wood fibre business

TRANSCRIPT

May 2, 2013 WOOD FIBRE BUSINESS

Presentation

1

Forward-Looking Statements

This presentation contains forward-looking statements about matters such as:

forecasted EBITDA, operating income and depreciation; the outlook for the

business; our ability to consummate the acquisition of the facilities in Wawa and

Atikokan, Ontario; successful integration and future performance of acquired

assets or businesses; successful design, implementation and execution of growth

projects; Rentech’s plans for market share of the wood pellet industry; sale and

transport of wood pellets; and plans for sustainability. These statements are based

on management’s current expectations and actual results may differ materially as a

result of various risks and uncertainties. Other factors that could cause actual

results to differ from those reflected in the forward-looking statements are set forth

in Rentech’s prior press releases and periodic public filings with the Securities and

Exchange Commission, which are available via Rentech’s website at

www.rentechinc.com. The forward-looking statements in this presentation are made

as of the date of this presentation and Rentech does not undertake to revise or

update these forward-looking statements, except to the extent that it is required to

do so under applicable law.

Copyright © 2013 Rentech, Inc. No reproduction in whole or in part without written

permission of Rentech, Inc. All rights reserved.

2

Rentech Enters Wood Fibre Processing Business…

Rentech announced today a series of actions to enter new lines of

business in wood fibre processing:

• Acquired Fulghum Fibres, Inc.: High-volume wood handling and wood chip services

for the pulp products industry

• Agreements to acquire two facilities in Ontario for conversion to pellet

manufacturing: Entry into the rapidly growing market to supply wood pellets to

utilities for power generation, with global demand expected to triple to 50MM metric

tons by 2020

• Contracts to sell and transport >4MM metric tons of pellets from the two facilities in

Ontario, and signed a joint venture with a partner experienced in pellet plant

construction and operation

3

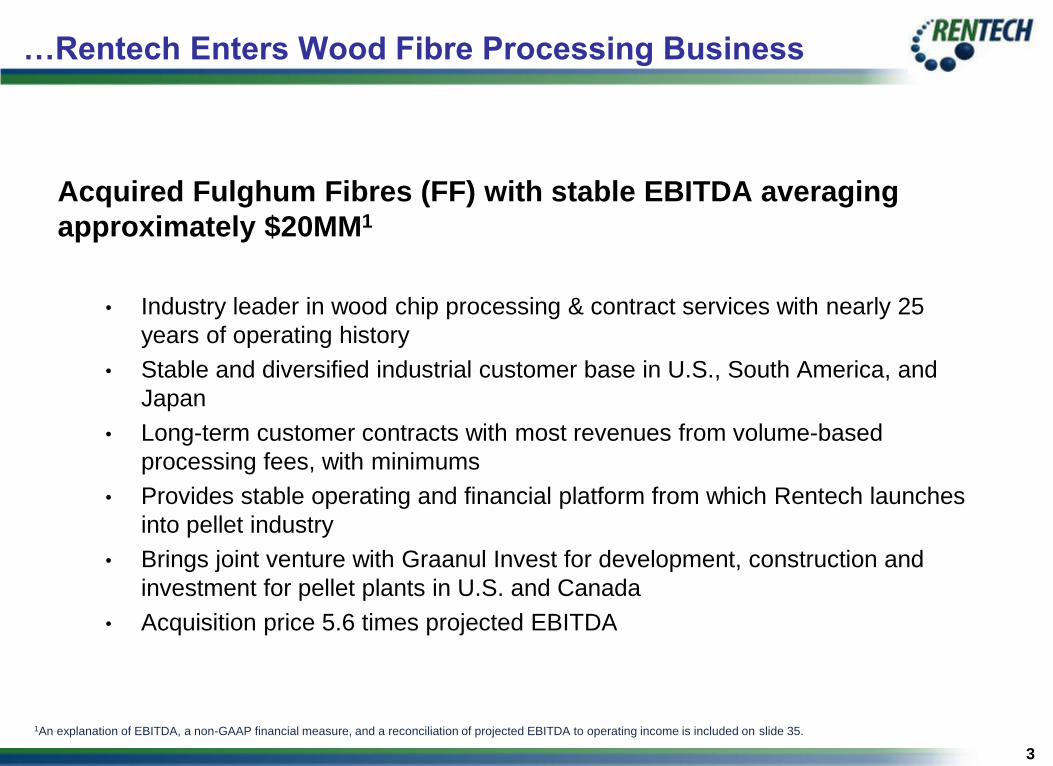

…Rentech Enters Wood Fibre Processing Business

Acquired Fulghum Fibres (FF) with stable EBITDA averaging

approximately $20MM1

• Industry leader in wood chip processing & contract services with nearly 25

years of operating history

• Stable and diversified industrial customer base in U.S., South America, and

Japan

• Long-term customer contracts with most revenues from volume-based

processing fees, with minimums

• Provides stable operating and financial platform from which Rentech launches

into pellet industry

• Brings joint venture with Graanul Invest for development, construction and

investment for pellet plants in U.S. and Canada

• Acquisition price 5.6 times projected EBITDA

1An explanation of EBITDA, a non-GAAP financial measure, and a reconciliation of projected EBITDA to operating income is included on slide 35.

4

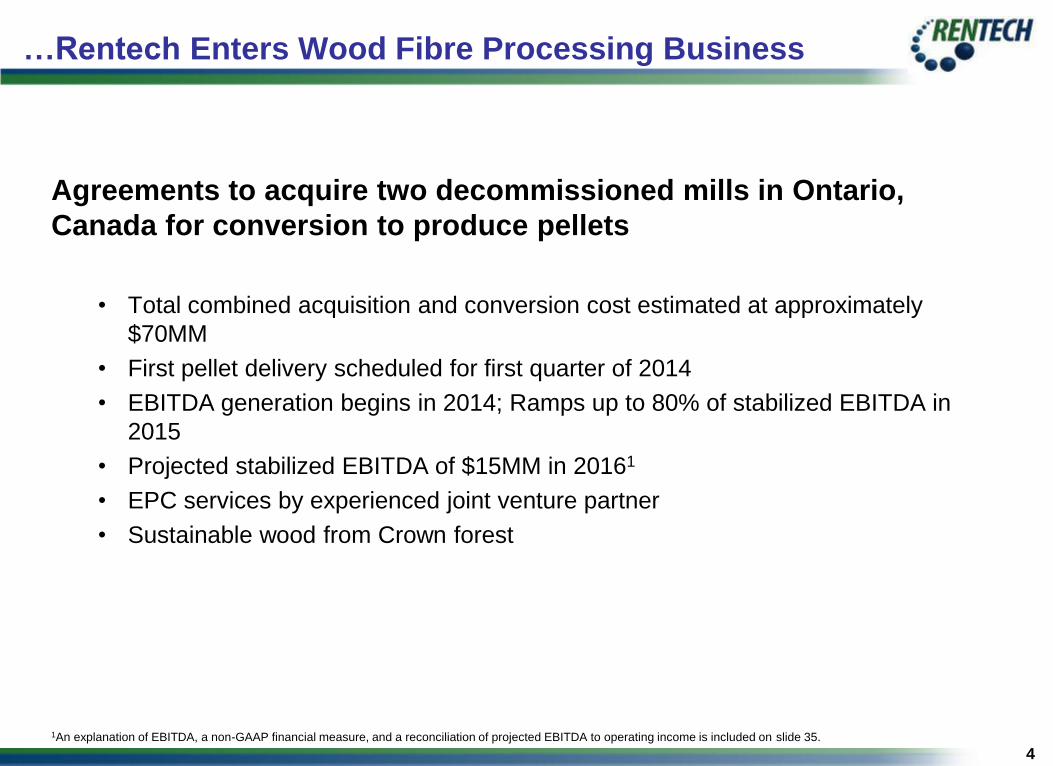

…Rentech Enters Wood Fibre Processing Business

Agreements to acquire two decommissioned mills in Ontario,

Canada for conversion to produce pellets

• Total combined acquisition and conversion cost estimated at approximately

$70MM

• First pellet delivery scheduled for first quarter of 2014

• EBITDA generation begins in 2014; Ramps up to 80% of stabilized EBITDA in

2015

• Projected stabilized EBITDA of $15MM in 20161

• EPC services by experienced joint venture partner

• Sustainable wood from Crown forest

1An explanation of EBITDA, a non-GAAP financial measure, and a reconciliation of projected EBITDA to operating income is included on slide 35.

5

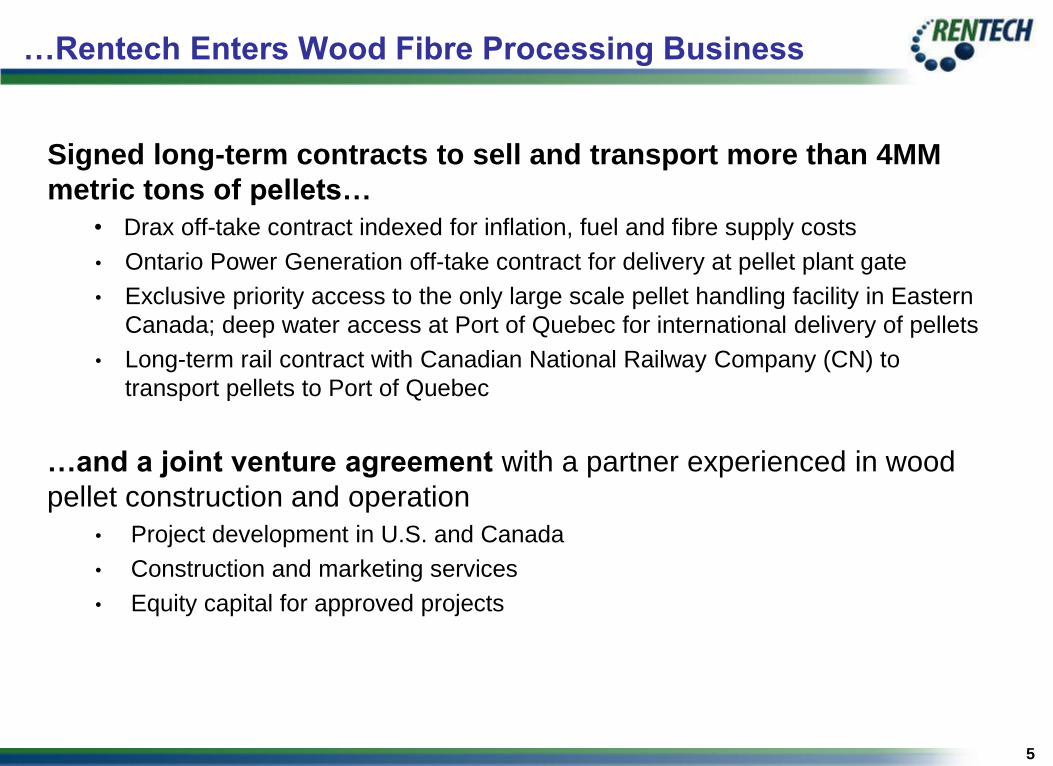

…Rentech Enters Wood Fibre Processing Business

Signed long-term contracts to sell and transport more than 4MM

metric tons of pellets…

• Drax off-take contract indexed for inflation, fuel and fibre supply costs

• Ontario Power Generation off-take contract for delivery at pellet plant gate

• Exclusive priority access to the only large scale pellet handling facility in Eastern

