why nations succeed the institutional and political in ... · to de ne the institutional di erence...

TRANSCRIPT

Why Nations Succeed

The Institutional and Political Influence on Prosperity

Jincheng Zhang

Yiqian Lu

November, 2016

1

Abstract

We answered the question of “why nations succeed” by deriving the resource

allocation between human capital and political capital for agents of various po-

litical statuses within economies of distinct institutions. The equilibrium al-

location depends on how political power is open and fair to all citizens, how

influential agents can exert their political power, the threshold level to reap po-

litical benefits and the relationship between human capital investment efficiency

and interest rate. Our analysis raises an alternative view on describing how in-

stitutions can affect economic development and provides a possible explanation

on the economic success of both democratic and authoritarian societies.

JEL Classification: P16, P26, J24, O11, O38

Keywords: Institutions; Political Capital; Human Capital

2

1 Introduction

To the unease of believers of ideal societies, evidence of political power prevails

in all communities, be it small or large, rich or poor, capitalism or socialism. Po-

litical power exists in all forms, such as lobbying, media control, bribery, nepotism

and even the choice of regime. Within a country, the discrepancy in political capi-

tal among economic participants can affect their behavior and the pattern of their

interaction, thus affecting structural evolution of the country; meanwhile, the insti-

tutional difference among different countries would create distinct evolution patterns

for market participants subject to their political capital discrepancy. This paper fo-

cuses on the impact of political capital discrepancy and institutional difference on

corporate behavior and market evolution. To be specific, we examined how the

difference among nations’ institutions (democracy or authoritarian), the efficacy of

company’s political power and relative political status of companies would affect

firm’s resource allocation between human capital and political capital investment.

Essentially there are tight link between human capital and economic growth. It

is concluded that human capital is associated with knowledge and skills, contributing

to economic development that depends on advances in technological and scientific

knowledge. (Gary S. Becker, Kevin M. Murphy, and Robert Tamura 1994). Barro

(1989) studies the education impact on per capita level growth among approximate

100 countries and proposes the argument that human capital investment plays a piv-

otal role in subsequent economic growth. It has been found (Romer 1989) that initial

literacy level has no additional explanatory power on growth rates on investment

but help predict the subsequent rate of investment and economic development.

With the development of Corruption Perceptions Index, it is now easier to find

the empirical relationship between corruption and economic development. In empir-

ical studies conducted by Pellegrini and Gerlagh (2004), corruption has been found

to have a negative effect on economic growth. Corruption is also studied as case

studies for various countries, such as Vietnam, South Korea and Philippines, Italy

and many others. When it comes to democratic and market-oriented economies,

government intervention in the economy is often referred to as rent seeking activi-

ties. Krueger (1974) discusses the ways where rent seeking is competitive. Following

Bentley’s pioneering work (1908) and stimulated by Stigler (1975), Peltzman and

Posner (1974), Becker (1983) build a model of political competition among pressure

groups. Under political equilibrium, all groups–defined by occupation, industry,

3

income, geography and other characteristics–maximize their incomes by spending

their optimal amount on political pressure, given the productivity of their expendi-

tures and the behavior of other groups. Indeed, the interference of government in

the economy are not pervasive in all societies for no reason. Market participants

face the dilemma of seeking political support or investing in its core competency

despite the institutional difference of countries. If we carefully consider these insti-

tutional difference among nations, does the difference between the process of “rent

seeking” which describes a money-dominated bidding process, and the process of

“corruption” which depicts a subtle and more complicated efforts, have the same or

different implications on economic development? Our answer is different, depending

on the country’s political institutions.

Now let’s treat political advantages as one type of asset called “political capital”

similar to human capital, regardless of which channel the participants acquire the

advantages. In a world that’s not perfectly free (i.e. affected by political power),

relative abundance of political capital can yield extra income to a group in forms

such as subsidies, free licences, tax exemptions, preferential policies, etc.; on the

contrary, lack of political capital often leads to losses to the group of interest, and

the losses in many occasions are not as financially explicit, such as more red tapes

in licensing process, stricter regulations and restrictions on qualifications and harsh

finance environment. Although political capital itself does not enhance productivity,

a group’s comparative abundance or deficiency in political capital can boost or hurt

its profitability as well as its business strategy. In our model following the work

of Ehrlich and Lui (1999), political capital partially redistributes the income of the

society without affecting the total output of all entities.

To define the institutional difference among nations, we find the recent work

“why nations fail” by Acemoglu and Robinson (2012) provides a helpful framework.

They argue that political institutions can be divided into two kinds - “extractive”

institutions in which a “small” group of individuals do their best to exploit - in the

sense of Marx - the rest of the population, and “inclusive” institutions in which

“many” people are included in the process of governing hence the exploitation pro-

cess is either attenuated or absent. While they successfully apply their reasoning to

most of the nations, they dodge the question that why countries such as Singapore,

where only a few people are included in the process of governing, succeed. Their ar-

gument is that countries that have extractive institutions cannot sustain long-term

4

economic growth even if they can experience a short-term rapid growth. In our

model, we translate the inclusiveness of institutions as how easy it is to accumu-

late political power and impose this power to gain economic benefits. The result of

our model provides a strong and effective amendment to Acemoglu and Robinson’s

theories where we have explained the East Asia’s “success” which is a phenomenon

that can maintain its stability.

For nations with inclusive institutions, political capital usually accumulates

through lobbying, media control and advocacy, all of which are generally consid-

ered “competitive rent seeking”; while for nations with extractive institutions, po-

litical capital is usually acquired through more interpersonal interactions such as

bribery, nepotism and political marriages. The difference, however, cannot always

be measured quantitatively since the implicit cost of many behaviors could not be

monetized. However, all behaviors above take efforts and time from the economic

participants, and can be measured in the sense of the opportunity cost behind those

efforts seeking political advantages. For example, an agent in an inclusive econ-

omy chooses to hire lobbyists at the cost of giving up investment in research and

development using the same amount of resource; on the other hand, an agent in

an extractive economy spend time and effort to build relationship with the ones in

power by letting go the chances to attract more employees of high capacity and im-

prove the efficiency of business. For economic participants in nations of whichever

institutions, they are always weighing the costs and benefits from investing between

political capital and human capital (and other investments that can improve pro-

ductivity of their businesses). Therefore the percentage of all resources available

(monetary or non-monetary including time, efforts and other expenditures) invested

in human capital and political capital can be taken as the decisions made from this

weighing and balancing all direct and indirect trade-offs.

With the concept of opportunity cost in mind, Isaac Ehrlich, Francis Lui (1999)

develop two complementary models to demonstrate the endogenous development of

corruption and growth. Their paper makes a significant contribution by introducing

time constraint imposed on individuals considering resource allocation to human

capital or political capital. In addition, they assume that corruption affects individ-

uals’ income by creating an add-on profit or loss to individuals’ production income

depending on their relative political capital stock, which is contrary to the common

belief that corruption imposes a social cost to all participants. These two assump-

5

tions lay a solid theoretical foundation for the model we develop in this paper.

Different from Ehrlich and Lui (1999), this paper applies the same assumptions to a

corporate setting and instead of maximizing the utility from an infinite consumption

stream, the corporate agent maximizes its discounted inter-temporal profit level in

this paper.

The conclusion from Ehrlich and Lui’s paper is intriguing where they deduce

three equilibrium in both of their homogeneous and heterogeneous agents cases:

low-level stagnant equilibrium (poverty trap), stagnant “development” equilibrium

and persistent “growth” equilibrium. The crucial difference among these three equi-

librium stages is the investment in human capital, which is considered as the engine

of economy’s growth. In fact, Adam Smith in “the Wealth of Nation” wrote down

the very first sentence, “The greatest improvement in the productive powers of labor,

and the greater part of the skill, dexterity, and judgement with which it is anywhere

directed or applied, seem to have been the effects of the division of labor.” In our

model, we use the investment in human capital as the proxy to discuss the growth

of nations.

The reallocation of resource due to varying political capital was discussed in

various forms. Song, Storesletten and Zilibotti (2011) have constructed a two-sector

model to explain the coexistence of high growth, high return to capital and a grow-

ing foreign surplus in China’s economic transformation. By demonstrating the re-

allocation of capital and labor from less productive externally financed firms to

more productive entrepreneurial firms who have less access to external financing,

Song implies that less productive firms have comparatively more political capital

which grants them easier access to financing resources. In reality, political capital

varies widely since political power can exist in a great variety of forms besides state-

ownership, making it sometimes difficult to classify them into binary categories-less

productive externally financed firms and more productive internally financed firms:

first, the percentage of equity owned by government (state or local government) can

vary from single digits to 100%; second, productive private enterprise may choose

to hire relatives of government officials, invite people who are politically powerful

on the company’s board, or get around with government interference with other

tactics in order to be favoured by the bureaucrats and receive “income transfer”

from political advantages; third, the level of political capital can vary across time

for companies who change their resource allocation strategy (e.g. political capital

6

v.s. human capital) in different time frames. In our model, the political status of

firms vary continuously throughout history and political advantages impose on a

company based on its relative political capital stock rather than absolute capital

stock. In other words, the political status of a firm needs to be ranked with its

peers to see how much political capital is accumulated in this firm compared with

other firms who are also competing for political preference by resource allocation to

political endeavors.

