witan pacific investment trust plc...witan pacific investment trust 10 source: datastream (to...

TRANSCRIPT

WITAN PACIFIC INVESTMENT TRUST PLC

110th Annual General Meeting

June 2017

These slides are intended to highlight some key points about Witan Pacific Investment Trust plc, for

the use of shareholders, analysts and other professional investors. This material is for

informational purposes only and does not constitute a solicitation or a personal recommendation in

any jurisdiction.

No reliance may be placed for any purpose on the information and opinions contained in this document or

their accuracy or completeness. No part of this material may be copied, photocopied or duplicated in any

form or distributed to any person that is not an employee, officer, director or authorised agent of the

recipient, without Witan Investment Services Limited’s prior permission.

Important note: Please remember that past performance is not a guide to future performance. Witan

Pacific Investment Trust is an equity investment. The value of an investment and the income from it

can fall as well as rise as a result of currency and market fluctuations and you may not get back the

amount originally invested.

Issued and approved by Witan Investment Services Limited. Witan Investment Services Limited is

registered in England no.5272533 of 14 Queen Anne’s Gate, London SW1H9AA. The VAT registration

number for Witan Investment Services Limited is 863573889.Witan Investment Services Limited provides

investment products and services and is authorised and regulated by the Financial Conduct Authority.

MSCI information. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making)

any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of

any future performance analysis, forecast or prediction, The MSCI information is provided on an “as is” basis and the user of this information assumes

the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or

creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of

originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information.

Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive,

consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

DISCLAIMER

WITAN PACIFIC INVESTMENT TRUST 2

AGENDA

WITAN PACIFIC INVESTMENT TRUST 3

• Chair’s Overview

• Investment Review

‒ Manager video commentaries

‒ Summary from Witan Investment Services

• Question and answer discussion

• Formal business of the meeting

• Tea

CHAIR’S OVERVIEWSarah Bates

INVESTMENT OBJECTIVE

WITAN PACIFIC INVESTMENT TRUST 5

• To provide shareholders with long term capital and income growth from

a diversified portfolio of investments in the Asia Pacific region,

employing an active multi-manager approach

• To grow the dividend in real terms over the long term

• To outperform the MSCI AC Asia Pacific Index (£), the Company’s

benchmark

ORGANISATIONAL STRUCTURE

WITAN PACIFIC INVESTMENT TRUST 6

Aberdeen

Portfolio Managers

Board

Executive Manager

Service Providers

Matthews

Gavekal

Witan Pacific

Witan Investment

Services

CapitaCompany Secretary

JPMorganCustodian

BNP ParibasFund Accounting

PWCAuditors

FULL YEAR TO 31 JANUARY 2017

WITAN PACIFIC INVESTMENT TRUST 7

• NAV total return of 30.7%, compared with benchmark 35.3%

• Share price total return of 26.1%

• Outperformed in 8 out of the 12 financial years since becoming

multi-manager in May 2005

• Final dividend of 2.55p, making 4.75p for the full year (+2.2%)

• Net assets £217m (2016: £170m)

