why are entrepreneurs more risk-loving? - numerons · pdf file07.04.2012 · why are...

TRANSCRIPT

Why are entrepreneurs more risk-loving?

On the reference dependencies of entrepreneurial decision making

Abstract

Empirical evidence on the risk propensity of entrepreneurs has produced inconclusive

results. One reason might be that most studies consider risk propensity as a stable personality

trait, thereby covering only one of the research streams on risk-taking behavior. In this

article, we consider the situational factors of risk propensity as described by prospect theory.

We show that entrepreneurs set significantly higher reference points than do non-

entrepreneurs. For a given distribution of outcomes, this behavior can explain a subsequent

willingness to take on more risks. Furthermore, we find that need for achievement has a

direct and a mediating effect on the formation of the reference point. In contrast, we do not

find a significant effect of optimism.

2

Introduction

Although a high number of new ventures fail within their first years, thousands of people

start their own business each year (Headd, 2003). An important topic in the research on

entrepreneurship is therefore why some people become entrepreneurs and which personal

characteristics differentiate entrepreneurs from managers and other groups. Despite decades

of research, scholars still have only limited understanding of the factors and decision

processes that lead an individual to become an entrepreneur (Markman, Balkin, & Baron,

2002; Shane & Venkataraman, 2000). The study of individual differences has therefore

remained a key topic of investigation in the field of entrepreneurship research (Mitchell et al.,

2007).

One important explanation for entrepreneurship is that entrepreneurs are people who are

willing to take risks, even in uncertain environments (Knight, 1921). Kihlstrom and Laffont

(1979) were the first to formalize the idea that entrepreneurs tend to be less risk-averse than

other people. Iyigun and Owen (1998) argue in a similar vein that risk-averse individuals are

less likely to become entrepreneurs in a developed economy where there is already a large

number of safe jobs. Moskowitz and Vissing-Jorgensen (2002) prove that average returns

from poorly diversified private equity are unattractive. Based on this finding they suggest that

one explanation for start-up activity is that entrepreneurs are more financially risk-tolerant

than managers or other employees.1

While theoretically appealing, these empirical findings about the risk-taking behavior of

entrepreneurs are inconclusive. For example, Cramer et al. (2002) find that risk-aversion is a

deterrent to entrepreneurship. In contrast, Xu and Ruef (2004) find that nascent entrepreneurs

are more risk-averse than non-entrepreneurs. In the psychological research, one meta-analysis

by Stewart and Roth (2001) shows that the risk propensity of entrepreneurs is indeed greater

than that of managers. In contrast, another meta-analysis by Miner and Raju (2004) including

3 different studies draws the opposite conclusion: that entrepreneurs are more risk-averse than

managers. They conclude that “it is not yet time to shut down the research engine” (p.12).2

Most of the studies on risk propensity consider risk taking as an individual trait that should

remain stable over time (Stewart & Roth, 2001). However, this approach covers only one of

the research streams on risk-taking behavior. Another important theme pertains to prospect

theory (Kahneman & Tversky, 1979) which stresses the situational factors that influence risk

attitudes. According to prospect theory, whether an outcome is perceived as a gain or as a

loss compared to a reference point has a strong influence on risk taking behavior. In general,

people exhibit risk aversion in the domain of gains, risk seeking behavior in the domain of

losses, and show significantly greater aversion to losses than an appreciation of gains.

Surprisingly, though prospect theory plays an important role in the explanation of risk taking

behavior, to our knowledge no studies of the differences in risk taking behavior between

entrepreneurs and non-entrepreneurs take this concept into account.

The purpose of the present study is to use prospect theory to offer an explanation why

some entrepreneurs are more risk loving than others. Risk taking might not always be a direct

and stable personality trait. Instead, risk attitudes might be influenced by other personality

traits that affect the assessment of the situation given reference-dependent preferences.

The determinant of risk attitudes in prospect theory is the reference point that distinguishes

gains from losses. We employ a newly developed method by Arkes et al. (2008) to compare

the reference point formation in entrepreneurs and in a control group: Subjects answered

questions in a hypothetical stock trading scenario. We asked subjects what stock price today

would generate the same utility as a previous change in a stock price. This approach allowed

us to calculate the newly formed reference point.

4

We find that entrepreneurs on average set a higher reference point than non-entrepreneurs.

This behavior can have a significant impact on risk attitudes, especially when the person has

little control over the situation. With a higher reference point and a given distribution of

outcomes, more potential outcomes will represent a loss compared to the reference point.

Prospect theory predicts that people in a loss situation will show more risk seeking behavior

than people who are not in a loss situation.

Naturally, the next question is why entrepreneurs should have higher reference points.

Reference dependency has been used in many fields to explain risk attitudes that are

inconsistent with expected utility theory (see Camerer, 2000, for an overview). However,

little is known about what exactly a reference point is (Köszegi & Rabin, 2006) and about the

psychology behind the formation and evolution of reference points over time; prospect theory

does not include hypotheses (Kahneman, 1992; Lehner, 2000). At present there is no

generally accepted theory on the formation of reference points.

Often the reference point is considered to be the status quo, e.g. an existing income level or

a current endowment (Plott & Zeiler, 2005; Thaler, 1999). Lately some authors have argued

that reference points are rational expectations held in the recent past about future outcomes

(Köszegi & Rabin, 2006, 2007; Hack & Lammers, 2008). For example, Winer (1986)

predicts brand choice of different products, assuming that price expectations determine the

reference point. Heath et al. (1999) argue that goals can act as reference points and serve as

evaluative standards even though they may never be an existing state or condition. Along

these lines, Camerer et al. (1997) examine why New York City cab drivers work longer hours

on bad days, taking a target income as the reference point. Rizzo and Zeckhauser (2003) take

the same kind of reference point to explain physicians’ behavior.

