wk health cluster hugh yarrington member executive board november 5, 2002 philadelphia

TRANSCRIPT

WK Health Cluster

Hugh Yarrington Member Executive Board

November 5, 2002 Philadelphia

2

Agenda Agenda

9:30 – 10:00 Global Strategy - Hugh Yarrington

10:00 – 11:00 Strategy in-depth - Christopher Ainsley + Q&A

11:00 – 11:15 Coffee break

11:15 – 12:15 Business Unit Strategies - CEOs

12:15 – 13:30 Lunch

13:30 – 16:30 Break-out sessions: Product demos

16:30 – 16:45 Closing Remarks – Hugh Yarrington

3

Health Cluster – The Story Today

New Strategy to Focus on HealthNew Strategy to Focus on Health

Divestment of KAP (E 600 mln)Divestment of KAP (E 600 mln)

New Structure to Leverage Health AssetsNew Structure to Leverage Health Assets

Roll-out Product Development 2002-05Roll-out Product Development 2002-05

IT & Organizational SynergiesIT & Organizational Synergies

Development of Clinical Tools Growth BusinessDevelopment of Clinical Tools Growth Business

Pursue Uncontested No 1 StatusPursue Uncontested No 1 Status

4

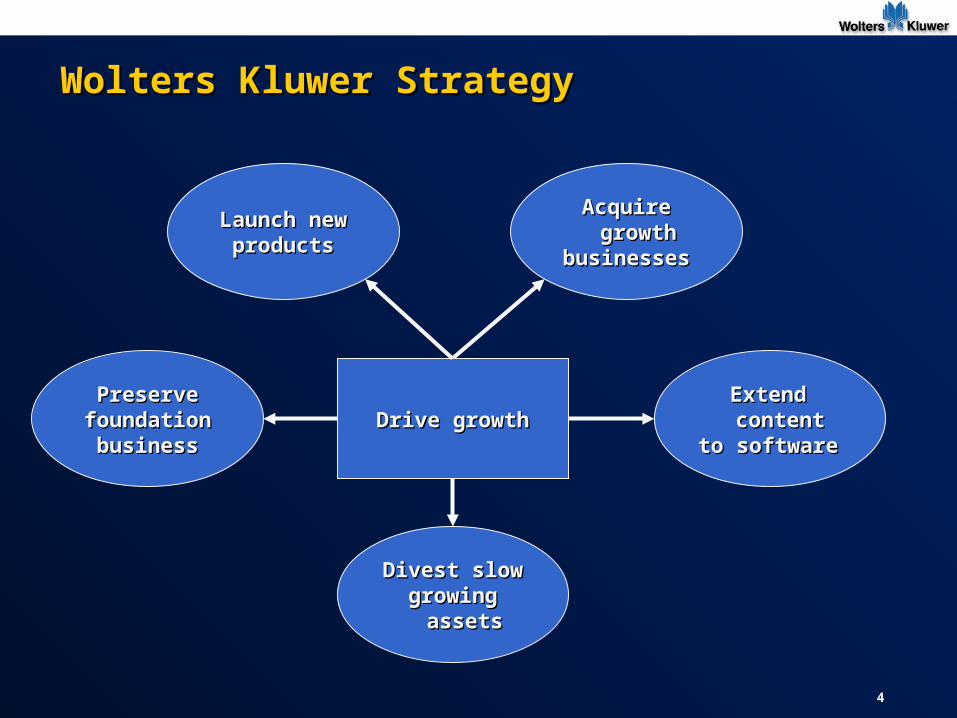

Wolters Kluwer StrategyWolters Kluwer Strategy

Drive growthDrive growth

Launch newLaunch newproductsproducts

Divest slowDivest slowgrowing assetsgrowing assets

Extend contentExtend contentto softwareto software

PreservePreservefoundationfoundationbusinessbusiness

Acquire growthAcquire growthbusinessesbusinesses

5

Launch New Products

HY-I 2001 HY-I 2002

Fiscal Advice Journal: internet tool Fiscal Advice Journal: internet tool enabling customers to send tailor-made enabling customers to send tailor-made newsletters to their clients, The newsletters to their clients, The NetherlandsNetherlands

Legal Announcements and Formalities: a Legal Announcements and Formalities: a workflow tool, Franceworkflow tool, France

CCH Securities Compliance tracker: a CCH Securities Compliance tracker: a daily news service on securities rules and daily news service on securities rules and regulations, CCH USregulations, CCH US

All Health cluster content loaded onto Ovid All Health cluster content loaded onto Ovid platformplatform

Redaktion D, on line language course, Redaktion D, on line language course, Germany (joint venture with Goethe Germany (joint venture with Goethe Institute)Institute)

Revenues from new products Revenues from new products (EUR mln)(EUR mln)

68.868.881.181.1

Selected examples Selected examples

New products are launchedNew products are launchedin the past 12 monthsin the past 12 months

+18%+18%

6

Acquire Growth Businesses…Acquire Growth Businesses…

Emphasis onEmphasis onacquiring strongacquiring strongsoftware companiessoftware companiesin growing marketsin growing markets

ArtelArtel

CiceronCiceron

Compliance ToolsCompliance Tools

ICCICC

Moorehouse BlackMoorehouse Black

UniformUniform

Val InformatiqueVal Informatique

AverageAverageprojectedprojectedgrowth rate ofgrowth rate ofrevenues is revenues is 17% p.a.17% p.a.

Selected examples of HY-I acquisitionsSelected examples of HY-I acquisitions

7

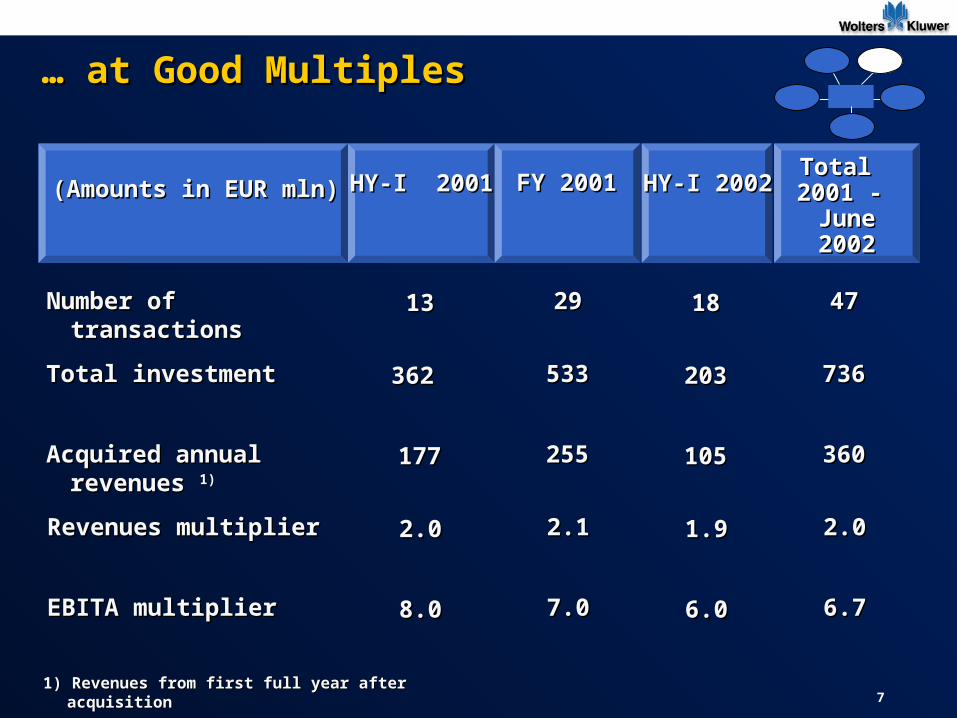

TotalTotal2001 - 2001 -

June 2002June 2002

… … at Good Multiplesat Good Multiples

HY-I 2001HY-I 2001 HY-I 2002HY-I 2002

Number of transactionsNumber of transactions

Total investmentTotal investment

Acquired annual revenuesAcquired annual revenues 1)1)

Revenues multiplierRevenues multiplier

EBITA multiplierEBITA multiplier

1313

362 362

177177

2.02.0

8.08.0

2929

533533

255255

2.12.1

7.07.0

(Amounts in EUR mln)(Amounts in EUR mln)

1818

203203

105105

1.91.9

6.06.0

4747

736736

360360

2.02.0

6.76.7

FY 2001FY 2001

1) Revenues from first full year after acquisition1) Revenues from first full year after acquisition

8

Extend Content to SoftwareExtend Content to Software

Total revenues per business type (%)Total revenues per business type (%)

HY-I 2001HY-I 2001 HY-I 2002HY-I 2002

100%100%

Revenue increase year on year (%)Revenue increase year on year (%)

Static contentStatic content

Dynamic contentDynamic content

Smart toolsSmart tools

IntegratedIntegratedsolutionssolutions

100%100%

48.048.0

34.134.1

12.412.4

5.55.5

44.444.4

36.036.0

13.013.0

6.66.6

Static contentStatic content

Dynamic contentDynamic content

Smart toolsSmart tools

IntegratedIntegratedsolutionssolutions

1515

1313

2929

11

ContinuingContinuingrevenuerevenue

Total continuingTotal continuingrevenue (EUR M.)revenue (EUR M.)