• NAV total return of 195.8% since the adoption of the multi-manager

approach in 2005, compared with 183.1% for the benchmark

Please see disclaimer on slide 2

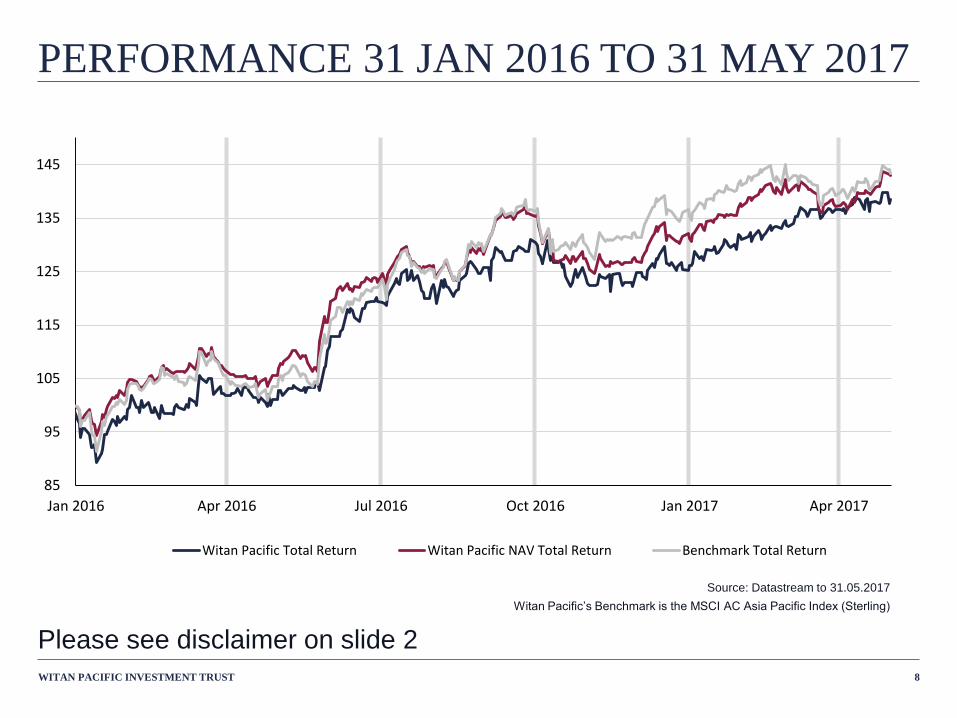

PERFORMANCE 31 JAN 2016 TO 31 MAY 2017

WITAN PACIFIC INVESTMENT TRUST 8

Source: Datastream to 31.05.2017

Witan Pacific’s Benchmark is the MSCI AC Asia Pacific Index (Sterling)

85

95

105

115

125

135

145

Jan 2016 Apr 2016 Jul 2016 Oct 2016 Jan 2017 Apr 2017

Witan Pacific Total Return Witan Pacific NAV Total Return Benchmark Total Return

Please see disclaimer on slide 2

• Final dividend of 2.55p,

making 4.75p for full year

• 2.2% increase over previous

year (CPI 1.8%)

• 12 consecutive years of

dividend growth

• The regular dividend is 4.5

times that paid in 2005

• Revenue reserves are circa

3 times annual dividend

WITAN PACIFIC DIVIDEND RECORD

WITAN PACIFIC INVESTMENT TRUST 9

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Regular dividend Special dividend

Policy – The Company aims to grow the

dividend in real terms over the long term

Source: Witan Pacific

Please see disclaimer on slide 2

DISCOUNT AND SHARE BUYBACKS (TO 31.05.2017)

WITAN PACIFIC INVESTMENT TRUST 10

Source: Datastream (to 31.05.2017)

• Discount widened in 2016 due to market volatility and Brexit uncertainty, pace of buybacks

increased in response to the widening discount

• 713,979 shares repurchased in the financial year to 31 Jan 2017

• 1.6m shares repurchased in the current financial year at discounts between 11% and 17%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Witan Pacific Discount (30 day average)

Please see disclaimer on slide 2

INVESTMENT REVIEWJames Hart, Investment Director

Witan Investment Services

HIGHLIGHTS FROM THE FINANCIAL YEAR

WITAN PACIFIC INVESTMENT TRUST 12

• Fluctuating hopes for economic growth which improved over the year

• Improved sentiment in Asia and particularly in emerging markets as

commodity prices recovered

• Asian corporate earnings showing signs of improvement

• Significant political shocks from the Brexit vote, US Presidential election and

South Korean impeachment

• Global interest rates appear to have troughed as economic policy edges

towards targeting tax cuts and investment spending

• These macro factors drove stock market rotation which made life difficult for

the majority of active managers, including our own

MANAGER STRUCTURE (AS AT 31.01.2017)

WITAN PACIFIC INVESTMENT TRUST 13

Annualised performance is since inception excludes cash balances held centrally by Witan Pacific

Gavekal returns are adjusted for 1.5% annual management fee charged within the

UCITS OEIC, of which 0.75% is rebated to the Company directly outside the fund.