Canada; deep water access at Port of Quebec for international delivery of pellets

• Long-term rail contract with Canadian National Railway Company (CN) to

transport pellets to Port of Quebec

…and a joint venture agreement with a partner experienced in wood

pellet construction and operation

• Project development in U.S. and Canada

• Construction and marketing services

• Equity capital for approved projects

6

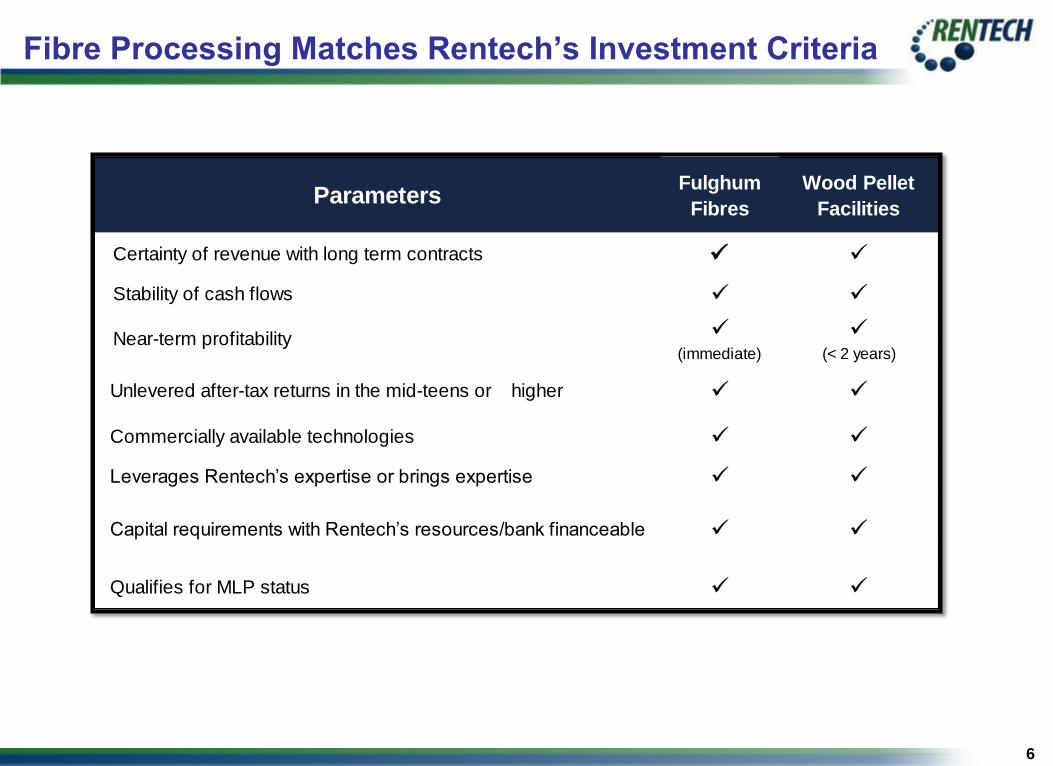

Fibre Processing Matches Rentech’s Investment Criteria

ParametersFulghum

Fibres

Wood Pellet

Facilities

Certainty of revenue with long term contracts

Stability of cash flows

(immediate) (< 2 years)

Unlevered after-tax returns in the mid-teens or higher

Commercially available technologies

Leverages Rentech’s expertise or brings expertise

Qualifies for MLP status

Near-term profitability

Capital requirements with Rentech’s resources/bank financeable

7

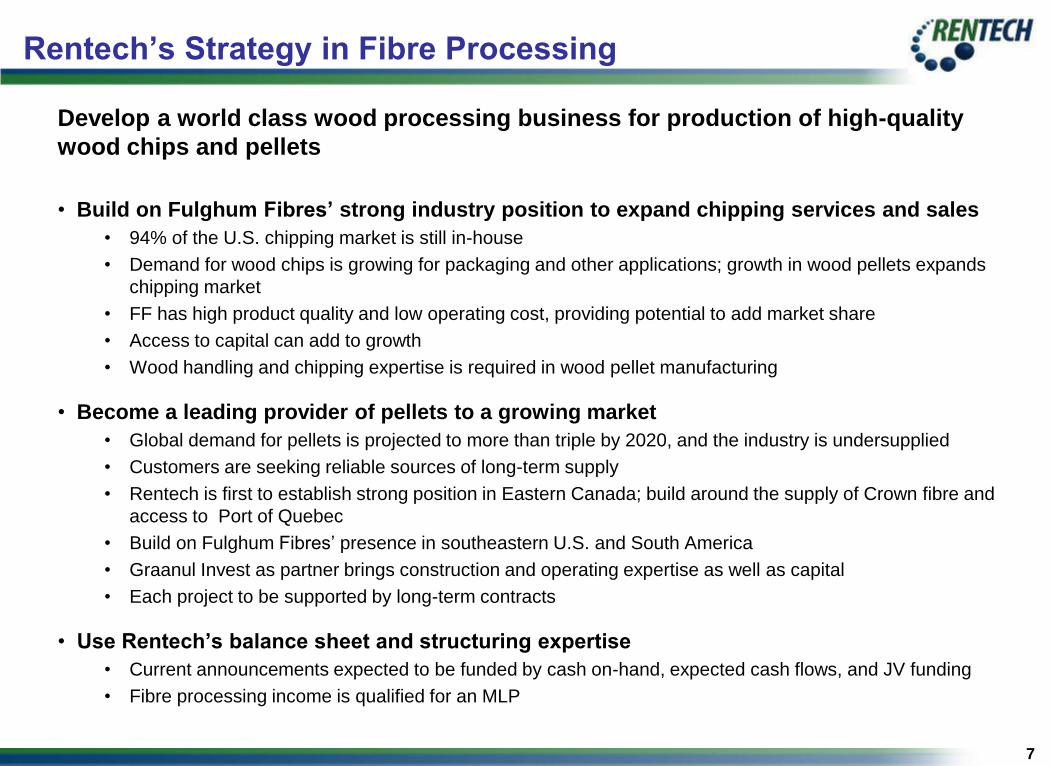

Rentech’s Strategy in Fibre Processing

Develop a world class wood processing business for production of high-quality

wood chips and pellets

• Build on Fulghum Fibres’ strong industry position to expand chipping services and sales

• 94% of the U.S. chipping market is still in-house

• Demand for wood chips is growing for packaging and other applications; growth in wood pellets expands

chipping market

• FF has high product quality and low operating cost, providing potential to add market share

• Access to capital can add to growth

• Wood handling and chipping expertise is required in wood pellet manufacturing

• Become a leading provider of pellets to a growing market

• Global demand for pellets is projected to more than triple by 2020, and the industry is undersupplied

• Customers are seeking reliable sources of long-term supply

• Rentech is first to establish strong position in Eastern Canada; build around the supply of Crown fibre and

access to Port of Quebec

• Build on Fulghum Fibres’ presence in southeastern U.S. and South America

• Graanul Invest as partner brings construction and operating expertise as well as capital

• Each project to be supported by long-term contracts

• Use Rentech’s balance sheet and structuring expertise

• Current announcements expected to be funded by cash on-hand, expected cash flows, and JV funding

