what mobile-first consumers want from … · 2017-03-27 · what mobile-first consumers want from...

TRANSCRIPT

1

WHAT MOBILE-FIRST CONSUMERS WANT FROM BRANDS.Findings from Fetch’s Global Mobile Consumer Survey.

2

RESEARCHOBJECTIVES.At Fetch we recognise that the world is going mobile.We understand that globally more and more people now come with a smartphone permanently attached. We know that as people spend more time with their multi-functional mobile devices they are becoming more reliant on them.

But what we did not know with certainty was exactly what proportion of the modern consumer audience currently see themselves as addicted to their devices, how theseconsumers behave and how they want to interact withbrands and businesses via their most personal screen.

We felt that this insight would be helpful for marketers, across industry categories, as they grapple with how to reach and engage these most modern of technology-reliant audiences.

We conducted research in order to answer some key questions:

• How many people now see themselves as addicted to their devices?

• How does their behaviour differ from less addicted mobile phone users?

• What can brands and businesses do to engage and convert these addicted mobile consumers?

3

RESEARCHMETHODOLOGY.

Working with our colleagues within Dentsu Aegis Network, we conducted a wide ranging survey across 8 markets in Europe (UK, Sweden, Germany), North America (both US and Canada) and emerging markets (Brazil, Indonesia and India).

In total we surveyed over 16,000 smartphone owners (18+ years old).Respondent data was weighted* to match age and gender and populationsize of the smartphone market in each country. *Weighted using Pew Research Center Global Attitudes & trends report.

Each respondent was asked to complete a 10 minute online questionnaire to gain insight into:

• Attitudes towards mobile phones.

• Mobile & app usage behaviour.

• Mobile shopping attitudes.

• Attitudes to brand advertising & communications on mobile.

4

RESPONDENTDATA ANALYSIS.We asked questions about mobile phone usage as well as attitudes about the respondents’ mobile device reliance and addiction.We then used a number of analytical techniques (such as factor and cluster analysis) to pull apart three different mobile consumer segments.

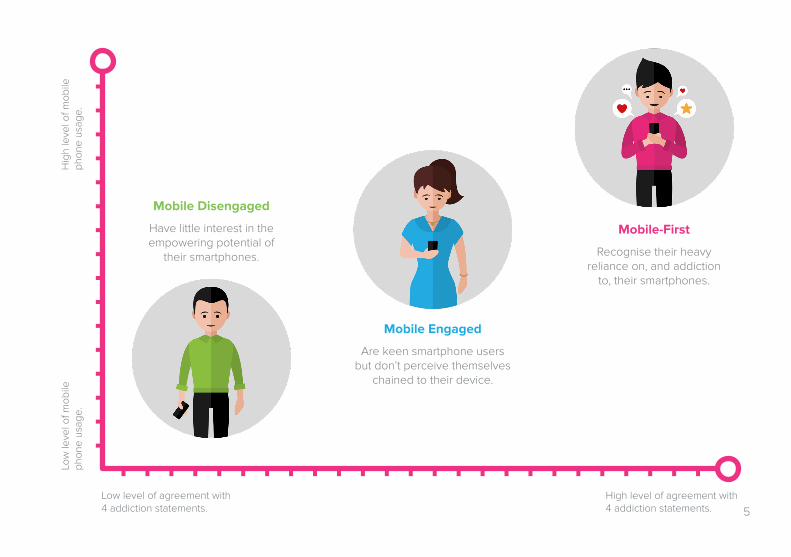

Those with high levels of mobile phone usage and agreementto addiction statements we called Mobile-First.

Those with medium to high levels of mobile phone usage andagreement to addiction statements we called Mobile Engaged.

Those with low levels of mobile phone usage and agreementto addiction statements we called Mobile Disengaged.

5Low level of agreement with 4 addiction statements.

Mobile Disengaged

Have little interest in the empowering potential of

their smartphones.

Mobile Engaged

Are keen smartphone users but don’t perceive themselves

chained to their device.

Mobile-First

Recognise their heavyreliance on, and addiction

to, their smartphones.

Low

leve

l of m

obile

ph

one

usag

e.H

igh

leve

l of m

obile

ph

one

usag

e.

High level of agreement with 4 addiction statements.

6

HOW LARGE IS THE MOBILE-FIRST AUDIENCE?

7

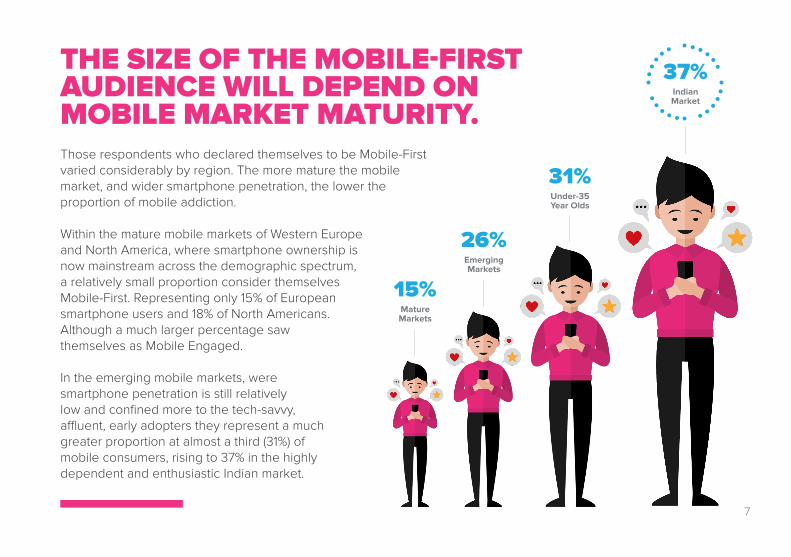

THE SIZE OF THE MOBILE-FIRST AUDIENCE WILL DEPEND ONMOBILE MARKET MATURITY.Those respondents who declared themselves to be Mobile-Firstvaried considerably by region. The more mature the mobilemarket, and wider smartphone penetration, the lower theproportion of mobile addiction.

Within the mature mobile markets of Western Europeand North America, where smartphone ownership isnow mainstream across the demographic spectrum, a relatively small proportion consider themselvesMobile-First. Representing only 15% of Europeansmartphone users and 18% of North Americans.Although a much larger percentage sawthemselves as Mobile Engaged.