For a specific economy, companies’ capacity to accumulate political capital and

influence policy making might result in different resource allocation strategy, de-

pending on whether the company is in an economy with extractive or inclusive in-

stitutions. The debate of what kind of institutions foster or hinder economic growth

has been going on for a long time. Przeworski and Limongi (1993) have summarized

the debate on democracy, where they attach an interesting table showing the findings

in about twenty papers, all holding different opinions on what level of democracy or

authoritarian yields fastest growth. The impact of political institutions on corpo-

rates political activity has not been discussed as much. In as early as 1986, Useems

book “The inner circle: Large corporations and the rise of business political activity

in the US and UK” expressed concerns to the rising political activity from large

enterprises. Hillman, Zardkoohi and Bierman (1999) have found clear evidence of

a positive relationship between one type of political strategy, personal service, and

firm performance. Hansen and Mitchell (2000) has examined the political activities

of Fortune 500 firms, along with an oversampling of U.S. affiliates of large foreign in-

vestors for the 1987 to 1988 election cycle. Ansolabehere, de Figueiredo, and Snyder

(2003) has argued that political contributions should not be viewed as investment

in the political process but merely as a form of consumption good. Milyo, Primo,

and Groseclose (2000) have shown that large political action committee contributors

spend 20 to 60 times more on lobbying expenses than they do on hard money con-

tributions. Cooper, Gulen and Ovtchinnikov (2009) have documented a strong and

robust positive correlation between firms political contribution practices and their

future abnormal returns, and it is likely that only large firms can afford to pay these

political contributions. Their findings are partially confirmed in our modeling where

we found large companies tend to invest more in political capital only in inclusive in-

stitutions. The case for extractive institutions, however, is more complicated, which

will be discussed in more detail in the following sections.

7

The literature regarding the impact of political institutions on division of labor

is relatively limited. The inspiring work of Becker (1994) “The Division of Labor,

Coordination Costs, and Knowledge” discusses how specialization and the division

of labor depend on coordination costs, and also on the amount and extent of knowl-

edge. He also comments that “Countries with lower coordination costs due to stabler

and more efficient laws, or other reasons, not only have larger outputs, but they also

tend to grow faster because lower cost stimulate investments in knowledge by raising

the advantages of a more extensive division of labor.” without specifying how the

“stabler and more efficient laws” takes effect on the coordination costs. This insti-

tutional effect is studied more closely by Yang and Sachs (2003). They theorize that

the delimitation and protection of property rights is the ultimate driver of labor

division.

The remaining sections of this article are organized as follows. Section 2 builds

the benchmark model and discusses the case without political intervention. Sec-

tion 3 shows three different equilibrium cases under various exogenous conditions of

parameters. Section 4 provides detailed case studies to help understand why some

nations succeed while others fail and section 5 concludes the whole article. The

most remarkable contribution of this article is that it originally points out there ex-

ists an alternative way towards long-term economic prosperity other than political

and economic intuitions being intrinsic at the same time.

2 Equilibrium under no political intervention

In this section we build an infinite-period heterogeneous agent model. Each

company in the framework attempts to maximize its discounted intertemporal profit

level.

max∞∑t=0

1

(1 + rt)tP it ,∀i (1)

where rt is the t-year yield rate and P it represents profit level for agent i in period t.

Here for simplicity at the very beginning we assume each agent faces homogeneous

credit constraints and discounted rate so that rt only relies on t but not i. Later

we will relax the homogeneous discount rate assumption and unveil the dynamic

equilibrium under more general assumptions.

The profit is endogenously determined in each period with the engine of human

8

capital accumulation. Following Isaac Ehrlich, Francis Lui (1999)’s approach, we

assume the human capital is decided by

H it+1 = A(H̄ i +H i

t)hit (2)

where H it means human capital endowment is period t for company i. hit denotes

fraction of time spent on acquiring human capital in period t for agent i and A

human-capital-augmenting technology coefficient. H̄ i here, however, denotes raw

human capital capacity such as manual labor for ith agent, which can be obtained

without any human capital obtaining effort . For instance, people who possess raw

human capital only should be able to accomplish simple task like housekeeping and

mowing.

Meanwhile, there exists a second type of capital, say political capital in this

framework, which is generated by

Qit+1 = B(λH̄ i +Qit)qit (3)

where Qit denotes political capital and qit the fraction of time spent on investing

political capital accumulation for agent i at time t. B is the political accessibility co-

efficient, which denotes fairness and openness of the public policy decision-making

process. A higher B represents a more inclusive political institution. Raw labor

with a multiplier λ is also introduced into the function of political capital accu-

mulation, which is consistent with a reasonable assumption that the company with

more people should have a large capacity of political endowment. Examples of po-

litical capitals could vary under different political and economic institutions (see

Acemoglu (2012)’s definition of intrinsic and extractive intuition). For instance, po-

litical capital includes lobbying power, dominance of media, political contributions

for countries with intrinsic institutions. On the contrary, for extractive intuitions,

bribery amount, the relationship with political entity leaders or dictators could be

widely regarded as political capital. In our framework, political capital plays a

crucial role in realized profit function through output redistribution while human

capital affects profit function through contribution to higher technology efficiency.

Without loss of generality, total time endowment within one period is set as 1

for all agents. Consequently, the remaining time for company i to do production in

9

period t is calculated as

eit = 1− hit − qit (4)

and the raw profit is set by

Y it = C(H̄ i +H i

t)ett (5)

where Y it is the raw profit level and C represents Hicks-neutral technological progress.

The realized profit is as follows.

P it = Y it [1 + θ ln(

QitQ∗t

)] (6)

where θ denotes the political influential level, which is the amount under government

intervention and regulation. In a hypothetical society with government intervention

level θ = 0, it is intuitive and straightforward that each agent will choose qit = 0,∀i, t

since acquiring political capital is nothing but wastes of time contributing to dis-

counted profit level. Q∗t denotes political beneficiary threshold , which is the me-

dian political capital level with zero realized government intervention gain or loss.

Agents with stronger political power Qit > Qt are accompanied by positive subsidies

or transferring income. On the contrary, Qit < Qt denotes a net loss. I will raise

two examples under intrinsic and extractive intuitions, respectively, to illustrate the

economic implication of θ. (1) In the countries with intrinsic intuitions, a restau-

rant chain company could donate an increasing amount of political contributions

to support senators or representatives favoring low sales taxes. Once the Act of

reducing tax rate is passed, they will be the beneficiary of both increased sales and

less tax obligation. (2) The corresponding example in those extractive countries is

a different story. The restaurant company could bribe the bureaucrats in food regu-

lation department. The bureaucrats, therefore, will be reluctant to issue restaurant

license to its competitors or simply fine heavily the competitors under some unrea-

sonable excuse such as “low food quality” or “unqualified sanitary condition” even

for highly-qualified restaurant competitors.

Since it is a close economy, the aggregate political redistribution gain for com-

panies with Qi > Q∗ should be equal to the aggregate loss suffering by agents with

Qi < Q∗. ∑i

Y it =

∑i

P it =∑i

Y it [1 + θ ln

QitQ∗t

], ∀t (7)

And the median political capital level Q∗t is also determined by the above equation.

10

For instance, if all agents have the same raw profit level Y it and the distribution of

political capital follows log-normal distribution lnN(µ, σ2), the Q∗t will be exactly

eµ since lnQitQ∗t

remains symmetric.

The Ehrlich & Lui’s (1997) framework makes similar assumptions on the con-

sumption function, but it suffers from the following weakness and could be eliminated

in our firm-level profit-based approach. Firstly, with θ high enough, those agents

with low political capital should have a negative profit level during that particular

period, which is consistent and ubiquitous in those developing economies. However,

in Ehrlich & Lui’s (1997) approach, their model did not wipe out the possibilities

of a negative consumption level, leading to inappropriate and unconvincing conclu-

sion. Secondly, it is more rational to assume that profits instead of consumptions

suffer from linear-form extraction gain/loss. The linear tax-consumption relation-

ship is not consistent with permanent income hypothesis while in our approach the

linear-type tax-profit approach is in conform with the hypothesis.

