what’s happening tuesday december 16, 2008. doug lindholm & william mcarthur council on state...

TRANSCRIPT

What’sHappening

Tuesday

December 16, 2008

Doug Lindholm & William McArthurCouncil on State Taxation Tyco Electronics

Fred MarcusPrincipal, Horwood, Marcus, and Berk, Cht.Matt LauerMatt Lauer

Ginny Buckner KisslingPrincipal, Ryan, Inc.Meredith VieiraMeredith Vieira

Hosted by

&&

Chris Matthews & Chris Matthews & Tom BrokawTom Brokaw

withwith

Program Jack Harper, North CarolinaBruce Ely, AlabamaJonathan Block, Maine / New HampshireJeff Saviano, MassachusettsTom Steele, CaliforniaMark Eidman, TexasFred Nicely, OhioPat Van Tiflin, Michigan

Program Kurt Kawafuchi, HawaiiJohn Barrie, MissouriDale Busacker, MinnesotaJason Wyman, IllinoisJames Wetzler, New YorkDick Genetelli, New YorkDavid Shipley, Pennsylvania / New Jersey

NEWS BREAKNEWS BREAK

Presented by

&

Marc SimonettiAssociate

Sutherland Asbill & Brennan

Bill TownsendPartner

Fowler White Boggs Banker LLP

FEATURING SPECIAL GUESTS:

Mr. Mark EidmanPartner

Scott, Douglass & McConnico LLPAustin, Texas

Mr. Fred NicelyTax Counsel

Council On State TaxationWashington, DC

Mr. Patrick Van TiflinPartner

Honigman, Miller, Schwartz, and Cohn LLP

Lansing, Michigan

FEATURING SPECIAL GUESTS:

Mr. James WetzlerDirector, Multi-State Tax Group

Deloitte Tax LLPNew York, New York

Mr. Richard GenetelliPresident

The Genetelli Consulting GroupNew York, New York

Mr. David ShipleySpecial Counsel

McCarter & English, LLPPhiladelphia, Pennsylvania

PowerPoint Presentation

To access this presentation, go to:www.ryanco.com

orwww.saltlawyers.com

North Carolina Developments

Mr. Jack HarperVice President, Corporate TaxWachovia CorporationCharlotte, North Carolina

Wal-Mart Stores East v. Tolson, 06 CVS 3938 Sam’s East v. Tolson, 06 CVS 3929

• North Carolina Department of Revenue forced combination of Wal-Mart Stores, REIT and REIT Holding Company

• Disallowed REIT’s dividends paid deduction and REIT Holding Company DRD

• Wal-Mart sues for refund• Extensive Wall Street Journal Coverage on Tax

Advice Received from Ernst & Young

Wal-Mart Stores East v. Tolson, 06 CVS 3938 Sam’s East v. Tolson, 06 CVS 3929

• Trial Court Rules Against Wal-Mart on all Counts• Wal-Mart appeals to N.C. Court of Appeals.• Oral Arguments held Late October 2008• Decision expected January 2009

In the Matter of the Summons Issued to Ernst & Young, LLP et al.; No. COA07-1219, North Carolina Court of Appeals (August 5, 2008)

• NC Department of Revenue Issues Summons to E&Y to Produce Documents

• Work Product Privilege Claim Rejected by Trial Judge• Wal-Mart Intervenes and Appeals to NC Court of Appeals• Documents Remanded Back for in camera Review• Appeals Court Rules Summons is Subject to Rules of Civil

Procedure• DOR Appeals to NC Supreme Court on Rules of Civil Procedure

Issue

Other North Carolina Developments

• Franchise Tax Changes for REITs (no reduction to capital stock base for aggregate market value of investments).

• Corporate Tax Return Due Date Changed.• Guidance Issued for Alternative Apportionment

Requests.

Alabama Developments

Mr. Bruce ElyPartnerBradley Arant Rose & White LLPBirmingham, Alabama

Recent Developments in Alabama

• Never-ending Franchise Tax Litigation -- is there finally an end (a refund) in sight? Vulcan Lands, Inc. v. ADOR

• Add-Back Statute Litigation and Legislation -- VFJ Ventures, Inc. v. ADOR and Alabama Act 2008-543

• Facially Discriminatory Business Privilege Tax Deduction -- AT&T Corp. v. ADOR

Recent Developments in Alabama• Business/Non-business/Non-unitary Income Resulting

from Stock Sale: Tate & Lyle Ingredients Americas, Inc. v. ADOR

• Is Unitary Combined Reporting Coming to Alabama? An update and some very unofficial predictions

• Bad Debt Sales Tax Litigation: Does anybody get the deduction? Home Depot USA v. ADOR/Wells Fargo Financial v. ADOR

NEWS BREAKNEWS BREAK

Maine / New Hampshire DevelopmentsMr. Jonathan BlockPartnerPierce Atwood LLPPortland, Maine

Massachusetts Developments

Mr. Jeffrey SavianoNortheast Director of State and Local TaxErnst & Young LLPNew York, New York / Boston, Massachusetts

Maine: Aircraft Use Tax

• Assessing 5% Use Tax on Aircraft that Land in Maine• There are several possible statutory exemptions, but

M.R.S. is interpreting them as applying only to in-state purchases of aircraft

• M.R.S. interpretation discriminates against interstate commerce

• Many court challenges pending• Applies also to yachts

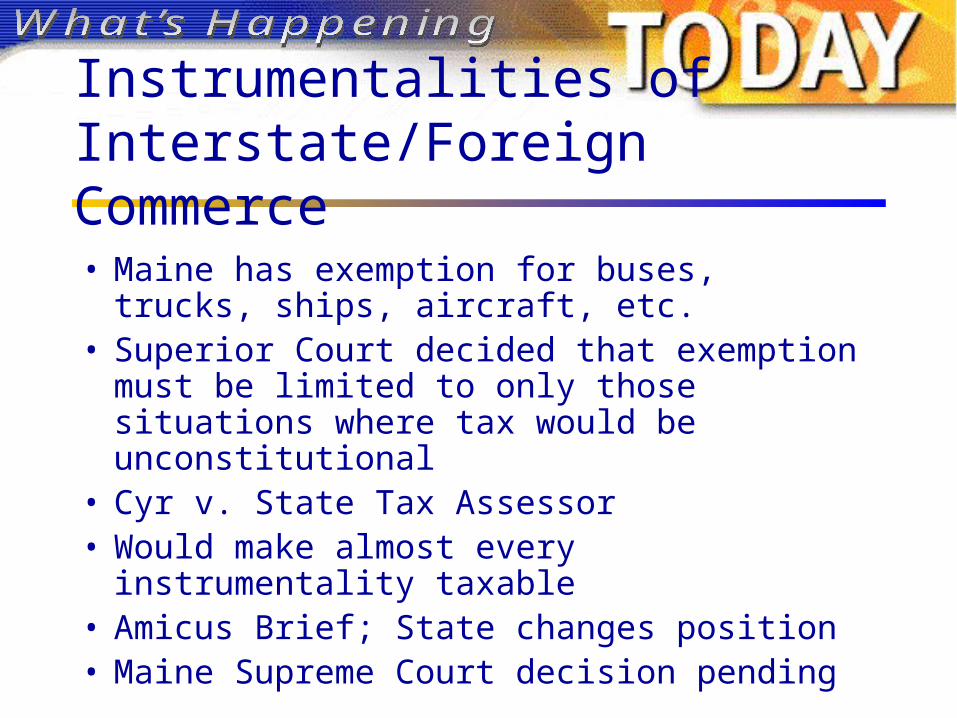

Instrumentalities of Interstate/Foreign Commerce

• Maine has exemption for buses, trucks, ships, aircraft, etc.

