world bank documentdocuments.worldbank.org/curated/en/272101468311976258/pdf/multi0page.pdf · 100...

TRANSCRIPT

RESTRICTED

FILE COPY Report No. AE-27

This report is for official use only by the Bank Group and specifically authorized organizationsor persons. It may not be published, quoted or cited without Bank Group authorization. TheBank Group does not accept responsibility for the accuracy or completeness of the report.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

THE ECONOMIC DEVELOPMENT

AND PROSPECTS

OF

THE SUDAN

(in four volumes)

VOLUME IV

ANNEX 3: THE TRANSPORT SECTOR

June 9, 1972

Eastern Africa Department

Pub

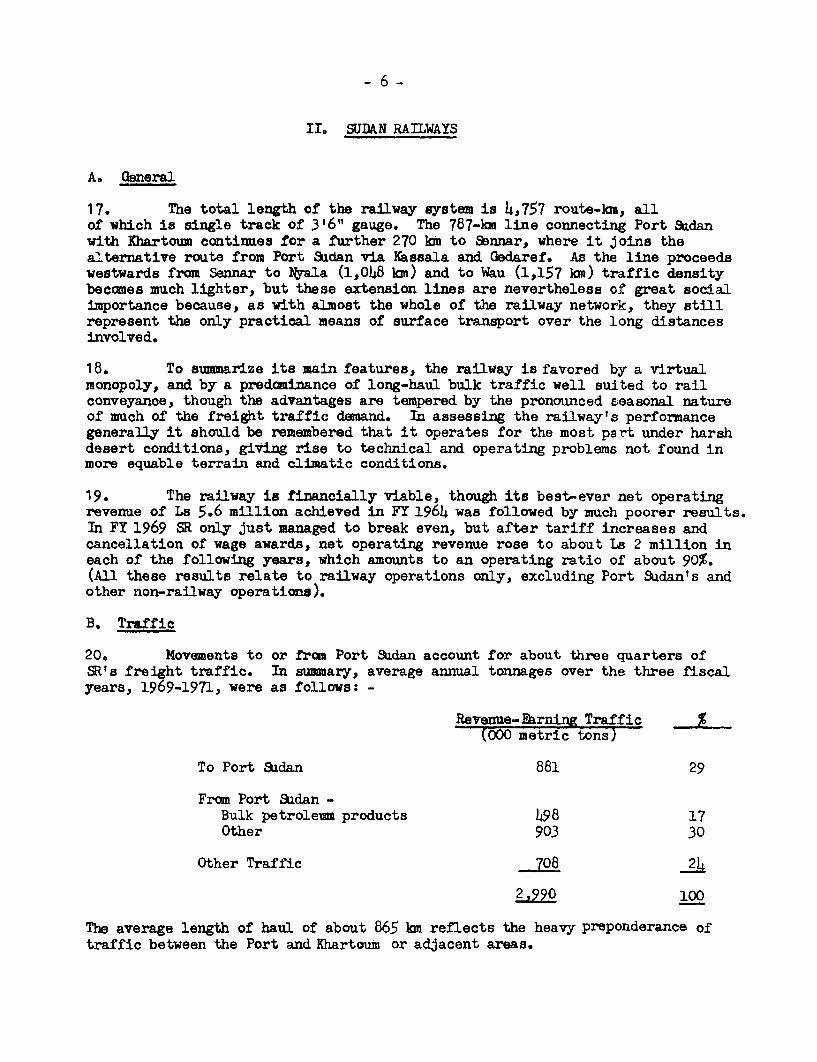

lic D

iscl

osur

e A

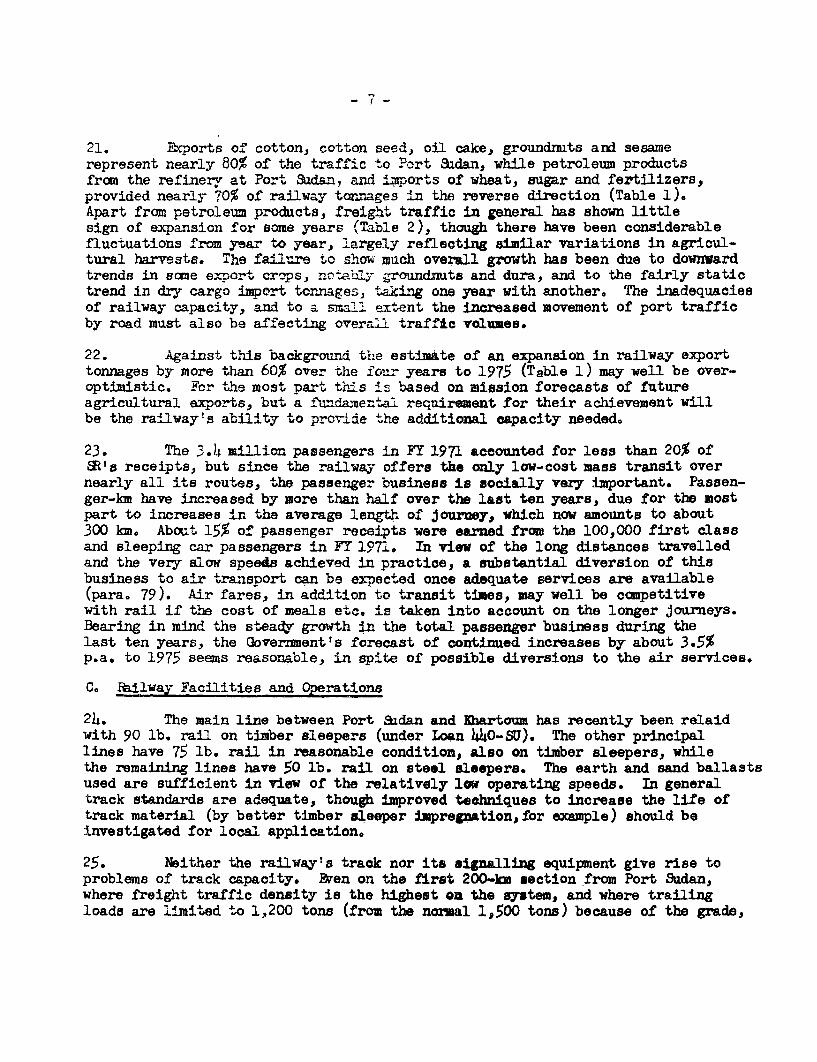

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

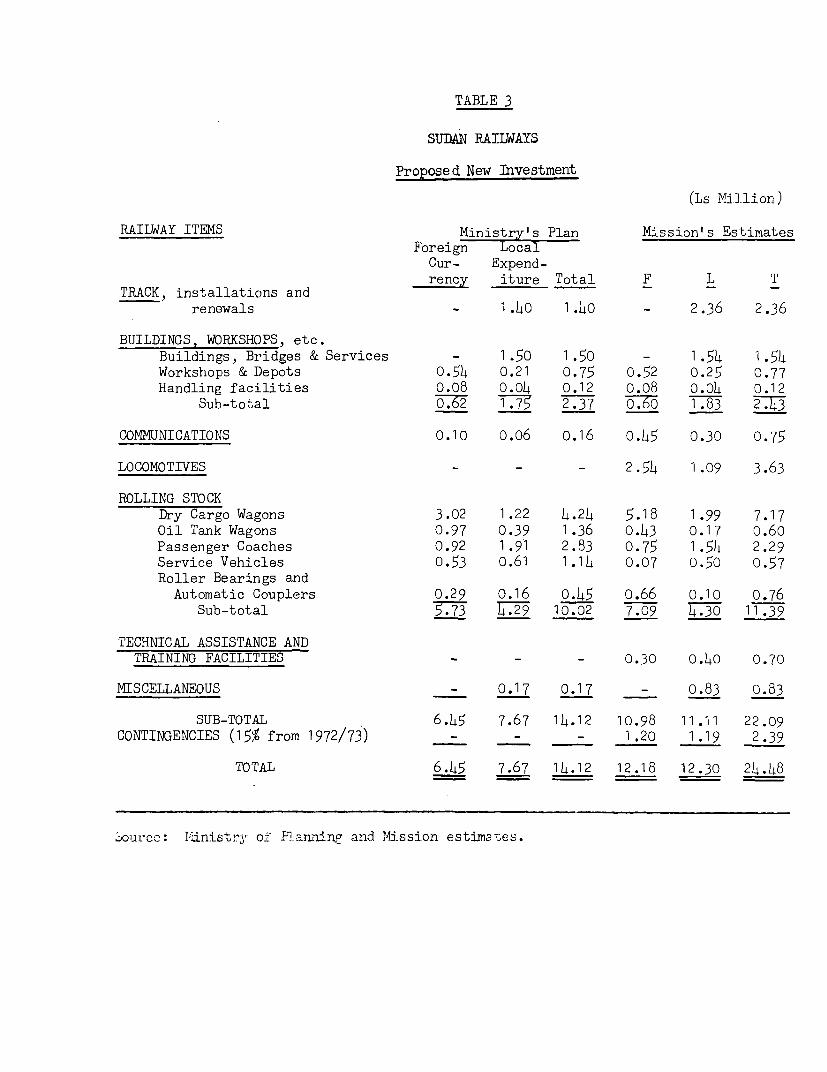

e A

utho

rized

EQUIVALENTS

Currency

100 Sudanese Piasters 1 L Sudan1 L Sudan (Is or Ls) = U.S. $2.8721 U.S. $ 5 3.8 Piasters

Area

1 Feddan = 1.0.38 acres

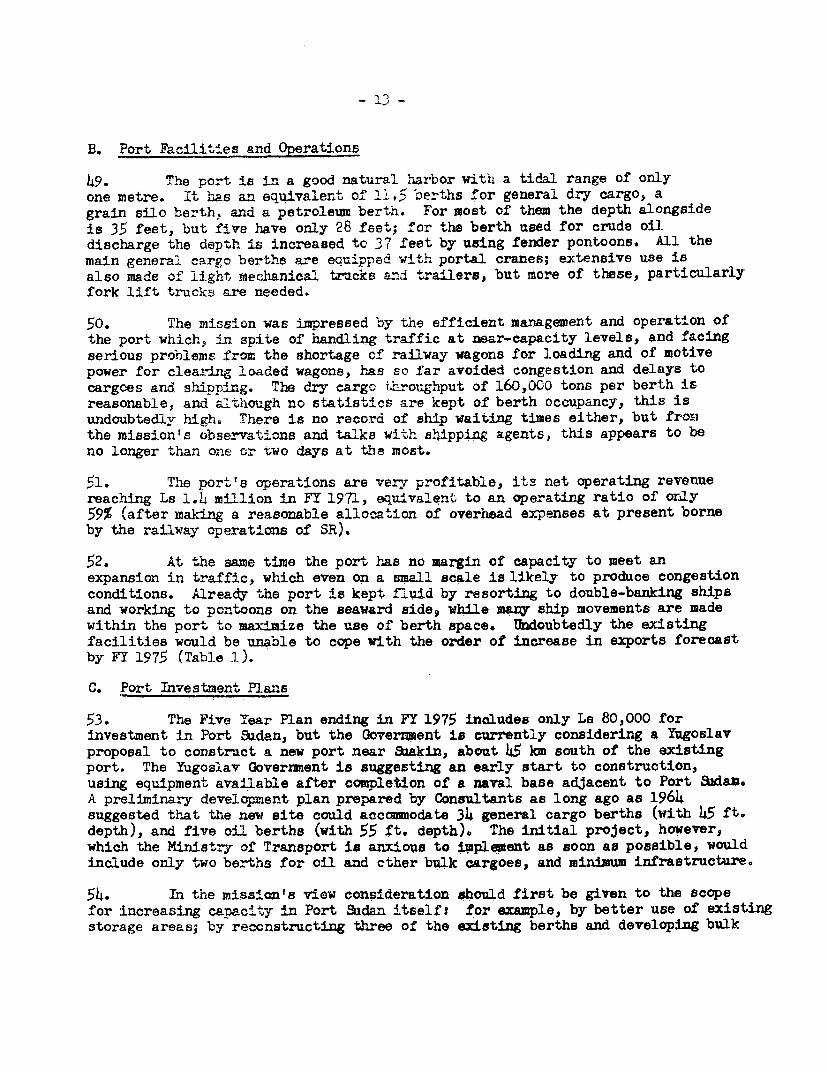

Weight

1 Bale = L20 lbs. (approx.)1 large Kantar = 315 lbs.Tons are short tons of 2,000 lbs., unless otherwisestated.

THE MISSION

This report is based on the findings of a mission which visitedthe Sadan during November and December, 1971. The mission consisted ofthe following:

Kudlapur G.V. Krishna Chief of MissionShawki Farag General EconomistShankar Acharya Economist - Public EnterprisesM. Altaf Hussain Agricultural EconomistDonald H. Bickers Transportation EconomistRobert W. MacDonald Financial AnalystF.D.T. Reid Highway EhgineerJames M. Kesson

(Consultant) Railway Ehgineer

Messrs. Stanley Please (Economic Program Department), A. Sani ELDarwish (Industrial Projects Department) and Vialil E. Nougaim (DevelopmentFinance Companies Department) also joined the mission for brief periods inan advisory capacity.

The principal author of this volums is Dbnald H. Bickers.

THE EOONDMIC DEVELOPMENT AND PROSPECTS OF THE SUDAN

VOLUME IV, ANNEX 3

THE TRAUSPORT SECTOR

TABLE OF CONTENTS

Page No.MAP

SUMMARY

I. THE SECTOR AS A WHOLE

A. General 1B. The Imediate Problem of Railway Capacity 2C. Organization 4D. The Five Year Development Plan, FY 1971 4

to 1975

II. SUDAN RAILWAYS 6

A. General 6B. Traffic 6C. Railway Facilities and Operations 7D. Management and Staff 9E. The Railway's Investment Plan 10

III. PORT SUDAN 12

A. General 12B. Port Facilities and Operations 13C. Port Investment Plans 13

IV. THE SUDAN SHIPPING LINE 15

V. INIAND WATERWAYS 17

VI. ROADS 19

A. Road Construction and Maintenance 19B. Road Vehicles 20

VIIo AVIATION 21

VIII. RECWMMENDED ACTION 24

APPENDIX - SrATISTICAL TABLES

CHART

ARAB REPUBLIC -

SUDAN OF EGYPT _

MAIN TRANSPORTATION di i°Jollo

INFRASTRUCTURE ._'.a,a'~ River service ''

, Railway ' N r . \SLcon

t Airport N O R T H RN- - -Bituminous surfaced roads N jor la

Roads and trocks, ail season K arna ...-I7 " loSt '',.

Roads and tracks, dry seoson Ti

-. - International boundaries A.ta :.DARFUR Provinces < **a]'!.-\ 9

....... Provincial boundaries ................ .... . .Shard.- ..

%t National capital u \

% Proviniol capital * Jt Towns and villages .KHARTC . t h;

( ', B. h, d W M edan,

i#ClV r.u-elcaf er b tI, -F > , MARRA -> S lZb

I J R~~~~~~~~~~~~~~~~~"

1 ' Zolinslel s _ _ a > g <^ 9 1> F A N , iT' 0 donoit $

J '. t ~~~~~~~~~~~/ K 5- -2z~2., N . 5> ,i' ^, > 9' . { *- h a~~~~~~~~~Saa can'

C E N T R A L .: i /: 3" ..) /E ~N'

| ~AFRfCAN !;;^t ; k1-

O1 100 iOS 300 4CS 0 R,g 9'' ,-'E TH!O PI Alrtomeofroo7aB AriR E L erG HCA ZAL f U P P E R

