wi seminar series - cottingham & butler · 2019-11-19 · wi seminar series cottingham &...

TRANSCRIPT

Presented By |

WI Seminar Series

Cottingham & Butler

March 14-15, 2017

Employee Benefits

Revolutionizing Healthcare

Through Transparency

Employer Presentation

Company Overview

Who We Are

HST is at the forefront of Value-

Based Payments (VBP). Since

2009, we have helped reduce our

clients healthcare costs.

What We Do

We provide pricing solutions

that reduce healthcare costs for

payers and consumers.

We bring pricing accountability

through transparency.

Our Goal

We are revolutionizing healthcare

through pricing transparency.

Through value-based payments

we are bending the cost curve

downward.

Headquarters

We are located

in Irvine, California.

© 2016 HST All Rights Reserved | Confidential | page 4

VBP Facts About HST

2%

Push

Back

15Pricing

Databases

43States

Covered

98%

Acceptance

Rate

LESS

THAN

© 2016 HST All Rights Reserved | Confidential | page 5

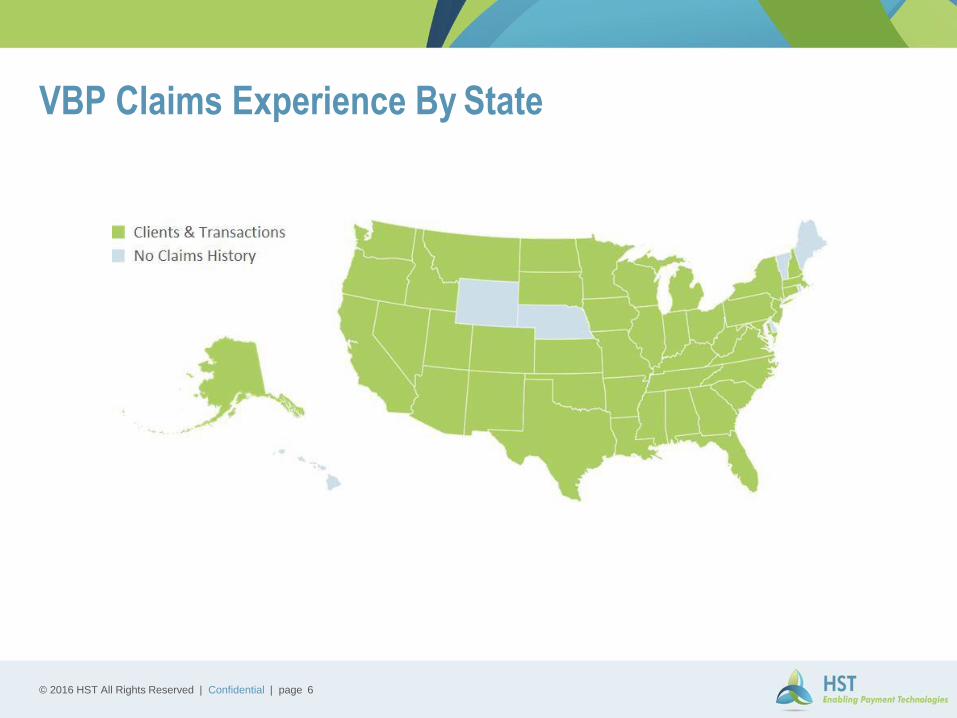

VBP Claims Experience By State

© 2016 HST All Rights Reserved | Confidential | page 6

What is Value-Based Payments?

VBP is a reimbursement that uses Medicare and Cost Information to determine the

prevailing price for medical services.

Types of VBP

• Medicare factor equivalent

• VBP Health Plan

• Cost Plus

• Procedure specific

• Consumer driven

Quality

• Frequency of services as a leading indicator

• Readmission rates – outcomes

• Top hospital evaluation criteria

• High risk procedures and diagnosis

© 2016 HST All Rights Reserved | Confidential | page 7

Client Profile & Situation

• 1200 employees self funded

• 12 months of paid facility claims

• Utilized a BUCAPPO

• No benchmarking or R&C (UCR) language

HST Involvement

• Improved reimbursements using VBP; Medicare

at 140%

• Turnkey solution from pricing databases, plan doc,

prepricing, and consumer app

• Stop-loss rates reduce claims expense andadmin

fees

Case Study

© 2016 HST All Rights Reserved | Confidential | page 8

Employee Experience – I.D. Card

For physicians

A physician network is utilized that has both inand

out-of-network benefits for all physician services

(primary care and specialists).

