what will hr look like in the future

TRANSCRIPT

PURELY

PAYROLLA ONE STOP MAGAZINE FOR BUSY PAYROLL & HR PROFESSIONALS

Auto enrolment and SMEsCharities and Equality ActManaging Office Relationships The end of the SSP scheme? Why social media will not work for you 2014 TUPE changesPayroll for international employees

FEBRUARY 2014

What will HR look like in the futureALSO IN THIS ISSUE...

We all know payroll can be a real headache. It’s complex, time-consuming and an absolute nightmare if you get it wrong. At Moorepay, we support thousands of business owners and professionals to make their lives easier. With our flexible payroll solutions, we can help you get on with what you do best - running your business or department.

So whatever the size or complexity of your business, we have the perfect solution. Moorepay is a leading supplier of payroll, HR and compliance solutions to businesses large and small.

What next? To focus on doing more with your business, give us a call on 0845 184 4615 or email [email protected]

f /moorepay @moorepay in Join Moorepay

Focus your time and energy on doing more by outsourcing your payroll to us.

Focus on

0845 184 4615www.moorepay.co.uk

21

Key Dates 2014

HMRC Online Tax Return

31st January

HM Treasury Publish 2014 Budget

19th March

CIPD HR Software Show

Come and visit us!18-19th June

Key Dates

England & Wales Only Bank Holiday

Scotland Only Bank Holiday

Northern Ireland Only Bank Holiday

UK Bank Holiday

f /moorepay @moorepay in Join Moorepay | Leading supplier of payroll, HR and compliance solutions to businesses large and small.

2014January

S M T W T F S

1 2 3 4 40

5 6 7 8 9 10 11 41

12 13 14 15 16 17 18 42

19 20 21 22 23 24 25 43

26 27 28 29 30 31

Tax Week

February

S M T W T F S

1 44

2 3 4 5 6 7 8 45

9 10 11 12 13 14 15 46

16 17 18 19 20 21 22 47

23 24 25 26 27 28

Tax Week

March

S M T W T F S

1

2 3 4 5 6 7 8 49

9 10 11 12 13 14 15 50

16 17 18 19 20 21 22 51

23 24 25 26 27 28 29 52

30 31

Tax Week

48

April

S M T W T F S

1 2 3 4 5 1

6 7 8 9 10 11 12 2

13 14 15 16 17 18 19 3

20 21 22 23 24 25 26 4

27 28 29 30

Tax Week

21

October

S M T W T F S

1 2 3 4 26

5 6 7 8 9 10 11 27

12 13 14 15 16 17 18 28

19 20 21 22 23 24 25 29

26 27 28 29 30 31

Tax Week

December

S M T W T F S

1 2 3 4 5 6 35

7 8 9 10 11 12 13 36

14 15 16 17 18 19 20 37

21 22 23 24 25 26 27 38

28 29 30 31

Tax WeekSeptember

S M T W T F S

1 2 3 4 5 6 22

7 8 9 10 11 12 13 23

14 15 16 17 18 19 20 24

21 22 23 24 25 26 27 25

28 29 30

Tax Week

May

S M T W T F S

1 2 3 5

4 5 6 7 8 9 10 6

11 12 13 14 15 16 17 7

18 19 20 21 22 23 24 8

25 26 27 28 29 30 31

Tax Week

June

S M T W T F S

1 2 3 4 5 6 7 9

8 9 10 11 12 13 14 10

15 16 17 18 19 20 21 11

22 23 24 25 26 27 28 12

29 30

Tax Week

S M T W T F S

1 2 3 4 5 13

6 7 8 9 10 11 12 14

13 14 15 16 17 18 19 15

20 21 22 23 24 25 26 16

27 28 29 30 31

Tax Week

July August

S M T W T F S

1 2

3 4 5 6 7 8 9 18

10 11 12 13 14 15 16 19

17 18 19 20 21 22 23 20

24 25 26 27 28 29 30 21

31

Tax Week

17

25

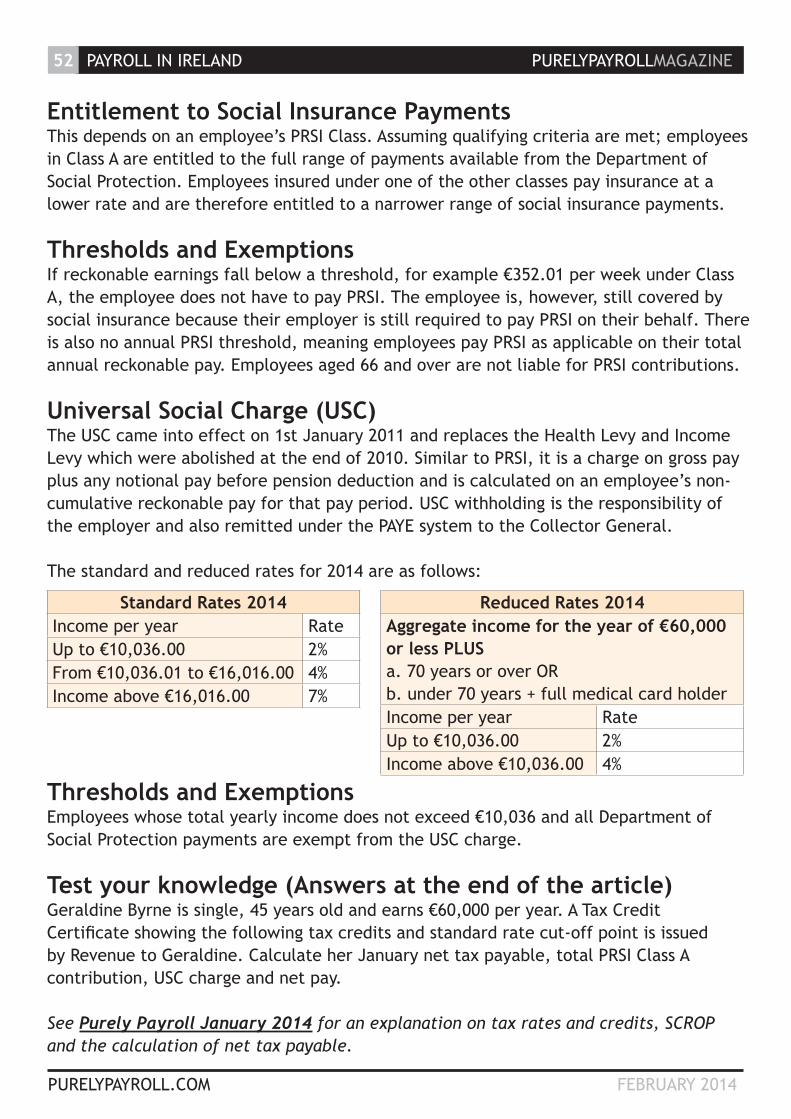

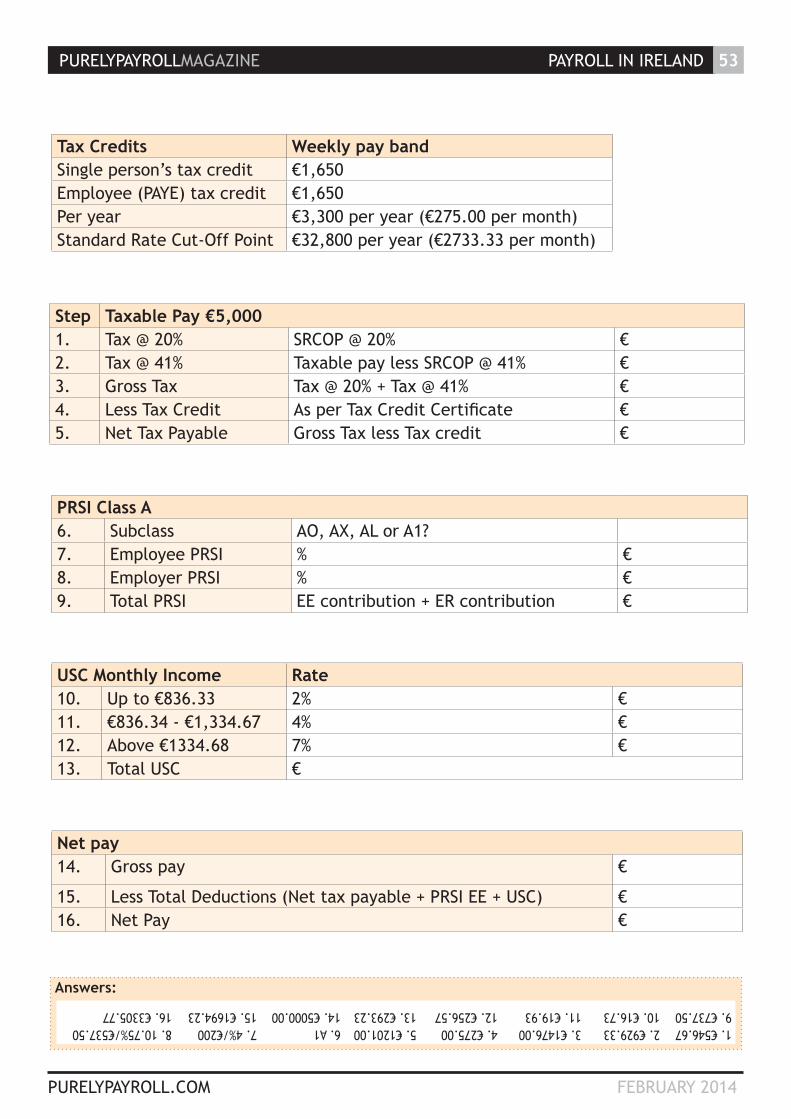

Tax Facts Find out all the latest

tax facts that affect your business at www.moorepay.co.uk

or scan the QR code:

