what is this thing called internal controls? review of concepts value of internal controls

TRANSCRIPT

What is this thing called Internal Controls?Review of ConceptsValue of Internal Controls

Internal Controls

Internal controls are a system consisting of specific policies and procedures designed to provide management with reasonable assurance that the goals and objectives it believes important to the entity will be met.

Why have Internal Controls?

Promote operational efficiency and effectivenessProvide reliable financial informationSafeguard assets and recordsEncourage adherence to prescribed policiesComply with regulatory agencies

Basic Concepts of Internal Controls

Management, not auditors, must establish and maintain the entity’s controlsInternal controls structure should provide reasonable assurance that financial reports are correctly statedNo system can be regarded as completely effectiveShould be applied to manual and computerized systems

Value of Internal Controls

Transactions are:validproperty authorizedRecordedproperly valuedProperly classifiedTimelyReconciled to subsidiary records

Control Environment Consists of:

Management philosophy and operating style

Tone at the top

Organization structureSeparation of dutiesFiscal officer reporting lines

Assignment of authority and responsibility

Does everyone understand their role?Responsibility without authority

Control Environment Consists of:Competent, knowledgeable personnel

Personnel policies and proceduresTraining and development

Communication and information systemsInternal audit function

Either in-source or outsource

External influences ComplianceExternal auditors

Design a Control System

Identify RISKS in your environmentMission - ComplianceTransactional - Assets

Identify control pointsAnalyze potential EXPOSURESDesign system to mitigate RISKS

Internal Control Procedures

PersonnelProper procedures for authorizationAdequate separation of dutiesAdequate documents and recordsPhysical control over assets and recordsIndependent checks on performances

Other Elements to Remember:

Consistency of policy compliance Coordination in a decentralized environmentCompleteness and relevancy of policiesIssue escalation and resolution processAccountabilityFlow of financial information

Other Elements to Remember – con’t

Linkages between technology, process and organizational structureAlignment of University objectives, risks and controlsEarly warning systemsTraining and other HR mechanismsTools and techniques for monitoring

Key Concepts to Retain

Internal control is a process. It is a means to an end, not an end itself.Internal control is affected by people. It is not just manuals and policies, but the people at all levels of the organization.Internal control can be expected to provide reasonable assurance, not absolute assurance, to an entities management or board.

Front Page Test

Ask yourself, and ask your boss, how would you feel if this decision were displayed on the front page of the newspaper?

This can be a very effective guage for appropriateness

Source: Protiviti KnowledgeLeader (www.knowledgeleader.com)

Assessing Risks and Internal Controls

Your Role as Process Owner

General Expectations

• Acknowledge your responsibility for the design, implementation and maintenance of the control structure within your business processes

• Contribute direction to identify, prioritize and review risks and controls

• Remove obstacles for compliance; remedy control deficiencies

• Continue or begin a program of self-assessment and testing to monitor the controls within your processes

• Quarterly, - confirm key controls are implemented and effective- maintain documentation to support this assessment - sign backup certifications supporting overall Section 302 and 404 assertions

Immediate Action Items

• Educate your personnel about these requirements and this effort

• Reinforce internal focus on controls within your area

• Surface any risks, concerns or issues promptly to allow adequate attention for correction (don’t wait for an audit!)

• Fix control gaps as soon as possible

For all businesses there are risks that exist and that need to be identified and addressed in order to prevent or minimize losses. Risk is the threat that an event, action, or non-action will adversely affect an organization’s ability to achieve its business objectives and execute its strategies successfully. Risk is measured in terms of consequences and likelihood. The following process is used for assessing risks: identifying risks, sourcing risks and measuring risks. Overall, you should focus on the high risks affecting your operations.

What are Risks?

Identifying Risks

Sourcing Business Risks

Sourcing Risks

PrioritizingRisks

Considerations

• Evaluate the nature and types of errors and omissions that could occur, i.e., “what can go wrong”

• Consider significant risks (errors and omissions) that are common in the industry or have been experienced in prior years

• Information Technology risks (i.e. - access, backups, security, data integrity)

• Volume, size, complexity and homogeneity of the individual transactions processed through a given account or group of accounts (revenue, receivables)

• Susceptibility to error or omission as well as manipulation or loss

• Robustness versus subjectiveness of the processes for determining significant estimates

• Extent of change in the business and its expected effect

• Other risks extending beyond potential material errors or omissions in the financial statements

Risk Considerations

For all significant processes identify points within the flow of transactions or process stream where there can be failures to achieve the following assertions:Assertion Description

Authorization Management has defined and communicated criteria for recognizing economic events and authorizing transactions.