The state variables in this framework are H it and Qit and choice variables are

hit and qit, for i ∈ I and t = 0, 1, .... Consequently, we could have the following two

Euler Equations.

eit+1 =(1 + rt+1)(1 + θ ln

QitQ∗t)

A(1 + θ lnQit+1

Q∗t+1

)(8)

andH̄ i +H i

t

H̄ i +H it+1

=θQ∗t+1B(λH̄ i +Qit)

A(1 + θ lnQit+1

Q∗t+1

)(9)

Where H it+1 = A(H̄ i + Ht)ht We have reach out the policy function of deter-

mining ht if the politically influential level θ > 0

hit =

Xit+1

H̄i+Hit− H̄ i

A(H̄ i +H it)

(10)

Where

Xit+1 =

θQ∗t+1B(λH̄ i +Qit)

A(1 + θ lnQit+1

Q∗t+1

)(11)

The economic meaning of those two policy functions is intuitive. The marginal

profit gain from production alone should be equal to the discounted marginal profit

gain for investing in human capital for the future periods, which itself is equivalent

to the discounted marginal profit obtaining political capital to seek additional tax

11

bracket/income transfer gain and/or avoid redistribution penalty loss.

If there did not exist government fiscal policy or any business intervention,

θ = 0. In this case we will have only one policy function with respect to human

capital investment choice. It is meaningless to invest any political capital as the

marginal profit contribution of political capital is nothing but negative number. In

this case,

hit+1 = 1− 1 + rt+1

A, ∀t (12)

(i) Equilibrium I: no human capital accumulation. Notice the natural constraint

0 ≤ ht ≤ 1. When A ≤ 1 + rt, the rational choice of human capital investment

ht = 0, denoting a zero human-capital-accumulation economy. The human capital

technology level remains at a low level so that the raw labor production efficiency

outweighs human capital investment, leading a stagnant economic growth situation.

Assuming flat interest rate term structure rt ≡ r, the value of a corporate is fully

determined by the initial raw human capital endowment, say H̄ i.

V (H̄ i) =

∞∑t=0

CH̄ i

(1 + r)t=CH̄ i(1 + r)

r(13)

which is quite similar to the traditional discount cash flow pricing model.

(ii) Equilibrium II: Decreasing human capital growth.

In this case, we assume 1 + rt < A < 2rt. By assuming initial political capital

endowment H0 = H̄ i and flat term-structure rt ≡ r, ∀t, we have Ht+1 = A(H̄ +

Ht)(1− 1+rtA ). The human capital for each period is calculated as

H it =

H̄ i((2A− 2r − 3)(A− r − 1)t −A+ r + 1

)A− r − 2

,∀t (14)

The value for an agent with intial human capital H̄ under flat term structure rt ≡

r, ∀t is

V (H̄) =∞∑t=0

1

(1 + r)tPt

=∞∑t=0

C(r + 1)1−t(H̄((2A−2r−3)(A−r−1)t−A+r+1)

A−r−2 + H̄

)A

=CH̄(r + 1)2(2r + 1)

Ar(2(r + 1)−A)

(15)

The value of the stock is a finite number with human capital Ht decreasing each

12

period by approximately 1− (A− 1− r) (where A− 1− r is less than 1) percent.

From the expression of the agent value, we could derive without difficulty that

∂V (H̄)∂H̄

> 0, meaning stock value increases with a large initial (raw) human capital.

From this point of view, corporation with initial larger number of workers should

be accompanied by a larger share price. ∂V (H̄)∂C = constant > 0, representing linear

positive contribution of Hicks-neutral technology progress.

Meanwhile, the marginal share price on human-capital-accumulating technology

progress is positive.

dV

dA=

2CH̄(r + 1)2(2r + 1)(A− r − 1)

A2r(A− 2(r + 1))2> 0 (16)

Although a higher A could lower current proportion of production, the invest-

ment on future human capital accumulation contributes positively to the aggregate

discounted profit level with a higher production efficiency for the periods after.

At the same time, the second derivative with respect to A is also positive.

d2V

dA2= −

2CH̄(r + 1)2(2r + 1)(3A2 − 6A(r + 1) + 4(r + 1)2

)A3r(A− 2(r + 1))3

= −2CH̄(r + 1)2(2r + 1)

(3(A− (1 + r))2 + (r + 1)2

)A3r(A− 2(r + 1))3

> 0

(17)

The positive second-level differential means the human-capital accumulation

technology progress can accelerate intrinsic value of a firm. This result explains why

human capital enhancing technology plays a more productive role than production

technology in boosting share values. Besides contribution to production efficiency,

human capital accumulation technology itself, such as a faster self-studying search

engine like Google or an efficient online learning platform like Coursera, could lift

future human capital accumulation speed, resulting in even higher production tech-

nology. In the field of theoretical physics, Albert Einstein, standing on the accom-

plishment of Newton’s theoretical framework, was able to step forward to make the

world-changing contribution by developing the theory of relativity.

Similar to the traditional model, ∂V∂r < 0 and ∂2V∂r2

> 0 (proof is in the appendix

A1 & A2), indicating a diminishing firm value with respect to increase in interest

rate at a decreasing scale. A high interest hurts the value of a corporation through

not only decreasing the present value of future profit, but reducing the incentive for

future human capital investment.

(iii) Equilibrium III: Increasing human capital growth with finite share value.

13

This equilibrium happens when 2 + r < A < 2(1 + r). Most of the properties in

Equilibrium III is the same as Equilibrium II. The only difference is that the human

capital accumulation growth rate is positive for each period, which is still slower

than the growth of interest discount rate ((1 + r)t), forming a finite company share

price.

(iv) Equilibrium IV: Increasing human capital growth with unbounded share

price.

When human capital technology is high enough, i.e. A ≥ 2(1 + r), S(H̄) =∞.

This is equivalent to the case g > r in the discounted cash flow with growth model.

In this case, the approximate growth rate for human capital and profit level are

A−1− r, which even exceed the interest discount rate ((1+r)t), yielding an infinite

share price.

Figure 1: The relationship between firm value, human-capital-augmenting technol-ogy and interest rate

Figure 1 reflects the relationship between firm value, human-capital-augmenting

technology and interest rate when we normalizing C = 1 and H̄ = 1. Figure 2 shows

the case when interest rate equals 0.25 to provide a sectional view of share value.

14

There is a sudden jump at the threshold point A = 1.25 when shifting from Equilib-

rium I to Equilibrium II. Surpassing the critical point switches the economic growth

pattern from producing with raw labor to human capital accumulation. Figure 3

shows the case of A = 1.5 how firm value diminishes with interest rate at a decreasing

scale.

Figure 2: Firm value when r = 0.25

Figure 3: Firm value when A = 1.5

15

3 Equilibrium under political intervention

Now we switch to the case when the politically influential coefficient θ is not

zero. Different from Daron Acemoglu and James Robinson’s dichotomous defini-

tion of intrinsic and extractive institution, B and θ depict institutional differences

through continuous function. While, it is without any controversies that North Ko-

rea accounts for extractive institutions while the South is intrinsic, it is hard to judge

without any ambiguity whether Thailand’s institution is intrinsic or not. Allowing

continuous changes leave more room for picturing differences between countries’

regimes.

Define Sit =QitQ∗t

as the relative social status for agent i in period t. In the steady

state of hit and qit under constant inter-temporal relative social status assumption,

we have the following equilibrium conditions.

hie + qie =A− (1 + r)

A(18)

andH̄ i +H i

t

H̄ i +A(H̄ i +H it)h

ie

=θQ∗t+1B(λH̄ i +Q∗tS

ie)

A(1 + θ lnSie)(19)

where hie, qie, e

ie, S

ie are the steady state of hit, q

it, e

it, S

it respectively. And a flat

term structure rt ≡ r is assumed. Let τ = argmint hit, q

it, e

it, S

it all enter steady

state. With the recurrence definition of H it and Qit the following expressions can be

reached out.

H it = (H i

τ +AH̄ ihieAhie − 1

)(Ahie)t−τ − AH̄ ihie

Ahie − 1(20)

and

Qit = (Qiτ +BλH̄ iqieBqie − 1

)(Bqie)t−τ − BλH̄ iqie

Bqie − 1(21)

There exists three cases under the natural constraint of A ≥ 1 + r

(i) Equilibrium I. (Stagnant human capital accumulation whereHt cannot grow)

When A ≤ 2+r, we have hie <1A , ie. Ahie < 1. In this case hit keeps decreasing with

respect to t and consequently the steady state human capital accumulation hie = 0

and Hei = 0. With equation (19) we could have Q∗t+1 is also at its steady state Q∗e,

where Q∗e is the median agent’s equilibrium political capital and H̄ is the median

agent’s initial raw human capital endowment.

