wish you all a happy deepawali & shubh samvat 2069...

TRANSCRIPT

Wish you all a Happy Deepawali& Shubh Samvat 2069

November 2012

Details Page No

Overview on Indian Capital Markets 3

Investment Theme for Investing in India 4

Market Outlook 2013E-15E 5-7

Why India stands favorite for global investors? 8-11

Msearch Equity Portfolio Performance October 2012 & January 2012 12-13

Stocks Idea for Samvat 2069 14

SpiceJet Ltd 15

Prozone CSC Ltd 16

Omkar Speciality Chemicals Ltd 17

OnMobile Global Ltd 18

Innoventive Industries Ltd 19

Heritage Foods (India) Ltd 20

MCX India Ltd 21

Tech Mahindra Ltd 22

Axis Bank Ltd , Bata India Ltd , Sterlite Industries India ltd, Maruti Suzuki India Ltd, IGL Ltd, ShasunPharma Ltd, Aditya Birla Nuvo Ltd 23-29

Index

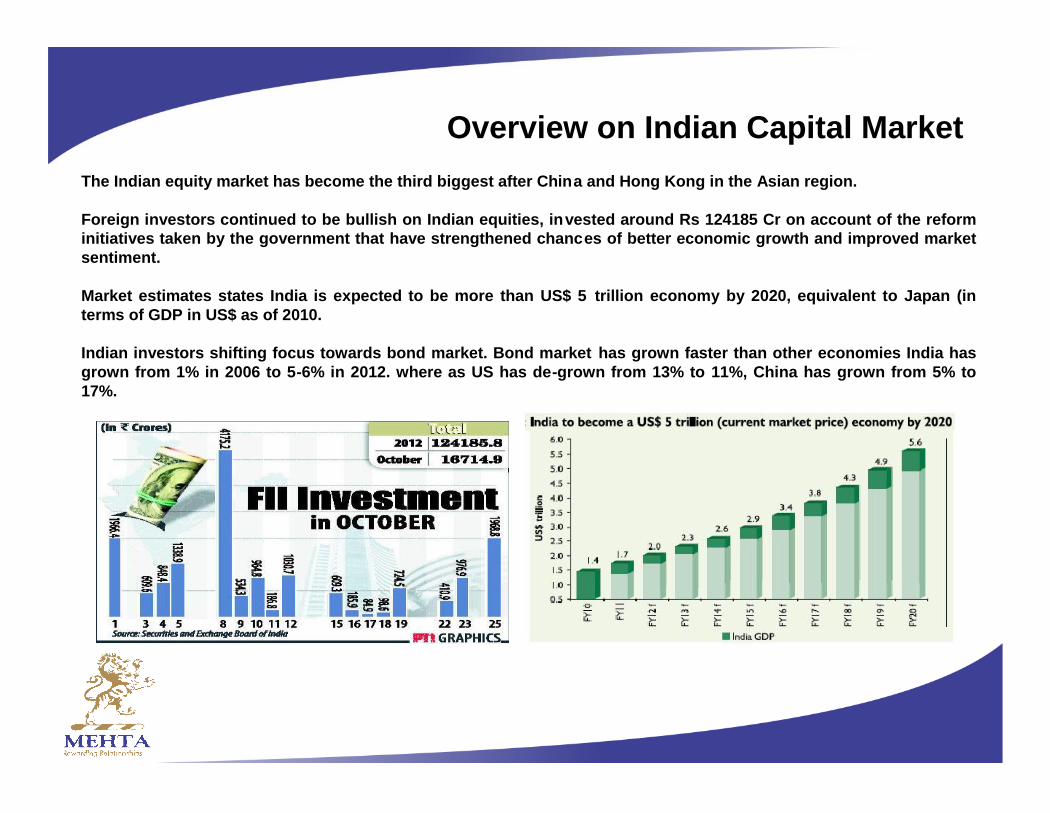

Overview on Indian Capital MarketThe Indian equity market has become the third biggest after China and Hong Kong in the Asian region.

Foreign investors continued to be bullish on Indian equities, invested around Rs 124185 Cr on account of the reforminitiatives taken by the government that have strengthened chances of better economic growth and improved marketsentiment.

Market estimates states India is expected to be more than US$ 5 trillion economy by 2020, equivalent to Japan (interms of GDP in US$ as of 2010.

Indian investors shifting focus towards bond market. Bond market has grown faster than other economies India hasgrown from 1% in 2006 to 5-6% in 2012. where as US has de-grown from 13% to 11%, China has grown from 5% to17%.

Theme for Investing in India

Our strategy is to focus on domestic themes.

Government Economic Reform and Consumption are the themes where wehave been bullish on. Recent Economic reforms show the government isdetermined to mend the economy and regain the confidence of foreigninvestors.

Indian Government is serious about fiscal consolidation and encouraginginvestment through reforms like opening up the retail and airlines sector toforeign investment, controlling fiscal deficit through disinvestment of Govtstakes, etc. The measure is aimed to rein in a ballooning fiscal deficit andavoid a credit rating downgrade to junk.

After an almost 21% rise so far this year, driven by a rush of foreigninstitutional inflows after the government’s policy push, we are seeking moresuch pro-business measures, including an increase in the foreign directinvestment limit in the insurance sector, which will keep Indian marketattractive.

We expect Indian Equity Markets to be on Upbeat on Optimism as Govt.continues Reforms Agenda. We want to focus on sectors and stocks thatexhibit strong growth and provide visibility to earnings.

“Reforming Indian Growth Story”

Action Plan for 2012-2014E

FDI in Retail Sector.

FDI in Aviation.

FDI in Insurance.

Decontrolling Diesel pricing

Disinvestment Govt Stakes

New Banking licences & GST

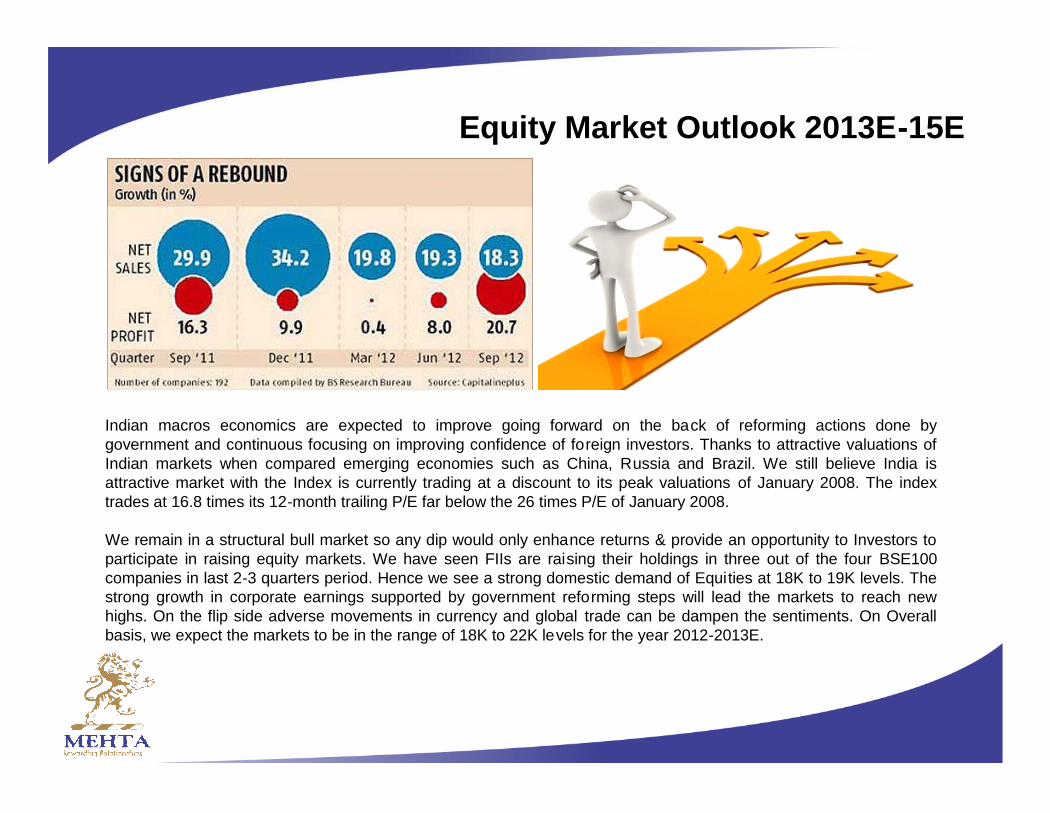

Equity Market Outlook 2013E-15E

Indian macros economics are expected to improve going forward on the back of reforming actions done bygovernment and continuous focusing on improving confidence of foreign investors. Thanks to attractive valuations ofIndian markets when compared emerging economies such as China, Russia and Brazil. We still believe India isattractive market with the Index is currently trading at a discount to its peak valuations of January 2008. The indextrades at 16.8 times its 12-month trailing P/E far below the 26 times P/E of January 2008.

We remain in a structural bull market so any dip would only enhance returns & provide an opportunity to Investors toparticipate in raising equity markets. We have seen FIIs are raising their holdings in three out of the four BSE100companies in last 2-3 quarters period. Hence we see a strong domestic demand of Equities at 18K to 19K levels. Thestrong growth in corporate earnings supported by government reforming steps will lead the markets to reach newhighs. On the flip side adverse movements in currency and global trade can be dampen the sentiments. On Overallbasis, we expect the markets to be in the range of 18K to 22K levels for the year 2012-2013E.

