working with parliament for better government - fmi*igf maxwell en.pdf · working with parliament...

TRANSCRIPT

Working with Parliament for Better

Government

Office of the Auditor General of Canada

Neil Maxwell

28 November 2013

FMI PD Week

2

Topics

• Who we are

• What we do

• Safeguards to independence

• Where we fit in the Canadian political system

• Legislative auditing

• Environmental mandate

• Office budget, staff, and structure

• Accountability of the Auditor General

• Promoting better government

3

Who we are

• The Auditor General of Canada is an Officer of

Parliament (carries out work for Parliament and is

accountable to Parliament).

• The Auditor General’s authority comes from

Parliament and is outlined in the

– Auditor General Act,

– Financial Administration Act,

– Federal Accountability Act, and

– many other statutes.

4

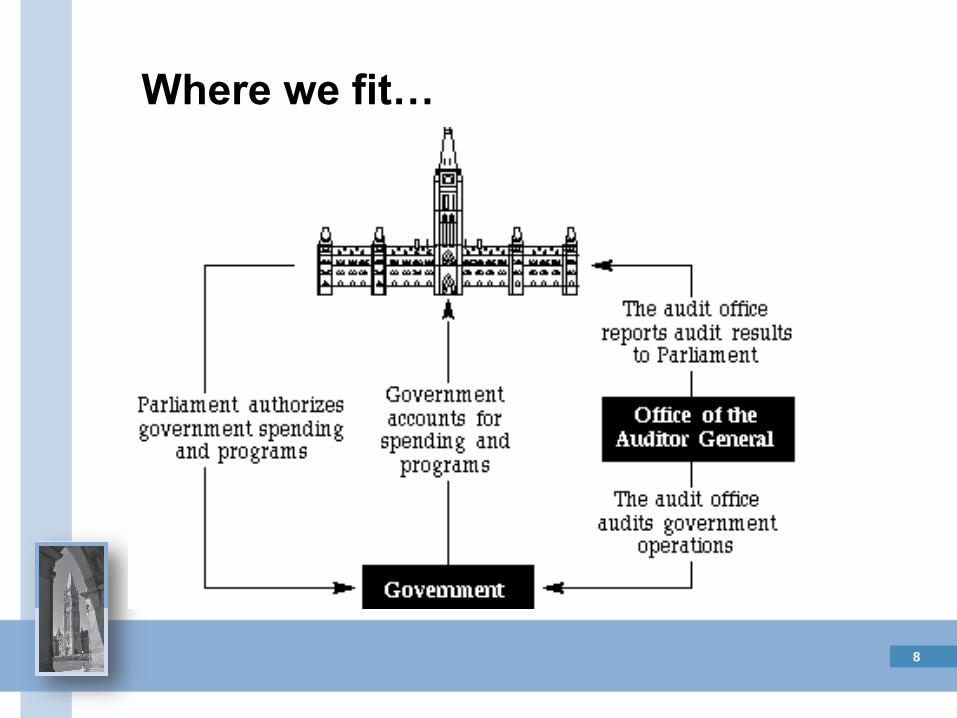

What we do

We serve Parliament

• One of Parliament’s main jobs is to hold the federal

government accountable for its use of taxpayer dollars.

• To provide effective scrutiny and oversight, MPs and Senators

need objective, fact-based information about how well the

government spends and manages public funds.

• The Auditor General serves Parliament by providing

objective and reliable information about government

operations, gathered through audits.

5

What we do…

We are legislative auditors

• We audit federal government departments and agencies,

most Crown corporations, and many other federal

organizations, as well as the northern territories.

• The work we do is called legislative auditing because it

provides objective information that legislatures can draw on to

hold government to account for its spending and performance.

6

What we do…

• We report publicly to the House of Commons on matters the

Office believes should be brought to the House’s attention.

• We testify before parliamentary committees on our audits.

7

Safeguards to Independence

Independence from government is vital to our credibility and to our ability to provide objective information.