Completeness and Accuracy

All transactions and other events and circumstances that occurred during a specific period and should have been recognized in that period, have, in fact, been recorded or considered. Therefore, there are no unrecorded assets, liabilities or transactions and no omitted disclosures.

All, and only economic events meeting management’s criteria are converted to transactions accurately and accepted for processing on a timely basis. All accepted transactions are processed accurately in accordance with management’s policies and on a timely basis. Events affecting more than one system result in transactions that are reflected by each system in the same accounting period.

Recorded transactions represented economic events that actually occurred during a stated period of time.

Evaluation of Balances Assets, liabilities, revenues and expenses are recorded at appropriate amounts in accordance with relevant accounting principles.

Report and database contents are periodically evaluated. Evaluation involves judgmental determinations of value. Provide reasonable assurance that reported information can be reconciled with reality.

Assertions

Presentation, Classification and Disclosure

The captions, disclosures and other items in the financial statements are properly described and classified as well as fairly presented in conformity with generally accepted accounting principles.

Access to Assets Physical safeguards should permit access to assets only in accordance with management’s authorization.

Substantiation of Balances

Report and database contents should be periodically substantiated. Substantiation is an independent check of processing results, and is most effective if completed in an environment in which there is segregation of incompatible duties. There is reasonable assurance that reported information can be reconciled with reality.

Rights and Obligations Assets and liabilities reported on the balance sheet are bona fide rights and obligations of the entity as of that point in time.

Management should clearly identify the personnel who have primary custodial responsibility for each category of assets, critical forms and records, processing areas and processing procedures. To the extent possible, responsibility for the physical custody of an asset should be vested in employees who have no responsibility for, and are denied access to, accounting for the asset and vice versa.

Assertions

Assertions (Continued)

Assertion Description

What are Internal Controls?

Management must control identified risks to help the Company:

• achieve its performance and profitability targets,• prevent loss of resources,• ensure reliable financial reporting, and• ensure compliance with laws and regulations, avoiding damage to its

reputation and other consequences. In summary, internal controls can help our company get where it wants to go, and avoid pitfalls and surprises along the way. DEFINITION OF INTERNAL CONTROL

Internal control is a process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories:

• Effectiveness and efficiency of operations• Reliability of financial reporting• Compliance with applicable laws and regulations

Internal Control Myths and Facts

MYTHS:

Internal control starts with a strong set of policies and procedures.

Internal control: That’s why we have internal auditors!

Internal control is a finance thing.

Internal controls are essentially negative, like a list of “thou-shalt-nots.”

Internal controls take time away from our core activities of making products, selling, and serving customers.

FACTS:

Internal control starts with a strong control environment.

While internal auditors play a key role in the system of control, management is the primary owner of internal control.

Internal control is integral to every aspect of business.

Internal control makes the right things happen the first time.

Internal controls should be built “into,” not “onto” business processes.

Source: Institute of Internal Auditors, 2003

Internal Control Structure

Monitoring:• Monthly reviews of performance

reports• Internal audit function

Control Activities:• Purchasing limits• Approvals• Security• Reconciliations• Specific policies

Risk Assessment:• Monthly Risk Control

meetings• Internal audit risk

assessment

Control Environment:

• Tone from the top• Corporate Policies• Organizational

authority

Information & Communication:

• Vision and values survey• Issue resolution calls• Reporting• Corporate communications

(e-mail, meetings)

In many cases, you perform controls and interact with the control structure every day, perhaps without even realizing it.

An internal control structure is simply a different way of viewing the business – a perspective that focuses on doing the right things in the right way.

MONITORING

INFORMATION AND COMMUNICATION

CONTROL ACTIVITIES

RISK ASSESSMENT

CONTROL ENVIRONMENT

Control definition reflects certain fundamental concepts:

Internal control is a process. It's a means to an end, not an end in itself.