θQ∗eB(λH̄ +Q∗e)

A= 1 (22)

16

So we reach out the expression of Q∗e

Q∗e =−θBλH̄ +

√(θBλH̄)2 + 4AθB

2θB(23)

where

q∗e =Q∗e

BλH̄ +BQ∗e(24)

under the condition1

q∗e≤ A− 1− r

A(25)

ie

A >1 + r

1− qie(26)

It is straightforward to show that the relative social status of agent i in each period

is the ratio of raw human capital H̄ i for ith company to median raw human capital

endowment H̄.

Si0 = Si1 = ... = Sie = ... =H̄ i

H̄(27)

with Qi0 = λH̄ i and Qit+1 = B(λH̄ i + Qit)qie = B(λH̄ i + Qit)q

ie = −BλH̄iqie

Bqie−1for

∀t ≥ τ .

We could show that dq∗edθ < 0 (in the Appendix A3). Recalling θ denotes marginal

redistribution power between different social status, the equilibrium time effort to

accumulate political capital decreases with θ increases when there are no human

capital accumulation.

In this case, the after-redistribution profit is

P it = CH̄ i(1− qie)(1 + θ lnH̄ i

H̄) (28)

and the share value for the median company under stagnant equilibrium when en-

tering the steady state is

Vθ(H̄) =

∞∑t=0

CH̄ i(1− qie)(1 + θ ln H̄i

H̄)

(1 + r)t=CH̄ i(1− qie)(1 + θ ln H̄i

H̄)(1 + r)

r(29)

Clearly the value of firm under stagnant equilibrium is higher under larger ex-

ogenous Hicks-neutral production technology C, political-capital accumulation tech-

nology B, initial human capital endowment H̄ i and lower interest rate r. The most

remarkable result in this equilibrium, however, is that dVθdθ > 0, which means a higher

17

social unequal level could lead to a higher firm/stock value when firms only use raw

labor but no human capital to conduct production.

For the non-median corporation with relative social status Si, the policy func-

tion for determining qie is as follows.

θQ∗e(λH̄i +Qie) = A(1 + θ lnSie) (30)

where

qie =Qie

BλH̄ +BQie(31)

.

With the tool of comparative static analysis, it could be demonstrated that

dqiedSie

< 0 and dQiedqie

> 0 (proof in Appendix A4), which is consistent with the definition

of Sit that higher-rank agent has more political capital and devotes more time in

accumulating political resources.

The share value of the firm with relative class level Si is

V Si

θ =

∞∑t=0

CH̄ i(1− qie)(1 + θ lnSi)

(1 + r)t=CH̄ i(1− qie)(1 + θ lnSi)(1 + r)

r(32)

In the Appendix A5 we could demonstrateV S

i

θ

dSi> 0 if and only if B > 1.

North Korea, to some extent, could be a suitable example depicting this equilibrium.

The marginal gain from accumulating political capital exceeds marginal loss from

relinquished production time for the sake of political capital accumulation. In this

case, upper class has a far better agent value than lower class. For a rational agent,

the reasonable choice is to make social status as high as possible. In North Korea’s

example, closely following the dictator seems to be the only rational choice for all

agents, by fair means or foul.

Mathematically, it is also valid whereV S

i

θ

dSi< 0 when B < 1. However, since we

can hardly find any corresponding example in modern society, we will not consider

this possibility.

Equilibrium I is stable.

(ii) Equilibrium II and III. (Increase in human capital accumulation)

As Equilibrium I could fail to depict the real world for most countries in 21st cen-

tury, we switch to the Equilibrium II where exists steady growth in human capital

accumulation. The condition Ah > 1 is sufficient to guarantee the existence of

18

Equilibrium II. With Equation (19) and (20), it could be reached out that

limt→∞

H̄ i +H it

H̄ i +H it+1

=1

Ahie(33)

We rewrite equation (19),

(A− r − 1

A− qie)θQ∗t+1B(λH̄ i +Q∗tS

ie) = 1 + θ lnSie (34)

From the above equation it could be found Qit is bounded and we should have at

the equilibrium state

limt→∞

Qti =BλH̄ iqie1−Bqie

(35)

when

B <1

qie(36)

which means the political-capital accumulation speed is slow in this equilibrium. If

Q∗t is replaced with q∗t , then

(A− r − 1

A− qie)

BλH̄ iqie1−Bqie

B(λH̄ i +BλH̄ iqie1−Bqie

) =Sieθ

+ Sie lnSie (37)

with

0 ≤ qie

<

1

B, if

1

B≤ A− r − 1

A

≤ A

A− r − 1, if

1

B>A− r − 1

A

(38)

We have two cases with different democracy level B.

Equilibrium II (Democratic Equilibrium): When 1B ≤

A−r−1A , i.e. B ≥

AA−r−1 , for higher class agents with Sidem ≥ 1, no matter what θ is, there exists one

unique equilibrium state {qidem, hidem, eidem}. For lower class agents with Sidem < 1, if

and only if θ ≤ − 1lnSidem

, there exists one unique equilibrium state {qidem, hidem, eidem}.

For all 0 < Sidem <∞, we have

(a) (w.r.t social status)∂qidem∂Sidem

> 0,∂hidem∂Sidem

< 0,∂eidem∂Sidem

= 0

(b) (w.r.t. political influence coefficient)∂qidem∂θ < 0,

∂hidem∂θ > 0,

∂eidem∂θ = 0

(c) (w.r.t. to democracy level)∂qidem∂B < 0,

∂hidem∂B > 0,

∂eidem∂B = 0

(d) (w.r.t how raw human capital impacts initial political endowments)∂qidem∂λ < 0,

∂hidem∂λ > 0,

∂eidem∂λ = 0

19

(e) (w.r.t. human capital accumulation coefficient)∂qidem∂A < 0,

∂hidem∂A > 0,

∂eidem∂A <

0

(f) (w.r.t. interest rate)∂qidem∂r > 0,

∂hidem∂r < 0,

∂eidem∂r > 0

Proof is in Appendix B1.

In the democratic case (B high enough) a unique equilibrium could be reached

with relative small proportion of allocation on political capital and large on human

capital accumulation (comparing to Equilibrium III Authoritarian Case in the

following context). In our benchmark model human capital is the only accelera-

tor of long-term economic growth. Property (a) indicates that political advantaged

agents invest less in human capital than in political capital because marginal profit

from investing an additional unit of political capital is higher. It is demonstrated in

property (b) that the country with large political influence (θ) should enjoy a higher

prosperity level. Most low-rank agents in the social rank pyramid respond to high

political influence by reducing inefficient political capital investment, leading to an

increase in human capital stock. The most remarkable property is that the growth

level strictly increases with respect to democracy level. Different from Acemoglu and

Robinson’s dichotomous definition of institution (intrinsic and extractive), we adopt

political capital accumulation speed (B) to capture the democracy level, which is

allowed to be continuous in our approach. From property (c), it is explicitly stated

without ambiguity that human capital accumulation is positively related to the in-

clusiveness of political institution. The economic intuition of property (d) could

be better interpreted as labor union. Recalling the definition of political capital

accumulation, λ is a good indicator reflecting the strength of union. Property (d)

demonstrates that countries with high union power is accompanied by high human

capital investment level. Property (e) and (f) is the natural extension of previous

deduction in the previous content of this article, where human capital investment

increases with high human-capital-augmenting technology and low interest rate con-

dition.

In Figure 4 we simulate the Democratic Equilibrium with B = 2, H̄ i = 1, λ = 1,

A = 5, r = 0.1.

When B is not high enough, say B < AA−r−1 , the following authoritarian equi-

librium is reached out.

Equilibrium III (Authoritarian Equilibrium) When 1B > A−r−1

A , i.e. B <

AA−r−1 , there are two equilibrium states.