o.ein~~ ~ ~ ~ ~ 'or'a-vrr<jrJ- "-- to t'tTARA-

C t,5> ! . \ ~~~~~~~~~~~N I L E

( ~ ~ ~ ~ ~ ~ ~~ gN~ EN ra.n a

R-b~~~~~~~~~~~~~~7

I adoE , U A O R I A

N F "'~ R,* I C A t 0 mS /R 4&Z A IR*

-SUDAGANDA .

MARCIS 1972 I1RD 3803

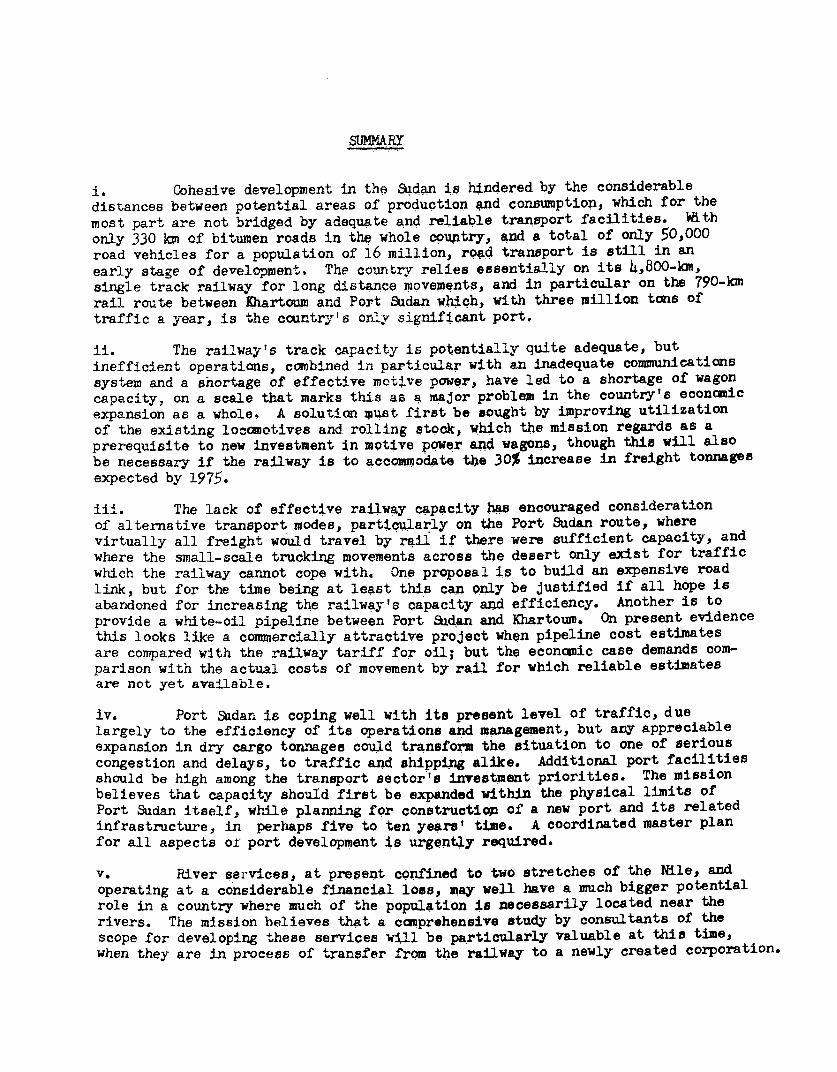

i. Cohesive development in the Sadan is hindered by the considerabledistances between potential areas of production and consumption, which for themost part are not bridged by adequate and reliable transport facilities. Withonly 330 km of bitumen roads in the whole country, and a total of only 50,000road vehicles for a population of 16 million, road transport is still in anearly stage of development. The country relies essentially on its 4,800-km,single track railway for long distance movements, and in particular on the 790-kmrail route between Khartoum and Port Sudan which, with three million tons oftraffic a year, is the country's onLy significant port.

ii. The railway's track capacity is potentially quite adequate, butinefficient operations, combined in particular with an inadequate communicationssystem and a snortage of effective motive power, have led to a shortage of wagoncapacity, on a scale that marks this as a major problem in the country's economicexpansion as a whole. A solution must first be aought by improving utilizationof the existing locomotives and rolling stock, which the mission regards as aprerequisite to new investment in motive power and wagons, though this will alsobe necessary if the railway is to accommodate the 30% increase in freight tonnagesexpected by 1975.

iii. The lack of effective railway capacity ha.s encouraged considerationof alternative transport modes, particularly on the Port Sudan route, wherevirtually all freight would travel by rail if there were sufficient capacity, andwhere the small-scale trucking movements across the desert only exist for trafficwhich the railway cannot cope with. One proposal is to build an expensive roadlink, but for the time being at least this can only be Justified if all hope isabandoned for increasing the railway's capacity and efficiency. Another is toprovide a white-oil pipeline between Port Sudan and Khartoum. On present evidencethis looks like a commercially attractive project when pipeline cost estimatesare compared with the railway tariff for oil; but the economic case demands com-parison with the actual costs of movement by rail for which reliable estimatesare not yet available.

iv. Port Sudan is coping well with its present level of traffic, duelargely to the efficiency of its operations and management, but any appreciableexpansion in dry cargo tonnages could transform the situation to one of seriouscongestion and delays, to traffic and shipping alike. Additional port facilitiesshould be high among the transport sector's investment priorities. The missionbelieves that capacity should first be expanded within the physical limits ofPort Sudan itself, while planning for constructiop of a new port and its relatedinfrastructure, in perhaps five to ten years' time. A coordinated master planfor all aspects of port development is urgently required.

vs River services, at present confined to two stretches of the Nile, andoperating at a considerable financial lots, may well have a much bigger potentialrole in a country where much of the population is necessarily located near therivers. The mission believes that a comprohensive study by consultants of thescope for developJng these services will be particularly valuable at this time,when they are in process of transfer from the railway to a newly created corporation.