1,6001,600 1,7471,747

99

9

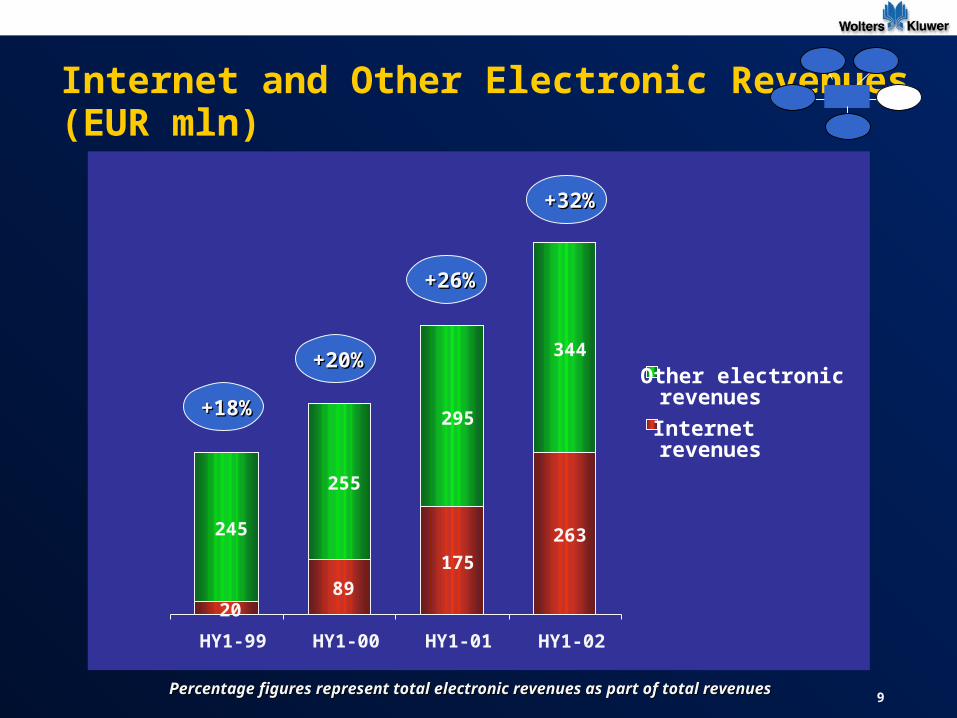

Internet and Other Electronic Revenues (EUR mln)

2089

175

263245

255

295

344

HY1-99 HY1-00 HY1-01 HY1-02

Other electronicrevenues

Internetrevenues

Percentage figures represent total electronic revenues as part of total revenuesPercentage figures represent total electronic revenues as part of total revenues

+32%+32%

+26%+26%

+20%+20%

+18%+18%

10

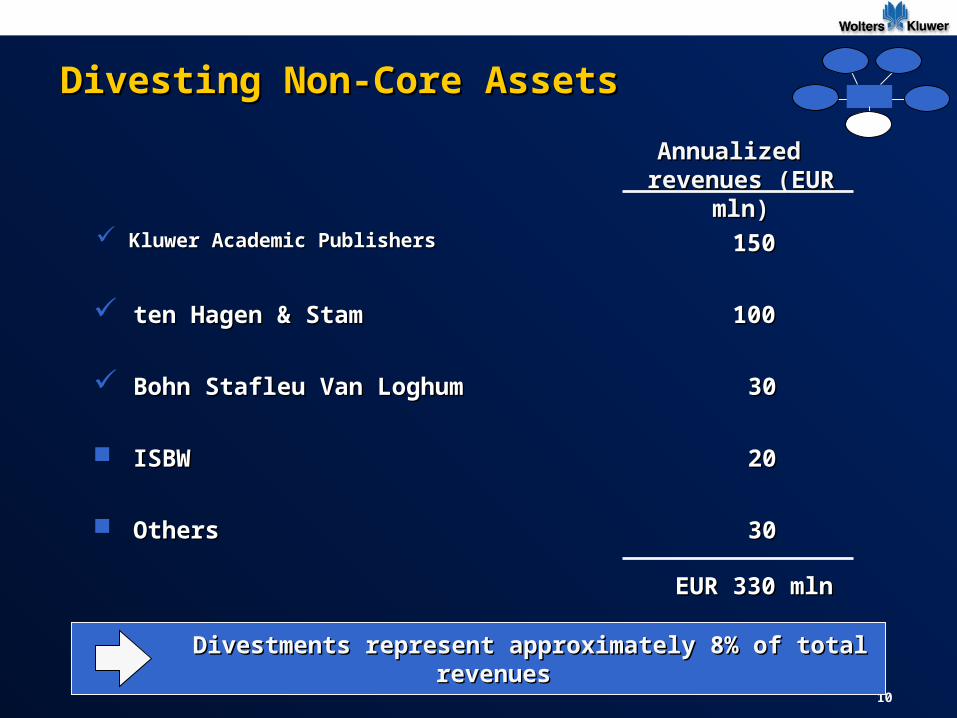

Divesting Non-Core AssetsDivesting Non-Core Assets

Kluwer Academic PublishersKluwer Academic Publishers

ten Hagen & Stamten Hagen & Stam

Bohn Stafleu Van LoghumBohn Stafleu Van Loghum

ISBWISBW

OthersOthers

Annualized revenues Annualized revenues (EUR mln)(EUR mln)

115050

3030

2020

3030

EUR 3EUR 3330 mln0 mln

100100

Divestments represent approximately 8% of total revenuesDivestments represent approximately 8% of total revenues

11

Preserve Foundation BusinessPreserve Foundation Business

Implement retention/loyalty programs Implement retention/loyalty programs

Increase effectiveness of sales and marketing Increase effectiveness of sales and marketing Sales force restructuring/reinforcementSales force restructuring/reinforcement CRMCRM

Pursue value driven pricing policiesPursue value driven pricing policies

Enhance product qualityEnhance product quality

12

Wolters Kluwer Health: Financial Results

EUR mln

RevenuesRevenues EBITAEBITA MarginMargin

Organic growth improved to 7% (as at 1H 2002)Organic growth improved to 7% (as at 1H 2002)

58103

372

298

HY-I 2001 HY-I 2002

4751

HY-I 2001 HY-I 2002

ElectronicRevenues

15.7

13.7

HY-I 2001 HY-I 2002

+25%+25% +9%+9% (20%)(20%)

13

Wolters Kluwer Health: Strategic FocusWolters Kluwer Health: Strategic Focus

Reorganize to serve health and medical professionalsReorganize to serve health and medical professionals Four customer-facing business units createdFour customer-facing business units created New CEOs and management teams in placeNew CEOs and management teams in place Marketing approach and channels rationalized Marketing approach and channels rationalized Back office and systems work scheduled for 2002/3Back office and systems work scheduled for 2002/3

Divest non-conforming assetsDivest non-conforming assets KAP purchase agreement signedKAP purchase agreement signed

Revitalize textbook, research, institutional research businessesRevitalize textbook, research, institutional research businesses Improved society, author, and distributor relationships Increased investment in new product development Improved distributor contacts Reduced cycle times

14

Wolters Kluwer Health: Strategic Focus, cont.Wolters Kluwer Health: Strategic Focus, cont.