• Superior Court decided that exemption must be limited to only those situations where tax would be unconstitutional

• Cyr v. State Tax Assessor• Would make almost every instrumentality taxable• Amicus Brief; State changes position• Maine Supreme Court decision pending

Constitutional Issue May Be Raised at Any time

• State v. Thompson• Taxpayer failed to appeal residency issue in a timely

manner• State filed collection action• Taxpayer attempted to raise non-residency as a

defense• Maine Supreme Court: Residency issue could be

collaterally attacked notwithstanding failure to appeal underlying assessment

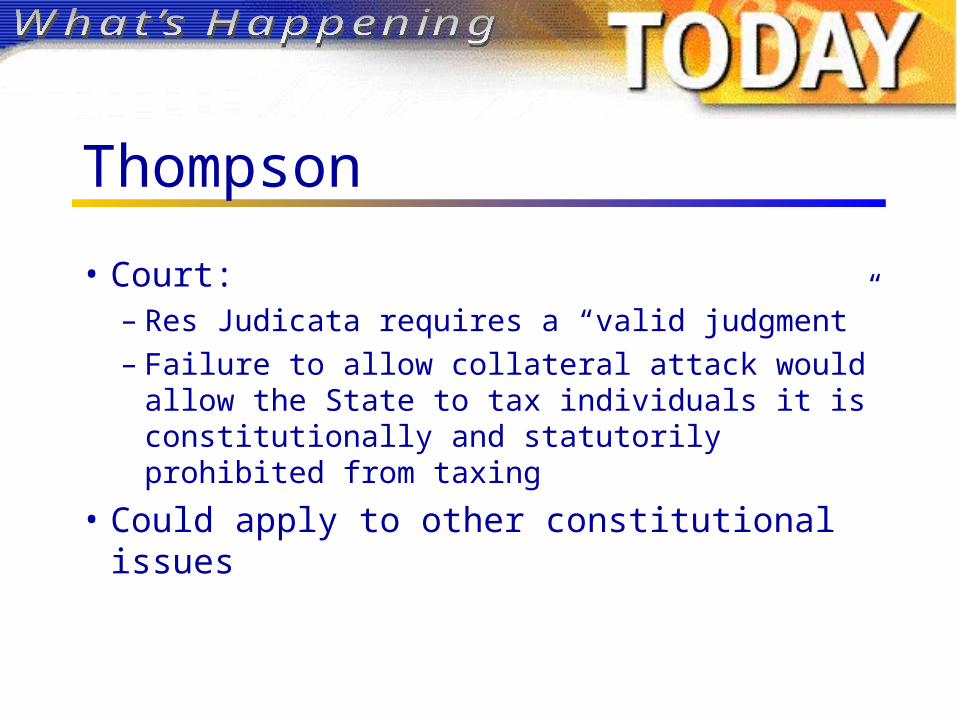

Thompson

• Court: – Res Judicata requires a “valid judgment”– Failure to allow collateral attack would allow the

State to tax individuals it is constitutionally and statutorily prohibited from taxing

• Could apply to other constitutional issues

Apportionment: Nelnet v. Assessor• Student Loan company• Assessor argued that interest and servicing

fees were Maine numerator sales because they were “incidental” to sales made in Maine; i.e. loans disbursed to Maine colleges

• Maine/MTC Rule: “interest income, service charges, …incidental to a sale must be included as sales in the state to which the sale is attributable…”

Nelnet Case

• Superior Court: Interest income not incidental to a “sale”. A loan is not a sale. Loan income (i.e. interest) is not incidental to any sale. It is the predominant purpose of the transaction

Income Producing Activities

• Court: Only activities of the “taxpayers” (i.e. Maine-nexus members of the unitary group) may be considered in analysis

• Me Rule: IPA does not include activities performed on behalf of taxpayer, such as those performed by independent contractor

• Assessor: Activities performed by employees of non-nexus unitary business entities may not be considered

Nelnet

• Nelnet: Rule excluding IC’s from consideration in determining IPA inconsistent with IPA statute. No such limitation in statute.

• Court: Activities of employees of other group members are not akin to activities of an IC and must be included in IPA analysis

Nelnet• Summary• Interest income not “incidental” to a Maine sale• Only Maine-nexus corporations of UB are considered

for purposes of determining IPA• Activities of employees of other group members

performed on behalf of Maine-nexus entities are considered

• COP was greater in another State; therefore not Maine sales

• Subject to appeal

Alternative Apportionment Formulas

• Assessor pushing hard• E.g., entertainment producers

– Apportionment by audience• Case by case basis; no rules• Penalties for failure to anticipate

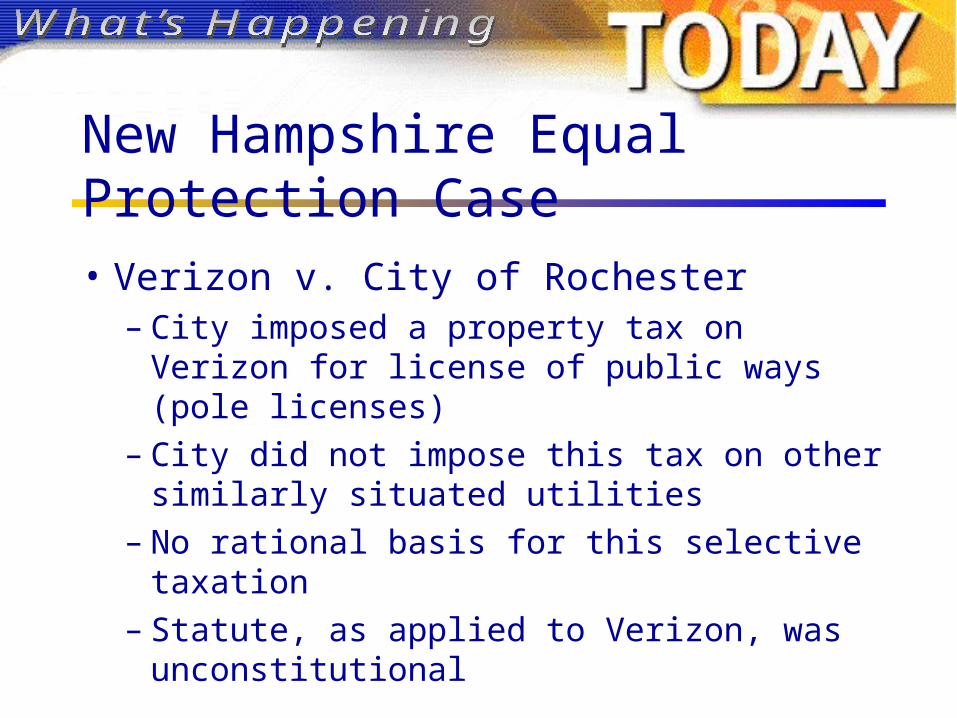

New Hampshire Equal Protection Case

• Verizon v. City of Rochester– City imposed a property tax on Verizon for license of

public ways (pole licenses)– City did not impose this tax on other similarly situated

utilities– No rational basis for this selective taxation– Statute, as applied to Verizon, was unconstitutional