Internal control is effected by people. It's not merely policy manuals and forms, but people at every level of an organization.

Internal control can be expected to provide only reasonable assurance, not absolute assurance, to an entity's management and board.Objectives of Internal Control

Internal controls are established to further strengthen:

The reliability and integrity of information. Compliance with policies, plans, procedures, laws and regulations. The safeguarding of assets. The economical and efficient use of resources. The accomplishment of established objectives and goals for operations or

programs.

Concepts and Objectives

Redefining the control focus The new approach to controlling business risks may be characterized by the “new rules” of “prevent and monitor” and “build in quality” as opposed to the “old rules” of “detect and correct” and “inspect in quality.” This means a paradigm shift in the traditional viewpoint of control as illustrated in the following table:

Old Paradigm New Paradigm

Only AUDITORS and TREASURY are concerned about risks and controls

EVERYONE, including operations, is concerned about managing business risks

FRAGMENTATION – Every function and department does its own thing (“SILO MANAGEMENT”)

Business risk assessment and control are FOCUSED and COORDINATED with senior level OVERSIGHT

NO BUSINESS RISK CONTROL POLICY

FORMAL BUSINESS RISK CONTROL POLICY approved by management and the board

INSPECT for and DETECT business risk and REACT to it

ANTICIPATE and PREVENT business risk at the source and MONITOR business risk controls continuously

Ineffective PEOPLE are the primary source of business risk

Ineffective PROCESSES are the primary source of business risk

Control Focus

CONTROL TECHNIQUES Prevention techniques are designed to provide reasonable assurance that only valid transactions are recognized, approved and submitted for processing. Therefore, many of the preventive techniques are applied before the processing activity occurs. In most situations, preventive techniques are likely to be more effective in a strong control environment, when management authorization criteria are well-defined and properly communicated.

Control type definitions:Preventive - ManualPreventive - System

Examples of preventive controls include: • Segregation of duties (Preventive-Manual)• Business systems integrity and continuity controls, e.g., application design

standards, change controls, security controls, systems backup and recovery (Preventive – System)

• Physical safeguard and access restriction controls (human, financial, physical and information assets) (Preventive-Manual)

• Effective planning/budgeting process (Preventive-Manual)• Effective "whistle blowing" processes (Preventive-Manual)

Control Techniques

CONTROL TYPES Detection techniques are designed to provide reasonable assurance that errors and irregularities are discovered and corrected on a timely basis. Detection techniques normally are performed after processing has been completed. They are particularly important in an environment that has relatively weak preventive techniques. That is, when front-end approval and processing techniques do not provide reasonable assurance that unacceptable transactions are prevented from being processed or do not assure that all approved transactions are processed accurately. In this case, after-the-fact techniques become more important in detecting and correcting processing errors. Control type definitions:Detective - ManualDetective - System

Examples of detection techniques include:• Reconciliation of batch balance reports to control logs maintained by originating

departments. (Detective – Manual)• Reconciliation of cycle inventory counts with perpetual records. (Detective –

Manual)• Review and approval of reference file maintenance (“was-is”) reports. (Detective

– Manual)• Comparison of reported results with plans and budgets. (Detective – Manual)• Reconciliation of subsidiary ledger balances with the general ledger. (Detective –

Manual)• Reconciliation of interface amounts exiting one system and entering another.

(Detective – System)• Review of on-line access and transaction logs. (Detective – System)

Control Techniques

Conclusion Why all this trouble?

• Compliance with a very visible law

• Puts teeth into the value statement, “Do it right the first time”

• Additional comfort and “tightness” that the company is doing the right things and communicating the right information internally, to the auditors and to the public

• Over time, the metrics that evolve to monitor the control areas can provide insight for key business decisions

• Documentation will provide communication tool with management and improve ability to train and share information

What happens if we don’t do this?• Less formal control structures leave room for risks to become real issues

• External Auditor may not sign their attestation of our control structure

• Potential SEC investigation

• Investor, lender and customer confidence will be further weakened, affecting stock price and available financing

What are the next steps?• Continue communication

• Validation of process documentation

• Identification and sourcing of risks and controls

Appendix - COSO Components Defined

The Committee of Sponsoring Organizations of the Treadway Commission (COSO), was formed in 1985 to improve the quality of financial reporting through business ethics, effective internal controls and corporate governance. Based on these principles, they developed and published the COSO framework in 1992 as a foundation for establishing internal control systems and determining their effectiveness.