Ovid is and “open platform” and the “health and medical” leaderOvid is and “open platform” and the “health and medical” leader Number of “A” titlesNumber of “A” titles Number of medical titlesNumber of medical titles Number of publishing partnersNumber of publishing partners Monthly growth in total titles Monthly growth in total titles Number of page viewsNumber of page views Number of end-usersNumber of end-users Market penetration (segment, national, international)Market penetration (segment, national, international) Spend per purchaserSpend per purchaser Spend per userSpend per user

Accelerate clinical tools developmentAccelerate clinical tools development Medi-Span provides great opportunitiesMedi-Span provides great opportunities Market for clinical tools about to explodeMarket for clinical tools about to explode

Increase growth organically and by acquisitionIncrease growth organically and by acquisition Organic revenue growth at 7% (as at 1H 2002)Organic revenue growth at 7% (as at 1H 2002) Acquisition program in place and actively pursuing target companiesAcquisition program in place and actively pursuing target companies

16

Health Is an Attractive Market for Wolters KluwerHealth Is an Attractive Market for Wolters Kluwer

A large market Approximately $4.0bn Roughly 40% of the global STM market

A growing market Underlying growth of 2-5%. More rapid expansion in pharmaceutical, clinical tools, payors and allied health

Additional growth opportunities through market share gains Consolidation in traditional segments: ~50% of the market controlled by small

players

Suited to our strengths Concentrated in the US (65% of revenues) Largely English-language (85% of revenue)

Largely distinct from the Scientific/Technical market Content, Authors, Societies, Libraries and End-users

17

Our Vision

Become the global leader in information for

health and medical professionals

Focus on Pharma Solutions, Medical Research, Professional and Education, and Clinical Tools

Primary customers: English reading professionals globally

PhysiciansNursesMedical StudentsNursing StudentsAllied Health Professionals (e.g.

physical therapists, chiropractors)PharmacistsMedical Schools/Teaching hospitals

Community hospitals Pharmaceutical Sales and Marketing Pharmaceutical Research Biotech and Biomedical Research Medical Device companies Payors Institutional Science (focused on medical and

health-related science)

Markets served

18

Our Vision: What’s Changing

Medicine and Health Electronic-centric Organized by customer groups Ovid: Key component of the

strategy Clinical Tools: New business unit

with critical mass Pharma: Concentrated Objective: Leadership of

defendable segment

Science, Technical and Medicine Print-centric Organized by operating companies Ovid: Extension of publishing

Clinical Tools: Opportunistic venture Pharma: Scattered Objective: Participation in broad

markets

TODAY & TOMORROWYESTERDAY

19

Customer-Facing Business Units

Old Business Units

Adis

Ovid/Silver Platter

LWW-Medical

LWW-Education

Facts & Comparisons/ Medi-Span

KAP

Markets Served

• Pharmaceutical Sales and Pharmaceutical Sales and MarketingMarketing

• Pharmaceutical ResearchPharmaceutical Research• Biotech ResearchBiotech Research• Medical Device CompaniesMedical Device Companies

• Medical Schools/Teaching Medical Schools/Teaching hospitalshospitals

• Community hospitalsCommunity hospitals• Biomedical ResearchBiomedical Research

• PhysiciansPhysicians• NursesNurses• Allied HealthAllied Health• Medical, Nursing and Allied Medical, Nursing and Allied

Health StudentsHealth Students• Institutional ScienceInstitutional Science

• PharmacistsPharmacists• Pharmacy StudentsPharmacy Students• PayorsPayors

New Business Units

Pharma Solutions

Medical Research

Professional and Education

Clinical Tools

Divested

20

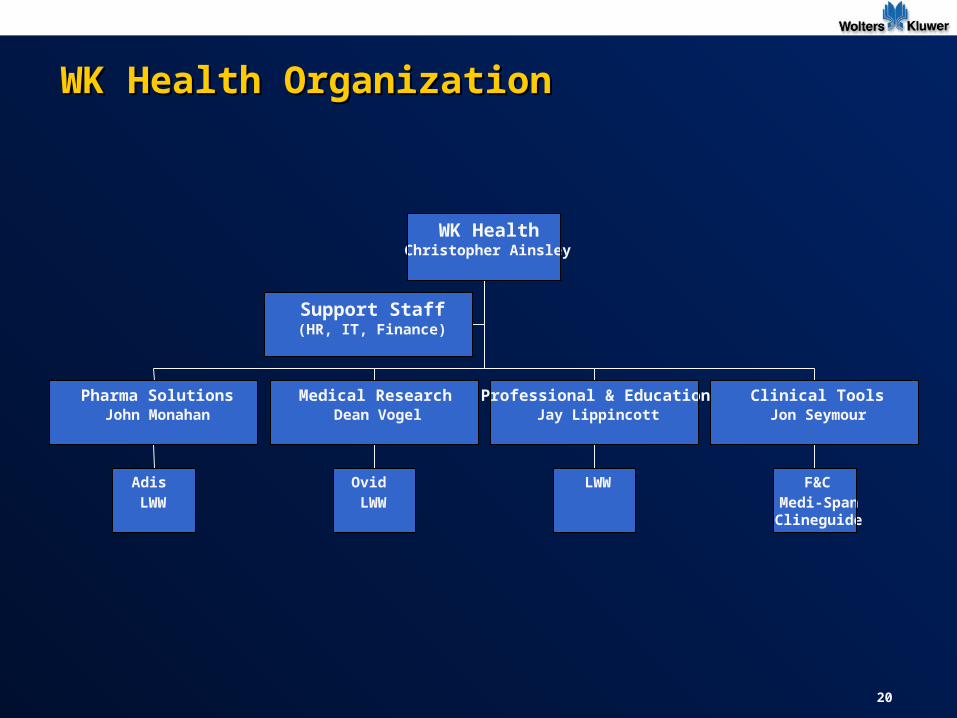

WK Health OrganizationWK Health Organization

Support Staff(HR, IT, Finance)

Adis LWW

Pharma SolutionsJohn Monahan

Ovid LWW

Medical ResearchDean Vogel

LWW

Professional & EducationJay Lippincott

F&CMedi-SpanClineguide

Clinical ToolsJon Seymour

WK HealthChristopher Ainsley

21

WK Health: 2002(E) Business Unit Revenues

Clinical ToolsClinical Tools

Pharma Pharma SolutionsSolutions

Professional Professional & Education& Education

Medical Medical ResearchResearch

Total WK Health: Total WK Health: ~ $730 Million~ $730 Million

~ $320 Million~ $320 Million

~$60 Million~$60 Million

~ $120 Million~ $120 Million

~ $230 Million~ $230 Million

22

WK Health: 2002(E) Business Unit FTEs

Clinical ToolsClinical Tools

Pharma Pharma SolutionsSolutions

Professional Professional & Education& Education

Medical Medical ResearchResearch

Total WK Health:Total WK Health: ~2,390 FTEs ~2,390 FTEs

~ 710 FTEs~ 710 FTEs

~ 240 FTEs~ 240 FTEs

~ 570 FTEs~ 570 FTEs

~ 870 FTEs~ 870 FTEs

23

WK Health: 2002(E) Print/Electronic Revenue Mix

050

100150200250300350

Med

Res

earc

h

Pro

ffes

ion

al&

Ed

uca

tio

n

Ph

arm

a

Cli

nic

alT

oo

ls

Electronic Print Other

$ i

n M

illi

on

s

24

Implementing Our StrategyImplementing Our Strategy

Reorganize to focus on health and medical Reorganize to focus on health and medical

Expand our portfolio of top medical contentExpand our portfolio of top medical content

Increase market share in medical research Increase market share in medical research

Accelerate development of clinical toolsAccelerate development of clinical tools

Revitalize core text and reference businessRevitalize core text and reference business

Grow pharmaceutical sales by restructuring and acquiringGrow pharmaceutical sales by restructuring and acquiring

Increase growth organically and by acquisitionIncrease growth organically and by acquisition

25

Reorganize to Focus on Health and MedicalReorganize to Focus on Health and Medical

Leadership: Recruited and developed strong leadership team

Processes: Improved the way we work together Finance Technology Human Resources

Implementation Teams: Task forces targeting growth opportunities Global Medical Research Professional and Education Pharmaceuticals Clinical Tools