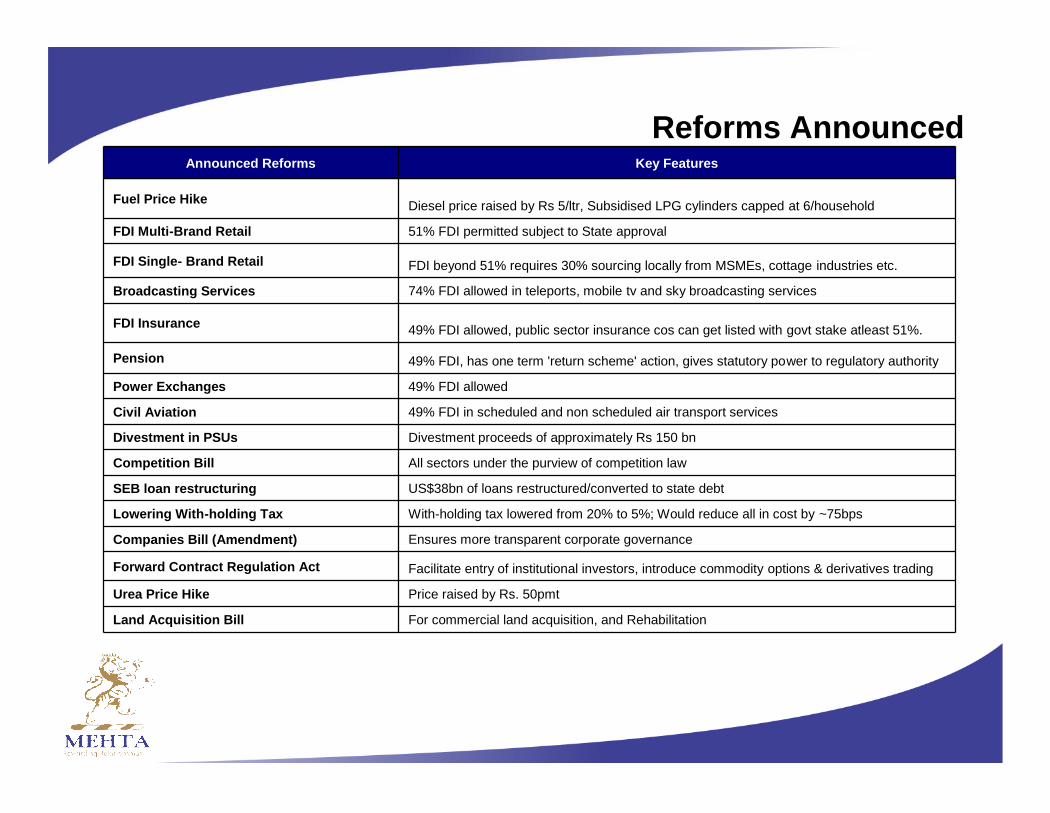

Reforms AnnouncedAnnounced Reforms Key Features

Fuel Price Hike Diesel price raised by Rs 5/ltr, Subsidised LPG cylinders capped at 6/household

FDI Multi-Brand Retail 51% FDI permitted subject to State approval

FDI Single- Brand Retail FDI beyond 51% requires 30% sourcing locally from MSMEs, cottage industries etc.

Broadcasting Services 74% FDI allowed in teleports, mobile tv and sky broadcasting services

FDI Insurance 49% FDI allowed, public sector insurance cos can get listed with govt stake atleast 51%.

Pension 49% FDI, has one term 'return scheme' action, gives statutory power to regulatory authority

Power Exchanges 49% FDI allowed

Civil Aviation 49% FDI in scheduled and non scheduled air transport services

Divestment in PSUs Divestment proceeds of approximately Rs 150 bn

Competition Bill All sectors under the purview of competition law

SEB loan restructuring US$38bn of loans restructured/converted to state debt

Lowering With-holding Tax With-holding tax lowered from 20% to 5%; Would reduce all in cost by ~75bps

Companies Bill (Amendment) Ensures more transparent corporate governance

Forward Contract Regulation Act Facilitate entry of institutional investors, introduce commodity options & derivatives trading

Urea Price Hike Price raised by Rs. 50pmt

Land Acquisition Bill For commercial land acquisition, and Rehabilitation

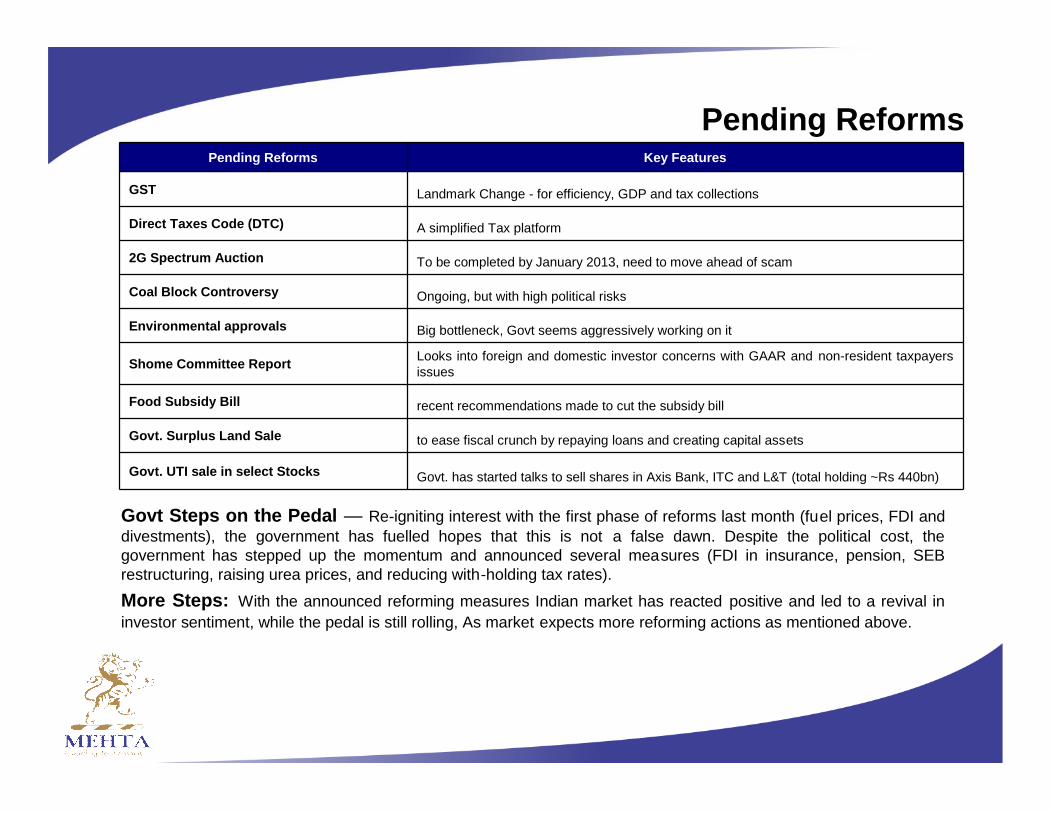

Pending ReformsPending Reforms Key Features

GST Landmark Change - for efficiency, GDP and tax collections

Direct Taxes Code (DTC) A simplified Tax platform

2G Spectrum Auction To be completed by January 2013, need to move ahead of scam

Coal Block Controversy Ongoing, but with high political risks

Environmental approvals Big bottleneck, Govt seems aggressively working on it

Shome Committee Report Looks into foreign and domestic investor concerns with GAAR and non-resident taxpayersissues

Food Subsidy Bill recent recommendations made to cut the subsidy bill

Govt. Surplus Land Sale to ease fiscal crunch by repaying loans and creating capital assets

Govt. UTI sale in select Stocks Govt. has started talks to sell shares in Axis Bank, ITC and L&T (total holding ~Rs 440bn)

Govt Steps on the Pedal — Re-igniting interest with the first phase of reforms last month (fuel prices, FDI anddivestments), the government has fuelled hopes that this is not a false dawn. Despite the political cost, thegovernment has stepped up the momentum and announced several measures (FDI in insurance, pension, SEBrestructuring, raising urea prices, and reducing with-holding tax rates).

More Steps: With the announced reforming measures Indian market has reacted positive and led to a revival ininvestor sentiment, while the pedal is still rolling, As market expects more reforming actions as mentioned above.

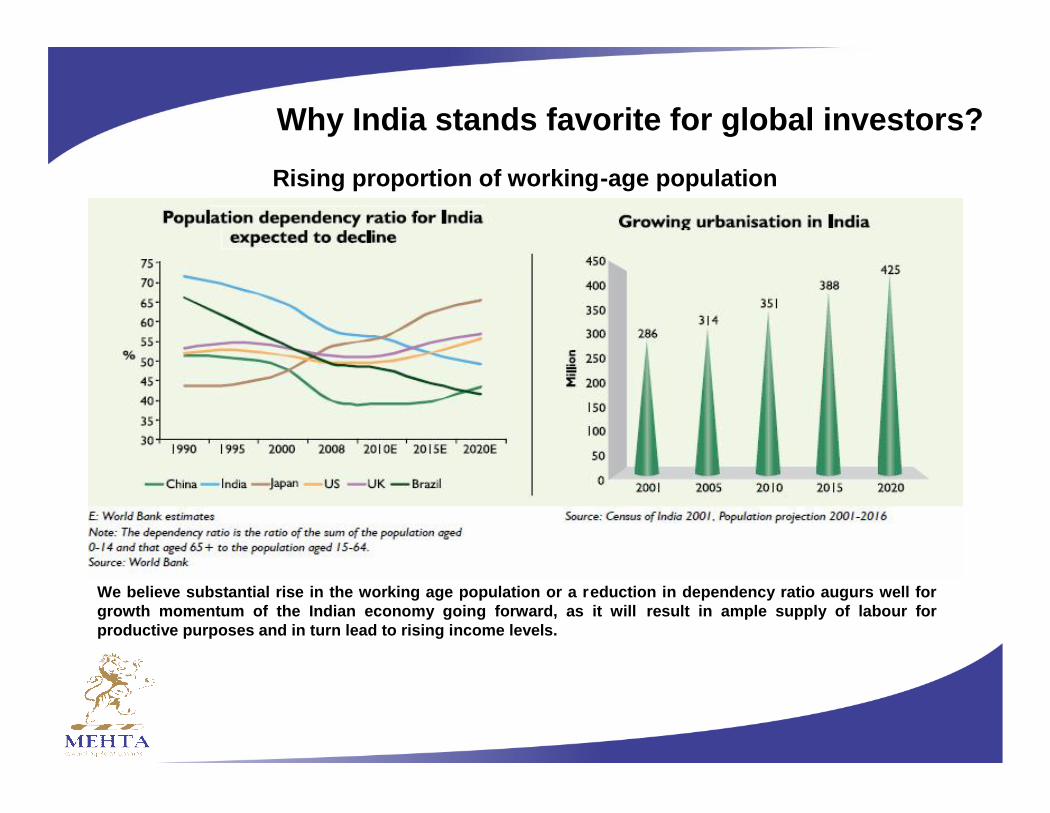

Why India stands favorite for global investors?

Why India stands favorite for global investors?

Rising proportion of working-age population

We believe substantial rise in the working age population or a reduction in dependency ratio augurs well forgrowth momentum of the Indian economy going forward, as it will result in ample supply of labour forproductive purposes and in turn lead to rising income levels.