Massachusetts Legislation• Adoption of Unitary Reporting Required for Tax Years

Beginning on or After 1 January 2009– 50% ownership threshold. – Unitary business broadly defined – Tax imposed on a “water’s edge” basis

• Certain foreign affiliates included• Ten year election to use worldwide group• Ten year election to include non-unitary members of

federal affiliated group

Massachusetts Legislation

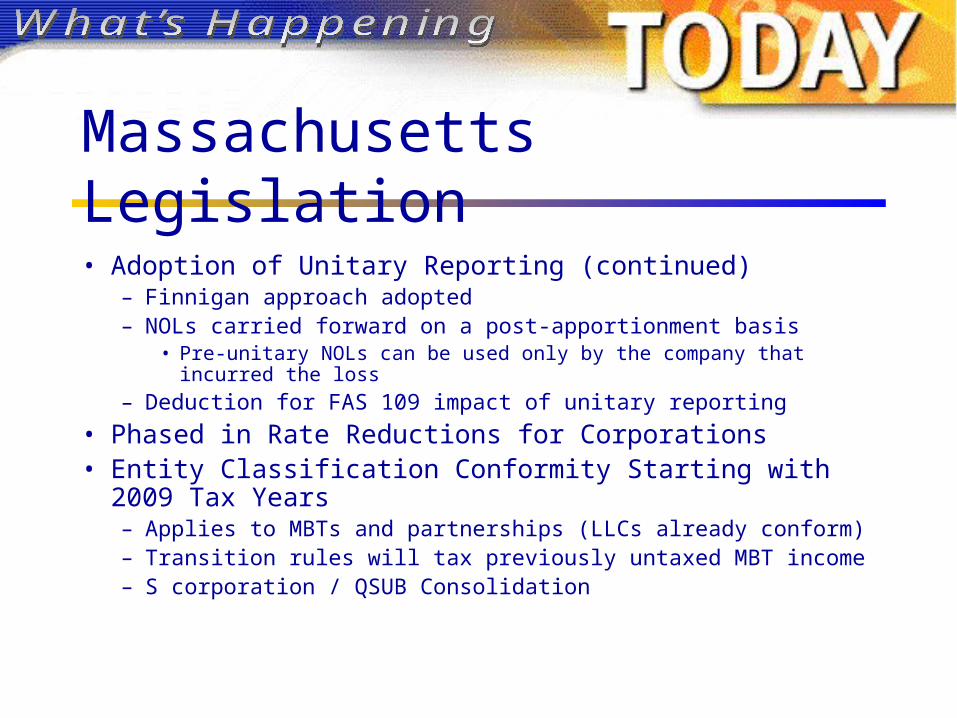

• Adoption of Unitary Reporting (continued)– Finnigan approach adopted– NOLs carried forward on a post-apportionment basis

• Pre-unitary NOLs can be used only by the company that incurred the loss– Deduction for FAS 109 impact of unitary reporting

• Phased in Rate Reductions for Corporations• Entity Classification Conformity Starting with 2009 Tax Years

– Applies to MBTs and partnerships (LLCs already conform) – Transition rules will tax previously untaxed MBT income – S corporation / QSUB Consolidation

Massachusetts Legislation• Public Law 86-272 no Longer Applicable to Non-Income Measure

of the Excise• Massachusetts Specific Basis Rules Adopted• Goodwill Eliminated from Massachusetts Sales Factor• Incentives for Life Sciences Companies

– Administered by the Life Sciences Center – Maximum annual benefit: $25M per year– Incentives include: FDA user fee credit, ITC, research credit, throwback

relief, expanded NOL, orphan drug deduction, sales tax exemptions, R&D classification, additional cash grants and loans

California Developments

Mr. Thomas SteelePartnerMorrison & Foerster LLPSan Francisco, California

California in Economic Crisis• As of September, 2008

– Projected State Budget Shortfall for 2008-2009: $15 billion– Three way struggle:

• Assembly Republicans (“Cut expenditures”) • Assembly Democrats (“Raise taxes”)• Governor (“Structural reform required”)

– Solution:• Spending cuts• Borrowing• Accelerate tax revenues• Commission to Study Alternatives : Report due April 15, 2009

– Professor Pomp appointed to Commission

Steps to Accelerate Tax Revenues

• New Strict Liability Penalty for Underpayments of Corporate Tax (R&T Code sec. 19138)– Understatement in any taxable year in excess of $1 million

• Taxes of members of combined group to be aggregated– Taxable years beginning on or after 1/1/03– Penalty of 20% of entire understatement– Understatements applicable to tax years beginning before 1/1/08

may be eliminated by amended return and payment before 5/31/09

– Relief only if FTB erred in computing penalty amount

Steps to Accelerate Tax Revenues

• New penalty in addition to other penalties• Not applicable if due to “change of law” or

reliance on written legal ruling by the Chief Counsel

Steps to Accelerate Tax Revenues

• Example– Taxpayer XYZ suffers $100 million asset loss in 2003– Responding to prior Amnesty Penalty, XYZ overpays 2003

tax and files a California claim for refund for $10 million– Pending resolution of claim, XYZ continues to claim in 2003

and later years amortization deductions of $10 million per year (worth $1 million in California taxes) relating to asset that became worthless acknowledging such deductions will be reversed when claim is granted

Steps to Accelerate Tax Revenues

• Example (continued)– Assuming 2003 claim is granted in full by FTB in 2010:

• FTB owes XYZ $10 million (plus interest) for 2003• XYZ owes $7 million (plus interest) for understated

income for 2003 – 2009 • Despite a net refund due, XYZ apparently owes $1.2

million (20% of $6 million) in penalties• Only offsets which occur in the same year reduce penalty

Steps to Accelerate Tax Revenues

• NOLs Suspended for 2 years (1/1/08-1/1/10)– Carry over period increased for suspension– Move to 20 year period– NOL carry back starting 2011

• LLC Fee accelerated to June of current tax year• Temporary 50% limits on credits (2008-2009)

Steps to Accelerate Tax Revenues

• Modification of Federal Estimated Taxes Rules (R&T Code secs. 19125 & 19136.3)– Early period quarterly installments now exceed 25% – 90% of prior year’s income doesn’t apply to AGI of

$1 million or more – Applicable to tax years beginning on or after 1/1/09

Continuing Economic Crisis

As of December 4, 2008– Projected additional budget shortfall of $11 billion– Discussion of New Taxes: Governor’s proposal

• 1.5% increase in state sales tax (for three years) to create nation’s highest sales tax (8.75% to 10.75% depending upon the district)

• Expansion of sales tax to cover certain services (e.g. appliance and furniture repair, amusement fees, vehicle repair, amusement parks, sporting and golf fees, veterinary services).