For inpatient and outpatient claims

For inpatient and outpatient services, you canuse

any facility you choose. VBP is openaccess.

Any procedure that requires use of a medical facility

must be pre-certified at least 7 days prior to service

as indicated on your I.D. Card.

Urgent and emergent care is treated like any other

medical services in that VBP will be applied based

on the plan guidelines.

© 2016 HST All Rights Reserved | Confidential | page 9

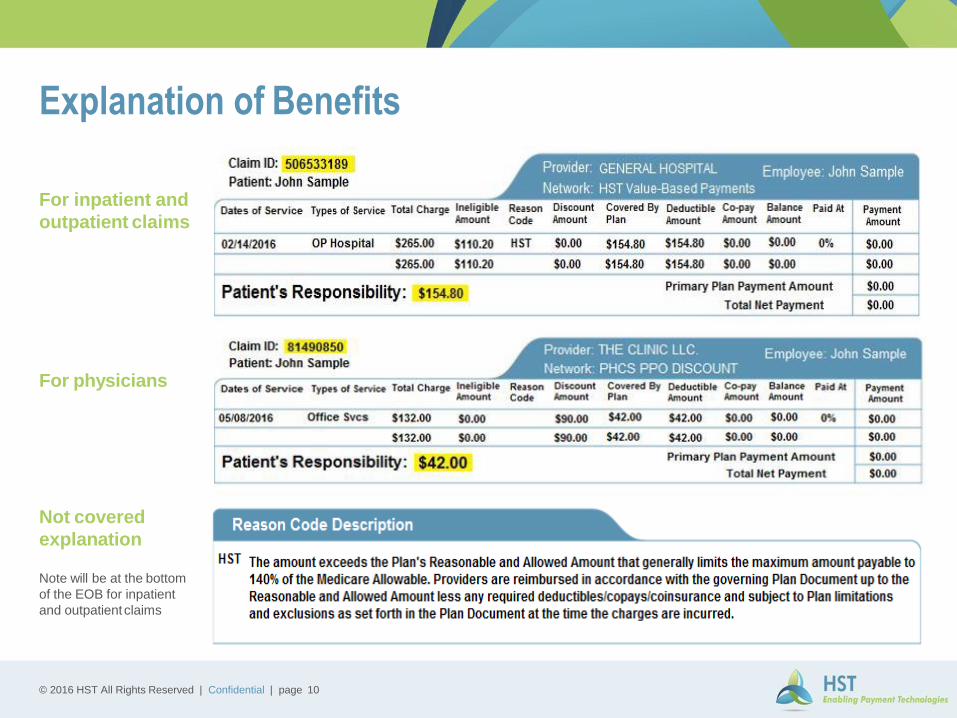

Explanation of Benefits

For inpatient and

outpatient claims

For physicians

Not covered

explanation

Note will be at the bottom

of the EOB for inpatient

and outpatientclaims

© 2016 HST All Rights Reserved | Confidential | page 10

How the VBP Plan Works

*TPA (Third-Party Administrator)

1.Provider calls for pre-

certification

2.Provider is notified of

pre-priced amount for

the service

3.Medical treatment or

services are received

by you or your family

member

4.The provider submits a

bill for services to TPA

for payment

5.TPA remits payment to

the provider based

upon the pre-priced

amount

7.TPA issues an

Explanation of Benefit

(EOB) to you and the

provider

6.You pay deductible and

co-insurance

© 2016 HST All Rights Reserved | Confidential | page 11

Employee Communication Tools

Patient Advocacy Center (PAC)

• Patient advocate to assist in dealing with unexpected

medical costs and verify fair prices on medical

services

HST Connect

• Mobile app offers you 24/7 access to your planinformation, ID Card, eligibility and coverage

Print Campaigns

• Handbook, posters

Member Communication

• Enrollment packet, benefits guide, newsletters and

memorandums

Educational Videos

Sample of open enrollment newsletter

© 2016 HST All Rights Reserved | Confidential | page 12

HST’s Patient Advocacy Center (PAC)

Member

Provider Communications

Inquiries Handled by PAC

Drafts Member Letters

Protects and Guides

Provider

Handles Communications

NegotiatesAgreements

Reviews Plan Language

Explains Reimbursement

Protecting

Members

© 2016 HST All Rights Reserved | Confidential | page 13

Healthcare Pricing Trends

Typical Renewal Inflation

Fully-Insured of 12% vs. Self-Funded of 8% vs. RBP tracking Medicare at 1%.

