when cost can kill ethical challenges facing cost accountants

Post on 19-Dec-2015

217 views

TRANSCRIPT

When Cost Can KillEthical Challenges Facing Cost Accountants

When Cost Can KillEthical Challenges Facing Cost Accountants

Ukleja Center for Ethical Leadership, CSULB

2

Why do cost accountants need ethics?

What are the consequences of unethical cost accounting behavior?

Why do cost accountants need ethics?

What are the consequences of unethical cost accounting behavior?

Ukleja Center for Ethical Leadership, CSULB

3

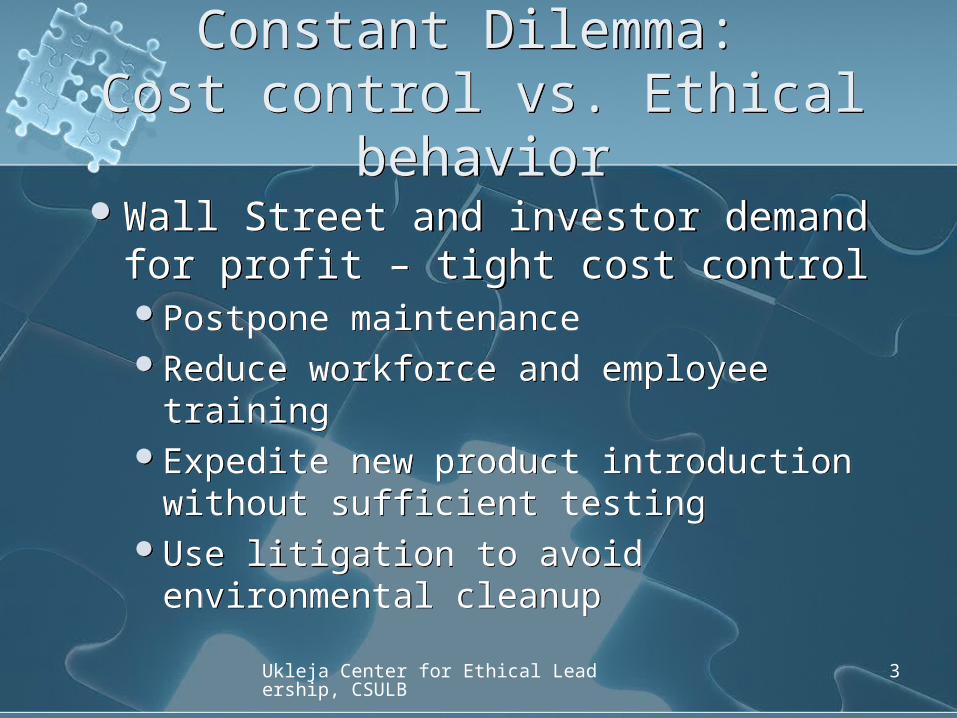

Constant Dilemma: Cost control vs. Ethical

behavior

Constant Dilemma: Cost control vs. Ethical

behaviorWall Street and investor demand

for profit – tight cost controlPostpone maintenanceReduce workforce and employee

trainingExpedite new product introduction

without sufficient testingUse litigation to avoid environmental

cleanup

Wall Street and investor demand for profit – tight cost controlPostpone maintenanceReduce workforce and employee

trainingExpedite new product introduction

without sufficient testingUse litigation to avoid environmental

cleanup

Ukleja Center for Ethical Leadership, CSULB

4

Constant Dilemma: Cost control vs. Ethical

behavior

Constant Dilemma: Cost control vs. Ethical

behaviorCan cost cutting go too far?

Illegal practiceHuman rights violationEnvironmental violation

Can cost cutting go too far?Illegal practiceHuman rights violationEnvironmental violation