The Auditor General

– is appointed for 10 years and can be removed only by both the Senate and House of Commons;

– can choose what, when, and how to audit;

– has the right to access any information required to conduct an audit;

– has the freedom to recruit his or her own staff; and

– reports directly to Parliament through the Speaker, not a government minister.

8

Where we fit…

9

Types of legislative auditing

Financial auditing

– Annual audit of summary financial statements of the Government of Canada (included in Public Accounts of Canada) and the three territories

– Annual audits of Crown corporations and other entities (federal and territorial)

Performance auditing

– 25-30 audits of federal departments and agencies each year

Special examinations of federal Crown corporations

– At least once every 10 years for each Crown corporation

10

Types of auditing…

Financial audits

• Indicate whether the government is keeping proper

accounts and records, and presenting its financial

information fairly.

• Offer assurance on the credibility of government

financial reports.

11

Types of auditing…

Performance audits

• Assess whether government programs are being

managed with due regard for economy, efficiency and

the environment, and have measures in place to

determine effectiveness.

• Examine management practices, controls and reporting

systems, and compare them to the government’s own

policies and best practices.

• May comment on policy implementation, but not on

policy itself.

12

Types of auditing…

Special examinations of Crown corporations

• A type of performance audit that is required at least once every 10 years.

• The Auditor General provides an opinion on the management of the corporation as a whole.

• Reports go to the corporations' boards of directors.

• Crown corporations are required to make these reports public by posting them on their website.

13

More on performance auditing…

• Performance audits are the most visible of our audits since they are tabled in Parliament twice a year and receive wide media coverage.

• Planning of audits begins several years in advance.

• Audits may cover:

– a single government program or activity, e.g. pesticide regulation;

– an area of responsibility involving several departments or agencies, e.g. protection of cultural heritage; or

– an issue that affects many departments, e.g. security of information technology.

14

More on performance auditing…

• We select audit topics on the basis of risk, significance, interest to parliamentarians, and available resources.

• We do not audit topics that fall outside our mandate. These include policy decisions (which are the prerogative of Parliament and government), areas under exclusive provincial or municipal jurisdiction, and the affairs of First Nations.

• We pay particular attention to requests for audits from parliamentary committees, but the ultimate decision about what to audit rests with the Auditor General.

15

Sectoral audit topics

• Aboriginal Affairs

• Economic Development

• Environment and Sustainable Development (covered by the CESD)

• Financial Management and Control

• Health of Canadians

• Human Resource Management

• International Affairs

• Law and Order

• The North

• Parliamentary and

Government Oversight

• Procurement and Asset

Management

• Revenue Collection

• Science and Technology

• Security and Emergency

Management

• Service Delivery and

Information Technology

• Small Entities

16

How do we ensure the quality of our

audits?

• Auditing standards and highly qualified professionals

• Quality management system

• Code of values and ethics

• Guidance of experts

• Independent assurance

• External reviews

• Staying up-to-date with innovations in legislative auditing

17

Environmental mandate

• In 1995, the Auditor General Act was amended to

create the position of Commissioner of the

Environment and Sustainable Development

(CESD) within the OAG.

• Conducting performance audits on environmental

issues is a key part of our audit work.

18

Commissioner of the Environment and

Sustainable Development

The Commissioner leads a team that

audits government’s management of environmental issues;

monitors and reports how well the federal government is doing in meeting its commitments to sustainable development, including the extent to which federal departments have contributed to meeting the targets and goals set out in the Federal Sustainable Development Strategy; and

administers an environmental petitions process.

19

OAG budget and staff

• Roughly $80 million

• Approximately 600 employees

• Our staff is highly qualified and multidisciplinary. We have accountants, engineers, lawyers, management specialists, information technology professionals, environmental specialists, economists, historians and sociologists.

• All professional staff have graduate or bachelor's degrees and professional designations, and many have additional credentials.

20

OAG Structure

• Auditors are organized into teams assigned to specific sectorial audit topics, departments, agencies, or Crown corporations.

• Several teams make up a Group, which is headed by an Assistant Auditor General (AAG).

