wind power suppliers’ challenge to meet utility standards …or conservative utilities ability to...

TRANSCRIPT

Wind power suppliers’ challenge to meet utility standards…or conservative utilities ability to understand wind power?

May 2007

2

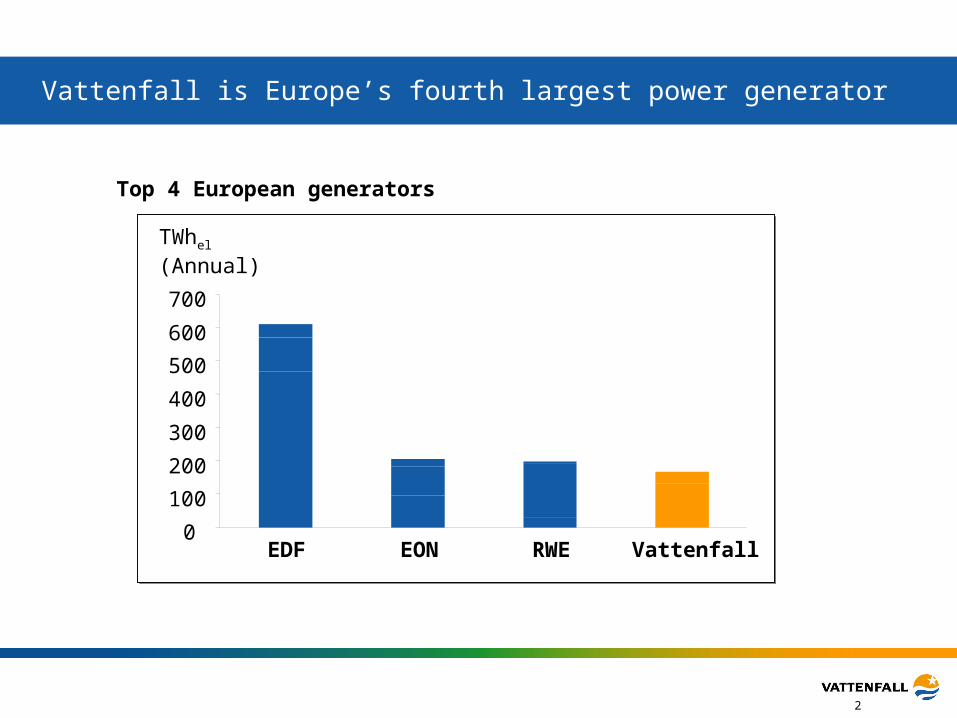

Vattenfall is Europe’s fourth largest power generator

0

100

200

300

400

500

600

700

EDF EON RWE Vattenfall

TWhel

(Annual)

Top 4 European generators

3

Vattenfall is a north European, traditional power producer

Hydro

Nuclear

Fossil

Wind power, bio-fuel and waste

Vattenfall power generation 2006

Current core markets

Current additional markets

Vattenfall markets (May 2007)

165 TWhel

Hydro

Nuclear

Fossil

Other RES

4

• Current portfolio not sustainable from a CO2 perspective

• Vattenfall needs a larger long term portfolio – growth

Wind power is the largest scale RES alternative currently available

Vattenfall wants to grow its RES portfolioVattenfall wind power assets May 2007

165 MW0,5 TWh

311 MW0,8 TWh

90 MW0,3 TWh

600 MW1,7 TWhel

Vattenfall’s aspires for an important position in wind power as well

30 MW0,1 TWh

Vattenfall is prepared to invest 5-10 billion Euro in wind power the next decade

Vattenfall is prepared to invest 5-10 billion Euro in wind power the next decade

5

Vattenfall perceives some supplier issues going forward

System perspective

Generation – Vattenfall’s business

Cost control

• Optimisation on plant level

– Guarantees

– Component suppliers

• Service contracts

– O&M scale harder to achieve

– Philosophy – control

• Double-digit grow for decades to come……eternal delivery challenges

• Where is the customer cost perspective?– Our best guess: Production economics and

supply chain management

6

Happy investors will allocate a lot more money to wind power

2007 2025

CAGR 10%A successful wind industry

CAGR 20%An importantwind industry

Annual wind installations

7

Backupp

8

The global wind power expansion has created large wind power producers

Source: BTM World Market Update 2006

Top 14 wind power generators (end of 2005)

0 1 000 2 000 3 000 4 000

Essent

Vattenfall

RWE

EdF/EnXco

EdP

Shell Renewables

ENEL

DONG

EUROS Energy

Endesa

Babcock Brown

Acciona

Iberdrola

FPL 3 500

4 150*

1 700

1 180

800

750

750

750

740

740

700

600

550

480

Installed MW

• European companies dominate the market

– Only three non-European companies in the top-15 list

• Countries with historically strong support systems for wind power dominate the worldwide capacity

– Three Spanish companies in the top-5

* Including the acquisition of Scottish Power 2007

9

Vattenfall is Europe’s fourth largest power generator

0

100

200

300

400

500

600

700

EDF EON RWE Vattenfall

TWhel

(Annual)

Top 4 European generators

RES

Fossil

Nuclear

10

Wind power suppliers gaining strength, which will ultimately benefit customers

Repower

Siemens

Suzlon

Gamesa

Enercon

GE

Vestas

Large industrials

Large independents

Wind turbine market structure 2005

• Strong consolidation on-going• Industrial production capabilities entering industry

– Areva and Suzlon bids for Repower 2007– Siemens acquired Bonus 2004– GE acquired Enron Wind 2002

• As suppliers grow larger and more capable, production economy likely to improve

• New market entrants expected in booming industry

– Mitsubishi growing strongly in Asia

Source: BTM March 2006

Mitsubishi

11

The learning curve for wind power has historically indicated 13% price decrease for doubled cumulative output

Learning curves for emerging technologies1

Production economy indicates lower prices• Wind power’s cumulative output is currently doubling

every four years, indicating 13% cost reduction every four years

• There may be potential for steeper price decreases: – Strong growth has meant focus on delivery, not

cost– Historic rapid technology development has meant

short production runs

Business environment maintains price levels• Future strong demand limits medium term and possibly

long term price potential • Vattenfall’s potential to affect prices is limited by the fact

that Vattenfall’s ambitions amount to <1% of industry output

Source: Vattenfall 3C initiative

Wind power learning curve