world bank document - documents & reports - all...

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 52876-MV

INTERNATIONAL DEVELOPMENT ASSOCIATION

PROGRAM DOCUMENT

FOR A PROPOSED DEVELOPMENT POLICY CREDIT

IN THE AMOUNT OF SDR 8.5 MILLION, INCLUDING SDR 1 MILLION IN PILOT CRISIS RESPONSE WINDOW RESOURCES

(US$13.7 MILLION EQUIVALENT)

TO

THE REPUBLIC OF MALDIVES

FOR AN

ECONOMIC STABILIZATION AND RECOVERY PROGRAM

February 16,20 10

Poverty Reduction and Economic Management Department Maldives and Sri Lanka Country Department South Asia Region

This document has a restricted distribution and may be used by recipients only in the performance o f their off icial duties. I t s contents mav not otherwise be disclosed without Wor ld Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

AAA ABS ADB

AGO

BML

CAS CCTF csc DPC DRP DSA EMP EPPS FY GDP GFS GoM HIES

IBRD

IDA IFC IF1 IHDP IMF JSAN LDP

LIC DSA

MBP MDGs MECC MMA

THE REPUBLIC OF MALDIVES - GOVERNMENT FISCAL YEAR January, 1 st - December, 3 1 st

CURRENCY EQUIVALENTS Exchange Rate Effective as o f 30 November 2009

Currency Unit = Maldivian Rufiyaa 1 .OO Rufiyaa = US$0.078 US$1.00 = 12.8 Rufiyaa

Metric System WEIGHTS AND MEASURES

ABBREVIATIONS AND ACRONYMS

Analytical and Advisory Activities Absolute Poverty Benefit Asian Development Bank

Auditor General’s Office

Bank o f Maldives

Country Assistance Strategy Climate Change Trust Fund Civil Service Commission Development Policy Credit Dhivehi Rayyithunge Party Debt Sustainability Analysis Environment Management Project Economic Policy Planning Section Fiscal Year Gross Domestic Product Government Finance Statistics Government of Maldives Household Income and Expenditure Survey International Bank for Reconstruction and Development International Development Association International Finance Corporation International Finance Institutions Integrated Human Development Project International Monetary Fund Joint Staff Advisory Note Letter of Development Policy Low-income country Debt Sustainability Analysis Mobile Phone Banking Project Millennium Development Goals Macro Economic Co-ordination Committee Maldives Monetary Authority

MOE MOFT MOHF MTDS MTEF MVR NAPA OM0 PAS PC PEFA PER PFM

PHRD

PPG PPP

PSAP

PSIA PSIP REER ROSC SAP SBA SDR SP STELCO TA TVM UNDP MDP VOM VPA

Ministry o f Education Ministry of Finance and Treasury Ministry of Health and Family Medium Term Debt Management Strategy Medium-Term Expenditure Framework Maldivian Rufiyaa National Adaptation Program of Action Open Market Operations Public Accounting System Privatization Committee Public Expenditure and Financial Accountability Public Expenditure Review Public Financial Management Japan Policy and Human Resources Development Trust Fund Public and Publicly Guaranteed Public Private Partnerships Pension and Social Protection Administrative Project (PSAP) Poverty and Social Impact Analysis Public Sector Investment Program Real Effective Exchange Rate Report on the Observance of Standards and Codes Strategic Action Plan Stand-By Agreement Special Drawing Rights Social Protection State - Owned Electric Company Technical Assistance TV Maldives United Nations Development Program Maldives Democratic Party Voice o f Maldives Vulnerability and Poverty Assessment

i

FOR OFFICIAL USE ONLY

Vice President: Isabel Guerrero

Sector Director: Emesto May Sector Manager: Miria Pigato

Country Director: Naoko Ishii

Task Team Leaders: Francis Rowe and Kirthisri Rajatha Wijeweera

The Maldives Development Policy Credit was prepared by an IDA team consisting of Francis Rowe and Kirthisri Rajatha Wijeweera (SASEPNo-Task Team Leaders, Shahnaz Sultana Ahmed, Rita Soni, and Zeenath Marikkar (SASEP), John Speakman (SASFP), Mir iam Witana (SAWS), Manoj Jain (SASFM), Ranjana Mukherjee (SASGP), Nobuo Yoshida, and Tomoyuki Sho (SASEP), Puja Datta (SASSP), and Richard Damania (SASDI). Sebastian Desuss (AFTP4) and Marco Scuriatti (SACOl) are the peer reviewers.

.. 11

This document has a restricted distribution and may be used by recipients only in the performance o f their off icial duties. I t s contents may not be otherwise disclosed without Wor ld Bank authorization.

THE REPUBLIC OF MALDIVES ECONOMIC STABILIZATION AND RECOVERY PROGRAM

TABLE OF CONTENTS

I . INTRODUCTION ........................................................................................................................................ 1 I1 . COUNTRY CONTEXT ............................................................................................................................. 2

A . RECENT POLITICAL AND ECONOMIC DEVELOPMENTS ............................................................. 2 B . MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY ................................................... 6 C . POVERTY REDUCTION AND SOCIAL DEVELOPMENT ................................................................. 8 D . THE GOVERNMENT’S CRISIS RESPONSE AND MEDIUM-TERM DEVELOPMENT PLAN ...... 9

I11 . BANK SUPPORT TO THE GOVERNMENT’S PROGRAM ........................................................... 12 A . LINK TO CAS ........................................................................................................................................ 12 B . COLLABORATION WITH IMF AND OTHER DONORS .................................................................. 14 C . RELATIONSHIP TO OTHER BANK OPERATIONS ......................................................................... 14 D . LESSONS LEARNED ........................................................................................................................... 15 E . ANALYTIC UNDERPINNINGS ........................................................................................................... 15

I V . THE PROPOSED DEVELOPMENT POLICY CREDIT ................................................................... 16 A . RATIONALE AND OBJECTIVES ....................................................................................................... 16 B . DESIGN AND FOCUS OF THE PROPOSED OPERATION ............................................................... 16

V . OPERATION IMPLEMENTATION ..................................................................................................... 25 A . POVERTY AND SOCIAL IMPACT ANALYSIS ................................................................................ 25 B . ENVIRONMENTAL ASPECTS ............................................................................................................ 28 C . IMPLEMENTATION AND MONITORING ........................................................................................ 29 D . FIDUCIARY ASPECTS, DISBURSMENTS AND AUDITING .......................................................... 29 E . RISK AND RISK MITIGATION ........................................................................................................... 30

ANNEXES 1 . LETTER OF DEVELOPMENT POLICY 2 . DEVELOPMENT POLICY CREDIT POLICY MATRIX 3 . MACRECONOMIC INDICATORS 4 . FUND RELATIONS NOTE

6 . COUNTRY AT A GLANCE 5 . JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

... 111

CREDIT AND PROGRAM SUMMARY

THE REPUBLIC OF MALDIVES

ECONOMIC STABILIZATION AND RECOVERY PROGRAM

Borrower

Implementing Agency

Financing Data

Operation Type

Main Policy Areas

Key Outcome Indicators

Program Development Objective(s) and Contribution to CAS

The Republic o f Maldives

Ministry o f Finance and Treasury

IDA Credit o n standard IDA terms Amount: SDR 8.5 mi l l ion including SDR 1 mi l l ion in Pilot Crisis Response Window Resources (US$ 13.7 million) The proposed operation i s processed under IDA Financial Crisis Response Fast-Track Facility

The operation i s the f i rs t o f a proposed two-operation programmatic series

Economic Growth, Public Financial Management, Public Enterprise Reform, Public Private Partnerships and Social Protection.

The key outcome indicators are: an economic growth rate o f 3 percent in 201 0 and 5 percent in 201 1, key elements o f the Strategic Act ion Plan have been costed, greater transparency in the presentation o f the Government’s annual Budget, and increased coverage o f the social safety net program. The proposed operation aims to support the Government’s efforts to bring about economic recovery, while protecting the vulnerable. It aims to support the Government achieve its development objectives set out in the Strategic Act ion Plan (SAP). The SAP aims to redefine the role o f the state in the economy to achieve upper-middle income status, ensure more equitable access to services and opportunities, improve service delivery, facilitate economic diversification, and support better environmental practices to sustain growth and adapt to global climate change. Much o f the plan i s to be implemented through the private sector where possible or public-private partnerships (PPPs) with the aim to minimizing fiscal impact given the weak fiscal position. The proposed operation is also consistent with the Maldives Country Assistance Strategy (CAS) FY2008- 12 which aims to support government efforts to better manage the economy and public finances. The CAS calls for a possible development pol icy operation in FY2010. The IMF and the Asian

iv

Risks and Risk Mitigation

Operation ID

Development Bank are providing support to the Government program to help regain macroeconomic stability.

