willamette community bank€¦ · willamette community bank notes to financial statements 7 note 1...

TRANSCRIPT

Report of Independent Auditors and Financial Statements for

Willamette Community Bank

December 31, 2016 and 2015

CONTENTS PAGEREPORTOFINDEPENDENTAUDITORS 1–2FINANCIALSTATEMENTS Balancesheets 3 Statementsofincome 4 Statementsofcomprehensiveincome 5 Statementsofchangesinshareholders’equity 5 Statementsofcashflows 6 Notestofinancialstatements 7–32

1

REPORTOFINDEPENDENTAUDITORSTotheBoardofDirectorsandShareholdersofWillametteCommunityBankReportontheFinancialStatementsWe have audited the accompanying financial statements of Willamette Community Bank, whichcomprisethebalancesheetsasofDecember31,2016and2015,andtherelatedstatementsofincome,comprehensive income,changes inshareholders’equity,andcash flowsfor theyearsthenended,andtherelatednotestothefinancialstatements.Management’sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica;thisincludesthe design, implementation, andmaintenance of internal control relevant to the preparation and fairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor’sResponsibilityOur responsibility is to express an opinion on these financial statements based on our audits. Weconductedouraudits inaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica.Thosestandardsrequirethatweplanandperformtheauditstoobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthe financial statements. The procedures selected depend on the auditor’s judgment, including theassessmentof therisksofmaterialmisstatementof the financialstatements,whetherdue to fraudorerror. Inmakingthoseriskassessments, theauditorconsidersinternalcontrolrelevant to theentity’spreparationand fairpresentationof the financial statements inorder todesignauditprocedures thatare appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit alsoincludes evaluating the appropriateness of accounting policies used and the reasonableness ofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinion.

2

REPORTOFINDEPENDENTAUDITORS(continued)OpinionIn our opinion, the financial statements referred to above present fairly, in allmaterial respects, thefinancialpositionofWillametteCommunityBankasofDecember31,2016and2015,andtheresultsofits operations and its cash flows for the years then ended in accordance with accounting principlesgenerallyacceptedintheUnitedStatesofAmerica.Portland,OregonMarch9,2017

3

WILLAMETTECOMMUNITYBANKBALANCESHEETS

2016 2015

ASSETSCashandcashequivalents 10,172,246$ 7,734,111$Investmentsecuritiesavailable‐for‐sale,atfairvalue 6,849,499 11,240,128Investmentsecuritiesheld‐to‐maturity,atamortizedcost 5,312,932 4,501,176Restrictedequitysecurities 218,700 213,300Loans,net 73,487,030 72,864,459Premisesandequipment,net 1,392,164 1,457,414Accruedinterestandotherassets 848,876 871,383

Totalassets 98,281,447$ 98,881,971$

LIABILITIESNon‐interestbearingdemanddeposits 22,320,671$ 21,346,989$Interest‐bearingdemanddeposits 9,396,876 9,239,406Moneymarketandsavingsaccounts 49,541,267 50,829,324Timedeposits 5,855,472 6,881,645

Totaldeposits 87,114,286 88,297,364

Accruedinterestandotherliabilities 97,274 56,262

Totalliabilities 87,211,560 88,353,626

COMMITMENTSANDCONTINGENCIES(Note10and12)

SHAREHOLDERS'EQUITYCommonstock,noparvalue,10,000,000sharesauthorized

1,019,112sharesissuedandoutstandingatDecember31,2016and2015 8,816,839 8,681,680

Retainedearnings 2,275,816 1,852,456Accumulatedothercomprehensiveloss (22,768) (5,791)

Totalshareholders'equity 11,069,887 10,528,345

Totalliabilitiesandshareholders'equity 98,281,447$ 98,881,971$

December31,

4

WILLAMETTECOMMUNITYBANKSTATEMENTSOFINCOME

2016 2015

INTERESTINCOMEInterestandfeesonloans 4,124,161$ 3,915,539$Interestoninvestmentsecurities 310,327 341,654Otherinterestincome 29,916 23,718

Totalinterestincome 4,464,404 4,280,911

INTERESTEXPENSEInterest‐bearingdemand,moneymarket,andsavingsdeposits 154,421 114,581Timeandotherborrowings 31,666 52,373

Totalinterestexpense 186,087 166,954

NETINTERESTINCOME 4,278,317 4,113,957LOANLOSSPROVISION(RECAPTURE) 20,000 (100,000)

Netinterestincomeafterloanlossprovision(recapture) 4,258,317 4,213,957

NON‐INTERESTINCOMEInterchangefeeincome 120,160 126,974Servicechargesondepositaccounts 79,175 76,014Gainsonsalesandearlyredemptionsofsecurities 11,277 1,300Other 47,572 39,636

Totalnon‐interestincome 258,184 243,924

NON‐INTERESTEXPENSESalariesandemployeebenefits 2,014,153 1,946,377Premisesandequipment 574,331 587,023Dataprocessing 402,923 415,490Legalandprofessional 209,030 124,839FDICAssessment 65,683 130,169Advertising,marketingandbusinessdevelopment 60,374 43,627Other 391,488 315,786

Totalnon‐interestexpenses 3,717,982 3,563,311

Incomebeforeincometaxes 798,519 893,270Provisionforincometaxes 240,000 302,800

NETINCOME 558,519$ 590,470$

Basicanddilutedearningspercommonshare 0.55$ 0.58$

YearsEndedDecember31,

5

WILLAMETTECOMMUNITYBANKSTATEMENTSOFCOMPREHENSIVEINCOME

2016 2015

NETINCOME 558,519$ 590,470$

OTHERCOMPREHENSIVEINCOMEUnrealizedholdinggains(losses)duringperiod (14,446) (28,550)Reclassificationadjustmentforamountsincludedinnetincome (11,277) (1,300)

Othercomprehensivelossbeforeincometaxes (25,723) (29,850)Incometaxbenefitrelatedtoitemsofothercomprehensiveloss (8,746) (10,149)

Othercomprehensiveloss,netoftax (16,977) (19,701)

Comprehensiveincome 541,542$ 570,769$

YearsEndedDecember31,

STATEMENTSOFCHANGESINSHAREHOLDERS’EQUITY

AccumulatedOther Total

Numberof Common Retained Comprehensive Shareholders'Shares Stock Earnings Income(Loss) Equity

BalancesatDecember31,2014 998,999 8,681,680$ 1,261,986$ 13,910$ 9,957,576$

Netincome ‐ ‐ 590,470 ‐ 590,470

Othercomprehensiveloss ‐ ‐ ‐ (19,701) (19,701)

BalancesatDecember31,2015 998,999 8,681,680 1,852,456 (5,791) 10,528,345

2%stockdividend 20,113 135,159 (135,159) ‐ ‐

Netincome ‐ ‐ 558,519 ‐ 558,519

Othercomprehensiveloss ‐ ‐ ‐ (16,977) (16,977)

BalancesatDecember31,2016 1,019,112 8,816,839$ 2,275,816$ (22,768)$ 11,069,887$

6

WILLAMETTECOMMUNITYBANKSTATEMENTSOFCASHFLOWS

2016 2015

CASHFLOWSFROMOPERATINGACTIVITIESNetincome 558,519$ 590,470$Adjustmentstoreconcilenetincometonetcashprovided

byoperatingactivitiesDepreciationandamortization 135,938 142,403Loanlossprovision(recapture) 20,000 (100,000)Netamortizationofpremiums/discountsoninvestmentsecurities 87,940 176,078Gainsonsalesandearlyredemptionsofsecurities (11,277) (1,300)Impairmentofotherrealestateowned ‐ 4,203Lossondispositionofequipment 554 982Deferredincometaxes(decrease)increase (2,381) 78,182Changesincertainassetsandliabilities

Accruedinterestandotherassets 38,133 (52,561)Accruedinterestandotherliabilities 41,012 (59,206)

Netcashfromoperatingactivities 868,438 779,251

CASHFLOWSFROMINVESTINGACTIVITIESPurchasesofavailable‐for‐salesecurities (2,505,735) ‐Proceedsfromsales,maturities,calls,andprincipalpayments

receivedonavailable‐for‐salesecurities 6,815,362 6,282,843Purchasesofheld‐to‐maturitysecurities (833,140) (1,527,621)PurchaseofFederalHomeLoanBankstock (5,400) (57,700)Netincreaseinloans (642,571) (5,382,331)Proceedsfromsaleofotherrealestateowned ‐ 6,797Purchasesofcomputersoftware (4,499) (6,977)Purchasesofpremisesandequipment (71,242) (44,045)

Netcashfrominvestingactivities 2,752,775 (729,034)

CASHFLOWSFROMFINANCINGACTIVITIESNet(decrease)increaseindeposits (1,183,078) 4,029,970

Netcashfromfinancingactivities (1,183,078) 4,029,970

Netdecreaseincashandcashequivalents 2,438,135 4,080,187Cashandcashequivalentsatbeginningofyear 7,734,111 3,653,924