© 2016 HST All Rights Reserved | Confidential | page 14

Benefits of VBP

Transparency

Increase visibility into healthcare

expenses

Accountability

Gain understanding on

healthcare costs

Sustainability

Maximize your budget with our

sustainable long term value

Predictability

Know what your costs will be,

today and in the future

Value

Bend the cost curve downward

while increasing value

© 2016 HST All Rights Reserved | Confidential | page 15

Why HST?

Fixed fee (PEPM)

versus percentage

of billed charges

Integrate pre-pricing

navigator estimate

at point of

authorization

Balance billing

handled by the

PatientAdvocacy

Center along with

stop loss/MGU

partners

Collaborative approach

versus legalistic and

adversarial

Comprehensive

databases to establish

price to value versus

limited data

Achieves lowest claims

cost by combining

reference pricing, fixed

fees and stop loss

discounts

© 2016 HST All Rights Reserved | Confidential | page 16

Thank You

Revolutionizing Healthcare Through Transparency

Visit Us

Visit our website at

www.hstechnology.com

Contact Us

You can contact us at

800-292-0536

Claim Analysis

To receive a claim analysis,

touch base with us at

© 2016 HST All Rights Reserved | Confidential | page 17

Proprietary and Confidential © 2016 Truveris, Inc. 1

Technology in Pharmacy Management

Truveris Provides Rx Visibility To Key Stakeholders

OUR MISSION

We are on a mission to save

Americans money by

democratizing data &

access across the

prescription drug industry

through technology. We

work with the largest

payers and providers to

develop innovative

solutions that drive

measurable results to our

clients.

1

9

3/8/17 Proprietary and Confidential © 2016 Truveris, Inc.

$375b

2015 2016 2017 2018 2019Source: PWC Health Research Institute: Behind the Numbers 2015 in conjunction with CVS Caremark

2020

$450b

$650bTrend Drivers

• New drugs coming to market faster

• More expensive drugs

• Existing drugs receiving more disease treatment approvals

• Inflation disconnection to typical economicmarket forces

• Aging population and obesity epidemic

Pharmacy Benefits Market Doubling Over Five Years

2

0

3/8/17 Proprietary and Confidential © 2016 Truveris, Inc.

• Once upon a time…

• There was a PrinCesS (PCS)

A PBM Fable

Proprietary and Confidential © 2016 Truveris,

Inc.

6

Why Am I Here?

Proprietary and Confidential © 2016 Truveris,

Inc.

7

• Caveat Emptor

• Market Failure

• Moreover, since asymmetries of information give rise to market

power, and perfect competition is required if markets are to be

efficient, it is perhaps not surprising that markets with information

asymmetries and other information imperfections are far from

efficient.

Joseph Stiglitz, Nobel Prize Lecture, December 8, 2001

2 31Associated Pain Points of Lifecycle Management

Across all lifecycle states, inefficiencies hamper effective business operations. Status quo

processes lack:

• INSIGHT: Granular market intelligence, apples-to-apples financial comparison

• OVERSIGHT: Claim processing errors

• ACCESS: Steps are resource intensive, often exceeding available bandwidth and restricting the ability for

smaller teams to access these critical services

3/8/17 6

Plan

Design

Plan

Vendor

Live Plan

Performance

Cost v. Selection & Monitoring &

Member Impact Evaluation Audit

Proprietary and Confidential © 2016 Truveris, Inc.

Pharmacy Vendor Procurement & Bill Review

3/8/17 7

The Solution: Truveris Platforms Serve All Market Segments

COMPETITIVE QUOTES

• Top pharmacy benefit rates

• Best-in-class legal terms

EASY CONTRACTING

• Software-as-a-Service processes

• No client resources required

OVERSIGHT

• Ongoing bill review

• Financial performance reports Proprietary and Confidential © 2016 Truveris,

Inc.