November

S M T W T F S

1

2 3 4 5 6 7 8 31

9 10 11 12 13 14 15 32

16 17 18 19 20 21 22 33

23 24 25 26 27 28 29 34

30

Tax Week

30

Scan the QR code below or visit www.moorepay.co.uk/resources

Download our 2014 Calendar

PURELYPAYROLLMAGAZINE THE TEAM 03

meet the teameditorial

contributors in this issue

ADRIAN HOBBS

SUSAN BALL

MELANIE PIZZEY

KATE UPCRAFT

RICHARD LINSKELL

BILLIE EADIE

TIM KELSEY

STEVE PHILLIPDENIS BARNARD

EMMA BARLETT SINEAD STACK

STUART HALL

LEE HAMILTON TREVOR BETTANY

ANNE-MARIE BALFOUR

Contributing editor

Editor

Contributing editor

Contributing editor

Contributing editor

Contributing editor

salespublisher

PURELYPAYROLL.COM FEBRUARY 2014

CONTENTS PURELYPAYROLLMAGAZINE

PURELYPAYROLL.COM FEBRUARY 2014

04

contents06

0813

2218

23

News: Things you really need to know

Charities and Equality Act

Dates for your diary

Managing Office Relationships

What will HR look like in the future

Auto enrolment and SMEs

Managing Office Relationships

Auto enrolment and SMEs Charities and Equality Act

Why social media will not work for you

What will HR look like in the future

26The end of the SSP scheme?

PURELYPAYROLLMAGAZINE CONTENTS 05

PURELYPAYROLL.COM FEBRUARY 2014

contents30

A word from our editor2014 is going to be a very important year for the automatic enrolment of eligible employees into pension saving. This is because 2014 sees a ‘spike’ in numbers of employers having to comply – employers with little or no pension experience. And payroll will be at the forefront of making automatic enrolment work. In her article on Automatic Enrolment & SMEs, Kate Upcraft highlights the challenges ahead for those professionals who’ll be at the forefront of helping employers comply with their automatic enrolment duties.

Another payroll article highlights the important tax issues when you have employees going outside the UK to work; and we speculate on whether the Statutory Sick Pay scheme may end up fading away. Sinead Stack presents Part 2 of her coverage of running a payroll in the Republic of Ireland.

Our lead feature by Denis Barnard, What will HR look like in the future?, engages in some crystal ball gazing; some practical advice is offered on how to deal with workplace romances; a review of the TUPE changes that came in from 31st January is highlighted; and there’s coverage of how the Equalities Act 2010 applies to the charities sector.

Enjoy!

Why social media will not work for you

3334

4640

50

Questions you ask

2014 TUPE changes

Payroll for international employees

Find a new business partner

Payroll in Ireland, Part 2

NEWS PURELYPAYROLLMAGAZINE06

PURELYPAYROLL.COM FEBRUARY 2014

Things you really

need to knowChanges to administration of employee share schemes from April 2014Do you operate any kind of employee share scheme in your business? If so, the following is a must read. This is because HMRC is changing the way both new and existing employee share schemes and arrangements are administered.

Further...

HMRC publishes guidance on ending the tax year 2013/14 under RTIHMRC have published guidance to help Real Time Information employers cope with what will be for the majority their first tax year-end under RTI.

Further...

Guidance on the amended TUPE regulations coming into force 31st January 2014The Department for Business, Innovation and Skills has published guidance, Employment Rights on a Transfer of Undertakings, on the changes to the 2006 TUPE regulations that have recently become law

Further....

Updated Real Time Information guidance published by HMRCHMRC have made software developers aware of changes to the operation of Real Time Information from the start of the tax year 2014/15 and where developers, employers, and agents can go for further information.

Further...

Requiring SCONs to be shown on Full Payment SubmissionsHMRC have provided some further information about the mandatory requirement to show Scheme Contracted-out Numbers (SCON) on FPS returns from the beginning of the tax year 2014/15.

Further...

Reasons for submitting a late RTI returnFrom the start of the tax year 2014/15, HMRC is changing its RTI specifications to enable employers to insert a reason code as to why a particular Full Payment Summary return is ‘late’ being submitted online to HMRC.

Further...

Could automatic enrolment into pension saving be about to derail?The National Employment Savings Trust (a government sponsored national not-for-profit pension scheme) sees serious problems ahead for all those smaller employers who must start staging in to automatic enrolment during 2014.

Further...

Sharp increase in numbers of employers staging into auto enrolment during 2014The Pensions Regulator has published updated statistics showing around 30,000 medium-sized employers (50-250 workers) will reach their automatic enrolment staging date between this April and the end of 2014.

Further...

Government consults further on use of zero hours contractsOn 19 December 2013, the Department for Business, Innovation and Skills issued a consultation concerning Zero hours employment contracts.

Further...

Employers set to see £200 per employee wiped off their NICs bill by end of this ParliamentFrom 6 April 2014, the new ‘Employment Allowance’ will wipe out up to £2,000 off the total National Insurance bill of every business.

Further...

Sharp rise expected in penalties for failing to pay minimum wageOn 15 January, it was announced that rogue employers who do not pay their workers the National Minimum Wage (NMW) will face an increased penalty of up to £20,000 as part of a government crackdown.

Further...

PURELYPAYROLLMAGAZINE NEWS

PURELYPAYROLL.COM FEBRUARY 2014

07

Sponsored by

AUTO ENROLMENT AND SMES PURELYPAYROLLMAGAZINE08

PURELYPAYROLL.COM FEBRUARY 2014

Auto enrolment-challenges for SMEs and their agents!

PURELYPAYROLLMAGAZINE AUTO ENROLMENT AND SMES 09

PURELYPAYROLL.COM FEBRUARY 2014

Whether you, as an accountant, IFA, or payroll bureau, are willing or able to take on that role needs serious consideration, even if you have the expertise, do you have the capability to support all your clients who may be staging simultaneously?

Kate Upcraft

Auto enrolment-challenges for SMEs and their agents!

The largest employers not only already had pension schemes; they also had extensive in-house technical knowledge of government pension policy and legislation – not quite the same for the small business owner.

So in this article we will explore some of the common areas of concern that will allow payroll bureaus and agents to prepare for the tidal wave of questions.

Resource crunch?The statistics in respect of the numbers of SMEs (Small and Medium Enterprises) who are staging in 2014 indicate the huge demands that will be placed on the ‘support’ community, be that an accountant, Independent Financial Advisor, or payroll bureau. In April, May, and July 2014, 30,000 schemes will stage; that compares to around 6,000 in total who staged in the first 12 months of the auto-enrolment duties.

Those large employers were able to engage the services of employee benefit consultants and pension administrators and to establish internal project teams covering every affected discipline from procurement, to IT, to payroll. SMEs do not have the luxury of the financial resources to source external support nor the expert resource internally.

Whilst we can learn some useful lessons from the experience of the large employers who have already gone through auto-enrolment staging, as the duties roll out to small and medium sized employers new and different challenges present themselves, not least because this group may well look to their accountants and payroll agents as their single source of expert support.

AUTO ENROLMENT AND SMES PURELYPAYROLLMAGAZINE10

PURELYPAYROLL.COM FEBRUARY 2014

MiddlewareThe large employers in many cases also either had the resources to have bespoke systems created or were able to deal with the complexities of the auto-enrolment legislation by taking the radical approach of contractual auto-enrolment. This avoided assessment and a plethora of communication with employees and also to took the bottom line hit if opt-outs did not materialise to expected levels – which they didn’t!

Neither of these options will be open to SMEs, as the cost imperative means that they will need to use existing or off the shelf systems to assess and postpone in order to auto-enrol as few individuals as possible.

From a systems’ perspective, the pensions industry is keen to recoup its investment in developing both bespoke software and middleware hub solutions by selling these to the next tranche of staging employers. However the landscape has changed and with RTI live, the vast majority of payroll software providers now have at the very least assessment capability within their products, rendering middleware unnecessary.

For the large employers, middleware was essential to deliver the statutory notices to the workforce if their payroll and HR software had no such facility or it was a chargeable extra module, as manual preparation of notices was not feasible. But middleware came with a surprise impact for many of those who signed on the dotted line - the failure to realise that in order to carry out assessment and comms, that week’s or month’s payroll data had to be

captured early so it could be processed by the middleware and delivered back to the employer ready for the payroll run. Because of this some employers have had to totally re-engineer payroll processing deadlines that wouldn’t have been necessary if middleware was not in use.

As the volumes of statutory notices are much smaller as we move into SME territory the message has to be ‘find out what your current HR and payroll systems can do for you and then just plug the gaps’, don’t rush out to buy middleware that you may not need.

