why banks invest in blockchain (and not in bitcoin)

TRANSCRIPT

Koen Vingerhoets – find me on

Why are financial institutions investing in blockchain (and not in bitcoin)?Koen Vingerhoets@IthronKoen

All views are my own.

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

2008 – “Satoshi Nakamoto” writes…

Bitcoin is a unique transfer of value

Blockchain persists all the unique transfers

2008 – “Satoshi Nakamoto” schrijft…

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

The fairytale of Satoshi Nakamoto, the Unicorn and the Big Bank.

“What if… Satoshi is a bank employee in 2017?”

Introducing S. NAKAMOTO : bank employee

And a rather anonymous Big Bank

Satoshi is full of ideas & knowledge… but who listens?

“Join our 2017 Idea Competition and fly to Silicon Valley!”

Satoshi joins the competition with her idea…

“Blockchain: a shared, resilient & protected ledger for anything”

Satoshi has to explain it often to her Big Bank colleagues

Both Business & IT are interested but… also involved.

Three key drivers of “blockchain”

- Cryptography science has made the recording of tamper-proof data in a chain of digital blocks possible;

- Game theory explains how trust in others can be replaced mathematically via multiple actors that force self-interested rational behavior;

- Software engineering connects it all over the internet to achieve scale.

The blockchain is, from a technical point of view,

A unique, public and transparent distributed ledger That stores all transactions immutably and Permits predefined actions on data in those transactions In a cryptographically secured environment.

The blockchain is, from a business point of view,

A shared platform On which parties who don’t know or trust each other Are able to collaborate with respect for privacy Without relying on a possibly corrupt administrator.

Satoshi gathers a team of believers

The “Blockchain” idea ends in the top 3!

Our brave Satoshi has to present “blockchain” …

… to the Big Bank’s Board of Directors!

Even in fairytales, people have to work…

Satoshi elaborates her idea in the early hours of the night.

The great day arrives… and this is what she said.

“Dear management, colleagues, I am Satoshi Nakamoto.”

Why? The customer experience!

- People buy a house, not a mortgage or an insurance product (despite ourefforts to sell products)

- Then they have to visit a big bank to get the money they need for the house of their dreams.

- Then they need an insurance to protectour money and the house of theirdreams.

How? Blockchain as catalyst.

- Efficiency gains in our own internaland intra-bank processes : lessreconciliation, less (manual) checks,…

- New offerings for our customers, exploring markets we didn’t enter before

- Ecosystems to join or to build with a shared ledger of secured, trusted data

What? Some blockchain ideas

- Efficiency- Car Loan & Mortgage- X-border X-currency realtime payment

- New offerings- A Trade Finance for the SME market- Store secured documents in a vault

- Ecosystems could be the most powerful(side)effect of blockchain

- Ecosystems

But… Some challenges lie ahead!

- Collaboration between banks?

- Integration with legacy systems?

- It’s just an idea, we’ll have to learn the possibilities of this nascent technology

- Extra security or disruptive tech?

- No clear regulations (yet)

- Why choose blockchain for FinTech?

And… what if we don’t?

Just imagine someone uses blockchain- To exchange value over the internet- Between unknown parties- Without central regulation/steering

Satoshi NakamotoBank Employee

VOTETEAM “BLOCKCHAIN”

TOSILICON VALLEY!

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

Three drivers for financial institutions1. Efficiency gains (eg. Santander estimates $20 Bn / year)2. New Business (eg. Digital Trade Chain wins EFMA award)3. Ecosystems

Three drivers for blockchain ideation1. Cryptography science2. Gaming theory3. Software engineering & internet

Three hurdles to tackle1. Collaboration2. Regulations3. Integration

How to pay for services? How to insure goods?

We are still here!

What can our customers do?What’s our efficiency gain?

The new fabric of trust.

Who is who on our systems? Who to trust in misfortune?

Identity is the new money.