27

Full RFP | Customizable Process | Vendor Scoring

PBM BIDDING & SELECTION

• Only independent re-pricing adjudication

engine in industry

• View bids in an apples-to-apples

comparison using code based classification

of drugs

• Only platform in industry that shows

blinded leader results to all bidders to drive

competition

• Quantitative and qualitative vendor ranking

within hours of vendor submission

• Average 45 day project completion

Proprietary and Confidential © 2016 Truveris,

Inc.

28

Free PBM Quotes | Competitive Rates | Award in Minutes

PBM BIDDING & SELECTION

• Payers under 3500 lives can benefit from

pre-negotiated rates and scale

• Run pharmacy benefit quotes in under 15

minutes

• View 3-year cost projections

• Simply click to award business

Proprietary and Confidential © 2016 Truveris,

Inc.

29

SaaS | Cloud-hosted | Multi-tenant | Infinitely scalable

PLATFORM CAPABILITIES

• Review Bills Concurrently

• Identify Overcharges

• Maintain Plan Integrity

• Mitigate Fiduciary Liability

• Track Effective Rates

• Enforce Guarantees

• Audit Retrospectively

283/8/17 Proprietary and Confidential © 2016 Truveris, Inc.

Pharmacy Stop Loss

WHO

Self-insured plans with greater than 200 employees or 400 lives

looking for protection against the uncertain costs associated

with providing pharmacy benefits.

WHAT

Truveris has partnered with Swiss Re to offer pharmacy stop

loss that will cap pharmacy spend. This includes specialty

spend and can also be attached to any TruBid or RxChoice

opportunity.

WHY

For fully-insured plans looking to self insure but afraid of

losing the “insurance” aspect, stop loss allows for savings from

self-insuring while maintaining protection. For self-insured

plans concerned about costs, stop loss provides a cap.

Insurance For Self-Insured Plans

293/8/17 Proprietary and Confidential © 2016 Truveris, Inc.

3/8/17 13Proprietary and Confidential © 2016 Truveris, Inc.

Thank You

Risk Management

Presented By |

The Cornerstones of Alternative Risk

Financing & Risk ManagementElliot LePoidevin, Colin Green & Katie Hensley

C&B RISK MANAGEMENT WI TEAM

Elliot LePoidevinSenior Account Executive

Colin GreenSenior Account Executive

Katie HensleyWorker’s Compensation

Specialist

TODAY’S AGENDA

• C&B - Alternative Program Design

• The Traditional Insurance Dilemma

• Alternative Risk Financing Program Design Options

• Safety

• Claims Best Practices

COTTINGHAM & BUTLER – ALTERNATIVE PROGRAM DESIGN

THE INSURANCE DILEMMA

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

2012 2013 2014 2015 2016

Premium

Losses

Many companies would be better off not buying insurance and paying their claims out of pocket, but don’t want to take on the

risk of a bad loss year (ie: 2015).

THE INSURANCE DILEMMA

2011 2012 2013 2014 2015

$19.5

$35.1

$63.4

$55.9 $56.6

Annual Property & Casualty Insurer Profit (Billions)

INSURANCE MARKETPLACE VOLATILITY

Combined Ratio = (Incurred Losses + Operating Expenses) / Earned Premiums

110.1%

115.8%

107.5%

100.1%

98.4%

100.8%

92.6%

95.7%

101.0%

99.3%

100.8%

106.3%

102.4%

96.7% 97.2%96.0%

90%

95%

100%

105%

110%

115%

120%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Property & Casualty Industry Combined Ratio

STANDARD/TRADITIONAL INSURANCE

Acknowledgements:

• Pricing is cyclical and based on the market, not individual results.

• The top performing companies subsidize the worst.

• The insurance company retains profit and investment income

Best in class organizations are doing something different

Traditional Insurance Marketplace

Best in Class

ALTERNATIVE RISK FINANCING PROGRAMS

Alternative Risk Financing Program

Design Options

RISK MANAGEMENT

Basic Acknowledgment

• Most losses can be controlled, but some are inevitable

Basic Approach

• Retain losses that are predictable

• Transfer losses that are not – losses catastrophic in nature

• Find the best solution for managing risk over a period of time

• Find the most effective method in reducing the total cost of risk

MEMBER-OWNED GROUP CAPTIVES

• Simply, an insurance company owned by its’ policyholders created to lower the cost of insurance over the long-term by pooling resources.

• Annual premium consists of funds to cover the operations of the captive and funds to pay losses.

• Losses below the captive retention are paid by the members; large losses over the retention are transferred to an insurance company.