In the emerging mobile markets, weresmartphone penetration is still relativelylow and confined more to the tech-savvy,affluent, early adopters they represent a muchgreater proportion at almost a third (31%) ofmobile consumers, rising to 37% in the highlydependent and enthusiastic Indian market.

37%IndianMarket

31%Under-35Year Olds

26%EmergingMarkets

15%MatureMarkets

8

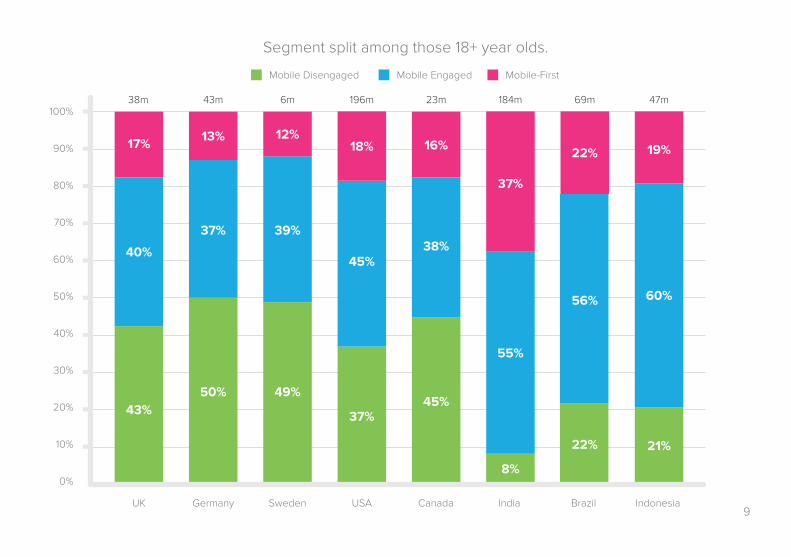

EVERY LOCAL MARKET WILL HAVEA DIFFERENT LEVEL OF MOBILEENGAGEMENT & DEPENDENCY.At a market level we saw that the relationship users have with their smartphones varied considerably.

Within Europe, we found that Germany and Sweden hadconsiderably lower Mobile-First audience penetration than the UK. Almost half of smartphone users in these markets showed little dependency on their multi-functional devices.

The North American markets of US and Canada showeda slightly higher level of mobile addiction than Europe.

Within the less developed emerging markets there wereconsiderable differences in the levels of Mobile-First. At 37% India has almost double the level of Mobile-First audience than Indonesia. The high levels in the Indian market being due to the fact that the smartphone audience in this market is particularly young, the majority being under 35. And Mobile-First audiences are much, not surprisingly, more prevalent amongst the younger audience – who have grown up mobile empowered.

9

Segment split among those 18+ year olds.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

UK

Mobile Disengaged Mobile Engaged Mobile-First

Germany Sweden USA Canada India Brazil Indonesia

43%50% 49%

37%45%

8%

22% 21%

55%

56% 60%

37%

22% 19%

38%

16%

45%

18%

39%

12%

37%

13%

40%

17%

38m 43m 6m 196m 23m 184m 69m 47m

10

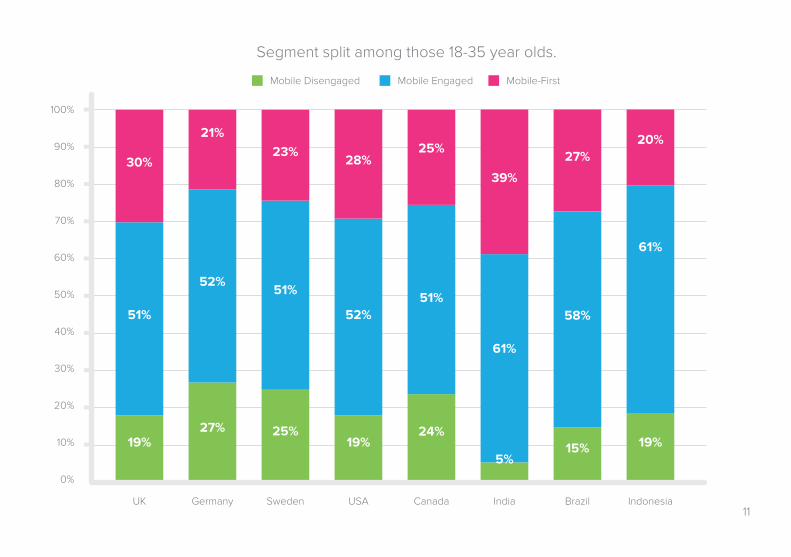

THE RISE OF THEUNDER 35 YEAR OLD MOBILE-FIRST USE.When considering the under 35 year old respondents acrossmarkets the percentage of Mobile-First and Mobile Engagedusers amongst the smartphone audience increases significantly.It also levels out across the globe.

Amongst this younger age group the difference between theUK proportion of Mobile-First (at 30%) and the India proportion(at 39%) is much more closely related.

In fact relatively few younger smartphone users claim not tobe engaged with their devices. The highest proportion ofMobile Disengaged under 35 years old were present in Germany, at 27%.

These younger, device-dependent, Mobile-First consumerswill represent an ever growing portion of consumer target audiences in the future. As such marketers need to considerthe mindset and behaviours of this group and adjust their marketing communications accordingly.

11

19%27% 25%

19%24%

5%15% 19%

61%

58%

61%

39%

27%20%

51%

25%

52%

28%

51%

23%

52%

21%

51%

30%

Segment split among those 18-35 year olds.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

UK

Mobile Disengaged Mobile Engaged Mobile-First

Germany Sweden USA Canada India Brazil Indonesia

12

HOW DO MOBILE-FIRST CONSUMERS ACCESS TRADITIONAL MEDIA?

13

THE SMARTPHONE IS THE MAIN SOURCE OF NEWS, MEDIA AND ENTERTAINMENT AMONGST MOBILE-FIRST CONSUMERS.Mobile-First consumers make full use of theirmultifunctional smartphones by using the widest range of its content features and functionalities. They all agree that their mobile phone is their main source of entertainment. With almost all listening to music via their device and most playing games.

They are the heaviest app users, with the majority using messaging, social, video and news app’s on a regular / daily basis. Mobile-First consumers also regularly consume traditional media such as news, TV and radio via their device.