• Fibre processing income is qualified for an MLP

8

Fulghum Fibres Transaction Overview

9

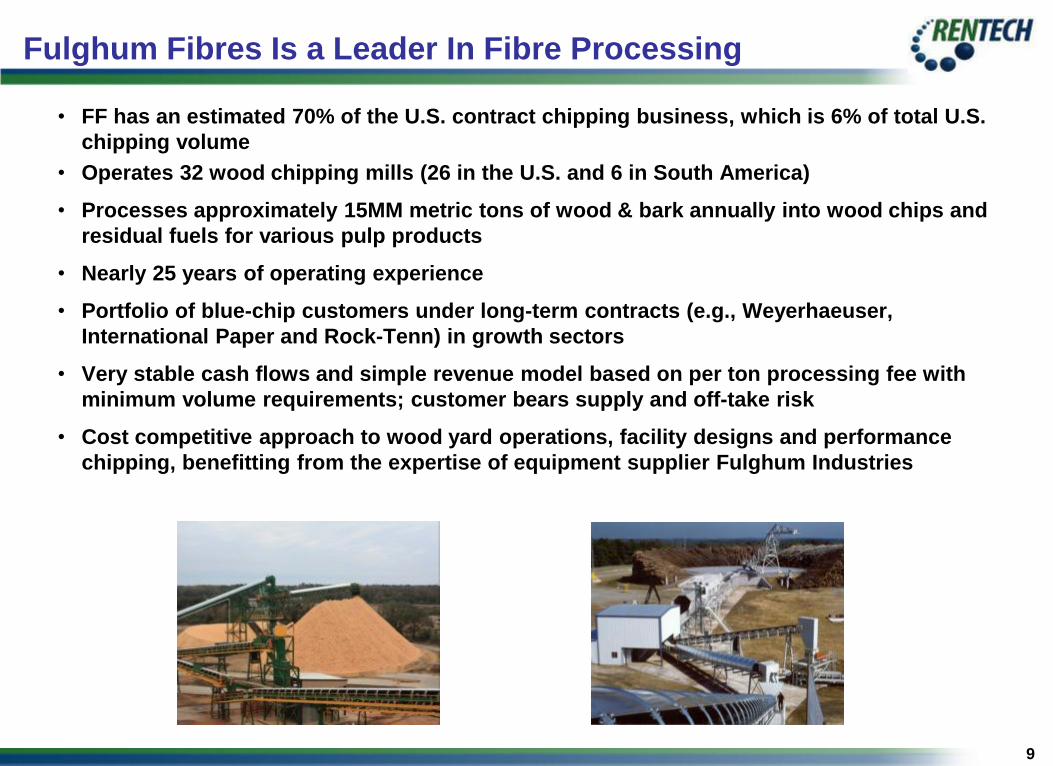

Fulghum Fibres Is a Leader In Fibre Processing

• FF has an estimated 70% of the U.S. contract chipping business, which is 6% of total U.S.

chipping volume

• Operates 32 wood chipping mills (26 in the U.S. and 6 in South America)

• Processes approximately 15MM metric tons of wood & bark annually into wood chips and

residual fuels for various pulp products

• Nearly 25 years of operating experience

• Portfolio of blue-chip customers under long-term contracts (e.g., Weyerhaeuser,

International Paper and Rock-Tenn) in growth sectors

• Very stable cash flows and simple revenue model based on per ton processing fee with

minimum volume requirements; customer bears supply and off-take risk

• Cost competitive approach to wood yard operations, facility designs and performance

chipping, benefitting from the expertise of equipment supplier Fulghum Industries

10

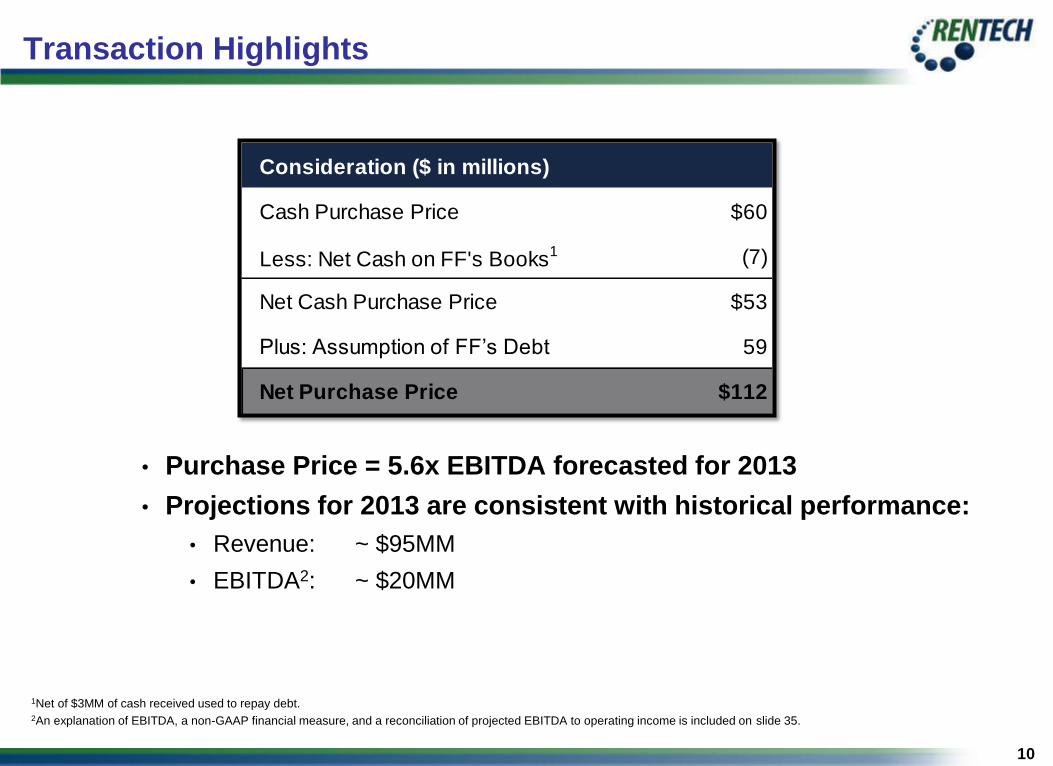

Transaction Highlights

1Net of $3MM of cash received used to repay debt.

2An explanation of EBITDA, a non-GAAP financial measure, and a reconciliation of projected EBITDA to operating income is included on slide 35.

• Purchase Price = 5.6x EBITDA forecasted for 2013

• Projections for 2013 are consistent with historical performance:

• Revenue: ~ $95MM

• EBITDA2: ~ $20MM

Consideration ($ in millions)

Cash Purchase Price $60

Less: Net Cash on FF's Books1 (7)

Net Cash Purchase Price $53

Plus: Assumption of FF’s Debt 59

Net Purchase Price $112

11

Business Model: Low Risk and Stability

• Long operating history with stable cash flow

• Customer retention of over 95% for the past nearly 25 years

• Over 60% of 2013 forecasted EBITDA is contracted through 2017

• Business diversification

• Services customers in 6 different product lines

• Operates in U.S. and South America

• Customers in U.S., South America and Japan

• Low risk structure

• Established equipment & technology: benefits of Fulghum Industries’ expertise

• Majority of revenues are from volume based services fees

• No stumpage, harvesting or delivery risk in service contacts

• Management continuity

• FF’s senior management has an average of 30 years experience and remains in place post-acquisition

• Growth

• U.S. contract chipping services is a growing industry

• 94% of chipping is still in-house with integrated producers

• 90% of FF’s annual production is tied to pulp products with highest growth projections for industry products

12

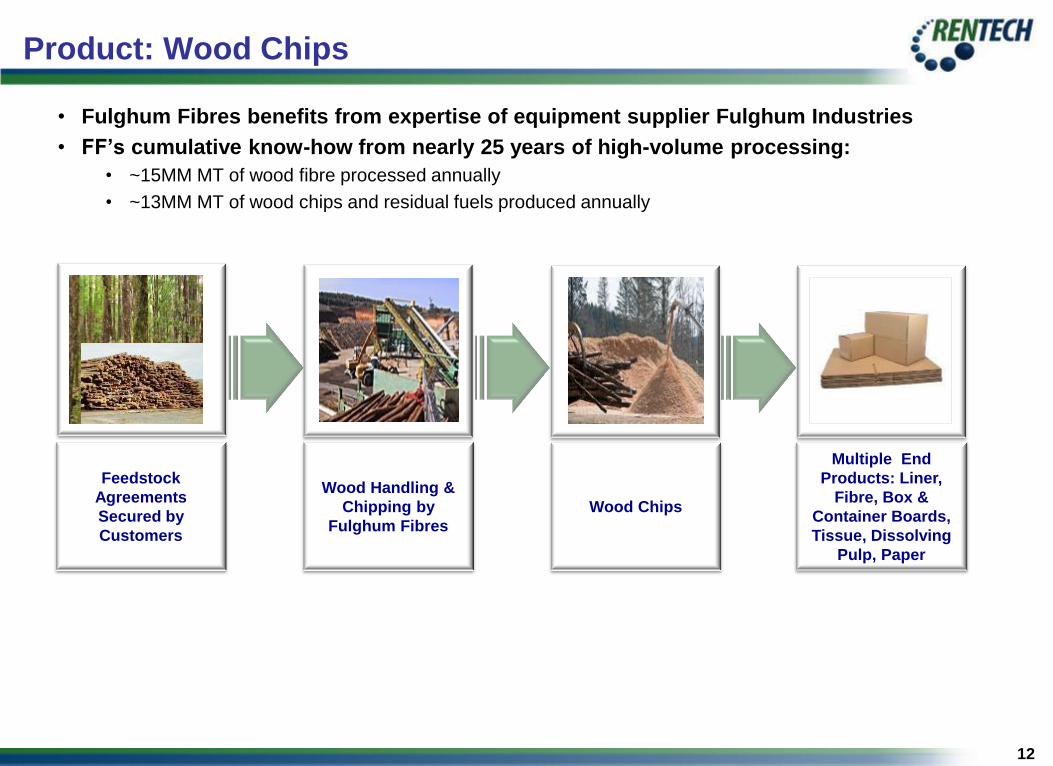

• Fulghum Fibres benefits from expertise of equipment supplier Fulghum Industries

• FF’s cumulative know-how from nearly 25 years of high-volume processing:

• ~15MM MT of wood fibre processed annually

• ~13MM MT of wood chips and residual fuels produced annually

Product: Wood Chips

Feedstock

Agreements

Secured by

Customers

Wood Handling &

Chipping by

Fulghum Fibres

Wood Chips

Multiple End

Products: Liner,

Fibre, Box &

Container Boards,

Tissue, Dissolving

Pulp, Paper

13

Competitive Advantage: Lower Cost and Higher Quality

FF has the flexibility to produce high quality chips of varying sizes to meet a variety

of customer chip specifications at a low cost

Design Expertise

Fulghum Fibres

Operational Feedback

Fulghum Industries

Loop results in continuous improvement in

equipment, quality and efficiency

14

“Blue-Chip” Customers Under Long-Term Contracts

• Fulghum Fibres has long-term contracts with most of its customers

• 60% of current volume is contracted through 2017

• Average contract length is 5-7 years

• Most customers are large, established companies with long operating history

• Exposure to any one customer does not exceed 16% of total volume

• Customer retention and contract renewal have historically been very strong

NORTH AMERICAN

CUSTOMERS

SOUTH AMERICAN

CUSTOMERS

Weyerhaeuser Nippon Paper

Georgia Pacific Mitsubishi

Graphic Packaging Sumitomo

International Paper Oji Paper

Kronospan Daio Paper

MeadWestvaco Arauco

Packaging Corp America CMPC

Potlatch Masisa

Rayonier Bosques Cautin

RockTenn Forestal Atlantico / Portucel

Woodland Forestal Los Lagos / Marasumi

15

End Markets For Chips Are Projected to Grow

Final usage of chips produced by Fulghum Fibres:

World Tissue Consumption RISI Forecast 2012-2027

World Boxboard and Paperboard Consumption RISI Forecast 2012-2027

Remaining 10% for rayon and medium density fiberboard; projected growth of 3-4% for 15 years

~40% for boxboard

RISI forecasts growth of 2.8% pa 2012-2027 and that

US boxboard exports will increase 50%.