The main risks to the proposed operation include political risk, the macroeconomic framework, vulnerability to external shocks, and limited technical capacity. Democracy in the Maldives is very much in a nascent stage and the Government o f President Nasheed lacks a parliamentary majority, which could significantly constrain the Government’s plans going forward. Political risks are l ikely to be a feature for the entire length o f the proposed program period. Given the size and form o f the Government’s fiscal adjustment program there are significant implementation r isks that may hamper the country’s growth. The strength o f the global economic recovery presents upside and downside risks to the proposed operation. A stronger-than- expected recovery in Europe - the largest tourist source - would help boost tourist arrivals, real GDP growth and government revenues in the Maldives, helping to ease the impact o f the fiscal adjustment in 2010. Alternatively, a slow and anemic global recovery would suppress a revival in tourism, GDP growth and FDI, while also making the fiscal adjustment more challenging. A s a small, open, and undiversified economy, the Maldives i s vulnerable to the adverse effects o f external shocks such as an o i l price shock. The focus on government revenues generation measures in the IMF and ADB programs will help mitigate the risk o f external shocks translating into large macroeconomic imbalances. Limited technical capacity i s one o f the leading development constraints in the Maldives. Capacity constraints significantly impact al l aspects o f government functions and the authorities in the recent past have sought increased technical assistance (TA) interventions from multi-lateral donors such as the World Bank, IMF and the ADB. Specific TA has not been built into the program, but capacity constraints were reflected in the program design.

P114463

V

I. INTRODUCTION

1. This proposed operation supports the new Government’s program to stabilize the economy and puts in place some of the key elements needed for a sound recovery. I t supports the Government’s reforms aimed at restoring fiscal sustainability and i ts efforts to implement i ts medium-term Strategic Action Plan. Both the financing and the policy actions supported by the operation come at a time when there are initial signs o f an economic recovery and evidence that the Government’s fiscal austerity measures are helping to put the fiscal deficit on a sustainable path. In this regard, the operation will underpin economic growth by helping to reduce the large macroeconomic imbalances that occurred in 2009.

2. The tourism sector-and the Maldivian economy at large-immediately felt the impact of the global recession, but some indications of recovery are now emerging. The tourism sector in Maldives i s the lifeblood o f the economy accounting for 30 percent o f GDP. The global crisis resulted in a 9 percent contraction in tourist arrivals through September 2009 compared to 2008. However, recent tourist arrivals data show a pick-up from the trough reached in July 2009. Following an 11 percent year-on-year increase in arrivals in October, arrivals increased a further by 7 percent in November. Revised projections now point to a full-year decline o f 3.5 percent in 2009 compared to a 7 percent decline anticipated at the beginning o f the year. GDP i s estimated to contract by 4 percent in 2009 and the current account deficit i s projected to reach nearly 30 percent o f GDP.

3. While the 2009 fiscal deficit i s very high, fiscal austerity measures and the improving economy are beginning to slowly turn the situation around. The fiscal deficit i s expected to have reached almost 28 percent o f GDP in 2009, down from earlier estimates o f 33 percent o f GDP. Fiscal data i s not available beyond September 2009, at which point revenues were down 23 percent compared to the f i rs t nine months o f 2008. However, in step with higher tourist arrivals and higher- than-expected import duties - as imports have rebounded more strongly than expected-revenues have picked up. This combined with the Government’s recent expenditure reductions-including a temporary cut o f public sector staffs’ salaries o f about 15 percent implemented from October 2009-suggests that the fiscal situation i s gradually improving

4. The Government i s committed to a reform program that has at its core a sharp fiscal adjustment. The Government has designed and i s implementing a program that would stabilize the macroeconomic situation through a significant fiscal adjustment and a scaling-up o f external financing. The IMF approved a 36-month combined Stand-By Arrangement and External Shocks Facility o f US$92.5 million (or 700 percent o f quota) on December 4, 2009. The ADB has approved a US$35 million budget support operation with half being disbursed in 2010 and the other half planned for mid-2011. This coordinated external financing i s meant to preserve confidence in the economy, reduce the country risk premium and thereby stimulate economic growth.

5. This proposed operation i s focused on helping the Government to implement its SAP, which aims to fundamentally change the role o f the state in the economy. The operation benefits from strong Government ownership and implementation commitment from the highest levels o f Government. The focus on public financial management - by addressing key institutional shortcomings in budget preparation and implementation - aims to enable the Ministry o f Finance and Treasury to recognize budget overruns early so that they can be addressed in a timely fashion.

1

The focus on public enterprise reform supports the Government’s ambitious public private partnership program, while underpinning fiscal sustainability. The social protection measures help cushion the impact o f what will be a significant structural change in the economy. The Bank’s proposed operation is the f i rst o f a two-operation programmatic series and i s being processed under the IDA Financial Crisis Response Fast-Track Facility. The operation also benefits from an additional SDR 1 mi l l ion allocation from IDA’S Crisis Response Window.

6. This first operation in the proposed two operation series will support the Bank’s already strong program of engagement with the authorities. The synergies between the social protection components o f this operation, next proposed operation in the series, and the recently approved Pension and Social Protection Administration project (PSAP) i s one important example. The result that is expected to be achieved in this area i s the implementation o f a new integrated social protection strategy that is well-targeted and fiscally sustainable. The proposed series i s also helping to bolster technical assistance (TA) and capacity building activities, l ike the Bank’s recent Governance Diagnostics work, the Government’s Public Accounting System project which i s expected to lead to the development o f a modern public accounting and financial management information system, the debt management technical assistance program and the public sector restructuring TA. These TA and capacity building efforts are expected to grow in strength as implementation o f the Government’s reform program progresses.

11. COUNTRY CONTEXT

A. POLITICAL AND ECONOMIC DEVELOPMENTS

7. For much o f the last three decades Maldives has been a development success story. In the early 1980s it was one o f the world’s twenty poorest countries with a population o f 156,000. Today, with a population o f just over 300,000, it is on i t s way towards achieving middle-income status with a per capita GDP approaching $2,800. Poverty rates, as measured by the headcount ratio, have fallen steeply, from 40 percent in 1997 to 28 percent in 2004. Other human development indicators - including infant mortality, maternal mortality, and educational attainment - have registered similar improvements. The sustained growth and rising prosperity o f the last three decades was founded on political stability and a private sector-led tourism industry based upon the country’s extraordinary natural assets. The Maldives consists o f 1,192 small tropical islands that cross strategic shipping routes and it has a marine environment that i s r ichly diverse. With more territorial sea than land, marine resources have played a vital role shaping the contours o f economic development, with nature-based tourism and fishing being the main drivers o f economic growth.

8. The political economy of the Maldives changed significantly post-2004, with the new Government inheriting unsustainable Government finances in 2008. Political and institutional reforms initiated in late 2003 resulted in the “Roadmap for Reform Agenda” in early 2006. The country’s f i rs t multi-party elections were held in 2008. In the run up to the elections, government spending increased considerably to reach 63 percent o f GDP in 2008 from 36 percent o f GDP in 2004. The public service wage bil l was a primary source o f the increase in recurrent expenditures, as both the number o f public sector employees and their wages have increased substantially. The total pay package increased by over 150 percent from 2004 to 2008 and the public service now

2

represents one-third o f the labor force.’ These and other recurrent spending went far beyond the needs o f the 2004 Tsunami reconstruction efforts.2

9. The first ever multi-party Presidential elections were held in October 2008, followed by the first ever multi-party parliamentary elections on May gth 2009. In the Presidential election, Mohammed Nasheed o f the Maldives Democratic Party (MDP) defeated former President Gayoom in the second round run-off to become the 4* President o f the Maldives. In the parliamentary elections, President Nasheed’s MDP secured 28 seats in the 77-member assembly coming second to the main opposition Dhivehi Rayyithunge Party (DRP) o f former President Gayoom and its coalition allies which secured 35 seats.

