what next for africa ? citac africa llp africa... · what next for africa ? mark elliott ... •...

TRANSCRIPT

ARA Week, March 2017 1

CITAC Africa LLP

The Downstream African Energy

Specialist

What Next for Africa ?

Mark Elliott

Chairman CITAC Africa Ltd

Cape Town, March 2017

ARA Week, March 2017 2

CITAC Africa LLP

The Downstream African Energy

Specialist

What Next for African

Downstream?

Mark Elliott

Chairman CITAC Africa Ltd

Cape Town, March 2017

ARA Week, March 2017 3

Outline

• African growth1.

• Specification changes and refining outlook2.

• Logistics infrastructure3.

• Marketing and distribution4.

• LPG, LNG and renewable energy5.

• Why regulation is the key to success6.

ARA Week, March 2017 4

4

African growth1.

ARA Week, March 2017 5

Mid-term economic growth: focus is on recovery

-1

0

1

2

3

4

5

6

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

%

Source: IMF (Oct'16)

Economic Growth Outlook

SSA

MENA

World

G7

Euro area

ARA Week, March 2017 6

AFRICA balances to 2030

50,000

70,000

90,000

110,000

130,000

150,000

170,000

190,000

210,000

230,000

250,000

000m t

Africa's Growing Clean Product Shortfall

(2000-2030)

Clean products demand

Clean products demand (f)

Clean product output

Output (forecast Scenario 1)

Output (forecast Scenario 2)

148.3mn

mt

81.6mn

mt

ARA Week, March 2017 7

7

Specification changes and refining outlook2.

ARA Week, March 2017 8

Product quality: New momentum has led to

government action on specifications

• Precipitated government action, mainly in Nigeria

and Ghana

• Dutch ports joined the debate – may face legal

challenge

The end result is good for ARA - increased

focus on AFRI specifications campaign

and ARA policy

ARA Week, March 2017 9

Focus on sulphur reduction

ARA Week, March 2017 10

ARA Specs Policy derives from landmark studies (WB/ARA 2009, Wood McKenzie 2014, etc.)

Policy (brief summary):

1. AFRI specifications for all Africa – to get adopted by

the African Union

2. Governments: AFRI 4 by 2020, AFRI 5 by 2030

3. Governments: value refinery on all socio- economic

benefits

4. “3 legged stool” – fuels, vehicles and testing

5. Regional specifications based on supply chains, not

political boundaries

6. ARA members working with governments and

regional organisations

ARA Week, March 2017 11

Africa: 20 years behind Europe

ARA Week, March 2017 12

Future specification challenges

ARA Week, March 2017 13

Does desulphurisation reward the investing

refinery?

• 2014 Wood Mackenzie - ARA “Value of Refining Study”:

“…the investment required is typically very significant and

may exceed $500mn in some specific situations.

Experience of clean fuels programs in Europe and

elsewhere suggests that refiners are unlikely to receive a

commercial return on any such investment.

Product prices for higher quality fuels tend to command

only a modest market premium over the poorer quality

alternative.…we consider that African refiners are

extremely unlikely to invest in improved environmental

performance unless mandated to do so.”

ARA Week, March 2017 14

MARPOL Impact may be short-term positive for

WAF

• ULSSR/VGO (<0.5% sulphur) values increase

• for two years?

ARA Week, March 2017 15

Refining developments

• Algeria: refinery expansion and new projects

• Egypt: new projects announced

• South Africa: Chevref (+ Caltex marketing) for sale

• Angola: Lobito refinery project put on hold

• Uganda: Looking for new investors

• Kenya: Essar leaves KPRL - conversion to crude

terminal

• Nigeria: Dangote progessing (fertiliser plant

construction started?)

• Cameroon: SONARA expansion tie-in delayed

• Specification changes require refinery investment

ARA Week, March 2017 16

Refining needs fundamental policy changes

• SSA governments’ commitment to refining needs to

be confirmed:

compare to Middle East and North Africa

commitment to ongoing capital needs

• Ex-refinery prices based on import parity pricing plus

logistic and other costs:

but should they also take into account:? The socio-economic advantages of refining,

supply security etc?*

? The national health benefit of upgrading

quality?**

• If so, governments must be willing to support refinery

investments

*ARA Wood Mackenzie study (2014)

**WB/ARA study (2009)

ARA Week, March 2017 17

Logistics infrastructure3.