- ii -

vi. The Five Year Plan ending in FY 1975 rightly gives much moreemphasis to road constructioi than in earlier years. Even more important isthe need to expand the quite inadequate scale and quality of road maintenance.An IDA credit now under consideration would provide funds and consulting ser-vices to strengthen the Department of Roads, to finance equipment and materialsfor road maintenance, betterment and rehabilitation works, and to carry outpreinvestment studies as a basis for defining investment priorities.

vii. The future operations of Sudan Airways will be confined to domesticand regional services. This will require significant investments to improvethe domestic airports, and in particular to provide night landing facilities,which are now only available at Khartoum. A feasibility study of improvementsat twelve airports is at present under review.

viii. A sumary of transport investment requirements, and of actionrecommended by the mission, is given in Chapter VIII.

I. THE SECTOR AS A WHOLE

A. General

1. Economic development in the Sudan has been concentrated substan-tially on an area within 400 km to the south and east of Khartoum. Onereason is the combination of good soils and water from the White and BlueNiles and their tributaries, but another crucial factor is that this regionis relatively close to the country's only coast line on the Red Sea, and toits only significant seaport at Port Sidan, The fact that most of the areais still more than 800 km from Port Sudan, and separated from it by almostuninhabited desert, serves to emphasize the severe constraint of distance,even where transport facilities exist, on the development of more remoteparts of the country, which is the biggest in Africa. In the south a hugeregion offers fertile soils and adequate water for agriculture, but since itlies some 2,000 km from Port Sudan, its development depends on success inproviding import substitutes for other. parts of the country such as timber,sugar and coffee, or on easily transportable exports such as processed tea.In the west the Jebel Marra area has been identified by FAO experts as offeringconsiderable potential for horticultural and other crops, but although lessthan 200 km from the nearest railhead at INrala, it is 1,400 km from Khartoum,and over 2,000 km from Port 9udan, and air transport offers no solution at thepresent level of costs.

2. In view of the development of areas close to Khartoum, it is notsurprising that traffic by rail, by far the country's most important transportmode, is also heavily concentrated on the routes connecting this region toPort Sadan. In terms of ton-km, nearly 60% of freight traffic on &adan Railways(SR) moves on the main line between the Port and 1hartoum, which accounts foronly 17% of the railway's total network. The two linea from Port Sudan, one viaKhartoum and the other via Kassala, together account for three quarters of SR'stotal freight traffic. In contrast the Western and Southern Etension lines toDrala and Wau, which increased SR's route-km by one third when completed in1961, carry only about 8% of total ton-km, and have an average freight trafficdensity of only about 180,000 tons a year compared with nearly two million tonsover the Port S9dan - Khartoum route.

3. The railway's monopolistic position haa not been significantlyaffected by the development of other modes. Modern highways only exist on anextremely small scale, the only serious competition with rail being confinedto one route between Khartoum and %d Medani, where the 186-km highway accountsfor over half the total 330 km of bitumen road in the whole country. A majorexpansion of road construction is plaenned, but the first need is for feederroads to the railway rather than highways competing with it. The only two reg-ular river services, to Juba in the south, and between Karima and Dongola inthe north, do not compete with the railway, but serve as extensions fram it.Internal air transport offers strong competition in the superior-class passengerfield, but has no material impact on the 97% of rail passengers travelling atlower fares. Domestic air freight is insignifioant.

B. The Immediate Problem of Railwa, Capacity

4. Sudan Railways have played a crucial role in the country's develop-ment from a subsistence economy, and the continuing situation of almost completedependence on the railway emphasizes the need for adequate rail facilities asa prerequisite for future economic development. The mission was given evidencefrom many quarters, however, of the railway's inability to provide satisfactoryservice, and in particular to offer sufficient capacity to meet traffic demands.If railway operations were reasonably efficient the capacity of the track itselfwould be more than adequate. The chief complaint, expressed by all the shippersinterviewed, concerned the difficulty of obtaining empty wagons for loading,though two of the prime reasons for this - the shortage of motive power and pro-tracted Journey times - were themselves the direct source of other complaints.

5. A partial solution to the capacity problem might be sought byencouraging shippers, and exporters in particular, to limit their demands onthe railway during the peak months. Seasonal differentials in railway tariffsmight be considered, and the more extensive use of storage to divert m)re trafficto the off-peak months is a subject deserving close investigation. A itudy of thestorage question by the Ministry of TranBport and the railway is now iunderway.In FT 1971 the railway tanage of exports via Port 9udan was nearly 60% higher inthe six months from January to June than during the rest of the year, in spite ofthe fact that peak traffic was limited by the railway's inability to carry all thetraffic offered.

6. To even out peak demands, however, would not provide a complete answer,and indeed it now seems that the railway is finding difficulty in providing evenfor the off-peak requirements. Daring the "off peak" months starting July 1971,for example, railway movements of petroleum products from the refinery at PortSudan fell so far short of requirements that by the beginning of December the oilcompanies' bulk stocks amounted to only 24% of their up-country storage capacity,compared with 63% a year earlier. January to June is the peak period for salesof petroleum products as well as for the railway, so it appeared that a specialeffort would be needed to avert a fuel shortage, just at the time when the demandsof other railway traffic were reaching their seasonal maximum.

7. As another example, the mission was informed that exports of chromeore, which are not affected by the peak, could be increased from 10,000 to about100,000 tons a year except for the railway's inability to cope with such a volume.Again, a recent shortage of cement was said to be due essentially to the insuf-ficient supply of railway wagons, which eventually made it necessary to curtailcement production.

8. Frcm the public corporations and private merchants in the agriculturalsector, the mission received numerous accounts of export crops deteriorating,missing markets, or being sold at low prices locally, because no transport wasavailable. Merchants in Khartoum pointed out that with the road rates to PortSudan very much higher than the railway's they only use road transport as a lastresort, while the value of many export crops is so low that they either move byrail or not at all. Others in Wau, importing dura (sorghum) and other produceinto the area, maintained that when a railway wagon was eventually obtained the

- 3 -

railway journey could frequently be measured in terms of many weeks rather thandays.

9. Accepting that evidence from railway customers is not necessarilyobjective, the fact that some 1,300 road vehicles a month are carrying freighttraffic to and from Port &udan is itself an undoubted result of the railway'sinability to provide an adequate service. The track across the desert is sopooIr that no private cars and no trucks larger than five or six tons capacityattempt the 790-km journey between Khartoum and Port 9hdan. The truckerscharge rates varying between about Ls 15 to La 20 per ton for good-loading importtraffic, and Ls 4 to La 7 per ton for back-loads of exports. These are usuallymuch higher than the equivalent rail rates, which vary between about La 2 andLs 7 per ton depending on the commodity, but irrespective of the direction offlow. The road service owes its existence solely to the current shortcomings ofthe railway, and could hardly survive if a reasonably prompt and reliable railservice were available.

10. The great importance to the economy of the route to Port Sudan, andthe frustration of shippers with the railwa'1s performance (aggravated by therailway's lack of proper customer relations), haa led to pressure for developmentof alternative transport facilities between the Port and the main producing andconsuming areas. One possibility is to extend the proposed Wad Medani - Gedarefroad for a further 770 Im to Port 9udan (para. 71). Detailed engineering forthis section by Italian consultants is already available, and the Government wouldlike to have the whole road completed as soon as possible. In the mission's view,it would not be reasonable to accept the railway's present shortcominga as a per-manent feature, and to allocate a high priority to this road accordingly. North ofKassala it would carry virtually no local traffic, while the distances to Port9adan from Kassala (550 km), Gedaref (770 km), Wad Medani (1,000 km) and Khartoum(1,200 kim) would mean that movement costs would be prohibitive to most export andimport traffic so long as the competing railway could maintain a moderate standardof efficiency.

11. A second proposal under study is to construct an oil pipeline parallelto the railway for most of the distance between Port 32dan and Xhartoum. Thelatest study (by Parsons Brown) recomends an 8" pipe to carry refined fuels otherthan fuel oil, which would continue to be rail-borne. Movement of these productsfrom Port Sadan is expected to amount to 450o,000 tons p.a. by 19741, after deduct-ing flows to deatinations for which transfer to the pipeline would be impracticable.Diversion of this traffic dould be serious for the railway which, however, isempowered by law to operate a pipeline itself, or alternatively could be conpen-sated for the loss of revenue, as recommended by the Consultants. Capital costsof the proposal are estimated at La 6.35 million and operating costs, initially,at La 314,000 a year. On a crude calculation, assuming a 20-year life for thepipeline, and interest charges of 10% p.a. these estimates amount to a cost ofLa 2.11 (US$6.1) per ton at 450,000 tons a year. From the oil companies' pointof view, the average rail charge that would be saved by shipment through thepipeline, and where necessary on-forwarding traffic by rail from take-off points atAtbara and Khartowm, would be Ls 4.40 (US$12.6) per ton at current railway ratelevels. The railway's tariff for this traffic, however, is set without regard tothe costs attributable to its movement, which may well be much lower than the ratescharged. It would be dangerous to speculate on the relative economics of a pipelineon the basis of simple comparison with the railway's tariff alone.