• Unused loss funds are returned to each individual member as dividends.

Loss Funds

Operating Costs

Annual Premium

Potential Dividend

Stop Loss Insurance

MEMBER-OWNED GROUP CAPTIVES

Benefits:

• Return of unused loss funds (aka: profit) plus investment income to the member.

• Greater control of costs while still protecting from catastrophe

• Superior claims and safety (TPA/Consultants vs. the Ins. Company)

Considerations:

• Collateral requirements

• Captive structure and performance (NOT all created equal)

• Current partners and selection process

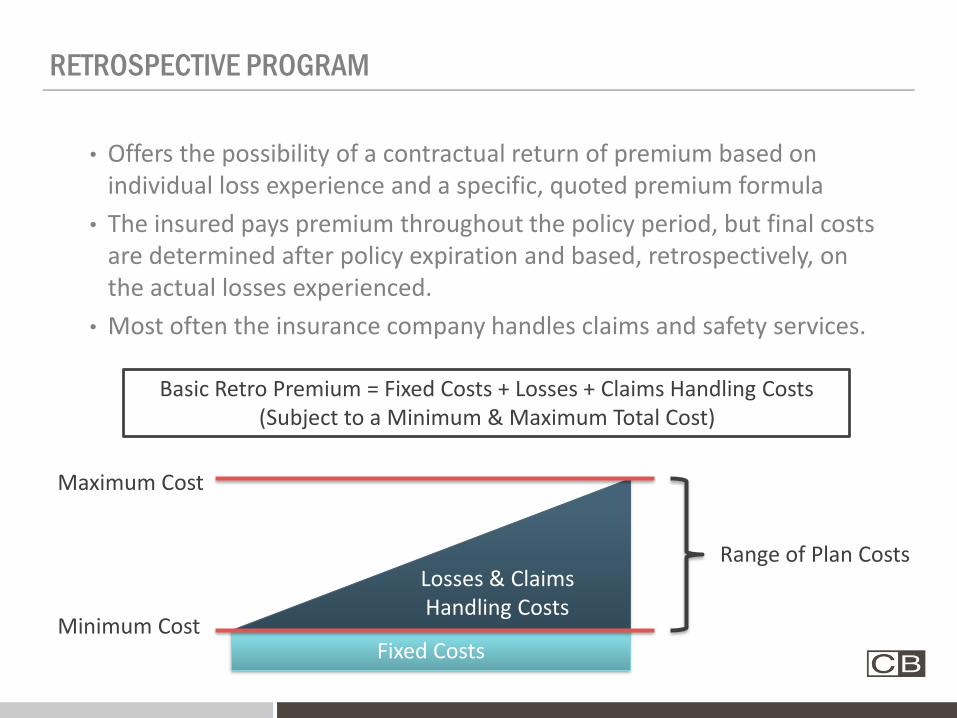

RETROSPECTIVE PROGRAM

• Offers the possibility of a contractual return of premium based on individual loss experience and a specific, quoted premium formula

• The insured pays premium throughout the policy period, but final costs are determined after policy expiration and based, retrospectively, on the actual losses experienced.

• Most often the insurance company handles claims and safety services.

Basic Retro Premium = Fixed Costs + Losses + Claims Handling Costs(Subject to a Minimum & Maximum Total Cost)

Losses & Claims Handling Costs

Fixed Costs

Maximum Cost

Minimum Cost

Range of Plan Costs

RETROSPECTIVE RATING

Benefits:

• Ability to drive down costs relatively quickly

• Alignment between safety and claims practices and cost of risk

• Highly flexible program design (Paid, Incurred, Reduced Pay-In, Lines of Coverage)

Considerations:

• Upside risk can be substantial

• Collateral requirements

• Limited control over claims and safety resources

SELF INSURANCE

• A retention plan in which the insured retains all or a major portion of its own risk.

• The insured contracts with TPA and other administrative partners or, in some cases, handles in-house.

• Typically combined with specific and/or aggregate stop-loss insurance.

Self-Insured Retention

Operating Costs

Stop Loss Insurance

Insured controls claims, safety, compliance and admin.

SELF INSURANCE

Benefits:

• Low fixed/operating costs as minimal risk is being transferred – long-term cost savings maximized.

• High level of control over claims, safety, and administrative components.