10. The Government was elected on a program of smaller government and stronger service delivery. Two core principles o f the current Government’s Strategic Action Plan are to reduce the role o f the state in the economy and to ensure that government expenditures are based on sustainable revenues. An ambitious privatization and public private partnership (PPP) program i s underway as i s fiscal consolidation that rests heavily o n public service reform. Both efforts were originally conceived as ways to promote more efficient service delivery to the people o f Maldives and to ensure sustainable economic growth and poverty reduction, but are now also seen as key measures to help reduce macroeconomic imbalances.

11. The global financial crisis exposed the unsustainable level o f fiscal expenditures in recent years. The government’s revenue base i s narrow and volatile; it consists largely o f import duties, tourism receipts, dividends from state-owned enterprises and resort lease rentals. Both tax and non-tax revenues are driven mainly by the fortunes o f the tourism sector. The downturn in tourism with the onset o f the global economic crisis has led to a decline in tourist related revenues (direct tourism tax revenues have declined sharply) bringing the unsustainable level o f government expenditures into sharp ~ O C U S . ~

The average growth rate in the number o f public employees over this period was 6.5 percent implying that that bulk o f 1

the wage bi l l increase was due to wage increases. * In late 2004, the country was hit by the tsunami that devastated many parts o f South Asia. I t displaced 29,000 people from their homes and caused damage equivalent to 62 percent o f GDP.

Historically, grants have been between 2 and 5 percent o f GDP. The fiscal deficit including grants was 13.6 percent in 2008 and i s expected to be 26 percent o f GDP in 2009.

3

Figure 1. Maldives: Central Government Finances

Government Expenditures

Government Revenues

! ..................... ......

2w0 2004 2w0

-Tax Revenue Non-Tax Revenue

- - - R e r o r t t e s r e RentlRight 8x11) - ' ToYrimTax (Right axis)

Government Compensation and Employment

i' 25 40,000 1' 2 < nnn 1 ............................................................................................

20

15

10

5

0

2000 2002 2004 2006 2008

-Government Employment(Left axis) -Wages& Salaries (% of GDP)

0 -

5

-10 '

3 -15 -

-30

!

Fiscal Deficit (excluding grants)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: Maldives Monetary Authority, IMF and Bank staff estimates.

......................................................................................

0

-50

-100

-150 y)

.200 0 5 -250

-300

-350

-400

-35 i .................................................................................................

12. Fiscal imbalances mirror external imbalances. Accelerating government expenditure since 2004 played a role in driving up imports to over 90 percent o f GDP in 2008. The multi-year boom in food and fuel prices, and strong demand for resort-related construction materials prior to the onset o f the global crisis, also contributed to the exceptional import growth o f recent years. The pace o f import growth far outstripped the robust growth in export o f services (especially tourism) prior to the crisis. Consequently, large and growing current account deficit resulted, reaching 53 percent o f GDP in 2008. With the sharp decline in commodity prices in the f i rs t half o f 2009 and extensive foreign exchange rationing, pressures on the import bill have eased and the deficit is expected to fall to 30 percent o f GDP in 2009.

13. Financing the current account deficit has become increasingly difficult. Deficits were mainly financed through private capital inflows, foreign borrowing by commercial banks and official financing (multilateral and bilateral) until mid-2008. But since then, private capital inflows have slowed and foreign banks have cut credit facilities to domestic branches during the current financial crisis. The Maldives Monetary Authority (MMA) has relied on drawing down foreign exchange reserves to cover the balance. Gross official reserves were bolstered in mid-March with

4

the disbursement o f US$50 million o f a US$lOO mill ion loan from the Indian Government. However, reserves quickly fe l l back from a peak o f US$267 million. Gross reserves have fluctuated below 3 months o f imports throughout 2009.

14. Low and declining foreign exchange reserves r isks undermining the exchange rate peg. The rufiyaa has been pegged to the US dollar at a rate o f MVR12.8 since 2001. The low reserve cover has meant that the MMA i s rationing foreign exchange in the economy. The real effective excliange rate has appreciated 12 percent since mid-2008, but remains below levels reached in 2005. Consumer price inflation has been declining in recent months, driven in large part by falling international commodity prices relative to 2008. The recent depreciation o f the U S dollar against major international currencies i s also helping to contain real exchange rate appreciation pressures.

15. Recent IMF analysis of the real effective exchange rate indicates that the gains of a devaluation o r a move to a floating regime would be small and uncertain while the costs would be substantial. In particular, the typical benefits associated with expenditure switching after a devaluation would be limited by the extremely small non-tradable sector in the economy. As such, there are almost no import-substituting sectors in the economy. Moreover, analysis based on purchasing power parity (PPP) exchange rates suggests that the currency i s only modestly overvalued. The core source o f external imbalances i s not the real effective exchange rate (REER), but the recent fiscal expansion.

16. Macroeconomic imbalances and the global crisis have also put stress on the banking system. Expansionary fiscal policy and high budget deficits led to dramatic public sector credit expansion in 2008 and the first half of 2009. In the absence o f an effective non-bank sector, much o f the domestic financing requirement falls on the banking sector. This public sector credit expansion i s crowding out private sector credit and putting the banks’ balance sheets at risk. Foreign exchange rationing i s also exposing banks to dollar liquidity shocks. These stresses are compounded by the bank’s high exposure to tourism, the concentration o f loans to a few borrowers, and limited financing options (e.g., lines o f credit, parent financing) since the onset o f the global financial crisis. Consequently, the risk o f growing non-performing loans i s rising. The state-owned Bank o f Maldives (BML), which accounts for,about 40 percent o f commercial bank assets, saw i t s non-performing-loans ratio increase significantly last year. More broadly, the net foreign asset position o f the banking sector has been negative since July 2008, leaving the banks susceptible to a possible depreciation o f the rufiyaa.

5

Figure 2. Maldives: External Sector Developments and Consumer Prices

Current Account Deficit Gross Foreign Exchange Reserves

75 70 65

60

2004 2005 2006 2007 2008 2009

!::#' i . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I

Real Effective Exchange Rate (2000=100)

95

250 3

200

2 150

100 1

0 50

Consumer Price Inflation ..................................................... ............................................................ lo .I--

16 1 /2 ............................................................................................................................. I

Source: Maldives Monetary Authority, IMF and World Bank staff.

B. MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY

17. A return to robust economic growth in 2010 and beyond will depend heavily on a rebound in the tourism sector. A stronger-than-expected recovery in Europe - the largest tourist sending region - would help boost tourist arrivals, real GDP growth and government revenues. A rebound in global growth and an easing o f global credit constraints would also help foreign direct investment and stalled resort developments to pick up. GDP i s expected to contract by 4 percent in 2009 after growing 5.8 percent in 2008 and 7.2 percent in 2007. While foreign exchange rationing and a decline in fish catch also contributed to the result, the main driver o f the growth slowdown has been a fal l in tourist arrivals. Recent tourist arrivals data suggest that the expected rebound in the tourist sector in 2010 may materialize, but perhaps not by enough to help generate much more than 3 percent real GDP growth.

6

18. Signs of a rebound in tourism are evident in the latest arrival numbers. Tourist arrivals data show a pick-up from the bottom reached in July in the second ha l f o f 2009. Following an 11 percent year-on-year increase in arrivals in October, tourist arrivals increased by 7 percent in November. Revised projections now point to a seasonally adjusted decline o f 3.5 percent in 2009 compared to a 7 percent decline anticipated at the beginning o f the year. The recent depreciation o f the dollar against the Euro and major Asian currencies has helped boost the competitiveness o f the sector. The growing share o f Asian tourists seen in the last decade is another factor that may bode wel l for prospects for the rest o f this year, as many Asian countries are emerging from the global financial crisis quicker than other regions.

19. Traditionally, the fisheries sector has also been an engine of growth. While a distance second compared to the tourism sector, the sector does account for about 10 percent o f GDP and is the only other significant source o f foreign exchange for the e ~ o n o m y . ~ Fish catch levels have been o n a continual decline since 2006. The causes o f the drop in fish-catch are poorly understood, but may be related to changing ocean currents or fuel price increases. The total volume o f fish exports (excluding l ive fish) dropped by 38 percent in the first half o f 2009 relative to 2008 and earning from fish exports dropped by 43 percent during the period. The current rebound in international tuna prices will help the fisheries sector outlook.

