who can be self- funded? - c.ymcdn.com · 4/10/14 1 julie cink, prior lake-savage area schools what...

TRANSCRIPT

4/10/14

1

Julie Cink, Prior Lake-Savage Area Schools

What is Self-Funded Health Insurance??

� A self-insured group health plan (or a 'self-insured' plan) is one in which the school district assumes the financial risk for providing health care benefits to its employees.

� Self-insured districts set up a special fund to pay incurred

claims, as well as administrative costs from Third Party Administrators (TPAs).

� In practical terms, self-insured districts pay for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier, (which is known as a fully-insured plan).

Who Can Be Self-Funded?

� Many school districts can be self-insured. It is all about managing the risk.

� Districts over 200 employees should be comparing this option to a fully-insured plan.

4/10/14

2

Steps to Become Self-Funded

Where to Start? � Discuss this option with your broker.

(They help you with these steps!) � Request 2-3 years of claims data from

your health insurance company � Total all Health Ins expenses. Include:

Administrative costs (cost to process claims) Stop-loss coverage (reinsurance) Soft costs (fitness discounts, wellness fees) Claims

� Compare cost of all expenses to the total premium paid.

Claims � The claims are the claims are the claims. � Being Self-Funded or Fully-Funded doesn’t

matter when it comes to claims. � If claims are higher than expected, rates

will increase.

4/10/14

3

Provider Discounts Health insurance providers (or TPAs) negotiate discounts with hospitals, clinics, doctors, pharmacies, etc., to lower the cost of claims. It is important that districts determine which TPA offers the best provider discounts, as this has the biggest impact on over-all claim costs.

What Can You Control?

Administrative Fees Administrative fees include (but not limited to) the following:

Claims processing Network Access Fee – fee charged to access

provider discounts Fitness Discounts and Wellness Programs Nurse Advice Line

4/10/14

4

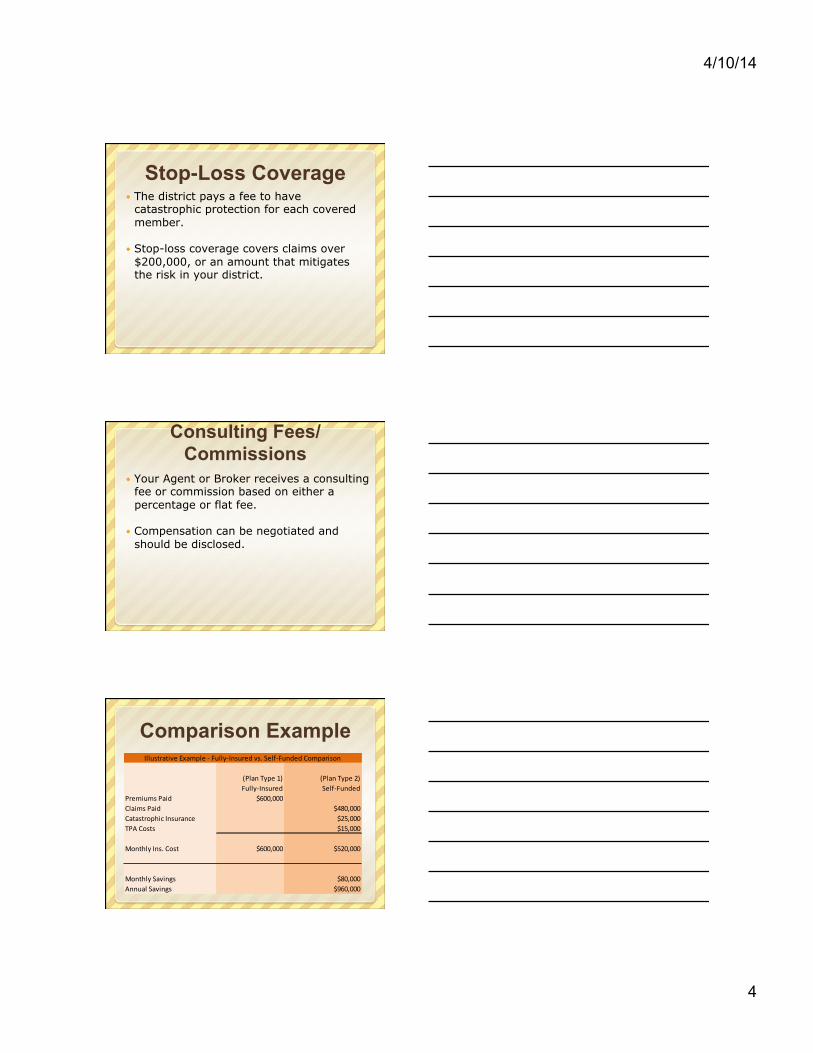

Stop-Loss Coverage � The district pays a fee to have

catastrophic protection for each covered member.

� Stop-loss coverage covers claims over

$200,000, or an amount that mitigates the risk in your district.

Consulting Fees/Commissions

� Your Agent or Broker receives a consulting fee or commission based on either a percentage or flat fee.

� Compensation can be negotiated and

should be disclosed.

Comparison Example Illustrative Example -‐ Fully-‐Insured vs. Self-‐Funded Comparison

(Plan Type 1) (Plan Type 2)Fully-‐Insured Self-‐Funded

Premiums Paid $600,000Claims Paid $480,000Catastrophic Insurance $25,000TPA Costs $15,000

Monthly Ins. Cost $600,000 $520,000

Monthly Savings $80,000Annual Savings $960,000

4/10/14

5

“PROs” to Self-Funded Option

� It is the District’s and Employee’s Plan. � You can tailor your insurance options to

meet the needs of your employees/district � No need to worry about any changes in

“aggregate value”. � Transparency � Employee understanding and involvement. � Ability to build a fund balance to off-set

future premium increases.

What is the Risk?

Risk Factors � Multiple Catastrophic Events

A spike in high case events - Medical claims that are >$50,000 and < $200,000.

� Accurately funding for projected costs –

critical to have a consultant/broker that understands self-funding and underwriting.

4/10/14

6

Other Considerations � School Board Approval � Largest Bargaining Unit Approval � File Plan with Dept of Commerce � Multiple Educational Staff Meetings � Thorough Review of Stop-Loss Provisions

Insurance Committee � Monthly Meetings � Transparency in costs � On-going knowledge of anticipated

premium increases � More knowledge of the health insurance

plan and offerings. � More knowledge of what areas are driving

increases in premium. � Set fund balance reserve targets.

District Office Workload � Minimal Increased workload for Business

Office – Need to create and maintain a separate account for Health Insurance.

4/10/14

7

Questions?