10% for tissue products

~30% for containerboard <10% for printing paper

Source: RISI. 2012. World Pulp and Recovered Paper 15-yr Forecast. V12 N3.

World Containerboard Consumption RISI Forecast 2012-2027

RISI forecasts growth of 4.1% pa 2012-2027

World Printing & Writing Consumption RISI Forecast 2012-2027

RISI forecasts growth of 3.5% pa 2012-2027 RISI forecasts growth of 0.8% pa 2012-2027

16

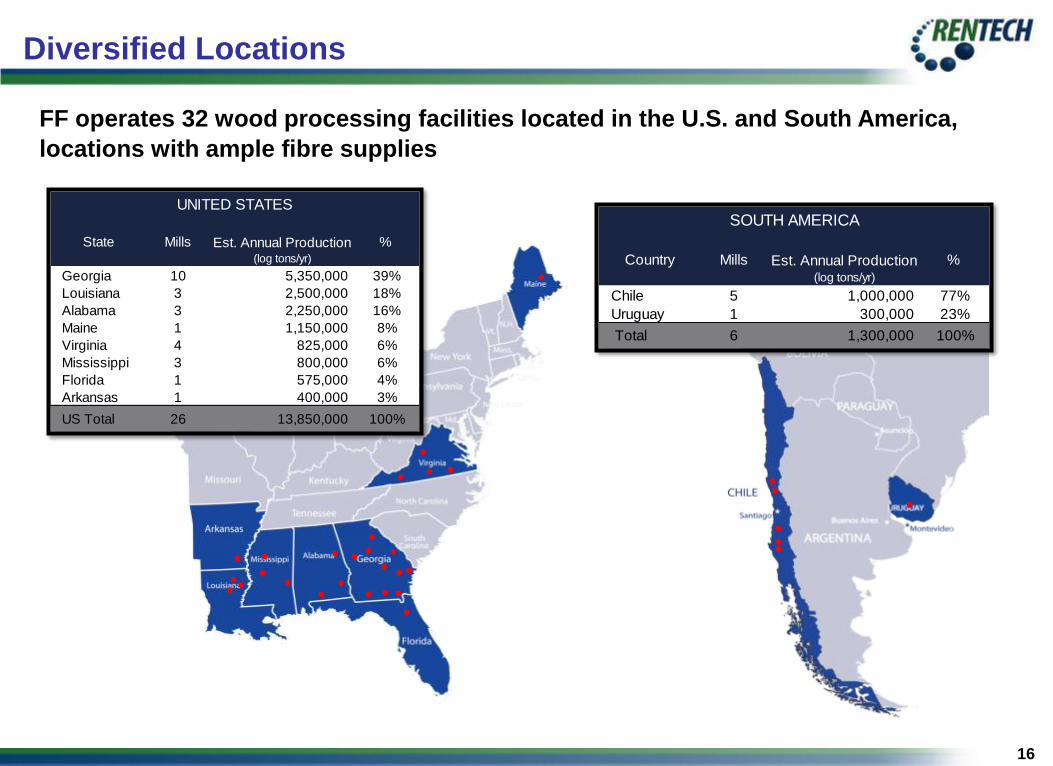

Diversified Locations

FF operates 32 wood processing facilities located in the U.S. and South America,

locations with ample fibre supplies

Country Mills Est. Annual Production (log tons/yr)

%

Chile 5 1,000,000 77%

Uruguay 1 300,000 23%

Total 6 1,300,000 100%

SOUTH AMERICA

State Mills Est. Annual Production (log tons/yr)

%

Georgia 10 5,350,000 39%

Louisiana 3 2,500,000 18%

Alabama 3 2,250,000 16%

Maine 1 1,150,000 8%

Virginia 4 825,000 6%

Mississippi 3 800,000 6%

Florida 1 575,000 4%

Arkansas 1 400,000 3%

US Total 26 13,850,000 100%

UNITED STATES

17

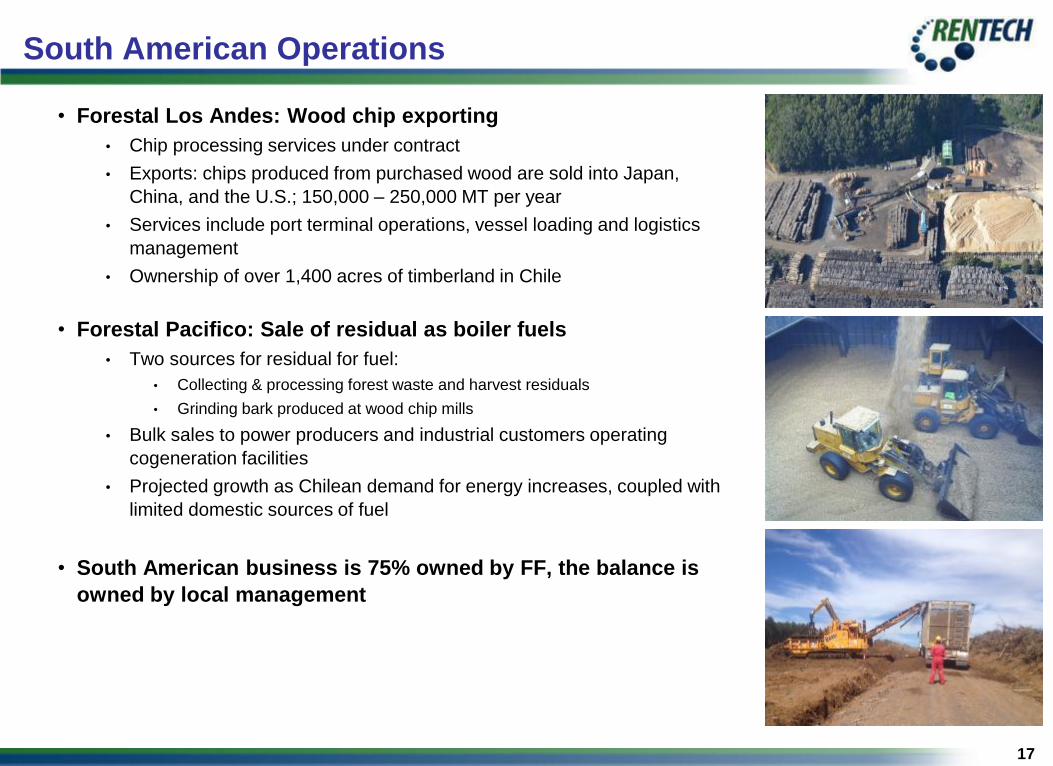

South American Operations

• Forestal Los Andes: Wood chip exporting

• Chip processing services under contract

• Exports: chips produced from purchased wood are sold into Japan,

China, and the U.S.; 150,000 – 250,000 MT per year

• Services include port terminal operations, vessel loading and logistics

management

• Ownership of over 1,400 acres of timberland in Chile

• Forestal Pacifico: Sale of residual as boiler fuels

• Two sources for residual for fuel:

• Collecting & processing forest waste and harvest residuals

• Grinding bark produced at wood chip mills

• Bulk sales to power producers and industrial customers operating

cogeneration facilities

• Projected growth as Chilean demand for energy increases, coupled with

limited domestic sources of fuel

• South American business is 75% owned by FF, the balance is

owned by local management

18

Plant Layouts to Meet Customers’ Needs

• Customer is responsible for log deliveries to the wood yard and scheduling of finished chip load out

• FF’s expertise includes high-volume wood handling, debarking, custom chipping, storage, reclaiming and

load out

• South American operations also include buying & selling wood, and growing of trees for chip export