Each of these factors of status quo, expectations, or goals could be differently perceived by

entrepreneurs and non-entrepreneurs, thus resulting in different reference points.3 In addition,

5 psychological research has shown that the combination of several of these factors may

determine the formation of the reference point (Blount, Thomas-Hunt, & Neale, 1996).We

are therefore not able to offer a definitive answer to the question of why entrepreneurs set

higher reference points. However, we make a first step in this direction and discuss and test

for two potential personality traits that could affect the formation of expectations and goals:

need for achievement, and optimism. We focus our discussion on expectations and goals

since they leave more room for personal differences than does the observable status quo.

In our experiment we consider a situation in which the individual has no influence on the

outcome (stock price performance). In this setting, with a higher reference point, more

outcomes will be perceived as losses relative to the reference point, resulting in subsequent

risk seeking behavior. Why should an individual set a high reference point? Goals have been

assumed to play a role in the formation of reference points. In addition, they are an important

factor in the context of achievement motivation. We therefore consider the role of the need

for achievement on the formation of a reference point.

Prior research has shown that entrepreneurs are high in need for achievement (Collins,

Hanges, & Locke, 2004). However, this concept is usually associated with situations that are

to some extent controlled by the individual. The reason that we nonetheless consider need for

achievement in our setting is that entrepreneurs have also been found to have a significantly

higher illusion of control compared to others (Simon, Houghton, & Aquino, 2000). People

who have a high need for achievement and who believe that they can control largely

uncontrollable events might therefore set themselves more difficult goals for themselves. We

find that need for achievement has a significant positive effect on the willingness to start a

venture and on the formation of the reference point.

The second personality trait that we consider is dispositional optimism. Several studies

have shown that entrepreneurs are more optimistic than non-entrepreneurs (Puri & Robinson,

6 2004). Optimism is directly related to positive expectations. It also has an indirect effect on

individual goal setting through the optimism that it is possible to meet challenging goals.

However, we find no significant effect of optimism on the formation of the reference point.

The remainder of the paper is structured as follows. In Section 2, we discuss our

hypotheses in greater detail. In Section 3, we present our experimental design. In Section 4,

we describe the empirical findings, and discuss our results. Section 5 concludes.

Hypotheses

Reference point formation

According to prospect theory (Kahneman & Tversky, 1979), situational factors can have an

important impact on risk attitudes. In general, people exhibit risk aversion if they consider

themselves in the domain of gains and risk seeking behavior in the domain of losses.

However, the perception of gains and losses is not based on the person’s overall wealth but

on the relation of the outcome compared to the individual reference point. Therefore, for a

given distribution of outcomes, people with a higher reference point will find themselves

more often in the domain of losses (see Figure 1).

<Please insert Figure 1: Different reference points and impact on gain/loss region >

At some point in time t=1 one person has a lower reference point R1 compared to another

person with reference point Re1. In t=2 an outcome will occur with outcomes distributed

between Ol2 and Oh

2. Then there exist some actual outcomes O2 that are perceived by the first

individual as a gain and by the second individual as a loss. With prospect theory preferences

the second individual would demonstrate more risk seeking behavior than the first.

7

Risk attitudes could be quite different if both individuals were able to spend effort in order

to influence the outcome. According to prospect theory, people are more averse to losses than

appreciative of gains. Therefore, the second individual in our example would have a

motivation to spend more effort in order to reach a higher outcome and to not find herself in a

loss situation. This behavior has been observed in experimental settings (Heath, Larrick, &

Wu, 1999). Therefore, in our experimental design we examine reference point formation for

an event that the individual cannot control (stock price movement).

Many theoretical models assume that entrepreneurs are more risk seeking than non-

entrepreneurs (see, for example, Kihlstrom and Laffont, 1979; Iyigun and Owen, 1998).

However, the empirical findings have been mixed (Miner & Raju, 2004; Stewart & Roth,

2001). One reason for the different findings might be the different experimental designs, in

which the reference point plays or does not play a role. We assume that entrepreneurs will set

a higher reference point that would subsequently result in more risk seeking behavior. This

leads to the following hypothesis:

H1: People who set a higher reference point are more likely to envision forming a venture.

Need for Achievement

Goals have been found to be one important factor in the formation of reference points

(Camerer, Babcock, Loewenstein, & Thaler, 1997; Heath et al., 1999). Differences in goal

setting behavior could therefore explain differences in risk propensity due to prospect theory

preferences. As goals play an important role in achievement motivation, one might conclude

that reference point adaptation and achievement motivation are to some extent related.

In order to assess achievement motivation, we consider the multidimensional concept of

need for achievement. It refers to an individual’s wish to take responsibility for finding

8 solutions to problems, master complex tasks and set ambitious goals (McClelland, 1961).

People who have a strong need for achievement set challenging but achievable goals for

themselves, assume personal responsibility for the accomplishment of those goals, and are

highly persistent in the pursuit of these goals.

It has been shown that performance and career satisfaction are higher when there is a good

fit between work characteristics and personality (Holland, 1985). It was further argued that

entrepreneurial positions have more of those characteristics that people with a high need for

achievement prefer. Thus it seems likely that these people would be attracted to

entrepreneurial jobs (McClelland, 1961). Empirical evidence has generally supported this

hypothesis.4 Most studies document a significant positive correlation between high

achievement motivation and the decision to become self-employed (Johnson, 1990). A

current meta-analysis, comprising 41 studies linking entrepreneurship and achievement

motivation, found that achievement motivation was significantly correlated with choice of an

entrepreneurial career (Collins, Hanges, & Locke, 2004).

H2a: People who are high in need for achievement are more likely to envision forming a

venture.

Need for achievement has been usually associated with situations that are under the control

of the individual. In contrast, our study is concerned with reference point formation when the

individual has no influence on the outcome (see reasoning above). Therefore, we cannot

directly assume that people who are high in need for achievement will set a high reference

point.

There is, however, one reason why we might find some impact of need for achievement:

entrepreneurs have been found to have a significantly higher illusion of control than non-

entrepreneurs (Keh, Foo, & Lim, 2002; Simon, Houghton, & Aquino, 2000). Illusion of

9 control is a bias that occurs when individuals overestimate the extent to which their skill can

increase performance in situations where chance actually plays a large part (Langer, 1975).