12. A recent study of the railway's costs and tariffs concludes thatrevenues from oil traffic in wagon loads of 20 tone or more, which account fornearly all the bulk movements, not only cover direct operating costa but alsooffer at least an average contribution to the railway's indirect costs. Theseresults, however, are based on a crude calculation which in far from takingaccount of all the special elements involved in carrying bulk oil. Before enter-ing into a major comituent for a pipeline, comparative railway costo should beestimated in such a way as to refleot the specific costs of tank wagoni, wagonturnaround times between particular points., train loading, terminal conts, eto.An attempt should also be made to judge the effect. of reasonable and praotioalimprovements in railway effioieneV on the estimates of present oil traffic costs.It is necessary in addition to stimate the railway expenditure that wouldreally be saved as a result of diverting oil traffic to a pipeline: For example,the capital costs of the existing tank wagon fleet would not be saved by uchdiversion, which would only allow the railways to escape from future tank wagonpurchases. A. proper analysis of railway expenditures on such a basis might wellaffect the optimum timing for construction of the pipeline. So far there hasbeen no attempt to investigate the railway's costm in this way, though this shouldbe regarded as an essential supplement to the existing studies. The m .asionrecammends that for this purpose a specialist in railway traffic costi-ug shouldbe engaged for a short period, And that a decision on the pipeline should awaithis conclusions.

C. Organization

13. A major reshaping of Government administration for transport is atpresent underway, and in some respects is still at the planning stage. In general,it amounts to a praiseworthy move to coordinate nearly all the public transportagencies under one Ministry of Tranaport, while at the same time preserving asubstantial measure of autonomy for the individual modes. The Roads Division hasbeen transferred to the Ministry from the former Ministry of Pablic Works, andupgraded to a Department. Only the airports, under the Department of CivilAviation (Ministry of Defense) remain outside the Ministry, though there ie arecent proposal to confine &dan Airways to domestic and regional routes, itsinternational services being tranaferred to a new corporation under the Ministryof Defense. Separate corporations are also being created to take over Port Sadanand the river services from &xdan Railways. The railway's hotels have alreadybeen transferred to a new corporation.

D. The Five Year Development Plan, FY 1971 to 1975

14. The Government plans public investment expenditure of about La 48million in the transport sector during the five years ending in FY 1975, whichwould be more than twice that achieved during the previous five years. Althoughexpenditure of at least this order is likely to be justified, there must bedoubts on the practical scope for implementing the ambitious program, which wouldincrease the transport sector's share of total public investment to 18%, comparedwith 16% in the last five years. In summary the comparison is as follows:

(La Million)

Estimated Actual ProposedInvestment Investzment

FY 1966 to 1970 FY 1971 to 197 DifferenceRailways 14.1' -1 L' Z1- 1E7Port %dan le4 0.1 - 1.3Inland Waterways o.4h 0.8 + 0.4Road Construction 2.0 23.3 +421.3Airports and Air

Navigation 0.3 1.3 + 1.0Sudan Airways 1.9 5.0 + 3.1Sudan Sipping Line + 3.5

21.8 L +26.3

15. Investnent in the in)dividual modes is considered in the followingchapters. Sane of the major featu,res of the Plan are the sharp increase inproposed expenditure on road construction, which is badly needed; a majorexpansion in the Sadan Sipping Line's fleet, which is probably justified inpresent circumstances; and replacement aircraft for international services,an item that would be difficult to defend on grounds of commercial viability.In spite of the overall increase in proposed spending, it is intended tocut back investment in the railway and Port &udan. The mission feels thereis a strong case for increasing the allocation to the railway, and that majornew port investment will soon be esEential, though most of the latter will falloutside the Plan period.

*16. It should be noted that all amounts shown in the Government's FiveYear Plan include import duties. In the case of the railway inveatment, forexample, these amoumt to scome Ls 2.6 million of the Ls 14.1 million.

- 6 -

II SUDAN RAILWAYS

A. General

17. The total length of the railway system is 4,757 route-km, allof which is single track of 316"? gauge. The 787-kn line connecting Port 9danwith Khartoum continues for a further 270 km to Sennar, where it joins thealternative route from Port 9udan via Kassala and Gbdaref. As the line proceedswestwards from Sennar to 1Nyala (1,048 km) and to Wau (1,157 km) traffic densitybecomes much lighter, but these extension lines are nevertheless of great socialimportance because, as with almost the whole of the railway network, they stillrepresent the only practical means of surface transport over the long distancesinvolved.

18. To simmarize its main features, the railway is favored by a virtualmonopoly, and by a predominance of long-haul bulk traffic well suited to railconveyance, though the advantages are tempered by the pronounced seasonal natureof much of the freight traffic demand. In assessing the railway's performancegenerally it should be remembered that it operates for the most part under harshdesert conditions, giving rise to technical and operating problems not found inmore equable terrain and climatic conditions.

19. The railway is financially viable, though its best-ever net operatingrevenue of La 5.6 million achieved in FY 1964 was followed by much poorer results.In FY 1969 SR only just managed to break even, but after tariff increases andcancellation of wage awards, net operating revenue rose to about Ls 2 million ineach of the following years, which amounts to an operating ratio of about 90%.(All these results relate to railway operations only, excluding Port Sudan's andother non-railway operations).

B. Traffic

20. Movements to or from Port Sudan account for about three quarters ofSR's freight traffic. In simuary, average annual tonnages over the three fiscalyears, 1969-1971, were as follows: -

Revenue-Ehrnine Traffic _(000 metric tons)

To Port S9dan 881 29

From Port Sudan -

Bulk petroleum products b98 17Other 903 30

Other Traffic 708 24

2,990 100

The average length of haul of about 865 km reflects the heavy preponderance oftraffic between the Port and Khartoum or adjacent areas.

21. Exports of cotton, cotton seed, oil cake, groundnmts and sesamerepresent nearly 80% of the traffic to Port 3adan, while petroleum productsfrom the refinery at Port Sudan, and Jmports of wheat, sugar and fertilizers,provided nearly 70% of railway tornages in the reverse direction (Table 1).Apart from petroleum products, freight traffic in general has shown littlesign of expansion for some years (Table 2), though there have been considerablefluctuations from year to year, largely reflecting similar variations in agricul-tural harvests. The failure to show much overall growth has been due to downwardtrends in same export crops, notably- groundnuts and dura, and to the fairly statictrend in dry cargo import tonnages, taking one year with another. The inadequaciesof railway capacity, and to a small extent the increased movement of port trafficby road must also be affecting overall traffic volumes.

22. Against this background thrze estimite of an expansion in railway exporttonnages by more than 60% over the four years to 1975 (Table 1) may well be over-optimistic. For the most part this is based on mission forecasts of futureagricultural exports, but a fundamental requirement for their achievement willbe the railway's ability to provide the additional capacity needed.

23. The 3.4 million passengers in FY 1971 accounted for less than 20% ofSRts receipts, but since the railway offers the only low-cost mass transit overnearly all its routes, the passenger business is socially very important. Passen-ger-km have increased by more than half over the last ten years, due for the mostpart to increases in the average length of journey, which now amounts to about300 km. About 15% of passenger receipts were earned from the 100,000 first classand sleeping car passengers in FY 1°71, In view of the long distances travelledand the very slow speeds achieved in practice, a substantial diversion of thisbusiness to air transport can be expected once adequate services are available(para. 79). Air fares, in addition to transit times, may well be competitivewith rail if the cost of meals etc. is taken into account on the longer journeys.Bearing in mind the steady growth in the total passenger business during thelast ten years, the Government's forecast of continued increases by about 3.5%p.a. to 1975 seems reaso.nable, in spite of possible diversions to the air services.

C. Railway Facilities and Operations

24. The main line between Port Sidan and Khartoum has recently been relaidwith 90 lb. rail on timber sleepers (under Loan 440-SU). The other principallines have 75 lb. rail in reasonable condition, also on timber sleepers, whilethe remaining lines have 50 lb. rail on steel sleepers. The earth and sand ballastsused are sufficient in view of the relatively low operating speeds. In generaltrack standards are adequate, though improved teohniques to increase the life oftrack material (by better timber sleeper impregnation, for example) should beinvestigated for local application.

25. Neither the railway's track nor its signalling equipment give rise toproblems of track capacity. &en on the first 200-km section from Port Sudan,where freight traffic density is the highest on the system, and where trailingloads are limited to 1,200 tons (from the normal 1,500 tons) because of the grade,

- 8 -

the mission considers that the number of train movements could be increasedby about 50% with eziating facilities. Additional crossing loops are atpresent uzmecesoary, but could be installed without difficulty if further linecapacity is eventually required, while the length and weight of trains couldbe increased simply by double-heading or employing more powerful locomotives.

26. In spite of operating well below potential line capacity on all itsroutes, substantial delays and late running are an everyday feature of the rail-way's operations. The working timetable bears only remote relationship to actualworking, with the direct result that the effective capacity of the track isreduced, and with the indirect consequence that the poorer utilization of loco-motives, rolling stock and train crews limits their effective capacity as well.

27. The reasons for this situation are numerous and complex. An importantfactor could well be the acoeptauoe of delays by railway staff as an inevitableoperating fact, particularly after a period when morale has probably eroded asfast as their real wages and salaries. The railway's recent annmal reports, inrecording the proportion of trains arriving on time as varying between 3% and 7%,regularly refer to the effects of engine failures, engineering works, sandstormsand heavy rains. In addition the mission feels that a serious handiecp is thelack of adequate telecommunications, and a system of train control that appears torecord events rather-than to have a prompt influence upon them. It is true thatthe railway has to cope with washouts after rainstorms and line blockages or delaysdue to sandstorms, but these cannot be blamed for the daily experience of laterunning. In some sections sand blowing across the track and blocking points isa daily problem, but hardly an insurmountable one.

28. Delays in traffic are a primary cause of the poor diesel locomotiveutilization, which fell from 85,000 train-km per available main line diesel inFT 1964 to under 70,000 train-km in FY 1971. The railway management points outthat, with only 57 diesel units available in the earlier year, compared with79 in 1971, they were allocated to work offering the best opportunities for goodutilization, leaving steam to work the poorer diagrams; but given the long distancesworked by the railway, an average figure of 85,000 train km a year should by nomeans be regarded as an impractical target.

29. The utilization of the 103 main-line diesels (which account for only halfof the main-line locomotives, but for 80% of the train-km) is also impaired bytheir low level of availability. This is currently down to about 70% of the totalfleet due, partly to a shortage of spare parts, and to continuing difficulty withthe cooling system of the fifteen Cockerill-Ougree locomotives. With spares nowarriving, SR believes that availability of the diesel fleet will soon be up to 75%(or to 88% if the Cockerill-Oagree locomotives are excluded). If a satisfactoryimprovement is not achieved, then in view of the critical need for making betteruse of the existing fleet, the mission recommends that SR should seek technicalassistance for its diesel maintenance.