20. Financing growing fiscal and external imbalances in recent years has increased the risk of debt distress. Defici t financing through unsterilized monetization has made up a growing share o f total financing, as external options have diminished during the global financial crisis. Deficit monetization in the form o f government borrowing from the MMA through virtually unlimited access to the ways and means account made up about 9 percent o f GDP in 2008 and has accounted for another 10 percent so far this year. Growth in private external debt used to finance resort construction also grew sharply prior to the onset o f the global financial crisis. Going forward, the expected large fiscal deficits are assumed to be financed primarily through a combination o f concessional external funds (including grants) and (to a lesser extent) domestic debt.

21. The Government’s adjustment program, with its focus on fiscal consolidation, aims to address the root causes of the current macroeconomic imbalances, preserving the exchange rate regime at its current level. In essence, Government efforts are aimed at reducing the fiscal deficit through a reduction o f the wage bill -while protecting social spending - and introducing new revenue measures to broaden, the tax base. These actions are being supported by a tightening o f domestic currency liquidity and a halting o f the monetization o f the fiscal deficit. While there are implementation risks, this well-focused Government program i s adequate to restore macroeconomic balances, the pre-requisite for putting the economy back on track and restoring growth.

22. The recent joint Bank-Fund debt sustainability analysis indicates that Maldives i s at a moderate risk o f public external debt distress (Annex 4). Vulnerabilities related to total public debt are higher, and addressing them will require timely implementation o f the authorities’ strong fiscal adjustment program. The borrowing space in the short and medium terms has shrunk after the recent accumulation o f large fiscal and external deficits. The build-up o f private external debt prior to the onset o f the global financial crisis and o f public domestic debt (mainly owed to the Maldives Monetary Authority, MMA) in the last two years has intensified the debt burden. Key r isks for debt

The sector employs about 1 1 percent o f the workforce and fish processing accounts for the bulk o f manufacturing activity and domestic merchandise exports.

7

sustainability are large future shocks to exports or fiscal pol icy slippages. This assessment rests heavily on the implementation o f the Government’s proposed fiscal adjustment. Recent growth in private external debt increases the risk o f external debt distress. Private external debt adds about 40 percentage points to the external public debt to GDP ratio, putting the total external debt ratio at 77 percent. Much o f this debt i s at maturities o f less than 10 years, at market interest rates and denominated in U.S. dollars. The stock has accelerated in recent years in line with the boom in resort construction prior to the global financial crisis. Given the rationing o f foreign exchange in the economy currently, servicing this debt is becoming increasingly difficult. Implementation o f the Government’s reform program will help to reduce foreign exchange rationing.

Table 1. Maldives: Selected Economic and Vulnerability Indicators

2oW 2M)5 2006 2007 2008 2009 2010 2011 2012 EBt. Projection

OUTPUT AND PRICES

Real GDP Inflation (period average) Inflation (endaf-period) GDP deflator

CENTRALGOMRNMENT FINANCES

Revenue and grants Fqenditure and net lending Overall balance Overall balance excl grants Financing

Foreign Domestic

Ofwhich: Privatiration receipts

Public debt External Domestic

MONETARY ACCOUNTS

Broad money Domestic credit

NFA o f c o m r c i a l banks (in millions of US$, e.o p ) Net Forexposition o f c o m r c i a l banks (in millions ofUS$, e 0.p

Ofwhich: To private sector

BALANCEOF PAYMENTS

Current account Of which:

%orts Domestic Re-eqorts

Imports Nonfactor services, net

Capital and fmancial account (mcl e&o) Ofwhich:

General government, net Banks and other sectors, net

Overall balance

Gross international reserves (in millions ofUS%; e o p ) In months ofGNFS imports In percent ofshort-term debt at remaining maturity

External debt Mediumand long-term Short-term I n percent ofdomestic GNFS exports

External debt service (in percent o f domestic GNFS eqorts)

Exchange rate (ru!jiaaRTS$, e o p )

MEMORANDUM ITEM

GDP (in millions of rufyiaa) GIIP (in nullions of US %)

9 5 6 3

I O 1 2 4

34 2 36 0 -1 8 -2 5 1 8 4 1

-2 3 0 2

55 2 401 15 1

32 8 32 6 57 6 600 27 0

-15 8

23 3 15 8 7 5

-72 7 45 1 21 4

3 2 I 4 6 5 7

204 4 3 4

585 0

42 7 41 6

1 0 52 7 5 0

12 8

9,939 776

-46 2 5 2 9 1 2

47 7 59 0

-11 3 -19 8 11 3 2 4 8 8 0 4

649 41 3 23 6

117 63 2 54 5

4 0 0 38 0

-36 4

21 6 13 8 7 8

-87 4 146 34 1

2 5 30 6 -2 3

I87 1 2 6

261 0

53 0 47 9

5 0 93 1

9 0

12 8

9,596 750

(Annual percentage change)

18.0 7 2 5.8 -4.0 3.4 3 6 7 6 119 5 5 4.5 3.9 10.4 8 6 6 7 4.7 3 5 7.4 13 0 11.0 4.0

(ln percent ofGDP)

52.1 558 490 36.3 37.0 59.3 60.8 62.8 650 54.8 -1 2 4.9 -13.8 -288 -178

-14.6 -127 -18 5 -33 6 -189 7 2 4 9 138 288 178 4.5 4 6 3.8 12.7 4.2 2.7 0.4 100 16 1 136 0.4 0 3 0.3 0 1 2.6

6 2 9 664 686 916 960 3 9 6 39.8 37.4 46.8 545

448 41.5 23.4 265 31 2

(Annual percentage change, unless othenvise indicated)

206 23 7 23.6 9 4 6 7 3 7 6 458 434 5 7 7 5 495 492 330 4 1 -21

-145 0 -338.0 -437.0 -416.0 -4660 72.0 640 141.0

(ln percent ofGDP, unless othenvise indicated)

-33 0

24 6 14 8 9 9

-89 I 35 0 37 9

4 2 26 0 4 9

232 2 2 7

168 0

62 8 52 8 I O 0 83 7 9 0

12 8

11,717 915

-41 5

21 6 I O 2 11 4

-91 5 36 0 48 8

3 4 37 1 7 3

3100 3 0

121 0

79 7 62 6 170

111 0 12 0

12 8

13,493 1,054

-51 4 -29 6

26 2 16 1 I O 0 6 6 I 6 2 9 5

-96 8 -58 2 29 4 220 460 30 5

5 3 8 4 33 3 14 6 -5 4 0 9

241 3 217 0 1 8 3 2

80 0 81 0

76 9 82 0 59 9 67 0 I 7 0 I 5 0

1140 I69 0 12 0 I 7 0

12 8 12 8

16,137 17,192 1,261 1,343

-23 4

17 7 6 9

I O 7 -58 8 28 4 20 6

-1 9 20 4 -2 8

291 0 3 1

88 0

80 0 68 0 13 0

I47 0 24 0

12 8

18,480 1,444

3 7 6 3 6 3 6 3

43 4 47 5 -42 -5 2 4 2 2 0 2 2 1 3

87 9 50 4 37 5

-13 1

I 7 7 6 8

I O 8 -55 9 33 0 I 1 1

-1 2 103 -2 0

305 0 3 1

1180

71 0 60 0 10 0

124 0 22 0

12 8

20,354 1,590

4 1 3 5 3 5 3 5

442 41 9 -3 6 -46 3 6 2 6 1 1 0 8

82 5 47 0 35 5

-11 I

11 8 6 8

11 0 -55 9 36 3 12 5

0 6 11 1 1 4

347 0 3 4

143 0

65 0 56 0

8 0 109 0 15 0

I 2 8

21,935 1,714

Sources. Maldivian authorities, and Fund staff estimates and projections.

8

C. POVERTY REDUCTION AND SOCIAL DEVELOPMENT

23. Returning to positive rates o f economic growth i s a pre-requisite for sustaining the country’s impressive progress in improving human development outcomes. Despite the challenges o f a dispersed population, the Maldives has achieved notable development progress in recent decades through a combination o f private sector-led tourism development and improving public service provision. Annual real GDP growth has averaged over seven percent in the last 25 years, contributing to a sharp reduction in poverty. Poverty rates, as measured by the headcount ratio, have fallen steeply, from 4Opercent in 1997 to 28 percent in 2004.5

24. Other human development indicators - infant mortality, maternal mortality, or educational attainment - have registered similar improvements. The country i s on track to meet most o f the Mil lennium Development Goals (MDGs), and has already met the MDGs on eradicating extreme poverty and hunger, achieving universal primary education, reducing chi ld mortality, improving maternal health, and combating HIV/AIDS , malaria and other diseases6 Efforts to promote gender equality and empower women, as wel l as ensuring environmental sustainability and effective climate adaptation will need to be sustained to reach these MDGs. Moreover, while poverty has declined sharply overall in recent years, vulnerability and inequality are a concern, as a significant number o f people fe l l ba’ck into poverty during the recent crisis, and the disparities between remote islands with small populations and the capital Male region remain substantial.