Values, Behavior & Culture: Developed common values to establish new culture and drive change in strategy

26

Expand Our Portfolio of Top Medical Content

Achievements

Renewed AHA journal contract = $185 million Renewed AHA journal contract = $185 million Licensed 171 new titles from six publishers including 15 “A” titlesLicensed 171 new titles from six publishers including 15 “A” titles Moved all owned content to Ovid PlatformMoved all owned content to Ovid Platform

Next Steps

Pursue all “A” medical content for online platform Pursue all “A” medical content for online platform

Rationale

Provide the “must-have” content on the preferred platformProvide the “must-have” content on the preferred platform Aggregate databases and content from many publishersAggregate databases and content from many publishers

27

Increase Market Share in Medical Research

Achievements

Introduced new Introduced new content content packages and new pricing Ovid platform achieved a 62% increase in Internet usage and a 35%

increase in peak concurrent users

Next Steps

Manage customer migration from print to online with the right pricing and Manage customer migration from print to online with the right pricing and content packagescontent packages

Further penetrate international and community hospital marketsFurther penetrate international and community hospital markets

Rationale

Reinforce our leadership in institutional research segments Reinforce our leadership in institutional research segments Support WK Health goal of expanding role in electronic distribution of contentSupport WK Health goal of expanding role in electronic distribution of content

28

Accelerate Clinical Tools Development

Achievements

Medi-Span acquired 2002 – integrating F&C and Medi-Span Medi-Span acquired 2002 – integrating F&C and Medi-Span New CEO named 9/02; preliminary strategy identifiedNew CEO named 9/02; preliminary strategy identified

Next Steps

Develop disease management and drug information business strategy Develop disease management and drug information business strategy Complete integrated data tool; exit FDB editorial agreementComplete integrated data tool; exit FDB editorial agreement Explore acquisitions and partnership opportunitiesExplore acquisitions and partnership opportunities

Rationale

Place multiple “bets” in evolving clinical tools marketPlace multiple “bets” in evolving clinical tools market With multiple interests at the point of care, need to embed/integrate WK With multiple interests at the point of care, need to embed/integrate WK

Health content in more general systemsHealth content in more general systems

29

Revitalize Core Text & Reference BusinessRevitalize Core Text & Reference Business

Achievements

Established new management teamEstablished new management team Created market focused organization – improving relationshipsCreated market focused organization – improving relationships

Next Steps

Investing in market research to drive customer-focused product Investing in market research to drive customer-focused product developmentdevelopment

Developing stronger relationships with distributors, authors, and Developing stronger relationships with distributors, authors, and customerscustomers

Rationale

Near-term stronger performance depends on sourcing of top content and Near-term stronger performance depends on sourcing of top content and developing stronger relationships with customersdeveloping stronger relationships with customers

Longer term, books will have significant value as an element of our Longer term, books will have significant value as an element of our clinical tools strategyclinical tools strategy

30

Growth and Restructuring in Pharma

Achievements

New CEO named 8/02New CEO named 8/02 Acquisition plan developed Acquisition plan developed Restructuring business to improve market penetration and leverage Restructuring business to improve market penetration and leverage

strengths and assetsstrengths and assets

Next Steps

Complete key acquisitionsComplete key acquisitions Continue development of new electronic productsContinue development of new electronic products

Rationale

Pharma companies need to get products to market faster to maximize Pharma companies need to get products to market faster to maximize returns returns

Opportunity to establish strategic leadership by leading an aggressive Opportunity to establish strategic leadership by leading an aggressive industry consolidation campaignindustry consolidation campaign

31

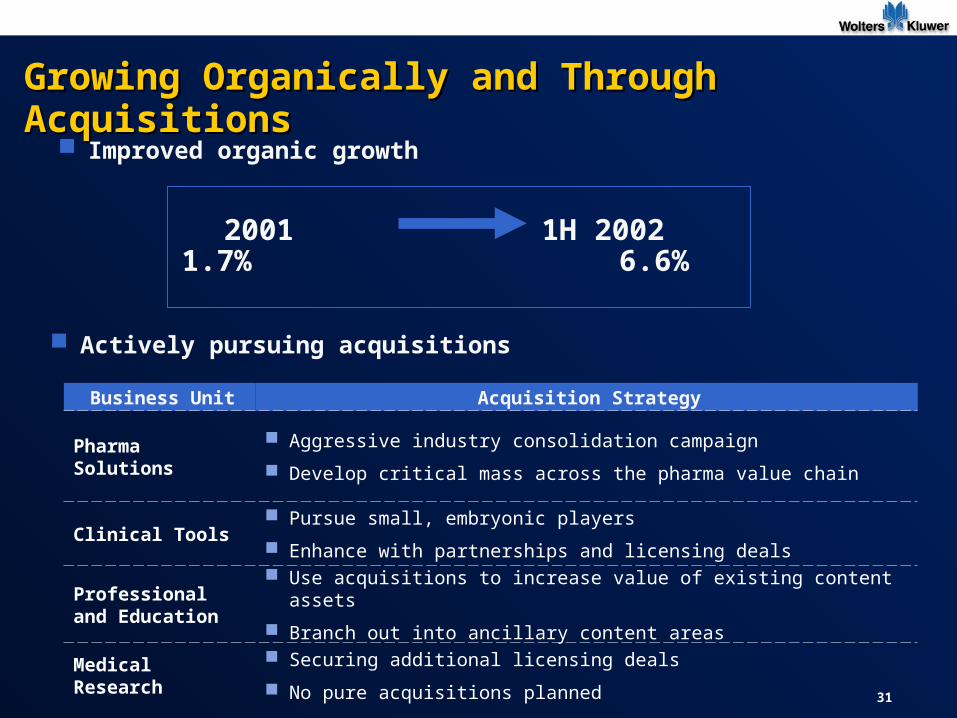

Growing Organically and Through AcquisitionsGrowing Organically and Through Acquisitions

Improved organic growth

2001 1H 2002 1.7% 6.6%

Actively pursuing acquisitions

Business Unit Acquisition Strategy

Pharma Solutions Aggressive industry consolidation campaign

Develop critical mass across the pharma value chain

Clinical Tools Pursue small, embryonic players

Enhance with partnerships and licensing deals

Professional and Education

Use acquisitions to increase value of existing content assets

Branch out into ancillary content areas

Medical Research Securing additional licensing deals

No pure acquisitions planned

32

WK Health: Key Strengths & Challenges

Strengths

Strong proprietary content

Strong pipeline of electronic products

Excellent brands & market position

Revitalized and focused management team

Recurring revenue business model

Large and growing market segments

Challenges

Building a customer-focused organization

Rebuilding our critical processes and systems

34

Market OverviewMarket Overview

Medical Research combines the premiere clinical journals of LWW with the leading online medical platform at Ovid

Target Market & Size

Focus on information managers, clinicians, medical and student researchers purchasing through institutions: medical libraries, biomedical research facilities, teaching and community hospitals

U.S. institutional medical market is approximately $1.8 billion and growing approximately 5%

Key Trends

Institutional libraries represent the majority of medical information spending

Trends in medical information spending suggest that the share of institutional buying is likely to grow in the future

As customers migrate online, there is an opportunity to capture spend

English remains the “lingua franca” of medical research creating a global medical marketplace