CostsPreparation is everything with auto-enrolment and it is a salutary lesson that a quarter of large employers felt they spent more than they needed to on the project because of rushed decision making due to allowing insufficient time before staging.

According to ‘Finding your way out of the auto enrolment maze’ - new research from the independent economic consultancy Centre for Economic Business Research (Cebr), the cost of auto-enrolment implementation for small businesses (1-4 employees) was £8,900, this figure rises to £12,600 for small-medium businesses of 100 employees, and £15,600 for companies employing 250 people. This is further supported by a survey in May 2013 by consultancy Benefex that found that 79% of employers felt ongoing administration was the biggest challenge in terms of resourcing and cost.

For example some providers have higher charges if the employer does not hold email addresses for 80% of prospective members as the provider wants to be able to communicate electronically with them to contain costs.

Decisions, decisions One of the real benefits for SMEs is that they can learn from the experience of others. As auto-enrolment involves such key strategic decisions no one should be afraid to ask for references from others in their sector in respect of the chosen pension provider or those who are already using an auto-enrolment solution from their payroll software developer.

PURELYPAYROLL.COM FEBRUARY 2014

PURELYPAYROLLMAGAZINE AUTO ENROLMENT AND SMES 11

DataMuch of the feedback from those already staged into auto-enrolment has centred on the need for clean and good quality data to smooth the implementation process. Whilst a lot of personal data will have been cleansed ready for RTI there will doubtless be areas that did not feature in RTI preparation that are key to the success of pension interfaces and achieving good terms from a pension provider.

Therefore, a cheaper upfront solution that leaves the employer with a lot of manual workarounds could be fine for those with small numbers to auto-enrol and few employees with variable earnings, but a real issue for example in a weekly payroll retail environment – one size most definitely does not fit all.

Of course that presupposes that the key strategic decisions are taken quickly, getting auto-enrolment on the directors’ agenda can use up valuable time and that’s before the talking starts!

AUTO ENROLMENT AND SMES PURELYPAYROLLMAGAZINE12

PURELYPAYROLL.COM FEBRUARY 2014

A typical payroll bureau with 300 clients may find that not only are all of them staging very close together

but that each has chosen a different pension provider

and all need a bespoke electronic interface of employee data after each payroll run to set up schemes as cheaply as possible.

It is a brave payroll agent who doesn’t consider the chargeable time involved in creating all these bespoke interfaces. Some agents I have spoken to have naively assumed all their clients would use NEST (National Employment Savings Trust) or that all dealings are with The Pension Regulator who then farms out files to providers - this may seem basic but pensions are new territory for both SMEs and some of their agents.

Opt-outsOpt-out rates will be key to cost control for SMEs so is vital that they carry out an initial assessment of eligible, non-eligible and worker numbers using live payroll data to consider the cost impact.

Experience from the large employers indicates that opt outs are higher amongst the over 50’s who are likely to have already secured their retirement finances. Other reasons for opt out naturally relate to financial priorities and, interestingly, the likelihood of moving on from the employer in the near future. SMEs will be able to use these trends to assess their likely opt-out percentage and whether they will differ from the average of around 10%.

In conclusion…So whilst there are lessons to learn from year one of auto-enrolment, perhaps the key message is that the challenges for SMEs are very different and we shouldn’t underestimate how much support these clients will need.

The legislation around auto-enrolment is very complex and some will need legal advice just to decide who is in scope as a worker and what pay elements need to be included in qualifying earnings.

The good news is that Steve Webb the pension minister has listened to the concerns of the payroll industry and introduced simplification around pay reference periods that took effect on 1st November 2013; with longer windows to action auto-enrolment in place from 1 April 2014; and further simplification promised.

But there’s no room for complacency - RTI was a walk in the park compared to auto enrolment!

PURELYPAYROLLMAGAZINE CHARITIES AND THE EQUALITY ACT 13

PURELYPAYROLL.COM FEBRUARY 2014

CHARITIES AND THE EQUALITY

ACT 2010

CHARITIES AND THE EQUALITY ACT PURELYPAYROLLMAGAZINE14

PURELYPAYROLL.COM FEBRUARY 2014

There are three main triggers when the Act must be actively considered by Charities; when a new charity is set up, when charities merge and if a charity changes its “objects”.

There are few legal reference points for charities, save the Catholic Care case which showed the drastic consequences of failure to comply with the Act. If an existing charity operates in a prohibited way, its Trustees should take immediate remedial steps or risk claims and financial liability. A prospective charity risks its registration being refused if its purpose is prohibited by the Act. Every charitable activity or restriction by a charity of its activities, triggers obligations under the Act.

Emma Bartlett

The impact of the Equality Act 2010 (the Act) on Charities is not well understood and there is limited guidance available. The Act tightened exceptions in anti-discrimination law previously protecting charities. Charities will discriminate in favour of particular persons to the exclusion of others and therefore need to ensure that their charitable activities are compliant.

PURELYPAYROLLMAGAZINE CHARITIES AND THE EQUALITY ACT 15

Charity Commission guidance on the Act is light. In 2013, the University of Liverpool published an in-depth study of the impact of the Act on charities, concluding that older charities, religious ones, and higher education charities were most at risk or most affected by the Act.

What is unlawful discrimination?The Act makes it unlawful to discriminate, because of one or more of nine protected characteristics and identifies different types of discrimination. Unlawful discrimination need not be intentional. It is easy to fall foul of the Act’s restrictions.

For example, indirect age discrimination can arise if a charity’s policy disallows help to unemployed people with less than five years’ work experience; older unemployed workers are more likely to be able to meet this criteria leading to younger workers being prejudiced.

The charities exceptionThe Act recognises when a charity’s purpose may favour or exclude a particular group with a protected characteristic.This will be lawful provided the purpose falls within the charity’s statutory exception.

For example, a charity for the promotion of a particular religion within the community will need to rely on the charities exception to avoid unlawfully discriminating against other religions excluded from benefit.

PURELYPAYROLL.COM FEBRUARY 2014

The exception is subject to two conditions:1. The charity’s governing document must

detail the principal purpose of allowing only persons sharing a particular protected characteristic to benefit.

2. The restriction must be (i) a proportionate means of achieving a legitimate aim or (ii) for the purpose of preventing or compensating for disadvantage linked with the protected characteristic.

For example, a charity’s aim is to help high unemployment of a particular religion within the community, could potentially fall within 2(ii) if the unemployment of that particular religious group in the community is higher than that for the general population (i.e. the group is sufficiently disadvantaged).

Other exceptions Trustees need to be aware of other statutory exceptions:

Men or women only fundraising - it is permissible for there to be a men only or women only fundraising in aid of that charity.

For example, Race for Life is a nationwide women only event that raises money for Cancer Research UK.

Membership based on religious belief - membership of charities can be based on religious belief, even if the charity is not set up for religious purposes, provided the requirement was in place prior to 18 May 2005.

CHARITIES AND THE EQUALITY ACT PURELYPAYROLLMAGAZINE16

PURELYPAYROLL.COM FEBRUARY 2014

For example, the Scouts Association which requires children joining to promise to do their best to do their duty to God. Restricting membership of associations - some charities are also associations (for example, the British Deaf Association). An association is any group with 25 or more members which has rules to control how someone becomes a member. It is permissible under the Act to restrict membership to people who share a protected characteristic (apart from a person’s colour) which would enable, for example, the BDA to limit membership to people who are deaf or have hearing loss.

Positive action - charities can take positive action (such as giving a particular disadvantaged group accelerated access to services or training opportunities) providing it is a proportionate means of achieving one of the following aims: (i) enabling such a particular group to overcome or minimise a disadvantage connected with it; (ii) meeting needs specific to people who share the protected characteristic; (iii) enabling a particular group to participate in an activity where their participation is disproportionately low.

For, example, a children’s centre charity working specifically in a community which is predominantly Polish, but where few Polish parents and children use its services. Permissible positive action includes short term waiver or reduced admission fees to encourage attendance.

Permissible activity - if the charity in the above example simply took steps to advertise and explain its children’s centre services to the Polish community, there would arguably be no less favourable treatment to others; permissible activity under the Act.

Religious or belief organisations - charities, and non-commercial organisations, whose purpose is to: (i) practice, teach or advance a religion or belief, or; (ii) enable people of the religion or belief to receive a benefit or engage in any activity with the framework of that religion or belief, or; (iii) promote good relations between people of different religions or belief beliefs; can restrict membership and access to activities, services or facilities on the basis of religion or belief, where this is necessary to comply with the purpose of the organisation or to avoid causing offence to members of the religion or belief.

Such charities can also discriminate on the basis of sexual orientation in order to avoid conflict with the strongly held convictions of members of the religion or belief, but not in relation to any activity carried out on behalf of a public body under a contract with that body.

The Catholic Care caseIn the Catholic Care (Diocese of Leeds) v Charity Commission for England and Wales and another [2010], the faith based adoption society appealed against a Charity Commission decision not to approve amended objects intended to bring it within anti-discriminatory provisions. Catholic Care had initially appealed the Charity Commission’s rejection to the Charity Tribunal and then appealed that decision to the High Court. The High Court gave a small victory to Catholic Care, directing the Charity Commission to reconsider its application to change its objects clause in order to come within the statutory exception.