• The Auditor General, AAGs, and the CESD form the Executive Committee, which provides overall strategic, professional, and administrative direction for the Office.

21

Structure of the OAG

• Main office in Ottawa, and four regional offices

located in Vancouver, Edmonton, Montreal, and

Halifax.

• Several external committees advise the Auditor

General:

– Panel of Senior Advisors;

– Independent Advisory Committee; and

– Panels of Advisors on Aboriginal Issues.

22

How is the Auditor General held to

account?

• The OAG submits annual spending estimates to Parliament, and the Auditor General goes before the Standing Committee on Public Accounts to explain our spending and discuss the Office’s plans and management practices.

• An external auditor appointed by Treasury Board also audits the OAG’s financial operations every year. The auditor's report is submitted to Treasury Board and tabled in the House of Commons.

23

How is the Auditor General held to

account?

• The OAG voluntarily subjects itself to independent external reviews by peers. – In 1999, an external auditing firm examined our quality

management system for annual audits. – In 2003, an international committee of our peers examined our

performance audit practices. – In 2010, an international committee of our peers led by the

National Audit Office of Australia examined all three of our main audit practices.

• The OAG voluntarily subjects itself to internal audits and they are made public.

• The OAG is subject to review by other Officers of Parliament (e.g.: Privacy, Information, etc.)

(The reports are posted on our website.)

24

Working together for better government

• Parliament, the Auditor General and the federal government have distinct powers and responsibilities.

• Working together, all three can help improve the management of government programs and services, and the way government accounts to Parliament and Canadians.

25

Working together for better

government…

Parliament

• Parliament holds the government to account through its system of parliamentary committees.

• These committees may review Auditor General reports, summon departmental representatives to hearings, and make recommendations for action.

26

Working together for better

government…

Office of the Auditor General

• We audit significant issues and report what we find to

Parliament. We report good practices, areas requiring

attention, and make recommendations for improvement.

• The OAG cannot compel the government to implement its

recommendations.

• We carry out selective follow-up audits two or more years

after a report to assess whether or not departments have

made satisfactory progress in addressing issues we raised.

27

Working together for better

government…

Federal Government

• The government sets priorities, and provides

programs and services to Canadians according to

the direction set in laws passed by Parliament.

• It may also implement changes recommended in

Auditor General reports.

28

Working together for better government…

Relation to Internal Audit -

a shared view on the value of audit

• Whether a legislative auditor or internal auditor we have a

number of shared objectives – Solid audit work adds value to the organizations we serve

– Good government

– Sound stewardship of public funds

– Improvement in management practices

– Assurances to Parliament on what is working well, and what needs improvements

29

Working together for better government…

Coordinating our work

• To avoid duplication and minimize the audit burden on

departmental managers

• Where possible, we would like to rely on the work of

internal audit

• Reliance on the work of IA works best when

– It is coordinated at the time audit plans are developed

– Scope, timing and approach is consistent

• It does require us to do some work to justify our reliance

on the work of internal audit

30

Working together for better government…

Reliance on the work of internal audit

• Requires that we assess the internal audit activity in

terms of

– Organizational status

– Scope of the function

– Knowledge and competence

– Due care

31

Working together for better

government…

Parliamentary Committees

• AG Reports and Public Accounts tabled in the House of

Commons are automatically referred to the Public Accounts Committee.

• CESD reports go to the Environment and Sustainable Development Committee.

• Parliamentary Committees hold public hearings on OAG findings, and ensure departments respond to identified concerns.

• The OAG participates in an average of 25 to 35 committee hearings a year.

32

View of parliamentarians

• In past surveys, parliamentarians have said that our

audits added value and are an important source of

information for supporting their committee work.

33

Does government ever improve?

• Since we launched our Status Report in 2002, we

have reported that departments have made

satisfactory progress in more than half of our

follow-up audits, with the exception of

environmental issues.

• In general, things do change for the better.

34

To sum up…

• The OAG is a world leader in legislative auditing.

• We are proud to play our part in helping

government improve.

35

For more information

Please visit our website:

www.oag-bvg.gc.ca