• An oil severance tax of 9.9 percent of gross value of oil produced in California. Low-value stripper oil would be exempt, as would oil owned or produced by the state or local governments

• Increases excise taxes on alcoholic beverages by the equivalent of a nickel a drink (1.5 ounces of spirits, 12 ounces of beer, or 5 ounces of wine), effective March 1, 2009

– Other alternatives under discussion

LLC Litigation

• Ventas Finance I, LLC v. FTB, 165 Cal. App. 4th 1207 (2008)– Follows Northwest Energetic– LLC fee a tax, not a fee– Under Complete Auto must be apportioned rather than

based on 100% of gross receipts wherever earned– Taxpayer stipulated to proper apportionment

percentages for income tax

LLC Litigation

• Ventas Finance I, LLC v. FTB, 165 Cal. App. 4th 1207 (2008) Continued– Court adopted those apportionment percentages to

determine the lawful tax v. unconstitutional amount to be refunded

– Attorney fees under CCP sec. 1021.5 but remanded to see if taxpayer still a “successful party” and as to amount

– Taxpayer’s petition to the California Supreme Court was denied

Gross or Net Receipts in Sales Factor

• Continuing confusion despite (or because of) Cal. Supreme Court’s decisions in Microsoft and General Motors– What is debt and what is marketable security?

• FTB fix? See Regulation 25137(c)(1)(D) (gross receipts from treasury function activity to be thrown out of sales factor unless taxpayer establishes taxpayer demonstrates this treatment creates distortion)

Gross or Net Receipts in Sales Factor

• Continuing confusion despite (or because of) Cal. Supreme Court’s decisions in Microsoft and General Motors– What is distortion?

• Qualitative v. Quantitative distortion • Super-unitary test?• Compare profit margins where activities are not “Super-

unitary”

Gross or Net Receipts in Sales Factor

• General Mills, Inc. v. FTB, No. 439929 (Cal. Super. Ct., SF County, 9/26/2007), appeal pending– Gross Receipts from commodity sales in futures market

not “true sales” because not binding obligations, have no value at inception and not driven by profit motives

• Inconsistent with factual record, long legal history of futures contracts and federal tax treatment

• Inconsistent with California Supreme Court’s decision in Microsoft holding that sales of marketable securities generated “gross receipts”

Gross or Net Receipts in Sales Factor

• Microsoft v. FTB II (Sup. Ct. SF County)– Distortion cuts both ways: e.g., no intangibles in the

property factor

Retribution

• Hyatt v. FTB, No. A382999 (Nev. Dist. Ct., 8th Dist., 8/6/08)– Follows decision by U.S. Supreme Court that

California FTB not immune from suit for tortious conduct in Nevada

– Jury award of $138 million in compensatory damages

Retribution

• Hyatt v. FTB, No. A382999 (Nev. Dist. Ct., 8th Dist., 8/6/08)– Jury award of $250 million in punitive damages– Based on evidence of outrageous auditor conduct

including • sifting through Hyatt’s trash• unfounded accusations to Hyatt’s friends • religious slurs

What’sHappening

Tuesday

December 16, 2008

FEATURING SPECIAL GUESTS:

Mr. Mark EidmanPartner

Scott, Douglass & McConnico LLPAustin, Texas

Mr. Fred NicelyTax Counsel

Council On State TaxationWashington, DC

Mr. Patrick Van TiflinPartner

Honigman, Miller, Schwartz, and Cohn LLP

Lansing, Michigan

Margin Tax Uncertainties

• What is included in “total revenue”?• What is included in “cost of goods sold”?• What is included in “compensation”?• Do I qualify for a specific revenue deduction?• Do I qualify for the lower tax rate for retailers and

wholesalers?

Texas

Total Revenue

• The starting point for the total revenue calculation is line 1c of the federal return

• Any methodology acceptable for reporting line 1c under federal law is acceptable for Texas franchise tax purposes

• Gross or net reporting may be used

Texas

Cost of Goods Sold

• Includes “taxes paid in relation to acquiring or producing any material, or taxes paid in relation to services that are a direct cost of production”

• Does not include “selling costs” or “distribution costs”

• Is the tax in question a tax on production or a tax on sales or distribution?

Texas

Compensation

• Includes wages, compensation, and benefits• Benefits do not include employee discounts,

payroll taxes, or “working condition amounts” provided so employees can perform their jobs

• What is included in working condition amounts?

Texas

Specific Deductions

• Management companies may exclude reimbursements of specified costs from total revenue

• Definition of “management company” is very broad• The Comptroller intends to issue guidance clarifying

the deduction and excluding shipping companies

Texas

Retailers/Wholesalers

• Tax rate is .5% for entities primarily engaged in retail or wholesale trade

• Who qualifies?– Standard Industrial Classification Manual – Utilities excluded– Revenue from retail/wholesale trade must be greater than

revenue from other trades, and less than 50% of revenue from retail/wholesale trade can come from the sale of products it or an affiliated entity produces

• What does “produces” mean?

Texas

Future Legislative Changes

• Potential legislative changes to be considered during the 2009 legislative session:– Apportionment:

• Which standard will be used for unitary combined reports?– Joyce or Finnegan.– Certain legislative leaders believe Joyce method is a “loophole.”– Information from Finnegan reporting requirement.

– Special deductions for certain industries– Deductibility of 1099 payments.