20

Figure 4: Democratic Equilibrium: the relationship between q and θ

(i) Equilibrium IIIG (Good Authoritarian Equilibrium) {qiautg, hiautg, eiautg}

when (a) Siaut ≥ 1, θ ≥ θ(Saut) or (b) Siaut < 1 , θ(Saut) ≤ θ ≤ − 1lnSiaut

, where θ(Siaut)

is a threshold depending on Siaut. The property of good authoritarian equilibrium

is the same as Equilibrium II (Democratic Equilibrium) {qidem, hidem, eidem}

(ii) Equilibrium IIIB (Bad Authoritarian Equilibrium) {qiautb, hiautb, eiautb}

when (a) Siaut ≥ 1, θ ≥ θ(Saut) or (b) Siaut < 1 , θ(Saut) ≤ θ ≤ − 1lnSiaut

, where the

threshold function θ(Siaut) is the same as good equilibrium case. When we compare

good equilibrium {qiautg, hiautg, eiautg} with bad equilibirium {qiautb, hiautb, eiautb}, we

have

qiautg ≥ q∗ ≥ qiautb, hiautg ≤A− r − 1

A− q∗ ≤ hiautb, eiautg = eiautb =

1 + r

A(39)

where

0 < q∗ =A− r − 1

2A+B +Br −AB<A− r − 1

A<

1

B(40)

21

and following 6 properties.

(a) (w.r.t social status)∂qiautb∂Siaut

< 0,∂hiautb∂Siaut

> 0,∂eiautb∂Siaut

= 0

(b) (w.r.t. political influence coefficient)∂qiautb∂θ > 0,

∂hiautb∂θ < 0,

∂eiautb∂θ = 0

(c) (w.r.t. to democracy level)∂qiautb∂B > 0,

∂hiautb∂B < 0,

∂eiautb∂B = 0

(d) (w.r.t how raw human capital impacts initial political endowments)∂qiautb∂λ > 0,

∂hiautb∂λ < 0,

∂eiautb∂λ = 0

(e) (w.r.t. human capital accumulation coefficient)∂qiautb∂A > 0,

∂hiautb∂A indeter-

mined,∂eiautb∂A < 0

(f) (w.r.t. interest rate)∂qiautb∂r < 0,

∂hiautb∂r indertermined,

∂eiautb∂r > 0

Proof is in Appendix B2.

In the authoritarian case, there exist two equilibrium. One is called “good”

authoritarian equilibrium while the other is “bad”. The characteristics of good au-

thoritarian equilibrium is the similar to democratic one. More prestigious firms

invest more in human capital but not political resources. A larger political influ-

ence coefficient leads to an increasing human capital accumulation effort while the

enhancement of democratic level improves human capital condition. Typical coun-

tries staying in this authoritarian “good” equilibrium include Singapore, Qatar and

United Arab Emirates. On the other hand, “bad” authoritarian equilibrium has

very different characteristics. Examples could be Cambodia, Russia and Indonesia.

The equilibrium investing in political capital increases with decreasing social ranks,

where firms lack of political capital have to put much effort in political capital accu-

mulation to avoid being exploited thoroughly. All agents respond to an increasing

level of political influence coefficient θ by throwing more time spent on political

investments, which is exactly contrary to the democratic and authoritarian “good”

equilibrium. Property (c) demonstrates that the increasing democracy level B in

“bad” authoritarian equilibrium could make the whole economy worse with less hu-

man capital accumulation. The democracy reform of Soviet Union under president

Mikhail Gorbachev could be a good example reflecting this property. Unless the im-

provement could switch bad authoritarian equilibrium to good or democratic one,

the incomplete democracy reform itself could stimulate agents in the economy to

quit investment in human capital and turn back to invest in political capital.

22

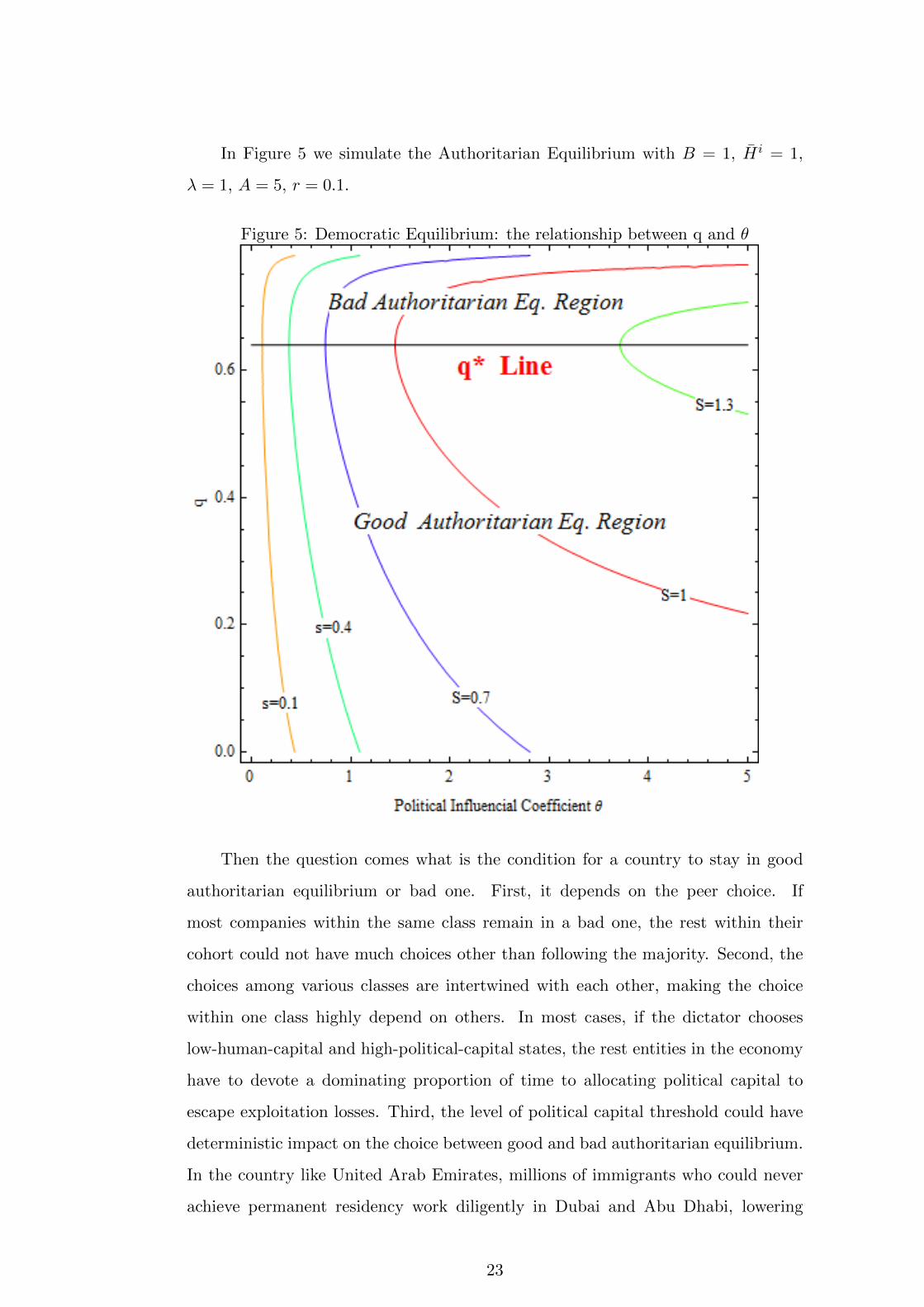

In Figure 5 we simulate the Authoritarian Equilibrium with B = 1, H̄ i = 1,

λ = 1, A = 5, r = 0.1.

Figure 5: Democratic Equilibrium: the relationship between q and θ

Then the question comes what is the condition for a country to stay in good

authoritarian equilibrium or bad one. First, it depends on the peer choice. If

most companies within the same class remain in a bad one, the rest within their

cohort could not have much choices other than following the majority. Second, the

choices among various classes are intertwined with each other, making the choice

within one class highly depend on others. In most cases, if the dictator chooses

low-human-capital and high-political-capital states, the rest entities in the economy

have to devote a dominating proportion of time to allocating political capital to

escape exploitation losses. Third, the level of political capital threshold could have

deterministic impact on the choice between good and bad authoritarian equilibrium.

In the country like United Arab Emirates, millions of immigrants who could never

achieve permanent residency work diligently in Dubai and Abu Dhabi, lowering

23

local political beneficial threshold Q∗. The differences of immigration policy partly

explain why United Arab Emirates stays in the good authoritarian equilibrium while

Vietnam with fewer immigrants is in the bad one.

4 Case Study

Equilibrium I

In Equilibrium I, there is no human capital accumulation because A ≤ 2 + r.

This describes the situation in many least developed countries, where political insta-

bility, prevalence of human rights invasion and ongoing warfare drive up the discount

rate to a level so high that any substantial human capital accumulation becomes not

worthwhile. This equilibrium most likely depicts the case in those least developed

countries such as North Korea, Syria and many Sub-Saharan countries. In Middle

East Asian and Sub-Saharan countries that are without centralized political author-

ities, citizens cannot be certain about what the social order will be like in the near

future and therefore, cannot commit themselves to making long-term investment

in any education or training. In North Korea, although there exists a centralized

government, the inflation rate has remained at high level varying between 30% to

triple digits. At the same time, North Korean citizens lack most of basic human

rights such as basic education, which yields a relatively small A (human capital ac-

cumulation technology coefficient). In our model, these two factors combined trap

the country in economic stagnancy despite a centralized political authority.