30. A new cooling system fitted to three of the Cockerill-Ougree locomotivesis proving reasonably satisfactory; hence SR is planning to convert six more, butthis cannot be completed before about April 1973. aince this costs about Ls 10,000a unit, which is low in relation to the price of a new locomotive, there is probablya good case for converting all fifteen units even if they are limited to secondaryduties in the longer term.

-9-

31. The fleet of over 5,000 froight wagons (excluding service vehicles)includes 600 tank wagons, and about 550 reserved for non-revenue earning dutiesoThe average wagon loading of over 20 tons is quite high, but with an empty wagonproportion of only 27%, the aver4ge turnarqund time of 10.5 days (over the lastthree years) is disappointing, particularly at a time when there is an unmis-takable shortage of wagon capacity. CGiven this shortage, empty wagon movementsmay well be less than necessary to ensre pr pt service, while the good wggonloading may only emphasize that shippers load as heavily as possible when wagonsare in short aupply.

32. In identifying remedies for the wagon shortage, which will tend toworsen if the forecasts of potential traffic demands are borne out, the firstemphasis should be given to increasing the availability of motive power andimproving the utilization of locomotives in traffic, to avoid the current situa-tion where wagons are standing empty or under load awaiting motive power.

33. The next essential is for An effective means of wagon control, andhere again there is need for a better communications system. The mission believesthat the Government cormittee, set up in. the 1970/71 season to allocate wagonsto traffic in an attempt to avoid the previogs season's shortages, was bound toprove unsuccessful, because it was too far removed from actual operations. Itseems essential that SR should remain responsible for day-to-day wagon allocation,with the Government setting priorities, if neceovary, on a longer-term basis.

34. SR owns about 390 passenger coaches, and about 50 dining and luggagecoaches; in addition there are 200 service coaches and saloons provided principall)for the use of railway staff. Some of these vehicles are undoubtedly justifiedby the needs of operations and railway managepent, but apart from the costs ofproviding and maintaining this fleet, their use of train capacity, at a time whenmotive pOwer is in such short supply, is a matter calling for close attention.

35. The railway workshops at Atbara cover a wide range of activities,including body construction for passenger and freight cars, and the manufactmxreof some 90% of all components required for maintaining the steam locomotive fleet.The variety and sophistication of skills shown by the workshops' staff is impressi-.and should be of considerable value in other employment when the steam locomotivesare phased out, together with much of the railway's need for these technicalaptitudes.

D. Management and Staff

36. SR's management staff give an impression of considerable technicalcompetence as individuals, but there appears to be need for more purposeful andcoordinated planning based on a broader overall view. One reason may well be themanagement organization itself, wh4ch at middle levels seems somewhat diffuse,without clear lines of authority.

37. The mission believes that the management structure and staff positionsshould be reviewed and strengthened, with reference especially to direction andplanning. It is understood that steps in this direction are already being taken,and that technical assistance in this respect would be welcomed.

- 10 -

38. The strong criticism of the railway from Government agencies and thepublic in general (paras. 4 to 9) is accentuated by the lack of adequate communica-tion between the railway and its customers. Local officers say they have noauthority to discuss or follow up customer complaints or problems, but must referthem to headquarters, which is isolated at Atbara, 300 km from Khartoum and farfrom the railway's main customers. The mission was informed of the Governmentintention to relocate the railwayt s headquarters in Khartoum, and to examine thescope for system-wide delegation of customer relations and other functions.

39. The number of SR staff (railway operations only), which has been risingsteadily for some years, has now reached 30,000. This is more than 10% higherthan in FY 1964, when a similar level of traffic was carried. It is understoodthat in the past the Government has insisted on the railway's retention of casuallabor as permanent staff, even after they were no longer required. The intentionis to reduce the number by about 1,000 a year through normal attrition, until alevel of about 25,000 is achieved. The retirement age is now 50 to 55 and shouldnot be lowered further to achieve a faster loss of staff; on the contrary, therailway can ill afford to lose its best personnel between those ages, particularlyin the management grades.

40. There are training schools for new entrants and lower grade staff,while graduates from technical schools are given training as charge hands in theworkshops, and SR's engineers, of university graduate Btandard, are given threeor four years' training, about half of it overseas. Training for lower grades atdepartmental level is uncoordinated, and it is also insufficient for staff advancingthrough the organization, particularly for junior and senior supervisory duties.An I.L.0. expert who recently reviewed the facilities has suggested their reorgan-ization; a new central training school is envisaged. The mission considers thisimportant, and recommends provision for technical assistance and facilities in theinvestment plan.

E. The Railway's Investment Plan

41. The Five Year Plan ending in FY 1975 includes La l million invest-ment expenditure for the railway. The mission believes that to meet forecasttraffic demands this sum might well have to be raised to Ls 24 million (Table 3),but recognizes that expenditure of this order may well be impractical duringthe Plan period. Among the reasons for the increase, the most important isthe mission's proposal to strengthen SR's motive power fleet. The first essen-tial is to improve the availability and utilization of existing locomotives,but it is calculated that even after making reasonable assumptions about improvedefficiency, another fifteen diesel electric locomotives (2,100 hp) are requiredto provide a wore adequate service for existing traffic and to meet projectedtraffic volumes. It is also recommended that some ten new diesel shunters shouldbe added to the existing fleet of 59 to continue the progressive reduction insteam traction.

42. If traffic and other eatimates gre acourate, these additions wouldstill require retention of some 50 existing vax locomotives for main line andshunting operations. The mission would like to oee coRplete elimination ofsteam traction as soon as possible, not oniy to gain the full benefits of moreeconomical diesel traction, but because a combination of steam and diesel locomo-tives considerably increases the difficulties of efficient and low-cost main-tenance. However, in view of the general shortage of investment funds at thistime, and the possibility that the traffic forecasts may prove to be over-optimistic,it seems prudent to plan for full dieoelizat±on by stages, retaining some steamtraction for use or storage as traffic requires.

43. The Plan provides for about 1,400 new freight wagons, but having regardto the traffic forecasts, and after allowing for improved wagon turnaround times,the mission estimates that replacement of some 8QO wagons more than 40 years old,and the addition of a further 900 units (1,700 in total), is likely to be justifiedtAs with the locomotives, this estimate is delberately on the low side, and ifthe forecast of traffic demand is fully re4lizd it is expected that some of theolder units will have to be retained beyonxi the Plan period. The estimate includes100 new 40-ton tank wagons, at a total cost f 4about La 600,000. If a pipelineis constructed between Port Suden and 1baxtQm (pgras. 11 and 12) none of thesewould be needed after it comes into operati>i, bt acme at least would be requiredto meet increased traffic demande in the intqrip yegrs. Since their effectivelife would be very short, the pipeline inveptiption should include a carefulestimate of the minimum wagon needs for this i4trim period.

44la. Also included in the Plq.n are 200 new pan8enger coaches, and provisionfor rebuilding some existing paesenger stok. Accepting that some 80 coachesover 50 years old will need replacement, tbe 1aL4 e of 120 new units, represent-ing a 30% increase in the fleet, seems too h,igh in relAtion to the expectedincrease in traffic; a total acquisition of 120 u4ts should be adequate.

45. Among other items in the Plan, the misaion recommends increased expen-diture on telecommunications. The allocation for track renewals also seemsunduly low. On the other hand some econq.y might be sought in the proposed expen-diture on service vehicles, by making use of the older units due for replacementif necessary.

- 12 -

III. PORT SUDAN

A. General

46. In view of its geographical position, the &Sdan's maritime tradewas particularly affected when the &iez Canal closed in 1967. The consequencesare illustrated by the Cape surcharge on freight rates, which is 50% on trafficto West Ehropean ports and 75% for Mediterranean ports. They are also reflectedin the number of ships calling at Port Sudan, which dropped from 1,254 inFY 1967 to only 756 in F! 1971 , while the average cargo loaded or unloaded atPort &Sdan increased correspondingly from 1,850 tons to 4,200 tonB per shipcalling. The absence of ahipping space previously available from vessels passingthrough the Canial has made it necessary to charter many ships for 9udan trafficalone,itth the result that Port &Sdan is handling whole shiploads of timber,fertilizers and other commodities much more frequently than in the past.

Traffic

47. The Port has handled the following tonnages in recent years:

(000 tona) 2

Extorts Inports TotalFinancial ky Fetrolevm Dry Petroleum Dry Petroleum

Year CArso Products Cargo Products Cargo Products Total

1966 751 135 816 640 1,567 775 2,342

1967 682 148 758 711 1,440 859 2,299

1968 754 137 842 741 1,596 878 2,474

1969 832 113 674 787 1,506 900 2,406

1970 794 136 691 871 1,485 1,007 2,492

1971 900 159 999 1,074 1,899 1,233 3,132

1/ Bunker fuel and transhipped traffic is excluded.

48. The commodity analysis of railway traffic to and from Port Sudan(Table 1) also gives a good indication of the port's traffic. Since the refineryclose to the Pbrt began operations in 1964, the largest single commodity handledhas been imported crude oil. The refinery's capacity was recently increasedfrom a crude intake of 3,050 tons per day to 3,300 tons but, owing to the inadequaterailway capacity for up-country movement, its throughput has been limited to between2,400 and 2,800 tons.

B. Port Facilities and Operations

49. The port is in a good natural harbor with a tidal range of onlyone metre. It has an equivalent of 11.5 berths for general dry cargo, agrain silo berth, and a petroleunm berth. For most of them the depth alongsideis 35 feet, but five have only 28 feet; for the berth used for crude oildischarge the depth is increased to 37 feet by using fender pontoons. All themain general cargo berths are eouioped with portal cranes; extensive use isalso made of light mechanical trucks and trailers, but more of these, particularlyfork lft trucks are needed.

50. The mission was impressed by the efficient management and operation ofthe port which, inl spite of handling traffic at near-capacity levels, and facingserious problems from the shortage ef railway wagons for loading and of motivepower for clearing loaded wagons, has so far avoided congestion and delays tocargoes and shipping. The dry cargo tihroughput of 160,000 tons per berth isreasonable. and altlough no statisics are kept of berth occupancy, this isundoubtedly high. There is no racord of ship waiting times either, but fronthe missions observations and talks with Bl4ipping agents, this appears to beno lorger than one or two days at the most.