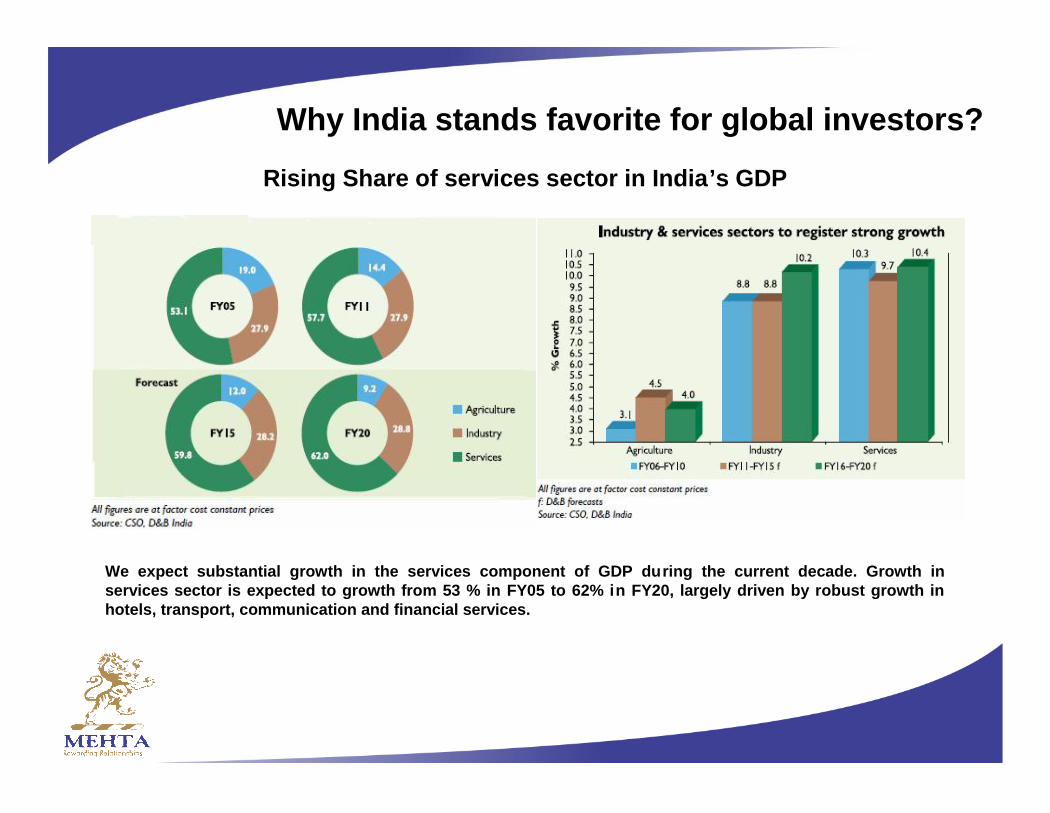

Why India stands favorite for global investors?

Rising Share of services sector in India’s GDP

We expect substantial growth in the services component of GDP during the current decade. Growth inservices sector is expected to growth from 53 % in FY05 to 62% in FY20, largely driven by robust growth inhotels, transport, communication and financial services.

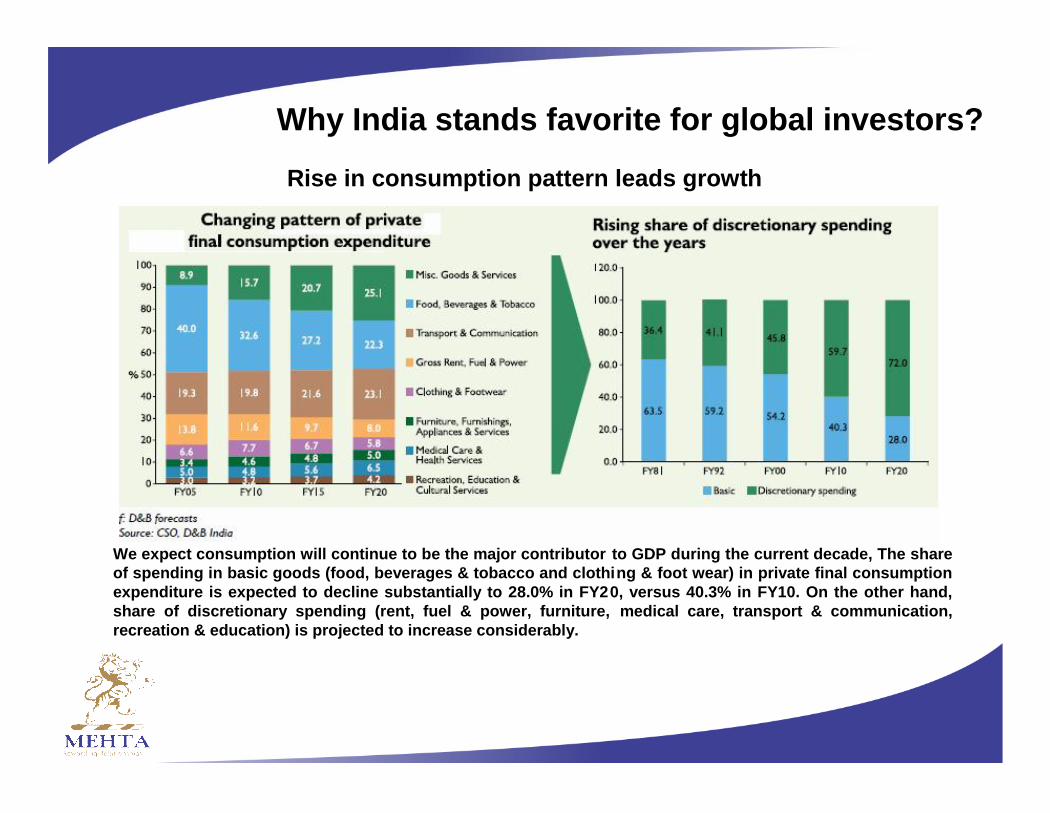

Why India stands favorite for global investors?

Rise in consumption pattern leads growth

We expect consumption will continue to be the major contributor to GDP during the current decade, The shareof spending in basic goods (food, beverages & tobacco and clothing & foot wear) in private final consumptionexpenditure is expected to decline substantially to 28.0% in FY20, versus 40.3% in FY10. On the other hand,share of discretionary spending (rent, fuel & power, furniture, medical care, transport & communication,recreation & education) is projected to increase considerably.