Cashandcashequivalentsatendofyear 10,172,246$ 7,734,111$

SUPPLEMENTALDISCLOSUREOFCASHFLOWINFORMATIONCashpaidforinterest 184,433$ 175,043$

Cashpaidforincometaxes 210,000$ 228,628$

SUPPLEMENTALDISCLOSUREOFNONCASHINVESTINGANDFINANCINGACTIVITIES

Changesinfairvalueofavailable‐for‐saleinvestmentsecurities, (16,977)$ (19,701)$

netoftax

Issuanceofstockdividend 135,159$ ‐$

YearsEndedDecember31,

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

7

Note1–OrganizationandSummaryofSignificantAccountingPoliciesOrganization–WillametteCommunityBank (theBank) isa state‐chartered,FDIC‐insured institutionheadquarteredinAlbany,Oregon,withbranchesinLebanonandAlbany,Oregonandaloanproductionoffice in Salem, Oregon. The Bank offers a full range of traditional banking products and services,primarily to business, professional and consumer customers located in Linn and Benton counties ofOregon. The Bank is subject to the regulations of certain federal and state agencies and undergoesperiodicexaminationbythoseregulatoryauthorities.The Bank declared a 2% stock dividend during 2016. All per share amounts and calculations in theaccompanyingfinancialstatementshavebeenrestatedtoreflecttheeffectsofthestockdividend.Method of accounting and use of estimates – The financial statements have been prepared inaccordance with generally accepted accounting principles and reporting practices applicable to thebankingindustry.Inpreparingthefinancialstatements,managementisrequiredtomakeestimatesandassumptionsthataffectthereportedamountsofassetsandliabilitiesasofthedateofthebalancesheetandrevenuesandexpensesduringthereportingperiod.Actualresultscoulddifferfromthoseestimates.The most significant estimates or assumptions made by management relate to the adequacy of theallowance for loan losses, the fair valueof available‐for‐sale investment securities andother financialinstruments,andtheusefullivesandmethodsofdepreciatingpremisesandequipment.Cashandcashequivalents–Forpurposesofreportingcashflows,cashandcashequivalentsincludecash and due from banks, interest‐bearing deposits at other financial institutions with originalmaturitiesof90daysorlessandFederalFundssoldovernight.Fromtimetotime,theBankholdscashdeposits at other financial institutions in excess of FDIC insured limits. However, as the Bank placesthesedepositswithlarge,well‐capitalizedfinancialinstitutions,managementbelievestheriskoflosstobe minimal. The Bank processes transactions through correspondent accounts with Pacific CoastBankers’Bank(PCBB),UnitedBankers’Bank(UBB),andThe IndependentBankers’Bank(TIB).PCBBrequires that theBankmaintain a reserve in the formofdeposit balances,whichwere$245,000and$250,000asofDecember31,2016and2015,respectively.UBBrequirestheBankmaintainanominalreserve account balance. TIB requires that the Bankmaintain a deposit balance reserve, which was$100,000asofDecember31,2016.Investment securities – The Bank is required to specifically identify its investment securities as“available‐for‐sale,”“held‐to‐maturity,”or“tradingaccounts.”Debtsecuritiesthatmanagementhasthepositiveintentandabilitytoholdtomaturityareclassifiedas“held‐to‐maturity,”andsuchsecuritiesarereportedatamortizedcost.Securitiesareclassifiedas“available‐for‐sale”iftheinstrumentmaybesoldinresponsetosuchfactorsas:(1)changesinmarketinterestratesandrelatedchangesinprepaymentrisk,(2)needsfor liquidity,(3)changes intheavailabilityofandtheyieldonalternative instruments,and(4)changesinfundingsourcesandterms.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

8

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Gains or losses on the sale of available‐for‐sale securities are determined using the specific‐identificationmethod.Unrealizedholdinggainsandlosses,netoftax,onavailable‐for‐salesecuritiesarecarriedasaccumulatedothercomprehensiveincomeorlosswithinshareholders’equityuntilrealized.Fairvaluesfortheseinvestmentsecuritiesaregenerallybasedonquotedmarketpricesforthesameorsimilarinstruments.Declinesinthefairvalueofindividualavailable‐for‐salesecuritiesbelowtheircostthatareother‐than‐temporaryresultinwrite‐downsoftheindividualsecuritiestotheirfairvalue.Suchrelatedwrite‐downswouldbeincludedinearningsasother‐than‐temporaryimpairmentlosses.Premiumsanddiscountsarerecognizedininterestincomeusingtheeffectiveinterestmethodovertheperiodtomaturity.Management reviews investment securities on an ongoing basis for the presence of other‐than‐temporary impairment (OTTI) or permanent impairment, taking into consideration current marketconditions;fairvalueinrelationshiptocost;extentandnatureofthechangeinfairvalue;issuerratingchangesandtrends;whethermanagementintendstosellasecurityorifitislikelythattheBankwillberequiredtosellthesecuritybeforerecoveryoftheamortizedcostbasisoftheinvestment,whichmaybematurity;andotherfactors.Fordebtsecurities,ifmanagementintendstosellthesecurityoritislikelythattheBankwillberequiredtosellthesecuritybeforerecoveringitscostbasis,theentireimpairmentlosswouldberecognizedinearningsasanOTTI.Ifmanagementdoesnotintendtosellthesecurityandit isnot likely that theBankwillbe required to sell the security,butmanagementdoesnotexpect torecovertheentirecarryingvalueofthesecurity,onlytheportionofthe impairment lossrepresentingcreditlosseswouldberecognizedinearnings.The credit lossona security ismeasuredas thedifferencebetween theamortized costbasis and thepresent value of the cash flows expected to be collected. Projected cash flows are discounted by theoriginalor currenteffective interest ratedependingon thenatureof the securitybeingmeasured forpotential OTTI. The remaining impairment related to all other factors, representing the differencebetweenthepresentvalueofthecashflowsexpectedtobecollectedandfairvalue, isrecognizedasachargetoothercomprehensiveincomeorloss.Restricted equity securities – The Bank’s investment in Federal Home Loan Bank of Des Moines(FHLB) stock is a restricted investment carried at par value, which approximates its fair value. As amemberoftheFHLBsystem,theBankisrequiredtomaintainaminimumlevelofinvestmentinFHLBstock,basedonspecificpercentagesofitsassets.TheBankmayrequestredemptionatparvalueofanystockinexcessoftheamounttheBankisrequiredtohold.StockredemptionsareatthediscretionoftheFHLB.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

9

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)StockintheFHLBisclassifiedasrestrictedstockandisevaluatedforimpairmentateachreportingdate.The determination of whether the investment is impaired is based on the Bank’s assessment of theultimate recoverability of par value rather than by recognizing temporary declines in value. Thedeterminationofwhetheradeclineaffectstheultimaterecoverabilityisinfluencedbycriteria,suchas(1)thesignificanceofthedeclineinthenetassetsoftheFHLBascomparedtothecapitalstockamountfortheFHLBandthelengthoftimethissituationhaspersisted,(2)commitmentsbytheFHLBtomakepayments required by law or regulation and the level of such payments in relation to the operatingperformanceoftheFHLB,(3)the impactofthe legislativeandregulatorychangesoninstitutionsand,accordingly,onthecustomerbaseoftheFHLB,and(4)theliquiditypositionoftheFHLB.TheBankhasconcludedthatitsFHLBstockinvestmentwasnotimpairedasofDecember31,2016and2015.The Bank’s investment in PCBB stock is a restricted investment carried at par value, whichapproximates its fair value. PCBB operates under a special purpose charter to provide wholesalecorrespondentbankingservicestodepositoryinstitutions.Bystatute,100%ofPCBB’soutstandingstockisheldbydepositoryinstitutionsthatutilizeitscorrespondentbankingservices.StockredemptionsaremadeatthediscretionofthePCBB.Loans,net–Loansarestatedattheamountofunpaidprincipal,reducedbyanallowanceforloanlossesandunearnedloanfees.Interestonloansiscalculatedbythesimple‐interestmethodondailybalancesof the principal amount outstanding. Loan origination fees and certain direct origination costs arecapitalizedandrecognizedasanadjustmenttoyieldoverthecontractuallifeoftherelatedloan.Theallowanceforloanlossesisestablishedthroughaprovisionforloanlosseschargedasanexpensetothe statement of income. Loans are charged against the allowance for loan losseswhenmanagementbelieves that the collectability of principal is unlikely. The allowance is an amount thatmanagementbelieveswill be adequate to absorb probable losses on existing loans thatmaybecomeuncollectible,basedonprior lossexperienceandevaluationsof thecollectabilityof loans.Theevaluationstake intoconsiderationsuch factorsaschanges in thenatureandvolumeof the loanportfolio,overallportfolioquality, review of specific problem loans, and current economic conditions that may affect theborrower’sability topay.Various regulatoryagencies, as a routinepartof theirexaminationprocess,will periodically review theBank’s allowance for loan losses. Such agenciesmay require theBank torecognizeadditions to theallowancebasedon their judgmentof informationavailable to themat thetimeofexaminations.Aloanisconsideredtobeimpairedwhen,basedoncurrentinformationandevents,itisprobablethatthe Bank will be unable to collect all amounts due (both interest and principal) according to thecontractual terms of the loan agreement. Specific loans evaluated for impairment are adjusted to thelower of cost or fair value. As a practical expedient, fair value may be measured based on a loan’sobservablemarketpriceorthefairvalueoftheunderlyingcollateralsecuringtheloan.Collateralmaybereal estate or business assets, including equipment. The value of collateral is determined based onindependent appraisals. Accrual of interest is discontinued on impaired loans when managementbelieves,afterconsideringeconomicandbusinessconditions,collectionefforts,andcollateralposition,thattheborrower’sfinancialconditionissuchthatcollectionofinterestisdoubtful.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

10

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Whentheaccrualofinterestisdiscontinued,allunpaidaccruedinterestisreversed.Interestincomeissubsequentlyrecognized,andtheaccrualof interest isreinstated,onlyafterscheduledcashpaymentsarereceivedandthecollectionofprincipalinfullisassured.A troubleddebt restructuring isa formal reorganizationofa loanwhereby theBank, foreconomicorlegal reasons related to the borrower’s financial difficulties, grants a concession to the borrower.Concessionsmaybegrantedinvariousforms,includingreductioninthestatedinterestrate,reductionintheloanbalanceoraccruedinterest,andextensionofthematuritydate.Troubleddebtrestructuringsare evaluated at the timeof restructure for impairment, and, if impaired, are subjected to theBank’simpairedloanaccountingpolicy.Premisesandequipment,net– Leasehold improvements, furniture and equipment are recorded atcost, lessaccumulateddepreciationandamortization.Depreciationiscomputedusingthestraight‐linemethod over the expected useful lives of the assets, ranging from two to ten years. Leaseholdimprovementsareamortizedusingthestraight‐linemethodoverthetermsoftherelatedleasesortheestimated lives of the improvements,whichever is shorter. The costs ofmaintenance and repairs areexpensedastheyareincurred,whilemajorexpendituresforleaseholdimprovementsandbettermentsarecapitalized.Other real estate owned – Other real estate owned, which represents property acquired throughforeclosure or deeds in lieu of foreclosure, is carried at the lower of cost or estimated net realizablevalue.Anyexcessoftheloanbalanceovertheestimatedfairvalueofthepropertyatthetimeoftransfer,lessestimateddispositioncosts,ischargedtotheallowanceforloanlossesandanyexcessestimatedfairvalueovertheloan’scarryingvalueisrecognizedfirstasarecoverytotheallowanceforloanlosses,totheextentthatamountshavebeencharged‐offforthatloan.Then,anyfairvalueinexcessoftheloan’scarrying value is recognized as a reduction in noninterest expense. Subsequent write‐downs to fairvalue,ifany,oranydispositiongainsorlossesareincludedinnoninterestexpense.Incometaxes–Incometaxesareaccountedforusinganassetandliabilityapproachthatrequirestherecognitionofdeferredtaxassetsandliabilitiesfortheexpectedfuturetaxconsequencesoftemporarydifferences between the financial statement and tax basis of assets and liabilities at the applicableenactedtaxrates.Avaluationallowanceisprovidedwhenitismorelikelythannotthatsomeportionorallofthedeferredtaxassetswillnotberealized.TheBankevaluatestherealizabilityofitsdeferredtaxassetsbyassessingtheneedforavaluationallowanceandbyadjustingtheamountofsuchallowance,ifnecessary.TheBankrecognizesthetaxbenefitfromuncertaintaxpositionsonlyifitismorelikelythannotthatthetaxpositionswillbesustainedonexaminationbythetaxingauthorities,basedonthetechnicalmeritsofthe position. A tax benefit is measured based on the largest benefit that has a greater than 50%likelihood of being realized upon ultimate settlement. The Bank recognizes interest and penaltiesrelatedtoincometaxmattersinincometaxexpense.TheBankdoesnotanticipatethattheamountofunrecognizedtaxbenefitswillsignificantlyincreaseordecreaseinthenext12months.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