Portfolio Manager

(inception)% managed

Performance

12m

Benchmark

12m

Annualised

Performance

Annualised

Benchmark

Performance

Aberdeen

(31.05.05)43.4 +39.2 +35.3 +11.4 +9.3

Matthews

(30.04.12)46.4 +28.4 +35.3 +13.3 +11.3

Gavekal

(24.04.12)10.2 +22.3 +35.3 +10.1 +11.5

TRUST PERFORMANCE 31st MAY 2005 to 31st JANUARY 2017

Cumulative

NAV TR

Cumulative

Benchmark

Annualised

NAV TR

Annualised

Benchmark

Total return

(since 31.05.05)100.0 +195.8 +183.1 +9.7% +9.3%

Source: WM Performance Services/Morningstar

All performance to 31.01.2017

Please see disclaimer on slide 2

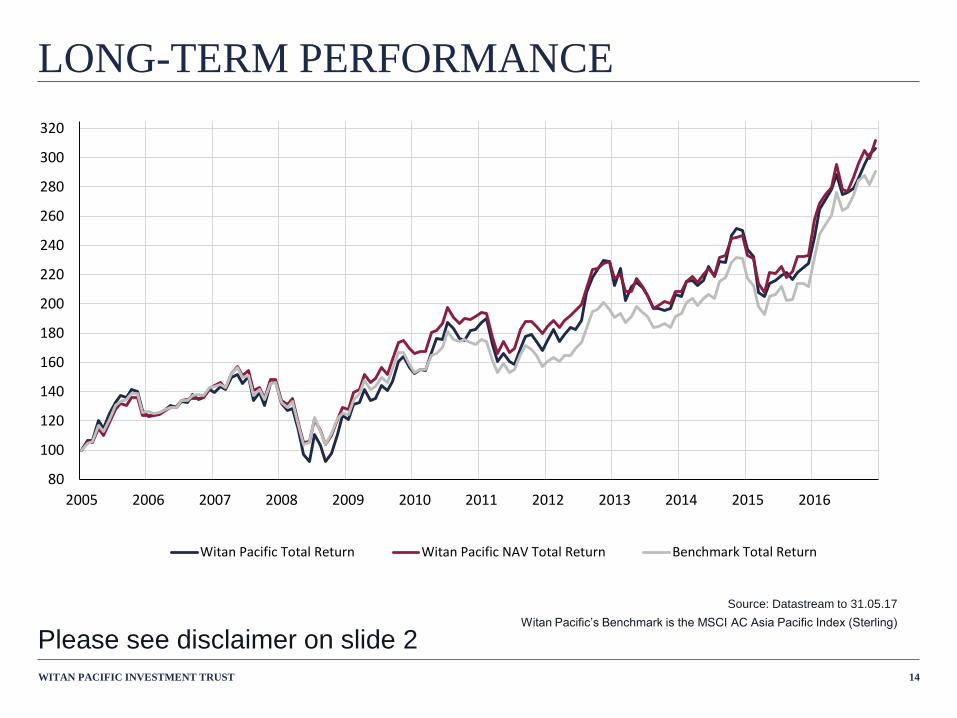

LONG-TERM PERFORMANCE

WITAN PACIFIC INVESTMENT TRUST 14

Source: Datastream to 31.05.17

Witan Pacific’s Benchmark is the MSCI AC Asia Pacific Index (Sterling)

80

100

120

140

160

180

200

220

240

260

280

300

320

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Witan Pacific Total Return Witan Pacific NAV Total Return Benchmark Total Return

Please see disclaimer on slide 2

RELATIVE PERFORMANCE

WITAN PACIFIC INVESTMENT TRUST 15

Source: Datastream to 31.05.17

Witan Pacific’s Benchmark is the MSCI AC Asia Pacific Index (Sterling)