Ukleja Center for Ethical Leadership, CSULB

5

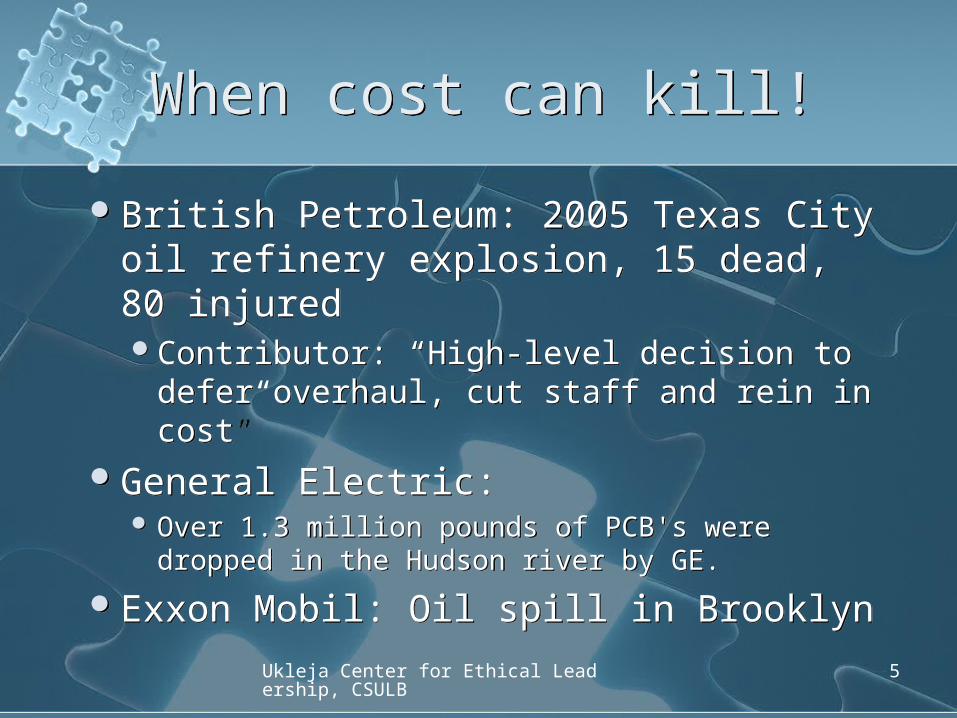

When cost can kill!When cost can kill!

British Petroleum: 2005 Texas City oil refinery explosion, 15 dead, 80 injuredContributor: “High-level decision to

defer overhaul, cut staff and rein in cost”

General Electric: Over 1.3 million pounds of PCB's were

dropped in the Hudson river by GE.

Exxon Mobil: Oil spill in Brooklyn

British Petroleum: 2005 Texas City oil refinery explosion, 15 dead, 80 injuredContributor: “High-level decision to

defer overhaul, cut staff and rein in cost”

General Electric: Over 1.3 million pounds of PCB's were

dropped in the Hudson river by GE.

Exxon Mobil: Oil spill in Brooklyn

Ukleja Center for Ethical Leadership, CSULB

6

OverviewOverview

I. Standards of Ethical ConductII. Cost Accounting Ethical DilemmasIII. Procedures to Resolve an Ethical

DilemmaIV. Measures to Prevent Unethical

Conduct

I. Standards of Ethical ConductII. Cost Accounting Ethical DilemmasIII. Procedures to Resolve an Ethical

DilemmaIV. Measures to Prevent Unethical

Conduct

Ukleja Center for Ethical Leadership, CSULB

7

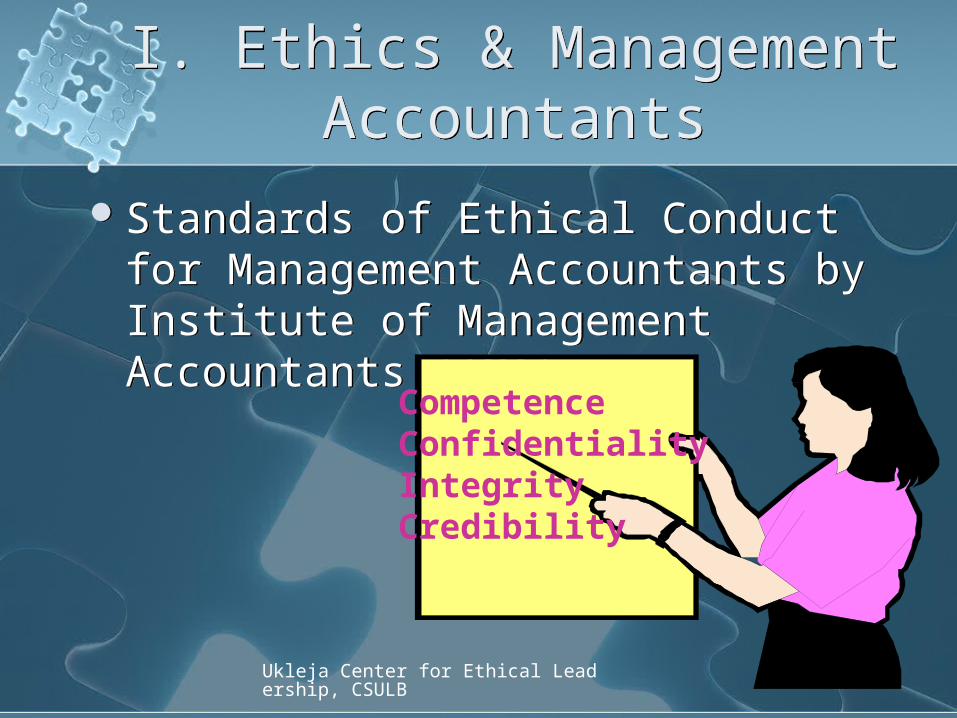

I. Ethics & Management Accountants

I. Ethics & Management Accountants

Ethics: Branch of philosophy concerned with the nature of ultimate value and the standards by which human actions can be judged right or wrong. Britannica Concise Encyclopedia