Their beloved mobile phone is not only their main source of entertainment but also seen as a tool that helps them manage and document their life.

14

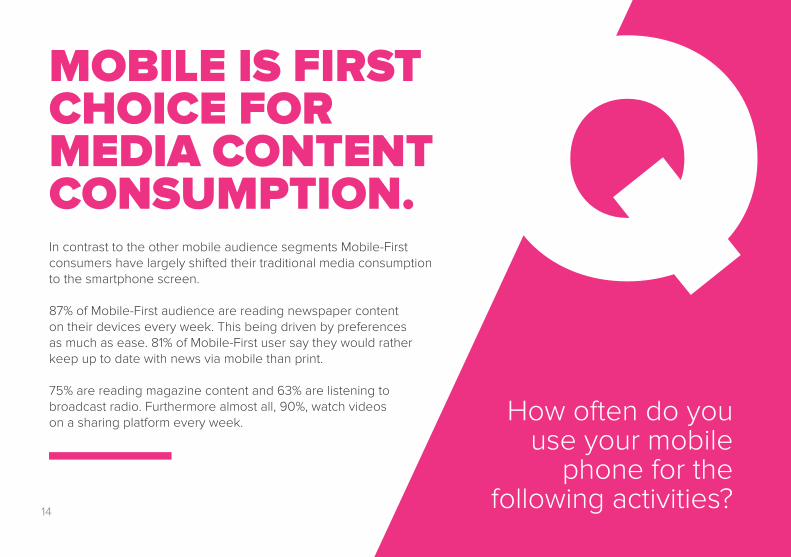

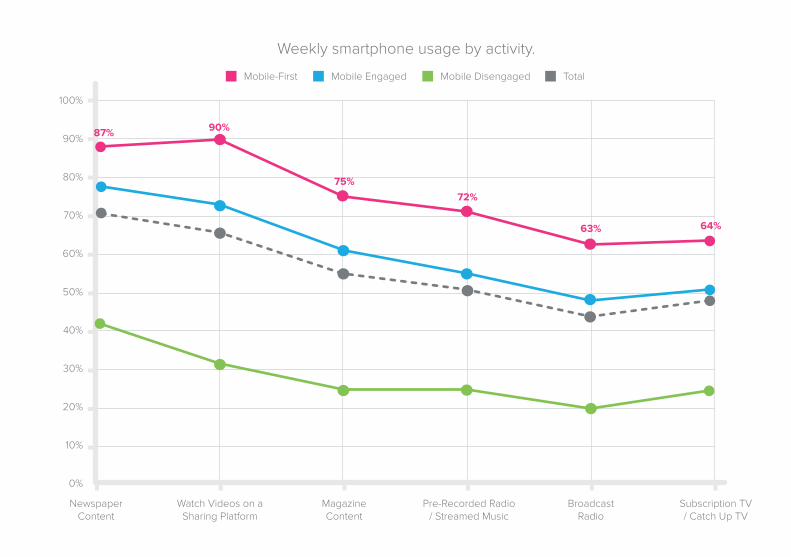

MOBILE IS FIRST CHOICE FORMEDIA CONTENTCONSUMPTION.In contrast to the other mobile audience segments Mobile-First consumers have largely shifted their traditional media consumption to the smartphone screen.

87% of Mobile-First audience are reading newspaper contenton their devices every week. This being driven by preferencesas much as ease. 81% of Mobile-First user say they would rather keep up to date with news via mobile than print.

75% are reading magazine content and 63% are listening tobroadcast radio. Furthermore almost all, 90%, watch videoson a sharing platform every week.

QHow often do you

use your mobilephone for the

following activities?

15

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

NewspaperContent

Watch Videos on a Sharing Platform

MagazineContent

Pre-Recorded Radio/ Streamed Music

BroadcastRadio

90%

75%72%

63% 64%

Weekly smartphone usage by activity.

Mobile-First Mobile Engaged Mobile Disengaged Total

87%

Subscription TV/ Catch Up TV

16

MOST MOBILECONTENTCONSUMPTIONIS APP-BASEDFOR MOBILE-FIRSTCONSUMERS.Mobile-First consumers spend the majority of their timein app’s (82% versus 19% amongst Disengaged), valuingthe ease and speed of use.

Over 85% use app’s to access video content every week(compared to 32% of Disengaged). 74% use app’s to accessnews content every week (compared to 33% of Disengaged.

And a high proportion of Mobile-First users will be accessingapps weekly for Gaming (73%), Music (73%), Sport (56%), Health& Fitness (55%).

Mobile-First users are likely to be the early adopters of new apps in the marketplace.

QHow often do

you use thefollowing types

of app’s?

17

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Messaging

Social M

edia

Watching Video / C

ontent

GamingMusic

Banking / F

inance

Shopping

Transp

ort / M

ap / Dire

ctions

Sport

Video Callin

g

Health & Fitn

ess

Business

/ Jobs

Live Stre

aming

Holiday /

Trave

l

Restaurant /

Order Food

Dating

News / M

agazine

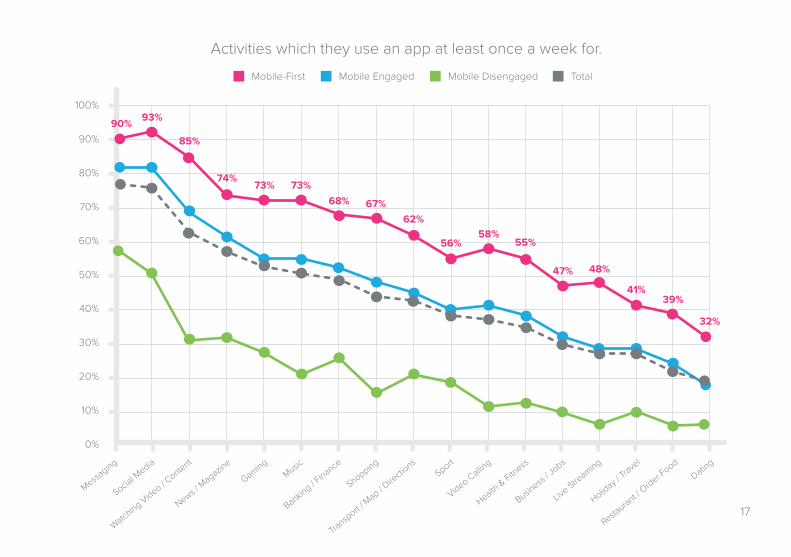

Activities which they use an app at least once a week for.