35

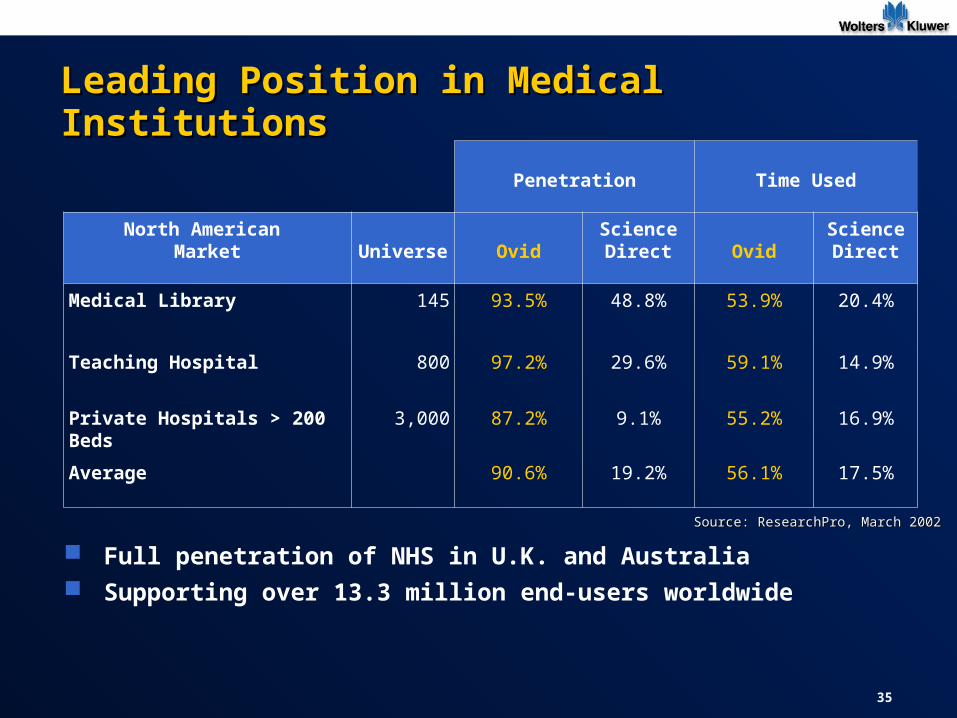

Leading Position in Medical InstitutionsLeading Position in Medical Institutions

Penetration Time Used

North American Market Universe Ovid

ScienceDirect Ovid

ScienceDirect

Medical Library 145 93.5% 48.8% 53.9% 20.4%

Teaching Hospital 800 97.2% 29.6% 59.1% 14.9%

Private Hospitals > 200 Beds 3,000 87.2% 9.1% 55.2% 16.9%

Average 90.6% 19.2% 56.1% 17.5%

Full penetration of NHS in U.K. and Australia Supporting over 13.3 million end-users worldwide

Source: ResearchPro, March 2002Source: ResearchPro, March 2002

36

Leading Source of Medical ContentLeading Source of Medical ContentDec 31,

2001 September 30, 2002ScienceDirect

September 30, 2002

Live Live%

Increase

Bibliographic Abstracts136.5 Mln 150.8 Mln 10.5% 30.0 Mln

Full Text Journals

“A” List Titles 74 98 32.5% 73

Other Medical Titles 459 725 58.0% 478

Total Medical Titles 533 824 54.6% 551

Book Content 102 168 64.7% 0

Greatest breadth of content through bibliographic layer Greatest depth of medical content through full text journals Unique addition of book content Completed loading of all LWW content on the Ovid platform

37

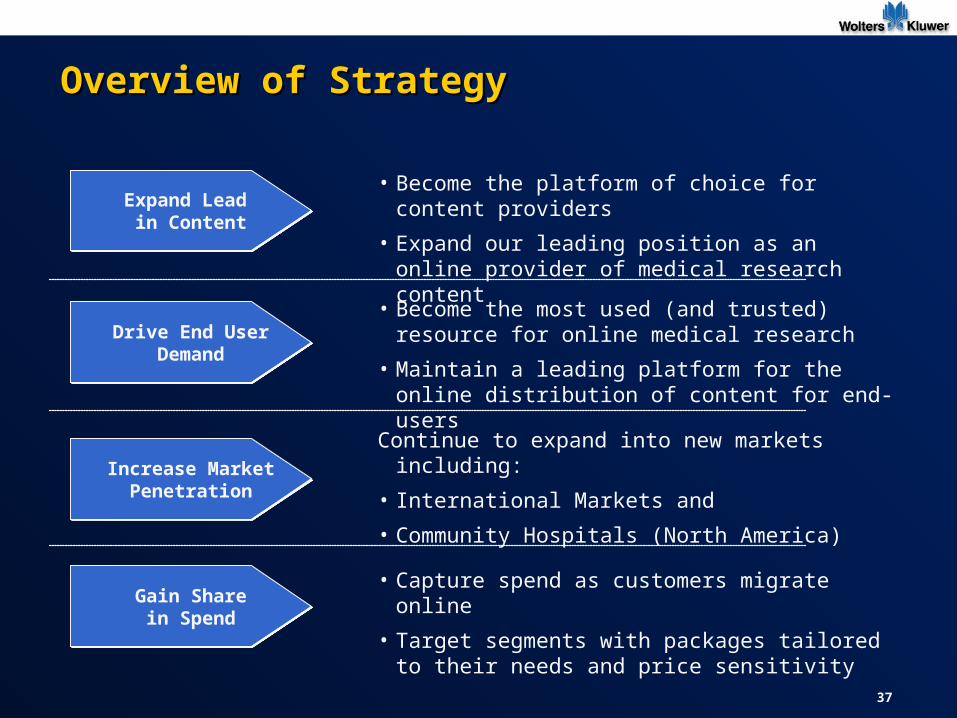

Overview of StrategyOverview of Strategy

Gain Sharein Spend

Gain Sharein Spend

Expand Lead in Content

Expand Lead in Content

• Become the platform of choice for content providers

• Expand our leading position as an online provider of medical research content

Increase MarketPenetration

Increase MarketPenetration

Drive End UserDemand

Drive End UserDemand

• Become the most used (and trusted) resource for online medical research

• Maintain a leading platform for the online distribution of content for end-users

Continue to expand into new markets including:

• International Markets and

• Community Hospitals (North America)

• Capture spend as customers migrate online

• Target segments with packages tailored to their needs and price sensitivity

38

SilverPlatter IntegrationSilverPlatter Integration

Progress Report

Consolidation of SilverPlatter and Ovid sales forces and product management organizations

Migrated to a single fulfillment system with a single view of customer base

Enabled cross-selling of content across platforms

Consolidated all areas of operations including finance, accounting, customer service and technical support

Relaunched brand – “Energize Your Thinking”

Strategic Benefits

Created leadership position in the medical market

Expanded local sales presence in key international markets

Provided an installed customer base for the sale of full text content

39

Implementing the StrategyImplementing the Strategy

Gain Sharein Spend

Gain Sharein Spend

• Implemented account planning process to identify additional spend opportunities through customer profiles

• Completed customer segmentation of Ovid customer base• Captured LWW print spend to accelerate online migration through

bundled pricing incentives

Expand Lead in Content

Expand Lead in Content

• All LWW content loaded onto the Ovid platform• Increased number of “A” list journals by 32.5% to 98• Increased total number of journals by 54.6% to 824• Increased book content by 64.7% to 168

Increase MarketPenetration

Increase MarketPenetration

• Leveraged local sales offices to penetrate the international clinical marketplace – first success in Germany/Sweden

• Created content packages focused on penetrating the community hospital market in the United States

Drive End UserDemand

Drive End UserDemand

• Increase of 35% on number of concurrent users (4,100) • Increase of 62% in page views to 152 million• Numerous software feature releases focused on end-user

functionality including Ovid@Hand and PIN Support

Accomplishments

40

Summary

Medical Research has the leading online platform (Ovid) in the medical market as defined by penetration and usage

The combination of the LWW publishing program and third party licensing skills enable a rapid expansion of content offerings

A deeper integration of the LWW and Ovid organizations will enable WK to more fully leverage our market position

Ovid and SilverPlatter have been fully integrated within twelve months of the SilverPlatter acquisition

41

Medical Research – Product Demo

Patti Corbett, Vice President, Marketing and Customer Development

Will discuss and demonstrate Ovid's Web-based biomedical information solutions for information professionals and clinicians

43

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

VISION

To be the dominant and most trusted healthcare information provider to individuals in all global markets and for all stages

of their professional development

KEY STRATEGIES

Implement and practice a customer-focused approach throughout the unit, including the extensive use of market research

Work collaboratively with other WK Health units to fully exploit our high-quality content through all media and all channels

Publish more successful first editions in targeted markets and increase market share of product revisions

Strengthen management of key sales channels, i.e., direct marketing, international, and wholesale/retail

Continue to concentrate on (print) base business, but also expand program of electronic solutions

44

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

MARKET OVERVIEWProfessional & Education serves individual customers in Medicine,

Nursing, and the Health Professions

Medicine Physicians and Medical Students US Market Size = $500 Million WK Health Share = 20% Growth Rate = 2-3% Primary Competitors: Elsevier, McGraw-Hill, UpToDate