The decision provides useful clarification on the interpretation of this legislation. The case was the first in which a court or tribunal had to consider the correct interpretation of the statutory charities exemption.

Charities can ignore the statutory exception if: It does not restrict who may benefit (i.e. there is therefore no disadvantage to a particular group with a protected characteristic and so no contravention of the Act).

It does restrict who can benefit from its work, but the restriction does not relate to particular group with a protected characteristic (i.e. so no contravention of the Act, although be vigilant to any indirect discrimination risk mentioned above.).

A restriction does relate to particular group with a protected characteristic, but it can be justified using other provisions in the Act.

The charity is for the benefit of disabled people generally. Please note that if a charity’s purpose is restricted to benefit people with a specific disability (e.g. cancer) then this will need to fall within the charity exception or the Act’s other exceptions.

PURELYPAYROLLMAGAZINE SHARED PARENTAL LEAVE 17

PURELYPAYROLL.COM FEBRUARY 2014

We recommend charities review restrictions in their governing document which favour persons with a protected characteristic.

Trustees should ensure that the charity’s purpose falls within the Act’s exceptions.

Trustees should be aware that a change in circumstances could lead to the charity’s purpose falling outside of a statutory exception.

For example, if a charity’s purpose is to help a particular religious group whose unemployment rates are higher than the national average, that purpose may cease to fall within the charities exception if over time that unemployment rate decreases. Amendments to charitable purposes would warrant detailed legal advice.

WHAT WILL HR LOOK LIKE IN THE FUTURE PURELYPAYROLLMAGAZINE18

PURELYPAYROLL.COM FEBRUARY 2014

What will HR look like in the future?

PURELYPAYROLLMAGAZINE WHAT WILL HR LOOK LIKE IN THE FUTURE 19

PURELYPAYROLL.COM FEBRUARY 2014

Two of the questions that people seem to like asking me (usually over a glass of wine) are: What impact will increasingly sophisticated HR software have on the profession? and: What will HR look like in the future?

I’ll try to give my own very personal viewpoints on these in the course of this article.

Over the past year or two I have written and spoken at some length about not only making the business case for choosing the best HR and payroll software, but also ensuring the right priority is attached to the project.

When I talk to clients about the elements that comprise the economic argument, they seem to think of cost savings expressed in money rather than in terms of FTE (Full Time Equivalent); and yet nearly all of my empirical findings come back to time saved by smarter technology, and this translates more readily into FTE. As I start to talk about this, there is an embarrassed

What will HR look like in the future? Denis Barnard

shuffling of feet; HR don’t want to be seen as putting people out of work, especially their own.

Coupled with that reaction is the fear of comfort zone loss. On the one hand,

HR proclaims that is could be more strategic if it wasn’t bogged down with administrative functions,

with the other, it clings on fiercely to what it has, perpetuates the gatekeeping role, and gratefully accepts more new stuff that no-one else wants.

Whether the profession likes it or not, there are technological advances in the software that they use – or will be using - that render a lot of administrative activities defunct. And the gatekeeping will have to end, too.

Let’s consider some typical tasks:Organisation Charts These can very

often be the Organisational Development version of painting the Forth Bridge; they are an ongoing work in progress, compiled manually in Visio or PowerPoint, are never accurate in real time; many departments seem to keep their own versions that are at variance with the central one.

WHAT WILL HR LOOK LIKE IN THE FUTURE PURELYPAYROLLMAGAZINE20

PURELYPAYROLL.COM FEBRUARY 2014

Approvals When it comes to things like recruiting replacement staff, organisations with low trust and poor processes often require multiple signatures, even though the salary and post were already established in the headcount budget at the beginning of the year. Who, more often than not, gets the task of collecting these signatures? I always remember at one place the CEO needed a new manager and went out and recruited the person; it took HR five weeks a posteriori to garner the necessary six signatures to approve the hire.

How much holiday do I have left? How many HR (and some payroll) departments field a barrage of requests for information on remaining holiday entitlement from employees?

Starters and Leavers How do we ensure that an incoming new employee has access to the computer system from Day One, is included in the Life Assurance and Pension schemes, is known to reception and on the phone list, and so on? That their probation period is tracked and remaindered? How do we remember to have property such as mobile phones, laptops, and security passes returned?

Generating management reports for the Board or functional directors Whether we are prepared to admit it or not, many HR people do not have sufficient confidence to run a raw report and distribute it, either because it has not been set up correctly, or because there is a lack of knowledge of the report writing application. To compensate for this, there exist manual interventions, data manipulation, work-arounds and, in extreme cases, parallel employee databases held in Access or Excel.

Do all or any of the above seem familiar? Of course they do, and the interesting thing is that they – and other administrative chores – can all be streamlined and automated by a good HR & payroll software product where tools such as Work Flow, Triggered Actions, and Self Service are featured. Not only will such a system take the heavy lifting in its stride, but it also reduces the potential for error or omission.

I have some rule of thumb calculations, gathered over some years, that indicate the amount of FTE that can be saved over the five to seven year typical lifetime for this type of software, and the figures are significant. Let’s assume a modest total saving of ten FTE over a seven year period, what are the implications for the staff currently engaged on these routine tasks? Can they in fact be re-deployed to function as strategists?

This is a question that the whole profession will have to confront sooner rather than later. That there should at least exist the possibility of administrative staff being strategic should be evidenced by the number of 20-something HR Masters holders I have encountered doing routine tasks in their departments.

And the vision for HR in the future? In the 1970s and ‘80s many organisations had what was known as a “machine room” where an array of NCR- type machines were operated to run the organisational ledgers. Those same ledgers are now run by a smaller number of professionals on accounting software. So where are those former operators now? Did they transfer over to being accountants? I think we can figure out the answer to that.

Business SolutionsPensionAuto-Enrolment:Are you ready?As PAE staging dates approach for many, is your organisation prepared for the challenges ahead...

Have you considered the costs associated

with the change? Will you require

additional headcount within the payroll

team to manage the adoption of new

processes? Are procedures in place to

facilitate the increased interaction with

HR? What is your payroll software supplier

doing to ensure you are supported

through the transition?

If you are unsure of the answers to any

of these questions, then please visit our

dedicated Auto-Enrolment microsite for

information on what is required from

employers or take the opportunity to

explore potential costs using our

Auto-enrolment calculator.

Click to try our calculator or visit: www.advancedcomputersoftware.com/autoenrol

Call: 01582 714810Email: [email protected]

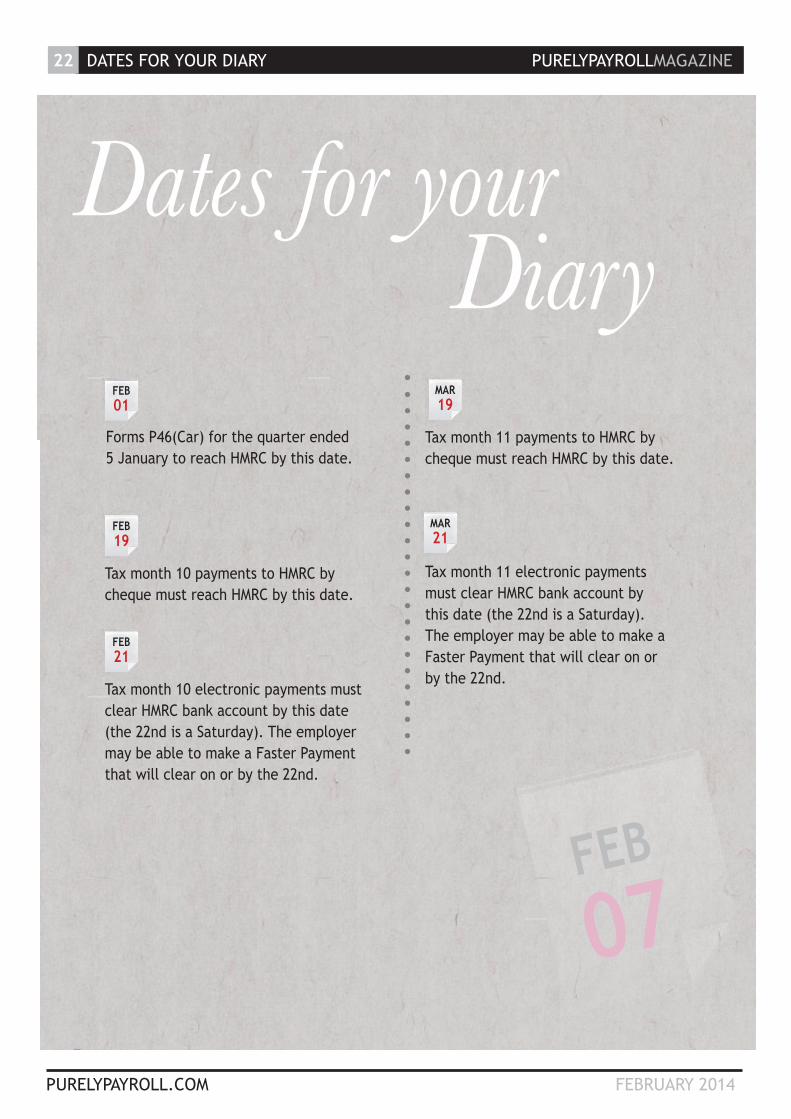

Tax month 7 payments to HMRC by cheque must reach HMRC by this date.