Equilibrium II

When A ≤ 2+r and B ≥ AA−r−1 , countries fall into the status of Equilibrium II,

which largely reflects the reality in democratic nations since B is the political access

coefficient. Democratic countries here refer to countries that are politically inclusive

and where the access to political power is generally open and fair to everyone.

United States is definitely a good example since everyone can acquire political capital

through various channels, such as military service, advocacy work and community

service. The election process involves almost all citizens and have a high level of

procedural transparency. Others countries that qualify for this category include

United Kingdom, Canada, Australia, and developing democratic countries including

Brazil and India.

Within the same country, companies enjoying more abundant stock of political

capital will choose to invest more in political capital while companies that rank

24

lower in relative political capital stock will invest more in human capital according

to Equilibrium II property (a). This deduced property is in conformity with our

observations that at an initial stage, small companies focus on its core competency

and technology and when they grow bigger, they start to participate more actively

in industrial standard establishment and seek more connections with policy makers

and regulators. Although they can still invest a great deal in human resource, on

a relative scale they mostly allocate more resource in public relations and politics

compared to at initial stage of their businesses.

If we examine across countries with distinct political environment, investment

in political capital decrease or human capital investment increases with respect to B

or θ increase. United States, in our modeling, enjoys a high level of both B and θ,

and it has been investing a huge amount in human capital. While B describes how

easy political capital is accessible to everyone, theta means how influential compa-

nies can exert this political power. The property indicates that when it is easier to

gain and execute political capital (B and θ is larger) countries invest more human

capital. This might be somehow counter-intuitive but it is in fact reasonable if we

think about it. United States actually has a higher B and theta compared to Brazil

and India. Why? Because in the United States, electoral process and policy making

are much more transparent and routine. For example, in 1995, Congress passed the

Lobbying Disclosure Act (LDA) that defined the term “lobbyist” as “any individual

who is employed or retained by a client for financial or other compensation for ser-

vices that include more than one lobbying contact.”, and all legal documents of this

sort make political activity a smoother and more standardized process manageable

and accessible to all market participants. In this case, companies do not have to

engage in illegal activities or wander around grey legal and policy arena to accu-

mulate and execute political power and therefore, choose to invest more “effort” in

human capital. California has been the heart of Democratic states due to Demo-

crat’s favourable policies on immigrants and regulation freedom. Since 2008, the

Internet firms, software companies, computer manufacturers and data processors

that comprise Silicon Valley have delivered more than 172 million dollars in cam-

paign contributions for federal elections, according to data compiled by the Center

for Responsive Politics. This amount is not as much if we look at another case in

India. In 2013, Indian government launched an investigation on the allegations that

Wal-Mart had bribed officials in New Delhi to gain access to India’s lucrative retail

25

market, amount of which is disclosed at around 25 million dollars. Assertions that

lobbying is tantamount to bribery are common in India, reflecting that the coun-

try’s legal and policy ambivalence towards the practice is not formally regulated.

As a result, endemic corruption slows down the development in India and impedes

investment in technology and human capital. Brazil shares a similar story and is

thus deeply sunk in distress due to corruption and bribery scandals.

Equilibrium IIIG

In both Equilibrium IIIG and IIIB, countries who have the property of B <

AA−r−1 are classified into “authoritarian” regimes. In the case of Equilibrium IIIG,

authoritarian countries enjoy similar resource allocation strategy in human and po-

litical capital to countries in Equilibrium II. However, if authoritarian countries

unfortunately fall into Equilibrium IIIB, the properties can change massively and

generally witness much more investment in political capital rather than human cap-

ital. In reality, we can find only a few countries satisfying these characteristics,

including Singapore and Qatar. Constitutionally, Singapore is a parliamentary re-

public with a Westminster system of unicameral parliamentary government. How-

ever, as People’s Action Party has been in control since Singapore’s independence,

this country is mostly regarded as an authoritarian if not autarky. Qatar is known

as an absolute monarchy. However, both Singapore and Qatar are among the richest

countries: Singapore has GDP per capita of more than 50,000 US dollars and Qatar

more than 70,000 US dollars.

There are two factors playing a major part in drawing countries to either equi-

librium. The first factor is Q∗, the politically influential threshold. Note that both

Singapore and Qatar have large population of foreign workers. Singapore has 1.4

million foreign workers equivalent to 25% of total population. Qatar is notorious of

its exploitation of migrant workers which construct more than 90% of its popula-

tion. High percentage of migrant workers lowers countries’ Q∗ level, which means

that for most companies established by citizens with political rights, they receive ex-

tra benefits aside from their own production. Migrant workers provide products and

services generating bonus revenues to citizens through government income-transfer

such as taxes. The second factor that drives authoritarian countries into this equi-

librium rather than Equilibrium IIIB is the result of choices made by the majority

of companies at similar Q levels, which was ultimately decided by the highest polit-

ical class of the societies. For example, under the system of meritocracy forged by

26

renowned First Prime Minister Lee Kuan Yew, Singapore government was highly ef-

fective and introduced legislation giving the Corrupt Practices Investigation Bureau

(CPIB) great power to conduct arrests, search, call up witnesses, and investigate

bank accounts and income-tax returns of the suspected officials. The choice of curb-

ing investment in political power made by the leader is equivalent to a strong pull

to the good equilibrium for the authoritarian country. Similar in Qatar, the gov-

ernment has streamlined its regulations regarding business practices and engaged

in reforms from above that have liberalized the Qatar’s economy and increased its

strength and viability, which makes it among the highest performing countries in the

Middle East and North Africa. The initial “choice” from the highest-ranked political

leaders also play a major part in securing the countries on the “good” equilibrium

together with the factor of Q∗.

Equilibrium IIIB

Equilibrium IIIB reflects authoritarian countries who unfortunately stay with

the “bad” equilibrium. Typical countries include many of those in South Asia such

as Cambodia and Bangladesh, in Middle Asia such as Tajikistan and Kyrgyzstan,

and in Africa such as Uganda and Kenya. In this status, citizens put more efforts

in acquiring political power than human capital, although their human capital still

grows very slowly compared to countries in Equilibrium I stagnant economy where

human capital deteriorates over time. The properties of this equilibrium are exactly

opposite to Equilibrium IIIG. Within the same country, companies enjoying more

abundant stock of political capital will choose to invest less in political capital.

If we examine across countries with distinct political environment, investment in

political capital increase or human capital investment decreases with respect to B

or θ increase. The property indicates that when it is easier to gain and execute

political capital (B and θ is larger), countries invest less human capital.

These contrary properties relative to democratic equilibrium provide a possible

explanation on why issues can emerge if authoritarian countries, without changing

their political regimes, directly copy some specific policies from United States. For

example, Unites States’ legalizing lobbying activities, which is clearly the action to

increase B and θ in our model, might never take place in authoritarian countries,

because political leaders are aware of the disastrous consequences that could result

from this policy shift: all will choose to invest as much as possible in political capital

and the economy will suffer. Instead, political leaders in authoritarian countries

27

usually advocate anti-corruption moves and exert all efforts to crack down nepotism

and bribery although these actions are futile for most of time. In these authoritarian

countries, if autocrats imprudently decide to adopt more politically inclusive policies

such as legalizing lobby activities and granting more policy-making influence to

companies, their own political power might be eroded and the country will be kicked

off on the path towards a politically inclusive country if B becomes larger than AA−r−1

which is condition for countries to stay in Equilibrium II. Acemoglu in his book

(2012) has also reached similar conclusions that autocrats choose to stay autocrats

because making the regime politically or economically inclusive will result in the

deprivation of their own power.

Transitional Status

Like any theoretical models, the listed equilibrium cannot fully describe all coun-

tries in the world. Many countries, however, are in the transitional status somewhere

in between these equilibrium discussed. For example, China, being identified as an

“authoritarian” regime, has witnessed fast economic growth during past decades

of reform and opening up economic policy. However, its political inclusiveness has

not been improved at the same scale of economic policy reform. There are three

directions China might fall onto: Equilibrium II, Equilibrium IIIG and Equilibrium

IIIB.