Mobile-First Mobile Engaged Mobile Disengaged Total

90% 93%

85%

74%73% 73%

68% 67%62%

56%58%

55%

47% 48%

41%39%

32%

18

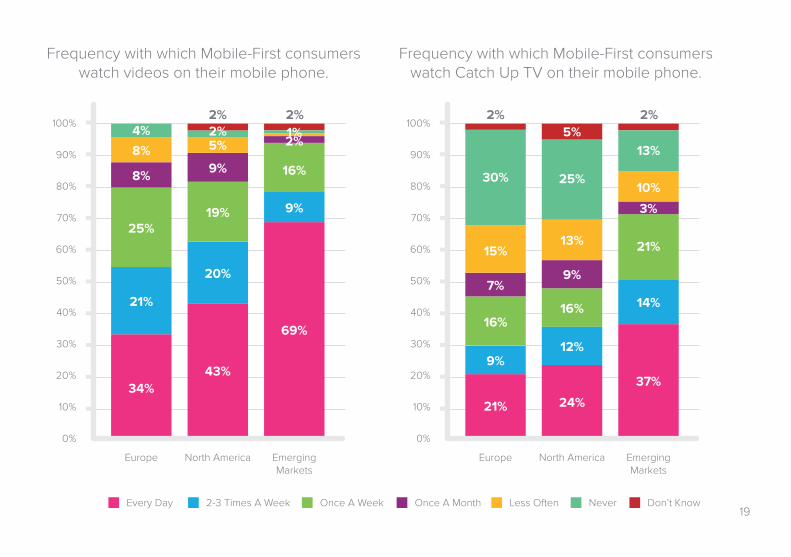

Across all regions at least a third of Mobile-First consumers claim to watch video on their mobile daily. With 34% in Europe, 43% in North America and a significant 69% in emerging markets.

And this is not necessarily user generated or low quality, short form content. Many use their devices now to watch broadcastTV programmes on their device.

46% of Europeans watch catch up TV on mobile weekly,52% of Americans, and 72% of emerging markets.

How often do youuse your mobile

phone for thefollowing activities?

QMANY MOBILE-FIRST CONSUMERS AREAVID, DAILYMOBILE VIDEOVIEWERS.

19

34%21%

43%

24%

69%

37%

21%

9%

20%

12%

9%

14%

25%

16%

19%

16%

16%

21%

8%

7%

9%

9%

2%

3%

8%

15%

5%

13%

4%

30%

2%

25%

2%5%

2%2% 2%

Frequency with which Mobile-First consumerswatch videos on their mobile phone.

Frequency with which Mobile-First consumers watch Catch Up TV on their mobile phone.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Europe EuropeNorth America North AmericaEmerging Markets

Emerging Markets

Every Day 2-3 Times A Week Once A Week Once A Month Less Often Never Don’t Know

1%

10%

13%

20

HOW DO MOBILE-FIRST CONSUMERS ACCESS SOCIAL MEDIA?

21

THE SMARTPHONE IS THE MOBILE-FIRSTCONSUMERS MAIN SOURCE OF NEWS,MEDIA AND ENTERTAINMENT.Mobile-First consumers are compulsive social media users who use their mobile phones to manage their daily social lives.

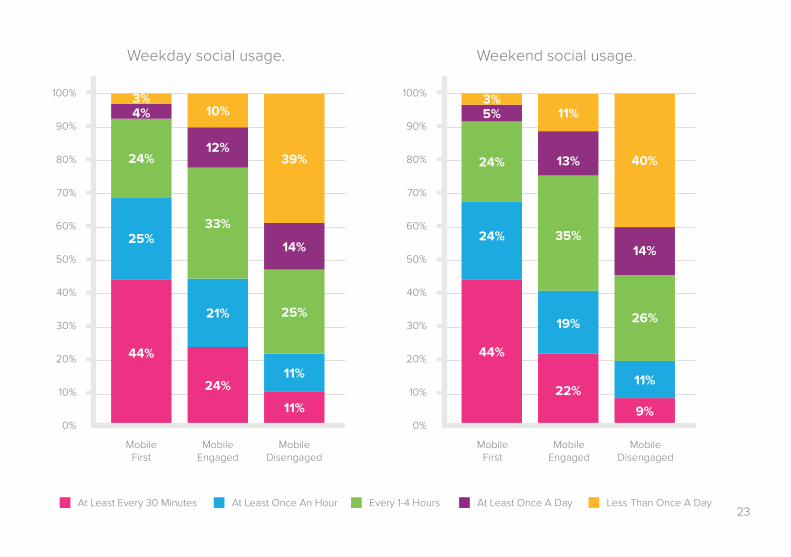

More than 68% claim to use social networks on their phone at least once every hour during the week or at weekends (more than 3 times as many as theMobile Disengaged) and almost all claim to visit a social media platform at least once a day.

And they are not only communicating with theirsocial network on these mobile channels, they are also willingly participating with advertising brands. They are 4x more likely to say they frequently notice advertising in social media and 8x more likely to share content than Disengaged.

22

Whether a weekday or the weekend, 44% of Mobile-First consumers claim to use mobile social media at least every 30 minutes. And an additional 25% claim to use social media at least once an hour. This goes a long way to explaining their high dependency and addiction to their small screens.

How often doyou use your

mobile phone tovisit social networks

sites or app’s?

QALMOST 70% OF MOBILE-FIRST CONSUMERS ACCESS SOCIAL MEDIA EVERY HOURTHROUGHOUT THE WEEK.