markets

Satellite Mills

For customers who have

limited space for wood

yards or want to expand

fibre procurement into other

forested regions

Over-the-Fence Mills For customers who want

chip processing operations

at arm’s length from

adjacent pulp mill

Integrated Operations For fully-integrated

customers that prefer to

outsource their wood yard

operations

19

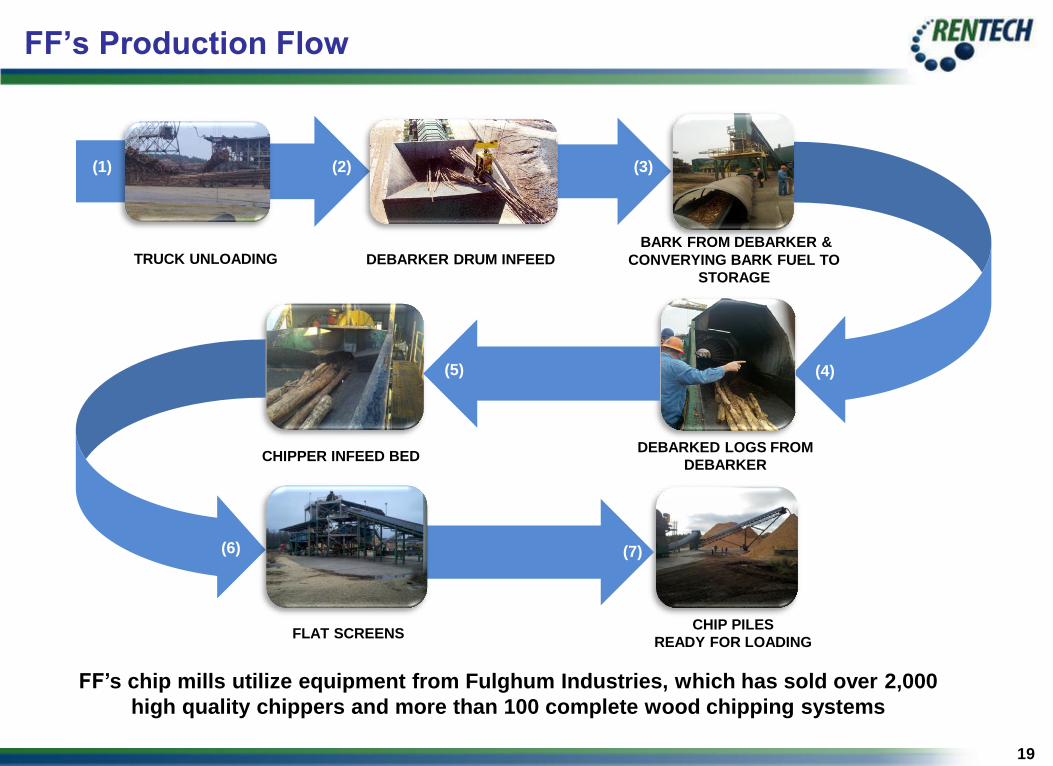

FF’s Production Flow

TRUCK UNLOADING DEBARKER DRUM INFEED

BARK FROM DEBARKER &

CONVERYING BARK FUEL TO

STORAGE

DEBARKED LOGS FROM

DEBARKER CHIPPER INFEED BED

FLAT SCREENS CHIP PILES

READY FOR LOADING

(1) (2) (3)

(6) (7)

(5) (4)

FF’s chip mills utilize equipment from Fulghum Industries, which has sold over 2,000

high quality chippers and more than 100 complete wood chipping systems

20

Growth Opportunities

Better access to capital should open up opportunities for additional customer

penetration and entry into other developing markets for paper products

• Provide additional wood yard management services to existing customers

• Capture outsourcing of wood yard management service (low capital investment)

• Co-locate pellet mills at chipping mills

• Relationships and expertise with fibre procurement companies can be extended for pellet supply

• Complementary front-end processing

• Transferrable operating expertise

• Acquire additional chip processing operating permits at mills currently operated by

integrated forestry companies (pulp mills and/or sawmill log yard operations)

• Establish chip mills in countries with low-cost feedstock

• Expand barks and residual fuel production in South America

21

Integration of Fulghum Fibres

• The Fulghum Fibres name will be retained

• Outstanding brand equity developed over nearly 25 years

• Customers and employees are extraordinarily loyal to the Fulghum tradition

• Continued association with Fulghum Industries

• Continuity of senior management

22

Launch of Pellet Business

23

Wood Pellets Business

Rentech expects to become the largest supplier of wood pellets in Eastern Canada

to the Canadian and European utility markets based on today’s announced

contracts

• Wood Supply: Crown fibre supply based on relationship with the Province of Ontario

• Sustainably managed forestlands

• Attractive fibre chemistry for use in power generation and heating applications

• Production: Acquire two decommissioned fibre board facilities for swift conversion into pellet

plants to produce 485K metric tons annually

• Construction & Operations: Partner Graanul Invest brings extensive EPC and operations

experience; Fulghum Fibres’ operational experience is directly applicable

• Off-take: Two take-or-pay 10-year off-take contracts

• Drax off-take price is indexed for inflation, fuel and fiber costs

• Ontario Power Generation (“OPG”) deliveries FOB plant gate

• Transport: Long-term rail contract with CN for plant-to-port transportation

• Port: 15-year agreement with Quebec Stevedoring Company Limited, for exclusive priority access

to pellet infrastructure to be built at the Port of Quebec

24

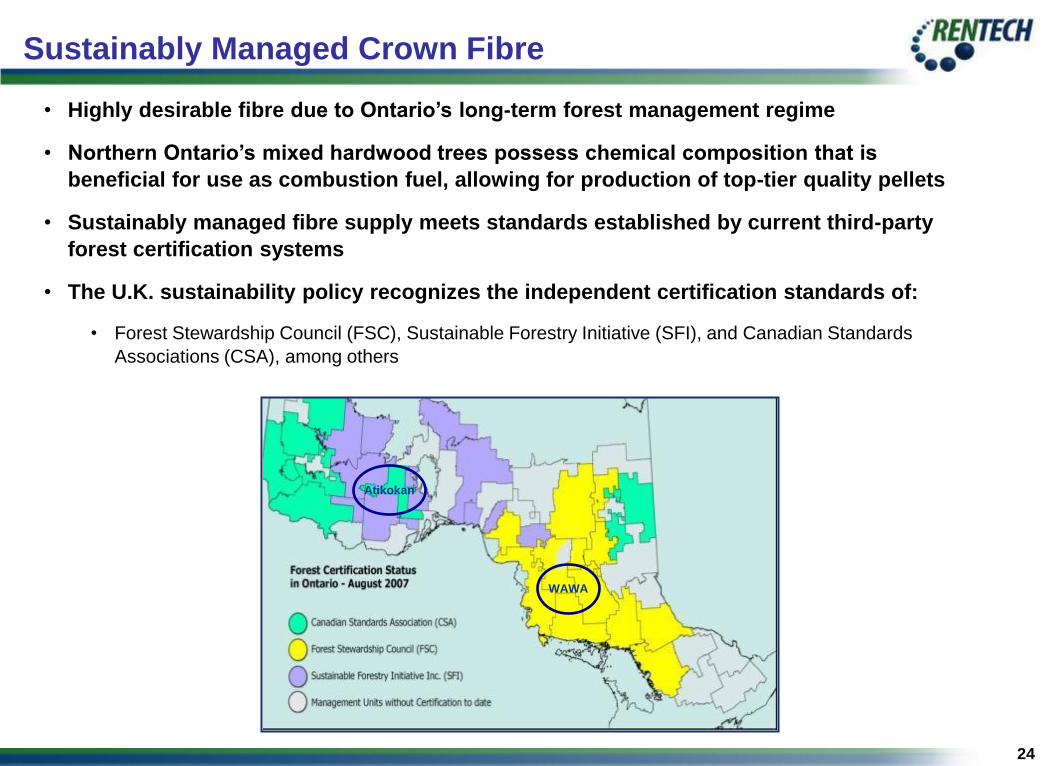

Sustainably Managed Crown Fibre

WAWA

Atikokan

• Highly desirable fibre due to Ontario’s long-term forest management regime

• Northern Ontario’s mixed hardwood trees possess chemical composition that is

beneficial for use as combustion fuel, allowing for production of top-tier quality pellets

• Sustainably managed fibre supply meets standards established by current third-party

forest certification systems

• The U.K. sustainability policy recognizes the independent certification standards of:

• Forest Stewardship Council (FSC), Sustainable Forestry Initiative (SFI), and Canadian Standards

Associations (CSA), among others

25

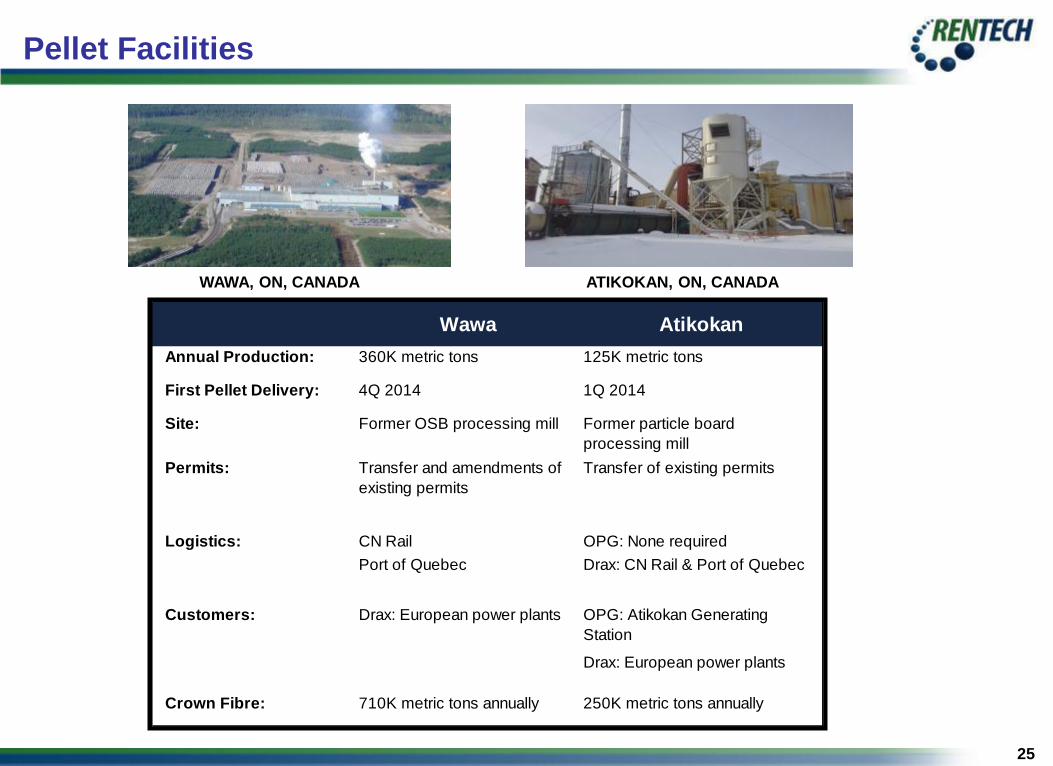

Pellet Facilities

WAWA, ON, CANADA ATIKOKAN, ON, CANADA

Wawa Atikokan

Annual Production: 360K metric tons 125K metric tons

First Pellet Delivery: 4Q 2014 1Q 2014

Site: Former OSB processing mill Former particle board

processing mill

Permits: Transfer and amendments of

existing permits

Transfer of existing permits

CN Rail OPG: None required

Port of Quebec Drax: CN Rail & Port of Quebec

OPG: Atikokan Generating

Station

Drax: European power plants

Crown Fibre: 710K metric tons annually 250K metric tons annually

Logistics:

Customers: Drax: European power plants

26

Rentech / Graanul Invest Joint Venture

• Joint-venture is specific to the development,

construction and operation of pellet projects in the U.S.