51. The port Is operations are very profitabie, its net operating revenuereaching Ls 1. million in FY 1971, equivalent to an operating ratio of orly59% (after making a reasonable allocation of overhead expenses at present borneby the railway operations of SR).

52. At the same time the port has no margin of capacity to meet anexpansion in traffic, which even on a small scale is likely to produce congestionconditions. Already the port is kept fluid by resorting to double-banking shipsand working to pontoons on the seaward side, while iazy ship movements are madewithin the port to maximize the use of berth space. Undoubtedly the existingfacilities would be unable to cope with the order of increase in exports foreoastby FY 1975 (Table 1).

C. Port Investment Plans

53. The Five Year Plan ending in FY 1975 includes only La 80,000 forinvestment in Port &adan, but the Government is currently considering a Yugoslavproposal to constract a new port near Suakin, about 45 km south of the existingport. The Yugoslav Government is suggesting an early start to construction,using equipment available after completion of a naval base adjacent to Port Sadao.A preliminary development plan prepared by Consultants as long ago as 1964suggested that the nenw site could accommodate 34 general cargo berths (with 45 ft.depth), and five oil berths (with 55 ft. depth). The initial project, however,which the Ministry of Transport in anxious to implepent as soon as possible, wouldinclude only two berths for oil and other bulk cargoes, and minimum infrastructure.

54. In the mission's view consideration ghould first be given to the scopefor increasing capaclty in Port Sidan itselfs for example, by better use of existingstorage areas; by reconstructing three of the existing berths and developing bulk

- 14 -

storage facilities on the extensive unused area behind them; and by unloadingcrude oil outside the haz-bor, which would not only release berth apace, butalso eliminate interruptions to dry cargo movement whenever oil is being off-loaded, and reduce the fire hazard in the harbor. By these means it may bepossible to delay for sone years the need for an entirely new port which, togetherwith its rail and road connections and other essential infrastructure, might welldemand a heavy investment overalle It must also be remembered that the conversionof existing berths at Port 9hdan to large-scale container operations could increasetheir capacity to up to a million tons a year per berth and eliminate the need fora new port within the foreseeable future. The development of container servicescannot be initiated by the Sadan Goverrment alone, but any new investments in thefacilities at Port 9udan should certainly be made in the light of possible containeroperations in the future, particularly after the Snez Canal is reopened.

55. The first need is for a comprehensive plan for port development,:toset out the requirements and coordinate the timing of additional facilities atPort Sidan and construction at a new site. No such master plan exists, but themission believes the expansion of port facilities should be considered in threephases as follows:

(i) measures to provide additional storage, lighterage andmooring facilitiea in the existing port area (up toFr 1975);

(ii) reconstruction or provision of additional deep water berths,bulk storage and handling facilities at the existing port(FY 1975 to 1977); and

(iii) initial construction of a new port, or introduction ofcontainerization to meet further capacity requirements(FY 1977 to 19815.

56. The mission estimates that some La 5.5 million would be required inthe Plan period to FT 1975 to complete Phase I and to embark on Phase TI; thelatter will need a further Le 3.6 million for completion after FY 1975 (Table 4).These estimates, which are necessarily very tentative, include provision for amaster plan study and engineering for Phase II.

- 15 -

IV. THE SUDAN SHIPPING LINE

57. The &ez Canal's closure, serious as it is to the Sudan's economy,has created very favorable conditions from the much narrower viewpoint of theSudan Shipping Line, which no longer has to ccopete for cargoes with shipspassing en route for the Canal. In view of its small fleet of only five vessels,however, and the lengthy journey around the Cape (which takes 30 days to WesternEarope compared with only 15 via the Canal), the Line still only carries about100,000 tons (about 6%) of the country's dry cargo exports and imports.

58. The Company was formerly owned in equal shares by the Sudan andYugoslav Governments, but was taken over by the former in 1967. Its shippingcapacity has fluctuated in recent years as follows:

No. Ships Total Fleet Capacity(Gross Registered Tons)

Before October 1970 4 20,000

One ship lost inOctober 1970 3 15,000

Two ships (each of7,000 aRT) acquiredin 1971 5 29,000

Two ships (7 000 and13,000 GRT5 due fordelivery in 1972 7 49,000

The vessels work solely on non-stop services to North Sea and Atlantic portsin l1rope, calling at Hodeidah and Jeddah on the return journey. With thebig expansion in capacity planned for this year a new service to the Far Eastis being considered.

,9. In spite of disruption caused by the loss of one of its 5,000 tonvessels in 1970, the Company's financial results for that calendar year wereas follows:

(Ls 000)

Revenue 2,087&penditure (including

capital servicing) 1,765Net Revenue 322

- 16 -

This was equivalent to an operating ratio of 85%. The good result was duein part to the Company's other profitable activities as shipping agents andin stevedoring, warehousing and chartering. It was also the result of theSuez Canal closure which provided a favorable climate for its shippingoperations. The mission believes, however, that it reflects in addition anefficient management which, since the Company's creation in 1962, has built itinto a sound commercial undertaking. This has been achieved with continuingYugoslav technical assistance, but the Company has not received anv preferentialtreatzment from the Government. (liven this situation, there is prc)ably littlerisk attached to the big increase in the Line's shipping capacity, which hasmore than doubled since the Canal was closed. The reopening will immediatelyresult in much tougher competition, but in view of the Line's small share oftotal 9udanese trade, it should be able to retain a satisfactory proportion inthe future, particularly if the big increases projected in export tonnages arerealized in practice.

- 17 -

V. INLAND WATERWAYS

60. As a means of transportation, the Nile has not achieved the sameimportance in the Sudan as in Egypt. This is partly because it is not sonavigable as in Egypt and could not accommodate, for example, the 900-tontwo-barge units operating between Aswan and Cairo. It is also because freighttraffic is dominated by exports and imports through Port 9udan, which is 450 kmfrom the nearest point of the Dile.

61. The White Nile is nevertheless important as the most practical meansof surface transport between Khartoum and the southern cities of Malakal andJuba. Traffic on this 1,400 km route amounts to about 170,000 passengers a yearand 100,000 tons of freight, nine-tenths of which is in the southerly direction.The imbalance of traffic, together with the use of barges no bigger than 100 tonscapacity, is inevitably reflected in high operating costs per ton. Anotheroperational problem is the obstruction caused by water hyacinth and the hugemarshlands of the Sadd north of Juba. There is also a dam near Khartoum which,though navigable, is frequently closed to shipping to prevent the hyacinth fromspreading downstream. In practice r±ver traffic to the south is transhippodfrom rail at Kosti instead of working through from Khartoum on the river.

62. The only other significant river service is on a 290-km reach in thenorth, from the railhead at Karima to Dongola, which carries about 100,000 passen-gers and 40,000 tons of freight a year. A service from Wadi Halfa northwards intoEgypt was suspended after completion of the Aswan Dam and creation of the NasserLake. The intention was to build a new port on the lakeshore at Wadi Halfa andto offer an improved service to Aswan, but the final water level has not yet beenestablished, because water from the lake is apparently leaking through the sur-rounding strata. In the meantime the only movements into Egypt are by smallprivate vessels.

63. The General Manager for the new corporation for river services wasappointed in October 1971, and full separation from the railways is expected bymid-1972. This move should create the right conditions for revitalizing theriver services, but the new management, although enthusiastic, appreciates thesubstantial problems involved. Financially their operations are continually indeficit, with expenditures half as high again as their annual revenue of aboutLs 1 million. With a total fleet of 250 units (excluding 130 service craft),capacity shortages still arise, notable for bulk fuel oil movements8 One reasonis the delay experienced in maintenance and repair work, which is now to be partlydecentralized from Khartoum in an effort to improve the availability of vessels.Another is the water hyacinth and other navigational problems south of Khartoum,which lengthen journey times and reduce effective capacity.

64. In spite of the inherent problems, the mission agrees that every meansshould be considered for expanding the river services and developing them intoan efficient and viable entity. Civen the lack of other surface transport, itis essential that operations on the two existing routes should be preserved. Itshould also be noted that once stability returns to the south the Juba servicecan initially offer a considerable capacity at negligible extra cost for the

movement of crops northwards, owing to the heavy excess of tonnage now beingshipped southwards. On other stretohes of the Nile, new services are beingconsidered for specific traffic flows; for example, the substantial cementtonnages from Atbara to Khartoum. The fact that large sections of the country'spopulation are of necessity located close to the river offers a general hopethat water transport could be used on a larger scale.

65. With the new corporation for river transport now being ctreated, themission believes that a comprehensive study of the scope for developing the riverservices further would be valuable and timely. This should examina technical con-straints such as navigational problems on the river, and should al3o consider suchquestions as the size and type of vessels and the structure of the Corporation(with special empbasis on the maintenance function), in addition to emploring thepotential market for water transport. It is understood that a study is beingundertaken by Rumanian consultants, but details of their terms of reference arenot known.

VI. ROADS

A. Road Construction and Maintenance

66. In the whole of the Sadan there are only 330 km of bitumen-surfaced highways outside the tons, nearly all of them in the vicinity ofKhartoum. Ir. addition there are some 5,500 km of gravel and earth roadsand tracks maintained by the Department of Roads (DOR), and a further 12,000 kmor more within the jurisdiction of local authorities.

67. The total of roads and tracks is thus put at between 18,000 and19,000 km, but this figure is not really meaningful, because in many parts ofthe desert vehicles move at will without following a particular alignment.Conversely, the lack of maintenance haa left many so-called roads and tracks insuch poor condition that they do not offer an acceptable right-of-way. Accordingto the DOR, its expenditure on labor, materials and fuel for maintenan-e averagedless than La 50,000 a year over the past five years, which was totally inadequatefor the roads under its jurisdiction.

680 Urgent as it is to extend the road system, the first essential mustbe to rehabilitate the existing highways. To this end, the Bank Group is presen-tly considering a project with the main purpose of providing equipment andmaterials for the DOR, and of offering expertise to assist in reorganizing theDepartment, with the prime purpose of enabling it to carry out maintenance andurgently-needed betterment works on an adequate scale. The project, to befinanced by a US$7.0 million IDA credit, would also include feasibility studiesand detailed engineering for some 500 km of new road construction.