25. The Government i s seeking to consolidate human development gains while also responding to the current challenges. The SAP seeks to increase the quality o f service provision to a standard commensurate with the country’s income levels. It also aims to address key emerging issues such as vulnerability, malnutrition, fertility, and youth unemployment which represent significant implications for other aspects o f social and human development, including education and economic productivity. The current macroeconomic crisis i s an additional challenge to the successful implementation o f i t s development plans, but the approach adopted by Government i s one that seeks to address the short-term challenge o f crisis management while st i l l ensuring that the core principles o f i t s development plan remain intact.

D. THE GOVERNMENT’S CRISIS RESPONSE AND MEDIUM-TERM DEVELOPMENT PLAN

26. The Government’s measures are designed to regain macroeconomic stability and lay the foundations for future economic growth. The SAP aims to redefine the role o f the state in the economy to achieve upper-middle income status, ensure more equitable access to services and opportunities, improve service delivery, facilitate economic diversification, and support better environmental practices to sustain growth and adapt to global climate change. M u c h o f the plan is to be implemented through the private sector where possible or public-private partnerships (PPPs). Ultimately the SAP seeks to establish an integrated transport network, ensure affordable living

The GoM reports these poverty rates in the PRSP based on a poverty line of Rf. 15 per day, which i s equivalent to US$ 1.17 using the nominal exchange rate, or US$3.45 in purchasing power parity (PPP) terms. Recent poverty rates are not available. However, the impact of the current global economic crisis could be expected to have increased the poverty rates.

Millennium Development Goals - Maldives Country Report 2007, Government of Maldives.

9

costs, provide affordable housing, ensure affordable and quality healthcare and stem the entry o f narcotics into the country.

27. A fundamental component of the Government’s SAP i s to engage the private sector in the provision o f goods and services that are currently being provided by the state. A policy that includes privatization o f state owned enterprises, setting up joint ventures with the domestic and international investors, corporatization o f state entities and a program o f public private partnerships would guide implementation o f the S A P . The Privatization Committee, composed o f cabinet members, and other Government officials and chaired by the Minister o f C iv i l Aviation, has been set up to implement the Government’s vision. All three IFIs - the World Bank Group, the Fund and the ADB - are supporting complementary components o f the Government’s plan.

28. The Government’s long term development plan i s an ambitious new vision f o r Maldives. It reflects a commitment to fundamentally changing the economic system o f the country to one that i s based on private sector led investment and underpinned by good governance and strong accountability. At the same time, the Government recognizes that the new democratic political system needs careful nurturing to entrench it and promote i t s growth. The Government’s ability to deliver on these promises has been compromised by the impacts o f the global financial crisis, the unsustainable fiscal expenditures inherited from the previous administration and the challenge o f weak capacity across al l levels o f Government.

29. Fully recognizing the severity of the immediate situation, the Government has been active in the last few months implementing a coherent stabilization program supported by IMF financing. The main element o f the Government’s program i s expenditure reduction. It has implemented wage cuts for the public service in October 2009 and has cut domestically financed capital expenditures. Regarding public service reforms, implementation o f the redundancies planned for 2009 and 20 10 is underway with 1,200 o f the expected 9,000 redundancies taking place from July to November 2009. Plans for the reduction o f the additional staff are being developed and discussed with the C iv i l Service Commission. The Government has also increased the electricity tari f f charged by state-owned electricity company (STELCO) by an average o f 35 percent (for Male residents, with increases for the rest o f the country planned for early 2010). These actions have taken place in an extremely challenging environment, particularly considering the lack o f a parliamentary majority for the Government.

30. Revenue measures also figure prominently in the Government’s program. Plans are underway to introduce a goods and services tax on the tourism sector, which will be additional to the existing flat-rate bed tax, and to accelerate implementation o f the business profits tax. The goods and services tax will be applied to the other sectors o f the economy by 201 1. The Government has also stopped monetizing the deficit. The overriding objective o f these measures i s to put government revenues on a more stable and reliable basis.

31. These measures are expected to place the fiscal deficit on a sustainable path. The fiscal consolidation measures taken by the Government are expected to reduce the fiscal deficit (excluding grants) from an expected 28 percent o f GDP in 2009 to less than 5 percent o f GDP in 2012. The weight o f the measures will come into effect in 2010 and in 201 1 where the deficit i s expected to decline to 18.9 percent and 5.2 percent, respectively. Complementary measures are being taken through a tightening o f monetary policy and measures to strengthen the capital and

10

liquidity position o f the banking sector. The Government expects that these measures will promote faster economic growth by providing a stronger macroeconomic pol icy framework and reducing external financing constraints. With successful implementation o f this program, the team’s assessment i s that the macroeconomic policy stance o f the Maldives i s adequate (see Annex 2).

32. The austerity measures are to be complemented with social support measures. In addition to severance packages that are mandated under the Civil Service Act the government plans to introduce a retraining program for those that lose their jobs in the public service. They have also announced plans for student loans and loans for those who wish to start small and medium sized enterprises. For the poor and vulnerable who will be most affected by the increase in electricity tariffs the Government will introduce targeted consumer subsidies. Section IV provides additional detail on these measures.

11

Box 1. Key Features o f the IMF Program

The IMF program i s a blended financing arrangement comprising: (a) SDR 49.2 mil l ion (or 600 percent o f quota) Stand-By Arrangement (SBA) over 36-months, and (b) SDR 8.2 mil l ion (100 percent o f quota) Exogenous Shock Facility-High Access Component over 24-months. In US$ terms the (combined) assistance amounts to $92.5 mi l l ion over 3-years. The core o f the policy framework that underlies the program i s a strong fiscal adjustment to contain aggregate demand and put public finances back on a sustainable medium-term path. Fiscal measures are complemented by monetary tightening and measures to strengthen the banking sector.

Fiscal measures Reduction in civi l service wages o f between 10 and 20 percent depending on rank. This adjustment w i l l be reversed when domestic Government revenues reach 7 bil l ion rufiyaas, which i s projected for 201 1. Civ i l service staff reductions to total 9,000 by end-2010. Of these, some 3,200 civi l servants w i l l be transferred to the private sector through the Government’s corporatization process. Operational spending and non-priority domestically financed capital spending are also to be reduced by 2 percent o f GDP and 1 percent respectively (prior action). Electricity tariffs raised by 40 to 60 percent depending on consumption bracket (prior action) and a mechanism for automatic price revision in step with global o i l prices w i l l be implemented. Revenue measures include an increase in the airport tax rate o f 29 percent, the expansion o f the business profits tax (structural benchmark), introduced o f a 6 percent ad valorem hotel room tax (structural benchmark), and the introduction o f a goods and services tax by early 201 1 (structural benchmark).

Monetary measures Monetary policy w i l l support fiscal adjustment efforts by tightening domestic liquidity in order to stem reserve losses. Halting the monetization o f the fiscal deficit has been key in this regard. Domestic fmancing o f the deficit w i l l be restricted to t-bill placements. An auction system for t-bill placements w i l l be set up by end-2009 (structural benchmark). The Government debt stock with the MMA has been converted into tradable securities (prior action). In August, the MMA started using these securities as collateral to conduct open market operations (OMOs) through reverse repos, another attempt at tightening monetary policy. Under the program no adjustment to the exchange rate regime i s anticipated as the combination o f strong fiscal adjustment and monetary tightening i s expected to relieve pressure on the exchange rate. In the event that the proposed measures prove insufficient to curb pressure on the rufiyaa, the authorities would seek alternative policy action including a possible adjustment to the exchange rate regime.