11

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)There were no interest and penalties related to income taxes recognized for the years endedDecember31,2016and2015.TheBankfilesU.S.federalandOregonstateincometaxreturns,whicharesubjecttoexaminationbythetaxingauthoritiesforyears2013andlater.Advertising–TheBankexpensesadvertisingandmarketingcostsastheyareincurred.Advertisingandmarketing costs were $60,374 and $43,626 for the years ended December 31, 2016 and 2015,respectively.Earningsper shareof common stock – Basic earnings per share of common stock is computed bydividing net income available to common shareholders by theweighted average number of commonsharesoutstandingduringtheperiod.Dilutedearningspershareofcommonstockiscomputedsimilarlytobasicearningspershareof commonstock,except that thedenominator is increased to include thenumber of additional common shares related to stockwarrants thatwould have been outstanding ifsuchdilutivepotentialcommonshareshadbeenissued,unlesstheyaredeterminedtobeanti‐dilutive.Off‐balancesheetfinancialinstruments–Intheordinarycourseofbusiness,theBankentersintooff‐balancesheet financial instrumentsconsistingofcommitments toextendcredit, commercial lettersofcredit,andstandbylettersofcredit.Thesefinancialinstrumentsarerecordedinthefinancialstatementswhentheyarefundedorrelatedfeesareincurredorreceived.TheBankmaintainsanallowanceforoff‐balance sheet items, established as an accrued liability through charges to noninterest expense. Theallowanceisanamountthatmanagementbelieveswillbeadequatetoabsorbpossiblelossesassociatedwithoff‐balancesheetcreditrisk.Theevaluationstakeintoconsiderationsuchfactorsaschangesinthenatureandvolumeof thecommitmentstoextendcreditandundisbursedbalancesofexisting linesofcreditandlettersofcredit.Fairvalueofassetsandliabilities–Fairvalueisdefinedasthepricethatwouldbereceivedtosellanasset, or paid to transfer a liability, in an orderly transaction between market participants at themeasurementdate.TheBankdeterminesfairvaluebaseduponquotedpriceswhenavailableorthroughtheuseofalternativeapproaches,suchasmatrixormodelpricing,whenmarketquotesarenotreadilyaccessibleoravailable.Thevaluationtechniquesusedarebasedonobservableandunobservableinputs.Observable inputs reflectmarketdataobtained from independentsources,whileunobservable inputsreflecttheBank’smarketassumptions.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

12

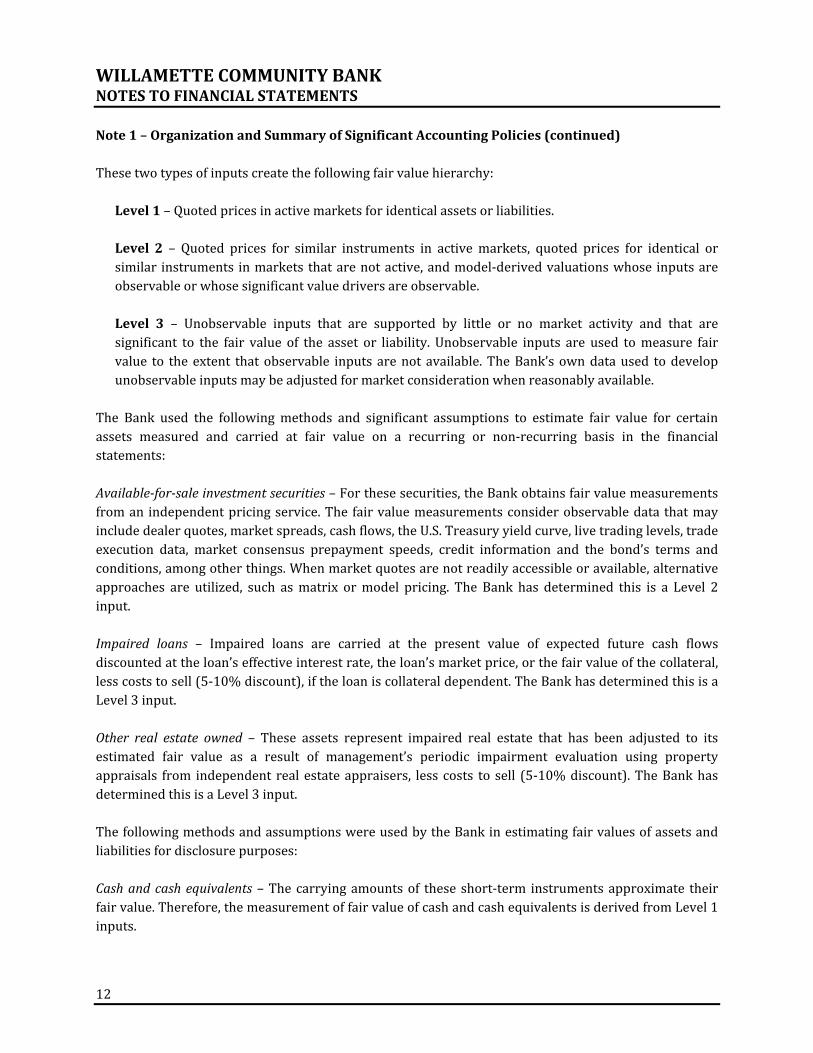

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Thesetwotypesofinputscreatethefollowingfairvaluehierarchy:

Level1–Quotedpricesinactivemarketsforidenticalassetsorliabilities.Level2 – Quoted prices for similar instruments in activemarkets, quoted prices for identical orsimilar instruments inmarkets thatarenotactive,andmodel‐derivedvaluationswhose inputsareobservableorwhosesignificantvaluedriversareobservable.Level 3 – Unobservable inputs that are supported by little or no market activity and that aresignificant to the fair value of the asset or liability. Unobservable inputs are used tomeasure fairvalue to theextent thatobservable inputs arenot available.TheBank’sowndataused todevelopunobservableinputsmaybeadjustedformarketconsiderationwhenreasonablyavailable.

The Bank used the followingmethods and significant assumptions to estimate fair value for certainassets measured and carried at fair value on a recurring or non‐recurring basis in the financialstatements:Available‐for‐saleinvestmentsecurities–Forthesesecurities,theBankobtainsfairvaluemeasurementsfroman independentpricingservice.The fairvaluemeasurementsconsiderobservabledatathatmayincludedealerquotes,marketspreads,cashflows,theU.S.Treasuryyieldcurve,livetradinglevels,tradeexecution data, market consensus prepayment speeds, credit information and the bond’s terms andconditions,amongotherthings.Whenmarketquotesarenotreadilyaccessibleoravailable,alternativeapproaches are utilized, such asmatrix ormodel pricing. The Bank has determined this is a Level 2input.Impaired loans – Impaired loans are carried at the present value of expected future cash flowsdiscountedattheloan’seffectiveinterestrate,theloan’smarketprice,orthefairvalueofthecollateral,lesscoststosell(5‐10%discount),iftheloaniscollateraldependent.TheBankhasdeterminedthisisaLevel3input.Other real estate owned – These assets represent impaired real estate that has been adjusted to itsestimated fair value as a result of management’s periodic impairment evaluation using propertyappraisals from independent realestateappraisers, less costs to sell (5‐10%discount).TheBankhasdeterminedthisisaLevel3input.ThefollowingmethodsandassumptionswereusedbytheBankinestimatingfairvaluesofassetsandliabilitiesfordisclosurepurposes:Cashandcashequivalents–Thecarryingamountsof these short‐term instrumentsapproximate theirfairvalue.Therefore,themeasurementoffairvalueofcashandcashequivalentsisderivedfromLevel1inputs.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

13

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Held‐to‐maturity investmentsecurities–Thefairvaluesofthesesecuritiesarebasedonquotedmarketpricesordealerquotes,ifavailable.Ifaquotedmarketpriceisnotavailable,fairvalueisestimatedusingquotedmarketpricesforsimilarsecurities.Whenmarketquotesarenotreadilyaccessibleoravailable,alternativeapproachesareutilized,suchasmatrixormodelpricing.TheBankhasdeterminedtheseareLevel2inputs.Restrictedequitysecurities–Duetosignificantrestrictionsonthesesecurities,thefairvalueofFederalHomeLoanBank(FHLB)andPacificCoastBankers’Bank(PCBB)stockisconsideredtobeequivalenttothevalueithasifredeemedbytheFHLBorPCBB,respectively.However,thereisnoactivemarketforexchanging these securities to a willing party other than the FHLB or PCBB; as such, the Bank hasdeterminedtheseareLevel2inputs.Loansreceivable–Forvariablerateloansthatrepricefrequentlyandhavenosignificantchangeincreditrisk, fair values are based on carrying values. Fair values for fixed‐rate loans are estimated usingdiscountedcashflowanalyses,usinginterestratescurrentlybeingofferedforloanswithsimilartermsto borrowers of similar credit quality. Fair values for impaired loans are estimated using discountedcashflowanalysesorunderlyingcollateralvalues,whereapplicable.TheBankhasdeterminedtheseareLevel3inputs.Depositliabilities–Thefairvaluesdisclosedfordemanddepositsare,bydefinition,equaltotheamountpayableondemandatthereportingdate(theircarryingamounts),whichisdeterminedusingLevel1inputs. The carrying amounts of variable rate, fixed‐termmoneymarket accounts, and certificates ofdeposit (CDs) approximate their fair values at the reporting date. Fair values for fixed‐rate CDs areestimatedusingadiscountedcashflowcalculationthatappliesinterestratescurrentlybeingofferedoncertificates to a schedule of aggregated expectedmonthlymaturities on time deposits. The Bank hasdeterminedtheseareLevel2inputs.Lines of credit and other borrowings – The fair value of the Bank’s borrowings is estimated using adiscountedcashflowanalysisbasedontheBank’scurrentincrementalborrowingrateforsimilartypesofborrowingarrangements.TheBankhasdeterminedtheseareLevel2inputs.Off‐balance sheet instruments – The Bank’s off‐balance sheet instruments include unfundedcommitmentstoextendcredit,andstandbylettersofcredit.Thefairvalueoftheseinstrumentsisnotconsidered practicable to estimate because of the lack of quoted market prices and the inability toestimate fair value without incurring excessive costs. Given the uncertainty of a commitment beingdrawnupon, it isnotreasonabletoestimatethe fairvalueof thesecommitments; therefore, theBankhasnotmadeanydisclosureonthefairvalueofoff‐balancesheetfinancialinstruments.Reclassifications – Certain reclassifications have been made to the 2015 financial statements toconformwithcurrentyearpresentations.Thesereclassificationshavenoeffectonpreviouslyreportednetincomeorearningspershare.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