69. The published version of the Five Year Plan ending in FY 1975 includesLs 17.6 million for the design and construction of roads, but although only anestimated Ls 0.5 million was spent in FY 1971, the DOR advised the mission thatexpenditures are likely to increase to over La 23 million for the whole period.This compares with investment of only Ls 2 million during the previous five years,and reflects the higher priority now being given to highway construction.

70. The Ls 23 million budgeted for the DOR comprises the following items:

(Ls 000)Survey and Design of Roads 536Construction of Jur River Bridge 750Dilling-Kadugli road-asphalting 1,250Khartoum-Wad Medani road-asphalting 765Wad Medani-Gedaref road-construction 10,000kbrala-Xas-Zalingi road-construction 7,000Bridge improvements 8Road maintenance equipment 3,018

23.327

- 20 -

Another major item, outside the DOR budget, is construction of a new roadbridge over the Blue Nile in Khartoum, which was recently completed at a cost ofLe 2.3 million.

71. The biggest project is to link Wad Medani and Gedaref (227 11) witha high-standard asphalt road, the cost of which includes a Ls 3 million bridgeacross the Blue ?LLe. rne People's Republic of China is expected to financeand construct this road, which represents a logical extension to the busyKhartoum-Wad Medani link, and will provide the essential outlet for the Rahadirrigation project area. There ia every indication that this is a good project,but the mission has expressed a preliminary view that its early coaLtinuation toPort Sudan is only likely to deserve high priority if hope is aban;loned forsecuring adequate railway capacity to serve the port (para. 10) and only afterits economic feasibility has been thoroughly investigated.

72. For the Gedaref-Port Sidan extenaion, and other roads under con-sideration, it is clearly preferable to avoid establishing priorities beforethe feasibility studies under the proposed Ilh cradit are availabla. For thisreason it would be preferable to delay construction of the costly ramla-Zalingiroad (210 km), if this is possible without prejudicing the agricul ;ural projectat Jebel Marra which it is designed to serve. Alternatively, economies in designstandards should be sought to reduce its costs, which have now risen from Ls 4million to an estimated Ls 7 xillion.

B. Road Vehicles

73. The growth rate in the number of motor vehicles was nearly 8% a yearover the last decade, but in view of the very slow development of the highwaynetwork, it is not surprising that total motor vehicle registrations still nixrberlittle more than 50,000, or one vehicle per 300 people, and one motor car per600 people. (In neighboring Kenya, the figures are in the order of one vehicleper 80, and one automobile per 150 persons). To illustrate the likely effectof an improved highway system on the demand for vehicles, the Khartoum-Wad 4edaniroad (186 km), the best in the country, completed only a few years ago and nowbeing resurfaced and strengthened under the Plan, is said to carry between 2,000and 3,000 vehicles a day, which represents a surprising proportion of the totalvehicles in use all over the country.

- ?1 -

VII. AVIATJON

9udan Airways

74. Sudan Airways was formerly a department of the Ministry of Communica-tions, but was established as a semi-autonomous corporation in 1967. In principle

it is charged with operating on a cammercial basis, though the Minister of Trans-port can direct 4±t tSo provide serrices which need not be financially viable. Inrecent years its operations have comtinually failed to show a profit; in FY 1971.its net deficit was Ls 487,000.

75. The airline's fleet for scheduled services ecmprises two de HavilandComet 4-C aircraft, three Fokker Friendships aad three de Haviland Twln Otters.The Comets, flying the international routes to Europe, the Middle East andEastern Africa, are nearly ten years old. In view of their obsolescense, togetherwith the problems of maintaining a regular timetable wIth only two aircraft, itis not surprising that their operations are commercially urnsatisfactory. Theiraverage utilization, though atil not high, has improved from five to more thanseven hours a day over the last few year0, but average load factors are less than30% on some routes and only 43% overall.

76. In fac ig up to the problem of aircraft replacement, and of operating aninternational fleet of only two aircraft, it is understood that Sudan Ai.rways willin future withdraw frox the internatiqrn4L business, these services beipg trans-ferred to another agency under the Ministry of Defense, and operating in closecollaboration with Xhwait Airways. This seeps to offer a praiseworthy solutionin a dfficualt situation.

77. Three more Fokker Friend hBps are to be converted from military serviceto join the three already operated by the airline. These aircraft seem adequatefor the domestic and regional routes they serve, though their operations haveproved unprofitable, due largely to a low average utilization of only five hoursa day, which tth airline blames principally on the absence of night landingfacilities at. al domestic airports except Kharto. In con with other air-craft, maximum loadings are also limnited by the effect of the intense sinmer heaton take-off weights. The overall passenger lead factor on the Friendship serviceswas 554% in FY 1971. which was satisfactory aa an average, but hid considerabledifferences between particular routes. Loadings were exceptionally high on theKhartoum/i E Obeld and hQazounm/Port aidan routes, where much business must havebeen lost through lack of capacity.

78. The Twin Otters were introduced into service six years ago when theDouglas DC-3 fleet was phased out. Their scheduled operations are confined toroutes with landing etrips unsuiteble for the Friendships, where their averageutilization is a very poor 2.5 hours a day.

79. Sidan Airways' domestlc traffic still amounts to little more than50,000 passengers a year while domestic air freight totals less than 1,000 tonsannually. Given the serious shortage of aurface transport facilities, andprotracted jourmey timep by rail, there should be scope for considerable expan-sion if the airline can offer sufficient capacity on the most popular routes.

- 22 -

Domestic passenger fares have not increased since the airline began operations25 years ago, but they are stlll quite high compared with other countries. FromKhartoum the one-way fare is the equivalent of Ls 0.023 per km (lO.4 U.S0 centsper mile) to Port Sdan, and Ls 0.030 per km (13.9 UoSe cents per mile) to Wau.Any review of fares should clearly be selective rather than global, having regardto the individual route characteristics, including the scope for attractingpassengers frcm the railway (whose first class and sleepin car passengers aretwice as numerous as all the airlines' domestic passengers), and for generatingnew traffic,

80. Sudan Airways' revenues from the international services a e more thantwice those from the domestic business, but there is a little doubt that concen-tration on the daoestic and regional routes wl 1 offer a more ratiosal basis forthe Corporation's future0 Airline passengers wi11 remain very smal; in numbercompared with those travelling by rail and other modes, but they will largely bedrawn from the ranks of management and government who, in a country of this size,and with surface transport as unsatisfactory as it is, will have to rely on airtravel to play an easential part in cohesive national development. To emphasizethe point, it may be noted that the distance between the Red Sea coast and thesouth-western extremes of the country is about the same as between London andWarsaw, or between the northern and southern borders of the United States.

The Airports

81. There are twenty airports served by scheduled flights, but only KhartoumAirport can accept aircraft bigger or faster than Sudan Airways' Fokker Friendships.More important to domestic services, only Khartoum has night landing facilities,which restricts aircraft movements and limits the scope for good utilization 0 Ingeneral, runways and ground facilities are minimal at the principal airports, butapart from lack of approach and runway lighting the condition of the airports isnot seriously impeding aircraft operations.

82. A report by Duteh Consultants (N. V. NA00) on feasibility studies forimprovements of the twelve most important airports (excluding Khartoum) was sub-mitted to the Government in July 1971. These are as follows:

No. Passenger Average AnnualDistance Arrivals Growth Rate in

from Khartoum and Departures Passenger Traffic(hoM ) - (Year 1969)a/ 1961 to 1969 a!

Port &adan 661 28,300 1108%E Obeid 370 10,000 7.2%Malakls 674 9,900 19.6%Juba 1,195 8,400 12.9%EL Fasher 810 7,800 7Q0%Wau 1,005 5,800 13.4%Wad Medani 170 5,700 2.7%Kassala 405 3,800 13.0%EL Geneina 1,117 3,500 1'2.5%Atbara 280 2,500 3305%Gedaref 252 n,a. n.a.*ala 916 n,a. n.a.

a' Fcludes transit passengers 9,/ Average annual growth rate excluding Gedaref and Nyala

- 23 -

83. The number of passengers served by these airports is quite small,and although the growth rate of traffic at scme of the-m is high (from a smallbase), the average growth is somewhat lower than the world-wide experience.However, if the mission is correct in believing that a rapid expansion indomestic air travel should be encouraged as an important factor in the country'sdeveloprent, and if 3udan Airways can provide the increases in capacity required,the Conaultants' estimate of accelerated future growth rates, equivalent to anaverage of about 14 to 15% a year is considered quite realistice

84. At the same time, without fUrther investigation the mission cannotsupport the Consultants' proposal for investmeet of Ls 15.L million (US$W4 million)in the twelve airports over a seven-year period. This figure seems dispropor-tionately high in the light of urgent investment priorities elsewhere in theeconomy. In addition, every effort should be made to keep down the costs of airtravel, including the ground facilities, to emphasize that it is not a luxury,and to seek a broader base for traffic expansiQn than the very small section ofthe community now travelling by air. To the proposed investment must be addedadditional expenditure on Khartoum Airport which, although limited to a Ls 436,000allocation in FY 1971-75 Plan, can be expeoted to demand much bigger sumssubsequently.

85. Airport landing fees in th.e %dan are very high; the fee for a Cometis US$344, compared with charges paid to other countries by Sudan Airways rangingfrom about US$140.160. For a Boeing 707 the fee is US$840, compared with US$380at New York or US$300 at Bogota. The Justification for such high fees may welllie in the relatively small number of movements resulting in high operating costsper aircraft landirg. Without having seen an analysis of airport costs, themission can only comment that with large airport investments in prospect, this isprobably no time to consider reductions in landing fees; at Khartoum, as at thedomestic airports, improvements to facilities are likely to be a surer way toencourage expansions in traffic and services.