Texas

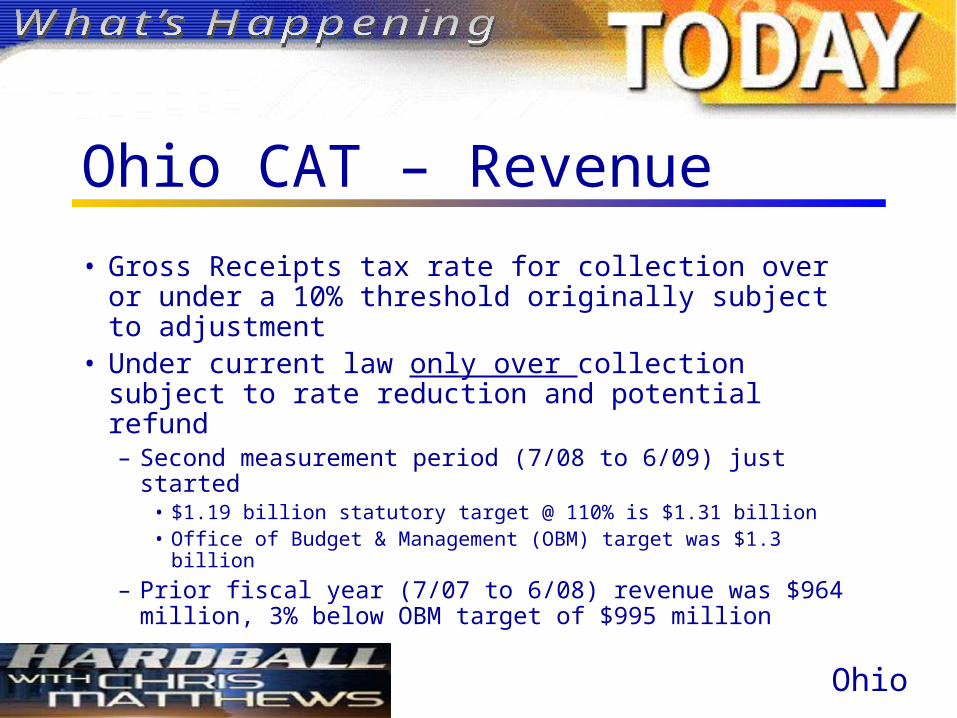

Ohio CAT – Revenue

• Gross Receipts tax rate for collection over or under a 10% threshold originally subject to adjustment

• Under current law only over collection subject to rate reduction and potential refund– Second measurement period (7/08 to 6/09) just started

• $1.19 billion statutory target @ 110% is $1.31 billion• Office of Budget & Management (OBM) target was $1.3 billion

– Prior fiscal year (7/07 to 6/08) revenue was $964 million, 3% below OBM target of $995 million

Ohio

Are the Other Taxes Really Being Phased Out?

• Last year for general businesses to file a personal property tax return was 2008; telecommunications companies have until 2010 and most utilities remain subject to tax

• Last year for general businesses to file a corporation franchise tax return is 2009

• Full 21% phase-down of Ohio’s personal property tax takes place in 2009

Ohio

Is the CAT a Transactional Tax? What’s the Impact?

• Ohio’s Constitution– Two provisions address food ($188 million)

• Food for off-premise consumption, and• Items used to manufacture food or food sold at wholesale, including

packaging– One provision addresses motor fuel ($139 million)

• Revenue raised from taxes or fees imposed on motor fuel must be spent for public road projects

• Does it impact state’s economic nexus provision? • As a transactional tax would it be subject to the Quill physical presence

standard?

Ohio

Future of the CAT

• Weak economy – will the CAT be adjusted to balance the state’s budget?

• Adverse litigation on food and/or motor fuel– Increase CAT– Subject those industries to alternative taxes (e.g., franchise tax and/or property tax)

• Disfavor of using a Gross Receipts Tax– Adjustments for pyramiding of tax– Pressure for tax credits for investments in the state– Tax based on ability to pay – income based

Ohio

Nexus – Constitutional Issues

• Does in-state physical presence for more than one day constitute “substantial” nexus?

• Is economic nexus sufficient to establish “substantial” nexus?

Michigan

Expense Disallowance – Constitutional Issues

• Does the addback requirement result in effectively taxing the out of state recipient?

• Does the addback requirement result in taxation of income that is out of all appropriate proportion to activity done within the state?

Michigan

Apportionable Income – Constitutional Issue

• Does the definition of “business activity” include income that is not constitutionally apportionable to the state?

Michigan

Unitary Business – Constitutional Issue

• Does the definition of “unitary group” result in unfair apportionment of income that is not constitutionally apportionable to Michigan?

Michigan

Finnigan – Constitutional Issue

• Does inclusion in the sales factor numerator of in-state sales made by affiliates that do not have nexus in the state result in unconstitutional inclusion of income apportioned to the state?

Michigan

State Specific Credits – Constitutional Issues

• Do state specific credits unconstitutionally discriminate against interstate activities?

• Do state specific credits result in unfair apportionment?

Michigan

Administrative Provisions (continued)

• Sec. 205.27a(2) . . . The taxpayer shall not claim a refund of any amount paid to the department after the expiration of 4 years after the date set for the filing of the original return . . .

• Sec. 205.27a(6) Notwithstanding the provisions of subsection (2), a claim for refund based upon the validity of a tax law based on the laws or constitution of the United State or the state constitution of 1963 shall not be paid unless the claim is filed within 90 days after the date set for filing a return

Michigan

NEWS BREAKNEWS BREAK

Hawaii Developments

Mr. Kurt KawafuchiDirectorHawaii Department of TaxationHonolulu, Hawaii

Agenda

• An in-depth review of significant developments from the Hawaii region.– Revitalization and Stimulus Initiatives– Current Developments– Compliance Projects– Pending Administrative Guidance

Governor Lingle’s 5-Point Economic Revitalization Plan

• Increase Tourism Marketing• Fiscal Stimulus: Investment in Facilities and

Infrastructure• Lower Fees and Tax Relief• Attract Capital & Investment: Green or Renewable

Energy Initiatives, e.g., Electric Cars• Partnerships with Private & Federal Government and

Attracting Federal Funds

Department’s Initiatives

• Encouraging and Stimulating Investment and Economic Activity

• Creating Fairness and a Level-Playing Field by Addressing the Tax Gap

• Improving Services, e.g., periodic GE tax forms

Current Developments

• Cash Bond Deposits to Suspend Running of Interest

• Effective immediately. • Will toll 8.0% interest; but taxpayer earns no interest. • Similar to Rev. Proc. 84-58. • Must make disclosures. • Entitled to return of money. • Accomplished through agreement.

Current Developments

• Elimination of “Pay to Play” Requirement• All controversies get “one bite of the apple” for free. • No need to prepay tax to the Taxation Board of Review of

Tax Appeal Court.• Must pay for second appeal.• Applies to all taxes.

Current Developments

• Enactment of “Deemed Denial” Statute• Allows taxpayers to sue for a refund after 180 days of the

date of the claim; provided that notice of denial was not provided within that period.

• Deemed denials are to be reviewed by the Taxation Board of Review or the Tax Appeal Court “on the merits.”

• First case litigating under this theory is currently docketed. (Research Credit controversy)

Current Developments

• Background• Hawaii does not have a sales tax. • Rather, it has a gross proceeds general excise tax equal

to 4% of essentially all business transactions. • Hawaii has a 0.5% wholesale rate on TPP and services. • A privilege tax on gross income with several exemptions. • Prior to 2007, no local tax on business proceeds.

Current Developments

• New Legislation• Law was amended to provide for a 0.5% GET rate for

proceeds from goods or services provided to satisfy a warranty obligation. Reduces rate from 4.0% to 0.5%.

• Must be a "true warranty," versus an extended warrant that is more like insurance.

• Effective July 1, 2008.

Current Developments

• Baker & Taylor: Hawaii Supreme Court held that taxpayer had nexus and upheld 4.0% general excise tax but reversed 0.5% tax rate

• Hawaii Legislature passed legislation to clarify Baker & Taylor retroactively to codify a prior administrative rule (i.e., regulation). This las gave rise to a string of use tax refund cases.