To reach Equilibrium II, China needs to switch to a regime more politically

inclusive just like the democracy reform Taiwan experienced during 1980s after

Kaohsiung Incident. This requires politically-influential upper class to relinquish

a substantial political power and liberate political capital market, and therefore,

considerably increase B to a level higher than AA−r−1 . This without doubt a depriva-

tion of political upper class’s vested interest. The process can be extremely bumpy

and might cause painful turbulence to China’s economy. The number of countries

who enjoy a sustainable growth by human capital accumulation in Equilibrium IIIG

are relatively limited compared to Equilibrium I. We have only found Singapore,

Qatar and maybe the United Arab Emirates who are successful in economic growth.

Common characteristics among them include: 1. The size of their economies is small,

which simplifies the process of streamlining regulations regarding business practices

and any liberalization schemes; 2. Their economies depend heavily on migrant work-

ers. China is an economy with much more complicated properties including regional

development difference, rural-urban divide, aging societies and homogeneity of labor

28

force (few immigrants). Therefore if China is to progress towards Equilibrium IIIG,

there might not be proper role-models to follow. If China fails to transition into

Equilibrium II or IIIG, the only option left in our model is IIIB, the equilibrium

for most of the underdeveloped nations now where economic development is largely

restrained under a stable authoritarian regime.

5 Concluding Remarks

This paper has explored different ways nations can develop. By finding stable

statuses under assumptions of parameters, we have identified theoretical develop-

ment patterns for stagnant countries, politically inclusive countries and authoritarian

countries. For politically inclusive countries, there exists only one equilibrium and

the share of resource allocation to human capital depends on how effective political

capital can influence production redistribution and the politically beneficial thresh-

old. For authoritarian countries, unlike mainstream argument that their economic

growth is most likely unsustainable, our modeling result suggests that it is possible

for those countries to enjoy long-lasting economic development as well if they hap-

pens to stay with the “good” equilibrium given proper political and policy nudges.

We believe these results to be important for understanding why nations succeed and

provide a theoretical framework where practical policy-making can be built on.

This article also sheds light on future research in political and development

economics. The precise calibration and estimation of political accessibility index B

and political influence parameter θ is beyond further research, which is somehow

different from current widely-used democracy or corruption index. At least from

Equilibrium IIIG we know there are more than one way towards long-term economic

prosperity. But what is the initial motive for authoritarian countries like Singapore,

Qatar leaning to high human capital and low political capital investment? For

example, what drives Singapore to enact immigrant-friendly policy thus lowering

the local political beneficial threshold Q∗ so that it could have more chance getting

close to good authoritarian equilibrium? Could the size of economy play a part? Or

it is simply because Singapore is lucky enough to have Cambridge First Class Honor

graduate Lee Kuan Yew as its founding father while unfortunate for Philippines to

have rapacious Ferdinand Marcos. This, of course, calls for future works.

29

Appendix

A1. The proof of ∂V∂r < 0.

∂V

∂r=CH̄(r + 1)

(−A

(4r2 + r − 1

)+ 4r3 + 4r2 − 2r − 2

)Ar2(A− 2(r + 1))2

≤CH̄(r + 1)

(−2(1 + r)

(4r2 + r − 1

)+ 4r3 + 4r2 − 2r − 2

)Ar2(A− 2(r + 1))2

=CH̄(r + 1)(−2r(1 + 3r + 2r2)

Ar2(A− 2(r + 1))2

< 0

(41)

given 1 + r < A < 2(1 + r)

A2. The proof of ∂2V∂r2

> 0.

∂2V

∂r2= −

2CH̄(A2(2r3 + 1

)+ 2A(r − 2)(r + 1)2 + 4(r + 1)3

)Ar3(A− 2(r + 1))3

= −2CH̄

((1 + 2r3)(A+ (−2+r)(1+r)2

2(1+2r3))2 + (1+r)3(12−8r−5r2+31r3)

4(1+2r3)

)Ar3(A− 2(r + 1))3

> 0

(42)

given 1 + r < A < 2(1 + r)

A3. The proof of dq∗edθ < 0.

We take the total differentiation of

θQ∗eB(λH̄ +Q∗e) = A (43)

we have

Q∗eB(λH̄)dθ + θB(λH̄ + 2Q∗e)dQ∗e = 0 (44)

dθ

dQ∗e= −θB(λH̄ + 2Q∗e)

Q∗eB(λH̄)< 0 (45)

Noticedq∗edQ∗e

=BλH̄

(BλH̄ +BQ∗e)2> 0 (46)

Use the chain rule we havedq∗edθ

=dq∗edQ∗e

dQ∗edθ

< 0 (47)

30

A4. Proof of dqiedSie

> 0 and dqiedQie

> 0

We take the total differentiation of

θQ∗e(λH̄i +Qie) = A(1 + θ lnSie) (48)

we have

θQ∗edQie =

Aθ

SiedSie (49)

We could havedQiedSie

=A

Q∗eSie

> 0 (50)

NoticedqiedQie

> 0 (51)

Use the chain rule we havedqiedθ

=dqiedQie

dQiedθ

> 0 (52)

A5. Proof ofdV S

i

θ

dSi> 0 when B > 1 and

dV Si

θ

dSi< 0 when B < 1 where

V Si

θ =

∞∑t=0

CH̄ i(1− qie)(1 + θ lnSi)

(1 + r)t=CH̄ i(1− qie)(1 + θ lnSi)(1 + r)

r(53)

we only need to show ddSie

(1− qie)(1 + θ lnSi)<=>

0 if B<=>

1

Notice

d

dSie(1− qie)(1 + θ lnSi)

=dSiedQie

d

dQie(1− qie)(1 + θ lnSi)

=dSiedQie

d

dQie(1− Qie

BλH̄ i +BQie)(θQ∗e(λH̄

i +Qie)

A)

=dSiedQie

Q∗eθ(Qie +Hλ)

(BQie

(BQie+BH̄iλ)2− 1

BQie+BH̄iλ

)A

+Q∗eθ

(1− Qie

BQie+BH̄iλ

)A

=dSiedQie

(−1 +B)Q∗eθ

AB

<=>

0

(54)

31

if and only if B<=>

1 since dSiedQie

> 0. The statement is proved.

B1. Proof of Equilibrium II

First we prove a Lemma.

Lemma. Under B ≥ AA−r−1 and 0 ≤ qidem < 1

B , we have AB−A−B−Br ≥ 0 and

A− r − 1−Aqidem > 0.

AB −A−B −Br ≥ 0

⇔ AB −Br −B ≥ A

⇔ B ≥ A

A− r − 1

(55)

and

A− r − 1−Aqidem > 0

⇔ qidem <A− r − 1

A

This is because qidem <1

B≤ A− r − 1

A

(56)

Lemma is proved.

With

(A− r − 1

A− qidem)

BλH̄ iqidem1−Bqidem

B(λH̄ i +BλH̄ iqidem1−Bqidem

) =Sidemθ

+ Sidem lnSidem (57)

we define

LHS(qidem) = (A− r − 1

A− qidem)

BλH̄ iqidem1−Bqidem

B(λH̄ i +BλH̄ iqidem1−Bqidem

) (58)

Notice LHS(0) = 0 and limqidem→1BLHS(qidem) =∞, then we show

dLHS(qidem)

dqidem> 0

dLHS(qidem)

dqidem= −

B2H̄ i2(A(1 + (−2 +B)qidem)− (1 +Bqidem)(1 + r))λ2

A(−1 +Bqidem)3

= −B2H̄ i2λ2(qidem(AB −A−B −Br) + (A− r − 1−Aqidem))

A(−1 +Bqidem)3

> 0

(59)

The last inequality is due to Lemma and Bqidem < 1

we define

RHS(θ, Sidem) =Sidemθ

+ Sidem lnSidem (60)

32

If Sidem ≥ 1, with any θ ≥ 0, we have RHS(θ, Sidem) ≥ 0. Thanks to Intermediate

Value Theorem, we could show there exists a unique qidem ∈ [0, 1B ) to make the

LHS = RHS. If Sidem < 1, when θ < − 1lnSidem

, RHS < 0, the equilibrium does not

exist; when θ ≥ − 1lnSidem

, RHS ≥ 0, it exists a unique equilibrium qidem ∈ [0, 1B )

SincedLHS(qidem)

dqidem> 0 for qidem ∈ [0, 1

B ), we have

dqidemdRHS

> 0 (61)

and with dRHSdSidem

> 0 and dRHSdθ < 0 we have

∂qidem∂Sidem

> 0 and∂qidem∂θ < 0. Under

qidem + hidem = A−r−1A , we could reach out

∂hidem∂Sidem

< 0,∂hidem∂θ < 0,

∂eidem∂Sidem

= 0,

∂eidem∂θ = 0,

By calculating the total differetiation of LHS and rearraning terms, we have

∂qidem∂B

=2qidem(1 +A(−1 + qidem) + r)

B[qidem(AB −A−B −Br) + (A− r − 1−Aqidem)]< 0 (62)

The inequality is because of Lemma. So∂hidem∂B > 0,

∂eidem∂B = 0.