IMA principles:

Ethics: Branch of philosophy concerned with the nature of ultimate value and the standards by which human actions can be judged right or wrong. Britannica Concise Encyclopedia

IMA principles:HonestyFairnessObjectivityResponsibility

Ukleja Center for Ethical Leadership, CSULB

8

I. Ethics & Management Accountants

I. Ethics & Management Accountants

Standards of Ethical Conduct for Management Accountants by Institute of Management Accountants (IMA)

Standards of Ethical Conduct for Management Accountants by Institute of Management Accountants (IMA)

CompetenceConfidentialityIntegrityCredibility

Ukleja Center for Ethical Leadership, CSULB

9

CompetenceMembers have a responsibility

to:

CompetenceMembers have a responsibility

to:Maintain an appropriate level of

professional expertise by continually developing knowledge and skills

Perform their professional duties in accordance with relevant laws, regulations, and technical standards

Maintain an appropriate level of professional expertise by continually developing knowledge and skills

Perform their professional duties in accordance with relevant laws, regulations, and technical standards

Ukleja Center for Ethical Leadership, CSULB

10

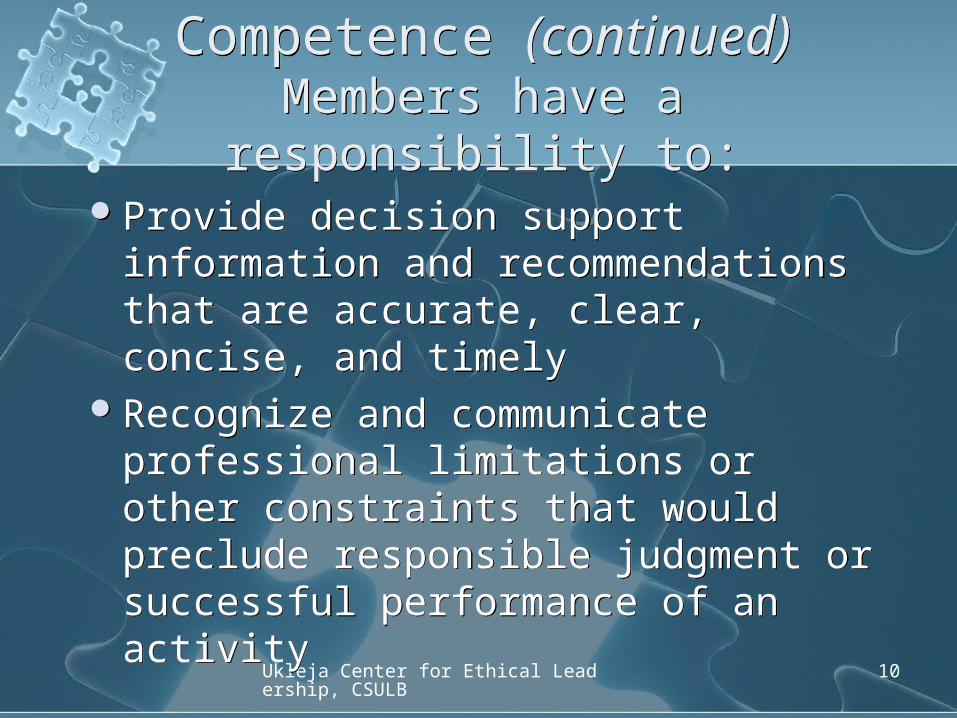

Competence (continued)Members have a responsibility

to:

Competence (continued)Members have a responsibility

to:Provide decision support

information and recommendations that are accurate, clear, concise, and timely

Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity

Provide decision support information and recommendations that are accurate, clear, concise, and timely

Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity

Ukleja Center for Ethical Leadership, CSULB

11

Confidentiality Members have a responsibility

to:

Confidentiality Members have a responsibility

to:Keep information confidential

except when disclosure is authorized or legally required.

Inform all relevant parties regarding appropriate use of confidential information. Monitor subordinates’ activities to ensure compliance.

Refrain from using confidential information for unethical or illegal advantage

Keep information confidential except when disclosure is authorized or legally required.

Inform all relevant parties regarding appropriate use of confidential information. Monitor subordinates’ activities to ensure compliance.

Refrain from using confidential information for unethical or illegal advantage

Ukleja Center for Ethical Leadership, CSULB

12

Integrity Members have a responsibility

to:

Integrity Members have a responsibility

to: Mitigate actual conflicts of interest,

regularly communicate with business associates to avoid apparent conflicts of interest. Advise all appropriate parties of any potential conflict.

Refrain from engaging in any conduct that would prejudice carrying out duties ethically

Abstain from engaging in or supporting any activity that might discredit the profession.

Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent conflicts of interest. Advise all appropriate parties of any potential conflict.