12

6

39210

111

5748

23

44% 44%

24% 22%11% 9%

25% 24%

21%19%

11% 11%

24% 24%

33%35%

25% 26%

4% 5%

12%13%

14%

39%

14%

3% 3%10% 11%

Weekday social usage. Weekend social usage.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

MobileFirst

MobileFirst

MobileEngaged

MobileEngaged

MobileDisengaged

MobileDisengaged

At Least Every 30 Minutes At Least Once An Hour Every 1-4 Hours At Least Once A Day Less Than Once A Day

40%

24

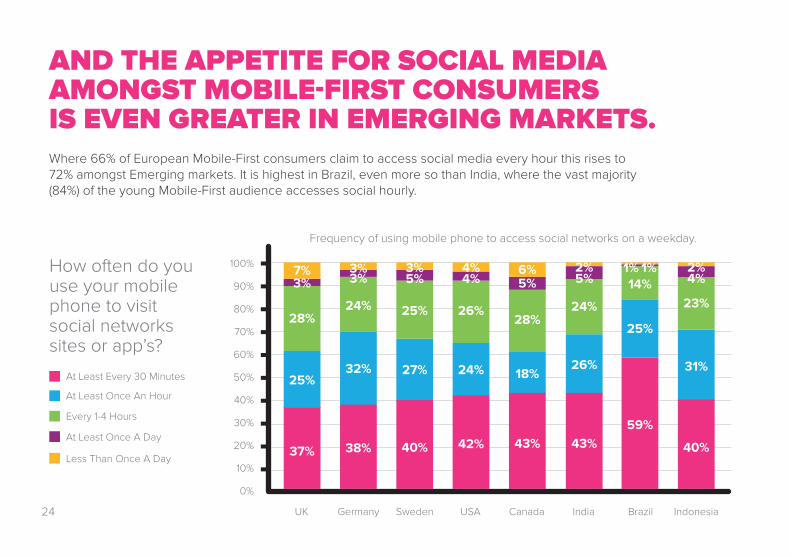

Where 66% of European Mobile-First consumers claim to access social media every hour this rises to72% amongst Emerging markets. It is highest in Brazil, even more so than India, where the vast majority (84%) of the young Mobile-First audience accesses social hourly.

AND THE APPETITE FOR SOCIAL MEDIA AMONGST MOBILE-FIRST CONSUMERSIS EVEN GREATER IN EMERGING MARKETS.

How often do you use your mobile phone to visitsocial networks sites or app’s?

37%

25%32%

28%24%

3% 3% 5% 4% 5% 5% 4%1%1%3% 4% 6% 2% 2%3%7%

38% 40%

27% 24% 18%26%

25%

31%

14%

26%28%

24% 23%25%

42% 43% 43%59%

40%

Frequency of using mobile phone to access social networks on a weekday.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

UK Germany Sweden USA Canada India Brazil Indonesia

At Least Every 30 Minutes

At Least Once An Hour

Every 1-4 Hours

At Least Once A Day

Less Than Once A Day

25

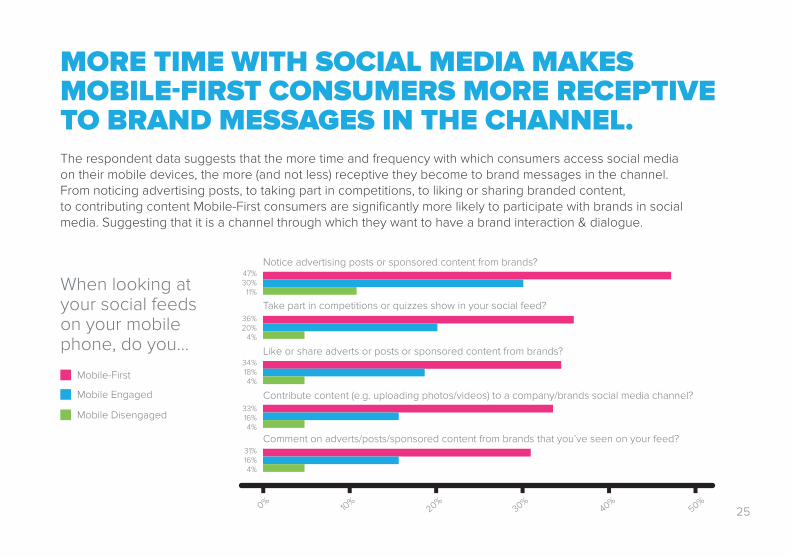

The respondent data suggests that the more time and frequency with which consumers access social media on their mobile devices, the more (and not less) receptive they become to brand messages in the channel. From noticing advertising posts, to taking part in competitions, to liking or sharing branded content,to contributing content Mobile-First consumers are significantly more likely to participate with brands in social media. Suggesting that it is a channel through which they want to have a brand interaction & dialogue.

MORE TIME WITH SOCIAL MEDIA MAKESMOBILE-FIRST CONSUMERS MORE RECEPTIVE TO BRAND MESSAGES IN THE CHANNEL.

When looking at your social feeds on your mobile phone, do you...

Mobile-First

Notice advertising posts or sponsored content from brands?47%30%

11%

36%20%

4%

34%18%4%

33%16%4%

31%16%4%

Take part in competitions or quizzes show in your social feed?

Like or share adverts or posts or sponsored content from brands?

Contribute content (e.g. uploading photos/videos) to a company/brands social media channel?

Comment on adverts/posts/sponsored content from brands that you’ve seen on your feed?

Mobile Engaged

Mobile Disengaged

0%10

%20%

30%40%

50%

26

HOW DO MOBILE-FIRST CONSUMERS WANT TO INTERACT WITH BRANDS & BUSINESSES?

27

Mobile-First consumers see their smartphone as an important assistant in their everyday consumer lifestyle and shopping behaviour. They use it to help them make more informed, intelligent and efficient decisions about the products and services they purchase. They do this by conducting extensive research on their mobile phone pre-shopping and checking reviews, prices and offers when in-store.

The more time people spend with their smartphones the more theywant to engage with brands and businesses via their device. Mobile-Firstconsumers are not ad blind and are, in fact, more receptive to brandcommunications through the device than others. They are willing to be targeted as long as they receive personalised and relevant messages.

However, they are not willing to work hard for this brand relationship!If a brand / business website is not optimised and easy to navigatethey will just go elsewhere!

MOBILE-FIRST CONSUMERS WANT AND EXPECT TOEASILY INTERACT WITHBUSINESSES AND BRANDSVIA THEIR SMARTPHONES.