FEB

07PURELYPAYROLL.COM FEBRUARY 2014

Tax month 10 payments to HMRC by cheque must reach HMRC by this date.

Tax month 10 electronic payments must clear HMRC bank account by this date (the 22nd is a Saturday). The employer may be able to make a Faster Payment that will clear on or by the 22nd.

Tax month 11 payments to HMRC by cheque must reach HMRC by this date.

Tax month 11 electronic payments must clear HMRC bank account by this date (the 22nd is a Saturday). The employer may be able to make a Faster Payment that will clear on or by the 22nd.

Forms P46(Car) for the quarter ended 5 January to reach HMRC by this date.

Dates for your Diary

FEB19

FEB21

MAR19

MAR21

FEB01

DATES FOR YOUR DIARY PURELYPAYROLLMAGAZINE22

PURELYPAYROLLMAGAZINE MANAGING OFFICE RELATIONSHIPS 23

PURELYPAYROLL.COM FEBRUARY 2014

Managing office relationships

Stuart Hall

Whether their eyes meet across a crowded board room or sparks fly as they both reach for the hole- punch, office romances are inevitable. The long hours spent together, the mutual interests, and the romantic fantasies imprinted on our minds by Hollywood, can lead to whirlwind romances sprouting up all over the office.

MANAGING OFFICE RELATIONSHIPS PURELYPAYROLLMAGAZINE24

PURELYPAYROLL.COM FEBRUARY 2014

But what is one couples real life Rom-com can fast become the HR department’s nightmare. From messy breakups to disgruntled ex’s, love affairs can take their toll on the entire office affecting morale and performance. Yet the days of banning workplace lovers has passed, so how exactly should office romance be managed?

But what happens when the honeymoon ends…

When cupid’s arrow strikes and employees enter a relationship it can cause serious, well founded, concerns for an employer and conclude in potential complications to the business.

Witnessing examples of public affection can make others feel uncomfortable and distract them from the task at hand. This feeling of unease is multiplied further when displayed between two employees of differing work levels. Jealousy takes hold of the masses, fearing that favouritism will be shown to the lower ranking partner.

Worse still is when a relationship ends. The disruption caused by couples who never quite reached ‘happily ever after’ can be calamitous. After or even during a break up tensions are high, the mood is low, and the affects can be seen rippling through the entire office. A feeling of discomfort will embed itself in employees creating a tense, prickly atmosphere. If the problem fails to resolve itself quickly a boss may be obliged to set up disciplinary hearings potentially leading to official warnings or perhaps worse.

It all becomes very messy when one (or both) of the love-struck parties are either married or in a relationship

When romance blossoms…Romantic liaisons in the workplace are not uncommon with 40% of employees confessing to having met their spouse at the office and 56% of workers admitting to having an inter-company relationship at some stage.

Happiness is infectious. When a relationship is flourishing, a couple’s morale will be through the roof. Their all round happy demeanour and can do attitude will most certainly rub off on their co-workers; consequentially improving the office’s work efficiency and team spirit.

A couple with mutual interests and commitments can benefit the business. By understanding the stresses that come with their job, and that occasionally one of the partners may be busy, it can relieve some worries that come with out of work relationships. Instead of panicking about whether their partner won’t understand their long hours they can give their undivided attention to work. The capacity to discuss work issues at home with someone who appreciates the scenario can be constructive to working through an employee’s problem, allowing them to approach it appropriately the following day.

PURELYPAYROLLMAGAZINE MANAGING OFFICE RELATIONSHIPS 25

PURELYPAYROLL.COM FEBRUARY 2014

with someone else. It’s not unheard of for the estranged lover to storm into an office and confront their partner’s new interest. This would clearly be an unwelcome distraction in the office and is highly unprofessional. What if potential clients witnessed it?

It is essential that office relationships are handled carefully by employers.

Steps to Managing Office Relationships

1. Be open and honest with your employees. Sensible employers construct a very clear policy revolving employee romances and within it, stipulate what behaviour is deemed as unacceptable and how professionalism must be a priority. This honesty however works both ways with the employer requiring full disclosure, i.e. if two employees decide to be in a relationship they should make the employer aware.

2. Make it clear you do not encourage office relationships. Although it’s seen as unwise to ban them completely you can make it clear that you do not encourage them. This is important in case the worse should occur; your standpoint is recorded and clear from the outset.

3. Have a contract in place for employees. Despite seeming over the top, stipulating the rules and regulations surrounding behaviour and sexual harassment will be crucial to avoiding lawsuits. Their signed recognition of these policies releases the employer of any legal worries.

4. Keep managers properly informed. Ensure line managers are aware of the situation and are prepared for concerns from other employees. A relationship in the office, if not managed, could affect them.

The financial ramifications of a poorly handled case can be disastrous with some employees being known to sue their company for millions. In 2011, a UBS employee who had broken up with her supervisor brought a sexual harassment lawsuit against the company. UBS were made to pay £10.6 million.

The fundamental issue regarding office relationships is that employers are involved despite their wishes to the contrary. They should put as many systems in place as possible to safeguard not only their company but themselves from prosecution. This being said, with it being a month for valentines, don’t stand in the way of love. Who knows it could just be the real thing…

SICK PAY PURELYPAYROLLMAGAZINE26

Two of the proposals put forward in the above document were the abolition of the Percentage Threshold Scheme, which is taking place from 6 April 2014 (more below), and the removal of the statutory requirement on employers to maintain sick pay records.

PURELYPAYROLL.COM FEBRUARY 2014

The end of the Statutory Sick Pay scheme?

Back in January 2013, the Department for Work and Pensions published Fitness for work: the Government response to ‘Health at work – an independent review of sickness absence

Keeping SSP recordsIn their Review, the DWP stated: “Under current legislation, employers are required to maintain records of sickness absence lasting four days or more and details of Statutory Sick Pay (SSP) payments for each employee for three years after the end of each tax year. The Government recognises the

importance of maintaining records for sickness absence and payroll, and their key role in helping businesses to manage absence and costs. However, bearing in mind the statutory burden it places upon employers, the Review recommended the abolition of obligatory SSP record keeping requirements.”

But then a few lines down it goes on

Q Questions You Ask... Answers that Work

Answer from Adrian Hobbs

Question

MAY 2012 PURELYPAYROLL.COM

AThe whole of the government’s thrust concerning company cars is to drive down pollution. This means the more fuel e�cient and lower a car’s CO2 emissions the less income tax an employee will pay.

When deciding what type of car to go for, the �rst step will be to ascertain any car’s CO2 emissions. At Appendix 2 of HMRC booklet 480(2012), you can �nd tables for the tax years 2011/12 to 2013/14 setting out the percentage of a car’s list price that will be taxed depending on its level of emissions. At Budget 2012, tables for the tax year 2014/15 to 2016/17 were published.

These tables show the ‘squeeze’ on emissions. Except for ultra-low carbon emission cars, the tables start with a percentage of 15% of the car’s list price. For 2011/12, a car needs to have a rounded down CO2 �gure of 121g/km to be taxed at 15%; for the tax year 2016/17, the car will need a CO2 �gure of less than 95g/km to be taxed at the same rate. In other words, if an employee wants to pay less tax by 2016/17 they’ll have to be driving an ultra-low carbon emission car.

Diesel cars generally have a much lower CO2 rate than equivalent petrol cars. But they’ve been hit by an extra 3% supplement. The good news is that this supplement is being withdrawn from 6 April 2016, so that diesel cars are subjected to the same level of tax as petrol cars. So providing diesel cars may still be one of your best options – they have lower CO2 emissions, and they manage more miles to the gallon. However, against this must be set the often additional capital cost of purchasing a diesel car, and the currently much more expensive price of diesel.

Of course, LPG fuelled cars, whether a petrol/LPG hybrid or a car that only runs on LPG, could prove tax e�cient. They also generally have lower CO2 emissions than cars that just run on petrol. Also, LPG is cheaper than petrol or diesel, and the number of fuel stations selling LPG is growing all the time. As at 4 April 2012, average UK prices at the pump were 78.7p/litre for LPG; 141p/litre for petrol; and 147.3p/litre for diesel. But then we don’t know what the government may do to LPG prices in the years to come!

Answers from Adrian Hobbs

PURELYPAYROLLMAGAZINE SICK PAY 27

PURELYPAYROLL.COM FEBRUARY 2014

to state: “Employers are required to maintain records to comply with PAYE regulations, and in the event of a dispute with an employee around non-payment of SSP they may be asked by HMRC to produce evidence of absence and payment to defend a case. Employers who fail to pay SSP or pay incorrect amounts of SSP are also liable to a

penalty.”This is what I cannot get my head

around – if employers are still required to pay Statutory Sick Pay (SSP) to eligible workers, and they can be required to “produce evidence of absence and payment” where there is a dispute, how can the “obligatory SSP record keeping requirements” be abolished?

Abolition of PTS scheme from April 2014From 6 April 2014, the Percentage Threshold Scheme for the recovery of SSP is being abolished. The PTS compensates employers for higher-than-average sickness absence. Currently, only about 100,000 employers claim PTS recovery each year with a cost to the Exchequer of approximately £50 million per annum. Most SSP recovery payments are for small sums.