& Canada

• Significant strategic value in partnering:

• 50:50 equity partnership between Rentech and Graanul

• Commitment to produce 1.25 million metric tons of pellets in

Canada and the U.S.

• Graanul brings EPC, operating, and marketing expertise

• Graanul to provide backstop for pellet excess and shortfalls

• Rentech to provide 50% of project cost as loan

• Graanul Invest

• Established in 2003 and one of the largest pellet producers

globally

• Designs, builds and operates its own pellet facilities

• 6 operating pellet facilities in Europe

• 830K metric tons of annual pellet production • ~50% of production sold to European utilities under long-term

contracts with remaining sold into the spot market

• Cost competitive high-quality pellet production due to expertise

gained from being its own EPC contractor and operator

• Project management of all phases of development from design to

construction and start-up

27

Pellet Processing Flow

Fulghum Fibres Expertise

Graanul Invest Expertise

Log Debarking & Chipping Raw Material Handling

Rail

Loading

28

Long-term Off-take Contracts

Drax Power Limited

• Contracted revenues for 400K metric tons of wood pellets annually over the next 10 years

• Contract price is indexed for inflation, fuel and fibre supply pricing

• Establishes strategic relationship with Drax

• Currently the largest importer of wood pellets into the U.K.

• Drax is expected to require approximately 7MM metric tons of pellets per year by 2017 to fulfill biomass requirement

to convert half of its power station (supplies average 7% of total U.K. electricity) from coal to biomass

Ontario Power Generation (OPG)

• A Crown corporation and Ontario’s largest power generator

• Supply 45K metric tons of wood pellets annually over the next 10 years

• Option by OPG to increase to 90K metric tons annually

• Contract is FOB at plant gate (no logistics costs )

• OPG is phasing out the use of coal to produce electricity by 2015

29

Secure Logistics Infrastructure

CN – Rail Logistics

• Contract secured for rail services from Ontario to Port of Quebec

• Rentech will be expected to lease more than 200 rail cars for dedicated trains

• Establishes strategic relationship with CN – opens eastern market for rail

transport

• Year-round track accessibility

• Existing rail network creates opportunities for future pellet production and/or

consolidation in bordering New England states (U.S.) and Eastern

Provinces (Canada)

Port of Quebec – Quebec Stevedoring

• 15-year contract with Quebec Stevedoring Company Limited for Stevedoring

services • Includes capital lease obligations for Rentech of approximately $20 million for

construction of dedicated terminalling infrastructure

• Largest inland port capable of handling Panamax vessels • Largest ship class targeted by Drax to transport wood pellets into U.K.

• The largest bulk terminal in Eastern Canada

• Year-round terminal access

• Significant economies of scale as Rentech develops Eastern Canada

presence

• Offers direct and expedient route to Europe

• Surrounded by forests, in contrast to coastal ports

30

Financial Overview

31

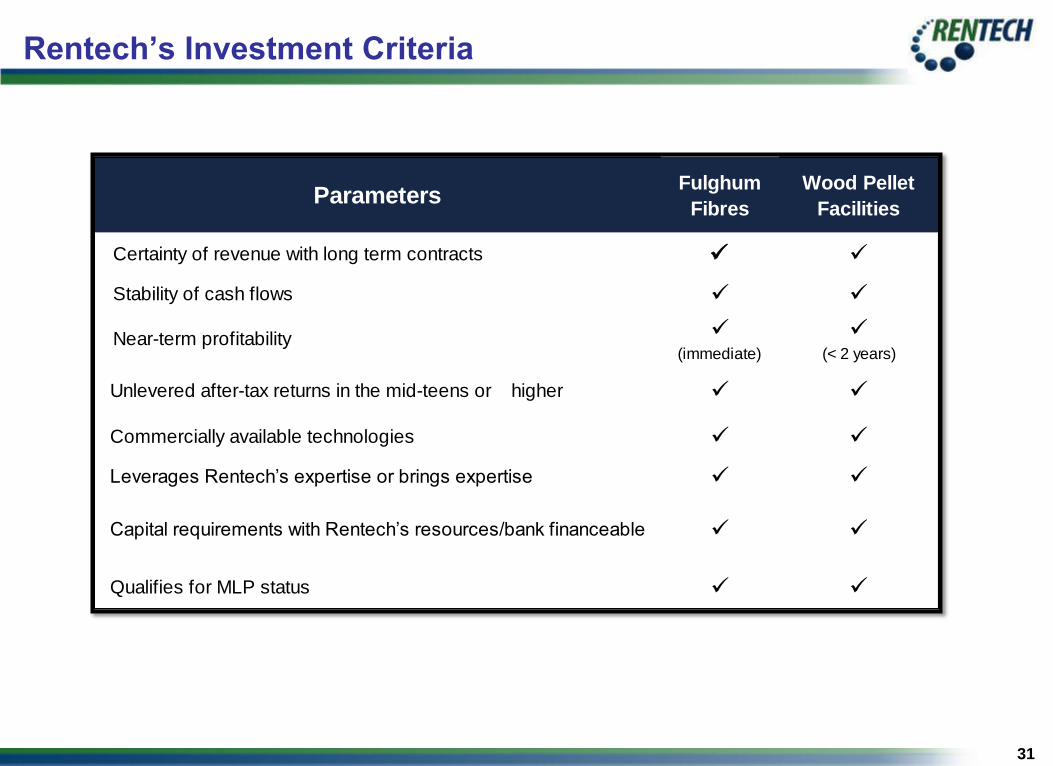

Rentech’s Investment Criteria

ParametersFulghum

Fibres

Wood Pellet

Facilities

Certainty of revenue with long term contracts

Stability of cash flows

(immediate) (< 2 years)

Unlevered after-tax returns in the mid-teens or higher

Commercially available technologies

Leverages Rentech’s expertise or brings expertise

Qualifies for MLP status

Near-term profitability

Capital requirements with Rentech’s resources/bank financeable

32

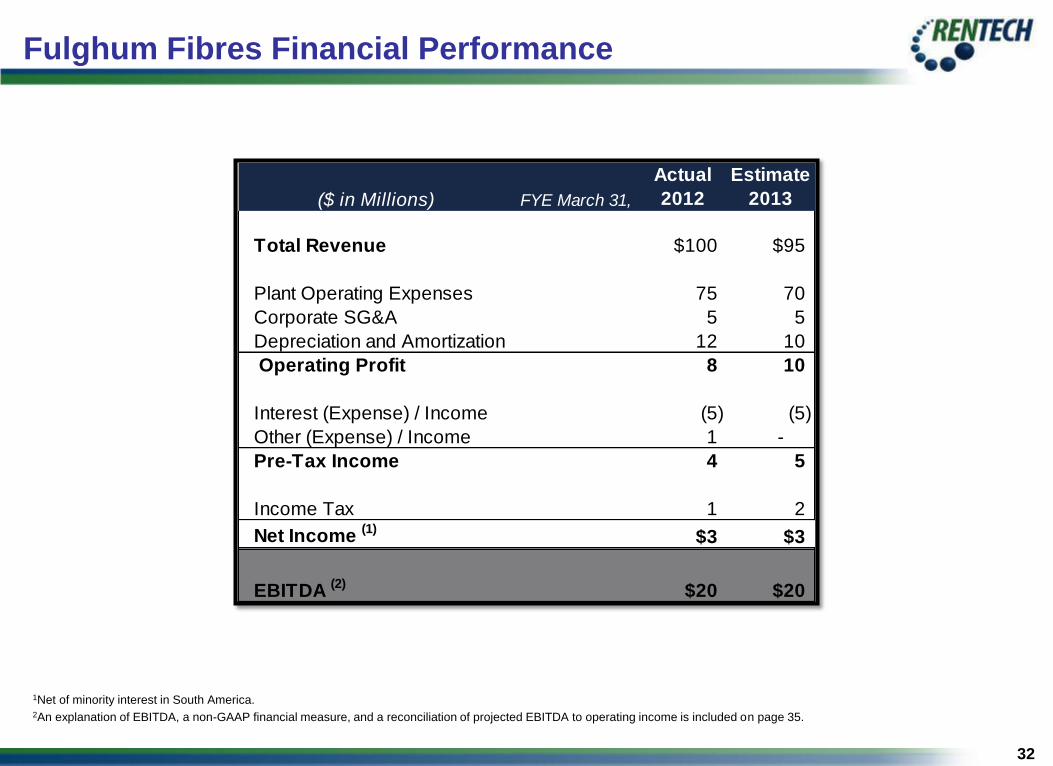

Fulghum Fibres Financial Performance

1Net of minority interest in South America. 2An explanation of EBITDA, a non-GAAP financial measure, and a reconciliation of projected EBITDA to operating income is included on page 35.