28

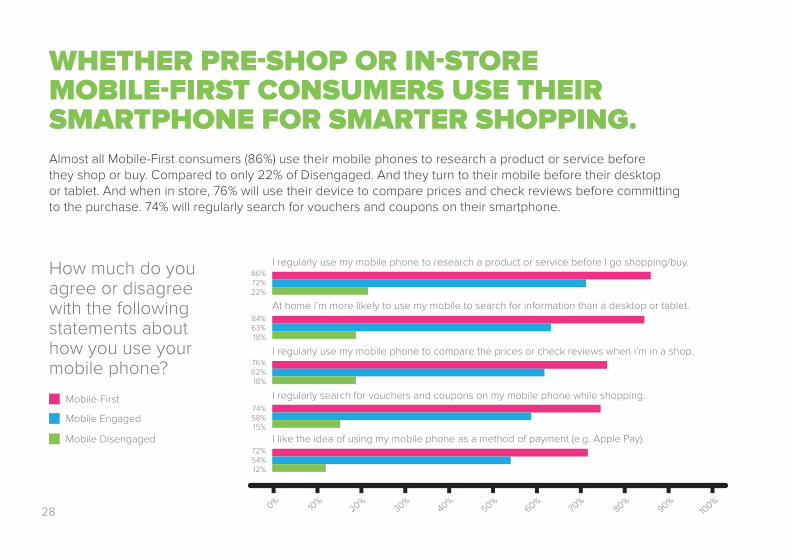

Almost all Mobile-First consumers (86%) use their mobile phones to research a product or service beforethey shop or buy. Compared to only 22% of Disengaged. And they turn to their mobile before their desktopor tablet. And when in store, 76% will use their device to compare prices and check reviews before committing to the purchase. 74% will regularly search for vouchers and coupons on their smartphone.

WHETHER PRE-SHOP OR IN-STOREMOBILE-FIRST CONSUMERS USE THEIRSMARTPHONE FOR SMARTER SHOPPING.

I regularly use my mobile phone to research a product or service before I go shopping/buy.86%72%22%

84%63%18%

76%62%18%

74%58%15%

72%54%12%

At home i’m more likely to use my mobile to search for information than a desktop or tablet.

I regularly use my mobile phone to compare the prices or check reviews when i’m in a shop.

I regularly search for vouchers and coupons on my mobile phone while shopping.

I like the idea of using my mobile phone as a method of payment (e.g. Apple Pay).

0%10

%20%

30%40%

50%60%

70%

80%90%

100%

How much do you agree or disagree with the following statements about how you use your mobile phone?

Mobile-First

Mobile Engaged

Mobile Disengaged

29

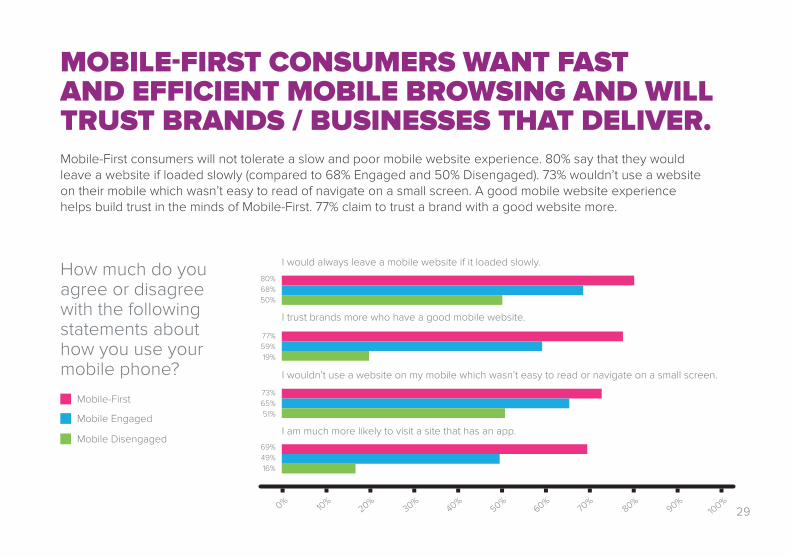

Mobile-First consumers will not tolerate a slow and poor mobile website experience. 80% say that they would leave a website if loaded slowly (compared to 68% Engaged and 50% Disengaged). 73% wouldn’t use a website on their mobile which wasn’t easy to read of navigate on a small screen. A good mobile website experience helps build trust in the minds of Mobile-First. 77% claim to trust a brand with a good website more.

MOBILE-FIRST CONSUMERS WANT FASTAND EFFICIENT MOBILE BROWSING AND WILL TRUST BRANDS / BUSINESSES THAT DELIVER.

0%10

%20%

30%40%

50%60%

70%

80%90%

100%

I would always leave a mobile website if it loaded slowly.

80%68%50%

77%59%19%

73%65%51%

69%49%16%

I trust brands more who have a good mobile website.

I wouldn’t use a website on my mobile which wasn’t easy to read or navigate on a small screen.

I am much more likely to visit a site that has an app.

How much do you agree or disagree with the following statements about how you use your mobile phone?

Mobile-First

Mobile Engaged

Mobile Disengaged

30

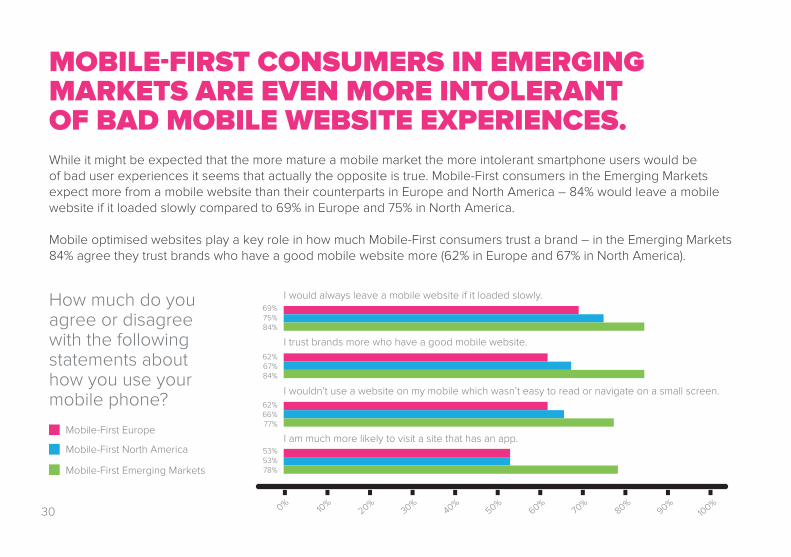

While it might be expected that the more mature a mobile market the more intolerant smartphone users would be of bad user experiences it seems that actually the opposite is true. Mobile-First consumers in the Emerging Markets expect more from a mobile website than their counterparts in Europe and North America – 84% would leave a mobile website if it loaded slowly compared to 69% in Europe and 75% in North America.