Financial Sector Measures Strengthen the financial position o f the Bank o f Maldives. The Government has signaled their intention to restructure BML’s portfolio, ensure rapid action for recovery o f collateral on defalted debt, and if necessary, secure a capital infusion. The Government’s preferred option i s to find a strategic partner to take over the State’s shares. The authorities w i l l seek passage o f the Banking Law and the reforms to the M M A Act by end-2010 (structural benchmark).

111. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM

A. LINKTOCAS

34. The Maldives Country Assistance Strategy (CAS) was jointly prepared by the Bank and the IFC and approved by the Board on January 8,2008. The proposed World Bank Group assistance program seeks to further three strategic development outcomes: (a) a well-managed economy attracting increased investment; (b) increased quality o f education in support o f a better

12

skilled workforce; and (c) improved capacity to manage the country’s pristine, but fragile, natural environment.

35. The CAS rests on three pillars:

0 Pillar I: Economic and fiscal governance, aiming to support the Government’s efforts to manage i t s economy and finances better, while strengthening the investment climate. Pillar 11: Human development and social protection, seeking to strengthen the quality o f public services for human development and social protection. Pillar 111: Environmental management, bolstering efforts to strengthen environmental management capacity and skills, build a sound knowledge base to better address the environmental r isks facing the country, mitigate threats to nature based tourism by improving environmental infrastructure, and implement a strategy to build climate resilience and adapt to the impending risks o f climate change.

0

36. These pillars and strategic outcomes were to be supported through IDA credits, strategic IFC investments and Advisory Services and a flexible program of AAA. IDA investment loans programmed in the CAS for FY08 and FY09 included the three new IDA operations proposed in the CAS - mobile phone banking, environmental management and pension administration - that have now been approved by the Board. For the last three years o f the CAS period, the strategy proposed a programmatic, policy-based investment model and assumed that the Bank Group program would be more specifically defined as part o f the CAS Progress Report process.

37. Staff have initiated work on the CAS Progress Report which will examine CAS implementation and results to date, and discuss the future direction of the Bank’s program. In September 2009, an all-day workshop was held with Government officials, including President Nasheed and key ministers. The meeting included most o f the Bank’s regional management team and senior Bank and IFC staff working o n the Maldives. Key results f rom the retreat and subsequent staff consultations with Government indicate that the three original pillars o f the CAS have remained broadly valid, while the Government would l ike specific support in the fol lowing areas: i) macroeconomic (especially fiscal) reform with particular emphasis on c iv i l service reforms and technical assistance to retrain retrenched public servants , ii) creating the framework for PPP and support for transactions, iii) improving the social safety net, iv) good governance, specifically to initiate diagnostic work needed to help develop the Government’s Governance and Anti- Corruption Strategy, v) economic diversification, vi) employment, and vii) climate change. Given the need for policy reform in the country and the limited resources available for project preparation and AAA, the preferred approach for IDA i s to use the development policy lending instrument, while also providing TA in a few key areas.

38. This proposed operation i s aligned with the CAS - especially Pillar 1 but also the second pillar with includes social protection. The CAS calls for a possible development pol icy operation in FY 10. The pol icy actions supported by this proposed operation would be focused on helping the Government to put in place key elements to support economic growth.

13

B. COLLABORATION WITH IMF AND OTHER DONORS

39. The Bank has been working in close coordination with the IMF and the ADB to put together complementary programs of support for the Government’s reform package. Bank and Fund staff have carried out regular consultations to align programs o f support. Three joint missions were undertaken between June and September 2009, with one being a tripartite mission that included an ADB representative to work on the debt sustainability analysis. An important component o f the collaboration has been agreeing to a division o f labor that builds on each institutions’ comparative advantages and the past areas o f engagement with the Government. The teams have also been careful to realize implementation capacity constraints o f the Government. The ADB and the IMF have taken the lead on various areas o f tax reform, while the Bank i s taking the lead on aspects o f medium-term expenditure reform, budget implementation and social safety nets. The ADB i s working closely with the Government on i t s privatization agenda, while the World Bank and IFC are focused on public-private partnership (PPP) aspects o f the agenda.7

40. IF1 financing will support the Government’s economic growth promotion efforts. The IMF Board in early December approved a 36-month combined Stand-By Arrangement and External Shocks Facility o f US$92.5 mill ion (or 700 percent o f quota). The ADB approved a US$35 million budget support operation half disbursed in 2010 and a roughly equal amount planned for disbursement in mid-2011. The Bank i s proposing a single tranche DPC o f US$13.7 million this year, which could be followed by another operation o f similar value next year. The operations are presented in a programmatic series and include a medium-term framework o f support, given the protracted nature o f the challenges that the Government i s facing. The coordinated programs o f support from IFIs will be a critical input for mobilizing additional support for the Government at a Donors’ Forum scheduled for March o f this year.

C. RELATIONSHIP TO OTHER BANK OPERATIONS

41. This proposed operation complements each o f the ongoing operations under the current CAS. The proposed operation has as i t s core objective to aid the Government in regaining sustained growth and poverty reduction. I t does so in a way that helps build institutional capacity that can facilitate better service delivery, support a stronger investment climate and promote better social protection. The ongoing operations include an Integrated Human Development Project (IHDP) o f $15.6 million approved in May 2004, a Mobile Phone Banking Project (MBP) o f US$7.7 million approved in April 2008, an Environmental Management Project (EMP) for US$l3.2 million approved in May 2008, a post-Tsunami Emergency project o f US$14 million co-financed by the European Commission’ and a Pension and Social Protection Administration Project (PSAP) for US$3.6 million approved on May 12, 2009. The Bank i s also preparing a US$9.7 million Climate Change Trust Fund (CCTF) Program to be financed by the European Commission for delivery in September 2010.

42. The ongoing IDA program and this proposed operation are complementary to IFC’s work program in the country. Working towards the agreed strategic development outcomes o f the World Bank Group CAS for FY 08-12, IFC’s main focus in the CAS period to date has been in

’ Specifically, the Bank is helping the government to establish a PPP framework, while the IFC is helping them structure PPP transactions. Project closes in January 2010. 8

14

four key areas - tourism, financial markets, renewable energyhlimate change and infrastructure. IFC's advisory services program has assisted the Maldives Monetary Authority (MMA) in establishing and strengthening prudential guidelines (e.g. in Islamic Banking) and also provided technical assistance to help set up a Credit Bureau. During the previous CAS period the IFC committed a total of U S $47.8 mi l l ion in both debt and equity, consisting o f four projects in the financial, tourism, logistics and telecommunications sectors. IFC has more than doubled its commitments to about US$103 mi l l ion (or roughly twice that o f IDA) in the f i rs t part o f the current CAS period (2008 to June 2009).