Nursing Nurses and Nursing Students US Market Size = $200 Million WK Health Share = 55% Growth Rate = 3-5% Primary Competitors: Elsevier, Thomson

Health Professions Various Allied Health Professionals and Students US Market Size = $150 Million WK Health Share = 20% Growth Rate = 7+% Primary Competitors: Elsevier, Thomson

45

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

MARKET TRENDS Market dominated by Elsevier and Wolters Kluwer

Selected markets are growing – student enrollments in nursing and the health professions, and nursing professionals

Other markets are flat – medical education and practice

Customers want up-to-date information

Student markets are being negatively impacted by used textbooks and sharing of resources

Customers are looking for print and electronic product combinations

Rapid growth in PDA handheld products

46

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

PRODUCT OVERVIEW 4,000 Textbooks and Reference Titles

375 New Books Published Each Year

60 Periodicals

50 Electronic Products, Including PDAs

TOP PRODUCTS Nursing 2002

American Journal of Nursing

Brunner & Suddarth’s Textbook of Medical Surgical Nursing, 9th Edition

Cancer: Principles and Practice of Oncology, 6th Edition

Clinically Oriented Anatomy, 4th Edition

47

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

IMPLEMENTING THE STRATEGY: WHERE WE ARE

Created market-focused organization structure

Established new management team

Improved relationships with key wholesalers

Implemented market research program to drive product development

Reallocated resources to growth areas

Working cooperatively with other WK Health units to maximize

exploitation of content and increase development of new print and

electronic products

48

PROFESSIONAL & EDUCATIONPROFESSIONAL & EDUCATION

SUMMARY

Print business remains important to customers and WK Health

Collaboration with other WK Health units will lead to improved results

Wealth of high-quality content assets presents significant opportunity

to WK Health

A customer-focused organization and operation will lead to improved

product development and increased sales

49

PROFESSIONAL & EDUCATION

PRODUCT DEMOS

Jim Ryan, Vice President, Medicine

Will explain and demonstrate Professional & Education’s PDA program for medical practitioners

Diana Mason, Editor-in-Chief, American Journal of Nursing

Will describe Professional & Education’s market-leading nursing periodical publishing program and how the Springhouse acquisition has been successfully integrated and increased our strength in the market

51

Pharma Solutions

VISION

Become the leading provider of communications and information solutions to the global pharmaceutical, biotech,

and medical device industries

KEY STRATEGIES

Focus on Pharmaceuticals, Biotechnology, and Medical Device companies

Develop Greater Depth & Breadth Across the Product Life Cycle

Move From Purchased Data to Suite of Flexible Solutions

Aggressive Acquisition & Expansion Plan

52

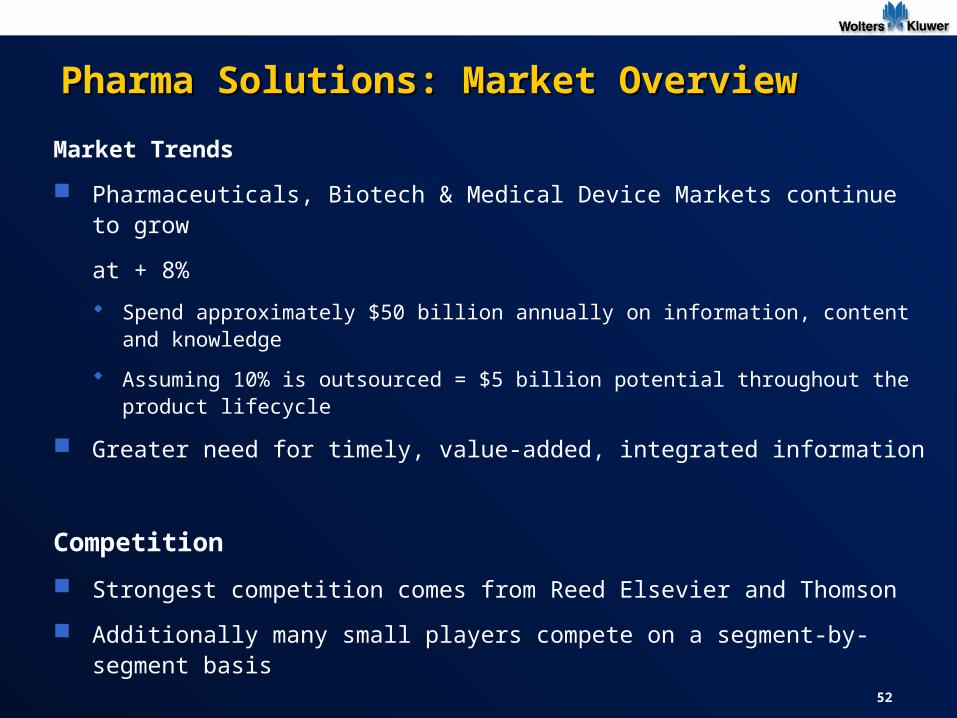

Pharma Solutions: Market OverviewPharma Solutions: Market Overview

Market Trends

Pharmaceuticals, Biotech & Medical Device Markets continue to grow

at + 8%

Spend approximately $50 billion annually on information, content and knowledge

Assuming 10% is outsourced = $5 billion potential throughout the product lifecycle

Greater need for timely, value-added, integrated information

Competition

Strongest competition comes from Reed Elsevier and Thomson

Additionally many small players compete on a segment-by-segment basis

53

Pharma Solutions: OpportunitiesPharma Solutions: Opportunities

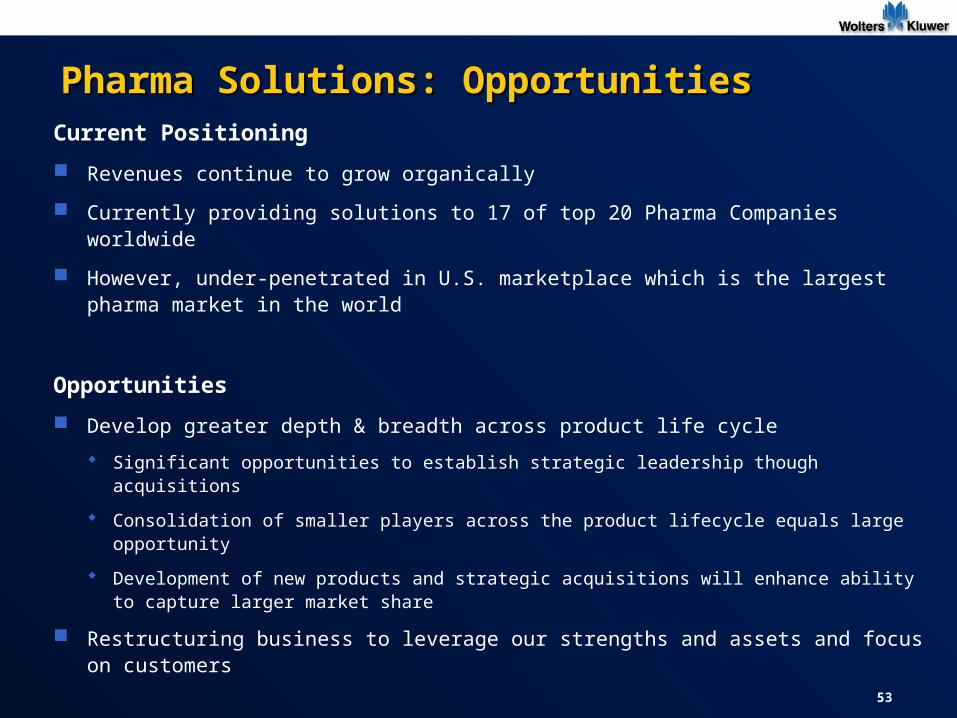

Current Positioning

Revenues continue to grow organically

Currently providing solutions to 17 of top 20 Pharma Companies worldwide

However, under-penetrated in U.S. marketplace which is the largest pharma market in the world

Opportunities

Develop greater depth & breadth across product life cycle

Significant opportunities to establish strategic leadership though acquisitions

Consolidation of smaller players across the product lifecycle equals large opportunity

Development of new products and strategic acquisitions will enhance ability to capture larger market share

Restructuring business to leverage our strengths and assets and focus on customers