Instead, the PTS funding will be moved into a new health and work assessment and advisory service to help employees who’ve been incapacitated for four weeks or more get back to work. Chapter 2 of the above Review provides more information concerning how the new service is expected to work. The new service is expected to be introduced by the end of 2014.

DWP expect the annual cost of the new service to fall between £25 million and £50 million and that around 560,000 absentees will use it every year. The new scheme will employ occupational health nurses, occupational therapists, physiotherapists, occupational physicians, and other appropriate experts, and will recommend interventions at a total cost

SICK PAY PURELYPAYROLLMAGAZINE28

In other words, these are the very statutory records that would be required to settle a dispute about absence and payment of SSP. And yet the DWP recommends such statutory record keeping requirement be abolished. You see what I mean?

PURELYPAYROLL.COM FEBRUARY 2014

The current statutory requirement to keep SSP records extends to keeping a record of (as per HMRC Helpsheet E14 to 5 April 2014):

all dates of employee sickness lasting four or more days in a row, including for employees who are under 16 years old

a record of the payment dates and the amount paid during each PIW [Period of Incapacity for Work] the date the pay period began a record of any unpaid SSP with reasons form SSP2 Statutory Sick Pay (SSP) record sheet to help you keep a record of your payments.

The only way the keeping of SSP records could be abolished is if employers didn’t have a statutory liability to pay SSP in the first place.

May be that’s what the government is leaning towards. Another proposal recommended by DWP is “commissioning research to explore the details of sickness absence management and sick pay regimes in different types of organisations.” In other words, if the majority of employers are meeting a satisfactory level of sick pay, why impose statutory requirements on all employers that really only apply to that minority of employers who only currently pay SSP? Therefore, might it be that employers will no longer be required to pay SSP, but rather be encouraged to devote more resources to managing sickness absence and getting incapacitated workers back to work more quickly?

The first step towards this possible eventuality is the abolition of the Percentage Threshold Scheme (PTS).

of between £20 million and £85 million. The benefit to the government of

this outlay is the increase in revenues from income tax and National Insurance contributions from workers getting back more quickly to productive working – forecast at £100 to £215 million, and in reduced benefit expenditures of a further £30 to £60 million. DWP estimate that employers will save £80 to £165 million a year in reduced sickness absence payments, while economic output will increase by £450 to £900 million. The DWP estimate that it costs employers £9 billion a year to deal with work absences, so any reduction in these figures must be welcome.

With the abolition of PTS, DWP estimate that employers will save the cost of the additional administrative burden associated with the scheme, saving employers costs of between £2.5 and £5 million per annum.

Although PTS is being abolished from April 2014, employers will still be able to make claims for reimbursement of SSP under PTS (paid for sickness periods up to 5 April 2014) until the end of the 2015/16 tax year.

Tax exemption for employer financed health-related interventionsA targeted upcoming tax exemption was announced in the 2013 Budget, so that an employer can obtain a certain amount of income tax exemption on monies spent to help employees back to work.

In the 5th December Autumn Statement 2013 it was announced: “As announced in Budget 2013, legislation will be introduced to exempt from

income tax expenditure by employers on recommended medical treatment where an employee has been absent from work due to ill-health or injury. Following consultation, the Government will extend the exemption to medical treatments recommended by employer-arranged occupational health services. The exemption will be subject to an annual cap of £500 per employee, and is likely to come into effect in autumn 2014.”

Therefore, in conclusion…The government’s whole policy thrust

seems to be geared towards the better control of sickness absence in the first place, and then the rapid intervention of employers and their health advisors to get incapacitated workers back into work as quickly and as reasonably as possible.

PURELYPAYROLLMAGAZINE SICK PAY 29

PURELYPAYROLL.COM FEBRUARY 2014

Therefore, in conclusion…

The government’s whole policy thrust seems to be geared towards the better control of sickness absence in the first place, and then the rapid intervention of employers and their health advisors to get incapacitated workers back into work as quickly and as reasonably as possible.

Therefore, as employers will no longer be able to recovery any SSP at all from April 2014 onwards, and with the new health and work assessment and advisory service coming on-stream later in 2014, and the upcoming income tax exemption for an employer’s medical interventions, may be the statutory requirement to pay a specific amount of SSP will end up being scrapped?

WHY SOCIAL MEDIA WILL NOT WORK FOR YOU PURELYPAYROLLMAGAZINE30

PURELYPAYROLL.COM FEBRUARY 2014

Disappointingly, the conclusion I have come to is that for many of the people who engage our services, social media will be a complete waste of their time! And here’s why…

Steve Phillip

One of my greatest frustrations is witnessing the initial enthusiasm of some of our clients to learn how to use LinkedIn and other social media to grow their business, and then watching it turn into a complete lack of any progress.

For some time, I have asked myself, why it is that Pareto’s 80/20 principle appears to apply itself so rigorously to the progress of these clients? Often, once training has happened, 20% of our course participants go away and do great things, building networks, engaging with useful contacts, and then turning that engagement into new business. As for the remaining 80%…

Why social media will not work for you - The unpleasant truthThere’s a well-used saying ‘If you always do what you’ve always done, you’ll always get what you’ve always got’. This saying applies to social media and it’s why many individuals and teams are failing to make LinkedIn et al, work for their businesses.

Disappointingly, the conclusion I have come to is that for many of the people who engage our services, social media will be a complete waste of their time! And here’s why…

Sir Ken Robinson, the brilliant creativity expert, explains in one of his Ted Talks, how many people have become brainwashed by an education process which has much akin to the fast food industry. This franchise

PURELYPAYROLLMAGAZINE WHY SOCIAL MEDIA WILL NOT WORK FOR YOU 31

PURELYPAYROLL.COM FEBRUARY 2014

a known, as well as a like and trust, factor with your audience.

The mistakes most businesses makeUnfortunately, the mistake I see most businesses make is to expect social media to work when applying a fast food, franchise mentality.

Let me use a further analogy – Most of us can drive a car and often with the minimal of conscious effort. A Formula 1 car has the power to enable you to drive faster than you could ever imagine and in the right hands it can help you become a world champion.

Why social media will not work for you - The unpleasant truth

concept, applied to the objective of building brand awareness and marketing, would have us believe that if we replicate other successful models and implement their strategies, to the letter, then we will be successful. To some degree this may be true. However …

The greatest challenge you face in business, I believe, is how you stand out from the crowd, especially, when faced with previously unparalleled levels of competition. The solution can be found in your uniqueness – your ability to differentiate what you have to offer your clients and how you communicate that difference, whilst building

WHY SOCIAL MEDIA WILL NOT WORK FOR YOU PURELYPAYROLLMAGAZINE32

PURELYPAYROLL.COM FEBRUARY 2014

To succeed in business, using social media, it is vital that you “disenthrall” yourself (free yourself from a controlling force or influence) of the things you have always done, recognise that professional networking and marketing has changed and then rise with the occasion – only then will you truly succeed.

However, it only takes a few seconds, sat in the cockpit of such a vehicle, to appreciate that just getting out of first gear, into second, is a major feat in itself.

You need lessons and a significant number of laps under your belt to make any kind of progress in a Formula 1 car. With practise and time, you will eventually manage to get into, 2nd, 3rd, 4th gear and beyond – your lap times become faster, and eventually you’re competing with the big boys. You’ve just had to learn to drive a car all over again, and I’d suggest that mastering social media is no different.

When in history, as a professional, have you had the facility to search, locate, and engage with virtually anyone in business you choose, often for free and generally within seconds – from a device that fits in the palm of your hand? You now have the Formula 1 of marketing vehicles and you want to use it to become a world champion – but without lessons and without putting in the laps? No wonder so many are failing to win the constructor’s championship, when it comes to using social media!

Here is the uncomfortable truth… If you really want social media to work and generate more opportunities for you to do business, with more people, then you need to identify your uniqueness, communicate it clearly via your social media profiles and messaging and… you must put in the laps.

Certainly, your regularly scheduled

LinkedIn status updates and tweets will get your brand seen by more people, more often. However, they will do little to create interest and barely achieve anything if you’re looking to attract new clients – unless you’re prepared to engage and involve yourself in conversations, with those

you want to do business with.You see, if you’re someone who

struggles to reply to emails and phone messages, what makes you think you’re going to be any more effective with your communication when using social media? The truth is, you probably won’t be.

We must all recognise that times have changed and if you keep on doing what is comfortable and familiar, you will not grow. Ken Robinson, in his talk, explains that anyone who is over the age of 25 still wears a wristwatch, when those under 25 choose not to. Why is this? The over 25s have always worn a wristwatch and would not consider not doing so. The under 25 year old has grown up in a digital age, where time is everywhere; they have moved with the times.

Abraham Lincoln’s Second Annual Address to congress on 1st December 1862 sums it up extremely well. “The dogmas of the quiet past are inadequate to the stormy present. The occasion is piled high with difficulty, and we must rise with the occasion. As our case is new, so we must think anew and act anew. We must disenthrall ourselves, and then we shall save our country.”

questions answers

Can you please tell me how the payment of bank holidays fits in with an employee’s entitlement to a minimum amount of paid annual leave each year?