D. LESSONS LEARNED

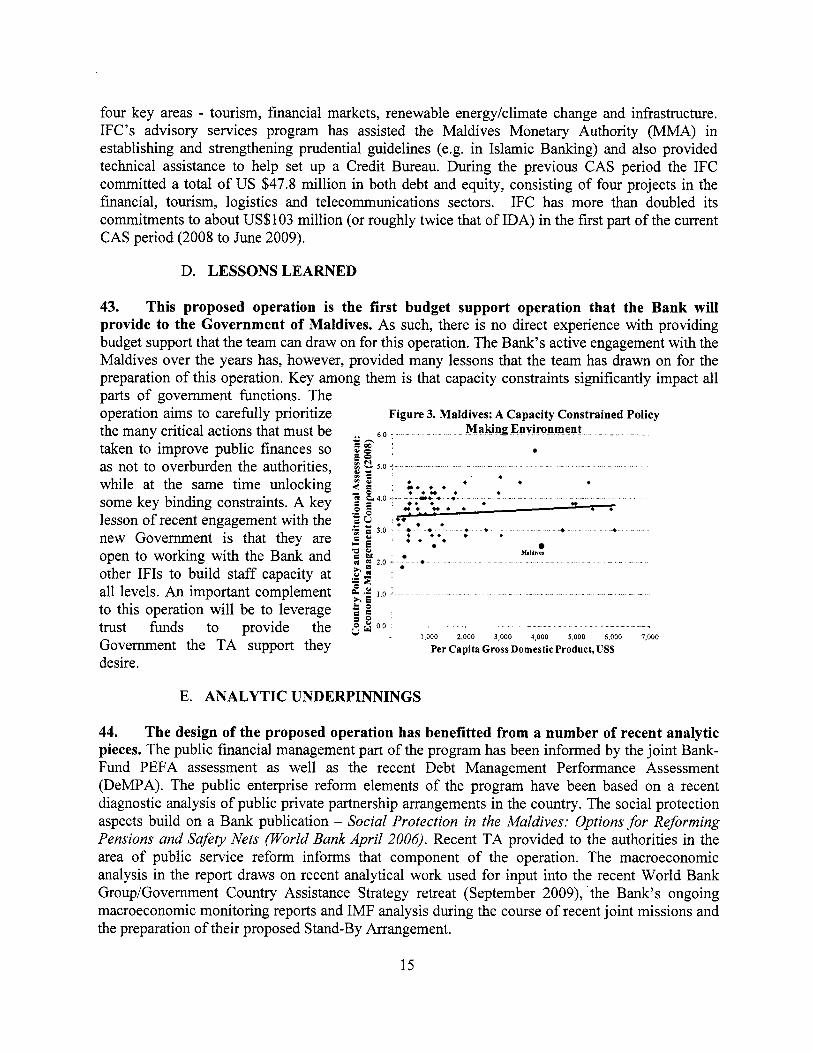

43. This proposed operation i s the first budget support operation that the Bank will provide to the Government of Maldives. As such, there i s no direct experience with providing budget support that the team can draw on for this operation. The Bank's active engagement with the Maldives over the years has, however, provided many lessons that the team has drawn o n for the preparation o f this operation. Key among them is that capacity constraints significantly impact al l parts o f government functions. The operation aims to carefully prioritize the many critical actions that must be taken to improve public finances so as not to overburden the authorities, while at the same time unlocking some key binding constraints. A key lesson o f recent engagement with the new Government is that they are open to working with the Bank and other IFIs to build staff capacity at al l levels. An important complement to this operation will be to leverage trust funds to provide the Government the TA support they desire.

Figure 3. Maldives: A Capacity Constrained Policy 6 0 Making Environment

u - a m 0 0 I

; & o s

MdJhci

Per Capita GrossDornestic Product,US%

E. ANALYTIC UNDERPINNINGS

44. The design of the proposed operation has benefitted from a number o f recent analytic pieces. The public financial management part o f the program has been informed by the jo int Bank- Fund PEFA assessment as well as the recent Debt Management Performance Assessment (DeMPA). The public enterprise reform elements o f the program have been based on a recent diagnostic analysis o f public private partnership arrangements in the country. The social protection aspects build on a Bank publication - Social Protection in the Maldives: Options for Reforming Pensions and Safety Nets (World Bank April 2006). Recent TA provided to the authorities in the area o f public service reform informs that component o f the operation. The macroeconomic analysis in the report draws on recent analytical work used for input into the recent World Bank Group/Government Country Assistance Strategy retreat (September 2009), 'the Bank's ongoing macroeconomic monitoring reports and IMF analysis during the course o f recent jo int missions and the preparation o f their proposed Stand-By Arrangement.

15

IV. THE PROPOSED DEVELOPMENT POLICY CREDIT

A. RATIONALE AND OBJECTIVES

45. The proposed development policy credit aims to underpin the Government’s efforts to restore economic growth and protect the vulnerable. There are three main areas o f the Government’s plan that this proposed operation will support:

a. Public Financial Management: There are several institutional changes that the Government is working on to ensure that budget preparation, implementation and monitoring processes are improved so as to support the delivery o f credible budgets within a sustainable medium-term framework. The proposed operation will focus on changes to the medium-term expenditure framework, within year monitoring o f budget outturns and improving overall budget accountability.

b. Public Enterprise Reform: A key principle o f the Government’s development plan i s to reduce the role o f the state in the economy. It i s also seen as a way to underpin the fiscal austerity measures to help ensure their sustainability. The proposed operation aims to guide the drive for PPPs in a way that minimizes future fiscal risks to the Government and ensures that the privatization process i s conducted transparently and communicated effectively to relevant stakeholders.

c. Social Protection: The Government’s fiscal measures, especially the increase in STELCO’s tariff structure, necessitate wel l targeted safety net programs to cushion the impact o f rising prices. Existing safety net programs are ad hoc and overlapping, and the Government intends to unify and improve them over time. In the meantime, the Government is introducing electricity, water and food subsidies to protect poor households from the rise in utility prices. This and the next proposed operation will support the development o f a new eligibility criteria for the recently introduced subsidies, while helping to build the foundations for a more harmonized national social protection system.

46. The Government’s reform program warrants rapid financial and analytic response from the Bank. Even under normal circumstances the Government’s development plan would warrant Bank and other donor support given l imited domestic resources. The effect o f the current global financial crisis has exposed a legacy o f poor fiscal policy that is in urgent need o f rebalancing in conjunction with significant external financing. The Government has presented a credible reform plan that aims to address the current fiscal imbalances and restore growth. The Bank’s financial support i s a key complement to the IMF and ADB financing that is expected this year and next. Additionally, the proposed areas o f support identified for this operation may help in harnessing other donor financing during the Maldives Donor’s Forum planned for end-March 201 0.

B. DESIGN AND FOCUS OF THE PROPOSED OPERATION

47. Policy actions supported by this proposed operation are focused on helping the Government to restore the economic fundamentals for a growth recovery. The focus on public financial management by addressing key institutional shortcomings in budget preparation and

16

implementation aims to enable the Ministry o f Finance and Treasury to recognize budget overruns early so that they can be addressed early. The focus on public enterprise reform supports the Government’s ambitious public private partnership program, while underpinning fiscal sustainability. The social protection measures help cushion the impact o f what is to be a significant structural change in the economy.

48. The policy actions supported by this proposed operation have been chosen strategically from the Government’s broad reform agenda. The choice o f the pol icy actions reflect the enormous challenge o f marshalling the l imited Government capacity to undertake measures that will help regain fiscal sustainability. L i ke several other small-island economies, capacity o f Government i s not commensurate with typical indicators o f the level o f development. In this context, the policy actions are focused on the critically important elements o f the reform program that are realistically achievable and set the basis for future economic growth. The proposed programmatic structure o f the operation also supports the Government’s effort to build reform momentum during i t s early tenure in Government and allows the Bank to gauge implementation progress.

17

Box 2. Application of Good Practice Principles on Development Policy Lending Operations

Principle 1: Reinforce ownership

The proposed operation i s closely aligned with the Government’s priorities documented in the SAP, with its ambition to implement their development plan through PPPs where possible. The program chooses those policy measures that the Government deems essential to the successful implementation of their program while complementing other donor assistance.

Principle 2: Agree up front with the government and other financial partners on a coordinated accountability framework

The policy matrix that underpins this proposed operation was developed jointly with the Maldivian authorities and was discussed with the ADB and the IMF during i t s development phase to align with their programs of support.

Principle 3: Customize the accountability framework and modalities of Bank support to country circumstances

Given the urgent need to reduce macroeconomic imbalances in the economy, the proposed operation has been designed under IDA’S Fast Track Facility. The timing, design, and scope o f the operation are thus customized based on this urgency, but also on the limited capacity of the Government. Nevertheless, it i s fblly consistent with the Government’s medium-term plans for poverty reduction and improved service delivery.

Principle 4: Streamline critical actions for achieving results

The proposed operation i s the first in a proposed programmatic series. The prior actions for the first operation are limited to 4, while the triggers for the proposed second operation have been limited to 8. The Government’s policy actions number well over 30 when considering the actions under the programs of support from the IMF and the ADB. The prior actions and triggers considered here are focused on achieving key results under the Government’s program and are supported by milestones that aim to provide analytic support for sound implementation.

Principle 5: Conduct transparent progress reviews conducive to predictable and performance based financial support

Progress made with implementation of reforms and achievement of outcome goals will be monitored through regular macroeconomic updates and discussed frequently with the authorities. These activities will provide clear guidance to the Government for when and if the resources associated with the second proposed operation would flow to Government.

Public Financial Management

49. The current fiscal crisis has brought into focus the long-standing weaknesses in budgetary processes. The current fiscal imbalances are due in part to expenditure policies that were not based on a realistic forecast o f Government revenues. The Bank has been working with the authorities in recent years to help implement a Medium-Term Expenditure Framework. A key result o f this work has been the presentation o f the 2009 budget in a 3-year framework. A key challenge moving forward would be to instill greater realism into budgets by adopting conventional GFS standards. Realism has been inhibited by the requirements o f the Public Finance Act to show

18

balanced budgets each year. One way authorities achieve this result is to include al l expected privatization receipts and the sale o f state assets as a revenue item.g Implementing expenditure policies on the basis o f highly uncertain revenue outturns has been one reason for the rise o f expenditures to unsustainable levels. A joint Bank-Fund Public Expenditure and Financial Accountability (PEFA) assessment was recently completed in October 2009 and a comprehensive action plan for improvement has been agreed, which will be monitored during the implementation o f the proposed program.

