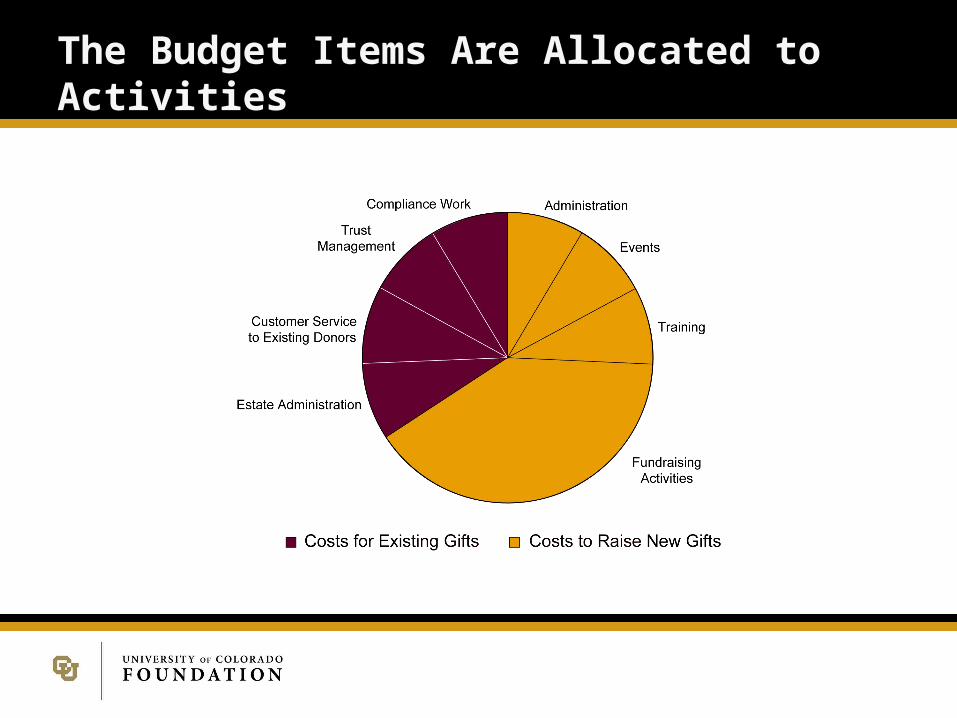

Gift Planning Budget Items

Salaries and benefits Promotional activities and events Travel Gift management fees not charged to trusts Legal and compliance Professional development Overhead and other operating costs

The Budget Items Are Allocated to Activities

Et Voilà!

We estimated our cost to raise a present value planned gift dollar to be nine cents

Additionally, we decided to defray costs of administering certain existing and new gifts by charging expenses to the trusts

Costs

PV of Gifts= $0.09

Dollars Raised by Gift Type(Millions of Present Value Dollars)

Fiscal Year ‘07Plan Actual

Fiscal Year ‘08Plan Actual

Fiscal Year ‘09Plan Actual

Fiscal Year ‘10Plan as of 12/31

LIGs(internal)

$2.8 $0.5 $2.8 $14.8 $2.8 $0.1 $2.8 $0.02

LIGs(external)

0.6 0.1 0.6 0.1 0.6 0.8 0.6 0

Outright & IRA

0.9 2.0 0.9 4.9 0.9 7.9 0.9 .98

RevocableIntentions

3.7 7.0 3.7 1.7 3.7 1.3 3.7 7.9

Total $8.0 $9.6 $8.0 $21.4 $8.0 $11.8 $8.0 $9.0

Cost per PV Raised $0.06 $0.03 $0.03 $0.06

Some Observations

Consistently exceeded goals Actual cost to raise a dollar beat estimates Different “winning” category every year Revocable category is understated Some assumptions were inaccurate Looking forward

If we add costs will we add revenue? How can we get more cost-efficient? Should we focus on older donors (higher PV)?

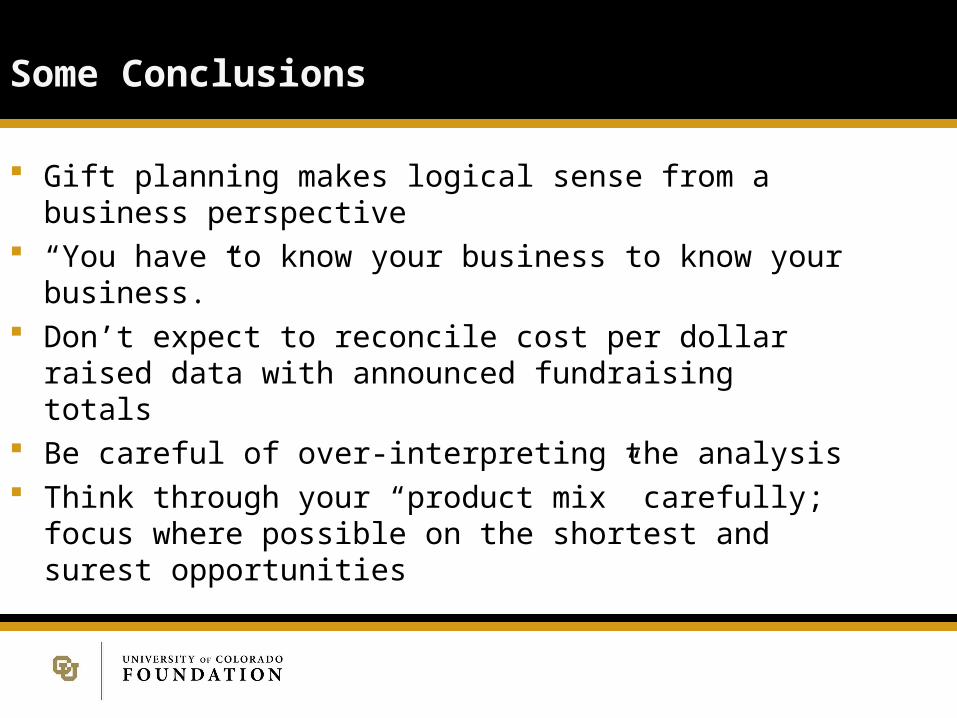

Some Conclusions

Gift planning makes logical sense from a business perspective

“You have to know your business to know your business.”

Don’t expect to reconcile cost per dollar raised data with announced fundraising totals

Be careful of over-interpreting the analysis Think through your “product mix” carefully; focus where

possible on the shortest and surest opportunities

Other ways to measure a program

Evaluate based on the effectiveness or charitable impact the charity makes

Marginal costs/Diminishing Returns?

Discussion

What questions do you have? Has your VP of Development or your CFO asked you to

justify the value of your gift planning program? How have you responded? Have you used other

methods to make the case?

The End