($ in Millions) FYE March 31,

Actual

2012

Estimate

2013

Total Revenue $100 $95

Plant Operating Expenses 75 70

Corporate SG&A 5 5

Depreciation and Amortization 12 10

Operating Profit 8 10

Interest (Expense) / Income (5) (5)

Other (Expense) / Income 1 -

Pre-Tax Income 4 5

Income Tax 1 2

Net Income (1)

$3 $3

EBITDA (2)

$20 $20

33

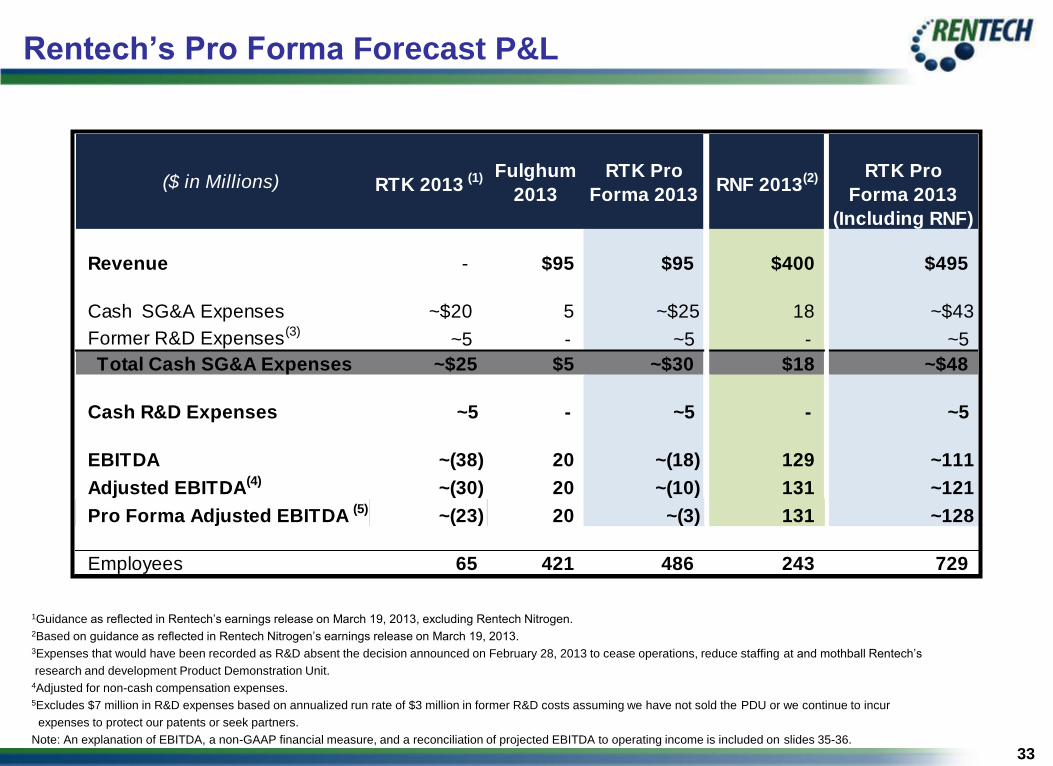

Rentech’s Pro Forma Forecast P&L

1Guidance as reflected in Rentech’s earnings release on March 19, 2013, excluding Rentech Nitrogen. 2Based on guidance as reflected in Rentech Nitrogen’s earnings release on March 19, 2013. 3Expenses that would have been recorded as R&D absent the decision announced on February 28, 2013 to cease operations, reduce staffing at and mothball Rentech’s

research and development Product Demonstration Unit. 4Adjusted for non-cash compensation expenses. 5Excludes $7 million in R&D expenses based on annualized run rate of $3 million in former R&D costs assuming we have not sold the PDU or we continue to incur

expenses to protect our patents or seek partners.

Note: An explanation of EBITDA, a non-GAAP financial measure, and a reconciliation of projected EBITDA to operating income is included on slides 35-36.

($ in Millions) RTK 2013 (1) Fulghum

2013

RTK Pro

Forma 2013RNF 2013

(2) RTK Pro

Forma 2013

(Including RNF)

Revenue - $95 $95 $400 $495

Cash SG&A Expenses ~$20 5 ~$25 18 ~$43

Former R&D Expenses(3)

~5 - ~5 - ~5

Total Cash SG&A Expenses ~$25 $5 ~$30 $18 ~$48

Cash R&D Expenses ~5 - ~5 - ~5

EBITDA ~(38) 20 ~(18) 129 ~111

Adjusted EBITDA(4)

~(30) 20 ~(10) 131 ~121

Pro Forma Adjusted EBITDA (5)

~(23) 20 ~(3) 131 ~128

Employees 65 421 486 243 729

34

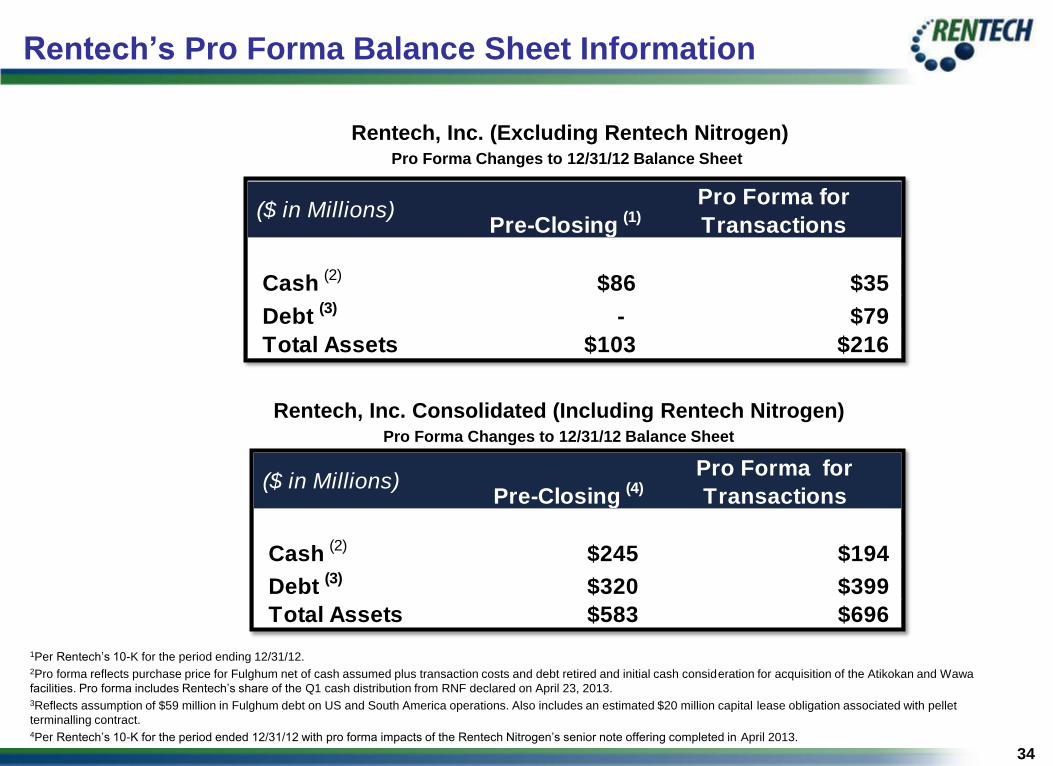

Rentech’s Pro Forma Balance Sheet Information

Rentech, Inc. (Excluding Rentech Nitrogen) Pro Forma Changes to 12/31/12 Balance Sheet

Rentech, Inc. Consolidated (Including Rentech Nitrogen) Pro Forma Changes to 12/31/12 Balance Sheet

1Per Rentech’s 10-K for the period ending 12/31/12. 2Pro forma reflects purchase price for Fulghum net of cash assumed plus transaction costs and debt retired and initial cash consideration for acquisition of the Atikokan and Wawa

facilities. Pro forma includes Rentech’s share of the Q1 cash distribution from RNF declared on April 23, 2013. 3Reflects assumption of $59 million in Fulghum debt on US and South America operations. Also includes an estimated $20 million capital lease obligation associated with pellet

terminalling contract. 4Per Rentech’s 10-K for the period ended 12/31/12 with pro forma impacts of the Rentech Nitrogen’s senior note offering completed in April 2013.

($ in Millions)Pre-Closing

(4)Pro Forma for

Transactions

Cash (2)

$245 $194

Debt (3)

$320 $399

Total Assets $583 $696

($ in Millions)Pre-Closing

(1)Pro Forma for

Transactions

Cash (2)

$86 $35

Debt (3)

- $79

Total Assets $103 $216

35

Disclosure Regarding Non-GAAP Financial Measures

EBITDA is defined as operating income plus depreciation expense. EBITDA is used as a supplemental financial measure by management and by

external users of our financial statements, such as investors and commercial banks, to assess:

• The financial performance of our assets without regard to financing methods, capital structure or historical cost basis; and

• Our operating performance and return on invested capital compared to those of other publicly traded limited partnerships and other public

companies, without regard to financing methods and capital structure.

EBITDA should not be considered an alternative to net income, operating income, net cash provided by operating activities or any other measure of

financial performance or liquidity presented in accordance with GAAP. EBITDA may have material limitations as a performance measure because it

excludes items that are necessary elements of our costs and operations. In addition, EBITDA presented by other companies may not be comparable to

our presentation, since each company may define these terms differently.

The table below reconcile EBITDA to operating income for the fiscal twelve months ended March 31, 2012, March 31, 2013 and forecast calendar

twelve months ending December 31, 2013, respectively, for Fulghum Fibres.

Reconciliation from Operating Income:

1Depreciation does not reflect any step-up in asset basis resulting from purchase price allocation.

Fulghum Fibres EBITDA ($ in Millions) FY 2012 FY 2013 CY 2013

Operating Income $8 $10 $10

Plus: Depreciation & Amortization (1)

12 10 10

EBITDA $20 $20 $20

The table below reconciles the estimated stabilized EBITDA to operating income for the Wawa and Atikokan facilities (unaudited

estimate, stated in millions).