Refrain from engaging in any conduct that would prejudice carrying out duties ethically

Abstain from engaging in or supporting any activity that might discredit the profession.

Ukleja Center for Ethical Leadership, CSULB

13

Credibility Members have a responsibility

to:

Credibility Members have a responsibility

to: Communicate information fairly and

objectively Disclose all relevant information that

could reasonably be expected to influence an intended user’s understanding of the reports, analyses, or recommendations

Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law.

Communicate information fairly and objectively

Disclose all relevant information that could reasonably be expected to influence an intended user’s understanding of the reports, analyses, or recommendations

Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law.

Ukleja Center for Ethical Leadership, CSULB

14

II. Cost Accounting Ethical Dilemmas

II. Cost Accounting Ethical Dilemmas

The role of Cost Accountants in corporate decision-makingPlanning and budgetingProject cost-benefit analysesPerformance report after

implementation

The role of Cost Accountants in corporate decision-makingPlanning and budgetingProject cost-benefit analysesPerformance report after

implementation

Ukleja Center for Ethical Leadership, CSULB

15

Dilemmas ExamplesDilemmas Examples

A. Cost controlA1. Labor costA2. Regular maintenance and repair

costA3. Environmental cleanup cost

B. Cost estimates C. Cost reportingD. Performance measure

A. Cost controlA1. Labor costA2. Regular maintenance and repair

costA3. Environmental cleanup cost

B. Cost estimates C. Cost reportingD. Performance measure

Ukleja Center for Ethical Leadership, CSULB

16

A1. Labor costA1. Labor cost

Measures to reduce labor costOutsource to overseasReduce healthcare coverageCut workforce and employee trainingUse illegal immigrants and below

minimum wage pay

Measures to reduce labor costOutsource to overseasReduce healthcare coverageCut workforce and employee trainingUse illegal immigrants and below

minimum wage pay

Ukleja Center for Ethical Leadership, CSULB

17

A1. Labor costA1. Labor cost

Wal-Mart 2003: 245 illegal immigrants arrested; they were hired to clean the stores by cleaning companies contracting with Wal-Mart.

General Motors 2007: plans to eliminate 30k of its 113k US hourly factory positions while expanding in India and China

Wal-Mart 2003: 245 illegal immigrants arrested; they were hired to clean the stores by cleaning companies contracting with Wal-Mart.

General Motors 2007: plans to eliminate 30k of its 113k US hourly factory positions while expanding in India and China

Ukleja Center for Ethical Leadership, CSULB

18

A1. Labor costA1. Labor cost

Any good example of labor control?Mittal Steel

Promise of no layoffProfit-sharingOur people is our culture

Any good example of labor control?Mittal Steel

Promise of no layoffProfit-sharingOur people is our culture

Ukleja Center for Ethical Leadership, CSULB

19

A2. Maintenance costA2. Maintenance cost

Cut or delay regular maintenance and repair costs for immediate boost in bottom lineMyopic behavior with higher future

remedy costUnsustainable cost cutting that adds

noise in earnings signal

Cut or delay regular maintenance and repair costs for immediate boost in bottom lineMyopic behavior with higher future

remedy costUnsustainable cost cutting that adds

noise in earnings signal

Ukleja Center for Ethical Leadership, CSULB

20

A3: Environmental costA3: Environmental cost

PreventionEvaluate and select suppliers and

pollution control equipmentDesign process and productsEvaluate environmental riskRecycling

DetectionEnvironmental auditing and inspectionTesting and measurement for

contamination

PreventionEvaluate and select suppliers and

pollution control equipmentDesign process and productsEvaluate environmental riskRecycling

DetectionEnvironmental auditing and inspectionTesting and measurement for

contamination

Ukleja Center for Ethical Leadership, CSULB

21

A3: Environmental costA3: Environmental cost

Internal failure:Pollution control and toxic waste

managementLicensing facilities for pollution

External failure:Cleaning up polluted water and soilCleaning up oil spillSettling personal injury claimsDamaging ecosystemLoose sales due to reputation

Internal failure:Pollution control and toxic waste

managementLicensing facilities for pollution

External failure:Cleaning up polluted water and soilCleaning up oil spillSettling personal injury claimsDamaging ecosystemLoose sales due to reputation

Ukleja Center for Ethical Leadership, CSULB

22

A3: Environmental costsA3: Environmental costs

Environmental cost report and product costing

Companies that saved millions by reducing or eliminating environmental impactGMCommonwealth EdisonAndersen Corp.Xerox Europe

Environmental cost report and product costing

Companies that saved millions by reducing or eliminating environmental impactGMCommonwealth EdisonAndersen Corp.Xerox Europe