- 24 -

VIII, REXIMEND ACTION

86. The Goverment's Five Year Plan includes public investment ofse"e La 41 milion for transportation in the five year. ending in 1974/75(para. 14)1 This is more than twice the achievement during the previous fiveyears, and there must be some doubts on the probability of implementing thewhole program within the Plan period. But in planning for a satisfactory rateof expansion in the economy within the next few years there is no dor bt about thecritical need for substantial investments in the transport sector. Acceptingthe problems of implementation, the mission actual-ly estimates the investmentrquirement at a somewhat higher level than The Governxent, if transport isto keep pace with plans in other sectors. In sumary, the comparative figuresare as follow:

Pr22osed Invesent FY 197 - 1975

(Ls Million)

Five Year Mission'sPIan Estimates Difference

Railways 14.1 21,0 + 7.9Ports XI? 5.5 + 5$4Inland Waterways 0.B 0.8 -

Road Cnstruction 23.3 23.3Airports and Air NIvigation 1 3 1.3 -Sudan Airways 5.0 5.0Sadan Shipping Line -. > _

___ 60.411.)_

87c For the railway, the zlisa±-on bel±eves the investment target shouldbe substantially more asiitious than in the Plan. In Table 3, the requirementis put at Ls 24.48 million, but since a program of this order would most probablyhave to extend beyond 197v5, a figure of La 2'1 million is estimated for the Planperiod. It should be emphasized that the Juatification for additional investmentwould be strengthened by any significant improvement which the railway is ableto bring about in the utilization of existinig equipment. The moanagement of therailway should endeavor to demonstrate that all possible steps have been takento this end.

B8e The mission believes that an expansion of port capacity is becomixgurgent, and that substantial invesment in Fort xdan, accompanied by coordinatedplanning for construction of a second port vithin, say, five to ten years, offersthe most rational solution (Table 4). Plan for a new port would be subject toreview in the Light of any propodse developnent of containerized traffic throughPort Sudan.

- 25 -

89. The mission is not suggesting changes in the investment targetsfor other transport nodes, though these vill u3doubtedly be subject to altera-tion, particularly as the results of sp'ecific investment studies are taken intoaccount. For the river services, the misaion believes that a ccmprehensivestudy of the development potential sho3ld be completed as soon as possible(pnra. 65). For the roads, a study of investment priorities is proposed forfJnancing under the DA credit (para. 68). For the internal airports the con-PuLtants' feasJbility study is aiready -. ail^±le, and could well provide thebaria for early investment decisions (anras. 81 to 84).

90. Although feasibility studies nf un. oLl pipeline between Port &idanA.nd Khartoum have also been completed, thbe-yission believes tbere is urgent needto supplement these by investigating comparative costs of conveyance by rail(pareas. 11 and 12). -Ihe cor.lusions would clearly be as important to futurerailwar inMestaemts in tank wagona, and assooiated motive power, as to a decioionto construct a pipeline.

APPENDIX

SrATISTICAL TABLES

INDEX

Table No.

1 Average Railway FreIght Tonnage (Revenue-earning) byCammodity in FY 1969-71 and Estimates for FY 1975

2 Railway Freight Tornages (Revenue-earning) in FinancialYears 1964 to 1971

3 Proposed New investment in &zdan Railways

4 Proposed New Invertm8nt in Port 9hdan

TABIE 1

SUDAN RAILXAYS

Average Railway Freight Tonnage (Revenue-EArni*) bh Commodity in FY 1969-1971ani Estimates for 1975

(000 Metric Tons)

To Port Sudan From Port S3udan Other Traffic Total TrafficAverage Average Avcrago Average

of 3 Years Estimate of 3 Years Estimte of 3 Years Estimate of 3 Years EstimteConmmodity 19i9-1971 for 19.75 169-1971 for 3975 196 -Th5lf for 197 1969-1971 for 175 Commodi ty

Cotton 222 230 - - 60 60 282 290 CottonCotton seed 133 95 - - 26 30 159 125 Cotton seedOilcake 160 310 - - - 160 310 OilcaleOther arnial fedcirig stuffs 17 20 - - 17 20 Other animal feeding stu-ffsGroundnuts 88 220 - 6 10 94 230 GrorininutsSorghum ard millets 42 200 6 - 138 170 186 370 Sorghum ard mil3letsSesame 83 100 - - a3 100 SesameOum 32 50 - - - - 32 o0 GumCOeent 11 20 4 - 135 175 150 19S CemantChroma Ore 10 1/ 85 - - - 10 8$ Chrome OreTimber - 29 35 - - 29 35 Timberflour - - 29 - - - 29 - FlourWheat - - 9 150 13 ?V 162 170 WheatSugar - - 125 95 18 26 143 120 SugarFer tiliners - - 105 130 - - 105 130 FertilizersSalt - - 53 59 53 $5 SaltSacks - - 24 30 - 24i 30 SacksTextiles- - - - 8 10 TextilesLubricating oil - - 16 25 - - 16 25 Lubricatirg oilOther pac/ked patroleun products 53 100 - - 53 100 Other packed petrolewu productsCharcoal - - 9 10 9 10 CharcoalBrtet -e -e 29 30 29 30 DatesFirewood - - - - 32 30 32 30 FirewoodOther (ircludiag livestock) 93 100 02 242 300h 627 765 Other (irlwlirig livestock)

TOTAL (excluding bulk petroleumproducts) 881 1.430 Vo3 _2_5 708 86o 2_4 3s285

Bu3k petrolcum products - - 498 630 - 498 630

GRAND TOTAL h1h0 ll l25 _7 2,9 3.91S

1975 as % of Avreage, 1969-71 - 162% - 116% 121% - 131%

1/ Estimate

Source: 1969-71, Sudan Railways1975, Mission Projectiorns

TABLE 2

SUDAN RAL-WAY6

Rai-way Freight Tonnages (Revenue Farning) inFinancial Years 196h4 to 1971

(000 Metric Tons).

Total TrafficFrom Port Sadan Excluding IncludingBulk Bulk Bulk

To Petroleum Other Petroleum PetroleumPort Sudan Products Other Traffic Products Products

1964 77 352 1,206 631 2,722 3,0741965 805 321 917 583 2,305 2,6261966 682 319 790 653 2,285 2,6041967 781 375 750 764 2,295 2 6701968 813 392 698 642 2,153 2,5451969 929 439 848 688 2,h65 2,9041970 843 509 875 778 2,496 3,0051971 872 546 986 658 2,516 3,062

Average annual traff'icin 3 years: -

196J4-66 8h4 331 971 622 2,437 2,7681969-71 881 498 903 706 2,492 2,990

1972 goo 540 980 740 2,620 3,1601973 1,000 570 985 775 2,760 3,3301974 1,200 600 990 815 3,005 3,6051975 1,430 630 995 860 3,285 3,915

Source: Sudan Railways ancd Mission Estimates.

TABLE 3

SUDAN RAILWAYS

Proposed New Investment

(Ls Million)

RAILWAY ITEMS Ministr's Plan Mission's Estimates

Foreign LocalCur- Expend-rency iture Total F L T

TRACK, installations andrenewals _ 1.40 1.40 - 2.36 2.36

BUILDINGS, WORKSHOPS, etc.Buildings, Bridges & Services - 1.50 1.50 - 1.54 1.54Workshops & Depots 0.54 0.21 0.75 0.52 0.25 0.77Handling facilities 0.08 0.O4 0.12 0.08 0.04 0.12

Sub-total 0§6 17 7 2.37 g060 1.83 T2T7

COMMUNICATIONS 0.10 0.06 0.16 0.45 0.30 0.75

LOCOMOTIVES - - - 2.54 1.09 3.63

ROLLING STOCKDry Cargo Wagons 3.02 1.22 4.24 5.18 1.99 7.17Oil Tank Wagons 0.97 0.39 1.36 0.43 0.17 O.60Passenger Coaches 0.92 1.91 2.83 0.75 1.54 2.29Service Vehicles 0.53 0.61 1.14 0.07 0.50 0.57Roller Bearings andAutomatic Couplers 0.29 0.16 0.45 0.66 0.10 0.76

Sub-total 5.77 3 =29 10.02 7.09 7.30 11.39

TECHNICAL ASSISTANCE ANDTRAINING FACILITIES - - - 0.30 0.40 0.70

MISCELLANEOUS 0.17 0.17 0 0.83 0.83

SUB-TOTAL 6.45 7.67 14.12 10.98 11.11 22.09CONTINGENCIES (15% from 1972/73) - - - 1.20 1.19 2.39

TOTAL 6.45 7.67 14.12 12.18 12.30 24.48

Lource: IHnistry o_f Panning and Mission estimates.

TABLE 4

PORT SUDAN

Proposed New Investment(Ls Million)

PORT ITEMS Government's Five Year Plan Mission's EstimatesForeign Local

Cur- Expend-rency iture Total F L T

Miscellaneous Items 0.05 0.03 0.08Phase I (see beo)1.71 1.51 3.22Part of Phase II b 1.30 0.96 2.26

Total for five years 70/71-74/75 0.05 0.03 0.08 3.01 2.47 5.48

PHASE I - INTERIM MEASURES AT PORT SUDAN

Estimated expenditure 1970/71 0.13 0.07 0.201971/72 0.12 0.08 0.20

Sub-total 0:27 .1 70Proposed e,xpenditure 1972/73 to 1974/75

Additional storage and facilities 0.67 0.60 1.27Additional lighterage and anchorage facilities 0.20 0.30 0.50Preliminary and final engineering for Phase II 0.40 - 0.40

1970/71-1974/75 Total 1.2 2 1.05 2.57Contingencies - 15% on 1972/73 to 1974/75 items 0.19 0.14 0.33Customs & other duties (say) - 0.32 0.32

PHASE I TOTAL 1.71 771T 3.22

PHASE II -. DEVELOPMENT OF PORT SUDAN TO MAXIMUM CAPACITY

Proposed expenditure 1974/75 to 1976/77Sea anchorage for oil tankers 1.00 0.50 1.50Reconstruction of berths 16-18 2.00 1.00 3.00

Total 3 -.00 T -. TO 42 5Contingencies 15% -0-. 0.22 J0 7Customs (say) - 0.66 0.66

PHASE II TOTAL 3. -. 5.83Of which, estimated expenditure 1974/75 1.30 707 2.2

1975/76-1976/77 2.15 1.42 3.57

PHASE III - DEVELOPMENT OF NEW FACILITIES

Development of second port 1976/77-1980/81 6.50 3.50 10.00Customs (say) - 1.20 1.20

PHASE III TOTAL 0 7-0 17T

jouce:!i~i1)f osIm~T.e:

CHART

SUDAN

GOVERMKENT ORGANIZATION IN THE TRANSPORT SECTOR

Minister of TransportI Minister of Defense

Deputy Minister IDepartment ofCivil Aviation

9udan Sadan Sudan Shipping DepartmentRailways Airways Line of Roads

Port InlandSudan Waterways 1/

1/ Sbon to become separate corporations.