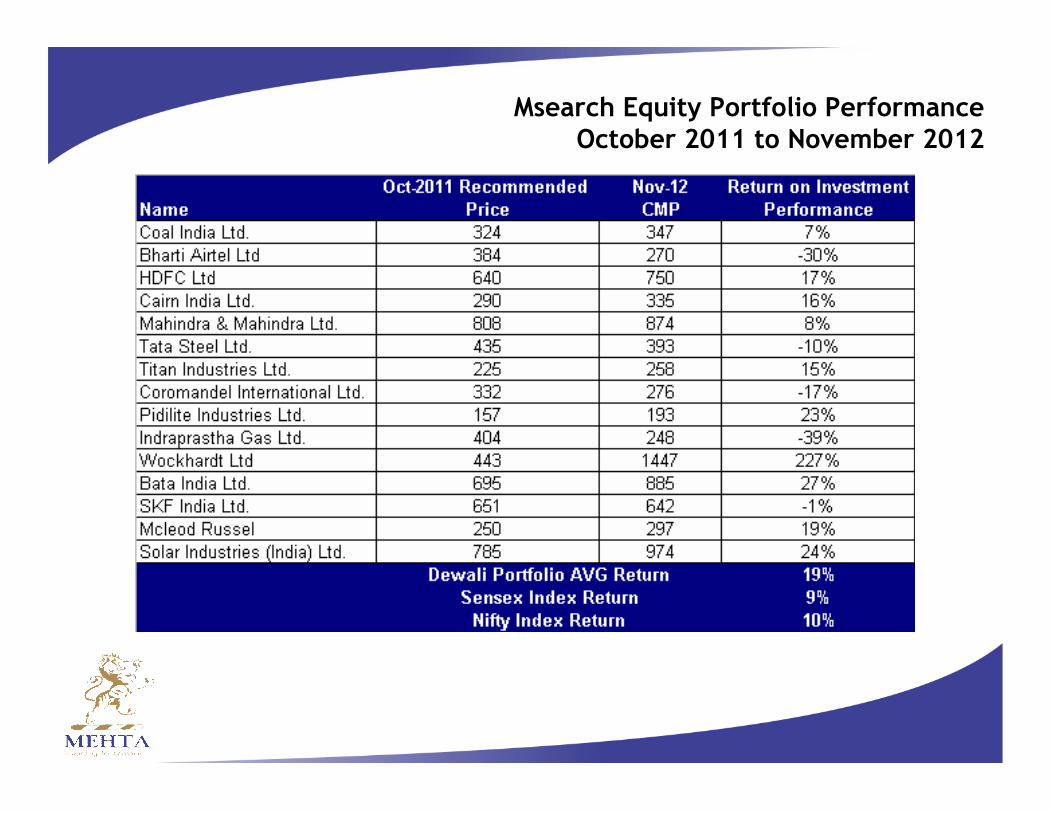

Msearch Equity Portfolio PerformanceOctober 2011 to November 2012

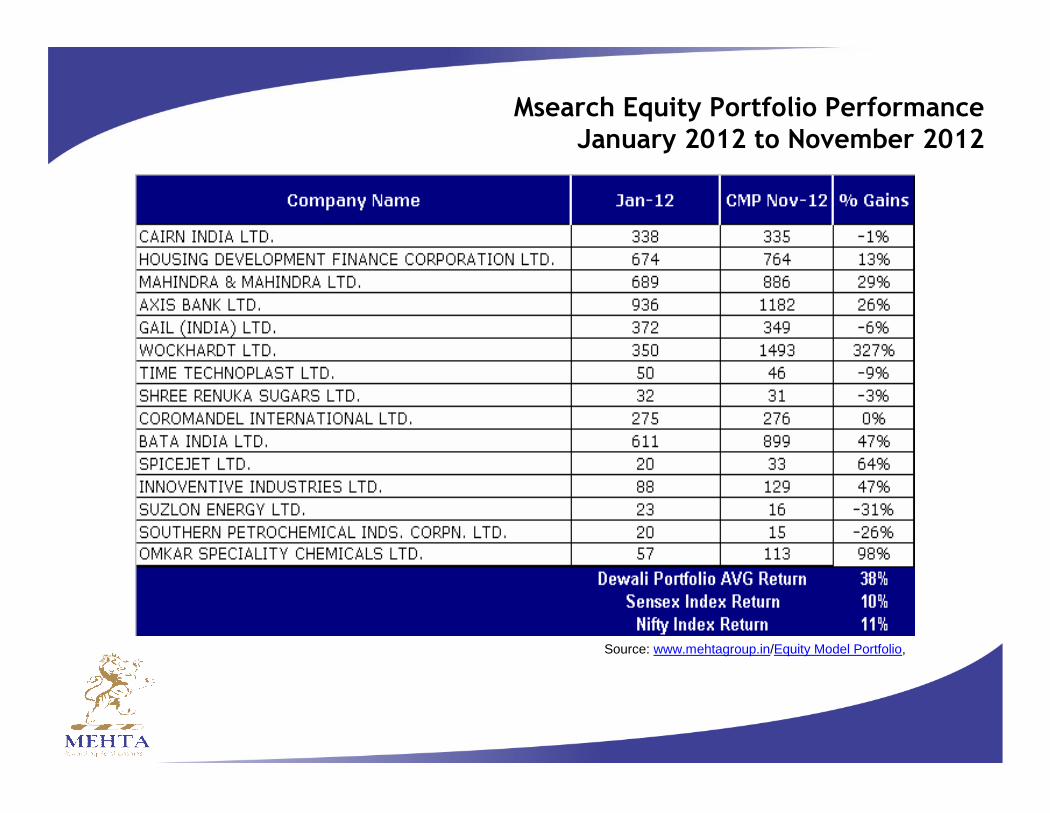

Msearch Equity Portfolio PerformanceJanuary 2012 to November 2012

Source: www.mehtagroup.in/Equity Model Portfolio,

SpiceJet Ltd

Recommendation: Buy Market Cap Rs: 1755 Cr Cmp Rs: 36

About the Company

SpiceJet is a leading low-cost airline headquartered in Chennai, India owned by KalanithiMaran. By 2012, it is the third largest Indian Airline in terms of market share ahead of AirIndia, Kingfisher Airlines and GoAir. The Company has international operations in countriessuch, as Kathmandu, Colombo and Dubai. During the fiscal year ended March 2012, theCompany carried 10.89 mn passengers, in operations included 47 aircraft covering 39destinations and operating 281 flights per day.Investment Rationale

• Preferred Airline for FDI reforms as and when it happens, because of its operationalefficiency, Low cost business model works out to yield more on domestic route and healthyexpansion plans to explore international route.

• A strong recovery in yield in the domestic sector and rationalization of its international routeshould enable SpiceJet post substantially lower losses in FY13 and strong profits in FY14.

Financial Overview (Rs Cr) FY2011 FY2012 1QFY2012

Net Sales 2938 3998 1467

EBIDTA 146 -518 76

PAT 101 -606 56

EPS 3 - 1

Stock Details Rs in Cr

Dividend Yield -

Networth -157

Equity Capital 484

FV 10

PE (x) 9

Book Value -

52 Week H/L 41/15

Prozone CSC Ltd

Recommendation: Buy Market Cap Rs: 492 Cr Cmp Rs: 32

About the Company

Prozone CSC (PZ) is a real estate developer jointly promoted by the Chaturvedi Family(Provogue fame) and UK's most valuable retail space owner - Capital Shopping Centres(CSC). This partnership was formed in 2007 under the listed company, Provogue Ltd, whichwas spinoff to a new listed entity in Sep'12. The India promoters hold 35.1stake in thecompany while CSC holds 32.4% stake.

Investment Rationale

• A unique proposition in real estate: Blend of strong B/s, annuity income generatingasset, tier-2 cities land bank and a experienced international partner makes Prozone a nicheplayer with virtually a debt free balance sheet.

• Fully paid land bank of 17.8msf (10.1msf (PZ share) across six tier-2 cities in India, PZplans to develop 10msf (6msf PZ share) over next 5 years including 1.3msf of retail mall

• Well planed project pipeline for next 3 years which would generate healthy cash flow.

• CSC’s partnership adds a lot of credibility to the company’s bandwidth and governedbusiness approach Capital Store Centers (CSC) is one of the UK’s most valuable retailasset owners. The company operates 10 of the 25 large retail assets in UK and is valued at ~3bn pounds.

Stock Details Rs in Cr

Dividend Yield -

Networth 614

Equity Capital 31

FV 2

PE (x) -

Book Value 26

52 Week H/L 35/21

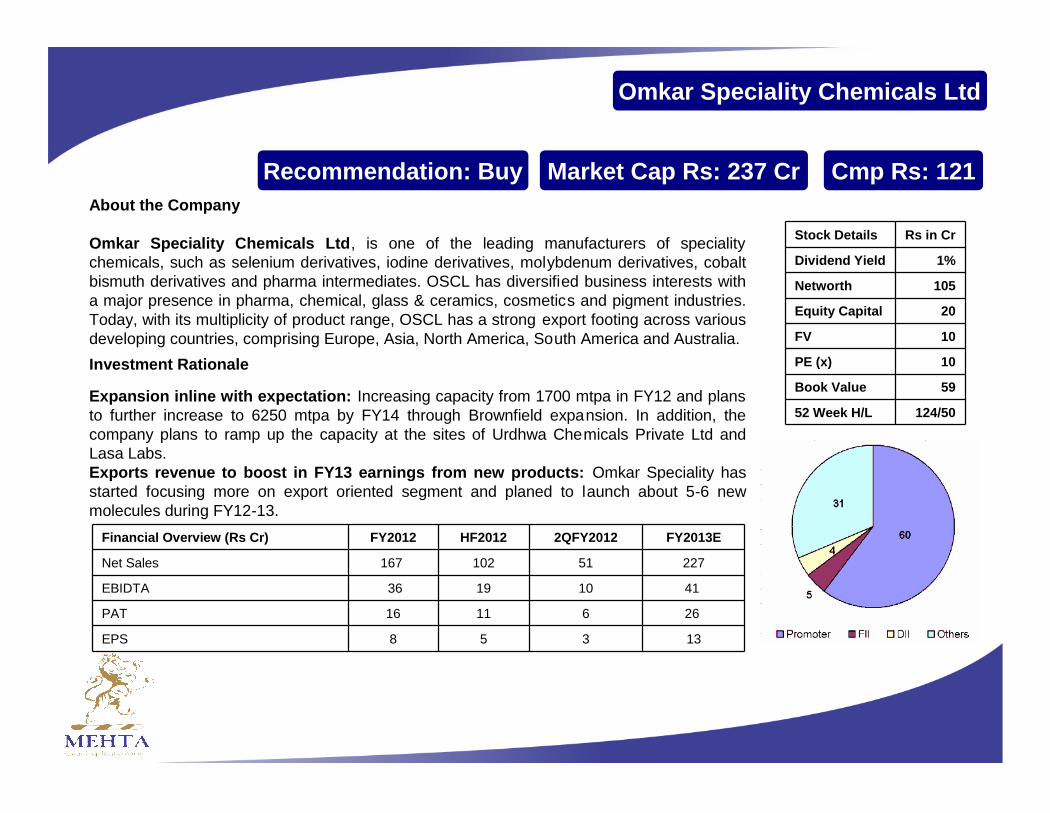

Omkar Speciality Chemicals Ltd

Recommendation: Buy Market Cap Rs: 237 Cr Cmp Rs: 121About the Company

Omkar Speciality Chemicals Ltd, is one of the leading manufacturers of specialitychemicals, such as selenium derivatives, iodine derivatives, molybdenum derivatives, cobaltbismuth derivatives and pharma intermediates. OSCL has diversified business interests witha major presence in pharma, chemical, glass & ceramics, cosmetics and pigment industries.Today, with its multiplicity of product range, OSCL has a strong export footing across variousdeveloping countries, comprising Europe, Asia, North America, South America and Australia.Investment Rationale

Expansion inline with expectation: Increasing capacity from 1700 mtpa in FY12 and plansto further increase to 6250 mtpa by FY14 through Brownfield expansion. In addition, thecompany plans to ramp up the capacity at the sites of Urdhwa Chemicals Private Ltd andLasa Labs.Exports revenue to boost in FY13 earnings from new products: Omkar Speciality hasstarted focusing more on export oriented segment and planed to launch about 5-6 newmolecules during FY12-13.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 167 102 51 227

EBIDTA 36 19 10 41

PAT 16 11 6 26

EPS 8 5 3 13

Stock Details Rs in Cr

Dividend Yield 1%

Networth 105

Equity Capital 20

FV 10

PE (x) 10

Book Value 59

52 Week H/L 124/50

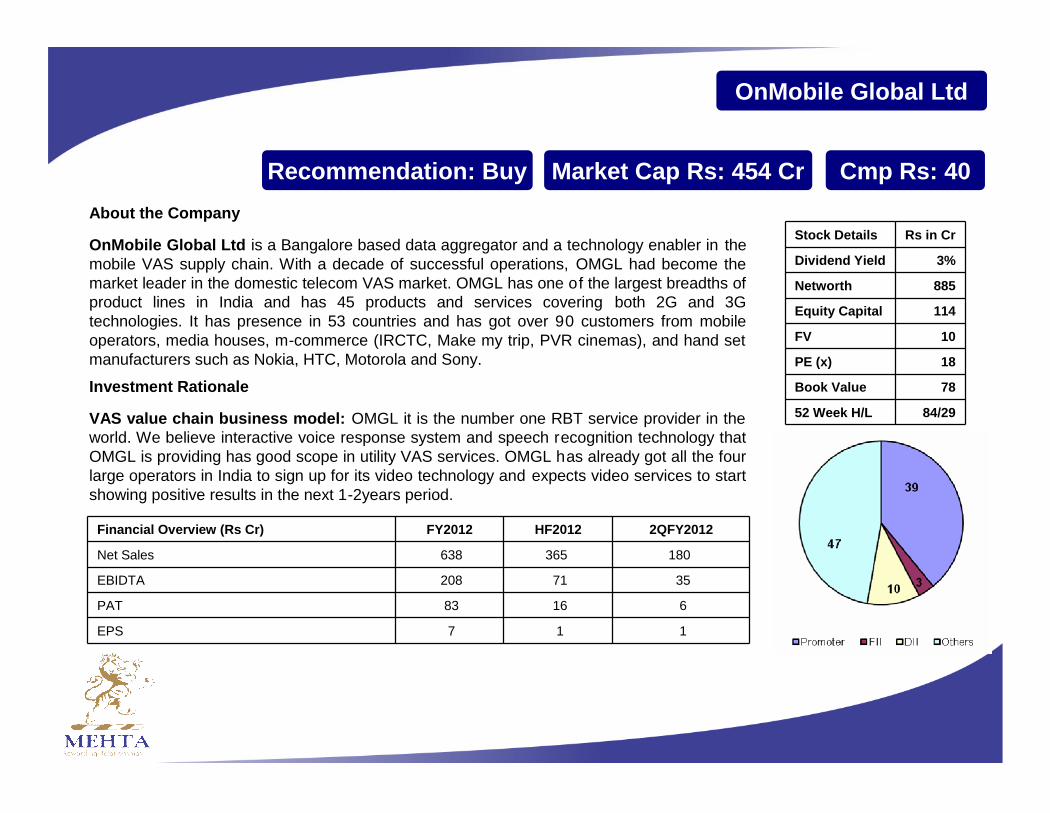

OnMobile Global Ltd

Recommendation: Buy Market Cap Rs: 454 Cr Cmp Rs: 40About the Company

OnMobile Global Ltd is a Bangalore based data aggregator and a technology enabler in themobile VAS supply chain. With a decade of successful operations, OMGL had become themarket leader in the domestic telecom VAS market. OMGL has one of the largest breadths ofproduct lines in India and has 45 products and services covering both 2G and 3Gtechnologies. It has presence in 53 countries and has got over 90 customers from mobileoperators, media houses, m-commerce (IRCTC, Make my trip, PVR cinemas), and hand setmanufacturers such as Nokia, HTC, Motorola and Sony.