Control Environment• The control environment sets the tone of an organization, influencing the control

consciousness of its people. It is the foundation for all other components of internal control, providing discipline and structure. Control environment factors include the integrity, ethical values and competence of the entity's people; management's philosophy and operating style; the way management assigns authority and responsibility and organizes and develops its people; and the attention and direction provided by the board of directors.

Risk Assessment• Every entity faces a variety of risks from external and internal sources that must be

assessed. A precondition to risk assessment is establishment of objectives, linked at different levels and internally consistent. Risk assessment is the identification and analysis of relevant risks to achievement of the objectives, forming a basis for determining how the risks should be managed. Because economic, industry, regulatory and operating conditions will continue to change, mechanisms are needed to identify and deal with the special risks associated with change.

Control Activities Control activities are the policies and procedures that help ensure management directives

are carried out. They help ensure that necessary actions are taken to address risks to achievement of the entity's objectives. Control activities occur throughout the organization, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications, reconciliations, reviews of operating performance, security of assets and segregation of duties.

Appendix - COSO Components Defined (cont.)

Information and Communication• Pertinent information must be identified, captured and communicated in a form and

timeframe that enables people to carry out their responsibilities. Information systems produce reports, containing operational, financial and compliance-related information, that make it possible to run and control the business. They deal not only with internally generated data, but also information about external events, activities and conditions necessary to informed business decision-making and external reporting. Effective communication also must occur in a broader sense, flowing down, across and up the organization. All personnel must receive a clear message from top management that control responsibilities must be taken seriously. They must understand their own role in the internal control system, as well as how individual activities relate to the work of others. They must have a means of communicating significant information upstream. There also needs to be effective communication with external parties, such as customers, suppliers, regulators and shareholders.

Monitoring• Internal control systems need to be monitored -- a process that assesses the quality of

the system's performance over time. This is accomplished through ongoing monitoring activities, separate evaluations or a combination of the two. Ongoing monitoring occurs in the course of operations. It includes regular management and supervisory activities, and other actions personnel take in performing their duties. The scope and frequency of separate evaluations will depend primarily on an assessment of risks and the effectiveness of ongoing monitoring procedures. Internal control deficiencies should be reported upstream, with serious matters reported to top management and the board.

Applying COSO’s

Enterprise Risk Management —

Integrated FrameworkSeptember 29, 2004

Today’s organizations are concerned about:

Risk ManagementGovernanceControlAssurance (and Consulting)

ERM Defined:“… a process, effected by an entity's board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risks to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.”

Source: COSO Enterprise Risk Management – Integrated Framework. 2004. COSO.

Why ERM Is Important Underlying principles:

• Every entity, whether for-profit or not, exists to realize value for its stakeholders.

• Value is created, preserved, or eroded by management decisions in all activities, from setting strategy to operating the enterprise day-to-day.

Why ERM Is Important

ERM supports value creation by enabling management to:

• Deal effectively with potential future events that create uncertainty.

• Respond in a manner that reduces the likelihood of downside outcomes and increases the upside.

This COSO ERM framework defines essential components, suggests a common language, and provides clear direction and guidance for enterprise risk management.

Enterprise Risk Management — Integrated Framework

The ERM Framework

Entity objectives can be viewed in the

context of four categories:

• Strategic • Operations• Reporting• Compliance

The ERM Framework

ERM considers activities at all levelsof the organization:

• Enterprise-level• Division or

subsidiary• Business unit

processes

Enterprise risk managementrequires an entity to take a portfolio view of risk.

The ERM Framework

Management considers how individual risks interrelate.

Management develops a portfolio view from two perspectives:

- Business unit level- Entity level

The ERM Framework

The eight componentsof the frameworkare interrelated …

The ERM Framework

Internal EnvironmentEstablishes a philosophy regarding risk management. It recognizes that unexpected as well as expected events may occur.

Establishes the entity’s risk culture.

Considers all other aspects of how the organization’s actions may affect its risk culture.

Objective Setting• Is applied when management considers

risks strategy in the setting of objectives.