PURELYPAYROLL.COM FEBRUARY 2014

Firstly, ordinary employees are not legally entitled to be paid for bank holidays; it’s only bank employees that have that right. Whether other employees are entitled to be paid is up to what is agreed between employees and employer. It’s always recommended that, for example, any details about paid bank holidays are expressly stated in terms and conditions.

When the statutory entitlement to paid annual leave was first introduced, employees were entitled to four weeks’ paid annual leave (e.g. 20 days for someone working five days a week). Employers were allowed to include as part of this, for example, 20 days, any bank holidays. Effectively this meant employee’s annual leave could end up being only 12 days, with eight days having to be taken as bank holidays.

Q Questions You Ask... Answers that Work

Answer from Adrian Hobbs

Question

MAY 2012 PURELYPAYROLL.COM

AThe whole of the government’s thrust concerning company cars is to drive down pollution. This means the more fuel e�cient and lower a car’s CO2 emissions the less income tax an employee will pay.

When deciding what type of car to go for, the �rst step will be to ascertain any car’s CO2 emissions. At Appendix 2 of HMRC booklet 480(2012), you can �nd tables for the tax years 2011/12 to 2013/14 setting out the percentage of a car’s list price that will be taxed depending on its level of emissions. At Budget 2012, tables for the tax year 2014/15 to 2016/17 were published.

These tables show the ‘squeeze’ on emissions. Except for ultra-low carbon emission cars, the tables start with a percentage of 15% of the car’s list price. For 2011/12, a car needs to have a rounded down CO2 �gure of 121g/km to be taxed at 15%; for the tax year 2016/17, the car will need a CO2 �gure of less than 95g/km to be taxed at the same rate. In other words, if an employee wants to pay less tax by 2016/17 they’ll have to be driving an ultra-low carbon emission car.

Diesel cars generally have a much lower CO2 rate than equivalent petrol cars. But they’ve been hit by an extra 3% supplement. The good news is that this supplement is being withdrawn from 6 April 2016, so that diesel cars are subjected to the same level of tax as petrol cars. So providing diesel cars may still be one of your best options – they have lower CO2 emissions, and they manage more miles to the gallon. However, against this must be set the often additional capital cost of purchasing a diesel car, and the currently much more expensive price of diesel.

Of course, LPG fuelled cars, whether a petrol/LPG hybrid or a car that only runs on LPG, could prove tax e�cient. They also generally have lower CO2 emissions than cars that just run on petrol. Also, LPG is cheaper than petrol or diesel, and the number of fuel stations selling LPG is growing all the time. As at 4 April 2012, average UK prices at the pump were 78.7p/litre for LPG; 141p/litre for petrol; and 147.3p/litre for diesel. But then we don’t know what the government may do to LPG prices in the years to come!

Answers from Adrian Hobbs

The unions objected to this practice and the government agreed, from April 2009, to introduce a minimum entitlement to 5.6 weeks’ paid annual leave (e.g. a maximum of 28 days for someone working at least five days a week or more). Therefore, where an employer includes bank holidays in an employee’s statutory entitlement to paid annual leave, most employees will still end up with being able to take an additional four weeks’ paid leave (e.g. 20 days for someone working five days a week).

Many employers now allow employees to take a full up to 28 days’ paid annual leave, and pay for bank holidays taken in addition. Employers can agree whatever they like with employees as long as they comply with an employee’s minimum statutory rights.

PURELYPAYROLLMAGAZINE Q&A 33

2014 TUPE CHANGES PURELYPAYROLLMAGAZINE34

PURELYPAYROLL.COM FEBRUARY 2014

The Transfer of Undertakings (Protection of Employment) Regulations 2006 (TUPE) provides protection for employees when there is a business transfer. The Government has been reviewing employment rights legislation as part of its ‘red tape challenge’ commitment to deregulation and to avoid what it regards as unnecessary “gold plating” of EU Directives.

Anne-Marie Balfour

Trevor Bettany

2014 TUPE changes

PURELYPAYROLLMAGAZINE 2014 TUPE CHANGES 35

PURELYPAYROLL.COM FEBRUARY 2014

As a result, amending legislation has been put in place. On 10 January 2014, a final draft of the snappily entitled Collective Redundancies and Transfer of Undertakings (Protection of Employment)(Amendment) Regulations 2014 was laid before Parliament. These Regulations came into force on 31 January 2014. What changes do these new Regulations contain?

The Transfer of Undertakings (Protection of Employment) Regulations 2006 (TUPE) provides protection for employees when there is a business transfer. The Government has been reviewing employment rights legislation as part of its ‘red tape challenge’ commitment to deregulation and to avoid what it regards as unnecessary “gold plating” of EU Directives.

The most eye-catching original proposal put out for consultation was to abolish “service provision changes”, which the UK introduced in 2006 to make clear that TUPE applied to outsourcing, the changeover of contractors, and contracting back in-house.

However, the underlying EU Acquired Rights Directive did not require the UK to apply TUPE to service provision changes and therefore represents “gold-plating.” The consultation exercise provoked an outcry of complaints that the abolition of “service provision changes” would restore the uncertainty which they were introduced to avoid. The Government hastily changed its view and now regards service provision changes as an example of “where good regulation, additional to that required by the European Directive, can deliver benefits for both businesses and individuals.” In this instance, it is correct.

Whilst some of the more far-reaching original proposals have been dropped, significant changes remain.

2014 TUPE CHANGES PURELYPAYROLLMAGAZINE36

PURELYPAYROLL.COM FEBRUARY 2014

Service provision changesWhilst service provision changes have been retained, they have also been clarified. The new regulations make it clear that the activities to be performed post-transfer must be “fundamentally the same as the activities carried out previously”.

Narrower unfair dismissal protectionPrior to 31 January 2014, a dismissal was automatically unfair if the reason for that dismissal was either (i) the transfer (unless for an ETO reason) or (ii) a reason connected with the transfer.

Following the changes, only a dismissal on ground (i) will be automatically unfair. A dismissal for a reason merely connected with the transfer will not be automatically unfair.

In practice, there will be disputes about whether a dismissal is because of the transfer or for a reason ‘connected with’ the transfer.

Variation of termsFollowing a TUPE transfer, the transferee (the ‘new’ employer) often wishes to harmonise the terms and conditions of the transferred employees with the rest of its workforce. However, TUPE provided that detrimental changes to terms and conditions by reason of the transfer or a reason connected with the transfer would be void – even if the employee agrees – unless the change is for an ETO reason. Harmonisation is not an ETO reason.

The Government wanted to make variations easier for transferees. It is, however, constrained by the provisions of

the EU Directive. The amendments that the new regulations make in this area are: Variation is now permitted (subject to normal principles) if:

The sole or principal reason for the change is not the transfer itself;

The sole or principal reason for the change is an ETO reason, provided that the employer and employee agree that variation; or

The terms of the contract permit the employer to make such a variation (which begs the question - is it a variation at all?);

The terms being varied are incorporated from a collective agreement and:

More than one year has passed since the transfer; and

The overall rights and obligations in the employee’s contract, when considered together, are no less favourable.

ETOs - economic, technical or organisational reasonsA dismissal by reason of a transfer will not be automatically unfair if it is for an ‘economic, technical or organisational’ reason entailing changes in the workforce (ETO).

Similarly, a variation of contract by reason of a transfer will not be invalid if it is for an ETO.

However, it is not always easy to identify what counts as ‘changes in the workforce’ when seeking to establish an ETO. Redundancy dismissals and

variations of contract often arise when the transferee changes the place of work. The new regulations assist by confirming that changes in the location of the workforce count as ‘changes in the workforce’.

Terms and Conditions determined by collective agreementsSome employees’ terms and conditions are determined by collective agreements made between a trade union and the employer. Previously, it has been unclear whether, and to what extent, terms and conditions determined by collective agreements would be amended post transfer by changes in a collective agreement to which the transferee is not party and therefore has no opportunity to negotiate.

The new regulations provide statutory clarity that a ‘static’ approach applies. Terms and conditions determined by any collective agreements will be frozen at the point of transfer. Any subsequent changes will not automatically transfer, so long as the transferee is not a participant in the collective bargaining process for such change.

Further, those terms can be varied when more than one year has passed following the transfer, provided that the contract terms are, overall, no less favourable to the employee.

Pre-transfer collective redundancy consultationA transferee will often wish to implement redundancies or vary contracts on or following a transfer. If 20 or more

PURELYPAYROLLMAGAZINE 2014 TUPE CHANGES 37

PURELYPAYROLL.COM FEBRUARY 2014

redundancies are proposed, a collective “redundancy” process will be triggered. This requires a 30 day consultation period, rising to 45 days for 100+ redundancies. This consultation is distinct from the separate statutory duty to inform and consult with representatives of affected employees under TUPE.

Previously, a transferee could only lawfully commence the collective redundancy process once it became the employer – i.e. on or after the transfer date. In practice, many employers took a chance and consulted earlier to limit delay.

The new regulations confirm that, where a TUPE transfer is likely, collective redundancy consultation by a transferee that takes place before that TUPE transfer still “counts”. There is, however, no obligation to do so and the transferor (the ‘old’ employer) must agree. Sometimes, of course, the transferor will not want to give the transferee direct access to its employees, for commercial reasons.