ARA Week, March 2017 18

Investment in downstream oil infrastructure

Storage:• Angola: new SBM and storage• S. Africa: Cape Town, Durban, Richards Bay

• Namibia: Walvis Bay

• Mozambique: Nacala, Matola

• DRC: Ango-Ango;

• Rwanda: Kigali;

• Malawi: Lilongwe, Blantyre, Mzuzu

• Liberia: Monrovia, etc.

Railways:• Kenya: Standard gauge railway

• Ethiopia: Djibouti-Addis Abeba railway

• Tanzania/Zambia: Tazara

Pipelines - Nigeria: NNPC privatising?

ARA Week, March 2017 19

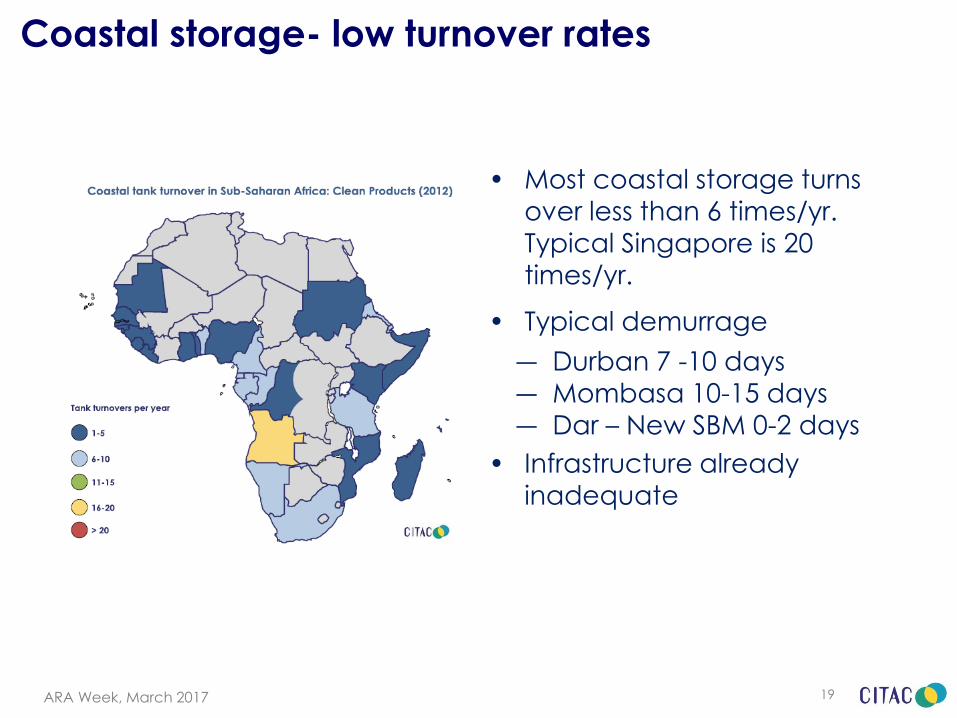

Coastal storage- low turnover rates

• Most coastal storage turns

over less than 6 times/yr. Typical Singapore is 20

times/yr.

• Typical demurrage

― Durban 7 -10 days

― Mombasa 10-15 days

― Dar – New SBM 0-2 days

• Infrastructure already inadequate

ARA Week, March 2017 20

Investment in this sector may not all be wise…

• …encouraged by regulated price structures which

compensate inefficiency and poor supply

planning?

• …controlling key entry points, but competitive and

safe supply routes may change (Beira?, Matola?,

Lagos?,Jorf Lasfar?)

• …tank turnaround remains low by global standards

Good regulation needed to reward investment in

efficiency and HSEQ

ARA Week, March 2017 21

Need for logistic efficiency & improved

supply planning

ARA Week, March 2017 22

Marketing and distribution4.