• CompUSA Tax Appeal Court decision

• Prospective Relief in Certain Circumstances• Modifications post-Baker & Taylor extending the use tax to imports of "sales"

is applied prospectively and also, apply Halliburton principles. Plan to issue a Tax Information Release.

Current Developments

• Honolulu’s County Surcharge• First local tax in Hawaii history. • Prior to January 1, 2007, no local municipality had a tax

on the sales proceeds of a business. • Applies to all transactions at the 4% rate. • Effective tax rate with proceeds sourced to Honolulu is

4.5%.

Current Developments

• Honolulu’s County Surcharge (cont’d.)• Sourcing Rules Developed

– Tangible Personal Property—where delivered– Services—where consumed– Commissions—where services rendered– Rental Personal Property—where property used– Rental Real Property—where property located– Contracting—where job located– Interest—where investment controlled– Theaters and Amusements—where event located

Compliance Projects

• Fairness and Addressing the “Tax Gap”• Apportionment and Multistate Taxpayers• Transfer Pricing Abuse• The Cash Economy• Monitoring Development Elsewhere

– Economic Nexus (MBNA and Lanco)– Online Travel Company litigation

Pending Administrative Guidance

• Cash Bond Deposits--TIR• Taxation of the Film Industry—Rules• Export Incentives/Use Tax/0.5% Wholesale

Transactions—Rules• Scientific Contract GET Exemption—TIR• 41(d) Prototype—TIR• Halliburton Analysis—TIR

Missouri Developments

Mr. John BarriePartnerBryan Cave LLPWashington, DC

Nexus in Missouri – Sales and Use and Corporate Income Tax (Letter Ruling LR4643, April 1, 2008)

• Out-of-state sales person travels to Missouri to generate sales. Most of purchases delivered by company’s own trucks into Missouri.

• Company required to collect and remit Missouri use tax on sales to Missouri customers.

• Company subject to Missouri corporate income and franchise taxes– engaged in business in Missouri and deriving income from

Missouri sources.

Nexus in Missouri – Instate Advertising (Letter Ruling LR4702, April 21, 2008)

• Non-nexus vendor did not get nexus by advertising products in Missouri.

• Vendor did not have any physical presence in Missouri.

• US mail to deliver products to Missouri customers.

Electronic Transfers in Missouri – Sales tax exposure? (Letter Rulings LR5052 and LR5058, August 29, 2008)

• Sales of electronic courses offered via the internet not subject to Missouri sales or use tax – interactive computer services and electronic publishing not subject to tax.

• Sales or use tax should be collected on cost of materials unless the fee for course materials is separately stated and sales tax collected from attendees.

• Sales of downloadable copyrighted photographs over the Internet in exchange for a monthly fee not subject to sales or use tax – not a transfer of tangible personal property.

IRC 1031 “Like Kind” Exhanges – Not eligible for Missouri “Trade In” Rules if Intermediary Used

• Great Southern Bank v. Director of Revenue, Missouri Supreme Court November 4, 2008.

• Taxpayer exchanged airplanes through use of a qualified intermediary that satisfied IRC 1031 “like kind” exchange rules.

• Taxpayer sought to only pay use tax on increase in value of new airplane over cost of old airplane under Missouri’s “trade in” rule.

• Court found two separate transactions – therefore not eligible for “trade in” rule.

Statute of Limitations – Saturday means Friday

• Insurance Company of the State of PA, et al. Director of Revenue et al, Missouri Supreme Court November 4, 2008.

• Out-of –state insurers sought refunds of the tax they overpaid with respect to insurance premiums. Refund claims mailed on Friday, June 1, 2007 – received by Department of Revenue on Monday, June 4, 2007.

• Statute of Limitations expired on Saturday, June 2, 2007.• Refunds denied as untimely since statute providing for

refund claims did not have either a timely mailing or Saturday rule.

Fees Paid to Fitness Facility Subject to Sales Tax

• Michael Jaudes Fitness Edge, Inc. v. Director of Revenue, Missouri Supreme Court, April 1, 2008.

• Because the fitness facilities constituted a place of recreation, fees subject to sales tax.

• Court found that the distinction between fees paid for personal training sessions in a place of recreations (taxable) and fees paid directly to a personal trainer on an independent basis (nontaxable) a reasonable one

– no violation of Missouri's Constitutional uniformity requirement

Bowling League Qualified as a Civic Organization

• Missouri State USBC Association v. Director of Revenue, Missouri Supreme Court, April 29, 2008.

• Bowling league qualified as a tax exempt “civic” organization because its activities were recreational and available to public at large.

NEWS BREAKNEWS BREAK

Minnesota Developments

Mr. Dale BusackerDirector, State and Local TaxesGrant Thornton LLPMinneapolis, Minnesota

What Happened in 2008?

• Streamlined conformity – repeal of the fur tax• Income tax conformity – through February 13, 2008• Bonus depreciation – 80% addback and deduct this

amount over five years• Disallow payments to a governmental agency for

violation of a law

What Happened in 2008?(continued)

• Tax debtor data match• Corporate Tax Reform Commission - report due

February 15, 2009• Sales Tax Increase of .375% starting July 1, 2009 to

fund programs to improve the outdoors, water quality, parks and the arts

• More tax auditors approved

Foreign Operating Corporation

• 80% of income must be from foreign sources

• Addback for payments made to FOC for interest, royalties, factoring, or for DPD from a captive REIT

• Economic substance Grant of authority to Revenue Department Provision not enacted

HMN Financial – Pending in Tax Court

• Minnesota bank owns an FOC which owns a REIT. The bank contributed one-third of its Minnesota mortgage loan portfolio to the REIT. Bank dismantled structure within two months after law was changed in 2005.

• Department's Position:• Transfer of the loan portfolio to the REIT lacked economic

substance.• Payroll with the bank needs to be imputed to the FOC.• The bank never acted on its business purpose for the REIT or for

the FOC.

BNSF Railway – Pending in Tax Court

• BNSF Railway owed about $5.5 billion to two of its subsidiaries located in Canada and which were FOCs. The Department admits that these two companies qualify as FOCs.

• Department's Position:• The interest payments lack economic substance and business

purpose• No business purpose or economic substance to capitalize these

FOCs with more than $5 billion in intercompany notes

Challenge to JOBZ

• Olson Case• December 18, 2007 – Appeals Court said taxpayers

lack standing. The decision was not appealed.

• Interstate Motor Trucks• Filed by businesses who claim that they directly

compete with businesses who receive benefits under JOBZ.

• October 10, 2008 – District Court said taxpayers lack standing.

Income Received by Former Residents

• Law change – Minnesota will tax income that was earned while a resident but was received while a nonresident.