50. The first prior action in this component of the program i s to present the 2010 budget in a 3-year rolling framework that conforms to Government Finance Statistics 1986. The GFS presentation will be made in parallel to the existing formulation until a change to the Public Finance Act can be made. The objective o f this action i s to reduce the over-optimism on fiscal deficit projections once the fiscal consolidation efforts are undertaken. Re-establishing the Macroeconomic Coordinating Committee (MECC) ahead o f the presentation o f the 2010 budget and setting a timetable for regular meetings and outputs will help move the MTEF beyond simply a tool used for presentational purposes to a more credible pol icy instrument.

51. Weak expenditure control and monitoring i s also inhibiting the use of the MTEF as a policy tool. The budget preparation process st i l l has a one-year focus. The initial annual budget allocations are typically in line with medium-term government priorities, but these allocations change considerably during the year. The final allocations are made based on ad-hoc decisions due to inadequate (and not up to date) knowledge o f budget outturns and arbitrary developments in the processing o f project loans and grants, rather than being driven by systematic, medium-term objectives. The lack o f a transparent budget release and the absence o f reliable and timely reporting mechanisms, leads to an ad-hoc, non-transparent approach to in-year budget adjustments.

52. The Bank has been working with Government to produce reliable and timely reporting mechanisms through implementation of a Public Accounting System (PAS). The PAS project is expected to lead to the development o f a modern public accounting and financial management information system that will automate many aspects o f the accounting and budget management o f government. PAS will facilitate substantial improvements in budget execution, internal control, cash management, accounting and fiscal reporting. With full implementation it can create a basis for improvements in budget planning and in management o f fiscal risks. PAS implementation reached an important milestone in M a y 2009 when it became operational with respect to general ledger and payment processing for Male-based agencies. The system has now been fully implemented in Phase I agencies (Ministry o f Finance & Treasury, Customs and Department o f Inland Revenue).

53. The second prior action in this component of the program i s to implement Phase I1 o f the PAS project in three government agencies. Five key government agencies have been targeted for Phase two implementation - President’s Office, Department o f National Planning, C iv i l Service Commission, Ministry o f Education, and Addu Ato l l o f which the rollout to the former three was completed in December 2009 and the other two in early 2010. Implementation o f this prior action will support the requirement under the L a w on Public Finance 2006 (effective in 2009) to produce financial statements o f the Government, which have not yet been prepared and

The Auditor General’s Report o f 2008 on government finances i s highly critical o f the budget presentation that i s 9

required under the Public Finance Act.

19

published. To date, the annual budget provides a 'budget to actual' utilization report, which contains spending estimates but does not consist o f financial statements prepared using acceptable standards. Triggers for the proposed second operation are to (a) publish the f i rst audited financial statements of Government for 2009 and (6) issue revised Public Finance regulations (including procurement regulations) to establish adherence to internationally accepted public sector accounting standards, enhancing internal control pamework and improving spending eflciency. The objective o f these measures is to underpin fiscal expenditure discipline in the face o f revenue shocks to maintain fiscal discipline at both the sectoral and macro level.

54. Cash and debt management practices add to budget uncertainty. Cash flows are estimated by the Treasury on an annual basis but not updated periodically. The Treasury makes cash in- and outflow forecasts for the 12 months o f the budget year based on past seasonal patterns. I t does not use expenditure planning information from l ine ministries. The MMA has generally accommodated cash f low shortages by providing T-bills to the banking system (on behalf o f the Government) and/or providing access to the Ways and Means account and extending direct short term loans. The Treasury does not provide any in-year cash f l ow updates to the MMA. Debt management operations suffer f rom lack o f capacity to perform basic functions o f debt recording and reporting, and a lack o f coordination among key agencies, especially the MMA, making debt service projections that go into the budget highly uncertain.

55. The third prior action in this component of the operation i s for the Government to prepare a forecasting methodology for monthly revenues that can be updated monthly and presented to the Fiscal Affairs and Economic Policy Division of the MoFT. The objective o f th i s prior action i s to provide policy makers with an updated position o f government revenues and the outlook to reduce the fiscal impact o f revenue shocks. It also aims to support the Government in making timely in-year budget adjustments.

56. Capital expenditure policy i s also a key source o f budget uncertainty. Capital expenditures are heavily influenced by the Government's Public Sector Investment Program (PSIP). The annual PSIP is prepared by the MoFT and its composition i s determined on the basis o f an indicative domestic resource figure as wel l funds available through external aid. A key shortcoming o f the PSIP process i s the insufficient regard for future recurrent cost implications o f new capital projects, which i s in part due to the focus o f the budget process on one-year planning." The PSIP process also suffers from inadequate analysis o f the economic viability, a rationalization o f using public resources for the proposed activity, or an investigation o f the opportunity costs o f choosing a particular project. A trigger for the proposed second operation is to unzjj the PSIP with the rest of capital and recurrent expenditures on a 3-year basis.

57. The fourth action in this component o f the program i s to construct a single unified public sector pay and employment database. One of the key challenges preventing the MoFT from making within year budget adjustments is the lack o f timely information on expenditure outturns. A key component o f expenditures i s the. wage bill for public servants. While there i s data on the number o f public servants employed and their pay packages, there is no one unified and reconciled database that i s updated regularly. T o address this issue, the fourth prior action is to

lo Although in recent years actual capital expenditures tended to be lower than budgeted due to implementation capacity constraints.

20

establish a comprehensive database o f a l l public sector employees and their total pay packages that can be updated semi-annually until the human resources module o f the public accounts system is fully functional. Each month the M o F T will monitor the treasury’s disbursement figures for the salary bill, by base pay and allowances, and compare against the baseline figures o f the database so that accurate budget out-turns can be measured during the year.

58. The appointment o f the first independent Auditor General in 2008 was an important step toward improving governance in Maldives. Until April 2007, the Auditor General’s Office (AGO) reported to the President and the audit reports were not sent to or scrutinized by the Parliament. An IDF Grant provided by the World Bank in 2006 helped enact the Audit Act o f 2007 which established AGO as the Supreme Audit Institution. Under the new AG, risk based strategic audits for 2008 were conducted across central government audit entities, some o f which had not been audited for decades. The nature o f audit was expanded from the detailed transactions-level compliance audits to include performance audits and the audit reports were posted on AGO website as soon as they were tabled in the People’s Majlis. This received extensive public interest and the Auditor General held press conferences in providing ex-post oversight over government systems o f PFM. In spite o f having had considerable impact, much needs to be done to fol low up on these audit findings and enhance the scope and coverage o f the other accountability institutions in Maldives such as the office o f the Attorney General, Tender Evaluation Board, the Anti-Corruption Commission and the Prosecutor General’s Office.

Public Enterprise Re form

59. In his first Presidential address to Parliament, President Nasheed made it clear that his Government would change the role o f the state in the economy. A fundamental component o f the Government’s Strategic Action Plan would be to engage the private sector in the provision o f goods and services that had previously been provided by the state. A pol icy that includes privatization o f state owned enterprises, setting up joint ventures with the domestic and international investors, corporatization o f state entities and a program o f public private partnerships would guide implementation o f the SAP. The Privatization Committee, composed o f cabinet members and other Government officials and chaired by the Minister o f C iv i l Aviation and Communication, has been set up to implement the Government’s vision.

60. There are a number of reasons why public enterprise reform, a privatization agenda and public private partnerships (PPPs) are important for Maldives. These include: (i) better public financial discipline, (ii) fiscal benefits in terms o f lump sum receipts, ongoing revenues and reduced expenditures, (iii) greater economic efficiency - better labor and capital productivity, (iv) improved service delivery, and (v) the introduction o f private sector innovation to the operation and financing o f service delivery. These benefits are not unique to Maldives, but are particularly relevant in the current context where the recent history o f increasing government expenditures together with the expansion o f the c iv i l service and lack o f focus on service delivery precipitated the current fiscal imbalances.