People who are high in need for achievement and who believe that they can control largely

uncontrollable events are therefore likely to set themselves more demanding goals for these

events. Accordingly, we hypothesize the following:

H2b: People who are high in need for achievement will set a higher reference point.

Optimism

Expectations, goals, or both may play an important role in the formation of a reference

point. One personality trait that could influence the attitude towards both of these factors is

dispositional optimism: a bias to, across time and situation, hold positive expectations

(Wrosch & Scheier, 2003). People who are dispositionally optimistic believe that, in general,

they will meet their life goals (Chang, 2001). Therefore, optimism can have a direct effect on

expectations. It can also have an indirect effect on the goal setting of the individual through

the optimism to meet challenging goals.

Studies have shown that entrepreneurs are characterized by high optimism (Cooper, Woo,

& Dunkelberg, 1988) and are even more optimistic than other people (Puri & Robinson,

2004). Some researchers have gone further and considered entrepreneurs to be overly

optimistic: this overoptimism limits the search for information (Kaish & Gilad, 1991) and

generates rosy forecasts of the future (Kahneman & Lovallo, 1993). However, some studies

have found no significant relationship between optimism and the decision to start a venture

(Simon, Houghton, & Aquino, 2000).

H3a: People who are highly optimistic are more likely to envision forming a venture.

H3b: People who are highly optimistic will set a higher reference point.

10

Mediating effects

The previous hypotheses argue that higher achievement motivation and higher optimism

will result in higher reference points; as a result, people who set higher reference points have

higher entrepreneurial intentions. In other words, reference point adaptation mediates the

relationship between achievement motivation, optimism and entrepreneurial intention. We

therefore hypothesize that

H2c: The relationship between need for achievement and entrepreneurial intention is

partly mediated by reference point adaptation.

H3c: The relationship between optimism and entrepreneurial intention is partly mediated

by reference point adaptation.

Method

Subjects

A total of 64 business undergraduates at a large German university, the Technische

Universität Dortmund, answered our questionnaire in a classroom setting. All students

voluntarily filled out the questionnaire. The mean age of the participants was 22. Forty-five

percent of the participants were women.

This study examines the decision processes of individuals who envision forming a venture.

Another approach could have been to study people who have already done so. As suggested

by several researchers, there could be key differences in the way entrepreneurs and those

willing to become entrepreneurs process information (e.g. Baron 1998). Especially the

mediating effects of illusion of control on risk propensity proved to be different (Keh, Foo, &

11 Lim, 2002; Simon, Houghton, & Aquino, 2000). This could be due to the fact that

entrepreneurs have already experienced the (un-)controllability of market risks and therefore

have fewer illusions of control. In order to avoid possible interfering influences we examined

students who had not yet established their own venture (Krueger & Brazeal, 1994; Shaver &

Scott, 1991).

Operationalization of variables

A questionnaire was constructed to measure the two independent factors (achievement

motivation and optimism), the mediating variable (reference point adaptation), the dependent

variable (entrepreneurial intention), and two control variables (general risk propensity,

gender). Participants were asked to fill out a paper-based questionnaire which took

approximately 15 minutes to complete. In the following we briefly describe each of the

variables in the order in which they were mentioned in the questionnaire:

Reference point adaptation: To estimate reference point adaptations we presented the

following scenario taken from Arkes et al. (2008) and translated into German: “Two months

ago, you bought a stock for 30€ per share. One month ago, you were delighted to learn the

stock was trading higher – at 36€ per share. This month, you decide to check the stock’s price

again. At what price would the stock need to trade today to make you just as happy with the

stock’s price this month as you were when you learned the stock had risen from 30€ to 36€

last month?” After reading the scenario, participants were asked to indicate the stock price

generating the same utility as the previous price increase.

This procedure allows us to calculate the magnitude of the reference point adaptation under

the assumptions that the purchase price serves as the initial reference point (P0=R0) and that

the value function remains stable over time. The reasoning is the following: the previous

12 price change is assessed based on the initial reference point R0 resulting in utility UR0(P1) in

t=1. We ask subjects what stock price P* in t=2 will generate the same utility. For example,

without a shift in the reference point, subjects will still state P1. We are interested in the new

reference point R* with UR*(P*)=UR0(P1). Under the assumption that the shape of the value

function remains unchanged, the following equation holds:

P* - R* = P1 – R0 => ∆R = R* - R0 = P* - P1 (1)

Given this equality we are able to derive the reference point adaptation (∆R).

Entrepreneurial intention: Following Lüthje and Franke (2003), we asked participants

about their intention to start their own business within the next five years. A 4-point Likert

scale was used, ranging from “very improbable” to “very probable.”

Achievement motivation: To capture respondents’ achievement motivation we use the

Cesarec-Marke Personality Scheme (CMPS). The literature extensively discussed the distinct

differences between projective and self-reported measures of achievement motivation. While

McClelland (1972) stated that projective measures (like the TAT) are the only accurate way

to assess achievement motivation, because achievement motivation is a subconscious trait,

Spangler (1992) reported psychometric deficiencies of the TAT. Collins et al. (2004) found

that both projective and self-report measures are equally valid when predicting

entrepreneurial behaviour. For practical reasons we used a self-report measure (CMPS).

There are 165 questions on the CMPS, of which 15 concern achievement motivation. We

asked participants to answer all 15 and five filler questions. All questions were translated into

German. For each question participants had a forced choice between “yes” or “no.” The

number of “yes” answers results in an achievement score with a value of 15 for individuals

with the highest achievement motivation. The scale was reliable with α = .68.

13

Optimism: After a review of the literature, we chose the German version of the Life

Orientation Test (LOT) (Scheier & Carver, 1985) to deduce participants’ optimism. The LOT

consists of eight 5-point Likert-type items plus four filler items ranging from “strongly

disagree” to “strongly agree.” The test provides a single summary score, with high scores

indicating a more optimistic orientation and low scores indicating more pessimistic

orientation. The alpha reliability for testing optimism using this scale was 0.79.