Employee Liability InformationWhere TUPE applies, the transferor has always been obliged to provide ‘employee liability information’ to the transferee. This involves providing certain information about the employment terms and liabilities which the transferee will inherit and must honour.

Having originally proposed the removal of the obligation altogether, as a result of further opposition to the proposal, the obligation has not only been retained but beefed up. Employee liability information must now be provided 28

2014 TUPE CHANGES PURELYPAYROLLMAGAZINE38

PURELYPAYROLL.COM FEBRUARY 2014

(rather than 14) days prior to the transfer. Whilst the change is helpful to

transferees, some regard it as a missed opportunity to broaden the scope of the information that must be provided. For example, there is still no obligation to provide information relating to employees’ share options or non-contractual benefits.

Micro Businesses and consultationEmployers are obliged to inform and consult with elected representatives

of affected employees affected by a transfer.

The new regulations allow businesses with ten or fewer employees to consult directly with the employees, rather than with their elected representatives - unless there is a recognised trade union or existing representatives.

A new TUPE guidance document will be published in due course by the Department for Business, Innovation and Skills. Acas have also promised to publish updated guidance.

Timing of the Changes

Employee liability information - must be provided 28 days, rather than 14 days, prior to TUPE transfers that take place on or after 1 May 2014.

Collective agreements - the statutory clarification applies to transfers taking place on or after 31 January 2014. However, given the decision in Parkwood Leisure Limited v Alemo Herron, this merely clarifies the current legal position.

Definition of ETO ‘changes in the workforce’ and narrower automatic unfair dismissal protection - applies to transfers taking place on or after 31 January 2014 and notice to terminate the employment is given (or, where no notice is given, the employment terminates) on or after 31 January 2014.

Pre-transfer redundancy consultation - unclear, but unlikely to apply to consultation taking place before 31 January 2014.

Micro businesses (direct TUPE consultation) - applies only to transfers taking place on or after 31 July 2014.

Variation of terms - Transfers taking place on or after 31 January 2014 and variations agreed on or after that date.

Service provision changes - new wording applies to TUPE transfers that take place on or after 31 January 2014.

For further information contact: [email protected]

purelypayroll.com

Purely PayrollNo.3, 8 Brentwood RoadBrentwood, Essex. CM13 3QHT: 00 44 1277 888760

Purely Payroll provides specialist global payroll training courses

both In-house and public, in any location across the globe.

Our specialist trainers can tailor make a course to fit your requirements

Global Payroll/HR Solutions

Advanced Business Solutionst: 01582 714 873e: [email protected]: www.advancedcomputer software.com/absc: Duncan Miller

Cintra HR & Payroll Servicest: 0191 478 7000e: [email protected]: www.cintra.co.ukc: Nham Lee

EMS Ltdt: 0207 562 2445e: [email protected]: www.expat-services.co.ukc: Mark Jacklin

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

Frontier Softwaret: 0845 370 3210e: [email protected]: www.frontiersoftware.comc: Sales Team

Cegedim SRHt: 0870 888 1034e: [email protected]: www.cegedim-srh.comc: Dave Hull

Integrated International Payroll Ltdt: +44 0208 144 8760e: [email protected]: www.iipay.comc: Vanessa Knowlden

Global Payroll/HR Outsourced Payroll Solutions

Cegedim SRH is a European payroll bureau, we help companies focus on their core business by delivering competencies specific to managing Payroll and Human Resources. Cegedim SRH utilises TEAMSHCM, its new Global HR management and Payroll platform developed with Java technology. Cegedim SRH offers outsourcing services tailored to each company, regardless of its size, sector or geographic scope (national, multi-national or International). this includes companies ranging in size from mid-market to large corporations.

Cegedim SRHt: 0870 888 1034e: [email protected]: www.cegedim-srh.comc: Dave Hull

PURELYPAYROLL.COM FEBRUARY 2014

DIRECTORY PURELYPAYROLLMAGAZINE40

tech

Find a new business partner Purely Payroll Magazine Directory profiles your organisation each month to payroll and HR professionals

Liberata UK Ltdt: 0208 603 3300e: [email protected]: www.liberata.comc: Stuart Clark

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

Bond Payroll Servicest: 01903 707123e: [email protected]: www.bondpayrollservices.comc: James Payne Outsourced Payroll Solutions

Carval Computing Ltdt: 01098 787700e: [email protected]: www.carval.co.ukc: Emma Clare

Cintra HR & Payroll Servicest: 0191 478 7000e: [email protected]: www.cintra.co.ukc: Nham Lee

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

Frontier Softwaret: 0845 370 3210e: [email protected]: www.frontiersoftware.comc: Sales Team

Liberata UK Ltdt: 0208 603 3300e: [email protected]: www.liberata.comc: Stuart Clark

Intelligo Software Limitedt: 0800 0390116e: [email protected]: www.intelligosoftware.co.ukc: Fiona Cullinane

Cegedim SRHt: 0870 888 1034e: [email protected]: www.cegedim-srh.comc: Dave Hull

Integrated International Payroll Ltdt: +44 0208 144 8760e: [email protected]: www.iipay.comc: Vanessa Knowlden

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

PURELYPAYROLL.COM FEBRUARY 2014

PURELYPAYROLLMAGAZINE DIRECTORY 41

Saget: 0845 111 99 88e: customer. [email protected]: www.sage.co.uk/outsourcec: Pierre Chan

Wealden Computing Servicest: 020 8364 7177e: [email protected]: www.wealden.netc: George Williams

Bond Payroll Servicest: 01903 707123e: [email protected]: www.bondpayrollservices.comc: James Payne

P11D Expenses and Benefits

Carval Computing Ltdt: 01098 787700e: [email protected]: www.carval.co.ukc: Emma Clare

Cintra HR & Payroll Servicest: 0191 478 7000e: [email protected]: www.cintra.co.ukc: Nham Lee

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

Liberata UK Ltdt: 0208 603 3300e: [email protected]: www.liberata.comc: Stuart Clark

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

Saget: 0800 6940568e: [email protected]: www.snowdropkcs.co.ukc: Pierre Chan

Bond Payroll Servicest: 01903 707123e: [email protected]: www.bondpayrollservices.comc: James Payne

Payroll Consultancy

Integrated International Payroll Ltdt: +44 0208 144 8760e: [email protected]: www.iipay.comc: Vanessa Knowlden

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

Liberata UK Ltdt: 0208 603 3300e: [email protected]: www.liberata.comc: Stuart Clark

PURELYPAYROLL.COM FEBRUARY 2014

DIRECTORY PURELYPAYROLLMAGAZINE42

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Payroll Alliancet: 020 8401 1828/9e: [email protected]: www.payrollalliance.comc: Linda Pullan

Purely Payrollt: 020 3291 2995e: [email protected]: www.purely-payroll.comc: Melanie Pizzey

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

Bond Payroll Servicest: 01903 707123e: [email protected]: www.bondpayrollservices.comc: James Payne

Payroll & HR Software Providers

Advanced Business Solutionst: 01582 714 873e: [email protected]: www.advancedcomputer software.com/absc: Duncan Miller

Bottomline Technologiest: 01420 547600e: [email protected]: www.albany.co.ukc: Jacqui Powell

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

Bond Payritet: +44 (0) 1293 789940 e: [email protected]: www.bondpayrite.comc: Robert Cooper

Bond Teamspiritt: 01376 519413e: [email protected]: www.bondteamspirit.comc: Joanne Ward

Carval Computing Ltdt: 01098 787700e: [email protected]: www.carval.co.ukc: Emma Clare

Cascade HR Ltdt: 0113 2554115e: Andy.court@cascadehr. co.ukw: www.cascadehr.co.ukc: Andy Court

Integrated International Payroll Ltdt: +44 0208 144 8760e: [email protected]: www.iipay.comc: Vanessa Knowlden

Frontier Softwaret: 0845 370 3210e: [email protected]: www.frontiersoftware.comc: Sales Team

PURELYPAYROLL.COM FEBRUARY 2014

PURELYPAYROLLMAGAZINE DIRECTORY 43

Intelligo Software Limitedt: 0800 0390116e: [email protected]: www.intelligosoftware.co.ukc: Fiona Cullinane

Moorepayt: 0845 184 4615e: [email protected]: www.moorepay.co.ukc: Fran Williams

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

Saget: 0800 6940568e: [email protected]: www.snowdropkcs.co.ukc: Pierre Chan

Wealden Computing Servicest: 020 8364 7177e: [email protected]: www.wealden.netc: George Williams

PURELYPAYROLL.COM FEBRUARY 2014

Bond Payroll Servicest: 01903 707123e: [email protected]: www.bondpayrollservices.comc: James Payne

Recruitment

Employer Services Ltd t: 01277 230656 e: [email protected]: www.employerservices.co.ukc: Kim Hutchings

NorthgateArinsot: 0800 035 0545e: [email protected]: www.northgatearinso.co.ukc: Sally Greene

Purely Payrollt: 020 3291 2995e: [email protected]: www.purely-payroll.comc: Melanie Pizzey

Safe Computingt: 0844 583 2134e: [email protected]: www.safecomputing.co.ukc: Renata Jones

Time & Attendance

Advanced Business Solutionst: 01582 714 873e: [email protected]: www.advancedcomputer software.com/absc: Duncan Miller