14

Note1–OrganizationandSummaryofSignificantAccountingPolicies(continued)Subsequentevents–Subsequenteventsareeventsortransactionsthatoccurafterthebalancesheetdate but before financial statements are issued. The Bank recognizes in the financial statements theeffects of all subsequent events that provide additional evidence about conditions that existed at thedate of the balance sheet, including estimates inherent in the process of preparing the financialstatements.TheBank’sfinancialstatementsdonotrecognizesubsequenteventsthatprovideevidenceaboutconditionsthatdidnotexistatthedateofthebalancesheet,butaroseafterthebalancesheetdateandbeforefinancialstatementsareavailabletobeissued.The Bank has evaluated subsequent events through March 9, 2017, which is the date the financialstatementsbecameavailableforissuance.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

15

Note2–InvestmentSecuritiesThe amortized cost and estimated fair values of available‐for‐sale and held‐to‐maturity investmentsecuritiesatDecember31,2016and2015:

Gross GrossAmortized Unrealized Unrealized Estimated

Cost Gains Losses FairValueAvailable‐for‐saleinvestmentsecurities

U.S.Governmenttreasurynotes 500,000$ ‐$ (156)$ 499,844$U.S.Governmentagencynotes 2,505,415 637 (40,126) 2,465,926U.S.Governmentagencymortgage‐backedsecurities 360,830 ‐ (1,137) 359,693U.S.Government/agencycollateralized

mortgageobligations 3,517,751 15,444 (9,159) 3,524,036

6,883,996$ 16,081$ (50,578)$ 6,849,499$

Held‐to‐maturityinvestmentsecuritiesMunicipalbonds‐generalobligations 3,642,282$ 88,053$ (38,430)$ 3,691,905$Municipalbonds‐revenue 1,670,650 38,060 (515) 1,708,195

5,312,932$ 126,113$ (38,945)$ 5,400,100$

Gross GrossAmortized Unrealized Unrealized Estimated

Cost Gains Losses FairValueAvailable‐for‐saleinvestmentsecurities

U.S.Governmentagencynotes 500,000$ ‐$ (970)$ 499,030$U.S.Governmentagencymortgage‐backedsecurities 912,873 ‐ (6,164) 906,709U.S.Government/agencycollateralized

mortgageobligations 9,836,029 35,268 (36,908) 9,834,389

11,248,902$ 35,268$ (44,042)$ 11,240,128$

Held‐to‐maturityinvestmentsecuritiesMunicipalbonds‐generalobligations 2,831,023$ 142,814$ ‐$ 2,973,837$Municipalbonds‐revenue 1,670,153 108,142 ‐ 1,778,295

4,501,176$ 250,956$ ‐$ 4,752,132$

December31,2016

December31,2015

TheBankhadonegeneralobligationsmunicipalbond,onerevenuemunicipalbond,eightcollateralizedmortgage obligation securities, one treasury note security, four agency note securities, and twomortgage‐backed securities in the following tablewithgrossunrealized lossesatDecember31,2016.Includedinthetotalsabovewasonecollateralizedmortgageobligationsecuritythathadbeeninagrossunrealized loss position for greater than one year. At December 31, 2015, the bank had thirteencollateralized mortgage obligations securities, one agency note security, and four mortgage‐backedsecuritieswithgrossunrealizedlosses.Includedinthetotalsabovewerethreecollateralizedmortgageobligations with gross unrealized loss positions greater than one year. The Bank evaluated theseunrealized losses and determined that the declines in value at December 31, 2016 and 2015 weretemporaryandrelatedtothechangeinmarketinterestratessincethedateoftheirpurchases.TheBankcurrently has the ability to hold these securities until maturity or until market conditions favorablyaffectvalue.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

16

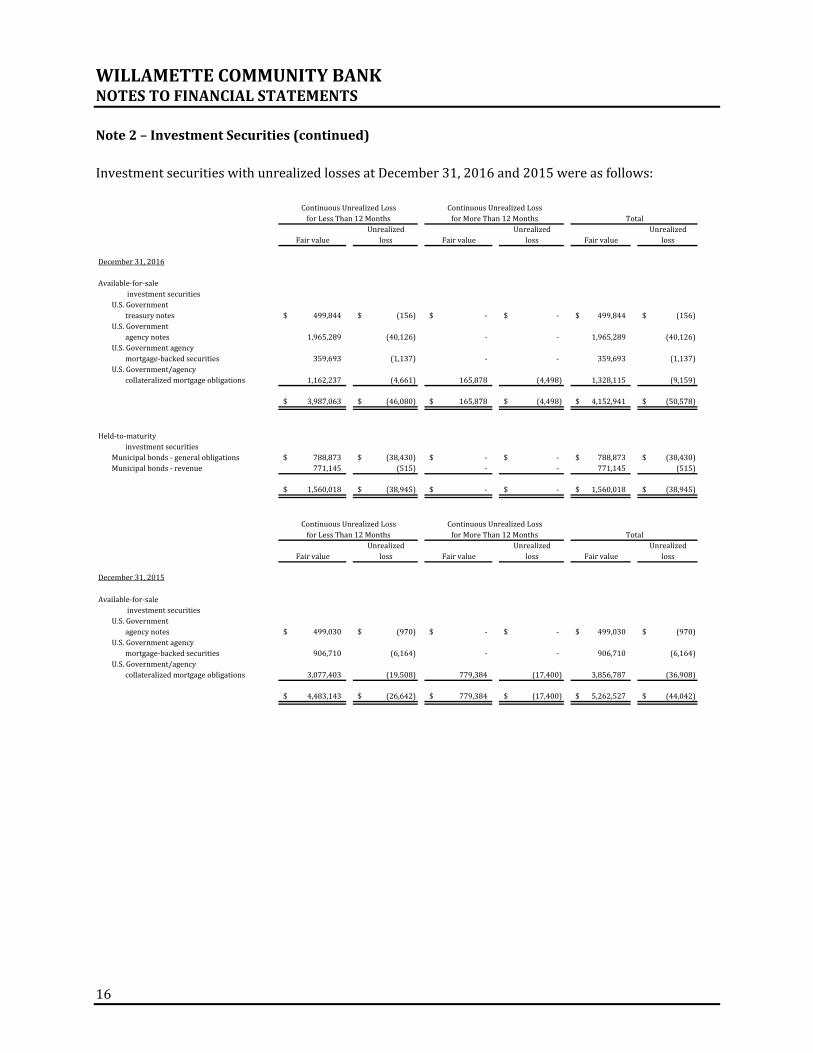

Note2–InvestmentSecurities(continued)InvestmentsecuritieswithunrealizedlossesatDecember31,2016and2015wereasfollows:

Unrealized Unrealized UnrealizedFairvalue loss Fairvalue loss Fairvalue loss

December31,2016

Available‐for‐saleinvestmentsecurities

U.S.Governmenttreasurynotes 499,844$ (156)$ ‐$ ‐$ 499,844$ (156)$

U.S.Governmentagencynotes 1,965,289 (40,126) ‐ ‐ 1,965,289 (40,126)

U.S.Governmentagencymortgage‐backedsecurities 359,693 (1,137) ‐ ‐ 359,693 (1,137)

U.S.Government/agencycollateralizedmortgageobligations 1,162,237 (4,661) 165,878 (4,498) 1,328,115 (9,159)

3,987,063$ (46,080)$ 165,878$ (4,498)$ 4,152,941$ (50,578)$

Held‐to‐maturityinvestmentsecurities

Municipalbonds‐generalobligations 788,873$ (38,430)$ ‐$ ‐$ 788,873$ (38,430)$Municipalbonds‐revenue 771,145 (515) ‐ ‐ 771,145 (515)

1,560,018$ (38,945)$ ‐$ ‐$ 1,560,018$ (38,945)$

Unrealized Unrealized UnrealizedFairvalue loss Fairvalue loss Fairvalue loss

December31,2015

Available‐for‐saleinvestmentsecurities

U.S.Governmentagencynotes 499,030$ (970)$ ‐$ ‐$ 499,030$ (970)$

U.S.Governmentagencymortgage‐backedsecurities 906,710 (6,164) ‐ ‐ 906,710 (6,164)

U.S.Government/agencycollateralizedmortgageobligations 3,077,403 (19,508) 779,384 (17,400) 3,856,787 (36,908)

4,483,143$ (26,642)$ 779,384$ (17,400)$ 5,262,527$ (44,042)$

forLessThan12Months forMoreThan12Months Total

ContinuousUnrealizedLossforLessThan12Months

ContinuousUnrealizedLossforMoreThan12Months Total

ContinuousUnrealizedLoss ContinuousUnrealizedLoss

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

17

Note2–InvestmentSecurities(continued)The amortized cost and estimated fair value of available‐for‐sale and held‐to‐maturity investmentsecurities at December31,2016, by contractualmaturity, are shownbelow. Expectedmaturitiesmaydifferfromcontractualmaturitiesbecauseborrowerscouldhavetherighttocallorprepayobligationswithorwithoutcallorprepaymentpenalties.