54

Pharma Solutions: Strengthening Depth & Breadth Across Product Life Cycle

COMMUNICATIONS PLANNING TOOLS

VA

LU

E

STRATEGIC REPORTS HEALTHCARE COMMUNICATIONS

RDI CME

SUPPLEMENTS REPRINTS

SUBSCRIPTIONS JOURNALS

DISCOVERY CLINICAL TRIALS PRE-LAUNCH LAUNCH POST LAUNCH

CTI

55

Pharma Solutions: ProductsPharma Solutions: Products

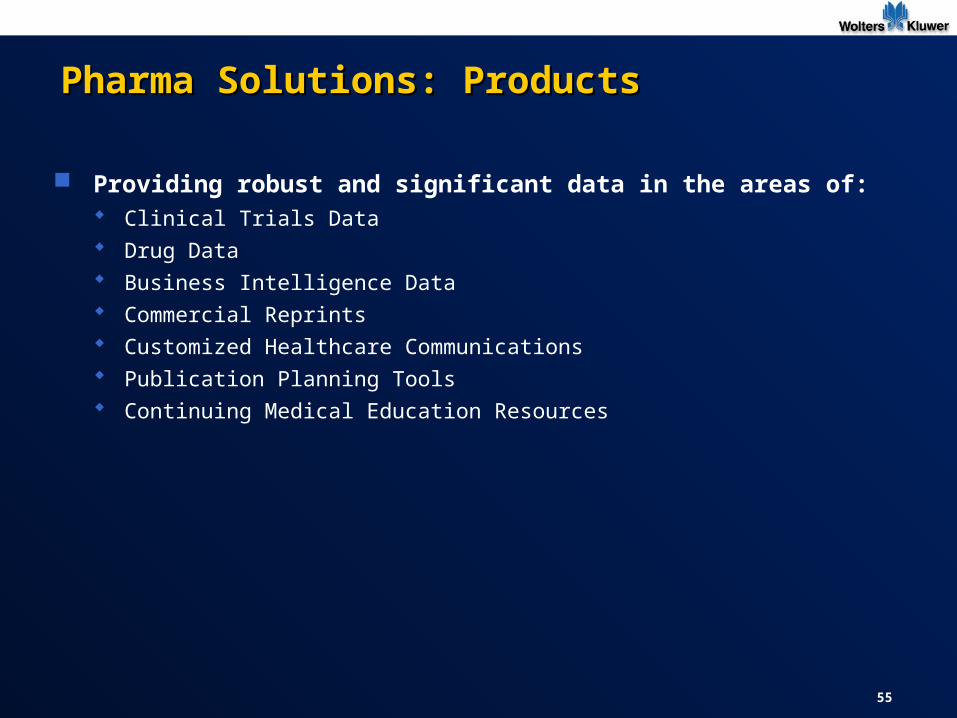

Providing robust and significant data in the areas of: Clinical Trials Data Drug Data Business Intelligence Data Commercial Reprints Customized Healthcare Communications Publication Planning Tools Continuing Medical Education Resources

56

Implementing the Strategy: Where we are

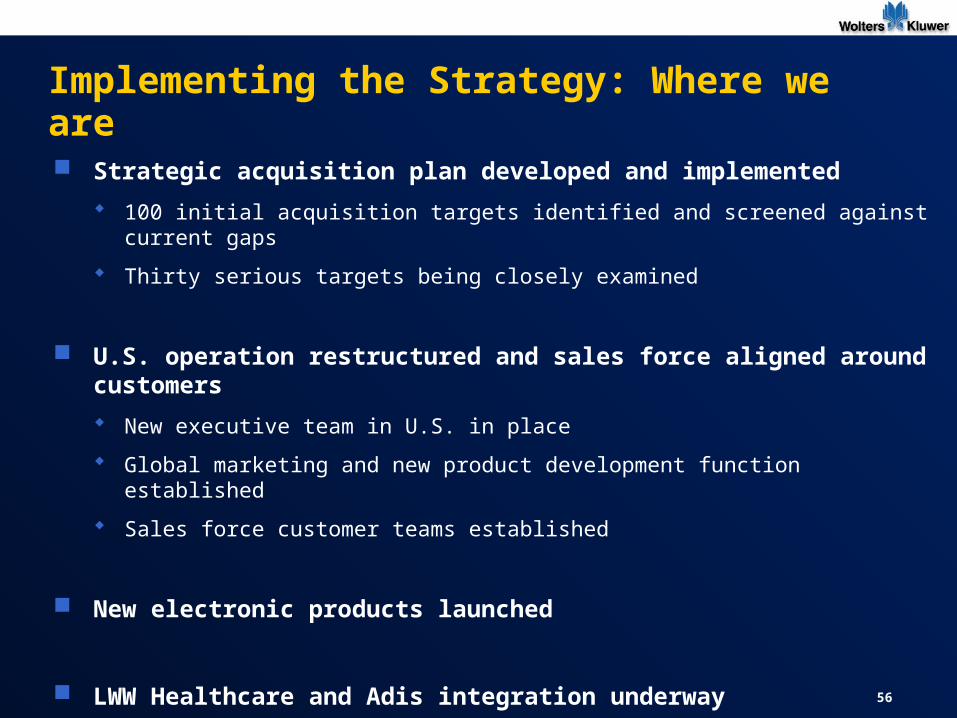

Strategic acquisition plan developed and implemented

100 initial acquisition targets identified and screened against current gaps

Thirty serious targets being closely examined

U.S. operation restructured and sales force aligned around customers

New executive team in U.S. in place

Global marketing and new product development function established

Sales force customer teams established

New electronic products launched

LWW Healthcare and Adis integration underway

57

Pharma Solutions: Summary

Combined LWW and ADIS International to form Pharma Solutions, a

strong global solution provider

History of strong organic growth

Commitment to develop greater depth and breadth across the product

lifecycle through new product development and acquisitions

Penetration into US marketplace is a priority

Move from data provider to suite of flexible solutions

58

Pharma Solutions: Product Demos

John Monahan, CEO, Pharma Solutions

John Starzewski, Vice President, Strategic Marketing Services

Will describe and demonstrate, several of the Pharma Solutions core offerings,

including: Clinical Trials Insight R & D Insight AdisZenith Publication Planning Tool

60

Clinical Tools: Focus and Guiding Principles Clinical Tools: Focus and Guiding Principles

Focus Forward-looking unit focused on the application of emerging technologies to

healthcare information needs Dramatic growth opportunities will exist -- our goal is to lead Timing: understanding state of technology and market forces is critical First example: e-prescribing

Guiding Principles Technology will inexorably creep out to the front lines of healthcare…to the

clinicians The breakthrough products for clinicians have not yet been made Print products should be derivatives of electronic products, not vice-versa Collaboration between Clinical Tools and other business units creates unique

potential We will need to innovate and take risks

61

Clinical Tools: Current Product LinesClinical Tools: Current Product Lines

Three synergistic organizations being integrated into one Three synergistic organizations being integrated into one working groupworking group

Referential drug info <--> Integrated drug info <--> Integrated Referential drug info <--> Integrated drug info <--> Integrated disease infodisease info

62

Clinical Tools: Vision Clinical Tools: Vision

Deliver tools to healthcare professionals that make them “information professionals”

Reduce medical errors…and capitalize on that financially!