Control Variables: As mentioned, risk taking is a behavior influenced by, among other

things, by trait, cognitive perceptions, and situational factors (Sitkin & Pablo, 1992).

Different perceptions of risk are not part of our study and to incorporate the situational factor

we measure the reference point adaptation. Therefore, we focus on risk propensity in terms of

a general personality trait as a control in this study. We measure risk propensity by asking

about the general willingness to take risk on a 10-point Likert-scale. This general measure

was shown to predict all risk taking behaviors, especially those relevant for entrepreneurial

decisions like financial risk taking and career risk taking (Dohmen et al., 2005).

Demographic information was also collected in the questionnaire. Due to low variance in

age, race and education variables of the sample, only gender as a potential influencing factor

was included in the analysis (Xu & Ruef, 2004).

Results and Discussion

Descriptive statistics for the dependent variable show that six subjects state a very high

probability of starting their own business within the next five years. Seven subjects stated that

they quite probably intend to start their own business, 25 say that this is quite improbable

while 26 subjects judge the chance as very improbable (mean = 3.11, standard deviation =

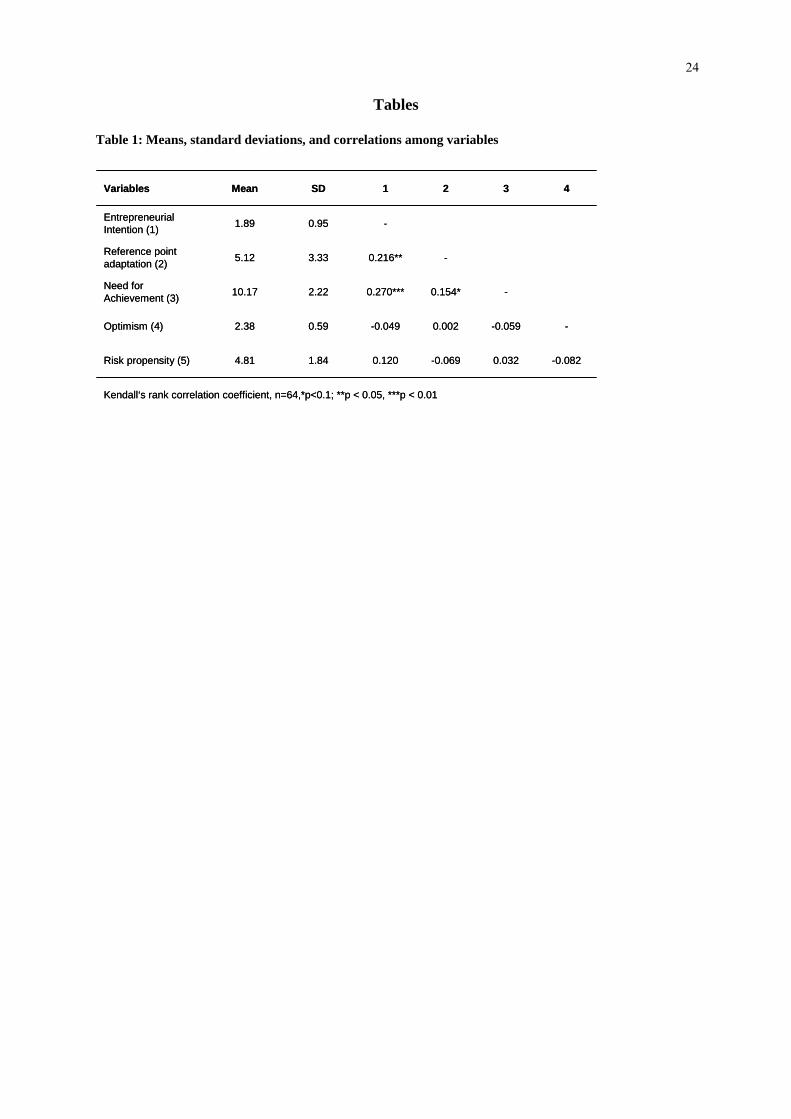

14 0.945). Means, standard deviations (SD), and correlations for all variables are shown in Table

1.

<Please insert Table 1: Means, standard deviations, and correlations among variables >

The correlation matrix indicates that, beside a significant correlation between reference

point adaptation and need for achievement, no correlation exists between the independent

variables. We therefore conclude that problems of collinearity between the variables do not

exist.