Amortized Estimated Amortized EstimatedCost FairValue Cost FairValue

Dueinoneyearorless 500,000$ 499,844$ ‐$ ‐$Dueafteronethroughfiveyears 2,505,415 2,465,926 813,062 823,424Dueafterfivethroughtenyears ‐ ‐ 3,021,682 3,041,057Dueaftertenyears ‐ ‐ 1,478,188 1,535,619Collateralizedmortgageobligationsand

mortgage‐backedsecurities 3,878,581 3,883,729 ‐ ‐

Total 6,883,996$ 6,849,499$ 5,312,932$ 5,400,100$

SecuritiesAvailable‐for‐Sale SecuritiesHeld‐to‐Maturity

In 2016 and 2015 there were gross gains from the sales of securities of $11,277 and $1,300,respectively.At December 31, 2016, available‐for‐sale investment securities of $1,950,250 and held‐to‐maturitysecurities of $4,541,272, were pledged to secure public funds, as permitted or required by law. AtDecember 31, 2015, available‐for‐sale investments securities of $2,508,078 and held‐to‐maturitysecuritiesof$3,730,017werepledgedtosecurepublicfunds,aspermittedorrequiredbylaw.Note3–LoansAsofDecember31,theloanportfolioconsistedofthefollowing:

2016 2015

Realestateloans 53,398,338$ 56,195,083$Commercial 16,947,956 13,008,136Agricultural 3,786,980 3,933,142Consumer 307,961 680,453Otherandoverdrafts 286,074 279,754

74,727,309 74,096,568Lessunearnedloanfees,net (283,504) (302,939)Lessallowanceforloanlosses (956,775) (929,170)

Loans,net 73,487,030$ 72,864,459$

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

18

Note4–AllowanceforLoanLossesThe following table displays the allocation of, and activity within, the allowance for loan losses tosignificantsegmentsoftheloanportfolioasofandfortheyearendedDecember31,2016:

RealEstate Commercial Agricultural Consumer Other Totals

Allowance 737,818$ 138,286$ 36,541$ 13,500$ 3,025$ 929,170$Balance,beginningoftheperiod

Charge‐offs ‐ ‐ ‐ (292) ‐ (292)Recoveries ‐ ‐ ‐ 7,897 ‐ 7,897Provisionforloanlosses 15,000 5,000 ‐ ‐ ‐ 20,000

Balance,endoftheperiod 752,818$ 143,286$ 36,541$ 21,105$ 3,025$ 956,775$

Endingbalanceindividuallyevaluatedforimpairment ‐$ 35,700$ ‐$ 6,100$ ‐$ 41,800$

Endingbalancecollectivelyevaluatedforimpairment 752,818$ 107,586$ 36,541$ 15,005$ 3,025$ 914,975$

LoansEndingbalance 53,398,338$ 16,947,956$ 3,786,980$ 307,961$ 286,074$ 74,727,309$

Endingbalanceindividuallyevaluatedforimpairment 3,048,429$ 237,885$ ‐$ 23,213$ ‐$ 3,309,527$

Endingbalancecollectivelyevaluatedforimpairment 50,349,909$ 16,710,071$ 3,786,980$ 284,748$ 286,074$ 71,417,782$

2016

TransactionsintheallowanceforloanlossesfortheyearendedDecember31,2015wereasfollows:

RealEstate Commercial Agricultural Consumer Other Totals

Allowance 840,818$ 120,681$ 26,541$ 32,584$ 6,025$ 1,026,649$Balance,beginningoftheperiod

Charge‐offs ‐ ‐ ‐ (16,084) ‐ (16,084)Recoveries ‐ 18,605 ‐ ‐ ‐ 18,605Provisionforloanlosses (103,000) (1,000) 10,000 (3,000) (3,000) (100,000)

Balance,endoftheperiod 737,818$ 138,286$ 36,541$ 13,500$ 3,025$ 929,170$

Endingbalanceindividuallyevaluatedforimpairment 600$ 15,800$ ‐$ 7,200$ ‐$ 23,600$

Endingbalancecollectivelyevaluatedforimpairment 737,218$ 122,486$ 36,541$ 6,300$ 3,025$ 905,570$

LoansEndingbalance 56,195,083$ 13,008,136$ 3,933,142$ 680,453$ 279,754$ 74,096,568$

Endingbalanceindividuallyevaluatedforimpairment 1,482,170$ 266,096$ ‐$ 32,331$ ‐$ 1,780,597$

Endingbalancecollectivelyevaluatedforimpairment 54,712,913$ 12,742,040$ 3,933,142$ 648,122$ 279,754$ 72,315,971$

2015

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

19

Note4–AllowanceforLoanLosses(continued)Creditqualityindicators–TheBank’sriskratingmethodologyassignsriskratingsrangingfrom1to8,whereahigherratingrepresentshigherrisk.The8riskratingcategoriescanbegenerallydescribedbythefollowinggroupings:Pass(riskrating1through3)–Theseloansrangefromminimalcreditrisktohigherthanaverage,butstill acceptable, credit risk. Primary repayment sources generate satisfactory debt service coverageundernormalconditions.Cashflowfromrecurringsourcesisexpectedtocontinuetoproduceadequatedebtservicecapacity.Therearemanycategorieswithinthepassdefinition,butnoneoftheloansrisetothelevelofWatch.Watch (risk rating 4) – Loans are graded as Watch when, for various reasons, close monitoring isrequired. This includes loans that have performed satisfactorily, but because of recent events,deteriorating trends, or signs of developing problems require close monitoring. While continuedsatisfactoryperformanceisexpected,thesituation,ifnotmonitored,coulddevelopintoweaknessesthatresultintheloanbeingadverselyriskrated.Special Mention (risk rated 5) – A Special Mention loan has potential weaknesses that deservemanagement’s close attention. If left uncorrected, these potential weaknesses may result indeteriorationoftherepaymentprospectsfortheassetortheBank’screditpositionatsomefuturedate.They contain unfavorable characteristics and are generally undesirable. Loans in this category arecurrentlyprotectedbutarepotentiallyweakandconstituteanundueandunwarrantedcreditrisk,butnot to the point of a Substandard classification. Unlike a Substandard credit, there is a reasonableexpectationthatthesetemporaryissueswillbecorrectedwithinthenormalcourseofbusiness,ratherthanliquidationofassets,andinareasonableperiodoftime.Substandard(riskrated6)–ASubstandardassetisinadequatelyprotectedbythecurrentsoundworthandpayingcapacityof theobligororof thecollateralpledged, ifany.Assetssoclassifiedhaveawell‐defined weakness or weaknesses that jeopardize the orderly repayment of the debt. They arecharacterizedbythedistinctpossibilitythattheBankwillsustainsomelossifthedeficienciesarenotcorrected. Loss potential, while existing in the aggregate amount of substandard assets, does notnecessarilyexistineachindividualassetclassifiedasSubstandard.Thelikelyneedtoliquidateassetstocorrecttheproblem,ratherthanrepaymentfromsuccessfuloperations,isthekeydistinctionbetweenSpecialMentionandSubstandardloans.Doubtful(riskrated7)–LoansclassifiedasDoubtfulhavealltheweaknessesinherentinoneclassifiedasSubstandardwiththeaddedcharacteristicthattheweaknessesmakecollectionorliquidationinfull,onthebasisofcurrentlyexistingfacts,conditionsandvalues,highlyquestionableandimprobable.Thepossibilityof loss isextremelyhigh,butbecauseofcertain importantandreasonablyspecificpendingfactors,whichmaywork towards strengthening of the asset, classification as a Loss (and immediatecharge‐off)isdeferreduntilmoreexactstatusmaybedetermined.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

20

Note4–AllowanceforLoanLosses(continued)Loss (risk rated 8) – These loans are considered uncollectible and of such little value that theircontinuanceasactiveassetsoftheBankisnotwarranted.Thisclassificationdoesnotmeanthattheloanhasnorecoveryorsalvagevalue,butratherthatitisnotpracticalordesirabletodeferwritingitoffasan asset. While Loss is an active grade in the risk rating system, any loan considered to be in thiscategoryistobecharged‐offassoonaspossible.ThefollowingtablesshowcreditqualityindicatorsasofDecember31,2016and2015:

2016 2015 2016 2015 2016 2015

GradePass 51,848,151$ 54,439,044$ 16,742,491$ 12,802,824$ 3,786,980$ 3,933,142$SpecialMention ‐ 123,426 ‐ ‐ ‐ ‐Substandard 1,550,187 1,632,614 205,465 205,312 ‐ ‐Doubtful ‐ ‐ ‐ ‐ ‐ ‐Loss ‐ ‐ ‐ ‐ ‐ ‐

53,398,338$ 56,195,084$ 16,947,956$ 13,008,136$ 3,786,980$ 3,933,142$

2016 2015 2016 2015 2016 2015

GradePass 289,546$ 651,765$ 286,074$ 279,754$ 72,953,242$ 72,106,529$SpecialMention ‐ ‐ ‐ ‐ ‐ 123,426Substandard 18,415 28,688 ‐ ‐ 1,774,067 1,866,614Doubtful ‐ ‐ ‐ ‐ ‐Loss ‐ ‐ ‐ ‐ ‐ ‐

307,961$ 680,453$ 286,074$ 279,754$ 74,727,309$ 74,096,569$

AgricultureRealEstate Commercial

Consumer TotalsOther

ThefollowingtableshowstheageanalysisofpastdueloansasofDecember31,2016and2015:

Over Over9030‐59Days 60‐89Days 90Days Total Total DaysandPastDue PastDue PastDue PastDue Current Loans Accruing

December31,2016Realestate 221,753$ ‐$ 166,723$ 388,476$ 53,009,862$ 53,398,338$ ‐$Commercial ‐ 149,950 55,515 205,465 16,742,491 16,947,956 ‐Agriculture ‐ ‐ ‐ ‐ 3,786,980 3,786,980 ‐Consumer ‐ ‐ ‐ ‐ 307,961 307,961 ‐Otherandoverdrafts ‐ ‐ ‐ ‐ 286,074 286,074 ‐

Total 221,753$ 149,950$ 222,238$ 593,941$ 74,133,368$ 74,727,309$ ‐$

December31,2015Realestate ‐$ ‐$ ‐$ ‐$ 56,195,083$ 56,195,083$ ‐$Commercial ‐ ‐ ‐ ‐ 16,941,278 13,008,136 ‐Agriculture ‐ ‐ ‐ ‐ 3,933,142 3,933,142 ‐Consumer ‐ ‐ ‐ ‐ 680,453 680,453Otherandoverdrafts ‐ ‐ ‐ ‐ 279,754 279,754 ‐