Ukleja Center for Ethical Leadership, CSULB

23

B. Cost estimatesB. Cost estimates

Under-estimate R&D costsUnder-estimate break-even points

for new productsUnder-estimate time to test and

launch new productsOver-estimate chance of FDA or

other regulatory approval

Under-estimate R&D costsUnder-estimate break-even points

for new productsUnder-estimate time to test and

launch new productsOver-estimate chance of FDA or

other regulatory approval

Ukleja Center for Ethical Leadership, CSULB

24

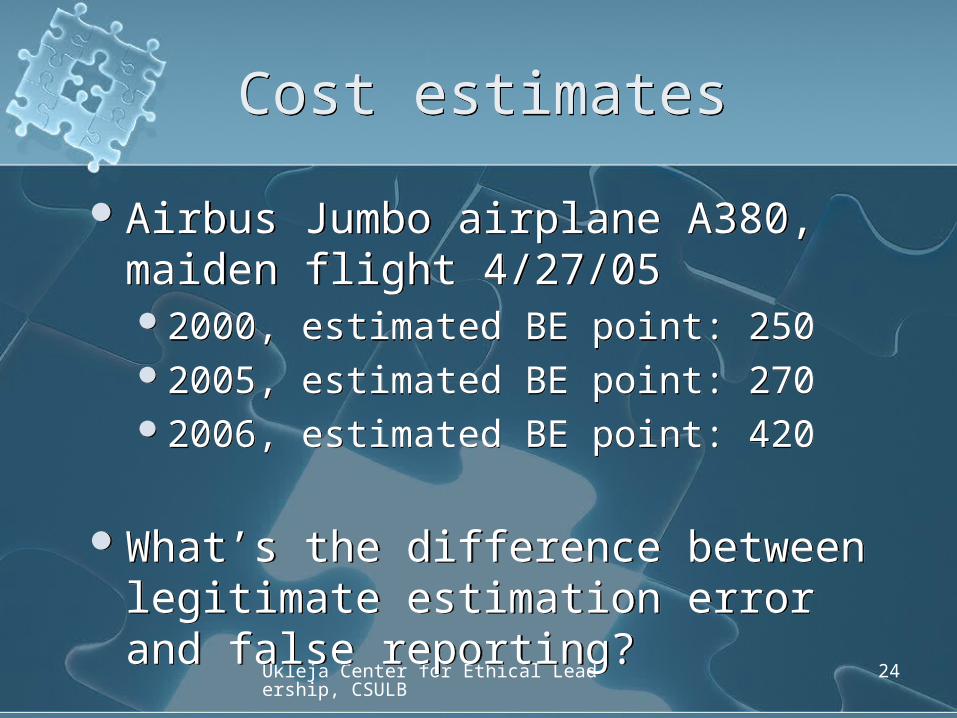

Cost estimatesCost estimates

Airbus Jumbo airplane A380, maiden flight 4/27/052000, estimated BE point: 2502005, estimated BE point: 2702006, estimated BE point: 420

What’s the difference between legitimate estimation error and false reporting?

Airbus Jumbo airplane A380, maiden flight 4/27/052000, estimated BE point: 2502005, estimated BE point: 2702006, estimated BE point: 420

What’s the difference between legitimate estimation error and false reporting?

Ukleja Center for Ethical Leadership, CSULB

25

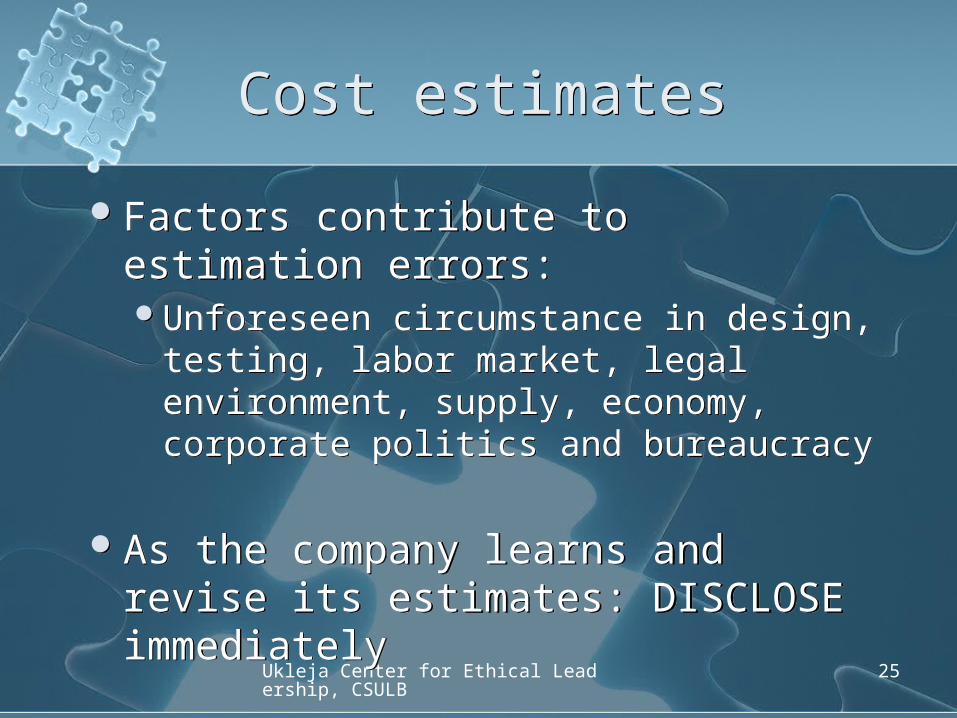

Cost estimatesCost estimates

Factors contribute to estimation errors:Unforeseen circumstance in design,

testing, labor market, legal environment, supply, economy, corporate politics and bureaucracy