Logical steps for financial institutions in distributed ledger tech

IT research : scalability, resilience,…

Legal research : legal/compliance/risk, regulator,…

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

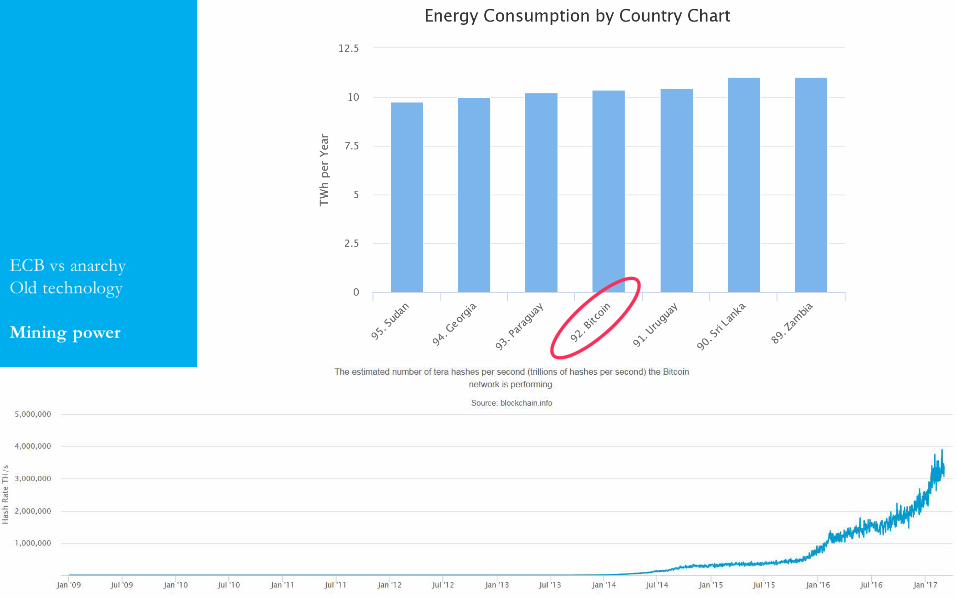

ECB vs anarchy

ECB vs anarchy

Old technology

ECB vs anarchy

Old technology

ECB vs anarchyOld technology

Mining power

Hashes per second on the bitcoin blockchain – proof of work

09/2013

05/2011

01/2016

09/2016

ECB vs anarchyOld technology

Mining power

ECB vs anarchyOld technology

Mining power

2012 bitcoin mining farm

ECB vs anarchyOld technology

Mining power

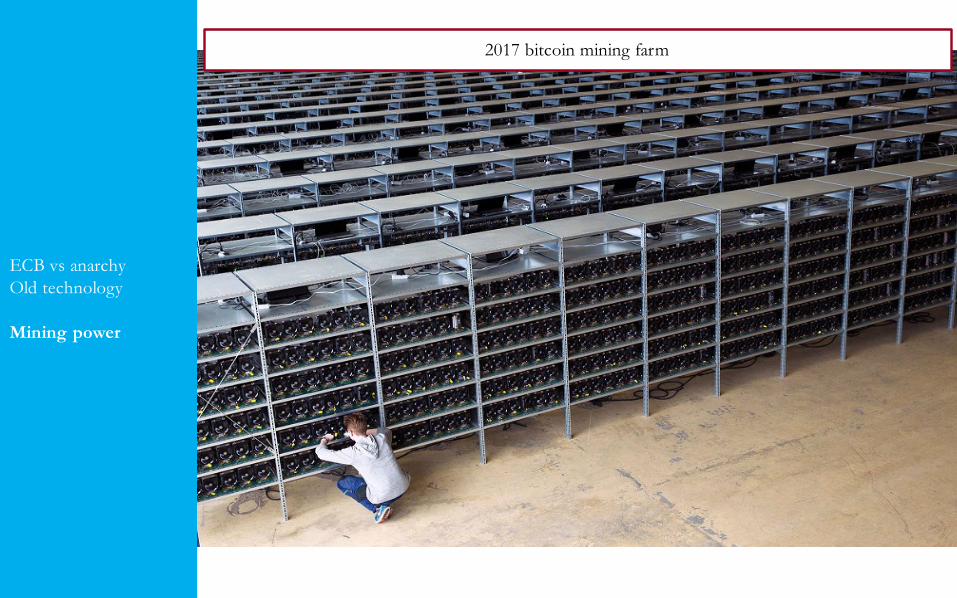

2017 bitcoin mining farm

ECB vs anarchyOld technology

Mining power

Say “cheese” to 91% of the hashing power (and know that 51% is already a risk)

ECB vs anarchyOld technologyMining power

Coin or investment?

ECB vs anarchyOld technologyMining power

Coin or investment?

ECB vs anarchyOld technologyMining power

Coin or investment?

ECB vs anarchyOld technologyMining power

Coin or investment?

ECB vs anarchyOld technologyMining powerCoin or investment?

For the unbanked

How to get bitcoin?

Buy it

Fromsomeone else

On anexchange

Mine it

Rent a miner

Buy a miner

Get a gift And thenwot, mate?

ECB vs anarchyOld technologyMining powerCoin or investment?

For the unbanked

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbanked

Bye bye banks!

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbanked

Bye bye banks!

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!

Identity provider

A bitcoin transaction is sound proof of one thing:The sending account had at least the required funds.

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!