Total ‐$ ‐$ ‐$ ‐$ 78,029,710$ 74,096,568$ ‐$

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

21

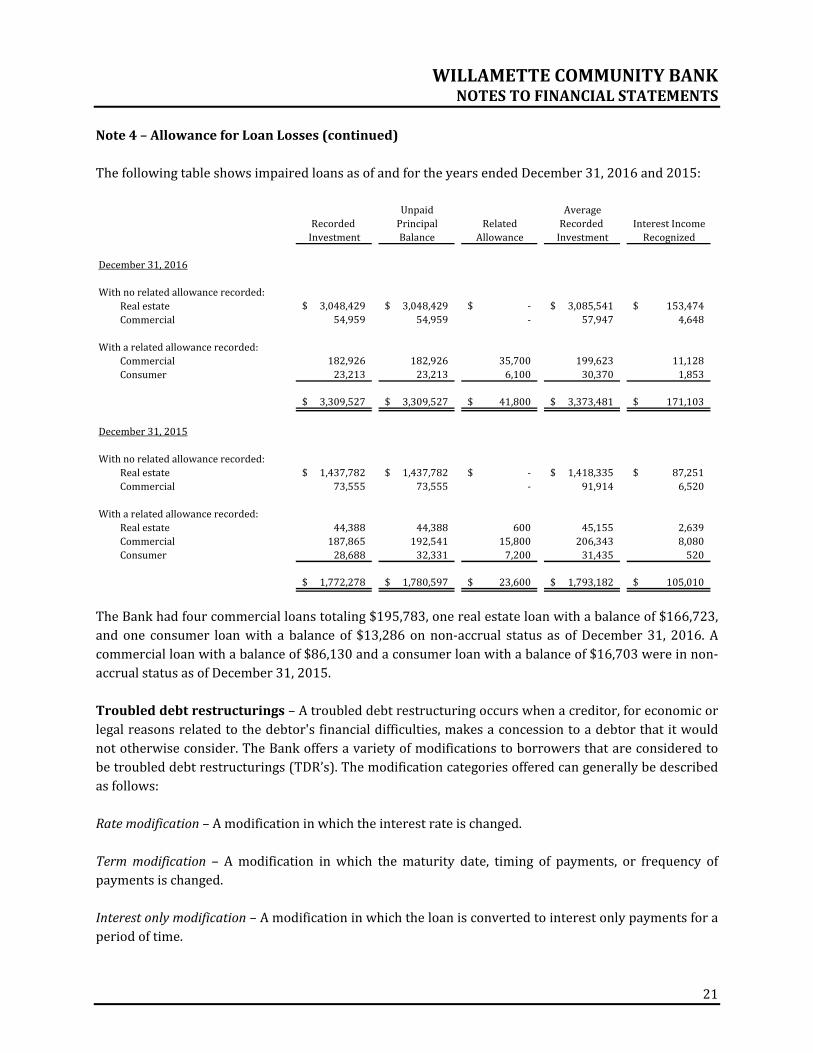

Note4–AllowanceforLoanLosses(continued)ThefollowingtableshowsimpairedloansasofandfortheyearsendedDecember31,2016and2015:

Unpaid AverageRecorded Principal Related Recorded InterestIncomeInvestment Balance Allowance Investment Recognized

December31,2016

Withnorelatedallowancerecorded:Realestate 3,048,429$ 3,048,429$ ‐$ 3,085,541$ 153,474$Commercial 54,959 54,959 ‐ 57,947 4,648

Witharelatedallowancerecorded:Commercial 182,926 182,926 35,700 199,623 11,128Consumer 23,213 23,213 6,100 30,370 1,853

3,309,527$ 3,309,527$ 41,800$ 3,373,481$ 171,103$

December31,2015

Withnorelatedallowancerecorded:Realestate 1,437,782$ 1,437,782$ ‐$ 1,418,335$ 87,251$Commercial 73,555 73,555 ‐ 91,914 6,520

Witharelatedallowancerecorded:Realestate 44,388 44,388 600 45,155 2,639Commercial 187,865 192,541 15,800 206,343 8,080Consumer 28,688 32,331 7,200 31,435 520

1,772,278$ 1,780,597$ 23,600$ 1,793,182$ 105,010$

TheBankhadfourcommercialloanstotaling$195,783,onerealestateloanwithabalanceof$166,723,andone consumer loanwith a balance of $13,286onnon‐accrual status as ofDecember31, 2016. Acommercialloanwithabalanceof$86,130andaconsumerloanwithabalanceof$16,703wereinnon‐accrualstatusasofDecember31,2015.Troubleddebtrestructurings–Atroubleddebtrestructuringoccurswhenacreditor,foreconomicorlegalreasonsrelatedtothedebtor'sfinancialdifficulties,makesaconcessiontoadebtorthatitwouldnototherwiseconsider.TheBankoffersavarietyofmodificationstoborrowersthatareconsideredtobetroubleddebtrestructurings(TDR’s).Themodificationcategoriesofferedcangenerallybedescribedasfollows:Ratemodification–Amodificationinwhichtheinterestrateischanged.Termmodification – Amodification inwhich thematurity date, timing of payments, or frequency ofpaymentsischanged.Interestonlymodification–Amodificationinwhichtheloanisconvertedtointerestonlypaymentsforaperiodoftime.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

22

Note4–AllowanceforLoanLosses(continued)Paymentmodification–Amodificationinwhichthedollaramountofthepaymentischanged,otherthananinterestonlymodificationdescribedabove.Combinationmodification – Any other type of modification, including the use of multiple categoriesabove.AtDecember31,2016and2015,$1,726,036and$1,755,575, respectively, in loanswere classifiedastroubleddebtrestructurings.NewlyrestructuredloansduringtheyearsendedDecember31,2016and2015wereasfollows:

Outstanding OutstandingRecorded RecordedInvestment Investment Impairment

Numberof Before After Concession AmountatContracts Modification Modification Granted December31

December31,2016

Commercial 1 96,463$ 96,463$ Noteterm(s) ‐$

Total 1 96,463$ 96,463$ ‐$

December31,2015

Realestate 2 1,284,959$ 1,357,670$ Noteterm(s) 600$Commercialandagricultural 3 218,359 218,359 Noteterm(s) 15,700

Total 5 1,503,318$ 1,576,029$ 16,300$

During2016,therewerenoloansmodifiedastroubleddebtrestructuringsthathadapaymentdefaultwithin12monthsoftherestructuredate.Thereweretwocommercialloanstotaling$140,267thatwererestructured during 2015, which subsequently had a payment default within 12 months of therestructuredate.Troubleddebtrestructuringonnonaccrualstatustotaled$140,267and$86,130asofDecember 31, 2016 and 2015, respectively. Therewere no available commitments to lend additionalfundsontroubleddebtrestructuringsasofDecember31,2016and2015.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

23

Note5–PremisesandEquipmentAsofDecember31,thecompositionofpremisesandequipmentissummarizedasfollows:

2016 2015

Landandimprovements 336,939$ 336,939$Leaseholdimprovements 435,410 435,410Building 1,097,164 1,097,164Furnitureandequipment 817,252 812,724Constructioninprogress 52,924 ‐

2,739,689 2,682,237Lessaccumulateddepreciationandamortization (1,347,525) (1,224,823)

Premisesandequipment,net 1,392,164$ 1,457,414$

Depreciationandamortizationexpensewas$135,938and$142,403fortheyearsendedDecember31,2016and2015,respectively.Note6–TimeDepositsThe aggregate amount of certificates of deposit $250,000 and over totaled $941,326 and $0, as ofDecember31,2016and2015,respectively.AtDecember31,2016,thescheduledannualmaturitiesofalltimedepositswereasfollows:2017 3,053,502$2018 2,074,4072019 654,6222020 72,941

5,855,472$

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

24

Note7–LinesofCreditandOtherBorrowingsAtDecember31,2016,theBankhadborrowingavailabilityofapproximately$2,750,000underitsCashManagement Advance ("CMA") facility with the Federal Home Loan Bank of Des Moines. The CMAfacility is secured by multifamily, residential‐mortgage loans. In addition, the Bank maintains anunsecured$3,000,000federalfundsfacilitywithitsprimarycorrespondentbank,PacificCoastBankers'Bank. Both facilities were fully available at December 31, 2016. The Bank alsomaintains a discountwindow primary credit facility with the Federal Reserve Bank of San Francisco, which had a fullyavailableborrowinglimitofapproximately$2,600,000asofDecember31,2016.Thediscountwindowfacilityissecuredbypledgedcommercialrealestateloans.TheBankalsomaintainsfederalfundlineswith the IndependentBankersBank and theUnitedBankersBank,with anunsecured, fully availableborrowinglimitof$2,600,000and$5,000,000,respectively.Note8–IncomeTaxesTheprovisionforincometaxesconsistsofthefollowingfortheyearsendedDecember31:

2016 2015Current

Federal 189,947$ 186,718$State 58,314 46,275Lessstatetaxcreditbenefit (5,880) (8,375)

242,381 224,618

DeferredFederal (1,941) 63,782State (440) 14,400

(2,381) 78,182

Provisionforincometaxes 240,000$ 302,800$

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

25

Note8–IncomeTaxes(continued)Deferred income taxes represent the tax effect of differences in timingbetween financial income andtaxable income. As of December 31, 2016 and 2015, net deferred tax benefits are included in thecategoryaccruedinterestreceivableandotherassets intheaccompanyingbalancesheetsandincludethefollowingcomponents:

2016 2015

Deferredtaxassets:Allowanceforloanlosses 325,050$ 317,570$Statetaxcredits 21,841 31,932Marketadjustmentoninvestmentsecurities

available‐for‐sale 13,172 2,983Otherreserves 38 17,627

360,101 370,112Deferredtaxliabilities:

Accruedinterestreceivable (141,842) (153,839)Prepaidexpenses (61,230) (55,877)Booktaxdepreciationdifferences (6,804) (900)

(209,876) (210,616)

Netdeferredtaxasset 150,225$ 159,496$

Management believes, based upon the Bank’s historical performance, the deferred tax assets will berealizedinthenormalcourseofoperations,andhasdeterminedthatnovaluationallowanceisdeemednecessaryasofDecember31,2016or2015.The following summarizes the differences between the provision for income taxes for financialstatementpurposesand the federal statutory rateof34.00% for theyears endedDecember31,2016and2015:

Federaltaxatstatutoryrates 271,495$ 34.00% 303,712$ 34.00%Stateincometaxes,netoffederaleffect 34,783 4.36% 38,911 4.36%Taxexemptincome (57,662) ‐7.22% (37,067) ‐4.15%Other (8,616) ‐1.08% (2,756) ‐0.31%

240,000$ 30.06% 302,800$ 33.90%

2016 2015

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

26

Note9–TransactionswithRelatedPartiesCertaindirectors,executiveofficers,andprincipalshareholdersarecustomersofandhavehadbankingtransactions with the Bank in the ordinary course of business, and the Bank expects to have suchtransactionsinthefuture.Managementbelievesloansandcommitmentstoloanfundsincludedinsuchtransactionsaremadeincompliancewithapplicablelawsonsubstantiallyequivalentterms(includinginterest rates and collateral) as those prevailing at the time for comparable transactions with otherpersonsand,intheopinionofthemanagementoftheBank,donotinvolvemorethanthenormalriskofcollectionorpresentanyotherunfavorablefeatures.AtDecember31,2016and2015,loansoutstandingtodirectorsandtheiraffiliateswereasfollows:

2016 2015

Beginningbalance 2,081,764$ 2,201,831$Additionsorrenewals ‐ ‐Removedfromrelatedpartystatus (1,690,473) ‐Repayments (30,971) (120,067)

Endingbalance 360,320$ 2,081,764$

At December 31, 2016, there were no unused commitments to extend credit to directors and theiraffiliates.Related‐party deposits held by the Bank at December 31, 2016 and 2015 were $3,760,894 and$1,409,097,respectively.Note10–FinancialInstrumentswithOff‐BalanceSheetRiskIn thenormalcourseofbusiness, inorder tomeet the financingneedsof itscustomers, theBank isaparty to financial instruments with off‐balance sheet risk. These financial instruments includecommitmentstoextendcreditandtheissuanceofstandbylettersofcredit.Theseinstrumentsinvolve,tovaryingdegrees,elementsofcreditandinterest‐raterisk inexcessoftheamountrecognizedinthebalancesheets.TheBank’sexposuretocreditlossintheeventofnonperformancebytheotherpartytothe financial instrument for commitments to extend credit and standby letters of credit written isrepresented by the notional amount of those instruments. The Bank uses the same credit policies inmakingcommitmentsandconditionalobligationsasitdoesforon‐balancesheetinstruments.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

27

Note10–FinancialInstrumentswithOff‐BalanceSheetRisk(continued)A summaryof thenotionalamountsof theBank’s financial instrumentswithoff‐balance sheet riskatDecember31,2016and2015,areasfollows:

2016 2015

Commitmentstoextendcreditbytype:Realestate 6,943,588$ 5,847,300$Commercial 12,652,653 8,231,729Agricultural 3,484,642 3,126,803Consumer 147,433 158,345Other 1,200,839 1,226,015Standbyletterofcredit 17,000 17,000

Totalcommitmentstoextendcredit 24,446,155$ 18,607,192$

Theundisbursedbalanceofexistinglinesofcreditrepresentsagreementstolendtocustomers,aslongasthereisnoviolationofanyconditionestablishedinthecontract.Commitmentsgenerallyhavefixedexpiration dates or other termination clauses andmay require payment of a fee. Sincemany of thecommitmentsareexpectedtoexpirewithoutbeingdrawnupon,thetotalcommitmentamountsdonotnecessarilyrepresentfuturecashrequirements.Theamountofcollateralobtained,ifdeemednecessaryby the Bank upon extension of credit, is based on management’s credit evaluation of the customer.Collateral held varies butmay include cash, accounts receivable, inventory, property and equipment,securitiesandrealestate.Standby letters of credit written are conditional commitments issued by the Bank to guarantee theperformance of a customer to a third party. The credit risk involved in issuing letters of credit isessentially the same as that involved in extending loan facilities to customers. The Bank holds cash,accounts receivable, inventories, equipment, securities, and real estate as collateral supporting thosecommitmentsforwhichcollateralisdeemednecessary.The Bank maintains a reserve for off‐balance‐sheet credit exposure representing management’srecognitionoftheassumedrisksofextendingcredit.Thereserveforoff‐balancesheetcreditexposuretotaled $100 and $500 at December 31,2016 and 2015, respectively, and is included with accruedinterestandotherliabilitiesintheaccompanyingstatementsoffinancialcondition.Note11–ConcentrationsofCreditRiskAmajorityoftheBank’sloansandcommitmentstolendhavebeengrantedtocustomersintheBank’smarketarea.Thedistributionofcommitmentstoextendcreditapproximatesthedistributionof loansoutstanding.ThemajorityofsuchcustomersarealsodepositorsoftheBank.ConcentrationsofcreditbytypeofloanaresetforthinNote3.TheBank’sloanpoliciesdonotallowtheextensionofcredittoanysingleborrowerinexcessof25%oftheBank’scapital(15%forotherthanrealestatesecuredloans).

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

28

Note12–CommitmentsandContingenciesLeasecommitments–AsofDecember31,2016,theBankleaseditsofficespaceinLebanon,Oregon,underanoperating leaseagreementwhichexpiresonMarch20,2018,andincludesa fixedescalationclause. During 2016, the Bank entered into a sub‐lease for office space in Salem, Oregon, under anoperatingagreementwhichexpiresMarch1,2028.Approximatefutureminimumpaymentsundertheseleaseagreementsareasfollows:

2017 118,892$2018 95,2652019 87,6542020 89,8452021 92,091Thereafter 513,600

997,347$

YearsendingDecember31,

Rent expense, including common area maintenance, was $71,030 and $68,211 for the years endedDecember31,2016and2015,respectively.Legalcontingencies–TheBankmaybecomeadefendantincertainclaimsandlegalactionsarisingintheordinary courseof business. In theopinionofmanagement, after consultationwith legal counsel,there are no matters presently known that are expected to have a material adverse effect on thefinancialconditionoftheBank.Note13–EmployeeBenefitPlanThe Bank has adopted a 401(k) savings investment plan which allows employees to defer certainamountsofcompensationforincometaxpurposesundersection401(k)oftheInternalRevenueCode.Essentially,allemployeesovertheageof18areeligibletoparticipateintheplan.Employeesmayelecttodeferandcontributeuptothestatutorylimits.TheircontributionsandthoseoftheBank,whicharediscretionary,areinvestedinemployee‐designatedfunds.TheBank’smatchingcontributionstotheplanwere$54,899and$55,142 for theyears endedDecember31,2016and2015, respectively, andwererecordedasemployeebenefitsexpense.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

29

Note14–StockWarrantsAspartoftheBank'sinitialstockoffering,commonstockwarrantswereissuedtoeachpurchaseroftheBank'scommonstockatarateofonewarrantforeveryfivesharespurchased.Additionally,seedcapitalinvestors receivedwarrants at a rateof onewarrant for every sharepurchased to the extent of seedcapitalinvested.Thewarrantsentitledholderstopurchaseoneadditionalshareofcommonstockatastock‐dividendadjustedpriceof$9.52untilexpirationonMay5,2013.InSeptember2011,theBank'sBoardofDirectorsapprovedanextensionoftheexpirationdatetoMay5,2016.InApril2016,theBoardofDirectorsapprovedanotherextensionof theexpirationdate toMay5,2019.Warrantsoutstandingtotaled103,852and101,816atDecember31,2016and2015,respectively.Note15–BasicandDilutedEarningsperCommonShareThenumeratoranddenominatorusedincomputingbasicanddilutedearningspercommonsharefortheyearsendedDecember31,2016and2015wereasfollows:

NetIncome Shares Per‐share(numerator) (denominator) amount

2016558,519$ 1,019,112 0.55$

NetIncome Shares Per‐share(numerator) (denominator) amount

2015590,470$ 1,019,112 0.58$

Basicanddilutedearningspercommonshare

Basicanddilutedearningspercommonshare

Because the impactonearningsper share from theoutstandingwarrantswasdetermined tobeanti‐dilutive,basicanddilutedearningspersharewereequivalent.Note16–RegulatoryMattersThe Bank is subject to various regulatory capital requirements administered by federal and statebanking agencies. Failure tomeetminimum capital requirements can trigger certainmandatory andpossiblyadditionaldiscretionaryactionsbyregulatorsthat,ifundertaken,couldhaveadirectmaterialeffect on the Bank’s financial statements. Under capital adequacy guidelines and the regulatoryframework for prompt corrective action, banks must meet specific capital guidelines that involvequantitativemeasuresoftheBank’sassets, liabilities,andcertainoff‐balancesheetitemsascalculatedunderregulatoryaccountingpractices.Capitalamountsandclassificationsarealsosubjecttoqualitativejudgmentsbytheregulatorsaboutcomponents,riskweightings,andotherfactors.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

30

Note16–RegulatoryMatters(continued)Quantitative measures, established by regulation to ensure capital adequacy, require the Bank tomaintain minimum amounts and ratios (set forth in the table below) of total Tier 1 capital to risk‐weightedassetsandofTier1capitaltoaverageassets(asdefinedintheregulations).The Bank’s and the Company’s capital amounts and ratios are substantially equivalent and as ofDecember31,2016and2015,areasfollows:

Amount Ratio Amount Ratio Amount Ratio(dollarsinthousands)

December31,2016:

Totalrisk‐basedcapitalratio‐Totalcapital(torisk‐weightedassets) 12,040$ 13.1% 7,358$ 8.0% 9,198$ 10.0%

Tier1risk‐basedcapitalratio‐Tier1capital(torisk‐weightedassets) 11,083 12.0% 5,519 6.0% 7,358 8.0%

Commonequitytier1torisk‐weightedassets 11,083 12.0% 4,139 4.5% 5,979 6.5%Leverageratio‐

Tier1capital(toaverageassets) 11,083 11.5% 3,864 4.0% 4,830 5.0%

December31,2015:

Totalrisk‐basedcapitalratio‐Totalcapital(torisk‐weightedassets) 11,458 13.5% 6,743 8.0% 6,961 10.0%

Tier1risk‐basedcapitalratio‐Tier1capital(torisk‐weightedassets) 10,528 12.4% 5,057 6.0% 4,176 8.0%