Investment Rationale

VAS value chain business model: OMGL it is the number one RBT service provider in theworld. We believe interactive voice response system and speech recognition technology thatOMGL is providing has good scope in utility VAS services. OMGL has already got all the fourlarge operators in India to sign up for its video technology and expects video services to startshowing positive results in the next 1-2years period.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012

Net Sales 638 365 180

EBIDTA 208 71 35

PAT 83 16 6

EPS 7 1 1

Stock Details Rs in Cr

Dividend Yield 3%

Networth 885

Equity Capital 114

FV 10

PE (x) 18

Book Value 78

52 Week H/L 84/29

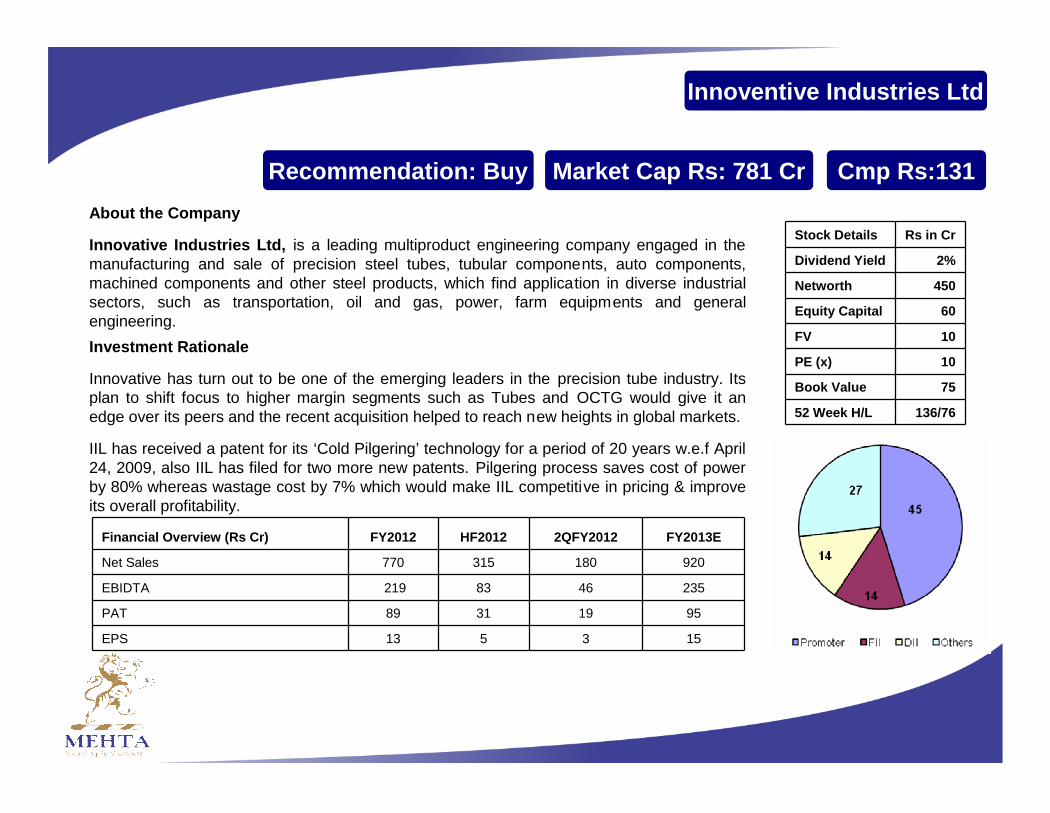

Innoventive Industries Ltd

Recommendation: Buy Market Cap Rs: 781 Cr Cmp Rs:131About the Company

Innovative Industries Ltd, is a leading multiproduct engineering company engaged in themanufacturing and sale of precision steel tubes, tubular components, auto components,machined components and other steel products, which find application in diverse industrialsectors, such as transportation, oil and gas, power, farm equipments and generalengineering.Investment Rationale

Innovative has turn out to be one of the emerging leaders in the precision tube industry. Itsplan to shift focus to higher margin segments such as Tubes and OCTG would give it anedge over its peers and the recent acquisition helped to reach new heights in global markets.

IIL has received a patent for its ‘Cold Pilgering’ technology for a period of 20 years w.e.f April24, 2009, also IIL has filed for two more new patents. Pilgering process saves cost of powerby 80% whereas wastage cost by 7% which would make IIL competitive in pricing & improveits overall profitability.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 770 315 180 920

EBIDTA 219 83 46 235

PAT 89 31 19 95

EPS 13 5 3 15

Stock Details Rs in Cr

Dividend Yield 2%

Networth 450

Equity Capital 60

FV 10

PE (x) 10

Book Value 75

52 Week H/L 136/76

Heritage Foods (India) Ltd

Recommendation: Buy Market Cap Rs: 506 Cr Cmp Rs: 439About the Company:

Heritage Foods (India) Ltd (commonly known as Heritage) is one of the largest privatesector dairy enterprises in Southern India. It is engaged in segments: Dairy, Retail, Agri,Bakery, HFRL, SPV and Heritage Conpro Limited. Presently Heritage’s milk products havemarket presence in Andhra Pradesh, Karnataka, Kerala, Tamil Nadu and Maharastra and itsretail stores across Bangalore, Chennai and Hyderabad.

Investment Rationale

One stop shop for daily needs through its various verticals. This integrated business modelwhich includes farming, processing ,retailing ,baking and diary - Heritage is a company withno comparable listed players.

Market leader in Andhra Pradesh, with nearly 14% market share, Heritage Foods is wellplaced to reap benefits of the secular growth in the under-penetrated milk business, which isgrowing at a CAGR of 17.3% and commanding a strong brand name in south Indian market.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 1393 816 402 1650

EBIDTA 57 47 27 98

PAT 9 23 14 52

EPS 8 20 13 43

Stock Details Rs in Cr

Dividend Yield 0.45%

Networth 90

Equity Capital 12

FV 10

PE (x) 9

Book Value 100

52 Week H/L 455/133

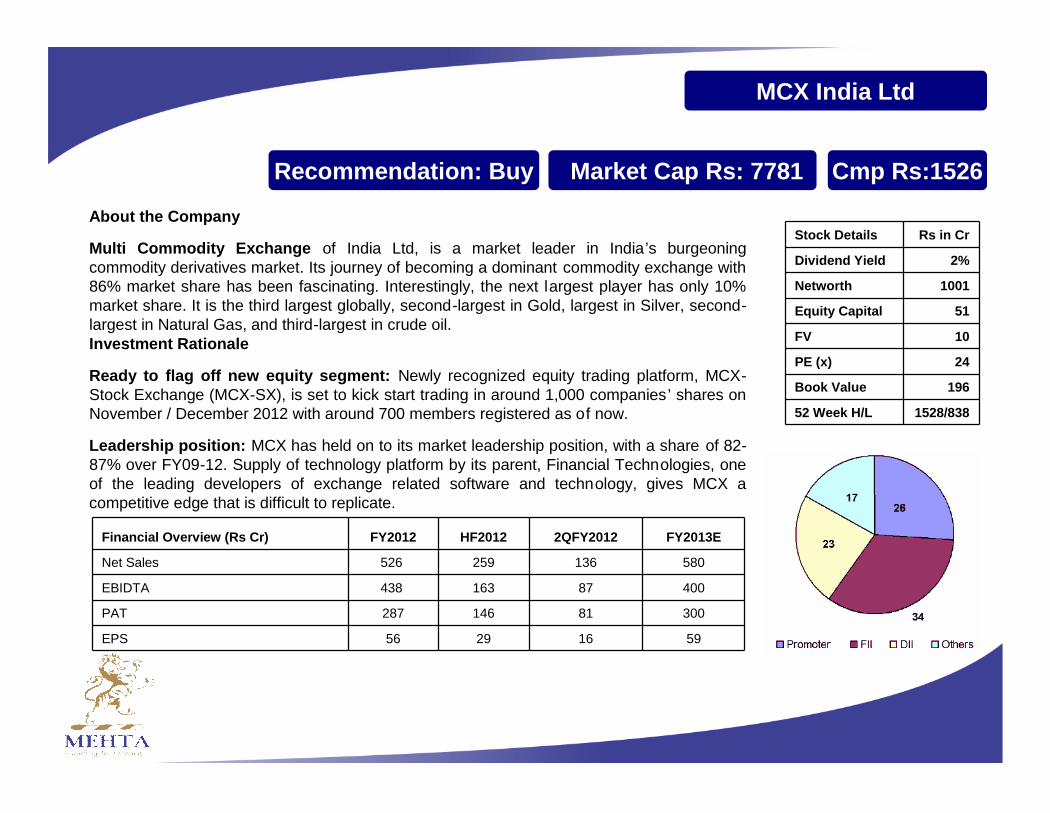

MCX India Ltd

Recommendation: Buy Market Cap Rs: 7781 CrCmp Rs:1526

About the Company

Multi Commodity Exchange of India Ltd, is a market leader in India’s burgeoningcommodity derivatives market. Its journey of becoming a dominant commodity exchange with86% market share has been fascinating. Interestingly, the next largest player has only 10%market share. It is the third largest globally, second-largest in Gold, largest in Silver, second-largest in Natural Gas, and third-largest in crude oil.Investment Rationale

Ready to flag off new equity segment: Newly recognized equity trading platform, MCX-Stock Exchange (MCX-SX), is set to kick start trading in around 1,000 companies’ shares onNovember / December 2012 with around 700 members registered as of now.