As the company learns and revise its estimates: DISCLOSE immediately

Factors contribute to estimation errors:Unforeseen circumstance in design,

testing, labor market, legal environment, supply, economy, corporate politics and bureaucracy

As the company learns and revise its estimates: DISCLOSE immediately

Ukleja Center for Ethical Leadership, CSULB

26

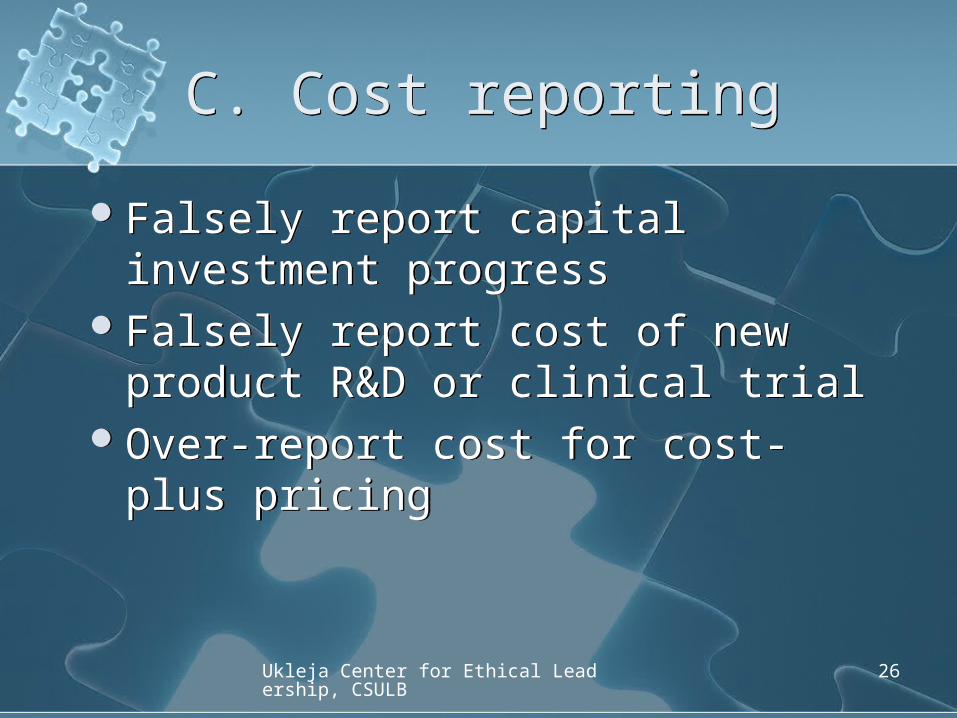

C. Cost reportingC. Cost reporting

Falsely report capital investment progress

Falsely report cost of new product R&D or clinical trial

Over-report cost for cost-plus pricing

Falsely report capital investment progress

Falsely report cost of new product R&D or clinical trial

Over-report cost for cost-plus pricing

Ukleja Center for Ethical Leadership, CSULB

27

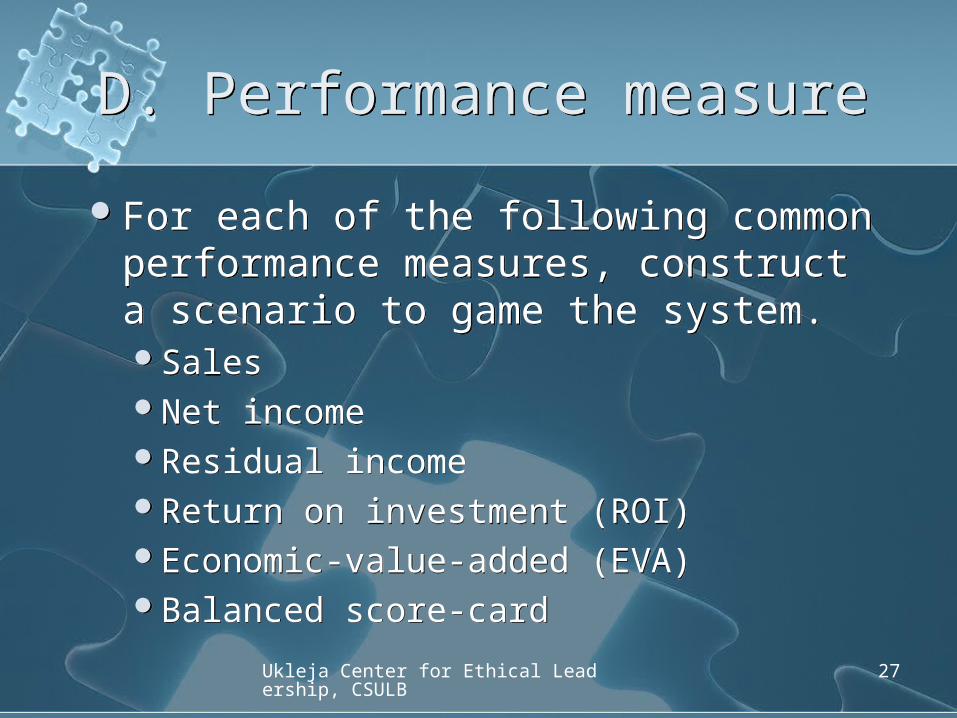

D. Performance measureD. Performance measure

For each of the following common performance measures, construct a scenario to game the system.SalesNet incomeResidual incomeReturn on investment (ROI)Economic-value-added (EVA)Balanced score-card

For each of the following common performance measures, construct a scenario to game the system.SalesNet incomeResidual incomeReturn on investment (ROI)Economic-value-added (EVA)Balanced score-card

Ukleja Center for Ethical Leadership, CSULB

28

III. Before You Blow the Whistle

III. Before You Blow the Whistle

Steps you can take before resignation

What can you expect for whistle blowing?

Laws that protect whistleblower.

Steps you can take before resignation

What can you expect for whistle blowing?

Laws that protect whistleblower.

Ukleja Center for Ethical Leadership, CSULB

29

Steps you should considerSteps you should consider

Report it to higher management

If the higher (or highest) management personnel are involved in the unethical behavior, talk to the Chief Ethics Officer, ethics or audit committee

Consult a lawyer

Resign

Blow the Whistle

Report it to higher management

If the higher (or highest) management personnel are involved in the unethical behavior, talk to the Chief Ethics Officer, ethics or audit committee

Consult a lawyer

Resign

Blow the Whistle

Ukleja Center for Ethical Leadership, CSULB

30

Outside SourcesOutside Sources

IMA ethics helpline: 1-800-245-1383

AICPA: ethics decision tree