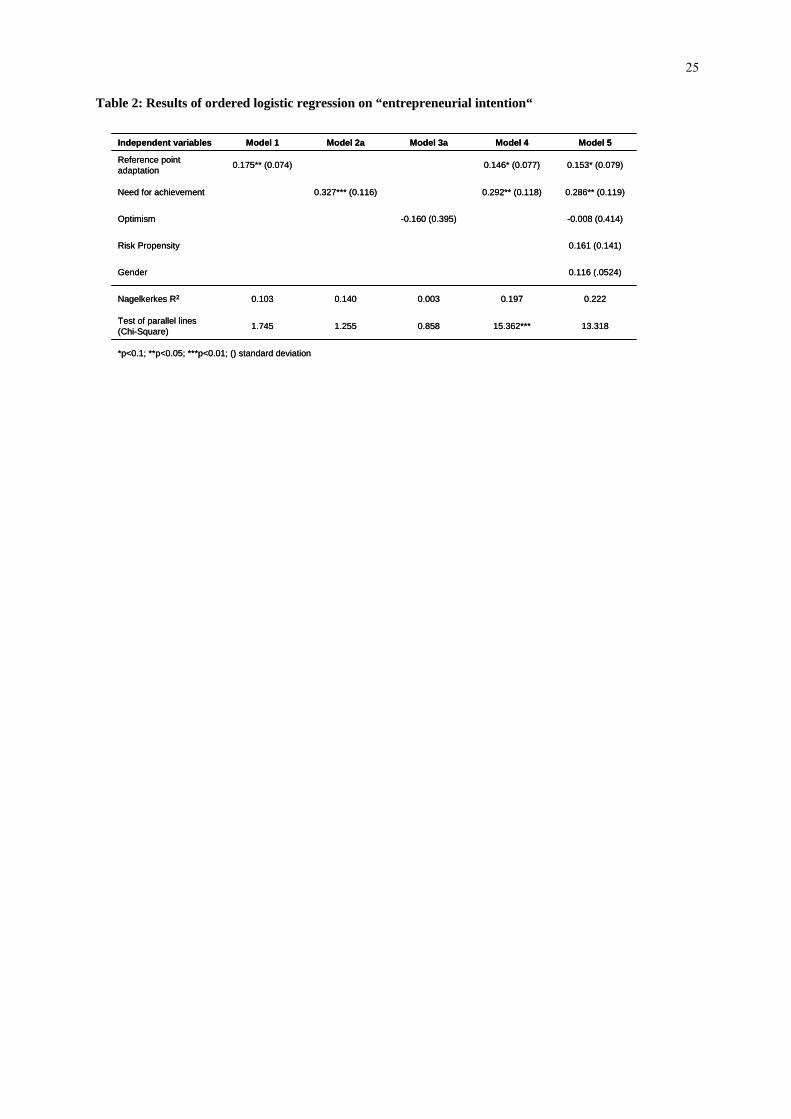

We test the direct effect of reference point adaptation on entrepreneurial intention posited

in Hypothesis 1 using an ordered logistic regression (Model 1). Regression showed a highly

significant positive relationship, supporting Hypothesis 1. The stronger the reference point

adaptation the higher is one’s entrepreneurial intention. The same held for Hypothesis 2a,

stating that a higher need for achievement will result in a stronger intention to start one’s own

venture (Model 2a). Ordered logistic regression corroborates the hypothesized relationship on

a significant level, too. Only for Hypothesis 3a one cannot find significant support (Model

3a). In our sample optimism does not influence one’s entrepreneurial intention.

Our results on optimism are in line with findings by Simon et al. (2000) but contradicting,

for example, those of Puri and Robinson (2004). This might be attributable to different

methods of measuring optimism. While Simon et al.’s work (2000), like ours, captured

optimism using a multi-item scale, Puri and Robinson (2004) measure optimism by

comparing individuals’ self-reported life expectancy to that implied by actuarial tables.

Measuring optimism based on a single and potentially emotional question could produce

different results.

15 <Please insert Table 2: Results of ordered logistic regression on “entrepreneurial

intention“>

Even after controlling for risk propensity and gender, both reference point adaptation and

need for achievement significantly explain some of the variance of entrepreneurial intention

(Model 5). Interestingly none of the control variables were significant, indicating that in our

sample, trait induced risk propensity does not affect one’s intention to start a venture.

This is in line with several findings in the literature (Miner & Raju, 2004). However while

trait induced risk propensity does not play a role, situational induced risk propensity, due to

different reference point adaptations might be could still affect actual risk taking behavior.

An indication of the possible impact of reference dependency on entrepreneurs’ risk

propensity is the following: Stewart and Roth (2001) found larger differences in risk

propensity between entrepreneurs and non-entrepreneurs for those entrepreneurs whose

primary goals are venture growth versus those whose focus is on producing family income. It

is possible that entrepreneurs with growth intentions set themselves more ambitious goals,

resulting in stronger reference point adaptation and thus a higher (situation induced) risk

propensity. We conclude that in order to arrive at a better understanding of the influence of

risk propensity on entrepreneurial intention one must take situational antecedents influencing

reference point adaptation into account.

To verify Hypotheses 2c and 3c, that is, proving the mediation effect of reference point

adaptation, four conditions had to be met (Baron & Kenny, 1986). First, the independent

variables (need for achievement, optimism) had to affect the mediator (reference point

adaptation); second, the independent variables had to affect the dependent variable

(entrepreneurial intention); third, the mediator had to affect the dependent variable; and

16 fourth, the effect of the independent variables in a multiple regression of independent and

mediator variables on the dependent variable had to be less than in the simple regression.