Leadership position: MCX has held on to its market leadership position, with a share of 82-87% over FY09-12. Supply of technology platform by its parent, Financial Technologies, oneof the leading developers of exchange related software and technology, gives MCX acompetitive edge that is difficult to replicate.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 526 259 136 580

EBIDTA 438 163 87 400

PAT 287 146 81 300

EPS 56 29 16 59

Stock Details Rs in Cr

Dividend Yield 2%

Networth 1001

Equity Capital 51

FV 10

PE (x) 24

Book Value 196

52 Week H/L 1528/838

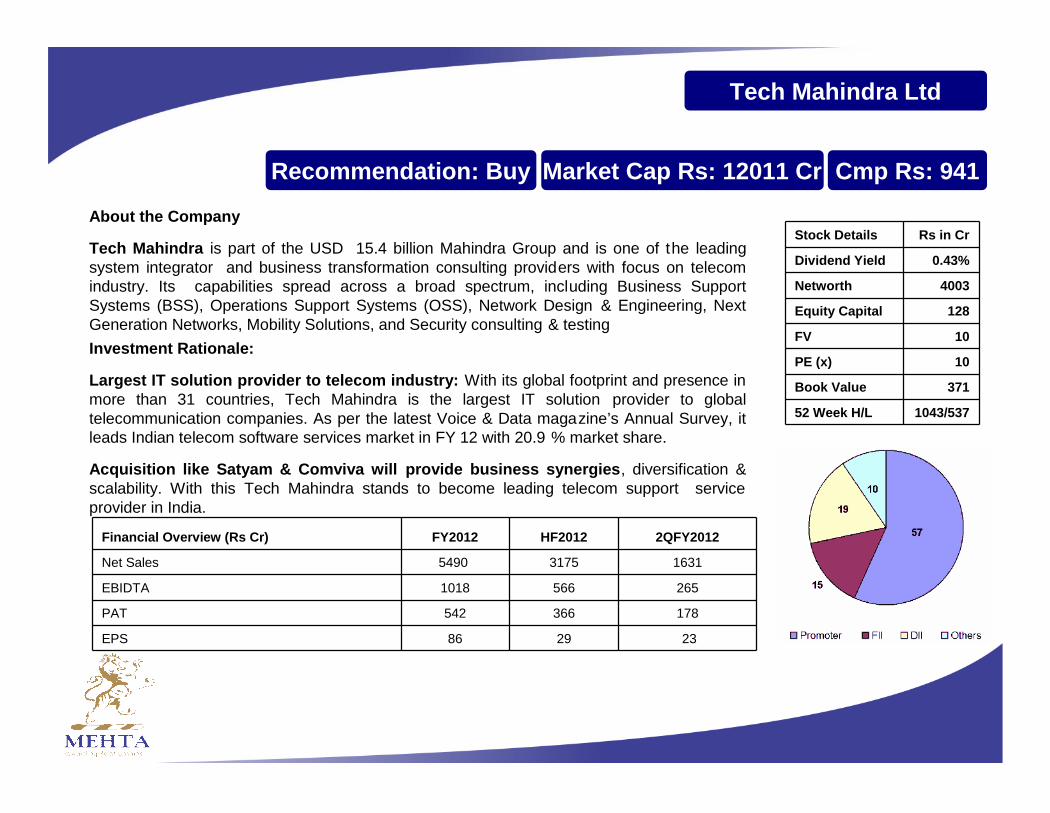

Tech Mahindra Ltd

Recommendation: Buy Market Cap Rs: 12011 Cr Cmp Rs: 941

About the Company

Tech Mahindra is part of the USD 15.4 billion Mahindra Group and is one of the leadingsystem integrator and business transformation consulting providers with focus on telecomindustry. Its capabilities spread across a broad spectrum, including Business SupportSystems (BSS), Operations Support Systems (OSS), Network Design & Engineering, NextGeneration Networks, Mobility Solutions, and Security consulting & testingInvestment Rationale:

Largest IT solution provider to telecom industry: With its global footprint and presence inmore than 31 countries, Tech Mahindra is the largest IT solution provider to globaltelecommunication companies. As per the latest Voice & Data magazine’s Annual Survey, itleads Indian telecom software services market in FY 12 with 20.9 % market share.

Acquisition like Satyam & Comviva will provide business synergies, diversification &scalability. With this Tech Mahindra stands to become leading telecom support serviceprovider in India.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012

Net Sales 5490 3175 1631

EBIDTA 1018 566 265

PAT 542 366 178

EPS 86 29 23

Stock Details Rs in Cr

Dividend Yield 0.43%

Networth 4003

Equity Capital 128

FV 10

PE (x) 10

Book Value 371

52 Week H/L 1043/537

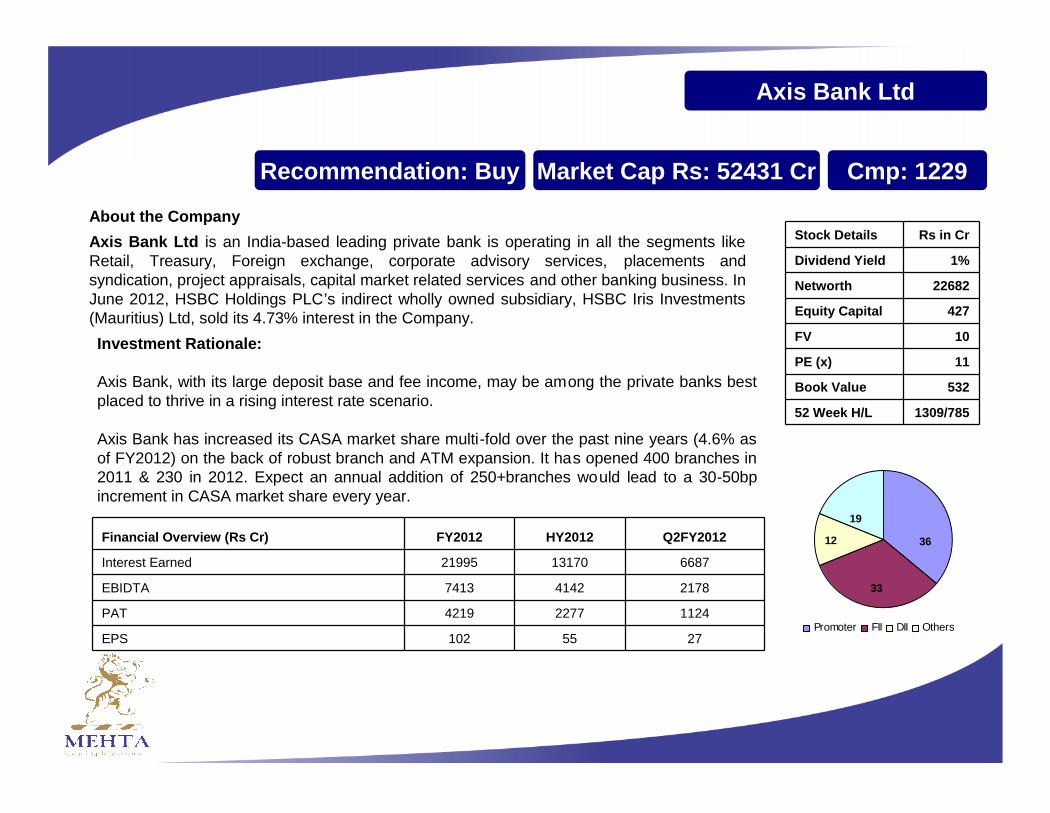

Axis Bank Ltd

Recommendation: Buy Market Cap Rs: 52431 Cr Cmp: 1229

About the CompanyAxis Bank Ltd is an India-based leading private bank is operating in all the segments likeRetail, Treasury, Foreign exchange, corporate advisory services, placements andsyndication, project appraisals, capital market related services and other banking business. InJune 2012, HSBC Holdings PLC’s indirect wholly owned subsidiary, HSBC Iris Investments(Mauritius) Ltd, sold its 4.73% interest in the Company.Investment Rationale:

Axis Bank, with its large deposit base and fee income, may be among the private banks bestplaced to thrive in a rising interest rate scenario.

Axis Bank has increased its CASA market share multi-fold over the past nine years (4.6% asof FY2012) on the back of robust branch and ATM expansion. It has opened 400 branches in2011 & 230 in 2012. Expect an annual addition of 250+branches would lead to a 30-50bpincrement in CASA market share every year.

Financial Overview (Rs Cr) FY2012 HY2012 Q2FY2012

Interest Earned 21995 13170 6687

EBIDTA 7413 4142 2178

PAT 4219 2277 1124

EPS 102 55 27

Stock Details Rs in Cr

Dividend Yield 1%

Networth 22682

Equity Capital 427

FV 10

PE (x) 11

Book Value 532

52 Week H/L 1309/785

19

12 36

33

Promoter FII DII Others

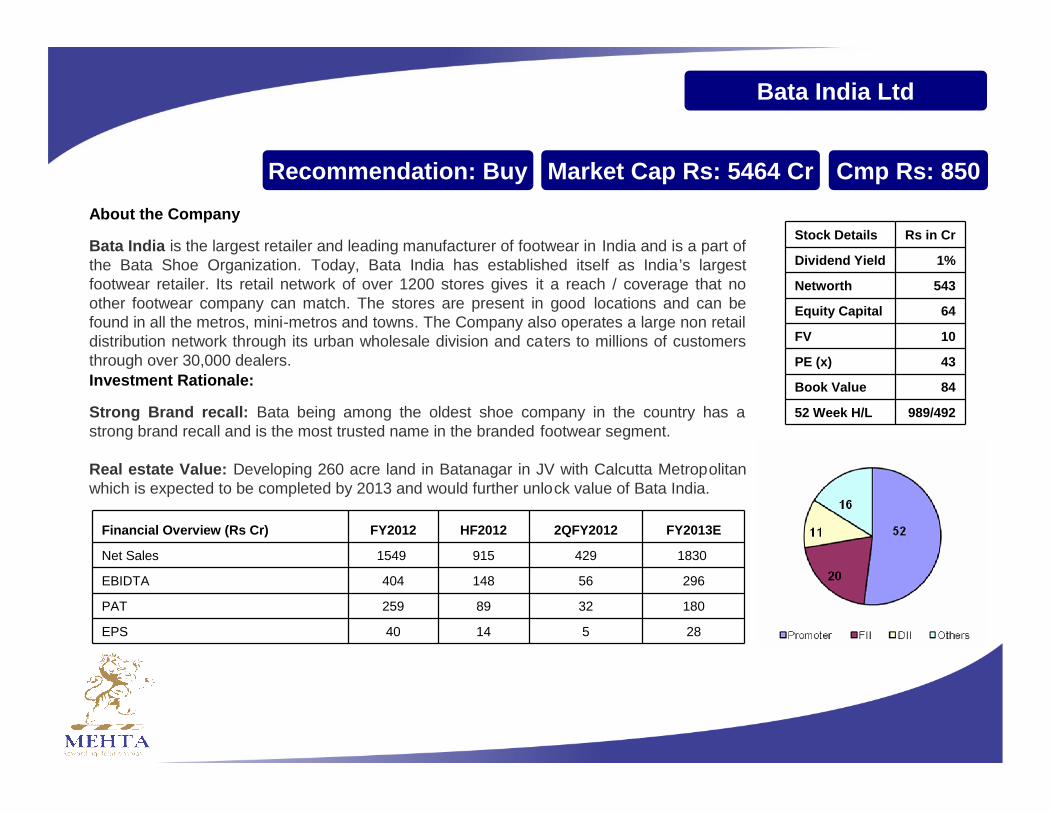

Bata India Ltd

Recommendation: Buy Market Cap Rs: 5464 Cr Cmp Rs: 850About the Company

Bata India is the largest retailer and leading manufacturer of footwear in India and is a part ofthe Bata Shoe Organization. Today, Bata India has established itself as India’s largestfootwear retailer. Its retail network of over 1200 stores gives it a reach / coverage that noother footwear company can match. The stores are present in good locations and can befound in all the metros, mini-metros and towns. The Company also operates a large non retaildistribution network through its urban wholesale division and caters to millions of customersthrough over 30,000 dealers.Investment Rationale:

Strong Brand recall: Bata being among the oldest shoe company in the country has astrong brand recall and is the most trusted name in the branded footwear segment.