• Revenue Notice 8-10 and Withholding Tax Fact Sheet 19 Severance pay Equity based awards Other non-statutory deferred compensation

• Administrative issues and penalty relief

Sales Tax – Transfers to a SMLLC

• Law exempts transactions that qualify under §351 or 721

• Rule Hearing held June 30, 2008 – ALJ decision issued September 3

• Held: Transfers to SMLLC not covered under the law and are taxable

• Lack of consideration – is receipt of a membership interest in a SMLLC consideration?

Illinois Developments

Mr. Jason WymanPartnerDeloitte Tax LLPChicago, Illinois

What Type of Receipt is it?Type of receipt Sourced to Throw out rule

Tangible personal property

Delivery point None

Intangible — dealer Customer location None

Intangible — nondealer Income producing activity

No income- producing activity

Intellectual property Where utilized < 50% of gross receipts

Service Where received TP not taxable in state of receipt

Rendition of Services• Prior law:

– Each income-producing activity was sourced to Illinois if a greater proportion of the cost of performance took place in Illinois than outside Illinois (e.g., >50%)

– Cost of performance only included direct costs, under GAAP– Favors out of state service providers

Rendition of Services• For years ending on or after December 31, 2008, IITA

304(a)(3)(c-5)(iv) provides ordering rules for determining sourcing of services– Sales of services are in Illinois if the services are received

in Illinois– Deemed receipt at the Ordering Office– Deemed receipt at the Billing Address

Rendition of Services• The fixed place of business rule

– Gross receipts from the performance of services provided to a corporation, partnership, or trust may only be attributed to a state where that corporation, partnership, or trust has a fixed place of business

– The term “fixed place of business” has the same meaning as that term is given in IRC Section 864 and the related Treasury regulations. IITA 1501(a)(9.5)

Rendition of Services• The ordering office rule

– The services shall be deemed to be received at the location of the office of the customer from which the services were ordered if• The state where the services are received is not readily

determinable, or • The customer which is a corporation, partnership, or trust does not

have a fixed place of business in the state where the services are received

Rendition of Services• The billing address rule

– If the ordering office cannot be determined, the services shall be deemed to be received at the office of the customer to which the services are billed

Rendition of Services• Throw out rule

– If the taxpayer is not taxable in the state in which the services are received, the sale is excluded from both the numerator and the denominator of the sales factor

– Taxability in another state as defined in Existing Regulation 100.3200, which is the same regulation as used for throwback

Interest and Sales of Intangible Property• IITA 304(a)(3)(C-5)(iii)(a)

– Dealers in Intangibles within the meaning of IRC Section 475(c)(1)• IRC Section 475(c)(1) states that a “dealer in securities” is a

taxpayer who– Regularly purchases securities from or sells securities to customers in the

ordinary course of a trade or business; or– Regularly offers to enter into, assume, offset, assign, or otherwise terminate

positions in securities with customers in the ordinary course of a trade or business

– GIL - IT 08-0028 – expands beyond stated IRC securities

Interest and Sales of Intangible Property• For Dealers in Intangibles

– The income from the sale of intangible property is sourced to Illinois if it is received from a customer in Illinois

– Residence or domicile is deemed to be the billing address, unless the taxpayer has actual knowledge of the residence or domicile

– Applies to Interest, net gains (but not less than zero) and other items of income from intangible personal property

Interest and Sales of Intangible Property• IITA 304(a)(3)(C-5)(iii)(b)• In the case of all other taxpayers

– If the greater portion of the income-producing activity takes place in Illinois, based on the cost of performance

– Applies to Interest, net gains (but not less than zero) and other items of income from intangible personal property

– However, under the Existing Regulation 100.3370(c)(3)(A) the mere holding of an intangible is not an income-producing activity

Interest and Sales of Intangible Property

• Existing Regulation 100.3380(c)(2)– Incidental or occasional sales of assets used in the regular

course of the taxpayer’s trade or business are excluded from the sales factor.

– According to the IDOR this applies to sales of intangible property

Publishing Services• Under Sale of Services — statute directs IDOR to

adopt rules for Publishing Services – IITA 304(a)(3)(C-5)(iv)

• Draft Regulation Section 100.3373• Publishing Services — publishing, selling, licensing or

distributing newspapers, magazines, periodicals, trade journals or other printed material.

• Does not include licensing of Intellectual Property covered under IITA 304(a)(3)(B-1)

Publishing Services• Printed Material — physical embodiment or printed

version of any thought or expression, including a play, story, article, column or other literary, commercial, educational, artistic or other written or printed work

• May be contained on any property or medium including electronic medium

• Excludes Broadcasting covered by Section 100.3372

• Excludes licensing of Intellectual Property covered under IITA 304(a)(3)(B-1)

Publishing Services• Publishing sales include

– Gross receipts from sale of printed material in form of tangible personal property as provided in Sections 100.3370(c) [destination and throwback rules] and 100.3380(c) [special rules]

– Other Gross receipts from advertising and sale, rental, or other use of customer lists using the taxpayer’s Circulation Factor

• Circulation Factor — for each individual publication the in-state circulation over total circulation– Rating statistics reflected in sources, such as Audit Bureau of

Circulations– Source must be consistently used year to year

Publishing Services • Fixed Place of Business Rule — receipts from Corporation,

Partnership or Trust cannot be sourced to a state where Customer does not have a fixed place of business

• Services Sourced To Ordering Office when– Customer does not have a Fixed Place of Business in the state

where services are received or– If the state where received is Not Readily Determinable

• Services Sourced to Billing Address if Ordering Office cannot be determined

• Throw Out Rule — if Taxpayer is not taxable in state where service is received

Intellectual Property• For tax years ending on or after 12/31/1999 • Throw Out Rule — IITA 304(a)(3)(B-2)

– “Gross receipts from the license, sale, or other disposition of patents, copyrights, trademarks and similar items of intangible personal property”

– ARE EXCLUDED from Numerator and Denominator• Exception

– Such Receipts are 50% or more of Unitary Business Group’s Total Receipts

– For current and 2 preceding tax years• Test is for the entire Unitary Business Group

Intellectual Property• Draft Regulation 100.3370(a)(2)(F)

– Gross Receipts includes damages and settlements from claims for infringements

– Gross Receipts from licensing, sale, or other disposition of patents include ONLY amounts received from person using the patent in production, fabrication, or manufacturing

– Gross Receipts from licensing, sale, or other disposition of copyright include ONLY amounts received from person engaged in printing or other publication of material protected by copyright

– Does not include — Publishing or Broadcasting within Sections 100.3372 or 100.3373

Intellectual Property• Draft Regulation 100.3370(a)(2)(F) — limits the scope

of throw out rule• Note that draft regulation would take license of

computer software or music for personal use out of this rule

• Existing Regulation 100.3380(c)(5) — net gains from sale of business intangibles, including patents and copyrights, are included in the factor

Intellectual Property• For tax years ending on or after 12/31/1999 • IITA 304(a)(3)(B-1)

– Only applies if more than 50% receipts for current year and previous 2 years are from IP

• Treated as IL sales– Patents if employed in production in IL– Copyrights if printing or publication originates in IL– Trademarks and other IP if commercial domicile of purchaser is in IL

Intellectual Property

• If production or publication occurs in more than one state, then amount in IL is receipt from transaction multiplied by– Licensee’s receipts from product produced in IL – divided by licensee’s receipts from all product produced

• Throw Out Rule - If place of utilization cannot be determined from taxpayer’s books and records

NEWS BREAKNEWS BREAK

What’sHappening

Tuesday

December 16, 2008

FEATURING SPECIAL GUESTS:

Mr. James WetzlerDirector, Multi-State Tax Group

Deloitte Tax LLPNew York, New York

Mr. Richard GenetelliPresident

The Genetelli Consulting GroupNew York, New York

Mr. David ShipleyPartner

McCarter & English, LLPPhiladelphia, Pennsylvania

• Budget deficits– Significant audit activity

• Forced combination• De-combination

• Planning strategies– Assess implications

Combined Reporting Developments and Controversies

NY

NY VDA Program• VDA program

– NY has historically negotiated VDA’s and Pre-Audit Payment Agreements.