95

100

105

110

115

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

NAV Relative to benchmark

Please see disclaimer on slide 2

TOP 20 INVESTMENTS…

WITAN PACIFIC INVESTMENT TRUST 16

% %

1 Samsung Electronics 2.8 11 LG Chemical 1.3

2 Japan Tobacco 2.3 12 Shin-Etsu Chemical 1.3

3 Taiwan Semiconductor 2.3 13 Mitsubishi UFJ Financial Group 1.3

4 HSBC 2.1 14 Singapore Tech Engineering 1.2

5 Minth Group 2.0 15 Keyence Corp 1.2

6 Seven & I Holdings 1.7 16 AIA Group 1.2

7 China Mobile 1.6 17 Fanuc 1.2

8 United Overseas Bank 1.6 18 Sumitomo Mitsui Financial Group 1.2

9 BGF Retail Company 1.6 19 Sinopec 1.1

10 Shenzhou International 1.4 20 CapitaLand 1.0

By size of investment as a proportion of Witan Pacific’s overall portfolio

On a look through basis across managers, excluding open-end funds

Source: BNP Paribas as at 31 May 2017

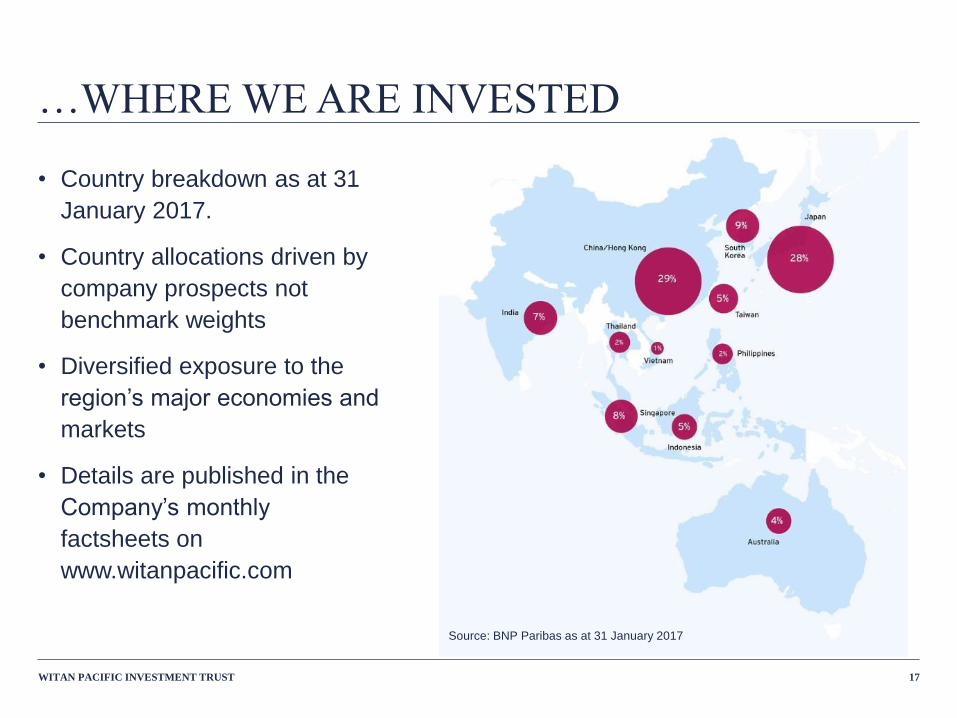

…WHERE WE ARE INVESTED

WITAN PACIFIC INVESTMENT TRUST 17

• Country breakdown as at 31

January 2017.

• Country allocations driven by

company prospects not

benchmark weights

• Diversified exposure to the

region’s major economies and

markets

• Details are published in the

Company’s monthly

factsheets on

www.witanpacific.com

Source: BNP Paribas as at 31 January 2017

REGIONAL PROSPECTS

WITAN PACIFIC INVESTMENT TRUST 18

• Home to 60% of the world’s population, a high standard of education, economic transition. Increased interdependence across the region

• Asian economic ‘miracle’ driven by a high rate of investment and productivity leading to increasing consumption and savings

• Political change accelerating, should lead to improved public governance, improved shareholder rights and a more business-friendly environment

• Chinese slowdown is part of a long-term trend and evolution from a low cost producer to a service economy

• Japan showing signs of life following unprecedented monetary policy action to boost the domestic economy

Please see disclaimer on slide 2

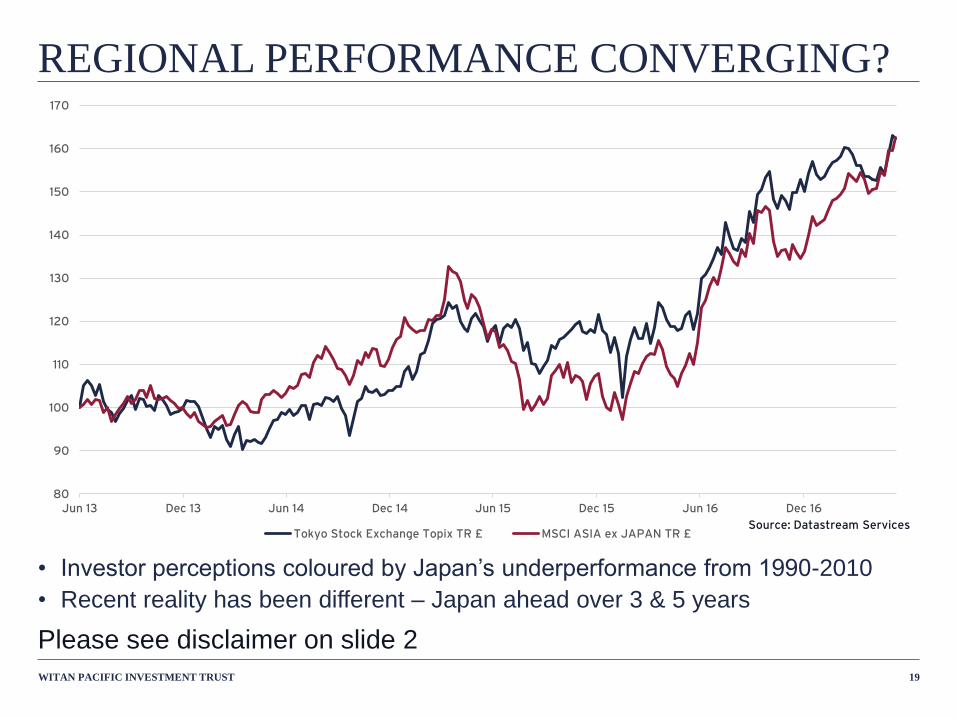

REGIONAL PERFORMANCE CONVERGING?