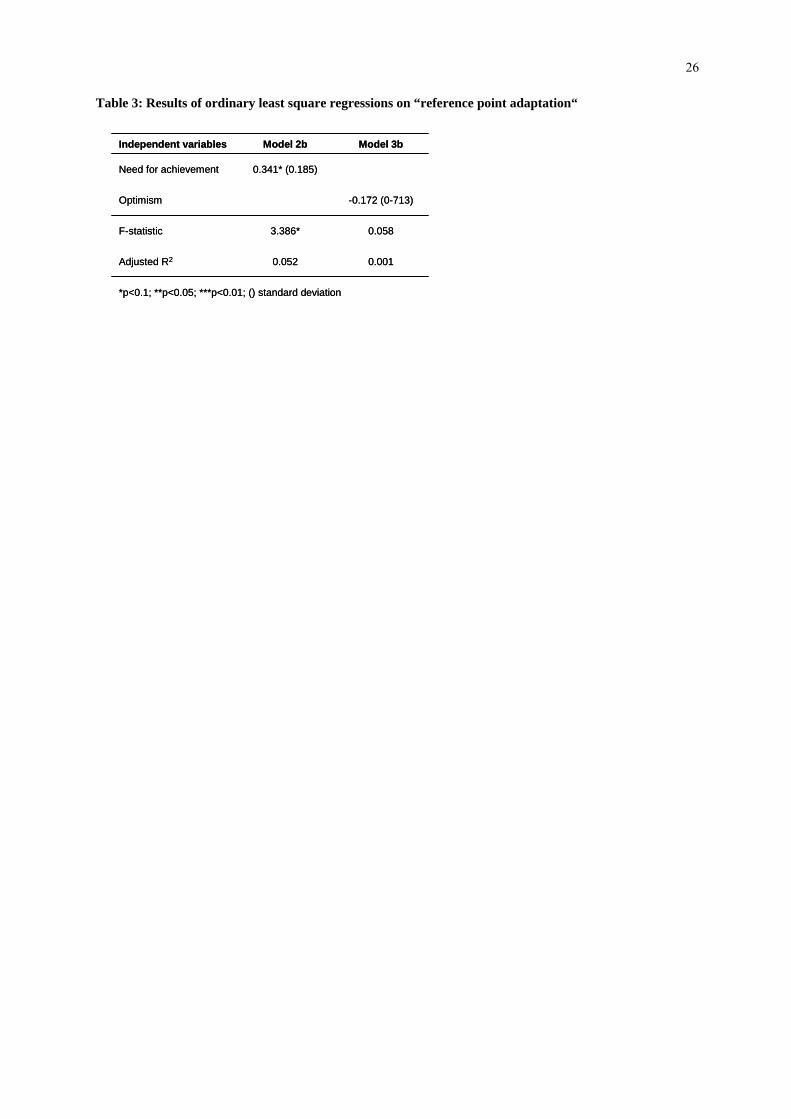

Models 2b and 3b (see Table 3) report the results of the first condition: the relationship

between the independent variables and the mediator. We conducted an ordinary least square

regression confirming the positive relationship between need for achievement and reference

point adaptation on a significance level of only 10% (Hypothesis 2b).

We were thus only able to confirm Hypothesis 2b on a weak significance level. One reason

could be that need for achievement is usually associated with situations that are under the

control of the individual, which is not the case in our setting. We might find stronger support

if we had controlled for illusion of control. Apart from the illusion of control, other factors

might influence the relationship between need for achievement and reference point

adaptation, like overconfidence. Future research should therefore include moderators like

illusion of control or overconfidence.

While need for achievement does influence reference point adaptation, we cannot confirm

a significant relationship between optimism and reference point adaptation (Hypothesis 3b).

<Please insert Table 3: Results of ordinary least square regressions on “reference point

adaptation“>

We have already documented the direct effects of the independent variables (Models 2a

and 3a) as well as the direct effect of the mediator (Model 1) on the dependent variable

(Model 1) in Table 2. Regarding need for achievement, we find a strong significant

relationship with entrepreneurial intention, thus fulfilling the second condition. Optimism,

however, was not significantly related to the intention to start a venture. Hypothesis 3c was

not corroborated. We therefore excluded optimism from the subsequent analysis. The third

17 condition, the direct effect of the mediator on the independent variable, was also met (Model

1).

Finally, Model 4 simultaneously regressed need for achievement and reference point

adaptation on entrepreneurial intention. To examine the last condition, we compared the

coefficient for need for achievement in Model 2a to the coefficient in Model 4. The

comparison displayed that the coefficient decrease in magnitude after adding reference point

adaptation, suggesting a mediated relationship. Furthermore, the coefficient for reference

point adaptation in Model 4 was still significant, supporting a partial rather than a full

mediation. Thus Hypothesis 2c was supported.

In summary, we were able to confirm both the direct and mediating effects of reference

point adaptation and the direct effect of need for achievement on entrepreneurial intention.

Results therefore support the assumption that the situational dimension of risk propensity

does play an important role in the explanation of entrepreneurial behavior.

Conclusion

Despite decades of research, the determinants of entrepreneurship are still not yet well

understood. One important aspect of entrepreneurial behavior is the willingness to take risks.

Many theoretical models have therefore assumed that entrepreneurs are less risk averse than

non-entrepreneurs. However, empirical evidence regarding risk propensity has produced

inconclusive results. One reason for these different results might be that most studies consider

risk propensity as an individual trait that should be stable over time. However, this approach

covers only one of the research streams on risk-taking behavior.

To our knowledge, this paper is the first that considers the situational factors as described

by prospect theory to explain different risk attitudes by entrepreneurs and non-entrepreneurs.

18 In particular, we examine differences in the formation of the reference point. With a higher

reference point and a given distribution of outcomes, more potential outcomes are perceived

as a loss compared to the reference point. Prospect theory predicts that people in a loss

situation will show more risk seeking behavior than people who are not in such a situation.

We indeed find that entrepreneurs set a significantly higher reference point than do other

individuals. Subsequently we examine the role of need for achievement and optimism in this

relationship. We show that need for achievement has a direct effect on reference point

formation. In contrast, we do not find a significant effect of optimism.

There are some limitations of our study. The advantage of the current method is that it

allows direct measurements of the adaptation of the reference point. However, this advantage

comes at a cost. An important limitation is our assumption of risk attitudes based on prospect

theory. We assume that people who set a high reference point in a setting where they are not

able to control the outcome will find themselves more often in a loss situation and therefore

will show more risk seeking behavior. A future study should directly test for risk propensity

in a setting where prior information has resulted in participants’ adaptation of the reference

point (e.g. choices between lotteries). This research design could also address a further

limitation of this kind of questionnaire study: subjects’ decisions have no monetary

consequences.

Another avenue for future research would be to consider differences in reference point

formation between people who envision starting a venture and people who have already done

so. Prior research has shown that there could be important differences between the two

groups, for example regarding the mediating effect of illusion of control on risk propensity

(Simon et al., 2000).

A further interesting question concerns the role of other personality traits in the formation

of reference points. In particular, tests for illusion of control and overconfidence – both traits

19 that have often been found to be significantly associated with the decision to start a business–

are promising directions for future research. All in all, this kind of study could not only add

to the research on entrepreneurship but also to the broader field of research on factors that

influence the formation of reference points over time (Köszegi & Rabin, 2007).

20

References

Arkes, H.R., Hirshleifer, D., Jiang, D., & Lim, S. (2008). Reference point adaptation: Tests in the domain of security trading. Organizational Behavior and Human Decision Processes, 105, 67-81.

Baron, R.A. (1998). Cognitive Mechanisms in Entrepreneurship: why and when entrepreneurs think differently than other persons. Journal of Business Venturing, 13, 275-294.

Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173-1182.

Blount, S., Thomas-Hunt, M. C., & Neale, M. A. (1996). The Price Is Right - Or Is It? A Reference Point Model of Two-Party Price Negotiations. Organizational Behavior and Human Decision Processes, 68(1), 1-12.