Mobile optimised websites play a key role in how much Mobile-First consumers trust a brand – in the Emerging Markets 84% agree they trust brands who have a good mobile website more (62% in Europe and 67% in North America).

MOBILE-FIRST CONSUMERS IN EMERGINGMARKETS ARE EVEN MORE INTOLERANTOF BAD MOBILE WEBSITE EXPERIENCES.

0%10

%20%

30%40%

50%60%

70%

80%90%

100%

I would always leave a mobile website if it loaded slowly.69%75%84%

62%67%84%

62%66%77%

53%53%78%

I trust brands more who have a good mobile website.

I wouldn’t use a website on my mobile which wasn’t easy to read or navigate on a small screen.

I am much more likely to visit a site that has an app.

How much do you agree or disagree with the following statements about how you use your mobile phone?

Mobile-First Europe

Mobile-First North America

Mobile-First Emerging Markets

31

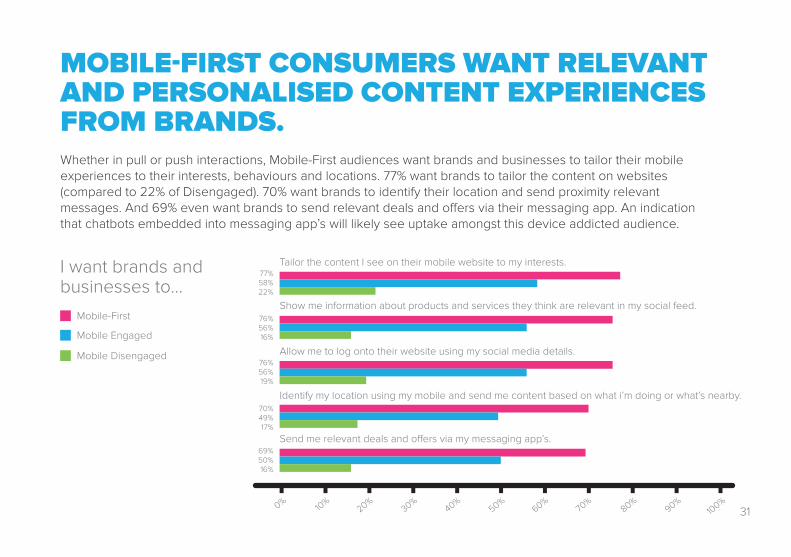

Whether in pull or push interactions, Mobile-First audiences want brands and businesses to tailor their mobile experiences to their interests, behaviours and locations. 77% want brands to tailor the content on websites(compared to 22% of Disengaged). 70% want brands to identify their location and send proximity relevantmessages. And 69% even want brands to send relevant deals and offers via their messaging app. An indication that chatbots embedded into messaging app’s will likely see uptake amongst this device addicted audience.

MOBILE-FIRST CONSUMERS WANT RELEVANT AND PERSONALISED CONTENT EXPERIENCES FROM BRANDS.

Tailor the content I see on their mobile website to my interests.77%58%22%

76%56%16%

76%56%19%

70%49%17%

69%50%16%

Show me information about products and services they think are relevant in my social feed.

Allow me to log onto their website using my social media details.

Identify my location using my mobile and send me content based on what i’m doing or what’s nearby.

Send me relevant deals and offers via my messaging app’s.

0%10

%20%

30%40%

50%60%

70%

80%90%

100%

I want brands andbusinesses to...

Mobile-First

Mobile Engaged

Mobile Disengaged

32

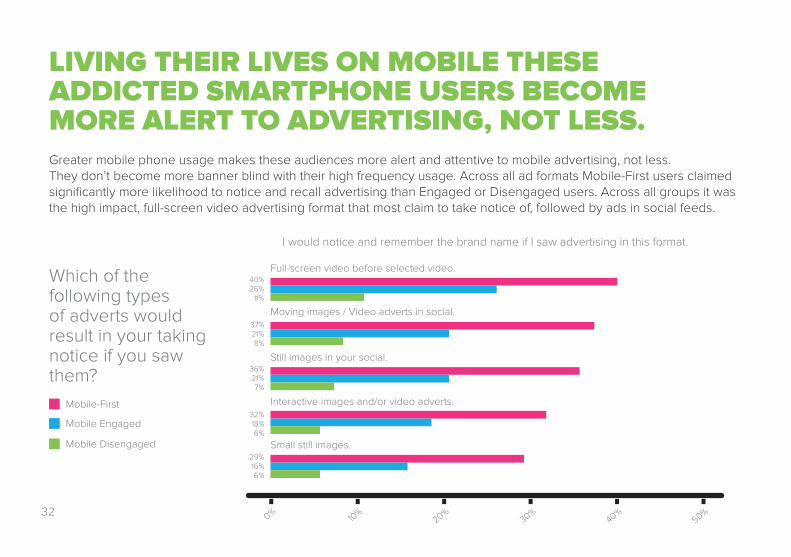

Greater mobile phone usage makes these audiences more alert and attentive to mobile advertising, not less.They don’t become more banner blind with their high frequency usage. Across all ad formats Mobile-First users claimedsignificantly more likelihood to notice and recall advertising than Engaged or Disengaged users. Across all groups it was the high impact, full-screen video advertising format that most claim to take notice of, followed by ads in social feeds.

LIVING THEIR LIVES ON MOBILE THESEADDICTED SMARTPHONE USERS BECOME MORE ALERT TO ADVERTISING, NOT LESS.

Which of thefollowing typesof adverts wouldresult in your taking notice if you saw them?

Mobile-First

Full-screen video before selected video.40%26%

11%

37%21%8%

36%21%7%

32%18%6%

29%16%6%

Moving images / Video adverts in social.

Still images in your social.

Interactive images and/or video adverts.

Small still images.

Mobile Engaged

Mobile Disengaged

0%10

%20%

30%40%

50%

I would notice and remember the brand name if I saw advertising in this format.