• Forms the risk appetite of the entity — a high-level view of how much risk management and the board are willing to accept.

• Risk tolerance, the acceptable level of variation around objectives, is aligned with risk appetite.

Event Identification

• Differentiates risks and opportunities.

• Events that may have a negative impact represent risks.

• Events that may have a positive impact represent natural offsets (opportunities), which management channels back to strategy setting.

Event Identification

• Involves identifying those incidents, occurring internally or externally, that could affect strategy and achievement of objectives.

• Addresses how internal and external factors combine and interact to influence the risk profile.

Risk Assessment• Allows an entity to understand the

extent to which potential events might impact objectives.

• Assesses risks from two perspectives:- Likelihood- Impact

• Is used to assess risks and is normally also used to measure the related objectives.

Risk Assessment

• Employs a combination of both qualitative and quantitative risk assessment methodologies.

• Relates time horizons to objective horizons.

• Assesses risk on both an inherent and a residual basis.

Risk Response• Identifies and evaluates possible

responses to risk.

• Evaluates options in relation to entity’s risk appetite, cost vs. benefit of potential risk responses, and degree to which a response will reduce impact and/or likelihood.

• Selects and executes response based on evaluation of the portfolio of risks and responses.

Control Activities

• Policies and procedures that help ensure that the risk responses, as well as other entity directives, are carried out.

• Occur throughout the organization, at all levels and in all functions.

• Include application and general information technology controls.

Management identifies, captures, and communicates pertinent information in a form and timeframe that enables people to carry out their responsibilities.

Communication occurs in a broader sense, flowing down, across, and up the organization.

Information & Communication

Monitoring

Effectiveness of the other ERM components is monitored through:

• Ongoing monitoring activities.

• Separate evaluations.

• A combination of the two.

Internal Control

A strong system of internalcontrol is essential to effectiveenterprise risk management.

• Expands and elaborates on elements of internal control as set out in COSO’s“control framework.”

• Includes objective setting as a separate component. Objectives are a “prerequisite” for internal control.

• Expands the control framework’s “Financial Reporting” and “Risk Assessment.”

Relationship to Internal Control — Integrated Framework

ERM Roles & Responsibilities

Management

The board of directors Risk officers

Internal auditors

Internal AuditorsPlay an important role in monitoring ERM, but do NOT have primary responsibility for its implementation or maintenance.

Assist management and the board or audit committee in the process by:

- Monitoring - Evaluating- Examining - Reporting

- Recommending improvements

Visit the guidance section of The IIA’s Web site for The IIA’s position paper, “Role of Internal Auditing’s in Enterprise Risk Management.”

Internal Auditors

2010.A1 – The internal audit activity’s plan of engagements should be based on a risk assessment, undertaken at least annually.

2120.A1 – Based on the results of the risk assessment, the internal audit activity should evaluate the adequacy and effectiveness of controls encompassing the organization’s governance, operations, and information systems.

2210.A1 – When planning the engagement, the internal auditor should identify and assess risks relevant to the activity under review. The engagement objectives should reflect the results of the risk assessment.

Standards

1. Organizational design of business2. Establishing an ERM organization3. Performing risk assessments4. Determining overall risk appetite5. Identifying risk responses6. Communication of risk results7. Monitoring8. Oversight & periodic review

by management

Key Implementation Factors

Organizational Design

Strategies of the business

Key business objectives

Related objectives that cascade down the organization from key business objectives

Assignment of responsibilities to organizational elements and leaders (linkage)

Example: LinkageMission – To provide high-quality accessible and affordable community-based health care

Strategic Objective – To be the first or second largest, full-service health care provider in mid-size metropolitan markets

Related Objective – To initiate dialogue with leadership of 10 top under-performing hospitals and negotiate agreements with two this year

Establish ERM

Determine a risk philosophy

Survey risk culture

Consider organizational integrity and ethical values

Decide roles and responsibilities

Example: ERM Organization

ERM Director

ERM Director

Vice President andChief Risk Officer

Vice President andChief Risk Officer

Corporate Credit Risk Manager

Corporate Credit Risk Manager

Insurance Risk Manager

Insurance Risk Manager

ERMManager

ERMManager

ERMManager

ERMManager

StaffStaff StaffStaffStaffStaff

FES Commodity

Risk Mg.Director

FES Commodity

Risk Mg.Director

Risk assessment is the identification and analysis of risks to the achievement of business objectives. It forms a basis for determining how risks should be managed.