– New law creates legal basis for program and right to participate.

• Receipt of notice no bar to participating• However, ongoing criminal investigation or audit is a bar• Not available for reportable or listed transactions

– Eliminates need for anonymity

New York

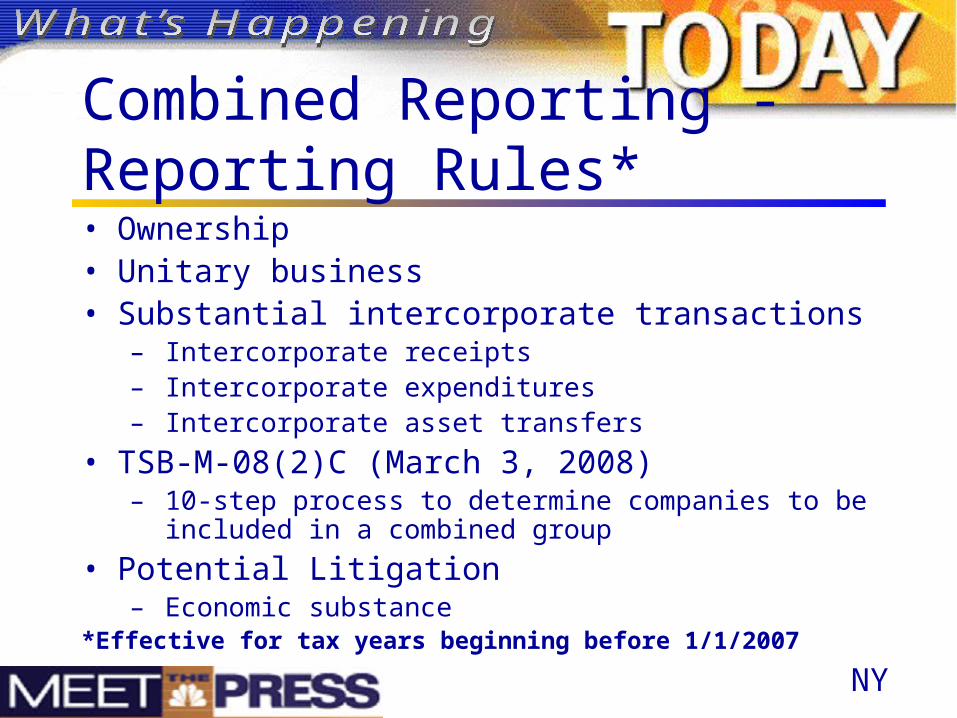

• Ownership• Unitary business• Distortion• Critical issues

– Documentation– New combination rules in New York State

*Effective for tax years beginning before 1/1/2007

Combined Reporting - General Requirements*

NY

Sourcing of Receipts from Electronic Activities• NY law contains a residual category of “other business receipts”

sourced to where the income is earned. Tax Law §210.3(a)(2)(D)• Advisory opinions provided for customer based

sourcing of income from electronic sale of various intangibles. See TSB-A-02(3)C (dealing with Internet sales of gift certificates), TSB-A-99(16)C (dealing with information services accessed electronically), and TSB-A-00(15)C (also dealing with information services)

• On audit, the Department has been treating a variety of electronic activities as “other business receipts” and asserting customer-based sourcing.

• Litigation expected New York

• Ownership• Unitary business• Substantial intercorporate transactions

– Intercorporate receipts– Intercorporate expenditures– Intercorporate asset transfers

• TSB-M-08(2)C (March 3, 2008)– 10-step process to determine companies to be included in a combined

group• Potential Litigation

– Economic substance*Effective for tax years beginning before 1/1/2007

Combined Reporting - Reporting Rules*

NY

• Unitary business• Distortion

– How much is needed• Sale of a subsidiary

– Bausch and Lomb decision• TSB-M08(3)C (March 10, 2008)

Significant Controversies

NY

Pennsylvania Taxation of Computer Software

• Graham Packaging – Commonwealth Court - sale of electronically transmitted software is taxable.

• Department’s Reaction – Changed position and began taxing electronic delivery but limited case to software and not other digital goods.

• Dechert – Commonwealth Court followed Graham Packaging; Argued before PA Supreme Court.

PA

Pennsylvania Treatment of Intangible Holding Companies

• Intangible Addback Statute – Not the preferred method but may be considered as a revenue raiser.

• Geoffrey Regulation? – Department is “reading cases” and “examining options.”

• Current position is not to assert intangible nexus.

PA

Throwout Rule - Litigation

• The New Jersey Tax Court held that the throwout rule is facially constitutional finding that it could operate constitutionally in some instances such as where 1) Receipts excluded from sales-factor; denominator are generated from New Jersey; 2) It has no material effect on sales factor; and 3) The property and payroll factors temper the effect of the throwout rule on the sale factor.

NJ

Throwout – Legislative Changes• Assembly Bill 2722 / Senate Bill 1874 – Repeals

the throwout rule.• Passed Assembly on October 27, 2008.• Amended version unanimously passed Senate on

November 24, 2008 and Assembly on December 15, 2008.

• Fiscal Note projects cost to be $89 million.

NJ

New Jersey Cases• Praxair – Intangible nexus only applicable from 1996

forward; Remanded on penalty issue.• New Jersey Natural Gas – No regular place of

business, no right to apportion, but taxpayer permitted taxes paid credit.

• Clorox – Transfer to subsidiary in IRC § 351 transaction does not require “recoupling” with federal depreciation.

NJ

Changes at the Division of Taxation

• Retired – Richard Schrader (Asst. Dir. of Audit), Bill Bryan (Chief, Conferences and Appeals), Nick Catalano (Chief, Regulatory Services) and John Metzger (Regulatory Services).

• Promoted – Denise Lambert-Harding (Deputy Director), Michele Bartolomei (Asst. Director of Audit), Paul Provost (Chief, Conferences & Appeals).

NJ

What’sHappening

Tuesday

December 16, 2008

Holiday Greetings!

To access this presentation, go to:www.ryanco.com

orwww.saltlawyers.com