Disease-centric decision support

Distance learning

“Digital human”

Attention to medical device industry in addition to pharmaceutical industry

63

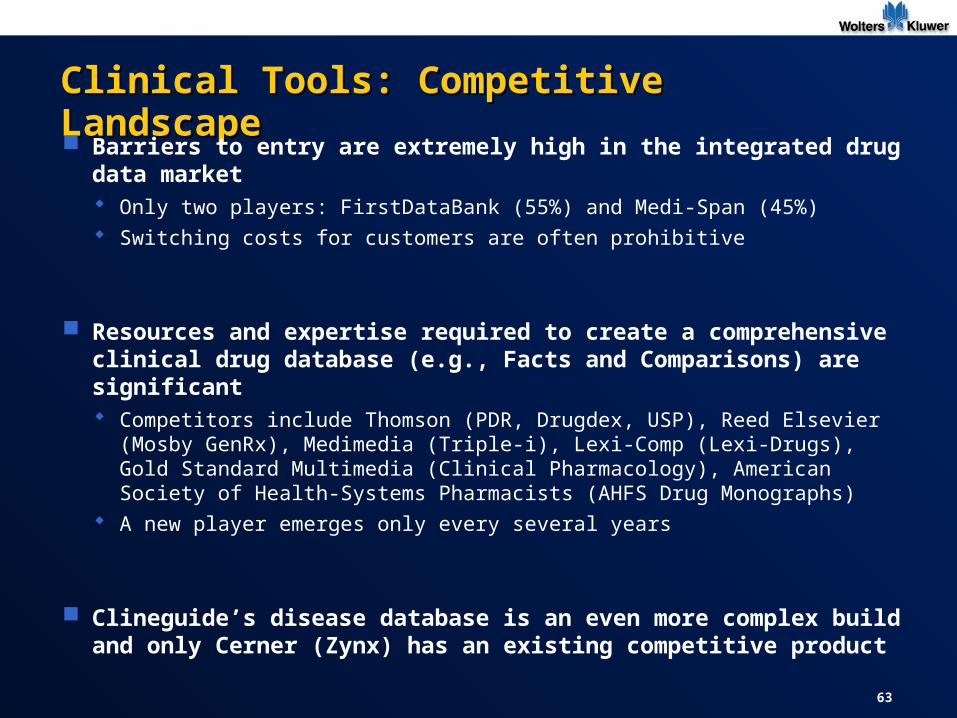

Clinical Tools: Competitive Landscape Clinical Tools: Competitive Landscape

Barriers to entry are extremely high in the integrated drug data market Only two players: FirstDataBank (55%) and Medi-Span (45%) Switching costs for customers are often prohibitive

Resources and expertise required to create a comprehensive clinical drug database (e.g., Facts and Comparisons) are significant Competitors include Thomson (PDR, Drugdex, USP), Reed Elsevier (Mosby

GenRx), Medimedia (Triple-i), Lexi-Comp (Lexi-Drugs), Gold Standard Multimedia (Clinical Pharmacology), American Society of Health-Systems Pharmacists (AHFS Drug Monographs)

A new player emerges only every several years

Clineguide’s disease database is an even more complex build and only Cerner (Zynx) has an existing competitive product

64

Retail Pharmacy40%

Hospital Pharmacy24%

Physician Offices8%

Drug Benefits Administrators

8%Pharma

7%

Individuals and Students

4%

Others9%

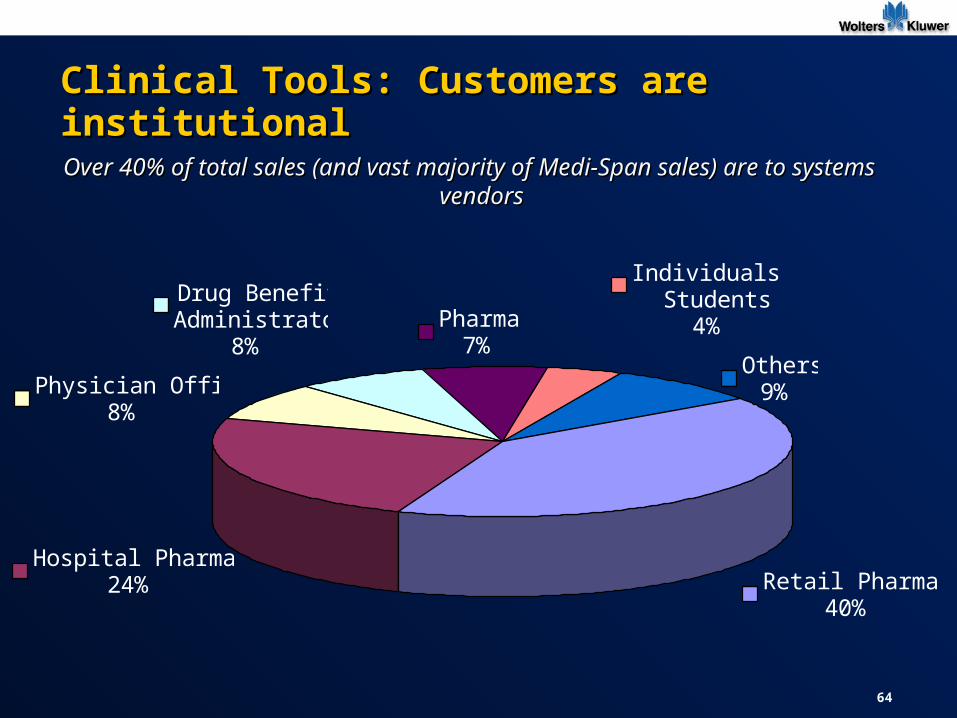

Over 40% of total sales (and vast majority of Medi-Span sales) are to systems Over 40% of total sales (and vast majority of Medi-Span sales) are to systems vendorsvendors

Clinical Tools: Customers are institutional Clinical Tools: Customers are institutional

65

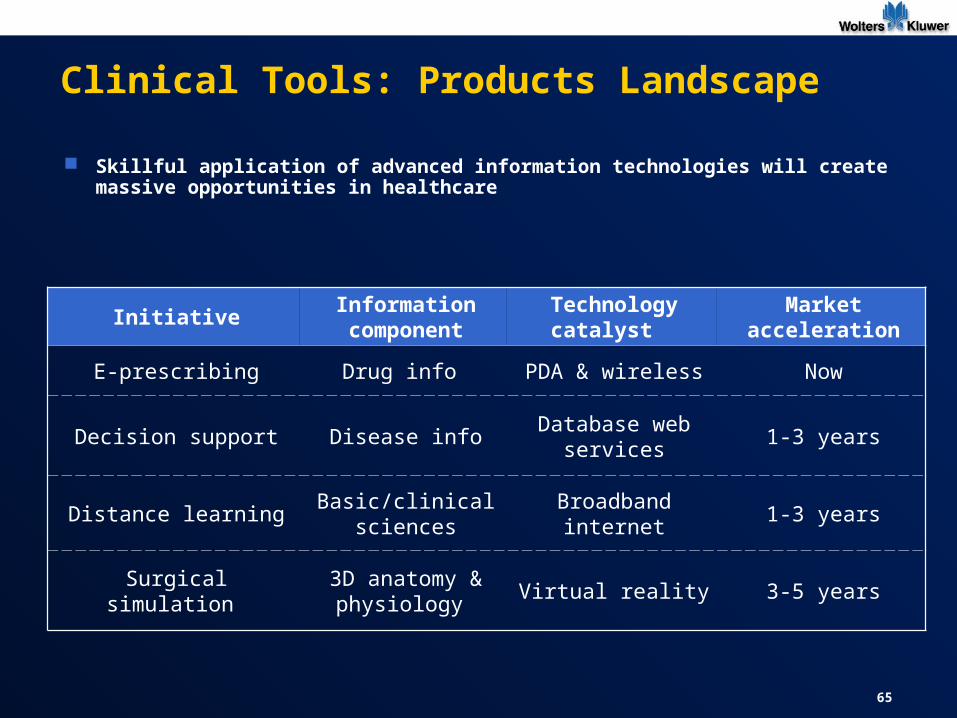

Clinical Tools: Products Landscape

Skillful application of advanced information technologies will create massive opportunities in healthcare

InitiativeInformation component

Technology catalyst

Market acceleration

E-prescribing Drug info PDA & wireless Now

Decision support Disease infoDatabase web

services1-3 years

Distance learningBasic/clinical

sciencesBroadband internet 1-3 years

Surgical simulation 3D anatomy &

physiology Virtual reality 3-5 years

66

Clinical Tools: Clinical Tools: Goals for 2003

Continue to integrate the existing product lines and operations, providing the market with novel and compelling products

Add new leadership in marketing to support an integrated and well-trained sales force

Establish operational stability and continue solid market momentum into 2004

Participate aggressively in acquisition market

Set stage for payoff in 2004 and beyond

67

Clinical Tools: Product Demos

Russ Worley, Managing Director, Medi-Span

Leslie Mills, Senior Product Developer, Medi-Span

Will explain and demonstrate the Medi-Span product line

Jon Seymour, MD, CEO, Clinical Tools

Will explain and demonstrate the Clineguide/eFacts web-based products