Camerer, C. F., Babcock, L., Loewenstein, G., & Thaler, R. H. (1997). Labor Supply of New York City Cabdrivers: One Day at a Time. Quarterly Journal of Economics, 112(2), 407-441.

Chang, E. (2001). Introduction: Optimism and Pessimism and Moving Beyond the most Fundamental Question. Optimism and Pessimism. . Washington, D.C.: American Psychological Association.

Collins, C. J., Hanges, P. J., & Locke, E. A. (2004). The Relationship of Achievement Motivation to Entrepreneurial Behavior: A Meta-Analysis. Human Performance, 17(1), 95-117.

Cooper, A. C., Woo, C. Y., & Dunkelberg, W. C. (1988). Entrepreneurs' perceived chances for success. Journal of Business Venturing, 3(2), 97-108.

Dohmen, T., Falk, A., Huffman, D., Sunde, U., Schupp, J., & Wagner, G. G. (2005). Individual Risk Attitudes: New Evidence from Large, Representative, Experimentally-Validated Survey. Working Paper.

Frank, R.H. (1985). Choosing the Right Pond: Human Behavior and the Quest for Status. New York: Oxford University Press.

Frey, R.S. (1984). Need for achievement, entrepreneurship, and economic growth: a critique of the McClelland theses. Social Science Journal, 21, 125-134.

Hack, A., & Lammers, F. (2008). The Role of Expectations in the Formation of Reference Points over Time. Working Paper.

Hansemark, O.C. (2003). Need for achievement, locus of control and the prediction of business start-ups: A longitudinal study. Journal of Economic Psychology, 24, 301-319.

Headd, B. (2003). Redefining business success: Distinguishing between closure and failure. Journal of Small Business Economics, 21, 51-61.

Heath, C., Larrick, R. P., & Wu, G. (1999). Goals as Reference Points. Cognitive Psychology, 38(1), 79-109. Holland, J. L. (1985). Making vocational choices. Englewood Cliffs, NJ: Prentice Hall. Johnson, B. R. (1990). Toward a multidimensional model of entrepreneurship: The case of achievement

motivation and the entrepreneur. Entrepreneurship Theory and Practice, 14(3), 39-54. Kahneman, D. (1992). Reference Points, Anchors, Norms, and Mixed Feelings. Organizational Behavior and

Human Decision Processes, 51, 296-312. Kahneman, D., & Lovallo, D. (1993). Timid Choices and Bold Forecasts: A Cognitive Perspective on Risk

Taking. Management Science, 39(1), 17-31. Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision Under Risk. Econometrica,

47(2), 263-291. Kaish, S., & Gilad, B. (1991). Characteristics of opportunities search of entrepreneurs versus executives:

Sources, interests, general alertness. Journal of Business Venturing, 6(1), 45-61. Keh, H. T., Foo, M. D., & Lim, B. C. (2002). Opportunity Evaluation under Risky Conditions: The Cognitive

Processes of Entrepreneurs. Entrepreneurship Theory and Practice, 27(2), 125-148. Knight, E. H. (1921). Risk, Uncertainty, and Profit. New York: Houghton Mifflin. Köszegi, B., & Rabin, M. (2006). A Model of Reference-Dependent Preferences. Quarterly Journal of

Economics, 121(4), 1133-1165. Köszegi, B., & Rabin, M. (2007). Reference-Dependent Risk Attitudes. American Economic Review, 97(4),

1047-1073. Krueger, N. F., & Brazeal, D. V. (1994). Entrepreneurial potential and potential entrepreneurs.

Entrepreneurship Theory and Practice, 18(3), 91-104. Langer, E. J. (1975). The illusion of control. Journal of Personality and Social Psychology, 32(2), 311-328. Lehner, J. M. (2000). Shifts of Reference Points for Framing of Strategic Decisions and Changing Risk-Return

Associations. Management Science 46, 63-76. Ho, V. T. & Levesque, L. L. (2005). With a Little Help from My Friends (and Substitutes): Social Referents and

Influence in Psychological Contract Fulfillment. Organization Science, 16, 275-289. Lüthje, C., & Franke, N. (2003). the 'making' of an entrepreneur: testing a model of entrepreneurial intent

among engineering students at MIT. R&D Management, 33(2), 135-147.

21 Markman, G. D., Balkin, D. B., & Baron, R. A. (2002). Inventors and new venture formation: The effects of

general self-efficacy and regretful thinking. Entrepreneurship Theory and Practice, 27(2), 149-166. McClelland, D. C. (1961). The achieving society. Princeton, NJ: Van Nostrand. Miner, J. B., & Raju, N. S. (2004). Risk Propensity Differences Between Managers and Entrepreneurs and

Between Low- and High-Growth Entrepreneurs: A Reply in a More Conservative Vein. Journal of Applied Psychology, 89(1), 3-13.

Mitchell, R. K., Busenitz, L. W., Bird, B., Gaglio, C. M., McMullen, J. S., Morse, E. A., et al. (2007). The Central Question in Entrepreneurial Cognition Research 2007. Entrepreneurship Theory and Practice, 31, 1-27.

Newman, A.F. (2007). Risk-Bearing and Entrepreneurship. Journal of Economic Theory, 137, 11-26. Plott, C. R., & Zeiler, K. (2005). The Willingness to Pay-Willingness to Accept Gap, the "Endowment Effect",

Subjective Misconceptions, and Experimental Procedures for Eliciting Valuations. American Economic Review 95, 530-545.

Puri, M., & Robinson, D. T. (2004). Optimism, work/life choices, and entrepreneurship. Working Paper. Scheier, M. F., & Carver, C. S. (1985). Optimism, coping, and health: Assessment and implications of

generalized outcome expectancies. Health Psychology, 5, 219-247. Shane, S., & Venkataraman, S. (2000). The promise of entrepreneurship as a field of research. Academy of

Management Review, 25, 217-226. Shaver, K. G., & Scott, L. R. (1991). Person, process, choice: The psychology of new venture creation.