Real estate Value: Developing 260 acre land in Batanagar in JV with Calcutta Metropolitanwhich is expected to be completed by 2013 and would further unlock value of Bata India.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 1549 915 429 1830

EBIDTA 404 148 56 296

PAT 259 89 32 180

EPS 40 14 5 28

Stock Details Rs in Cr

Dividend Yield 1%

Networth 543

Equity Capital 64

FV 10

PE (x) 43

Book Value 84

52 Week H/L 989/492

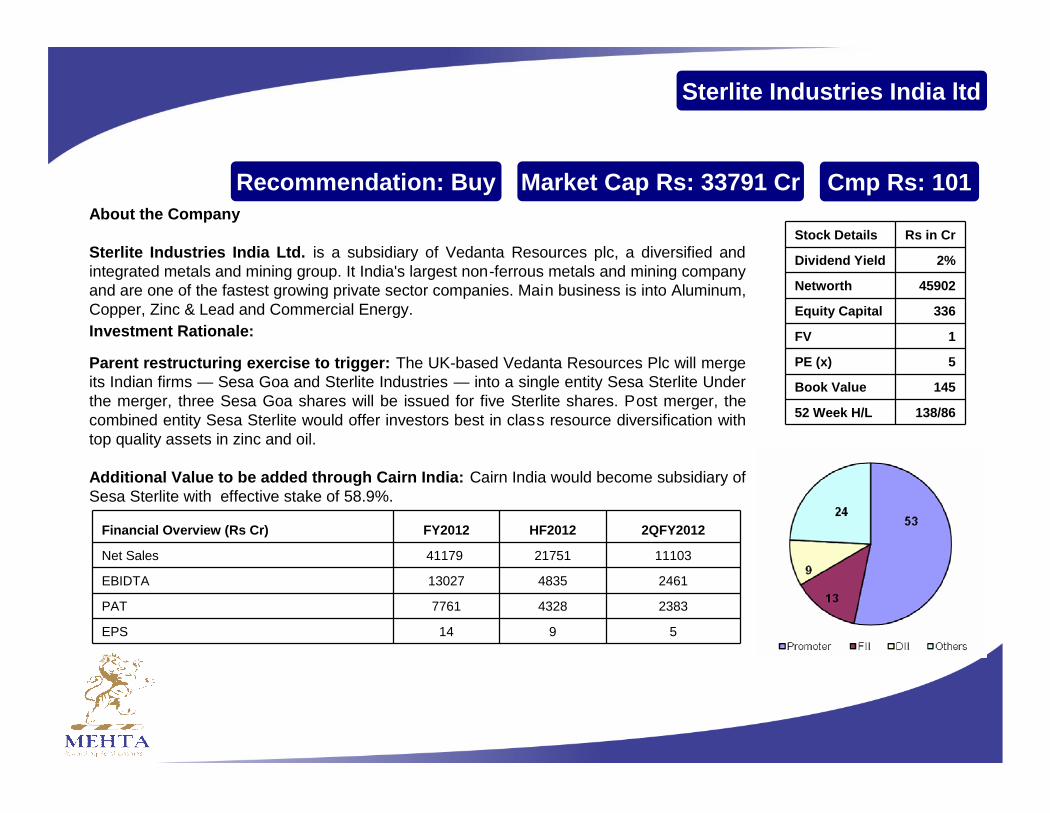

Sterlite Industries India ltd

Recommendation: Buy Market Cap Rs: 33791 Cr Cmp Rs: 101About the Company

Sterlite Industries India Ltd. is a subsidiary of Vedanta Resources plc, a diversified andintegrated metals and mining group. It India's largest non-ferrous metals and mining companyand are one of the fastest growing private sector companies. Main business is into Aluminum,Copper, Zinc & Lead and Commercial Energy.Investment Rationale:

Parent restructuring exercise to trigger: The UK-based Vedanta Resources Plc will mergeits Indian firms — Sesa Goa and Sterlite Industries — into a single entity Sesa Sterlite Underthe merger, three Sesa Goa shares will be issued for five Sterlite shares. Post merger, thecombined entity Sesa Sterlite would offer investors best in class resource diversification withtop quality assets in zinc and oil.

Additional Value to be added through Cairn India: Cairn India would become subsidiary ofSesa Sterlite with effective stake of 58.9%.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012

Net Sales 41179 21751 11103

EBIDTA 13027 4835 2461

PAT 7761 4328 2383

EPS 14 9 5

Stock Details Rs in Cr

Dividend Yield 2%

Networth 45902

Equity Capital 336

FV 1

PE (x) 5

Book Value 145

52 Week H/L 138/86

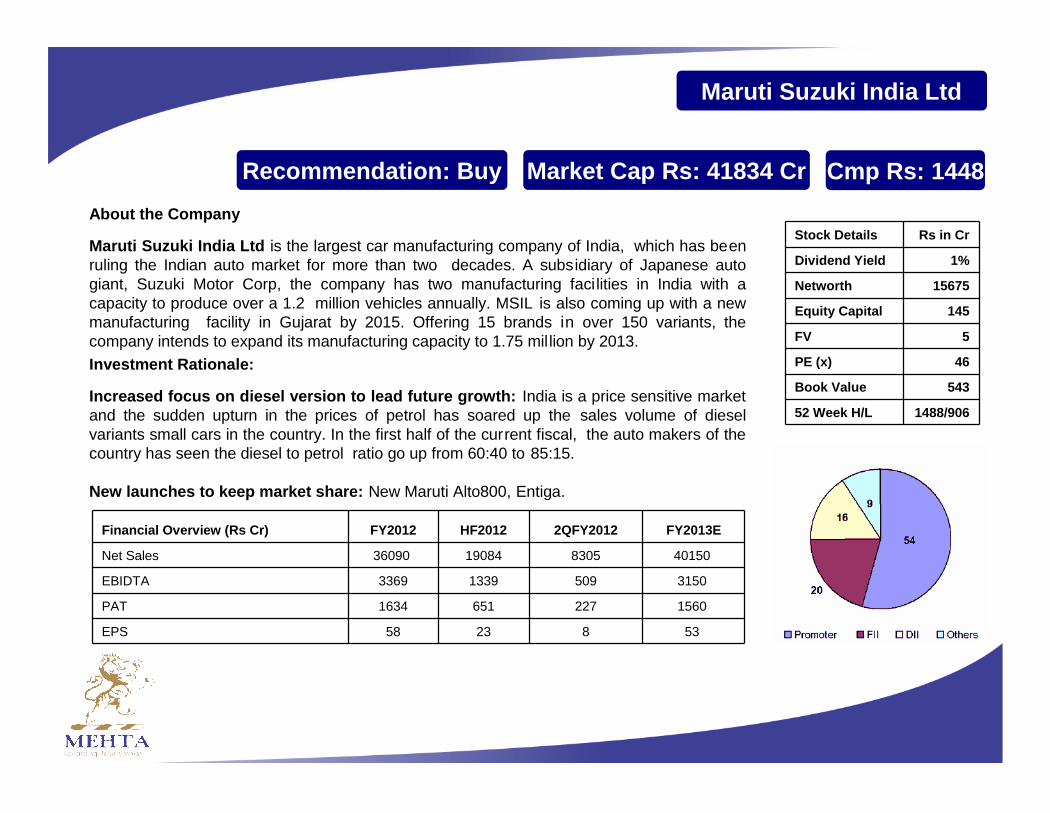

Maruti Suzuki India Ltd

Recommendation: Buy Market Cap Rs: 41834 Cr Cmp Rs: 1448About the Company

Maruti Suzuki India Ltd is the largest car manufacturing company of India, which has beenruling the Indian auto market for more than two decades. A subsidiary of Japanese autogiant, Suzuki Motor Corp, the company has two manufacturing facilities in India with acapacity to produce over a 1.2 million vehicles annually. MSIL is also coming up with a newmanufacturing facility in Gujarat by 2015. Offering 15 brands in over 150 variants, thecompany intends to expand its manufacturing capacity to 1.75 million by 2013.Investment Rationale:

Increased focus on diesel version to lead future growth: India is a price sensitive marketand the sudden upturn in the prices of petrol has soared up the sales volume of dieselvariants small cars in the country. In the first half of the current fiscal, the auto makers of thecountry has seen the diesel to petrol ratio go up from 60:40 to 85:15.