ARA Week, March 2017 23

• “Old Majors” continue to exit: Shell: divests 20% of Vivo

Caltex: South Africa for sale

Exxon: Nigeria sold to NIPCO

• Total: investing heavily - Angola, Mozambique, Cote

d’Ivoire, EAC, Egypt

• Pan-Africans building - Puma, Vivo, Oryx, Engen Nigeria: Vitol – Oando (OVH)

South Africa: Puma

Mali: Oryx – 16 new stations

• Local players: NOC Ethiopia, Afriquia Morocco,

Lake Oil EAC

• National companies changing – Petroci sells to

Puma but NOC’s growing in Botswana, Egypt,

Malawi

Marketing – “New Majors” get stronger

ARA Week, March 2017 24

Scramble for African markets

• Finding the right station

• And the right operator

• Margins often high and guaranteed

• Investment in brand differentiation (Shell,

Total)

• Future: increase

focus on service

(C-stores, food

fuel cards)

Regulation is key

ARA Week, March 2017 25

Tank truck accidents in Africa are worst in World

Source: WHO

ARA Week, March 2017 26

Is HSE (health, safety and environment) improving?

• “Old Majors” exit was a cause for concern

• Total, Vivo & Puma raising the standards*

• But small independent distributors and truckers can

be sub-standard

• Bulk transport by pipeline and rail will lower

accident rate – but difficult to justify investment

(markets small)

• Aviation fuel quality control is a concern

Need for improved, enforced regulation

*ARA Forum presentations

ARA Week, March 2017 27

LPG, LNG and renewable energy5.

ARA Week, March 201728

Primary energy mix forecast

41% 43% 41% 39% 36%

27% 26% 27%29%

29%

27% 25% 23%21%

20%

4%

1% 2% 4% 6% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2020 2025 2030 2035