If you must below the whistle, make sure you have the proper evidence to support your claim.

IMA ethics helpline: 1-800-245-1383

AICPA: ethics decision tree

If you must below the whistle, make sure you have the proper evidence to support your claim.

Ukleja Center for Ethical Leadership, CSULB

31

What can you expect for whistle blowing?

What can you expect for whistle blowing?

Get firedLose your house and savingsSmeared reputationUnable to find another jobLong and tiresome lawsuit

Get firedLose your house and savingsSmeared reputationUnable to find another jobLong and tiresome lawsuit

Ukleja Center for Ethical Leadership, CSULB

32

Legislation on ethicsLegislation on ethics

Securities and Exchange Act 1933 and 1934

Foreign Corrupt Practices Act of 1977

FIDCA Improvement Act of 1991Private Securities Litigation Reform

Act of 1995Federal False Claims ActSarbanes-Oxley Act of 2002

Securities and Exchange Act 1933 and 1934

Foreign Corrupt Practices Act of 1977

FIDCA Improvement Act of 1991Private Securities Litigation Reform

Act of 1995Federal False Claims ActSarbanes-Oxley Act of 2002

Ukleja Center for Ethical Leadership, CSULB

33

Laws that protect whistleblower.

Laws that protect whistleblower.

Federal False Claims Act 15% - 25% of settlement proceeds

Sarbanes-Oxley Act of 2002 TITLE VIII--CORPORATE AND CRIMINAL FRAUD ACCOUNTA

BILITY

Sec. 801. Short title.Short title.Sec. 802. Criminal penalties for altering documents. Criminal penalties for altering documents.Sec. 803. Debts nondischargeable if incurred in violation Debts nondischargeable if incurred in violation of securities fraud laws.of securities fraud laws.Sec. 804. Statute of limitations for securities fraud.Statute of limitations for securities fraud.Sec. 805. Review of Federal Sentencing Guidelines for Review of Federal Sentencing Guidelines for obstruction of justice and extensive criminal fraud.obstruction of justice and extensive criminal fraud.

Sec. 806. Protection for employees of publicly Protection for employees of publicly traded companies who provide evidence of traded companies who provide evidence of fraud.fraud.

Sec. 807. Criminal penalties for defrauding shareholders Criminal penalties for defrauding shareholders of publicly traded companies.of publicly traded companies.