Assess Risk

Environmental Risks• Capital Availability• Regulatory, Political, and Legal• Financial Markets and Shareholder Relations

Process Risks• Operations Risk• Empowerment Risk• Information Processing / Technology Risk• Integrity Risk• Financial Risk

Information for Decision Making• Operational Risk• Financial Risk• Strategic Risk

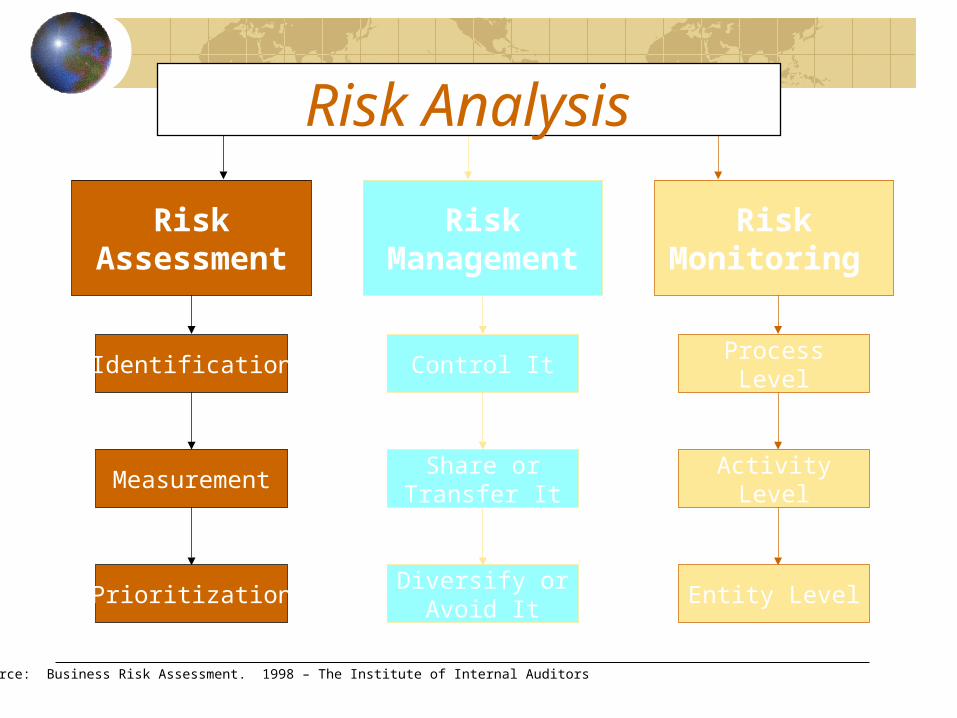

Example: Risk Model

Source: Business Risk Assessment. 1998 – The Institute of Internal Auditors

Control It

Share orTransfer It

Diversify orAvoid It

RiskManagement

ProcessLevel

ActivityLevel

Entity Level

RiskMonitoring

Identification

Measurement

Prioritization

RiskAssessment

Risk Analysis

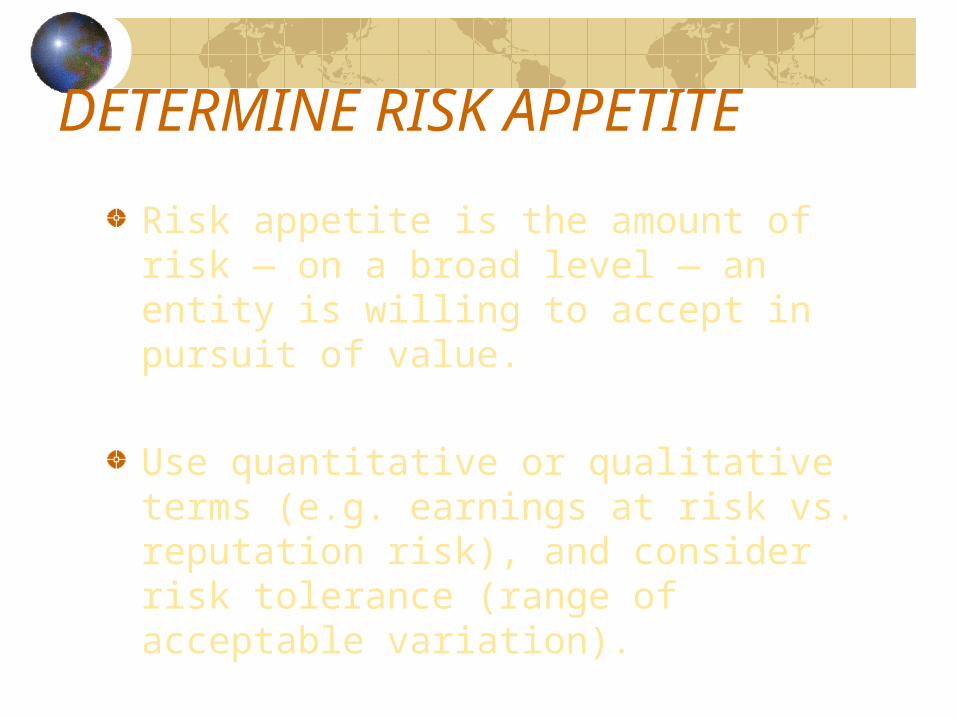

DETERMINE RISK APPETITE

Risk appetite is the amount of risk — on a broad level — an entity is willing to accept in pursuit of value.

Use quantitative or qualitative terms (e.g. earnings at risk vs. reputation risk), and consider risk tolerance (range of acceptable variation).

Key questions:

• What risks will the organization not accept? (e.g. environmental or quality compromises)

• What risks will the organization take on new initiatives? (e.g. new product lines)

• What risks will the organization accept for competing objectives? (e.g. gross profit vs. market share?)

DETERMINE RISK APPETITE

Quantification of risk exposure

Options available:- Accept = monitor- Avoid = eliminate (get out of situation)

- Reduce = institute controls- Share = partner with someone

(e.g. insurance)

Residual risk (unmitigated risk – e.g. shrinkage)

IDENTIFY RISK RESPONSES

Impact vs. Probability

Control

Share Mitigate & Control

Accept

High Risk

Medium Risk

Medium Risk

Low Risk

Low

High

High

IMPACT

PROBABILITY

Low

High

High

IMPACT

PROBABILITY

High Risk

Medium Risk

Medium Risk

Low Risk

Example: Call Center Risk Assessment

• Loss of phones• Loss of computers

• Credit risk• Customer has a long wait• Customer can’t get through• Customer can’t get answers

• Entry errors • Equipment obsolescence• Repeat calls for same problem