Reconciliation from Operating Income:

WAWA & ATIKOKAN FACILITIES ($ in Millions) 2016

Operating Income $3

Plus: Depreciation & Amortization 12

EBITDA $15

36

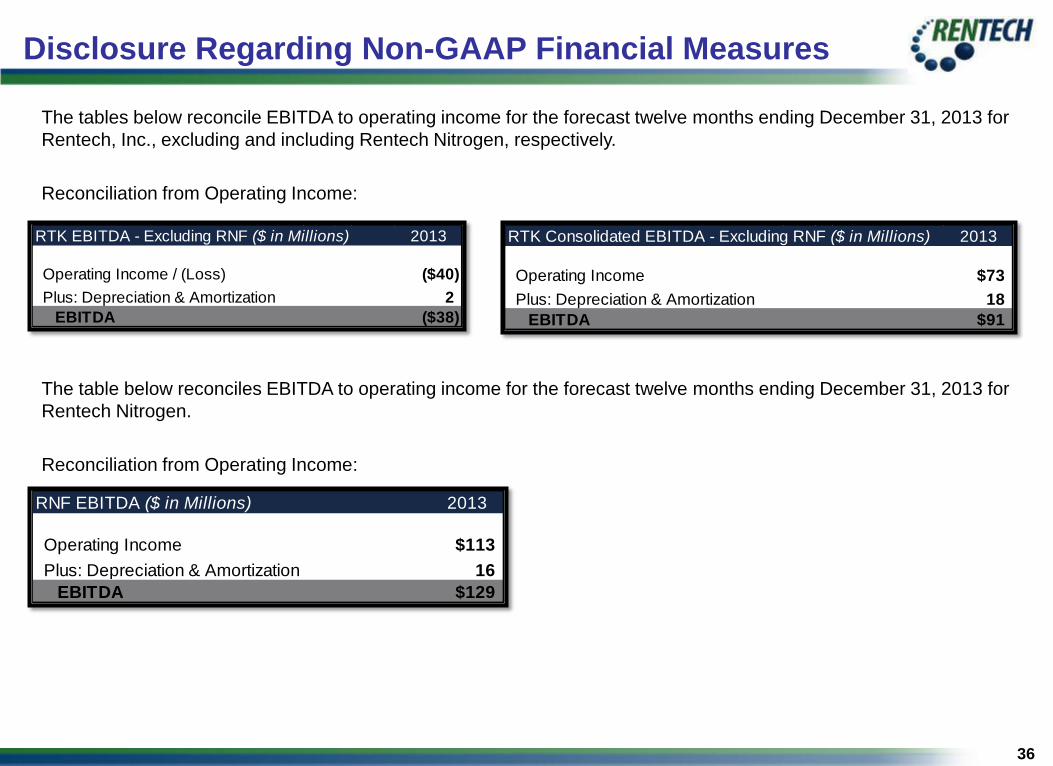

Disclosure Regarding Non-GAAP Financial Measures

The tables below reconcile EBITDA to operating income for the forecast twelve months ending December 31, 2013 for

Rentech, Inc., excluding and including Rentech Nitrogen, respectively.

Reconciliation from Operating Income:

The table below reconciles EBITDA to operating income for the forecast twelve months ending December 31, 2013 for

Rentech Nitrogen.

Reconciliation from Operating Income:

RTK EBITDA - Excluding RNF ($ in Millions) 2013

Operating Income / (Loss) ($40)

Plus: Depreciation & Amortization 2

EBITDA ($38)

RTK Consolidated EBITDA - Excluding RNF ($ in Millions) 2013

Operating Income $73

Plus: Depreciation & Amortization 18

EBITDA $91

RNF EBITDA ($ in Millions) 2013

Operating Income $113

Plus: Depreciation & Amortization 16

EBITDA $129

37

Integration

38

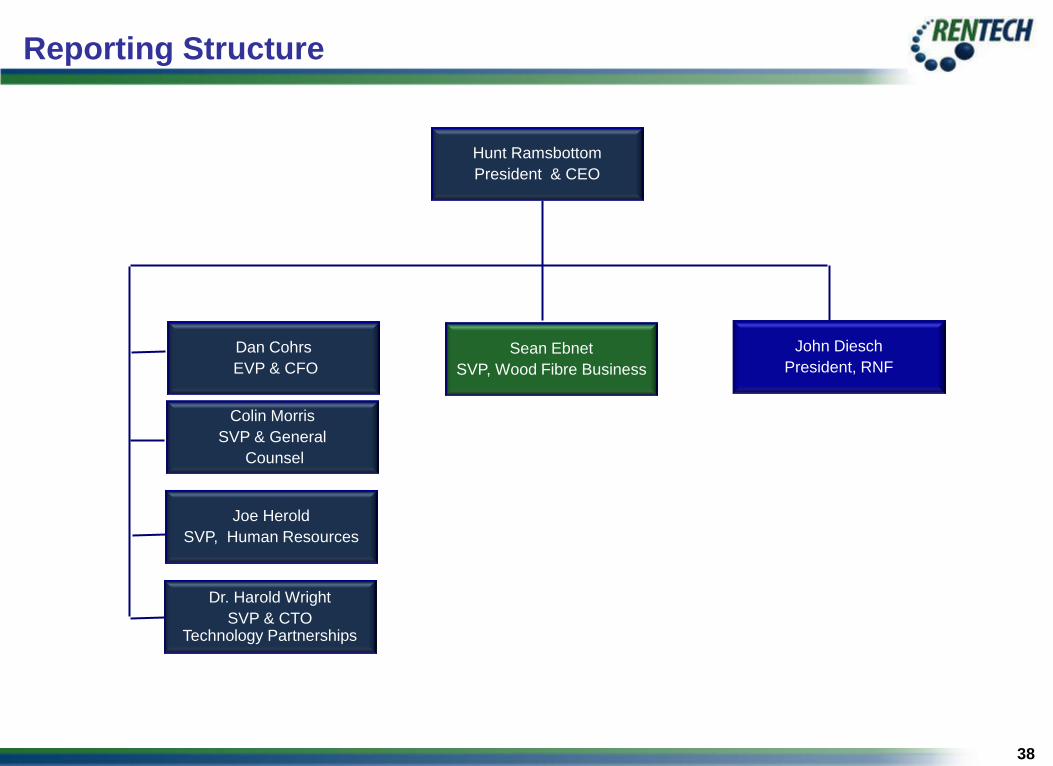

Reporting Structure

Hunt Ramsbottom

President & CEO

Joe Herold

SVP, Human Resources

Colin Morris

SVP & General

Counsel

Dr. Harold Wright

SVP & CTO Technology Partnerships

Dan Cohrs

EVP & CFO

John Diesch

President, RNF

Sean Ebnet

SVP, Wood Fibre Business

39

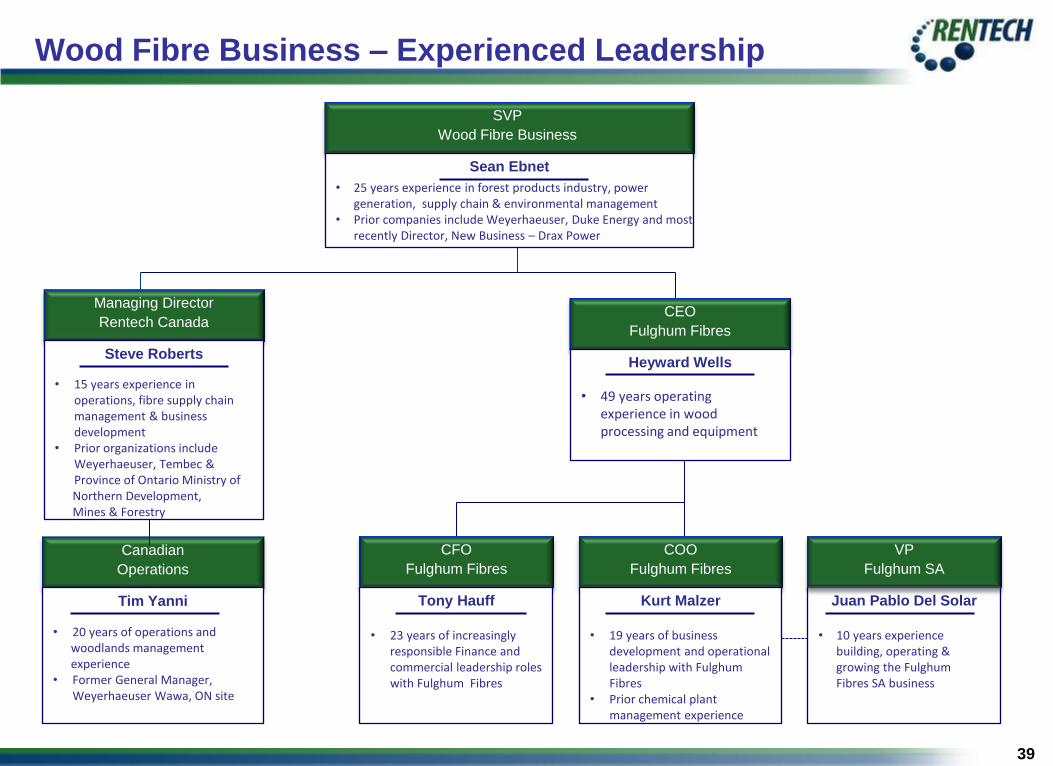

Wood Fibre Business – Experienced Leadership

Managing Director

Rentech Canada

Steve Roberts

• 15 years experience in operations, fibre supply chain management & business development

• Prior organizations include Weyerhaeuser, Tembec & Province of Ontario Ministry of

Northern Development, Mines & Forestry

COO

Fulghum Fibres

Kurt Malzer

• 19 years of business development and operational leadership with Fulghum Fibres

• Prior chemical plant management experience

CFO

Fulghum Fibres

Tony Hauff

• 23 years of increasingly responsible Finance and commercial leadership roles with Fulghum Fibres

Canadian

Operations

Tim Yanni

• 20 years of operations and woodlands management experience • Former General Manager,

Weyerhaeuser Wawa, ON site

CEO

Fulghum Fibres

Heyward Wells

• 49 years operating experience in wood processing and equipment

SVP

Wood Fibre Business

Sean Ebnet

• 25 years experience in forest products industry, power generation, supply chain & environmental management

• Prior companies include Weyerhaeuser, Duke Energy and most recently Director, New Business – Drax Power

Juan Pablo Del Solar

VP

Fulghum SA

• 10 years experience building, operating & growing the Fulghum Fibres SA business

40

WOOD FIBRE BUSINESS

Presentation