33

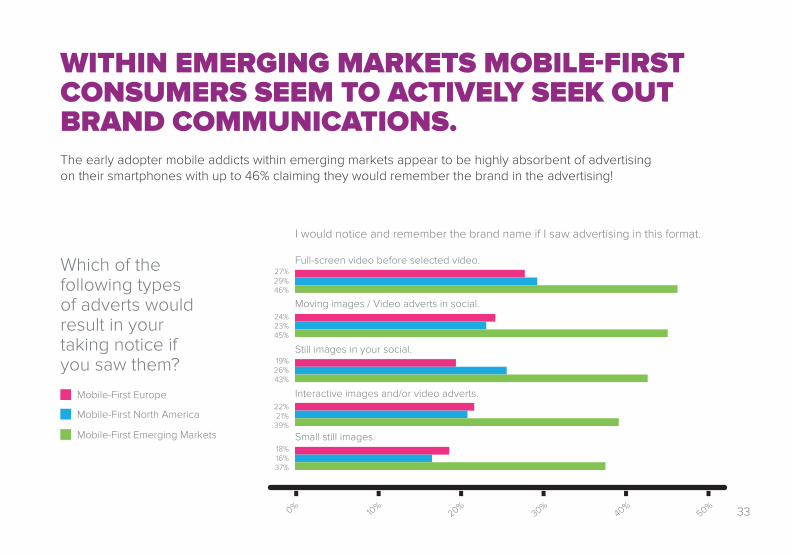

The early adopter mobile addicts within emerging markets appear to be highly absorbent of advertising on their smartphones with up to 46% claiming they would remember the brand in the advertising!

WITHIN EMERGING MARKETS MOBILE-FIRST CONSUMERS SEEM TO ACTIVELY SEEK OUT BRAND COMMUNICATIONS.

Which of thefollowing types of adverts would result in your taking notice if you saw them?

Mobile-First Europe

Full-screen video before selected video.27%29%46%

24%23%45%

19%26%43%

22%21%39%

18%16%37%

Moving images / Video adverts in social.

Still images in your social.

Interactive images and/or video adverts.

Small still images.

Mobile-First North America

Mobile-First Emerging Markets

0%10

%20%

30%40%

50%

I would notice and remember the brand name if I saw advertising in this format.

34

HOW SHOULD MARKETERSAPPROACH MOBILE-FIRST CONSUMERS?

35

ALL MARKETERS NOW NEED TO BE DEVELOPING COMMUNICATIONS

WITH THE MOBILE-FIRSTCONSUMER IN MIND.

As the research findingshave shown, amongstsmartphone users today thereis a significant portion who areself-proclaimed Mobile-First addicts.These people live their daily lives through their mobile phone– as their main source of news, content and entertainment,their tool to manage their social life, document their life and help with their shopping. Being highly prevalent amongst the under35 year old generation, and within the less mature, emerging mobile markets, their numbers are only likely to rise.

As such all marketers now need to recognise this growingmodern consumer type and look to satisfy the needs, desiresand expectations of this demanding and unforgiving audience. They not only need to deliver an optimised and personalisedmobile experience,in their micro-moments, but also start topredict consumers’ future needs and requirements and make anticipatory personalised recommendations to them. Delivering on this will be the way to the hearts and minds of the MobileFirst consumer.

36

Targeting an internationalaudience across developed and emerging markets?

Consider the differing levels ofMobile-First behaviour in markets and how to calibrate plans accordingly.

Consider that the vast majority will be Mobile-First (or Mobile Engaged) consumers.

Consider that Mobile-Firstconsumers are likely to consume this content on their small screen.

Consider that it needs to be as mobileoptimised and personalised as possibleto satisfy, and build trust, with MobileFirst consumers.

Consider that the Mobile-First consumeris the most likely to notice and react.

Targeting an under35 year old audience?

Planning & buying traditional / broadcast media (TV, radio, or print) advertising?

Developing mobilecontent & experiences?

Planning & buyingmobile advertising?

SOME CONSIDERATIONS.

37

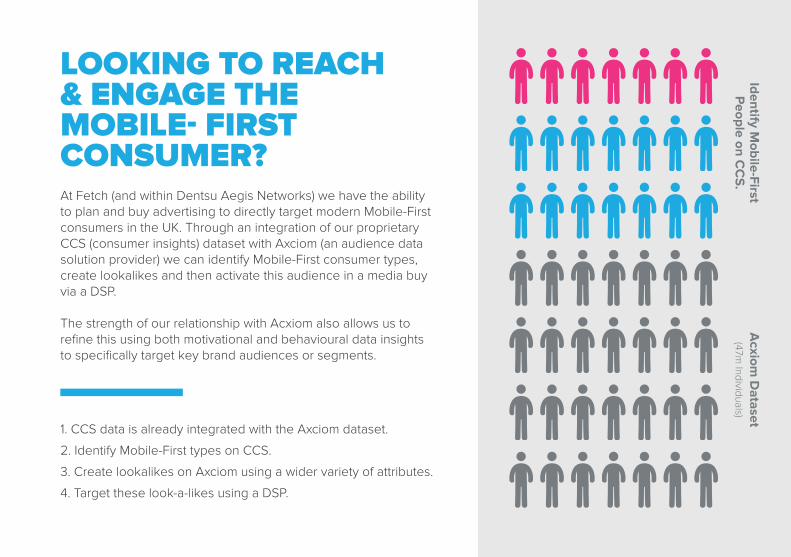

LOOKING TO REACH& ENGAGE THEMOBILE- FIRSTCONSUMER?At Fetch (and within Dentsu Aegis Networks) we have the ability to plan and buy advertising to directly target modern Mobile-First consumers in the UK. Through an integration of our proprietary CCS (consumer insights) dataset with Axciom (an audience data solution provider) we can identify Mobile-First consumer types, create lookalikes and then activate this audience in a media buy via a DSP.

The strength of our relationship with Acxiom also allows us to refine this using both motivational and behavioural data insightsto specifically target key brand audiences or segments.

1. CCS data is already integrated with the Axciom dataset.

2. Identify Mobile-First types on CCS.

3. Create lookalikes on Axciom using a wider variety of attributes.

4. Target these look-a-likes using a DSP.

Acxiom

Dataset

(47m Individuals)

Identify Mobile-First

People on C

CS

.

38

AuthorJulian Smith, Head of Strategy & [email protected]

ContactsJonathan Dove, Business Development Director - UK/[email protected]

Linsey Loy, Client Development Director - [email protected]

#MobileFirstMarch 2017