Federal False Claims Act 15% - 25% of settlement proceeds

Sarbanes-Oxley Act of 2002 TITLE VIII--CORPORATE AND CRIMINAL FRAUD ACCOUNTA

BILITY

Sec. 801. Short title.Short title.Sec. 802. Criminal penalties for altering documents. Criminal penalties for altering documents.Sec. 803. Debts nondischargeable if incurred in violation Debts nondischargeable if incurred in violation of securities fraud laws.of securities fraud laws.Sec. 804. Statute of limitations for securities fraud.Statute of limitations for securities fraud.Sec. 805. Review of Federal Sentencing Guidelines for Review of Federal Sentencing Guidelines for obstruction of justice and extensive criminal fraud.obstruction of justice and extensive criminal fraud.

Sec. 806. Protection for employees of publicly Protection for employees of publicly traded companies who provide evidence of traded companies who provide evidence of fraud.fraud.

Sec. 807. Criminal penalties for defrauding shareholders Criminal penalties for defrauding shareholders of publicly traded companies.of publicly traded companies.

Ukleja Center for Ethical Leadership, CSULB

34

SOX - continuedSOX - continued

TITLE IX--WHITE-COLLAR CRIME PENALTY ENHANCEMENTS

Sec. 901. Short title.Sec. 902. Attempts and conspiracies to commit criminal fraud offenses.Sec. 903. Criminal penalties for mail and wire fraud.Sec. 904. Criminal penalties for violations of the Employee Retirement Income Security Act of 1974.Sec. 905. Amendment to sentencing guidelines relating to certain white-collar offenses.Sec. 906. Corporate responsibility for financial reports.

TITLE IX--WHITE-COLLAR CRIME PENALTY ENHANCEMENTS

Sec. 901. Short title.Sec. 902. Attempts and conspiracies to commit criminal fraud offenses.Sec. 903. Criminal penalties for mail and wire fraud.Sec. 904. Criminal penalties for violations of the Employee Retirement Income Security Act of 1974.Sec. 905. Amendment to sentencing guidelines relating to certain white-collar offenses.Sec. 906. Corporate responsibility for financial reports.

Ukleja Center for Ethical Leadership, CSULB

35

SOX - continuedSOX - continued

TITLE XI--CORPORATE FRAUD AND TITLE XI--CORPORATE FRAUD AND ACCOUNTABILITYACCOUNTABILITYSec. 1101. Short title.Sec. 1101. Short title.Sec. 1102. Tampering with a record or otherwise Sec. 1102. Tampering with a record or otherwise impeding an official proceeding.impeding an official proceeding.Sec. 1103. Temporary freeze authority for the Sec. 1103. Temporary freeze authority for the Securities and Exchange Commission.Securities and Exchange Commission.Sec. 1104. Amendment to the Federal Sec. 1104. Amendment to the Federal Sentencing Guidelines.Sentencing Guidelines.Sec. 1105. Authority of the Commission to Sec. 1105. Authority of the Commission to prohibit persons from serving as officers or prohibit persons from serving as officers or directors.directors.Sec. 1106. Increased criminal penalties under Sec. 1106. Increased criminal penalties under Securities Exchange Act of 1934.Securities Exchange Act of 1934.Sec. 1107. Retaliation against informants. Sec. 1107. Retaliation against informants.

TITLE XI--CORPORATE FRAUD AND TITLE XI--CORPORATE FRAUD AND ACCOUNTABILITYACCOUNTABILITYSec. 1101. Short title.Sec. 1101. Short title.Sec. 1102. Tampering with a record or otherwise Sec. 1102. Tampering with a record or otherwise impeding an official proceeding.impeding an official proceeding.Sec. 1103. Temporary freeze authority for the Sec. 1103. Temporary freeze authority for the Securities and Exchange Commission.Securities and Exchange Commission.Sec. 1104. Amendment to the Federal Sec. 1104. Amendment to the Federal Sentencing Guidelines.Sentencing Guidelines.Sec. 1105. Authority of the Commission to Sec. 1105. Authority of the Commission to prohibit persons from serving as officers or prohibit persons from serving as officers or directors.directors.Sec. 1106. Increased criminal penalties under Sec. 1106. Increased criminal penalties under Securities Exchange Act of 1934.Securities Exchange Act of 1934.Sec. 1107. Retaliation against informants. Sec. 1107. Retaliation against informants.

Ukleja Center for Ethical Leadership, CSULB

36

IV. Measures Company can Take

IV. Measures Company can Take

Code of ethicsChief Ethics OfficerEthics committeeEthics hotlineMandatory ethics training

Code of ethicsChief Ethics OfficerEthics committeeEthics hotlineMandatory ethics training

Ukleja Center for Ethical Leadership, CSULB

37

An open, transparent and ethical corporate culture is much more

effective than rules-based approach!

An open, transparent and ethical corporate culture is much more

effective than rules-based approach!