African Energy Mix forecast

Renewables

Hydro

Nuclear

Coal

Gas

Oil

Source: IEA

ARA Week, March 2017 29

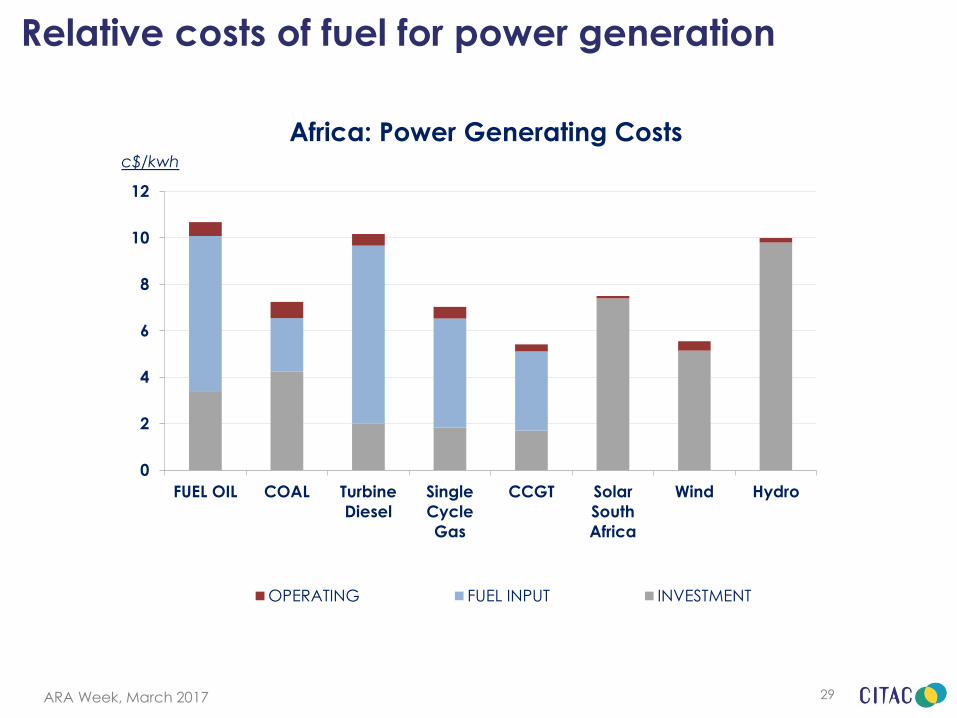

Relative costs of fuel for power generation

0

2

4

6

8

10

12

FUEL OIL COAL Turbine

Diesel

Single

Cycle

Gas

CCGT Solar

South

Africa

Wind Hydro

c$/kwh

Africa: Power Generating Costs

OPERATING FUEL INPUT INVESTMENT

ARA Week, March 2017 30

Developing the propane market in Africa

30

• Large global oversupply

• Propane readily available – Angola, Nigeria,

US Gulf

• Replace gasoil/fuel oil in localised/off-grid

powergen, e.g. industry, mining – dedicated

systems

• Retail – continue to need 80/20 or 70/30

Butane/Propane mix

ARA Week, March 2017 31

Will gas/LNG and renewables replace oil?

• Natural gas - power industry in North Africa, Nigeria,

Côte d’Ivoire (RCI)

• New gas supply: Ghana, Mozambique, Tanzania,

Kenya, Egypt – displace coal and fuel oil in power

and mining

• LNG imports increasing – RCI, Egypt, S. Africa?

• Large scale solar is competitive with oil and will

displace some diesel, particularly in off-grid

generation

• Growth of local distributed power solutions –

renewables and thermal will have an impact

ARA Week, March 2017 32

Why regulation is the key to success6.

ARA Week, March 2017 33

Regulator Structures: still mainly government

REGULATOR STRUCTURE Petroleum - Downstream Petroleum - upstream Electricity

Algeria Ministry(ARH) Ministry(ARH) CREG

Angola Ministry Ministry HIRSEA*

Burkina Faso Prime Minister (CIDPH) Ministry ARSE

Cote d'Ivoire Ministry (DGH) Ministry (DGH) ANARE

Egypt Ministry - EGPC Ministry - EGPC Egypt ERA

Ghana NPA Petroleum Commission Energy Commission

Kenya ERC Ministry ERC

Mauretania Ministry (CNH) Ministry Regulatory authority

Mozambique Ministry(MIREM) Ministry(MIREM) CNELEC

Nigeria Ministry - DPR Ministry - DPR NERC

Senegal Ministry Ministry CRSEMinistry (Refining/retail)

NERSA(Pipelines,storage) PASA, NERSA NERSATanzania EWURA* EWURA* EWURA*Uganda Ministry (MEMD) Ministry (MEMD) ERA

Zambia ERB Ministry ERB

Zimbabwe ZERA ZERA ZERA

South Africa

ARA Week, March 2017 34

Regulators protect interest of consumers,

investors and other stakeholders

Downstream scope often includes:• Depot and service station construction

• Ex refinery prices

• Pump pricing and price structures

• Industry import processes

• Fuel quality - product marking, sanctions

• Refining, storage & distribution

• HSE standards and monitoring

Also sometimes electricity and water

ARA Week, March 2017 35

Regulators must apply the law

Regulators must:

• Enforce the rule of law

• Stay out of politics and not be influenced by

changes of government

• Be honest

• Be impartial

• Be independent

• Control, test, enforce

• Invest in equipment and technology

Give confidence to investors

ARA Week, March 2017 36

Are regulators fit for the task ahead?

• Stronger, separate, independent downstream

regulation needed in many countries

• Need to be independent of politics

• Over-regulation discourages investment and

leads to investment in the wrong places

• Free markets generally lead to “good” investment

• Good, independent regulation is the single most

important requirement to assure future investment

and create investor confidence

ARA Week, March 2017 37

CITAC Africa LtdAldermary House

10-15 Queen Street

London, UK

EC4N 1TX

Tel: +44 (0)207 343 0014

E-mail: [email protected]

Web: www.citac.com

CITAC® is a registered trademark. Any reproduction of information

contained within this presentation requires CITAC’s permission.