• Cash flow benefits

Considerations:

• High volatility in costs

• Administrative requirements

• Compliance with contractual obligations

Insurance Program Design Spectrum

Low Risk High Risk

Risk Appetite/Premium Volatility for each program solution:

Guaranteed Cost

Risk Retained: none

Volatility: low

Cash Flow: low

Security: none

PROS:

No upside risk

Dividend Potential (WC)

Stable cash flow

CONS:

Good losses benefit insurer

Premium affected by mod

Premium up/down based on

losses and market conditions

Group Captive

Risk Retained: moderate

Volatility: moderate

Cash Flow: low

Security: required

PROS:

High dividend potential

Unbundled claims/safety

Interest income on loss funds

Member/Owned benefits

Smoothes insurance cycles

Potential tax advantages

WC/GL/Auto combined

CONS:

Relatively higher fixed costs

Assessment potential

Collateral requirements

Retrospective

Risk Retained: moderate

Volatility: moderate

Cash Flow: low or high

Security: low

PROS:

High return potential

Little or no collateral

Unbundled claims & savings

Dedicated claim adjusters/team

Incurred or Paid Basis

Limited upside exposure

CONS:

Higher aggregate risk

Collateral requirements

Large Deductible

Risk Retained: moderate high

Volatility: high

Cash Flow: low or high

Security: high

PROS:

High return potential

Low fixed costs

Incurred or Paid Basis

Unbundled claims possible

CONS:

Higher collateral requirement

Higher aggregate risk

Collateral can tie to carrier

Self Insurance

Risk Retained: moderate high

Volatility: high

Cash Flow: high

Security: moderate

PROS:

Lowest fixed cost potential

Unbundled claims/safety

Cash flow benefit

No collateral required for

carrier (possible for state)

CONS:

Application for state approval

Upside risk

State by state issue, would

need WC for other states

Assessment Potential

ALTERNATIVE RISK FINANCING

OVERALL CONSIDERATIONS/QUESTIONS

To move to an alternative risk program, you would need to believe:• You can control and prevent the majority of your losses; your good loss

years over time will far outweigh your bad loss years. • You are willing to bet on yourself and assume more risk to receive a greater

reward. • There is a difference in claims handling and safety services and they can

benefit your company when there is buy in from upper management. • You have a long-term view on your business and risk management

To stay in the standard market, you would need to believe:• Your loss experience will get worse over time not better, or your losses are

unpredictable and difficult to control.• Your guaranteed cost premium rates will stay stable and not increase over

time.• You prefer a more conservative approach to handle your insurance that

likely costs more money over time. • You are not in a financial position to accept any ‘upside’ risk

ALTERNATIVE RISK FINANCING PROGRAMS

ALTERNATIVE RISK FINANCING PROGRAMS

Safety & Risk Management

Claims Handling Best

Practices

Four Keys to Effective Safety Program

MANAGEMENT BUY-IN/SUPPORT

GOALS

TRENDING DATA

Major Injury

Minor Injury

Near Misses

Unsafe Behaviors

TRENDING DATA

ACCOUNTABILITY

Main purpose: Establish how the program/culture will be enforced.

ACCOUNTABILITY

ASK YOURSELF

• Are safety and risk management priorities throughout the organization?

• Can all of your employees articulate the company’s safety goals?

• If you could not see the OSHA log or Experience Mod Worksheet, what else would you look for to tell if the organization’s safety program was performing well?

• What processes would be in place and how would you know they were working, other than a lack of accidents?

• How are your company’s leaders, managers, and supervisors held accountable for safety and risk management?

Presented By |

Claims Philosophy

Katie Hensley, AICWorkers’ Compensation Specialist

DIRECT IMPACT-MOD

COMMUNICATION

• Reduces the likelihood of attorney involvement

• Improves morale

• Speeds up recovery

• Reduces claim costs

UNDERSTANDING THE EMPLOYEE

• Morbidities- Weight- Age- Smoker- Pregnant

• Personality- Mental health

• Claims History/Experience- Professional Claimant/Bad experience…

ACCIDENT INVESTIGATION

• Importance of Documenting/Reporting

• Protects everyone

• How you can help the adjuster (photos, witness statement, red flags…)

RETURN TO WORK

Time off Work Chances of Returning to Work

6 months 50%

1 year 25%

2 years 0-2%

TEAMWORK

QUESTIONS

Thank you for attending!