New launches to keep market share: New Maruti Alto800, Entiga.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 36090 19084 8305 40150

EBIDTA 3369 1339 509 3150

PAT 1634 651 227 1560

EPS 58 23 8 53

Stock Details Rs in Cr

Dividend Yield 1%

Networth 15675

Equity Capital 145

FV 5

PE (x) 46

Book Value 543

52 Week H/L 1488/906

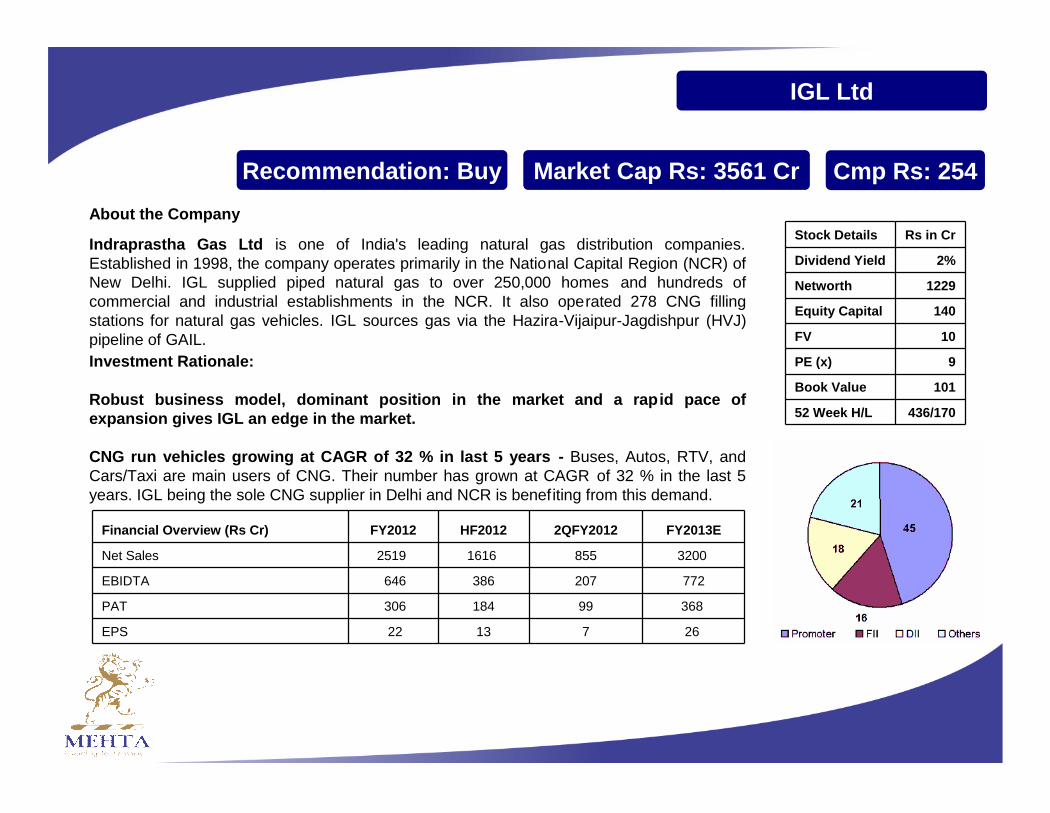

IGL Ltd

Recommendation: Buy Market Cap Rs: 3561 Cr Cmp Rs: 254About the Company

Indraprastha Gas Ltd is one of India's leading natural gas distribution companies.Established in 1998, the company operates primarily in the National Capital Region (NCR) ofNew Delhi. IGL supplied piped natural gas to over 250,000 homes and hundreds ofcommercial and industrial establishments in the NCR. It also operated 278 CNG fillingstations for natural gas vehicles. IGL sources gas via the Hazira-Vijaipur-Jagdishpur (HVJ)pipeline of GAIL.Investment Rationale:

Robust business model, dominant position in the market and a rapid pace ofexpansion gives IGL an edge in the market.

CNG run vehicles growing at CAGR of 32 % in last 5 years - Buses, Autos, RTV, andCars/Taxi are main users of CNG. Their number has grown at CAGR of 32 % in the last 5years. IGL being the sole CNG supplier in Delhi and NCR is benefiting from this demand.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012 FY2013E

Net Sales 2519 1616 855 3200

EBIDTA 646 386 207 772

PAT 306 184 99 368

EPS 22 13 7 26

Stock Details Rs in Cr

Dividend Yield 2%

Networth 1229

Equity Capital 140

FV 10

PE (x) 9

Book Value 101

52 Week H/L 436/170

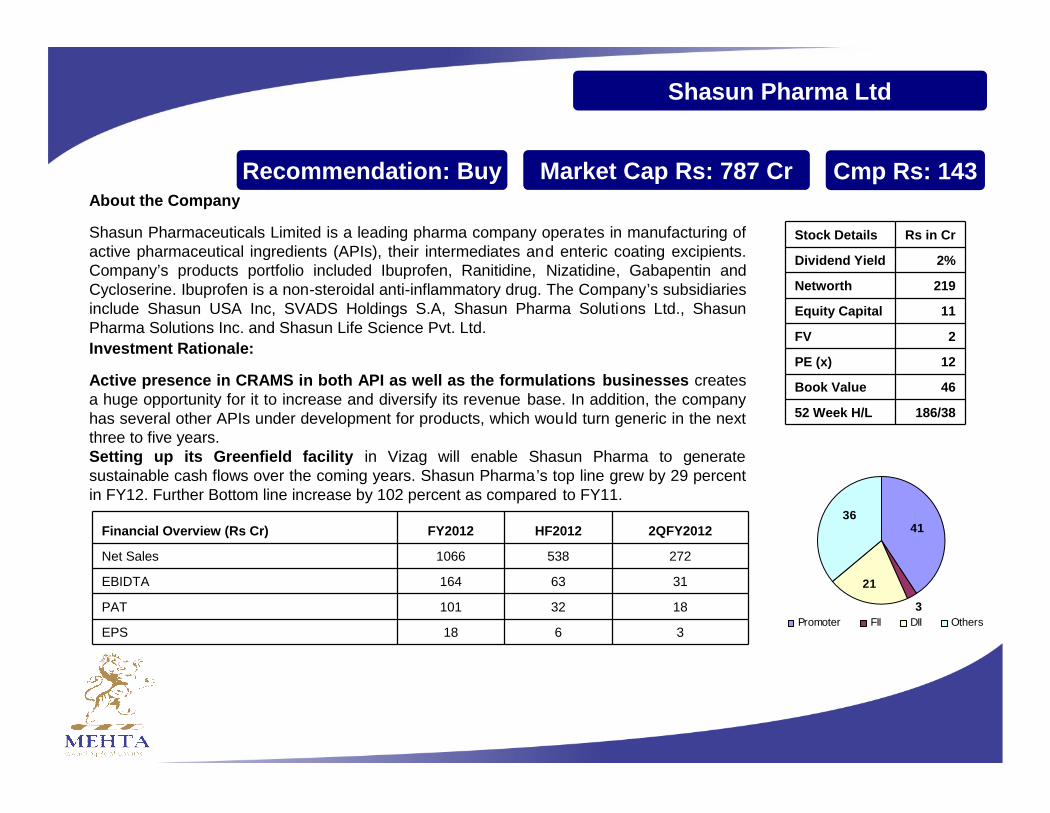

Shasun Pharma Ltd

Recommendation: Buy Market Cap Rs: 787 Cr Cmp Rs: 143About the Company

Shasun Pharmaceuticals Limited is a leading pharma company operates in manufacturing ofactive pharmaceutical ingredients (APIs), their intermediates and enteric coating excipients.Company’s products portfolio included Ibuprofen, Ranitidine, Nizatidine, Gabapentin andCycloserine. Ibuprofen is a non-steroidal anti-inflammatory drug. The Company’s subsidiariesinclude Shasun USA Inc, SVADS Holdings S.A, Shasun Pharma Solutions Ltd., ShasunPharma Solutions Inc. and Shasun Life Science Pvt. Ltd.Investment Rationale:

Active presence in CRAMS in both API as well as the formulations businesses createsa huge opportunity for it to increase and diversify its revenue base. In addition, the companyhas several other APIs under development for products, which would turn generic in the nextthree to five years.Setting up its Greenfield facility in Vizag will enable Shasun Pharma to generatesustainable cash flows over the coming years. Shasun Pharma’s top line grew by 29 percentin FY12. Further Bottom line increase by 102 percent as compared to FY11.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012

Net Sales 1066 538 272

EBIDTA 164 63 31

PAT 101 32 18

EPS 18 6 3

Stock Details Rs in Cr

Dividend Yield 2%

Networth 219

Equity Capital 11

FV 2

PE (x) 12

Book Value 46

52 Week H/L 186/38

3

36

21

41

Promoter FII DII Others

Aditya Birla Nuvo Ltd

Recommendation: Buy Market Cap Rs: 10727 Cr Cmp Rs: 945About the Company

Aditya Birla Nuvo Ltd, a part of Aditya Birla Group is a diversified business conglomeratewith business interest in insurance, mutual funds, other financial services, telecom, BPO, ITservices, garments, carbon black, fertilisers, textiles and insulators.

Investment Rationale:

1)Holds 25.31% stake in Idea Cellular, whichranks among the top 10 cellular operators inthe world and 3rd largest cellular operator inIndia.

2)Owns 50% of Birla Sun Life AssetManagement Company (BSAMC). BSAMC isthe 4th largest asset-management company inIndia.

Financial Overview (Rs Cr) FY2012 HF2012 2QFY2012

Net Sales 21840 11314 5992

EBIDTA 3290 1758 913

PAT 1010 649 342

EPS 78 57 27

Stock Details Rs in Cr

Dividend Yield 1%

Networth 7496

Equity Capital 114

FV 10

PE (x) 9

Book Value 715

52 Week H/L 1029/710

3) Madura Garments, a fashion & lifestyledivision, is the largest premium brandedapparel player in India with 1,129exclusive brand outlets spanning across1.6 million sq ft. Its power brands areLouis Philippe, Van Heusen, Allen Solly &Peter England.

4) Manufacturing vertical includes severalbusinesses such as Carbon Black (2ndlargest manufacturer in India.

18

18

13 51

Promoter FII DII Others

Products Available

Msearch Market Outlook… Msearch Picks for the day… Msearch Company Coverage for Investment… Msearch IPO Flash Notes… Msearch Quarterly Result Update… Msearch Event coverage update… Msearch Equity Portfolio

Team behind the performance

• CA Rakeshh Mehta (Chairman)• CA Prasant Bhansaali (Director)• Mr. Prashanth Tapse (AVP Research)• Mr. Pankaj Sharma (Research Analyst)• Mr Vinay Tiwari (Research Analyst)• M/s Pooja Jain (Research Analyst)

Thank You !Corporate Office: Mehta Group

612, Arun Chambers, Tardeo Road, Mumbai 400034Tel: +91 22 40070100, Fax: +91 22 40070102

Email: [email protected]: www.mehtagroup.in

Disclaimer: This presentation may contain confidential, proprietary or legally privileged information. It should not be used by any one who is not the original intended recipient. If you haveerroneously received this message, please delete it immediately and notify the sender. The recipient acknowledges that Mehta Group. is unable to exercise control or ensure or guarantee theintegrity of/over the contents of the information contained in e-mail transmission and further acknowledges that any views expressed in this messages are those of the individual sender anddoes not bind Mehta Group unless the sender does so expressly with due authority with Mehta Group. Neither Mehta Capital management Pvt. Ltd., nor its directors, employees, agents orrepresentatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with theuse of the information.