• Fraud• Lost transactions• Employee morale

Control Risk Control Objective Activity

Completeness Material Accrual of transaction open liabilities not recorded

Invoices accrued after closing

Issue: Invoices go to field and AP is not aware of liability.

Example: Accounts Payable Process

Dashboard of risks and related responses (visual status of where key risks stand relative to risk tolerances)

Flowcharts of processes with key controls noted

Narratives of business objectives linked to operational risks and responses

List of key risks to be monitored or used

Management understanding of key business risk responsibility and communication of assignments

Communicate Results

Monitor

Collect and display information

Perform analysis- Risks are being properly addressed- Controls are working to mitigate risks

Accountability for risks

Ownership

Updates- Changes in business

objectives- Changes in systems- Changes in processes

Management Oversight & Periodic Review

Internal auditors can add value by:

Reviewing critical control systems and risk management processes.

Performing an effectiveness review of management's risk assessments and the internal controls.

Providing advice in the design and improvement of control systems and risk mitigation strategies.

Implementing a risk-based approach to planning and executing the internal audit process.

Ensuring that internal auditing’s resources are directed at those areas most important to the organization.

Challenging the basis of management’s risk assessments and evaluating the adequacy and effectiveness of risk treatment strategies.

Internal auditors can add value by:

Facilitating ERM workshops.

Defining risk tolerances where none have been identified, based on internal auditing's experience, judgment, and consultation with management.

Internal auditors can add value by:

For more information

On COSO’s

Enterprise Risk Management— Integrated Framework,

visit

www.coso.orgor

www.theiia.org

This presentation

was produced

by

Applying COSO’s

Enterprise Risk Management —

Integrated Framework