Similarly we have

∂qidem∂λ

= −2qidem(−1 +Bqidem)(1 +A(−1 + qidem) + r)

λ[qidem(AB −A−B −Br) + (A− r − 1−Aqidem)]< 0 (63)

So∂hidem∂λ > 0,

∂eidem∂λ = 0.

And∂qidem∂A

=qidem(−1 +Bqidem)(1 + r)

A[qidem(AB −A−B −Br) + (A− r − 1−Aqidem)]< 0 (64)

and∂eidem∂A = − r+1

A2 < 0. With constraint hidem+qidem+eidem = 1, we have∂hidem∂A > 0.

Similarly we could demonstrate∂qidem∂r > 0,

∂hidem∂r < 0,

∂eidem∂r > 0

B2. Proof of Equilibrium III

First we prove another Lemma*.

Lemma*. Under A > 1 + r, B < AA−r−1 and 0 ≤ qiautb < A

A−r−1 , we have

2A+B +Br −AB > A and thus 0 < q∗ = A−r−12A+B+Br−AB < A−r−1

A .

33

0 < q∗ =A− r − 1

2A+B +Br −AB<A− r − 1

A

⇔ 2A+B +Br −AB > A

⇔ AB −Br −B < A

⇔ B <A

A− r − 1

(65)

Lemma* is proved.

we define

LHS(qiautb) = (A− r − 1

A− qiautb)

BλH̄ iqiautb1−Bqiautb

B(λH̄ i +BλH̄ iqiautb1−Bqiautb

) (66)

Notice LHS(0) = 0 and LHS( AA−r−1) = 0. While

dLHS(qiautb)

dqiautb

=−B2H̄ i2λ2(qiautb(AB − 2A−B −Br) + (A− r − 1))

A(−1 +Bqiautb)3

⇒

> 0 if 0 < qiautb < q∗

< 0 if q∗ < qiautb <A− r − 1

A

(67)

Define

RHS(θ, Siaut) =Siautθ

+ Siaut lnSiaut (68)

If Siaut ≥ 1 and θ(Siaut) ≥Siaut

LHS(q∗)−Siaut lnSiautor if Siaut < 1 and

SiautLHS(q∗)−Siaut lnSiaut

≤

θ(Siaut) ≤ − 1lnSiaut

, there exists two equilibrium states with qiautg ≤ q∗ ≤ qiautb that

makes LHS = RHS under Intermediate Value Theorem.

The properties of {qiautg, hiautg, eiautg} are the same as {qidem, hidem, eidem} while prop-

erties of {qiautb, hiautb, eiautb} opposite {qidem, hidem, eidem} with similar demonstration

procedure in 2A.

34

References

Acemoglu, Daron, and James Robinson. Why nations fail: The origins of

power, prosperity, and poverty. Crown Business, 2012.

Ansolabehere, Stephen, John M. De Figueiredo, and James M. Snyder.

“Why is there so little money in US politics?.” The Journal of Economic Per-

spectives 17.1 (2003): 105-130.

Antrs, Pol, Luis Garicano, and Esteban Rossi-Hansberg. Offshoring in a

knowledge economy. No. w11094. National Bureau of Economic Research,

2005.

Antrs, Pol, and Davin Chor. “Organizing the global value chain.” Econometrica

81.6 (2013): 2127-2204.

Antras, Pol. “forthcoming, Grossman-Hart (1986) Goes Global: Incomplete

Contracts, Property Rights, and the International Organization of Production.”

Journal of Law and Economics.

Bai, Jie, et al. “Firm Growth and Corruption: Empirical Evidence from Vietnam.”

(2016).

Barro, Robert J. Economic growth in a cross section of countries. No. w3120.

National Bureau of Economic Research, 1989.

Becker, Gary S. “A theory of competition among pressure groups for political

influence.” The Quarterly Journal of Economics (1983): 371-400.

Becker, Gary S., and Kevin M. Murphy. “The division of labor, coordination

costs, and knowledge.” Human Capital: A Theoretical and Empirical Analysis

with Special Reference to Education (3rd Edition). The University of Chicago

Press, 1994. 299-322.

Becker, Gary S., Kevin M. Murphy, and Robert Tamura. “Human capital,

fertility, and economic growth.” Human Capital: A Theoretical and Empirical

Analysis with Special Reference to Education (3rd Edition). The University of

Chicago Press, 1994. 323-350.

Cooper, Michael J., Huseyin Gulen, and Alexei V. Ovtchinnikov. “Cor-

porate political contributions and stock returns.” The Journal of Finance 65.2

(2010): 687-724.

Del Monte, Alfredo, and Erasmo Papagni. “Public expenditure, corruption,

and economic growth: the case of Italy.” European journal of political economy

17.1 (2001): 1-16.

35

Ehrlich, Isaac, and Francis T. Lui. “Bureaucratic corruption and endogenous

economic growth.” Journal of Political Economy 107.S6 (1999): S270-S293.

Faccio, Mara, Ronald W. Masulis, and John McConnell. “Political connec-

tions and corporate bailouts.” The Journal of Finance 61.6 (2006): 2597-2635.

Faccio, Mara. “Politically connected firms.” The American economic review 96.1

(2006): 369-386.

Gibbs, Jack P., and Walter T. Martin. “Urbanization, technology, and the

division of labor: International patterns.” American sociological review (1962):

667-677.

Hansen, Wendy L., and Neil J. Mitchell. “Disaggregating and explaining

corporate political activity: Domestic and foreign corporations in national pol-

itics.” American Political Science Review 94.04 (2000): 891-903.

Hillman, Amy J., Asghar Zardkoohi, and Leonard Bierman. “Corporate

political strategies and firm performance: Indications of firm-specific benefits

from personal service in the US government.” Strategic Management Journal

20.1 (1999): 67-81.

Kang, David C. Crony capitalism: Corruption and development in South Korea

and the Philippines. Cambridge University Press, 2002.

Kim, Jongwook, and Joseph T. Mahoney. “Property rights theory, transac-

tion costs theory, and agency theory: an organizational economics approach to

strategic management.” Managerial and decision economics 26.4 (2005): 223-

242.

Krueger, Anne O. “The political economy of the rent-seeking society.” The Amer-

ican economic review 64.3 (1974): 291-303.

Limongi, Fernando, and Adam Przeworski. “Political regimes and economic

growth.” Journal of Economic Perspectives 7.3 (1993): 51-69.

Mauro, Paolo. “Corruption and growth.” The quarterly journal of economics

(1995): 681-712.

Milyo, Jeffrey, David Primo, and Timothy Groseclose. “Corporate PAC

campaign contributions in perspective.” Business and Politics 2.1 (2000): 75-

88.

Nguyen, Thuy Thu, and Mathijs A. Van Dijk. “Corruption, growth, and

governance: Private vs. state-owned firms in Vietnam.” Journal of Banking &

Finance 36.11 (2012): 2935-2948.

36

Pellegrini, Lorenzo, and Reyer Gerlagh. “Corruption’s effect on growth and

its transmission channels.” Kyklos 57.3 (2004): 429-456.

Posner, Richard A. “Economic approach to law.” Tex. L. Rev. 53 (1974): 757.

Rodriguez-Clare, Andres. “The division of labor and economic development.”

Journal of Development Economics 49.1 (1996): 3-32.

Romer, Paul M. Human capital and growth: theory and evidence. No. w3173.

National Bureau of Economic Research, 1989.

Song, Zheng, Kjetil Storesletten, and Fabrizio Zilibotti. “Growing like

china.” The American Economic Review 101.1 (2011): 196-233.

Stigler, George J. “The Division of Labor is Limited by the Extent of the Market.”

The Journal of Political Economy (1951): 185-193.

Stigler, George Joseph. The citizen and the state: Essays on regulation. Vol.

834. Chicago: University of Chicago Press, 1975.

Useem, Michael. The inner circle: Large corporations and the rise of business

political activity in the US and UK. Oxford University Press, 1986.

Yang, Xiaokai, and Dingsheng Zhang. “Endogenous structure of the division

of labor, endogenous trade policy regime, and a dual structure in economic

development.” Annals of Economics and Finance 1.1 (2000): 211-230.

Yang, Xiaokai, and Jeffrey D. Sachs. Economic development and the division

of labor. John Wiley & Sons, 2008.

37