Entrepreneurship Theory and Practice, 16(2), 23-45. Simon, M., Houghton, S. M., & Aquino, K. (2000). Cognitive biases, risk perception, and venture formation:

How individuals decide to start companies. Journal of Business Venturing, 15(2), 113-134. Sitkin, S. B., & Pablo, A. L. (1992). Reconceptualizing the determinants of risk behavior. Academy of

Management Review, 17(1), 9-38. Stewart, W. H., & Roth, P. L. (2001). Risk Propensity Differences Between Entrepreneurs and Managers: A

Meta-Analytic Review. Journal of Applied Psychology, 86(1), 145-153. Thaler, R. H. (1999). Mental Accounting Matters. Journal of Behavioral Decision Making 12, 183-206. Weber, E.U. & Milliman, R.A. (1997). Perceived risk attitudes: Relating risk perception to risky choice.

Management Science, 43, 123-144. Wrosch, C., & Scheier, M. F. (2003). Personality and quality of life: The importance of optimism and goal

adjustment. Quality of Life Research, 12(1), 59-72. Wu, B. & Knott, A.M. (2006). Entrepreneurial Risk and Market Entry. Management Science, 52, 1315-1330. Xu, H., & Ruef, M. (2004). The myth of the risk-tolerant entrepreneur. Strategic Organization, 2(4), 331-355.

22

Author Note

Funding for this research was provided by the Volkswagenstiftung, Hannover, Germany.

23

Footnotes

1 Newman (2007) has published one of the few theoretical papers in economics that argues to the contrary that

risk-based explanations for entrepreneurship are inadequate. He assumes that agents are able to insure

entrepreneurial risks but that moral hazard prevents full insurance. He finds that in this setting the decision to

become an entrepreneur based on risk preferences produces implausible results.

2 Some attempts have been made to reconcile the risk-bearing characterization of entrepreneurs with the

inconsistent empirical findings. For example, some scholars suggested that risk taking behavior results not

only from risk-propensity which is the tendency to take actions that one has judged to be risky but from a

combination of risk propensity and risk perception (Weber & Milliman, 1997). Risk perception is defined as

a decisions maker’s assessment of the risk inherent in a situation (Sitkin & Pablo, 1992). Empirical research

indeed supports the hypothesis that individuals who perceive less risk are more likely to evaluate an

opportunity more favorably and are more likely to start their own venture (Simon et al. 2000; Keh et al.

2002). Another attempt to reconcile the different findings is the study by Wu and Knott (2006). They

differentiate demand uncertainty from ability uncertainty and propose that entrepreneurs are risk-averse with

respect to the first concept but overconfident and therefore “apparent risk-seeking” with respect to the

second.

3 One other important factor that has been identified in the literature to influence the reference point is social

comparisons (Frank, 1985; Ho & Levesque, 2005). Since our experiment does not induce social comparisons,

we do not consider this factor in our discussion.

4 For exceptions see Frey (1984) and Hansemark (2003).

24

Tables

Table 1: Means, standard deviations, and correlations among variables

-0.216**3.335.12Reference point adaptation (2)

Kendall‘s rank correlation coefficient, n=64,*p<0.1; **p < 0.05, ***p < 0.01

-0.0820.032-0.0690.1201.844.81Risk propensity (5)

--0.0590.002-0.0490.592.38Optimism (4)

-0.154*0.270***2.2210.17Need forAchievement (3)

-0.951.89EntrepreneurialIntention (1)

4321SDMeanVariables

-0.216**3.335.12Reference point adaptation (2)

Kendall‘s rank correlation coefficient, n=64,*p<0.1; **p < 0.05, ***p < 0.01

-0.0820.032-0.0690.1201.844.81Risk propensity (5)

--0.0590.002-0.0490.592.38Optimism (4)

-0.154*0.270***2.2210.17Need forAchievement (3)

-0.951.89EntrepreneurialIntention (1)

4321SDMeanVariables

25 Table 2: Results of ordered logistic regression on “entrepreneurial intention“

13.318

0.222

0.116 (.0524)

0.161 (0.141)

-0.008 (0.414)

0.286** (0.119)

0.153* (0.079)

Model 5

Gender

Risk Propensity

15.362***

0.197

0.292** (0.118)

0.146* (0.077)

Model 4

0.858

0.003

-0.160 (0.395)

Model 3a

1.255

0.140

0.327*** (0.116)

Model 2aModel 1Independent variables

*p<0.1; **p<0.05; ***p<0.01; () standard deviation

1.745

0.103

Test of parallel lines(Chi-Square)

Nagelkerkes R2

Optimism

Need for achievement

0.175** (0.074)Reference point adaptation

13.318

0.222

0.116 (.0524)

0.161 (0.141)

-0.008 (0.414)

0.286** (0.119)

0.153* (0.079)

Model 5

Gender

Risk Propensity

15.362***

0.197

0.292** (0.118)

0.146* (0.077)

Model 4

0.858

0.003

-0.160 (0.395)

Model 3a

1.255

0.140

0.327*** (0.116)

Model 2aModel 1Independent variables

*p<0.1; **p<0.05; ***p<0.01; () standard deviation

1.745

0.103

Test of parallel lines(Chi-Square)

Nagelkerkes R2

Optimism

Need for achievement

0.175** (0.074)Reference point adaptation

26 Table 3: Results of ordinary least square regressions on “reference point adaptation“

0.001

0.058

-0.172 (0-713)

Model 3bModel 2bIndependent variables

*p<0.1; **p<0.05; ***p<0.01; () standard deviation

0.052

3.386*

Adjusted R2

F-statistic

Optimism

0.341* (0.185)Need for achievement

0.001

0.058

-0.172 (0-713)

Model 3bModel 2bIndependent variables

*p<0.1; **p<0.05; ***p<0.01; () standard deviation

0.052

3.386*

Adjusted R2

F-statistic

Optimism

0.341* (0.185)Need for achievement

27

Figures

Figure 1: Different reference points and impact on gain/loss region