Source: Datastream Services

WITAN PACIFIC INVESTMENT TRUST 19

• Investor perceptions coloured by Japan’s underperformance from 1990-2010

• Recent reality has been different – Japan ahead over 3 & 5 years

80

90

100

110

120

130

140

150

160

170

Jun 13 Dec 13 Jun 14 Dec 14 Jun 15 Dec 15 Jun 16 Dec 16

Tokyo Stock Exchange Topix TR £ MSCI ASIA ex JAPAN TR £

Please see disclaimer on slide 2

CURRENT FINANCIAL YEAR

WITAN PACIFIC INVESTMENT TRUST 20

• Outperforming year to date. NAV total return (at 9 June) 11.9%, ahead of

Benchmark 8.8%. Share price total return 13.8%

• Discount to NAV has narrowed but remains at a relatively wide level

• Share repurchase activity has increased

• Asian markets have generally performed well so far this year. Japan has

underperformed its regional peers

• Sterling exchange rates will continue to be influenced by Brexit negotiations and

the UK political environment – especially after the General Election

Please see disclaimer on slide 2

SUMMARY

WITAN PACIFIC INVESTMENT TRUST 21

• Objective: to outperform the regional index in total return terms and deliver real

income growth

• Managers actively select investments independent of benchmark weightings

• Record of dividend growth and total return outperformance since the

inception of the multi-manager strategy in 2005

• Year to 31 January 2017: A volatile but rewarding period for equity investors in

Asia. Sterling weakness provided a boost to capital values for UK investors

whilst relative performance was more difficult

• Outlook: An encouraging start to the current year. Regional prospects driven by

economic and corporate earnings growth. Attractive (absolute and relative)

valuations. Political reform leads to investor friendly environment. Fears of

protectionism probably overdone

Please see disclaimer on slide 2

LONGER-TERM PERSPECTIVE

WITAN PACIFIC INVESTMENT TRUST 22

Source: Morningstar

All performance for the discrete years to 31.03.17

TR= Total Return

Individual years to end-Mar 2017 2016 2015 2014 2013

MSCI AC Asia Pacific Index TR [A] 34.6 -6.4 22.3 -4.7 15.9

Witan Pacific Share Price TR 33.2 -10.1 26.2 -12.5 25.0

Witan Pacific NAV TR [B] 31.1 -5.0 20.9 -10.2 18.0

Relative NAV performance [B-A] -3.5 1.4 -1.4 -5.4 2.1

Over 10 years (May 2007 to May 2017): NAV total return of 119.0% and a share

price return of 116.6%, compared with the benchmark’s 103.2%.

Please see disclaimer on slide 2

THANKYOU

WITAN PACIFIC INVESTMENT TRUST

SUMMARY OF PROXY VOTES 2017

WITAN PACIFIC INVESTMENT TRUST 24

Resolution Votes Cast Total Votes For plus

DiscretionFor Against Discretion Withheld Total Cast

(excluding

withheld)

134,748,670 6,140 80,725 16,207 34,835,535 34,829,395

234,764,622 3,135 80,725 3,260 34,848,482 34,845,347

334,231,397 395,543 81,537 143,264 34,708,477 34,312,934

434,202,906 368,367 81,537 198,931 34,652,810 34,284,443

534,501,809 146,494 80,885 122,553 34,729,188 34,582,694

633,881,927 791,878 80,725 97,211 34,754,530 33,962,652

734,615,404 70,882 80,931 84,524 34,767,217 34,696,335

834,007,402 423,687 80,931 339,721 34,512,020 34,088,333

934,377,094 312,287 80,931 81,429 34,770,312 34,458,025

1034,590,905 159,857 80,931 20,047 34,831,693 34,671,836

1134,183,619 568,724 77,438 21,961 34,829,781 34,261,057

SUMMARY OF PROXY VOTES

WITAN PACIFIC INVESTMENT TRUST 25

Total Shares in Issue = 65,944,000

Total Voting Rights = 63,410,9431

Percentage of Shares Voted = 54.94%2

1 Voting rights as at 12 June 2017. Voting rights exclude shares

held in treasury.

2 Percentage based on validly received proxy votes prior to the

meeting in respect of Resolution 1.