Commonequitytier1torisk‐weightedassets 10,528 12.4% 3,793 4.5% 5,479 6.5%Leverageratio‐

Tier1capital(toaverageassets) 10,528 10.8% 3,919 4.0% 4,280 5.0%

Actual AdequacyPurposes ActionProvisions

ToBeConsideredWell‐CapitalizedUnder

ForCapital PromptCorrective

As of the most recent notifications from its regulatory agencies, the Bank was categorized as well‐capitalized under the regulatory framework for prompt corrective action. To be categorized asadequately capitalized, the Bank must maintain minimum total risk‐based capital, Tier 1 risk‐basedcapital,andTier1leveragecapitalratiosassetforthinthefollowingtable.TherearenoconditionsoreventssincethatnotificationthatmanagementbelievesmayhavechangedtheBank’scategory.TheBankisrequiredtoestablishandphase‐ina“conservationbuffer,”consistingofacommonequityTier1capitalamountequalto2.5%ofrisk‐weightedassetsby2019.Aninstitutionthatdoesnotmeetthe conservation buffer requirement will be subject to restrictions on certain activities, includingpaymentofdividends,stockrepurchases,anddiscretionarybonusestoexecutiveofficers.Thephase‐inbeganin2016andincreases0.625%annuallyuntilfullyphased‐inby2019.Dividends–Regulationsof theFDICdonotpermit theBanktopaydividendson itscommonstock ifshareholders’equitywouldtherebybereducedbelowtheBank’sregulatorycapitalrequirements.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

31

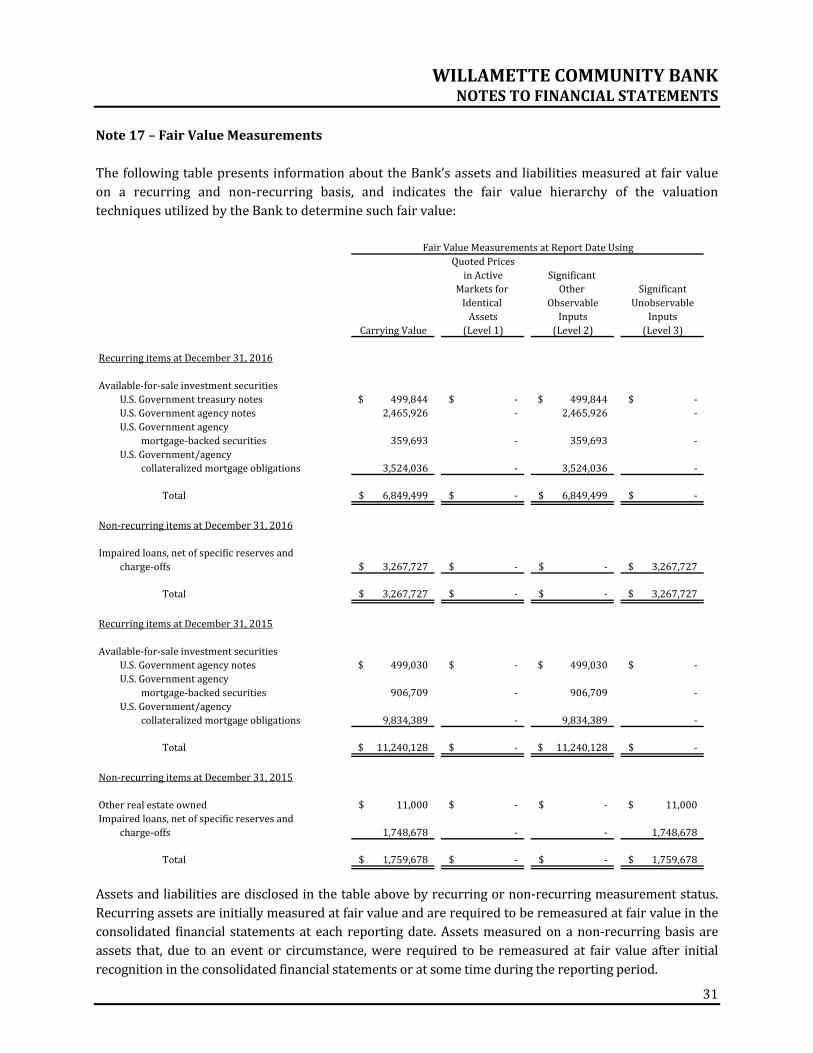

Note17–FairValueMeasurementsThefollowingtablepresentsinformationabouttheBank’sassetsandliabilitiesmeasuredatfairvalueon a recurring and non‐recurring basis, and indicates the fair value hierarchy of the valuationtechniquesutilizedbytheBanktodeterminesuchfairvalue:

QuotedPricesinActive Significant

Marketsfor Other SignificantIdentical Observable UnobservableAssets Inputs Inputs

CarryingValue (Level1) (Level2) (Level3)

RecurringitemsatDecember31,2016

Available‐for‐saleinvestmentsecuritiesU.S.Governmenttreasurynotes 499,844$ ‐$ 499,844$ ‐$U.S.Governmentagencynotes 2,465,926 ‐ 2,465,926 ‐U.S.Governmentagency

mortgage‐backedsecurities 359,693 ‐ 359,693 ‐U.S.Government/agency

collateralizedmortgageobligations 3,524,036 ‐ 3,524,036 ‐

Total 6,849,499$ ‐$ 6,849,499$ ‐$

Non‐recurringitemsatDecember31,2016

Impairedloans,netofspecificreservesandcharge‐offs 3,267,727$ ‐$ ‐$ 3,267,727$

Total 3,267,727$ ‐$ ‐$ 3,267,727$

RecurringitemsatDecember31,2015

Available‐for‐saleinvestmentsecuritiesU.S.Governmentagencynotes 499,030$ ‐$ 499,030$ ‐$U.S.Governmentagency

mortgage‐backedsecurities 906,709 ‐ 906,709 ‐U.S.Government/agency

collateralizedmortgageobligations 9,834,389 ‐ 9,834,389 ‐

Total 11,240,128$ ‐$ 11,240,128$ ‐$

Non‐recurringitemsatDecember31,2015

Otherrealestateowned 11,000$ ‐$ ‐$ 11,000$Impairedloans,netofspecificreservesand

charge‐offs 1,748,678 ‐ ‐ 1,748,678

Total 1,759,678$ ‐$ ‐$ 1,759,678$

FairValueMeasurementsatReportDateUsing

Assetsandliabilitiesaredisclosedinthetableabovebyrecurringornon‐recurringmeasurementstatus.Recurringassetsareinitiallymeasuredatfairvalueandarerequiredtoberemeasuredatfairvalueintheconsolidated financial statementsat each reportingdate.Assetsmeasuredonanon‐recurringbasis areassets that, due to an event or circumstance,were required to be remeasured at fair value after initialrecognitionintheconsolidatedfinancialstatementsoratsometimeduringthereportingperiod.

WILLAMETTECOMMUNITYBANKNOTESTOFINANCIALSTATEMENTS

32

Note17–FairValueMeasurements(continued)Theloansintheprevioustablerepresentimpaired,collateraldependentloansthathavebeenadjustedtofair value with a specific valuation allowance. When management determines that the value of theunderlyingcollateralislessthantherecordedinvestmentintheloan,theBankrecognizesthisimpairmentandadjuststhecarryingvalueoftheloantofairvaluebycharging‐offtheamountoftheimpairmenttotheallowanceforloanlosses,orrecordingaspecificreserveintheallowanceforloanlosses.TheotherrealestateownedbalanceisrealestateinwhichtheBankhastakenownershipinpartialorfullsatisfaction of unpaid loans. At the time of foreclosure, other real estate owned is recorded at the netrealizablevalue,whichbecomestheproperty’snewbasis.Anywrite‐downsbasedontheasset’sfairvalueat the date of acquisition are charged to the allowance for loan and lease losses. After foreclosure,managementperiodicallyperformsvaluationssuchthattherealestateiscarriedatthelowerof itsnewcostbasisorfairvalue,netofestimatedcoststosell.Fairvalueadjustmentsonotherrealestateownedarerecordedasanet lossonrealestateowned.Thislossrepresentsimpairmentsonotherrealestateownedforadjustmentsbasedonthefairvalueoftherealestate.The following table discloses the estimated fair value and the related carrying value of the Bank’sfinancialassetsandliabilities, inaccordancewithdisclosuresaboutfairvalueoffinancialinstruments,asofDecember31,2016and2015:

FairValueatDecember31,2016CarryingValue Total Level1 Level2 Level3

FinancialassetsCashandduefrombanks 10,172,246$ 10,172,246$ 10,172,246$ ‐$ ‐$Investmentsecuritiesavailable‐for‐sale 6,849,499 6,849,499 ‐ 6,849,499 ‐Investmentsecuritiesheld‐to‐maturity 5,312,932 5,400,100 ‐ 5,400,100 ‐Restrictedequitysecurities 218,700 218,700 ‐ 218,700 ‐Loans,net 73,487,030 74,940,030 ‐ ‐ 74,940,030

FinancialliabilitiesNon‐interestbearingdemanddeposits 22,320,671 22,320,671 ‐ 22,320,671 ‐Interest‐bearingdemanddeposits 9,396,876 9,396,876 ‐ 9,396,876 ‐Moneymarketandsavingsaccounts 49,541,267 49,541,267 ‐ 49,541,267 ‐Timedeposits 5,855,472 6,105,472 ‐ 6,105,472 ‐

FairValueatDecember31,2015CarryingValue Total Level1 Level2 Level3

FinancialassetsCashandduefrombanks 7,734,111$ 7,734,111$ 7,734,111$ ‐$ ‐$Investmentsecuritiesavailable‐for‐sale 11,240,128 11,240,128 ‐ 11,240,128 ‐Investmentsecuritiesheld‐to‐maturity,atamortizedcost 4,501,176 4,752,132 ‐ 4,752,132 ‐Restrictedequitysecurities 213,300 213,300 ‐ 213,300 ‐Loans,net 72,864,459 72,219,459 ‐ ‐ 72,219,459

FinancialliabilitiesNon‐interestbearingdemanddeposits 21,346,989 21,346,989 ‐ 21,346,989 ‐Interest‐bearingdemanddeposits 9,239,406 9,239,406 ‐ 9,239,406 ‐Moneymarketandsavingsaccounts 50,829,324 50,829,324 ‐ 50,829,324 ‐Timedeposits 6,881,645 6,896,945 ‐ 6,896,945 ‐