Identity provider

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!Identity provider

Must… blockchain…

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!Identity provider

Must… blockchain…

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!Identity providerMust… blockchain…

Public & Permissionless

ECB vs anarchyOld technologyMining powerCoin or investment?For the unbankedBye bye banks!Identity providerMust… blockchain…

Public & Permissionless

- High risk investments- Fast worldwide “payments”

- If your money must be hidden- If the transaction must be hidden

- A digital asset that can’t be copied

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

D. Birch blockchain decision model

Our experiments / projects

Digital Trade ChainCash-on-ledger

Crowdfunding secondary marketsDocument authentication

Know Your CustomerCar Loans

Budget trackingUTI Management

Voluntary corporate actionsEuropean commercial paperQualitative reference data

ExperimentTrade Finance

Problem statement: SME’s have no proper coverage against the risks of international trade.

Lack of trust between SME’s• Unknown to each other• Delivery first vs Payment first• Unequal power between parties

leads to unequal conditions

Small margins within SME’s• Smaller transactions• High cost for a Letter of Credit,

relative to the value of the trade• No proper KBC products to cover

risks or to finance the transaction

Target market: Open account flows between EU parties

Export to distant destinations(Asia, Russia, Central Europe, Middle East and Africa)

Export EU destination

€245 bn

€70 bn

20% of Belgian export volume is todistant areas.

For these trade flows, documentaryletters of credit or collections are used.

>70% of Belgian Export volume is done with European counterparties.

TOP 3 countries: The Netherlands, France and Germany

60% of this trade is done with advance payment

The solution: A platform for SME’s willing to venture into international trade.

The KBC Digital Trade Chain offers• Support for Int’l Trade• Everything you need to follow up

your trade, cover its risks or optimize its financing

• Automatic payment when the contractual agreements are fulfilled

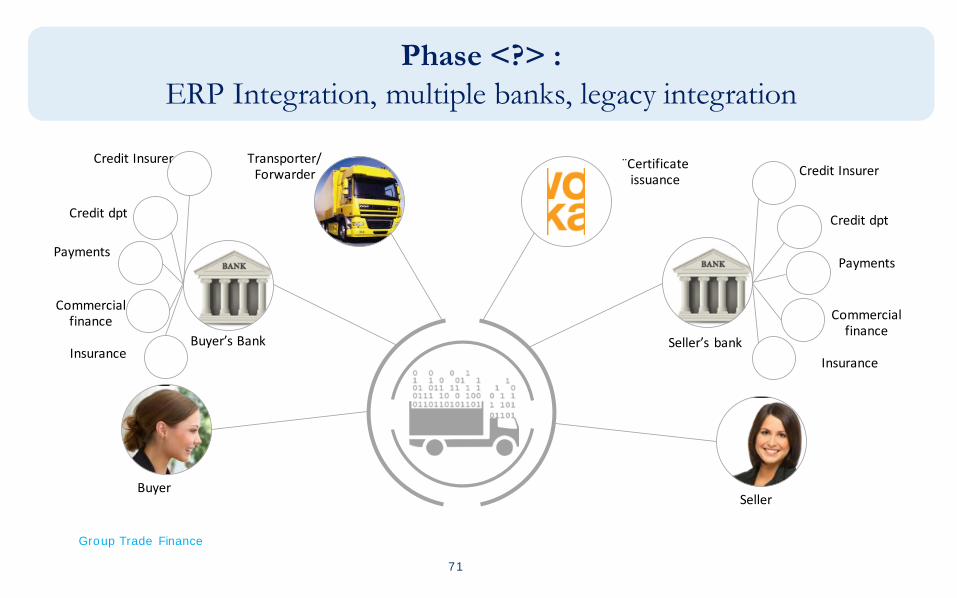

Phase 2 : ERP Integration, multiple banks, legacy integration

To enhance our experiment and move closer towards production, we studyfeasibility of - ERP integration (explicit customer

demand)- A multibank environment (technical

overhaul required)- Integration with our legacy systems (to

properly include our own offering)

Group Trade Finance

71

Buyer

Buyer’s Bank

Transporter/Forwarder

Seller

Seller’s bank

¨Certificateissuance Credit Insurer

Commercialfinance

Credit dpt

Payments

Insurance

Credit Insurer

Commercialfinance

Credit dpt

Payments

Insurance

Phase <?> : ERP Integration, multiple banks, legacy integration

TrustOwnership

Transparency

Traceability

Distributed

Smart contracts

Why use a blockchain?

Agenda

1. Shortest blockchain explanation ever

2. Omg! This sounds like a fairytale!?

3. Recap in 3*3

4. The holy bitcoin

5. Some fair tales @ KBC

6. Farewell!

Challenges ahead…

1. Blockchain strategy is about collaborating.2. Not just IT, also business is involved (risk appetite)3. Unpredictable reactions of regulator & Government4. Financial signals (ROI) are problematic. 5. Radical uncertainty is the norm (VUCA)

We

Banks sell trust and data.Blockchain is trust and data.

More info, questions or [email protected] (@IthronKoen)

Distributed Ledger Technolog y Adviser@ KBC Bank & Insurance

Disclaimer : I am not Satoshi Nakamoto, the search goes on!